20181025 analystenpresentatie london roadshow pp · london roadshow october 25, 2018 the connection...

TRANSCRIPT

London RoadshowLondon RoadshowLondon RoadshowLondon RoadshowOctober 25, 2018

The Connection to the world of Sustainable Tropical Agriculture 1

SIPEF financial statements SIPEF financial statements SIPEF financial statements SIPEF financial statements June 2018June 2018June 2018June 2018

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

2

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

3

1. SIPEF group - Company profile

The Connection to the world of Sustainable Tropical Agriculture 4

Agriculture • 1st segment of the supply chain - commodities

Tropical • Recent industrialised countries

Sustainable • Audited certifications

Connection • Publicly quotedPublicly quotedPublicly quotedPublicly quoted

1. SIPEF group - Company profile

The Connection to the world of Sustainable Tropical Agriculture 5

Continuous production

• Continuous crops

Diversified in product

• Palm oil : basic commodity for food (and recently energy)

• Rubber : cyclic business - tire industry

Diversified in origin

• Indonesia : leading producing country within Asian market

• PNG : export oriented with strong agronomical basics

1. SIPEF group - Company profileWorldwide

The Connection to the world of Sustainable Tropical Agriculture 6

1. SIPEF group - Company profileIndonesia

7

1. SIPEF group - Company profilePapua New Guinea

The Connection to the world of Sustainable Tropical Agriculture 8

1. SIPEF group - Company profilePlanted hectares summary – 30 June 2018

The Connection to the world of Sustainable Tropical Agriculture 9

Palm Rubber Tea Bananas Other Total % Group share

Indonesia 56 425 6 121 1 752 64 298 82% 57 936

PNG 13 622 13 622 17% 13 622

Ivory coast 690 42 732 1% 732

Total 70 047 6 121 1 752 690 42 78 652 100% 72 290

% 89% 8% 2% 1% 0% 100%

Group share 64 739 5 237 1 581 690 42 72 290

• In the coming 40 years, mankind will have to produce more food than in the previous 10 000 years put together

