2017 fall national meeting - national association of ... · john d. doak, chair oklahoma mike...

TRANSCRIPT

2017 Fall National Meeting

© 2017 National Association of Insurance Commissioners

Property and Casualty Insurance (C) Committee

December 3, 2017 Honolulu, Hawaii

© 2017 National Association of Insurance Commissioners 1

Date: 11/29/17

2017 Fall National Meeting Honolulu, Hawaii

PROPERTY AND CASUALTY INSURANCE (C) COMMITTEE

Sunday, December 3, 2017 1:00 – 2:30 p.m.

Hawaii Convention Center—Room 313 AB—Level 3

ROLL CALL John D. Doak, Chair Oklahoma Mike Chaney Mississippi David Altmaier, Vice Chair Florida Matthew Rosendale Montana Jim L. Ridling Alabama John G. Franchini New Mexico Katharine L. Wade Connecticut Jean Straight Oregon Jennifer Hammer Illinois Jessica Altman Pennsylvania James J. Donelon Louisiana Raymond G. Farmer South Carolina Al Redmer Jr. Maryland Larry Deiter South Dakota Chlora Lindley-Myers Missouri NAIC Support Staff: Aaron Brandenburg/Kris DeFrain/Eric Nordman

AGENDA

1. Consider Adoption of its Interim Minutes—Commissioner John D. Doak (OK) Attachment One

2. Consider Adoption of its Task Force and Working Group Reports Attachment Two

—Commissioner John D. Doak (OK) • Casualty Actuarial and Statistical (C) Task Force—Michael McKenney (PA) • Surplus Lines (C) Task Force—Commissioner James J. Donelon (LA) • Title Insurance (C) Task Force—Director Larry Deiter (SD) • Workers’ Compensation (C) Task Force—Director Lori K. Wing-Heier (AK) • Advisory Organization Examination Oversight (C) Working Group—Timothy Schott (ME) • Auto Insurance (C/D) Working Group—Commissioner Allen W. Kerr (AR) • Catastrophe Insurance (C) Working Group—Commissioner David Altmaier (FL) • Climate Change and Global Warming (C) Working Group—Commissioner Mike Kreidler (WA) • Creditor-Placed Insurance Model Act Review (C) Working Group—Commissioner David Altmaier (FL) • Medical Professional Liability (C) Working Group—Superintendent John G. Franchini (NM) • Public Adjuster (C/D) Working Group—Commissioner John D. Doak (OK) • Sharing Economy (C) Working Group—Commissioner Dave Jones (CA) • Terrorism Insurance Implementation (C) Working Group—Martha Lees (NY) • Transparency and Readability of Consumer Information (C) Working Group—Angela Nelson (MO) • Travel Insurance (C) Working Group—Commissioner Al Redmer Jr. (MD)

3. Hear a Presentation from FEMA Regarding the National Flood Insurance Program

—Roy Wright (Federal Emergency Management Agency—FEMA)

4. Hear Updates from the States and Jurisdictions Related to Recent Catastrophes Attachment Three —Commissioner John D. Doak (OK)

• Puerto Rico • Virgin Islands • Others

© 2017 National Association of Insurance Commissioners 2

5. Discuss the Modernization of Commercial Lines Attachment Four —Dave Snyder (Property Casualty Insurers Association of America—PCI)

6. Hear a Presentation from States Title—Adrienne Harris (States Title) Attachment Five

7. Discuss Any Other Matters Brought Before the Committee—Commissioner John D. Doak (OK)

8. Adjournment

W:\National Meetings\2017\Fall\Agenda\C Cmte.docx

© 2017 National Association of Insurance Commissioners

Attachment One Consider Adoption Interim Minutes

Attachment Property and Casualty Insurance (C) Committee

12/--/17

© 2017 National Association of Insurance Commissioners 1

Draft: 11/20/17

Property and Casualty Insurance (C) Committee Conference Call

November 9, 2017 The Property and Casualty Insurance (C) Committee met via conference call Nov. 9, 2017. The following Committee members participated: John D. Doak, Chair, and Buddy Combs (OK); David Altmaier, Vice Chair (FL); Jim L. Ridling represented by Charles Angell (AL); Katharine L. Wade represented by George Bradner (CT); Jennifer Hammer represented by Brett Gerger (IL); James J. Donelon (LA); Al Redmer Jr. represented by Cathy Grason (MD); Chlora Lindley-Myers represented by Angela Nelson (MO); Mike Chaney (MS); John G. Franchini represented by Ashley Hernandez (NM); Raymond G. Farmer and Kendall Buchanan (SC); and Larry Deiter (SD). Also participating were: Ken Allen (CA); Martha Lees (NY); and Marianne Baker, Cassie Brown, Debra Knight, Jamie Walker and Mark Worman (TX). 1. Adopted its Summer National Meeting Minutes Commissioner Altmaier made a motion, seconded by Commissioner Chaney, to adopt the Committee’s Aug. 8 minutes (see NAIC Proceedings – Summer 2017, Property and Casualty Insurance (C) Committee). The motion passed.

2. Adopted its 2018 Committee Charges

Commissioner Doak provided an overview of the 2018 proposed charges for the Committee and its working groups (Attachment ___). He said the 2018 proposed charges were similar to the 2017 charges, with a couple of suggested additions. Commissioner Doak explained the Committee received a referral from the Producer Licensing (D) Task Force on Oct. 13 asking the Committee to consider developing a white paper on pet insurance, to include a review of coverage options, product approval, marketing, rating and claims practices. Director Farmer made a motion, seconded by Commissioner Donelon, to adopt a new charge related to pet insurance. The motion passed. Commissioner Doak said the Climate Change and Global Warming (C) Working Group suggested an additional charge related to reviewing standards for a climate-related financial disclosure. He suggested the Committee defer this charge and perhaps discuss the issue at the Executive (EX) Committee. Commissioner Doak said the revised charges would direct a Lender-Placed Insurance Model Act (C) Working Group to focus on drafting a new model related to lender-placed insurance as it relates to mortgages. He said the model having to do with creditor-placed auto insurance, the Creditor-Placed Insurance Model Act (#375), has been open since 2013 and he would like to see the new model be completed soon. Birny Birnbaum (Center for Economic Justice—CEJ) said he opposes the change, because the existing charge already allows for the development of a model related to lender-placed insurance for mortgages. He said the new charge would eliminate the ability to make changes related to creditor-placed auto insurance, noting that the same issues that affect lender-placed homeowners insurance affect creditor-placed auto insurance. He noted that Wells Fargo falsely force-placed auto insurance policies. He said the current Model #375 is not strong enough to protect consumers. He said the Working Group should continue to work on both models. Commissioner Chaney made a motion, seconded by Director Deiter, to adopt the revised charge related to lender-placed insurance. The motion passed. 3. Heard an Update on the National Flood Insurance Program Brooke Stringer (NAIC) said the current reauthorization of the National Flood Insurance Program (NFIP) expires Dec. 8. She said the U.S. House of Representatives may vote during the week of Nov. 13 on a five-year NFIP reauthorization bill composed of seven individual flood reform bills that were approved by the House Financial Services Committee this summer.

Attachment Property and Casualty Insurance (C) Committee

12/--/17

© 2017 National Association of Insurance Commissioners 2

Ms. Stringer said the key themes of the bill have to do with choice, competition and addressing repetitive loss properties. She said the bill had stalled, but House Financial Services Committee Chairman Jeb Hensarling (R-TX) recently announced an agreement on the legislation with House Majority Whip Steve Scalise (R-LA). Some of the compromise areas are related to annual rates, multiple loss properties, excessive lifetime claims and lowering future risks to the NFIP. She said some of the policy provisions from the “NAIC Principles for National Flood Insurance Program (NFIP) Reauthorization” are included in the House package, including the Private Flood Insurance Market Development Act (H.R. 1422), which is sponsored by U.S. Rep. Dennis Ross (R-FL). Ms. Stringer said even if the House passes its reauthorization bill, it faces a difficult time in the U.S. Senate, where several NFIP proposals have been introduced. She said a lot of work will need to be done to reconcile all the outstanding policy issues in both chambers prior to the NFIP’s Dec. 8 expiration, noting that an additional short-term extension is possible. Commissioner Doak asked whether the NAIC would need to draft any other letters in support of legislation. Ms. Stringer said the NAIC wrote letters in favor of H.R. 1422, most recently in July. Commissioner Doak noted that Roy Wright (Federal Emergency Management Agency—FEMA) will address the Committee at the Fall National Meeting.

