46th annual taxation conference appraisal for ad valorem ... · 46th annual taxation conference...

TRANSCRIPT

46th Annual Taxation ConferenceAPPRAISAL for AD VALOREM

TAXATIONTAXATIONof Communications, Energy and Transportation Properties

July 24 – 28, 2016

Building a Cap Rate StudyHow Could Anything Go Wrong?How Could Anything Go Wrong?

Robert F. ReillyWillamette Management Associates

Keith FuquaColonial Pipeline CompanyWillamette Management Associates

Chicago, Illinois [email protected](773) 399-4318

Colonial Pipeline CompanyAlpharetta, Georgia [email protected](678) 762-2200

• This presentation will provide an overview of the • This presentation will provide an overview of the process of developing a unit valuation capitalization rate (“cap rate”) study.rate ( cap rate ) study.

• We will discuss some of the more complicated elements of the process and what you, the analyst, p y , y ,need to consider.

• We want to encourage interactive discussion among those in attendance.

• We want to give anyone who wants to build their own cap rate an analytical framework to consider.

• So let’s get started!!!2

• Our format will have Keith assume the role of an analyst • Our format will have Keith assume the role of an analyst who is building a cap rate study for the first time. As moderator, Robert will assume the role of the independent valuation advisor who helps navigate Keith through the process.

W ld lik h di i i h • We would like the audience to participate as much as you want. So, please ask questions and provide comments as we go.comments as we go.

• We realize that this topic deserves a 4-hour seminar. So this discussion will be a general overview of how the cap rate development process works. Hopefully, this format will be both informative and interesting. 3

• Consider the objective of the valuation analysis

• Develop the appropriate capital structure

• Develop a cost of debt rate component

• Develop a cost of equity rate component

• Arrive at a final capitalization rate conclusionp

4

Before we begin the quantitative or qualitative cap rate Before we begin the quantitative or qualitative cap rate development analysis, we should understand the valuation assignment:valuation assignment:

• What is the unit of operating property subject to valuation?

• What is the valuation date?

• What is the appropriate standard of value?What is the appropriate standard of value?

• Do we need to develop a yield capitalization rate or a direct capitalization rate?p

• What is the level of income that we will capitalize in our valuation?

5

• Is there any statutory guidance judicial precedent or • Is there any statutory guidance, judicial precedent, or administrative ruling in the subject taxing jurisdiction that we (the taxpayer, the taxing authority, or the that we (the taxpayer, the taxing authority, or the independent analyst) have to comply with?

• How do the answers to the above questions affect qour selection of:– the appropriate industry?– the appropriate capital structure?– the income tax rate?– the expected long-term growth rate?the expected long term growth rate?– the consideration of flotation costs?– other cap-rate-related valuation variables?

6

• Selecting comparable companies to use in the • Selecting comparable companies to use in the cap rate analysis

D V l Li St d d & P ' – Do we use Value Line, Standard & Poor's, or some other data source?

What criteria will we use to both select and reject – What criteria will we use to both select and reject potential comparable companies?•SIC code Key word search Not penny stock SIC code Key word search Not penny stock •Size Comparative Not an acquisition•Geography profitability target•Pure play Active trading Same income tax

consideration Not in bankruptcy status 7

• How do we define the subject company industry? • How do we define the subject company industry? By SIC code? By some other measure?

Are we selecting comparable public companies or • Are we selecting comparable public companies or guideline public companies?

I th diff b t bl • Is there a difference between comparable companies and guideline companies?

If h d th t ff t th th d i • If so, how does that affect the other procedures in the cap rate analysis?

8

• Are the comparable company selection criteria • Are the comparable company selection criteria the same for this income approach procedure as they would be for a market approach (say stock they would be for a market approach (say, stock and debt method) analysis?

• Does it matter which data source we use to select • Does it matter which data source we use to select the comparable companies?

• Is our selection criteria documented?• Is our selection criteria documented?

• Is our selection criteria replicable?

9

• Do we also have a documented rejection criteria?

• Bloomberg• Bloomberg

• FactSet

• MergentOnline

• Pitchbook

• S&P Capital IQ

• Thomson ONE

10

• We want to select companies that do exactly what our • We want to select companies that do exactly what our subject company does: move refined petroleum products. For example, we want to select Buckeye, p p , y ,Plains American, Plantation, Explorer, Express, Platts, Keystone!

• The problem is that many of these operating companies either (1) are just a small part of a much bigger corporate structure or (2) are privately held like bigger corporate structure or (2) are privately held like our subject company!

• Therefore our selected comparable companies end up • Therefore, our selected comparable companies end up being a blend of liquids lines and companies that operate liquids lines.

