2020 retirement. what is 2020 retirement? an exclusive service designed to help you deliver...

TRANSCRIPT

2020 Retirement

What is 2020 Retirement?

An exclusive service designed to help you deliver tailored financial planning advice to your clients while giving you the freedom to focus on what you do best, managing investments.

As the relationship manager you decide what level of involvement you will have in the 2020 Financial Planning Process.

Why 2020 Retirement?

1. By 2020, the youngest baby boomers will turn age 60.– 1 in 5 Canadians will be retired or planning to retire within 5 years.

(source: Canada’s Aging Population, Health Canada Report)

2. 50% of small business owners plan to retire by 2020.– 1 in 2 people employed by the private sector work for a small business.

(source: 2004 CIBC Small Business Outlook Poll)

3. Less than 20% of people have a retirement plan.– 1 in 3 workers nearing retirement worry about having adequate income.

(Source: 2007 Statistics Canada survey)

Canada’s Aging Population

In 2001, one Canadian in eight was aged 65 years or over. By 2026, one Canadian in five will have reached age 65.

Source: Canada’s Aging Population, Health Canada Report

Small Business Owners

60% have no real plans for exiting their businesses.

50% are planning to retire by 2020.

40% plan to sell their businesses to outside interests.

Source: 2004 CIBC Small Business Outlook Poll

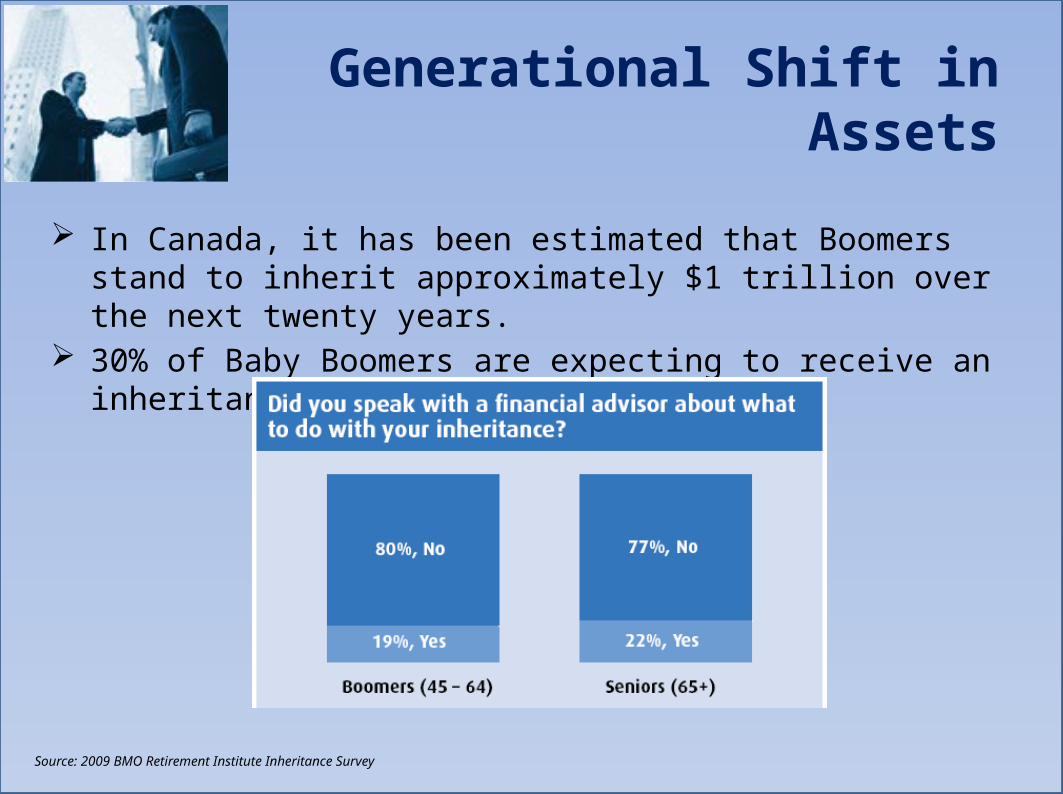

Generational Shift in Assets

In Canada, it has been estimated that Boomers stand to inherit approximately $1 trillion over the next twenty years.

30% of Baby Boomers are expecting to receive an inheritance.

Source: 2009 BMO Retirement Institute Inheritance Survey

Person

Corporation

Low Wealth High Wealth

Low Income Low IncomeHigh Income High Income

Operating Co. Holding Co.

