4 april 2011 asia equities daily focus periodicalimg.jrjimg.cn/2011/04/20110404151414415.pdfasia...

TRANSCRIPT

Asia Pan-Asia Strategy

4 April 2011

Asia Equities Daily Focus Today's research headlines Asian Edition

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Periodical

Asian Index Closings EQUITIES Close 1D Chg %Chg

SHSZ300 3272.73 1.53 4.62 HSCEI 13451.48 1.02 5.98 HSI 23801.90 1.17 3.33 TWSE 8705.13 0.25 -2.98 KOSPI 2121.01 0.68 3.41 FSSTI 3120.47 0.47 -2.18 KLCI 1555.38 0.66 2.40 SENSEX 19420.39 -0.13 -5.31 NIFTY 5826.05 -0.13 -5.03 SET 1064.35 1.61 3.06 JCI 3707.49 0.78 0.11 PCOMP 4129.54 1.84 -1.70 ASX200 4861.80 0.49 2.46 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.55 0.01 0.91 HK$ 7.78 0.01 -0.06 NT$ 29.27 0.48 0.12 Won 1091.20 0.53 3.19 S$ 1.26 0.03 1.85 M$ 3.03 -0.01 1.26 Rupee 44.59 0.38 0.27 Baht 30.24 0.13 -0.60 Rupiah 8696.00 0.14 3.45 Peso 43.36 -0.01 1.01 A$ 1.04 0.46 1.40

Source: Bloomberg Finance LP

Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 107.59 0.82 17.74 Brent 118.67 1.21 25.84 CRB 360.89 0.41 8.44 Copper 425.15 -1.13 -4.24 Gold (Spot) 1427.78 -0.32 0.49 Alum. (LME) 2648.00 0.72 7.21 Baltic Dry 1530.00 -0.97 -13.71

Source: Bloomberg Finance LP

DB CORPORATE ACCESS DB Access Indonesia Small Cap Corporate Day - SG 4/5 - 6 DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1

Research Team

Carissa Szeto Equity Focus (+852) 2203 6171 [email protected] Ching-Li Teo, CFA Equity Focus (+852) 2203 6206 [email protected]

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Nodita_ 1. 2.

TOP STORIES MSCI China Strategy Update Positive earnings momentum Hui Miao Page 5

China State Construction (3311.HK),HKD7.47 Buy Price Target HKD10.03

A fast-growing public housing developer; Initiate with Buy Tony Tsang Page 6

China Merchants Bank-H (3968.HK),HKD20.95 Buy Price Target HKD25.06

Valuation reflects superior quality, down to Hold Tracy Yu Page 7

China Macro Strategy PMI confirms positive macro trend Jun MaPage 8

RECOMMENDATION CHANGES

Acer Inc (2353.TW),TWD57.10 Hold Price Target TWD58.00

Downgrading to Hold on business model transition

Kc Kao

Page 9

ESTIMATE & TARGET PRICE CHANGES

Beijing Enterprises (0392.HK),HKD42.30 Buy Price Target HKD59.50

Growth to accelerate; Buy Eric ChengPage 10

LG Display (034220.KS),KRW35,450.00 Buy Price Target KRW43,000.00

Upside potential outweighs downsiderisk

Sc BaePage 11

Ascendas Real Estate (AEMN.SI),SGD2.00 Buy Price Target SGD2.28

Positioning for growth Gregory LuiPage 12

STRATEGY/ECONOMICS

US Equity Strategy Q1 2011 Earnings Preview Binky ChadhaPage 13

Exchange Rate Perspectives FX Intervention Can Brake, Not Break,

a Trend John Horner

Page 14

Asia Economics Special SBV raises the 7-day repo rate Juliana LeePage 15

Asia Economics Daily High but stable inflation in Asia Michael Spencer Page 16

Asia Rates Strategy Taking stock of issuance Sameer Goel Page 20

4 April 2011 Strategy Asia Equities Daily Focus

Page 2 Deutsche Bank AG/Hong Kong

Asia Local Markets Weekly Pick up in inflows Sameer Goel Page 21

Asia Credit Weekly A brief review of 1Q 2011 Gene Cheon Page 22

US Daily Economic Notes Solid employment growth to begetwage inflation

Joseph

LaVorgnePage 23

US Economics Weekly Jobs and prices to put the Fed in play Joseph

LaVorgnaPage 24

Global Commodities Daily Oil dynamics Adam

SieminskiPage 26

India Economics Weekly Understated WPI, Oct-Dec BOP, coreinfra sector growth

Taimur BaigPage 28

ADDITIONAL RESEARCH

China TMT Daily East meets west: Digital ads; also BIDU, GOOG

Alan Hellawell III Page 29

Tech Earnings Revisions Capitulation time for the bulls? Kishore Suratkal Page 30

Angang Steel (0347.HK),HKD10.64 Buy Price Target HKD15.00

On the improvement track; maintaining Buy

James KanPage 31

China CITIC Bank (0998.HK),HKD5.54 Buy Price Target HKD6.43

2010 NPAT up 50% YoY, boost by lower than expected costs

Tracy YuPage 32

China Mengniu Dairy (2319.HK),HKD20.10 Buy Price Target HKD27.00

Earnings growth to accelerate in 2011; maintaining Buy

Mabel WongPage 33

Dongfeng Motor (0489.HK),HKD12.78 Buy Price Target HKD17.80

Key takeaways from analyst briefing - Staying positive

Vincent HaPage 34

Guangdong Investment (0270.HK),HKD4.03 Buy Price Target HKD5.00

Positive surprise on dividend payout; Buy

Eric ChengPage 35

Shandong Weigao (1066.HK),HKD21.70 Buy Price Target HKD24.00

Unlocking value for JW Medical Jack HuPage 36

Weichai Power (2338.HK),HKD49.15 Hold Price Target HKD51.70

Normalizing growth; maintaining Hold Vincent HaPage 37

Taiwan Financials Pulse Money supply, rate hike, asset quality, Polaris merger

Nora HouPage 38

Automobiles & Components March US auto sales best ever for

Hyundai and Kia Sanjeev Rana

Page 39

Korean autos Carmakers' domestic sales up 8%, global sales up 11% YoY

Sanjeev RanaPage 40

Mapletree Logistics Trust (MAPL.SI),SGD0.90 Buy Price Target SGD1.06

Acquisition momentum continues Elaine KhooPage 41

Property Home prices slow in 1Q as measures take effect

Elaine KhooPage 42

DB CONFERENCE/CORPORATE DAY DB Access Indonesia Small Cap Corporate Day - SG 4/5 - 6 DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1

NDRs PT Nippon Indosari Corpindo (ROTI IJ) - HK 4/4 Evergrande Real Estate Group (3333 HK) - SG 4/5, SZX 4/6, PEK 4/8 PT Gajah Tunggal Tbk (GJTL IJ) - HK 4/7 - 8 NEW: China Railway Group (390 HK) - SG 4/11 - 12 New Oriental Education & Technology Group (EDU US) - HK 4/28 HTC Corporation (2498 TT) - SG 6/21 - 22, HK 6/23 - 24

DB ANALYST/SALES ROADSHOWS Tracy Yu & Sophia Lee: Regional Financial Strategy & HK Banks - HK 3/14 - 15, SG 3/16 - 18 Ajay Kapurd: Asia: Underperformance to continue? - HK 3/16 - 18 Rachman Koeswanto: Building Materials/Cement/Construction - SG 3/14 - 16, HK 3/17 - 18 Sc Bae: Korean Technology - SG 3/14 - 15, HK 3/16 - 18Taimur Baig: Economic outlook in India/Indonesia/Philippines - SG 3/17 - 18 Sanghi Han: Korea Construction and LS Corp./Utilities - HK 3/28 - 29, SG 3/30 - 31 Srinivas Rao: Telecom & Automotive - SG 3/28 - 29, HK 3/30 & 4/1 Christopher Wane: CROCI Global - HK 3/31 & 4/1, SEL 4/4, SG 4/5 - 6, PEK 4/7 John Kim: Korea Telecom - HK 4/1

DB INTERNATIONAL PRODUCT ROADSHOWS

Continental AG (CON GR) - HK 4/8 Lloyds Banking Group (LLOY LN) - PEK 4/13, HK 4/14, SG 4/15 Rod Lache: US Auto Industry - PEK 4/11, HK 4/14, SG 4/15 Marc Geall: European Software & IT - SG 4/12, HK 4/13 Torsten Slok, Chief International Economist: Global Economics - SEL 4/12, PEK 4/13, SG 4/14 China Shipping Container Liner (2866 HK): Metals & Mining - SG 4/12, HK 4/13, PEK 4/14 Fedex Corp. (FDX US) - HK 5/5, SG 5/6 Diageo (DGE LN) - HK 5/9, SG 5/10, PEK 5/11

Maxis (MXSC.KL),MYR5.39 Hold Price Target MYR4.60

Entering fixed-line market with launch of "Home Services"

Wei-Shi WuPage 43

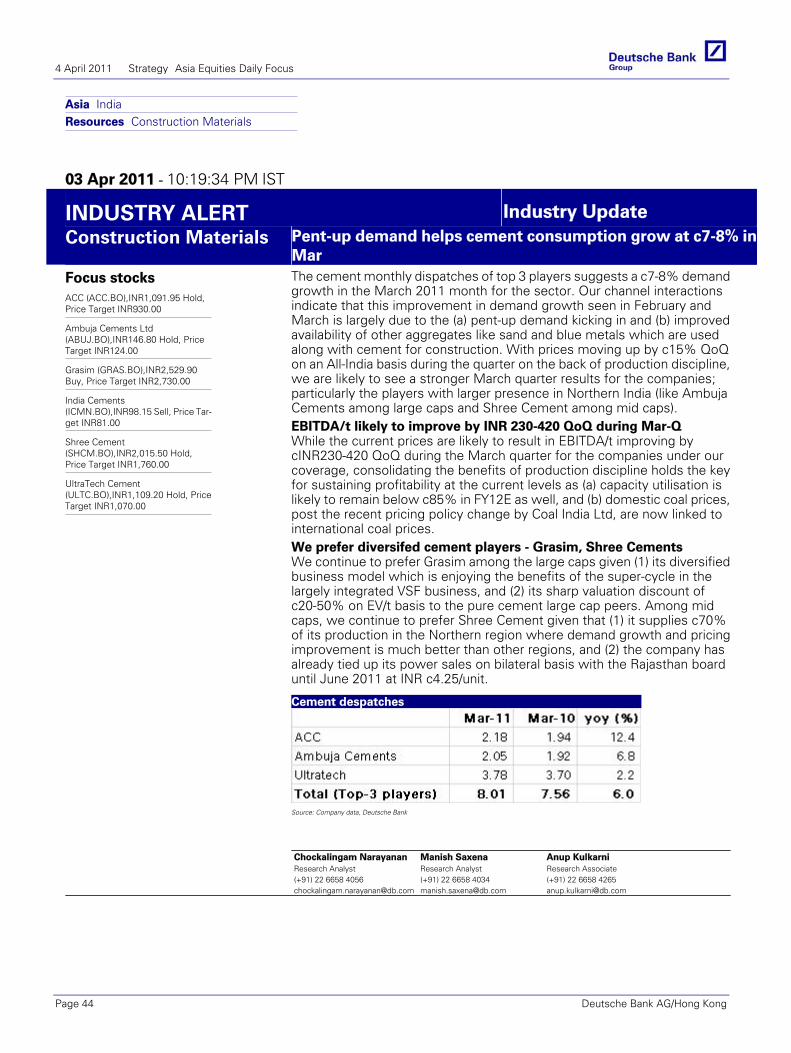

Construction Materials Pent-up demand helps cement consumption grow at c7-8% in Mar

