2016 global payments insight survey: retail banking · pdf file3 summary retail banks are...

TRANSCRIPT

1

2016 Global Payments Insight Survey: Retail Banking

Banking on the Future

2

Catalyst

Payment players need to rethink roles and relationships

The payments industry has always been an

ecosystem in which participants have

particular roles and relationships with others.

It is now changing rapidly as existing

participants continue to invest in technology

and adjust to new roles while new entrants,

particularly from the fintech world, continue

to create new business models and threaten

to displace incumbents.

Payment technologies and platforms bind

these participants together in a tight

ecosystem. Merchants and billing

organizations interact with corporate and

transaction banks in a different part of the

value chain than they do with their own

customers and with retail banks. However,

each have different and changing priorities as

well as common needs and goals.

How those touchpoints are changing, how

they affect the relationships between

different participants, what opportunities that

presents and what that means for their future

strategies is the subject of this series of

reports.

While much of the media attention is driven

by the fintech hype machine and filtered

through a consumer lens, there are

considerable shifts happening at the

regulatory, infrastructural and technology

level that will have a profound effect on the

way the payments industry operates. Market

participants will have to create business and

technical strategies to address the changes

and make decisions about their role in the

value chain.

In 2015, technology analyst house Ovum, in

conjunction with ACI Worldwide, conducted

the first annual Ovum Global Payments Insight

Survey. This global survey of merchants, retail

banks and corporate banks, and billing

organizations examines strategic plans and IT

investment trends, asking respondents about

their experiences, perceptions and

expectations of payments and how this is

shaping their behavior.

This retail banking focused report highlights

some of the key findings from the second year

of this research and provides an explanation

of how the views and perspectives of the

different players in the ecosystem contrast. It

is one part of a five-part series based on

Ovum’s 2016 survey. Those interested in the

reports focusing on merchants, billing

organizations and transaction banking should

visit www.aciworldwide.com/paymentsinsight

for further information.

Merchants & Billing

Organizations

Retail Banks

PAYMENTS

Corporate & Transaction

banks

3

Summary Retail banks are investing to protect their future

The retail payments industry is an increasingly

competitive space, and banks face mounting

pressure. The need to deliver on growing

expectations for enhanced payment

experiences while, in many cases, also

managing legacy IT and operating under tight

budget constraints is a significant challenge.

At the same time, pressure from new entrants

and other third parties is growing and

presents a real risk to the traditional position

of retail banks at the heart of the purchasing

journey.

This report examines these issues, drawing on

the results of Ovum’s Payment Insights Survey

for 2016. Key findings include:

53% of banks globally are growing their investments in payments IT in 2016.

78% of banks believe customers want a broader choice of payment tools.

66% of banks are investing to deliver new payment and value added services. Cost efficiencies are a priority for 60%.

Investments to core infrastructure remain a

key focus for the industry, largely to enable

and support new payment services while also

reducing ‘run the bank’ costs.

70% of banks have recently or are currently delivering replacement or upgraded card management systems.

The same proportion have made recent investments in fraud screening and detection capabilities.

52% plan to invest in their payment switch technology in the near future.

At the same time, there is a heavy focus on

the potential for immediate payments (IP)

infrastructure to provide a platform for new

value added customer propositions. While the

level of infrastructure development differs

across the industry, there is broad agreement

on the benefits this will provide.

61% of all banks believe immediate payments will bring benefits to consumers, rising to 71% in Asia.

The ability to deliver stronger personal financial management (PFM) offerings is seen as a key enhancement for over 80% of banks.

However, only 52% of banks believe it will generate revenue growth.

The overwhelming need for many banks to

deliver product and service innovation is

frequently at odds with the available budgets

and internal resources available. This, coupled

with the competitive threat from third party

entrants is leading to a growing acceptance of

the need to form partnerships in order to

meet customer expectations. While some of

this will be regulatory-driven, partnerships

will be an important theme in 2016.

