2020 annual report - ktaxa.cdn.axa-contento-118412.eu

TRANSCRIPT

2020Annual

Report

One AXA

Courage

Integrity

Customer First

4 Core Values

2 Krungthai-AXA Life Annual Report 2020

Contents

4 Core Values 2Contents 3Awards 4Message from the Chairman 6Company’s Information 7Registered Shareholders 7Corperate Governance 8Composition of the Board of Directors 9KTAXA Executive & Management Committee 10Independent Auditor’s Report 11 Statutory Financial Statement 12

3Krungthai-AXA Life Annual Report 2020

Awards

Brand & Digital

Prime Minister Insurance Award• Outstanding Development

Insurance Asia Awards • Marketing initiative of the Year • Digital Initiative of the Year

International Finance Awards• Most Innovative Marketing Campaign in the Sector – Know You Can Insurance Asia News Award: Awards for Excellence• Digital Insurer of the Year

Corporate Responsibility & Diversity

The Global Good Governance Awards• Best CSR Initiatives• 3G Diversity

The Global Economics Award • Best CSR Insurance Company in Thailand

International Business Magazine Award• Best CSR Initiative Thailand

4 Krungthai-AXA Life Annual Report 20204

Service & Health

International Finance Awards• Best Customer Service Life Insurance

The Global Economics Award• Most Customer-Centric Life Insurance Company

International Business Magazine Award• Health Insurance Provider Thailand

Insurance Asia News: Awards for Excellence • Health Insurance of the Year

Google Cloud• G Suit Customer Appreciation Award

Business+ Product of the Year • Saving Insurance• Health Service

HR

Kincentric• Thailand Best Employer

HR Asia• Best Company to Work for in Asia

The Asia Corporate Excellence & Sustainability Awards • Top Workplace in Asia

LOMA• LOMA Excellent in Education Award (EIE)• LOMA Educational Achievement Award (EAA)

People with Disability Employment Award

5Krungthai-AXA Life Annual Report 2020 5

While 2020 was certainly challenging in many ways, it also showed how strong we are as a company – even in the toughest of times.

Despite such challenging circumstances, I am proud of our collective efforts in executing our strategies and delivering results. Throughout 2020, we continued to invest in future growth by further improving our services to customers, especially in digital Health & Protection. Through the launch of Telehealth, our customers can now access expert medical care online and also avail of our prescription delivery service from the comfort of their own homes. Furthermore, KTAXA expanded its Care Coordination program to provide clients with a more effective and cost-efficient health service and to help improve their overall wellbeing.

KTAXA’s commitment to its customer-first approach is reflected in its number one customer NPS score in the market, and winning over 20 award programmes, including ‘Health Insurance Service of the Year’ at the Business+ Magazine 2020 awards, ‘Best Customer Service Life Insurance Company’ at the International Finance Awards 2020, ‘Best CSR Insurance Company’ at Global Business Outlook Awards 2020 and ‘Thailand Best Employers 2020’ from Kincentric.

The role of KTAXA is not restricted to just our relationship with our clients. It goes further to our effective participation in numerous climate change projects and our active contribution to local communities and philanthropic activities. KTAXA as Green Insurer has strong moral compass and commitment to the environment has also helped launch an ambitious ‘Go Green’ climate change strategy that aims to support a more sustainable company and cleaner environment by 2022.

Finally, I’d like to thank our over 2 million customers for their trust and continued loyalty. I must also thank our Shareholder, Shareholder’s team, Chief Executive, and all our executive management teams. In a year filled with challenge it is a testament to their professionalism, their resilience and commitment that KTAXA has adapted and achieved so much, always focused on our core purpose ‘to act for human progress by protecting what matters. I know their positive attitude and commitment will continue to ensure the company’s growth and success through 2021 and beyond.

Message from the Chairman

Mr. Somchai BoonnamsiriChairman of Krungthai-AXA Life Insurance Public Company Limited

6 Krungthai-AXA Life Annual Report 2020

Company Name Krungthai-AXA Life Insurance Public Company Limited

Registrar No. 0107555000376

Address 9, G Tower Grand Rama 9 Floor 1,20-27, Rama 9 Road, Huai Khwang, Huai Khwang, Bangkok 10310

Contact Tel. 0-2044-4000 Fax 0-244-4032

Business Type Life Insurance

Establishment Date 12 June 1997

Registered Capital 1,355,000,000 Baht

The Paid-up Capital 1,355,000,000 Baht

Type of Share Ordinary share

Par Value 10 Baht per share

Registered Shareholders as at 31 March 2020

Name of Registered Shareholders No. of Shares %of Shares Held

1. Krung Thai Bank Public Company Limited 67,750,000 50%

2. National Mutual International Pty. Ltd. 60,974,996 45%

3. Tri Rattana Chart Company Limited 6,774,999 5%

4. Mr. Phisud Dejakaisaya 2 0%

5. Mr. Puangsan Xumsai Na Ayudhya 1 0%

6. Mr. Somkid Arayaskul 1 0%

7. Mr. Anuwat Kosol 1 0%

Company’s Information

7Krungthai-AXA Life Annual Report 2020

Number of directors Gender gap pay

Nationality Diversity Directors’ average age

4 nationalities are represented on the Board

4 50.92

Years old

13 0/0Male and female members

received the equal pay

Corperate Governance

Board Diversity

8 Krungthai-AXA Life Annual Report 2020

Name and Nationality Position within the Board of Directors Directors’ fee paid for 2020

Bonus for 2020

First appointment/Term of office

Mr. Somchai BoonnamsiriThai Nationality

• Chairman of the Board of Directors• Chairman of the Audit and Compliance

Committee• Chairman of the Nomination and Remuneration

Committee

740,000 142,200 April 2019 Annual General Meeting/ 2022 Annual General Meeting

Ms. Ratchada PiyatassikulThai Nationality

• Director of the Board of Directors• Member of the Risk Management Committee

250,000 67,150 April 2017 Annual General Meeting/ 2023 Annual General Meeting

Mr. Rawin BoonyanusasnaThai Nationality

• Director of the Board of Directors• Chairman of the Investment Committee

420,000 150,100 April 2017 Annual General Meeting/2023 Annual General Meeting

Mr. Pichit JongsaliswangThai Nationality

• Director of the Board of Directors 140,000 - March 2020 Board of Directors Meeting / 2022 Annual General Meeting

Professor Dr Kriengsak ChareonwongsakThai Nationality

• Director of the Board of Directors• Chairman of the Risk Management Committee• Member of the Audit and Compliance

Committee• Member of the Investment Committee• Member of the Nomination and Remuneration

Committee

410,000 161,950 April 2018 Annual General Meeting/ 2021 Annual General Meeting

Ms. Wimol ChatameenaThai Nationality

• Director of the Board of Directors 200,000 - January 2020 Board of Directors Meeting / 2022 Annual General Meeting

Mr. Akarat Na RanongThai Nationality

• Director of the Board of Directors• Member of the Investment Committee• Member of the Nomination and Remuneration

Committee

320,000 94,800 April 2018 Annual General Meeting/ 2021 Annual General Meeting

Mrs. Sally Joy O’Hara*Australian Nationality

• Director of the Board of Directors• Member of the Risk Management Committee

- - April 2019 Annual General Meeting/ 2022 Annual General Meeting

Ms. Bubphawadee Owararinth*Thai Nationality

• Director of the Board of Directors - - February 2018 Board of Directors Meeting /2023 Annual General Meeting

Mr. Laurent Julien Cholvy*French Nationality

• Director of the Board of Directors• Member of the Risk Management Committee• Member of the Investment Committee

- - July 2019 Board of Directors Meeting / 2021 Annual General Meeting

Mrs. Sen Hang Cindy Tong*Canadian Nationality

• Director of the Board of Directors• Member of the Audit and Compliance

Committee• Member of the Nomination and Remuneration

Committee

- - February 2018 Board of Directors Meeting /2023 Annual General Meeting/

Mr. Sirote SwasdipanichThai Nationality

• Chairman of the Board of Directors• Chairman of the Audit and Compliance

Committee• Chairman of the Nomination and Remuneration

Committee

- 165,900 Retire by rotation in 2019 Annual General Meeting

Mr. Chainarong Eursithichai*Thai Nationality

• Director of the Board of Directors - - Resigned on 24 January 2020

Mr. Chanvit RungruangladaThai Nationality

• Director of the Board of Directors 60,000 47,400 Resigned on 24 March 2020

Mr. Chinavais SarasasThai Nationality

• Director of the Board of Directors 90,000 47,400 Retire by rotation in 2020 Annual General Meeting

* The Company has no policy to pay the remuneration of directors to the directors who are employees of the Company or AXA group.

