2nd original report on ulip

TRANSCRIPT

A PROJECT REPORT

ON

COMPARATIVE STUDY ON UNIT LINK INSURANCE POLICY IN THE

INDIAN INSURANCE MARKET WITH SPECIAL REFERENCE TO

KOTAK MAHINDRA OLD MUTUAL LIFE INSURANCE & TATA AIG

LIFE INSURANCE

SUBMITTED BY

ANAND INGOLE

UNDER THE GUIDANCE OF

MRS. ADITI TANDALE JOSHI

UNIVERSITY SEAT NO-

SUBMITTED TO

UNIVERSITY OF PUNE

IN THE PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF BBA

S.P.MANDALI’S

SIR PARASHURAMBHAU COLLEGE,

PUNE-30

1

ACKNOWLEDGEMENT

I extend my sincere thanks to our Coordinator Dr. Rashmi Hebalkar for her

valuable suggestion, encouragement and generous help and for their direct and

indirect support for completion of this work.

I wish to express my deepest sense of gratitude and indebtness to my esteemed

guide Prof. ADITI JOSHI, of BBA, S. P. College, Pune, for her expert guidance

and scholarly supervision, endless motivation, encouragements and freedom to

carry report work. I appreciate her dedication, professionalism, genuine concern

and most important, her spirit. I thank her from my heart and express my

indebtedness for her training, which will be a lifetime asset. It is my greatest

privilege to be one of her students.

It gives me immense pleasure to offer profound thanks to my colleagues and

friends, Atul, Ashish, Rajan, Pratik, Sagar,& Vighnesh [T.Y.B.B.A] for their

valuable comments, constant motivation, criticism and discussions giving shape

and design to the research work.

My heartiest thanks to my sisters, and all my other friends for their constant

support and for listening to all my complaints. No words are adequate to describe

my gratitude to my Mother, Father, Uncle, & Aunt for their patience,

understanding, unending love, motivation and for everything they have done in

making me what I am today.

2

TO WHOMSOEVER IT MAY CONCERN

This is to certify that Mr. ANAND INGOLE is a bonafide student of

S.P.College, Pune. He has successfully carried out his summer project titled

“COMPARATIVE STUDY ON UNIT LINK INSURANCE POLICY IN

THE INDIAN INSURANCE MARKET WITH SPECIAL REFERENCE TO

KOTAK MAHINDRA OLD MUTUAL LIFE INSURANCE & TATA AIG

LIFE INSURANCE”

We wish him all the best for his future

Mrs. ADITI TANDALE-JOSHI Dr. Rashmi Hebalkar

(Project Guide) (Coordinator BBA)

3

INDEX

SR. NO. TITLE PAGE NO

1 Chapter – I [Introduction]

1.1 Introduction

1.2 Title

1.3 Aim & Objective

1.4 Significance & Need

1.5 Scope & Limitations

1.6 Working Definition

1.7 Conclusion

2 Chapter – II [Review Literature]

2.1 Introduction

2.2 Review of books

2.3 Review of Articles

2.4 Company Literature

2.5 Conclusion

3 Chapter – III [Research Methodology]

3.1 Introduction

3.2 Research Methodology

3.2.1 Quantitative Methodology

3.2.2 Qualitative Methodology

3.3 Method of Data Collection

3.3.1 Primary Data

4

3.4 Research Design

3.5 Conclusion

4 Chapter – IV [Analysis Of Data]

4.1 Primary Data Analysis

4.2 Secondary Data Analysis

4.3 Conclusion

5 Chapter – V [Finding & Recommendations]

5.1 Finding

5.2 Suggestions / Recommendations

5.3 Area Of Further Study

5.4 Conclusion

5

CHAPTER-1

6

INTRODUCTION

1.1 INTRODUCTION OF INSURANCE

Today, only one business, which affects all walks of life, is insurance business.

That’s why insurance industry occupies a very important place among financial

services operative in the world. Owing to growing complexity of life, trade and

commerce, individuals as well as business firms are turning to insurance to manage

various risks. Therefore a proper knowledge of what insurance is and what purpose

does it serve to individual or an organization is therefore necessary.

7

The future is never certain . So it’s rightly said, “AN INSURANCE POLICY

IN HAND KEEPS THE TENSION AWAY.”

Insurance, essentially, is an arrangement where the losses experienced by a few are

extended over several who are exposed to similar risks. Insurance is a protection

against financial losses arising on the happening of an unexpected event. Insurance

companies collect premium to provide security for the purpose. In simple words it

is spreading of risks amongst many people.

i) LIFE INSURANCE: It is a fundamental part of a sound financial plan which

helps to insure your loved ones. Life insurance – the only instrument that takes

care of these 3 probabilities .

1.Children’s education & marriage

2. Wealth creation

3. Living death

ii) Benefits:

1) SAVINGS -For unforeseen circumstances.

2) EDUCATION -For child’s education and for higher studies.

3) RETIREMENT -Facilitates adequate savings for worry free retired life.

iii) Insurance ---a Flash back:

The earliest transaction of insurance as practiced today can be traced back to the

14th century AD. The business of insurance started with marine business by Traders

who used to gather in the Lloyd’s coffee house in London, wherein they had

agreed to insure their ships in transit.

The 1st Life Insurance Policy was issued on 18th June, 1583, on the life of

William Gibbons for a period of 12 months.

Life Insurance in its current form came in India from the UK, with the

establishment of British firm, Oriental Life insurance Company, in 1818

8

The 1st Indian insurance company was the Bombay Mutual Assurance

Society Ltd, formed in 1870.

By the year 1956, when the life insurance business was nationalized and the Life

Insurance Corporation Of India ltd (LIC) was formed on 1st September, 1956

and there were 245 companies existing at that time in India.

By 31.3.2002, eleven new insurers had been registered and had begun to transact

Life insurance business in India.