11

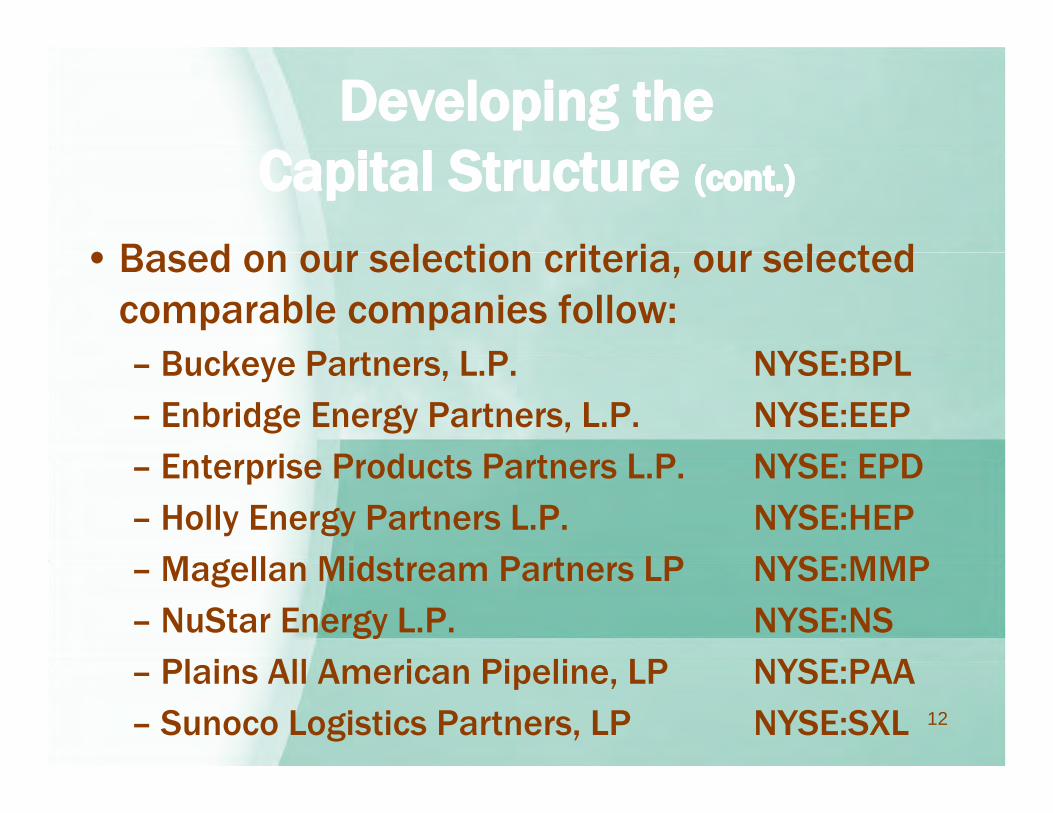

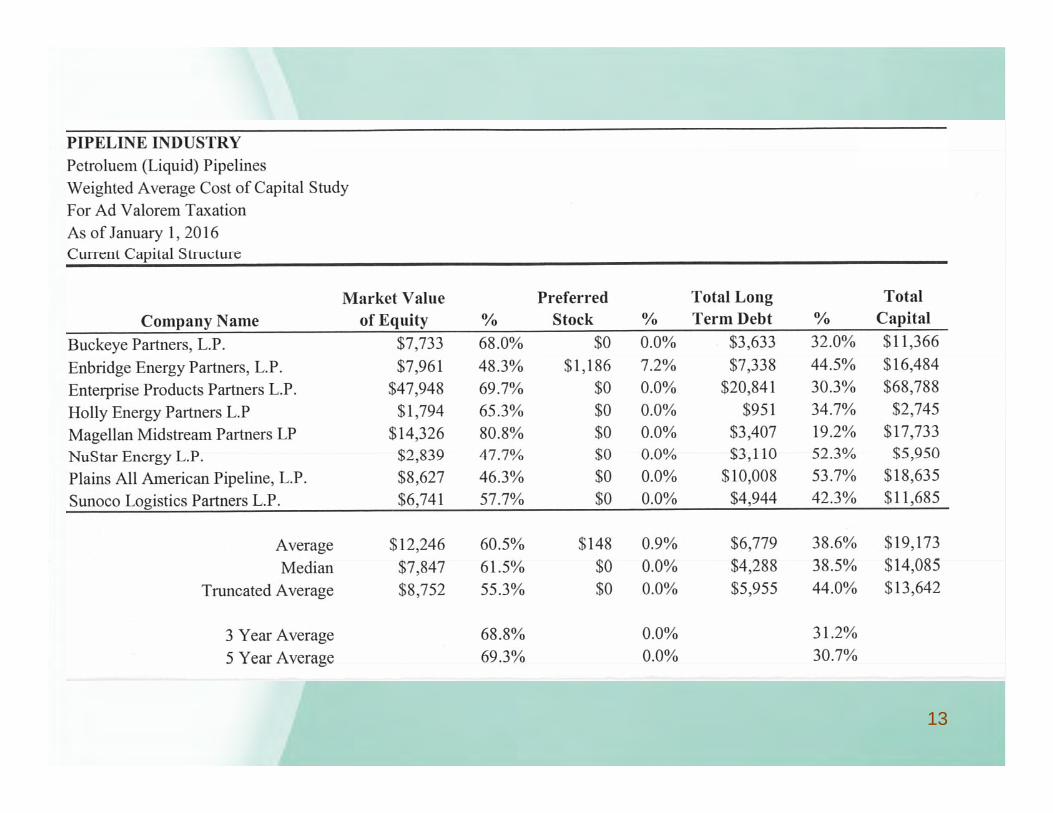

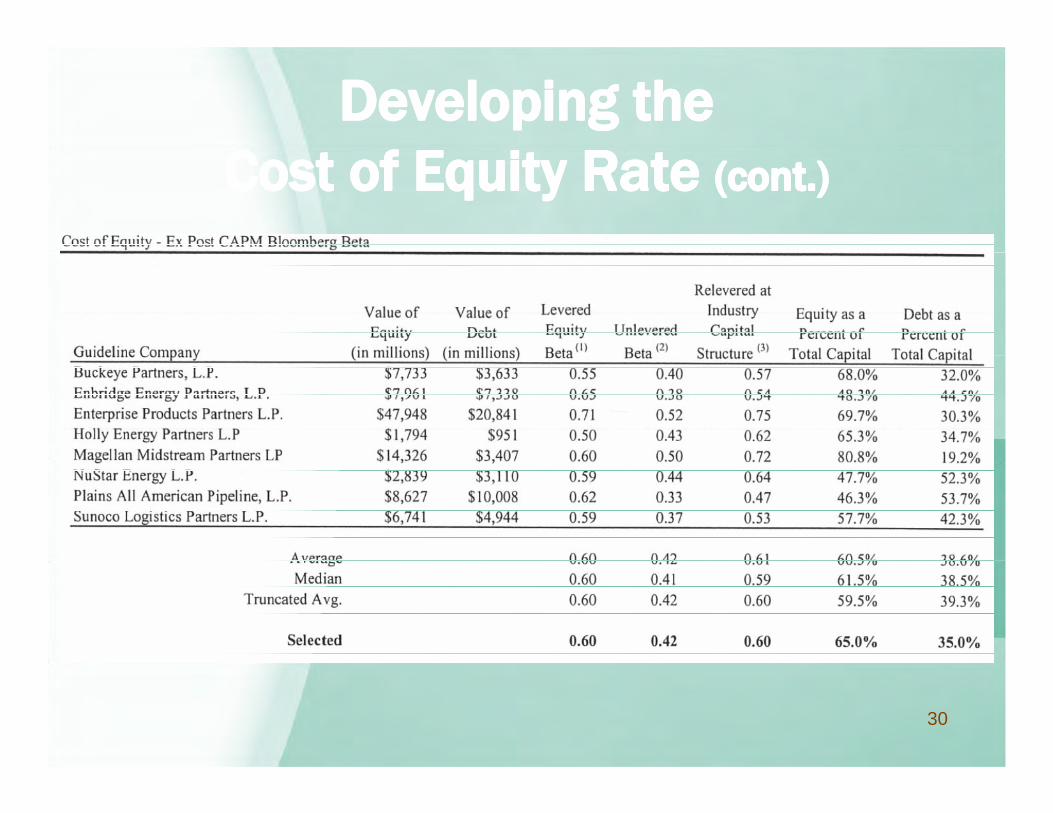

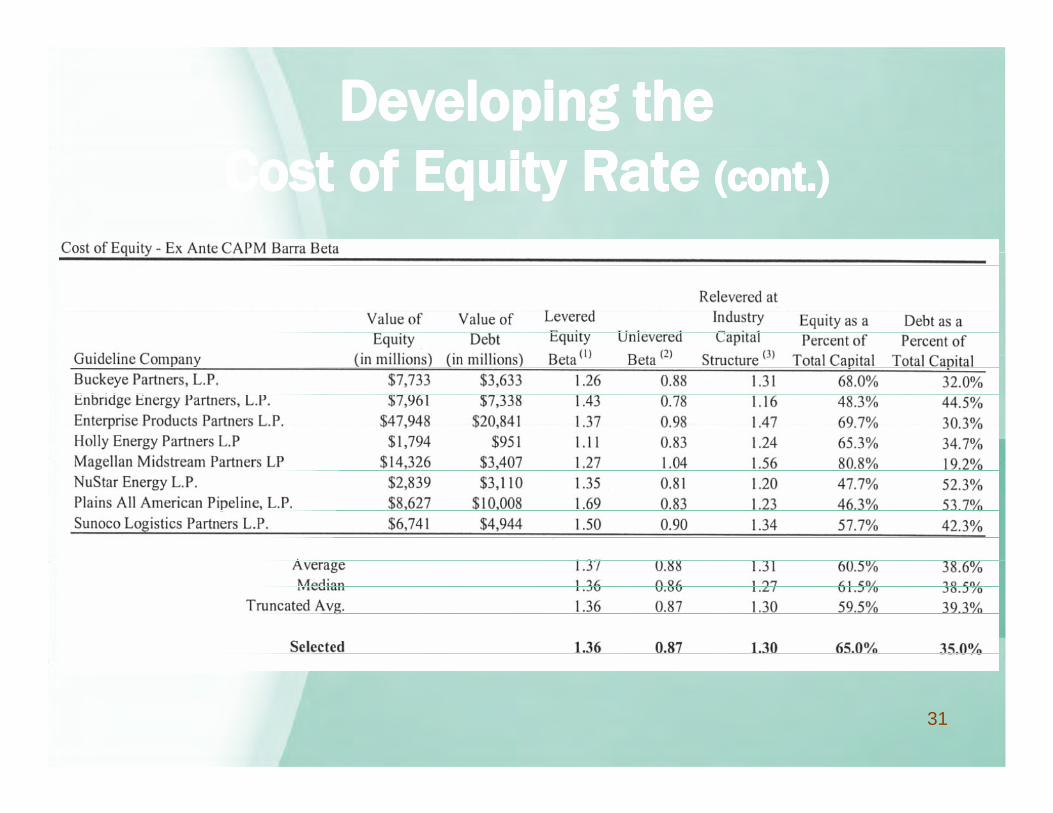

• Based on our selection criteria our selected • Based on our selection criteria, our selected comparable companies follow:

B k P t L P NYSE BPL– Buckeye Partners, L.P. NYSE:BPL– Enbridge Energy Partners, L.P. NYSE:EEP

E t i P d t P t L P NYSE EPD– Enterprise Products Partners L.P. NYSE: EPD– Holly Energy Partners L.P. NYSE:HEP

M g ll Mid t P t LP NYSE MMP– Magellan Midstream Partners LP NYSE:MMP– NuStar Energy L.P. NYSE:NS

Pl i All A i Pi li LP NYSE PAA– Plains All American Pipeline, LP NYSE:PAA– Sunoco Logistics Partners, LP NYSE:SXL 12

13

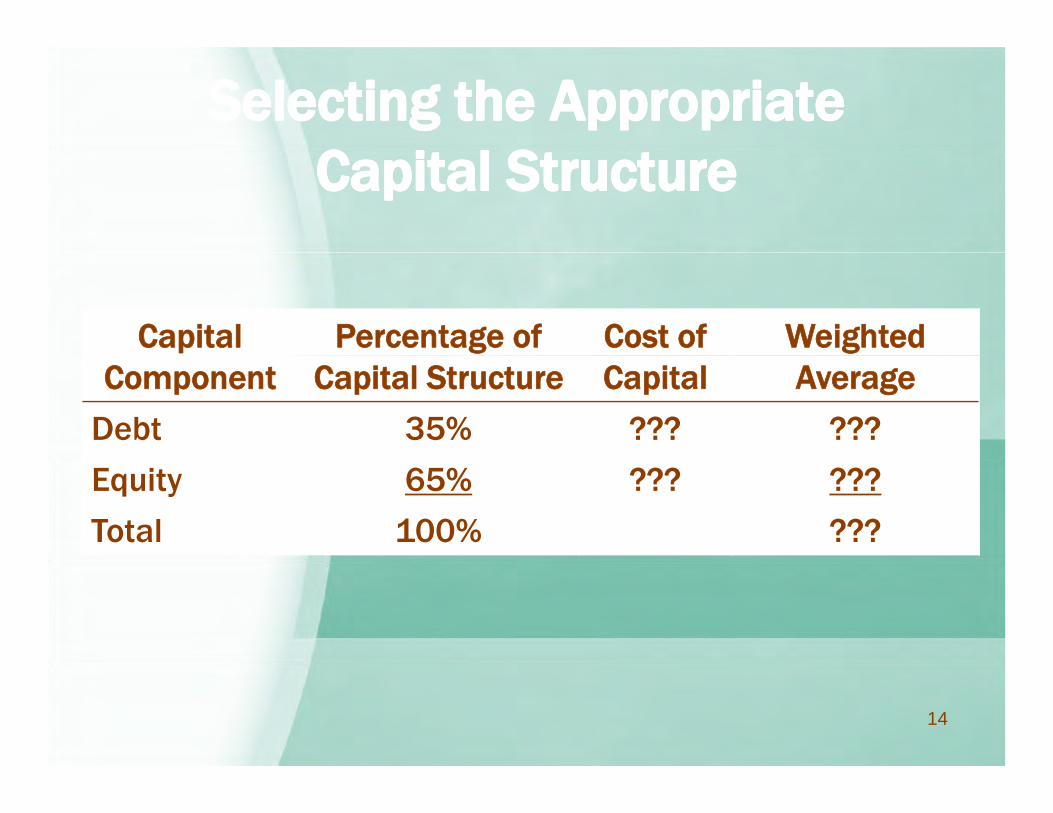

Capital Percentage of Cost of WeightedComponent Capital Structure Capital Average

Debt 35% ??? ???

Equity 65% ??? ???

Total 100% ???

14

• Do we select the industry average capital • Do we select the industry average capital structure?

Do we select the industry median capital • Do we select the industry median capital structure?

I th t l t • Is there a reason to select a mean versus a median?

D id th bj t it l • Do we consider the subject company capital structure?

• Do we consider the most comparable company capital structure? 15

• Do we round the selected capital structure?• Do we round the selected capital structure?

• How does our rounding convention affect our final cap rate conclusion?cap rate conclusion?

• How do we document the selection of the i t it l t t ?appropriate capital structure?

• Is that capital structure selection process li bl ?replicable?