Fo

rmer

Dir

ecto

rs

Composition of the Board of Directorson 31 December 2020

9Krungthai-AXA Life Annual Report 2020

Sally

O'H

ara

Chie

f Exe

cutiv

e O

ffice

r

Vaca

ntCh

ief P

rodu

ct O

ffice

r

Que

enie

Choi

Chie

f Hea

lthDe

velo

pmen

t Offi

cer

Patt

arap

olPa

rin

Chie

f Inv

estm

ent

& AL

M O

ffice

r

Bong

koch

Sook

moo

lCh

ief C

usto

mer

Ca

re O

ffice

r

Sara

swad

eeKu

pata

pong

Chie

f Hum

an R

esou

rces

Busi

ness

Par

tner

Offi

cer

Supa

porn

Kuna

nont

haw

atCh

ief

Und

erw

ritin

g O

ffice

r

Suka

nya

Thei

ngte

erat

hum

Chie

f Life

& H

ealth

Ope

ratio

ns O

ffice

r

Nap

hats

acho

lM

eeso

onto

rnDe

puty

Chi

ef

Fina

ncia

l Offi

cer

Nut

taw

ooth

TIya

wat

tana

roj

Chie

f Dis

trib

utio

n Tr

aini

ng O

ffice

r

Vaca

ntCh

ief B

anca

ssur

ance

O

ffice

r

Dr.U

qkri

tSr

idar

omon

tCh

ief A

genc

y O

ffice

r

Met

hit

Com

erCh

ief I

nfor

mat

ion

Offi

cer

Chai

naro

ngEu

rsith

icha

iCh

ief D

istr

ibut

ion

Offi

cer

Laur

ent

Chol

vyCh

ief F

inan

cial

Offi

cer

Paka

wip

aCh

aroe

ntra

Chie

f Cus

tom

er O

ffice

r

Bubp

haw

adee

Ow

arar

inth

Chie

f Peo

ple

Offi

cer

Yahy

a Ah

mad

Chie

f Ris

k O

ffice

r

Vaca

ntCh

ief

Actu

ary

Offi

cer

Vaca

ntCh

ief

Actu

ary

Offi

cer

Tipa

pan

Feun

gpun

yaCh

ief O

pera

ting

Offi

cer

KT

AX

A E

xec

uti

ve &

Man

agem

ent

Co

mm

itte

e

10 Krungthai-AXA Life Annual Report 2020

Sally

O'H

ara

Chie

f Exe

cutiv

e O

ffice

r

Vaca

ntCh

ief P

rodu

ct O

ffice

r

Que

enie

Choi

Chie

f Hea

lthDe

velo

pmen

t Offi

cer

Patt

arap

olPa

rin

Chie

f Inv

estm

ent

& AL

M O

ffice

r

Bong

koch

Sook

moo

lCh

ief C

usto

mer

Ca

re O

ffice

r

Sara

swad

eeKu

pata

pong

Chie

f Hum

an R

esou

rces

Busi

ness

Par

tner

Offi

cer

Supa

porn

Kuna

nont

haw

atCh

ief

Und

erw

ritin

g O

ffice

r

Suka

nya

Thei

ngte

erat

hum

Chie

f Life

& H

ealth

Ope

ratio

ns O

ffice

r

Nap

hats

acho

lM

eeso

onto

rnDe

puty

Chi

ef

Fina

ncia

l Offi

cer

Nut

taw

ooth

TIya

wat

tana

roj

Chie

f Dis

trib

utio

n Tr

aini

ng O

ffice

r

Vaca

ntCh

ief B

anca

ssur

ance

O

ffice

r

Dr.U

qkri

tSr

idar

omon

tCh

ief A

genc

y O

ffice

r

Met

hit

Com

erCh

ief I

nfor

mat

ion

Offi

cer

Chai

naro

ngEu

rsith

icha

iCh

ief D

istr

ibut

ion

Offi

cer

Laur

ent

Chol

vyCh

ief F

inan

cial

Offi

cer

Paka

wip

aCh

aroe

ntra

Chie

f Cus

tom

er O

ffice

r

Bubp

haw

adee

Ow

arar

inth

Chie

f Peo

ple

Offi

cer

Yahy

a Ah

mad

Chie

f Ris

k O

ffice

r

Vaca

ntCh

ief

Actu

ary

Offi

cer

Vaca

ntCh

ief

Actu

ary

Offi

cer

Tipa

pan

Feun

gpun

yaCh

ief O

pera

ting

Offi

cer

To the Shareholders of Krungthai-AXA Life Insurance Public Company Limited

My opinionIn my opinion, the financial statements present fairly, in all material respects, the financial position of Krungthai-AXA Life Insurance Public Company Limited (the “Company”) as at 31 December 2020, and its financial performance and its cash flows for the year then ended in accordance with Thai Financial Reporting Standards (“TFRS”).

What I have auditedThe Company’s financial statements comprise:

• the statement of financial position as at 31 December 2020;• the statement of comprehensive income for the year then ended;• the statement of changes in equity for the year then ended;• the statement of cash flows for the year then ended; and• the notes to the financial statements, which include significant

accounting policies and other explanatory information.

Basis for opinion

I conducted my audit in accordance with Thai Standards on Auditing (TSAs). My responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the financial statements section of my report. I am independent of the Company in accordance with the Code of Ethics for Professional Accountants issued by the Federation of Accounting Professions together with the ethical requirements that are relevant to my audit of the financial statements, and I have fulfilled my other ethical responsibilities in accordance with these requirements. I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my opinion.

Responsibilities of management for the financial statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with TFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and usingthe going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

The audit committee assists the management in discharging their responsibilities for overseeing the Company’s financial reporting process.

Auditor’s responsibilities for the audit of the financial statements My objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes my opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with TSAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with TSAs, I exercise professional judgment and maintain professional scepticism throughout the audit. I also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for my opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If I conclude that a material uncertainty exists, I am required to draw attention in my auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify my opinion. My conclusions are based on the audit evidence obtained up to the date of my auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

I communicate with the audit committee regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that I identify during my audit.

I also provide the audit committee with a statement that I have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on my independence, and where applicable, related safeguards.

PricewaterhouseCoopers ABAS Ltd.

Anothai LeekitwattanaCertified Public Accountant (Thailand) No. 3442Bangkok3 March 2021

Independent Auditor’s Report

11Krungthai-AXA Life Annual Report 2020

KRUNGTHAI-AXA LIFE INSURANCE PUBLIC COMPANY LIMITED

STATUTORY FINANCIAL STATEMENTS31 DECEMBER 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Financial PositionAs at 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Assets

Cash and cash equivalents 9, 33 3,669,030 3,866,059Premium receivable 10 1,585,630 1,654,581Accrued investment income 33 1,584,571 1,900,651Amounts due from reinsurance 11 109,600 141,811Derivative assets 12 3,124,560 4,403,329Investments

Investments in securities 13, 33, 34 304,951,619 297,329,292Loans and accrued interest receivables 14 13,974,164 12,693,240

Assets held to cover linked liabilities 15 10,827,714 10,281,684Leasehold improvements and equipment 16 332,938 341,487Right-of-use assets 17 640,348 -Intangible assets 18 319,656 382,629Agency security fund 870,408 790,469Accounts receivable - Investments 111,073 153,932Other assets 19, 33 148,912 212,795

Total assets 342,250,223 334,151,959

………………………..………………………………………… Directors

The accompanying notes are an integral part of these financial statements.

