2016 city of grand rapids income tax...

TRANSCRIPT

2016 CITY OF GRAND RAPIDS

INCOME TAX DEPARTMENT

WITHHOLDING TAX SPECIFICATIONS PACKET

PUBLISHED ON NOVEMBER 24, 2015

This document contains a final/production version of the Withholding Tax Forms and Specifications authorized by the City of Grand Rapids. These forms are issued pursuant to the Michigan Uniform City Income Tax Ordinance MCL 141.671.

Paper submission of questions and return forms approval can be mailed to:

John Schaut, Income Tax Administrator City of Grand Rapids Income Tax Department

300 Monroe Ave NW Suite 380 Grand Rapids MI 49503

Electronic submission of questions and return forms approval can be e-mailed to:

John Schaut, Income Tax Administrator [email protected]

TABLE OF CONTENTS Revised 10/05/2015

Page 1 Title Page Page 2 Table of Contents Page 4 Instructions for Software Companies

Page 4 Michigan Cities Levying an Income Tax Page 4 Michigan Cities Accepting Common Withholding Tax Forms Page 4 Michigan Cities Not Accepting Common Withholding Tax Forms Page 4 General Information Page 5 Governance Page 5 2016 Common Withholding Tax Forms, Schedules and Worksheets Page 5 Listing of Appendices Page 6 Approval of Forms Page 6 Submission of Written Questions or Printed Sample Forms Page 6 Electronic Submission of Questions or Sample Returns Page 5 Printing in Margins Page 6 Printing of Forms Page 6 Extension of Time to File Withholding Tax Return

Page 7 Withholding Tax Guide Page 7 Who Must Withhold Page 7 Withholding as a Convenience to Employee Page 7 Registration Page 8 From Whom To Withhold Page 8 Forms CF-W-4 Required Page 9 From What Compensation to Withhold Page 9 Payments Not Subject to Withholding Page 9 Income Tax Rates Page 10 Calculating the amount to Withhold Page 10 Computer Preparation of Payroll Page 11 Resident Employee Who Works in another City Page 11 Nonresident – Job Partly in a City Levying an Income Tax Page 11 Nonresident – Predominate Place of Employment Page 12 Payment of Tax Withheld Page 12 Employer’s Monthly Deposit for the First or Second Month of a

Quarter Page 12 Form CF-941- Employer’s Quarterly Return Page 12 Mailing Addresses for Mailing Withholding Tax Returns Page 12 Due Dates Page 13 Correction of Errors Over or Under Reporting Tax Withheld Page 13 Correction of Form W-2 Errors Over or Under Reporting Income Page 13 Annual Reports Page 14 Sale or Discontinuance of Business Page 14 Forms, Instructions and Information Page 14 Disclaimer Notice

Page 15 Employer’s Withholding Tax Forms and Instructions Page 15 General Instructions Page 15 Who is Required to Withhold Page 15 Withhold at the Following Tax Rates Page 16 Listing of Forms, Instructions and Monthly and Quarterly Due Dates Page 17 Form CF-6-IT, Notice of Change or Discontinuance Page 18 Forms CF-501 and CF-941, First Quarter Withholding Tax Forms

Page 19 Forms CF-501 and CF-941, Second Quarter Withholding Tax Forms

Page 20 Forms CF-501 and CF-941, Third Quarter Withholding Tax Forms Page 21 Forms CF-501 and CF-941, Fourth Quarter Withholding Tax Forms Page 22 Instructions for Forms CF-501 and CF-941 Page 23 Form CF-W-3, Employer’s Annual Reconciliation of Income Tax

Withheld Page 24 Form CF-W-3S, Supplement to Employer’s Annual Reconciliation

of Income Tax Withheld Page 25 Instructions for Form CF-W-3, Employer’s Annual Reconciliation of

Income Tax Withheld and Form CF-W-3S, Supplement to Employer’s Annual Reconciliation of Income Tax Withheld

Page 27 Penalty and Interest Worksheet Page 25 Other Withholding Tax Forms

Page 28 Form CF-SS-4, Withholding Tax Registration Page 21 Instructions for Form CF-SS-4 Page 33 Form CF-2678, Employee/Payor Appointment of Agent Page 35 Instructions for Form CF-2678, Employee/Payor Appointment of

Agent Page 36 Form CF-8655, Reporting Agent Authorization Page 37 Instructions for Form CF-8655, Reporting Agent Authorization Page 38 Form CF-W-4, Employee’s Withholding Certificate Page 39 Form 2848, Power of Attorney Authorization Page 40 Instructions for Form CF-2848, Power of Attorney Authorization

