2016 global communications gaap summit transition: · pdf filepwc 1. yes 2. no 4. it depends 6...

TRANSCRIPT

Transition: getting it right in a changing environment

2016 Global Communications GAAP Summit

Workshop 1: Leases

June 2016Global Communications GAAP Summit

PwC 2

Agenda

1. Identifying a lease

2. Lease term

3. Non-lease components

4. Interaction of IFRS 16 with IFRS 15 (lessors)

5. Variable lease payments

3

June 2016Global Communications GAAP Summit

PwC

How familiar are you with IFRS 16?

1. Very

2. Fairly

3. On my reading list!

Question

Global Communications GAAP Summit

PwC

June 2016

4

Identifying a lease

June 2016Global Communications GAAP Summit

PwC 5

PwC

1. Yes 2. No 4. It depends

6

June 2016Global Communications GAAP Summit

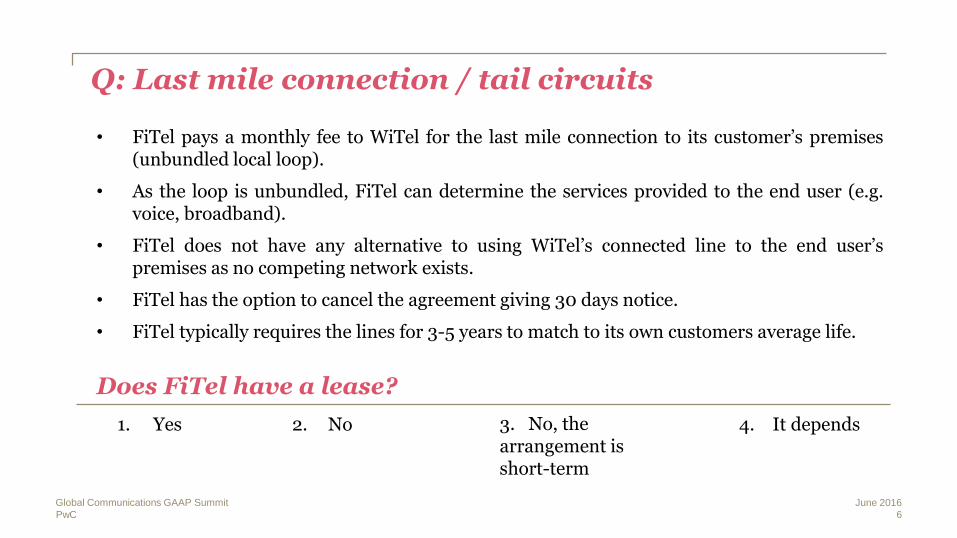

• FiTel pays a monthly fee to WiTel for the last mile connection to its customer’s premises(unbundled local loop).

• As the loop is unbundled, FiTel can determine the services provided to the end user (e.g.voice, broadband).

• FiTel does not have any alternative to using WiTel’s connected line to the end user’spremises as no competing network exists.

• FiTel has the option to cancel the agreement giving 30 days notice.

• FiTel typically requires the lines for 3-5 years to match to its own customers average life.

Does FiTel have a lease?

Q: Last mile connection / tail circuits

3. No, the arrangement is short-term

PwC

Proposed solution: Access fees for last mile connection

This is a lease

Criteria

Right to control the use

Met?

Only FiTel can transmit over the line

Identified assetThe line is dedicated from the exchange to the premises

Benefit throughout period of use

7

June 2016Global Communications GAAP Summit

4

4

4

PwC

1. Yes 2. No 4. It depends

8

June 2016Global Communications GAAP Summit

3. No, its only for 10 of 25 years

Q: Dark fibre IRU

• FiTel enters into a 10 year IRU with WiTel for the right to use a specified darkfibre cable.

• WiTel’s fibre has a 25 year useful economic life

• FiTel will light and operate the fibre for the 10 year period.

Is the 10 year IRU a lease?

PwC

Proposed solution: Dark fibre IRU

This is a lease

9

June 2016Global Communications GAAP Summit

Criteria

Right to control the use

Met?

