2_invbotdl_adani group presentation may 14

DESCRIPTION

SHARETRANSCRIPT

Thinking big Doing better

Resources Logistics Energy

Adani Group – Vision, Values and Commitment

2

To be globally admired leader in integrated infrastructure businesses with a deepcommitment to nation building. We shall be known for the scale of our ambition, speed ofexecution and quality of operation.

India:Generation:

9240 MW thermal capacity by 2014.

40 MW Solar Power Plant operational

Transmission:

2923km of transmission network.

CGD:

Operate in 3 cities in India.

India: No. 1 Port of India

(cargo handled)

Biggest Private Port Developer & Operator

4 Operating Ports

Developing 4 other terminals# pan India

Largest Private Rail.

Shipping:

• Own & operate 4 capesize vessels

India Largest trader of

Coal.

Mine developer and operator with 97 mtpa order book

Indonesia: Resource 269 mn tn

Mine life: 15 yrs

11 mtpa (peak)

Australia JORC Resource: 11

bn ton

Mine life:100 yrs

100 mtpa (peak)

Building an energy sufficient INDIA

with world class

Infrastructure and integrated value

chain

•Coal Trading•Coal Mining•Agro

Resources

• Sea Ports• Railways• Shipping

Logistics• Power

• Generation• Transmission• Trading

• CGDEnergy

#: Construction completed at coal terminal at Goa and Vizag

200 384

1,000 1,084 1,271

1,700

-

500

1,000

1,500

2,000

FY09 FY10 FY11 FY12 FY13 FY14

3,077 5,654

12,822

15,762 17,273

16,738

-

5,000

10,000

15,000

20,000

FY09 FY10 FY11 FY12 FY13 FY14

Adani Group – Thinking Big, Doing Better

3

Net Asset (USD mn)

EBIDTA (USD mn)

• Commercial Port in India

• Coal Import Terminal at Mundra

• Private Power Producer in India

• Mine Developer and Operator in India

• Trader of coal in India with consistent share of

about 50%

• Edible Oil Company in India in terms of market share

No.1 :-

Resources Logistics Energy

•Coal Trading

•Coal Mining

•Sea Ports

•Railways

•Power

• Generation• Transmission

Coal: Indigenous Supply Deficit to Continue

5

2012 2017 2020

602 84190036

70100

2

70

200

25%

640

981

1200

Units in MMTPA

Mining (AEL) Imports (AEL)

CIL & Other Imports AEL Market Share

Source: Ministry of Coal/XIIth FYP & Plan Working Group.

14%6%

Adani : Key Supplier to growing coal Demand

in India

• Coal demand driven predominantly by

Indian Power Sector – estimated to reach

~288 GW by 2017 from 245 GW as on 30th

Apr 14.

640*981* 1200*

Indigenous Supply Deficit in India

Growing Demand Increasing Demand-Supply Gap

100

185234

• Coal imports to cater the deficit arising from

the demand-supply gap.

• Indigenous supply to grow at slow pace of

7.5% against demand growth of 8.2%,

increasing the deficit from 15.6% in FY12 to

19.5% in FY20

• Coal imports to grow at 11.2% p.a. over 2012-2020

* Annual Demand

Coal Trading : Largest Integrated Coal Management

6

Multi-CountryProcurement

Multi modal Logistics

Customer Account Management

Financing

Consistent market share of

~50%

Map not to scale

South Africa

Richard Bay

Ports

Locations served

Indonesia

Indonesia

TarakanTanjung Bara

BontangSamarinda

Muara Satui TanjungPemancingan

Australia

Queensland

1019

29 33 3646

70

100

-

20

40

60

80

100

120

Mundra

GangavaramKakinada

Vishakhaptnam

Tuticorin

Haldia

Suratgarh

Tanda

Unchahar

SipatKorba

Koradi

Parli

Chanderpur

Simhadri

Kota

Chhabra

GandhinagarWanabori

Dadri

Panipat

Yamunagar

Hissar

Panki

Parichha

Harduaganj

Kahalgaon

Ramagundam

Kondapalli

North ChennaiMettur Tuticorin

Rihand

Vindyachal

Paradip

[Talcher]

