2018 buyer’s guide to lease accounting software · 2018 buyer’s guide to lease accounting...

TRANSCRIPT

Copyright © 2018 Nakisa Inc. All rights reserved.1

2018 Buyer’s Guide to Lease Accounting SoftwareA guide to help organizations facilitate the purchase of lease accounting software for compliance with IFRS 16 and ASC 842.

Copyright © 2018 Nakisa Inc. All rights reserved. 2

Leasing Landscape 3

Make Your Deadlines with Technology 4

End-to-End Lease Accounting 6

Lifecycle of a Lease 6

Data Abstraction 7

Lease Determination 8

Terms & Conditions and Initial Recognition 9

Accruals, Payments, and Event Management 9

Analytics and Reporting 10

Technical Considerations 12

Integration 12

Deployment 13

On Premise 13

Cloud 14

Standalone 14

Buyer Beware 16

Acquiring a Lease Accounting Solution 16

Table of Contents

Copyright © 2018 Nakisa Inc. All rights reserved.3

Leasing Landscape

By 2019, $3.3 trillion in operating lease obligations will be moved to company balance sheets worldwide, a direct result of the new IFRS 16 and ASC 842 regulations for leases. It is a simple-sounding change with massive downstream accounting implications. In addition to reflecting leasing activities on balance sheets, lessees will be required to provide qualitative and quantitative disclosures to help financial users assess the amount, timing, and uncertainty of cashflows arising from leases.

Many organizations enter into lease contracts to support their business operations. It is a means of acquiring the most up-to-date equipment, conserving working capital, and avoiding cash-devouring down payments. Today, leasing is one of the preferred ways to acquire assets. According to the Equipment Leasing Association of America, approximately 80 percent of U.S. companies lease some or all of their equipment. As a result, the new leasing standards will affect companies across all industries.

Approximately 80 percent of U.S. companies lease some or all of their equipment. As a result, the new leasing standards will affect companies across all industries.

Despite the significant size and dollar value of lease portfolios, most companies do not have formal processes to track existing assets or contracts. Often lease data is scattered across multiple systems from ERPs to Procurement and IT asset management technologies. Systems to record and capture the full inventory of leases, payment schedules, and key terms and conditions that will have an impact on financial calculations under the new standards are relatively new. Moreover, organizations have been slow to adopt the practice of automating workflows related to lease accounting and management.

13th Jan, 2016The IASB published the new lease accounting

standard - IFRS 16

25th Feb, 2016The FASB published the

new lease accounting standard - ASC 842

1st Jan, 2019IFRS 16 e�ective date -

Early adoption permitted

Next �scal year after 15th Dec. 2018

ASC 842 e�ective date

Copyright © 2018 Nakisa Inc. All rights reserved. 4

Today, most organizations use spreadsheets to track leasing activities. Unfortunately, spreadsheets are not a scalable or reliable method for tracking global lease portfolios since they are prone to accidental misuse and operator error, even by the most experienced users. Spreadsheets become an even greater liability when there is a change in the terms and condition of the contract that require the asset (right-of-use asset) and liability (lease liability) values to be remeasured. The impact of the regulations on lease processes are profound and businesses need to be aware of the requirements before trying to tackle lease compliance for IFRS 16 & ASC 842 with a spreadsheet solution. Relying on spreadsheets to provide a single source of truth for lease accounting could be the difference in your organization being compliant-ready or not.

Make Your Deadlines with Technology

Although the effective dates for the new lease accounting standards seem far away, they are rapidly approaching. Still, some companies have yet to analyze how the rules will impact their financial statements. One of the biggest obstacles to readiness is the availability of information about existing leases. The data required for compliance is abundant. Gathering, collating, and analyzing data sets of such volume manually is a costly and time-consuming task. Many organizations with legacy lease administration software are finding that they cannot use these applications to run lease accounting analysis under the new standards due to the complexity of event management. Consequently, these organizations are looking to adopt lease accounting and management software capable of acting as a central repository for lease data across a global lease portfolio.

The best solutions simplify lease accounting across the entire lease lifecycle from inception to termination and are built from the ground up to support compliance with the new lease accounting standards.

The best solutions help to streamline data collection, tracking, and validation to ensure access to accurate data across an organization.

Additionally, these solutions are capable of generating the necessary accounting calculations required under IFRS 16, ASC 842 and other current lease accounting standards (IAS 17 & ASC 840). Such functionalities enable organizations to optimize their lease management and effectively prepare for any lease obligations.