Partners Family Fixed Assets Liquid Assets

Retirement PlanningFinancial Management Asset ProtectionWealth Creation

Business ContinuationShareholders’ Agreement Estate SuccessionEstate Succession

Financial profile may include: Significant home equity Has discretionary income Maximum RRSP contributions Tax liability at death

Planning needs may include: Retirement Funding Minimizing Income Taxes Insurance Needs Asset Protection

Financial profile may include: High debt service ratio Little discretionary income No investment savings Living beyond their means

Planning needs may include: Budgeting and Cash Flow Debt

Elimination/Restructuring Insurance Needs Emergency Funds/Savings

Financial profile may include: Little home equity Has some discretionary income Limited investment savings High Standard of Living

Planning needs may include: Retirement Funding Debt

Elimination/Restructuring Insurance Needs Education Funding

Financial profile may include: Significant home equity Significant discretionary

income Maximum RRSP contributions Tax liability at deathPlanning needs may include: Estate Succession/Liquidity Minimizing Income Taxes Insurance Needs Tax-efficient Investing

Planning needs may include: Buy-Sell Agreements Buy-Sell Funding Key-Man Protection Minimizing Estate Taxes Creditor Protection Shareholder Retirement

Planning needs may include: Succession Planning Succession Funding Key-Man Protection Minimizing Estate Taxes Creditor Protection Retirement Funding

Planning needs may include: Liquidity Needs Minimizing Estate Taxes Tax Funding Creditor Protection Retirement Funding Estate

Distribution/Windup

Planning needs may include: Tax-efficient Investing Minimizing Estate Taxes Tax Funding Creditor Protection Retirement Funding Estate

Distribution/Windup

FINANCIAL PLANNING NEEDS MATRIX

© 2010 Financial Plan Advantage Ltd. www.fpadvantage.com

Case Study #1$2,500 revenue

Situation:• Married couple in early 30s expecting their second child• Dad works for a company that installs industrial fire protection equipment• Mom set aside her career to raise their childrenProblem:• Mom lost her group benefits when she decided not to return to work• Dad’s group benefits do not provide the financial security they want• They never seem to have any money left over at the end of the monthSolution:• Helped them setup a budget to prioritize where their money goes• Applied for a family life and critical illness insurance plan• Consolidated several small RRSP plans

Case Study #2$6,500 revenue

Situation:• Married couple in early 40s with 2 young children• Incorporated professional working for US based oil service company• Wanted to make a career change, work in AlbertaProblem:• Very extravagate lifestyle compared to their income• Did not pay income taxes with any regularity (1 year deferrals)• No insurance if dad became sick, injured or died, no retirement plansSolution:• Reduced spending and redirected savings to pay income taxes when due• Used borrowed funds to take advantage of unused RRSP contribution limits• Applied for life and critical illness insurance to protect family

Case Study #3$30,000 revenue

Situation:• Married couple in early 50s with 2 children and 3 grandchildren• Sold small business for several million 2 years ago• Husband has 6 months remaining on his employment contractProblem:• Half of investments trapped inside holding company and subject to DSC• Protecting the assets they had accumulated was a primary concern• No real plan to generate income in retirementSolution:• Consolidate investment holdings and eliminate DSC over time• Prepared retirement plan with a focus on creating tax efficient income • Legacy planning inside holding company for tax efficient estate distribution.

Case Study #4$100,000 revenue

Situation:• Successful family owned business that was recently restructured for taxes• Dad is in his early 60s, active in the business and is the controlling shareholder• Son and daughter hold only growth shares and run day to day operationsProblem:• Son is married with 2 children, daughter is divorced with no children• The business represents a significant percentage of the family’s wealth• No succession plans in place for the growth shareholdersSolution:• Key person life and critical illness insurance on the son and daughter• Converted term life insurance on ex-business partner as an investment• Future considerations: leverage corporate insured annuity to minimize tax

Case Study #5$400,000 revenue

Situation:• Successful family owned business, parents early 60s, sons mid 30s• In the process of completing an estate freeze and setting up a family trust • Dad, mom and 2 sons all active in day to day operationsProblem:• Significant income tax liability associated with the parent’s ownership• The sons are not yet fully capable of managing the business on their own• Nature of the business requires significant operating line of creditSolution:• Joint last to die life insurance on dad and mom for tax funding (estate freeze)• Key man life insurance on 2 sons (business value protector)• Creditor life insurance on dad equal to operating line of credit (tax deductible)

2020 Planning Process

1. Initial Meeting2. Review & Engagement3. Recommendations4. Follow-up & Review

1. Share of Wallet2. Retention of Assets3. Increased Revenue

Whole Wealth Approach

2020 Marketing Materials:

1. Financial Planning Matrix2. Client Referral Sheet3. Our resume & contact information4. 2020 Planning Guide5. 2020 Client Supplement6. 2020 Retirement PowerPoint

www.fpadvantage.com/MRC/IAHome.aspx

• Complete a financial plan for yourself so that you will have a first-hand understanding of the process and benefits planning provides.

• Meet with us one-on-one so that we can get to know you better and to discuss how we can best help you to increase your revenues.

Next Steps

Thank You