Mejia

Badarpur

Ennore

Dahej

Bedi Navlakhi

Kandla

Kolaghat

BakreshwarBandel

Sagardighi

Durgapur

Hazira

Goa

Tiroda

Mining LocationsPorts

Mundra

Machhakata

Dahej PortHazira Port

Parsa

Chhendipada

Parsa – KenteMormugao Port

Vizag

Kandla

7

Land Acquisition

Develop, Plan, Operate & Manage Mining

Operations

Establishment of Washery & Rejects based Power Plants

Logistic Solutions

State Chhattisgarh Orrisa

Mine Parsa -Kente

(RRUVNL)

Parsa (CSPGCL)

KenteExtension (RRUVNL)

Machhakata(MGCL)

Chendipada (UCMCCL)

Block Area (Sq Km) 27.67 12.52 17.00 20.43 21.91

Mineable Reserve (Mn MT)

452 150 200 1244 1589

Capacity at peak level (MMTPA)

15 5 7 30 40

Overall Stripping Ratio 5.16 5.46 5.10 2.44 2.75

Commencement of Production

Started Jan 13 2016 2017 2015 2016

Notes:1. RRVUNL – Rajasthan Rajya Vidyut Utpadan Nigam Limited ; 2. MGCL – Mahaguj Collieries Ltd. ; 3. CSPGCL – Chhattisgarh State Power Generation Company

Limited 4. UCMCCL - UCM Coal Company Limited

Coal Mining: Largest Mine Developer & Operator

8

Coal Mining: Indonesia

Indonesia

Bunyu Island

Coal Crushing

Coal Loading

Particulars Capacity

Location Bunyu Island, Indonesia

Resource 269 MMT (JORC)

Peak Capacity 11 MMTPA

Current Capacity 7 MMPTA

Coal Mining

9

Coal Mining: Carmichael Coal Mine

Acquisition• Adani Mining Pty Ltd, entered into Asset

sales agreement with LINC Energy inAugust, 2010 for ownership of EPC 1690

Location • Galilee Basin - Queensland, Australia

Resource Base • Thermal Coal – 11.04 Bn Tonnes (JORC)

ProductionTarget

• Phase I : 40 MTPA

Status• EIS approved for Carmichael Mine & Rail

project• EIS filed for NGBR Project

EIS – Environment Impact StatementNGBR – North Galilee Basin Rail

Proposed Rail Connectivity

Agro

10

• Capacity of 21000 MT of storage of Apple• State of Art Control Atmosphere Storage facility at 3 locations in Himachal

Pradesh• Distribution set up across India under brand “Farm-Pik”• One of largest importer of fruits into India

Agri Infrastructure: Fruits

• Operates storage capacities of 6,00,000 MT across 7 locations across India• Another 3,50,000 MT in development across 7 locations in Madhya Pradesh• State of Art mechanized storage facilities with private railway siding• Operates storages facilities under Build Own Operate model for FCI for 20 years

Agri Infrastructure: Food Grains

• Joint venture with Wilmar , Singapore• “FORTUNE” - India’s number 1 edible oil brand with more than 20% market share

(AC Nielson) • Revenues in excess of $ 2.5 Bn• Volumes more than 3.5 MMTPA• Major Exporter of Castor Oil/derivatives and Soya De-oiled cake• Manufacturing facilities spread across 18 locations pan India with 10k refining

& 7k crushing capacity

Edible Oil

Agri Infrastructure: Fruits

Agri Infrastructure: Food Grains

Resources Logistics Energy

•Coal Trading

•Coal Mining

•Sea Ports

•Railways

•Power

• Generation• Transmission

Ports & Logistics: Unique Asset Profile

India’s Gateway for International Trade

4 Ports having 14 terminals with 33 berths *(Mundra, Dahej, Hazira & Dhamra)

2 inland container depots at Patli (Punjab) and Kishangharh (Rajasthan) in the north of India

