5. production - ujep · pdf file•harmonize relationship between company and workers....

TRANSCRIPT

5. PRODUCTIONVALUE CHAIN, TYPES OF PRODUCTION, HUMAN RESOURCES, CORPORATE FINANCE

Value Chain

• A set of activities that a firm operating in a specific industry performs in order to deliver a valuable product or service for the market.

• Based on the process view of organizations, the idea of seeing a manufacturing (or service) organization as a system, made up of subsystems each with inputs, transformation processes and outputs

• Inputs, transformation processes, and outputs involve the acquisition and consumption of resources

• How value chain activities are carried out determines costs and affects profits2

Production

• Act of creating 'use' value or 'utility' that can satisfy a want or need.

• May or may not include factors of production other than labor.

• Any effort directed toward the realization of a desired product or service is a "productive" effort and the performance of such act is production.

3

Types of Production

• PRIMARY SECTOR

• SECONDARY SECTOR

• TERTIARY SECTOR

• QUATERNARY SECTOR

4

PRIMARY SECTOR

Agriculture – cultivation of animals, plants, fungi, and other life forms for food, fibre, and other products used to sustain life.

• Animal husbandry

• Farming

• Fishing

• Forestry

Resource extraction

• Fishing

• Logging

• Mining

• Extraction of petroleum

• Extraction of natural gas

• Water industry

5

SECONDARY SECTOR

• Involves the processing of raw materials from primary industries

• Includes the industries that produce a finished, tangible product

Construction

• Process that consists of the building or assembling of infrastructure, including buildings, roads, dams, etc.

Manufacturing

• process which involves tools and labor to produce goods for use or sale; ranges from handicraft to high tech industrial production

6

TERTIARY SECTOR

• This group is involved in the provision of services

• They include teachers, managers and other service providers

7

QUATERNARY SECTOR

Produces knowledge-based services

• Information industry

• Information generation and sharing

• Information technology

• Consulting services

• Education

• Research and development

• Financial planning services

8

Scale of Production

• CRAFT PRODUCTION

• MASS PRODUCTION

• BATCH PRODUCTION

• JOB PRODUCTION

9

CRAFT PRODUCTION

• The process of manufacturing by hand with or without the aid of tools

• In the craft manufacturing process, the final product is unique

• While the product may be of extremely high quality, the uniqueness can be detrimental as seen in the case of early automobiles

10

MASS PRODUCTION

• Mass production or flow production is the production of large amounts ofstandardized products, including and especially on assembly lines

• Involves making many copies of products, very quickly, using assembly line techniques to send partially complete products to workers who each work on anindividual step, rather than having a worker work on a whole product from start to finish

11

BATCH PRODUCTION

• The object is created stage by stage over a series of workstations, and differentbatches of products are made

• Does not require skilled workers and takes a short period of time

• Most common in bakeries and in the manufacture of sports shoes, pharmaceuticalingredients (apis), purifying water, inks, paints and adhesives

12

JOB PRODUCTION

• Jobbing or one-off production, involves producing custom work, such as a one-off product for a specific customer or a small batch of work in quantities usually less than those of mass-market products

• Examples include:

• Designing and implementing an advertising campaign

• Auditing the accounts of a large public limited company

• Building a new factory

• Installing machinery in a factory

• Machining a batch of parts per a CAD drawing supplied by a customer

• Building the Golden Gate bridge

13

Lean Manufacturing

• Lean production, often simply "lean„

• Systematic method for the elimination of waste within a manufacturing system

• "Value" is any action or process that a customer would be willing to pay for

• Lean is centered on making obvious what adds value by reducing everything else

Toyota Production System (TPS)

• TPS is renowned for its focus on reduction of the original Toyota seven wastes to improve overall customer value, but there are varying perspectives on how this is best achieved.

• The steady growth of Toyota, from a small company to the world's largest automaker, has focused attention on how it has achieved this success.

14

SEVEN WASTES

• Transportation

• Inventory

• Motion

• Waiting

• Over-processing

• Over-production

• Defects

• Latent skill

15

HUMAN RESOURCES

• Designed to maximize employee performance

• At the macro-level, HR is in charge of overseeing organizational leadership and culture

• Compliance with employment and labor laws, which differ by geography, and often oversees health, safety, and security

• Collective bargaining agreement – HR will typically also serve as the company's primary liaison with the employee's representatives (usually a labor union)

• Engages in lobbying efforts with governmental agencies

16

Human Resource Core Functions

• Staffing

• The recruitment and selection of potential employees, done through interviewing, applications, networking, etc.