12 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Financial PositionAs at 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Assets

Cash and cash equivalents 9, 33 3,669,030 3,866,059Premium receivable 10 1,585,630 1,654,581Accrued investment income 33 1,584,571 1,900,651Amounts due from reinsurance 11 109,600 141,811Derivative assets 12 3,124,560 4,403,329Investments

Investments in securities 13, 33, 34 304,951,619 297,329,292Loans and accrued interest receivables 14 13,974,164 12,693,240

Assets held to cover linked liabilities 15 10,827,714 10,281,684Leasehold improvements and equipment 16 332,938 341,487Right-of-use assets 17 640,348 -Intangible assets 18 319,656 382,629Agency security fund 870,408 790,469Accounts receivable - Investments 111,073 153,932Other assets 19, 33 148,912 212,795

Total assets 342,250,223 334,151,959

………………………..………………………………………… Directors

The accompanying notes are an integral part of these financial statements.

13Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Financial Position (Cont’d)As at 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Liabilities and equity

Liabilities

Insurance contract liabilities 20 269,338,052 255,621,493Investment contract liabilities 21 10,833,090 10,289,230Amount due to reinsurance 22, 33 203,367 186,629Derivative liabilities 12 529,550 182,364Income tax payable 71,954 4,057Employee benefits obligation 23 181,963 139,237Deferred tax liabilities 24 6,824,689 8,348,724Lease liabilities 25 697,743 -Agency security fund 870,408 790,469Accrued expenses 33 2,098,557 2,281,542Accounts payable - Investments 90,541 300,587Other liabilities 26, 33 2,877,193 4,682,028

Total liabilities 294,617,107 282,826,360

Equity

Share capitalRegistered

135,500,000 ordinary shares of Baht 10 per share 1,355,000 1,355,000

Issued and fully paid-up135,500,000 ordinary shares of

Baht 10 per share 1,355,000 1,355,000Retained earnings

Appropriated - legal reserve 135,500 135,500Unappropriated 18,883,313 17,340,389

27,259,303 32,494,710

Total equity 47,633,116 51,325,599

Total liabilities and equity 342,250,223 334,151,959

The accompanying notes are an integral part of these financial statements.

Other component of equity

Krungthai-AXA Life Insurance Public Company Limited Statement of Comprehensive IncomeFor the year ended 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Revenues

Gross written premium 53,103,546 58,105,092Less Ceded premium 33 (314,148) (319,593)

Net written premium 52,789,398 57,785,499(Less) Net change in unearned premium reserve (309,163) (240,213)

Net earned premium 52,480,235 57,545,286Fee and commission income 33 353,112 340,041Investment income 33 10,078,705 9,748,955Gains on investments 2,180,602 1,531,659Fair value losses (220,220) (90,817)Other income 47,979 56,933

Total revenues 64,920,413 69,132,057

Expenses

Change in long-term technical reserve 13,481,247 20,304,634Gross benefits and claims paid 37,782,600 34,045,149

33 (170,662) (354,123)

Net benefits and claims paid 37,611,938 33,691,026Commissions and brokerages 7,092,315 8,262,519Other underwriting expenses 510,567 708,284Operating expenses 28, 33 3,989,939 3,736,973Finance cost 25 22,034 -Expected credit loss 36 132,405 -Other expenses 1,477 543

Total expenses 62,841,922 66,703,979

Profit before income tax 2,078,491 2,428,078Income tax expense 30 360,149 546,952

Net profit 1,718,342 1,881,126

The accompanying notes are an integral part of these financial statements.

(Less) Benefits and claims paid recovered from reinsurers

14 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Financial Position (Cont’d)As at 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Liabilities and equity

Liabilities

Insurance contract liabilities 20 269,338,052 255,621,493Investment contract liabilities 21 10,833,090 10,289,230Amount due to reinsurance 22, 33 203,367 186,629Derivative liabilities 12 529,550 182,364Income tax payable 71,954 4,057Employee benefits obligation 23 181,963 139,237Deferred tax liabilities 24 6,824,689 8,348,724Lease liabilities 25 697,743 -Agency security fund 870,408 790,469Accrued expenses 33 2,098,557 2,281,542Accounts payable - Investments 90,541 300,587Other liabilities 26, 33 2,877,193 4,682,028

Total liabilities 294,617,107 282,826,360

Equity

Share capitalRegistered

135,500,000 ordinary shares of Baht 10 per share 1,355,000 1,355,000

Issued and fully paid-up135,500,000 ordinary shares of

Baht 10 per share 1,355,000 1,355,000Retained earnings

Appropriated - legal reserve 135,500 135,500Unappropriated 18,883,313 17,340,389

27,259,303 32,494,710

Total equity 47,633,116 51,325,599

Total liabilities and equity 342,250,223 334,151,959

The accompanying notes are an integral part of these financial statements.

Other component of equity

Krungthai-AXA Life Insurance Public Company Limited Statement of Comprehensive IncomeFor the year ended 31 December 2020

2020 2019Notes Thousand Baht Thousand Baht

Revenues

Gross written premium 53,103,546 58,105,092Less Ceded premium 33 (314,148) (319,593)

Net written premium 52,789,398 57,785,499(Less) Net change in unearned premium reserve (309,163) (240,213)

Net earned premium 52,480,235 57,545,286Fee and commission income 33 353,112 340,041Investment income 33 10,078,705 9,748,955Gains on investments 2,180,602 1,531,659Fair value losses (220,220) (90,817)Other income 47,979 56,933

Total revenues 64,920,413 69,132,057

Expenses

Change in long-term technical reserve 13,481,247 20,304,634Gross benefits and claims paid 37,782,600 34,045,149

33 (170,662) (354,123)

Net benefits and claims paid 37,611,938 33,691,026Commissions and brokerages 7,092,315 8,262,519Other underwriting expenses 510,567 708,284Operating expenses 28, 33 3,989,939 3,736,973Finance cost 25 22,034 -Expected credit loss 36 132,405 -Other expenses 1,477 543

Total expenses 62,841,922 66,703,979

Profit before income tax 2,078,491 2,428,078Income tax expense 30 360,149 546,952

Net profit 1,718,342 1,881,126

The accompanying notes are an integral part of these financial statements.

(Less) Benefits and claims paid recovered from reinsurers

15Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Comprehensive Income (Cont’d)For the year ended 31 December 2020

2020 2019Note Thousand Baht Thousand Baht

Other comprehensive income (loss)Items that will be reclassified subsequently to profit or lossGains (losses) from change in value of investments measured at fair value through other comprehensive income (3,356,118) 31,853,139Gains (losses) on cash flow hedges (1,206,189) 1,676,051Losses on deferred cost of hedging (128,177) -Items in other comprehensive income transferred

to profit or loss (2,060,864) (1,531,659)Income tax on item that will be reclassified subsequently

to profit or loss 1,350,270 (6,399,506)

Total items that will be reclassified subsequentlyto profit or loss (5,401,078) 25,598,025

Items that will not be reclassified subsequently to profit or lossActuarial loss on employee benefits obligation (16,772) (10,793)Income tax on item that will not be reclassified subsequently

to profit or loss 7,025 -

Total items that will not be reclassified subsequentlyto profit or loss (9,747) (10,793)

Other comprehensive income (loss) for the year, net of tax (5,410,825) 25,587,232

Total comprehensive income (loss) for the year (3,692,483) 27,468,358

Basic earnings per share (Baht) 32

Basic earning per share 12.68 13.88

The accompanying notes are an integral part of these financial statements.