Page 41 Appendices Page 41 Appendix A, Withholding Deposit Requirements Page 42 Appendix B, Exemption Amounts and Tax Rates for 2015 Page 43 Appendix C, Personal Exemptions Allowed for 2015 Page 44 Appendix D, Approved City Name Abbreviations to Use for

Completing Form W-2, Box 20 Page 45 Appendix E, Mailing Addresses for Mailing Withholding Tax Returns Page 46 Appendix F, Withholding Tax Contacts for Michigan Cities Levying

a City Income Tax Page 47 Appendix G, OCR Line Specifications for Withholding Tax Return

forms CF-501, CF-941 or CF-W-3 Page 51 Appendix H, Three Character City Name Abbreviation Page 52 Appendix I, Tax ID Check Digit Specifications Page 53 Appendix J, Cities Accepting ACH Debit or Credit Withholding

Payments and Return Filing and Cities Accepting Forms W-2 using Common Form CD-ROM Format

Page 54 Appendix K, Withholding Tax Sections of the Michigan Uniform City Income Tax Ordinance and the Regulations Adopted by Most Michigan Cities

Page 58 Appendix L, Withholding Tax Sections of the Michigan Uniform City Income Tax Ordinance

Page 64 Updates, Changes and Corrections to Appendices, Forms, Schedules and Worksheets Page 64 Updates, Changes and Corrections to Appendices, Forms,

Schedules and Worksheets

CITY OF GRAND RAPIDS INCOME TAX DEPARTMENT

2016 INCOME TAX WITHHOLDING INSTRUCTIONS FOR SOFTWARE COMPANIES, EMPLOYERS

AND PAYROLL PROCESSORS

General Information These instructions are to be used with the 2016 withholding tax forms contained in this packet. Additional information may be provided on the individual forms, form instructions or worksheets.

Since the Internal Revenue Code was amended relative to professional employee organizations (PEO’s) effective January 1, 2016, Form GR-SS-4, Employers Withholding Registration, has been revised and new Forms GR-2678, Employer/Payor Appointment or Agent, and GR-8655, Reporting Agent Authorization have been added. The cities are, in essence, following the IRC relative to registering as an employer for income tax withholding and for filing returns and paying city income tax withheld. The City of Grand Rapids needs to know: which employers are liable for withholding; which employers are using a reporting agent to file the employer’s withholding tax returns and who the agents are; which employers are using a payor agent who files and pays the employer’s withholding tax returns under the agent’s FEIN; and which employers use a PEO and what the PEO’s responsibilities are under the PEO agreement.

Form GR-W-3, Employer’s Annual Reconciliation of Income Tax Withheld, has been revised and reformatted to include the client employer’s name and FEIN when the Form GR-W-3 is filed under the withholding agent’s or CPEO’s FEIN.

A new Form GR-W-3S, Supplement to Employer’s Annual Reconciliation of Income Tax Withheld, has been added. Form GR-W-3S is to be filed with form GR-W-3 when either or both of the following conditions exist: the withholding tax has been paid under more than one FEIN; and/or the related Forms W-2 are filed under more than one FEIN.

2016 Grand Rapids Withholding Tax Forms, Schedules and Worksheets Listing of Withholding Tax Guide, Forms and Worksheets Withholding Tax Guide Form GR-SS-4, Employer’s Withholding Registration Form GR-2678, Employer/Payor Appointment of Agent Form GR-8655, Reporting Agent Authorization Employer’s Withholding Tax Forms and Instructions Booklet General Instructions Listing of Withholding Tax Forms in Booklet and Due Dates for Monthly (Form GR-

501) Deposits and Quarterly (Form GR-941) Returns Form GR-6-IT, Notice of Change or Discontinuance Forms GR-501 and Form GR-941, First Quarter Withholding Tax Forms Forms GR-501 and Form GR-941, Second Quarter Withholding Tax Forms Forms GR-501 and Form GR-941, Third Quarter Withholding Tax Forms Forms GR-501 and Form GR-941, Fourth Quarter Withholding Tax Forms Form GR-W-3, Employer’s Annual Reconciliation of Income Tax Withheld Form GR-W-3S, Supplement to Employer’s Annual Reconciliation of Income Tax

Withheld

Instructions for forms GR-501, Employer’s Monthly Deposit of Income Tax Withheld and Form GR-941, Employer’s Quarterly Deposit of Income Tax Withheld

