4d1163 – performance and cost analysis - seminar - © 2006 manuel fritsch, patrick wild, christian...

Post on 22-Dec-2015

218 views

TRANSCRIPT

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 1

Seminar:Performance and Cost Analysis

Author: Manuel FritschPatrick WildChristian Hellwig

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 2

Company & Value Chain

Course book: Chapter 1, 2

Research and

Development Design Supply Marketing PRODUCTION Distribution

Customer service

German Family Enterprise (1916)

Producing high performance chains

3 different locations (Munich, Landberg, Strakonice)

Value Chain

Developing chains

Dominated by functionality

Receivingsteel sheets

Core Process

• B2B• Exhibitions

• Outsourcing• JIT

Account-Manager / customer

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 3

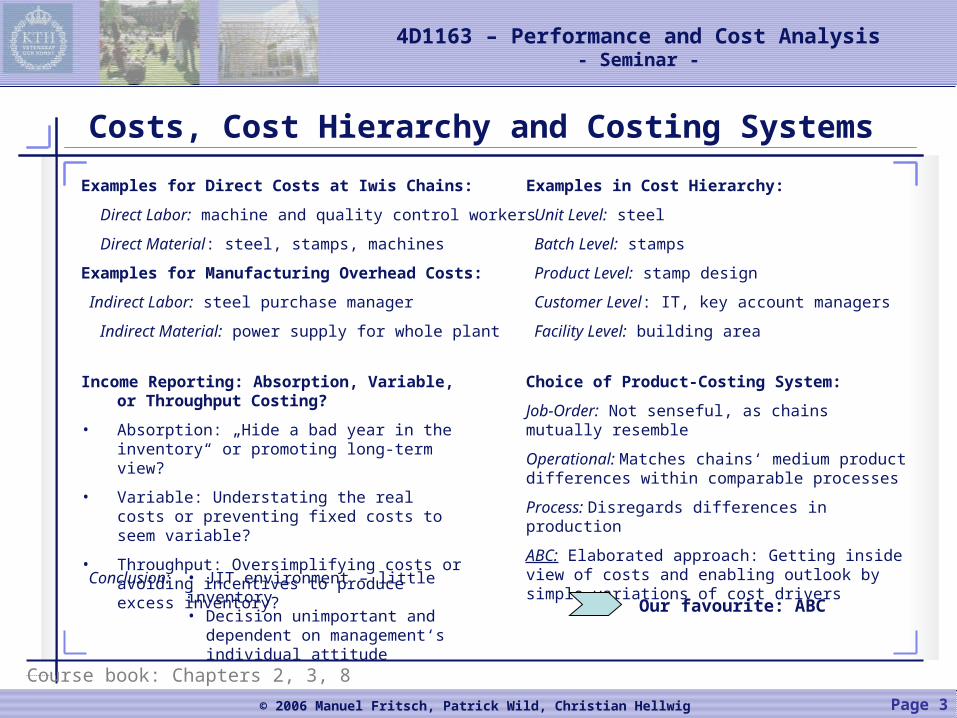

Costs, Cost Hierarchy and Costing Systems

Course book: Chapters 2, 3, 8

Examples for Direct Costs at Iwis Chains:

Direct Labor: machine and quality control workers

Direct Material: steel, stamps, machines

Examples for Manufacturing Overhead Costs:

Indirect Labor: steel purchase manager

Indirect Material: power supply for whole plant

Examples in Cost Hierarchy:

Unit Level: steel

Batch Level: stamps

Product Level: stamp design

Customer Level: IT, key account managers

Facility Level: building area

Income Reporting: Absorption, Variable, or Throughput Costing?

• Absorption: „Hide a bad year in the inventory“ or promoting long-term view?

• Variable: Understating the real costs or preventing fixed costs to seem variable?

• Throughput: Oversimplifying costs or avoiding incentives to produce excess inventory?

Conclusion: • JIT environment – little inventory• Decision unimportant and dependent on management‘s individual attitude

Choice of Product-Costing System:

Job-Order: Not senseful, as chains mutually resemble

Operational: Matches chains‘ medium product differences within comparable processes

Process: Disregards differences in production

ABC: Elaborated approach: Getting inside view of costs and enabling outlook by simple variations of cost drivers

Our favourite: ABC

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 4

ABC Approach

Course book: Chapter 4, 5

What if costs are considered too high? Identify costly production steps; ask „Why?“ repeatedly until the reason is found

Determine value-added/non-value-added activities

Take action to reduce primarily non-value-added activities (but consider the implications!)

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 5

Cost Volume Profit & Break-Even Point

Course book: Chapter 11, 12

Fixed cost: 1.039.988,89 €(Machines, Use of Factory…, including partial each SG&A and Manufacturing Overhead)

Variable costs per unit: 15,33 €Steel: 7,67 € / unit (unit level cost)Production of stamps: 6,80 € / unit (Batch level cost! 1 Batch = 5000 units)Stamp Exchange: 0,14 € / unit (Batch level cost!)Production QC Workers: 0,72 € / unit (Batch level cost!)