77% of banks would be prepared to form partnerships with existing online payment providers.

66% would work directly with retailers or billing organizations.

For many retail banks, the ability to deliver on

customer expectations will be increasingly

defined by how effectively they can deliver

internal infrastructure enhancements while

forming partnerships across the value chain.

4

The need for revenue growth has made payments a key focus area for retail banks Retail banks face growing pressure to deliver innovation in their payment services

Retail banking is an industry under pressure,

and particularly so when it comes to

payments. The need to invest in new products

and services to drive revenue growth – and in

the core infrastructure to deliver this – is top

of mind for many institutions, but budgets

remain constrained as banks are forced to

adjust to the lower margin post-crisis

environment.

At the same time, the pace of change in digital

commerce in particular has led to a steady

stream of new entrants to the value chain,

increasingly competing directly for customer

mindshare. With regulators in many

territories focused on fostering even greater

competition (PSD2 being a case in point),

banks are recognizing the need to invest in

order to remain central to the customer

purchasing journey. Indeed, the longer term

risk of disintermediation by third party wallets

and commerce platforms is a clear driver of

investment in payments technology.

While the industry was once very much

supply-led, payment services are now a

buyer’s market from the consumer

perspective and banks are fully aware of the

need to deliver on the payment experience

demanded by today’s end-users. At a global

level 78% of banks believe that consumers

want a broader choice of payment options.

This view is felt particularly strongly in

Europe, with 81% of banks in agreement.

Figure 1: Retail banks recognize that they need to deliver new services to customers

Source: 2016 Ovum Global Payments Insight Survey

31%

32%

25%

50%

46%

49%

18%

18%

24%

1%

5%

2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Europe

Americas

Asia

Proportion of respondents (sample: 298)

"Consumers want a broader choice of payment tools"

Strongly agree Agree Disagree Strongly disagree

5

Investment in payments technology will grow strongly in 2016, with delivering innovation and lowering cost as central drivers

In response to these challenges, bank

investment in payments technology will grow

strongly through 2016 and 2017. At a global

level 53% of banks are increasing their

spending in 2016 versus prior year levels, with

15% growing budgets by 5% or more. Similarly

high growth rates in 2015 highlight the degree

to which banks are consistently investing

further into their payment capabilities in

order to drive sustained revenue growth. In

contrast, just 12% of banks are reducing their

IT spend on payments, around the same level

seen in 2015.

At a regional level, Asia will see the highest

growth in 2016. In total, 65% of banks will

increase payments IT spending, compared to

51% in the Americas and 47% in Europe. In

the case of Asia, rising competitiveness and

rapid evolution in service delivery across the

region are important drivers of this growth.

The proportion of banks in the Americas and

Europe growing budgets for payments IT is

lower than in 2015, but nevertheless

highlights a strong proportion of the market

that is growing investments year on year. At

the same time, previous growth in spending

will be maintained at a large proportion of

banks, with 42% in Europe and 33% in the

Americas maintaining budgets at 2015 levels.

Figure 2: Over half of all banks will grow their spending on payments technology in 2016

Source: 2016 Ovum Global Payments Insight Survey

15%

15%

12%

18%

13%

9%

24%

19%

38%

41%

35%

35%

38%

49%

41%

39%

35%

33%

42%

37%

33%

32%

29%

28%

11%

10%

9%

10%

14%

9%

6%

13%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2016

2015

2016

2015

2016

2015

2016

2015

Glo

bal

Eur

ope

Am

eric

asA

sia

Proportion of respondents (2015 sample: 278; 2016 sample: 298)

How do you forecast your investment in payments technology to develop in the next 18-24 months?