16

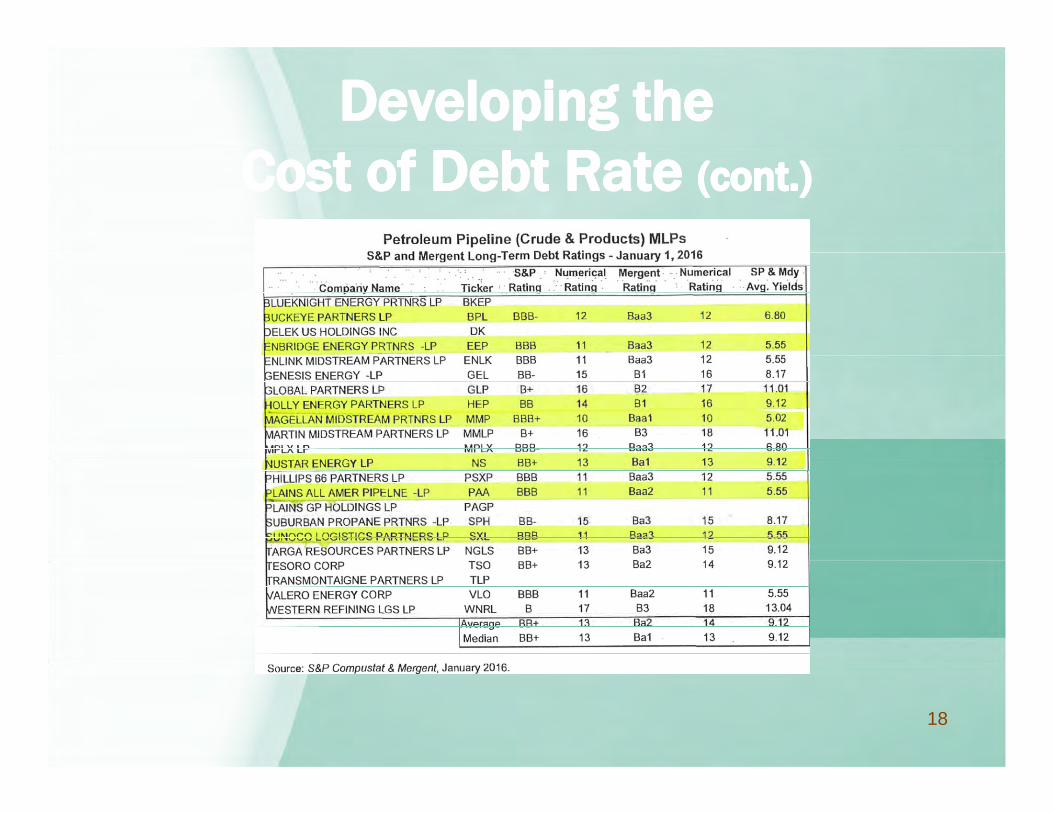

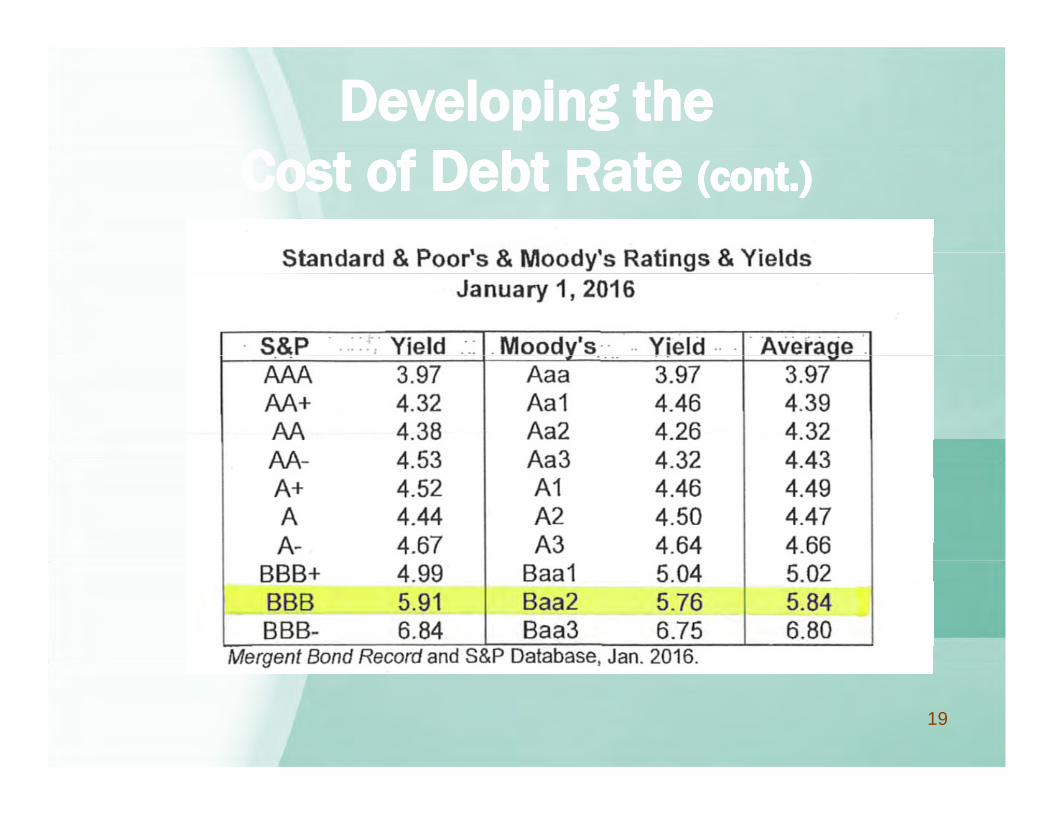

• Next, we want to consider what the market tells us about our selected comparable companies us about our selected comparable companies and about their respective costs of debt.

L t’ id th t d t f d bt d t f • Let’s consider the reported cost of debt data from S&P Compustat and Mergent

17

18

19

• Different data sources indicate different costs of • Different data sources indicate different costs of debt capital for the same comparable company

Do we rely on only the public companies • Do we rely on only the public companies considered in our capital structure analysis?

O d l b d i d t l f • Or, do we rely on a broader industry sample of comparable companies?

D l t di t f d bt?• Do we select a mean or a median cost of debt?

• Do we select the cost of debt of the most comparable companies?

20

• Do we consider the subject company cost of debt • Do we consider the subject company cost of debt capital?

• Do we round the selected cost of debt capital?• Do we round the selected cost of debt capital?

• Are all of the public company bonds actively traded?

• Are all of the bonds from public companies that have • Are all of the bonds from public companies that have the same income tax status of the subject company?

• How do we document the cost of debt selection • How do we document the cost of debt selection process?

• Is that cost of debt selection process replicable? Is that cost of debt selection process replicable?

21

Capital Percentage of Cost of WeightedComponent Capital Structure Capital Average

Debt 35% 5.84% 2.04%

Equity 65% ??? ???

Total 100% ???

22

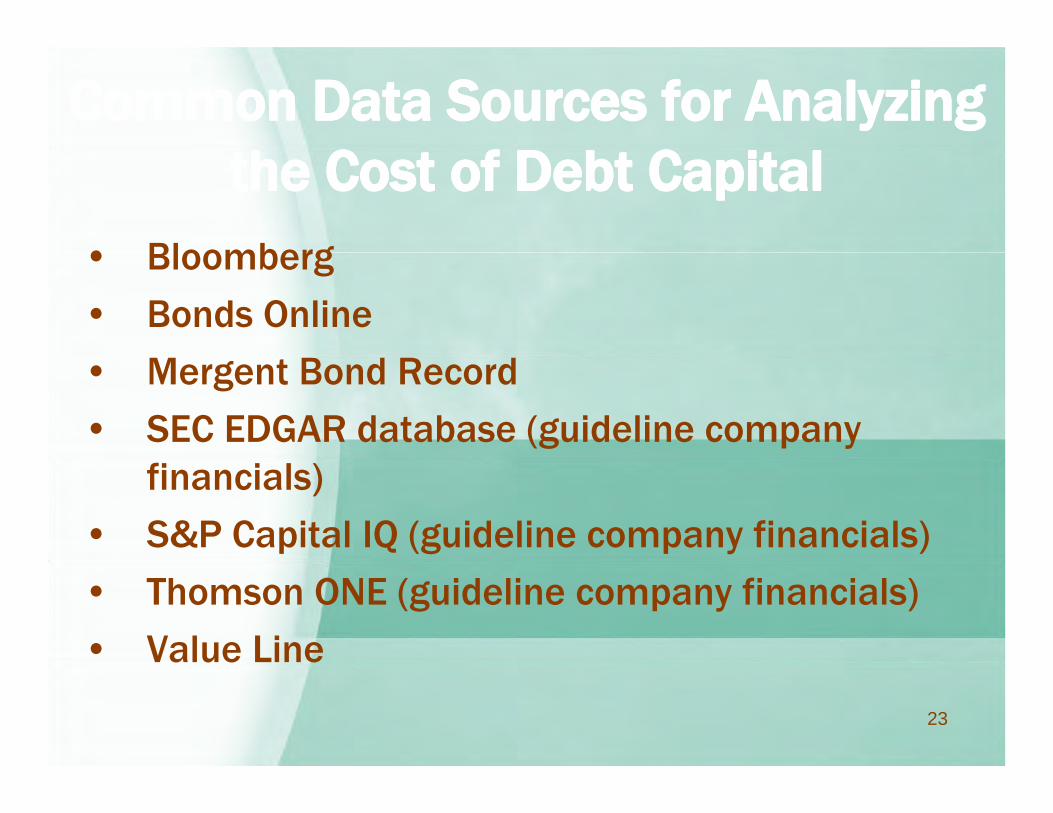

• Bloomberg• Bloomberg

• Bonds Online

• Mergent Bond Record

• SEC EDGAR database (guideline company financials)