Penalty and Interest Worksheet Form GR-W-3S, Supplement to Employer’s Annual Reconciliation of Income Tax

Withheld GR-W-4, Employee’s Withholding Certificate GR-2848, Power of Attorney Authorization

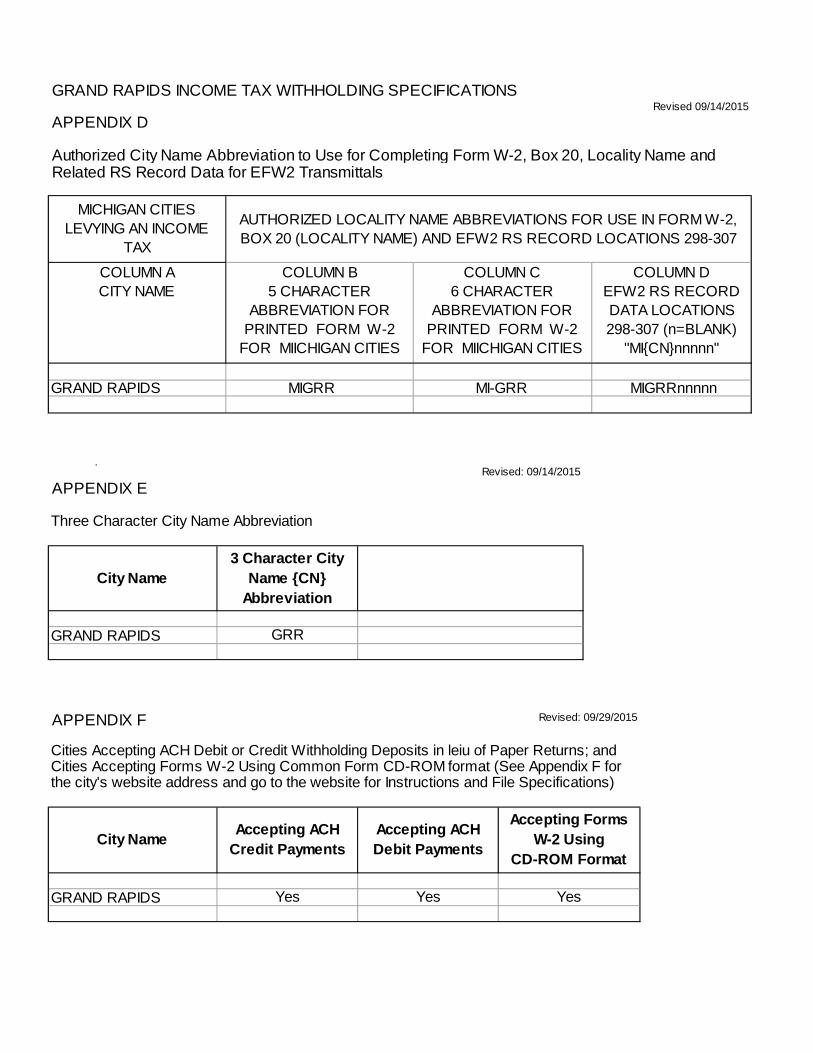

Listing of Appendices Appendix A, Cities Accepting Common Form Withholding Tax Returns, Exemption

Amounts and Tax Rates for Tax Year 2016 Appendix B, Personal Exemptions Allowed Appendix C, Withholding Deposit Requirements Appendix D, Authorized City Name Abbreviations to Use for Completing Form W-2, Box

20, Locality Name and Related RS Record Data for EFW2 Transmittals Appendix E, Three Character City Name Abbreviation Mailing Addresses for Mailing Withholding Tax Returns Appendix F, Cities accepting ACH Debit or Credit Withholding Payments and Return

Filing and Cities Accepting Forms W-2 using Common Form CD-ROM Format

Withholding Tax Contacts for Michigan Cities Levying a City Income Tax Appendix G, Mailing Addresses for Mailing Returns to Cities Accepting the Withholding

Tax Common Form Appendix H, Withholding Tax Contacts for Michigan Cities Levying a City Income Tax Appendix I, OCR Line Specifications for Withholding Tax Return forms GR-501, GR-941

or GR-W-3 Appendix J, Tax ID Check Digit Specifications Appendix K, Specifications for Employer Electronic Media Filing of City Forms W-2 Appendix L, Withholding Tax Sections of the Michigan Uniform City Income Tax

Ordinance and the Regulations Adopted by Most Michigan Cities

Approval of Forms The Common Form as produced by software must be submitted for approval to the Income Tax Administrator of the City of Grand Rapids. For 2016, submission of completed set sample forms for a scanning test is required.

