2q06 results presentation

TRANSCRIPT

0

Company’s Presentation2Q06

1

Forward-looking Statements

Notice Notice –– Data and OutlookData and Outlook

The material shown is a presentation of general information about Rossi Residencial S.A.’s record until the present date. It’s a summary of the information with no intention of being complete, that should not be taken under consideration by potential investors as a recommendation. We make no statements nor guarantee the correctness, the conformity or the scope of the following information and any investment decision should not be based on them.

Although ROSSI believes in the expectation and assumption contained on this statement, as well as the prospective information to be reasonable and also based on current data available to its management, ROSSI could not guarantee results nor future events. ROSSI fully exempts itself from the duty of updating any one of the prospective statement and information.

2

1. Highlights

2. Financial Information

3. Closing Remarks

3

Highlights

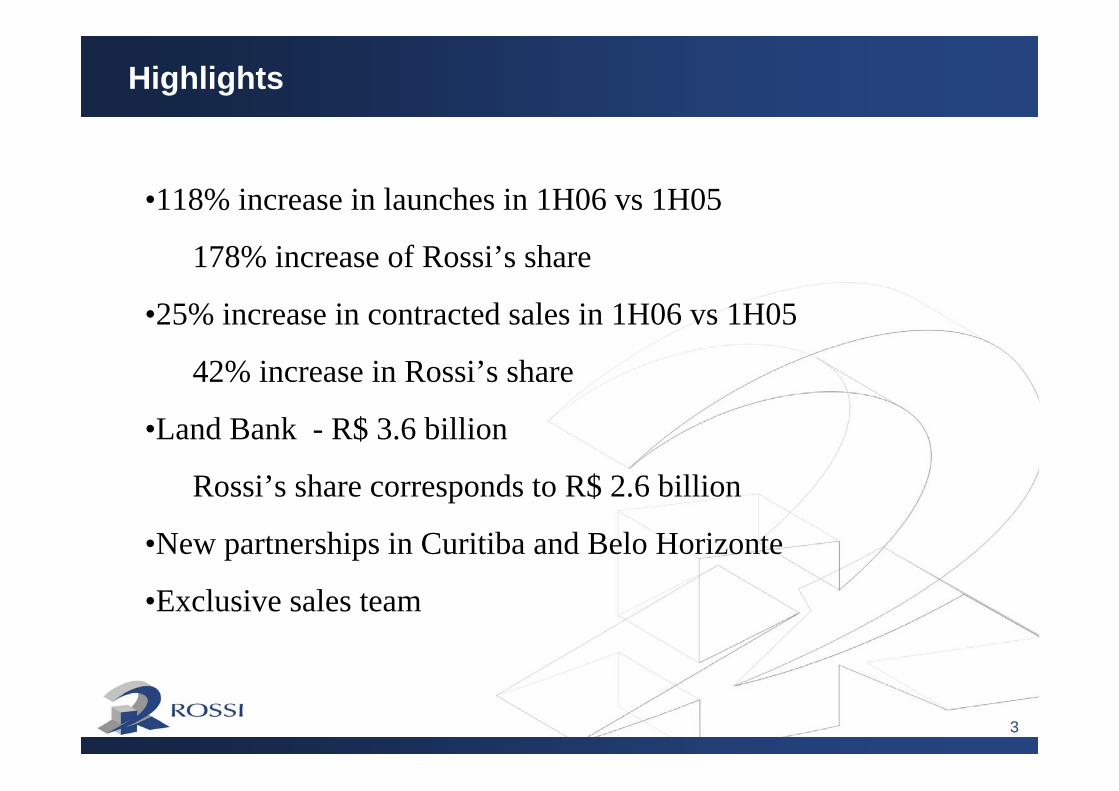

•118% increase in launches in 1H06 vs 1H05

178% increase of Rossi’s share

•25% increase in contracted sales in 1H06 vs 1H05

42% increase in Rossi’s share

•Land Bank - R$ 3.6 billion

Rossi’s share corresponds to R$ 2.6 billion

•New partnerships in Curitiba and Belo Horizonte

•Exclusive sales team

4

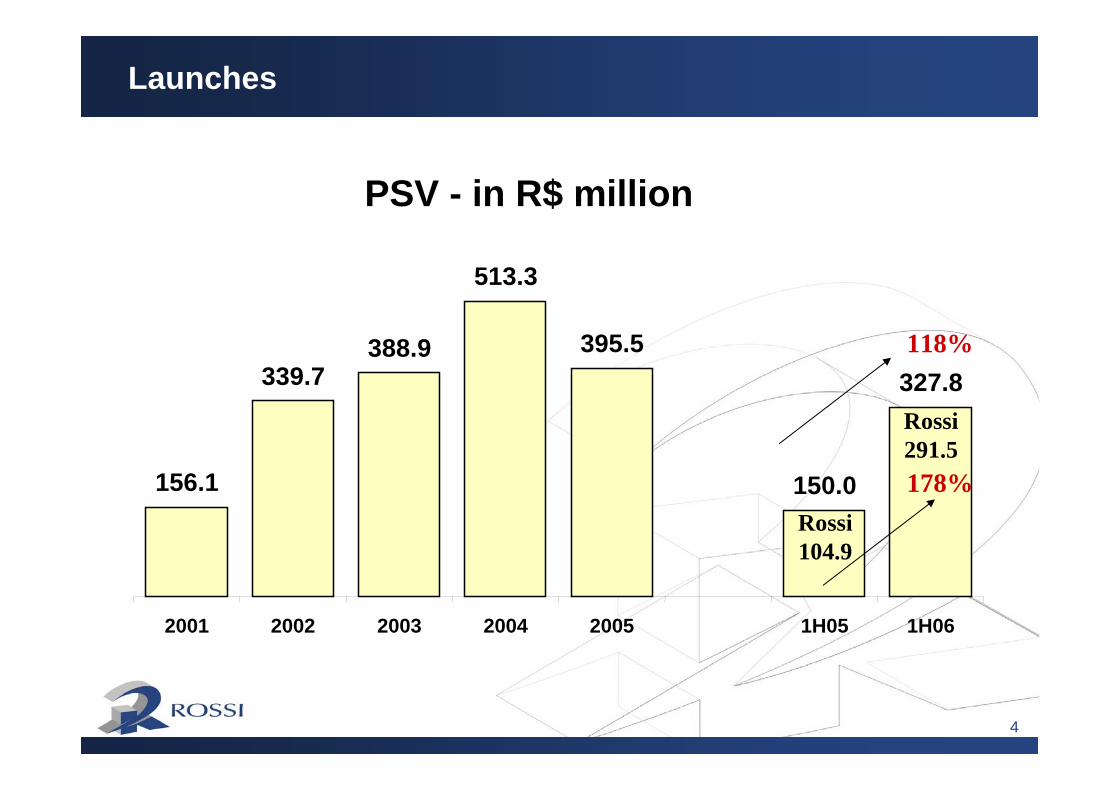

PSV - in R$ million

156.1

339.7388.9

513.3

395.5

150.0

327.8

2001 2002 2003 2004 2005 1H05 1H06

Launches

118%

Rossi104.9

Rossi291.5178%

