2017 annual report · jesus g. tabora nicolas r. tabora chairman president. 2017 annual report...

TRANSCRIPT

2017 ANNUAL REPORT

03 Corporate Profile04 Vision, Mission05 Business Model06 Financial Highlights07 Report to Stockholders09 Risk Management Framework16 AML Governance17 Corporate Governance19 Board of Directors30 Organizational Structure37 Stockholders38 Products and Services39 Banking Units40 Audited Financial Statements92 Capital Adequacy

2017 ANNUAL REPORT

Annual Report 2017 | Page 1 of 106

Rural Bank of Rosario (L.U.), Inc.

2017 ANNUAL REPORT

Annual Report 2017 | Page 2 of 106

RURALBANKOFROSARIOANGBANGKOPARASAINYO.

2017 ANNUAL REPORT

Annual Report 2017 | Page 3 of 106

The Rural Bank of Rosario (LU), Inc. was registered with the Securities andExchange Commission (SEC) under registration number 3761 and wasincorporated on February 21, 1969. The bank is organized under Republic Act(R.A.) No. 7353, otherwise known as the Rural Banks Act of 1992. The bankobtained its rural bank license from the Bangko Sentral ng Pilipinas (BSP) onMarch 13, 1969 and started its operation on March 22, 1969. The bank is engagedin rural banking services primarily to carry business of extending rural credit tosmall farmers and tenants to deserving rural industries or enterprises; and tohave an exercise all authority and powers to perform all acts and transacts allbusiness which may legally be had done by rural bank organize under and inaccordance with the Rural Bank’s Act. The bank transacts all business which maylegally exist or be amended and to have all other things thereto necessary andproper in connection with said purposes within such authority as may bedetermined by the Monetary Board of Bangko Sentral ng Pilipinas.

The RURAL BANK OF ROSARIO (LA UNION), INC. Board of Directors is composed ofseven (7) members; one (1) of them is an Independent Director.

The Bank’s principal place of business is located at National Highway, PoblacionEast, Rosario, La Union with extension office located at Rosario Public Market,Subusub, Rosario, La Union. It has five (5) branches which are located at Sto.Tomas, La Union, San Fabian, Sison, Pozorrubio and Binalonan Pangasinan. Thebank also have four (4) on site automated tellering machines located in the mainoffice in Rosario, La Union, Sto. Tomas Branch, San Fabian Branch and PozorrubioBranch.

With the support and guidance of its regulatory bodies, RBR aims to provide moreinnovative and convenient banking solutions to its growing customer base.

2017 ANNUAL REPORT

Annual Report 2017 | Page 4 of 106

To be a leading financial institution in Northern Luzon and a dependable partner inthe countryside development by 2020.

We will provide the best to the community with the highest degree of

and unparalleled .

We will be the catalyst of economic development offering a wide range of bankingproducts and innovative services through the concerted efforts of the dynamicfamily of the Rural Bank of Rosario as guided by the Lord Almighty.

Our Vision and Mission serve as the guiding path of the Bank in continuously providing the people ofNorth Luzon the best services it can give.

2017 ANNUAL REPORT

Annual Report 2017 | Page 5 of 106

The Bank’s growth path is embedded in its PLANS AND STRATEGIES. The RBR’s maingoal is to achieve a solid financial position by the end of 2018. To achieve its goal,the Bank is embattled to generate the net operational income of Php6.2M throughlending at least Php206M and to accept deposits in the amount of Php514M.

The target market of the Bank is the farmers from the Agricultural sector; thebusiness owners of small and medium enterprise and operators of transportationfrom the Commercial Sector; the manufacturers of hollow blocks, furniture andwelding shop including the rice millers from the Industrial sector; the bank alsooffers various loan products to private and government employees including theOFW’s and the pensioners; the bank also caters loans to barangay officials and RBRofficers and employees.

The Bank formulated various strategies to achieve these goals. Some of thestrategies are obtaining a master list copy of farmers, tenants and farm ownersfrom the Municipal Agricultures Office and will coordinate / conduct a scheduledmeeting with them to introduce the product of the Bank. The Bank will alsocontinue to distribute flyers and keep on posting an advertisement of the productto different Municipalities and public places.

Another strategy of the bank is to obtain an updated list of businesses with goodstanding record within the area of operations including the list of activetransportation operators to introduce the product of the bank that suits theirneeds in terms of financial assistance.

The Board and Senior Management will monitor the accomplishments and actionplans taken of all offices to ensure that all plans and strategies are implemented.

2017 ANNUAL REPORT

Annual Report 2017 | Page 6 of 106

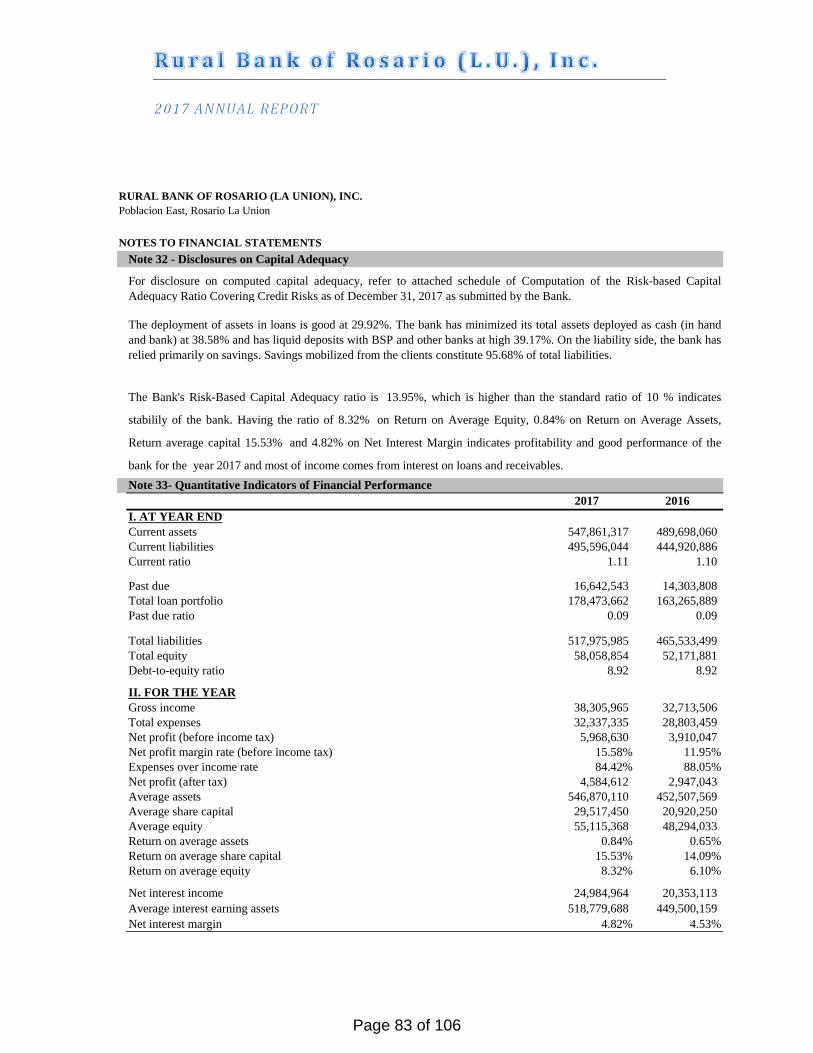

FINANCIAL SUMMARY 2017 2016

ProfitabilityTOTAL INTEREST INCOME 27,072,657 22,578,605TOTAL NON-INTEREST INCOME 11,233,308 10,134,901TOTAL NON-INTEREST EXPENSE 30,249,643 26,577,968PRE-PROVISION PROFITALLOWANCE FOR CREDIT LOSSES 1,719,082 1,771,121NET INCOME 4,584,612 2,947,043Selected Balance Sheet DataLIQUID ASSETS 375,512,982 334,874,776GROSS LOANS 182,251,605 166,778,735TOTAL ASSETS 576,034,839 517,705,381DEPOSITS 495,596,044 444,920,886TOTAL EQUITY 58,058,854 52,171,881Selected RatiosRETURN ON EQUITY 7.09% 5.53%RETURN ON ASSETS 0.82% 0.59%OthersOFFICERS 15 15STAFF 40 42

2017 ANNUAL REPORT

Annual Report 2017 | Page 7 of 106

REPORT TO STOCKHOLDERS

We would like to take this opportunity to express our deepest appreciation to our CLIENTS whohave trusted and continually patronized us, to our EMPLOYEES who have wholeheartedly giventhe best service to everyone and to our STOCKHOLDERS who unwaveringly supportedMANAGEMENT over the past years, as we continually embark on our journey as a leadingfinancial institution in Northern Luzon.

The past year has been a fulfilling and successful undertaking for the Rural Bank of Rosario (LaUnion), Inc. as we continually feel very proud of our achievements in taking our financialinstitution to a new level.

We are glad to share with you some very important strength of our Bank’s operations as ofDecember 2017.

Total Resources grew by 11.27% to Php576 million compared to previous year 2016,backed by continued growth in Deposits.

Total Deposit increased by 11.39% to Php495 million from Php444 million last year2016.

Total Loans rose to Php182.25 million, an increase of Php15.47 million compared toprevious year 2016.

Net Income reached Php4.47 million, a substantial increase over 2016.

The Bank’s Financial Performance demonstrated resilience amid a challenging businessenvironment and in spite of the presence of a variety of competitors.

Given all these challenges, we undertook initiatives to raise brand awareness and sustainedgrowth metrics through sustained marketing of LOANS and innovative new products such asAgricultural Loans and other services.

Our journey is about improving lives through lending activities, creating jobs and to promotefinancial inclusion that will enable Filipinos, especially the unserved and underserved ruralareas to receive and make payments as well as have a facility for store of value through ourdeposit products.

In pursuit of Good Governance, we continue to conduct several trainings and seminars toenhance our personnel capabilities through the Basic Rural Banking Course (BRBC),Management Training and Development Programs (MTP and MDP) and participating inrelevant trainings mostly conducted by the RBAP Foundation and other learning institutions.We also awarded the most outstanding employee award to recognize the efforts and initiativesof our executives and staff.

2017 ANNUAL REPORT

Annual Report 2017 | Page 8 of 106

We would like to acknowledge the dedication of our 55 personnel and thank them for theirefforts in working toward the Bank’s success and our clients for their continued trust andpatronage, the hallmark of our operations.

Jesus G. Tabora Nicolas R. TaboraChairman President

2017 ANNUAL REPORT

Annual Report 2017 | Page 9 of 106

The Bank is exposed to a variety of financial risk arising from its business activities. It enters intofinancial instrument contracts, which consist of AFS financial assets, HTM investments, loans andreceivables, and financial liabilities such as deposits and bills payable to finance the Bank’s operations.The main types of risk to which the Bank is exposed includes credit risk, liquidity risk, market/investmentrisk, interest rate risk, operations risk, legal risk, reputational risk and regulatory/compliance risk.

The effective management of risk has always been a fundamental element of Rural Bank of Rosario (LU),Inc. As a result, sound risk management is a reflection of the effectiveness of the Board and SeniorManagement in administering its portfolio of products, activities, processes and systems.

The Board of Directors created the Audit Committee to oversee the development of risk managementprogram of the Bank. The AC is responsible to closely monitor the system of limits to discretionaryauthority that the Board delegates to the management and ensures that the system remains effective.AC ensures that the limits are observed and that immediate corrective actions are taken whenever limitsare breached.

CREDIT RISK

Arises from the borrower’s failure to pay interest and/or loan principal at maturity date. The Bank isexposed to this risk for various financial instruments arising from granting loans and receivables tocustomers, including related parties.

The Bank’s credit risk strategy is to identify and ensure that the bank’s plan to grant credit based onvarious client segments and products, economic sectors, geographical location, currency and maturity.Ensures that the target market within each lending segment and highly diversified among the number ofindustries. In addition, credit / lending activity is not fully concentrated in a specific industry. The Bankalso considers the pricing strategy. The Bank also conducts an in-depth understanding of the client’sbusiness and their capabilities.

The senior management of the bank develops and establishes credit policies and credit administrationprocedures as a part of the overall credit risk management framework and gets those approved from

2017 ANNUAL REPORT

Annual Report 2017 | Page 10 of 106

Board. Such policies and procedures shall provide guidance to the concerned employees on varioustypes of lending such as but not limited to loans to MSME, Agri-Agra, Consumer loans, etc.;

The senior management of the bank develops and establishes credit policies and credit administrationprocedures such as:

- Detailed and formalized credit evaluation and appraisal process;- Credit approval authority at various hierarchy levels (i.e., BOD, CREDITCOM & Branch

Head/Branch Operations) for approving exceptions;- Risk identification, measurement, monitoring and control;- Risk acceptance criteria;- Credit origination and credit administration and loan documentation procedures;- Roles and responsibilities of units/staff involved in origination and management of credit;- Guidelines on management of problem loans.

The Bank adopts the Borrowers Risk Rating System (BRRS) and Cash Flow Analysis (CFA), which is asummary of the Bank’s individual credit exposure. This rating system categorized all credits into variousclasses on the basis of underlying credit quality. A well-structured credit rating framework is animportant tool for monitoring and controlling risk inherent in individual credits as well as in creditportfolios of a bank or a business line. The importance of BRRS framework becomes more eminent dueto the fact that historically major losses to banks stemmed from default in loan portfolios.