Increase a lot (5%+) Increase a little (1-5%) No change (0%)

Decrease a little (1-5%) Decrease a lot (5%+)

6

While the specific drivers of this increased

investment will vary by institution, there are

some strong themes that emerge at the

regional and global level when considering the

expected ROI. The most commonly cited

outcome is an increased range of payment

tools and services, which is top of mind for

67% of all banks. Closely linked to this is the

launch of added value services, with 66% of

banks focusing on this area. Improving the

speed of clearing and settlement is a priority

for 62% of the industry.

Cost reduction remains critically important,

with 60% of banks highlighting this as a key

objective. Managing and replacing legacy IT

remains the central challenge for many

institutions, as it can facilitate service

enhancements while freeing up resources for

further investment. With just over 40% of

banks reporting that operational costs for

their payments business have increased in the

previous 12 months, the scale of the

opportunity to drive efficiencies is clear.

Nevertheless, investing in new products and

services to drive topline growth remains the

over-arching priority. Figure 3 shows the top

three objectives from increased payments IT

investment at the regional level, and

highlights the common focus on revenue.

The focus on increasing the range of payment

options and launching added value services is

most acute in the Americas (led by the US),

with over 70% of banks looking to enhance

their offerings in both areas. Expanding the

range of payment options is also the most

pressing concern in Europe (67%).

Banks in Asia view added value services as the

leading priority. Data analytics, around both

account management/PFM solutions and

loyalty/marketing offerings will both feature

prominently in this space in 2016.

Improving the speed of clearing and

settlement has emerged as an important area

in Asia (62%) and Europe (64%), reflecting the

level of activity and debate around immediate

payments in both geographies

Figure 3: Driving revenue growth from new products and services is the overarching priority for banks in all regions

Source: 2016 Ovum Global Payments Insight Survey

63%

64%

67%

60%

62%

65%

67%

70%

71%

Introduce new payment services/tools

Improved speed of clearing and settlement

Increased range of payment options

Increased range of payment options

Improved speed of clearing and settlement

Launch value added services

Enhanced customer experience/reduced payment friction

Launch value added services

Increased range of payment options

Euro

peAs

iaAm

eric

as

Proportion of respondents (sample: 298)

What ROI would you expect if you increased your investment in payments technology?