4. Heard State Updates Related to Recent Catastrophes

a. Florida Commissioner Altmaier said, all things considered, the response to Hurricane Irma has gone as smoothly as one could hope. He said Florida is posting claims data on the department’s website. As of Nov. 3, 809,000 claims were filed, not including NFIP claims. He said the estimated losses for those claims are $5.5 billion. He said the claims are starting to level out a bit. He said most homeowners are insured by Florida domestic insurers, noting that the department is closely monitoring the capacity of each company. He said the department is not seeing anything of significant concern, but said it will be interesting to see what happens with reinsurance renewals. Commissioner Altmaier said the biggest issue in Florida has to do with the availability of claims adjusters. He said insurance companies indicated contractors were initially in Texas when Hurricane Irma hit and then many left for California to deal with wildfire claims. Because of this, loss adjustment expenses might be higher than one would anticipate due to the lack of availability of adjusters. He questioned whether anything could be done to solve that issue. He said the department will continue to monitor the claims process and work with the department’s Consumer Division. He said there is nothing that warrants a market conduct concern at this point. Commissioner Doak said the Committee should look at the issue of adjuster capacity. Mr. Bradner asked what would have happened if Hurricane Irma had continued on its original path. Commissioner Altmaier said the original path was projected to directly hit Miami as a Category 4 hurricane. He said all Florida property might have been subject to hurricane-strength winds. He said Florida conducts analyses to assess the ability of carriers to respond to various events. He said the state also conducts stress testing to model historic events.

b. Texas Ms. Brown said Hurricane Harvey hit Texas twice on Aug. 25 with two different landfalls. She said the department sent staff to disaster recovery centers to assist consumers with contacting insurers, minimizing losses and processing claims. She said fraud investigators were deployed to make sure contractors complied with law. She said the consumer help line was extended and the state coordinated with FEMA concerning the NFIP. She said a website was developed that provided assistance post-Harvey. Ms. Brown said the state processed requests for emergency adjuster licenses. The state also issued a data call related to claims, with the first data due Oct. 31. She said the state issued numerous bulletins with information for insurers on issues such as grace periods and underwriting. Ms. Baker said Texas coordinated with the NAIC in order to bring volunteers in to assist from other states. She said the state handled 3,900 consumer calls through Oct. 23. She said the state had received about 426 complaints. The fraud unit has talked to homeowners, warning about fraudulent adjusters and contractors.

Attachment Property and Casualty Insurance (C) Committee

12/--/17

© 2017 National Association of Insurance Commissioners 3

Ms. Walker said there had been about 7,500 adjuster licensing applications and 8,500 emergency adjuster licenses. She said the state issued 13,000 total adjuster licenses. She said a priority was put on having adjusters in the field. She said the state waived late fees and suspended penalties for deficient education hours. Ms. Knight said the state issued 11 bulletins on Oct. 26. She said many of these bulletins were drafted before the storm hit. The bulletins provided guidance that insurers would need such as waiving prior authorization requirements and grace periods for premium payments. She said later bulletins responded to emerging issues such as confusion over wind versus water. She said there ended up being a total of 23 bulletins issued. Ms. Baker said Texas issued claims-handling extensions. She said the Texas Windstorm Insurance Association (TWIA) also sought some extensions. She said the TWIA had more than 70,000 claims, with an ultimate loss of $1.13 billion. She said there were more than 90,000 NFIP claims, with a total payout of $4.3 billion. Mr. Worman explained the Texas data call is mandatory for all admitted and surplus lines insurers. Data is first due Oct. 31 and updates are due on the 15th of the month. He said other jurisdictions might be able to use their bulletin, data call and other information. Commissioner Chaney asked what the states are doing about flooded automobiles. He said there are about 1 million vehicles that are a total loss. Mr. Worman said Texas issued a bulletin related to salvage titles. He said Texas statute puts the duty on insurers to make sure total loss vehicles are retitled or salvaged. Commissioner Doak said there are some national databases that track vehicles with salvage titles. Commissioner Altmaier said there are 200,000 to 300,000 total loss vehicles resulting from Hurricane Irma. He said several states have issued consumer alerts. An NAIC consumer alert on the issue was subsequently distributed to the Committee. Mr. Byrd said the states should emphasize with insurers that there has to be a certificate of destruction on the vehicle and it cannot be titled again, noting that, often, the vehicle identification number must be removed. Mr. Birnbaum asked whether the states have monitored a potential spike in mortgage and auto loan delinquencies through lender-placed auto or homeowners insurance within data calls. Mr. Worman said lender-placed insurance is not broken out within the Texas data call. He said Texas is not monitoring spikes in lender-placed insurance placements. Commissioner Doak said the states typically monitor the markets through their consumer assistance divisions. Commissioner Altmaier said Florida did not break out lender-placed insurance within the data call, but does monitor data points to see if there are spikes warranting additional review. Mr. Birnbaum said some states exempt lender-placed insurance because they consider it to fall under credit insurance. Mr. Worman said lender-placed insurance would fall under commercial property insurance in Texas. Commissioner Doak said there may be a higher number of military individuals who have this type of coverage.

c. South Carolina Ms. Buchanan said South Carolina has had three consecutive years with a catastrophic event. She said Hurricane Irma did minimal damage in South Carolina, so the department was able to forgo some actions such as emergency regulations and extending the consumer call center. She said South Carolina issued a data call using the NAIC template. She said this is the third consecutive year South Carolina has issued a catastrophe data call. The current data call requests data in two time periods. She believes Hurricane Irma will have about one-tenth the losses of Hurricane Matthew. So far, the data call has found $90 million in incurred losses with 17,000 claims reported. She said the second and last report is due Jan. 8. She also said South Carolina has permitted 2,400 emergency adjusters. She said most damage has been related to storm surge in coastal counties. Ms. Buchanan said South Carolina used essentially the same bulletins and data calls as prior events.

d. California Mr. Allen provided an update on wildfires that have recently occurred in California. He said, as of Oct. 31, 15 major insurers have reported losses exceeding $3 billion. He said 43 lives have been lost and more than 10,000 partial residential properties have been damaged, with 4,000 total losses to residential property. He also said there have been 3,200 personal automobile losses. He said the department has 25 to 30 consumer assistance personnel out in the field. He said department detectives have educated consumers on how not to be victimized. Consumer service team members are meeting with consumers and

Attachment Property and Casualty Insurance (C) Committee

12/--/17

© 2017 National Association of Insurance Commissioners 4

helping with the claims process. Mr. Allen said Commissioner Dave Jones (CA) has issued a notice to insurers to expedite claims. The notice includes the voluntary expedited claims-handling guidelines to which most insurers agreed. He also said insurers are able to bring in out-of-state claims adjusters. He said California issued bulletins regarding solicitation and compensation requirements regarding public adjuster work.

Commissioner Doak said the Committee should work on creating a database of information available to all jurisdictions so they can use similar language in bulletins and other documentation.

e. Puerto Rico and U.S. Virgin Islands

Mr. Bradner asked if there was an update related to hurricanes affecting Puerto Rico. Commissioner Doak said he hopes Puerto Rico and the U.S. Virgin Islands are able to provide an update in the future. He said the NAIC has assisted by having Puerto Rico employees work in the NAIC Central Office in Kansas City, MO, as well as by drafting bulletins and a data call.

5. Heard Updates on the Status of Working Groups

a. Public Adjuster (C/D) Working Group

Mr. Combs said the Public Adjuster (C/D) Working Group plans to finish its work by the end of year. He said the Working Group has decided to create three documents that insurance companies could use: 1) a notice to consumers regarding public adjuster roles and what to look out for; 2) an insurance industry advisory to make sure differences are understood between the different types of adjusters; and 3) an advisory to contractors letting them know what can and cannot be done in the claims settlement process. He said the Working Group’s next call is Nov. 27, and it hopes to present its final product to the Committee at the Fall National Meeting.

b. Terrorism Insurance Implementation (C) Working Group

Ms. Lees said all states, led by the New York State Department of Financial Services, have conducted a data call for the past two years collecting terrorism risk insurance data from commercial insurers. She said the Federal Insurance Office (FIO) has also had a data call over that time. The states and the FIO have recently had discussions related to a joint data template. She said the states hope to release additional information concerning the 2018 data call in the next few weeks.

Mr. Birnbaum asked what information the FIO wants that requires a separate data call. Ms. Lees said the FIO has collected data at a higher level of granularity than the states.

c. Transparency and Readability of Consumer Information (C) Working Group

Ms. Nelson said the Working Group has been working on a request from the NAIC/Consumer Liaison Committee to consider the development of consumer resources tailored to flood insurance. She said the Working Group will focus on this work throughout 2018.

Having no further business, the Property and Casualty Insurance (C) Committee adjourned.

W:\National Meetings\2017\Fall\Cmte\C\11-09\11-9.docx

© 2017 National Association of Insurance Commissioners

Attachment Two Consider Adoption of its Task Force and

Working Group Reports

© 2017 National Association of Insurance Commissioners

Casualty Actuarial and Statistical (C) Task Force

© 2017 National Association of Insurance Commissioners 1

2017 Fall National Meeting

Honolulu, Hawaii

CASUALTY ACTUARIAL AND STATISTICAL (C) TASK FORCE Sunday, December 3, 2017

12:00 – 1:00 p.m.

Meeting Summary Report The Casualty Actuarial and Statistical (C) Task Force met Dec. 3, 2017. During this meeting, the Task Force: 1. Adopted its Summer National Meeting minutes.

2. Adopted its Nov. 14 and Oct.2/Sept. 12 minutes, which included the following action:

a. Adopted its 2018 proposed charges.

3. Adopted the report of the Actuarial Opinion (C) Working Group, including the Oct. 5, Sept. 26, Sept. 5, Aug. 22, and Aug. 15 minutes. During these meetings, the Working Group took the following action: a. Adopted the 2017 Regulatory Guidance on Property and Casualty Statutory Statements of Actuarial Opinion

(Regulatory Guidance). 4. Adopted the report of the Statistical Data (C) Working Group, including adoption of the Report on Profitability by Line

by State in 2016.

5. Summarized training on predictive modeling.

6. Heard reports on the status of the NAIC’s Appointed Actuary Job Analysis Project and on the charge regarding development of an Appointed Actuary Attestation of Qualification.