Selling Price: 65 €

Break-Even Point: 20.936 chains

But: We must consider step-wise growing batch-level costs!

We calculated the Break-even point by breaking down the batch-costs to a single unit.

20.936 units produce 5 batches including 25.000 units

Results in a sales revenue of -31.119,96 €

Sales Volume of the new Renault Chains

Solution: Produce other 543 chains chains * 65 € (selling price) - chains * 7,67 € (steel/unit) = 31.119,96 €

chains = 31.119,96 € / (65 € - 7,67 €)

chains ≈ 543

Final Break-Even Point: 21.479 chains

Break-even point

5000 10000 15000 20000 25000

38290

76580

114870

153160

191450

# chains

Costs

Calculated costs: ~ 160.330 €

Real costs: 191.450 €

Difference:~ 31.120 €

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 6

Quality & Time

Total Quality Management (TQM)

• Failures are not accepted, because one defective chain could destroy the whole engine

JIT Manufacturing

• JIT Manufacturing = “pull” manufacturing

• produce and deliver products just when needed

Customer-response time

• Because of flexible working hours, iwis has a very short customer-response time

Course book: Chapter 7

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 7

By-Products & Investment Decisions

Scrap metal as by-product

Because of the increasing metal prices, it is nowadays profitable to sell the scrap metal

Investment Decisions

Is it for iwis profitable to expand their business to bicycle chains?

Course book: Chapter 9, 14

No, because of the expected competition is the probability for losses very high

300

600

900

1200

1500

2001 2002 2003 2004 2005 2006

year

€

price of scrap metal charge of supplier

Break-even point

No

Yes

Yes

No

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 8

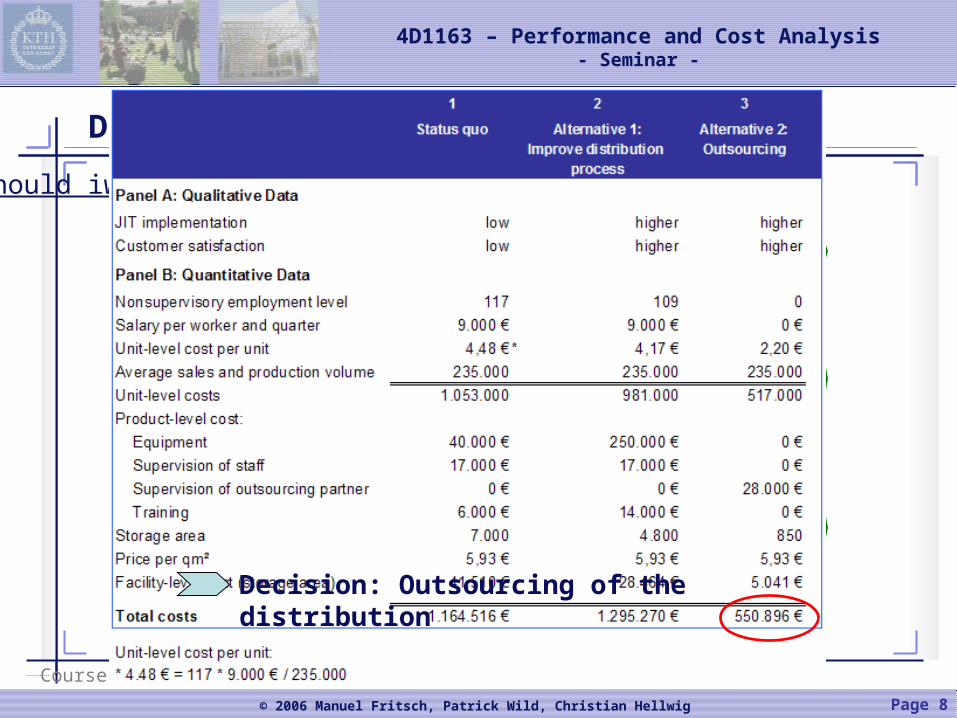

Maintain statusQuo?

Outsourcing

ImproveDistribution

Process

Status quoStatus quo is unacceptablebecause JIT requirements

are not matched

• JIT requirements matched• Higher equipment cost• Higher training cost• Same employment level• Higher quality employment

• not core-competence

• JIT requirements matched• Lower equipment cost• Fix cost per unit• Lower training cost

Improve distributionprocess

or outsource it?

Change

Course book: Chapter 13

Decision Making

Should iwis improve or outsource its distribution?

Decision: Outsourcing of the distribution

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 9

Selling, General, and Administrative Expense Budget

Course book: Chapter 15

• SG&A expense budget shows the planned amounts of expenditures for selling, general, and administrative expenses for a future budget.

• It is a helpful key tool for planning, control, and decision making

4D1163 – Performance and Cost Analysis- Seminar -

© 2006 Manuel Fritsch, Patrick Wild, Christian Hellwig Page 10

?

?

?

?

?

?

Thank you for your attention!

We will gladly answer

your questions!