1. SIPEF group - Company profilePalm oil in the world - Population growth

The Connection to the world of Sustainable Tropical Agriculture 10

• Population growth will have a

huge impact on future food

demands

• Rising middle class is causing diet

changes in developing countries

• Agricultural land is increasingly

becoming scarcer

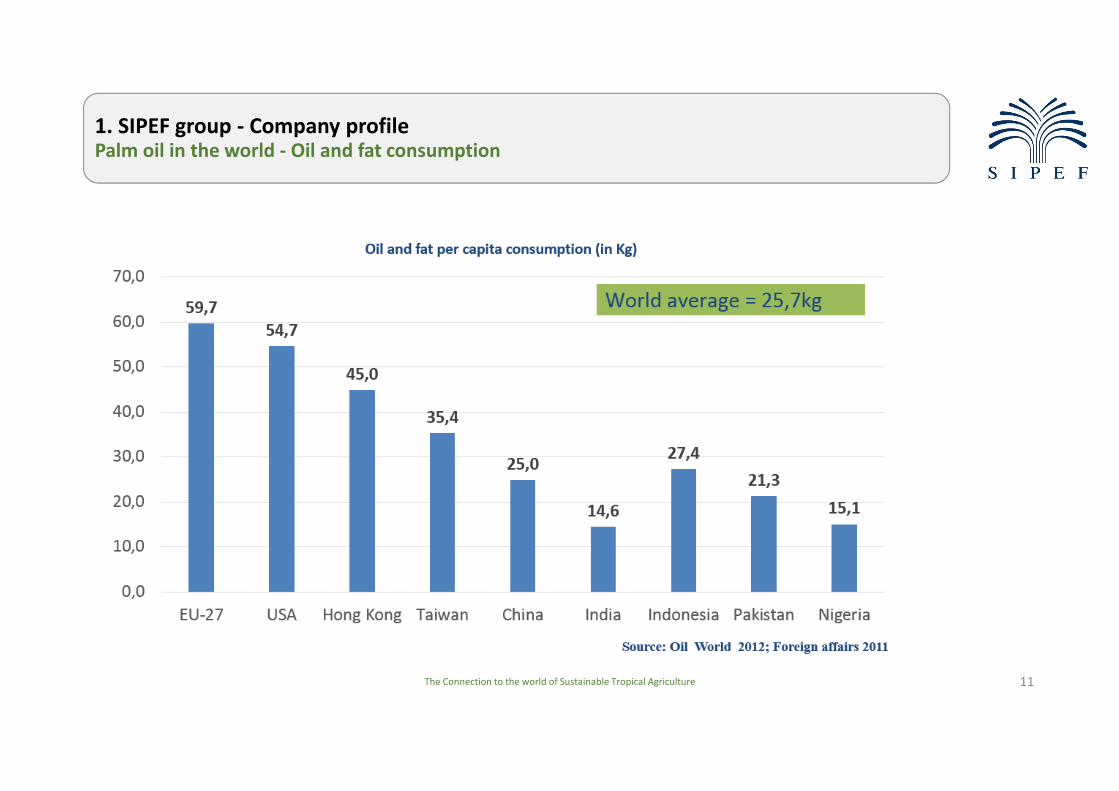

1. SIPEF group - Company profilePalm oil in the world - Oil and fat consumption

The Connection to the world of Sustainable Tropical Agriculture 11

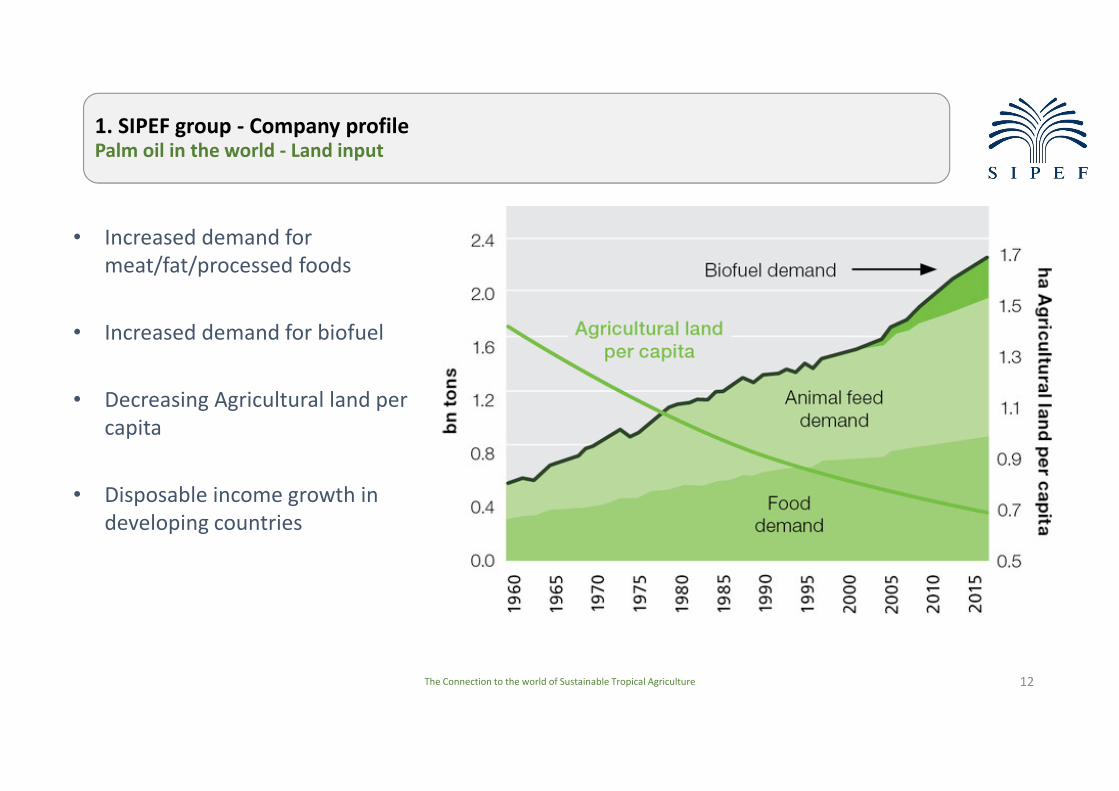

1. SIPEF group - Company profilePalm oil in the world - Land input

The Connection to the world of Sustainable Tropical Agriculture 12

• Increased demand for

meat/fat/processed foods

• Increased demand for biofuel

• Decreasing Agricultural land per

capita

• Disposable income growth in

developing countries

1. SIPEF group - Company profilePalm oil in the world - Sources for deforestation

The Connection to the world of Sustainable Tropical Agriculture 13

1. SIPEF group - Company profilePalm oil in the world - Vegetable oils

The Connection to the world of Sustainable Tropical Agriculture 14

31%

24%

12%

9%

4%

20%

2017: 220,0 million tonnes

Palm oil Soya oil

Rape oil Sunflower oil

Palm kernel and coconut oil Other oils/animals fats

16%

21%

11%9%

6%

37%

Palm oil Soya oil

Rape oil Sunflower oil

Palm kernel and coconut oil Other oils/animal fats

1994/95: 93,1 million tonnes

1. SIPEF group - Company profilePalm oil in the world - Comparison to other oils

The Connection to the world of Sustainable Tropical Agriculture 15

Resources used per vegetable oil:

1. SIPEF group - Company profilePalm oil in the world - Palm oil production

The Connection to the world of Sustainable Tropical Agriculture 16

54%

29%

4%

3%1%

6%

3%

2017 Palm oil production

(Total of 67,1 Mn Tonnes)

Indonesia Malaysia Thailand Africa Oceania Middle & South America Oth. Countries

1. SIPEF group - Company profilePalm oil in the world - Palm oil consumption

The Connection to the world of Sustainable Tropical Agriculture 17

11%

2%

2%

6%

65%

14%0%

2014/15 World consumption

Europe Russia North America South America Asia and the middle east Africa Oceania

1. SIPEF group - Company profilePalm oil in the world - Biodiesel

The Connection to the world of Sustainable Tropical Agriculture 18

12%

10%

20%

27%

10%

21%

31%

Biodiesel 2017

(Total of 35,2 Mn tonnes)

Other oils & fats Used cooking oil Rapeseed oil Soya oil Palm oil EU Palm oil non-EU

3,5 Mn ton

7,5 Mn ton

1. SIPEF group - Company profilePalm oil in the world - Sustainable palm oil

The Connection to the world of Sustainable Tropical Agriculture 19

In 2017 approximately 3,55 million tons entered the market as ‘segregated’ (100% traceable)

SIPEF = 100% certified oil and > 350.000 tons ‘segregated’

2,86 Million Ha RSPO certified production area

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

20

2. SIPEF group - ExpansionStrategy & expansion

The Connection to the world of Sustainable Tropical Agriculture 21

SIPEF group= 100.000 Ha planted (group’ share)

• Palmoil – Rubber – Bananas – Tea

• Indonesia – Papua New Guinea

Focus on core-business

Focus on ‘Sustainable Agriculture’ (RSPO)

Expansion of existing activities

Acquisition of new investments

Balanced leverage

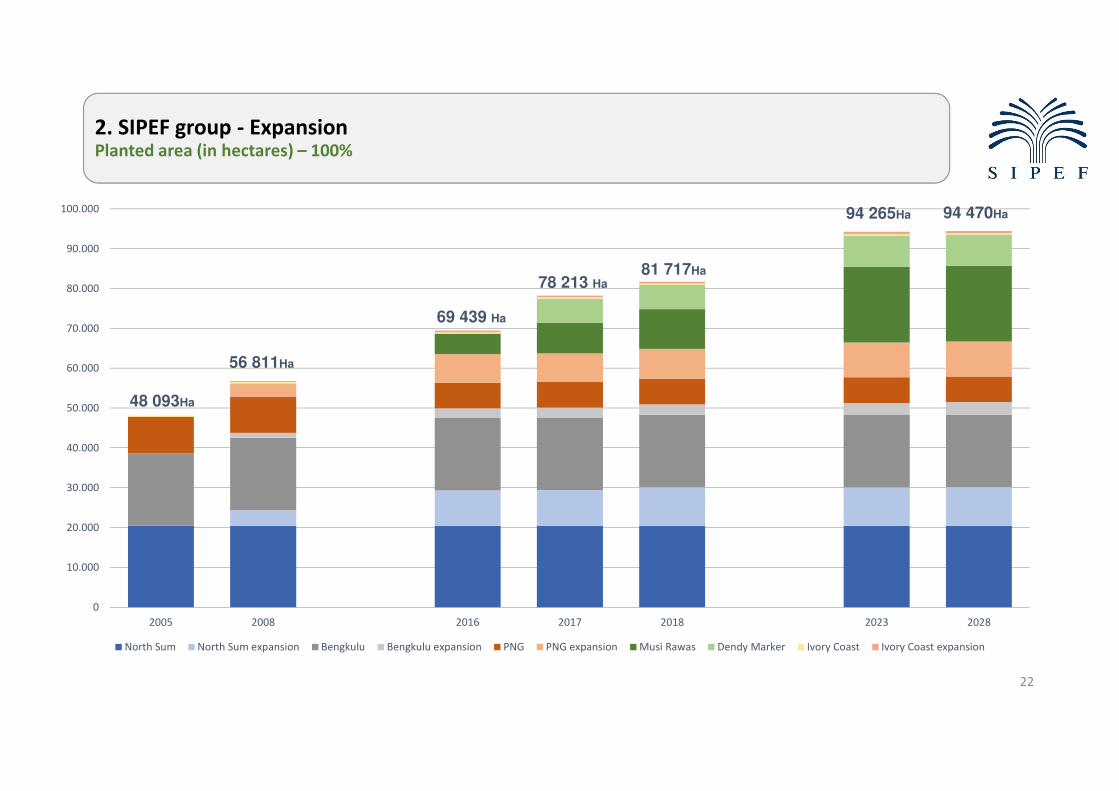

2. SIPEF group - ExpansionPlanted area (in hectares) – 100%

22

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

100.000

2005 2008 2016 2017 2018 2023 2028

North Sum North Sum expansion Bengkulu Bengkulu expansion PNG PNG expansion Musi Rawas Dendy Marker Ivory Coast Ivory Coast expansion