Submission of written questions or sample returns can be mailed to: John Schaut, Income Tax Administrator City of Grand Rapids Income Tax Department

300 Monroe Ave NW Suite 380 Grand Rapids, MI 49503

Phone: (616) 456-3823 Fax: (616) 456-4540 E-mail: [email protected]

Electronic submission of questions or sample returns can be e-mailed to: John Schaut, Income Tax Administrator E-mail: [email protected]

Printing in Margins The printing of any information including taxpayer, preparer identification, firm identification and/or account information in the left, right, top and bottom margins of any return form, worksheet, schedule or voucher submitted to a city for processing is absolutely prohibited.

Printing of Forms The following forms are to be printed as laid out in the forms packet: GR-501, Employer’s Monthly Deposit of Income Tax Withheld

GR-941, Employer’s Quarterly Return of Income Tax Withheld GR-W-3, Employer’s Annual Reconciliation of Income Tax Withheld GR-SS-4, Employer’s Withholding Registration GR-W-4, Employee’s Withholding Certificate GR-2848, Power of Attorney Authorization

Extension of Time to File a Withholding Tax Return No extensions of time are allowed relative to filing a return and making payment of income tax withheld.

Revised 10/15/2015

CITY OF GRAND RAPIDS INCOME TAX DEPARTMENT

WITHHOLDING TAX GUIDE

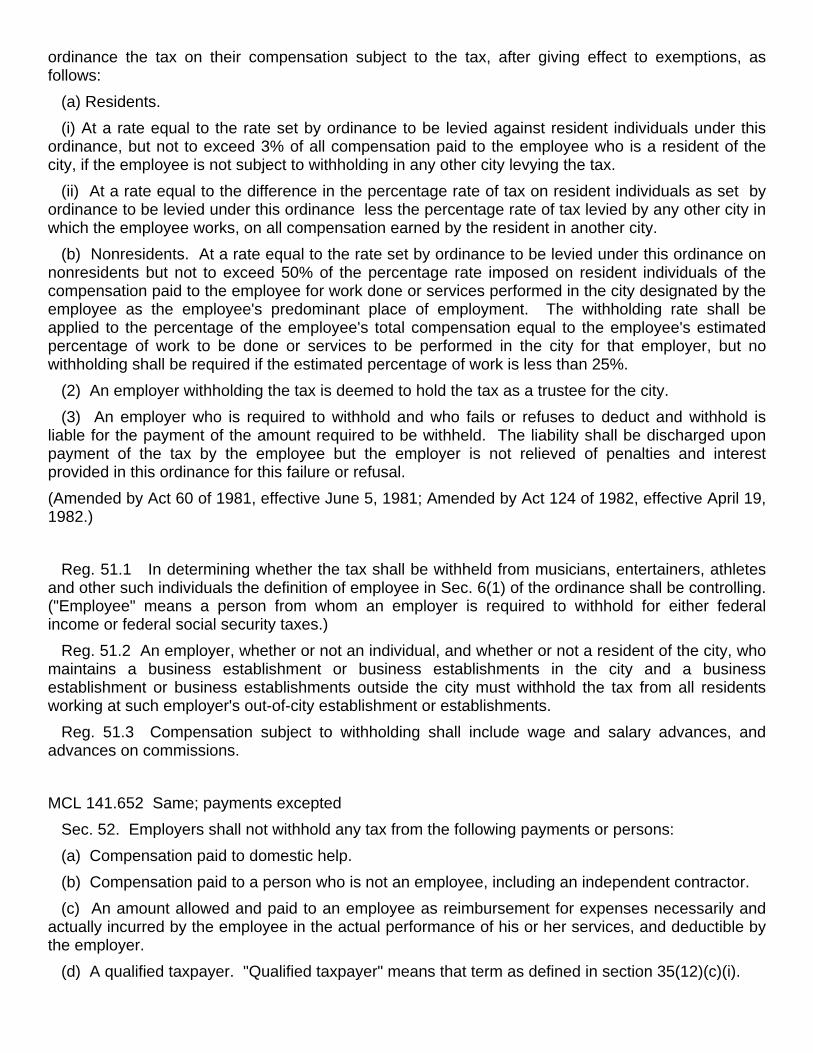

Revised 10/15/2015 WHO MUST WITHHOLD An employer who: has a location in the city; or is “doing business” in the city, even though the employer has no location in the city; is required to withhold the city’s income tax from wages paid to employees.