Terminals : Operational

Trial Runs at: 1 Coal terminal each at Vizag port and Mormugao Port

1 bulk terminal with total 4 berths at the Kandla 1 container terminal with 1 berth at the Ennore

Terminals: Being Developed

Energy Gateway

Crude – Crude Products Imports

2 operational SPM. Potential to develop 2 more SPM at Mundra Port

LNG Terminal being developed

Coal: Feeding Power Projects Across India

PAN India network of ports and terminals to handle coal cargo

Availability of Adequate Draft: Only “Deep Draft” Ports and Terminals of West India

• Deep water drafts: 17.5 – 20 Mtrs at Berth & 32 Mtrs at SPM at Mundra• Accommodates cape size bulk vessels & container cargo vessels of >14,000 TEUs, and • Very large crude carriers (“VLCCs”) of up to 360,000 DWTs

Supporting Facilities

• Mobile harbor cranes, conveyors, port crafts and other equipment and back-up and storage areas• Two ICDs at Patli and Kishanghar, to provide an outreach to land locked northern India• 6,641 hectares SEZ- Opportunity to expand storage and back up area

• Fleet of 13 dredgers capable of doing capital dredging across various marine conditions• 22 tug boats which are used to maneuver vessels inside out the port terminals

Port Craft and Mechanization

12

Ports & Logistics: Integrated Service Provider with a strategic location

13

Anchorage Pilotage Tug Pulling Berthing HandlingInternal

TransportStorage & Value Add

Evacuation(Rail-Road)

Natural Advantages at Adani PortsServicing Northern Western & Central Hinterlands

Location Advantages:• Close to one of the major global maritime trade routes• Bridging the resource rich Middle East, Africa and Australia, and regions

with high resource demand and consumer exports in East and North Asia and Europe

• Assets positioned on western and eastern coast of India to strategically service the land locked hinterland.

• Ample land available for development of incremental storage and evacuation infrastructure

Marine Advantages:• Ability to berth larger vessels, deeper natural drafts with lesser

maintenance dredging requirements Connectivity Advantages:• Low transit time to reach northern, western & central hinterland

– Rail routes traverse through the sparsely populated desert regions of Kutch and Rajasthan

– Well connected rail and road infrastructure to Mumbai & Delhi, key industrial hubs of India.

Ports & Logistics: Only PAN India Port Company

14

Particulars Mundra Dahej Hazira Dhamra Goa Vizag Kandla EnnoreCapacity (mmt)

Bulk 100 20 15 24 10 6 - -

Crude 50 - - - - - - -

Container (mn TEUs) 4 - 1.5 - - - - -

Operational 210 20 35 24 10 6 - -

LNG 5 - - - - - - -

Bulk 40 - 6 - - 20Containers (mn TEUs) - 1.4

Being Developed 45 - 6 - - 20 18

Total Capacity 255 20 35 30 10 6 20 18

Status Operational Trial Runs FY 16 FY 17

Expansion √ √ √ √ X X X √Berth Length-mtr 6384 566 1,580 800 300 310 1200 780

Mechanisation √ √ √ √ √ √ √ √

Connectivity

Road √ √ √ √ √ √ √ √

Rail √ √ √ √ √ √ √ √

Pipeline √ X X X X X X X

Air √ X X X X X X X

Revenue Share NIL NIL 3% > 10yrs 5% 20% 40% 25% 37%

Tariff Fixation Commercially Negotiated Regulated

Only indigenous PAN India Port Company…

A network of Multi Purpose Terminals, Coal Handling facilities and Container Terminals

across India

A network of Multi Purpose Terminals, Coal Handling facilities and Container Terminals

across India

Mundra

Hazira

Mormugao Vizag

Kishanghar

Patli

Ennore

Dahej

Kandla

Dhamra

Ports & Logistics: Key Milestones

15

2011• Terminal at Dahej becomes

operational • 20 million MT capacity now• 60 million MT of handling

capacity-commissions the world’s largest coal import terminal at Mundra

2009• Automobile handling

terminal commences operations

2010• Hazira: Sub - Concession

signed

2013• Mundra port

becomes 2nd largest in India

• Hazira became operational

2012• Doubling of the rail connectivity

between Mundra and Adipurcompleted

• Operations Commenced:• Container terminal - III

• Name changed to Adani Ports and Special Economic Zone Limited

2001• Commences

commercial operations

• Sets up first commercial terminal

2003• First container

terminal, MundraInternational Container Terminal commences operations

2002• 4 million MMT of cargo-Mundra

becomes largest private port in India

• Agreements signed with IOC and HMEL for setting up SPM and crude oil handling at Mundra