Copyright © 2018 Nakisa Inc. All rights reserved.5

The new lease accounting standards specify how organizations must recognize, measure, present, and disclose leases. The overall impact and effort is far more expansive than simply centralizing contract data and handling the initial recognition of right-of-use asset and lease liability. It requires subsequent measurement which involves amortization of the right-of-use asset and lease liability, accounting for lease modifications and providing quantitative disclosures. If an organization adopts the full retrospective method under IFRS 16 or modified retrospective method under ASC 842 without the transition relief, comparative numbers will need to be changed and there would be a need for parallel reporting. During the transition to the new standard, the lessee would need to know the overall liability (and ROU asset) balance they currently have under existing leases, and what the balance would be when they assess and classify these leases under the new standard. It’s important that any software solution incorporates the necessary functionally to produce the comparative reports.

Working out discounted cash flows to calculate lease liabilities (and ROU asset) can be extremely challenging to do at scale without specialized software. It becomes far more complicated when trying to aggregate a number of leased assets with different starting dates. The new standards provide guidance on how to measure and record ROU assets and lease liabilities at lease commencement, as well as subsequent measurements, modifications, and reassessments. Lease accounting technology should accelerate this process by centralizing data and automating accounting.

Your lease accounting technology must support the following lease accounting standards: FASB Topic ASC 842, IFRS 16, FASB Topic 840, IAS 17

Copyright © 2018 Nakisa Inc. All rights reserved. 6

| © 2017 Nakisa Inc. All Rights Reserved. nakisa.com

Full Lease Lifecycle Management for LesseesManaging Leases: From Inception to Termination and Beyond

Lease Determination Data Capturing Lease T&C and Contract Management

Classification, Amortization, Accruals & Payments

Event Management

Audit trail and Analytical & Regulatory Reporting

✓ Single repository for Lease Contract Administration and Lease Accounting

✓ Unit Tracking

✓ Track Approval Flow & Process

✓ Multi-GAAP and Multi-Ledger enabled (IFRS16 & ASC842)

✓ Segregate lease and non-lease items in payment

✓ Manages events (casualty, payment adjustments, modifications and more)

Lease Administration by Nakisa

As deadlines approach, organizations with considerable lease portfolios, with lease data dispersed both geographically and departmentally, may find adoption of the new standards to be rushed, complex, and challenging. What’s more, beyond the significant changes to accounting, the impact of the new standards will be far reaching from an operational perspective, placing additional pressure on internal resources and processes. Most organizations are undertaking an evaluation process to determine which lease accounting solutions are robust enough to tackle the changes made in the initial recognition, subsequent measurement and remeasurement of lease liability (and ROU asset) under the new standards.

End-to-End Lease Accounting It is not possible to effectively manage enterprise-wide leasing activities without understanding the context of the lease lifecycle. Without this context, leasing too easily can lapse into a disjointed series of ad hoc decision points with a high risk of key information falling through the cracks.

The following sections drill down for a deeper look at the lease lifecycle and detail how use of lease accounting technology can lay the foundation for implementing an end-to-end, closed loop approach. The goal here is to maximize efficiency, visibility, control, auditability, and cost-effectiveness of company-wide lease administration, while assuring compliance with the new standards.

Lifecycle of a Lease

A lease is a contract (i.e., an agreement between two or more parties that creates enforceable rights and obligations), or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (i.e., an identified asset) for a period of time in exchange for consideration.

Copyright © 2018 Nakisa Inc. All rights reserved.7

There are two main reasons why the data scope has changed significantly under the new lease accounting standards:

Contracts that had not been accounted for as leases in the past, may in fact meet the new definition of a lease. Some contracts include what are known as embedded leases. An embedded lease refers to the part of a contract that identifies assets that can be used and controlled. Therefore, a portion of the contract could be deemed as a lease contract, whereas the remaining portion could be considered as a service contact. Users may need to process both the service and the lease elements within the single solution to leave an appropriate audit trail.

Data Abstraction

Lay the foundation for your compliance initiatives by establishing a complete and accurate set of lease data. However, identifying, collecting, and organizing lease data can be a daunting task. The first step in the process is to develop a list of all of the data elements you need to collect. Your lease accounting software vendor should be able to provide a checklist of which data needs to be collected. In most cases, a data dictionary will be provided, outlining all of the fields in the solution. This makes it easy to identify what information is required from various stakeholders.