5

Launches breakdown

Per Regional Office

42%

29%

3%

27%

45%

16%

31%

9%

São Paulo Campinas Porto Alegre Rio de Janeiro

2005 1H06

6

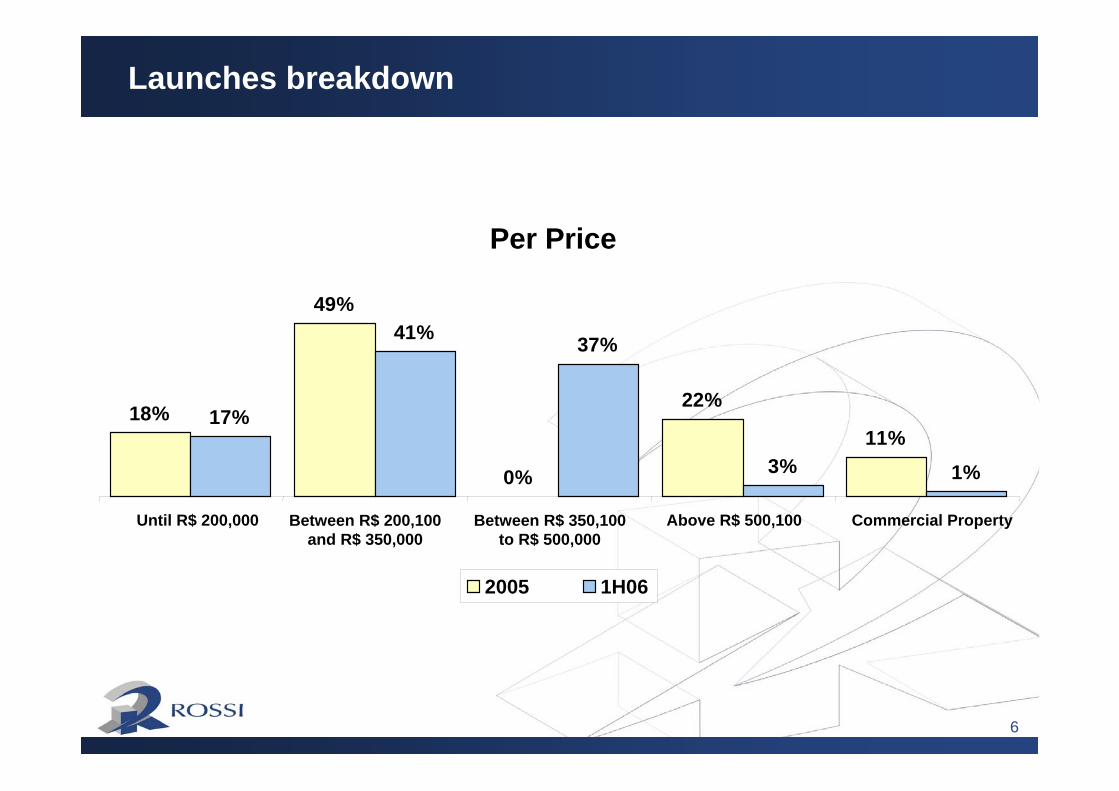

Launches breakdown

Per Price

18%

49%

0%

22%

11%17%

41% 37%

3% 1%

Until R$ 200,000 Between R$ 200,100and R$ 350,000

Between R$ 350,100to R$ 500,000

Above R$ 500,100 Commercial Property

2005 1H06

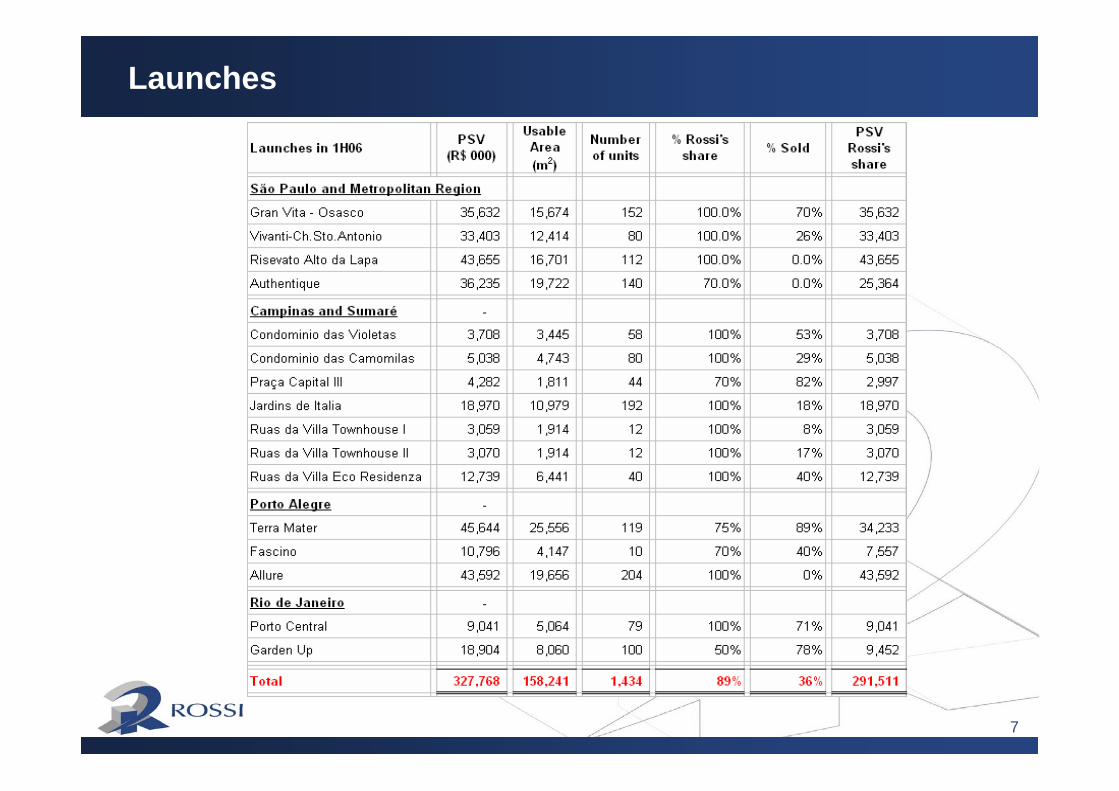

7

Launches

8

Sales - in R$ million

123.0

257.7 268.7

433.4 444.5

209.2261.6

2001 2002 2003 2004 2005 1H05 1H06

Contracted Sales – per period

2001 – 2005CAGR = 38%

25%

Rossi159.7

Rossi227.142%

9

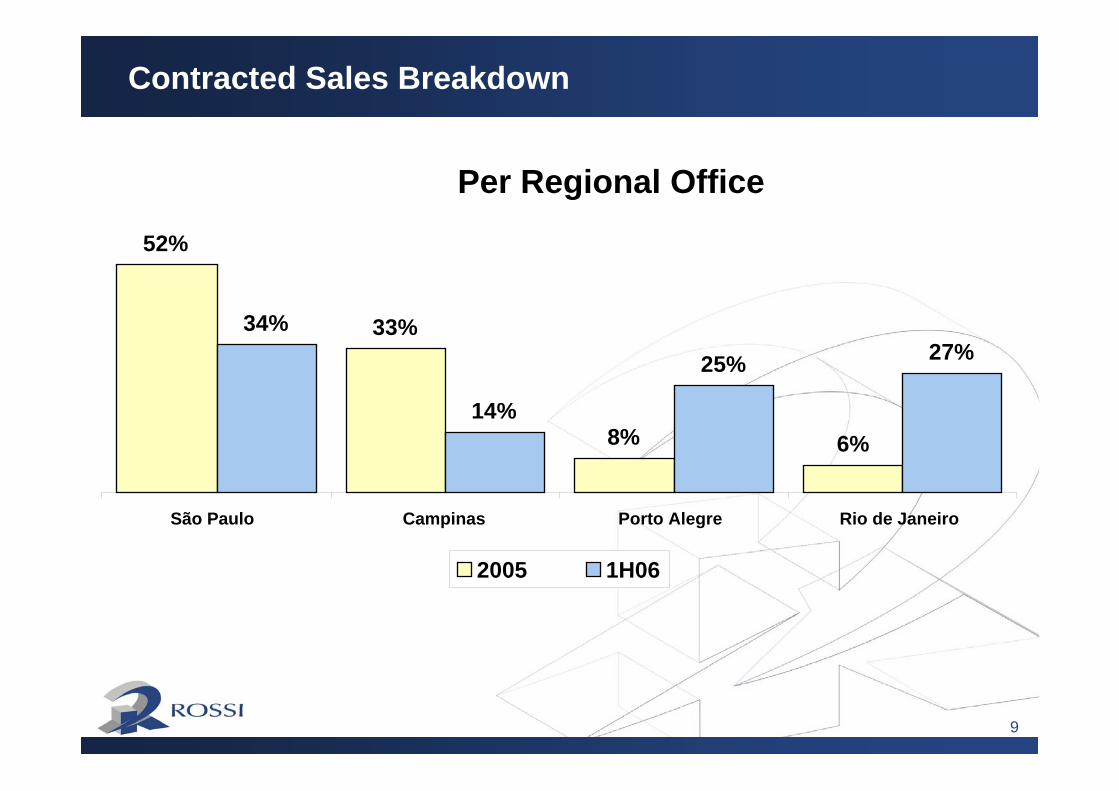

Contracted Sales Breakdown

Per Regional Office

52%

33%

8% 6%

34%

14%

25% 27%