IV) INSURANCE CLASSIFICATION

1.Life

2.Term

3.Endowment

4.Unit-linked

5.Money-back

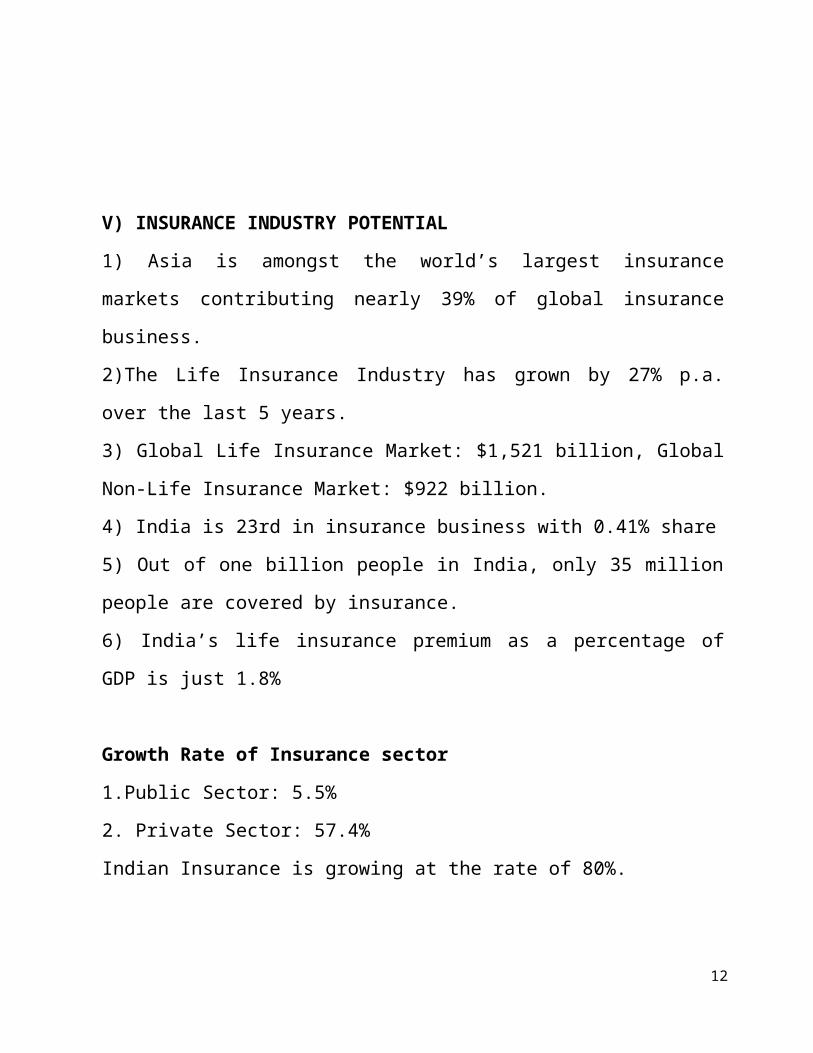

V) INSURANCE INDUSTRY POTENTIAL

1) Asia is amongst the world’s largest insurance markets contributing nearly 39%

of global insurance business.

2)The Life Insurance Industry has grown by 27% p.a. over the last 5 years.

3) Global Life Insurance Market: $1,521 billion, Global Non-Life Insurance

Market: $922 billion.

4) India is 23rd in insurance business with 0.41% share

5) Out of one billion people in India, only 35 million people are covered by

insurance.

9

6) India’s life insurance premium as a percentage of GDP is just 1.8%

Growth Rate of Insurance sector

1.Public Sector: 5.5%

2. Private Sector: 57.4%

Indian Insurance is growing at the rate of 80%.

LIFE INSURANCE COMPANIES IN INDIA

Public sector

1. Life Insurance Corporation of India

Private Players

2. AEGON Religare Life Insurance

3. Aviva Life Insurance

4. Bajaj Allianz Life Insurance

5. Bharti AXA Life Insurance Co Ltd

6. Birla Sunlife

10

7. CANARA HSBC Oriental Bank of Commerce LIFE INSURANCE

8. Star Union Dai-ichi Life Insurance

9. DLF Pramerica Life Insurance

10. Edelweiss Tokio Life Insurance Co. Ltd

11. HDFC Standard Life

12. Future Generali Life Insurance Co Ltd

13. ICICI Prudential

14. IDBI Federal Life Insurance

15. IndiaFirst Life Insurance Company

16. ING Vysya Life Insurance

17. Kotak Life Insurance

18. Max New York Life Insurance

19. MetLife India Life Insurance

20. Reliance Life Insurance Company Limited

21. Sahara Life Insurance

22. SBI Life Insurance Company Limited

23. Shriram Life Insurance

24. TATA AIG Life Insurance

WHAT IS AN ULIP (Unit Linked Insurance Plan)?

A policy, which provides for life insurance where the policy value at any time

Varies according to the value of the underlying assets at the time. ULIP is life

insurance solution that provides for the benefits of protection and flexibility in

investment. The investment is denoted as units and is represented by the value that

it has attained called as Net Asset Value (NAV).

A unit-linked insurance plan provides both insurance and investment benefit. In

unit linked plans, the premiums paid are invested in funds offered by the company;

the policyholder determines the appropriate ratio of investments into these funds.

11

The funds are generally invested in equities, debt instruments, money market

instruments, and government securities.

The value of the policy is determined on any day by multiplying the number of

units issued by the value of units on that day. The value of these units is called the

Net Asset Value (NAV) and is normally published in newspapers on a daily basis.

Unit-linked insurance products are risky because the premium money invested is

subject to market risk. The funds do not offer a guaranteed or assured return.

Insurance companies will only show you a projected return, which may or may not

be achieved during the term of the policy.

COMPANY PROFILE OF TATA AIG LIFE INSURANCE

It is a joint venture between TATA and AIG. It provides insurance cover for both

for life and group. It deals in all kinds of products. And now concentrates more on

UNIT LINKED PLANS.

It is Tata-AIG which consumers trust the more when it comes to giving exact claim

valuation, best in consumer satisfaction and trusted as the best in quick disposal of

claims.

12

Its working is based on Business brought up by Business Associates who are the

advisors/agents for the company.