• S&P Capital IQ (guideline company financials)

• Thomson ONE (guideline company financials)

• Value Line

23

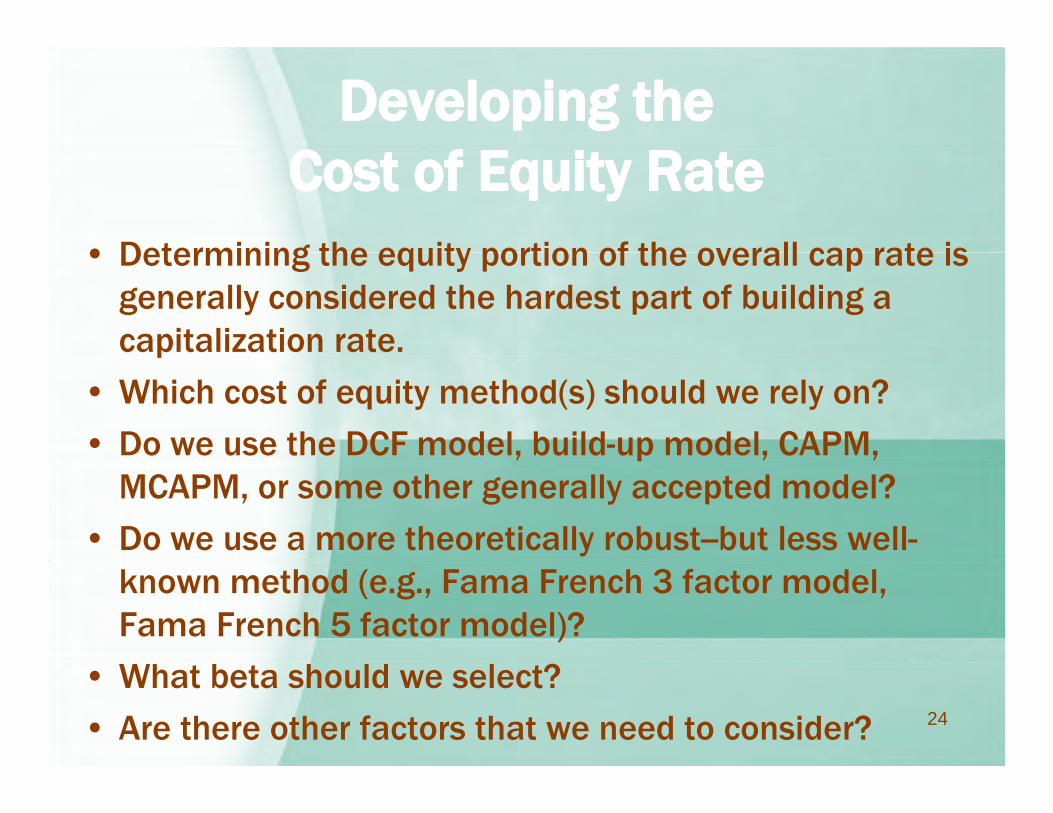

• Determining the equity portion of the overall cap rate is • Determining the equity portion of the overall cap rate is generally considered the hardest part of building a capitalization rate.p

• Which cost of equity method(s) should we rely on?

• Do we use the DCF model, build-up model, CAPM, , p , ,MCAPM, or some other generally accepted model?

• Do we use a more theoretically robust--but less well-known method (e.g., Fama French 3 factor model, Fama French 5 factor model)?

• What beta should we select?

• Are there other factors that we need to consider? 24

25

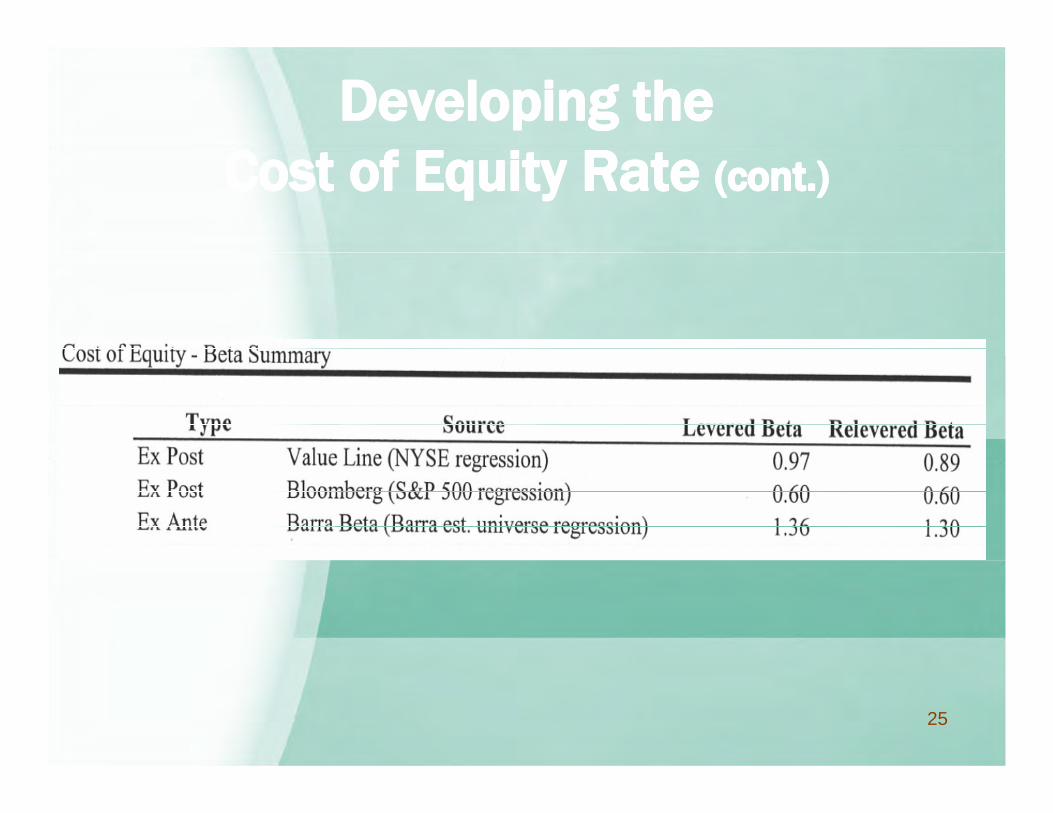

• Do we use the same comparable companies that we • Do we use the same comparable companies that we selected for our capital structure analysis?