Only FiTel can light and use the fibre

Identified assetThe end to end fibre strand is dedicated to FiTel

Benefit throughout period of use

4

4

4

PwC

1. Yes 2. No

10

June 2016Global Communications GAAP Summit

3. It depends

Q: Portion of an asset

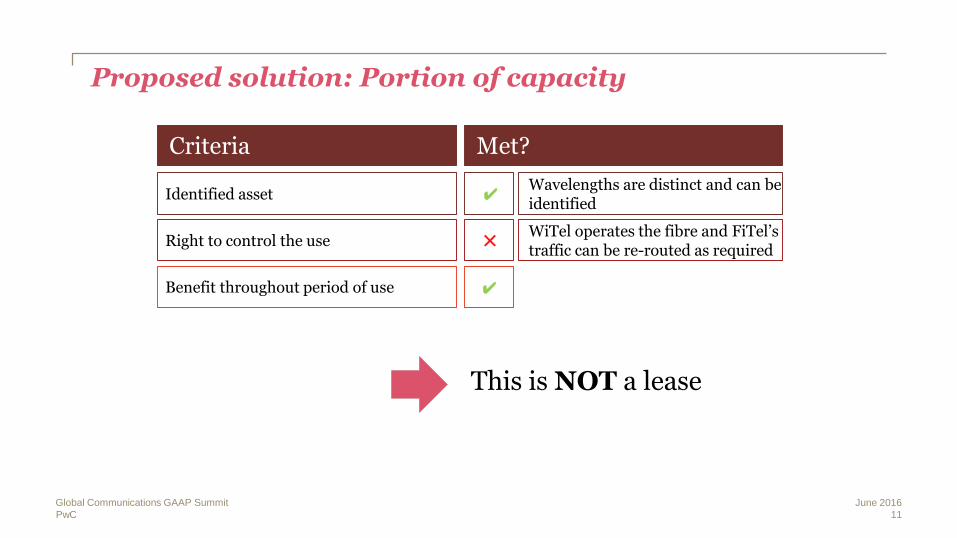

• FiTel enters into a 10 year contract with WiTel (supplier) for the right to 3wavelengths on a fibre strand running from Sydney to Perth.

• WiTel will light and operate the fibre for the period. The fibre has a 25 year usefuleconomic life.

• If there is an outage WiTel will either re-route FiTel’s traffic or pay compensationunder the SLAs in the agreement if re-routing is not possible.

Is the arrangement a lease for FiTel?

PwC

Proposed solution: Portion of capacity

This is NOT a lease

11

June 2016Global Communications GAAP Summit

Criteria

Right to control the use

Met?

