2020 statistical report of china’s bond market

TRANSCRIPT

2020 Statistical Report of China’s Bond Market

Statistics and Monitoring Department

China Central Depository & Clearing Co., Ltd.

January 15, 2021

Tel.: 86-10-88170157

Email: [email protected]

Contents

Preface........................................................................................................................................ 1

I. Status of China’s Bond Market in 2020 ................................................................................. 2

i. Total bond issuance increased sharply. ........................................................................... 2

ii. Total bond depository amount kept a stable growth. ..................................................... 3

iii. Bond market settlement volume grew faster. ............................................................... 5

iv. Bond yields dropped and then rose. .............................................................................. 7

v. Money market rates declined broadly. ........................................................................... 8

vi. Bond defaults remained on a level. ............................................................................... 9

II. Characteristics of the Bond Market in 2020 ........................................................................ 10

i. Vigorous issuance of anti-pandemic bonds .................................................................. 10

ii. Accelerated product innovation in the market ............................................................. 10

iii. Continuous institutional advance in the bond market ................................................ 11

iv. Overall progress in the opening-up of the bond market ............................................. 12

III. Suggestions for Future Development of the Bond Market ................................................ 13

i. To improve CGB’s role as a benchmark and CGB-related taxation arrangements. ..... 13

ii. To optimize credit ratings and market liquidity of LGBs............................................ 14

iii. To enhance the credit system and responsibility of intermediaries. ........................... 14

iv. To push forward see-through ABS supervision and standardized operation. ............. 14

v. To expand cross-border use of RMB bonds and internationalization of RMB. .......... 15

vi. To implement the requirements for safe development and base the financial market

on a solid footing. ............................................................................................................ 15

1

Preface

In 2020, China’s bond market kept going stably, with a substantial surge in issuance, a steady

increase in the outstanding amount, and a higher growth rate in settlement volume. To hedge

the adverse impact of the COVID-19 pandemic, monetary policies remained flexible and

appropriate. As a result, inter-bank market liquidity stayed reasonably abundant, money

market rates went down overall, bond yields dropped somewhat compared with last year after

a V-shaped movement, and bond credit risk intensified slightly. The bond market strongly

supported the nationwide pandemic control efforts, by issuing anti-pandemic bonds, rolling

out innovative green financial bonds, launching enterprise bonds under the registration-based

system, and diversified the lineup of pricing products. The bond market continued to make

institutional advances. Specifically, the registration-based system progressed smoothly, the

default disposal mechanism improved continuously, and the information disclosure policies

were unified and standardized. The market also sped up its opening-up pace, leading to a

substantial spike in the bond holdings by foreign investors. Despite the huge shocks brought

about by the pandemic and the profound and complex changes in international and domestic

situations, China’s bond market in 2020 provided important financial services and support for

the nationwide endeavors to fight against the pandemic and ensure economic development.

In 2021, the bond market will continue to underpin China’s economic development and

improve its role in facilitate direct financing. It is recommended to enable China government

bonds (CGBs) to continue functioning as a financial benchmark, boost liquidity of local

government bonds (LGBs), enhance the credit system, promote see-through supervision for

ABS, expand cross-border use of RMB bonds, and propel safe and sound development of

financial market infrastructures.

2

I. Status of China’s Bond Market in 2020

i. Total bond issuance increased sharply.

In 2020, total issuance of bonds of all types recorded RMB 37.75 trillion1, a YOY increase of

39.62%. Among these, RMB 21.87 trillion, or 57.94% of total, was issued and registered at

China Central Depository & Clearing Co., Ltd. (CCDC); RMB 9.69 trillion, or 25.66% of

total, was at Shanghai Clearing House (SHCH); and RMB 6.19 trillion, or 16.40%, was on

the exchanges. (Table 1)

Source: CCDC, SHCH and Wind

Figure 1 Bond issuance from 2005 to 2020 (in 100 million RMB)

Table 1 Bond issuance (in trillion RMB)

2020 2019 YoY Change %

Total 37.75 27.04 39.62% 100.00%

CCDC 21.87 15.31 42.91% 57.94%

SHCH 9.69 7.21 34.30% 25.66%

CSDC 6.19 4.52 36.93% 16.40%

Note:CSDC stands for China Securities Depository and Clearing Corporation Limited.

Source: CCDC, SHCH and Wind

In the inter-bank market, at CCDC, the issuance of book-entry CGBs was RMB 6.91 trillion,

up by 83.91% YOY; LGBs, RMB 6.44 trillion, up by 47.71%; policy bank bonds, RMB 4.90

trillion, up by 33.95%; commercial bank bonds, RMB 1.94 trillion, up by 21.13%; and credit

asset-backed securities (ABS), RMB 0.80 trillion, down by 16.53%. At SHCH, the issuance

of medium-term notes was RMB 2.29 trillion, up by 24.97% YOY; SCP (including SSCP),

RMB 4.99 trillion, up by 39.40%; and private targeted debt financing instruments, RMB 0.69

trillion, up by 11.99%. (Figure 2)

1 Inter-bank negotiable certificates of deposits (NCDs) were excluded from the issuance or the outstanding

amount. Issuance of NCD throughout the year amounted to RMB18.97 trillion, and the outstanding amount at

year-end was RMB11.15 trillion.