• Do we use a broader (say SIC composite) industry • Do we use a broader (say, SIC composite) industry beta metric?

• Do we use the industry large composite or the Do we use the industry large composite or the industry small composite—to reflect our subject company size?

• Do we consider the subject company beta?

• Do we use a mean beta or median beta?

• Or, do we consider the betas for the most comparable companies?

26

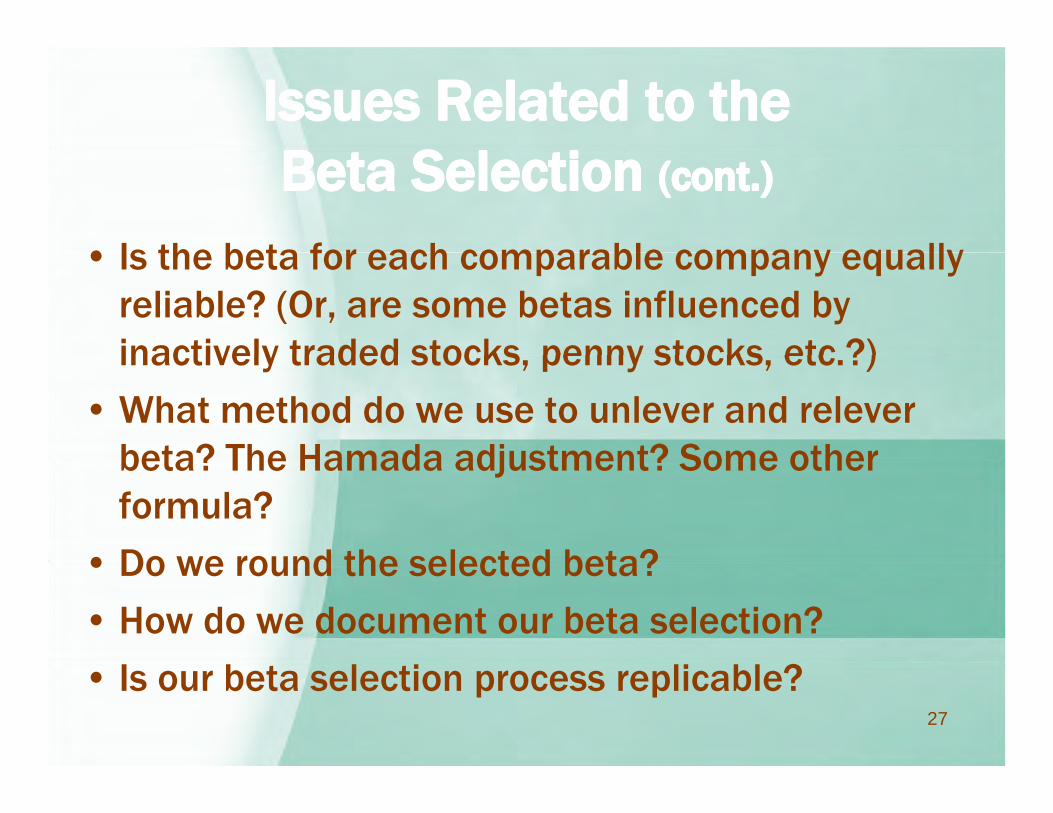

• Is the beta for each comparable company equally • Is the beta for each comparable company equally reliable? (Or, are some betas influenced by inactively traded stocks penny stocks etc ?)inactively traded stocks, penny stocks, etc.?)

• What method do we use to unlever and relever beta? The Hamada adjustment? Some other beta? The Hamada adjustment? Some other formula?

• Do we round the selected beta?• Do we round the selected beta?

• How do we document our beta selection?

• Is our beta selection process replicable?27

• Bloomberg• Bloomberg• Compustat• S&P Capital IQ• S&P Capital IQ• Value Line• Duff & Phelps Valuation Handbook Industry Cost • Duff & Phelps Valuation Handbook: Industry Cost

of Capital (for industry betas)• Barra Beta Book• Barra Beta Book

28

29

30

31

Cost of Equity - Ex Poste CAPM Calculation

Debt Preferred Equity Levered Relevered Weight Weight Weight Beta Beta

Selected data for Subject (Value Line beta) 35.0% 0.0% 65.0% 0.97 0.89

After-Tax Cost of Equity:

Long-Horizon

ERPSupply-

Side ERPRelevered beta 0 89 0 89

CAPM

Relevered beta 0.89 0.89 Market risk premium 5.80% 5.10% Beta-adjusted industry risk premium 5.16% 4.54% Add: Risk-free rate: normalized return on long-term Treasury bonds 4.00% 4.00% CAPM cost of equity 9.16% 8.54% Size risk premium 0.91% 0.91% MCAPM cost of equity 10.07% 9.45%

E ti t d C t f E it 9 86%Estimated Cost of Equity 9.86%

Debt Weight

Preferred Weight

Equity Weight

Levered Beta

Relevered Beta

Selected data for Subject (Bloomberg betas) 35.0% 0.0% 65.0% 0.60 0.60

CAPM

After-Tax Cost of Equity:

Long-Horizon

ERPSupply-

Side ERP Relevered beta 0.60 0.60 Market risk premium 5.80% 5.10% Beta-adjusted industry risk premium 3.50% 3.08% Add: Risk-free rate: normalized return on long-term Treasury bonds 4.00% 4.00%

CAPM cost of equity 7 50% 7 08%

32

CAPM cost of equity 7.50% 7.08% Size risk premium 0.91% 0.91% MCAPM cost of equity 8.41% 7.99%

Estimated Cost of Equity 8.27%

Cost of Equity - Ex Ante CAPM CalculationCost of Equity Ex Ante CAPM Calculation

Debt Weight

Preferred Weight

Equity Weight

Levered Beta

Relevered Beta

Selected data for Subject (Barra beta) 35.0% 0.0% 65.0% 1.36 1.30

After-Tax Cost of Equity:

Single-Stage DCF

ERPMulti-Stage DCF ERP

Merrill Lynch Est.

ERP

D&P Conditional

ERPRelevered beta 1.30 1.30 1.30 1.30

CAPM

Relevered beta 1.30 1.30 1.30 1.30 Market risk premium 9.50% 7.58% 7.10% 5.00% Beta-adjusted industry risk premium 12.32% 9.83% 9.21% 6.48% Add: Risk-free rate: normalized return on long-term Treasury bonds 4.00% 4.00% 4.00% 4.00% CAPM cost of equity 16.32% 13.83% 13.21% 10.48% Size risk premium 0.91% 0.91% 0.91% 0.91%p MCAPM cost of equity 17.23% 14.74% 14.12% 11.39%