São Paulo Campinas Porto Alegre Rio de Janeiro

2005 1H06

10

Contracted Sales Breakdown

Per Price

22%

42%

4%

21%

11%

30%

39%

18%10%

3%

2005 1H06

Until R$ 200,000 Between R$ 200,100and R$ 350,000

Between R$ 350,100to R$ 500,000

Above R$ 500,100 Commercial Property

11

Land Bank – m²

TOTAL BUILDABLE AREA in m2……2.7MM

USABLE AREA in m2 (+/- 60%)……………….1.6MM

12

Land Bank – R$ thousand

TOTAL POTENTIAL PSV.……………...R$3.6 billionPOTENTIAL PSV Rossi’s share (72%)...R$2.6 billion

Average sales price estimated (R$/m2 usable area)…R$2,250.00

13

Land Bank – performance

1.826

3.567

2.066 98%

Land Bank - in R$ MM

1,326 1,4722,628500 594

939

Dec'2005 Mar'2006 Jun'2006

Rossi Share Partners

1,826

3,567

2,066

14

Joint Venture

• Grupo THÁ – Curitiba PR

The Company announced a joint venture with Grupo THÁ (Curitiba – PR), to operate exclusively in the states of Paraná and Santa Catarina, through which 6 new projects, totaling R$ 200.0 million, will be launched within the next 12 months. The agreement grantsRossi first refusal in Grupo THÁ’s future business undertakings.

•Alicerce – Belo Horizonte MG

More recently, we formed a similar joint venture with AlicerceEmpreendimentos, to operate exclusively in Belo Horizonte – MG. The agreement envisages four projects, with a joint PSV of R$ 100 million.

15

Sales Team

This quarter the Company concluded the setting of its sales team, exclusively focused on selling Rossi’s developments.

The team, with 23 real estate brokers, aims to maintain the units sales liquidity after six months from the launch date.