7

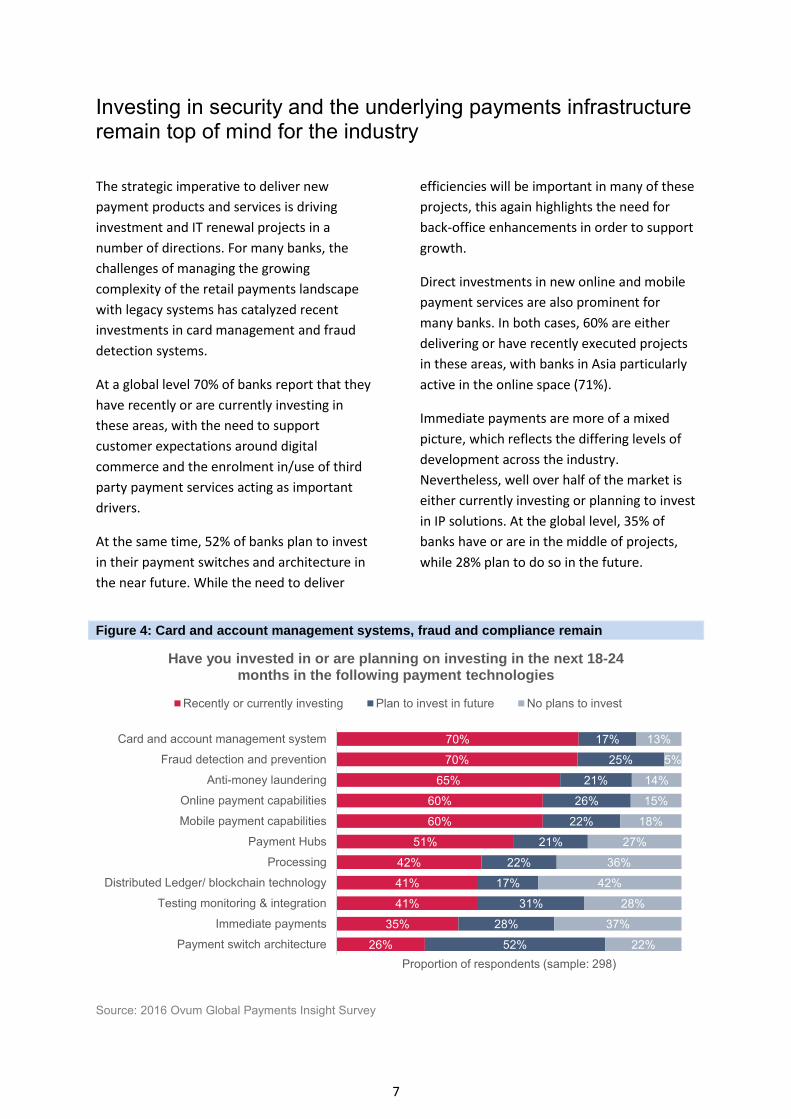

Investing in security and the underlying payments infrastructure remain top of mind for the industry

The strategic imperative to deliver new

payment products and services is driving

investment and IT renewal projects in a

number of directions. For many banks, the

challenges of managing the growing

complexity of the retail payments landscape

with legacy systems has catalyzed recent

investments in card management and fraud

detection systems.

At a global level 70% of banks report that they

have recently or are currently investing in

these areas, with the need to support

customer expectations around digital

commerce and the enrolment in/use of third

party payment services acting as important

drivers.

At the same time, 52% of banks plan to invest

in their payment switches and architecture in

the near future. While the need to deliver

efficiencies will be important in many of these

projects, this again highlights the need for

back-office enhancements in order to support

growth.

Direct investments in new online and mobile

payment services are also prominent for

many banks. In both cases, 60% are either

delivering or have recently executed projects

in these areas, with banks in Asia particularly

active in the online space (71%).

Immediate payments are more of a mixed

picture, which reflects the differing levels of

development across the industry.

Nevertheless, well over half of the market is

either currently investing or planning to invest

in IP solutions. At the global level, 35% of

banks have or are in the middle of projects,

while 28% plan to do so in the future.

Figure 4: Card and account management systems, fraud and compliance remain

Source: 2016 Ovum Global Payments Insight Survey

26%

35%

41%

41%

42%

51%

60%

60%

65%

70%

70%

52%

28%

31%

17%

22%

21%

22%

26%

21%

25%

17%

22%

37%

28%

42%

36%

27%

18%

15%

14%

5%

13%

Payment switch architecture

Immediate payments

Testing monitoring & integration

Distributed Ledger/ blockchain technology

Processing

Payment Hubs

Mobile payment capabilities

Online payment capabilities

Anti-money laundering

Fraud detection and prevention

Card and account management system

Proportion of respondents (sample: 298)

Have you invested in or are planning on investing in the next 18-24 months in the following payment technologies

Recently or currently investing Plan to invest in future No plans to invest

8

Immediate payments will deliver benefits to both banks and their customers The rollout of immediate payment infrastructure is being viewed as an important enabler for banks

With most major markets now either on the

path to creating immediate payments (IP)

infrastructure or with a live IP deployment,

the issue of how best to leverage the

opportunities it creates to drive revenue

growth is top of mind for retail banks.

Consumers are viewed as the group that

stands to benefit most heavily from real-time

24x7 payments, with 61% of banks reporting

this view. This perspective is particularly

strong in Asia, with 72% of banks taking this

position. The pace of innovation across many

markets in this region, particularly around

digital and social media-based commerce is

likely to be an important driver here, as will

high profile developments in Singapore and

Australia.