WiTel operates the fibre and FiTel’s traffic can be re-routed as required

Identified assetWavelengths are distinct and can be identified

Benefit throughout period of use

5

4

4

PwC

1. Yes 2. No

12

June 2016Global Communications GAAP Summit

3. It depends

Q: Tower sharing

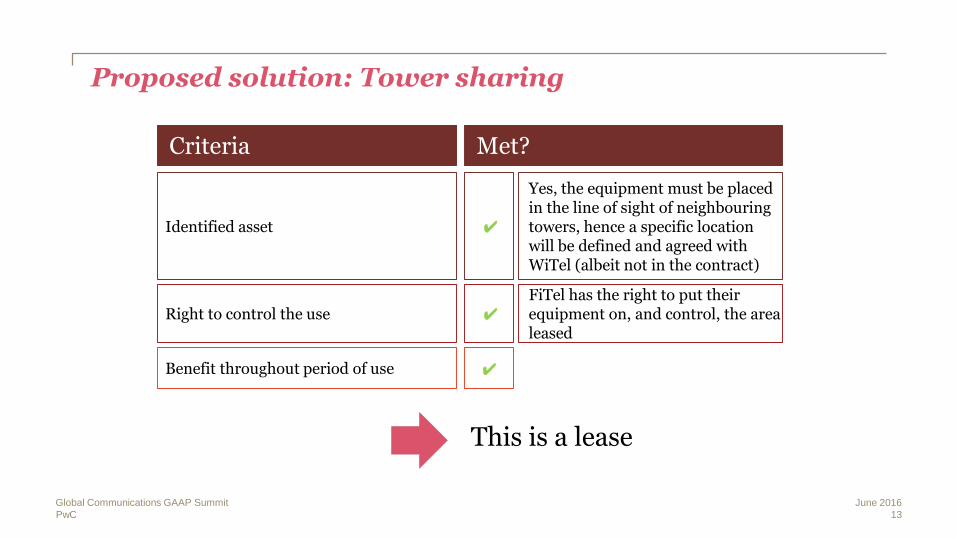

• FiTel enters into a 5 year contract with WiTel to allow it to use part of WiTel’s basestation for microwave transmission equipment in return for a monthly fee.

• The contract is silent on which part of the tower FiTel may use.

• WiTel may change the location of the transmission equipment but only with theagreement of FiTel’s engineers. FiTel can refuse to consent.

• FiTel has the option to extend the contract for a further 5 years. FiTel has a licence tooperate for 20 years and has assessed that the useful economic life of its ownedtowers is 20 years.

Is the tower share a lease for FiTel?

PwC

Proposed solution: Tower sharing

This is a lease

13

June 2016Global Communications GAAP Summit

Criteria

Right to control the use

Met?

FiTel has the right to put their equipment on, and control, the area leased

Identified asset

Yes, the equipment must be placed in the line of sight of neighbouring towers, hence a specific location will be defined and agreed with WiTel (albeit not in the contract)

Benefit throughout period of use

4

4

4

Lease term

June 2016Global Communications GAAP Summit

14

Lease term

Non-cancellable period of the

lease

Periods covered by an

option to terminate

Periods covered by an option to

extend+

+ the lessee is reasonably certainnot to exercise the option

the lessee is reasonably certainto exercise the option

if

if

When determining the lease term, consider:

- all relevant factors that create an economic incentive to exercise an option or not

- include only if it is reasonably certain that the lessee will exercise the option having considered the relevant economic factors.

15

June 2016Global Communications GAAP Summit

PwC

PwC

1. 30 days 2. 3 years

16

June 2016Global Communications GAAP Summit

3. 5 years

Q: Remember the last mile fees?

• The agreement was cancellable at 30 days notice, at FiTel’s option and theyhave no alternative than to use WiTel’s last mile connection.

• FiTel typically leases the access lines for 3-5 years in line with its own averagecustomer lives.

• The asset life of the underlying cables is 25 years.

• FiTel does not have any alternative to using WiTel’s connection to the premise.

What is the lease term?

3. 4 years (average customer term)

PwC

Proposed solution: Access fees for last mile

Is the right to cancel with 30 days notice relevant to the lease term?

Is there an economic incentive for FiTel not to terminate?

Yes – specifically covered by the standard in B35.

Probably yes – FiTel has no alternative asset to use to deliver the services to its customer and its average customer life is 3-5 years.

What is the lease term?Will require judgment. An answer may be 4 years – the average life of FiTel’s customers.