Examples of Data to Collect: Asset identification, Right to control, Purchase options, Lease terms, Payment process, Residual values

Copyright © 2018 Nakisa Inc. All rights reserved. 8

Under the current lease accounting standards, operating leases are typically reported off the balance sheet. As a result, most companies are able to comply by tracking estimated lease commitments. However, under the new lease accounting standards, tracking at the individual asset level will be required in order to capitalize and amortize each individual asset. Equipment leases frequently have multiple assets (potentially hundreds or thousands of assets) per lease schedule, increasing the volume and complexity of the accumulated data.

Before the effective date, organizations will need to bring all of their operating lease contracts into the solution. A tool to mass upload this data into the solution will streamline the initial data upload process. Commonly supported file types include .xls, .csv, and .txt. Look for a solution that supports the ability to attach images of lease documents into the solution. Data tagging is a helpful feature that allows users to tag areas of a lease document to make the data traceable for audit purposes.

Lease Determination

IFRS 16 and ASC 842 bring significant changes to lease accounting, particularly for lessees. The new standards contain a new definition of a lease. A contract is a lease, or contains a lease, if it conveys the right to control an identified asset for a period of time. However, there are a few additional considerations before you can determine if a contract is a lease or contains a lease: Who obtains substantially all of the economic benefit and has the right to direct use of the identified asset? Is the leased asset explicitly identified? Does the contract contain a lease as well as non-lease elements?

Lease accounting software can help streamline lease identification as well as help to determine the lease type. The new standards are complex enough for technical accountants. For non-accounting users a standard list of questions can be used to ensure accurate lease classification across an organization. Look for a solution that asks questions similar to the following to help with lease identification and determination:

01. Does the lease contain an identifiedasset?

02. Is this a service contract?

03. Does the customer have the right to obtain substantially all of the economic benefit from the use of the asset?

04. Is the lease for a low value asset?

05. Who has the right to direct how and for what purpose the asset is used throughout the lease term?

06. Is the lease term less than 12 months with no purchase option (IFRS) or no purchase option that is likely to be exercised (US GAAP)?

Copyright © 2018 Nakisa Inc. All rights reserved.9

Terms & Conditions and Initial Recognition

Under the new lease accounting standards, the initial measure of the lease liability by lessees could be different than the liability determined under the current standards. Initial recognition of the lease liability comes at the commencement date of a lease, where a lessee recognizes an ROU asset and a lease liability. At this stage, amortization schedules should be generated and filterable by contract level, schedule type, classification, and year. The ability to export amortization schedules allows for further analysis and sharing. Also, at this stage, any known payment terms and conditions should be captured. These terms and conditions can be the base amount or variable payments, escalating or step up rents, rents tied to an index, free rent periods, cash incentives, initial direct costs, prepaid costs, purchase options, extensions, and termination options. Look for a solution that makes managing terms and conditions easier, with the ability to add or hide fields as needed, as well as mass upload of many variable terms. Moreover, lease accounting technology should streamline lease management by applying terms and conditions when required, whether that’s at commencement or a contract event.

Accruals, Payments, and Event Management

It should go without saying that accounting capabilities are the most important part of any lease accounting solution. Regardless of which standard you need to comply with, IFRS 16, ASC 842, or both, the supporting lease accounting technology must share the same functionality and accounting capabilities. One key difference in the new rules is that certain changes in the decision to exercise the renewal, purchase, or termination options are subject to remeasurement of the lease liability (and ROU asset) and hence the lease liability (and ROU asset) is adjusted accordingly. With increasing balance sheet volatility, a lease accounting solution is required to determine the revised lease payments and recalculate the lease liability (and ROU asset).

Given the sheer size of most equipment lease portfolios, organizations will require a job scheduling feature to help automate the process further.

To avoid disruptions to your existing accounts payable process, look for a solution that can send payments to a lease reconciliation or a clearing account. Direct integration with an ERP system streamlines the payment process and makes it less prone to errors. Look for a solution that supports the capitalization of leased assets and liabilities in different batches at a different point in time, within the same contract, when they arrive. This is very helpful for handling fleet leases. Tracking by individual asset allows for unit specific amortization schedules and streamlines accounting for the casualty of a specific unit.

Copyright © 2018 Nakisa Inc. All rights reserved. 10

The new standards also provide guidance on how to measure and record lease modifications and reassessments. Lease accounting software should have functionality to address the entire breadth of enterprise lease accounting requirements, including modifications and reassessments, to ensure compliance with new lease accounting standards. In general, organizations should put significant focus on IFRS 16/ASC 842 event management during the vendor selection process to ensure that the solution is compliant with the new lease accounting standards.