Kru

ngth

ai-A

XA L

ife In

sura

nce

Publ

ic C

ompa

ny L

imite

dSt

atem

ent o

f Cha

nges

in E

quity

For t

he y

ear e

nded

31

Dec

embe

r 202

0

Unr

ealis

ed g

ains

(los

ses)

on c

hang

es in

val

ue o

fin

vest

men

ts m

easu

red

atG

ain

(loss

) on

Gai

n (lo

ss) o

nAc

tuar

ial l

oss

onIs

sued

and

fair

valu

e th

roug

h ot

her

cash

flow

defe

rred

cos

t e

mpl

oyee

paid

-up

Ret

aine

dco

mpr

ehen

sive

inco

me,

hedg

es,

of h

edgi

ng,

bene

fits

oblig

atio

n,sh

are

capi

tal

ear

ning

s n

et o

f tax

net

of t

ax n

et o

f tax

net

of t

axTo

tal

Tho

usan

d B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Beg

inni

ng b

alan

ce a

s at

1 J

anua

ry 2

020

1,35

5,00

017

,475

,889

30,9

19,0

731,

593,

989

-(1

8,35

2)51

,325

,599

Ret

rosp

ectiv

e ad

just

men

t fro

m a

dopt

ion

of n

ew

finan

cial

repo

rting

sta

ndar

ds (N

ote

4)-

(175

,418

)18

2,21

1(1

87,5

04)

180,

711

--

Beg

inni

ng b

alan

ce a

fter a

djus

tmen

t1,

355,

000

17,3

00,4

7131

,101

,284

1,40

6,48

518

0,71

1(1

8,35

2)51

,325

,599

Net

pro

fit-

1,71

8,34

2-

--

-1,

718,

342

Unr

ealis

ed lo

ss o

n ch

ange

s in

val

ue o

f inv

estm

ents

mea

sure

dat

fair

valu

e th

roug

h ot

her c

ompr

ehen

sive

inco

me,

net

of t

ax-

-(2

,684

,894

)-

--

(2,6

84,8

94)

Loss

on

cash

flow

hed

ges,

net

of t

ax-

--

(964

,951

)-

-(9

64,9

51)

Loss

on

defe

rred

cost

of h

edgi

ng, n

et o

f tax

--

--

(102

,542

)-

(102

,542

)Ite

ms

in o

ther

com

preh

ensi

ve in

com

e tra

nsfe

rred

topr

ofit

or lo

ss, n

et o

f tax

--

(1,9

08,8

49)

261,

010

(852

)-

(1,6

48,6

91)

Actu

aria

l los

s on

em

ploy

ee b

enef

its o

blig

atio

n, n

et o

f tax

--

--

-(9

,747

)(9

,747

)

Endi

ng b

alan

ce a

s at

31

Dec

embe

r 202

01,

355,

000

19,0

18,8

1326

,507

,541

702,

544

77,3

17(2

8,09

9)47

,633

,116

Beg

inni

ng b

alan

ce a

s at

1 J

anua

ry 2

019

1,35

5,00

015

,594

,763

6,66

1,88

925

3,14

8-

(7,5

59)

23,8

57,2

41N

et p

rofit

-1,

881,

126

--

--

1,88

1,12

6U

nrea

lised

gai

n on

cha

nges

in fa

ir va

lue

of a

vaila

ble-

for-s

ale

in

vest

men

ts, n

et o

f tax

--

25,4

82,5

11-

--

25,4

82,5

11G

ain

on c

ash

flow

hed

ge, n

et o

f tax

--

-1,

340,

841

--

1,34

0,84

1Ite

ms

in o

ther

com

preh

ensi

ve in

com

e tra

nsfe

rred

topr

ofit

or lo

ss, n

et o

f tax

--

(1,2

25,3

27)

--

-(1

,225

,327

)Ac

tuar

ial l

oss

on e

mpl

oyee

ben

efits

obl

igat

ion,

net

of t

ax-

--

--

(10,

793)

(10,

793)

Endi

ng b

alan

ce a

s at

31

Dec

embe

r 201

91,

355,

000

17,4

75,8

8930

,919

,073

1,59

3,98

9-

(18,

352)

51,3

25,5

99

The

acco

mpa

nyin

g no

tes

are

an in

tegr

al p

art o

f the

se fi

nanc

ial s

tate

men

ts.

Oth

er c

ompo

nent

s of

equ

ity

16 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company Limited Statement of Comprehensive Income (Cont’d)For the year ended 31 December 2020

2020 2019Note Thousand Baht Thousand Baht

Other comprehensive income (loss)Items that will be reclassified subsequently to profit or lossGains (losses) from change in value of investments measured at fair value through other comprehensive income (3,356,118) 31,853,139Gains (losses) on cash flow hedges (1,206,189) 1,676,051Losses on deferred cost of hedging (128,177) -Items in other comprehensive income transferred

to profit or loss (2,060,864) (1,531,659)Income tax on item that will be reclassified subsequently

to profit or loss 1,350,270 (6,399,506)

Total items that will be reclassified subsequentlyto profit or loss (5,401,078) 25,598,025

Items that will not be reclassified subsequently to profit or lossActuarial loss on employee benefits obligation (16,772) (10,793)Income tax on item that will not be reclassified subsequently

to profit or loss 7,025 -

Total items that will not be reclassified subsequentlyto profit or loss (9,747) (10,793)

Other comprehensive income (loss) for the year, net of tax (5,410,825) 25,587,232

Total comprehensive income (loss) for the year (3,692,483) 27,468,358

Basic earnings per share (Baht) 32

Basic earning per share 12.68 13.88

The accompanying notes are an integral part of these financial statements.

Kru

ngth

ai-A

XA L

ife In

sura

nce

Publ

ic C

ompa

ny L

imite

dSt

atem

ent o

f Cha

nges

in E

quity

For t

he y

ear e

nded

31

Dec

embe

r 202

0

Unr

ealis

ed g

ains

(los

ses)

on c

hang

es in

val

ue o

fin

vest

men

ts m

easu

red

atG

ain

(loss

) on

Gai

n (lo

ss) o

nAc

tuar

ial l

oss

onIs

sued

and

fair

valu

e th

roug

h ot

her

cash

flow

defe

rred

cos

t e

mpl

oyee

paid

-up

Ret

aine

dco

mpr

ehen

sive

inco

me,

hedg

es,

of h

edgi

ng,

bene

fits

oblig

atio

n,sh

are

capi

tal

ear

ning

s n

et o

f tax

net

of t

ax n

et o

f tax

net

of t

axTo

tal

Tho

usan

d B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Thou

sand

Bah

tTh

ousa

nd B

aht

Beg

inni

ng b

alan

ce a

s at

1 J

anua

ry 2

020

1,35

5,00

017

,475

,889

30,9

19,0

731,

593,

989

-(1

8,35

2)51

,325

,599

Ret

rosp

ectiv

e ad

just

men

t fro

m a

dopt

ion

of n

ew

finan

cial

repo

rting

sta

ndar

ds (N

ote

4)-

(175

,418

)18

2,21

1(1

87,5

04)

180,

711

--

Beg

inni

ng b

alan

ce a

fter a

djus

tmen

t1,

355,

000

17,3

00,4

7131

,101

,284

1,40

6,48

518

0,71

1(1

8,35

2)51

,325

,599

Net

pro

fit-

1,71

8,34

2-

--

-1,

718,

342

Unr

ealis

ed lo

ss o

n ch

ange

s in

val

ue o

f inv

estm

ents

mea

sure

dat

fair

valu

e th

roug

h ot

her c

ompr

ehen

sive

inco

me,

net

of t

ax-

-(2

,684

,894

)-

--

(2,6

84,8

94)

Loss

on

cash

flow

hed

ges,

net

of t

ax-

--

(964

,951

)-

-(9

64,9

51)

Loss

on

defe

rred

cost

of h

edgi

ng, n

et o

f tax

--

--

(102

,542

)-

(102

,542

)Ite

ms

in o

ther

com

preh

ensi

ve in

com

e tra

nsfe

rred

topr

ofit

or lo

ss, n

et o

f tax

--

(1,9

08,8

49)

261,

010

(852

)-

(1,6

48,6

91)

Actu

aria

l los

s on

em

ploy

ee b

enef

its o

blig

atio

n, n

et o

f tax

--

--

-(9

,747

)(9

,747

)