Chockalingam Narayanan Page 44

HUL (HLL.BO),INR284.05 Hold Price Target INR266.00

Mean reversion Harrish ZaveriPage 45

Mahindra & Mahindra (MAHM.BO),INR710.10 Buy Price Target INR820.00

March-11 volumes: robust tractor volumes; UVs lag

Srinivas Rao

Page 46

Maruti Suzuki Limited (MRTI.BO),INR1,274.35 Hold Price Target INR1,500.00

March-11 volumes:strong numbers; maintain Hold

Srinivas Rao

Page 47

Tata Motors Ltd (TAMO.BO),INR1,242.90 Buy Price Target INR1,465.00

March-11 volumes: in line nos; maintain as top pick

Srinivas Rao

Page 48

TVS Motor (TVSM.BO),INR61.75 Buy Price Target INR92.00

March-11 volumes: strong momentum; maintain Buy

Amyn PiraniPage 49

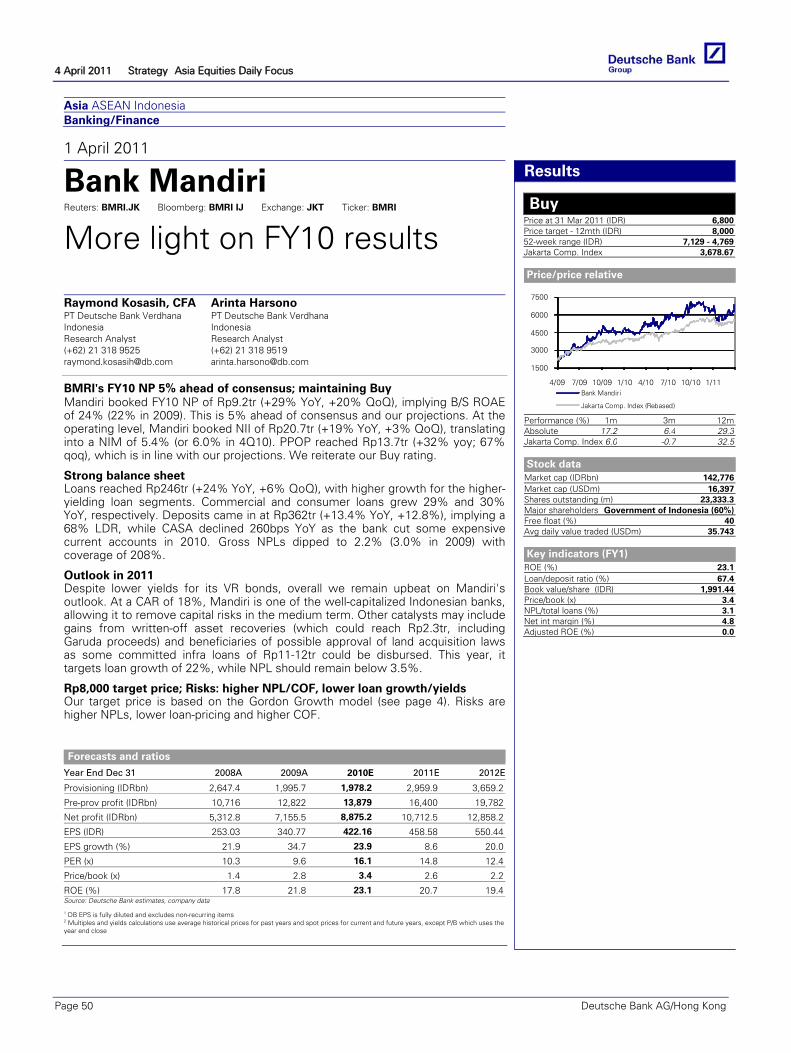

Bank Mandiri (BMRI.JK),IDR6,850.00 Buy Price Target IDR8,000.00

More light on FY10 results Raymond Kosasih Page 50

Bumi (BUMI.JK),IDR3,325.00 Hold NA

First take on FY10 - NP up by 63% YoY

Cherie KhoengPage 51

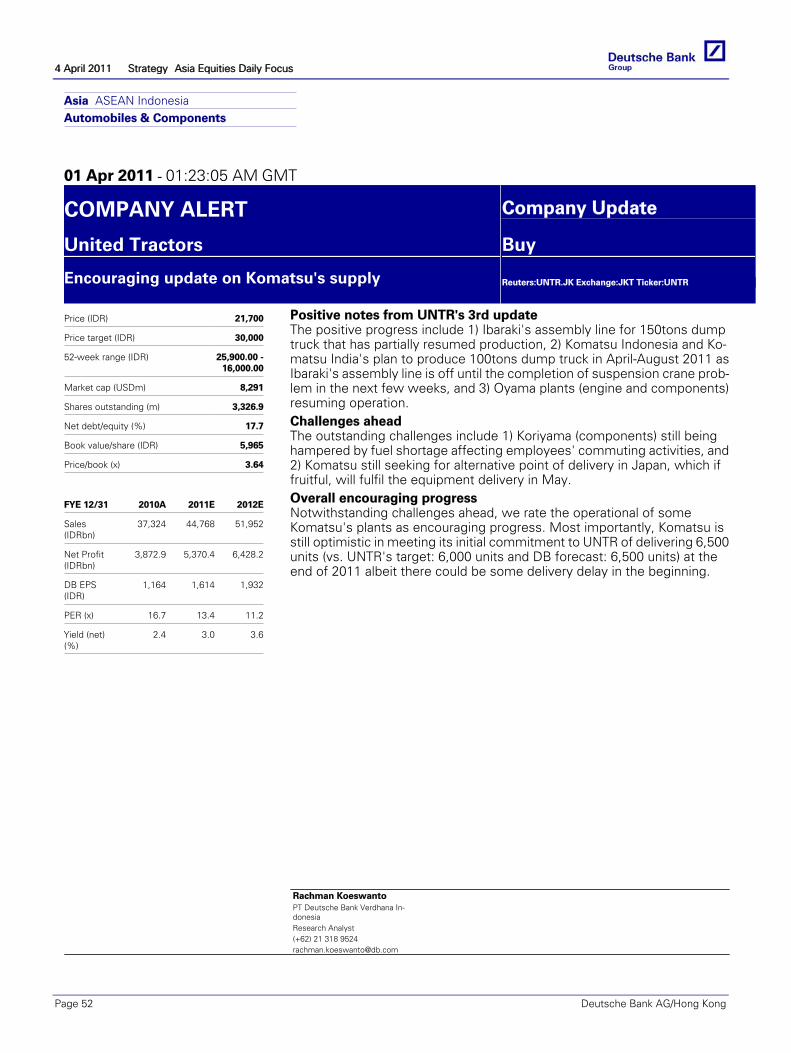

United Tractors (UNTR.JK),IDR21,450.00 Buy Price Target IDR30,000.00

Encouraging update on Komatsu's supply

Rachman Koeswanto Page 52

Kasikornbank (KBAN.BK),THB130.50 Buy Price Target THB164.00

Looking for solid 1Q11 earnings Worawat Saisuphatphol Page 53

Siam Cement (SCC.BK),THB353.00 Buy Price Target THB434.00

Takeaways from SCC Reverse Roadshow

Sansanee Srijamjuree Page 54

The notes and reports contained in this Daily are all excerpts of previously published documents. Please refer to the published notes on our web site for details on risks, valuations and earnings changes

4 April 2011 Strategy Asia Equities Daily Focus

Page 4 Deutsche Bank AG/Hong Kong

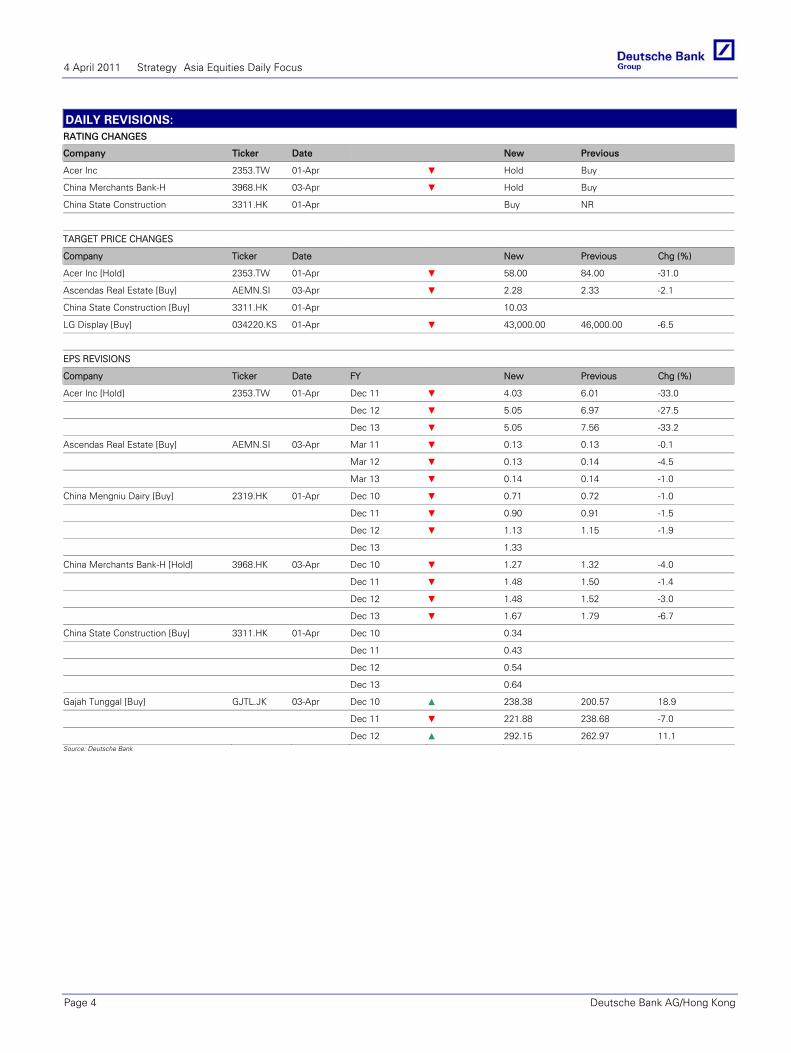

DAILY REVISIONS: RATING CHANGES

Company Ticker Date New Previous

Acer Inc 2353.TW 01-Apr ▼ Hold Buy

China Merchants Bank-H 3968.HK 03-Apr ▼ Hold Buy

China State Construction 3311.HK 01-Apr Buy NR

TARGET PRICE CHANGES

Company Ticker Date New Previous Chg (%)

Acer Inc [Hold] 2353.TW 01-Apr ▼ 58.00 84.00 -31.0

Ascendas Real Estate [Buy] AEMN.SI 03-Apr ▼ 2.28 2.33 -2.1

China State Construction [Buy] 3311.HK 01-Apr 10.03

LG Display [Buy] 034220.KS 01-Apr ▼ 43,000.00 46,000.00 -6.5

EPS REVISIONS

Company Ticker Date FY New Previous Chg (%)

Acer Inc [Hold] 2353.TW 01-Apr Dec 11 ▼ 4.03 6.01 -33.0

Dec 12 ▼ 5.05 6.97 -27.5

Dec 13 ▼ 5.05 7.56 -33.2

Ascendas Real Estate [Buy] AEMN.SI 03-Apr Mar 11 ▼ 0.13 0.13 -0.1

Mar 12 ▼ 0.13 0.14 -4.5

Mar 13 ▼ 0.14 0.14 -1.0

China Mengniu Dairy [Buy] 2319.HK 01-Apr Dec 10 ▼ 0.71 0.72 -1.0

Dec 11 ▼ 0.90 0.91 -1.5

Dec 12 ▼ 1.13 1.15 -1.9

Dec 13 1.33

China Merchants Bank-H [Hold] 3968.HK 03-Apr Dec 10 ▼ 1.27 1.32 -4.0

Dec 11 ▼ 1.48 1.50 -1.4

Dec 12 ▼ 1.48 1.52 -3.0

Dec 13 ▼ 1.67 1.79 -6.7

China State Construction [Buy] 3311.HK 01-Apr Dec 10 0.34

Dec 11 0.43

Dec 12 0.54

Dec 13 0.64

Gajah Tunggal [Buy] GJTL.JK 03-Apr Dec 10 ▲ 238.38 200.57 18.9

Dec 11 ▼ 221.88 238.68 -7.0

Dec 12 ▲ 292.15 262.97 11.1 Source: Deutsche Bank

Asia Hong Kong Strategy Update

1 April 2011

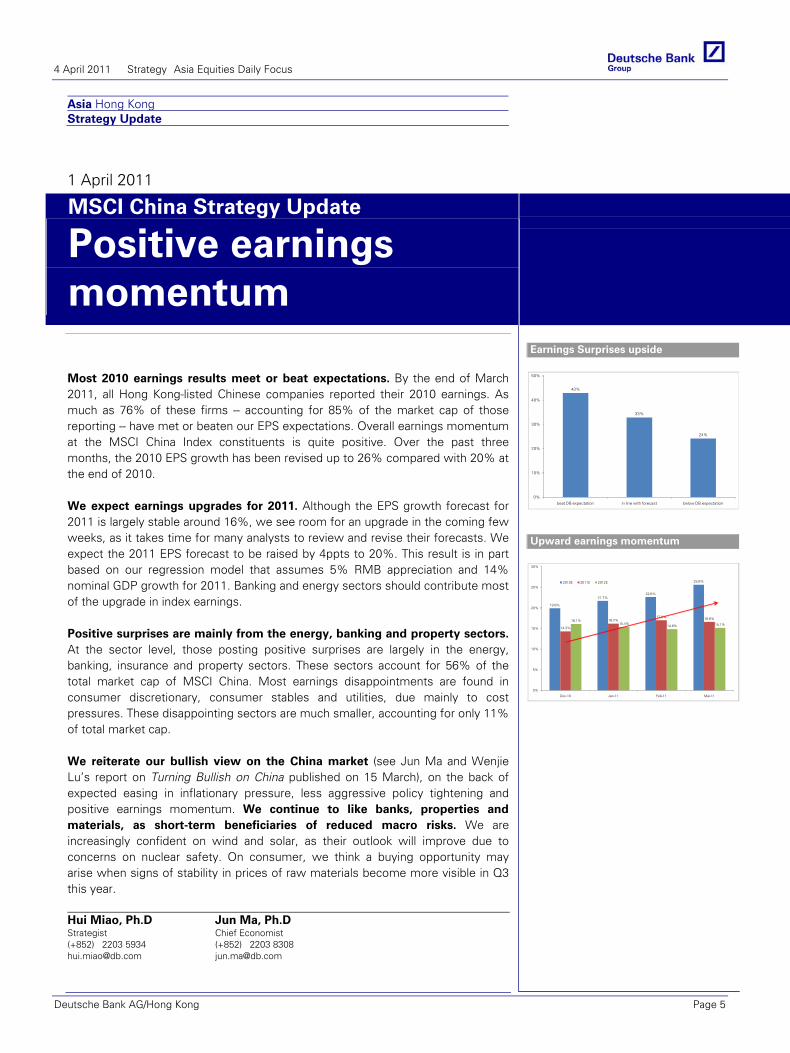

MSCI China Strategy Update

Positive earnings momentum

Hui Miao, Ph.D Strategist (+852) 2203 5934 [email protected]