16

FINANCIALINFORMATION

17

Financial information

Net Revenue - R$ MM

170.9 175.6

1H05 1H06

Gross Income - R$ MM

51.8 46.2

30.3%26.3%

1H05 1H06

Gross Income Gross Margin

Net Income (Adjusted)R$ MM

9.3

28.0

5.4%

15.9%

1H05 1H06

Net Income Net Margin

EBITDA (Adjusted)R$ MM

20.9 19.1

12.2% 10.9%

1H05 1H06

EBITDA EBITDA Margin

18

Contracted sales %

Booked revenues %

Contracted sales %

Booked revenues %

2006 Launches 64,311 50% 8,773 10% 119,275 46% 14,421 8%

2005 Launches 34,263 26% 11,393 13% 76,544 29% 19,848 11%

2004 Launches 10,569 8% 37,199 41% 24,529 9% 71,215 41%

2003 Launches 15,082 12% 24,263 27% 33,410 13% 60,933 35%

2002 Launches 5,669 4% 8,747 10% 7,827 3% 9,168 5%

Total 129,894 100% 90,375 100% 261,585 100% 175,585 100%

Year

1S062Q06

Contracted Sales x Booked revenues

76% 75%

81%78%

19

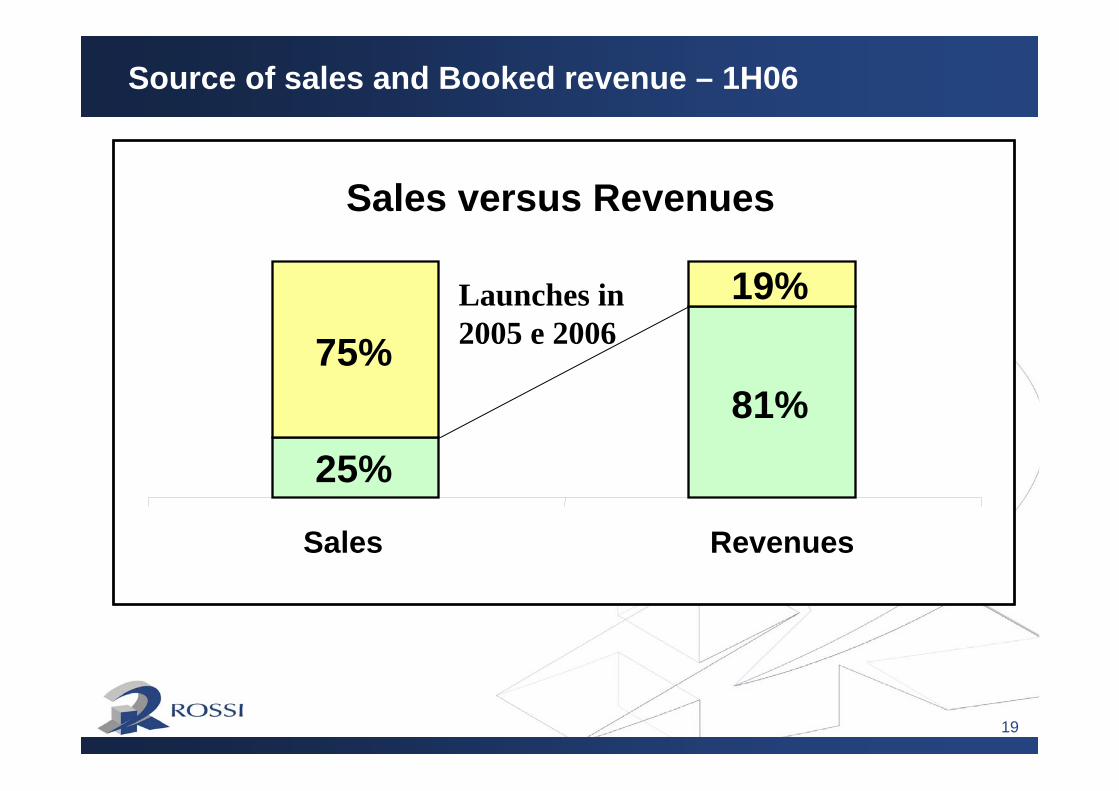

Sales versus Revenues

25%81%

75%19%

Sales Revenues

Source of sales and Booked revenue – 1H06

Launches in 2005 e 2006

20

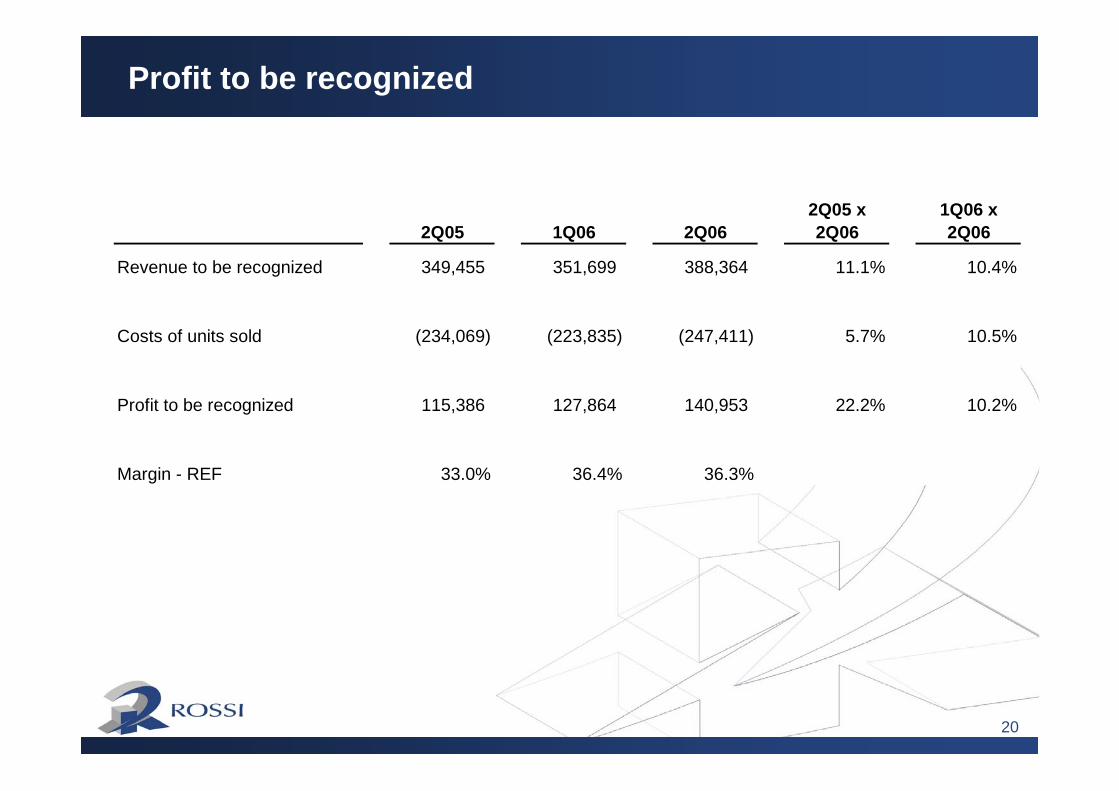

Profit to be recognized

2Q05 1Q06 2Q062Q05 x 2Q06

1Q06 x 2Q06

Revenue to be recognized 349,455 351,699 388,364 11.1% 10.4%

Costs of units sold (234,069) (223,835) (247,411) 5.7% 10.5%

Profit to be recognized 115,386 127,864 140,953 22.2% 10.2%