Areas of business

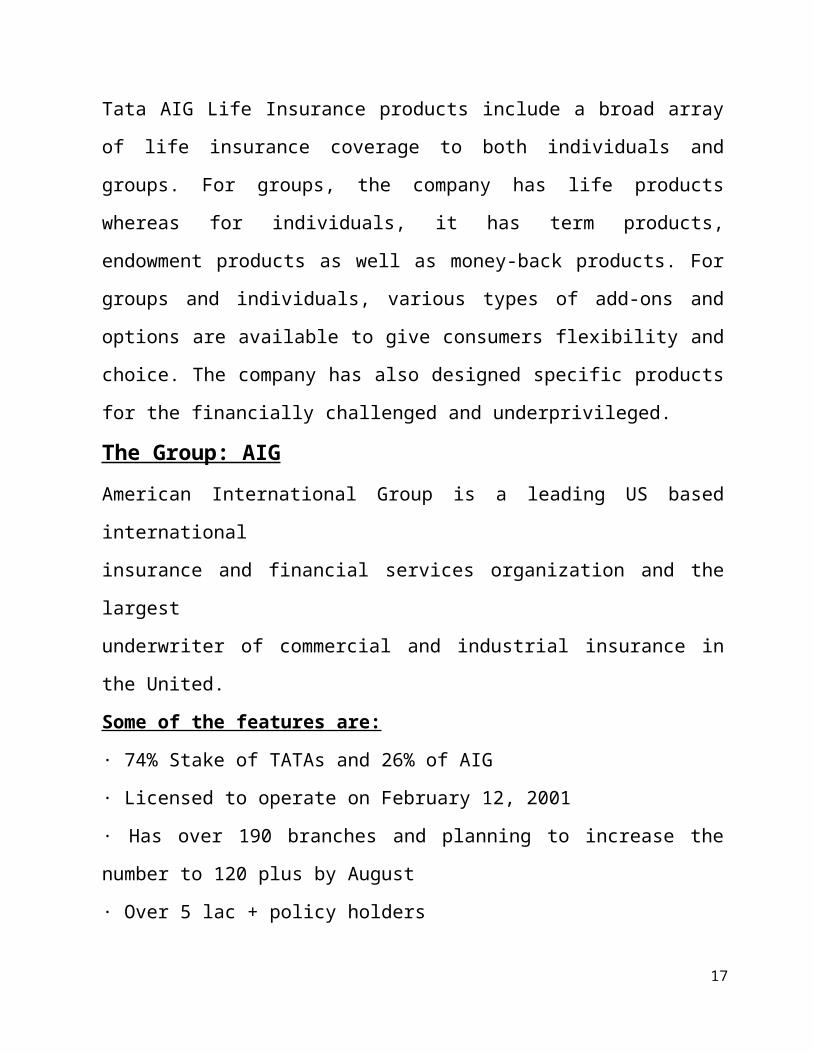

Tata AIG Life Insurance products include a broad array of life insurance coverage

to both individuals and groups. For groups, the company has life products whereas

for individuals, it has term products, endowment products as well as money-back

products. For groups and individuals, various types of add-ons and options are

available to give consumers flexibility and choice. The company has also designed

specific products for the financially challenged and underprivileged.

The Group: AIG

American International Group is a leading US based international

insurance and financial services organization and the largest

underwriter of commercial and industrial insurance in the United.

Some of the features are:

· 74% Stake of TATAs and 26% of AIG

· Licensed to operate on February 12, 2001

· Has over 190 branches and planning to increase the number to 120 plus by

August

· Over 5 lac + policy holders

Some of the features of TATA are:

1. Over 260,000employees

2. Operates in 130 countries worldwide

3. Trusted by over 3 million shareholders

4. Diversified business interest ( 92 companies)

5. Largest FOREX earner

13

6. Revenues of US $ 14.25 billion

7. Deep rooted commitment towards society.

Some of the features of AIG are:

1. In business since 1919

2. Over 80,000 employees worldwide

3. Presence in over 130 countries

4. Over 50 million customers worldwide

5. Revenues over US $ 81.3 billion

6. Ranks 4th on the FORBES 500 LIST OF 2003.

7. Deals in General and life insurance, asset management, financial services.

COMPANY PROFILE OF KOTAK MAHINDRA OLD MUTUAL

LIFE INSURANCE

Kotak Mahindra Old Mutual Life Insurance Limited Kotak Mahindra Old Mutual

Life Insurance Limited is a joint venture between Kotak Mahindra Bank Ltd. and

Old Mutual plc.

KOTAK GROUP is one of the top most financial product service providers in

India. It is one of India's leading financial conglomerates, offering complete

financial solutions that encompass every sphere of life. From commercial banking,

14

to stock broking, to mutual funds, to life insurance, to investment banking, the

group caters to the financial needs of individuals and corporate.

The group has a net worth of over Rs5,824 crores, employs around 10,800

people in its various businesses and has a distribution network of branches,

franchisees, representative offices and satellite offices across 370 cities and towns

in India and offices in New York, London, San Francisco, Dubai, Mauritius and

Singapore.

Old Mutual

Old Mutual plc is an international long-term savings, protection and investment

Group. Originating in South Africa in 1845, the Group provides life assurance,

asset management, banking and general insurance to more than 15 million

customers in Europe, the Americas, Africa and Asia. Old Mutual plc is listed on

the London Stock Exchange and the Johannesburg Stock Exchange, among others.

In the year ended 31 December 2010, the Group reported adjusted operating profit

before tax of £1.5 billion (on an IFRS basis) and had £309 billion of funds under

management, from core operations.

The KOTAK MAHINDRA Group was born in 1985 as Kotak Capital

Management Finance Limited. This company was promoted by

Uday kotak, Sidney A. Pinto and Kotak & Company. Industrialists Harish

Mahindra and Anand Mahindra took a stake in 1986, and that's when the company

changed its name to Kotak Mahindra Finance Limited. Since then it's been a

steady and confident journey to growth and success.

1.2- TITLE

15

COMPARATIVE STUDY ON ULIPS IN THE INDIAN INSURANCE

MARKET” WITH SPECIAL REFERENCE TO KOTAK MAHINDRA OLD

MUTUAL LIFE INSURANCE & TATA AIG LIFE INSURANCE

1.3 OBJECTIVES

1. Working of ULIP To find how ULIP plans differs from the other financial

products.

2.. Whether the long term investment of the investor are beneficial through ULIP

plan.

3. To compare the two companies ULIP plans with each other.

4.Find strength and weakness of ULIP plan.

5. Study of the consumer perception towards ULIP.

1.4 SIGNIFICANCE & NEED -

1.It helps to know difference between ULIP and other financial products.

2.It will help to know about buying behavior of consumer .

3.It will help to know consumer perception towards ulip

1.5 SCOPE AND LIMITATIONS

SCOPE OF THE STUDY

This study aims to make a comparative study of the Unit Linked Insurance Plans

(ULIPs) of KOTAK Life Insurance Company with that of some major selected

players in the Indian insurance market and study the consumer perception towards

16

various insurance products. The comparative analysis is based on the empirical

data collected from the PUNE city. The study also aims to discuss in detail the

various positioning strategies adopted by KOTAK in general.

ADVANTAGES OF STUDY-

The following are some of the advantages to study Unit linked plans

TO KNOW-

1.Extra protection riders between two companies..

2.Variable investment options.

3.Which company is good for investment.

4.whether it is beneficial to invest in ULIP policies.

5.Risk involved in investment.

LIMITATION OF THE STUDY-

Following are limitation of the study –

1.The study is done with reference to two companies only.

2.Information provided by the companies may not be true.

3.The study is confined only to a small segment of the entire population due to

time constraints and hence the results are applicable only to the city of pune city.

4.It is not always possible to evaluate companies under similar parameters since

many companies deal with various businesses thus clubbing all the companies on

the same parameters is not always possible.

1.6 WORKING DEFINITIONS

Definition of 'Insurance'

17

A contract (policy) in which an individual or entity receives financial protection

or reimbursement against losses from an insurance company. The company pools

clients' risks to make payments more affordable for the insured.