48 093Ha

56 811Ha

69 439 Ha

78 213 Ha

81 717Ha

94 265Ha 94 470Ha

2. SIPEF group - ExpansionSupply base (in hectares): own ha and outgrowers ha – 100%

The Connection to the world of Sustainable Tropical Agriculture 23

81

.71

7

87

.40

8

91

.20

3

93

.29

6

94

.09

9

94

.26

5

94

.33

1

94

.32

9

94

.44

1

94

.46

2

94

.47

0

19

.65

6

20

.53

8

21

.28

6

21

.65

2

21

.78

6

21

.78

6

21

.78

6

21

.78

6

21

.78

6

21

.78

6

21

.78

6

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Own ha Outgrowers ha

2. SIPEF group - Expansion100% CPO production (including plasma and outgrowers – NO FFB)

The Connection to the world of Sustainable Tropical Agriculture 24

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Outgrowers

Own

2028

Own: 480 Kton

Outg: 119 Kton

Total: 599 Kton

2. SIPEF group - ExpansionEvolution mature-immature ha oil palm – 100%

The Connection to the world of Sustainable Tropical Agriculture 25

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Mature Immature

2. SIPEF group - ExpansionYield per hectare CPO

The Connection to the world of Sustainable Tropical Agriculture 26

0

1

2

3

4

5

6

7

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Yie

ld/h

ect

are

CP

O

CPO/ha mature

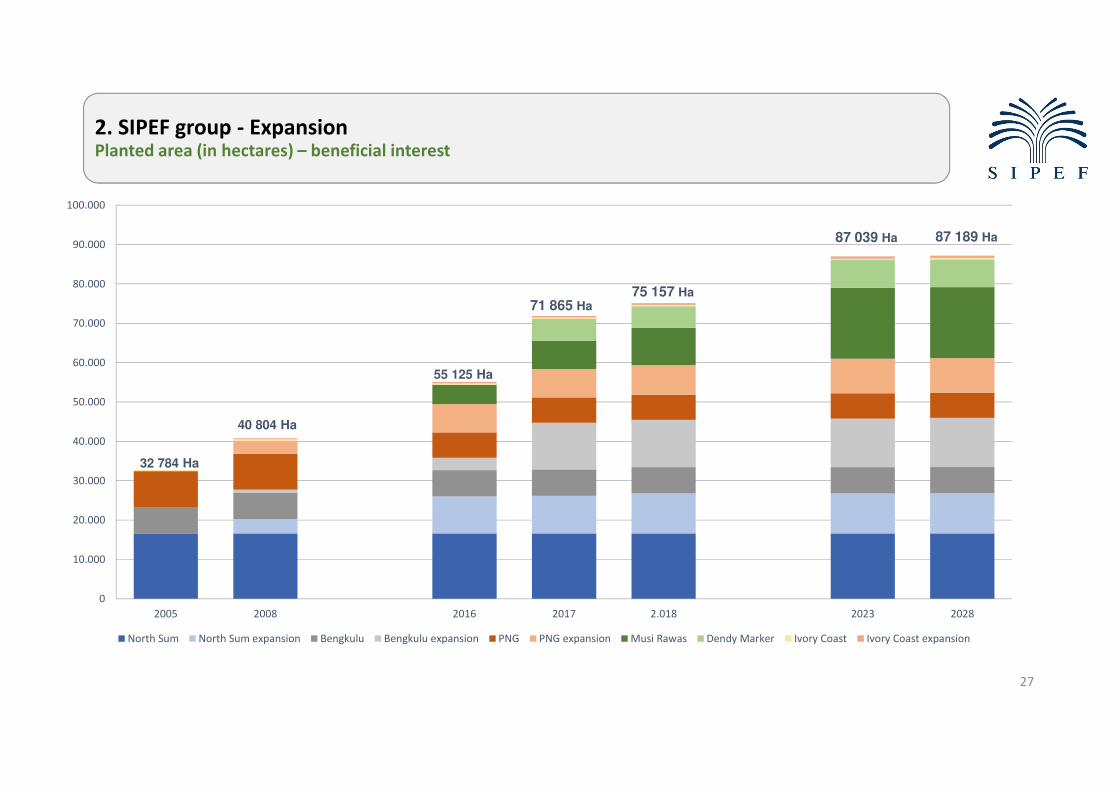

2. SIPEF group - ExpansionPlanted area (in hectares) – beneficial interest

27

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

100.000

2005 2008 2016 2017 2.018 2023 2028

North Sum North Sum expansion Bengkulu Bengkulu expansion PNG PNG expansion Musi Rawas Dendy Marker Ivory Coast Ivory Coast expansion