Jun Ma, Ph.D Chief Economist (+852) 2203 8308 [email protected]

Earnings Surprises upside

43%

33%

24%

0%

10%

20%

30%

40%

50%

beat DB expectation in line with forecast below DB expectation

Upward earnings momentum

19.9%

21.7%22.6%

25.6%

14.3%

16.2%17.0% 16.6%16.1%

15.4%14.8% 15.1%

0%

5%

10%

15%

20%

25%

30%

Dec-10 Jan-11 Feb-11 Mar-11

2010E 2011E 2012E

Most 2010 earnings results meet or beat expectations. By the end of March 2011, all Hong Kong-listed Chinese companies reported their 2010 earnings. As much as 76% of these firms -- accounting for 85% of the market cap of those reporting -- have met or beaten our EPS expectations. Overall earnings momentum at the MSCI China Index constituents is quite positive. Over the past three months, the 2010 EPS growth has been revised up to 26% compared with 20% at the end of 2010.

We expect earnings upgrades for 2011. Although the EPS growth forecast for 2011 is largely stable around 16%, we see room for an upgrade in the coming few weeks, as it takes time for many analysts to review and revise their forecasts. We expect the 2011 EPS forecast to be raised by 4ppts to 20%. This result is in part based on our regression model that assumes 5% RMB appreciation and 14% nominal GDP growth for 2011. Banking and energy sectors should contribute most of the upgrade in index earnings.

Positive surprises are mainly from the energy, banking and property sectors. At the sector level, those posting positive surprises are largely in the energy, banking, insurance and property sectors. These sectors account for 56% of the total market cap of MSCI China. Most earnings disappointments are found in consumer discretionary, consumer stables and utilities, due mainly to cost pressures. These disappointing sectors are much smaller, accounting for only 11% of total market cap.

We reiterate our bullish view on the China market (see Jun Ma and Wenjie Lu’s report on Turning Bullish on China published on 15 March), on the back of expected easing in inflationary pressure, less aggressive policy tightening and positive earnings momentum. We continue to like banks, properties and materials, as short-term beneficiaries of reduced macro risks. We are increasingly confident on wind and solar, as their outlook will improve due to concerns on nuclear safety. On consumer, we think a buying opportunity may arise when signs of stability in prices of raw materials become more visible in Q3 this year.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 5

Asia China Property Property

1 April 2011

China State Construction Reuters: 3311.HK Bloomberg: 3311 HK Exchange: HSI Ticker: 3311

A fast-growing public housing developer; Initiate with BuyTony Tsang Research Analyst (+852) 2203 6256 [email protected]

Jason Ching, CFA Research Analyst (+852) 2203 6205 [email protected]

Venant Chiang Research Analyst (+852) 2203 6183 [email protected]

Initiate with Buy, TP HK$10.03; strong upside from public housing The public housing system is now a priority of the central government. Through the provision of two value-added services – 1) public housing construction with good design, quality, safety and environmental protection, and 2) financing – to local governments, CSCI enjoys unique advantages over other contractors and developers when participating in China’s massive public housing development. This should present strong and sustainable long-term earnings growth for CSCI.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (HKDm) 9,706.1 11,982.9 16,726.1 25,873.2 30,268.3

EBITDA(HKDm) 535.3 1,003.4 1,520.0 2,341.6 2,824.5

Reported NPAT(HKDm) 674.1 1,036.3 1,488.5 1,990.4 2,355.9

DB EPS FD (HKD) 0.24 0.34 0.43 0.54 0.64

DB EPS growth (%) 32.3 41.6 26.1 26.5 18.4

PER (x) 10.7 11.6 16.5 13.1 11.0

EV/EBITDA (x) 9.6 13.1 15.6 9.5 7.2

Yield (net) (%) 2.8 2.8 1.7 1.8 2.0Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Coverage Change

Buy Price at 31 Mar 2011 (HKD) 7.10Price target - 12mth (HKD) 10.0352-week range (HKD) 8.48 - 2.26HANG SENG INDEX 23,528

Price/price relative

0

23

5

6

8

9

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11China State Construc

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -0.8 -3.3 134.3HANG SENG INDEX 0.8 2.1 10.8

Stock data

Market cap (HKDm) 25,448Market cap (USDm) 3,272Shares outstanding (m) 3,584.2Major shareholders –Free float (%) 36Avg daily value traded (USDm) 0.0

Key indicators (FY1)

ROE (%) 21.4Net debt/equity (%) -13.8Book value/share (HKD) 2.59Price/book (x) 2.7Net interest cover(x) –Operating profit margin (%) 8.4

Huge growth potential from government’s 36mn public housing units target The determination of the government in building up a public housing system in China is firm and clear, and the planned 36mn public housing units target opens up a new segment in the China property market with deep volume and huge market potential. The target is aggressive, as is the required funding (about RMB5.5tn on our estimates) and the big potential funding shortfalls of about RMB3-4tn that need to be filled partly by other enterprises – like CSCI – which could deliver quality public housing products to local governments and at the same time help resolve their financing challenges, and with these CSCI can enjoy higher margins.

CSCI is well positioned to expand its market share in public housing With its strong record in construction and civil engineering (>35 years’ experience), strong management team, strong financing capabilities (net cash now), and strong backing from parent CSCEC (the largest state-owned construction company), CSCI should enjoy unique advantages in grabbing market share in public housing via the BT model. Within a short time (July 2010-Jan 2011), CSCI has already obtained 3 large-scale public housing projects. CSCI’s target is a 1% market share in public housing in 2011-15, and if achieved, should allow for a net profit CAGR of about 30% for 2011-15. A higher achieved market share may present further upside.

Our DCF-based target price implies 41% potential upside Our HK$10.03 TP is based on our DCF analysis which factors in CSCI’s achieving a 1% market share in public housing in 2011-15, and various margin assumptions resulting in overall net margins of 8-9% in 2011-15. Key company-specific risks include the potential failure of CSCI to achieve its market share target and any weaker-than-expected implementation of public housing plans by local governments.

4 April 2011 Strategy Asia Equities Daily Focus

Page 6 Deutsche Bank AG/Hong Kong

Asia Hong Kong Banking/Finance Banks

3 April 2011

China Merchants Bank-H Reuters: 3968.HK Bloomberg: 3968 HK Exchange: HKG Ticker: 3968

Valuation reflects superior quality, down to HoldTracy Yu Research Analyst (+852) 2203 6191 [email protected]

Judy Zhang Research Analyst (+852) 2203 6193 [email protected]

Slowing growth poses risks to premium valuation; Downgraded to Hold We downgrade our rating on CMB to Hold from Buy and lower our TP to HK$22.5 which represents 12.7x 2012E P/E (sector P/E: 8x) as CMB might not be able to sustain the 20-30% valuation premium without growing faster than its peers. Our earnings forecasts, which assume high NIM of 2.9-3%, falling CIR and credit costs of below 50bps, should grow at a CAGR of 18% from 2010-2013E. Incorporating Rmb35bn of new capital, CMB's EPS CARG will be 13%. We take CMB out from our top picks and replace it with CCB, alongside with ICBC and ABC.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Pre-prov profit (CNYm) 25,286.0 38,780.0 52,512.3 56,565.2 64,781.9

Net profit (CNYm) 18,235.0 25,769.0 34,595.3 37,045.4 41,862.1

EPS (CNY) 1.08 1.27 1.48 1.48 1.67

PER (x) 12.7 13.7 11.9 11.9 10.6

Price/book (x) 3.70 2.75 2.26 1.97 1.72

DPS (net) (CNY) 0.21 0.29 0.30 0.32 0.37

Yield (net) (%) 1.5 1.7 1.7 1.8 2.1

ROE (%) 21.1 22.7 21.0 17.6 17.4Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Recommendation Change

Hold Price at 1 Apr 2011 (HKD) 20.95Price target - 12mth (HKD) 22.5952-week range (HKD) 23.50 - 17.06HANG SENG INDEX 23,802

Key changes

Rating Buy to Hold Price target 25.06 to 22.59 -9.9%Provisioning (FYE) 7,792.3 to 7,072.2 -9.2%Net int margin (FYE) 2.87 to 3.00 4.6%Net profit (FYE) 34,588.5 to 34,595.3 0.0%

Price/price relative

8

12

16

20

24

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11China Merchants Bank

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 9.7 6.8 -2.8HANG SENG INDEX 1.7 3.3 10.5

Stock data

Market cap (HKDm) 525,370Market cap (USDm) 67,535Shares outstanding (m) 21,577.0Major shareholders China Merchants Group (12.11%)Free float (%) 67Avg daily value traded (USDm) 58.8

Key indicators (FY1)

ROE (%) 21.0Loan/deposit ratio (%) 75.6Book value/share (CNY) 7.80Price/book (x) 2.3NPL/total loans (%) 0.7Net int margin (%) 3.00Adjusted ROE (%) 0.0

In line results for FY2010; Management outlook remains positive CMB reported net profit of Rmb25.8bn in 2010, up 41% yoy. We attribute the Rmb862m (or 9.8% qoq) increase in the NPL balance in 4Q 2010 to both tighter classification standards on LGFV loans (Rmb224m downgraded), mortgage (Rmb86m) and credit card loans (Rmb70m) and a significant reduction in write-offs, of almost Rmb1bn yoy, rather than a deterioration in asset quality. Management guidance on the outlook for 2011 was positive, expecting higher NIM, sustainable fee income growth and falling CIR and stable credit costs, to meet the provision coverage ratio of 2.5% of loans by 2014.

CMB to raise capital; waiting for a better window CMB has obtained a general mandate to increase 20% of its capital. Given that CMB’s tier 1 ratio of 8.04% is lower than its peers’, we expect the bank to raise Rmb35bn of capital this year by issuing 3.5bn new shares at Rmb9.86/shr. Our new target price of HK$22.59/shr incorporates the increase in new capital.