Margin - REF 33.0% 36.4% 36.3%

21

Net Debt

Indebtedness 2Q06 1Q06 Chg (%)Indebtedness - Short termFinancing for construction 74,442 67,974 9.5%Loans - working capital 2,078 1,882 10.4%Indebtedness - Long termFinancing for construction 24,000 25,159 -4.6%Loans - working capital 506 1,059 -52.2%Total debt 101,026 96,074 5.2%

Cash positionCash and cash equivalents 12,504 13,653 -8.4%Investments - short term 541,520 574,626 -5.8%Investments - long term 1,817 1,816 0.1%Total cash position 555,841 590,095 -5.8%

Net Debt -454,815 -494,021 -7.9%

22

CLOSING REMARKS

23

A question of time:

• Start-up of the development of the recent launches;

• Continuity of the launch plan;

• Scale economy and fixed costs;

• Business generated by recent joint ventures.

Promising Results

24

Why Rossi?

Interest decreaseCredit expansionMaturity extensionHigher demand for new property

Leadership at the Middle Class SegmentFlexibility to adjust according to demandExposure to different markets

Adequate Product Mix

Geographic diversificationPresence in regions with highhousing deficit

The Right Place

Deep local knowledge – regional offices

Experienced Management

30 executives with, at least, 30-year experience in the sectorSAP / Integrated operationsCapacity of managing a high number of projectsStrong market acknowledgment