55 125 Ha

71 865 Ha

75 157 Ha

87 189 Ha87 039 Ha

32 784 Ha

40 804 Ha

2. SIPEF group - ExpansionPlanted hectares and production of CPO (sale of FFB not included) (BI)

The Connection to the world of Sustainable Tropical Agriculture 28

100%

110%

120%

130%

140%

150%

160%

170%

180%

BI hectares

BI production

+ 74%

+ 23%

2. SIPEF group - ExpansionMusi Rawas expansion

The Connection to the world of Sustainable Tropical Agriculture 29

Sumatra

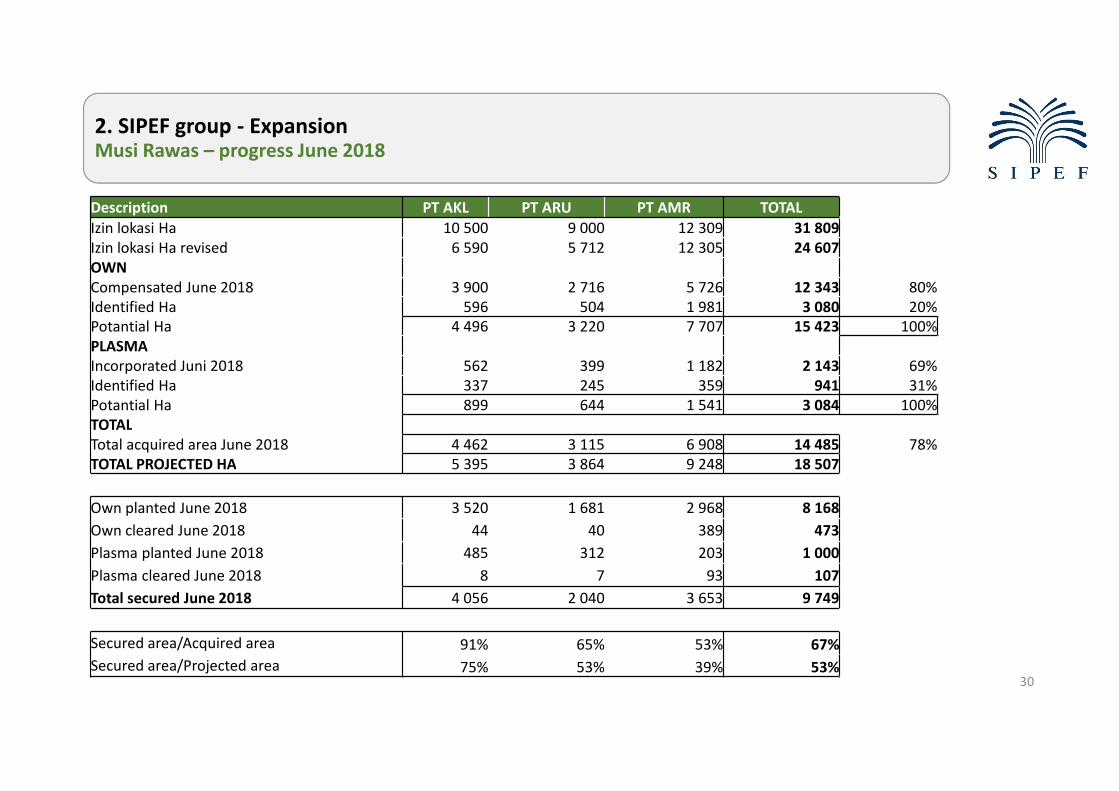

2. SIPEF group - ExpansionMusi Rawas – progress June 2018

30

Description PT AKL PT ARU PT AMR TOTAL

Izin lokasi Ha 10 500 9 000 12 309 31 809

Izin lokasi Ha revised 6 590 5 712 12 305 24 607

OWN

Compensated June 2018 3 900 2 716 5 726 12 343 80%

Identified Ha 596 504 1 981 3 080 20%

Potantial Ha 4 496 3 220 7 707 15 423 100%

PLASMA

Incorporated Juni 2018 562 399 1 182 2 143 69%

Identified Ha 337 245 359 941 31%

Potantial Ha 899 644 1 541 3 084 100%

TOTAL

Total acquired area June 2018 4 462 3 115 6 908 14 485 78%

TOTAL PROJECTED HA 5 395 3 864 9 248 18 507

Own planted June 2018 3 520 1 681 2 968 8 168

Own cleared June 2018 44 40 389 473

Plasma planted June 2018 485 312 203 1 000

Plasma cleared June 2018 8 7 93 107

Total secured June 2018 4 056 2 040 3 653 9 749

Secured area/Acquired area 91% 65% 53% 67%

Secured area/Projected area 75% 53% 39% 53%

2. SIPEF group - ExpansionMusi Rawas – progress June 2018

31

June 2018Compensation Ha Cleared/Planted Ha

Correct Planted Clearedplanted/

Area YTD 2017 jun/18 TOTAL YTD 2017 planted jun/18 jun/18 TOTALcompensated

AKL 3 759 141 3 900 3 776 -407 151 44 3 564 91,4%

ARU 2 626 90 2 716 1 558 -13 135 40 1 721 63,4%

AMR 4 789 937 5 726 2 410 -33 590 389 3 357 58,6%

Plasma 2 109 34 2 143 929 -39 110 107 1 107 51,7%

TOTAL 13 283 1 202 14 485 8 673 -491 986 580 9 749 67,3%

2. SIPEF group - ExpansionMusi Rawas – South Sumatra summary of project status

32

Latest update Izin Lokasi Expansion TOTAL Planted Identified Potential INTI PLASMA

HGU Izin Lokasi HGU/IZIN Cleared development

PT AKL 6 590 6 590 4 056 1 339 5 395 4 496 899

PT AKL II 3 137 3 137 0 1 569 1 569 1 307 261

PT ARU 5 712 5 712 2 040 1 824 3 864 3 220 644

PT AMR I+II 12 305 12 305 3 653 5 595 9 248 7 707 1 541

PT AMR III 1 303 1 303 0 652 652 543 109

Metafocus 4 201 4 201 0 2 101 2 101 1 750 350

Dendymarker 17 793 17 793 8 986 8 986 6 205 2 781

DIL Newplant 0 0 1 604 1 604 1 604 0

TOTAL 42 400 8 641 51 041 18 735 14 683 33 418 26 832 6 586

2. SIPEF group - ExpansionMusi Rawas compensated area June 2018

33

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

okt

/11

de

c/1

1

feb

/12

ap

r/1

2

jun

/12

au

g/1

2

okt

/12

de

c/1

2

feb

/13

ap

r/1

3

jun

/13

au

g/1

3

okt

/13

de

c/1

3

feb

/14

ap

r/1

4

jun

/14

au

g/1

4

okt

/14

de

c/1

4

feb

/15

ap

r/1

5

jun

/15

au

g/1

5

okt

/15

de

c/1

5

feb

/16

ap

r/1

6

jun

/16

au

g/1

6

okt

/16

de

c/1

6

feb

/17

ap

r/1

7

jun

/17

au

g/1

7

okt

/17

de

c/1

7

feb

/18

ap

r/1

8

jun

/18

au

g/1

8

okt

/18

de

c/1

8

Cumulative Compensated Area (Ha) ARU AMR AKL

2. SIPEF group - ExpansionMusi Rawas planted area up to june 2018

34

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

He

cta

res

Cumulative Planted Area (Ha) AKL ARU AMR

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

35

3. SIPEF group – Productions & pricesSeptember production 2018

36

In Tonnes September 2018 September 2017 YoY%

Palm oil own

- Tolan Tiga Group 53 313 50 639 5,3%

- UMW/TUM Group 32 423 29 928 8,3%

- Agro Muko Group 65 336 58 384 11,9%

- South Sumatra Group 3 990 360 1008%

- Hargy Oil Palms 62 450 61 341 1,8%

Total palm oil own 217 512 200 652 8,4%

Total palm oil outgrowers 44 168 45 393 -2,7%

Total palm oil 261 680 246 045 6,4%

In Tonnes September 2018 September 2017 YoY%

Total rubber 5 917 6 121 -3,3%

Total tea 1 658 1 747 -5,1%

Total bananas 20 563 22 115 -7,0%

3. SIPEF group – Productions & pricesMarkets

The Connection to the world of Sustainable Tropical Agriculture 3730/10/2018

Rating Bullish inputs Bearish inputs

Palm Oil

SO 530

ND 545

JFM 580

AMJ 595

Neutral - Malaysian production underperforming.

