28.06.2010 promoting affordable home ownership for mongolians through capital market development,...

TRANSCRIPT

MONGOLIAN MORTGAGE CORPORATION

Promoting affordable home ownership for Mongolians through

capital market development

2010. 06. 28Ulaanbaatar

MissionMission

Promotion and development of primary andPromotion and development of primary and secondary mortgage markets by raising medium to long term funds on domesticmedium to long term funds on domestic

and foreign capital markets through a series of capital market tools to create andseries of capital market tools to create and ensure the smooth functioning of a long-

term financing system to promote g y paffordable home ownership and urban development for Mongolia’s people.

Why MIK was established

- Liquidity for banks- Bank balance sheet managementg- Expand sound mortgage lending– Develop capital market– Develop capital market- Improve affordability of housing

creditcredit

3

MONGOLIAN MORTGAGE CORPORATIONMONGOLIAN MORTGAGE CORPORATION

Shareholders Shareholders

Established 06 09 2006Established 06.09.2006

MIK role is an Intermediary between primary mortgage market and secondaryprimary mortgage market and secondary mortgage market.

– Warehousing: purchase of pools of mortgages

Structure and issue capital market– Structure and issue capital market instruments

- Covered bondsCovered bonds- Asset backed securities

– Portfolio management, use varies financial instrument

Mortgage market overviewMortgage market overview Mortgage market /Debt; bln MNT/: 2007-2010

250

200

250

150

50

100

0

50

6

2005 2006 2007 2008 2009 I/2010 Apr-2010

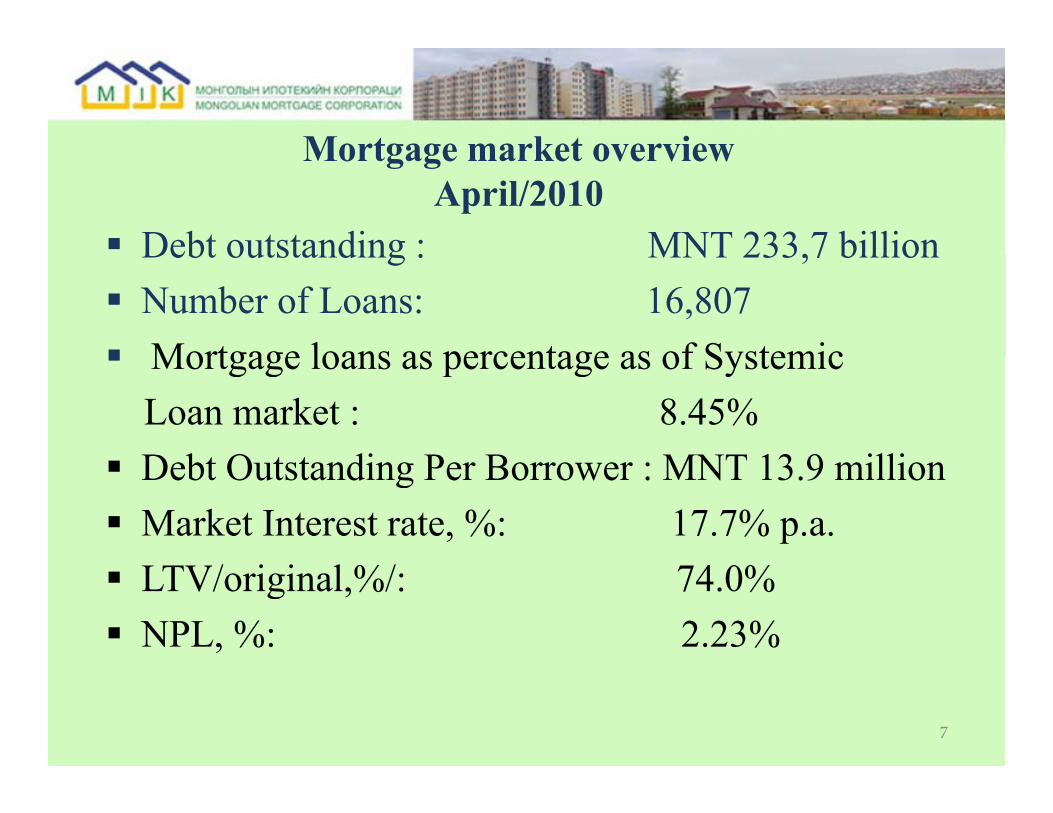

Mortgage market overview

Debt outstanding : MNT 233 7 billion

Mortgage market overview April/2010

Debt outstanding : MNT 233,7 billion Number of Loans: 16,807Mortgage loans as percentage as of SystemicMortgage loans as percentage as of Systemic Loan market : 8.45%D bt O t t di P B MNT 13 9 illiDebt Outstanding Per Borrower : MNT 13.9 million Market Interest rate, %: 17.7% p.a.LTV/original,%/: 74.0% NPL, %: 2.23%