2005• First non-captive Single

point mooring facility in India at Mundra Port

• A double-stack container train began operations

2007• Initial public offering of shares

oversubscribed 117 times• Operations Commenced:

• Multi Purpose Terminal II• Container terminalII

• Dahej: Sub-Concession Signed

2014• Mundra handles 101 mtpa of

cargo• Only port in India to handle

such large volumes• CT III assets operations by

AICTPL – 50-50 JV APSEZL-MSC

• Terminals at Mormugao and Vizag complete constructions

• APSEZL signs definite agreement to acquire DPCL –marks its foot steps on eastern coast of India

Ports & Logistics: The Differentiating Factors

16

2 1 1

7

1 2

12

2.01

6 6

3

Dry Liquid Containers

Turn Around Time (in days)

Mundra

Kandla

Mumbai

JNPT

0%

20%

40%

60%

80%

100%

Dry Liquid Containers

Berth Occupancy

Mundra

Kandla

Mumbai

JNPT

8294 58

65

0

50

100

150

200

Mundra Kandla Mumbai JNPT

Capacity & Cargo Handled (million MT)

Liquid

Container

Dry

CargoHandled

• Mundra Port provides the best vessel turn around time in the region ensuring advantage to customers

• Capacity utilization at competing ports is very high leading to congestion in operations

• Capacity expansion at competing ports is bound to take time and will be capital intensive

• Investments at our Ports have been done to ensure readily available capacity to handle additional cargo without any congestion

2

Ports & Logistics: Cargo Diversity Key Feature

17

3C: Coal, Container & Crude Traffic to Drive Volume in India

912

318 233 188 131 16221 2,019

0

1,000

2,000

3,000

FY12 Coal Containers Crude Iron Ore Fertilizers Others FY17

Cargo Handled in MMT)

696

981

559

795

0

300

600

900

1,200

FY12 FY17E

Coal: Critical for India’s Energy RequirementsMMT

Indigenous SupplyTotal Demand Refining Capacity

Crude Requirement

184

358

190

364

0

150

300

450

FY12 FY25E

Increasing crude importsMMT

Increasing Containerization

12

31

0

5

10

15

20

25

30

35

FY12 FY17E

Container traffic

No. 1 port to

service coal

requirements of

India

Services ~20% of

Indian coal

imports

No.1 port in India

No. 2 port to

handle

containers in

India;

Equipped to

handle up to 14K

TEUs vessels

2 operational

offshore single

point mooring

facilities

Long Term

Contracts with

IOCL, HPCL,

HMEL

TEUs

APSEZL’s Capability APSEZL’s Capability APSEZL’s Capability

Sources: Ministry of Shipping (GoI), Ministry of Road Transport and Highways (GoI), Indian Ports Association

Ports & Logistics: Growth Strategies

18

Become Gateway for Energy Resource Imports to India

Focus on Increasing Margins from OurOperational Facilities

Facilities in operation are positioned in West and South Gujarat to service northwest, west and central India

Developing terminals at the Mormugao Port and the Vizag Port to expand presence to southwest and southeast India

Growing presence on East coast with Vizag terminal

Growth on East coast through organic and inorganic means

Mundra already the enegry gate way fro India.