- Indonesia has increased the blending targets,

and 20% for the last quarter is realistic. 30%

for 2019 looks more feasible with Jokowi’s

support.

- Also more biodiesel exports, leading to

capacity constraints in Indo biodiesel industry.

- Petro market close to the $80 per barrel level.

- El Nino story becoming more vocal, 70%

chance. But looks to be a mild one.

- Latest MPOB report very disappointing, with slow exports

and stocks increasing more than expected

- Palm oil stocks remain high and will increase in the coming

months both in Indo and Mal.

- China/US trade war still having a negative impact on

agricultural products.

- USDA soybean production at a new record high, with

massive yields, leading to a very bearish US bean story.

- Bigger hectares in Brazil and Argy expected for soybeans

- Very good sun seed production in Ukraine and Russia, will

fight for Indian demand.

Rubber

RSS3 1460

SIR10 1344

Neutral - Rubber is cheap, touching cost of production! - Market long term outlook is that is still a small over-

production until 2025.

- High stocks in China.

- Customers very lackluster.

Tea Friendly - Winter demand kicking in - Pakistan instable politics / economy

3. SIPEF group – Productions & pricesMonthly palm oil (CIF Rotterdam USD/ton)

The Connection to the world of Sustainable Tropical Agriculture 38

500

550

600

650

700

750

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016

2017

2018

3. SIPEF group – Productions & pricesPalm oil (FOB Malaysia) and its main competitor (monthly prices)

The Connection to the world of Sustainable Tropical Agriculture 39

FOB Malaysia

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

20

06

M0

1

20

06

M0

4

20

06

M0

7

20

06

M1

0

20

07

M0

1

20

07

M0

4

20

07

M0

7

20

07

M1

0

20

08

M0

1

20

08

M0

4

20

08

M0

7

20

08

M1

0

20

09

M0

1

20

09

M0

4

20

09

M0

7

20

09

M1

0

20

10

M0

1

20

10

M0

4

20

10

M0

7

20

10

M1

0

20

11

M0

1

20

11

M0

4

20

11

M0

7

20

11

M1

0

20

12

M0

1

20

12

M0

4

20

12

M0

7

20

12

M1

0

20

13

M0

1

20

13

M0

4

20

13

M0

7

20

13

M1

0

20

14

M0

1

20

14

M0

4

20

14

M0

7

20

14

M1

0

20

15

M0

1

20

15

M0

4

20

15

M0

7

20

15

M1

0

20

16

M0

1

20

16

M0

4

20

16

M0

7

20

16

M1

0

20

17

M0

1

20

17

M0

4

20

17

M0

7

20

17

M1

0

20

18

M0

1

20

18

M0

4

20

18

M0

7

Palm oil Soybean oil

3. SIPEF group – Productions & pricesMonthly rubber (RSS3 Singapore USD/ton)

The Connection to the world of Sustainable Tropical Agriculture 40

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

2 600

2 800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016

2017

2018

3. SIPEF group – Productions & pricesMonthly tea prices (Mombasa/Nairobi auctions USD/ton)

The Connection to the world of Sustainable Tropical Agriculture 41

1 500

1 700

1 900

2 100

2 300

2 500

2 700

2 900

3 100

3 300

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016

2017

2018

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

42

4. SIPEF group – Financial performanceSales – Consolidated gross margin

43

Total consolidated turnover (including corporateTotal consolidated turnover (including corporateTotal consolidated turnover (including corporateTotal consolidated turnover (including corporate)– June 2018: 139 973 KUSD

– June 2017: 157 017 KUSD

134 541

8 8454 123

8 790

123 208

4 979 2 9298 342

-5 000

15 000

35 000

55 000

75 000

95 000

115 000

135 000

155 000

Palm Rubber Tea Bananas

2017 Sales 2017 Gross Margin 2018 Sales 2018 Gross Margin

38,4%

36,4%

30,7%-8,8% 8,4%

13,1%22,4%

15,8%

4. SIPEF group – Financial performanceGross profit –per product

44

In KUSD 2018 in % 2017 in %

Palm 44 819 96,2% 51 731 90,1%

Rubber -440 -0,9% 2 713 4,7%

Tea 383 0,8% 345 0,6%

Bananas 1 319 2,8% 1 966 3,4%

Corporate and others 515 1,1% 717 1,2%

Total 46 596 100,0% 57 472 100,0%

Gross profit (June YTD)

4. SIPEF group – Financial performanceProfit and loss statement (management presentation)

45

Profit and loss (June YTD)

In KUSD 2018 2017

Gross Profit 46 597 57 472

Services and administration -16 306 - 14 930

Other operating income/(charges) -361 1 007

Operating result 29 930 43 549

Financial income 1 089 784

Financial charges -1 497 -1 683

Exchange result -909 937

Profit before tax 28 613 43 587

Tax -9 479 -12 391

Profit after tax 19 134 31 196

Share of associates and JV’s -511 3 100

Result from continuing operations 18 623 34 296

4. SIPEF group – Financial performanceProfit and loss statement (management presentation)

46

Profit and loss (June YTD)

In KUSD 2018 2017

Result from continuing operations 18 623 34 296

Gain on sale BDM-ASCO 7 380 0

Revaluation gain acquisition PT Agro Muko 0 79 324

Profit for the period 26 003 113 620

Result from continuing operations share of the group 17 391 32 250

Gain on sale BDM-ASCO Share of the group 7 380 0

Revaluation gain acquisition PT Agro Muko Share of the group 0 75 182

Profit for the period Share of the group 24 771 107 432

4. SIPEF group – Financial performanceProfit and loss statement

47

Sale BDM-ASCO insurance

• As announced on 18 December 2017, the sale of BDM-ASCO was finalised and handed over on 7 June 2018

• Total net cash amount received: 20 467 KUSD (20 804 KUSD – 0.337 KUSD)

• Total one-off gain: 7 380 KUSD

• Deconsolidated as of 1 January 2018. The result up to 7 June 2018 was immaterial.