Fair valuation, CMB’s A-share price reflects a more sustainable premium We consider CMB’s valuation, at 12.9x 2011E P/E and 2.3x 2011E P/B (ROAE for 2012E: 17.6%), to be fair and its A-share price, which trades at around a 20% discount to its H-shares, reflects a more sustainable premium of 10-20% to its peers. We value CMB based on a three-stage GGM with a near-term and terminal ROAE of 18% and 16-17% and COE of 11%. Key downside risks include a larger-than-expected equity raising at a lower price, asset quality deterioration, asymmetric rate hikes and an increase in demand deposit rates. Upside risks include stronger-than-expected NIM expansion on higher rates.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 7

Asia Hong Kong Strategy Update

1 April 2011

China Macro Strategy

PMI confirms positive macro trend

Jun Ma, Ph.D Chief Economist (+852) 2203 8308 [email protected]

Wenjie Lu Research Analyst (+852) 2203 6187 [email protected]

China’s official manufacturing PMI released today (1 April) confirms the positive macro trend depicted by the HSBC PMI reported about a week ago that the growth momentum is strengthening and the inflationary pressure is easing. Specifically, the PMI rose to 53.4 in March, up 1.2ppts from February. The sub-indices of new orders and new export orders rose 0.9ppt and 1.6ppts respectively to 55.2 and 52.5. The production sub-index also recovered by 1.9ppts to 55.7. At the same time, the input price sub-index fell 1.8ppts to 68.3, indicating a slowing trend of cost inflation. Inventories of both raw materials and final products rose in March. At the macro level, these data points are supportive of our projection that yoy inflation will peak by the middle of the year and sequential (qoq, saar) GDP growth will recover to around 9% yoy in 2H, up from a relatively weaker 2Q (at around 8%). On inflation, the recent increase in inventories suggest that restocking-led PPI pressure will subside and should likely help contain CPI inflation in the second half of this year. The sectors that posted the strongest headline PMI readings are non-ferrous metal (58.6), machinery and equipment (56-58), metal products (56.1) and tobacco (56.4). The weaker sectors include paper and sports articles (46.9), petroleum processing (46.0) and ferrous metal (46.2). Looking into the details from the new orders and new export orders report, we see positive momentum for the following sectors: 1) Furniture, garment and electric machinery. Export orders sub-index for the three sectors rose by 25.1ppts (furniture), 22.6 ppts (electric machinery), and 7.2ppts (garment) in March from weak February levels which were distorted by CNY holidays. As these sectors account for about 30% of total merchandise exports, overall export growth should improve in the coming months. 2) Automobile. The new orders index for the transport sector (mainly auto) increased by a significant 4.6ppts to 59.2. This reading is now higher than the past five-year average of 58.5, indicating that the market concern of a sharp slowdown in auto demand may be overdone. 3) Machinery and equipment. Five sectors in this broad category posted their new orders index in the solid range of 55-67, with the export orders index in the range of 54-60. These numbers suggest machinery and equipment are well supported by strong domestic demand and rising export competitiveness.

4 April 2011 Strategy Asia Equities Daily Focus

Page 8 Deutsche Bank AG/Hong Kong

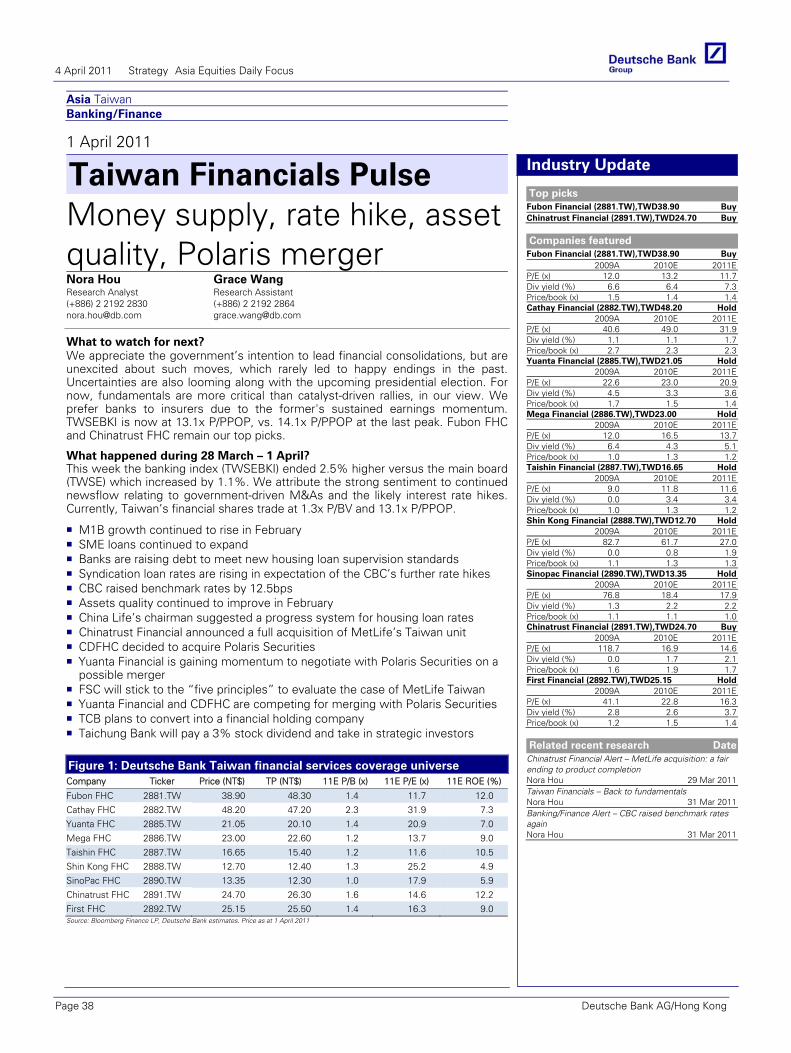

Asia Taiwan Technology Hardware & Equipment

1 April 2011

Acer Inc Reuters: 2353.TW Bloomberg: 2353 TT Exchange: TAI

Ticker: 2353

Downgrading to Hold on business model transitionKc Kao, MBA Research Analyst (+886) 2 2192 2831 [email protected]

Ivy Lee Research Associate (+886) 2 2192 2834 [email protected]

CEO change signals business model transitions Acer has announced that its CEO, Mr. Gianfranco Lanci, has resigned and that its Chairman, Mr. JT Wang, will assume the CEO position. We believe this signals major changes in the company’s business model and uncertainty over growth in the medium term. As a result, we are downgrading the stock to Hold and reducing our price target to NT$58. We are cutting our 2011-12E EPS by 33% and 28% respectively to reflect the transition.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (TWDm) 573,843.1 629,657.2 608,355.5 672,560.0 686,011.2

EBIT (TWDm) 15,341.4 18,200.8 14,053.8 17,674.9 17,652.3

Reported NPAT (TWDm) 11,354.6 15,074.4 11,403.0 14,299.9 14,297.9

DB EPS FD(TWD) 4.31 5.42 4.03 5.05 5.05

OLD DB EPS FD(TWD) 4.31 5.42 6.01 6.97 7.56

% Change 0.0% 0.0% -33.0% -27.5% -33.2%

DB EPS growth (%) -8.4 25.6 -25.6 25.4 -0.0

Yield (net) (%) 4.7 3.8 4.2 5.3 5.3

PER (x) 15.2 16.0 14.2 11.3 11.3Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Recommendation Change

Hold Price at 1 Apr 2011 (TWD) 57.10Price target - 12mth (TWD) 58.0052-week range (TWD) 98.10 - 57.10TWSE 8,705

Key changes

Rating Buy to Hold Price target 84.00 to 58.00 -31.0%Sales (FYE) 681,266 to 608,356 -10.7%Op prof margin (FYE) 3.1 to 2.3 -25.3%Net profit (FYE) 17,016.8 to 11,403.0 -33.0%

Price/price relative

50

6070

80

90

100

110

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Acer Inc

TWSE (Rebased)

Performance (%) 1m 3m 12mAbsolute -22.1 -36.6 -38.9TWSE -0.3 -3.0 8.6

Stock data

Market cap (TWDm) 161,623Market cap (USDm) 5,496Shares outstanding (m) 2,830.5Major shareholders Stan Shih & Family (5.4%)Free float (%) 94Avg daily value traded (USDm) 53.2

Key indicators (FY1)

ROE (%) 11.1Net debt/equity (%) -37.6Book value/share (TWD) 37.68Price/book (x) 1.52Net interest cover (x) –Operating profit margin (%) 2.3

Transitions likely lead to slower growth We believe the catalyst for Lanci’s resignation was the divergence of his views on the business model from those of other board members. Under the leadership of Lanci, Acer has focused on driving volume market share through competitive pricing. We think board members are taking the view that the business model has reached its limits (Acer has missed its guidance for two consecutive quarters). The company needs to modify its business model (e.g. invest more in R&D) to adapt to the new competitive environment (brought about by iPad). We view this as a major change which could lead to slower market share momentum and higher expenses during the transition.

Lower estimates to reflect business transition We lower our EPS to NT$4.03 for 11E (previously NT$6.01) and NT$5.05 for 12E (previously NT$6.97) as we apply more conservative assumptions to market share and OM. We now assume that Acer’s NB market share will remain flattish at 15.5-15.6% for 11E-12E and its OM will decline to 2.3%-2.6% in 11E-12E (from 2.9% in 10). We also do not factor in contributions from its new tablet PC, as we await actual sell-through data to better assess this new product.

Lowering price target to NT$58; risks: tablet PC/China business development We lower our price target to NT$58 (from NT$84) on lower earnings estimates and target P/E multiples (to reflect the company’s business transition in the medium term). Our NT$58 price target is based on 12x target P/E (mid-point of mid cycle and trough P/E) and 2H11E-1H12E EPS of NT$4.87. Key upside/downside risks are better-/worse-than-expected tablet PC developments and operations in China.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 9

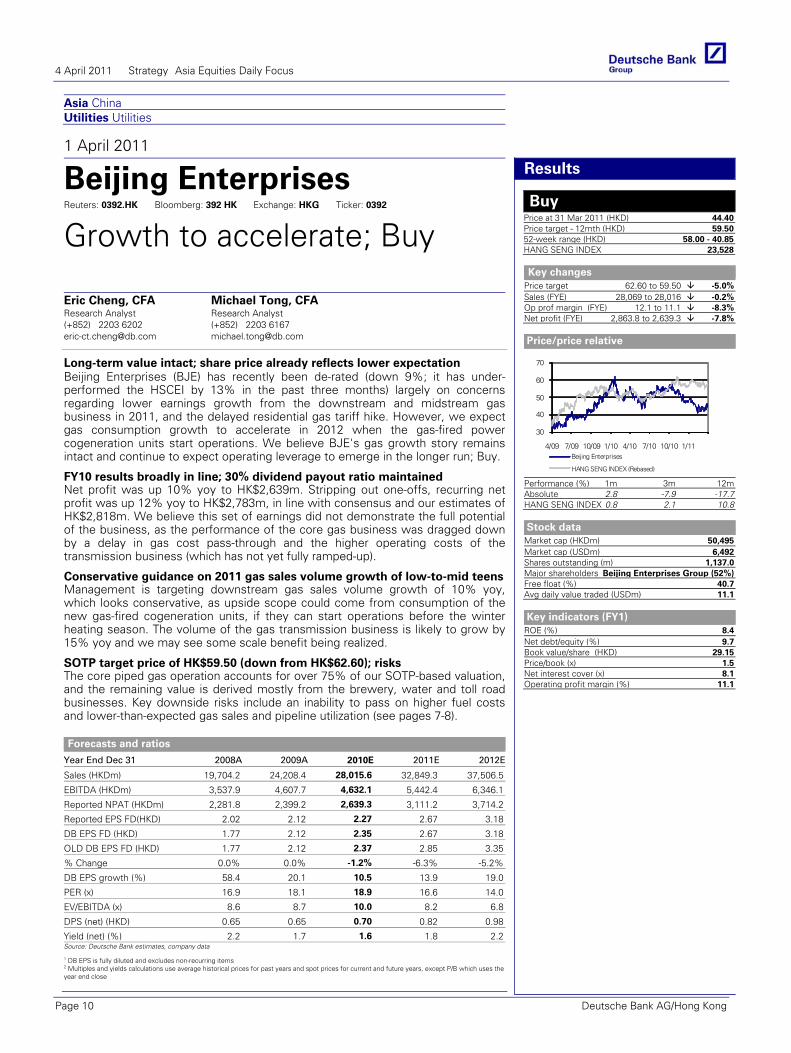

Asia China Utilities Utilities

1 April 2011

Beijing Enterprises Reuters: 0392.HK Bloomberg: 392 HK Exchange: HKG Ticker: 0392

Growth to accelerate; Buy

Eric Cheng, CFA Research Analyst (+852) 2203 6202 [email protected]

Michael Tong, CFA Research Analyst (+852) 2203 6167 [email protected]

Long-term value intact; share price already reflects lower expectation Beijing Enterprises (BJE) has recently been de-rated (down 9%; it has under-performed the HSCEI by 13% in the past three months) largely on concerns regarding lower earnings growth from the downstream and midstream gas business in 2011, and the delayed residential gas tariff hike. However, we expect gas consumption growth to accelerate in 2012 when the gas-fired power cogeneration units start operations. We believe BJE's gas growth story remains intact and continue to expect operating leverage to emerge in the longer run; Buy.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Sales (HKDm) 19,704.2 24,208.4 28,015.6 32,849.3 37,506.5

EBITDA (HKDm) 3,537.9 4,607.7 4,632.1 5,442.4 6,346.1

Reported NPAT (HKDm) 2,281.8 2,399.2 2,639.3 3,111.2 3,714.2

Reported EPS FD(HKD) 2.02 2.12 2.27 2.67 3.18

DB EPS FD (HKD) 1.77 2.12 2.35 2.67 3.18

OLD DB EPS FD (HKD) 1.77 2.12 2.37 2.85 3.35

% Change 0.0% 0.0% -1.2% -6.3% -5.2%

DB EPS growth (%) 58.4 20.1 10.5 13.9 19.0

PER (x) 16.9 18.1 18.9 16.6 14.0

EV/EBITDA (x) 8.6 8.7 10.0 8.2 6.8

DPS (net) (HKD) 0.65 0.65 0.70 0.82 0.98

Yield (net) (%) 2.2 1.7 1.6 1.8 2.2Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Results