7

МIK OPERATION

Total mortgage pools purchased – 8 times, MNT 9,9 billi

МIK OPERATION

billion.MIK registered covered bond- MNT 25 billion. MIK issued covered bond- MNT 6.3 billion.Investors:- Bank: MNT 5.7 billion- Insurance: MNT 0.6 billionListed as a Repo financing instrument. Currently working on issuing 15 billion MNT bond.

8

MIK Portfolio Performance Purchasing Type Structure at MIK

МIK OPERATION

MIK Portfolio Performance by end 05/2010

- Current loan: 96.0%

Purchasing Type Structure at MIK Portfolio,%

Current loan: 96.0%- Past due: 3.93%- NPL : 0 07%

WOR14%

- NPL : 0.07%

WR86%

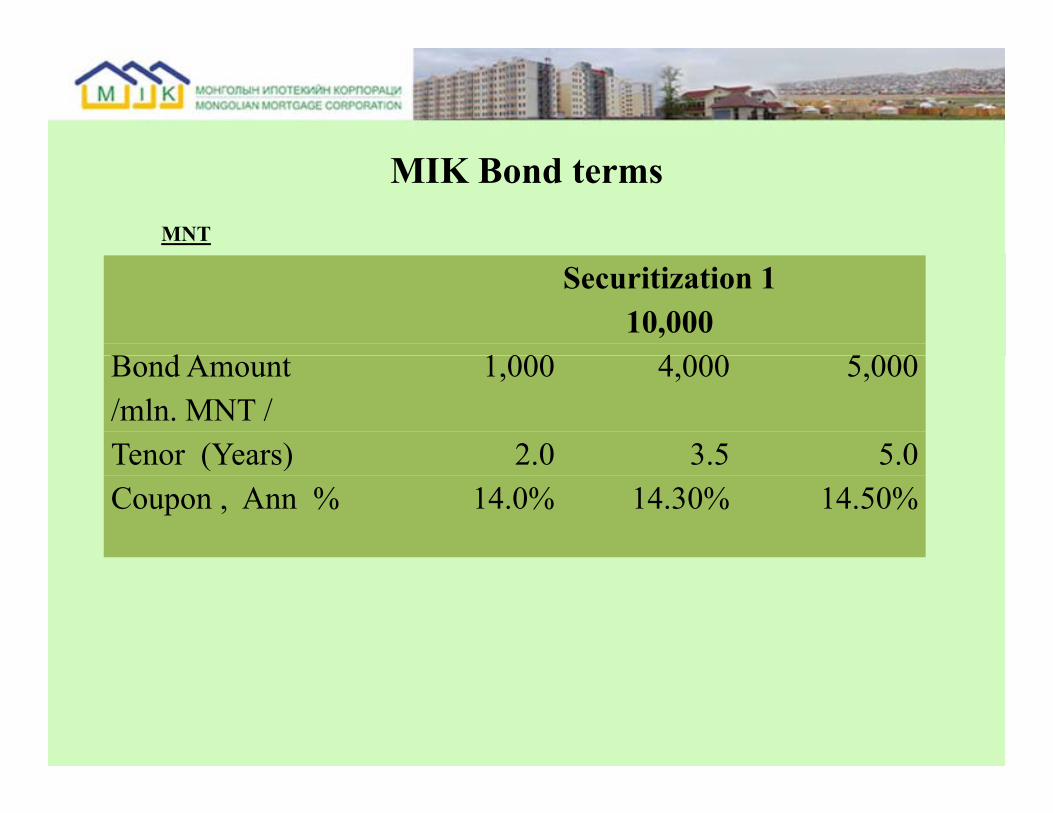

MIK Bond termsMNT

Securitization 110,000

B d A 1 000 4 000 5 000Bond Amount /mln. MNT /

1,000 4,000 5,000

Tenor (Years) 2 0 3 5 5 0Tenor (Years) 2.0 3.5 5.0Coupon , Ann % 14.0% 14.30% 14.50%