Estimated Cost of Equity 12.61%

33

34

35

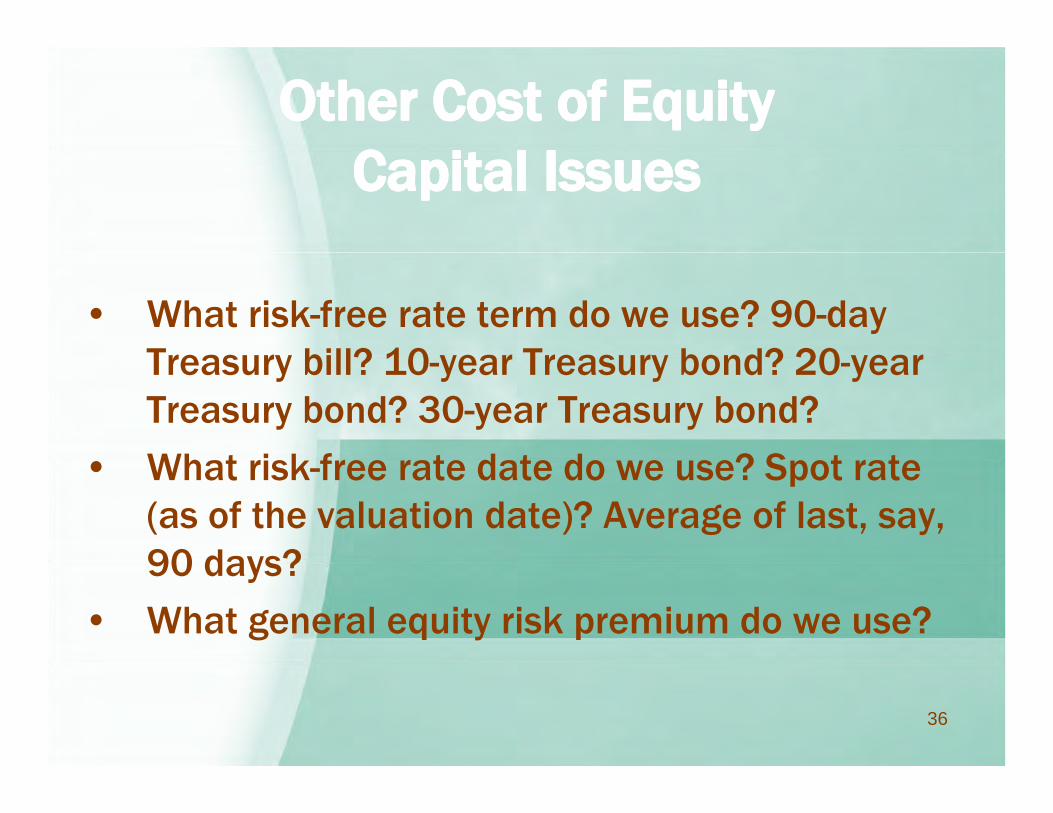

• What risk-free rate term do we use? 90-day Treasury bill? 10 year Treasury bond? 20 year Treasury bill? 10-year Treasury bond? 20-year Treasury bond? 30-year Treasury bond?

Wh t i k f t d t d ? S t t • What risk-free rate date do we use? Spot rate (as of the valuation date)? Average of last, say, 90 days?90 days?

• What general equity risk premium do we use?

36

• What adjustments to the basic CAPM do we • What adjustments to the basic CAPM do we make?

Size risk premium adjustments– Size risk premium adjustments• What size decile do we select?

• How do we justify the selection of a size risk premium?j y p

• Does our selection of a size risk premium bias the income approach value indication?

C ifi i k i dj t t– Company-specific risk premium adjustments• What company-specific factors do we adjust for?

• How large of a company-specific adjustment do we make?How large of a company specific adjustment do we make?

• How do we justify the selection of a company-specific risk premium?

37

• Is the CAPM different from the MCAPM? When is • Is the CAPM different from the MCAPM? When is it appropriate to use which model?

How does a significant range of cost of equity • How does a significant range of cost of equity indications affect the final selected cost of equity capital?equity capital?

• Do we round our cost of equity capital estimate?

H d d t th t f it it l • How do we document the cost of equity capital selection process?

• Is that cost of equity capital selection process replicable? 38

39

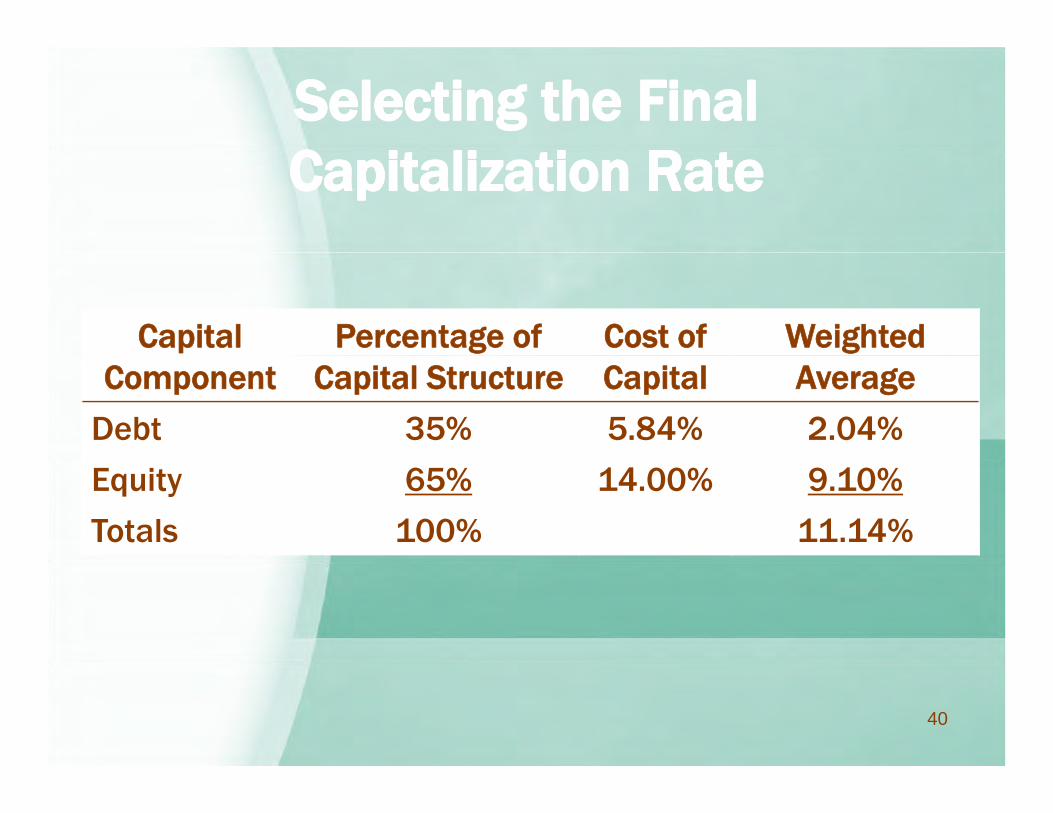

Capital Percentage of Cost of WeightedComponent Capital Structure Capital Average