3

Source: CCDC and SHCH

Figure 2 Bonds issuance in the inter-bank market in 2020

ii. Total bond depository amount kept a stable growth.

As of end-2020, total outstanding bonds under depository had reached RMB 104.32 trillion,

up by RMB 16.94 trillion or 19.38% YOY. The amount under CCDC depository was RMB

77.14 trillion, or 73.95% of the total market, comprising mainly CGBs, LGBs, and financial

bonds (Figure 3); that under SHCH, RMB 13.37 trillion, or 12.81% of the market; and that on

the exchanges, RMB 13.81 trillion, or 13.24% of the market. (Table 2)

Table 2 Bonds under depository (in trillion RMB)

Source: CCDC, SHCH and Wind

2020 2019 YoY Change %

Total 104.32 87.38 19.38% 100.00%

CCDC 77.14 64.98 18.72% 73.95%

SHCH 13.37 11.63 14.97% 12.81%

CSDC 13.81 10.78 28.14% 13.24%

LGBs Policy bank bonds

Commercial bank bonds

Enterprise bonds 1%

ABS 3%

SSCP

Private targeted debt financing instruments…

SCP 2%

Securities firm SCP… Other bonds

Government-backed agency bonds 1%

Book-entry CGBs

4

Source: CCDC

Figure 3 Breakdown of bonds under CCDC depository at end-2020

The following are observations regarding bonds under CCDC depository and structure of

holdings at end-2020 (Table 3):

1. Government bonds under depository went up compared to end-2019. They totaled RMB

45.63 trillion at end-2020, up by 22.59% YOY, of which book-entry CGBs went up by

26.99% YOY and LGBs grew by 20.52% YOY. As for the investor structure, commercial

banks continued to be the largest investor, holding 75.82% of the total. Insurance companies

and securities firms built up their holdings faster than others, recording a YOY growth rate of

106.88% and 97.56%, respectively.

2. The size of commercial bank bonds grew steadily, and supplementary capital instruments

developed swiftly. Outstanding commercial bank bonds totaled RMB 5.86 trillion, up by

24.82% YOY, of which outstanding other tier-1 capital instruments recorded a new high to

hit RMB 1.22 trillion, up by 113.83% YOY. As for the investor structure, overseas

institutions and other financial institutions increased their holdings at the fastest pace,

registering a YOY growth rate of 108.61% and 51.77%, respectively.

LGBs

Book-entry CGBs Policy bank bonds

Commercial bank bonds 8%

Enterprise bonds 4%

ABS 3%

Government-backed agency bonds 2%

Savings CGB 1%

Non-bank financial institution bonds 1%

Other bonds 0%

5

Table 3 Holding structure of bonds under CCDC depository at end-2020

Balance Institution

(in RMB 100 million)

Type

Policy

banks

Commercial

banks

Credit

cooperatives

Insurance

companies

Securities

firms

Other

financial

institutions

Unincorporated

products

Non-financial

institutions

Overseas

institutions Others Total

Book-entry

CGBs

2020 1138.35 122342.63 1666.68 4788.34 3906.95 945.64 15010.53 5.10 18775.81 25785.04 194365.07

YOY 7.71% 23.00% 76.56% 32.22% 132.33% 87.33% 36.98% -29.17% 43.69% 18.55% 26.99%

LGBs

2020 15165.41 215920.82 1485.48 5504.35 1087.49 343.10 7909.19 0.00 33.40 7076.30 254525.54

YOY -9.54% 18.64% 19.66% 306.62% 28.47% 81.90% 91.44% -- 32.02% 52.69% 20.52%

Government-

backed

agency bonds

2020 527.26 9320.51 138.72 1920.23 215.43 85.17 4323.88 0.21 57.19 636.39 17225.00

YOY 40.13% 4.72% -17.86% -4.67% -8.40% 674.27% -4.56% 0.00% 20.93% 44.21% 2.99%

Policy bank

bonds

2020 550.60 100365.82 5200.02 6021.72 1614.08 434.91 56278.64 0.20 9191.82 747.10 180404.90

YOY 24.34% 7.83% 8.25% -2.21% 1.36% 82.66% 25.44% 0.00% 84.42% -5.34% 14.95%

Commercial

bank bonds

2020 920.90 18390.34 284.18 3919.95 313.21 137.35 34325.27 2.00 327.15 0.00 58620.34

YOY 35.11% 16.91% -5.01% 19.96% 17.07% 51.77% 29.69% 0.00% 108.61% -100.00% 24.82%

Enterprise

bonds

2020 60.23 5096.73 98.29 697.73 1821.49 66.04 12504.86 1.76 98.38 8944.44 29389.95