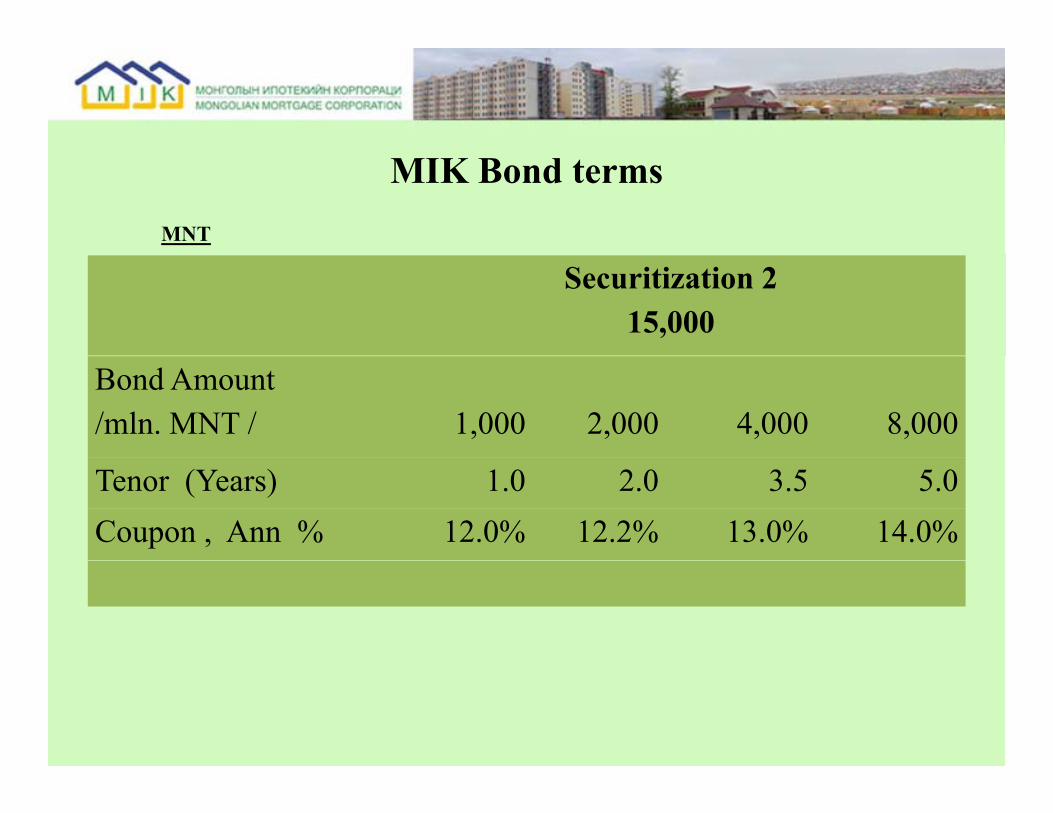

MIK Bond termsMNT

Securitization 215,000

Bond Amount /mln. MNT / 1,000 2,000 4,000 8,000

Tenor (Years) 1.0 2.0 3.5 5.0Coupon , Ann % 12.0% 12.2% 13.0% 14.0%

9

10Asset Equity

6

7

8

4

5

6

2

3

0

1

2007 2008 2009 IQ 20102007 2008 2009 IQ 2010MNT bln

МIK OPERATIONМIK OPERATION MIK debt outstanding/bln MNT/ : 2008.IV-2010.I

9

7

8

9

4

5

6

2

3

4

0

1

13

IV.2008 I.2009 II.2009 III.2009 IV.2009 I.2010

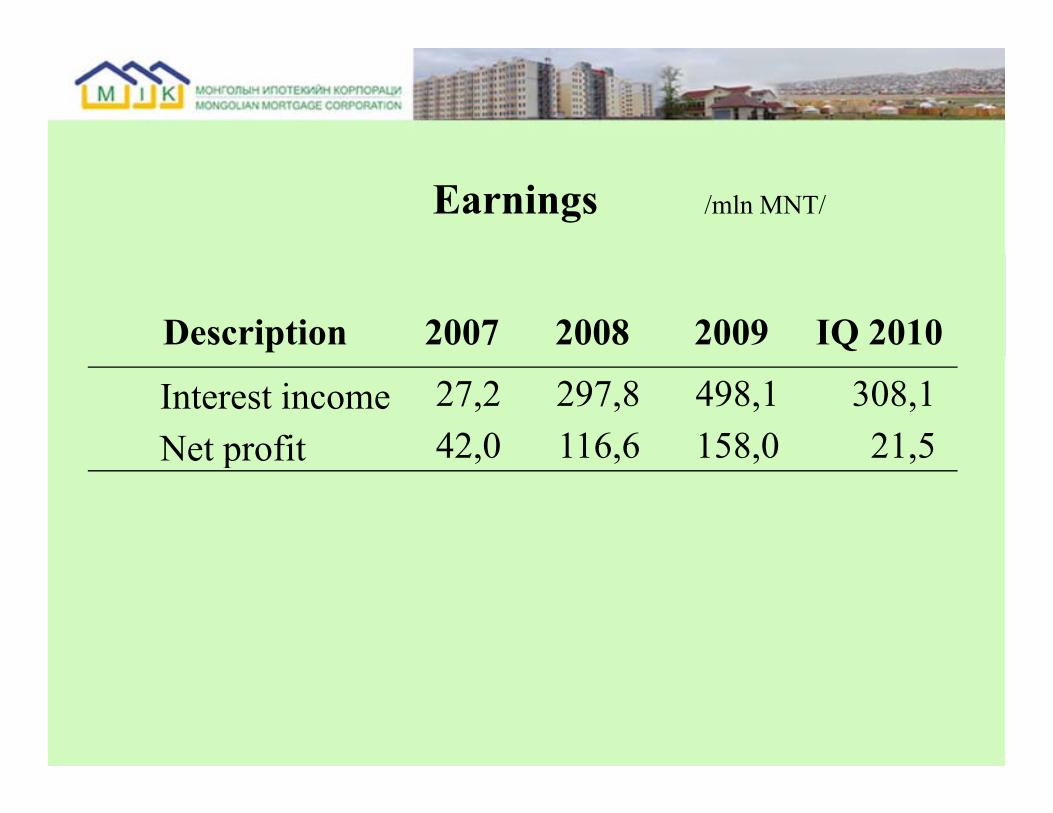

Earnings /mln MNT/

Description 2007 2008 2009 IQ 2010

Interest income 27,2 297,8 498,1 308,1Net profit 42,0 116,6 158,0 21,5Net profit ,0 6,6 58,0 ,5

МIK COOPERATIONМIK COOPERATION

15

KfW Loan and TA ProjectEuro 4.8 million loan for mortgage warehousing

Euro .9 million Technical assistance• December 2009 Consulting service was startedDecember 2009 Consulting service was started

with Frankfurt School of Management.• Minimum Quality Standards establishedMinimum Quality Standards established• IT improvement program was established

16

IFC cooperationIFC cooperationLocal consultancy and training

IFC’s Mortgage Lending Toolkit and training” was implemented in Mongolia with Shore Bank Consultancy Services.

• MIK has assisted to conduct seminars on mortgage and construction finance for local bank and NBFI staff.

Micro Housing Finance.

Goal: determine MHF needs in Mongolia and provide new MHF product.

• Market assessment.• Determine product type• Define risk management frameworkg• Manage workshop among potential providers• Develop Operational Manual for Mongolian market