Focusing on coal and crude oil cargo services and providing connectivity to power plants and petroleum refineries

All adani ports equipped to handle coal cargo

For crude oil cargo, two operational single point mooring facilities and have the potential to develop two additional single point mooring facilities at the Mundra Port

Potential to develop an LNG Terminal

Establish Pan-India PresencePursue Benefits of Both Long-term and Short-term Arrangements with Customers To enhance existing long term as well as short term

customer relationships for steady mix of contracted and spot cargo

Try to convert short and medium term arrangements into long term arrangements

Plan to continue to increase the amount of cargo pursuant to these arrangements by increasing our capacity and continuing to refine our operating procedures

Offer Customers Multi-cargo Ports and Related Infrastructure

Positioned growth plans to accommodate the diversity of throughput by developing multi-cargo ports and infrastructure to cater to the diverse cargo needs ofthe customers

1

2

5

3

4 Focusing on revenue maximization and cost

optimization

Focus on providing various value add services at the port to enhance the revenue horizon above marine, handling, storage and evacuation incomes.

Implementing globally benchmarked operational practices for reduction in operating costs

Use of information technology and mechanization at port facilities to reduce turnaround times, pilferage and wastage and resulting into minimal human intervention.

APSEZL

Resources Logistics Energy

•Coal Trading

•Coal Mining

•Sea Ports

•Railways

•Power

• Generation• Transmission

Power: Sectorial Demand continue to rise…

20

Average Deficit in the Last Decade:Peak deficit: 12%; Energy deficit: 9%

India – Installed Capacity: 245 GW*

Installed Capacity in India - Category

Source: 11th & 12th FYP, Ministry of Power, CEA* As on 30th Apr 2014

Units in GW

2012 2017 2020

132 204

240 39

50 57

5

10 19

25

25 32

Thermal Hydro Nuclear Renewables

200

288347

Peak & Energy Deficit : Year-wise

Hydro40 GW

Other32 GW

Nuclear5 GW

Thermal168 GW13361

6460 5741

2942 2384884

0

2000

4000

6000

8000

10000

12000

14000

16000

USA Russia UK China Brazil India

Lowest per capita electricity consumption

12% 12%14%

17%

12% 13% 13%11% 9%

5% 5%7% 8% 9% 10% 11% 10% 9% 8% 9%

4% 4%

Peak Deficit Energy Deficit