• Human resource development

• A continuous process of training and developing competent and adapted employees

• Compensation and benefits

• Motivation is the key to keeping employees highly productive

• Safety and health

• Employee and labor relations

• Keeping the employees' commitment and loyalty to the organization17

Human Resources Activities• Determine needs of the staff.

• Determine to use temporary staff or hire employees to fill these needs.• Recruit and train the best employees.

• Supervise the work.

• Harmonize relationship between company and workers.• Manage employee relations, unions and collective bargaining.

• Prepare employee records and personal policies.• Ensure high performance.

• Manage employee payroll, benefits and compensation.

• Ensure equal opportunities.• Deal with discrimination.

• Deal with performance issues.• Ensure that human resources practices conform to various regulations.

• Push the employee's motivation.

• Focus on individual who possess energy and capabilities to ensure the job done through people to achieve results.

18

Human Resources Activities

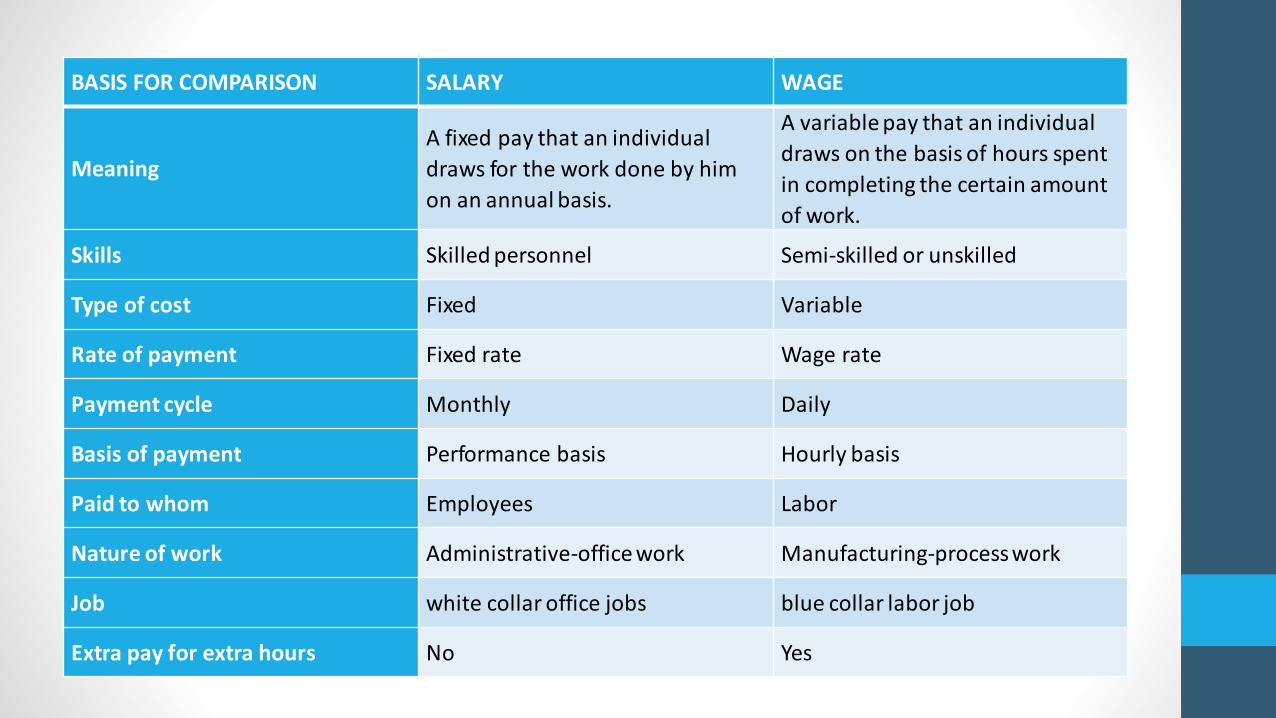

Wage

• Monetary compensation (or remuneration, personnel expenses, labor) paid by an employer to an employee in exchange for work done

• Payment may be calculated as:

• A fixed amount for each task completed (a task wage or piece rate)

• An hourly or daily rate, or based on an easily measured quantity of work done

• Wages are an example of expenses that are involved in running a business

Salary

• The employer pays an arranged amount at steady intervals (such as a week or month) regardless of hours worked, with commission which conditions pay on individual performance, and with compensation based on the performance of the company as a whole.

• Waged employees may also receive tips or gratuity paid directly by clients and employee benefits which are non-monetary forms of compensation.

19

BASIS FOR COMPARISON SALARY WAGE

Meaning

A fixed pay that an individual

draws for the work done by him

on an annual basis.

A variable pay that an individual

draws on the basis of hours spent

in completing the certain amount

of work.