YOY 37.20% 1.62% -29.54% -8.38% -1.61% -7.65% -10.07% -3.30% -27.79% 13.87% -1.32%

ABS

2020 15.14 13339.04 0.50 65.27 293.32 660.27 7158.89 0.00 278.25 7.28 21817.96

YOY -45.72% 27.78% -80.77% 13.26% 67.12% 20.83% -12.34% -- -4.15% -28.45% 10.66%

Source: CCDC

3. Non-bank financial institutions increased their holdings faster than the others. Non-bank

financial institutions such as insurance companies and securities firms held bonds of RMB

3.56 trillion at end-2020, recording a YOY growth rate of 36.03%. Their favorite types were

CGBs and policy bank bonds, which combined to 69.50% of their total holdings. The greatest

holding increase went to CGBs, which accounted for 89.14% of the total new holdings.

4. Overseas institutions continued to increase their holdings. As of end-2020, overseas

institutions had expanded their bond holdings with the total bonds held reaching RMB 2.88

trillion, up by RMB 1 trillion or 53.70% YOY. Their favorite types, by both aggregate

amount and increase of holdings, were CGBs and policy bank bonds, which combined to

97.92% of their total holdings and 98.48% of their holding increase. 76.09% of bonds they

held at CCDC were through the Global Connect scheme.

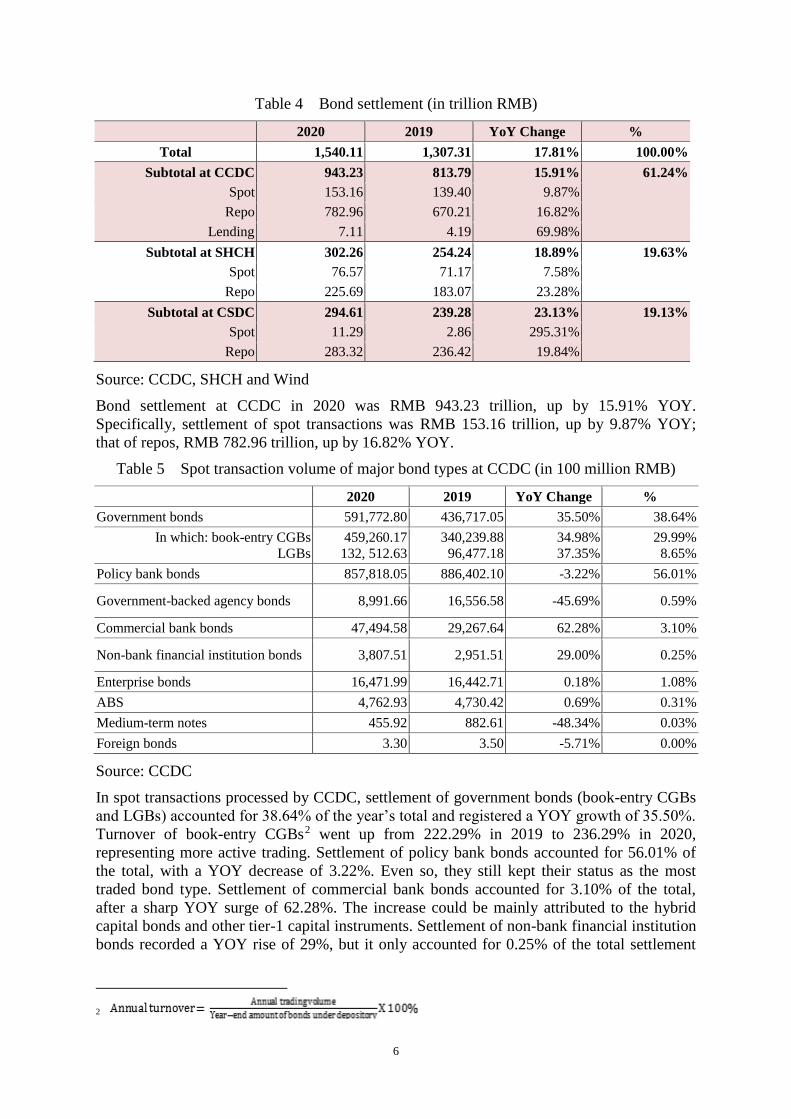

iii. Bond market settlement volume grew faster.