7. Heard reports from the American Academy of Actuaries (Academy) regarding the activities of its Committee on

Property and Liability Financial Reporting (COPLFR), its Council on Professionalism and its Casualty Practice Council.

8. Heard reports from the Casualty Actuarial Society (CAS) and the Society of Actuaries (SOA) on property casualty actuarial research.

W:\National Meetings\2017\Fall\Summaries\Final Summaries\CASTF.docx

© 2017 National Association of Insurance Commissioners

Surplus Lines (C) Task Force

© 2017 National Association of Insurance Commissioners 1

Conference Call

(In lieu of meeting at the 2017 Fall National Meeting)

SURPLUS LINES (C) TASK FORCE November 27, 2017

Summary Report

The Surplus Lines (C) Task Force met Nov. 28, 2017. During this meeting, the Task Force: 1. Adopted its Aug. 6 minutes, which included the following action:

a. Adopted its 2016 Spring National Meeting minutes. b. Adopted its 2018 proposed charges. c. Heard a report on a nonadmitted accident and health (A&H) and excess disability survey results. d. Heard an update on the Flood Insurance Market Parity and Modernization Act (H.R. 1422/S. 563).

2. Adopted a report from the Surplus Lines (C) Working Group.

3. Heard an update from the Nonadmitted A&H/Disability Drafting Group. 4. Heard an update on the Flood Insurance Market Parity and Modernization Act (H.R. 1422/S. 563).

5. Heard a discussion on the future collection processes of U.S. exposure related to the federal Terrorism Risk Insurance

Act (TRIA).

W:\National Meetings\2017\Fall\Summaries\SURL.docx

© 2017 National Association of Insurance Commissioners

Title Insurance (C) Task Force

© 2017 National Association of Insurance Commissioners 1

2017 Fall National Meeting Honolulu, Hawaii

TITLE INSURANCE (C) TASK FORCE

Saturday, December 2, 2017 1:30 – 2:30 p.m.

Meeting Summary Report

The Title Insurance (C) Task Force met Dec. 2, 2017. During this meeting, the Task Force: 1. Adopted its Oct. 16 minutes, which included the following action:

a. Adopted its Summer National Meeting minutes. b. Adopted its 2018 proposed charges.

2. Adopted the report of the Title Insurance Financial Reporting (C) Working Group, including its Sept. 7 minutes. During

this meeting, the Working Group took the following action: a. Discussed comments received on the proposal to include known claims reserve within Exhibit A of the Statement of

Actuarial Opinion and decided to not move forward with the proposal. b. Discussed aggregate industry reports created by NAIC staff from the exhibits in the title insurance annual financial

statement.

3. Heard a presentation from States Title regarding the use of predictive analytics in underwriting for title insurance.

4. Heard an update regarding title insurance education course materials developed by Michael Draminski (MI), Krystle Ledvina-Garcia (NE) and Otis Phillips (NM). Comments will be collected through Dec. 31.

5. Heard an update regarding the federal TRID Improvement Act of 2017 (H.R. 3978) to amend the federal Real Estate Settlement Procedures Act of 1974 to require the Consumer Financial Protection Bureau (CFPB) to allow for the calculation of the discounted rate title insurance companies may provide to consumers when they purchase a lender’s and owner’s title insurance policy simultaneously.

W:\National Meetings\2017\Fall\Summaries\TitleTF.docx

© 2017 National Association of Insurance Commissioners

Workers’ Compensation (C) Task Force

© 2017 National Association of Insurance Commissioners

No materials

© 2017 National Association of Insurance Commissioners

Advisory Organization Examination Oversight (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Auto Insurance (C/D) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Catastrophe Insurance (C) Working Group

© 2017 National Association of Insurance Commissioners 1

E-vote and Conference Call

CATASTROPHE INSURANCE (C) WORKING GROUP November 27, 2017 / November 6, 2017

Summary Report

The Catastrophe Insurance (C) Working Group conducted an e-vote that concluded Nov. 27, 2017, and met via conference call Nov. 6, 2017.

1. During its Nov. 27 e-vote, the Working Group:a. Adopted its Nov. 6 and Summer National Meeting minutes.

2. During its Nov. 6 call, the Working Group:a. Discussed next steps on updating the NAIC State Disaster Response Plan. The charge to update the disaster

response plan previously fell under the responsibility of the Catastrophe Response (C) Working Group, which wasrecently disbanded. The charge will be absorbed by the Catastrophe Insurance (C) Working Group. The WorkingGroup will continue drafting updates to the State Disaster Response Plan.

b. Discussed the consumer claims guide document. The Working Group discussed the voluntary survey sent to insurersvia the insurance trade organizations regarding basic data and information regarding claims practices. The purposeof the survey was to aid the Working Group in developing a model guideline, white paper or compilation of bestpractices to reduce post-disaster insurance recovery obstacles for consumers. While there were a limited number ofresponses, the survey provided feedback the Working Group with results will aid in the decisions regarding theinformation put in the claims guide.

W:\National Meetings\2017\Fall\Summaries\Draft Summaries\CatastropheWG.docx

© 2017 National Association of Insurance Commissioners

Climate Change and Global Warming (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Creditor-Placed Insurance Model Act Review (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Medical Professional Liability (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Public Adjustor (C/D) Working Group

© 2017 National Association of Insurance Commissioners 1

Conference Calls

PUBLIC ADJUSTER (D) WORKING GROUP November 27, 2017 / October 12, 2017

Summary Report

The Public Adjuster (D) Working Group met via conference call Nov. 27 and Oct. 12, 2017. 1. During its Nov. 27 call, the Working Group:

a. Adopted its Oct. 12 minutes. b. Discussed the draft Public Adjuster Consumer Outreach Notice. c. Discussed the draft Notice to Property and Casualty Insurance Companies. d. Discussed the draft Notice to Contractors.

2. During its Oct. 12 call, the Working Group:

a. Adopted its July 17 and June 26 minutes, which were adopted by the Market Regulation and Consumer Affairs (D) Committee.

b. Discussed the draft Public Adjuster Consumer Outreach Notice. The consumer notice explains the role of public adjusters and what consumers should know to identify a person who may not be acting as an appropriately licensed public adjuster.

c. Discussed the draft Notice to Property and Casualty Insurance Companies. This insurance industry notice addresses the insurance industry’s role in preventing the unauthorized practice public adjusting.

d. Discussed the draft Notice to Contractors. This notice explains what services contractors are permitted to do without a public adjuster license and what services require them to obtain a public adjuster license.

W:\National Meetings\2017\Fall\Summaries\Final Summaries\Conf Call Meetings\PAWG.docx

© 2017 National Association of Insurance Commissioners

Sharing Economy (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Terrorism Insurance Implementation (C) Working Group

No Materials

© 2017 National Association of Insurance Commissioners

Transparency and Readability of Consumer Information (C) Working

Group

© 2017 National Association of Insurance Commissioners 1

E-vote and Conference Calls(In lieu of the meeting at the 2017 Fall National Meeting)

TRANSPARENCY AND READABILITY OF CONSUMER INFORMATION (C) WORKING GROUP November 27, 2017 / November 9, 2017 / July 12, 2017 / June 22, 2017

Summary Report

The Transparency and Readability of Consumer Information (C) Working Group conducted an e-vote that concluded Nov. 27, 2017, and met via conference call Nov. 9, July 12 and June 22, 2017.

1. During its Nov. 27 e-vote, the Working Group:a. Adopted its July 12 and June 22 minutes.

2. During its Nov. 9 call, the Working Group:a. Discussed the flood insurance coverage shopping tool. The objective of the shopping tool is to increase the

consumer’s understanding regarding the need for flood insurance. The Working Group is going to use infographicsand design a web page template for state insurance departments to use to help build awareness regarding the needfor flood insurance. The Working Group also discussed ways to distribute this information most effectively.

b. Discussed the consumer claims guide document. The Working Group discussed the voluntary survey sent to insurersvia the insurance trade organizations regarding basic data and information regarding claims practices. The purposeof the survey was to aid the Working Group in developing a model guideline, white paper or compilation of bestpractices to reduce post-disaster insurance recovery obstacles for consumers. While there were a limited number ofresponses, the survey provided feedback to the Working Group with results that will aid in the decisions regardingthe information put in the claims guide.

3. During its July 12 call, the Working Group:a. Discussed baseline information gathered by NAIC regarding the information already available to consumers about

flood insurance.b. Discussed the necessity for the Working Group to convey to consumers and small businesses the need to purchase

flood insurance.

4. During its June 22 call, the Working Group:a. Discussed its charge to develop a shopping tool for flood insurance to aid homeowners, renters and business owners.

The Working Group contemplated the ways to reach consumers about the importance of buying flood insurance.The Working Group will focus on designing a website template to answer core questions regarding flood insurance.