Endi

ng b

alan

ce a

s at

31

Dec

embe

r 202

01,

355,

000

19,0

18,8

1326

,507

,541

702,

544

77,3

17(2

8,09

9)47

,633

,116

Beg

inni

ng b

alan

ce a

s at

1 J

anua

ry 2

019

1,35

5,00

015

,594

,763

6,66

1,88

925

3,14

8-

(7,5

59)

23,8

57,2

41N

et p

rofit

-1,

881,

126

--

--

1,88

1,12

6U

nrea

lised

gai

n on

cha

nges

in fa

ir va

lue

of a

vaila

ble-

for-s

ale

in

vest

men

ts, n

et o

f tax

--

25,4

82,5

11-

--

25,4

82,5

11G

ain

on c

ash

flow

hed

ge, n

et o

f tax

--

-1,

340,

841

--

1,34

0,84

1Ite

ms

in o

ther

com

preh

ensi

ve in

com

e tra

nsfe

rred

topr

ofit

or lo

ss, n

et o

f tax

--

(1,2

25,3

27)

--

-(1

,225

,327

)Ac

tuar

ial l

oss

on e

mpl

oyee

ben

efits

obl

igat

ion,

net

of t

ax-

--

--

(10,

793)

(10,

793)

Endi

ng b

alan

ce a

s at

31

Dec

embe

r 201

91,

355,

000

17,4

75,8

8930

,919

,073

1,59

3,98

9-

(18,

352)

51,3

25,5

99

The

acco

mpa

nyin

g no

tes

are

an in

tegr

al p

art o

f the

se fi

nanc

ial s

tate

men

ts.

Oth

er c

ompo

nent

s of

equ

ity

17Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedStatement of Cash FlowsFor the year ended 31 December 2020

2020 2019Thousand Baht Thousand Baht

Cash flows provided by (used in) operating activitiesWritten premium from direct insurance 52,600,677 57,828,625Cash received from investment contract liabilities 1,630,445 932,648Cash paid for investment contract liabilities (540,747) (569,461)Amount paid from reinsurance (333,433) (201,262)Interest income 9,085,260 9,088,473Dividend income 957,413 859,513Other income 69,719 108,941Gross benefits and claims paid from direct insurance (37,702,762) (33,040,661)Commissions and brokerages from direct insurance (7,337,109) (7,901,894)Other underwriting expenses (594,882) (708,284)Operating expenses (3,301,102) (3,512,499)Other expenses (1,475) (488)Income tax expense (458,993) (185,781)Cash received from sales investment in securities 118,057,633 127,337,625Cash paid to purchase investment in securities (131,224,115) (149,046,765)Loans (709,104) (977,079)Deposits at banks 223 249

Net cash provided by operating activities 197,648 11,900

Cash flows provided by (used in) investing activitiesCash inflows :

Leasehold improvements and equipment - 68

Net cash provided by investing activities - 68

Cash outflows :Leasehold improvements and equipment (138,041) (24,700)Computer software (93,026) (75,042)

Net cash used in investing activities (231,067) (99,742)

Net cash flows used in investing activities (231,067) (99,674)

The accompanying notes are an integral part of these financial statements.

Krungthai-AXA Life Insurance Public Company LimitedStatement of Cash FlowsFor the year ended 31 December 2020

2020 2019Thousand Baht Thousand Baht

Cash flows provided by (used in) financing activitiesCash outflows :

Cash paid for lease liabilities (163,610) -

Net cash used in financing activities (163,610) -

Net cash used in financing activities (163,610) -

Net decrease in cash and cash equivalents (197,029) (87,774)Cash and cash equivalents at beginning of the year 3,866,059 3,953,833

Cash and cash equivalents at end of the year 3,669,030 3,866,059

Non-cash transactions

The Company had the significant non-cash transactions as follows:

Payable from purchase of leasehold improvementsand computer software 33,492 36,387

The accompanying notes are an integral part of these financial statements.

18 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedStatement of Cash FlowsFor the year ended 31 December 2020

2020 2019Thousand Baht Thousand Baht

Cash flows provided by (used in) operating activitiesWritten premium from direct insurance 52,600,677 57,828,625Cash received from investment contract liabilities 1,630,445 932,648Cash paid for investment contract liabilities (540,747) (569,461)Amount paid from reinsurance (333,433) (201,262)Interest income 9,085,260 9,088,473Dividend income 957,413 859,513Other income 69,719 108,941Gross benefits and claims paid from direct insurance (37,702,762) (33,040,661)Commissions and brokerages from direct insurance (7,337,109) (7,901,894)Other underwriting expenses (594,882) (708,284)Operating expenses (3,301,102) (3,512,499)Other expenses (1,475) (488)Income tax expense (458,993) (185,781)Cash received from sales investment in securities 118,057,633 127,337,625Cash paid to purchase investment in securities (131,224,115) (149,046,765)Loans (709,104) (977,079)Deposits at banks 223 249

Net cash provided by operating activities 197,648 11,900

Cash flows provided by (used in) investing activitiesCash inflows :

Leasehold improvements and equipment - 68

Net cash provided by investing activities - 68

Cash outflows :Leasehold improvements and equipment (138,041) (24,700)Computer software (93,026) (75,042)

Net cash used in investing activities (231,067) (99,742)

Net cash flows used in investing activities (231,067) (99,674)

The accompanying notes are an integral part of these financial statements.

Krungthai-AXA Life Insurance Public Company LimitedStatement of Cash FlowsFor the year ended 31 December 2020

2020 2019Thousand Baht Thousand Baht

Cash flows provided by (used in) financing activitiesCash outflows :

Cash paid for lease liabilities (163,610) -

Net cash used in financing activities (163,610) -

Net cash used in financing activities (163,610) -

Net decrease in cash and cash equivalents (197,029) (87,774)Cash and cash equivalents at beginning of the year 3,866,059 3,953,833

Cash and cash equivalents at end of the year 3,669,030 3,866,059

Non-cash transactions

The Company had the significant non-cash transactions as follows:

Payable from purchase of leasehold improvementsand computer software 33,492 36,387

The accompanying notes are an integral part of these financial statements.

19Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

1 General information

Krungthai-AXA Life Insurance Public Company Limited (“the Company”) was registered as a limited company under the law of Thailand on 12 June 1997. The Company has changed to public company limited on 1 October 2012. The address of its registered office is as follows:

9, G Tower Grand Rama 9, Floor 1, 20-27, Rama 9 Road, Huai Khwang, Huai Khwang, Bangkok 10310.

The principal business operation of the Company is to provide life insurance including reinsurance services in Thailand.

The major shareholders of the Company are Krungthai Bank Public Company Limited and National Mutual International Pty. Ltd.

The financial statements have been approved by the Company’s management on 3 March 2021.

2 Basis of preparation

These financial statements are prepared in accordance with Thai Generally Accepted Accounting Principles under the Accounting Act B.E. 2543, being those Thai Financial Reporting Standards (TFRS) issued under the Accounting Profession Act B.E. 2547. In addition, the financial statements presentation are based on the formats of life insurance financial statements attached in an Office of Insurance Commission’s notification “Principle, methodology, condition and timing for preparation,submission and reporting of financial statements and operation performance for life insurance company (No.2) B.E. 2562” dated on 4 April 2019 (‘OIC Notification’).

The financial statements have been prepared under the historical cost convention except as disclosed in the accounting policies below.

The preparation of financial statements in conformity with Thai Generally Accepted Accounting Principles requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Company’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements are disclosed in Note 8.

An English version of the financial statements has been prepared from the financial statements that are in the Thai language. In the event of a conflict or a difference in interpretation between the two languages, the Thai language financial statements shall prevail.