17

June 2016Global Communications GAAP Summit

PwC

1. 5 years 2. 10 years

18

June 2016Global Communications GAAP Summit

3. 20 years

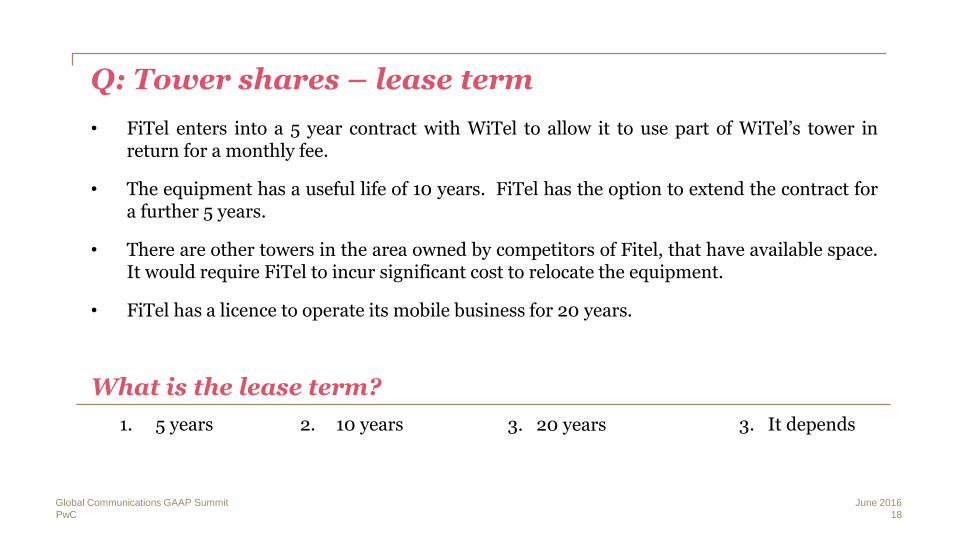

Q: Tower shares – lease term

3. It depends

• FiTel enters into a 5 year contract with WiTel to allow it to use part of WiTel’s tower inreturn for a monthly fee.

• The equipment has a useful life of 10 years. FiTel has the option to extend the contract fora further 5 years.

• There are other towers in the area owned by competitors of Fitel, that have available space.It would require FiTel to incur significant cost to relocate the equipment.

• FiTel has a licence to operate its mobile business for 20 years.

What is the lease term?

PwC

Proposed solution: Tower shares

Is the right to extend relevant to the lease term?

Is there an economic incentive for FiTel to renew?

Yes – specifically covered by the standard.

• High cost to move equipment to new tower

• Equipment still has 5 years useful life

• Risk of service disruption

What is the lease term?Will require judgment. An answer may be 10 years – the term of the initial contract plus the term of the extension.

19

June 2016Global Communications GAAP Summit

PwC

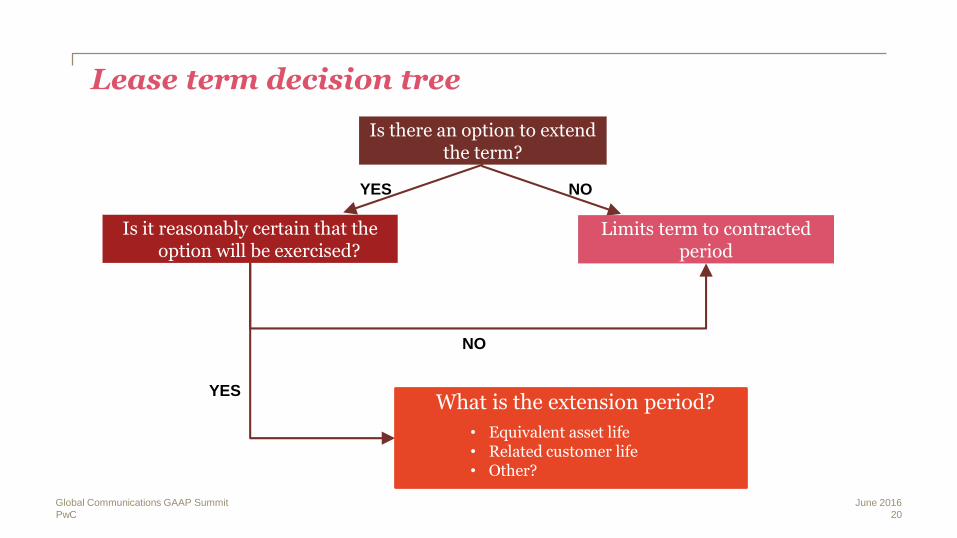

Lease term decision tree

Is there an option to extend the term?

YES NO

Limits term to contracted period

Is it reasonably certain that the option will be exercised?

What is the extension period?

• Equivalent asset life• Related customer life• Other?