The Right Time

25

APPENDIX

26

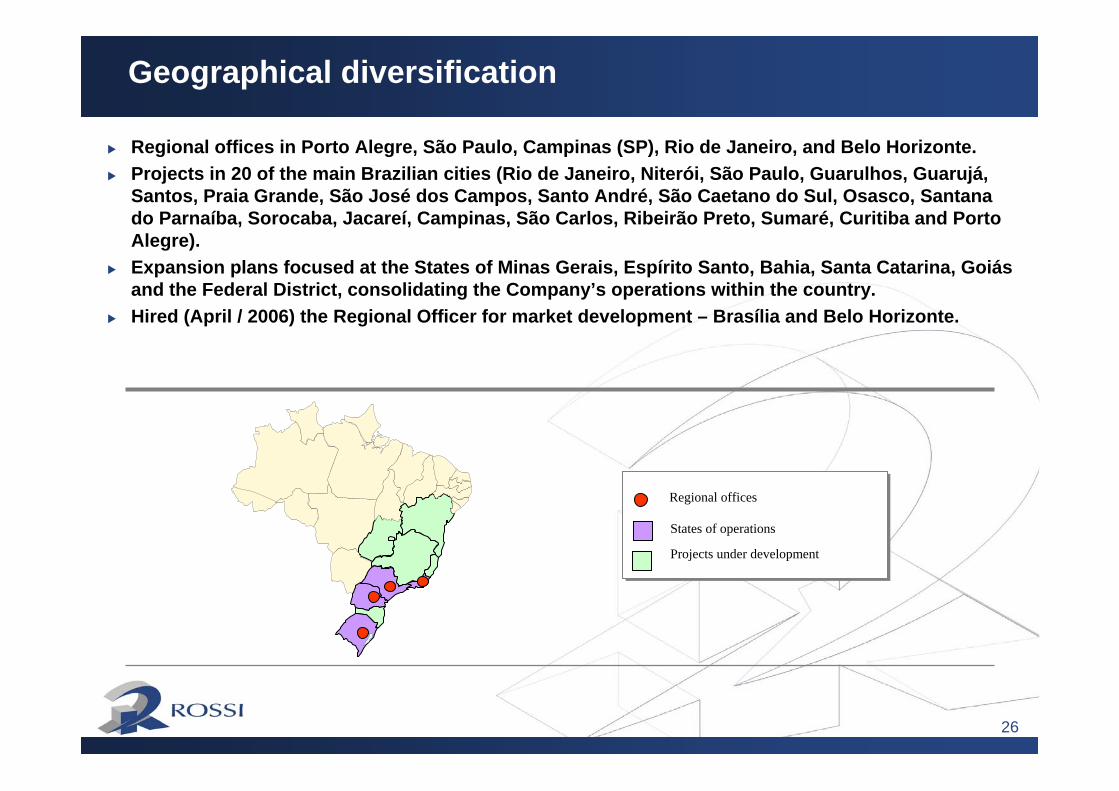

Geographical diversification

Regional offices

Projects under development

States of operations

Regional offices in Porto Alegre, São Paulo, Campinas (SP), Rio de Janeiro, and Belo Horizonte. Projects in 20 of the main Brazilian cities (Rio de Janeiro, Niterói, São Paulo, Guarulhos, Guarujá, Santos, Praia Grande, São José dos Campos, Santo André, São Caetano do Sul, Osasco, Santana do Parnaíba, Sorocaba, Jacareí, Campinas, São Carlos, Ribeirão Preto, Sumaré, Curitiba and Porto Alegre).Expansion plans focused at the States of Minas Gerais, Espírito Santo, Bahia, Santa Catarina, Goiásand the Federal District, consolidating the Company’s operations within the country.Hired (April / 2006) the Regional Officer for market development – Brasília and Belo Horizonte.

27

A Typical Project

Launch 6th Month 12th Month 18thMonth 24th Month 30th Month 36thMonth

0% 60% 80% 85% 90% 95% 100%

Cost Incurred in construction % - - 5% 41% 82% 100% 100%

- 14% 25% 47% 77% 100% 100%

- 8% 17% 24% 33% 44% 100%

CONSTRUCTION

Commercial Launch

Incorporation Confirmation

Start up of the projects

Keysdelivery

End of receivables

Repass

Accumulated sales %

Booked revenues %

Receivables %

28(2.800.000)

(2.550.000)

(2.300.000)

(2.050.000)

(1.800.000)

(1.550.000)

(1.300.000)

(1.050.000)

(800.000)

(550.000)

(300.000)

(50.000)

200.000

450.000

700.000

950.000

1.200.000

1.450.000

1.700.000

1.950.000

2.200.000

-5 -4 -3 -2 -1 1 2 3 4 5 6 7 8 9 11 12 13 14 15 16 17 18 19 20 21 22 23 26 27 29 30 31 32 33 34 35 36

With financing for development

Without financing for development

Investment financed by own cash or debt

• 30% of developments completed• 80% of units sold

Months

Intensive use of capital for expanding

growth

Cash Flow for a Typical Project

Purc

hase

of t

he s

ite

Com

mer

cial

Lau

nch

Beg

inni

ng o

f the

dev

elop

men

ts

Con

clus

ion

of th

e de

velo

pmen

tsD

eliv

ery

of th

e ke

ys

Secu

ritiz

atio

n