As outlined in IFRS 16 and ASC 842, a reassessment occurs when there is a change in cashflows related to the initial contractual terms and conditions. A modification, on the other hand, results from renegotiation of original contractual terms and conditions.

Look for the following functionalities out-of-the-box to support compliance initiatives:

Compliance Requirements Functionality

Lessee classification:

IFRS 16 (low-value vs short-term vs long-term leases)

ASC 842 (short-term vs finance vs operating leases)

Periodic postings for low-value leases, short-term leases and service contracts

Initial measurement and recognition of ROU asset and lease liability

Subsequent measurement of ROU asset and lease liability (ASC 842 finance & IFRS 16)

Subsequent measurement of ROU asset and lease liability (ASC 842 operating)

Lease reassessments

Lease modifications

Impairment recognition

Lease termination

Disclosure reports

Analytics and Reporting

Financial stakeholders require information in different formats, with various delivery requirements. Preparing reports to meet the demanding requirements of various stakeholders can be a daunting

| © 2017 Nakisa Inc. All Rights Reserved. nakisa.com

ReportingCentralized solution for contract data abstraction and compliance

Management Reports

Reconciliation Reports

Disclosure Reports

Copyright © 2018 Nakisa Inc. All rights reserved.11

| © 2017 Nakisa Inc. All Rights Reserved. nakisa.com

ReportingCentralized solution for contract data abstraction and compliance

Management Reports

Reconciliation Reports

Disclosure Reports

task. Lease accounting software should provide users with ad hoc access to global lease data in lists, charts, graphs, and tables in order to simplify the consumption of information. Finance teams should be able to view a high-level overview, easily collect reconciliation data, and share reports and dashboards with necessary stakeholders.

Key analytic and reporting features to look for: IFRS / GAAP-compliant report production, User specific reports and dashboards, Snapshot view of entire lease Portfolio, Dynamic filtering with drill-down capabilities

There are a few types of reports that should be included out-of-the-box to help facilitate lease management and accounting:

Disclosure reports are the quantitative requirements described in the new lease accounting standards. Look for a solution with disclosure reports that have been designed to provide the necessary information to prepare the required disclosures under IFRS 16 and ASC 842. Disclosure reports should provide users with a comprehensive overview of an entity’s leasing activities. Disclosure reporting, in connection with financial statements, are essential to an investor’s understanding of an organization’s current financial reality. Types of disclosure reports include liability balances, ROU asset roll forward, lease cost, cash flow, weighted average discount rate, and weighted average lease term.

Management reports are designed to enable managers and other relevant stakeholders to review the details for individual leases and portfolio items, and to review summary information that provides a high-level analysis of their current lease commitments. Management reports are typically set up to display the most critical information on a lease portfolio. Dynamic filtering capabilities allow users to

Copyright © 2018 Nakisa Inc. All rights reserved. 12

drill-down into specific leases that require a closer look. From here, it should be easy to trigger relevant actions and collaborate with other users.

Reconciliation reports provide a detailed list of all transactions that have been posted by a lease accounting system. They confirm whether the money leaving an account matches the amount that has been spent, ensuring the two are balanced at the end of the recording period. These reports are useful for reconciliation purposes and audit trails

Technical Considerations

Business requirements are important during the vendor selection process. But, don’t forget to evaluate technical considerations as well.

Integration

To support compliance initiatives for IFRS 16 and ASC 842 compliance, most large organizations will require an end-to-end lease accounting solution. To leverage the power of these solutions, they must be able to handle bi-directional communication with their core ERP system. When evaluating end-to-end lease accounting solutions, companies will most likely consider: out-of-the-box solutions, customized software, and self-developed products. When selecting a solution, the best-practice is out-of-the-box software as it represents integration/customizations savings and significant risk avoidance. The new lease accounting standard will affect the balance sheet of lessees in two ways. The lessees (users) will need to create an asset and a liability of the ROU asset or the leased asset. The accounting of both asset and liability are equally important. Integration with ERP system(s) is very important as lease liabilities and ROU assets will go through frequent remeasurements due to changes in the lease terms and conditions, and also due to changes in user decisions in terms of extension and termination. With compliance deadlines approaching quickly, you can’t afford any additional risks from customizations and need to ensure that your timelines are maintained.

Copyright © 2018 Nakisa Inc. All rights reserved.13

This late in the game, organizations should avoid 3rd party integrations as they often require highly complex customization projects. These projects tend to involve significant near-term and long-term risks in addition the upfront and recurring costs for customization hours. Look for a solution that natively integrates with your existing ERP system.