An internal rating framework would facilitate the Bank in a number of ways, such as:

- Credit selection- Amount of exposure- Tenure and price of facility- Frequency or intensity of monitoring- Analysis of migration of deteriorating credits and more accurate computation of future loan

loss provision- Deciding the level of Approving authority of loan.

CREDIT MANUAL INCORPORATING THE 7 Cs of Credit:

1. Character2. Capacity3. Capital4. Collateral

5. Conditions6. Cash Flow7. Commitment

2017 ANNUAL REPORT

Annual Report 2017 | Page 11 of 106

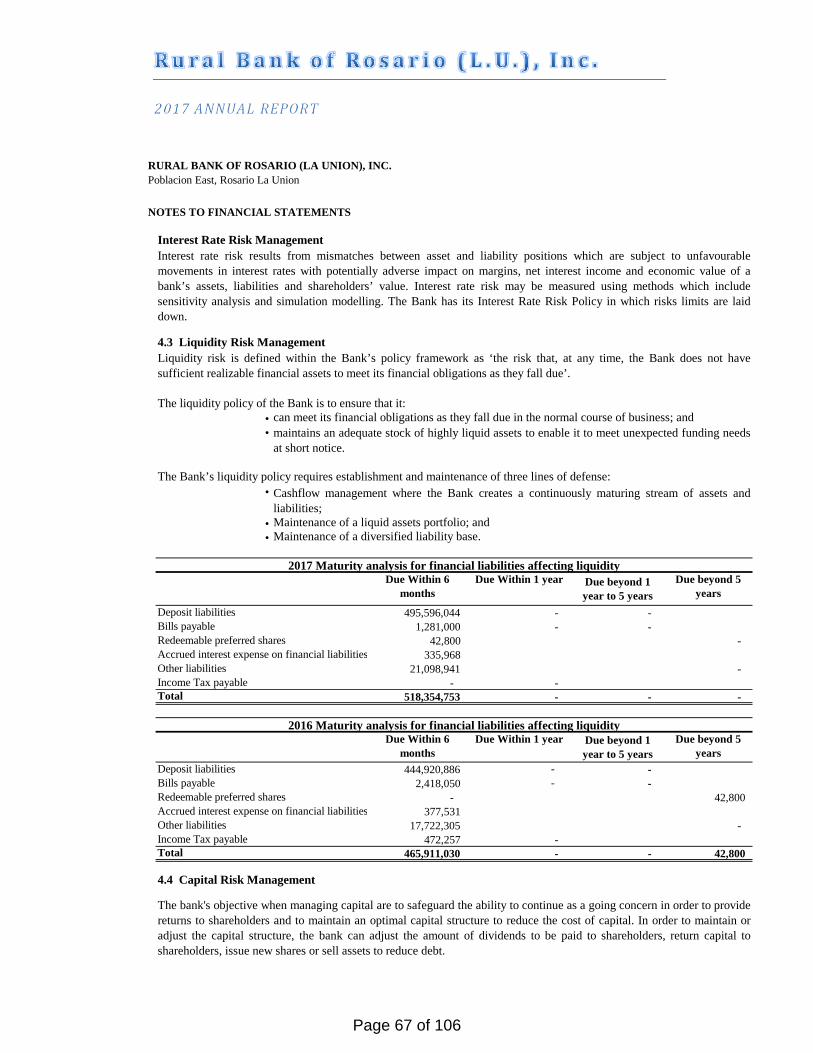

LIQUIDITY RISK

Arises from the failure to meet maturing obligations due to mismatch in cash flows and incidence of highpast due loans which may put pressure on the bank’s liquidity position.

BOD and Senior Management availed credit lines from major financial institutions through rediscountingfacilities to manage the liquidity position of the bank. The Management is not totally reliant on depositliabilities but also on the establishment of credit lines with financial institutions offering lower interestrates

Cash and Accounting Department together with the Bank management always maintain and monitorthe following:

List of maturing obligations such as time deposits, bills payable, etc.; and Weekly Report on Required and Available Reserves (WRRAR) if properly complied with.

Bank is fortified to promote their CASA deposit liabilities rather than Time Deposits to limit the exposureto large withdrawals from big/large time deposits. Strong internal control maintained by the Bank toallow the flow of collections from credit exposures and maintenance of funds from investments andbank deposit. The cash department and accounting department maintains, monitor and stress test itscash flow analysis/projection.

The accuracy of MIS reports and Daily Cash Position Report is vital to monitor the liquidity position ofthe bank. Cash department monitors daily the availability of sources of funds aside from deposit.Maturity Matching report and IBODI Management is also included in the monitoring activity of the CashDepartment together with the accounting department and the management.

MARKET AND INVESTMENT RISK

This is defined as the risk to earnings or capital arising from the possible deterioration in value ofacquired assets and decline in value of investments in equities and debt instruments.

These risks may arise from the following:

a. Risk that issuer may not be able to meet obligations promptlyb. Risk of decline in value of investments due to investment decisions which fail to take into

account

Marketability in investment instrument. If a bank cannot wait to hold on investment untilmaturity, there must be/may be buyers in the market willing to pay at a price that is close tobank’s acquisition cost so that the bank will not incur a loss

2017 ANNUAL REPORT

Annual Report 2017 | Page 12 of 106

Diversification of investment outlets Maturity and rate or return Type of issuer (to ensure payment on maturity) BSP regulations on limits and ceilings.

There are some mitigating factors for market and investment risk which includes the major investmentto any financial institution must be approved by the BOD and it shall be the responsibility of the seniormanagement & cash department to assess and identify the capabilities and stability of the financialinstitution before they recommend to the top management and BOD of where to invest the funds of theBank. This also includes the proper monitoring of maturing obligations be considered before aninvestment shall be made. Senior management & Cash Department also determines the benefits to bederived from investments, whether it could be used to increase the Risk-Based Capital Adequacy Ratioof the Bank.

INTEREST RATE RISK

This is the risk to earnings or capital arising from mismatches of the timing within which interest rateson assets and liabilities can be changed.

To be able to mitigate the risk, the Senior Management & Branch operations are responsible for surveyof interest rate to various banks. The accuracy of the MIS reports is also being implemented includinginterest rate and maturity matching report.

OPERATIONS RISK

Arising from the result of weakness in organizational structure, poor oversight functions of the Board ofDirectors and Senior Management, hiring policies, weak internal control system, and inadequatemanagement information system.

The objective of operational risk management is the same for credit, market and liquidity risks, and thatis to find out the extent of the financial institution’s operational risk exposure; to understand whatdrives it, to allocate capital against it and identify trends internally and externally that would helppredicting it. The management of specific operations risks is not a new practice, it has always beenimportant for banks to try to prevent fraud, maintain the integrity of internal controls, and reduce errorsin transactions processing, and so on. However, what is relatively new is the view of operational riskmanagement as a comprehensive practice comparable to the management of credit and market risks inprinciples. Failure to understand and manage operational risk, which is present in virtually all bankingtransactions and activities, may greatly increase the likelihood that some risks will go unrecognized anduncontrolled.

Ultimate accountability for operational risk management rests with the board, and the level of risk thatthe organization accepts, together with the basis for managing those risks is driven by those chargedwith overall responsibility for running the business;

2017 ANNUAL REPORT

Annual Report 2017 | Page 13 of 106

The board and top management should ensure that there is an effective, integrated operational riskmanagement framework. This should incorporate a clearly defined organization structure, with definedroles and responsibilities for all aspects of operational risk management/monitoring and appropriatetools that support the identification, assessment, control and reporting of key risks;

Operational risk policies and procedures that clearly define the way in which all aspects of operationalrisk are managed should be documented and communicated. These operational risk managementpolicies and procedures should be aligned to the overall business strategy and should support thecontinuous improvement to risk management;

All business and support functions should be an integral part of the overall operational risk managementframework in order to enable the institution to manage effectively the key operational risks facing theinstitution;

Like management should establish processes for the identification, assessment, mitigation, monitoringand reporting of operational risk that are appropriate to the needs of the institution, easy to implement,operate consistently over time and support an organization view of operational risks and materialfailures.

Senior management should transform the strategic direction given by the board through operational riskmanagement policy. Although the Board may delegate the management of this process, it must ensurethat its requirements are being executed. The policy should include:

The strategy given by the board of the bank; The system and procedures to institute effective operational risk management framework; The structure of operational risk management function and the roles and responsibilities of

individuals involved.

The policy should establish a process to ensure that any new or changed activity, such as new productsor systems conversions will be evaluated for operational risk prior to going online. It should be approvedby the board and documented. The management should ensure that it is communicated and understoodthroughout in the institution. The management also needs to place proper monitoring and controlprocess in order to have effective implementation of the policy.

Bank’s should identify and assess the operational risk inherent in all material products, activities,process and systems and its vulnerability to theses risk. Banks should also ensure that before newproducts and services are introduced or undertaken, the operational risk inherent in them is subject toadequate assessment procedures. While a number of techniques are evolving, operating risk remainsthe most difficult risk category to quantify. It would not be feasible at the moment to expect banks todevelop such measures. However, the banks could systematically tract and record frequency, severityand other information on individual loss events. Such a data could provide meaningful information forassessing the bank’s exposure to operational risk and developing a policy to mitigate/control that risk.

2017 ANNUAL REPORT

Annual Report 2017 | Page 14 of 106

Top management should establish a program to: Monitor assessment of the exposure to all types of operational risk faced by the Bank; Assess the quality and appropriateness of mitigating action, including the extent to which

identifiable risks can be transferred outside the institution.

Written policies and procedures in all aspect of the operations are very much essential to mitigate theexposure to operational risk. These should be manualized and need to be reinforced through a strongcontrol culture that promotes sound risk management practices. Banks should assess the feasibility ofalternative risk limitation and control strategies and should adjust their operational risk profile usingappropriate strategies, in light of their overall risk appetite and profile. To be effective, control activitiesshould be an integral part of the regular activities of a Bank.

Bank in place the following Manuals to ensure its ability to operate as going concern and ensure thatadequate controls and systems to identify and address problems before they become major concerns.

MITIGATING OPERATIONS RISK

Manual of Operations Deposit Manual Loan Operations Manual Accounting Manual Branch Banking Operation Manual Credit Risk Manual Risk Management Manual IA Manual Compliance Manual Security Manual Business Continuity Plan Contingency Funding Plan Employees Manual Succession Plan MLPP

2017 ANNUAL REPORT

Annual Report 2017 | Page 15 of 106

LEGAL RISK

This is the risk to earnings or capital that may arise as a result of unenforceable contracts, lawsuits, oradverse judgments.

The risk may arise from the following:

1. Possibility that contracts are not legally enforceable due to Failure to carefully review all contracts entered into by bank Breach of contract terms and conditions

2. Protracted court cases

The daily operations of the Bank always prove to be the most fertile ground for legal input. Anabundance of legal consequences can be found in the cash operations, accounting, credit and collection,appraisal, etc., Each area should have their own manuals, must be independent from each other andshould be very much aware of the legal consequences of their actions should they deviate from theoperating procedures of the Bank. Accuracy and enforceability of forms, contracts and MOA’s

REPUTATIONAL RISK

This is the risk arises from negative / adverse public opinion. Reputation risk is the threat to meetingexpectations that in turn precipitates a crisis. It is created when expectations are poorly managed andexceed capabilities, or when the Bank simply fails to execute. Negative media coverage is often blamedon marketing, but the internet now extends exposure far beyond the reach of marketing activities.Almost everything a company does, overtly or covertly, is a public form of communication. Anystakeholder with access to a keyboard and the internet can be a self-appointed investigative journalist.

A reputation crisis occurs when stakeholders change their expectations and behaviors. Customers stopdepositing their money, employees leave, loan borrowers lose interest in the products and services ofthe Bank, regulators and other partners withdraw their accreditation to the Bank, litigators andreporters inevitably pile on. Adding insult to injury, culpability and public opprobrium land on directorsand officers. For them, the stain of a reputation crisis can be personal and permanent.

Managing expectations is all about governance, operations and risk management—the blocking andtackling of running a business. Clearly, there can be perverse brilliance in a business strategy of settingexpectations very low. Less obvious, however, is the fact that public relations efforts to pump upexpectations or spin a story can backfire terribly if the campaign is not supported by operationalrealities. The BOD and Senior Management quickly analyze gaps in enterprise-level controls,

2017 ANNUAL REPORT

Annual Report 2017 | Page 16 of 106

conceptualize an ideal state and implement a roadmap to reduce reputation risk. Better expectationmanagement and operational controls are enabled by quantitative reputational controls, historicreviews of financials and related tools. These can help define the value at risk associated withreputational volatility and stakeholder expectations. Also, training for employees on how to answer /react to questions from the public is significant.

REGULATORY / COMPLIANCE RISK

The risk of legal or regulatory sanctions, financial loss, or loss to reputation a bank may suffer as a resultof its failure to comply with all applicable laws, regulations, and codes of conduct and standards of goodpractice.