W:\National Meetings\2017\Fall\Summaries\Draft Summaries\Transparency WG.docx

Attachment XX Property and Casualty Insurance (C) Committee

X/XX/XXXX

© 2017 National Association of Insurance Commissioners 1

Draft: 11/29/17

Transparency and Readability of Consumer Information (C) Working Group E-Vote

November 27, 2017 The Transparency and Readability of Consumer Information (C) Working Group of the Property and Casualty Insurance (C) Committee conducted an e-vote that concluded Nov. 27, 2017. The following Working Group members participated: Angela Nelson, Chair (MO); Ken Allen (CA); Michael Conway (CO); Brett Gerger (IL); Ron Henderson (LA); Joy Hatchette (MD); and Kathy Shortt (NC). 1. Adopted its July 12 and June 22 minutes The Working Group conducted an e-vote to consider adoption of its July 12 (Attachment XX-A) and June 22 (Attachment XX-B) minutes. A majority of the Working Group members voted in favor of adopting the minutes. The motion passed. Having no further business, the Transparency and Readability of Consumer Information (C) Working Group adjourned. W:\National Meetings\2017\Summer\Cmte\C\Transparency\1127 Evote Transparency Min.docx

Attachment XX Property and Casualty Insurance (C) Committee

12/XX/17

© 2017 National Association of Insurance Commissioners 1

Draft: 11/27/17

Transparency and Readability of Consumer Information (C) Working Group Conference Call

November 9, 2017 The Transparency and Readability of Consumer Information (C) Working Group of the Property and Casualty Insurance (C) Committee met via conference call Nov. 9, 2017. The following Working Group members participated: Angela Nelson, Chair, and Rebecca Helton (MO); Ken Allen and Joel Laucher (CA); Ron Henderson (LA); Joy Hatchette (MD); and Kathy Shortt (NC). Also participating were: Kate Kixmiller (IN); Kevin Curry (NJ); Tracy Klausmeier (UT); and Katie Johnson (VA). 1. Discussed the Flood Insurance Coverage Shopping Tool The objective of the flood insurance coverage shopping tool is to increase consumers’ understanding of the need for flood insurance, which may increase the uptake of flood insurance. It is important for consumers to understand the risk of flood and their exposure to flood. To accomplish this objective, the Working Group identified a few preliminary ideas regarding potential work products. The Working Group has decided using infographics is a useful way to build awareness and to get a specific message across. During its last conference call, the Working Group discussed video testimonies and the influence they can have on consumers. Seeing another person who experienced a situation regarding flood can help consumers understand the significance of such an event. The Working Group also discussed putting together information for the Departments of Insurance (DOI) via a website, hosted by the NAIC, or a template states can use. Infographics and testimony would be the types of items posted on the website or used in templates. It is also important to give consumers information regarding how to navigate the National Flood Insurance Program (NFIP). Ms. Nelson said she believes providing state DOI with a tip sheet and a toolbox regarding flood insurance would be preferable over a best practices document. This could include tweets to be used for consumer education regarding flood insurance. The tweets might include references to infographics and testimonials. It is also important for states to know how to reach out to the consumers in their communities, as well as engaging realtors and financial institutions in a discussion to work together to increase consumer awareness regarding flood insurance and the need for flood insurance. Mr. Henderson said Louisiana has engaged in conversations with the NFIP and the Federal Emergency Management Agency (FEMA) following several flood events they experienced this year regarding consumer outreach. He said the infomercials the NFIP used last year did not suitably convey the message regarding the purchase of flood insurance. Mr. Henderson said that 56 of their 64 parishes flooded last year, so he understands the need for outreach and the need for consumers to purchase flood insurance. He suggested engaging the NFIP to make sure the Working Group distributes the necessary information to consumers. Sonja Larkin-Thorne (Consumer Advocate) suggested a portable setup containing consumer educational materials that could be used in areas such as libraries or send the information to various towns to post the information. She said most people think flood insurance policies are expensive. While some are expensive, they are relatively inexpensive in low-risk flood zones. Many of the homeowners in Connecticut experiencing flood in the last two years lived in the low-risk flood zones. Mr. Henderson said the Louisiana DOI held town halls in many areas in conjunction with city councils, state representatives and state senators. He said the flood maps were redrawn in Louisiana two years prior to recent flooding, and many people that had flood insurance received letters from their mortgage companies stating they were no longer in high-risk flood zones and were no longer required to carry flood insurance in order to maintain their mortgage. Mr. Henderson said consumers need education at the agent point of sale, on the DOI’s website and through town halls, etc. Ms. Larkin-Thorne suggested asking insurers to put testimonials regarding flood insurance on their websites. Lisa Brown (American Insurance Association—AIA) said the AIA has a public website and a member’s only website. She said the AIA would be willing to put the testimonials on its public website. David Kodama (Property Casualty Insurers Association of America—PCI) shared his website with the NAIC, as it has an entire section with flood-related resources. He said there is an entire section regarding catastrophe risk, including information regarding wildfires, hurricanes, tornadoes and flood, as well as preparation for flood and what to do following a flood event. Mr. Kodama said his insurance company has a section on its website regarding flood insurance. NAIC staff will circulate links prior to the next conference call. Mr. Kodama said the PCI

Attachment XX Property and Casualty Insurance (C) Committee

12/XX/17

© 2017 National Association of Insurance Commissioners 2

found working with Wildfire Partners regarding mitigation efforts to protect your home and property from wildfire risk was helpful. The message was carried forward via local law enforcement, fire fighters, going house-to-house, and providing talks and at libraries and town hall meetings. These discussions provided information regarding the risk homeowners and property owners are exposed to and the measures they can take to protect their property, as well as the programs available to help with the financial cost to mitigate against these risks. Ms. Nelson said she will make a note of this to add to a toolbox. Ms. Nelson said the materials include links to the Pennsylvania DOI website pages regarding flood insurance. She said that the Pennsylvania DOI has web content devoted to flood insurance and that this content provides a good model to assist the Working Group in producing a template. Pennsylvania’s web content is straightforward and simple. The web content consists of a few questions and answers and provides beneficial information. Ms. Nelson said the web page consists of the following questions: “Why should I consider flood insurance?”; “I have homeowners’ or renters insurance. Aren’t I already covered?”; “How can I buy flood insurance?”; “What should I know about private insurance?”; “What should I know about surplus lines insurance?” and “I have been redrawn into a flood zone. Now what?” Ms. Nelson believes these questions are all suitable; however, she might rearrange the order of some of the questions, such as starting with the question “I have homeowners’ or renters insurance. Aren’t I already covered?” She said the question/answer format is a little text-heavy and believes the Working Group can incorporate some infographics. Ms. Nelson said the Pennsylvania DOI has a good portable document format (PDF) regarding auto salvage fraud and provides a list of agents providing surplus lines coverage, a list of private insurers licensed in Pennsylvania, information regarding position letters regarding a number of different facets regarding private flood insurance, and links to both FEMA and the NFIP. She said the Working Group might want to consider making the links to FEMA and the NFIP more pronounced. Karol Kitt (The University of Texas at Austin) said she likes infographics; however, she said they do not provide some of the underlying basic content. Ms. Nelson asked if providing a link to more detailed information would be an option. Ms. Larkin-Thorne and Ms. Kitt agreed this would be an acceptable option. Birny Birnbaum (CEJ) asked what the moment in time is where people are looking for information regarding flood insurance. Ms. Nelson said she envisioned this being when people purchase a home and possibly when they receive a renewal for their homeowners insurance. One of the problems with the renewal process is that it is an automated process and may not provide an appropriate trigger. Mr. Birnbaum said depending on when people are looking for information will determine the type of information they are seeking. He said it is important to optimize infographics for cell phone use. Ms. Hatchette said people are generally interested in the purchase of flood insurance when there is a large flood event in either their state or another state. She said following the catastrophic flooding in Texas, people started thinking about flood insurance. Ms. Nelson suggested adding a question regarding having seen flooding forecasted in a state or in another part of the country. Ms. Larkin-Thorne said California has recently experienced wildfires, and if they get significant amounts of rain, homes will be flooded. Ms. Brown said when Hurricane Harvey hit, the AIA received a call from its local NBC affiliate, and AIA sent its federal flood insurance guide. She is sending a link to the Facebook page used by NBC. Mr. Allen said currently, in California, there are no talks regarding flooding at the present time; however, if storms are forecasted, the local news stations do mention the flood risk possibility. This may be too little or too late, but it is talked about. Ms. Nelson said not all of Pennsylvania’s resources might be applicable to every state. Mr. Henderson sent information to NAIC staff to be distributed to the Working Group members. Ms. Larkin-Thorne asked how the DOI dealt with people thinking FEMA will bail them out in the case of a flood. Mr. Henderson said Louisiana uses statistics from past flood events. He said the average homeowner receives $8,500 from FEMA following a flood event, and he presents this to homeowners during various events. Mr. Henderson said the Louisiana DOI makes it a point to illustrate FEMA is not going to cover the cost of a home, and there may or may not be a grant program available. He said FEMA does not take into account the size of a person’s home; it looks at what living needs exist. Ms. Nelson said Missouri uses the three common myths regarding earthquake in a similar presentations. Ms. Nelson said she and NAIC staff could take a stab at mocking up a couple of infographics, as well as a mock front web page using Pennsylvania and Louisiana as resources. Mr. Allen said he believes simple infographics would be better than infographics that are too busy. The Working Group plans to meet via conference call following the Fall National Meeting. She asked the Working Group members to let the Working Group know if they have any good candidates to provide a testimonial regarding flood insurance. Having no further business, the Transparency and Readability of Consumer Information (C) Working Group adjourned. W:\National Meetings\2017\Fall\Cmte\C\Transparency\1109 Transparency Min.docx