In 2020, total settlement in the bond market stood at RMB 1,540.11 trillion, up by 17.81%

YOY, which was up by 3.13 percentage points than that in 2019. Specifically, bond

settlement at CCDC was RMB 943.23 trillion, or 61.24% of the total market, that at SHCH

was RMB 302.26 trillion, or 19.63% of the total market, and that on the exchanges was RMB

294.61 trillion, or 19.13% of the total market. Seen from the types of transaction, settlement

of spot transactions was RMB 241.02 trillion, up by 12.93% YOY; settlement of repos was

RMB 1,291.97 trillion, up by 18.56% YOY; and settlement of bond lending was RMB 7.11

trillion, up by 69.98% YOY. (Table 4)

6

Table 4 Bond settlement (in trillion RMB)

2020 2019 YoY Change %

Total 1,540.11 1,307.31 17.81% 100.00%

Subtotal at CCDC 943.23 813.79 15.91% 61.24%

Spot 153.16 139.40 9.87%

Repo 782.96 670.21 16.82%

Lending 7.11 4.19 69.98%

Subtotal at SHCH 302.26 254.24 18.89% 19.63%

Spot 76.57 71.17 7.58%

Repo 225.69 183.07 23.28%

Subtotal at CSDC 294.61 239.28 23.13% 19.13%

Spot 11.29 2.86 295.31%

Repo 283.32 236.42 19.84%

Source: CCDC, SHCH and Wind

Bond settlement at CCDC in 2020 was RMB 943.23 trillion, up by 15.91% YOY.

Specifically, settlement of spot transactions was RMB 153.16 trillion, up by 9.87% YOY;

that of repos, RMB 782.96 trillion, up by 16.82% YOY.

Table 5 Spot transaction volume of major bond types at CCDC (in 100 million RMB)

2020 2019 YoY Change %

Government bonds 591,772.80 436,717.05 35.50% 38.64%

In which: book-entry CGBs

LGBs

459,260.17

132, 512.63

340,239.88

96,477.18

34.98%

37.35%

29.99%

8.65%

Policy bank bonds 857,818.05 886,402.10 -3.22% 56.01%

Government-backed agency bonds 8,991.66 16,556.58 -45.69% 0.59%

Commercial bank bonds 47,494.58 29,267.64 62.28% 3.10%

Non-bank financial institution bonds 3,807.51 2,951.51 29.00% 0.25%

Enterprise bonds 16,471.99 16,442.71 0.18% 1.08%

ABS 4,762.93 4,730.42 0.69% 0.31%

Medium-term notes 455.92 882.61 -48.34% 0.03%

Foreign bonds 3.30 3.50 -5.71% 0.00%

Source: CCDC

In spot transactions processed by CCDC, settlement of government bonds (book-entry CGBs

and LGBs) accounted for 38.64% of the year’s total and registered a YOY growth of 35.50%.

Turnover of book-entry CGBs2 went up from 222.29% in 2019 to 236.29% in 2020,

representing more active trading. Settlement of policy bank bonds accounted for 56.01% of

the total, with a YOY decrease of 3.22%. Even so, they still kept their status as the most

traded bond type. Settlement of commercial bank bonds accounted for 3.10% of the total,

after a sharp YOY surge of 62.28%. The increase could be mainly attributed to the hybrid

capital bonds and other tier-1 capital instruments. Settlement of non-bank financial institution

bonds recorded a YOY rise of 29%, but it only accounted for 0.25% of the total settlement

2

7

amount. The increase was mainly credited to tier-2 capital instruments. Settlement of

enterprise bonds accounted for 1.08% of the total, with a YOY increase of 0.18%. (Table 5)

iv. Bond yields dropped and then rose.

Overall, bond yields went down slightly in 2020 over the previous year. Compared with 2019,

the daily average 10-year CGB yield went down 24 bps to 2.9441% in 2020, the daily

average 10-year CDB yield shrank by 24 bps to 3.3682%, and the daily average 10-year

enterprise bond yield fell 25 bps to 4.0744% (Figure 4).

Source: CCDC

Figure 4 Yield curves of major bond types (%)

Table 6 Yield changes of major bond types over end-2019 (bps)

Term CGBs Policy bank bonds Enterprise bonds

(AAA)

1Y 11 6 -6

3Y 9 7 8

5Y 6 -11 4

7Y 13 -9 3

10Y 1 -4 -12

15Y 11 -4 -6

30Y 1 -2 9

Arithmetic average 7.43 -2.43 0.00

Source: CCDC

Throughout 2020, bond yields fell first and then rose, revealing a V-shaped movement. From

January to April, affected by the pandemic, the yields of CGBs and policy bank bonds

plummeted, and those of enterprise bonds also declined though to a lesser degree. As China’s

ChinaBond CGB YTM: 10-year ChinaBond CDB Bond YTM: 10-year

ChinaBond Enterprise Bond YTM (AAA): 10-year

8

pandemic prevention and control measures achieved phased success after May, policies were

enhanced to hedge shocks, the national economy rebounded rapidly and the bond yield curves

went up in general. As of end-2020, various types of bonds saw their yields basically

returning to the levels at end-2019. Specifically, compared with end-2019, yields of CGBs of

key terms rose by 7.34 bps, those of policy bank bonds fell by 2.43 bps, and those of

enterprise bonds remained unchanged. (Table 6)

In 2020, bond prices went through a rapid rise and then a decline. The ChinaBond New

Composite Index (net price) rose rapidly from January to April, then gradually declined after

May, and rebounded slightly from late November to the year-end. As of end-2020, the above

index closed at 99.8606 points, a decrease of 0.73% from end-2019. In terms of volatility, it

reached 103.3877 points on April 29, the highest level of the year and fell to 99.1803 points

on November 20, the lowest of the year, marking a difference of 4.07%.