An employer is any “individual, partnership, association, corporation, nonprofit organization, governmental body or unit or agency, or any other entity that employs one or more persons on a salary, bonus, wage, commission or other basis, whether or not the employer is in a business.”

Starting January 1, 2016 as a result of an amendment to IRC Sec. 3511(a)(1), a professional employer organization (PEO):

1. Who is recognized by the Internal Revenue Service (IRS) as a certified professional employer organization (CPEO);

2. Has a PEO agreement with a client employer: a. Who has a location in the city or is “doing business” in the city; b. Under which the PEO is responsible for withholding and paying income tax withheld from

the client’s employees; 3. Meets the definition of employer under the Michigan Uniform City Income Tax Ordinance (MCL

141.606(2)); 4. Is considered to be a co-employer of the employees covered by the PEO agreement and the

client is also considered to be a co-employer of such employees. 5. Is responsible for withholding the city income tax from wages paid to employees; and 6. Is liable for filing returns and payment of the income tax withheld or the income tax that should

have been withheld from employee wages.

Example: A construction company from Ohio doing work in a city levying an income tax is required to withhold tax for that city even though it has no business location in the city.

An employer who is required to withhold tax for a city must withhold tax from all employees working in that city and from all residents of that city working anywhere for that employer.

A nonprofit organization in the city is required to withhold from its employees (even though it is not engaging in business activity in the usual sense).

WITHHOLDING AS A CONVENIENCE TO EMPLOYEE The City of Grand Rapids encourages employers not required to withhold tax to register and withhold for the convenience of their employees who are residents of that city. Convenience withholders must comply with the registration and filing requirements of the City’s Income Tax Ordinance.

REGISTRATION Every employer required to withhold income tax for the city must register by filing Form GR-SS-4, Employer’s Withholding Registration with the city. The registration requirement applies to a CPEO responsible for withholding city income tax under an agreement with an employer who has a location in the city or is “doing business” in the city.

The employer’s account number is their federal employer identification number (FEIN) followed by an uppercase W. An employer must immediately advise the city of a newly assigned FEIN by filing a Notice of Change or Discontinuance, Form GR-6-IT.

Employers using a reporting agent, an IRC Section 3504 Agent, or a PEO must file additional forms to provide information and disclosure of information to the payroll service provider.

Reporting Agent and Form GR-8655 Employers using a reporting agent must file Form GR-8655, Reporting Agent Authorization, with the city to authorize the reporting agent to: sign and file withholding tax returns; make deposits and payments of withholding tax; receive or request copies of tax information and other communications from the city income tax department; and receive otherwise confidential taxpayer information from the city to assist in responding to certain city income tax notices relating to the Form W-2 series of information returns. The employer’s withholding tax is paid and all withholding tax forms are filed under the employer’s FEIN. An employer using this type of reporting agent is solely liable for the filing of withholding tax returns and payment of the withholding tax due.

IRC Section 3504 Agent and Form GR-2678 An employer and a third party may file Form GR-2678, Employer/Payor Appoint of Agent, to authorize the third party as an agent of the employer under IRC section 3504, and for the third party to accept the appointment and become the employer’s agent.

Under this section of the IRC, the employer is authorizing the city income tax department to disclose otherwise confidential tax information to the agent relating to the authority granted under this appointment, including disclosures required to process Form GR-2678. The agent may contract with a third party, such as a reporting agent or certified public accountant, to prepare or file the returns covered by this appointment, or to make any required deposits and payments. Such contract may authorize the city income tax department to disclose confidential tax information of the employer/payer and agent to such third party. If a third party fails to file the returns or make the deposits and payments, the agent and employer/payer remain liable.

Professional Employer Organization PEO Prior to January 1, 2016 there is only one type of PEO, depending on the agreement with their client employer, which may or may not be a payroll service provider, a reporting agent or an IRC Section 3504 agent. After December 31, 2015 there are two types of PEOs. A certified PEO, one certified under IRC Sec. 3511(a)(1), and an uncertified PEO.

Information about a CPEO is found at the beginning of this booklet under the heading, “Who Must Withhold.” An uncertified PEO is like all PEOs prior to January 1, 2016 as noted in the above paragraph.

A completed registration, Form GR-SS-4, may be filed via E-mail, Fax or U.S. Mail. The e-mail address is [email protected], the Fax number is (616) 456-4540 and the mailing address is City of Grand Rapids Income Tax Dept. PO Box 347, Grand Rapids, MI 49501-0347.