Buy Price at 31 Mar 2011 (HKD) 44.40Price target - 12mth (HKD) 59.5052-week range (HKD) 58.00 - 40.85HANG SENG INDEX 23,528

Key changes

Price target 62.60 to 59.50 -5.0%Sales (FYE) 28,069 to 28,016 -0.2%Op prof margin (FYE) 12.1 to 11.1 -8.3%Net profit (FYE) 2,863.8 to 2,639.3 -7.8%

Price/price relative

30

40

50

60

70

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Beijing Enterprises

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 2.8 -7.9 -17.7HANG SENG INDEX 0.8 2.1 10.8

Stock data

Market cap (HKDm) 50,495Market cap (USDm) 6,492Shares outstanding (m) 1,137.0Major shareholders Beijing Enterprises Group (52%)Free float (%) 40.7Avg daily value traded (USDm) 11.1

Key indicators (FY1)

ROE (%) 8.4Net debt/equity (%) 9.7Book value/share (HKD) 29.15Price/book (x) 1.5Net interest cover (x) 8.1Operating profit margin (%) 11.1

FY10 results broadly in line; 30% dividend payout ratio maintained Net profit was up 10% yoy to HK$2,639m. Stripping out one-offs, recurring net profit was up 12% yoy to HK$2,783m, in line with consensus and our estimates of HK$2,818m. We believe this set of earnings did not demonstrate the full potential of the business, as the performance of the core gas business was dragged down by a delay in gas cost pass-through and the higher operating costs of the transmission business (which has not yet fully ramped-up).

Conservative guidance on 2011 gas sales volume growth of low-to-mid teens Management is targeting downstream gas sales volume growth of 10% yoy, which looks conservative, as upside scope could come from consumption of the new gas-fired cogeneration units, if they can start operations before the winter heating season. The volume of the gas transmission business is likely to grow by 15% yoy and we may see some scale benefit being realized.

SOTP target price of HK$59.50 (down from HK$62.60); risks The core piped gas operation accounts for over 75% of our SOTP-based valuation, and the remaining value is derived mostly from the brewery, water and toll road businesses. Key downside risks include an inability to pass on higher fuel costs and lower-than-expected gas sales and pipeline utilization (see pages 7-8).

4 April 2011 Strategy Asia Equities Daily Focus

Page 10 Deutsche Bank AG/Hong Kong

Asia Korea, Republic of Technology Hardware & Equipment

1 April 2011

LG Display Reuters: 034220.KS Bloomberg: 034220 KS Exchange: KSC Ticker: 034220

Upside potential outweighs downside risk Sc Bae Research Analyst (+82) 2 316 8907 [email protected]

Hoyer Jeong Research Associate (+82) 2 316 8912 [email protected]

Lowering target price on earnings cut; reiterating Buy on weakness We lower our target price for LGD by 7% to W43,000 on an earnings cut due to delayed demand recovery and rising concerns on cost cuts due to the Japan earthquake. However, we reiterate Buy believing that upside outweighs downside: 1) bottoming out LCD cycle in the long term due to TV demand price elasticity and potential capex cuts at the panel makers; 2) rising earnings contribution from non-commodity panels, mainly for Apple, 3) potential M/S gains in TV leveraging FPR technology, and 4) attractive valuations with 1.1x P/B vs. historical average of 1.6x.

Forecasts and ratios

Year End Dec 31 2008A 2009A 2010E 2011E 2012E

Sales (KRWbn) 16,264 20,614 25,512 26,005 27,410

EBIT (KRWbn) 1,246.8 982.7 1,310.5 1,190.9 2,006.5

EBITDA (KRWbn) 3,788 3,821 4,236 4,795 6,027

Reported NPAT (KRWbn) 1,086.9 1,027.5 1,156.3 1,140.5 1,864.4

DB EPS FD(KRW) 3,038 2,872 3,232 3,187 5,210

Price/BV (x) 0.81 1.39 1.15 1.06 0.93

ROE (%) 12.4 10.6 10.9 9.9 14.6

PER (x) 11.5 11.0 11.0 11.1 6.8Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Buy Price at 1 Apr 2011 (KRW) 35,450Price target - 12mth (KRW) 43,00052-week range (KRW) 47,900 - 33,250KOSPI 2,121.01

Key changes

Price target 46,000.00 to 43,000.00 -6.5%Sales (FYE) 25,511 to 25,512 0.0%Op prof margin (FYE) 5.1 to 5.1 0.0%Net profit (FYE) 1,155.9 to 1,156.3 0.0%

Price/price relative

2400028000320003600040000440004800052000

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11LG Display

KOSPI (Rebased)

Performance (%) 1m 3m 12mAbsolute -1.0 -10.9 -15.0KOSPI 9.4 3.4 23.4

Stock data

Market cap (KRWbn) 12,685Market cap (USDm) 11,563Shares outstanding (m) 357.8Major shareholders LG Electronics (37.9%)Free float (%) 65Avg daily value traded (USDm) 91.049

Key indicators (FY1)

ROE (%) 10.9Net debt/equity (%) 18.5Book value/share (KRW) 30,843Price/book (x) 1.15Net interest cover (x) 155.0Operating profit margin (%) 5.1

Earnings cut on delayed recovery and uncertainties regarding earthquake Our latest channel check suggests that despite some recent early signs of US TV demand recovery, the chance of meaningful panel price recovery in 2Q11 is weakening as set-makers and channels remain conservative about inventory management due to the lack of confidence in the demand. On the cost side, we are concerned that potential disruption in key components from Japan might weaken the bargaining power of panel makers vs. component makers in the near term. Reflecting these, we lower 2011/12E EPS by 29% and 11%, respectively.

Panel cycle is bottoming, two specific positives to drive distinctive recovery On the mid-to-longer term basis, we believe that the global panel industry is passing through the bottom, given: 1) panel makers are turning more conservative about capex plans and; 2) potential demand pickup in the US and emerging markets on LCD TV replacement cycle and price elasticity. In addition, we believe two company-specific positive catalysts such as FPR 3D panel and IPS based high-resolution IT panels should drive distinctive earnings recovery from 3Q11.

1.4x P/B on 2011E BVPS, risks In valuation, we continue to use a cyclical context historical P/B method where we apply 1.4x of P/B, which is a 20% discount to the historical mid-cycle multiple of 1.7x. We apply 20% discount reflecting lowered ROE profile due to slower demand growth than before. Weaker-than-expected TV demand in the US and irrational utilization rates by panel makers would be the major risks.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 11

Asia ASEAN Singapore Property Property Trust

2 April 2011

Ascendas Real Estate Reuters: AEMN.SI Bloomberg: AREIT SP Exchange: SES Ticker: AEMN

Positioning for growth

Gregory Lui, CFA Strategist (+65) 6423 5958 [email protected]

Elaine Khoo, CFA Research Analyst (+65) 6423 6435 [email protected]

Look beyond near term dilution; balance sheet primed for more acquisitions AREIT's recent equity raising signals an improving outlook for acquisitions and BTS opportunities which could enhance its steady growth profile. While the time lag in the completion of asset enhancements, BTS and recent China acquisition results in near term DPU dilution, further capital deployment given its sub-optimised balance sheet could boost medium term growth. We have reduced our TP by 2% to reflect the dilution and new cost of equity assumption; maintain Buy.

Forecasts and ratios

Year End Mar 31 2009A 2010A 2011E 2012E 2013E

Sales (SGDm) 396.5 413.7 449.4 475.9 511.9

Reported NPAT (SGDm) 94.4 148.0 600.5 269.9 293.8

Reported EPS FD(SGD) 0.06 0.08 0.32 0.13 0.14

PER (x) 33.1 22.1 6.2 15.5 14.3

DPU (SGD) 0.15 0.13 0.14 0.13 0.14

Yield (%) 8.2 7.5 6.8 6.6 7.2Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Company Update

Buy Price at 1 Apr 2011 (SGD) 2.00Price target - 12mth (SGD) 2.2852-week range (SGD) 2.29 - 1.82Straits Times Index 3,120

Key changes

Price target 2.33 to 2.28 -2.1%Sales(FYE) 450 to 449 -0.0%Op prof margin (FYE) 70.3 to 70.2 -0.3%Net profit(FYE) 292.8 to 600.5 105.1%

Price/price relative

1.2

1.6

2.0

2.4

2.8

4/09 7/09 10/09 1/10 4/10 7/10 10/10 1/11Ascendas Real Estate

Straits Times Index (Rebased)

Performance (%) 1m 3m 12mAbsolute -1.0 -3.4 3.1Straits Times Index 1.7 -2.2 6.0

Stock data

Market cap (SGDm) 3,753Market cap (USDm) 2,973Shares outstanding (m) 1,875.0Major shareholders Ascendas (20.6%)Free float (%) 65Avg daily value traded (USDm) 7.3

Key indicators (FY1)

ROE (%) 19.2Net debt/equity (%) 51.4Book value/share (SGD) 1.76Price/book (x) 1.1Net interest cover (x) 4.8Operating profit margin (%) 70.2

Acquisition of Neuros & Immunos and private placement completed The private placement was 2.55x oversubscribed at an issue price of S$1.94 (S$1.91-1.96 price range) or a 5.3% disc to the VWAP. Out of net proceeds of S$393.3m, S$126.2m will be used to repay ST borrowings used to fund the acquisition of Neuros & Immunos, S$35.9m for AREIT’s 11th BTS project, S$97m for ongoing AEIs, and S$117.6m for the forward purchase of the China business park property and the remainder for general working capital. We estimate a blended weighted average NPI yield on cost of around 7.5% for these projects compared to the implied cost of equity of c.7% based on the placement price.

Revising down FY12e DPU by 4%; conservative balance sheet position This reflects the dilution from the placement and staggered timing of income contribution from the various initiatives (from 1QFY12 to 2QFY13). AREIT announced a revaluation gain of S$307.6m (+6.3%) which together with the EFR brings gearing down from 34.7% to 30.1% accounting for all committed capex which is among the lowest vs. peers and should give it the flexibility and competitive edge in acquisitions. Mgmt is in discussion on a potential acquisition of a portfolio of properties of around S$200m (this brings gearing to 34%) which may be completed in the next 3-6 months. We have assumed a 7.0% acquisition yield in our forecast; additional acquisitions could provide a further boost to DPU.

Maintain Buy with revised TP of S$2.28; risks We revise our DDM-pegged target price from S$2.33 to S$2.28 (-2%) reflecting our revisions to earnings and Cost of Equity assumption (7.0% to 7.25%). AREIT is trading at 1.13x P/B (LT avg of 1.33x) and offering FY11e and FY12e yield of 6.8% and 6.6% respectively implying a 410bps spread for FY12. Risks: reversal of growth trends affecting leasing demand, credit risk from tenants on long sale & leaseback, development risk and acquisition risk.