As shown in Figure 4, 58% of retail banks also

expect to benefit (or are already benefitting)

from IP, with 54% expecting to deliver cost

savings as a result. The latter is particularly

important, as integration and other projects

related to IP will be a trigger for wider

infrastructure renewal and upgrades in some

banks.

At the same time, there remain some that are

skeptical on the potential of immediate

payments. At a global level 11% of banks see

no benefit in IP, with 15% of European banks

holding this view.

Figure 5: Immediate payments are seen as a clear opportunity to deliver new value to customers

Source: 2016 Ovum Global Payments Insight Survey

4%

11%

47%

52%

54%

56%

58%

61%

I have never heard of immediate payments

I see no benefit in immediate payments

Immediate payments will benefit businesses

Immediate payments will drive revenue growth for myorganization

Immediate payments will save my organizationmoney

Regulators are mandating the launch of immediatepayments in future

My organization benefits from immediate payments

Immediate payments will benefit consumers

Proportion of respondents (sample: 298)

Please select which statements best reflects your perceptions of immediate payments

9

Enhanced account information and liquidity management services are the key opportunities from immediate payments

While dedicated overlay services, such as P2P

or even retail payment solutions, built on top

of immediate payment infrastructure have

been the focus of most of the early

developments in this area to date, the bigger

picture is one of a transformation in the

customer experience: real time payments

opening the door to genuinely real time

banking.

The focus in the industry has begun to shift

into how immediate payments will catalyze a

series of new product and service innovations.

The most significant opportunity is around

business and account intelligence, with over

80% of banks in all regions highlighting this as

a key area of potential future benefits. On

both the retail and business/SME (small to

medium enterprise) account side, there is a

renewed focus on PFM and associated areas

in 2016 and IP is ideally positioned to support

further enhancements to these models.

Liquidity management, particularly from the

business/SME perspective, but also for the

bank itself, is also seen as a core benefit.

Shortening the payment cycle from T+2 or 3

into real-time delivers potentially significant

cashflow benefits of course, and is potentially

therefore also a source of revenue for banks.

The reduction in settlement risk is also a key

benefit for retail banks.

Figure 6: The ability to deliver better Business Intelligence and liquidity management services is expected to be a key benefit from IP

Source: 2016 Ovum Global Payments Insight Survey

74%

79%

80%

72%

74%

81%

74%

70%

81%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Customer service

Liquidity management

Business intelligence

Proportion of respondents (sample: 298)

Please select the areas where your customers and your organisation will see the greatest benefits from immediate payments