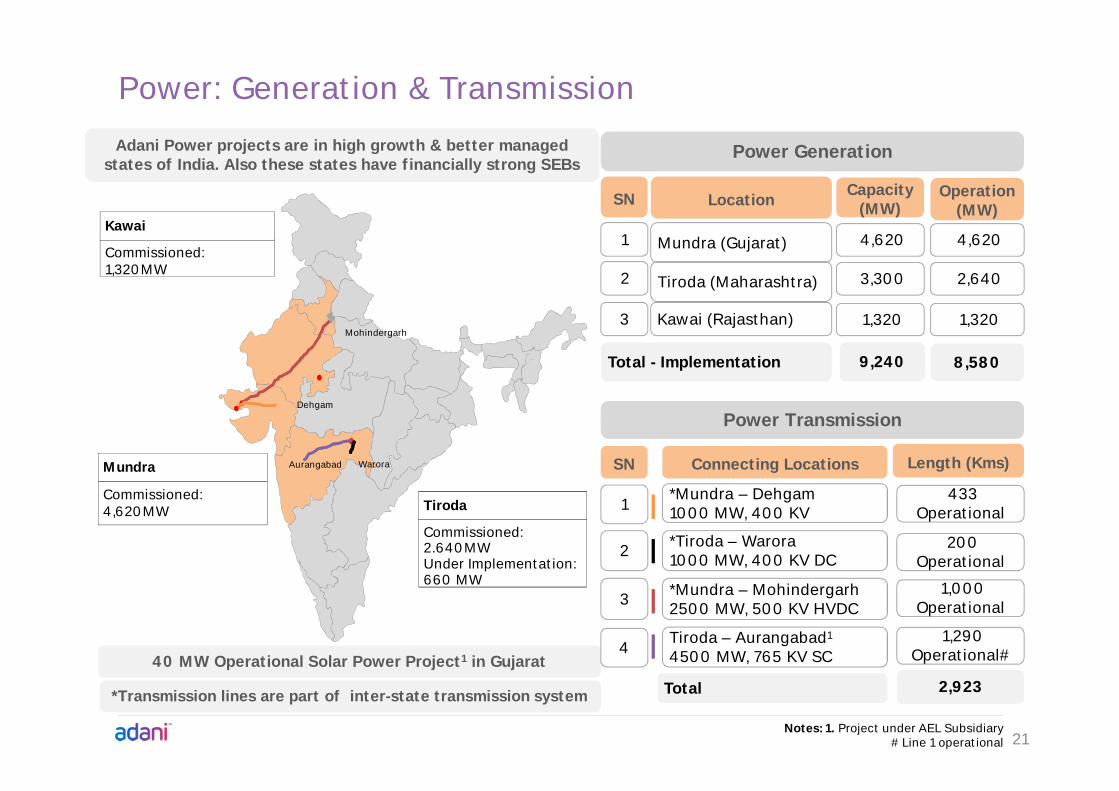

Power: Generation & Transmission

21Notes: 1. Project under AEL Subsidiary

# Line 1 operational

Commissioned: 2.640MW Under Implementation:660 MW

Commissioned: 1,320MW

Kawai

Commissioned: 4,620MW

Mundra

Tiroda

Dehgam

Mohindergarh

Aurangabad Warora

Adani Power projects are in high growth & better managed states of India. Also these states have financially strong SEBs

40 MW Operational Solar Power Project1 in Gujarat

SN LocationCapacity

(MW)

1 Mundra (Gujarat) 4,620

2 Tiroda (Maharashtra) 3,300

3 Kawai (Rajasthan) 1,320

Total - Implementation 9,240

Power Generation

Power Transmission

SN Connecting Locations Length (Kms)

1*Mundra – Dehgam1000 MW, 400 KV

433Operational

2 *Tiroda – Warora1000 MW, 400 KV DC

200 Operational

3 *Mundra – Mohindergarh2500 MW, 500 KV HVDC

1,000Operational

4Tiroda – Aurangabad1

4500 MW, 765 KV SC1,290

Operational#

Total 2,923

Operation(MW)

4,620

2,640

1,320

8,580

*Transmission lines are part of inter-state transmission system

22

Power: Fuel Security & Off-take in PlaceCustomer

TotalCapacity

(MW)

Capacitycontracted

(MW)

Levelisedtariff

(INR/unit)

PPA starts from

Coal AvailabilityQty (MMT)

Coal Required (MMT)

Tariff revision requested

Gujarat - GUVNL (330x4) 1,320 1,000 2.89 Feb-10

Imported Coal 10.2Gujarat - GUVNL (660x2) 1,320 1,000 2.35 Feb-12

CERC final order received; full coal cost pass

through

Haryana - UHBVNL & DHBVNL (660x3)

1,980 475 + 949 2.94 Aug-12 /Feb-13 FSA signed for 6.4 MMT 6.4

CERC final order received; full coal cost pass

through

Mundra 4,620 3,424 16.6

Maharashtra - MSEDCL (660x2) 1,320 1,320 2.64 Aug-12 FSA signed for 4.91 MMT

FSA - Tapering linkage signed for 800 MW

8.3

MERC final order received; full coal cost pass through

Maharashtra - MSEDCL (660x3)

660 125 + 4403.28**

Aug-14 / Feb-17

1,320 1200 Apr-14 MoU signed for 3.39 MMT 5.5

Tiroda 3,300 3,085 13.8

Rajasthan - RRVPNL (660x2) 1,320 1,200 3.24** Aug-13 MoU signed for 3.39 MMT 5.5 P

Kawai 1,320 1,200 5.5Grand Total 9240 7709^ 35.9

**Fuel & Fuel Transportation are linked to CERC escalation index in PPA tariff^ PPA Capacity 92% of Net capacity

Power: Compensatory Tariff

23

• CERC final order on compensatory tariff entitled Adani Power forrecovery of past losses

• SCOD to 31-Mar-13 - Rs 830 crs and shall be recovered in 36monthly EMIs from the date of the order