Source: CCDC

Figure 5 Trends of ChinaBond New Composite Index (net price)

v. Money market rates declined broadly.

Owing to the reasonably ample liquidity in the banking system, the money market rates went

down in general compared with last year. The daily average of overnight benchmark repo rate

(BR001) dropped 58 bps from 2019 to 1.60%, and the daily average of 7-day benchmark repo

rate (BR007) stood at 2.11%, down 49 bps (Figure 6). The daily average of overnight Shibor

fell 59 bps to 1.5912%, the daily average of 7-day Shibor dropped 48 bps to 2.1106%, and

the daily average of 3-month Shibor dropped 44 bps to 2.3968% (Figure 7).

ChinaBond New Composite

Index - total value - net price ChinaBond New Composite Index - total value - cash

bond settlement (in RMB 100 million)

9

Source: CCDC

Figure 6 Trends of BR (%)

Source: Shibor

Figure 7 Trends of SHIBOR (%)

vi. Bond defaults remained on a level.

In 2020, new defaults amounted to RMB 125.38 billion, a slight increase of 1.68% YOY,

which was 4.99 percentage points lower than that in 2019. In terms of the number of bonds,

113 bonds defaulted in 2020, down 30.25% YOY; as to the number of defaulting parties, 36

issuers defaulted on their debts, down by 26 from 2019, and 21 issuers among them had their

first defaults, down by 23.

Medium to high-rated bonds made the bulk of the new defaults and rollovers. The defaulted

and rolled-over bonds rated at AAA and AA+ amounted to RMB 73.12 billion and RMB

45.79 billion respectively, which combined to account for over 83% of the total, an increase

of 29 percentage points from 2019. The upward shift in the ratings of defaults and rollovers

was mainly due to growing defaults by state-owned enterprises (SOEs). In 2020, the SOE

defaulted on bonds totaling RMB 82.84 billion, a YOY increase of 473%, of which 92% were

bonds rated AA+ and above.

In addition, more negotiated rollovers were observed. Throughout 2020, 35 bonds, up by

52.17% YOY, turned to negotiated rollovers, which amounted to RMB 27.15 billion, up by

31.76% YOY. Of these bonds, only one was redeemed, which was valued at RMB 250

BR001 BR007

10

million; another three defaulted in the end, with a total value of RMB 1.5 billion. These

rollovers involved 23 issuers, an increase of 8 YOY.

II. Characteristics of the Bond Market in 2020

i. Vigorous issuance of anti-pandemic bonds

To fight the COVID-19 pandemic, the Politburo Bureau of the CPC Central Committee

pointed out that macroeconomic policies should be intensified to set off negative impacts. To

be specific, more proactive and effective fiscal policy would be used. The deficit-to-GDP rate

would be raised by issuing special anti-pandemic CGBs and LGBs to effectively buttress

economic stability. The People’s Bank of China (PBC) adopted a number of facilitation

measures to support financial institutions in issuing bonds to help fight the pandemic. CCDC

supported the issuance of special anti-pandemic CGBs and anti-pandemic financial bonds by

the Agricultural Development Bank of China (ADBC), China Development Bank (CDB), and

the Export-Import Bank of China (EXIM), and ensured the issues by Hubei Provincial

Government. Thus, CCDC provided technical and other professional support for the bond

market in its endeavors to combat COVID-19.

Throughout 2020, various types of bonds worth RMB 1,367.226 billion3 were issued to help

address impacts made by COVID-19. In this way, the bond market played an important role

in supporting the pandemic control efforts and promoting economic recovery. Of these bonds,

RMB 1,064.5 billion was issued at CCDC, accounting for 77.86% of the total.

ii. Accelerated product innovation in the market

1. Innovation in financial bonds continued.

First, financial bonds were issued to support green industries. ADBC issued its “Two

Mountains” bond to kick off the regular issuance to support ecological and environmental

protection. CDB issued the first Bond Connect green financial bonds to address climate

change, the proceeds of which would be used for green projects such as low-carbon

transportation, in a move to effectively slow down and curb climate change. The green bonds

issued by China Construction Bank (CCB) were listed on Nasdaq Dubai. This was the first

time for a Chinese-funded bank to do so. The bonds had received pre-issuance certification

from the Climate Bonds Initiative. Bank of China (BOC) had its dual-currency blue bond

priced and listed overseas, the first among global commercial issuers. Blue bonds, as a type

of green bonds, use the proceeds on sustainable development of marine economy (also known

as the blue economy). The proceeds of the BOC bond would be used to support the marine

sewage treatment projects and the offshore wind power projects.