Skills Skilled personnel Semi-skilled or unskilled

Type of cost Fixed Variable

Rate of payment Fixed rate Wage rate

Payment cycle Monthly Daily

Basis of payment Performance basis Hourly basis

Paid to whom Employees Labor

Nature of work Administrative-office work Manufacturing-process work

Job white collar office jobs blue collar labor job

Extra pay for extra hours No Yes

CORPORATE FINANCE

• Financial management concerned with all of the financial activities related to running a corporation

• Primarily concerned with maximizing shareholder value through long-term and short-term financial planning

Corporate finance involves:

• Financial management

• Financial analysis

• Accounting

• Investment banking

21

CORPORATE FINANCE

• Department or business unit, sometimes structured internally and sometimes outsourced, that prepares all of a company's financial numbers and then makes business recommendations based on those numbers

Capital investment decisions

• It first decides if a proposed investment should be made

• If the investment decision is accepted, corporate finance professionals then decide how the company should pay for it – with equity, debt or combination of both.

22

CORPORATE FINANCE

Short-term items include:

• the management of current assets and current liabilities

• inventory control

• investments

• other short-term financial issues

Long-term items include:

• new capital purchases

• investments

23

Financial Reporting

• Provide information on the changes in a firm's performance and financial position that can

be used to make financial and operating decisions

• To forecast the firm's ability to produce future earnings and as a means to assess the firm's

intrinsic value

• Other stakeholders, such as creditors, will use financial statements as a way to evaluate the

company's economic and competitive strength.

24

Financial Reporting

• The timing and the methodology used to record revenues and expenses may impact the

analysis and comparability of financial statements across companies

• Financial statements are prepared in most cases on the basis of three basic premises:

• The company will continue to operate (going-concern assumptions)

• Revenues are reported as they are earned within the specified accounting period

(revenues-recognition principle)

• Expenses should match generated revenues within the specified accounting period

(matching principle)

25

Financial Reporting

Cash-basis accounting

• recognizing revenue (income) and expenses when payments are made (when checks are issued) or when cash is received (and deposited in the bank)

Accrual accounting

• recognizing revenue in the accounting period in which it is earned, that is, when the company provides a product or service to a customer, regardless of when the company gets paid

• expenses are recorded when they are incurred instead of when they are paid for

26

Financial Reporting

• The diverse nature of business activities results in different financial statement presentation.

• The balance sheet (differently from company to company)

• The income statement

• Cash flow statements

• Knowing how to work with the numbers in a company's financial statements is an essential skill.

• The meaningful interpretation and analysis of balance sheets, income statements and cash flow statements to discern a company's investment qualities is the basis for smart investment choices. 27

Balance Sheet

The balance sheet provides information on:

• What the company owns (its assets)

• What it owes (its liabilities)

• The value of the business to its stockholders (the shareholders' equity) as of a specific date

It's called a balance sheet because the two sides balance out

A company has to pay for all the things it has (assets) by:

• either borrowing money (liabilities)

• or getting it from shareholders (shareholders' equity)28

Balance Sheet

Assets

• Economic resources that are expected to produce economic benefits for their owner.

Liabilities

• Obligations the company has to outside parties.

• Liabilities represent others' rights to the company's money or services. Examples include bank loans, debts to suppliers and debts to employees.

Shareholders' equity

• The value of a business to its owners after all of its obligations have been met.

• This net worth belongs to the owners.

• Shareholders' equity generally reflects the amount of capital the owners have invested, plus any profits generated that were subsequently reinvested in the company.

29

Balance Sheet

• The balance sheet must follow the following formula:

TOTAL ASSETS = TOTAL LIABILITIES + SHAREHOLDERS' EQUITY

• Each of the three segments of the balance sheet will have many accounts within it that document the value of each segment.

• Accounts such as cash, inventory and property are on the asset side of the balance sheet, while on the liability side there are accounts such as accounts payable or long-term debt.

• The exact accounts on a balance sheet will differ by company and by industry, as there is no one set template that accurately accommodates the differences between varying types of businesses. 30

31

Assets

CURRENT ASSETS

• These are assets that may be converted into cash, sold or consumed within a year or less

• Cash

• Marketable securities (short-term investments)

• Accounts receivable

• Notes receivable

• Inventory

• Prepaid expenses

LONG-TERM ASSETS

• These are assets that may not be converted into cash, sold or consumed within a year or less.

• Investments

• Fixed assets

• Other assets

• Intangible assets

32

Liabilities

CURRENT LIABILITIES

• These are debts that are due to be paid within one year or the operating cycle.