© 2017 National Association of Insurance Commissioners

Travel Insurance (C) Working Group

Attachment XX Property and Casualty Insurance (C) Committee

12/3/17

© 2017 National Association of Insurance Commissioners 1

Draft: 11/30/17

Travel Insurance (C) Working Group E-Vote

November 30, 2017

The Travel Insurance (C) Working Group of the Property and Casualty Insurance (C) Committee conducted an e-vote that concluded Nov. 30, 2017. The following Working Group members participated: Al Redmer Jr., Chair, and Cathy Grason (MD); David Altmaier, Vice Chair (FL); Susan Stapp and Dawn Withers (CA); Michael P. Rohan (IL); Tom Travis (LA); Tim Johnson (NC); Buddy Combs, Brian Gabbert and Tyler Laughlin (OK); Matthew Gendron (RI); Brett J. Barratt (UT); Rebecca Nichols (VA); and Jim Freeburg and John Haworth (WA). 1. Adopted its Nov. 27 Minutes The Working Group conducted an e-vote to consider adoption of its Nov. 27 minutes (Attachment XX-A). A majority of the Working Group members voted in favor of adopting the minutes. The motion passed. Having no further business, the Travel Insurance (C) Working Group adjourned. W:\National Meetings\2017\Fall\Cmte\C\Travel Insurance WG\11-27\11-27 Travel Ins WG e-vote min.docx

Attachment -A Property and Casualty Insurance (C) Committee

12/3/17

© 2017 National Association of Insurance Commissioners 1

Draft: 11/29/17

Travel Insurance (C) Working Group Conference Call

November 27, 2017 The Travel Insurance (C) Working Group of the Property and Casualty Insurance (C) Committee met via conference call Nov. 27, 2017. The following Working Group members participated: Al Redmer Jr., Chair, and Cathy Grason (MD); David Altmaier, Vice Chair (FL); Susan Stapp and Dawn Withers (CA); Michael P. Rohan (IL); Tom Travis (LA); Tim Johnson (NC); Buddy Combs, Brian Gabbert and Tyler Laughlin (OK); Matt Gendron (RI); Brett J. Barratt (UT); Rebecca Nichols (VA); and Jim Freeburg and John Haworth (WA). Also participating were: Tate Flott (KS); Don Layson (OH); and John Carter (TX). 1. Adopted its Nov. 13, Nov. 7, Oct. 31, Oct. 11, Oct. 6, Sept. 28 and Sept. 13 Minutes The Working Group reviewed the minutes of its Nov. 13 meeting, during which it took the following action: 1) reviewed its Nov. 7 minutes; 2) continued the discussion of the groups to be included in the definition of “eligible groups,” completing the review of the list of examples; 3) identified outstanding item to be discussed for “eligible groups” and deferred the discussion of a drafting note for the “travel insurance” definition to the next conference call; and 4) discussed next steps for continuing the review of the NAIC Travel Insurance Model Law (Model Act.) The Working Group also reviewed the minutes from previous conference calls held since the Summer National Meeting. In regard to the minutes from the Nov. 7 meeting, Denise Matthews (NAIC) said it had been brought to her attention that in the section related to the discussion of item (d), it would be clearer if the words “that language” were changed to “the phrase similar to the phrase deleted in item (c)” as otherwise it reads as if the Working Group voted to delete the word “guests” from the item (d) language. This is in paragraph 19 under item #2 in the minutes. She also said that the person identified in paragraph 23 as Ms. Grason was actually Ms. Alvarado. Commissioner Redmer asked if there was any discussion related to the proposed revisions to the Nov. 7 minutes. Commissioner Altmaier made a motion, seconded by Ms. Nichols, to adopt the amendments to the Nov. 7 minutes. The motion passed unanimously. Hearing no additional recommendations for amendments to the minutes, Commissioner Altmaier made a motion, seconded by Mr. Travis, to adopt the Working Group’s Nov. 13 (Attachment XX-A1), Nov. 7 (Attachment XX-A2), Oct. 31 (Attachment XX-A3), Oct. 11 (Attachment XX-A4), Oct. 6 (Attachment XX-A5), Sept. 28 (Attachment XX-A6) and Sept. 13 (Attachment XX-A7) minutes. The motion passed unanimously. 2. Conducted a Review of the Definition of “Eligible Groups” Commissioner Redmer asked for comments related to the Oklahoma/Louisiana proposed language for “eligible groups” (Attachment XX-A8.) Mr. Combs said the proposal keeps the “two (2) or more persons” language proposed earlier; adds “engaged in a common enterprise, or have an economic, education, or social affinity or relationship…” to avoid just any two people constituting a group; and adds the phrase “wherein with regard to any particular travel or type of travel or travelers, all members or customers of the group must have a common exposure to risk attendant to such travel” to ensure there is some common exposure to the same risks for each traveler who is a part of the group. Commissioner Redmer asked about the “common exposure to risk” attendant to such travel. He asked if travelers coming from different parts of the country would be considered to have similar risk. Mr. Combs said it would depend on how the filings come in, noting that the commissioner would make that determination. Mr. Barratt asked what impact this change would have on premium tax and, specifically, what the term “common carrier” refers to. He asked where the premium tax would be paid if the travelers were from two different states and the “common carrier” was in yet another state. Mr. Combs said the premium tax determinations were addressed in the Model Act by the Working Group previously, and it would be paid in the home state of the certificate holder. Mr. Barratt asked if the certificate holder would then be the carrier. John Fielding (Steptoe & Johnson LLP), representing the U.S. Travel Insurance Association (UStiA), said the premium tax would be paid where the certificate holder, which is the individual traveler, resides.

Attachment -A Property and Casualty Insurance (C) Committee

12/3/17

© 2017 National Association of Insurance Commissioners 2

Commissioner Redmer asked for any other questions or comments regarding the Oklahoma/Louisiana proposal. Hearing none, he asked the preference of the Working Group members regarding adding the proposed language to the definition of “eligible groups.” The Working Group members on the call unanimously agreed to add the proposed language to the Model Act. Birny Birnbaum (Center for Economic Justice—CEJ) said the CEJ has some comments about the adopted language, and it will raise them during the next review of the Model Act. 3. Conducted a Review of the Definition of “Travel Insurance” Commissioner Redmer asked for comments related to the “travel insurance” definition. Mr. Freeburg said Washington had previously offered some language to make a distinction between travel insurance and other similar types of coverage, which is the last sentence (Attachment XX-A9). He said Washington would prefer to stay with the language proposed (i.e., “Coverage for rental vehicle damage or item (4) above may only be offered as ancillary coverage to trip cancellation/interruption”) and not go with the drafting notes proposed by the UStiA (Attachment XX-A10). Mr. Fielding said the UStiA believes the language should stay as it was in the original draft and the last sentence should be deleted. He said that is because the language has been thoroughly vetted by the NAIC and the National Conference of Insurance Legislators (NCOIL) and has been adopted in 45 states. He said there have been no problems to date, and it is pending adoption in a couple of states. He said the UStiA, in an effort to try to bridge the gap, has recommended drafting notes to address situations in some states such as Washington. He said the UStiA believes this is a good compromise and the definition should be left as-is. Greg Mitchell (Frost Brown Todd LLC), representing the Tourism and Travel Industry Consumer Coalition (TTICC), reiterated what Mr. Fielding said, noting that he believes it would cause confusion if this language is not deleted. He said the TTICC is not aware of any problems this has caused in the states with this language already in place. Angela Gleason (American Insurance Association—AIA) said the AIA supports the comments made by Mr. Fielding; i.e., deleting the sentence and replacing it with the proposed drafting notes. Mr. Birnbaum said the CEJ supports the last sentence and opposes the drafting note the UStiA is proposing. He said the industry wants to sell rental car insurance and call it travel insurance, which he said will create regulatory arbitrage that should be avoided. He said it is not taking away consumer choice but eliminating a lack of clarity. Mr. Fielding said it is not rental car coverage but damage to rental car, and it is coverage that essentially covers what a traveler would be responsible for when physical damage to the car occurs. He said it is not a car rental policy that includes liability and other coverages. He said this has been a permitted practice for a number of years now. Mr. Combs asked Mr. Freeburg what consumer harm this language is trying to prevent. Mr. Freeburg said, in Washington, there are different laws on the books relating to rental car coverage, noting that it does not have the same distribution setup. He said the same goes for the medical plans, which are much more highly regulated, adding that Washington does not believe it is appropriate for a medical or rental car plan to be sold as a very limited line of travel. Mr. Combs said Oklahoma’s law already allows for this, so it would be a big change for Oklahoma. He questioned if it would make sense to add this language for the few states that do not. He said it sounds like a situation where a drafting note would be appropriate, so if a state treats this differently, it can use the language in the drafting notes. Ms. Nichols said Mr. Combs makes some good points. She said this is allowed in Virginia, as well, so it would be a change for them. Commissioner Redmer said if no action is taken, the last sentence will remain. Mr. Birnbaum said the harm in allowing this is having two regulatory options for the same product, which would create regulatory arbitrage. Mr. Combs said he does not agree that it would create regulatory arbitrage because it has to be incident to planned travel and must meet all of the other requirements of the Model Act in order to be sold as travel insurance. Mr. Birnbaum said this is identical to rental car insurance and will allow it to be called travel insurance. Mr. Combs said it includes some of the same things but is not as broad and, therefore, it is a different product.