Europe Asia Americas

10

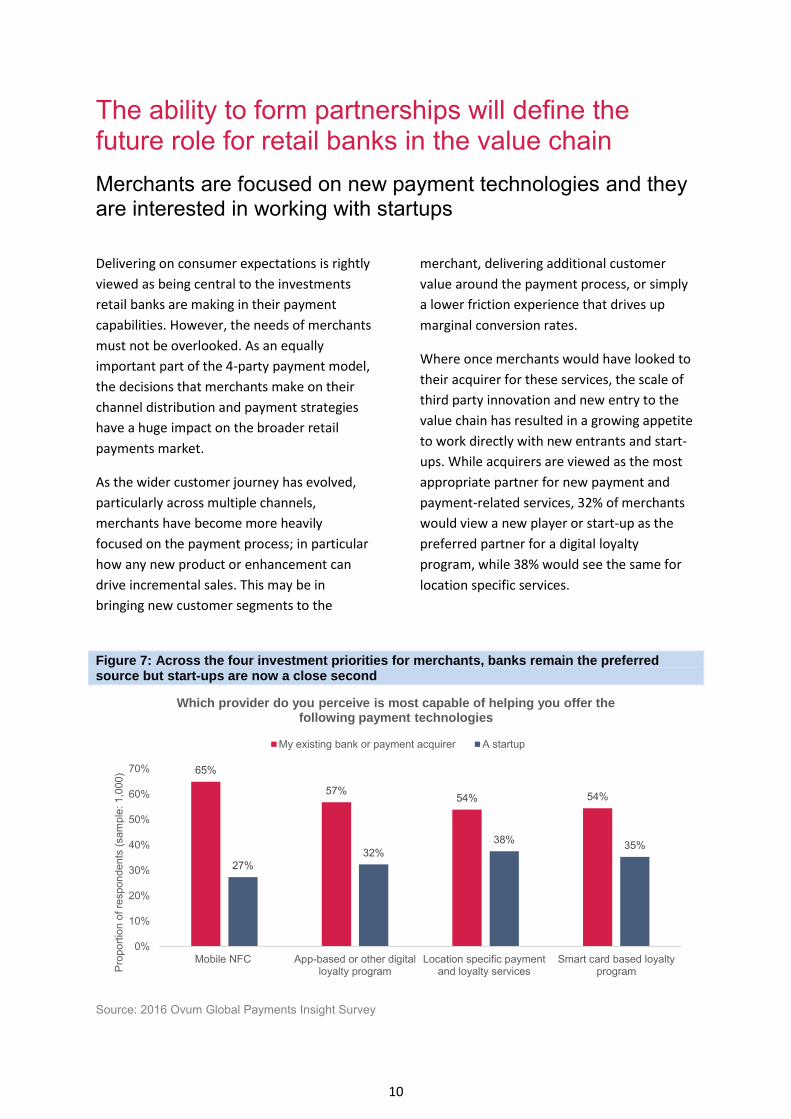

The ability to form partnerships will define the future role for retail banks in the value chain Merchants are focused on new payment technologies and they are interested in working with startups

Delivering on consumer expectations is rightly

viewed as being central to the investments

retail banks are making in their payment

capabilities. However, the needs of merchants

must not be overlooked. As an equally

important part of the 4-party payment model,

the decisions that merchants make on their

channel distribution and payment strategies

have a huge impact on the broader retail

payments market.

As the wider customer journey has evolved,

particularly across multiple channels,

merchants have become more heavily

focused on the payment process; in particular

how any new product or enhancement can

drive incremental sales. This may be in

bringing new customer segments to the

merchant, delivering additional customer

value around the payment process, or simply

a lower friction experience that drives up

marginal conversion rates.

Where once merchants would have looked to

their acquirer for these services, the scale of

third party innovation and new entry to the

value chain has resulted in a growing appetite

to work directly with new entrants and start-

ups. While acquirers are viewed as the most

appropriate partner for new payment and

payment-related services, 32% of merchants

would view a new player or start-up as the

preferred partner for a digital loyalty

program, while 38% would see the same for

location specific services.

Figure 7: Across the four investment priorities for merchants, banks remain the preferred source but start-ups are now a close second

Source: 2016 Ovum Global Payments Insight Survey

65%

57%54% 54%

27%32%

38% 35%

0%

10%

20%

30%

40%

50%

60%

70%

Mobile NFC App-based or other digitalloyalty program

Location specific paymentand loyalty services

Smart card based loyaltyprogramP

ropo

rtion

of r

espo

nden

ts (s

ampl

e: 1

,000

)

Which provider do you perceive is most capable of helping you offer the following payment technologies

My existing bank or payment acquirer A startup

11

Many banks are becoming open to the opportunities presented by working with third parties to deliver innovation

There is increasing acceptance in the industry

over the need to form partnerships in order to

deliver innovation. The realization that the

limitations of legacy infrastructure and costs

of compliance, alongside rapidly growing

customer expectations, cannot be easily

bridged. This is leading many to consider

working closely with third parties to ensure

that they remain in a central position in the

future payments value chain.

Online payment providers, such as PayPal and

Alipay, are the most favorable potential

partners. At a global level, over 75% of banks

would be prepared to form partnerships in

this space, with this rising to 81% in the

Americas. Given the growing reach and

influence of some of the bigger commerce

platforms in particular, this is not surprising,

but there are clear benefits that both groups

could bring to the future digital commerce

model.