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards

3.1 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2020 and are relevant to the Company

a) Financial instruments

The new financial standards related to financial instruments are as follows

TAS 32 Financial instruments: PresentationTFRS 7 Financial instruments: DisclosuresTFRS 9 Financial instrumentsTFRIC 16 Hedges of a net investment in a foreign operationTFRIC 19 Extinguishing financial liabilities with equity instrumentsThe Accounting

GuidanceFinancial instruments and disclosures for insurance companies’

accounting guidance

The new financial reporting standards related to financial instruments and TFAC Accounting Guidance introduce new classification and measurement requirements for financial instruments as well as provide derecognition guidance on financial assets and financial liabilities. The new guidance also provides an option for the Company to apply hedge accounting to reduce accounting mismatch between hedged item and hedging instrument. In addition, the new rule provides detailed guidance on financial instruments issued by the Company whether it is a liability or an equity. Among other things, they require extensive disclosure on financial instruments and related risks.

The new classification requirements of financial assets under TFRS9 require the Company to assess both i) business model for holding the financial assets; and ii) cash flow characteristics of the asset whether the contractual cash flows represent solely payments of principal and interest (SPPI). The classification affects the financial assets’ measurement. The new standard requires assessment of impairment of financial assets as well as contract assets and recognition of expected credit loss from initial recognition.

On 1 January 2020, the Company passes criteria of temporarily exemption from TFRS 9 Financial Instruments and TFRS 7 Financial Instruments: Disclosures under TFRS 4 (revised 2018) Insurance Contracts. The Company is eligible to apply the Accounting Guidance in relation to financial instruments and disclosure for insurance companies (‘The Accounting Guidance’) as the Company has not previously applied TFRS 9 Financial Instrument and the Company’s activities are predominantly connected with insurance business, based on the eligibility assessment that the total carrying amount of liabilities connected with insurance within the scope of TFRS 4 of Baht 210,741.8 million as at 1 January 2018 is greater than 90% of the total carrying amount of all its liabilities. Certain liabilities connected with insurance included investment contract liabilities measured at fair value through profit or loss of Baht 2,672.5 million and certain deferred tax liabilities of Baht 3,094.7 million.

20 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards

3.1 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2020 and are relevant to the Company

a) Financial instruments

The new financial standards related to financial instruments are as follows

TAS 32 Financial instruments: PresentationTFRS 7 Financial instruments: DisclosuresTFRS 9 Financial instrumentsTFRIC 16 Hedges of a net investment in a foreign operationTFRIC 19 Extinguishing financial liabilities with equity instrumentsThe Accounting

GuidanceFinancial instruments and disclosures for insurance companies’

accounting guidance

The new financial reporting standards related to financial instruments and TFAC Accounting Guidance introduce new classification and measurement requirements for financial instruments as well as provide derecognition guidance on financial assets and financial liabilities. The new guidance also provides an option for the Company to apply hedge accounting to reduce accounting mismatch between hedged item and hedging instrument. In addition, the new rule provides detailed guidance on financial instruments issued by the Company whether it is a liability or an equity. Among other things, they require extensive disclosure on financial instruments and related risks.

The new classification requirements of financial assets under TFRS9 require the Company to assess both i) business model for holding the financial assets; and ii) cash flow characteristics of the asset whether the contractual cash flows represent solely payments of principal and interest (SPPI). The classification affects the financial assets’ measurement. The new standard requires assessment of impairment of financial assets as well as contract assets and recognition of expected credit loss from initial recognition.

On 1 January 2020, the Company passes criteria of temporarily exemption from TFRS 9 Financial Instruments and TFRS 7 Financial Instruments: Disclosures under TFRS 4 (revised 2018) Insurance Contracts. The Company is eligible to apply the Accounting Guidance in relation to financial instruments and disclosure for insurance companies (‘The Accounting Guidance’) as the Company has not previously applied TFRS 9 Financial Instrument and the Company’s activities are predominantly connected with insurance business, based on the eligibility assessment that the total carrying amount of liabilities connected with insurance within the scope of TFRS 4 of Baht 210,741.8 million as at 1 January 2018 is greater than 90% of the total carrying amount of all its liabilities. Certain liabilities connected with insurance included investment contract liabilities measured at fair value through profit or loss of Baht 2,672.5 million and certain deferred tax liabilities of Baht 3,094.7 million.

21Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards (Cont’d)

3.1 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2020 and are relevant to the Company (Cont’d)

a) Financial instruments (Cont’d)

After the date of eligibility assessment, there has been no change in the Company’sactivities that requires a reassessment of the eligibility assessment.

Additional information on financial assets in relation to the election of the temporaryoption is illustrated per below:

Financial assets of the Company are separated into (i) financial assets withcontractual terms that give rise to cash flows that are solely payments of principaland interest on the principal amount outstanding (SPPI) in accordance with TFRS 9and are not held for trading or managed on fair value basis and (ii) all financial assetsother than those specified in (i).

The following table shows the fair value and change in fair value of these two groupsof financial assets:

Unit: Thousand Baht

Fair value as at 31 December 2020Change in fair value for the year ended

31 December 2020Financial assets

that met SPPI criteria and not held for trading or managed on fair value basis Others Total

Financial assets that met SPPI

criteria and not held for trading or managed on fair value basis Others Total

Debt securities 285,650,986 4,794,216 290,445,202 15,973,953 (1,364,692) 14,609,261 Equity and Derivatives - 17,639,182 17,639,182 - (8,257,497) (8,257,497)Other financial assets 5,513,586 870,408 6,383,994 (619,851) 79,939 (539,912)

Total 291,164,572 23,303,806 314,468,378 15,354,102 (9,542,250) 5,811,852

As of 31 December 2020, majority of other financial assets qualifying as SPPI includescash and cash equivalents and accrued investment income whereas the other is agency security fund.

Certain financial assets included within the financial statements, including policy loans under loans and accrued interest receivables, amount due from reinsurance,premium receivable and assets held to cover linked liabilities amounting to Baht 26,497 million are not included above since they are accounted for under TFRS 4.

The financial assets presented above that met SPPI criteria and not held for trading or managed on fair value basis are primarily debt securities.

There is a minor difference between the Accounting Guidance and TFRS 9 in terms of classification and measurement, impairment of equity securities and hybrid contracts. The classification is dependent on the purpose for which the investments were acquired; hence, there is no need to assess business model and cash flow characteristics. An impairment should be assessed not only debt securities but also equity securities. An embedded derivative shall be separated from the host and accounted for as a derivative.

The impact from the first-time adoption has been disclosed in Note 4.

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards (Cont’d)

3.1 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2020 and are relevant to the Company (Cont’d)

b) TFRS 16, Leases clarified where the Company is a lessee, certain standard willresult in almost all leases being recognised on the balance sheet as the distinctionbetween operating and finance leases is removed. A right-of-use asset and a leaseliability will be recognised, with exception on short-term and low-value leases.

On 1 January 2020, the Company has adopted the new lease standard in itsfinancial statements. The impact from the first-time adoption has been disclosed inNote 4.

c) Amendment to TAS 12, Income tax clarified that the income tax consequences ofdividends of financial instruments classified as equity should be recognisedaccording to where the past transactions or events that generated distributableprofits were recognised.

d) Amendment to TAS 19, Employee benefits (plan amendment, curtailment orsettlement) - clarified accounting for defined benefit plan amendments, curtailmentsand settlements that the updated assumptions on the date of change are applied todetermine current service cost and net interest for the remainder of the reportingperiod after the plan amendment, curtailment or settlement.

e) Amendment to TFRS 3, Business combinations clarified that obtaining control ofa business that is a joint operation is a business combination achieved in stages.The previously held interest is therefore re-measured.

f) TFRIC 23, Uncertainty over income tax treatments explained how to recogniseand measure deferred and current income tax assets and liabilities where there isuncertainty over a tax treatment. In particular, it discusses:

- that the Company should assume a tax authority will examine the uncertain taxtreatments and have full knowledge of all related information, i.e. that detectionrisk should be ignored.

- that the Company should reflect the effect of the uncertainty in its income taxaccounting when it is not probable that the tax authorities will accept the treatment.

- that the judgements and estimates made must be reassessed whenevercircumstances have changed or there is new information that affects the judgements.