Second, perpetual bonds started to be issued by private banks. With the approval of CBIRC

Zhejiang Office, MYbank was allowed to issue perpetual bonds up to RMB 5 billion, which

would be counted as other tier-1 capital. This was the first perpetual bond by a private bank

in China. It marked that private banks were now eligible issuers of perpetual bonds, allowing

more channels of capital replenishment for these banks.

2. Innovation in enterprise bonds flourished.

First, the first enterprise bonds under the registration-based system were launched. In April,

the first registration-based enterprise bond issuers, such as Shenzhen Metro Group Co., Ltd.

3 Data source: Wind

11

(SZMC) and Shanghai Lujiazui (Group) Co., Ltd., obtained the notice of enterprise bond

registration from the National Development and Reform Commission (NDRC), marking the

debut of registration-based enterprise bonds as per the new Securities Law. Subsequently,

SZMC managed to issue China’s first registration-based enterprise bond with a total amount

of RMB 6 billion. This issue was enabled by CCDC Shenzhen Center with a full set of issuer

services including consulting, application reception and review, customer service, operational

support and marketing.

Second, the first high-quality enterprise bond with the follow-on option was issued. In April,

China Chengtong Holding Group Ltd. (CCT) issued at CCDC the first high-quality enterprise

bond with a follow-on offering option, which amounted to RMB 3 billion. The planned

issuance amount for the first offering was RMB 1 billion, and investors made follow-on

subscriptions of RMB 3.45 billion, showing the market’s recognition of how high-quality

enterprise bonds.

3. Pricing products became more diversified.

In 2020, CCDC released new yield curves and indices, offering a classified and diversified

lineup of pricing products.

First, more classified yield curves were presented. CCDC created yield curves for the

highway industry, the power industry and the construction engineering industry. It published

yield curves for privately placed industry bonds and urban investment bonds, so as to meet

market demand. Besides, for yield curves of Chinese-issued US dollar bonds, CCDC

expanded the rating coverage and added standard terms and valuation. It also launched curves

and valuations for Chinese-issued EUR bonds, thus covering more offshore bonds by Chinese

issuers.

Second, new bond indices were launched. CCDC released the ChinaBond 0-5Y Yangtze

River Delta LGB Index, the ChinaBond 10Y Policy Bank Bond Strategy Index, the

ChinaBond Tier-2 Capital Bond Index, the ChinaBond Residential MBS Index, and the

ChinaBond ABS Index; the ChinaBond-CITIC Securities CGB Futures Deliverable Bond

Select Index, and the ChinaBond-GTJA 10Y CGB Futures Deliverable Bond Liquidity

Weighted Index; and the ChinaBond Credit Bond Value Factor Strategy Index and the

ChinaBond-Huaxia Asset Management ESG Select Bond Strategy Index. All of these

provided bond investors with performance benchmarks and targets for investment.

iii. Continuous institutional advance in the bond market

1. Credit bonds made progress towards registration-based issuance.

First, progress was made to allow registration-based issuance o enterprise bonds. In February,

the General Office of the State Council issued the Notice on the Implementation of the

Revised Securities Law, requiring that the public issuance of corporate bonds should be

registered with China Securities Regulatory Commission (CSRC) or NDRC. In March,

NDRC released the Notice on the Matters Concerning the Implementation of the Registration

System for Enterprise Bond Issuance, explaining the matters related to the implementation of

the registration system for the issuance of enterprise bonds. According to the notice, CCDC

was designated as the accepting agency and the review agency, and the National Association

of Financial Market Institutional Investors (NAFMII) was another review agency. In April,

the first batch of registration-based enterprise bonds was officially launched. In August,

CCDC published Q&A on the registration and issuance of enterprise bonds, providing useful

policy interpretation and guidance to facilitate the transition to registration-based issuance,

12

and enabling enterprise bonds to serve the real economy more efficiently under the

registration system.

Second, progress was made step by step to allow registration-based issuance of corporate

bonds. In August, CSRC solicited opinions publicly on the revision of the Administrative

Measures for the Issuance and Trading of Corporate Bonds. In November, Shanghai Stock

Exchange (SSE) issued rules to improve its mechanism for reviewing listing of corporate

bonds under the registration system.

2. The bond default disposal mechanisms were improved.

First, a bond default disposal mechanism was put in place. In January, PBC released an

announcement on the matters concerning the transfer of bonds defaulted upon maturity in the

inter-bank bond market. Accordingly, such bonds should be transferred through the trading

platform and the depository and settlement agency in the inter-bank bond market, with

delivery versus payment (DVP) adopted for settlement of bonds and funds. In March, the

National Interbank Funding Center issued the Rules on the Transfer of Bonds Defaulted upon

Maturity in the Inter-bank Market. In August, CCDC and SHCH co-released the Business

Rules of the Depository and Settlement Agency on the Transfer and Settlement of Bonds

Defaulted upon Maturity in the Inter-bank Bond Market, marking the establishment of a

mechanism through which the defaulted bonds could be transferred and settled in the

inter-bank market.

Second, there were further refined and specified provisions on bond default and substitution.