YES

NO

20

June 2016Global Communications GAAP Summit

PwC

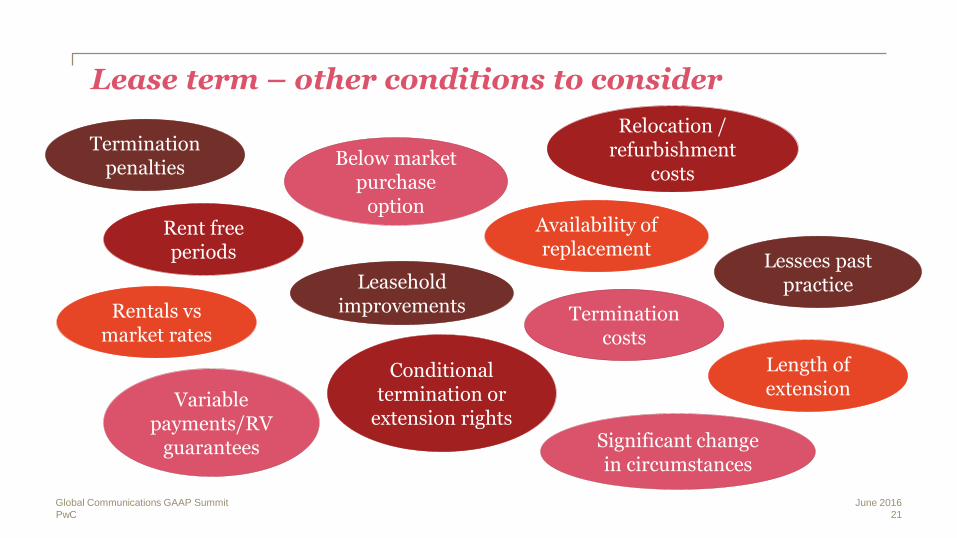

Lease term – other conditions to consider

Termination penalties

Rent free periods

Rentals vs market rates

Variable payments/RV

guarantees

Below market purchase

option

Leasehold improvements Termination

costs

Availability of replacement

Conditional termination or

extension rightsSignificant change in circumstances

Lessees past practice

Length of extension

Relocation / refurbishment

costs

21

June 2016Global Communications GAAP Summit

Non-lease components

22

June 2016Global Communications GAAP Summit

PwC

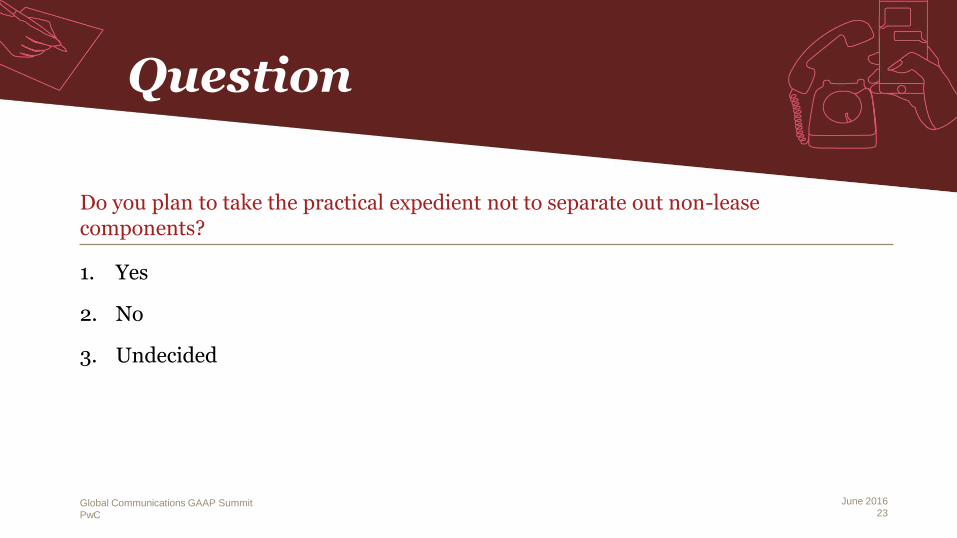

Do you plan to take the practical expedient not to separate out non-lease components?

1. Yes

2. No

3. Undecided

Question

Global Communications GAAP Summit

PwC

June 2016

23

PwC

1. €180,000 2. €132,000

24

June 2016Global Communications GAAP Summit

3. €123,744

Q: Non lease components – retail units

4. Not sure

• FiTel enters into a 3 year lease for a retail unit for €15,000 per quarter.