Attachment -A Property and Casualty Insurance (C) Committee

12/3/17

© 2017 National Association of Insurance Commissioners 3

Commissioner Altmaier asked if there were other members of the Working Group that would like to express an opinion or are not ready to make a decision at this time. Hearing none, Mr. Combs suggested striking the last sentence in the definition in Attachment XX-A9. Mr. Travis agreed with Mr. Combs’ suggested deletion. Mr. Freeburg pointed out that this will encompass not only rental car coverage but also medical coverage, allowing a standalone medical travel policy, which seems quite odd to be an inland marine product covering accident and health. He said he wanted to be sure the Working Group members are fully aware of that. Commissioner Altmaier asked the Working Group members if they were in favor of deleting the sentence. The Working Group members on the call agreed, with the exception of Washington and California. No states abstained. Commissioner Altmaier said this change will be reflected in the next draft version of the Model Act and will be exposed again for comment in the future. Mr. Travis suggested including the drafting notes proposed by the UStiA in the next draft version of the Model Act. Mr. Combs agreed with that suggestion. Commissioner Altmaier asked if the Working Group members on the call agreed with including the drafting notes proposed by the UStiA (Attachment XX-A11) in the next version of the Model Act. All of the members on the call agreed with that suggestion. 4. Discussed Next Steps Ms. Matthews said Commissioner Redmer would like to have another call of the Working Group after the Fall National Meeting and before the end of the year. She said the next section to be reviewed would be the Travel Protection Plans section, which includes the following definitions: fulfillment materials; cancellation fee waiver; and travel assistance services. Having no further business, the Travel Insurance (C) Working Group adjourned. W:\National Meetings\2017\Fall\Cmte\C\Travel Insurance WG\11-27 Travel Ins WG min.docx

© 2017 National Association of Insurance Commissioners

Attachment Three Hear Updates from the States and

Jurisdictions Related to Recent Catastrophes

11/29/2017

1

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA:

Experiences and Lessons Learned

A presentation by

Honorable Osbert E. PotterLieutenant Governor of the US Virgin Islands

and Commissioner of Insurancebefore the

National Association of Insurance CommissionersFall National Meeting; Sunday, December 3, 2017; 1:00 pm

Property and Casualty (C) CommitteeCommissioner John Doak, Chairman

1

The United States Virgin Islands

2

11/29/2017

2

3

IMPACT OF HURRICANES IRMA AND MARIA ON THE U.S. VIRGIN ISLANDS

Hurricane Irma:September 5, 2017

Hurricane Maria:September 19, 2017

4

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

Irma’s Destruction of Philadelphia Seventh Day Adventist Church, St. Thomas

11/29/2017

3

5

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

Hurricane Maria’s Destruction of Arthur A. Richards Junior High School, Frederiksted, St. Croix

6

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

The Honorable Kenneth E. Mapp, Governor The Honorable Osbert E. Potter, Lieutenant Governor

VISIONARY LEADERSHIP ON THE ROAD TO RECOVERY

11/29/2017

4

7

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

Disaster Declaration and Support from President and Mrs. Donald Trump

8

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

About 40% of the Territory has been re-energized, with a goal of 90% restoration byChristmas. Linemen from various locations stateside have aided the power restorationprocess.

Public schools have re-opened, with some campuses having split sessions.

Debris collection a major effort in the communities; as of November 22, 2017,236,000 cubic yards of material collected on St. Croix; 22,524 cubic yards on St.Thomas and 10,936 cubic yards had been collected from St. John.

Lieutenant Governor Osbert E. Potter, as Acting Governor onNovember 22, 2017, gave thanks for the continued progress inthe United States Virgin Islands on the eve of the Thanksgivingholiday. Speaking at Government House on St. Croix, theActing Governor expressed his gratitude to the People of theVirgin Islands and the Territory’s partners for continuing to rallyaround recovery efforts as life steadily returns to normalcy.Recovery efforts reported included:

11/29/2017

5

9

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

According to FEMA, 35,000 individuals and families have registered for assistanceafter the hurricanes. To date, the federal government has allocated more than $193.5million in approved funding. This includes $62 million in low interest loans, $109.5million in public assistance grants and $22 million in grants for individuals andfamilies, including more than $7 million for essential repairs to their homes.

The U.S. Small Business Administration can provide homeowners up to $200,000 torepair and replace homes, and up to $40,000 for homeowners and renters to repair andreplace personal property. SBA can also provide loans to businesses.

27,877 residents Territory-wide have applied for the Disaster Supplemental NutritionAssistance Program (D-SNAP).

10

WHAT WE LEARNED THAT WORKS

RESOURCE IDENTIFICATION Immediate Request for Presidential Disaster Declaration Immediate Activation of Virgin Islands Territorial Emergency Management

Agency’s (“VITEMA”) Emergency Operations Center (“EOC”) Mobilization of US Virgin Islands Resources at the EOC Established Sustainable Partnerships at the local level, with similarly

situated states, and with Federal partners

DAILY PUBLIC COMMUNICATIONS Daily Press Conferences

PUBLIC EDUCATION USVI Government Agencies required to conduct public education

activities via Radio and Press Releases

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIA

11/29/2017

6

11

The Office of the Lieutenant Governor, Division of Banking, Insurance and Financial Regulation mitigates hazards by licensing and regulating the banking, insurance an d financial services industries and protecting consumer interests.

The Division regulates banks; mortgage brokers and dealers; small loan companies;international financial services entities; securities and securities salespersons; moneytransmitters; non-bank ATMs; check cashers and currency exchange; insurance companies;insurance agencies; insurance producers (insurance agents & brokers, and adjusters); third partyadministrators; unclaimed property and debt management providers.

The Division has nearly thirty employees and conducts its duties and responsibilities through anAdministrative Unit; Licensing Examination Unit; Financial Services Unit; and Securities Unit.

OFFICE OF THE LIEUTENANT GOVERNOR DIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

WHAT WE LEARNED THAT WORKSPUBLIC EDUCATION ON THE ROLE OF THE INSURANCE COMMISSIONER

IN THE AFTERMATH OF A HURRICANE

Honorable Osbert E. Potter, Lieutenant Governor and Commissioner of InsuranceGwendolyn Hall Brady, Director, Division of Banking, Insurance and Financial Regulation

12

Why Property & Casualty Insurance is Important to the Territory’s Economic Recovery in the Aftermath of Hurricanes Irma and Maria

Available and affordable property and casualty insurance is vital to the protection ofVirgin Islands residents, their homes and automobiles, businesses, governmentbuildings and the Territory’s infrastructure.

The U.S. Virgin Islands has a subtropical climate with minimal seasonal change. TheTerritory has a hurricane season that extends from June 1st to November 30th annually.

A hurricane occurrence has a rippling domino effect on the Territory’s economy and itsinsurance industry.

Because hurricanes make the U.S. Virgin Islands catastrophic-prone, the availability andaffordability of property and casualty insurance is imperative to hazard mitigation and theTerritory’s economic survival.

OFFICE OF THE LIEUTENANT GOVERNOR DIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

11/29/2017

7

13

DATA CALLS FOR HURRICANES IRMA AND MARIA

The Division of Banking, Insurance and Financial Regulation (“Division”) is in theprocess of gathering Hurricane Irma and Hurricane Maria claims data from its licensedand authorized property and casualty insurers.

While claims paid data is not currently available from all of the insurers, the Division isaware of total projected losses from the insurers that write the majority of property andcasualty business in the Territory. The USVI total projected losses are as follows:

Hurricane Irma: $787,000,000.00 (Greatest impact was on St. Thomas & St. John)

Hurricane Maria: $445,200,000.00 (Greatest impact was on St. Croix)

OFFICE OF THE LIEUTENANT GOVERNOR DIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

14

1. Contacted targeted insurers that write 10% or more of the property & casualty insurancebusiness in the Territory to discuss total in-force aggregates; total projected losses peroccurrence; reinsurance, etc.;

2. Contacted targeted property & casualty brokers and agents that write for these insurers to assesstheir readiness to receive claims;

3. Contacted the National Association of Insurance Commissioners (“NAIC”) NAIC for assistancewith consumer complaints and data calls, as well as identification of states with extensivehurricane response experience. A dedicated Data Call email address was established.

4. Issued Bulletins to the insurance industry and the public and placed the Bulletins on theDivision’s website at www.ltg.gov.vi.

5. Executed a consumer education and protection program on how to conduct hazard mitigation(secure your property; prepare an inventory of damages; take photos); contact your agent orbroker; and file a claim.