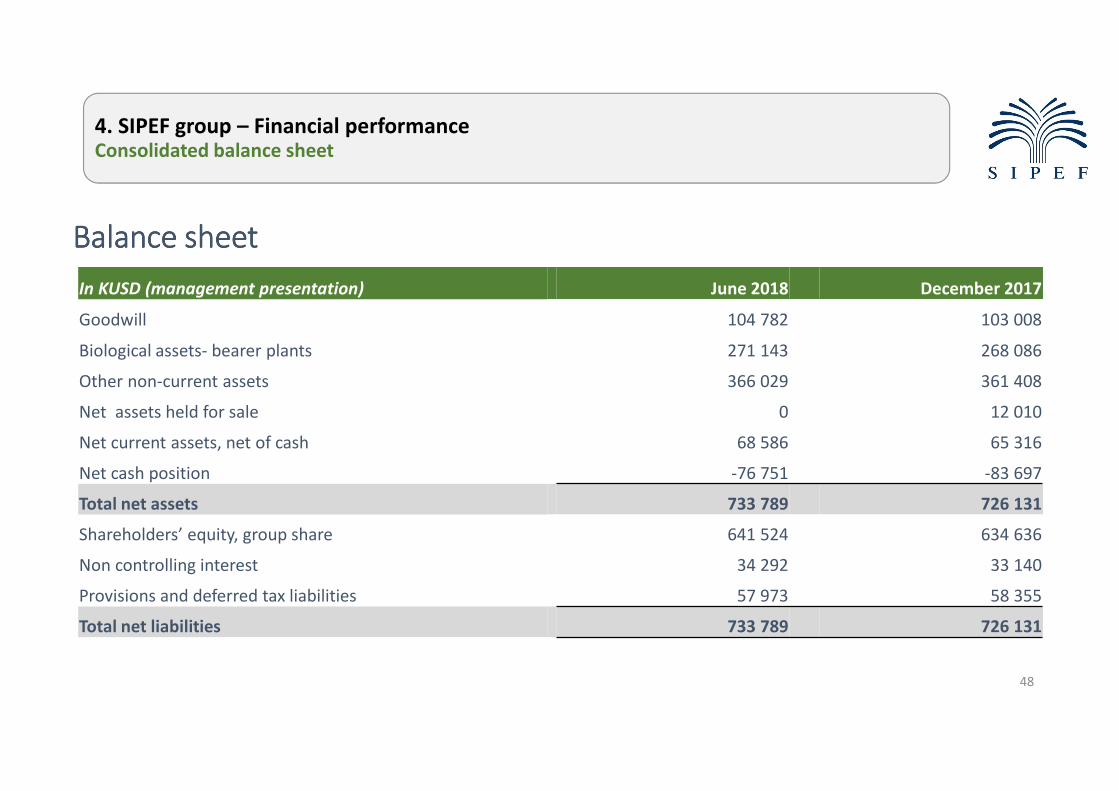

4. SIPEF group – Financial performanceConsolidated balance sheet

48

In KUSD (management presentation) June 2018 December 2017

Goodwill 104 782 103 008

Biological assets- bearer plants 271 143 268 086

Other non-current assets 366 029 361 408

Net assets held for sale 0 12 010

Net current assets, net of cash 68 586 65 316

Net cash position -76 751 -83 697

Total net assets 733 789 726 131

Shareholders’ equity, group share 641 524 634 636

Non controlling interest 34 292 33 140

Provisions and deferred tax liabilities 57 973 58 355

Total net liabilities 733 789 726 131

Balance sheetBalance sheetBalance sheetBalance sheet

4. SIPEF group – Financial performanceConsolidated cash flow

49

In KUSD (management presentation) June 2018 June 2017

Cash flow from operating activities 48 471 58 097

Change in net working capital -21 304 6 854

Income taxes paid -11 154 -2 021

Cash flow from operating activities after tax 16 013 62 930

Acquisitions intangible and tangible assets -29 194 -24 175

Sales of PP&E and financial assets (excl BDM-ASCO) 1 309 1 633

Acquisition financial assets -99 -350

Recurring free cash flow -11 971 40 037

Selling price BDM-ASCO 20 467 0

Purchase price PT Agro Muko 0 -124 977

Capital Increase 0 95 037

Other financing activities -16 537 5 486

Net increase in investments, cash and cash equivalents -8 041 15 583

Cash FlowCash FlowCash FlowCash Flow

4. SIPEF group – Financial performanceValue per hectare

50

Sensitivity 30/06/2018

Market price (closing 30/06/2018) 63,00EUR Share price EUR @ USD per hectare

50,00 8.908

Number of shares 10.579.328 55,00 9.733

Own shares -123.300 60,00 10.559

10.456.028 63,00 11.054

65,00 11.384

EUR/USD 1,1684 70,00 12.210

75,00 13.036

4. SIPEF group – Financial performanceDividend history

51

0,30 0,300,40

0,80 0,80

1,10

1,50

1,70 1,70

1,25 1,25

0,60

1,25

1,60

17%

23%22%

24%

21%

25% 25% 25%

32% 32%

30% 31% 31% 30%

0%

5%

10%

15%

20%

25%

30%

35%

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

1,80

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dividend History Sipef

EUR/share Pay-out

4. SIPEF group – Financial performanceProspects – comments press release October 18, 2018

52

Production

As in previous quarters, we observed an enduring increase in palm oil fruit and palm oil production

volumes across all SIPEF group plantations at the beginning of the fourth quarter. We maintain our

expectation of at least 9% growth in our palm oil production.

We do not expect a further fall in rubber volumes toward the end of the year. We expect the annual

volumes to recover.

Expectations remain rather negative for the disappointing tea production in Cibuni, Java.

For the banana production in Ivory Coast, the full impact of the steps taken to increase the volumes for

export to Europe will probably only be felt at the beginning of 2019.

Markets

The palm oil market is currently in its peak production period and will probably face high stocks until

the end of the year.

With the rather limited production growth ahead of us in 2019, this additional biodiesel demand will

certainly provide enough incentive for significantly higher markets.

The rubber market remains lacklustre and unless there is new input, it is likely to stay in this narrow

trading range.

Demand for tea in the Mombasa tea auction normally peaks during the fourth quarter, but sufficient

supplies in Kenya will limit the upside. We expect tea prices to remain range-bound with slight upticks.

4. SIPEF group – Financial performanceProspects – comments press release October 18, 2018

53

Cash flow and expansion

• Investment policy remains fully focused on expanding South Sumatra palm oil activities (PT Dendymarker and Musi Rawas)

• DIL will be increased to more than 10 000 hectares in the future, which will bring the total development in South Sumatra to +/- 33 000 hectares, of which 20% will belong to the local communities but will be exploited by us.

• To conclude, the additional acquisition of concessions earlier this year has opened the way to the growth of the SIPEF group into a company that, over a 5-year period, will approach 100 000 hectares under own management, of which 80 000 hectares are already planted and the supply base will reach 120 000 hectares.

Result

• To date we have sold 78% of our expected palm oil production at an average price of USD 694 CIF Rotterdam, premiums included, compared with 95% at USD 755 CIF Rotterdam at the same time last year.

• Given the considerable fall in palm oil and rubber sale prices, we expect the recurring result for the second half of 2018 to be approximately the same as for the first half of the year, which means the recurring annual results will be significantly lower than in 2017.

SummarySummarySummarySummary

1. SIPEF Group Company profile

2. SIPEF group - Expansion

3. SIPEF Group – Productions & prices

4. SIPEF group – Financial performance

5. Peer review

The Connection to the world of Sustainable Tropical Agriculture

54

5. Peer reviewDisclaimer

The information contained in this section is provided for your general information only and is not designed nor intended to offer anything more than information only.