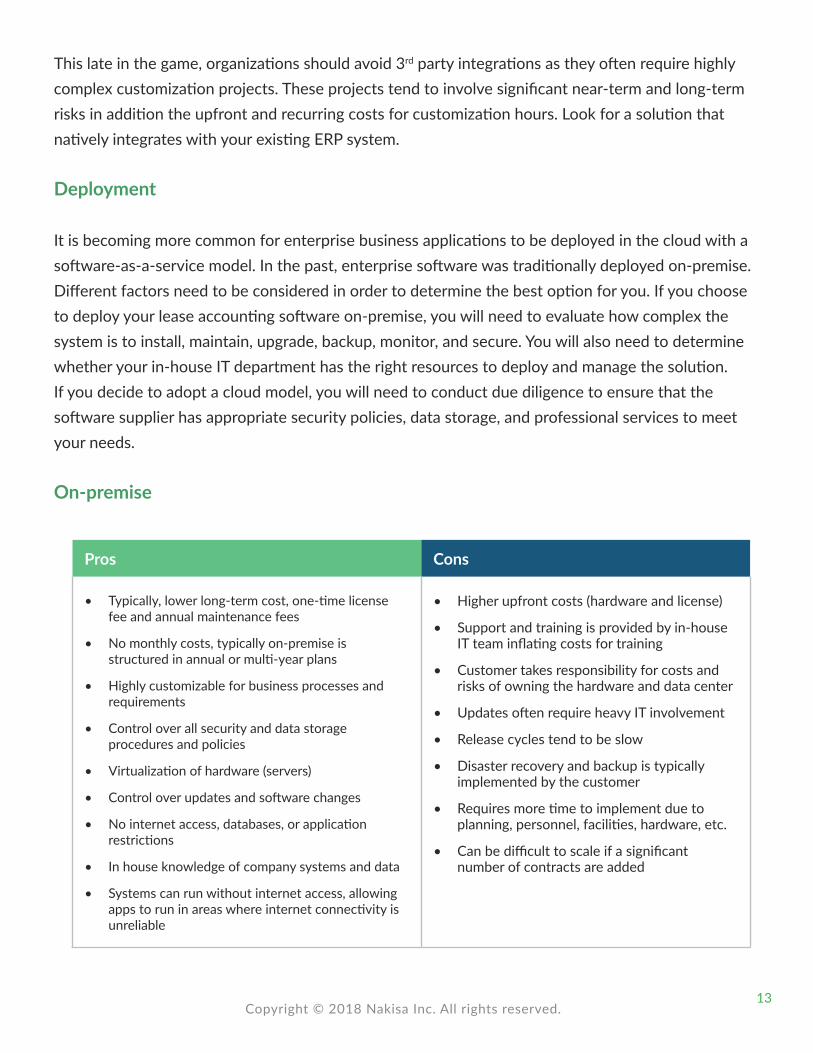

Deployment

It is becoming more common for enterprise business applications to be deployed in the cloud with a software-as-a-service model. In the past, enterprise software was traditionally deployed on-premise. Different factors need to be considered in order to determine the best option for you. If you choose to deploy your lease accounting software on-premise, you will need to evaluate how complex the system is to install, maintain, upgrade, backup, monitor, and secure. You will also need to determine whether your in-house IT department has the right resources to deploy and manage the solution. If you decide to adopt a cloud model, you will need to conduct due diligence to ensure that the software supplier has appropriate security policies, data storage, and professional services to meet your needs.

On-premise

Pros Cons

• Typically, lower long-term cost, one-time license fee and annual maintenance fees

• No monthly costs, typically on-premise is structured in annual or multi-year plans

• Highly customizable for business processes and requirements

• Control over all security and data storage procedures and policies

• Virtualization of hardware (servers)

• Control over updates and software changes

• No internet access, databases, or application restrictions

• In house knowledge of company systems and data

• Systems can run without internet access, allowing apps to run in areas where internet connectivity is unreliable

• Higher upfront costs (hardware and license)

• Support and training is provided by in-house IT team inflating costs for training

• Customer takes responsibility for costs and risks of owning the hardware and data center

• Updates often require heavy IT involvement

• Release cycles tend to be slow

• Disaster recovery and backup is typically implemented by the customer

• Requires more time to implement due to planning, personnel, facilities, hardware, etc.