4 April 2011 Strategy Asia Equities Daily Focus

Page 12 Deutsche Bank AG/Hong Kong

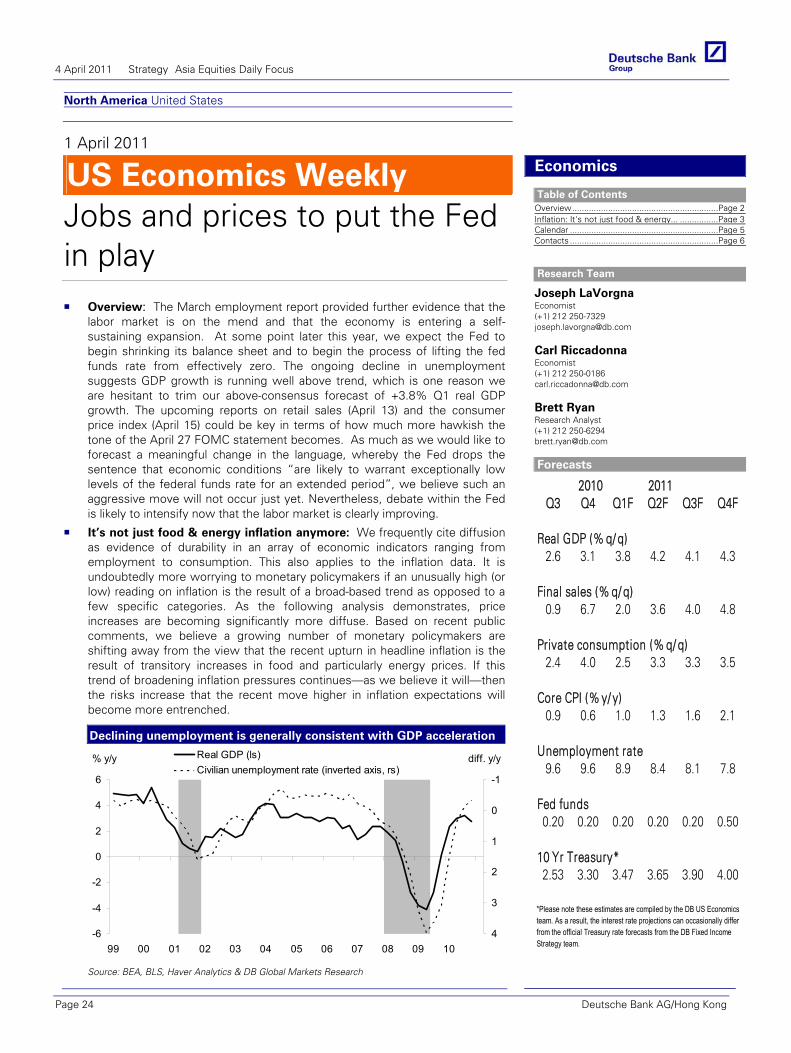

North America United States Strategy Update

31 March 2011

US Equity Strategy

Q1 2011 Earnings Preview

Binky Chadha Chief Strategist (+1) 212 250-4776 [email protected]

Keith Parker Strategist (+1) 212 250-7448 [email protected]

Parag Thatte Strategist (+1) 212 250-6605 [email protected]

Ju Wang Strategist (+1) 212 250-7911 [email protected]

What is Expected for Q1? ................................ Page 02Undemanding Bar for Q1 ................................. Page 03Risks Appear Priced In?.................................... Page 09What to Buy?.................................................... Page 11Views & Strategy Summary ............................. Page 22

Bar for Q1 earnings is low

121314151617181920212223

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Q4

10

Q1

11

121314151617181920212223

Surprise

Consensus EPS

S&P 500 Quarterly Operating EPS ($)

Sales growth taking over from margins

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

Dec

-97

Dec

-99

Dec

-01

Dec

-03

Dec

-05

Dec

-07

Dec

-09

Dec

-11

-50%-40%-30%-20%-10%0%10%20%30%40%50%

Recessions Sales MarginsS&P 500 ex Financials sales and margins yoy

Q1 margins look low given seasonality

-250 -150 -50 50 150

Materials Utilities

Telecom Healthcare Financials

Energy Cons Disc

Ex-FinancialsS&P 500

Cons Stap Industrials

Info Tech

-250 -150 -50 50 150

Q1 2011 Consensus

Historical Median

Q1 2011 Op EPS margin qoq consensus vs historical median for Q1 (since 1997, bps)

Q1 earnings should beat again (4%); affirmation of 2011 outlooks the key Already skeptical of sales & margin prospects, investors are looking to Q1 earnings to gauge whether the costs of the recent shocks (Middle East & Japan) can be absorbed by the recovery. We think Q1 earnings will beat again, but by a smaller amount: higher oil/commodity prices and costs of supply disruptions should be offset by already low margin expectations and other drivers of margins which remain supportive (improving pricing power, trailing labor costs & operating leverage). Additionally, we expect greater variation in results across sectors/stocks as micro continues to take over from macro. Guidance will remain conservative but we think 2011 earnings will be reaffirmed in the aggregate and CEO outlooks stay upbeat. We note that on current multiples, 2011 estimates imply 1480 for the S&P 500 by YE. Prior to the Middle East and Japan events, the multiple had been rising back toward fair value (16.4x) and this would add another 70 points.

Undemanding bar should offset higher oil/commodity price & Japan supply The consensus expects S&P 500 EPS to fall 3.4% qoq in a seasonally weak Q1. Sales growth appears reasonable, in-line with nominal GDP. Margin expectations are low once again. Consensus has predicted declines in margins for the last 6 quarters that have not materialized; margins are expected to decline 22bps in Q1 when they typically rise by 20bps. Top-down margin drivers point to modest upside. We estimate that rising pricing power (+40bps), declining ULC (+25bps), operating leverage (+15bps) will be sufficient to offset higher energy and material costs (-60 bps). The impact of Japan should be limited and industry specific. Across sectors, Financials could beat big given flat rates/better FICC in Q1 and low expectations. Tech estimates look low even with supply chain issues while Telecom and Utilities look high.

Expect continued conservative guidance, risks appear to be priced in Guidance/charges related to higher oil/commodity prices and Japan/supply issues could pose headline risk. However, the P/E is 20% below pre-recession levels at a stage of the recovery by which it typically has recovered fully.

Buy growth, sales upside, sector pairs, quality, payouts Earnings growth tends to remain above trend through this part of the cycle, with sales taking over from margins as the driver of growth. Heading into Q1 earnings, we reiterate our sector pair trades (Financials/Staples, Industrials/Utilities, Tech/ Telecom, Energy/Materials) which: (i) are up YTD; (ii) outperformed through last 4 earnings seasons; (iii) are positioned for the biggest sales upside; and (iv) hedge against oil/commodity price moves. Across stocks, high quality and firms doing big buybacks beat estimates the most in 2010 (buy DBUSQLTE and DBUSPAYE baskets). Growth stocks have been rewarded the most on beats; we highlight our Growth (DBUSGROW) basket. All 3 baskets outperformed notably in March.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 13

Global

31 March 2011

Exchange Rate Perspectives

FX Intervention Can Brake, Not Break, a Trend

Special Report

Research Team

John Horner Strategist (+61) 2 8258 2130 [email protected]

Mirza Baig Strategist (+65) 64235930 [email protected]

Fore

ign

Exc

han

ge

4 April 2011 Strategy Asia Equities Daily Focus

Page 14 Deutsche Bank AG/Hong Kong

Asia

01 Apr 2011 - 04:15:18 PM HKT

ASIA ECONOMICS SPECIAL EconomicsSBV raises the 7-day repo rate

The State Bank of Vietnam (SBV) raised its 7-day repo rate to 13% from12%, effective today. The rate was last hiked in late February, to 12% from11%, along with the refinancing and discount rates. In our view, today's ratehike highlights the SBV's commitment to curbing inflation, despite its neg-ative impact on growth. GDP growth slowed more than expected in Q12011, to 5.4% from 7.2% in Q4 2010, while headline CPI inflation continuedto head higher, to 13.9% in March from 12.3% in February. We expectinflation to head higher, at least well into the summer, as commodity andoil prices remain high. Note that the authorities raised prices of petrol,diesel, kerosene, fuel oil by 10%, 15% and 14% and 14%, respectively, thisweek. On the fiscal front, the authorties are preparing a list of none-coreinvestment projects to be cut, to achieve balanced growth. The governmentaims to bring down the 2011 budget deficit to below 5% of GDP from the5.3% aimed earlier. We think a more aggressive, concrete fiscal consolida-tion plan would go a long way in curbing inflationary expectations andfurther building public's confidence in the dong. While we are more confi-dent about the government's commitment to reducing budget deficit -- firsttime that the National Assembly identified inflation as the policy prioritywithout any reference to growth -- there are some concerns with respectto the pace of implementation due to the timing of ministerial reshuffling,which is scheduled to take place in mid-year. Until then, much of the burdenof macro-economic policy tightening may remain with the SBV.

Juliana LeeSenior Economist(+852) 2203 [email protected]

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 15

Asia

1 April 2011

Asia Economics Daily

High but stable inflation in Asia

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8303 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658 4909 [email protected]

Eco

no

mic

s

HIGHLIGHTS

China – Official PMI confirms positive macro trend India – Exports growth accelerates sharply in February Indonesia – Inflation remains high but stable; Trade surplus widens in February, to USD2.4bn South Korea – March inflation reach 4.7%yoy, breaching central bank target; Trade activities remain strong during March Thailand – Inflation rises to 3.1%yoy in March, in line with consensus

NEWS IN BRIEF

CHINA PMI (Mar). China’s official manufacturing PMI released today confirms the positive macro trend depicted by the HSBC PMI reported about a week ago: growth momentum is strengthening while inflationary pressure is easing. Specifically, the PMI rose to 53.4 in March, up 1.2ppts from February. The sub-indices of new orders and new export orders rose 0.9ppt and 1.6ppts respectively to 55.2 and 52.5. The production sub-index also recovered by 1.9ppts to 55.7. At the same time, the input price sub-index fell 1.8ppts to 68.3, indicating a slowing trend of cost inflation. Inventories of both raw materials and final products rose in March.

At the macro level, these data points are supportive of our projection that yoy inflation will peak by the middle of the year and sequential (qoq, saar) GDP growth will recover to around 9% yoy in H2, up from a relatively weaker Q2 (at around 8%). On inflation, the recent increase in inventories suggest that restocking-led PPI pressure will subside and should thus help contain CPI inflation in the second half of this year.

The sectors that posted the strongest headline PMI readings are non-ferrous metal (58.6), machinery and equipment (56-58), metal products (56.1) and tobacco (56.4). The weaker sectors include paper and sports articles (46.9), petroleum processing (46.0), and ferrous metal (46.2).

Looking into the details from the new orders and new export orders report, we see positive momentum for the following sectors:

1) Furniture, garment and electric machinery. These three sectors saw their export orders sub-index rising by 25.1ppts (furniture), 22.6 ppts (electric machinery), and 7.2ppts (garment) in March, from the weak Feb levels which were distorted by the CNY holiday. As these sectors account about 30% of total merchandise exports, overall export growth should improve in the coming months.

4 April 2011 Strategy Asia Equities Daily Focus

Page 16 Deutsche Bank AG/Hong Kong

2) Automobiles. The new orders index for the transport sector (mainly autos) increased by a significant 4.6ppts to 59.2. This reading is now higher the past 5 years’ average of 58.5. This indicates that market concerns of a sharp slowdown in auto demand may be overdone.

3) Machinery and equipment sectors. Five sectors in this broad category posted their new orders index in the very impressive range of 55-67, with the export orders index in the range of 54-60. These numbers suggest the machinery and equipment are well supported by strong domestic demand as well as rising export competitiveness.

In sum, we continue to believe that China’s macro outlook is improving as the reduced inflation pressure will lead to less aggressive policy tightening. At the sector level, in addition to property, banking, and materials that should benefit from the receding macro risks in the coming months, today’s PMI report also suggests that exporters, autos, and machinery will likely perform better than market expectations.

INDIA External trade (Feb). Exports rose by 49.7%yoy in February, following 32.4% rise in January. Imports rose by 21.2% in February as compared to 13.1% in January. Within the segment, non-oil imports surged by 31.0% in February, higher than 23.8% growth reported in January, reflecting firm domestic demand. Meanwhile, oil imports fell at a much slower pace of 0.3% in February vs. 7.8% decline reported in January. As a result of both strong exports and imports growth, the trade deficit stood almost stable at USD8.1bn (-USD8.0bn) in the month. Exports in absolute terms reached USD209bn in the first eleven months of FY2010/11, surpassing government’s target of USD200bn. Looking ahead, we expect strong exports growth to continue led by robust demand from US/Euro land as well as from regional partners.

INDONESIA CPI inflation (Mar). Thanks to sharply declining food prices (-1.9%mom, +13.6%yoy), Indonesia’s elevated inflation trajectory witnessed a mild relief in March, with headline inflation easing to 6.7%yoy, 0.1% lower than the previous month. Other than food prices easing, the remaining items in the CPI showed continued, moderate, upward movement (notably processed food, +0.3%mom, +5.6%yoy, and clothing, +0.4%mom, +7.7%yoy). Core inflation edged up to 4.5%.

Today’s data show that inflation remains high but stable in Indonesia for now, as administrative prices remain frozen. When and as petrol, LPG, electricity, toll, and transportation tariffs are adjusted, inflation would rise by another 200bps, on our estimates. This risk, combined with historically strong demand side pressure, should keep Bank Indonesia concerned. But we have seen ample indication from the central bank this year that it would act only after a sudden outbreak of inflation. Hence we expect no movement on monetary policy this month.

External trade (Feb). Exports rose by 28.9%yoy in February, up from 26.0% (revised) reported in January. By category, both oil and non-oil exports growth improved to 17.6% and 31.7% respectively in February, from 11.5% and 29.6% in January. With imports rising at a slower pace of 26.3% in February vs. 32.3% in January, the trade surplus widened from USD2.0bn to USD2.4bn in the same period. During the first two months of the year exports were up by 27.5% quite similar to the 28.6% average growth reported in H2. We expect strong exports growth to continue in the period ahead supported by robust demand from US and other emerging markets.