The information with respect to the companies included in the Peer Review was retrieved from publicly available information being annual reports and company websites on the one hand and from analyst reports we received on the other hand. In some cases we had to give our own interpretation to the available information in order to get comparable indicators.

As a consequence of using different sources combined with giving our own interpretation to the available information, the information may not always be correct and SIPEF does not accept any liability for loss and damage that may arise from relying upon this information.

The Connection to the world of Sustainable Tropical Agriculture 55

5. Peer reviewPrinciple assumptions

• Benchmark of main industrial competitors

• Age profile based on own ageing interpretation

• Market capitalization is calculated based on the average exchange rate & average share price of the year

• Benchmark based on own CPO productions of competitors:

• Representative sample of comparable industry competitors (2017): 32,3%

• Industrial comparable companies (50%)

The Connection to the world of Sustainable Tropical Agriculture 56

Tons

CPO own production benchmark (2017) 10.972.924

Worldwide production (Oilworld 2017) 66.860.000

5. Peer reviewOwn planted Oil Palm Hectares in KHa (2017)

The Connection to the world of Sustainable Tropical Agriculture 57

37

39

44

65

83

89

96

126

131

144

180

225

174

211

240

248

342

400

603

69

MP Evans

Socfinasia

R.E.A. Holdings

Anglo Eastern Plantations

SIPEF

Sampoerna Agro

Socfinaf

London Sumatra Indon

Eagle High Plantations

Bumitama

Genting Plantations

IOI Corporation

First Resources

Kuala Lumpur Kepong

Astra Agro Lestari

Wilmar International

Salim Ivomas Pratama

Felda Global Ventures

Golden Agri-Resources

Sime Darby

Plantation

Integrated

Sipef

5. Peer reviewAge Profile: Average age planted hectares (2017)

The Connection to the world of Sustainable Tropical Agriculture 58

7,0

8,4

8,9

10,0

10,0

10,0

10,0

10,8

11,1

14,1

15,0

15,2

11,0

12,4

13,2

14,5

14,5

15,0

16,0

10,3

MP Evans

Eagle High Plantations

Bumitama

Anglo Eastern Plantations

First Resources

Genting Plantations

Sampoerna Agro

SIPEF

Socfinaf

Wilmar International

R.E.A. Holdings

Kuala Lumpur Kepong

Sime Darby

Socfinasia

IOI Corporation

Felda Global Ventures

London Sumatra Indon

Salim Ivomas Pratama

Astra Agro Lestari

Golden Agri-Resources

Plantation

Integrated

Sipef

2016 2017 Var %

Average 11,74 11,97 1,9%

Sipef 9,91 10,26 3,5%

5. Peer reviewFFB Yield – MT/ha (2017)

59

9,3

13,1

14,1

14,9

15,6

16,1

17,5

18,2

18,4

19,1

19,9

22,2

14,8

15,4

19,0

19,4

20,5

21,4

21,7

23,9

Eagle High Plantations

Sampoerna Agro

Socfinaf

Salim Ivomas Pratama

London Sumatra Indon

Felda Global Ventures

R.E.A. Holdings

Bumitama

Anglo Eastern Plantations

First Resources

Genting Plantations

Wilmar International

Astra Agro Lestari

Sime Darby

MP Evans

Golden Agri-Resources

Kuala Lumpur Kepong

IOI Corporation

Socfinasia

SIPEF*

Plantation

Integrated

Sipef

* Sipef excluding PT Dendymarker acquired per 1 August 2017

The Connection to the world of Sustainable Tropical Agriculture

2016 2017 Var %

Average 16,9 17,8 5,2%

Sipef 22,4 23,9 6,6%

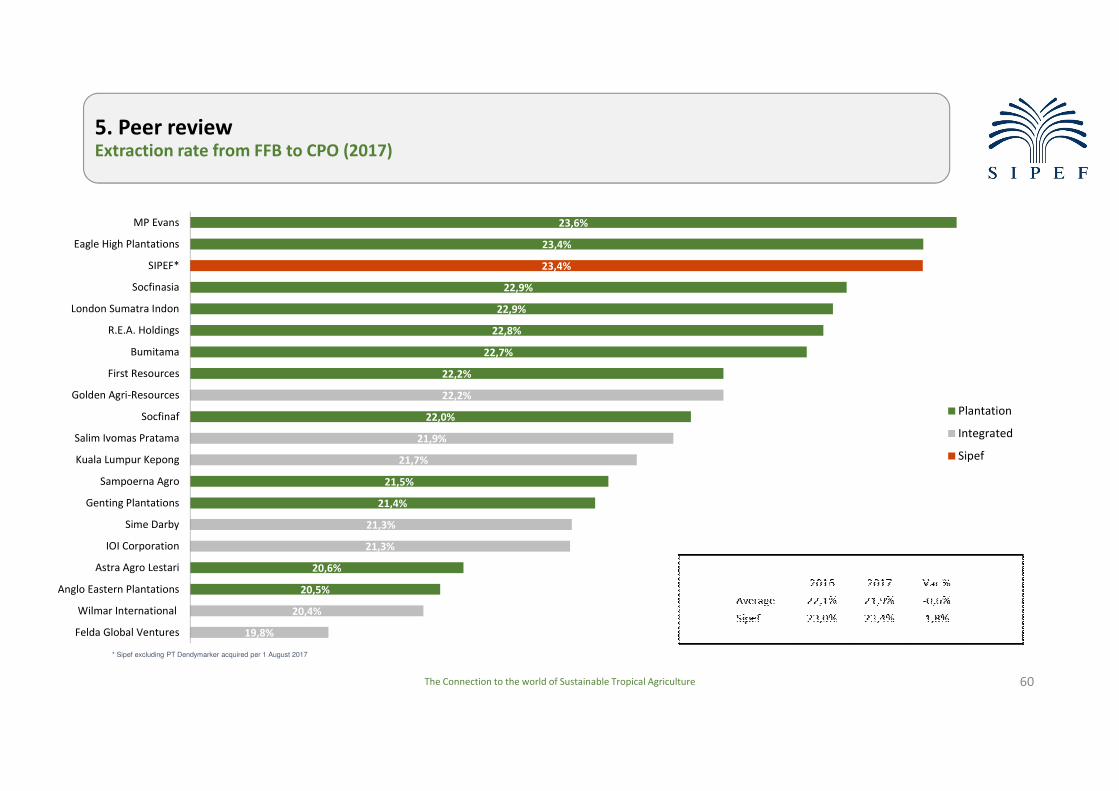

5. Peer reviewExtraction rate from FFB to CPO (2017)