• The €15,000 includes cleaning, security and advertising services provided by thelandlord.

• FiTel could have taken out the lease without the additional services for €11,000 perquarter. Other units pay €2,000 per quarter for third party cleaning services and getthe advertising for a cost of €500 per month and the security for €6,000 per annum(a total of €5000 per quarter).

What is the value of the right of use asset?

PwC

Proposed solution: Non-lease components

Firstly….is it a lease?

Retail site

Cleaning, security and advertising

Practical expedient allows FiTel to elect not to separate non-lease components from lease components

4

5

Account for the full €15,000 per quarter as a lease, hence the right to use asset will be €180,000 (undiscounted).

25

June 2016Global Communications GAAP Summit

Expedient taken

PwC

*This suggests a discount of €1,000 per qtr

Therefore, the right of use asset should be €123,744 ((€11,000 – €688) x 12 qtrs.) and the payment for the services should be charged at €4,688 per quarter.

Proposed solution: Non-lease components

Lease: €1,000 x €11,000/€16,000 = €688 Non lease: €1,000 x €5,000/€16,000 = €312

26

June 2016Global Communications GAAP Summit

Expedient not taken

Total Per Qtr

Lease component €132,000 €11,000

Non-lease component €60,000 €5,000

Total €192,000 €16,000*

Interaction of IFRS 15, IFRS 16 and IFRS 9 (lessors)

27

June 2016Global Communications GAAP Summit

PwC

Sale or lease? - quad play

• FiTel offers a quad play offering (fixed, broadband, mobile and TV services) toits customers for €100 per month on a 24 month contract.

• The offer includes a set top box, mobile handset, fixed landline and broadbandrouter.

Has FiTel entered into a lease for the equipment?

28

June 2016Global Communications GAAP Summit

1. Yes 2. No 3. Not sure

PwC

Sale or lease? - quad play more info

• Let’s assume the set top box has no additional functionality and just transmitsthe TV frequency.

• The set top box must be returned at the end of the contract term.

Has the set top box been leased or sold?

29

June 2016Global Communications GAAP Summit

1. Leased 2. Sold 3. Still not sure!

Identifying a lease – the new on/off decision

The contract depends on the use of an identified asset

Customer controls the use of the identified asset throughout the period of use2

1

Right to obtain substantially all of the economic benefits that result from using the asset throughout the period of use; and

No identified asset if the supplier has a substantive right to substitute the asset

Right to direct the use of the asset

and

32

June 2016Global Communications GAAP Summit

PwC

PwC

Sale or lease? - quad play

• Does a customer direct the use of an asset if it just transmits a signal? Isturning on the TV directing the use?

• Would your answer be different if the set top box had a Wi-Fi receiver forbroadband inbuilt?

• Would your answer be different if the set top box could be used on othernetworks?

31

June 2016Global Communications GAAP Summit

PwC

Sales vs lease – telco supply of equipment and service

Is outright control of the equipment transferred to the customer? *

No

Yes Apply IFRS 15 in identifying performance obligations

Is control of the right to use the equipment transferred for a period

of time? *

No

Yes

Apply IFRS 15 to services and IFRS 16 to equipment

* - If yes to either of these questions, equipment/lease is considered distinct

Global Communications GAAP Summit June 2016

34

PwC

Sale or lease? – quad play

Global Communications GAAP Summit

33

• FiTel offers a quad play offering to its customers for €100 per month on a 24month contract (€2,400).

• The offer includes a set top box, mobile handset, fixed landline and broadbandrouter.

• The equipment is sold for €500 on a standalone basis.

1. If the arrangement is a lease, how would it be presented?

2. If the arrangement is a sale, how would it be presented?

June 2016

PwC

Bringing it all together – revenue recognition for equipment

34

June 2016Global Communications GAAP Summit

Lease

Revenue(1) €475(2)

Lease receivable (IFRS 16) €475

Contract asset (IFRS 15)

(1) FiTel discloses its lease revenue separately in the notes to the Financial Statements.

(2) The impact of discounting is €25. FiTel concluded that because the impact at the contract level was 5%, it was not a significant financing component under IFRS 15.