• Can be difficult to scale if a significant number of contracts are added

Copyright © 2018 Nakisa Inc. All rights reserved. 14

Cloud

Pros Cons

• Lower upfront costs

• Maintenance costs may be lower in that they can be included in monthly costs and not as additional fees

• Cloud storage costs are decreasing allowing customers to purchase additional storage without significant cost increases

• Most providers maintain very secure environments

• Cloud services can be deployed in a matter of days/weeks/months because hardware and software are not needed

• Easy to scale as the required number of contracts increases/decreases

• Less IT involvement and less in-house technical skill is required for deployment, updates, and changes

• Vendor manages updates and backups

• Available on most devices anytime anywhere (with an internet connection) for easy access for remote workers

• Customers are subject to more frequent price increases due to the monthly pricing structure and lack of control over software updates and changes

• Premium support is usually only available with an added cost

• Little customization available for company specific needs

• Existing, customized integrations with on-premise systems or other cloud solutions can become unstable during upgrades due to rapid release and update schedules of cloud services

• Less control over security policies

• Some customers may not be able to ascertain exactly where data is stored or who truly has access to it

• Without an active internet connection, cloud-based solutions do not work

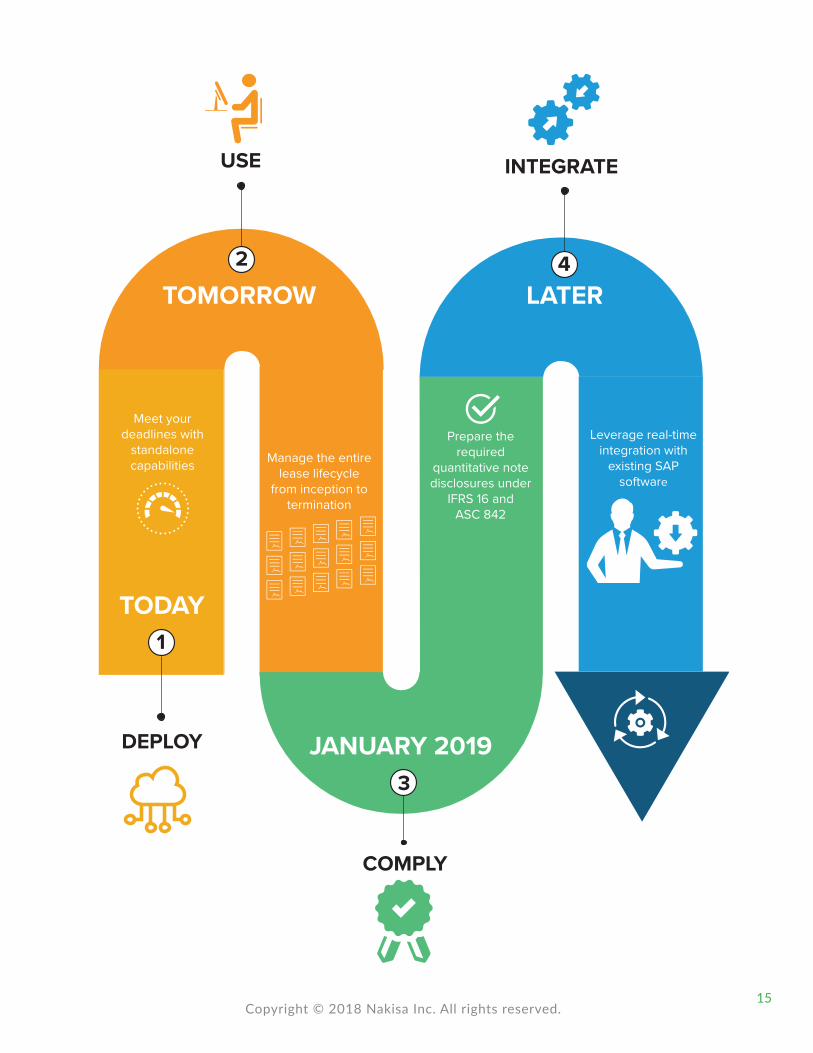

Standalone

The effective dates for the new standards are fast approaching. During implementation, one of the most time-consuming steps is integration and configuration with existing accounting and financial systems. Consider a solution with standalone capabilities to help accelerate the timeline from data collection to lease accounting. The best lease accounting systems will be able to stand on their own and help you make your compliance deadlines. Look for a solution where you retain the option of integration with your ERP system at any time. With such a short time horizon until the effective dates, the value of the additional time savings is incalculable. However, you won’t want to indefinitely defer the complex topic of ERP integration. Standalone capabilities can reduce your total implementation-footprint, provide faster access to a lease accounting solution that supports your IFRS 16 and ASC 842 compliance initiative, and accelerate adoption.