The Connection to the world of Sustainable Tropical Agriculture 60

20,5%

20,6%

21,4%

21,5%

22,0%

22,2%

22,7%

22,8%

22,9%

22,9%

23,4%

23,6%

19,8%

20,4%

21,3%

21,3%

21,7%

21,9%

22,2%

23,4%

Felda Global Ventures

Wilmar International

Anglo Eastern Plantations

Astra Agro Lestari

IOI Corporation

Sime Darby

Genting Plantations

Sampoerna Agro

Kuala Lumpur Kepong

Salim Ivomas Pratama

Socfinaf

Golden Agri-Resources

First Resources

Bumitama

R.E.A. Holdings

London Sumatra Indon

Socfinasia

SIPEF*

Eagle High Plantations

MP Evans

Plantation

Integrated

Sipef

* Sipef excluding PT Dendymarker acquired per 1 August 2017

5. Peer reviewCPO Yield – MT/ha (2017)

The Connection to the world of Sustainable Tropical Agriculture 61

2,17

2,82

3,11

3,41

3,56

3,59

3,66

3,94

3,94

4,04

4,70

5,53

3,06

3,25

3,88

4,14

4,55

4,61

4,64

5,58

Eagle High Plantations

Sampoerna Agro

Felda Global Ventures

Socfinaf

Salim Ivomas Pratama

London Sumatra Indon

R.E.A. Holdings

Anglo Eastern Plantations

Bumitama

Wilmar International

Astra Agro Lestari

Genting Plantations

First Resources

Sime Darby

Golden Agri-Resources

IOI Corporation

Kuala Lumpur Kepong

MP Evans

Socfinasia

SIPEF*

Plantation

Integrated

Sipef

* Sipef excluding PT Dendymarker acquired per 1 August 2017

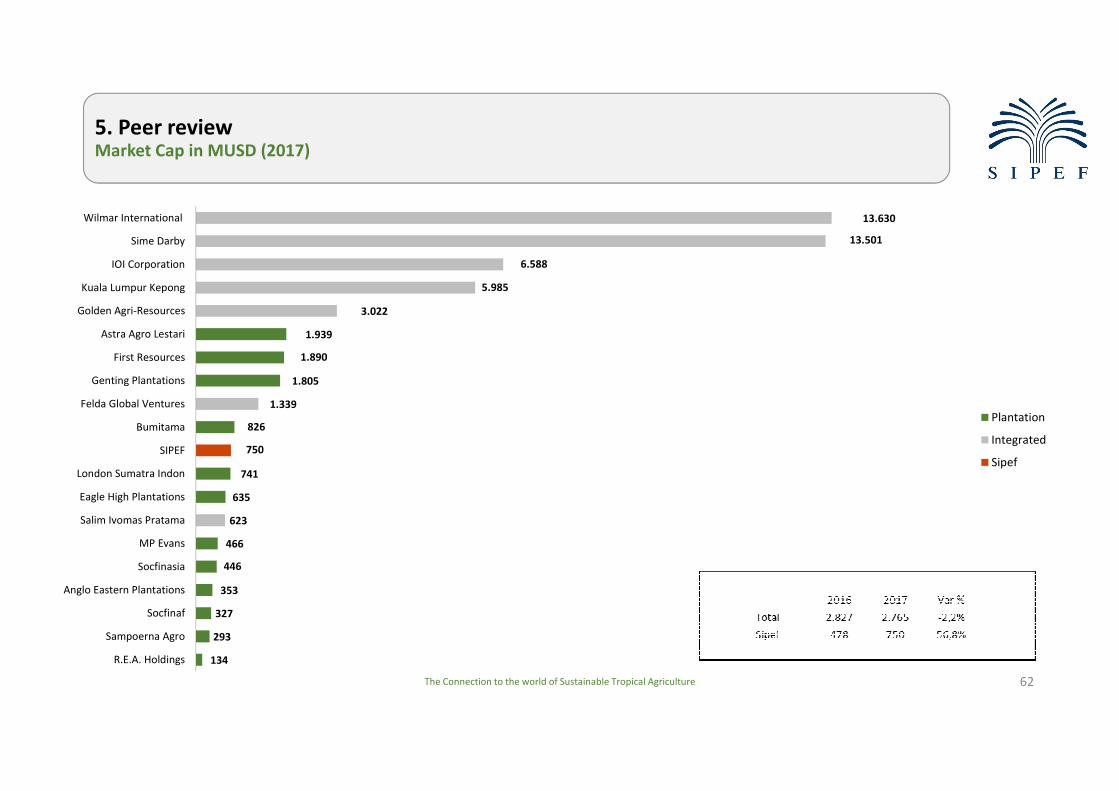

5. Peer reviewMarket Cap in MUSD (2017)

The Connection to the world of Sustainable Tropical Agriculture 62

134

293

327

353

446

466

635

741

826

1.805

1.890

1.939

623

1.339

3.022

5.985

6.588

13.501

13.630

750

R.E.A. Holdings

Sampoerna Agro

Socfinaf

Anglo Eastern Plantations

Socfinasia

MP Evans

Salim Ivomas Pratama

Eagle High Plantations

London Sumatra Indon

SIPEF

Bumitama

Felda Global Ventures

Genting Plantations

First Resources

Astra Agro Lestari

Golden Agri-Resources

Kuala Lumpur Kepong

IOI Corporation

Sime Darby

Wilmar International

Plantation

Integrated

Sipef

5. Peer reviewDividend Yields (based on average market cap 2017)

The Connection to the world of Sustainable Tropical Agriculture 63

0,0%

0,0%

0,5%

0,6%

1,2%

2,4%

2,6%

3,1%

3,5%

3,7%

3,7%

5,0%

1,9%

2,0%

2,1%

2,1%

2,7%

2,8%

2,9%

2,5%

Eagle High Plantations

R.E.A. Holdings

Anglo Eastern Plantations

Socfinaf

Sampoerna Agro

Salim Ivomas Pratama

Kuala Lumpur Kepong

IOI Corporation

Golden Agri-Resources

Genting Plantations

SIPEF

Bumitama

Sime Darby

Felda Global Ventures

Wilmar International

London Sumatra Indon

Astra Agro Lestari

First Resources

MP Evans

Socfinasia

Plantation

Integrated

Sipef

5. Peer reviewPrice Earning Ratio (based on average market cap 2017)

The Connection to the world of Sustainable Tropical Agriculture 64

0,0

0,0

9,4

9,8

12,9

13,0

13,1

13,6

13,7

15,8

19,3

26,0

45,4

11,2

16,3

23,8

25,9

38,1

40,8

12,4

Eagle High Plantations *

R.E.A. Holdings *

Bumitama

Anglo Eastern Plantations

Wilmar International

SIPEF

Astra Agro Lestari

London Sumatra Indon

Socfinaf

Sampoerna Agro

First Resources

Socfinasia

Salim Ivomas Pratama

MP Evans

Sime Darby

Kuala Lumpur Kepong

Genting Plantations

IOI Corporation

Golden Agri-Resources

Felda Global Ventures

Plantation

Integrated

Sipef

* Not included as irrelevant (profit close to break-even or loss for the year)

The Connection to the world of Sustainable Tropical Agriculture 65