• 1-Apr-13 to 28-Feb-14 - The compensatory tariff for the periodworks out - Rs 0.85/kwh for Gujarat Bid – 02 PPA andRs 0.36/kwh for Haryana PPA, and shall be recovered in 12monthly EMIs in accordance with the order

• CERC final order entitles Adani Power for full coal cost pass through

Compensatory

tariff

APL Phase III/IV

• Petition filed in MERC for for MSEDCL 1320 MW PPA to overcomethe hardship due to non-availability of captive coal mine

• MERC final order entitles APML for compensatory energy charge forsupply over and above 520 MW in the 1,320 MW PPA

• Compensatory energy charge at the current level of linkage (25%) for800 MW works out to Rs. 1.01/kWh

Compensatory

tariff

APML Phase I / II

Power: Other Developments

24

Pass through of additional imported coal cost

• Imported coal may be used to mitigate domestic coal shortage andincremental coal cost will be considered for pass-through over andabove existing PPA tariff

• Ministry of Coal has issued suitable orders supplementing the NewCoal Distribution Policy and MoP has issued appropriate advisory toregulators

12th Plan Power Projects – having PPA

• Government has asked CIL to work out modalities to provide longterm coal linkage to these projects

• Accordingly, till the time long term linkage is awarded CIL has agreedto provide coal to APRL (1320 MW) and APML Ph III (1320 MW)through MoU route. MoUs were signed for 3.39 MMT of Coalquantity for each project.

CCEA Directive

• CIL has allowed inter plant coal swapping which will result in overallbenefit due to savings in logistics cost and improved availability ofcoal to hinterland plants

• We have requested for conversion of 800 MW Tapering linkage(Received by APML in lieu of cancelled Lohara mine) into long termlinkage

Other

Developments

25

AEL assumes no responsibility to publicly amend, modify or revise any forward looking statements, on the basis of any subsequent development, information or events, or otherwise. Unless otherwise stated in this document, the information contained herein is based on management information and estimates. The information contained herein is subject to change without notice and past performance is not indicative of future results. AEL may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such revision or changes. No person is authorized to give any information or to make any representation not contained in and not consistent with this presentation and, if given or made, such information or representation must not be relied upon as having been authorized by or on behalf of AEL. This presentation is strictly confidential.This presentation does not constitute an offer or invitation to purchase or subscribe for any securities in any jurisdiction, including the United States. No part of its should form the basis of or be relied upon in connection with any investment decision or any contract or commitment to purchase or subscribe for any securities. None of our securities may be offered or sold in the United States, without registration under the U.S. Securities Act of 1933, as amended, or pursuant to an exemption from registration therefrom.This presentation is confidential and may not be copied or disseminated, in whole or in part, and in any manner.This presentation contains translations of certain Rupees amounts into U.S. dollar amounts at specified rates solely for the convenience of the reader.

Certain statements made in this presentation may not be based on historical information or facts and may be “forward-looking statements,” including those relating to general business plans and strategy of Adani Enterprises Limited (“AEL”) and Adani Ports and Special Economic Zone Limited (“APSEZ”) & Adani Power Limited (“APL”), their future outlook and growth prospects, and future developments in their businesses and their competitive and regulatory environment, and statements which contain words or phrases such as ‘will’, ‘expected to’, etc., or similar expressions or variations of such expressions. Actual results may differ materially from these forward-looking statements due to a number of factors, including future changes or developments in their business, their competitive environment, their ability to implement their strategies and initiatives and respond to technological changes and political, economic, regulatory and social conditions in India. This presentation does not constitute a prospectus, offering circular or offering memorandum or an offer, or a solicitation of any offer, to purchase or sell, any shares and should not be considered as a recommendation that any investor should subscribe for or purchase any of AEL’s shares. Neither this presentation nor any other documentation or information (or any part thereof) delivered or supplied under or in relation to the shares shall be deemed to constitute an offer of or an invitation by or on behalf of AEL. AEL, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to, the fairness, accuracy, completeness or correctness of any information or opinions contained herein. The information contained in this presentation, unless otherwise specified is only current as of the date of this presentation.

Legal disclaimer