Regulators and governments are issuing newer regulations to avoid future crises and cracking the whipdown on banking organizations that do not conform. As a result, the average business today isconfronted with a plethora of cross-industry regulations, each consisting of hundreds of requirementsand rules. Dealing with these requirements in a traditional manner is no longer cost-effective orefficient. It requires a renewed business model that analyzes compliance requirements, prioritizes theirimportance to the business, applies the appropriate control and monitors the system consistently. Therisk exposes the bank and its directors and officers to fines, monetary penalties and administrativesanctions.

Compliance risk, which is often overlooked as it blends into operational risk and transaction processing,is the risk to earnings or capital arising from violations of, or non-conformance with, laws, rules ®ulations, code of conduct, customer relationship rules or ethical standards. It encompasses all laws,as well as prudent ethical standards and contractual obligations. Compliance risk also arises in situationswhere the laws or rules governing certain bank products or activities of the bank's clients may beambiguous or untested. Compliance risk, also referred to as integrity risk sometimes, exposes theorganization to legal penalties, payment of damages, limitation of business opportunities, diminishedreputation, lessened expansion potential and the voiding of contracts.

To strengthen its compliance risk program, the banks need an efficient solution for conductingcompliance processes, identifying & assessing risks, implementing & monitoring controls andmitigating/eliminating the gaps across its vast operations.

Managing compliance risk has become a core skill that every bank must have in today’s highly regulatedindustry and a consolidated-or "enterprise-wide"-approach to compliance risk management has become"mission critical" for rural banking organizations.

ANTI-MONEY LAUNDERING

While striving to sustain economic development and poverty alleviation through, among others,corporate governance and public office transparency, the Philippines realized the need to contribute its

2017 ANNUAL REPORT

Annual Report 2017 | Page 17 of 106

share and play a vital role in the global fight against money laundering. The government thus recognizedthe compelling need to enact a responsive anti-money laundering legislation in order to establish andstrengthen an anti-money laundering regime in the country. The anti-money laundering law is expectedto strengthen the country’s financial institutions, increase investors’ confidence and eventually ensurethat the Philippines is not used as a site to launder dirty money to finance terrorists or legitimizeorganize crime fronts.

By the authority vested to the Bangko Sentral ng Pilipinas to issue guidelines and circulars on anti-money laundering (AML) and combating the financing of terrorism (CFT), in order to effectivelyimplement the provisions of Republic Act (R.A.) No. 9160, otherwise known as the "Anti-MoneyLaundering Act of 2001" (AMLA), as amended by R.A. Nos. 9194, 10167 and 10365, as provided underRule 18 of the Revised Implementing Rules and Regulations (RIRR) of the AMLA, as amended, as well asR.A. No. 10168 or The Terrorism Financing Prevention and Suppression Act of 2012, as provided underRule 27 of its Implementing Rules and Regulations (IRR), the Monetary Board, in its Resolution No. 334dated 23 February 2017, approved the amendments to Part Eight or the Anti-Money LaunderingRegulations of the Manual of Regulations for Banks (MORB).

The Rural Bank of Rosario (La Union), Inc. adopts the policies of the State to (a) protect the integrity andconfidentiality of bank accounts and ensure that the Philippines, in general, and the Rural Bank, inparticular, shall not be used, respectively, as a money laundering site and conduit for the proceeds of anunlawful activity as herein defined; and (b) to protect life, liberty and property from acts of terrorismand to condemn terrorism and those who support and finance it and reinforce the fight againstterrorism by criminalizing the financing of terrorism and related offenses. The Bank revised its Anti-Money Laundering Program and adopts the newly issued BSP Circular No. 950 dated 15 March 2017.

It is the policy of the Rural Bank of Rosario (La Union), Inc. to actively promote and pursue corporategovernance reforms and to consciously observe principles of accountability and transparency with theutmost degree of professionalism and effectiveness. The Board of Directors of RBR adopts the Manual ofCorporate Governance to steer the corporate organization toward excellence and competitiveness,locally and globally, thus enabling it to be a valuable partner of the government in nationaldevelopment. The Bank adopted the BSP Circular 969 that was issued on 22 August 2017 otherwiseknown as the Enhanced Corporate Governance Guidelines for BSP-SFI.

The powers and functions of RBR are exercised by the Board of Directors. The Board is the policy makingbody and is primarily responsible for good governance in RBR. Corollary to this main responsibility, theBoard shall chart the corporate strategy and set guidelines for accomplishment of corporate objectives,as well as provide an independent check on management.

2017 ANNUAL REPORT

Annual Report 2017 | Page 18 of 106

The responsibilities of Board are provided in its By-Laws and other relevant legislation, rules andregulations.

The business affairs of the bank is being conducted under the supervision and control of the Board ofnot less than five (5) nor more than eleven (11) directors which at all times be odd numbers. The holdersof common stock entitled to vote elects such directors in the manner provided in the Section 31 of Act1459 as amended (Corporation Law) whose qualifications is subject to the approval of the MonetaryBoard of the Central Bank of the Philippines. Only Filipino citizens are eligible for election to the Board.No individual is eligible to become or be a director if he is or becomes a candidate for or holder of anypublic office.

The executive officers of the Bank are the President, Vice-President, Secretaries, Bank Manager,Assistant Managers, Branch Heads and Cashiers who was elected by a majority vote of the entiremembership of the Board of Directors at its first meeting held after the annual stockholders meeting,and at such other times during the year as may be required to fill vacancies. The position of Secretaryand Cashier may be combined in one person.

The President is the Chief Executive Officer of the Bank. The primary role is to see to it that all ordersand resolutions of the Board of Directors, all orders of the Monetary Board of the Central Bank of thePhilippines, and all rules and regulations governing Rural Banks are carried into effect, and exercisessuch other powers and perform such other duties as are prescribed for the Office of the President in theby-laws. The Vice-President exercises the powers, authority and duties of the President during theabsence or inability to act of the latter.

The Secretary provides for the keeping of the records of the Bank and has the custody of the seal of thecorporation. The Secretary, in addition, exercise such other powers and perform such other duties as areprescribed for the Office of the Secretary and all other duties usually pertaining to that office, and suchother duties as may be prescribed from time to time by the Board of Directors.

Bank Manager/Assistant Managers/Branch Heads.- The Board of Directors shall provide for the positionof a Bank Manager/Assistant Managers/Branch Heads who shall have, subject to the control of theBoard of Directors, general management of the business affairs of the Bank.

A Compliance Officer is to oversee and coordinate the implementation of the compliance system. Hisresponsibility includes the identification, monitoring and controlling of compliance risk. Theappointment/designation of a compliance officer requires prior approval of the Monetary Board. Thebio-data of the proposed compliance officer is submitted to the appropriate department of the SES. Thecompliance officer has the skills and expertise to provide appropriate guidance and direction to the bankon the development, implementation and maintenance of the compliance program.

The Audit Committee assists the board in fulfilling its corporate governance responsibilities and ensuresthe board’s effectiveness and due observance of corporate governance principles and guidelines. The

2017 ANNUAL REPORT

Annual Report 2017 | Page 19 of 106

audit committee is composed of members of the board of directors; one is the independent director,including the Chairman.

Name Type of Directorship Number of yearsserved as Director

Number ofShares

Percentage ofshares

JESUS G. TABORA Executive Director 48 21,233 6.34%

NICOLAS R. TABORA Executive Director 29 8,088 2.41%

MARIANITA P. LADIA Non-executive Dir. 48 20,035 5.98%

SUSAN T. GUEVARA Executive Director 4 2,266 0.68%

CNTHIA BARBARA T. TUASON Non-executive Dir. 17 7,000 2.09%

NICHOLO ANDRE K. TABORA Non-executive Dir. 3 393 0.12%

ELVIRA E. BARROGA Independent Dir. 8 months 68 0.02%

A director shall have the following minimum qualifications enumerated in Subsec. X142.3 of BSPCircular 969:

1. He must be fit and proper for the position of a director. In determining whether a person is fitand proper for the position of a director, the following matters must be considered: integrity/ probity, physical / mental fitness; relevant education/financial literacy / training; possession ofcompetencies relevant to the job, such as knowledge and experience, skills, diligence andindependence of mind; and sufficiency of time to fully carry out responsibilities.

In assessing a director's integrity/probity, consideration shall be given to the director'smarket reputation, observed conduct and behavior, as well as his ability to continuouslycomply with company policies and applicable laws and regulations, including market conductrules, and the relevant requirements and standards of any regulatory body, professionalbody, clearing house or exchange, or government and any of its instrumentalities/agencies.

2017 ANNUAL REPORT

Annual Report 2017 | Page 20 of 106

An elected director has the burden to prove that he possesses all the foregoing minimumqualifications and none of the cases mentioned under Subsection X150.1. A director shall submitto the Bangko Sentral the required certifications and other documentary proof of suchqualifications using the Appendix 98 as guide within twenty (20) banking days from the dateof election. Non· submission of complete documentary requirements or their equivalent withinthe prescribed period shall be construed as his failure to establish his qualifications forthe position and results in his removal from the board of directors.

The Bangko Sentral shall also consider its own records in determining the qualifications of adirector.

The members of the board of directors shall possess the foregoing qualifications in addition tothose required or prescribed under R.A. No. 8791 and other applicable laws and regulations.

2. He must have attended a seminar on corporate governance for board of directors. A directorshall submit to the Bangko Sentral a certification of compliance with the Bangko Sentral-prescribed syllabus on corporate governance for first time directors and documentary proof ofsuch compliance: Provided, That the following persons are exempted from complying with theaforementioned requirement:

a. Filipino citizens with recognized stature, influence and reputation in the banking communityand whose business practices stand as testimonies to good corporate governance;

b. Distinguished Filipino and foreign nationals who served as senior officials in central banksand/or financial regulatory agencies, including former Monetary Board members; or

c. Former Chief Justices and Associate Justices of the Philippine Supreme Court:

Provided, further, that this exemption shall not apply to the annual training requirements forthe members of the board of directors.

Independent and non-executive directors

In selecting independent and non-executive directors, the number and types of entities where thecandidate is likewise elected as such, shall be considered to ensure that he will be able to devotesufficient time to effectively carry out his duties and responsibilities. In this regard, the following shallapply:

1. A non-executive director may concurrently serve as director in a maximum of five (5) publiclylisted companies. In applying this provision to concurrent directorship in entities within aconglomerate, each entity where the non- executive director is concurrently serving asdirector shall be separately considered in assessing compliance with this requirement; and

2. An independent director of a BSFI may only serve as such for a maximum cumulative term of nine(9) years. After which, the independent director shall be perpetually barred from serving as

2017 ANNUAL REPORT

Annual Report 2017 | Page 21 of 106

independent director in the same BSFI, but may continue to serve as regular director. The nine(9) year maximum cumulative term for independent directors shall be reckoned from 2012.

Members of the board of directors shall not be appointed as Corporate Secretary or Chief ComplianceOfficer.

Chairperson of the board of directors.

To promote checks and balances, the Chairperson of the board of directors shall be a non-executivedirector or an independent director, and must not have served as CEO of the BSFI within the past three(3) years. The positions of Chairperson and CEO shall not be held by one person. In exceptional caseswhere the position of Chairperson of the board of directors and CEO is allowed to be held by one (1)person as approved by the Monetary Board, a lead independent director shall be appointed.

For this purpose, the board of directors shall define the responsibilities of the lead independent director,which shall be documented in the corporate governance manual. The board of directors shall ensurethat the lead independent director functions in an environment that allows him to effectively challengethe CEO as circumstances may warrant. The lead independent director shall perform a more enhancedfunction over the other independent directors and shall: (1) lead the independent directors at boardof directors meetings in raising queries and pursuing matters; and (2) lead meetings of independentdirectors, without the presence of the executive directors.

In the case of the Rural Bank of Rosario (La Union), Inc., the Bank is categorized as simple or non-complex Bank. Only Audit Committee is required by the Bangko Sentral Pilipinas.

The BOD created Audit Committee to assist the Board in fulfilling its corporate governanceresponsibilities and ensures the Board’s effectiveness and due observance of corporate principles andguidelines.

Audit Committee

Chairman: Elvira E. Barroga (Independent Director)Members: Cynthia Barbara T. Tuason & Nicholo Andre K. Tabora

The audit committee is composed of three (3) members of the board of directors, who are non-executive directors; the Chairperson is the independent director.

2017 ANNUAL REPORT

Annual Report 2017 | Page 22 of 106

The audit committee shall have accounting, auditing, or related financial management expertise orexperience commensurate with the size, complexity of operations and risk profile of the BSFI. It shallhave access to independent experts to assist them in carrying out its responsibilities. The AC shall:

1. Oversee the financial reporting framework. The committee shall oversee the financial reportingprocess, practices, and controls. It shall ensure that the reporting framework enables thegeneration and preparation of accurate and comprehensive information and reports.

2. Monitor and evaluate the adequacy and effectiveness of the internal control system. Thecommittee shall oversee the implementation of internal control policies and activities. It shallalso ensure that periodic assessment of the internal control system is conducted to identify theweaknesses and evaluate its robustness considering the Bank’s risk profile and strategicdirection.

3. Oversee the internal audit function. The committee shall be responsible for theappointment/selection, remuneration, and dismissal of internal auditor. It shall review andapprove the audit scope and frequency. The committee shall ensure that the scope covers thereview of the effectiveness of the Bank’s internal controls, including financial, operationaland compliance controls, and risk management system. The committee shall functionally meetwith the head of internal audit and such meetings shall be duly minuted and adequatelydocumented. In this regard, the audit committee shall review and approve the performance andcompensation of the head of internal audit, and budget of the internal audit function.

4. Oversee the external audit function. The committee shall be responsible for the appointment,fees, and replacement of external auditor. It shall review and approve the engagement contractand ensure that the scope of audit likewise cover areas specifically prescribed by the BangkoSentral and other regulators.

5. Oversee implementation of corrective actions. The committee shall receive key audit reports,and ensure that senior management is taking necessary corrective actions in a timelymanner to address the weaknesses, non-compliance with policies, laws, and regulations andother issues identified by auditors and other control functions.

6. Investigate significant issues/concerns raised. The committee shall have explicit authority toinvestigate any matter within its terms of reference, have full access to and cooperation bymanagement, and have full discretion to invite any director or executive officer to attend itsmeetings.

7. Establish whistleblowing mechanism. The committee shall establish and maintain mechanismsby which officers and staff shall, in confidence, raise concerns about possible improprieties ormalpractices in matters of financial reporting, internal control, auditing or other issues topersons or entities that have the power to take corrective action. It shall ensure thatarrangements are in place for the independent investigation, appropriate follow-up action, andsubsequent resolution of complaints.

2017 ANNUAL REPORT

Annual Report 2017 | Page 23 of 106

Name of Directors BoardNumber of Meetings

Audit CommitteeNumber of Meetings

Attended % Attended %1. Jesus G. Tabora 25 100% n/a n/a2. Nicolas R. Tabora 25 100% n/a n/a3. Marianita P. Ladia 25 100% n/a n/a4. Nicholo Andre K. Tabora 25 100% 25 100%5. Susan T. Guevara 20 80% n/a n/a6. Cynthia Barbara T. Tuason 20 80% 20 80%7. Elvira E. Barroga 24 96% 24 96%

2017 ANNUAL REPORT

Annual Report 2017 | Page 24 of 106

ENGR. JESUS G. TABORA Chairman of the BoardNICOLAS R. TABORA President / CEOSUSAN T. GUEVARA Special Assistant to the PresidentVIRGINIA D. BASCO General ManagerRUSSELL CHARLES A. ANDRES Acting Compliance Officer IELLEN JOY O. BARUC Acting Internal Auditor IROCHELLE R. CASTRO Senior Bookkeeper / Head, Accounting DepartmentROGELIO S. SIMSIMAN Loan Officer / Head, Loans DepartmentMARIA LUISA F. DULAY Cashier / Head, Customer Service DepartmentSHIRLEY S. BASADRE Branch Banking Department Head / Branch Head, Sto. TomasANGELITO B. GABRILLO Branch Head, San FabianBUTCH L. MANALAYSAY Acting Branch Head, SisonRICHARD R. MURAO Branch Head, PozorrubioEMMALYN G. BRAGA Branch Head, BinalonanERLINDA E. RAMOS Human Resource Officer

The Board conducts self-assessment and peer assessment during Board meetings, evaluates anddiscusses the lowest rating. Senior Management is assessed in their individual capacity and all Officersand employees of the Bank on a regular basis. The results of the assessment are documented andanalyzed and facilitates for the effective performance of functions.

The Bank has a Basic Rural Banking Course (BRBC) seminar for all new employees of the Bank. Asidefrom the BRBC, the Bank has also a Management Training & Development Program, to train extensivelythe personnel in various Departments in order to prepare them to equally similar job/tasks and/or toassume a higher position.

The said trainings will give opportunities to all personnel to assume a higher position and/or vacancies inany of the Senior Officer level. The maximum duration of the program is 40 working days.

2017 ANNUAL REPORT

Annual Report 2017 | Page 25 of 106

With regards to the Directors, the Chairman of the Board ensures the conduct of proper orientation forfirst time director and provides training opportunities for all directors.

The Rural Bank of Rosario (L.U.) Inc. Retirement Manual was established and amended by virtue ofBoard Resolution No. 2016-128 dated September 29, 2016 in order to provide and anticipate thefinancial requirements of retiring employees.

In line with the Retirement Manual, a Succession Plan was established by virtue of Board ResolutionNumber 2017-131 dated October 12, 2017.

Succession Plan was established and amended for in the absence of any of the personnel in the HeadOffice and/or Branches, the Human Resource Officer shall appoint a reliever from the Head Office andall pending matters or duties shall be endorsed to the respective Department Heads or Branch Heads.

The Rural Bank of Rosario (L.U.) Inc. recognizes the need to strengthen its policy on related-partytransaction and other similar situations so as to prevent or mitigate abusive transactions with relatedparties and avoid risks of conflict of interest.

This is also in conformity with Rural Bank of Rosario (L.U.), Inc. adherence to the highest principles ofgood governance as the bank subscribes to the philosophy of integrity, accountability and transparencyin doing business.

The policy is intended to ensure that every Related Party Transaction in conducted in a manner that willprotect the Bank from conflict of interest which may arise between the Bank and its Related Parties; and

Ensure proper review, approval, ratification and disclosure of transactions between the Bank and any ofits Related Party/ ies as required in compliance with legal and regulatory requirements.

Related Parties shall cover the Bank’s Directors, Officers, Stockholders and Related Interests (DOSRI),and their close family members, as well as corresponding persons in affiliated companies. This shall alsoinclude such other person/juridical entity whose interest may pose potential conflict with the intereston the financial institution (FI)

Close Family Member persons related to the bank’s Directors, Officers and Stockholders (DOS) withinthe second degree of consanguinity or affinity, legitimate or common-law. These shall include the

2017 ANNUAL REPORT

Annual Report 2017 | Page 26 of 106

spouse, parent, child, brother, sister, grandparents, grandchild, parent-in-law, son/daughter-in-law,brother-/sister-in-law, grandparent-in-law of the FI’s DOS.

Material RPTs includes any financial transaction, arrangement or relationship in which the aggregateamount involved will or may exceed P5,000,000.00 in any year where a Related Party has or will havedirect or indirect material interest.

The Rural Bank of Rosario (L.U.) Inc. has an approved RPT policy under Board Resolution Number 2017-132 dated October 24, 2017.

The Bank has a Board approved Compliance Program and Internal Audit Plan/Program wherein theduties and responsibilities of Internal Audit and Compliance were defined. It also includes reviewprocess of the Board to ensure effectiveness and adequacy of Internal Control system.

Compliance ProgramBanking by its nature entails taking a wide array of risks. Risks are exposure to possible loss or injury thatmay affect capital and earnings. Nearly all transactions entered into by the bank involves risks. However,risk may also arise from action of bank or failure to comply with relevant laws, rules and regulationsissued by regulatory/supervisory bodies. The success of the bank is largely dependent on the ability ofits directors and officers to prudently manage risks. Compliance System designed specifically to identifyand mitigate Business Risk.

The Bangko Sentral ng Pilipinas (BSP) actively promotes the safety and soundness of the Philippinebanking system through an enabling policy and oversight environment. Such an environment isgoverned by the high standards and accepted practices of good corporate governance as collectivelydefined by the BSP and its supervised institutions. Pursuant to BSP Circulars No. 747, a ComplianceProgram/System is put in place and adopted by the RURAL BANK OF ROSARIO (LA UNION), INC. toprovide appropriate guidance and directions to the directors, officers, senior management and allpersonnel.

Reasonable steps to respond appropriately to the offense & to prevent further similar offenses –including any necessary modifications to its internal policies and procedures to prevent & detectviolations of law.

To mirror the level of awareness/knowledge on regulatory matters on specific complianceconcerns

Questions are based on frequency of formal & informal citations by the BSP Fines and penalties assessed for specific violations

2017 ANNUAL REPORT

Annual Report 2017 | Page 27 of 106

Results are submitted to the Board thru Audit Committee the Compliance Risk Assessment withcopies to Senior Management

Audit Plan/ProgramAn Audit Plan uses an audit risk model to quantify the risk rating of each audit unit. Audits will bescheduled by priority. This represents a departure from past practice which was based on less formaljudgment of risk and more on the passage of time since the last audit.

The Internal Audit Program shall define the policies and procedures that govern the conduct of internalauditing. It shall describe the underlying principles, policies, standards, procedures and processes in theperformance of internal audit activity by Internal Audit Department. The Attributes and PerformanceStandards of International Standards for the Professional Practice of Internal Auditing have beenconsidered in the Internal Audit Program.

The objective of a risk model is to optimize the assignment of audit resources through a comprehensiveunderstanding of the audit universe and the risks associated with each universe item. Defining an audituniverse is the first prerequisite to risk ranking. The audit universe to which the risk assessment will beapplied will be determined by the Internal Auditor. The determination of the audit universe will bebased on his knowledge of the company strategic plan and company operations, a review oforganization charts and function and responsibility statements of all company organizations (branches,office, units or sections ), and discussions with responsible management personnel.

Audit approaches or methodology is the framework or outline of a process which provides guidance andcontrol to help ensure the audit objectives are achieved.

The Internal Audit will consist of review of documents, interviews with key employees, and review ofwritten policies and procedures, inspections, data analysis, review of accounting entries and the usageof applicable audit tools. The audit will consist of the components described below. The phases arelisted in sequential order and should provide an overview of the sequencing of the proposedengagement.

As the audit progresses, the Internal Auditor/Staff shall provide draft report containing the initialfindings/observations in one or more risk areas. We expect that the branch/unit will respond quickly aspossible. Our team will compile all draft reports to branch/unit management during exit conference.

The final audit report is prepared based on the results of the exit conference. The auditee’s response toeach recommendation is also incorporated in the final report if it is available within a reasonable timeperiod following the discussion of the draft meeting. Confidential copies of the final report aredistributed to the head of office of the area audited and the Office of the President. The IA will presentthe final audit report to the Board thru Audit Committee.

2017 ANNUAL REPORT

Annual Report 2017 | Page 28 of 106

One of the primary responsibilities of professional auditors is to determine that the auditee takescorrective action or recommendations. This applies in all cases except where “senior management hasaccepted the risk of not taking action.”

Being an integral part of the internal audit process, follow-up should be scheduled along with the othersteps necessary to perform the audit. However, specific follow-up activity depends on the results of theaudit and can be carried out at the time the report draft is reviewed with concerned managementpersonnel or after the issuance of the report.

Rural Bank of Rosario recognizes the importance of customer protection in its financial dealings withclients. It fully supports the policy of the State to protect the interest of the consumers, promote theirwelfare and to establish standards of conduct for the banking industry. Further, the Bank believes tothe principle that the consumer is the driver of business; no business can survive without the patronageof consumers.

In this view, Rural Bank of Rosario has come up with its financial customer protection framework inorder to embolden the basic financial rights of its customers and establish standards of conduct ofbusiness between the clients and the Bank and its personnel.

For the past forty nine (49) years since its humble beginning, Rural Bank of Rosario has shown so muchconcern and fairness to its clients whether small or big. It treats clients with utmost courtesy andcommitted to maintain their respect, trust and confidence.

The Board of Directors (BOD) has the ultimate responsibility for the level of customer risk assumed byRural Bank of Rosario. Accordingly, the Board approves the Bank’s overall business strategies andsignificant policies, including those related to managing and taking customer risks.

The Board of Directors takes steps to develop an appropriate understanding of the customer risks theBank faces through briefings from auditors and experts external to the organization.

The Board of Directors is responsible for developing and maintaining a sound Customer Protection RiskManagement System that is integrated into the over-all framework for the entire product and servicelife-cycle.

Senior management is responsible for implementing a program to manage the customer compliancerisks associated with the Bank’s business model, including ensuring compliance with laws andregulations on both a long-term and a day-to-day basis. Accordingly, management should be fullyinvolved in its activities and possess sufficient knowledge of all major products to ensure that

2017 ANNUAL REPORT

Annual Report 2017 | Page 29 of 106

appropriate risk controls are in place and that accountability and lines of authority are clearlydelineated.

Senior management also is responsible for establishing and communicating a strong awareness of, andneed for, effective customer protection risk controls and high ethical standards.

The Board of Directors and Senior Management periodically review the effectiveness of the CustomerProtection Risk Management System (CPRMS) including how findings are reported and whether theaudit mechanism in place enables adequate oversight.

The Board and Senior Management anticipate and respond to customer protection risks that may arisefrom changes in the Bank’s competitive environment and to risks associated with new or changingregulatory or legal requirements.

Rural Bank of Rosario follows key protection principles in building up its good relations to its clients.Each principle is embedded in its operations, such as; credit extension, deposit taking and other bankingactivities involving the participation of its clients. The Bank ensures that the principles are carried outeffectively and efficiently by its employees through proper and regular orientation of bank policies andprocedures.

2017 ANNUAL REPORT

Annual Report 2017 | Page 30 of 106

Organizational Structure

2017 ANNUAL REPORT

Annual Report 2017 | Page 31 of 106

Board of Directors

FRONT SEAT: LEFT – MS. MARIANITA P. LADIA & ENGR. JESUS G. TABORASTANDING: L-R – NICOLO ANDRE K. TABORA, ELVIRA E. BARROGA, CYNTHIA BARBARA T.

TUASON, SUSAN T. GUEVARA AND NICOLAS R. TABORA

ENGR. JESUS G. TABORA CHAIRMAN OF THE BOARD

MS. MARIANITA P. LADIA VICE-CHAIRMAN OF THE BODMR. NICOLAS R. TABORA PRESIDENT/CEOCYNTHIA BARBARA T. TUASON DIRECTOR

SUSAN T. GUEVARA DIRECTOR

NICOLO ANDRE K. TABORA DIRECTOR

ELVIRA E. BARROGA INDEPENDENT DIRECTOR

2017 ANNUAL REPORT

Annual Report 2017 | Page 32 of 106

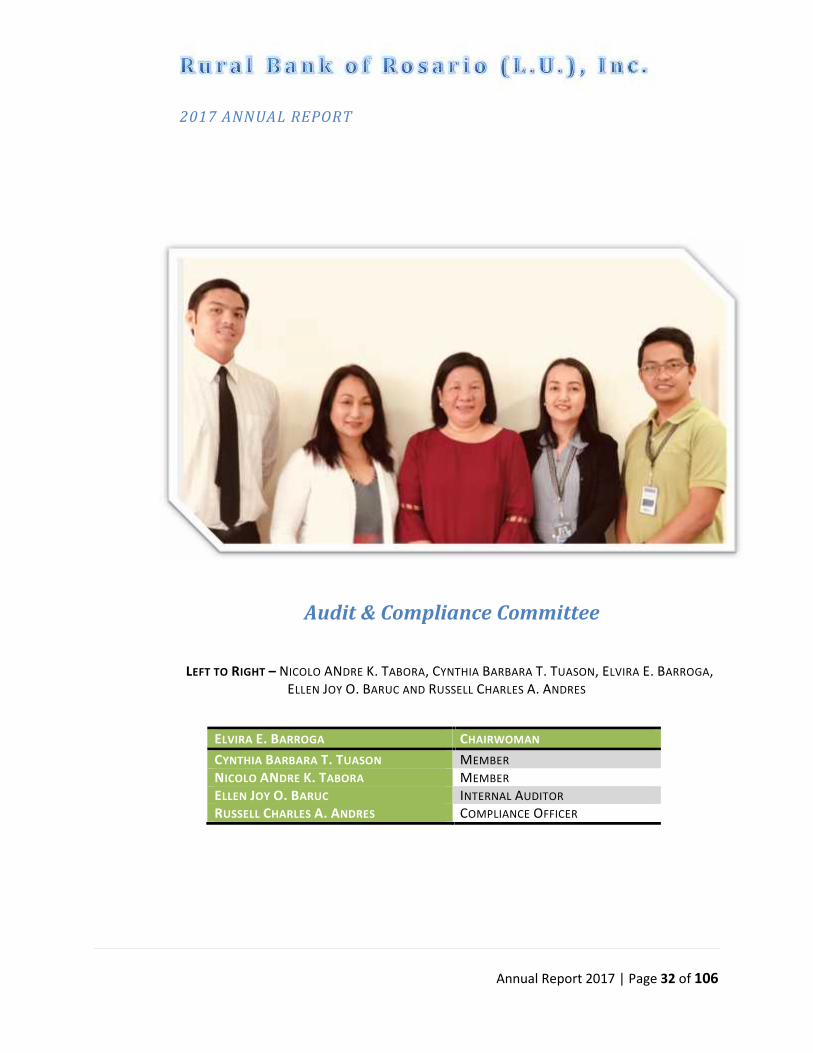

Audit & Compliance Committee

LEFT TO RIGHT – NICOLO ANDRE K. TABORA, CYNTHIA BARBARA T. TUASON, ELVIRA E. BARROGA,ELLEN JOY O. BARUC AND RUSSELL CHARLES A. ANDRES

ELVIRA E. BARROGA CHAIRWOMAN

CYNTHIA BARBARA T. TUASON MEMBERNICOLO ANDRE K. TABORA MEMBERELLEN JOY O. BARUC INTERNAL AUDITORRUSSELL CHARLES A. ANDRES COMPLIANCE OFFICER

2017 ANNUAL REPORT

Annual Report 2017 | Page 33 of 106

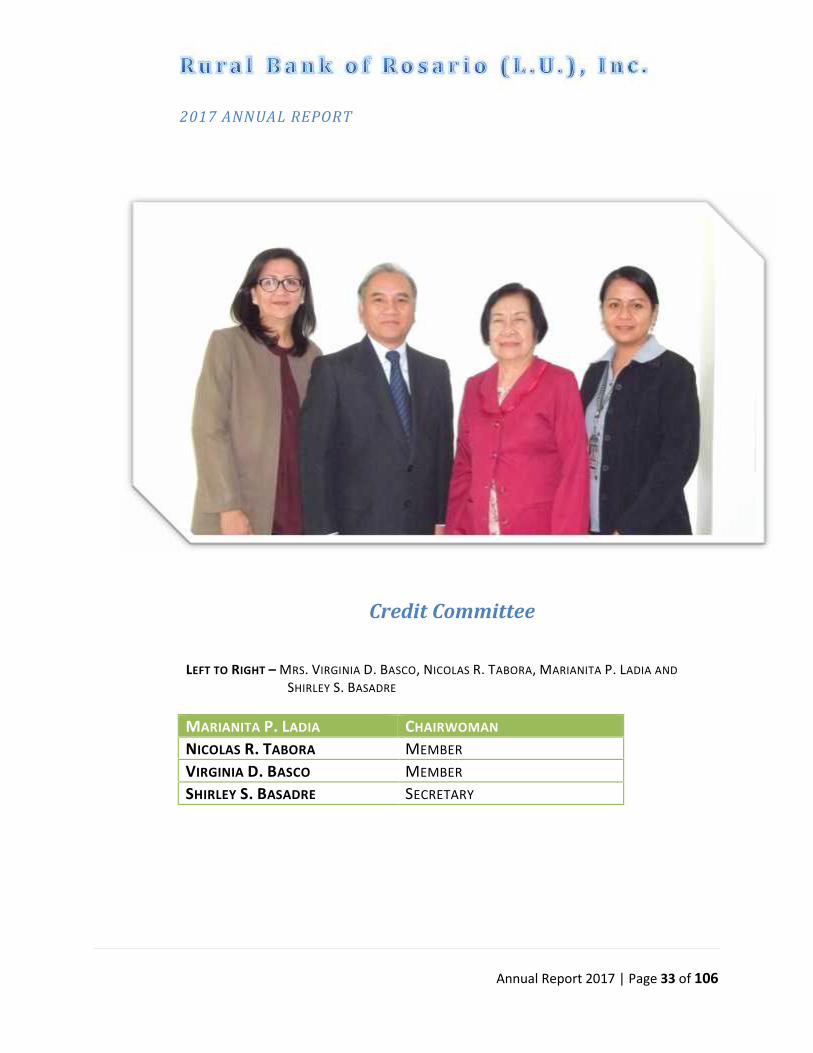

Credit Committee

LEFT TO RIGHT – MRS. VIRGINIA D. BASCO, NICOLAS R. TABORA, MARIANITA P. LADIA ANDSHIRLEY S. BASADRE

MARIANITA P. LADIA CHAIRWOMAN

NICOLAS R. TABORA MEMBER

VIRGINIA D. BASCO MEMBER

SHIRLEY S. BASADRE SECRETARY

2017 ANNUAL REPORT

Annual Report 2017 | Page 34 of 106

Personnel Committee

LEFT TO RIGHT – HAYDEE BERNADETTE D. HIPOLITO, VIRGINIA D. BASCO, CYNTHIA BARBARA T.TUASON, MARIANITA P. LADIA AND ERLINDA E. RAMOS

CYNTHIA BARBARA T. TUASON CHAIRWOMANMARIANITA P. LADIA MEMBER

VIRGINIA D. BASCO MEMBER

ERLINDA E. RAMOS MEMBER

HAYDEE BERNADETTE D. HIPOLITO SECRETARY

2017 ANNUAL REPORT

Annual Report 2017 | Page 35 of 106

Key Officers

LEFT TO RIGHT – ROGELIO S. SIMSIMAN, MARIA LUISA F. DULAY, ERLINDA E. RAMOS, SHIRLEY S.BASADRE, NICOLAS R. TABORA, VIRGINIA D. BASCO, ROCHELLE C. LOPEZ, ELLENJOY O. BARUC AND RUSSELL CHARLES A. ANDRES

NICOLAS R. TABORA PRESIDENT/CEOVIRGINIA D. BASCO GENERAL MANAGER

SHIRLEY S. BASADRE BRANCH BANKING HEAD

ROGELIO S. SIMSIMAN LOAN SUPERVISOR

ROCHELLE C. LOPEZ ACCOUNTING DEPT. HEAD

MARIA LUISA F. DULAY CASH DEPARTMENT HEAD

ELLEN JOY O. BARUC INTERNAL AUDITOR

RUSSELL CHARLES A. ANDRES COMPLIANCE OFFICER

ERLINDA E. RAMOS HR OFFICER

2017 ANNUAL REPORT

Annual Report 2017 | Page 36 of 106

Branch Heads

LEFT TO RIGHT – RICHARD R. MURAO, EMMALYN G. BRAGA, SHIRLEY S. BASADRE, ROSANNA G.TAYAG AND ANGELITO B. GABRILLO

SHIRLEY S. BASADRE STO. TOMAS BRANCHANGELITO B. GABRILLO SAN FABIAN BRANCH

ROSANNA G. TAYAG SISON BRANCH

RICHARD R. MURAO POZORRUBIO BRANCH

EMMALYN G. BRAGA BINALONAN BRANCH

2017 ANNUAL REPORT

Annual Report 2017 | Page 37 of 106

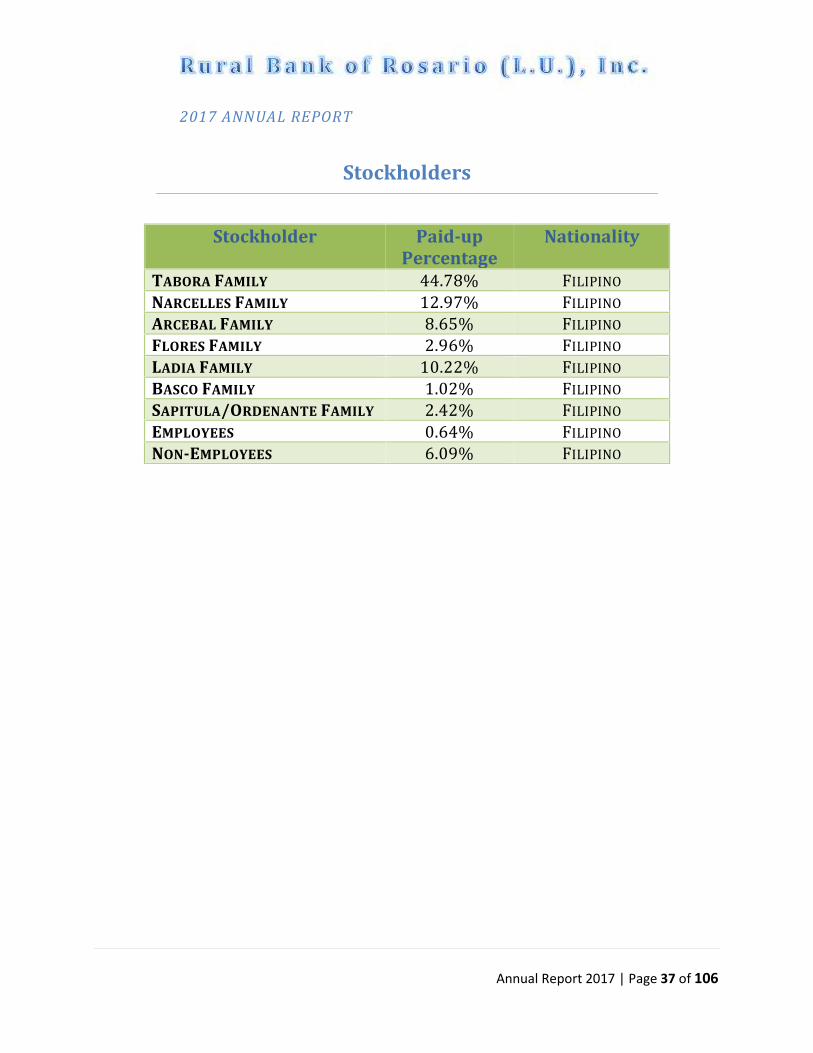

Stockholders

Stockholder Paid-upPercentage

Nationality

TABORA FAMILY 44.78% FILIPINONARCELLES FAMILY 12.97% FILIPINOARCEBAL FAMILY 8.65% FILIPINOFLORES FAMILY 2.96% FILIPINOLADIA FAMILY 10.22% FILIPINOBASCO FAMILY 1.02% FILIPINOSAPITULA/ORDENANTE FAMILY 2.42% FILIPINOEMPLOYEES 0.64% FILIPINONON-EMPLOYEES 6.09% FILIPINO

2017 ANNUAL REPORT

Annual Report 2017 | Page 38 of 106

Products and Services

The Rural Bank of Rosario (La Union), Inc. has a website wherein the list ofProducts and Services are posted including the foreclosed properties for sale.

The official website of the Bank is accessible at www.ruralbankofrosario.com .

Agricultural Loan Commercial Loan Industrial Loan Housing Loan Medium Term Loan Salary Loan (DepEd Employee) Motor Vehicle Financing SSS Pensioners Loan GSIS Pensioners Loan PVAO Pensioners Loan Tricycle Loan

Savings Deposit Time Deposit Demand Deposit (Current Account) Check Plus (Current Acct. with Interest) Special Savings (SSA) SSS Pensions/Payments Petnet Western Union Money Transfer-The fastest way

to send & receive money Gcash Money Transfer (Cash-in, Cash-out, GCASH

Remittance) ATM Services (Megalink, Bancnet, Expressnet,

Mastercard, Visa Card)

Micro insurance

2017 ANNUAL REPORT

Annual Report 2017 | Page 39 of 106

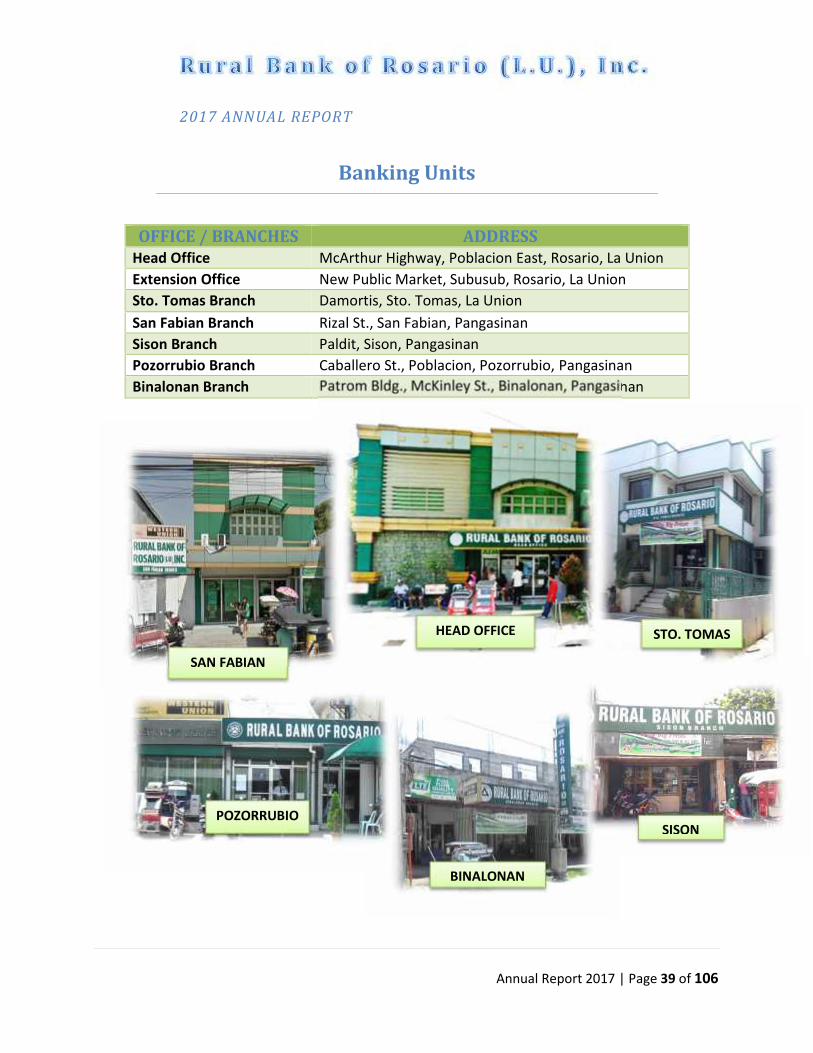

Banking Units

OFFICE / BRANCHES ADDRESSHead Office McArthur Highway, Poblacion East, Rosario, La UnionExtension Office New Public Market, Subusub, Rosario, La UnionSto. Tomas Branch Damortis, Sto. Tomas, La UnionSan Fabian Branch Rizal St., San Fabian, PangasinanSison Branch Paldit, Sison, PangasinanPozorrubio Branch Caballero St., Poblacion, Pozorrubio, PangasinanBinalonan Branch Patrom Bldg., McKinley St., Binalonan, Pangasinan

STO. TOMAS

SAN FABIAN

SISON

BINALONAN

HEAD OFFICE

POZORRUBIO

2017 ANNUAL REPORT

Annual Report 2017 | Page 40 of 106

AUDITEDFINANCIALSTATEMENTS

•

Management is responsible for the preparation and fair presentation of the financial statements in accordance with PFRSs and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

We conducted our audit in accordance with Philippine Standards on Auditing (PSAs)_ Our responsibilities under those standards are further described in the Auditor's Responsibilityfor the Audit of Financial Statements section of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the Philippines, the Code of Ethics for Professional Accountants in the Philippines, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believed that the audit evidence we have obtained is sufficientjand appropriate to provide a basis for our opinion

Basis for Opinion

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company as at December 31, 2017, and its financial performance and its cash flows for the year then ended in accordance with Philippine Financial Reporting Standards (PFRSs)

We have audited the financial statements of Rural Bank of Rosario (La Union), Inc., which comprise the Statement of Financial Position as\at December 31, 2017 and the Statement of Comprehensive Income, Statement of Changes in Equity and Statement of Cash Flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

Gentlemen:

The Stockholders and the Board of Directors Rural Bank of Rosario (La Union), Inc., Poblacion East, Rosario, La Union

Opinion

Independent }f_ucfitor's <J{eport

LAMBERTO D. AN Certified Public Accountant 79 4'11 Fortune Village 5, Vslenzuela City Tel. No.(02) 44{}-5315; Mobile No. (02) 510-4164; (0927) 6512686 Email : lamb [email protected] Tax & Management Consultant* Auditor* Accountant

1

Page 41 of 106

• • • • •

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exist related to events or conditions that may cast significant doubt on the Company's ability to continue as a going concern. If we conclude that material uncertainty exists, We are required to draw attention in auditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Company's to cease to continue as a going concern . •

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. • •

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control. •

•• • Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. •

• Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. As part of an audit in accordance with PSAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: •

• Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with PSAs will always detect a material misstatement when it exists . • Auditor's Responsibilities for the Audit of the Financial Statements • Those charged with governance are responsible for overseeing the Company's financial reporting process . • In preparing the financial statements, management is responsible for assessing the Company's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so .

• I -- • • 2

Page 42 of 106

--,...,,_~,

. .: APR!} i018 ~ ! r J., ;

' ''"·"- ! . '! \

.iild'&.~- (!;;' ,.- _· , r- . '._·· . 1'· I\.~ !;...~~".-ri-1101.. (,) C, ··v L 1 ,

~ J ,, .. ~,

!·, I' '

Valenzuela City March 08, 2018

Issued at Valenzuela City on Jan 4, 2018 TIN 13 5-941-825 BOA Cert. of Accreditation No. 3460

Until December 31, 2018 BSP Accreditation March 27, 2015 to March 27, 2018 BIR Accreditation No. 05-005020-1-2017

June 15, 2017 to June 15, 2020

Our audit was conducted for the purpose of forming an opinion on the basic financial statements taken as whole. The supplementary information on taxes and licenses in Note 25 to the financial statements is presented for purposes of filing with the Bureau of Internal Revenue and is not a required part of the basic financial statements. Such information is the responsibility of the management of Rural Bank of Rosario (La Union), Inc., The information has been subjected to the auditing procedures applied in my audit of the basic financial statements. In my opinion, the information is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

Report on the Supplementary Information Required Under Revenue Regulations 15-2010.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit

Page 43 of 106

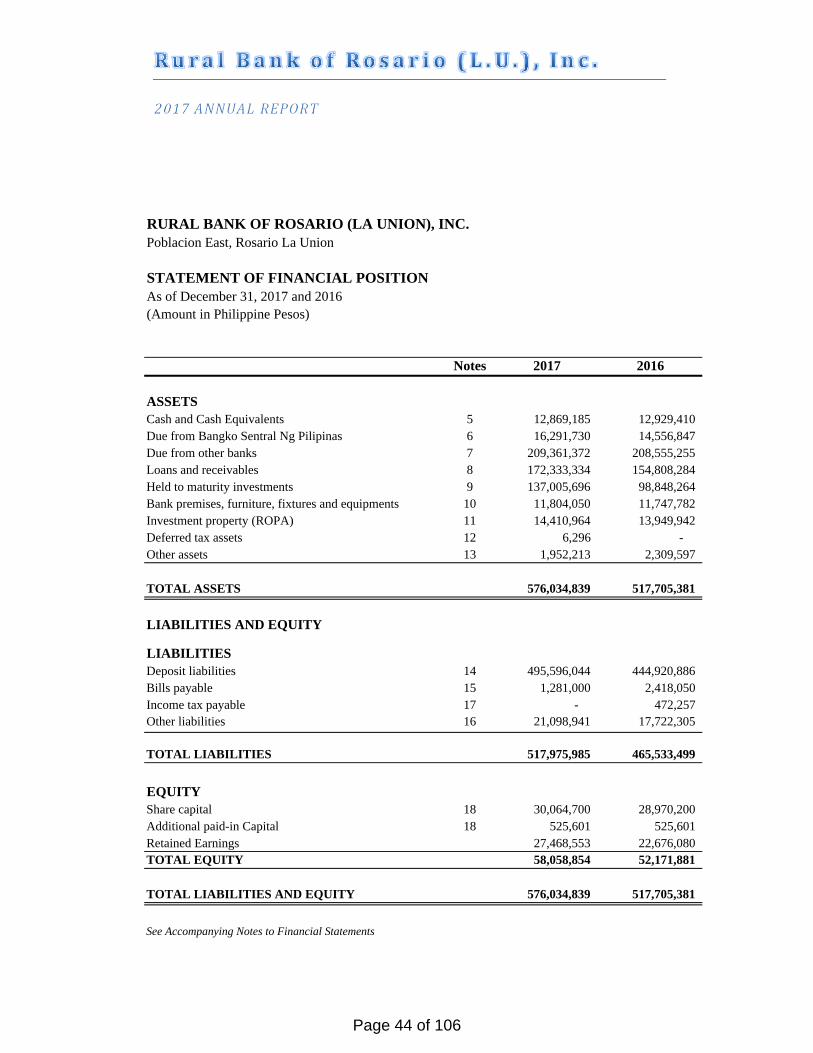

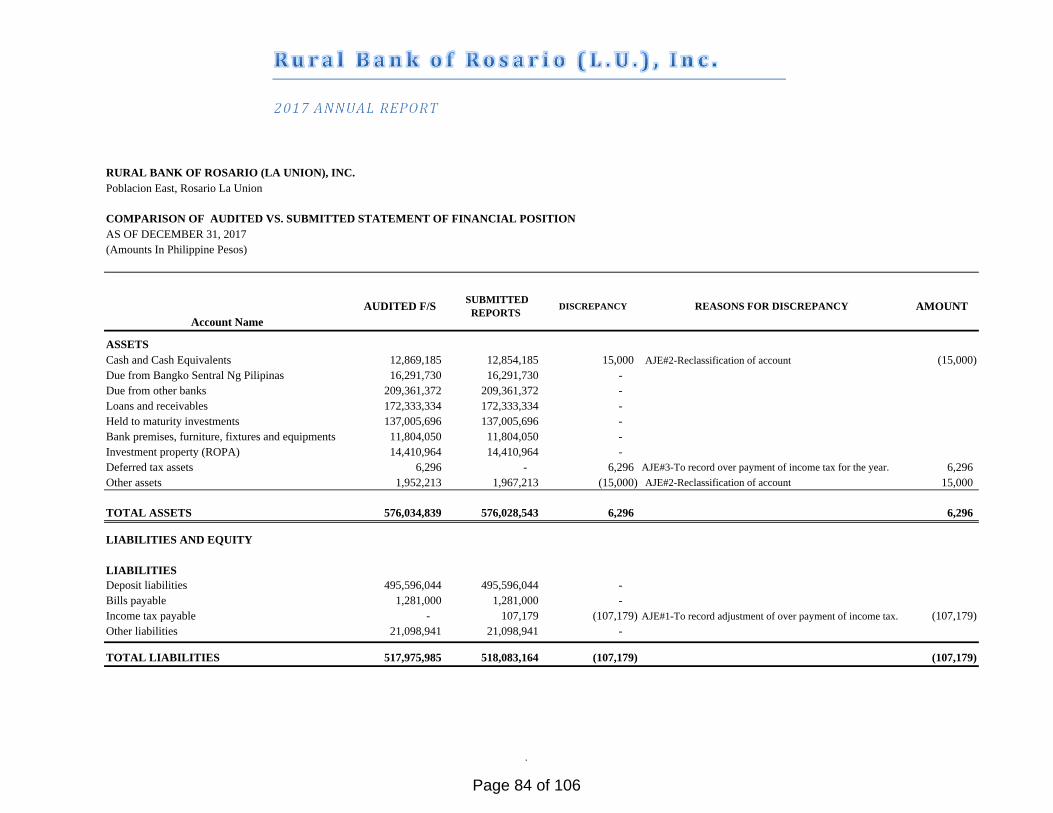

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

STATEMENT OF FINANCIAL POSITIONAs of December 31, 2017 and 2016(Amount in Philippine Pesos)

Notes 2017 2016

ASSETSCash and Cash Equivalents 5 12,869,185 12,929,410Due from Bangko Sentral Ng Pilipinas 6 16,291,730 14,556,847Due from other banks 7 209,361,372 208,555,255Loans and receivables 8 172,333,334 154,808,284Held to maturity investments 9 137,005,696 98,848,264Bank premises, furniture, fixtures and equipments 10 11,804,050 11,747,782Investment property (ROPA) 11 14,410,964 13,949,942Deferred tax assets 12 6,296 -Other assets 13 1,952,213 2,309,597

TOTAL ASSETS 576,034,839 517,705,381

LIABILITIES AND EQUITY

LIABILITIESDeposit liabilities 14 495,596,044 444,920,886Bills payable 15 1,281,000 2,418,050Income tax payable 17 - 472,257Other liabilities 16 21,098,941 17,722,305

TOTAL LIABILITIES 517,975,985 465,533,499

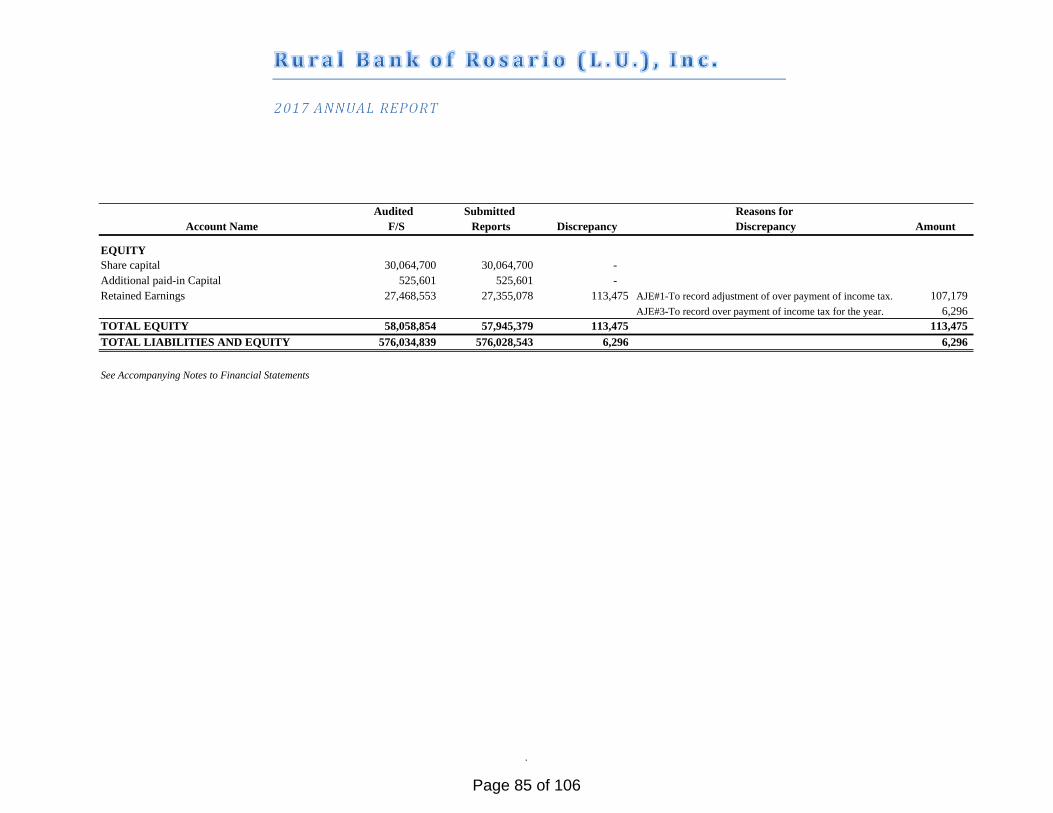

EQUITYShare capital 18 30,064,700 28,970,200Additional paid-in Capital 18 525,601 525,601Retained Earnings 27,468,553 22,676,080TOTAL EQUITY 58,058,854 52,171,881

TOTAL LIABILITIES AND EQUITY 576,034,839 517,705,381

See Accompanying Notes to Financial Statements

4

Page 44 of 106

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

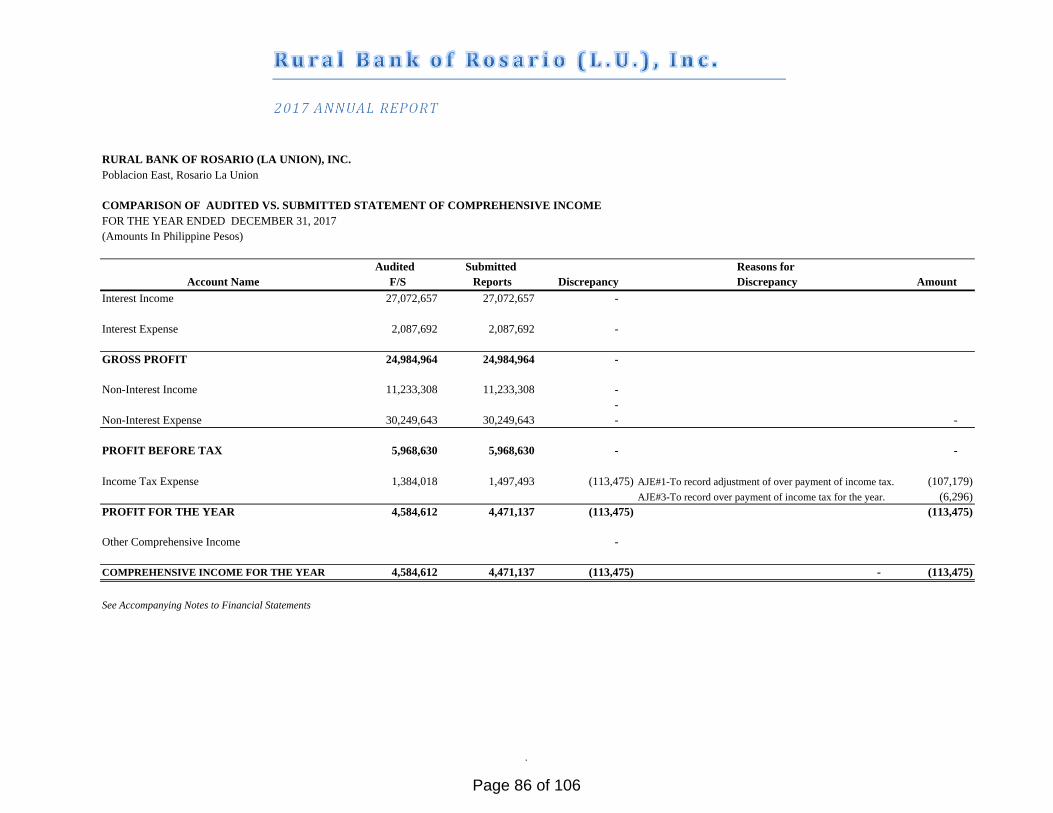

STATEMENT OF COMPREHENSIVE INCOME

For the years ended December 31, 2017 and 2016(Amount in Philippine Pesos)

Note 2017 2016

Interest Income 19 27,072,657 22,578,605

Interest Expense 20 2,087,692 2,225,492

GROSS PROFIT 24,984,964 20,353,113

Non-Interest Income 21 11,233,308 10,134,901

Non-Interest Expense 22 30,249,643 26,577,967

PROFIT BEFORE TAX 5,968,630 3,910,047

Income Tax Expense 24 1,384,018 963,004

PROFIT FOR THE YEAR 4,584,612 2,947,043

Other Comprehensive Income - -

COMPREHENSIVE INCOME FOR THE YEAR 4,584,612 2,947,043

EARNINGS PER SHARE 28 15.25 9.70

5

Page 45 of 106

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

STATEMENT OF CASH FLOWSFor the years ended December 31, 2017 and 2016(Amount in Philippine Pesos)

Notes 2017 2016

CASH FLOWS FROM OPERATING ACTIVITIES

PROFIT BEFORE TAX 5,968,630 3,910,047Adjustments to reconcile net income

to net cash provided by operating activities: Depreciation 22 1,437,639 1,630,754 Impairment Loss 22 1,902 26,717 Provision for credit losses on loans and receivables 22 1,717,181 1,771,120 Adjustments on surplus and undivided profits 27 207,860 (223,023) Changes in operating assets and liabilities: Decrease (Increase) in:

Due from Bangko Sentral Ng Pilipinas 6 (1,734,883) (2,332,363)Due from other banks 7 (806,117) (30,306,351)Loans and receivables 8 (19,242,231.28) (19,615,322)Investment property (ROPA) 11 (462,923.68) (6,544,283)Deferred tax assets 12 (6,296) -Other assets 13 357,384 (484,098)

Increase (Decrease) in:Deposit liabilities 14 50,675,158 75,606,159Other liabilities 16 3,376,635 5,918,781Cash generated from operations 41,489,939 29,358,138Tax paid 24 (1,856,275) (641,579)

39,633,663 28,716,559CASH FLOWS FROM INVESTING ACTIVITIES Increase (Decrease) in:

Bank premises, furniture, fixtures and equipments 10 (1,493,907) (1,814,308)Held to maturity investments 9 (38,157,432) (29,576,876)NET CASH FROM INVESTING ACTIVITIES (39,651,339) (31,391,184)

CASH FLOWS FROM FINANCING ACTIVITIESBills payable 15 (1,137,050) 232,292Declaration of Stock dividends 18 - (1,991,656)Capital share 18 1,094,500 2,461,000NET CASH FROM FINANCING ACTIVITIES (42,550) 701,636

NET INCREASE(DECREASE) IN CASH AND CASH EQUIVALENTS (60,226) (1,972,989)

CASH BALANCE AT BEGINNING OF YEAR 5 12,929,410 14,902,399

CASH BALANCE AT END OF YEAR 5 12,869,185 12,929,410See Accompanying Notes to Financial Statements

NET CASH FROM OPERATING ACTIVITIES

6

Page 46 of 106

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

STATEMENT OF CHANGES IN EQUITYFor the years ended December 31, 2017 and 2016(Amount in Philippine Pesos)

Preferred Common Free Reserve

Balance at 31 December 2015 26,509,200 525,601 21,900,917 42,800 48,978,518

Profit after tax for the year ended December 31, 2016 2,947,043 2,947,043Additional Capital Stock Common/Declaration of stock dividends 2,461,000 (1,991,656) 469,344Summary of Adjustment and charges (Note 27) (223,023) - (223,023)Balance at 31 December 2016 28,970,200 525,601 22,633,280 42,800 52,171,882

Profit after tax for the year ended December 31, 2017 4,584,612 4,584,612Additional Capital Stock Common 1,094,500 1,094,500Summary of Adjustment and charges (Note 27) 207,860 207,860Balance at 31 December 2017 30,064,700 525,601 27,425,753 42,800 58,058,854

See Accompanying Notes to Financial Statements

Share Capital Retained EarningsTotal

Paid-in-Capital

7

Page 47 of 106

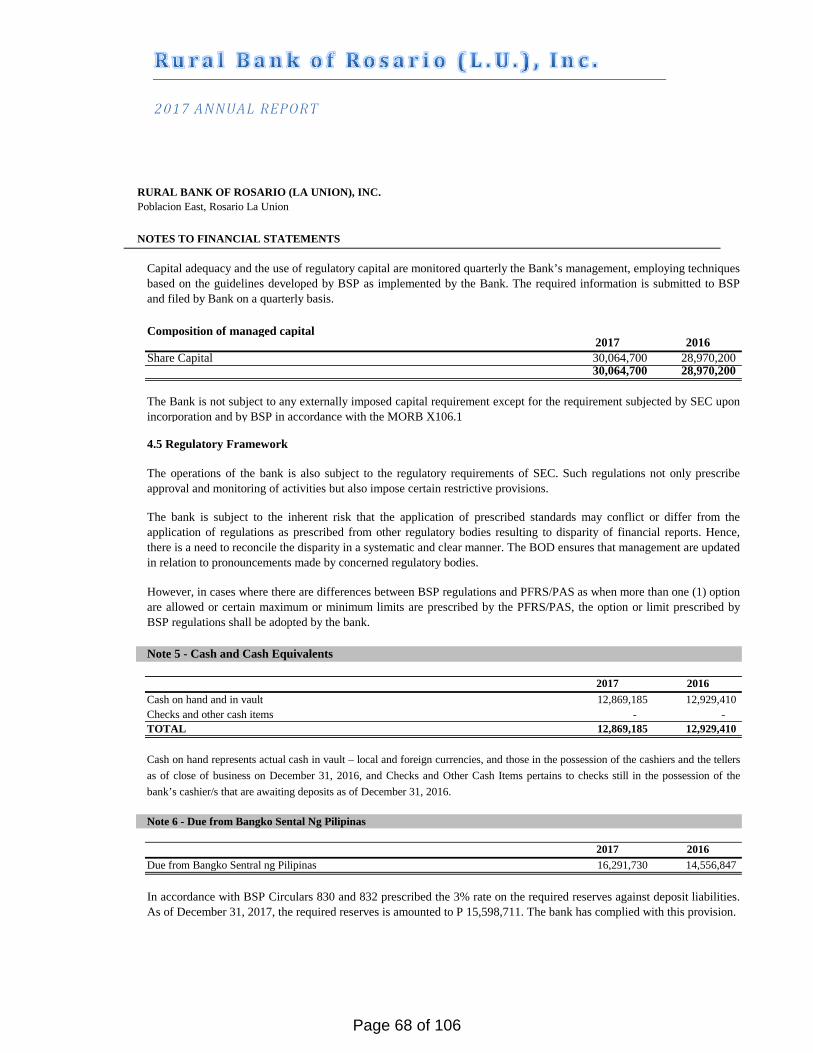

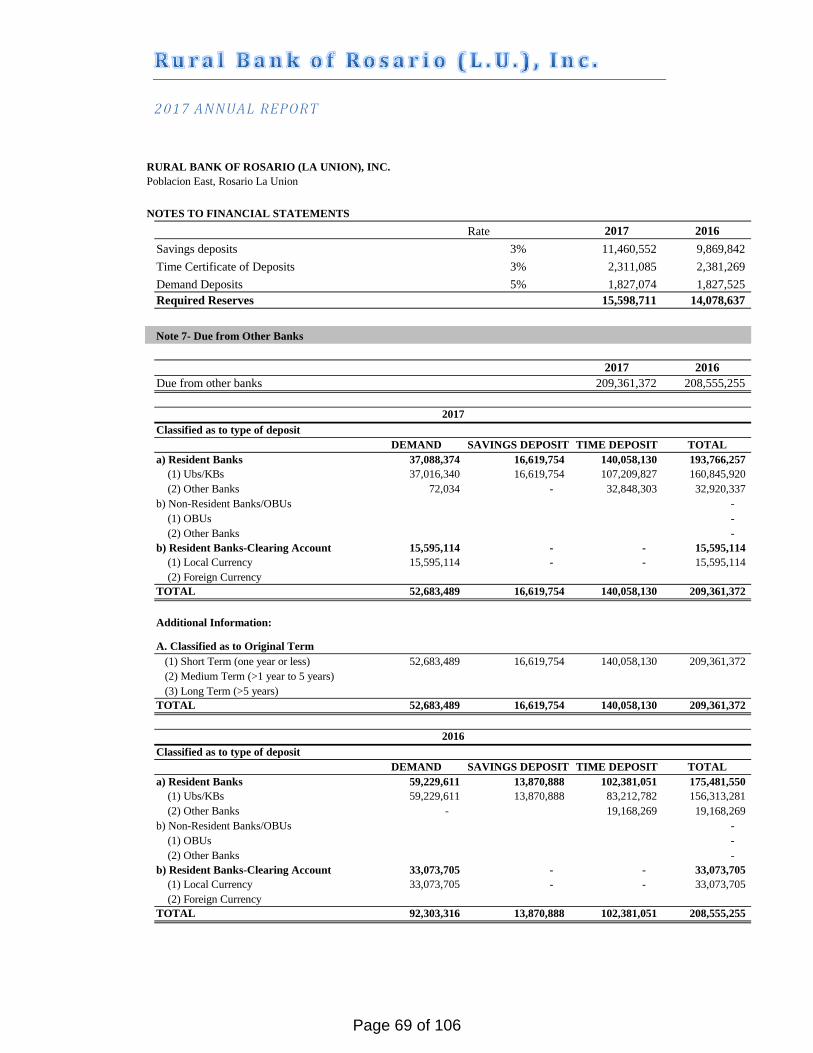

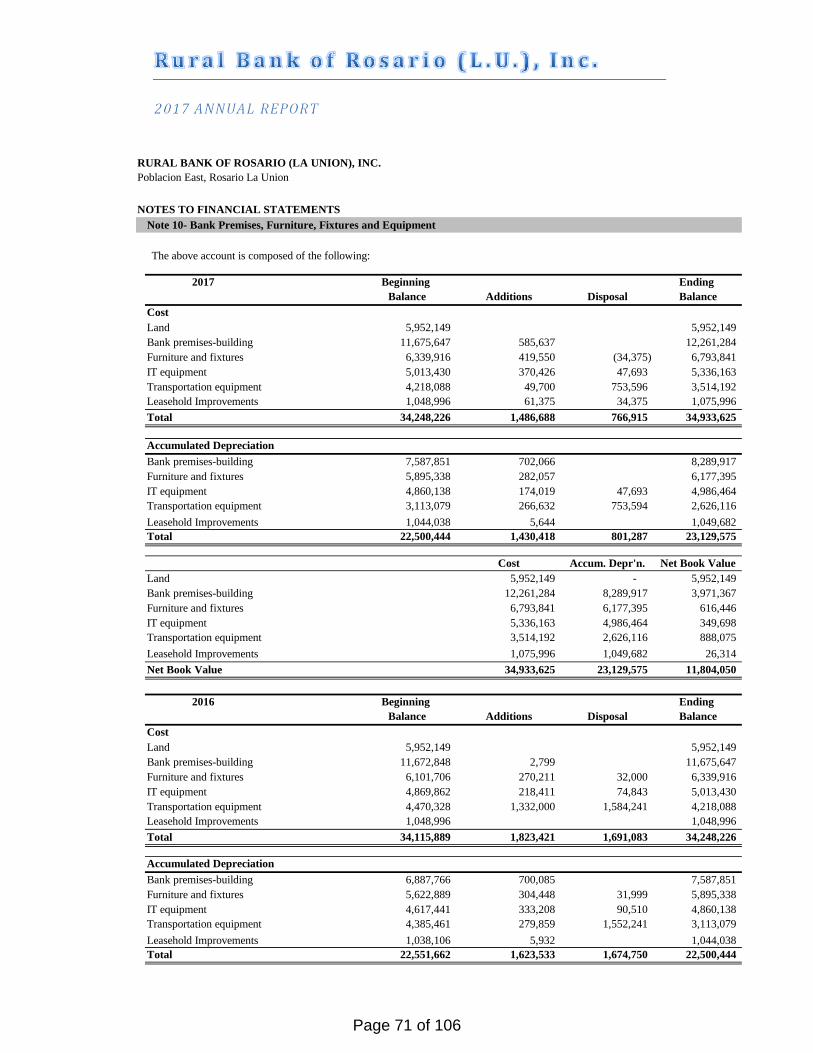

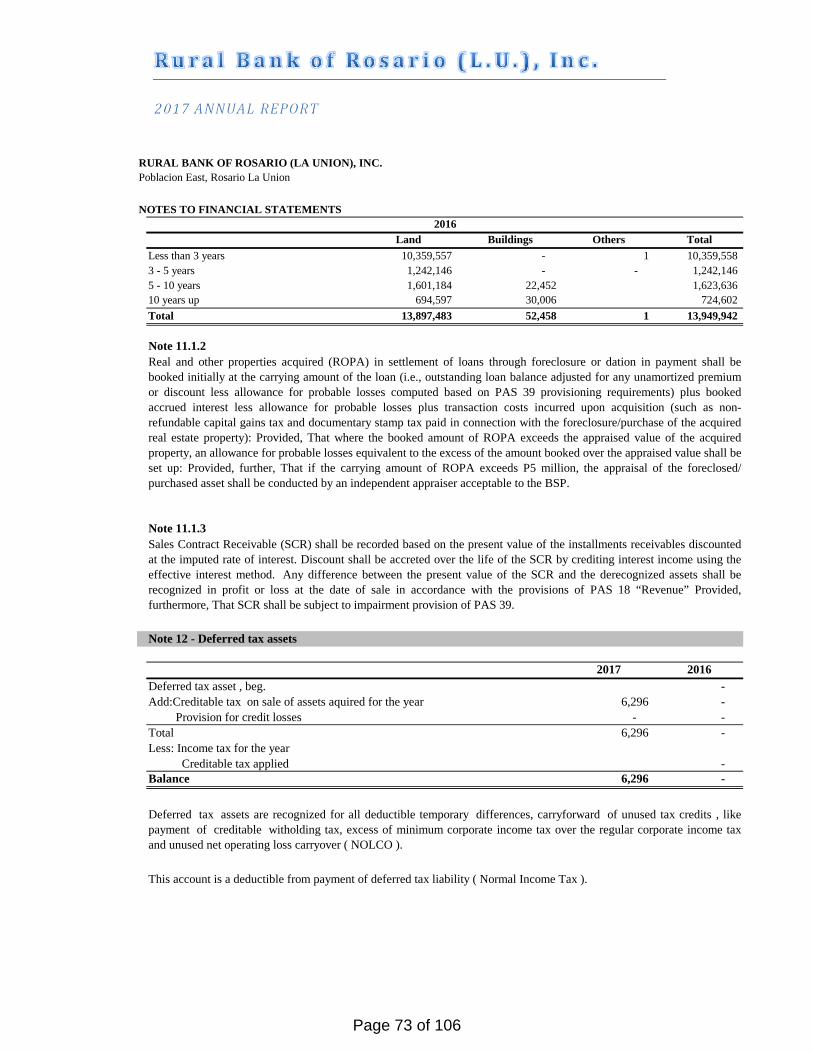

NOTES TO FINANCIAL STATEMENTS

For the years ended December 31, 2017 and 2016(Amount in Philippine Pesos)

Note 1 - Company Information

1.1 Incorporation and Operations

1.2 Approval for Issuance of Audited Financial Statements

Note 2 - Significant Accounting Policies

2.1 Basis of Preparation of Financial Statements

a) Statements of Compliance with Philippine Financial Reporting Standards

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

The Rural Bank of Rosario (L.U.), Inc. was registered with the Securities and Exchange Commission (SEC) underregistration number 3761 and was incorporated on February 21, 1969. The bank is organized under Republic Act (R.A.)No. 7353, otherwise known as the Rural Banks Act of 1992. The bank obtained its rural bank license from the BangkoSentral ng Pilipinas (BSP) on March 13, 1969 and started its operation on March 22, 1969. The bank is engaged in ruralbanking services primarily to carry business of extendng rural credit to small farmers and tenants to deserving ruralindustries or enterprises; and to have and exercise all authority and powers to perform all acts and transacts all businesswhich may legally be had and done by rural bank organized under and in accordance with the Rural Bank's Act. The banktransacts all business which may legally exist or be amended and to have all other things thereto necessary and proper inconnection with said purposes within such authority as may be determined by the Monetary Board of Bangko Sentral ngPilipinas.

The bank's principal place of business is located at Poblacion East, Rosario, La Union. It has five (5) branches which arelocated at Sison, Binalonan, San Fabian, Pozorrubio Pangasinan and Sto. Tomas, La Union . The bank also have four (4)on site automated tellering machines located in the main office in Rosario, La Union, Pozorrubio Branch, Sto. TomasBranch and Binalonan Branch.

The Board of Directors (BOD) of RURAL BANK OF ROSARIO (L.U.), INC. has reviewed, approved and authorizedthe issuance of the accompanying financial statements for the year ended December 31, 2017 (including thecomparative figures for the year ended December 31, 2016) on March 08, 2018.

A summary of more significant policies and practices of the bank are set forth below to facilitate the understanding ofdata presented in the financial statements.

The financial statements of the bank have been prepared using the accrual basis of accounting and in accordance withthe Philippine Financial Reporting Standards (PFRS). The term PFRS includes applicable PFRS, Philippine AccountingStandards (PAS) and interpretations which were approved by the Financial Reporting Standards Council (FRSC) from thepronouncements issued by the International Accounting Standards Boards also, the bank adopted the new FinancialReporting Package (FRP) prescribed by the Bangko Sentral Ng Pilipinas as per BSP Circular 512 dated February 03,2006. and adopted by SEC.

The RURAL BANK OF ROSARIO (LA UNON), Inc. Board of Directors is composed of Seven (7) members; one (1) of them is anIndependent Director.

8

Page 48 of 106

NOTES TO FINANCIAL STATEMENTS

RURAL BANK OF ROSARIO (LA UNION), INC.Poblacion East, Rosario La Union

c) Currency of Presentation

2.2 Adoption of Accounting and Reporting Standards

The bank qualifies as a non-publicly entity under the Philippine Accounting Standard 101 (PAS 101) - FinancialReporting Standards for Non-publicly Accountable Entities (NPAE). PAS 101 provides temporary relief to qualifiedsmall and medium entities iin the application of new Philippine Accounting Standards (PAS) and Philippine FinancialReporting Standards (PFRS) that became effective in 2005. Under this standard, a qualifying entity is allowed not toapply in its general purpose financial statements in t new PAS and PFRS but may still choose to apply any or all of thenew PFRS that become effective in 2007. PAS 101 shall be effective until 2010.

b) Presentation of Financial Statements