Definition of ULIP-

ULIP is an abbreviation for Unit Linked Insurance Policy. A ULIP is a life

insurance policy which provides a combination of risk cover and investment. The

dynamics of the capital market have a direct bearing on the performance of the

ULIPs. IN A UNIT LINKED POLICY, THE INVESTMENT RISK IS

GENERALLY BORNE BY THE INVESTOR.

CONCLUSION- In this chapter we studied about what is life insurance & ulip,

Meaning,definition of ulip, objective of the study,insurance companies in India,

company profile of KOTAK MAHINDRA AND TATA AIG LIFE INSURANCE

COMPANY

CHAPTER-2

18

REVIEW OF LITERATURE

2.1 ABOUT UNIT LINKED INSURANCE PLANS

1.INTRODUCTION

ULIPS, has possibly been the single largest innovation in the field of life insurance

in the past several decades. It wasn’t too long back, when the good old endowment

plan was the preferred way to insure oneself against an eventuality and to set aside

some savings to meet one’s financial objectives. Then insurance was thrown open

to the private sector. The result was the launch of a wide variety of insurance plans,

19

including the ULIPs.

Two factors were responsible for the advent of ULIPs on the domestic insurance

horizon.

First was the arrival of private insurance companies on the domestic scene. ULIPs

were one of the most significant innovations introduced by private insurers. The

other factor that saw investors take to ULIPs was the decline of assured return

endowment plans.

These were the two factors most instrumental in marking the arrival of ULIPs, but

another factor that has helped their cause is a booming stock market. While this

now appears as one of the primary reasons for their popularity, it is believed that

ULIPs have some fundamental positives like enhanced flexibility and merging of

investment and insurance in a single entity that have really endeared them to

individuals. ULIPs came to play in the 1960s and became very popular in western

Europe and Americas.

2)MEANING OF ULIPS

A policy, which provides for life insurance where the policy value at any time

varies according to the value of the underlying assets at the time. ULIP is life

insurance solution that provides for the benefits of protection and flexibility in

investment. The investment is denoted as units and is represented by the value that

it has attained called as Net Asset Value (NAV). In order to offset the erosion of

money, ULIPS are introduced. The Sum Assured is expressed in units whose price

is linked to an inflation related index.

20

In today’s times, ULIP provides solutions for insurance planning, financial needs,

financial planning for children’s future and retirement planning.

Features of ULIPs distinguish itself through the multiple benefits that it provides to

the customer which are as follows-

Life protection

Investment and Savings

Flexibility

Adjustable Life Cover

Investment Options

Transparency

Options to take additional cover against- Death due to accident-

Disability- Critical Illness- Surgeries·

Tax benefits.

3 ) ULIPS VERSUS ENDOWMENT

The following points help us to get a better idea how ULIPs differ from Traditional

(Endowment Plans)

1) SUM ASSURED:

This is the most fundamental difference between ULIPs and the traditional plans.

21

In case of endowment the agent will ask you “HOW MUCH INSURANCE

COVER DO YOU NEED?” & the premium is calculated as per the estimated sum

assured.

In case of ULIPs you are asked “HOW MUCH PREMIUM CAN YOU PAY?” &

accordingly the Sum Assured is estimated.

2) INVESTMENTS:

Endowment plans invest in-

1.Government Securities

2.Corporate bonds

3.Money market instruments

( no investment in the stock market)

ULIPs invest in

1.Equities

2.Bonds

3.G-secs

4.Money market.

3) FLEXIBILITY:

22

In case of ULIPs the investor can choose the fund in which he wants to

allocate his portfolio. He can go for pure Equity, or a combination of debtequity

,depending on his requirements.

The investor also has the option of switching from one fund to another .

Usually Free switches are given during the year.

This option is not available in case of Endowment.

4) TOP UP FACILITY:

A top up is a one time additional investment in the ULIP over and above the annual

premium. This feature works well when you have a surplus that you are looking to

invest in a market linked avenue, rather than keeping in an FD or Savings account.

This feature is not for Endowment.

5) TRANSPARENCY:

ULIPs are more transparent than Endowment Plans as their NAV is declared

EVERYDAY. As a result you can know how your ULIP has performed.

In case of Endowment, the insurance company sends you an annual statement of

bonus declared during the YEAR. , which gives us an idea how our plan is

performing.

6) LIQUIDITY:

23

Since ULIPs investments are NAV based it is possible to withdraw a portion of

Your investments before maturity (after 3yrs lock in period is over).The

withdrawal is possible provided the minimum fund value is maintained.

In case of Endowment, you can only Surrender your policy, but you wont get

everything that you have earned on your policy in terms of premium and bonus.

The Surrender Value is much less than the Sum Assured and the Bonus is also not

paid.

THUS investing in ULIPs or in ENDOWMENT depends on the person’s

RISK taking ability. A Risk Averse person may go for an Endowment,

Whereas a person who wants his corpus to appreciate and is ready to take

risks can go for ULIPs.

Therefore we can say that investing in ULIPs is the best in a growing

Economy as compared to the TRADITIONAL PLANS.

4) ULIPS AND YOU

IRDA has played a part in making ULIPs more investor friendly. Today more

individuals are opting for ULIPs to create wealth over a long term. Over here I

have outlined how ULIPs can help you to fulfill that responsibility.

24

1) If you are between 25 –35 years of age

ULIPs help you to save for your child’s education, marriage, planning for your

retirement and providing for your family in case of your absence.

ULIPs Child plan ------------- --------for your child’s education, marriage.

ULIPs Endowment plan------------- for helping you to meet investment objectives

like buying a house or setting up a business.

ULIPs Pension plan-------------------for your retirement. A long term retirement

planning could be done with an Equity push, as it is necessary to build up a strong

corpus to face your rigorous retirement.

2) If you are between 35 –45 years of age If you haven’t invested in ULIPs, it is

not too late even now.

You can opt for some ULIPs as mentioned earlier. Remember ,unlike

Endowment,which gets really expensive at an advanced age, ULIPs because of the

way they are , do not turn out to be expensive.

3) If you are above 45 years of age

In this age bracket, you have to review your insurance cover, taking into

consideration the changes of your life style, income needs, etc. By this time your

25

ULIP pension plan must have matured, so now you can opt for an Annuity

(immediate or deferred) depending on your need.