In July, PBC, NDRC, and CSRC jointly issued the Notice on the Matters Concerning the

Disposal of Defaulted Corporate Credit Bonds. Focused on the establishment of a unified

bond default response framework, the notice pointed out directions for addressing related

issues, such as issuers’ malicious evasion of debt repayment, problematic prospectus and lack

of sound market-based default disposal mechanisms. The release of the notice could propel

the endeavors to realize market-based and well-regulated disposal of defaulted bonds.

3. Information disclosure was standardized for credit bonds.

In December, PBC, NDRC, and CSRC jointly issued the Administrative Measures for the

Information Disclosure of Corporate Credit Bonds, which set forth unified requirements for

key elements, contents, time points, frequency and other aspects of information disclosure

with respect to corporate credit bonds. The introduction of the measures was an important

institutional measure to standardize disclosure of corporate bonds and to improve the bond

market as a whole.

iv. Overall progress in the opening-up of the bond market

1. Policies for overseas institutions became more enabling.

First, overseas institutions became able to participate in the market in more ways. In January,

the Ministry of Finance (MOF) instructed local financial departments to revise and improve

the measures for forming LGB underwriting syndicates, by allowing wholly foreign-owned

banks, joint Chinese-foreign banks and foreign bank branches to be syndicate members. Thus,

participation of foreign banks was extended from distribution and the secondary market to

underwriting of bonds. In March, CCDC launched recycling settlement and extended

settlement cycles to allow overseas investors greater flexibility in terms of settlement.

Second, facilitation was enhanced for overseas investors. In January, the State Administration

of Foreign Exchange (SAFE) issued the Notice on Relevant Matters Concerning the Foreign

13

Exchange Risk Management of Foreign Institutional Investors in the Inter-bank Bond Market

to provide foreign investors with more channels to hedge foreign exchange risks. In

September, PBC, CSRC and SAFE co-issued the Announcement on Matters Concerning the

Investments in the Chinese Bond Market by Foreign Institutional Investors (Consultation

Paper), with a view to further facilitating foreign investors’ participation.

2. Participation in international bond markets increased constantly.

First, offshore issuance of CGBs, sovereign bonds and central bank bills became a regular

practice. In 2020, MOF issued RMB CGBs totaling RMB 15 billion in Hong Kong. It issued

USD-denominated sovereign bonds of USD6 billion in October, and issued in November

EUR-denominated sovereign bonds of EUR4 billion at negative interest rates for the first

time. PBC issued in Hong Kong 12 central bank bills totaling RMB 155 billion.

Second, innovative issuance of financial bonds was achieved overseas. In January, CDB

issued GBP-denominated bonds totaling GBP1 billion in the offshore market. The deal was

the largest single issuance in the GBP bond market in recent years, and also the first

GBP-denominated bonds issued by a domestic Chinese bank. In August, ADBC issued the

first RMB policy bank bond in the offshore market. In September, BOC issued the first

Chinese-funded blue bond in the offshore market.

Third, RMB bonds were included into more global indices. In February, JPMorgan Chase

announced to include nine eligible highly liquid CGBs into its government bond index -

emerging markets (GBI-EM) indices. It was predicted to bring over USD20 billion into the

Chinese bond market.

3. Domestic and overseas institutions maintained communication and collaboration.

First, a seminar on cross-border bond ETF was hosted. In October, CCDC, along with China

Europe International Exchange (CEINEX), held the 2020 Online Seminar on Cross-border

Chinese Bond ETF to discuss opportunities and challenges facing the business.

Second, ChinaBond indices were listed on Singapore Exchange. In November, the NikkoAM

- ICBCSG China Bond ETF tracking the ChinaBond-ICBC RMB Bond Index was listed on

Singapore Exchange. It was the first EFT in Singapore to invest in CGBs and policy bank

bonds by tracking a ChinaBond.

Third, anti-pandemic panda bonds were issued. In April, the New Development Bank (NDB)

issued the first anti-pandemic panda bond totaling RMB 5 billion, which became the largest

single issue in the panda bond market. The Asian Infrastructure Investment Bank (AIIB)

issued another anti-pandemic panda bond totaling RMB 3 billion in June.

III. Suggestions for Future Development of the Bond Market

i. To improve CGB’s role as a benchmark and CGB-related taxation arrangements.

First, CGB yield curves need to be used as a pricing benchmark of deposit and loan interest

rates. As a market-oriented rate with great integrity and continuity, the CGB yield curves are

recommended to be gradually promoted as a pricing benchmark for deposits and loans

through pilot programs.

Second, CGB yield curves can be put into more use in macro policies. It is advised to use

these curves as an intermediary target of monetary policies. The relationship between the

CGB yields and the potential economic growth is relatively stable. On the premise of a stable

potential economic growth, the CGB yields can be used to measure the appropriateness of

14

monetary policies. Specifically, CGB maturity spreads reflect market expectations and thus

can provide reference for macroeconomic policies.