Retailers and billing institutions are also

viewed as prime candidates for partnership,

with 66% of banks interested in working more

closely with firms in these areas. In addition

to the fact that some retail banks may have

large retail or biller clients in their transaction

banking divisions, interest in open APIs –

particularly with reference to the PSD2 – will

be an important factor here.

Figure 8: Banks are becoming increasingly open to working with online payment providers, retailers and mass market technology companies to deliver innovation

Source: 2016 Ovum Global Payments Insight Survey

30%

36%

36%

35%

65%

71%

35%

41%

38%

44%

63%

76%

28%

33%

38%

46%

69%

81%

Specialist payment technology providers

Existing payment schemes/networks

Telecoms providers

Mass market technology companies

Retailers/Billers

Online Payment Providers

Proportion of respondents (sample: 298)

Would your organization consider working with the following types of payment providers in future?

Americas Asia Europe

Appendix Methodology

For its 2016 Global Payments Insight Survey Ovum, in conjunction with ACI Worldwide, created a 27

point questionnaire to understand how the current

and future landscape of the payments industry.

The study examines a range of themes, including:

Investment drivers and focus areas for 2016/17

Role of payments in broader strategic objectives

Attitudes to newer opportunities, such as immediate payments and blockchain

Payments IT spending plans and expected ROI

Preferred partners for delivering new services

The research focuses on four different industry

verticals and a total of 14 sub-industry verticals. The

lead categories are as follows:

Billing organizations Retail banking Merchants Transaction banking

The fieldwork was conducted with senior executives responsible for payments strategy and/or

payments IT strategy in each business, and was in the field from December 2015 - February 2016. In

total, 1,675 executives were interviewed, across 14 industry sub-verticals in 18 countries globally.

This report focuses on the retail banking industry. Those interested in the research on billing

organizations, retailers, or transaction banking are advised to visit

www.aciworldwide.com/paymentsinsight for further information.

Respondent Breakdown

Total Respondents 298

Respondents by Region Americas 48.3%

EMEA 22.8%

Asia Pacific 28.9%

Sub-verticals surveyed

Financial Institutions

Retail banking

Merchant acquiring

Example Respondent Titles

Director, Global Corporate Payments, Chief Operations Officer, Finance Director, Revenue Manager, Owner, etc.

Author Kieran Hines, Practice Leader, Financial Services Technology

Ovum Consulting We hope that this analysis will help you make informed and imaginative business decisions. If you

have further requirements, Ovum’s consulting team may be able to help you. For more information

about Ovum’s consulting capabilities, please contact us directly at [email protected].

Copyright notice and disclaimer The contents of this product are protected by international copyright laws, database rights and other intellectual property rights. The owner of these rights is Informa Telecoms and Media Limited, our affiliates or other third party licensors. All product and company names and logos contained within or appearing on this product are the trademarks, service marks or trading names of their respective owners, including Informa Telecoms and Media Limited. This product may not be copied, reproduced, distributed or transmitted in any form or by any means without the prior permission of Informa Telecoms and Media Limited. Whilst reasonable efforts have been made to ensure that the information and content of this product was correct as at the date of first publication, neither Informa Telecoms and Media Limited nor any person engaged or employed by Informa Telecoms and Media Limited accepts any liability for any errors, omissions or other inaccuracies. Readers should independently verify any facts and figures as no liability can be accepted in this regard - readers assume full responsibility and risk accordingly for their use of such information and content. Any views and/or opinions expressed in this product by individual authors or contributors are their personal views and/or opinions and do not necessarily reflect the views and/or opinions of Informa Telecoms and Media Limited.

CONTACT US

www.ovum.com [email protected]

INTERNATIONAL OFFICES

Beijing Dubai Hong Kong Hyderabad Johannesburg London Melbourne New York San Francisco Sao Paulo Tokyo