SOUTH KOREA CPI inflation (Mar). Inflation rose to a 29-month high of 4.7%yoy in March, up from 4.5% in February. By category, this was largely led by transport, inflation of which rose to 7.9% in March up from 6.6% in February, resulting from higher prices of the gasoline. Also, housing inflation rose at a faster pace of 4.1% in March, as compared to 3.7% in February. Meanwhile, food inflation still remained at elevated level, rising by 10.9% in March, albeit lower than 12.2% reported in February. Core inflation, which excludes volatile food and energy components rose further in March, to 3.3% from 3.1% in February, suggesting resilient domestic demand. Given the sharply rising international energy/commodity prices, we expect CPI inflation to remain above 4% for some time (averaging 4% in 2011), and thereby keeping the BoK on the path of monetary tightening, especially as housing prices in Seoul continue to recover.

External trade (Mar). Exports rose by 30.3%yoy in March, compared to 16.9% (revised down from 17.9%) in February. This was led by volatile vessel exports, which rose by 18.2% in March sharply reversing from 10.0% decline reported in February. On the other hand, both petroleum (56.7% in Mar vs. 58.2% in Feb) and steel (36.1% vs. 37.7%) witnessed stable export growth in the month. However, exports of electric and electronic goods plunged by 2.3% in March, against 5.5% growth in

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 17

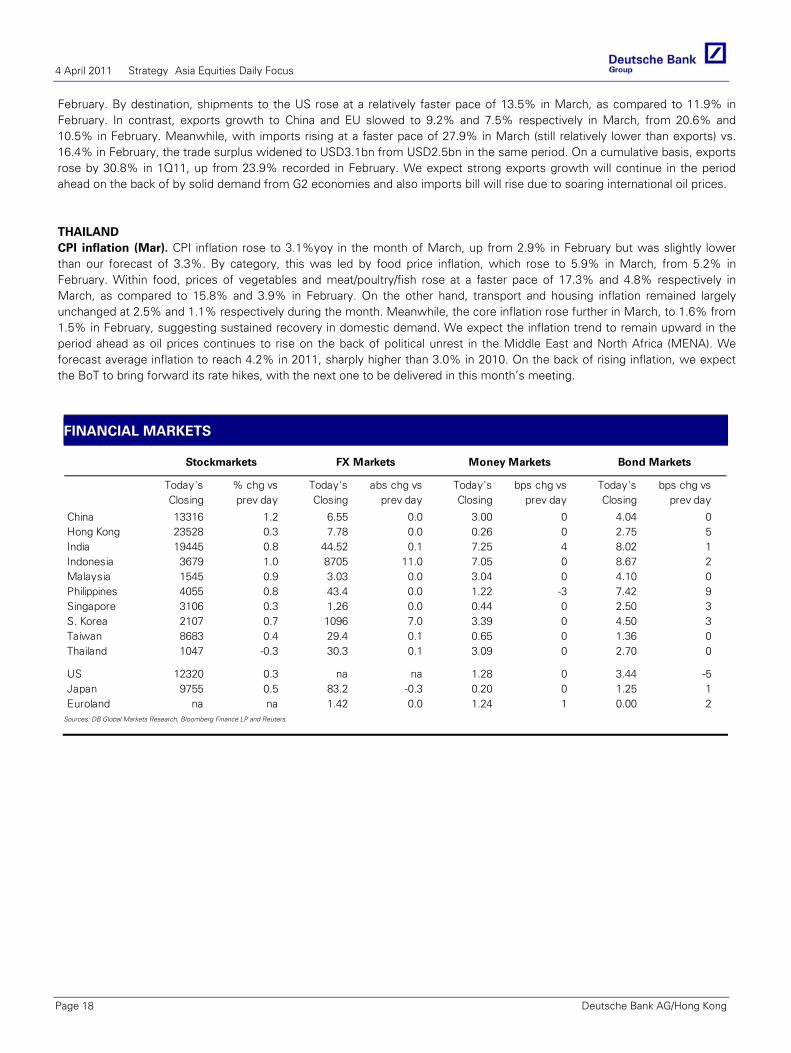

February. By destination, shipments to the US rose at a relatively faster pace of 13.5% in March, as compared to 11.9% in February. In contrast, exports growth to China and EU slowed to 9.2% and 7.5% respectively in March, from 20.6% and 10.5% in February. Meanwhile, with imports rising at a faster pace of 27.9% in March (still relatively lower than exports) vs. 16.4% in February, the trade surplus widened to USD3.1bn from USD2.5bn in the same period. On a cumulative basis, exports rose by 30.8% in 1Q11, up from 23.9% recorded in February. We expect strong exports growth will continue in the period ahead on the back of by solid demand from G2 economies and also imports bill will rise due to soaring international oil prices.

THAILAND CPI inflation (Mar). CPI inflation rose to 3.1%yoy in the month of March, up from 2.9% in February but was slightly lower than our forecast of 3.3%. By category, this was led by food price inflation, which rose to 5.9% in March, from 5.2% in February. Within food, prices of vegetables and meat/poultry/fish rose at a faster pace of 17.3% and 4.8% respectively in March, as compared to 15.8% and 3.9% in February. On the other hand, transport and housing inflation remained largely unchanged at 2.5% and 1.1% respectively during the month. Meanwhile, the core inflation rose further in March, to 1.6% from 1.5% in February, suggesting sustained recovery in domestic demand. We expect the inflation trend to remain upward in the period ahead as oil prices continues to rise on the back of political unrest in the Middle East and North Africa (MENA). We forecast average inflation to reach 4.2% in 2011, sharply higher than 3.0% in 2010. On the back of rising inflation, we expect the BoT to bring forward its rate hikes, with the next one to be delivered in this month’s meeting.

FINANCIAL MARKETS

Today's % chg vs Today's abs chg vs Today's bps chg vs Today's bps chg vsClosing prev day Closing prev day Closing prev day Closing prev day

China 13316 1.2 6.55 0.0 3.00 0 4.04 0Hong Kong 23528 0.3 7.78 0.0 0.26 0 2.75 5India 19445 0.8 44.52 0.1 7.25 4 8.02 1Indonesia 3679 1.0 8705 11.0 7.05 0 8.67 2Malaysia 1545 0.9 3.03 0.0 3.04 0 4.10 0Philippines 4055 0.8 43.4 0.0 1.22 -3 7.42 9Singapore 3106 0.3 1.26 0.0 0.44 0 2.50 3S. Korea 2107 0.7 1096 7.0 3.39 0 4.50 3Taiwan 8683 0.4 29.4 0.1 0.65 0 1.36 0Thailand 1047 -0.3 30.3 0.1 3.09 0 2.70 0

US 12320 0.3 na na 1.28 0 3.44 -5Japan 9755 0.5 83.2 -0.3 0.20 0 1.25 1Euroland na na 1.42 0.0 1.24 1 0.00 2

Stockmarkets FX Markets Money Markets Bond Markets

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

4 April 2011 Strategy Asia Equities Daily Focus

Page 18 Deutsche Bank AG/Hong Kong

ECONOMIC DIARY Country Release Period DB Expected Consensus Actual Previous

Monday, Mar 28Taiwan Leading Indicator Feb-MoM 0.2% NA 0.0% 0.1%Thailand Manufacturing Production Feb-YoY 1.8% 3.8% -3.4% 4.1%Vietnam Exports (ytd) Mar-YoY 43.9% NA 33.7% 40.3%

Imports (ytd) Mar-YoY 26.8% NA 23.8% 26.8%Trade Balance (ytd) Mar -USD2.4bn NA -USD3.1bn -USD1.8bn

Tuesday, Mar 29Philippines Industrial Production (Vol) Jan-YoY NA 25.8% 15.3%South Korea Current Account Balance Feb USD1.0bn NA USD1.2bn USD0.2bnVietnam GDP Q1-YoY 6.3% NA 5.4% 7.2%

Industrial Production (ytd) Mar-YoY 15.0% NA 14.1% 14.6%Retail Sales (ytd) Mar-YoY 24.0% NA 22.6% 23.7%

Wednesday, Mar 30Sri Lanka GDP Q4-YoY 7.7% 8.0% 8.6% 8.0%

Thursday, Mar 31Hong Kong Retail Sales (Value) Feb-YoY 6.6% 18.5% 8.6% 28.1%

Retail Sales (Volume) Feb-YoY 3.1% 13.8% 5.1% 23.6%Singapore Bank Credit Feb-YoY 16.3% NA 17.3% 16.1%South Korea Industrial production Feb-YoY 14.8% 9.6% 9.1% 13.4%

Service Industry Output Feb-YoY 3.9% NA 0.2% 4.6%Sri Lanka CPI Mar-YoY 8.9% 8.9% 8.6% 7.8%

Exports Jan-YoY 40.8% NA 72.4% 33.9%Imports Jan-YoY 11.6% NA 21.3% 30.8%Trade Balance Jan -USD0.6bn NA -USD0.7bn -USD0.5bn

Thailand Current Account Balance Feb USD1.2bn USD2.9bn USD3.8bn USD1.1bnEvents and Meeting:Taiwan:CBC Meeting (rate hike by 12.5bps to 1.75%)

Friday, Apr 1India Exports Feb-YoY 50.0% NA 49.7% 32.4%

Imports Feb-YoY 21.0% NA 21.2% 13.1%Trade Balance Feb -USD8.1bn NA -USD8.1bn -USD8.0bnCurrent Account Balance Q4 -USD7.0bn -USD9.2bn -USD9.7bn -USD16.8bn

Indonesia CPI Mar-YoY 7.0% 7.0% 6.7% 6.8%Exports Feb-YoY 25.0% 26.8% 28.9% 26.0%Imports Feb-YoY 30.0% 33.5% 26.3% 32.3%Trade Balance Feb USD1.6bn USD1.7bn USD2.4bn USD2.0bn

South Korea CPI Mar-YoY 4.8% 4.8% 4.7% 4.5%Core CPI Mar-YoY 3.5% NA 3.3% 3.1%Exports Mar-YoY 18.0% 20.1% 30.3% 16.9%Imports Mar-YoY 18.0% 21.5% 27.9% 16.4%Trade Balance Mar USD2.1bn USD1.9bn USD3.1bn USD2.5bn

Thailand CPI Mar-YoY 3.3% 3.1% 3.1% 2.9%Core CPI Mar-YoY 1.9% 1.5% 1.6% 1.5%FX Reserves Mar USD181.5bn USD179.2bn

Monday, Apr 4Indonesia FX Reserves Mar USD99.6bnSouth Korea FX Reserves Mar USD297.7bnTaiwan FX Reserves Mar USD390.7bn

Tuesday, Apr 5Malaysia Exports Feb-YoY 0.8% 5.0% 3.0%

Imports Feb-YoY 4.0% 14.4% 13.5%Trade Balance Feb MYR10.6bn MYR8.9bn MYR9.2bn

Philippines CPI Mar-YoY 4.5% 4.5% 4.3%Core CPI Mar-YoY 3.7% NA 3.5%

Events and Meeting:Australia:RBA Meeting

Wednesday, Apr 6Taiwan CPI Mar-YoY 2.1% 1.7% 1.3%

Core CPI Mar-YoY 1.3% NA 0.8%

Thursday, Apr 7Malaysia FX Reserves Mar USD109.8bnPhilippines Gross International Reserves Mar USD64.0bnSingapore FX Reserves Mar USD230.9bnEvents and Meeting:Japan:BoJ Meeting

Friday, Apr 8No major data release

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 19

Asia

1 April 2011

Asia Rates Strategy Taking stock of issuance

Market Update

Research Team

Sameer Goel Strategist (+65 ) 64236973 [email protected]

Linan Liu Strategist (+852) 2203 8709 [email protected]

Arjun Shetty Strategist (+65) 6423 5925 [email protected]

2011 local currency government bond

issuance – year/year change

-40%

-20%

0%

20%

40%

60%

THB TWD INR CNY KRW SGD HKD PHP IDR MYR

Gross Net

Source: Deutsche Bank, CEIC, Bloomberg Finance LP

*Calendar 2011 for all countries except HK and India (Apr11 to Mar12) and Thailand (Oct10-Sep11)

Offshore purchases of local currency

bonds in Asia-5*

-20

-15

-10

-5

0

5

10

15

20

F-07 J-07 O-07 F-08 J-08 O-08 F-09 J-09 O-09 F-10 J-10 O-10 F-11

USD bn

Source: Deutsche Bank, CEIC, BNM, FSS, SEBI, Bank Indonesia

*India, Indonesia, Korea, Malaysia, Thailand. Includes corporate bonds in IN, KR and MY.