5) EXPENSES IN ULIPs

Following expenses have to be incurred for ULIPs:

a) Mortality charges: charged by the company to cover the risk of an eventuality to

an

individual.

b) Administration Charges: charged by the company to cover the daily expenses,

overhead costs, agent’s commission etc.

c) Fund Management charges: are levied by Insurance companies to cover the

expenses incurred by them in managing ULIP monies. Charges are high for

managing monies in an Equity Fund.

d) ULIP Fund switch charges: Such are borne by the individuals when they decide

to switch their money form one type of find to another.

e) Top up Charges: A certain % is deducted from the Top up amount to recover the

expenses incurred on managing the same.

f) Cancellation/ Surrender charges: It is charged when an individual wishes to

surrender his ULIP policy.

6) HOW ULIPS MANAGE MONEY

ULIPs are different from traditional plans.

26

They invest their monies in Shares, bonds, G-secs, money market instruments in

varied proportions.

Insurance companies usually maintain 4 types of funds.

Growth Fund: 100% equity

Balanced Fund: 60% equity, 40% debt.

Debt Fund: 100% debt.

Money Market Funds 100% MM instruments for a period of one year RISKS

RETURNS.

In case of equity, the risk and return is the highest, and vice verse for Money

market instruments.

7) STEPS FOR ULIP SELECTION

1.Understand what ULIPs are all about.

2.Focus on your need and risk profile

3.Compare ULIP products from various insurance companies

4.Go for an experienced Insurance advisor

2.2 REVIEW OF ARTICLES

Probing your probity by

Swami Saran Sharma | 3/7/2012 1:00:12 PM moneycontrol.com

27

It’s the examination season, and last week I overheard a conversation between two

students on the number of sheets they used while answering. The discussion moved

towards how certain teachers award higher marks to students who use more sheets,

especially in subjects like English, history and economics. The insurance regulator

seems to be inspired by the examination season in releasing the proposed exposure

draft on guidelines on prospect product matrix for life insurance.

While the move will bring in the much-needed standardisation in filling insurance

forms, it is not suitable for the Indian market. First, the guideline assumes that

insurance is bought only by the literate. Next, the extent of details sought in the

proposal-cum-needs analysis form is too complex even for some of the aware

consumers to fill. I made a valiant attempt to fill the seven-page document in

which the first six sought several financial and personal details. Take for instance a

question like ‘Are you politically exposed?’ I see little value that an insurer will

derive from this response to arrive at the mortality risk I carry. There are

uncomfortable personal details sought like liabilities, expected inheritance, future

income and expenditure for the next 10 years! The past decade has seen such an

economic boom that any prediction on the future would have been off the mark.

Equally baffling is the column on expected returns from the policy; is it risk

transfer or investment that we are looking at? If it is the latter, it is no more

insurance.

I don’t think anyone will have easy access to his/her existing savings and

investment details, forget the details of existing policies.The proposed draft is

based on the premise that a prospective buyer will declare all the information the

insurer seeks. The approach is towards financial planning than figuring insurance

needs. Will this mean that the Insurance Regulatory Development Authority

(IRDA) will certify agents and distributors to qualify as financial planners to sell

28

insurance? It is unlikely for an agent to manage all the details listed in the form,

which is why the draft guideline provides a leeway to them by not binding them

with the details being sought.

According to the guideline, if the prospect refuses to provide information as sought

by the insurer, agent or broker; the latter shall certify such refusal on the proposal-

cum-needs analysis form. Many agents will use this lacuna and not get the form

filled completely, leading to mis-selling on record.

But will the form need to be filled by online buyers, and how will tele-calling

intermediaries handle the form? Overall, I find the move completely flawed. This

procedure is likely to work in societies with a high financial literacy. We are far

from such finesse in data gathering, analysis and maintenance. My worry is also

about the misuse of the data that I share with the insurer as it can compromise my

financial safety. This issue is far more complicated than the UID project if it is

enforced in its current form.

Lastly, if standardisation of the proposal form is allowed; it will do away with the

USP that each insurer has. Unlike tax forms, which can be standardised; life

insurance is a customised solution that can be tailored to suit the needs of a

prospect. Moreover, the experience of the advisor comes into play when suggesting

insurance plans. By adopting a template product-matrix to suit customer needs,

IRDA is assuming the limitations in an agent’s ability to suggest the right policy to

a client. And if the insurer has nothing that fits the prospect’s needs? It is unlikely

that an agent will suggest the client to buy one from a competitor.

29

Market Research Projects ICT Insurance Market Growth in India at 14%

CAGR Through 2015 by- find articles.com

MarketResearch.com has announced the addition of the new report "ICT in

Insurance Industry in India 2012," to their collection of IT Services market reports.

For more information, visit http://www.marketresearch.com/Netscribes-India-Pvt-

Ltd-v3676/ICT-Insurance-India-6823146/

ICT adoption in Insurance Industry is expected to witness a dynamic growth in the

ensuing years. Currently, the adoption of ICT in insurance industry is undergoing a

dynamic growth rate owing to the growing complexities arising from huge

customer base. Insurers primarily implement technology in the areas of customer

service, data analytics and process management.

With the ongoing growth in customer base and daily transactions, insurers in India

are gradually shifting their focus towards the adoption of ICT oriented tools,

services and platforms. Until now, the ICT adoption in insurance industry has

occurred in a phased manner, wherein it has exhibited a steady but impressive

growth rate over the years. "Judging by the current scenario in the market, ICT

spending by insurers in India stood at INR 76.17 bn in 2011 and is anticipated to

grow at a CAGR of around 14% til 2015," says Mr. Kalyan Banga, Product

Manager at Netscribes. Maturing along with technology standards, the current ICT

landscape within the insurance industry can be associated with rising demand and

cut throat competition amongst the ICT vendors. Types and attributes of the

solutions that experience the most demand within the insurance sector have also

changed over the years. "Primarily, technologies focused to provide better

customer services are preferred the most. Analysis of colossal amount of data and

information along with generating insights from these data are also experiencing

30

exponential surge in demand. Advancement in the field of mobile technology and

the immense popularity of social networking sites have also grabbed the attention

of industry significantly," noted Kalyan.

The report begins with a snapshot of the insurance industry which briefs about the

facts and figures of insurers operating in India. It lists down the number of insurers

operating in the sector along with the segmentation of public and private insurers.

The hierarchy of the Indian insurance industry is well illustrated for which it gives

a brief highlight about the operational model of the industry. It also enlists the

primary drivers and challenges for the overall insurance industry. "Primary reasons

to propel the market forward are comprised of young consumer segment, wide

range of products, technological advancement and growing middle class, whereas

the basic challenges faced by the sector are the tight premium rates and

dependence on overseas re-insurers," says Kalyan. Moving along, the report

features a section on the ICT in Insurance wherein the growth rate and spending on

ICT is enlisted in great details. "IT spending basically comprises the costs

associated with hardware, software and services while the telecom services mainly

include support and services," added Kalyan. The report covers an explicit break

up of IT expenses of insurers in terms of hardware, software and services.