17

MARKET INFRASTRUCURE AND LEGAL ENVIRONMENT

• Mortgage standardization procedure (October 2008)• Mortgage law ( July 2009)

MARKET INFRASTRUCURE AND LEGAL ENVIRONMENT

• Mortgage law ( July 2009)• Asset basked security law (April 2010)• Assisting to set up legal framework for domesticAssisting to set up legal framework for domestic

investors– Draft Amendment to Social Insurance Law– Insurance companies - FRC

• Legal environment for issuing MIK Bond FRC i t ti– FRC registration

– Shelf registration– OTC procedure /clearing house/– OTC procedure /clearing house/

I t b d f d l i ffi i t t k t d l tIssues to be done for developing efficient mortgage market development

e Political stability

men

t

fras

truc

ture

Standardization of mortgage loansPropert appraisal nm

ent

Political stabilityEconomic stabilityBalance on Supply and demand C ti d ti

env

iron

m

Mortgage lawMortgage securitySPV m

arke

t in

f Property appraisal Mortgage database systemMortgage insurance t e

nvir

on

Creating domestic potential investor AffordabilityCapacity development

l

Lega

l Pool registrationTax matterMIK legal status

y m

ortg

age

g gCredit bureauCapital market development M

arke

t Institutional capacityCoordination and linkages of market players

Prim

ary Rating

Income verification system

Quality of collateral •Efficiency of Urban planning, land development, construction quality•Effective operation and Effective operation and maintenance