Debt 35% 5.84% 2.04%

Equity 65% 14.00% 9.10%

Totals 100% 11.14%

40

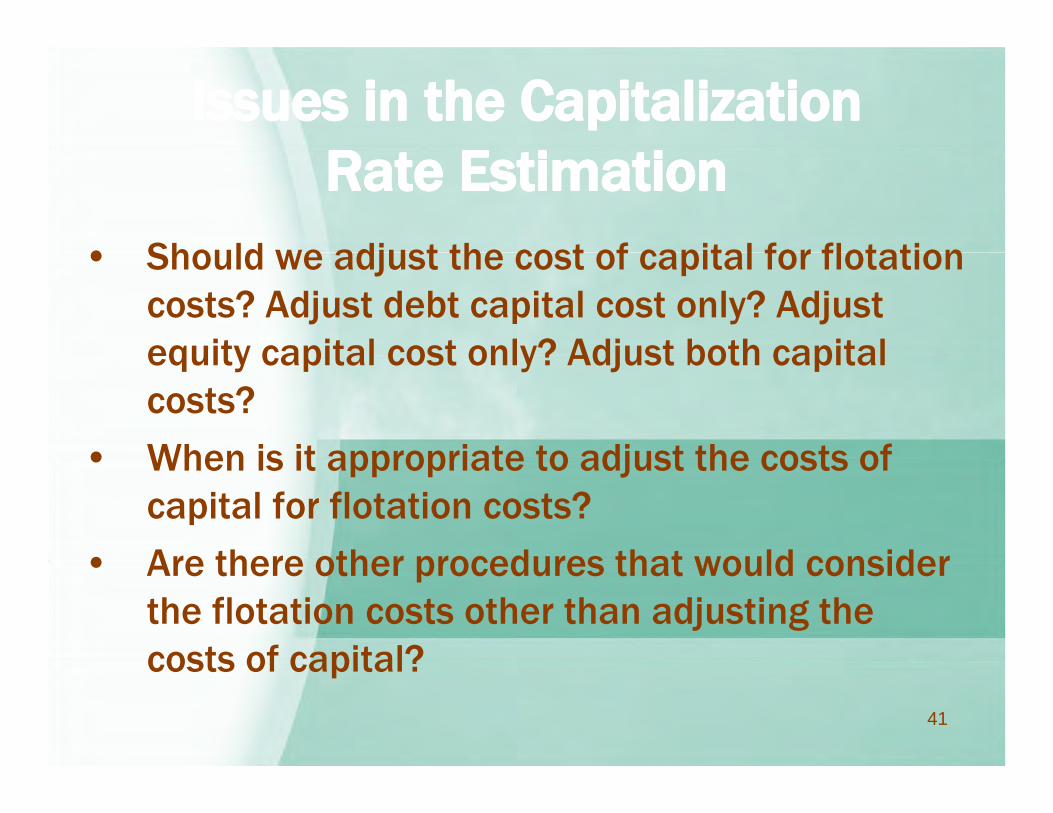

• Should we adjust the cost of capital for flotation • Should we adjust the cost of capital for flotation costs? Adjust debt capital cost only? Adjust equity capital cost only? Adjust both capital equity capital cost only? Adjust both capital costs?

• When is it appropriate to adjust the costs of • When is it appropriate to adjust the costs of capital for flotation costs?

• Are there other procedures that would consider • Are there other procedures that would consider the flotation costs other than adjusting the costs of capital?costs of capital?

41

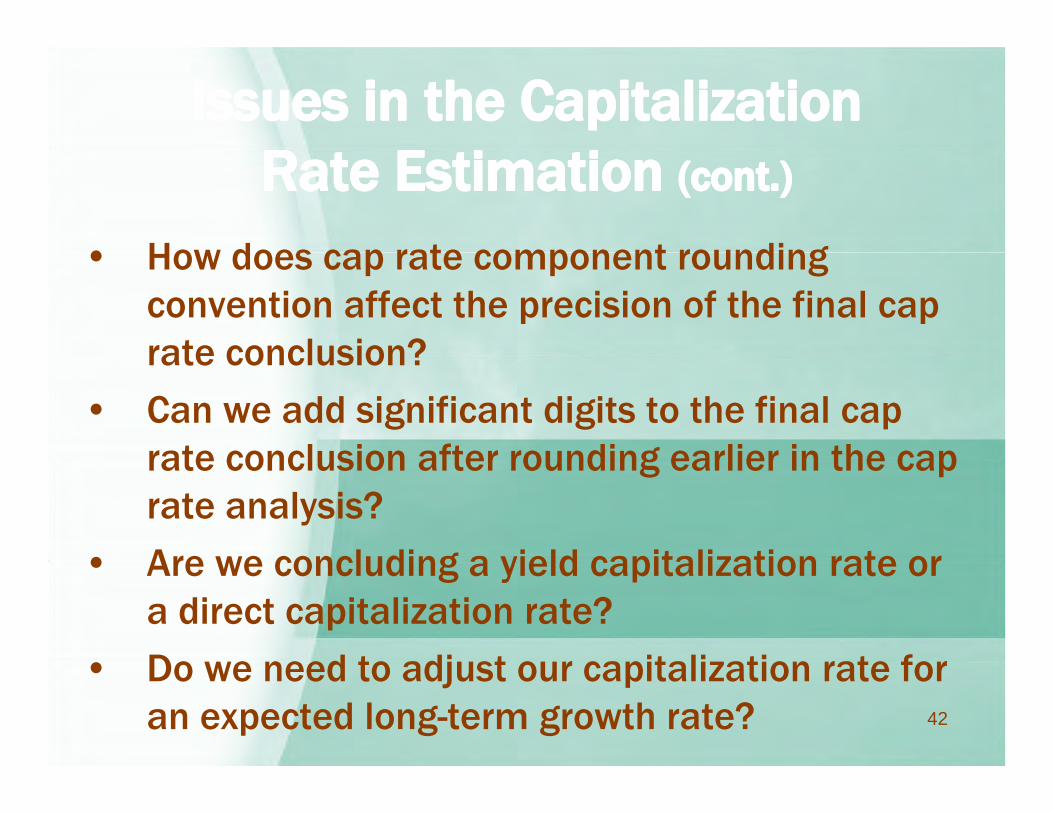

• How does cap rate component rounding • How does cap rate component rounding convention affect the precision of the final cap rate conclusion?rate conclusion?

• Can we add significant digits to the final cap rate conclusion after rounding earlier in the cap rate conclusion after rounding earlier in the cap rate analysis?

• Are we concluding a yield capitalization rate or • Are we concluding a yield capitalization rate or a direct capitalization rate?

• Do we need to adjust our capitalization rate for • Do we need to adjust our capitalization rate for an expected long-term growth rate? 42

• How do we select (and justify and document) • How do we select (and justify and document) the expected long-term growth rate?

Is the selected long term growth rate different • Is the selected long-term growth rate different for a unit valuation than it is for a business valuation?valuation?

• Is the concluded capitalization rate consistent with the measure of income that we will apply it with the measure of income that we will apply it to?

43

• The selected capitalization rate should be • The selected capitalization rate should be consistent with the purpose and objective of the analysis—including the unit of operating analysis—including the unit of operating property subject to taxation.

• The selected capitalization rate should be • The selected capitalization rate should be consistent with the income metric to which we will apply itwill apply it.

• The selected capitalization rate should be consistent with any required statutory authority consistent with any required statutory authority, judicial precedent, or administrative ruling. 44

• We should acknowledge that the selected • We should acknowledge that the selected capitalization rate will be influenced by the experience and judgment of the individual experience and judgment of the individual valuation analyst.

• That said, the selection (and rejection) of the That said, the selection (and rejection) of the individual valuation variables and the selection (and rejection) of the cost of capital ( j ) pmeasurement methods should be documented.

• Through that documentation, the capitalization g prate selection process should be transparent and replicable.

45