31

CHAPTER-3

RESEARCH DESIGN

RESEARCH DESIGN

(3.1) Introduction:

RESEARCH: Research in common parlance refers to a search for knowledge. One

can define Research as a scientific and systematic search for pertinent information

32

on a specific topic. In fact, research is an art of scientific investigation. Research is

an academic activity and as such the term should be used in a technical sense.

According to Clifford woody research comprises defining and redefine and

problems, formulating hypothesis or suggested solutions; collecting and organizing

and evaluating data; making deductions reaching conclusions; and at last carefully

testing the conclusions to determine whether they fit the formulating hypothesis. In

short, the search for knowledge injective and systematic method of finding solution

to a problem is research. The systematic approach concerning and the formulation

of a theory is also research. As term research refers to the systematic method.

3.2 Research Methodology:

Research methodology refers to the analysis of principles of methods, rules and

techniques. It involves the systematic study of methods which are applied to

analyze a specific project or study. In order to make the research organized and to

increase its reliability different methodologies are adopted. Research methodology

involves the collection of theories, concepts or ideas, comparative studies to

different approaches and individual methods which are conduced when a research

work is performed.

There are two main types of Research Methodology,

1- Quantitative methodology

2- Qualitative methodology

1- Quantitative methodology-

33

It is the type by which you test the significance of your hypothesis, in other

words you answer the words: How much Is there a relationship Quantitative

methods tend to be systematic and use numbers... Actually it is a deep sea.

2- Qualitative methodology

It is the type by which you are depending on your observations and descriptions. It

is subjectively and descriptive, no facts.... This kind of method is used to assess

knowledge, attitudes, behaviours, and opinions of people depending on the topic of

your research. Researcher, in this type of method uses his opinion and experience

which are not allowed to be used in quantitative method at all. About the types of

sample and sample size, I think they are apart of research design not apart of the

methodology.

METHOD OF DATA COLLECTION

Data to be collected

Data includes facts and figures, which are required to be collected to achiever the

objectives of the project.

3.2.1 Primary Data

The data that is being collected for the first time or to particularly fulfill the

objectives of the project is known as primary data.

The above primary data were collected through responses of consumer was

conducted through questionnaires prepared for them.

3.2.1 Secondary Data

34

Secondary data are that type of data, which are already assembled and need not to

collected from outside. These types of data were

i) Company Profile

ii) Product Profile

iii) Competitors Profile

35

CHAPTER -4 ANALYSIS OF DATA

36

4.1COMPARATIVE ANALYSIS OF ULIPS

This chapter covers the comparison of ULIPs of 2 Insurance companies, how much

growth the fund has showed since its Inception, returns for a period of one month

compared with the market and tracking of the NAVs for a period of one month.

Every Insurance company has got ULIPS suiting the varied requirements of the

customers. If one has to choose among the ULIP schemes provided by the

insurance, it is necessary to do a through comparison to choose the right one for

you.

ULIPs of 2 insurance companies are taken for comparison.

1)KOTAK MAHINDRA LIFE INSURANCE---------Advantage multiplier

2) TATA-AIG--------------------- Invest Assure II

37

4.2 ANALYSIS OF PRIMARY DATA

COMPANY

NAME

KOTAK MAHINDRA OLD

MUTUAL LIFE INSURANCE

(INVEST MAXIMA)

TATA AIG LIFE INSURANCE

(INVEST ASSURE )

1)POLICY

OBJECTIVE

A regular unit linked insurance

policy that offers flexible

investment options along with the

benefit of life insurance cover,

and an opportunity to earn

potentially higher returns on your

investment without sacrificing the

protection of your family

It is a unique, flexible insurance

plan which combines security of

life with the opportunity to

exploit the upside of the market

returns by investing in different

kinds of securities through

multiple fund options.

2)Eligilibility

Criteria

(Minimum,

Maximum age at

entry):-

Min: 0 years , Max : 65 years Min age= 30 days

Max age= 45,55,65 years

3) Policy term Regular Premium: 10, 15, 20, 25

& 30 yrs

Limited Premium: 10, 15, 20, 25

& 30 yrs

Single Premium: 10 yrs

15, 20, 30 years

38

4) Premium

(Minimum):-

Regular - `50,000 - `1,00,000

Limited – `75,000 - `1,00,000

Single – `1,00,000 - `2,50,000

20,000 p.a.

5) Mode of

Premium

Payment:-

Annually, single Annually, half yearly, quarterly,

monthly

6) Sum Assured

(Minimum,

Maximum):-

Single Premium:

Option I : 5 times SP

Option II : 1.25 times SP

AP: Annualised Premium

SP: Single Premium

For Insured's Age < 45 years:

Higher of (10*Annualised

Premium or 0.5*Policy

Term*Annualised Premium)

For Insured Age>= 45 years:

Higher of ( 7* Annualised

Premium or 0.25*Policy

Term*Annualised Premium)

7)Surrender

option/ partial

withdrawal

option

Partial Withdrawals will be

allowed after completion of five

policy years and provided five full

years premiums are paid.

Minimum amount for partial

withdrawal is `10,000. Minimum

Allowed only after 3 years form

the date of issuance of the

policy.Surrender charges are a

percentage of regular premiums

—Fund value. Charge Applicable

for 6 yrs---20 or

39

balance of one premium for

Regular & Limited Premium

payment option and `10,000 for

Single Premium Payment option

should be maintained in the Main

Account after Partial Withdrawals.

30 yr policy

Charge Applicable for 5 yrs----15

yr policy Surrender & partial

withdrawal Available Min of up

to 4 partial withdrawals

8)Reinstatement/

Revival

Applicable only for Regular and

Limited premium payment option.

A policy can be revived with or

without riders until the expiry of

the Notice Period. The

policyholder shall also have

the right to revive a discontinued

policy within two years from the

date of discontinuance and not

later than the expiry of lock in

period, in which case the

discontinuance charge will be

reversed.

If the premium remains unpaid at

the end of the Grace period and

the Policy has not been

completely withdrawn for its

Total Fund Value it can be

revived, within stipulated time

period subject to: (i)

Policyholder's written application

for revival; (ii) production of

Insured's current health certificate

and/or other evidence of

insurability satisfactory to us, if

required (iii) payment of all

overdue Regular Premiums.

9)Premium

Holiday

The policy brochure has no

mention of premium holiday

After completion of 3 years of the

policy, Premium Holiday facility

is given with a charge of 3% of

40

the regular premium.

10) Free look

Period

The policyholder is offered 15

days free look period, from the

date of receipt of the policy

wherein the Policyholder may

choose to return the policy within

15 days of receipt if he is not

agreeable with any of the terms

and conditions of the plan. Should

he choose to return the policy,

he/she shall be entitled to refund

of the premium paid after

adjustment for stamp duty,

administration expenses and

proportionate risk premium.