22 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards (Cont’d)

3.1 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2020 and are relevant to the Company (Cont’d)

b) TFRS 16, Leases clarified where the Company is a lessee, certain standard willresult in almost all leases being recognised on the balance sheet as the distinctionbetween operating and finance leases is removed. A right-of-use asset and a leaseliability will be recognised, with exception on short-term and low-value leases.

On 1 January 2020, the Company has adopted the new lease standard in itsfinancial statements. The impact from the first-time adoption has been disclosed inNote 4.

c) Amendment to TAS 12, Income tax clarified that the income tax consequences ofdividends of financial instruments classified as equity should be recognisedaccording to where the past transactions or events that generated distributableprofits were recognised.

d) Amendment to TAS 19, Employee benefits (plan amendment, curtailment orsettlement) - clarified accounting for defined benefit plan amendments, curtailmentsand settlements that the updated assumptions on the date of change are applied todetermine current service cost and net interest for the remainder of the reportingperiod after the plan amendment, curtailment or settlement.

e) Amendment to TFRS 3, Business combinations clarified that obtaining control ofa business that is a joint operation is a business combination achieved in stages.The previously held interest is therefore re-measured.

f) TFRIC 23, Uncertainty over income tax treatments explained how to recogniseand measure deferred and current income tax assets and liabilities where there isuncertainty over a tax treatment. In particular, it discusses:

- that the Company should assume a tax authority will examine the uncertain taxtreatments and have full knowledge of all related information, i.e. that detectionrisk should be ignored.

- that the Company should reflect the effect of the uncertainty in its income taxaccounting when it is not probable that the tax authorities will accept the treatment.

- that the judgements and estimates made must be reassessed whenevercircumstances have changed or there is new information that affects the judgements.

23Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

3 New and amended financial reporting standards (Cont’d)

3.2 New and amended financial reporting standards that are effective for accounting period beginning on or after 1 January 2021 and are relevant to the Company

Certain amended financial reporting standards have been issued that are not mandatory for current reporting period and have not been early adopted by the Company.

a) Revised Conceptual Framework for Financial Reporting added the following keyprincipals and guidance:

- Measurement basis, including factors in considering difference measurementbasis

- Presentation and disclosure, including classification of income and expenses inother comprehensive income

- Definition of a reporting entity, which maybe a legal entity, or a portion of an entity- Derecognition of assets and liabilities

The amendment also includes the revision to the definition of an asset and liability in the financial statements, and clarification to the prominence of stewardship in the objective of financial reporting.

b) Amendment to TFRS 3, Business combinations amended the definition ofa business which requires an acquisition to include an input and a substantiveprocess that together significantly contribute to the ability to create outputs. Thedefinition of the term ‘outputs’ is amended to focus on goods and services providedto customers and to exclude returns in the form of lower costs and other economicbenefits.

c) Amendment to TFRS 9, Financial instruments and TFRS 7, Financialinstruments amended to provide relief from applying specific hedge accountingrequirements to the uncertainty arising from interest rate benchmark reform such asIBOR. The amendment also requires disclosure of hedging relationships directlyaffected by the uncertainty.

d) Amendment to TAS 1, Presentation of financial statements and TAS 8,Accounting policies, changes in accounting estimates and errors amended thedefinition of materiality. The amendment allows for a consistent definition ofmateriality throughout the Thai Financial Reporting Standards and the ConceptualFramework for Financial Reporting. It also clarified when information is material andincorporates some of the guidance in TAS 1 about immaterial information.

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

4 Impacts from initial application of the new and revised financial reporting standards

This note explains the impact of the adoption of the financial reporting standards relate to financial instruments (TAS32 and the Accounting Guidance) and leases standard (TFRS 16) on the Company’s financial statements. The new accounting policies applied from 1 January 2020 were disclosed in Note 3.1.

The Company has adopted those accounting policies from 1 January 2020 by applying the modified retrospective approach. The comparative figures have not been restated. The reclassifications and the adjustments arising from the changes in accounting policies were therefore recognised in the statement of financial position as of 1 January 2020.

The impact of first-time adoption of new financial reporting standards on statements of financial position are as follows:

As at 31 December 2019

Previously reported

TAS 32 and The Accounting Guidance

Reclassifications and adjustments

TFRS 16Adjustments

As at 1 January 2020

RestatedNotes Thousand Baht Thousand Baht Thousand Baht Thousand Baht

AssetsAccrued investment income C 1,900,651 (352,113) - 1,548,538Loans and accrued interest

receivables C 12,693,240 352,113 - 13,045,353Right-of-use assets D - - 788,077 788,077Other assets D 212,795 - (1,392) 211,403

Total assets 14,806,686 - 786,685 15,593,371

Liabilities and equity

LiabilitiesLease liabilities D - - 829,401 829,401Other liabilities D 4,682,028 - (42,716) 4,639,312

Total liabilities 4,682,028 - 786,685 5,468,713

EquityUnrealised gains on changes

in value of investments measured at fair value throughother comprehensive income A 30,919,073 182,211 - 31,101,284

Gain (loss) on cash flow hedge B 1,593,989 (187,504) - 1,406,485Gain (loss) on deferred cost of

hedge B - 180,711 - 180,711Retained earnings A, B 17,475,889 (175,418) - 17,300,471

Total equity 49,988,951 - - 49,988,951

Total liabilities and equity 54,670,979 - 786,685 55,457,664

Note:A) Adjustments on impairment of financial assets (Note 4.1)B) Impacts from changes in classification of financial assets and cost of hedge reserve (Note 4.1)C) Change in presentation of accrued interest receivable on loans (Note 4.1)D) Recognition of right of use assets and lease liabilities under TFRS 16 (Note 4.2)

24 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

4 Impacts from initial application of the new and revised financial reporting standards

This note explains the impact of the adoption of the financial reporting standards relate to financial instruments (TAS32 and the Accounting Guidance) and leases standard (TFRS 16) on the Company’s financial statements. The new accounting policies applied from 1 January 2020 were disclosed in Note 3.1.

The Company has adopted those accounting policies from 1 January 2020 by applying the modified retrospective approach. The comparative figures have not been restated. The reclassifications and the adjustments arising from the changes in accounting policies were therefore recognised in the statement of financial position as of 1 January 2020.

The impact of first-time adoption of new financial reporting standards on statements of financial position are as follows:

As at 31 December 2019

Previously reported

TAS 32 and The Accounting Guidance

Reclassifications and adjustments

TFRS 16Adjustments

As at 1 January 2020

RestatedNotes Thousand Baht Thousand Baht Thousand Baht Thousand Baht

AssetsAccrued investment income C 1,900,651 (352,113) - 1,548,538Loans and accrued interest

receivables C 12,693,240 352,113 - 13,045,353Right-of-use assets D - - 788,077 788,077Other assets D 212,795 - (1,392) 211,403

Total assets 14,806,686 - 786,685 15,593,371

Liabilities and equity

LiabilitiesLease liabilities D - - 829,401 829,401Other liabilities D 4,682,028 - (42,716) 4,639,312

Total liabilities 4,682,028 - 786,685 5,468,713

EquityUnrealised gains on changes

in value of investments measured at fair value throughother comprehensive income A 30,919,073 182,211 - 31,101,284

Gain (loss) on cash flow hedge B 1,593,989 (187,504) - 1,406,485Gain (loss) on deferred cost of

hedge B - 180,711 - 180,711Retained earnings A, B 17,475,889 (175,418) - 17,300,471

Total equity 49,988,951 - - 49,988,951

Total liabilities and equity 54,670,979 - 786,685 55,457,664

Note:A) Adjustments on impairment of financial assets (Note 4.1)B) Impacts from changes in classification of financial assets and cost of hedge reserve (Note 4.1)C) Change in presentation of accrued interest receivable on loans (Note 4.1)D) Recognition of right of use assets and lease liabilities under TFRS 16 (Note 4.2)

25Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

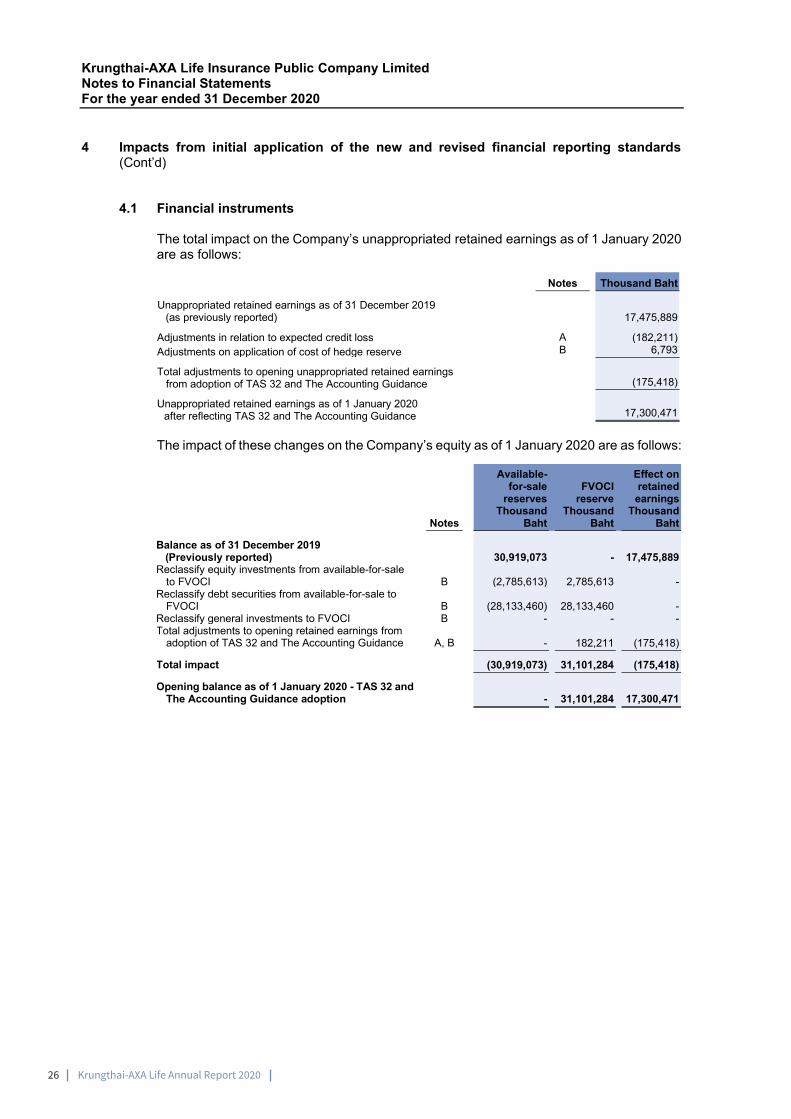

4 Impacts from initial application of the new and revised financial reporting standards (Cont’d)

4.1 Financial instruments

The total impact on the Company’s unappropriated retained earnings as of 1 January 2020 are as follows:

Notes Thousand Baht

Unappropriated retained earnings as of 31 December 2019 (as previously reported) 17,475,889

Adjustments in relation to expected credit loss A (182,211)Adjustments on application of cost of hedge reserve B 6,793

Total adjustments to opening unappropriated retained earnings from adoption of TAS 32 and The Accounting Guidance (175,418)

Unappropriated retained earnings as of 1 January 2020 after reflecting TAS 32 and The Accounting Guidance 17,300,471

The impact of these changes on the Company’s equity as of 1 January 2020 are as follows:

Notes

Available-for-sale

reservesThousand

Baht

FVOCIreserve

Thousand Baht

Effect onretainedearnings

Thousand Baht

Balance as of 31 December 2019(Previously reported) 30,919,073 - 17,475,889

Reclassify equity investments from available-for-sale to FVOCI B (2,785,613) 2,785,613 -

Reclassify debt securities from available-for-sale to FVOCI B (28,133,460) 28,133,460 -

Reclassify general investments to FVOCI B - - -Total adjustments to opening retained earnings from

adoption of TAS 32 and The Accounting Guidance A, B - 182,211 (175,418)

Total impact (30,919,073) 31,101,284 (175,418)

Opening balance as of 1 January 2020 - TAS 32 and The Accounting Guidance adoption - 31,101,284 17,300,471

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

4 Impacts from initial application of the new and revised financial reporting standards (Cont’d)

4.1 Financial instruments (Cont’d)

On 1 January 2020, the management has assessed and classified its financial instrumentsas follows:

Notes

Accrued income on

investmentsThousand

Baht

Available-for-sale

securitiesThousand

Baht

General investments

ThousandBaht

Investments measured at

FVOCIThousand

Baht

Loans and accrued interest

receivablesThousand

Baht

Cash flowhedge

reserveThousand

Baht

Cost of hedge

reserveThousand

BahtFinancial assetsBalance as at 31 December 2019 (Previously reported) 1,900,651 297,329,292 - - 12,693,240 1,593,989 -Adjustments in relation

to expected credit loss A - - - 182,211 - - -Reclassify cash flow

hedge reserve to cost of hedge reserve B - - - - - (187,504) 180,711

Reclassify equity investments from available-for-sale to FVOCI B - (26,594,563) - 26,594,563 - - -

Reclassify debt securitiesfrom available-for-sale

to FVOCI B - (270,734,729) - 270,734,729 - - -Reclassify general

investments to FVOCI B - - - - - - -Change in presentation

of accrued interest receivable C (352,113) - - - 352,113 - -

Opening balance 1 January 2020 –TAS 32 and the Accounting Guidance adoption 1,548,538 - - 297,511,503 13,045,353 1,406,485 180,711

The initial application of the new and revised financial reporting standards does not impact the classification of financial liabilities.

(a) Impairment of financial assets

The Company have following financial assets that are subject to the expected credit loss model:

• cash and cash equivalents• investment account receivables• other assets; and• debt investments carried at FVOCI.

The Company was required to revise its impairment methodology under The Accounting Guidance. The impact of the change in impairment methodology on the Company’s retained earnings at 1 January 2020 were Baht 182.2 million.

While i) cash and cash equivalents ii) investment account receivables and iii) other assets are subject to the new impairment requirement, management has considered that the identified impact was immaterial.

26 Krungthai-AXA Life Annual Report 2020

Krungthai-AXA Life Insurance Public Company LimitedNotes to Financial StatementsFor the year ended 31 December 2020

4 Impacts from initial application of the new and revised financial reporting standards (Cont’d)

4.1 Financial instruments (Cont’d)

On 1 January 2020, the management has assessed and classified its financial instrumentsas follows:

Notes

Accrued income on

investmentsThousand

Baht

Available-for-sale

securitiesThousand

Baht

General investments

ThousandBaht

Investments measured at

FVOCIThousand

Baht

Loans and accrued interest

receivablesThousand

Baht

Cash flowhedge

reserveThousand

Baht

Cost of hedge

reserveThousand

BahtFinancial assetsBalance as at 31 December 2019 (Previously reported) 1,900,651 297,329,292 - - 12,693,240 1,593,989 -Adjustments in relation

to expected credit loss A - - - 182,211 - - -Reclassify cash flow

hedge reserve to cost of hedge reserve B - - - - - (187,504) 180,711

Reclassify equity investments from available-for-sale to FVOCI B - (26,594,563) - 26,594,563 - - -

Reclassify debt securitiesfrom available-for-sale

to FVOCI B - (270,734,729) - 270,734,729 - - -Reclassify general

investments to FVOCI B - - - - - - -Change in presentation

of accrued interest receivable C (352,113) - - - 352,113 - -

Opening balance 1 January 2020 –TAS 32 and the Accounting Guidance adoption 1,548,538 - - 297,511,503 13,045,353 1,406,485 180,711

The initial application of the new and revised financial reporting standards does not impact the classification of financial liabilities.

(a) Impairment of financial assets

The Company have following financial assets that are subject to the expected credit loss model: