2016 outlook for u.s. construction

TRANSCRIPT

1

Dodge Data and Analytics

By: Richard Branch

Senior Economist

Dodge Data & Analytics

August 6, 2015

2016 Outlook

for U.S.

Construction

2

Today’s Agenda

Brief Macroeconomic overview

Nonresidential outlook

Multifamily outlook

Big picture review

Implications for VMA members

Questions

3

Economic growth is expected to pick up in 2015 after a disappointing start.

Key Economic

Forecasts

GDP

2014: 2.4%

2015: 2.3%

2016: 3.2%

Unemployment Rate

2014: 6.2%

2015: 5.3%

2016: 4.9%

CPI

2014: 1.6%

2015: 0.4%

2016: 2.6%

Fed Funds Rate

2014: 0.09%

2015: 0.2%

2016: 1.7%

U.S. Macroeconomic Picture

4

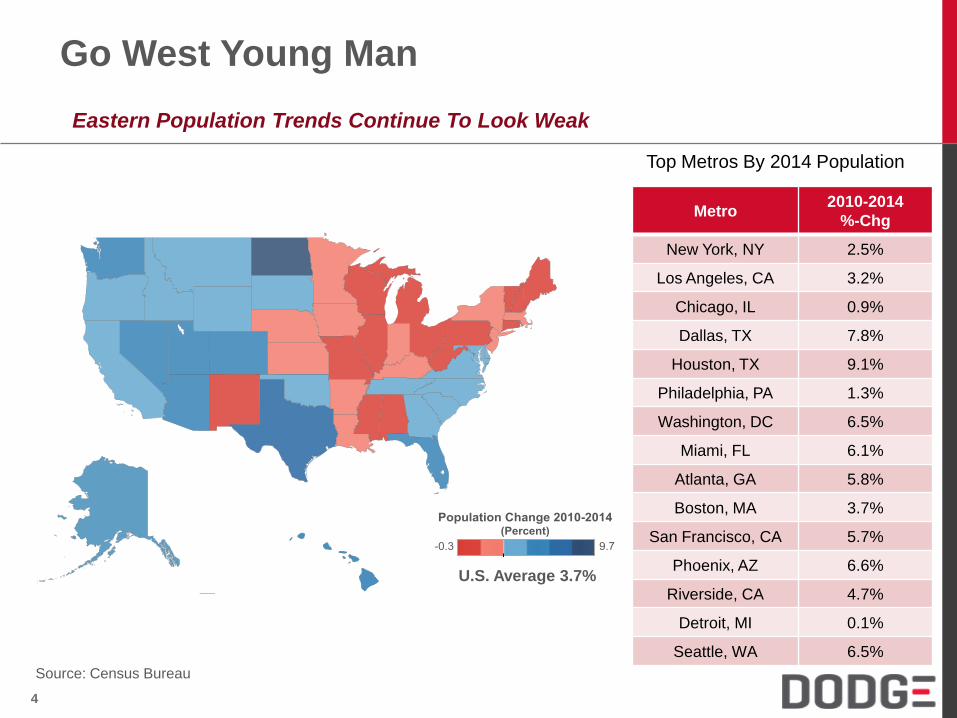

Eastern Population Trends Continue To Look Weak

Go West Young Man

Metro 2010-2014

%-Chg

New York, NY 2.5%

Los Angeles, CA 3.2%

Chicago, IL 0.9%

Dallas, TX 7.8%

Houston, TX 9.1%

Philadelphia, PA 1.3%

Washington, DC 6.5%

Miami, FL 6.1%

Atlanta, GA 5.8%

Boston, MA 3.7%

San Francisco, CA 5.7%

Phoenix, AZ 6.6%

Riverside, CA 4.7%

Detroit, MI 0.1%

Seattle, WA 6.5%

Top Metros By 2014 Population

Source: Census Bureau

U.S. Average 3.7%

5

2014 Size of Market - $591 billion

Relative Size of U.S. Construction Starts Market

.

6

Nonresidential Construction Market Cycles

Recovery in Place, But a Long Road Back

.

*Data is through 2015Q2

7

Commercial

Construction

Outlook

Dodge Data and Analytics

8

Commercial construction has made great progress.

Moderate pace of recovery to continue.

Commercial Construction Starts

Includes stores, offices, warehouses, hotels and auto sector

9

Retail Building Starts

Store construction making very slow progress.

Online sales gaining market share. Extreme discounters expanding.

Store renovations higher share of activity.

10

Retail Building Starts High vacancy rates and urban focus keeps the size of new projects historically low.

11

Retail Building Starts Discounters, dollar stores, supermarkets, and home stores are building the most.

Dodge Data & AnalyticsRetail Chain Construction Starts

First Four Months of 2015

Thous SqFt Thous $

1 Wal-Mart Store 3,521 570,322

2 Kroger Grocery Store 1,181 115,722

3 Wegmans Grocery Store 694 64,000

4 Dollar General 669 62,544

5 Publix Grocery Store 660 54,697

6 CVS Pharmacy 443 54,105

7 IKEA Furniture Store 351 46,041

8 HEB Grocery Store 453 43,700

9 Costco 598 40,716

10 Family Dollar 444 38,967

11 AutoZone Auto Parts Store 438 38,540

12 Nordstrom Store 0 33,150

13 Lowe's Home Center 395 30,060

14 Aldi Grocery Store 296 29,238

15 Dollar Tree 110 29,155

16 Tractor Supply Store 538 28,638

17 Whole Foods 84 28,313

18 Harbor Freight Tools 18 20,657

19 Menards Home Improvement 229 20,000

20 King Soopers 127 19,726

21 Goodwill Store 184 17,853

22 Rite Aid 90 17,589

23 Starbucks 25 17,357

24 Taco Bell Restaurant 41 16,381

25 Texas Roadhouse Restaurant 105 15,500

26 Wendy's Restaurant 38 13,618

27 Chick Fil A Restaurant 31 13,134

28 Food Lion Store 43 13,100

29 McDonalds Restaurant 60 12,606

30 The Fresh Market 74 12,574

# Chains Thous SqFt Thous $

Value Chains 3 4,303 628,891

Grocery Stores 9 3,612 381,070

Home store 5 1,531 145,396

Dollar Stores 3 1,223 130,666

Restaurants 6 299 88,596

Pharmacies 2 534 71,694

Other 2 438 71,690

12

Commercial Warehouse Starts

Warehouse construction continues to see healthy growth.

Regional distribution centers.

Effect of Panama Canal?

Strong dollar/weak global economies?

13

Commercial Warehouse Starts

Warehouse construction continues to see healthy growth.

2015 Q2 = 9.8%

2007 Cyclical Low = 9.8%

Source: CB Richard Ellis Econometric Advisors

14

Year-to-date 2015 Largest Warehouse Projects

Commercial Warehouse Starts

15

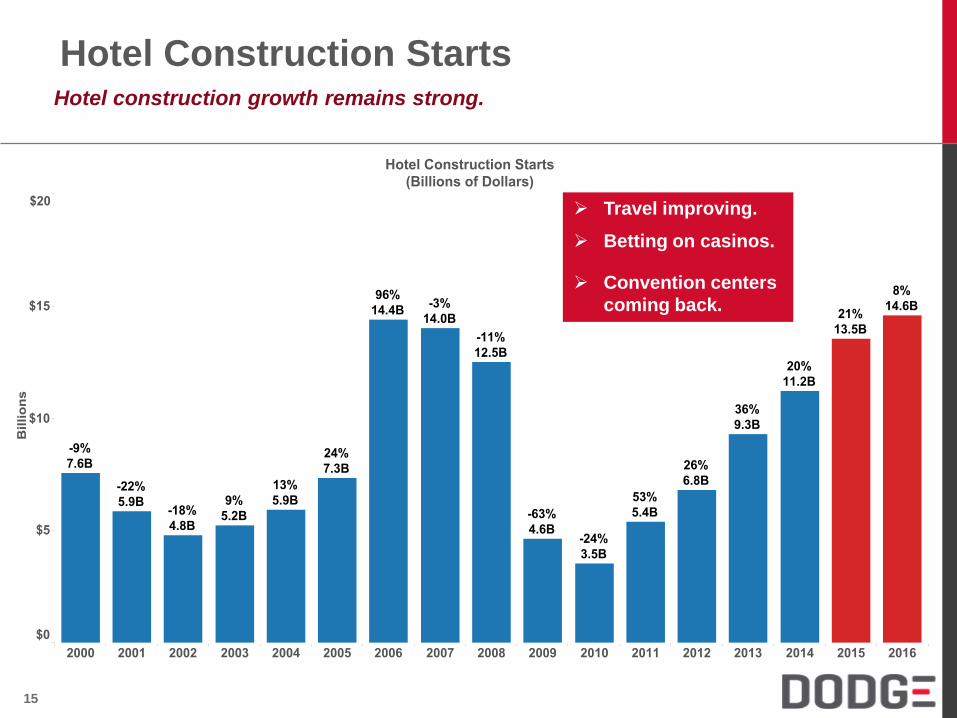

Hotel Construction Starts Hotel construction growth remains strong.

Travel improving.

Betting on casinos.

Convention centers

coming back.

16

Year-to-date 2015 Largest Hotel Projects

Hotel Construction Starts

17

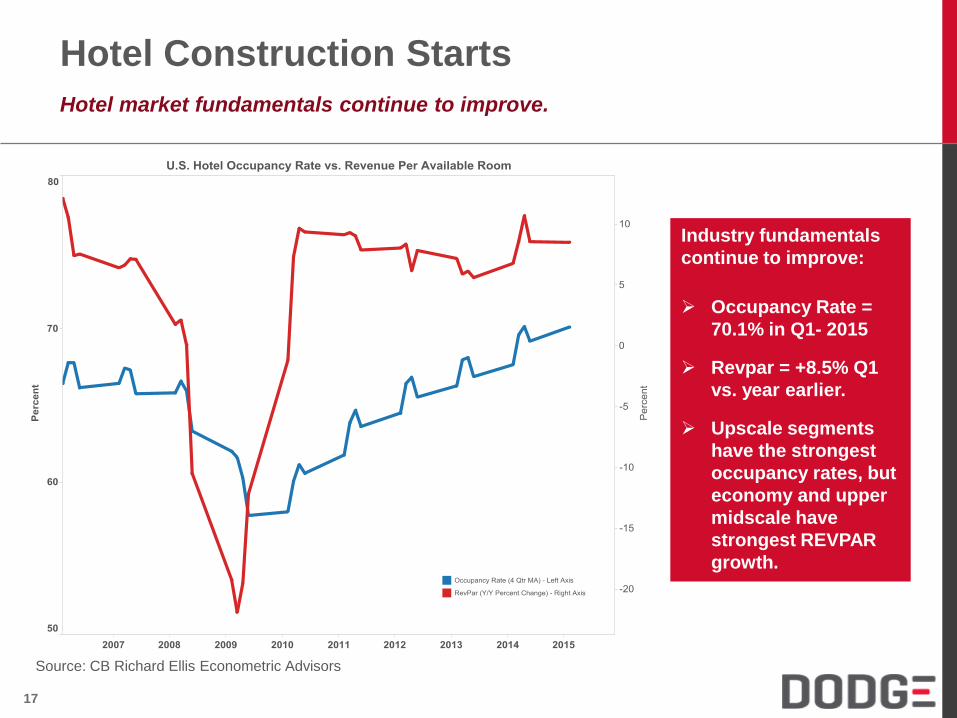

Hotel Construction Starts

Hotel market fundamentals continue to improve.

Industry fundamentals

continue to improve:

Occupancy Rate =

70.1% in Q1- 2015

Revpar = +8.5% Q1

vs. year earlier.

Upscale segments

have the strongest

occupancy rates, but

economy and upper

midscale have

strongest REVPAR

growth.

Source: CB Richard Ellis Econometric Advisors

18

Office Building Starts

Construction expansion was late, but has now begun to take hold.

Gov’t offices,

data centers, HQs

Speculative

development?

Rising office

employment.

19

Year-to-date 2015 Largest Office Projects

Office Construction Starts

20

Office vacancy rates continue to fall.

Overbuilding was less than in past cycles.

Rising employment

helping absorption.

Office market fundamentals (employment, vacancy rates) are improving.

Office Building Starts

2015 Q2 = 13.5%

2007 Cyclical Low = 12.4%

Source: CB Richard Ellis Econometric Advisors

21

Institutional

Construction

Outlook

Dodge Data and Analytics

22

Institutional buildings are beginning to turn the corner.

Stirrings of improving public

finances are enhancing outlook.

Institutional Building Starts

Includes education, dorms, healthcare, recreation, public , religious, and transportation

23

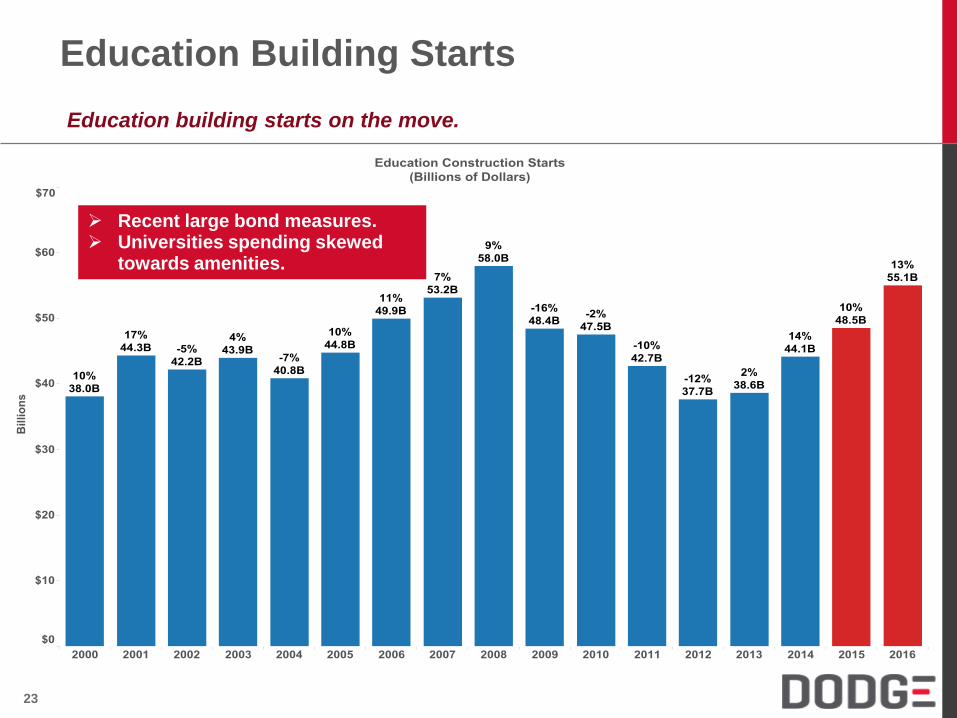

Education building starts on the move.

Recent large bond measures. Universities spending skewed

towards amenities.

Education Building Starts

24

School construction (K-12) is larger, but more volatile than college/univ. starts.

In 2014, sq. ft.

for K-12 school

construction

was 3.5 times

the size of the

post-secondary

market.

Back in the

1990s, it was

more than 7

times the size of

college starts.

Education Building Starts

25

Enrollment growth ultimately drives activity for many segments.

Education Building Starts

Elementary/ junior high school enrollments will grow faster than high school enrollments over the next five years.

College enrollments surged during the recession, but will grow more slowly as job opportunities improve.

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

36,000

37,000

38,000

39,000

40,000

41,000

42,000

Projections of School Enrollments by Grade (Thousands)

K-8 (left)

9-12 (right)

Source: NCES

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

College Enrollment (Thousands)

Source: NCES

Public School Enrollment K-12 by Regionin Thousands

2012 2022 Chg % Chg

US 49,636 52,952 3,316 6.7%

Northeast 7,904 7,972 68 0.9%

Midwest 10,556 10,724 168 1.6%

South 19,090 20,742 1,652 8.7%

West 12,086 13,513 1,427 11.8%

Source: NCES

26

Public school enrollment growth is strongest in the population magnets of the South and West.

Education Construction Starts

Public School Enrollment K-12 by StateLargest Gainers, Biggest Losers

2012 2022 Abs Chg % Chg 2012 2022 Abs Chg % Chg

TX 5,078 5,783 705 13.9% DC 73 69 -4 -5.5%

CA 6,287 6,884 597 9.5% MA 949 943 -6 -0.6%

FL 2,694 3,038 344 12.8% IN 1,037 1,026 -11 -1.1%

AZ 1,090 1,314 224 20.6% LA 706 694 -12 -1.7%

NC 1,515 1,678 163 10.8% NJ 1,347 1,330 -17 -1.3%

WA 1,049 1,193 144 13.7% AL 740 719 -21 -2.8%

GA 1,695 1,821 126 7.4% MS 488 464 -24 -4.9%

VA 1,262 1,384 122 9.7% WV 281 256 -25 -8.9%

MD 858 979 121 14.1% MI 1,558 1,521 -37 -2.4%

MN 846 960 114 13.5% OH 1,728 1,686 -42 -2.4%

Public School Enrollment K-12 by StateLargest Gainers, Biggest Losers

2012 2022 Abs Chg % Chg 2012 2022 Abs Chg % Chg

TX 5,078 5,783 705 13.9% DC 73 69 -4 -5.5%

CA 6,287 6,884 597 9.5% MA 949 943 -6 -0.6%

FL 2,694 3,038 344 12.8% IN 1,037 1,026 -11 -1.1%

AZ 1,090 1,314 224 20.6% LA 706 694 -12 -1.7%

NC 1,515 1,678 163 10.8% NJ 1,347 1,330 -17 -1.3%

WA 1,049 1,193 144 13.7% AL 740 719 -21 -2.8%

GA 1,695 1,821 126 7.4% MS 488 464 -24 -4.9%

VA 1,262 1,384 122 9.7% WV 281 256 -25 -8.9%

MD 858 979 121 14.1% MI 1,558 1,521 -37 -2.4%

MN 846 960 114 13.5% OH 1,728 1,686 -42 -2.4%

Biggest Losers Largest Gainers

Source: National Center for Education Statistics

27

Year-to-date 2015 Largest Education Projects

Education Construction Starts

28

Dorm starts have recovered to pre-recession levels

Colleges & universities in arms race. Endowment growth strong. Military construction budget stable.

Dormitory Building Starts

29

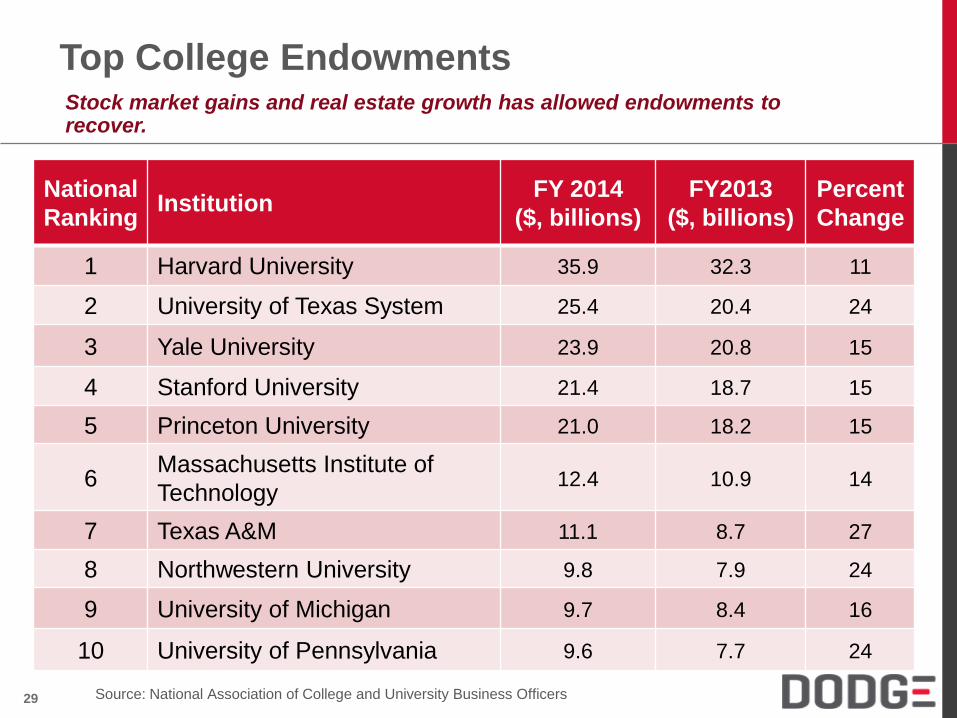

Stock market gains and real estate growth has allowed endowments to recover.

Top College Endowments

National

Ranking Institution

FY 2014

($, billions)

FY2013

($, billions)

Percent

Change

1 Harvard University 35.9 32.3 11

2 University of Texas System 25.4 20.4 24

3 Yale University 23.9 20.8 15

4 Stanford University 21.4 18.7 15

5 Princeton University 21.0 18.2 15

6 Massachusetts Institute of

Technology 12.4 10.9 14

7 Texas A&M 11.1 8.7 27

8 Northwestern University 9.8 7.9 24

9 University of Michigan 9.7 8.4 16

10 University of Pennsylvania 9.6 7.7 24

Source: National Association of College and University Business Officers

30

Year-to-date 2015 Largest Dorm Projects

Dormitory Construction Starts

31

Recovery in healthcare facilities kept on hold.

Uncertainty affecting activity.

Long-term support from

demographics and new

technology.

Healthcare Construction Starts

32

Top states for total and age 65+ population growth from 2013-2030 (based on 2000 Census)

Healthcare Construction Starts

State

Change in

Total

Population

(Thousands)

Percent Change

United States 46,050 15%

Arizona 3,246 49%

Nevada 1,120 40%

Florida 7,673 39%

North Carolina 3,255 33%

Texas 8,285 31%

Utah 803 28%

Georgia 2,602 26%

Colorado 1,271 24%

South Carolina 1,092 23%

Idaho 304 19%

South Dakota 154 18%

Washington 1,224 18%

State

Change in Total

Population > 65

(Thousands)

Percent Change

United States 29,442 66%

Arizona 1,258 123%

Wyoming 84 107%

Florida 3,851 106%

New Mexico 315 103%

Nevada 381 100%

North Dakota 97 95%

Virgin Islands 17 90%

Texas 2,575 87%

South Carolina 617 85%

Montana 139 85%

Alaska 56 84%

South Dakota 106 84%

Source: Economy.com

33

Year-to-date 2015 Largest Healthcare Projects

Healthcare Construction Starts

34

U.S.

Housing

Outlook

Dodge Data and Analytics

35

Multifamily housing turned the corner earlier thanks to rental market demand.

Rental demand on rise

Demographics key

Market improvement to continue

Multifamily Housing Starts

36

Top 20 year-to-date metros in 2015 based on dollar value of starts through June.