You have the right to cancel the

Policy by giving written notice to

the Company and receive the

premiums invested into the funds

at Unit Price as at the date of

cancellation along with the

charges paid after deducting a)

for proportionate Risk and Rider

Premium (if any) for the period

on cover b) Stamp duty and

medical examination costs which

have been incurred for issuing the

Policy. Such notice must be

signed by the Policyholder and

received directly by the Company

within 15 days after you receive

the Policy Document..

11)Grace Period: There is a Grace Period of 30 days

for the annual mode from the due

date for payment of premium. If

the premium is not paid until the

end of the Grace Period, within the

next 15 days Kotak Life Insurance

will send a notice to the

policyholder to either revive the

policy or terminate the policy

If you are unable to pay your

Regular Premium on time,

starting from the regular premium

paid to date, a grace period of 30

days will be offered for policies

on Annual, Semi- Annual or

Quarterly Modes. For Policies on

monthly mode the grace period

would be 15 days. During this

41

without any risk cover. The Notice

Period ends 30 days after receipt

of the notice by the policyholder.

In case of death during the Grace

Period and Notice Period, unpaid

premium shall be deducted from

the Basic Sum Assured.

period your policy is considered

to be in force with the risk cover

as per the terms & conditions of

the policy.

12)Settlement

Benefits

Entire maturity proceeds as an

immediate payout in one go OR

Part of the maturity proceeds as a

lump sum and part as

installments.OR

Whole amount as installments.

The installments can be taken over

a maximum period of 5 years.

You have the option to receive

your maturity benefit either in

lumpsum or in the from of

periodicalpayments over period

of time. This period will not

exceed 5 years from the maturity

date.

13)Premium

Redirection

Switch between fund options or

change your future premium

allocation as per your needs and to

maximize your returns.

Re direction of all the future

premiums under a policy, in an

alternative proportion to the

various Fund units is available.

14) Top Up

premium:-

Min: `20,000

Max: For Regular & Limited

Premium: 10 x AP

Minimum top up amount is Rs

5,000

42

15)Tax Benefits:- You can avail of tax benefits under

Section 80C and Section 10 (10D)

of Income Tax Act,

1961. Tax benefits are subject to

change in the tax laws. You are

advised to consult your Tax

Advisor for details.

Premiums paid under this plan

are eligible for tax benefits under

section 80C of the Income Tax

Act, 1961 and are subject to

modifications made thereto from

time to time. Moreover, life

insurance proceeds enjoy tax

benefits as per section 10(10D) of

the said Act.

16)CHARGES

Most of the life insurance companies incur certain charges which are as

follows:

a) MORTALITY CHARGES

b) FUND MANAGEMENT CHARGES

c) SWITCH OVER CHARGES

d) POLICY ADMINISTRATION CHARGES

A)MORTALITY CHARGES

AGE Kotak Mahindra life

insurance

Tata aig life insurance

43

20yrs 1.199 1.14

30yrs 1.404 1.435

40yrs 4.264 2.274

50yrs 6.293 9.022

20yrs 30yrs 40yrs 50yrs0

1

2

3

4

5

6

7

8

9

10

b) FUND MANAGEMENT CHARGES

44

(Only for Equity Fund)

53%47%

KOTAK MAHINDRA LIFE INSURANCE TATA AIG LIFE INSURANCE

C) SWITCH OVER CHARGES

45

KOTAK MAHINDRA LIFE

INSURANCE

1.35%

TATA AIG LIFE

INSURANCE

1.20%

Company Charges

KOTAK MAHINDRA

LIFE INSURANCE

500

TATA AIG LIFE

INSURANCE

100

KOTAK MAHINDRA LIFE INSURANCE TATA AIG LIFE INSURANCE0

100

200

300

400

500

600

d) POLICY ADMINISTRATION CHARGES

46

COMPANY CHARGES

KOTAK MAHINDRA LIFE

INSURANCE

500

TATA AIG LIFE

INSURANCE

150

KOTAK MAHINDRA TATA AIG0

100

200

300

400

500

600

47

GROWTH & RETURNS

THE GROWTH RATE OF ULIPS

THE NAVs taken over here only belong to The Equity Fund of the

Policies. (No other fund taken into consideration)

Growth rate of ULIPs

COMPANY Date of

Inception

NAV as

on

inception

Rs

NAV as on

29/2/2012

increase Growth%

KOTAK

MAHINDRA

10/8/2009 10 15.4573 5.4573 84.355 %

TATA AIG

LIFE

INSURANCE

15/01/2008 9.999 11.8904

1.8914 15.906%

In case of KOTAK MAHINDRA LIFE INSURANCE--------the Equity Fund has

grown up to 84.355% in 3 years from the date of inception.

In case of TATA AIG LIFE INSURANCE--------the Equity Fund has grown up

to 15.906% in 4years from the date of inception.

48

CONCLUSION- KOTAK MAHINDRA OLD MUTUAL LIFE INSURANCE

company’s ulip invest maxima has a great performance as compared to TATA

AIG’S invest assure.From invest maxima’s inception date it has shown 84%

increase within 3 years than of invest assure ‘s which has increased only by 15%

from its inception date. In next chapter we will study about overall findings and

recommendations.

49

CHAPTER -5 FINDINGS AND

RECOMMENDATIONS

50

MARKET SURVEY

A questionnaire was prepared, wherein 20 ulip insurers of different insurance

companies were asked to fill it. The reason for carrying out a market survey was to

1.Find strength and weakness of ULIP plan,2. Study of the consumer perception

towards ULIP. 3.To know other important aspects affecting the interest of the

policy holders.

1.Do you think privatization of insurance companies has increased insurance awareness & competition in general?

Feedback No.of Respondents

Percentage

Yes 15 75%

No 05 25%

51

75%

25%

YesNo

2.Do you think ULIP as investment is good as compared to:

Feedback No.of respondents

Percentage

Yes no Yes No Direct stock market investment

15 05 75% 25%

Mutual fund investment

12 08 60% 40%

Bank deposit 18 02 90% 10%

Postal investment-nsc

14 0 30% 70%

52

Direct

stock

market

investm

ent

Mutual fund in

vestm

ent

Bank d

eposit

Postal in

vestm

ent-n

sc0

4

8

12

16

20

No.of respondents Yes No.of respondents no

3.Do you know insurance is a risk protection +investment?

Feedback No.of Respondents

Percentage

Yes 18 90%

No 02 10%

53

90%

10%

YesNo

4.DO YOU KNOW FOLOWING ABOUT ULIP-

4.1 There is a wide range of variety of products in ULIP available

Feedback No.of Respondent

Percentage

54

sYes 16 80%

No 04 20%

Yes No

0

2

4

6

8

10

12

14

16

18

.