THE U.S. VIRGIN ISLANDS IN THE AFTERMATH OF HURRICANES IRMA AND MARIAWHAT THE DIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION LEARNED THAT WORKS

Implemented the Division’s Catastrophe Response Plan:

11/29/2017

8

15

I. BULLETIN 2017-10:Hurricane Irma and Hurricane Maria – Claims Adjusting and Adjusters

II. BULLETIN 2017-09:Data Call Relating to Hurricane Irma and Hurricane Maria Insurance Claims

III. BULLETIN 2017-08:Advises the Insurance Industry, Adjusters and Consumers Against Hurricane-related Misrepresentation and Fraudulent Claims

IV. BULLETIN 2017-07:Requirement of an Insurer to Submit to the Division a Written CatastrophePlan as a Condition for New and Renewal Licensure

V. BULLETIN 2017-06:Limits Public Adjuster Fees to 5% of the Insurance Proceeds Recovered onbehalf of a Home Owner or Residential Insured

LESSONS LEARNED BY THEDIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

THE IMPORTANCE OF BULLETINS AND PUBLIC EDUCATIONBulletins Issued (All BULLETINS are posted at www.ltg.gov.vi):

16

Licensure and Regulation of the Banking, Insurance and Financial Services Industries: Processes nearly 1,700 license applications annually (inclusive of all license types granted by the Division); Monitors the activities of all licensees to ensure compliance with applicable Virgin Islands and federal laws; Proposed the Virgin Islands Insurance Producer and Adjuster Licensing Act, which brings the licensing

requirements in concert with those of other jurisdictions

Consumer Protection & Education: Educates consumers on the importance of buying homeowners insurance with windstorm coverage. Educates

condominium owners and renters on the importance of buying content coverage. Advises consumers to buy a homeowners policy with windstorm coverage and a SEPARATE flood insurance

policy! Advises consumers who have an outstanding mortgage, to avoid force-placed insurance, because it protects only

the bank’s interest and not the replacement cost of the property. Develop educational Bulletins & Press Releases; place articles in local newspapers & appear on Radio and TV, as

means of protecting and educating consumers on hazard mitigation. Processes consumer complaints before and after a catastrophe. Encourages consumers to contact the Division to

ensure they are requesting services from a licensed producer.

OFFICE OF THE LIEUTENANT GOVERNOR, DIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

Hazard Mitigation Through Insurance Regulation, and Consumer Protection & Education

11/29/2017

9

17

For further information on the programs and services of the Office of the Lieutenant Governor,Division of Banking, Insurance and Financial Regulation, please visit www.ltg.gov.vi orcontact us at 340-774-7166 (St. Thomas and St. John) or 340-773-6459 (St. Croix).

OFFICE OF THE LIEUTENANT GOVERNORDIVISION OF BANKING, INSURANCE AND FINANCIAL REGULATION

© 2017 National Association of Insurance Commissioners

Attachment Four Discuss the Modernization of Commercial

Lines

11/30/2017

1

1

Regulatory Modernization to Help Commercial Lines of Insurance Work Even Better for America

NAIC

December, 2017

David F. Snyder, PCI

Outline

• Defining commercial lines of insurance and what roles it plays in supporting businesses, nonprofits, governments, and the public through financing, investing, and risk mitigation

• Identifying some of the challenges facing commercial insurers

• Reviewing previous NAIC and state regulators’ efforts to streamline regulatory processes

• Suggesting a way forward for us to help make commercial insurance more responsive to the needs of commercial consumers and the public

2

11/30/2017

2

Defining Commercial Insurance and the Critical Roles It Plays

• In 2016, commercial lines constituted 49% of total property casualty premiums, or approximately $294 billion in direct written premiums

• Commercial insurance is a major part of the US economy and is a diverse market that has evolved over time

• Commercial insurance provides needed coverage and related service to a wide range of businesses, nonprofits and government entities

• Commercial insurance helps minimize risk and enable commercial insureds to expand and create new jobs

3

Defining Commercial Insurance and the Critical Roles It Plays

• Commercial insurance coverage enables insureds to focus on their core missions and reinvest in their operations to better serve the public

• Commercial insurance premiums help finance public infrastructure through investment in municipal bonds

• Both insureds and the general public benefit from these roles

4

11/30/2017

3

Some General Challenges Facing Commercial Insurers

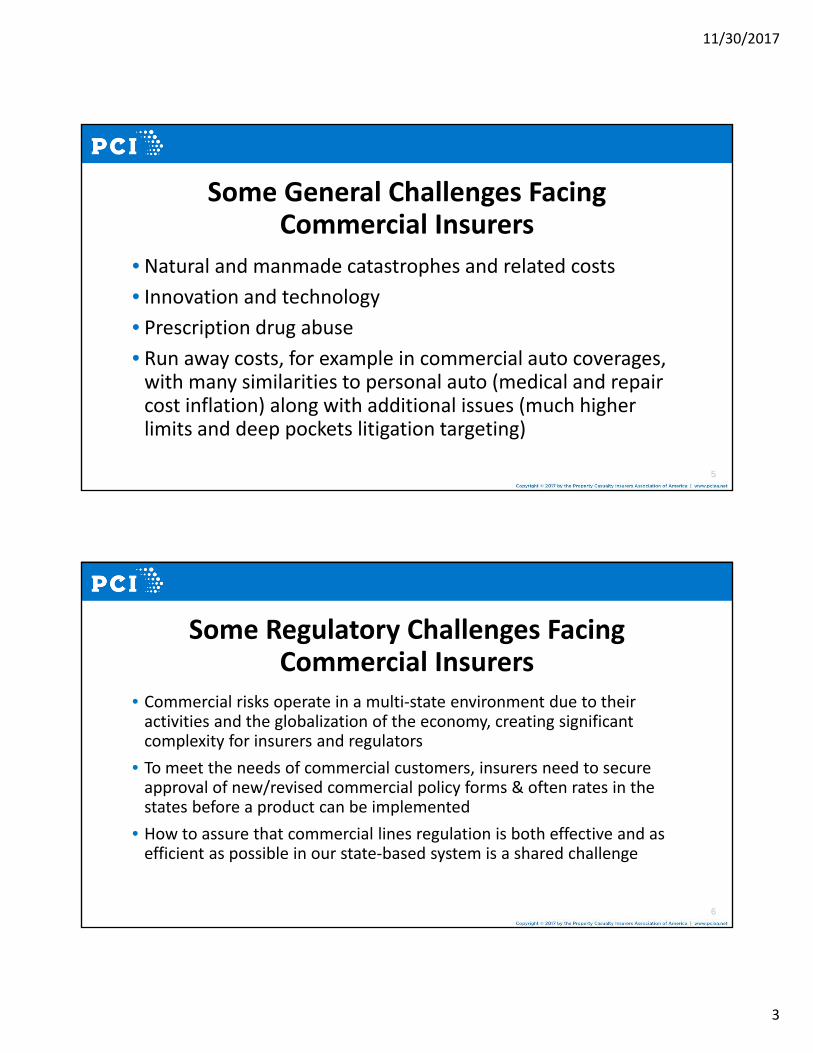

• Natural and manmade catastrophes and related costs

• Innovation and technology• Prescription drug abuse• Run away costs, for example in commercial auto coverages, with many similarities to personal auto (medical and repair cost inflation) along with additional issues (much higher limits and deep pockets litigation targeting)

5

Some Regulatory Challenges Facing Commercial Insurers

• Commercial risks operate in a multi‐state environment due to their activities and the globalization of the economy, creating significant complexity for insurers and regulators

• To meet the needs of commercial customers, insurers need to secure approval of new/revised commercial policy forms & often rates in the states before a product can be implemented

• How to assure that commercial lines regulation is both effective and as efficient as possible in our state‐based system is a shared challenge

6

11/30/2017

4

Previous NAIC and State Regulators’ Efforts to Improve Regulation

• Latest NAIC reform effort was in 2015 which produced four recommendations:

Ensure that individual consumers are protected when they are charged for commercial lines coverage

Consider allowing manuscript policies to be used without prior approval

Consider establishing conditions for exempting policies for multistate risks from form and rate filing requirements

Review existing state authority to improve the efficiency and effectiveness of rate and form review for commercial lines

• Need for follow up with the states

• Treasury recently endorsed commercial insurance regulatory modernization 7

Regulatory Improvement Suggestions

• Regulators and insurers should work together to meet the legitimate needs of commercial consumers

• Regulators and insurers should continue to address unproductive regulatory inefficiencies

• Regulators and insurers should consider creating an on‐going forum to address commercial lines issues and discuss best regulatory practices to address them

• Specific ideas for discussion could include:

Consider a single portal for insurance company data needed by many states, such as changes in officers and biographical information, to avoid multiplicative reporting of the same information

8

11/30/2017

5

Regulatory Improvement Suggestions

Adopt data call principles, as recently recommended by NCOIL

Review progress on prior regulatory modernization proposals

Work with insurers to identify specific state issues and adopt best regulatory practices for effective and efficient regulation

Work with insurers to identify and reduce underlying cost drivers and escalating compliance burdens

9

Conclusion

• Commercial lines of insurance are large, diverse and fundamentally important to America

• The many critical roles played by commercial insurance include compensation, investment in infrastructure, and prevention of losses

• Regulation has a critical role to play and should be both effective and efficient

• There is a growing consensus that some improvements in commercial lines regulation would be beneficial

10

11/30/2017

6

Conclusion

• An effective and efficient regulatory system for commercial insurance should result in greater choice, convenience, and innovation for the commercial insurance purchaser

• Regulators, the industry, and other stakeholders previously worked together on commercial lines regulatory modernization and should do so again

• Conversation should begin again to ensure that commercial lines insureds will have the insurance products they need to meet the demands of technological change and a global economy and that the benefits to the public from commercial insurance are maximized

11

© 2017 National Association of Insurance Commissioners

Attachment Five Hear a Presentation from States Title

States TitleCorporate Overview

every homeowner needs it

Everybody needs it~10M POLICIES WRITTEN IN 2015

(US)