Multifamily Housing Starts

37

Dodge Data & Analytics

Total Construction Outlook

38

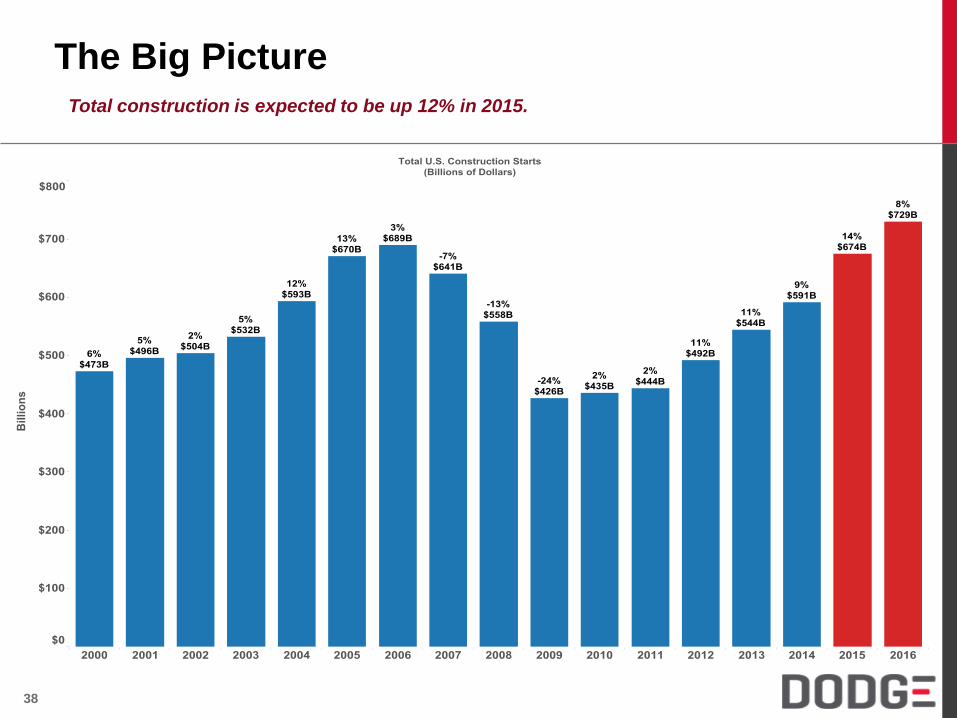

The Big Picture Total construction is expected to be up 12% in 2015.

39

The Big Picture Total construction is expected to be up 12% as the recovery becomes more complete.

40

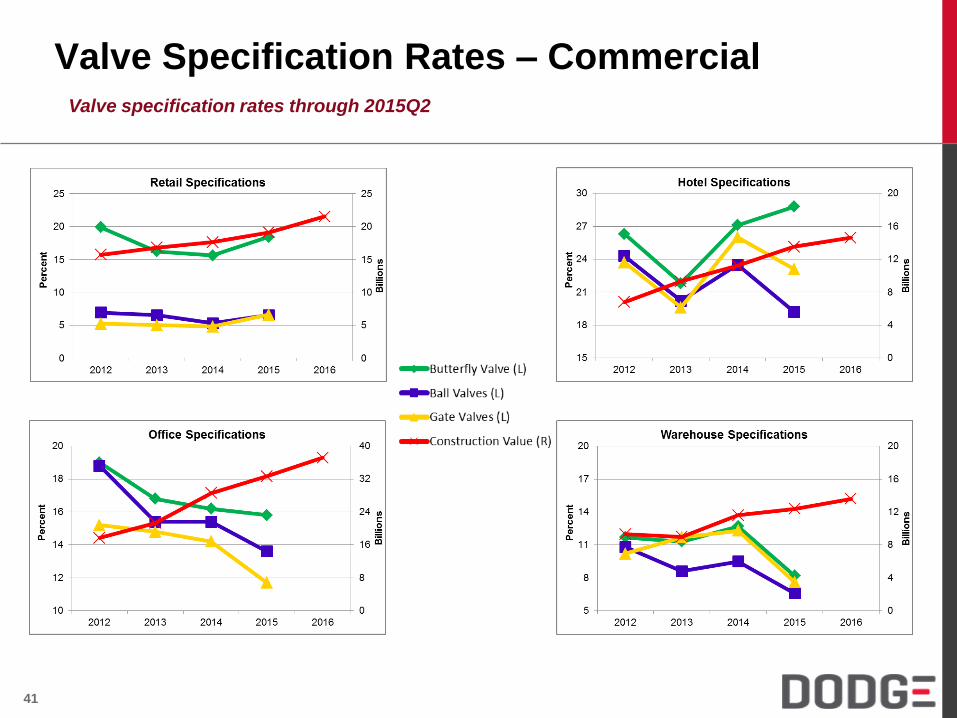

Implications for Valve Shipments Rising nonresidential construction starts a good sign for valve shipments

Source: Dodge Data & Analytics, Valve Manufacturers Association

41

Valve Specification Rates – Commercial Valve specification rates through 2015Q2

42

Valve Specification Rates – Institutional Valve specification rates through 2015Q2

43

Thank You!

Dodge Data and Analytics