4.2 There is transparency in ULIP

Feedback No.of Percentage

55

Respondents

Yes 12 60%

No 08 40%

12

8

YesNo

4.3 Stock market risk is borne by the policy holder.

56

Feedback No.of Respondents

Percentage

Yes 17 85%

No 03 15%

85%

15%

Yes No

4.4 In case of death claim fund value or sum assured, whichever is higher is paid to nominee.

Feedback No. of Respondents

Percentage

57

Yes 19 95%

No 01 05%

95%

5%

Yes No

4.5 If you pay premium for 3/5 years and then discontinue,the life insurer can foreclose your policy

Feedback No.of Percentage

58

Respondents

Yes 08 40%

No 12 60%

8; 40%12;

60%

YesNo

5.Do you know the benefits of ULIP depends on the performance of stock/money market and benefits of traditional policies on the performance of life insurance.

59

Feedback No.of Respondents

Percentage

Yes 15 75%

No 05 25%

75%

25%Yes No

6.Reasons for surrender of ULIPS-

1.Fluctuations instock market

60

2.unexpected returns3.investment for short term4.unaffordable amount of premium

Feedback No.of respondents

Percentage

Yes no Yes No Fluctuations in stock market

11 09 55% 45%

Unexpected returns

05 15 25% 75%

Investment for short term

02 18 10% 90%

Unfordable amount of premium

03 17 15% 85%

Fluctu

ations in

stock

market

Unexpect

ed re

turns

Investm

ent fo

r short

term

Unfordab

le am

ount of p

remium

02468

101214161820

No.of respondents YesNo.of respondents no

7.Codes of professional ethics are not implemented by the intermediaries in marketing of ULIP.

61

strongly Agree Agree to some extent

Neither0

2

4

6

8

10

12

14

16

No of respondents

No of respondents

8.What is te impact of life insurance advertisements in your mind.

62

Feedback No of respondents

percentage

stongly Agree

15 75%

Agree to some extent

02 10%

Neither 03 15%

85%

5% 10%

No of respondentsPositive Increase curiosity No impact

9.which media is attractive for te life insurance advertisement?

63

Feedback No of respondents

Percentage

Positive 17 85%

Increase curiosity

01 5%

No impact 02 10%

. 1 2 3 4

0

2

4

6

8

10

12

14

Feedback No of respondents

10.From whom you would like to buy the insurance policy?

Individual agents

64

Feedback No of respondents

Percentage

Newspaper and magazine

02 10%

Television 06 30%

Radio 02 10%

Any other-agents

12 50%

Corporate agentsBanks(bankassurance)Through internetDirectly from insurance co.

feedback No of respondents Percentage Individual agents 10 50%Corporate agents 0 0%Banks 04 20%Internet 04 20%Direct from company 02 10%

50%

20%

20%

10%

Individual agents Corporate agents Banks Internet Direct from company

FINDINGS

For the changes in ULIPs:

65

1. The amount of premium should be reduced in order to cater to the lower income

groups.

2. On maturity, the policy holder should receive the Fund value or the Sum

Assured whichever is higher, (as in the case of death benefit.)

3. Reduction in the charges.

4. Commission structure to be revised

5. Give a Pure traditional plan along with the ULIPs.

6. Remove the charges on surrender or partial withdrawal.

7. Increase the number of Switch options. as four is not enough.

8. Design ULIPs for meeting short term investment goals.

9. The investment style should be more aggressive

In case of KOTAK MAHINDRA LIFE INSURANCE--------the Equity Fund has

grown up to 84.355% in 3 years from the date of inception.

In case of TATA AIG LIFE INSURANCE--------the Equity Fund has grown up

to 15.906% in 4years from the date of inception.

KOTAK MAHINDRA OLD MUTUAL LIFE INSURANCE company’s ulip

invest maxima has a great performance as compared to TATA AIG’S invest

assure.From invest maxima’s inception date it has shown 84% increase within 3

years than of invest assure ‘s which has increased only by 15% from its inception

date. In next chapter we will study about overall findings and recommendations.

MY LEARNING FROM PROJECT

I have learnt many things which I might not be able to learn under

66

class room training like looking at the stock market terminal and

analyzing the stocks performance and thus designing the portfolio on the basis of

their performances.

First and the most important I learnt about ULIP Industry. Before this project I

dint have much knowledge about ULIP funds. But now I have good knowledge

about ULIP and INSURANCE INDUSTRY.

·

ANNEXURE

1.Do you think privatization of insurance companies has increased insurance awareness & competition in general?

1.yes2.no

2.Do you think ULIP as investment is good as compared to:

1. Direct stock market investment 2. Mutual fund investment3. Bank deposit4. Postal investment-nsc

3.Do you know insurance is a risk protection +investment?

1.yes

2.no

4.DO YOU KNOW FOLOWING ABOUT ULIP-

4.1 There is a wide range of variety of products in ULIP available

1.yes2.no

67

4.2 There is transparency in ULIP

1.yes2.no

4.3 Stock market risk is borne by the policy holder.

1.yes2.no

4.4 In case of death claim fund value or sum assured,whichever is higher is paid to nominee.

1.yes2.no

4.5 If you pay premium for 3/5 years and then discontinue,the life insurer can foreclose your policy

1.yes2.no

5.Do you know the benefits of ULIP depends on the performance of stock/money market and benefits of traditional policies on the performance of life insurance.

1.yes2.no

6.Reasons for surrender of ULIPS-

1.Fluctuations instock market 2.unexpected returns3.investment for short term4.unaffordable amount of premium

7.Codes of professional ethics are not implemented by the intermediaries in marketing of ULIP.

68

1.stongly Agree

2.Agree to some extent

3.Neither

8.What is te impact of life insurance advertisements in your mind.

1.Positive

2.Increase curiosity

3.No impact

9.which media is attractive for te life insurance advertisement?

1.Newspaper and magazine

2.Television

3.Radio

4.Any other-agents

10.From whom you would like to buy the insurance policy?

1.Individual agents2.Corporate agents3.Banks(bankassurance)4.Through internet5.Directly from insurance co.

69

BIBLIOGRAPHY

1. Money Outlook, 2011 edition

2. IRDA Annual Report

Websites:-

1. www.irdaindia.org

2. www.insuranceworld.com

3. www.findarticles.com

4. www.kotaklife.com

5.www.bimabazar.com

6.www.tataaiginsurance.com

70

Special Thanks to:-

Wikipedia, the free encyclopedia.htm

http://www.google.com

http://www.economywatch.com/business-and-financial/IPO-industry

71