A Consolidated Market with Extraordinarily Low Loss Ratios

$2.7

$5.4

$8.2

$10.9

$13.6

2010 2011 2012 2013 2014 2015

Fidelity

First American

Old Republic

Stewart

Other

Total Industry Revenues

$13.6 Billion6%

Net Income5%Claims

89%OpEx

Proprietary & Confidential

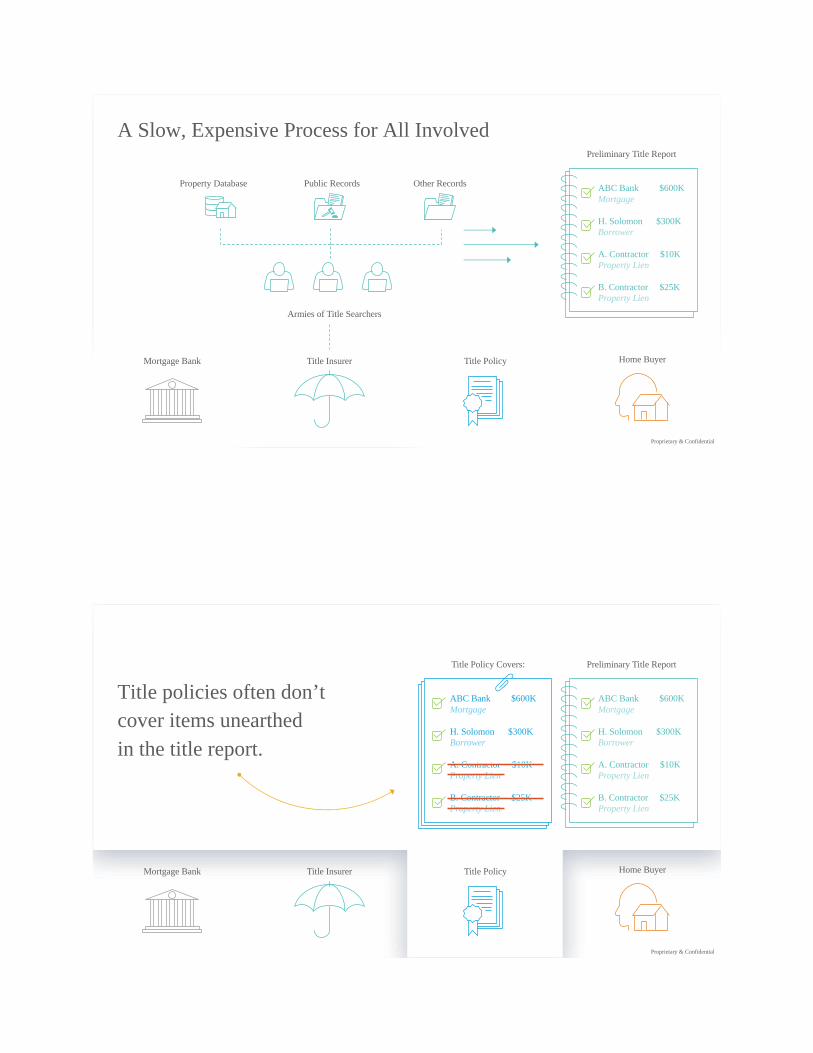

A Slow, Expensive Process for All Involved

Mortgage Bank Title Insurer Title Policy Home Buyer

Hires To Issue Paid for by

Which Covers

Proprietary & Confidential

Mortgage Bank Title Insurer Title Policy Home Buyer

Preliminary Title Report

A Slow, Expensive Process for All Involved

Armies of Title Searchers

Public Records ABC Bank $600KMortgage

H. Solomon $300KBorrower

A. Contractor $10KProperty Lien

B. Contractor $25KProperty Lien

Mortgage Bank Title Insurer Title Policy Home Buyer

Property Database Other Records

Proprietary & Confidential

Mortgage Bank Title Insurer Title Policy Home Buyer

ABC Bank $600KMortgage

H. Solomon $300KBorrower

A. Contractor $10KProperty Lien

B. Contractor $25KProperty Lien

Title policies often don’t cover items unearthed in the title report.

Title Policy Covers: Preliminary Title Report

ABC Bank $600KMortgage

H. Solomon $300KBorrower

A. Contractor $10KProperty Lien

B. Contractor $25KProperty Lien

Proprietary & Confidential

Mortgage Bank Title Insurer Title Policy Home Buyer

5–10 days of negotiation 15%of MB OpEx

We’d like you to cover these things.

Sorry.

You need to cover these things.

...OK.

ABC Bank $600KMortgage

H. Solomon $300KBorrower

A. Contractor $10KProperty Lien

B. Contractor $25KProperty Lien

Title Policy Covers: Preliminary Title Report

ABC Bank $600KMortgage

H. Solomon $300KBorrower

A. Contractor $10KProperty Lien

B. Contractor $25KProperty Lien

Proprietary & Confidential

Analytics-PoweredMortgage Bank Title Insurer Title Policy Home Buyer

5–10 Seconds

Public Data

Paid Data

PartnerData

Analytics Engine

100% Mortgage $600K

100% Borrower $300K

98% ±2 Prop. Lien ~$10K

88% ±12 Prop. Lien ~$25K

12% ±4 Prop. Lien ~$5K

It’s Time for Automated, Data-Driven Underwriting

Predicts

Generates

Proprietary & Confidential

OUR TITLE PACKAGE LOOKS AND FEELS EXACTLY LIKE YOU ARE USED TO SEEING

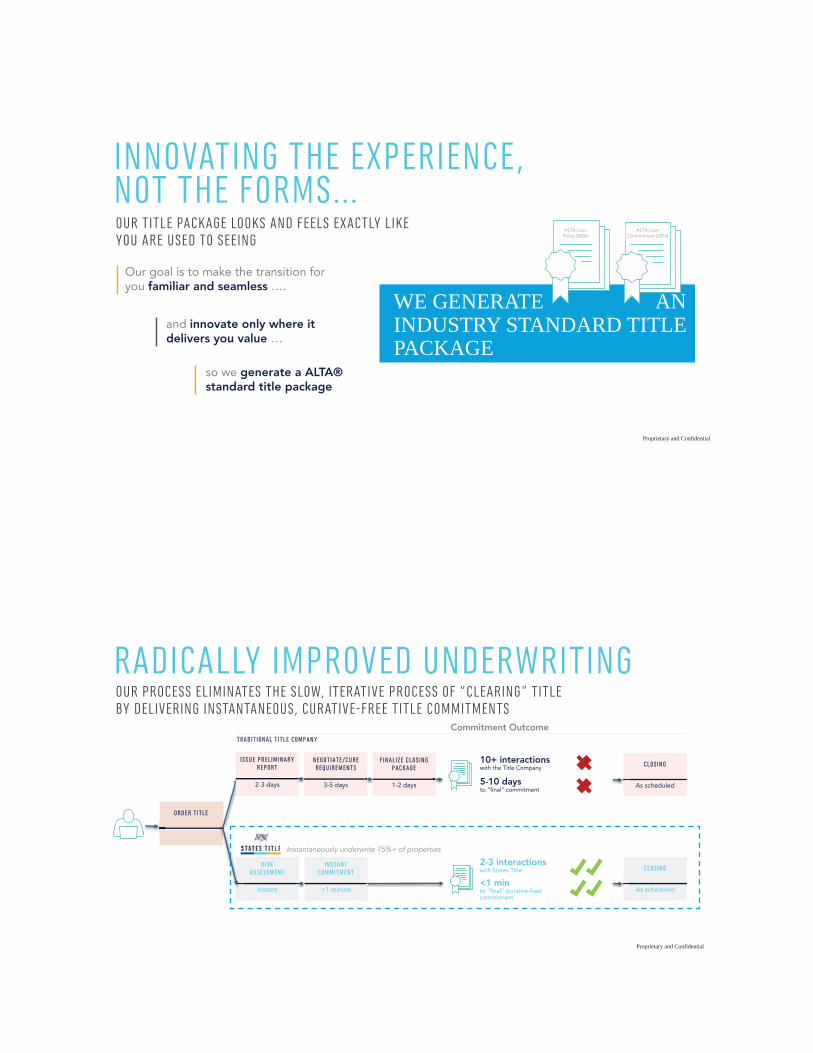

INNOVATING THE EXPERIENCE, NOT THE FORMS…

WE GENERATE AN INDUSTRY STANDARD TITLE PACKAGE

ALTA Loan Policy (2006)

ALTA Loan Commitment (2016)

and innovate only where it delivers you value …

so we generate a ALTA® standard title package

Our goal is to make the transition for you familiar and seamless ….

Proprietary and Confidential

OUR PROCESS ELIMINATES THE SLOW, ITERATIVE PROCESS OF “CLEARING” TITLEBY DELIVERING INSTANTANEOUS, CURATIVE-FREE TITLE COMMITMENTS

RADICALLY IMPROVED UNDERWRITING

ORD E R T ITLE

RIS K AS S E S S M E NT

Instant

INS TA NT C OM M ITM E NT

<1 minute

2-3 interactions with States Title

I S S UE P RE L IM INA RY RE P ORT

2-3 days

NE GOTIATE /C URE RE QUIRE M E NTS

3-5 days

F INALIZE C LOS ING P AC K AGE

1-2 days

C LOS ING

As scheduled

10+ interactions with the Title Company

Commitment OutcomeTRAD IT IONAL T ITLE C OM P ANY

<1 minto “final” (curative-free) commitment

5-10 daysto “final” commitment

Instantaneously underwrite 75%+ of properties

C LOS ING

As scheduled

Proprietary and Confidential