Copyright © 2018 Nakisa Inc. All rights reserved.15

1

2

3

4

DEPLOY

TODAY

TOMORROW

JANUARY 2019

LATER

COMPLY

Meet yourdeadlines with

standalonecapabilities

USE

Manage the entire lease lifecycle

from inception to termination

Prepare the required

quantitative note disclosures under

IFRS 16 and ASC 842

INTEGRATE

Leverage real-time integration with

existing SAP software

Copyright © 2018 Nakisa Inc. All rights reserved. 16

Buyer Beware

Real-Estate Lease Accounting Systems

Due to the single-asset nature of real-estate leases, real-estate focused applications don’t typically support tracking by individual units.

Many companies are tempted to use real-estate leasing solutions to manage equipment leases. However, the moveable assets and the way they are administered are very different from real-estate assets. Some differences are rather obvious. For example, real-estate leases are for land or building structures such as corporate offices, distribution centers, or manufacturing plants. Equipment leases represent a much more diverse category of assets from coffee machines to rail cars. The fundamental difference between equipment and real-estate leases is the number of units leased in a specific contract. Real-estate contracts may have a single unit whereas equipment contracts may have thousands of units within the same contract. Real-estate rents are market driven and are often based on a utility metric such as cost per square foot, whereas equipment lease rents are based on lease rate factors. These are just a few of the ways in which real-estate and equipment leases differ.

Organizations with very small equipment lease portfolios might be able to “make do” with an alternative leasing solution. However, organizations with large equipment lease portfolios will certainly require a dedicated solution. You will need to dig deeper than readily available marketing materials to understand a product’s ability to meet the needs of your complex lease portfolio. You may be surprised to find that many real-estate focused applications do not support the complexities of equipment leases such as (but not limited to) significant quantities, complexities associated with usage of assets, casualties, replacement of a single unit within a contract of multiple units.

Acquiring a Lease Accounting SolutionIt is common practice for organizations to seek out multiple bids for purchases to ensure that they are obtaining the most favourable price and contractual terms from vendors. The competitive bidding process can be used to ensure you obtain the best financing rates and contractual terms on your lease accounting software. The challenge of procurement is that it can take weeks, if not months, to complete an RFP process. Perhaps, the most time-intensive part of the procurement process is recruiting the right vendors to bid. To help attract the right vendors, make sure you give them the full picture. The following list of solution requirements can be used to help produce an RFP that includes the most important features of a lease accounting solution.

Copyright © 2018 Nakisa Inc. All rights reserved.17

Solution Requirements

Requirement Description Vendor 1 Vendor 2 Vendor 3

Data Abstraction

Centralized RepositoryAbility to group leases together in a single repository using a variety of criteria

Mass Data UploadData ingestion capabilities of the software (ability to ingest real-time vs. manual)

Upload File Types Supported flat files (.xls, .csv, .txt, etc.)

File Download Ability to download all data related to a master lease agreement

Standard FieldsStandard data elements that must be captured during the data abstraction process

Custom Fields Ability to configure the software to capture additional fields

Lease Documentation Ability to attach scanned lease documents

Lease Documentation File Types

Supported lease documentation file types (JPEG, TIFF, PDF, doc., etc.)

Data Tagging Ability to tag and highlight areas of attached documents for traceability

Contract Management

Search Functionality Solution’s search functionality including a list of searchable fields

Lease Determination Ability to standardize lease classification using a questionnaire

Override Ability for a user to override the lease classification

Copyright © 2018 Nakisa Inc. All rights reserved. 18

Hierarchy Display Ability to manage contracts using a multi-level contract structure

Asset Level Ability to track different components of a lease at the asset level

Alerts Configurable alerts and notifications

Approval Workflow Engine Solution approval workflow around lease accounting

Critical DatesAbility to track critical dates for end of term renewals, buyouts, and terminations

Terms & Conditions

Ability to add or upload the following terms:

• Base rent• Extensions• Payment reductions• Pre-payments• Index payments• Free rent• Cash incentives• Initial direct costs• Termination options• Purchase options

Financial Schedules

Ability to generate the following financial schedules:

• Lease liability amortization• Non-lease payment• Total payment schedules• Rent expense • Asset depreciation

Posting Schedule Ability to view accrual and payment postings

Amortization ScheduleAbility to create a lease liability and ROU asset amortization schedule for each lease