Third, taxation needs to be improved. At present, interest income incurred on CGBs held is

tax-free, while capital gains generated from trading of CGBs are taxable. Such a tax

distortion inhibits the trading activity of CGBs in the secondary market. An improved

taxation arrangement will boost financing functions and liquidity of the CGB market.

ii. To optimize credit ratings and market liquidity of LGBs.

First, efforts need to be made to improve the rating system for LGBs. Although a basic rating

system is in place, actual LGB ratings are barely differentiated in practice. Therefore, the

rating system should be improved to allow rating agencies to give more differentiated ratings

that honestly represent different financial conditions of the issuers or underlying projects.

Second, the LGB market needs to be optimized for better liquidity. Despite progress in recent

years, the LGB market is still plagued by low overall liquidity and geographically biased

liquidity. In response, actions need to be taken to increase the varieties of LGBs by

expanding interest payment and redemption methods, enriching the lineup of floating-rate

bonds, and developing hedging products such as LGB index options and futures at a proper

time. At the same time, it is necessary to roll out innovative products such as LGB ETFs, and

attract asset managers to invest in LGBs.

iii. To enhance the credit system and responsibility of intermediaries.

First, the credit system needs to be enhanced. It is imperative to improve assessment of lead

underwriters of credit bonds, and strengthen supervision measures and credit constraints on

enterprise bonds both before and after issuance. Besides, efforts need to be made to improve

regulatory rules, and put in place an open, transparent and efficient management system for

registration and issuance of enterprise bonds. Research and application should be conducted

to combine financial technology and regulatory approaches, and big data can be used in

innovative ways.

Second, information disclosure services can be made better. More work needs to be done to

monitor and forestall credit risks related to enterprise bonds, and to implement the

Administrative Measures on Information Disclosure of Corporate Credit Bonds. Meanwhile,

information disclosure needs to be standardized. Research needs to be conducted to enable

and facilitate disclose of ESG information, and explorations need to be made to establish a

green bond database and an environmental benefit information disclosure platform.

iv. To push forward see-through ABS supervision and standardized operation.

First, asset-level registration needs to be adopted for ABS. It is recommended to develop

standard disclosure forms for ABS, thus allowing standardized, electronic and

machine-readable disclosure, and enhancing transparency, investor protection and monitoring

of risks.

Second, standardization needs to be enhanced. Asset securitization and transfer of credit

assets are complementary ways to revitalize idle assets. It is advised to propel coordinated

development of these two operations, so that they can leverage on comparative advantages

and proper specialization to enhance efficiency of asset revitalization. An asset transfer

15

platform needs to be established, through which NPLs can be registered, transferred and

disposed of through standardized procedures. More standards need to be developed. In

accordance with the Guiding Opinions on Regulating the Asset Management Business of

Financial Institutions and the Rules for the Identification of Standardized Creditor’s Assets,

products enabling standardized transfer of credit assets need to be launched, a wider scope of

investors needs to be brought in, information disclosure need to be enhance and fair prices

need to be determined to boost market liquidity.

v. To expand cross-border use of RMB bonds and internationalization of RMB .

It is suggested to expand cross-border use of RMB assets, and reconstruct a more diverse and

balanced global collateral system. At present, global investors are seeking safe assets and the

mainstream collateral pool is facing deteriorating concentration risk. In this context, it is

imperative to promote cross-border use of RMB collateral, create a cross-border cooperation

ecosystem with RMB accepted as collateral in more markets, and try to develop an

international collateral service alliance so as to meet the needs of international investors for a

diversified collateral pool.

vi. To implement the requirements for safe development and base the financial market

on a solid footing.

The Fifth Plenary Session of the CPC 19th Central Committee proposed to make sure safe

development should run through the entire process of national development in all fields.

Financial market infrastructure is an important domain where the bond market can start to

pursue safe development. It is necessary to follow the guiding principles that the Central

Committee for Deepening Overall Reform proposed at its meeting for building a

well-organized, effectively-governed, advanced, reliable and flexible financial market

infrastructure system.

To be well-organized requires synergy between clear-cut positioning and connectivity, thus

forming a sound and orderly ecosystem. In this regard, a good reference is the ChinaBond

Solutions developed by CCDC, which features “centralized registration of ownership,

see-through oversight, multi-tiered services and win-win cooperation”. Effective governance

necessitates synergy between see-through supervision and respective regulatory functions,

thus forming an overall coordinated supervision system. A centralized registration and

depository system should cover the entire bond market and then be extended to other assets,

hence laying a solid foundation for safe development of the entire financial market. To be

advanced and reliable requires coordination of late-comer advantages and alignment with

international standards, thus forming an innovation-led business system. It is important to

avoid buckets effect by abstaining from simply putting different parts together. To be flexible

necessitates upholding bottom-line thinking and increasing institutional inclusiveness, thus

arriving at inclusive solutions. A unified back office needs to be built to cooperate with the

offshore front office, so as to extend the reach of policies and ensure safe development.