As we enter the second quarter for the year, we take a stock check of the issuance scenario year to date for local currency government bonds in Asia, and put forth our projections for supply of duration in Q2. A few observations at the outset:

Inspite of a challenging interest rate environment, government debt managers in Asia have by and large kept to their issuance plans, and have met what is in several cases a front loaded target for supply.

After a period of some reversal and uncertainty towards the end of 2010, offshore purchases of local currency bonds have picked up again this year, though still running at only around 60% of the pace from Q3 2010. This is particularly striking because data on dedicated EM index driven funds suggests one of the weakest quarters for inflows in the past 9 years.

In several markets in the region (most notably Malaysia), supply pressures will get more acute this quarter, as issuers try lengthening their maturity profile and taking advantage of relatively flat curves.

2011 LOCAL CURRENCY Government Bond Issuance Tally

Source: Deutsche Bank, CEIC, Bloomberg Finance LP

*Corresponding period in 2010 **Fiscal year starting April 2011 ***Fiscal year starting October 2010

Notes: (1) China includes CGBs, local government bonds and savings bonds. (2) HK includes Exchange Fund Notes and government bonds, excludes EF bills (3) India includes central government bonds only. (4) Indonesia includes FR, VR, T-bills, ORI, sukuks and private placements. Maturities include buybacks. (5) Korea includes KTB and KTBi, excludes MSBs. (6) Malaysia includes MGS, GII and syariah savings bonds. (7) Philippines includes T-bonds and retail bonds only. Excludes multi currency OFW bonds. (8) Singapore includes SGS and 1Y T-bills. (9) Taiwan includes TGBs, excludes T-bills. (10) Thailand includes loan bonds only.

2011 Full Year Gross Issuance Year to Date

Gross Maturities Net YTD As of % YTD % YTD 2010*

China CNY bn 1478 578 900 266 1-Apr 18% 12%

HK** HKD bn 37.5 20.5 17.0 0.0 1-Apr

India** INR tn 4.17 0.74 3.43 0.0 1-Apr

Indonesia IDR tn 173.7 74.0 99.7 56.1 1-Apr 32% 36%

Korea KRW tn 82.4 46.3 36.1 21.9 1-Apr 27% 34%

Malaysia MYR bn 91.9 45.3 46.6 24.5 1-Apr 27% 31%

Philippines PHP bn 597.3 306.0 287.3 29.7 31-Jan 5% 14%

Singapore SGD bn 22.8 18.7 4.1 7.4 1-Apr 32% 27%

Taiwan TWD bn 580.0 298.0 282.0 185.0 1-Apr 32% 36%

Thailand*** THB bn 400.0 161.0 239.0 171.4 1-Apr 43% 49%

4 April 2011 Strategy Asia Equities Daily Focus

Page 20 Deutsche Bank AG/Hong Kong

Asia

1 April 2011

Asia Local Markets Weekly Pick up in inflows

Strategy Update

Table of Contents Summary Market Views ................................... Page 02Economics........................................................ Page 03Fixed Income Strategy ..................................... Page 04Foreign Exchange Strategy .............................. Page 13Economic Diary ................................................ Page 15Bond Supply Monitor ....................................... Page 16Monetary Policy Monitor.................................. Page 17Local Markets Analytics ................................... Page 18Asian Economic Indicators ............................... Page 23

Research Team

Sameer Goel Strategist (+65 ) 64236973 [email protected]

Mirza Baig Strategist (+65) 64235930 [email protected]

Linan Liu Strategist (+852) 2203 8709 [email protected]

Arjun Shetty Strategist (+65) 6423 5925 [email protected]

Michael Spencer, Ph.D Chief Economist (++852) 22038303 [email protected]

Dennis Tan Strategist (+65) 6 423-5347 [email protected]

Str

ateg

y

Economics: Asian exports appear to be growing much more quickly in Q1 than they were in Q4 2010 – measured on a QoQ(saar) basis. Investors who look only at YoY growth rates may fail to recognize that the external impetus to growth is almost as strong as it was during the peak of the recovery from the global recession in 2009. We also update our Taylor Rule models for Asia.

Asia bond supply: As we enter the second quarter for the year, we take a stock check of the issuance scenario year to date for local currency government bonds in Asia, and put forth our projections for supply of duration in Q2. A few observations at the outset

In spite of a challenging interest rate environment, government debt managers in Asia have by and large kept to their issuance plans, and have met what is in several cases a front loaded target for supply.

After a period of some reversal and uncertainty towards the end of 2010, offshore purchases of local currency bonds have picked up again this year, though still running at only around 60% of the pace from Q3 2010. This is particularly striking because data on dedicated EM index driven funds suggests one of the weakest quarters for inflows in the past 9 years.

In several markets in the region (most notably Malaysia), supply pressures will get more acute this quarter, as issuers try lengthening their maturity profile and taking advantage of relatively flat curves

FX: Equity inflows to Asia are turning up; USD/KRW range has broken down and central banks' "lines in sand" elsewhere are likely to come under pressure in coming days. We add short USD/THB to our list of Asia FX recommendations.

4 April 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 21

Asia Corporate Credit

1 April 2011

Asia Credit Weekly

A brief review of 1Q 2011

Market Update

Table of Contents Credit opinion & top movers ........................... Page 2-3Key research & news ....................................... Page 04New issue monitor ........................................... Page 07Research catalogue .......................................... Page 10

Research Team

Gene Cheon Research Analyst (+65) 64236967 [email protected]

Jacphanie Cheung Research Analyst (+852) 2203 5930 [email protected]

Devinda Paranathanthri Research Analyst (+65) 64235718 [email protected]

Mathura Yogarajah Research Analyst (+65) 6 423-5721 [email protected]

Marie-Anne Garcia Research Analyst (+65) 6 423 5726 [email protected]

Weekly top-movers (IG)

11

9

8

6

6

-12

-13

-14

-18

-19

POHANG 4.25 '20

PETMK 7.88 '22

ICICI 6.63 '12

KORELE 5.25 '12

KORGAS 4.25 '20

KDB 4.38 '15

NOBLSP 8.50 '13

PETMK 4.25 '14

AXSBIN 4.75 '16

WOORIB 7.00 '15

Change in ASW (bp)

Weekly top-movers (HY)

3.5

3.5

2.3

2.1

2.0

-0.5

-0.6

-1.0

-1.0

-1.5

RNHEF 13.00 '16

RNHEF 11.75 '15

ROADKG 9.50 '15

EVERRE 13.00 '15

KAISAG 13.50 '15

PLNIJ 7.75 '20

STATSP 7.50 '15

PLNIJ 8.00 '19

BTELIJ 11.50 '15

CHINSC 10.50 '16

Change in mid-price

Source : Deutsche Bank

Co

rpo

rate

Cre

dit

As we come to the end of the first quarter, we take a minute to recap on the performance of the Asia ex-Japan credit. For most of 1Q, Asia has underperformed the spread movement globally and to a large extent this has been driven by the high yield market. Technical factors may have played a major role driving the movement. As of year-to-date, the cumulative inflows to EM debt funds stand at just 0.06% of AUM. With the exception of 2009, this represents the weakest start of any year in the past nine years. Additionally, there has been no slowdown in issuance this year, with total year-to-date issuance reaching US$20.4bn. However, despite the geo-political tensions in the MENA region and the Japan earthquake, credit markets overall have been resilient supported by strong liquidity in the market. We have not seen a knee-jerk reaction in Asia as a result of these events. On the fundamental side, full year results have shown strong improvement in-line with our expectations.

Going into the specifics, much of the movement in HY is attributable to the China property sector. Ongoing concerns relating to supply and policy concerns continue to be an overhang on the sector in the near term. Therefore, the sector has underperformed other bonds year-to-date (see figure 2). The key outperformers in HY have mostly been the Indonesian corporates. Asia IG has performed relatively better compared to HY. One reason could be the fact that issuance in the space has been somewhat slow in the first quarter, particularly in the banking sector. On the back of this, performance in IG has been driven by the banks.

This week has been dominated by various results announcements. In the property space, our top-pick Evergrande reported strong results with revenue growing more than 8x. This should reassure investors on its ability to deliver projects. In the Indon space, results from Gajah, Bumi and Indika are also in line with our expectations. The pipeline of new issues has built up over the past week. In the high yield space, Fufeng, Winsway and Uniflora have announced new issues. In the IG space, Franshion, POSCO, Hana and Woori are looking to come to the market.

This week’s highlights: West China Cement: Initiating with a CreditHold recommendation

Indika Energy: Maintain CreditHold on INDYIJ’12 and INDYIJ’16

Gajah Tunggal : FY10 results-managing volatile raw material prices

True Move Ltd : Right on track for 3G expansion

4 April 2011 Strategy Asia Equities Daily Focus

Page 22 Deutsche Bank AG/Hong Kong

North America United States

1 April 2011

US Daily Economic Notes

Solid employment growth to beget wage inflation 4

Eco

no

mic

s

Economic ResearchResearch TeamJoseph A. LaVorgna Chief US Economist 212 250-7329 [email protected]

Carl J. Riccadonna Senior US Economist 212-250-0186 [email protected]

Brett Ryan Economist 212-250-6294 [email protected]

Policy Speeches

9:05 am Atlanta Fed President Lockhart (non-voter) speaks on the U.S. economy in West Palm Beach, FL 9:30 am Chicago Fed President Evans (voter) speaks on the role of government in financial literacy at Money Smart Week in Chicago, IL 3:15 pm Chicago Fed President Evans (voter) speaks with Maria Bartiromo on CNBC about the economy and monetary policy in Chicago, IL 7:15 pm Fed Chairman Bernanke speaks on clearinghouses and financial stability at the Atlanta Fed’s 2011 financial markets conference in Stone Mountain, GA

Year End TargetsReal GDP growth: +4.1% Q4/Q4 Core PCE deflator: +2.1% Q4/Q4 Unemployment rate: 7.8% Fed Funds: 0.50%

Fed Policy

We expect fed funds to be range-bound between 0-25 bps through Q3 2011. The Fed is projected to hike rates to 0.50% in Q4 2011.

Post Employment Conference Call Replay # : (800) 642-1687 or (706) 645-9291 Int’l Conference ID: 29101415

150

Monday Release Forecast Previous Consensus There are no major economic data releases scheduled for today Source: Deutsche Bank, Bloomberg Finance LP

Commentary for Monday: March payrolls rose 216k compared to 194k in February, while the unemployment rate fell another tenth to 8.8%. Private sector hiring once again outperformed the headline rising 230k vs. 240k (revised up from 222k) previously. Thus, private sector job growth in the first quarter of the year was the strongest since Q1 2006. Goods producing employment rose 31k as manufacturing rose 17k (vs. 32k previously); and the service sector logged a gain of 199k (vs. 167k previously). Unsurprisingly, construction employment remained soft (-1k), and government layoffs (-14k) continued entirely as a result of layoffs at the local level (-15k). The length of the workweek was unchanged (at 34.3 hrs) following an upward revision to February. While some analysts may cite the one-tenth decline in the manufacturing workweek (to 40.5 hrs) as reason for concern, this sector added the most jobs in Q1 since the mid-1990s, so we are inclined to believe that this merely reflects a normalization of the number of hours for the existing workforce as new employees are being added. Case in point, aggregate hours in the manufacturing sector are up 4.5% annualized over Q4 2010. Average hourly earnings were flat for the second month in a row and stand just 1.7% above year ago levels. We are not overly concerned by the soft average hourly earnings figures, because wage inflation is a lagging indicator of the labor market—hence, we are unlikely to see much growth in hourly earnings until the employment recovery drives the unemployment rate lower. For example, in each of the business cycles since the early 1980s private payroll gains were deep into positive territory before wage inflation reaccelerated.

The decline in the unemployment rate (8.8% vs. 8.9%) is significant, because it caps off four consecutive months of decline (recall that it was 9.8% in November 2010). The drop was the result of strong employment in the household sector (291k vs. 250k previously.) The labor force participation rate held steady at 64.2% for the third month in a row, so this may be a sign the participation rate is bottoming. If it begins to drift higher, which would not be a surprise as the economy improves, this will make the hurdle marginally higher for the number of jobs needed to lower the unemployment rate (UR). However, since the pace of private sector hiring is accelerating (+1.6% y/y March vs. 0.9% in Q4), we remain confident the UR will continue to move meaningfully lower. –JL & CR

Wage and salary inflation is a lagging indicator of the labor market

-6

-4

-2

0

2

4

86 90 94 98 02 06 10

% y/y

1.5

2.0

2.5

3.0

3.5

4.0

4.5

% y/yAll employees: total pvt industries (ls)

Avg hourly earning in prod & nonsupervisory: total pvt industries (rs)

Source: BLS & DB Global Markets Research

4 April 2011 Strategy Asia Equities Daily Focus