• Such obligations will typically involve the use of current assets, the creation of another current liability or the providing of some service

• Bank indebtedness

• Accounts payable

• Wages payable (salaries), rent, tax and utilities

• Accrued liabilities (accrued expenses)

• Notes payable (short-term loans)

• Unearned revenues (customer prepayments)

• Dividends payable

• Current portion of long-term debt

• Current portion of capital-lease obligation

33

Liabilities

LONG-TERM LIABILITIES

• These are obligations that are reasonably expected to be liquidated at some date beyond one year or one operating cycle.

• Long-term obligations are reported as the present value of all future cash payments

• Notes payables

• Long-term debt (bonds payable)

• Deferred income tax liability

• Pension fund liability

• Long-term capital-lease obligation

34

Income Statement

• Financial statement that reports a company's financial performance over a specific accounting period

• Financial performance is assessed by giving a summary of how the business incurs its revenues and expenses through both operating and non-operating activities

• It also shows the net profit or loss incurred over a specific accounting period

• Unlike the balance sheet, which covers one moment in time, the income statement provides performance information about a time period

35

Income Statement

• Divided into two parts: operating and non-operating

• The operating portion of the income statement discloses information about revenues and expenses that are a direct result of regular business operations.

• For example, if a business creates sports equipment, it should make money through the sale and/or production of sports equipment.

• The non-operating section discloses revenue and expense information about activities that are not directly tied to a company's regular operations.

• Continuing with the same example, if the sports company sells real estate and investment securities, the gain from the sale is listed in the non-operating items section.

36

Income Statement

Analysts use the income statement for data to calculate financial ratios such as:

• Return on equity (ROE)

• Return on assets (ROA)

• Gross profit

• Operating profit

• Earnings before interest and taxes (EBIT)

• Earnings before interest taxes and amortization (EBITDA)

• Presented in a common-sized format, provides each line item on the income statement as a percent of sales

• Analysts can easily see which expenses make up the largest portion of sales

• Analysts also use the income statement to compare year-over-year (YOY) and quarter-over-quarter (QOQ) performance

• Typically provides two to three years of historical data for comparison

37

Cash Flow

The statement of cash flow reports the impact of a firm's operating, investing and financial activities on cash flows over an accounting period.

The cash flow statement shows the following:

• How the company obtains and spends cash

• Why there may be differences between net income and cash flows

• If the company generates enough cash from operation to sustain the business

• If the company generates enough cash to pay off existing debts as they mature

• If the company has enough cash to take advantage of new investment opportunities

39

Cash Flow

Segregation of Cash Flows

• The statement of cash flows is segregated into three sections:

• Operating activities

• Investing activities

• Financing activities

40

1. CASH FLOW FROM OPERATING ACTIVITIES (CFO)

CFO is cash flow that arises from normal operations

This includes:

Cash inflow (+)

• Revenue from sale of goods and services

• Interest (from debt instruments of other entities)

• Dividends (from equities of other entities)

Cash outflow (-)

• Payments to suppliers

• Payments to employees

• Payments to government

• Payments to lenders

• Payments for other expenses

41

2. CASH FLOW FROM INVESTING ACTIVITIES (CFI)

CFI is cash flow that arises from investment activities

This includes:

Cash inflow (+)

• Sale of property, plant and equipment

• Sale of debt or equity securities (other entities)

• Collection of principal on loans to other entities

Cash outflow (-)

• Purchase of property, plant and equipment

• Purchase of debt or equity securities (other entities)

• Lending to other entities 42

3. CASH FLOW FROM FINANCING ACTIVITIES (CFF)

CFF is cash flow that arises from raising (or decreasing) cash through the issuance (or retraction) of additional shares, or through short-term or long-term debt for the company's operations.

This includes:

Cash inflow (+)

• Sale of equity securities

• Issuance of debt securities

Cash outflow (-)

• Dividends to shareholders

• Redemption of long-term debt

• Redemption of capital stock 43

44

REPORTING NON-CASH INVESTING AND FINANCING TRANSACTIONS

Information for the preparation of the statement of cash flow is derived from three sources:

• Comparative balance sheets

• Current income statements

• Selected transaction data (footnotes)

Some investing and financing activities do not flow through the statement of cash flow because they do not require the use of cash.

45

REPORTING NON-CASH INVESTING AND FINANCING TRANSACTIONS

Examples Include:

• Conversion of debt to equity

• Conversion of preferred equity to common equity

• Acquisition of assets through capital leases

• Acquisition of long-term assets by issuing notes payable

• Acquisition of non-cash assets (patents, licenses) in exchange for shares or debt securities

Though these items are typically not included in the statement of cash flow, they can be found as footnotes to the financial statements.

46

Once Again

http://www.investopedia.com/terms/i/incomestatement.asp

http://www.investopedia.com/terms/b/balancesheet.asp

http://www.investopedia.com/terms/c/cashflow.asp

47