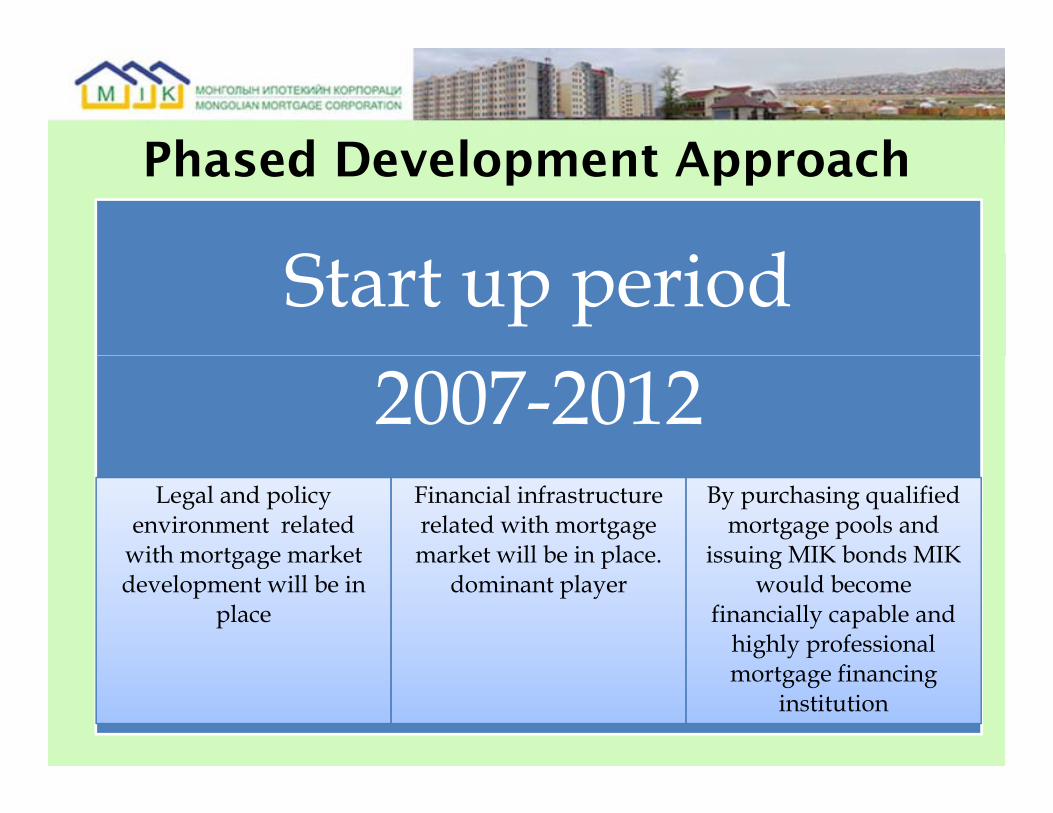

DEVELOPMENT PHASES DEVELOPMENT PHASES

Diversification 2017-2020

Development period 2013 20162013-2016

Start up period (setting up solid p pfoundation for mortgage market

development)2007-2012

Phased De elopment Approach Phased Development Approach

dStart up period2007-2012

Legal and policy environment related

with mortgage market

Financial infrastructure related with mortgage market will be in place.

By purchasing qualified mortgage pools and

issuing MIK bonds MIK with mortgage market development will be in

place

market will be in place. dominant player

issuing MIK bonds MIK would become

financially capable and highly professional mortgage financing

institution

MIK future business actions MIK future business actions

MLFSMF

MGFCapital increaseEquity investment

SMF-secondary mortgage facilityMLF- Mortgage lending facility

Commercially viable Affordable Housing finance system

MLF Mortgage lending facilityMGF- Mortgage Guarantee Facility

Housing finance system

THANK YOU

Mongolian Mortgage Corporation LLC /MIK/

MIK Building , United Nations street-38Chingeltei district-4, 15160Ulaabaatar Mongolia Ulaabaatar, Mongolia

www.mik.mn, [email protected]

l (9 6) 32826Tel: (976) 11-328267Fax (976) 11-313338

23