Automatic Postings Ability to post automatically to a connected ERP system

Copyright © 2018 Nakisa Inc. All rights reserved.19

On-demand Postings Ability to post manually to a connected ERP system

Audit LogAbility to view a list of all changes that have been made at any level of a contract structure

Master Data Update Ability to update master data

Service Contract Management

Ability to process service contracts in the system

Short-term Leases Ability to handle short-term leases, including extension and conversion

Lease Types Support for all types of leases

Accounting Capabilities

IFRS 16 Support for the new IASB lease accounting standard

IAS 17 Support for the current IASB lease accounting standard

FASB ASC 842 Support for the new US GAAP standard

FASB Topic ASC 840 Support for the current US GAAP standard

Multiple General Ledgers Ability to publish debits and credits to multiple general ledgers

Reassessments

Ability to record reassessments including

• Purchase options• Termination options• Extensions• Expected GRV amounts

Lease Modifications

Ability to add new terms and conditions, modify existing terms and conditions, and change the contract rate

Copyright © 2018 Nakisa Inc. All rights reserved. 20

Change Contracts

Ability to edit fields in a contract that do not have financial impact including

• Lessor • User notifications• Description

Asset Casualties Ability to enter casualty events

Adjustment Postings

Ability to view adjustment postings that result from performing a lease modification, reassessment, or casualty

Transition AccountingAbility to support transition accounting under IFRS 16 and ASC 842

Auditing and Reporting

Standard Reports Standard reports that come pre-configured with the application

Disclosure Reporting

Disclosure reporting with support for new leasing standards including a quantitative analysis of

• Liability balances• Lease cost disclosure• Cash flow• Weighted average discount rate• Weighted average lease term

Comparative ReportingAbility to create reports that compare journal entries from two different ledgers (ex. 840 & 842)

Roll Forward Ability to create roll forward reports that summarize changes during a given period

Management ReportsAbility to produce reports that allow managers to quickly understand the various levels of a lease contract

Custom Reports Ability to create custom reports to support additional analysis

Copyright © 2018 Nakisa Inc. All rights reserved.21

ReconciliationAbility to view a detailed list of all transactions that have been posted in a given period

Technical

International SearchAbility to publish smart search results to the end user where international characters are “flattened” or unused

Multilingual Ability to use the system in multiple languages including ___

Parallel Currencies Ability to write back to an ERP system in parallel currencies

Concurrent Users Ability to handle ___ number of concurrent users

Number of Lease Contracts Ability to handle ___ number of leases and scale up

Mobile Ability to access the application on mobile and tablet devices

Customizable UIAbility to customize the user interface including the ability to add or hide data fields

Integration Native integration with ___ ERP system

Standalone Capabilities Ability to use the solution without integrating with an ERP system

Information Security

Role-based Access Ability to limit features/functionality based on a user’s role

Single Sign-On Single sign-on capabilities

Data Scoping Ability to limit what data a user can see

Data Privacy Policy for securing confidential information

Copyright © 2018 Nakisa Inc. All rights reserved. 22

Security Audits Third-party security audit verification

Deployment

Cloud

Backup Backup of system, content and database files

Monitoring 24x7 monitoring of application performance

Security Data encryption, firewalls, intrusion detection

Upgrades Frequency and level of support required from customer

On-Premise

Operating Systems Support for Linux and Windows

Professional Services

Implementation Approach Typical implementation approach and model

Data Abstraction Process for capturing lease data and uploading it into the system

Training Availability of online or in-person training for users and administrators

Deployment Services Support for installation, upgrades, and integration

Accounting AdvisoryAny accounting services available to support transition to the new standards

Configuration (put it somewhere product related)

Level of customization or configuration typically required to get the system up and running

Implementation Timeline Typical implementation timeline and key milestones

Copyright © 2018 Nakisa Inc. All rights reserved.23

Implementation Partners Implementation partners

Customer Support

User Community Existing user community

Support Availability Days and times for technical and business support

Point of Contact Contact information for a designated support contact

Support Channels Channels available for support

Customer Satisfaction How vendors ensure customer satisfaction

Documentation Documentation available to end users

User Conference User conferences including the frequency and forum

Billing Billing process for professional services

Vendor

Corporate History Brief overview of your corporate history

Business Strategy Vendor’s vision, business strategy, or growth plan

Number of Customers Number of customers currently using your lease accounting software

Customer ReferralsCustomers using the vendor’s software and with contacts for reference

Partnership Alliances or partnerships with the big 4 or regional accounting firms

Accounting Expertise Number of CPAs the vendor has on staff