Sale

€500

€500

PwC

IFRS 9 Financial Instruments

35

June 2016Global Communications GAAP Summit

Lease SaleDelivered and billed

Accounts receivable €500

Lease receivable €475

Contract asset €500

IFRS 9 applies 4 4 4

- Impairment(1) 4 4 4

- Derecognition 4 4 4

(1) Lessee right to use asset is in the scope of IAS 36

PwC

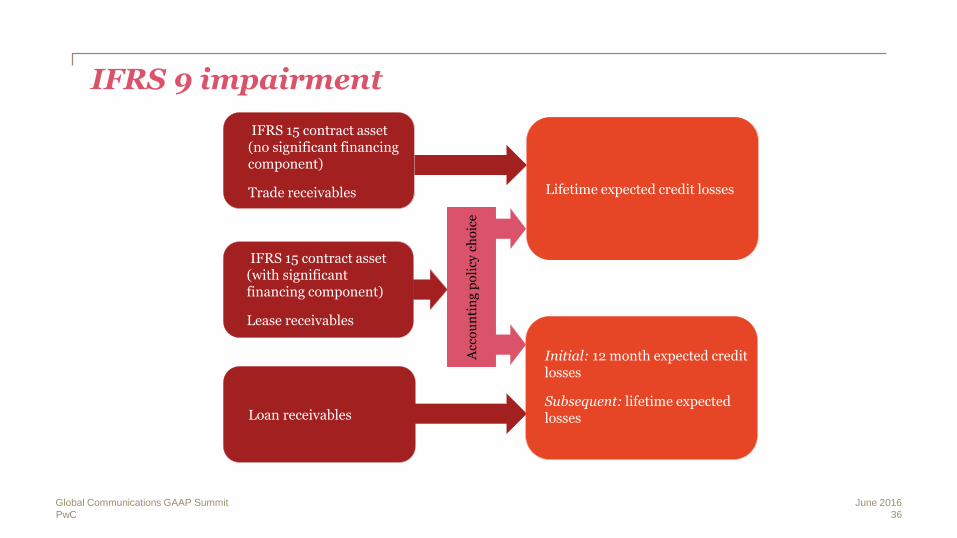

IFRS 15 contract asset (with significant financing component)

Lease receivables

Acc

ou

nti

ng

po

licy

ch

oic

e

IFRS 9 impairment

36

June 2016Global Communications GAAP Summit

IFRS 15 contract asset (no significant financing component)

Trade receivables

Loan receivables

Lifetime expected credit losses

Initial: 12 month expected credit losses

Subsequent: lifetime expected losses

June 2016

37

Variable lease payments

Global Communications GAAP Summit

PwC

PwC

Lease accounting

Right-of-use asset Lease liability

Restoration costs

Initial direct costs

Lease payments

Discount rate

Lease payments made before or at commencement date

Provision

Lease liability

Global Communications GAAP Summit June 201638

PwC

Q: Variable lease payments

• FiTel enters into a 3 year contract for a retail unit on the high street.

• Lease payments consists of:• Annual fixed payments of €100.• Fixed payments will increase every year on the basis of the increase of in the CPI (at

the commencement date CPI is 100 and 105 in year 2).• Variable lease payments determined as 1% of FiTel sales generated from the stores

estimated to be €20 per annum.

What is the amount of the lease liability at the beginning of Year 3?

1. €100 2. €105 3. €125

Global Communications GAAP Summit June 201639

PwC

Proposed solution: Variable lease payments

The lease liability is €105

Lease payments

Variable lease payments that depend on an index or rate

Included in the lease liability

4

Annual fixed payments 4

Variable lease payments that depend on other variable 5

Global Communications GAAP Summit June 201640

Kursalon Vienna

Dinner information

• Buses depart promptly at 18:30 from the hotel lobby

• Back here at 8:00am tomorrow morning

Global Communications GAAP Summit

PwC

June 2016

47

Thank you

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained

in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information

contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability,

responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision

based on it.

© 2016 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers

International Limited, each member firm of which is a separate legal entity.