FROM WHOM TO WITHHOLD Employers are required to withhold from the following employees:

1) All residents of the city whether or not they work in the city; and 2) All nonresidents of the city who have the city as their predominant place of employment (see

below).

An employee is defined as “a person from whom an employer is required to withhold for either federal income tax or social security taxes” (MCL141.606(1).

FORM GR-W-4 REQUIRED To determine each employee’s place of residence and predominant place of employment, an employer must have each employee fill out an Employee’s Withholding Certificate, Form GR-W-4. Only one Form GR-W-4 is required for each employee, even though the employee may be subject to withholding for two cities.

When properly filled out, Form GR-W-4 provides the employee’s city of residence and the two cities or communities in which the employee earns the greatest percentage of compensation from the employer. Most employees will only have one city of employment and will check the box indicating 100% as the percentage of compensation earned in that city. Form GR-W-4 is also the employee’s statement of the number of personal and dependency exemptions claimed. Form GR-W-4 is available on the city’s website. The website address for each city is listed in Appendix H.

If an employee fails or refuses to complete Form GR-W-4 upon the request of the employer, tax shall be withheld from the employee’s compensation at the city’s resident tax rate.

If the information submitted by an employee is not believed to be true, correct and complete, the city income tax department must be advised.

Do not mail GR-W-4 forms to the city; these are for the employer’s use and must be retained in the employer’s files.

FROM WHAT COMPENSATION TO WITHHOLD The Michigan Uniform City Income Tax Ordinance requires income tax be withheld from:

1) All compensation (salaries, wages, commissions, severance pay, bonuses, etc.) of a resident employee for services rendered or work performed regardless of whether such services or work are performed in or out of the city; and

2) All compensation of a nonresident employee for services rendered or work performed in the city where the city is the employee’s predominant place of employment.

Vacation, holiday, sick, severance, bonus, etc. pay paid to a nonresident employee who performs part but not all of their work or services in the city are taxable to the same extent that their normal compensation is taxable.

Example: A nonresident employee who is subject to withholding on 60% of their earnings, because 60% of their work is performed in a city levying a income tax, is also subject to withholding on 60% of their vacation, holiday, sick pay, severance pay, bonus, etc. pay. Wage payments during periods of sickness are also taxable.

PAYMENTS NOT SUBJECT TO WITHHOLDING Withholding does not apply to:

1) Wages paid to domestic help; 2) Fees paid to independent contractors who are not employees; 3) Payments to nonresident employees for work or services performed in the city, if the

predominant place of employment is not in that city; 4) Payment to a nonresident employee for work or services rendered outside of the city; 5) Pensions, annuities, worker’s compensation and similar benefits; 6) Amounts paid for sickness, personal injury or disability (so called excludable sick pay) to the

same extent that these amounts are exempt from federal income tax, but the employer must withhold from such payments if federal tax is withheld;

7) Amounts paid to an employee as reimbursement for expenses incurred in performing services.

An individual with income described in items 1, 2 and 3 above is not subject to withholding on such income. The individual is nevertheless required to file an annual return and report such income if the individual is a resident of a city levying an income tax, or is a nonresident earning such income in a city levying an income tax.

INCOME TAX RATES The resident tax rate is 1.5% and the nonresident tax rate is 0.0075%.

CALCULATING THE AMOUNT TO WITHHOLD The amount of city income tax to withhold is a straight percentage on compensation after an adjustment for personal and dependency exemptions. The personal exemptions amount is $600. The dependency exemptions allowed by the city is the same as allowed for federal income tax purposes. For the various pay periods the exemption value is divided by the number of pay periods in a year. Some examples follow:

Exemption Value $600.00 ` Weekly (52) $11.54 Bi-weekly (26) $23.08 Semi-monthly (24) $25.00 Monthly (12) $50.00 Per diem (365) $ 1.64

Personal exemptions are allowed for the employee and spouse. Additional personal exemptions are allowed for an employee or spouse who is: 65 years of age or older; blind (this is different from the federal rule); deaf; .or permanently disabled. An employee or spouse who is 65 years of age or older may not claim the additional personal exemption for being permanently disabled.

Dependency exemptions are allowed to the same extent allowed for federal income tax purposes.

The amounts in the preceding table are used to adjust gross pay for payroll withholding. The adjustment is the number of exemptions on Form GR-W-4 multiplied by the exemption value of the city. For a weekly payroll for an employee with three (3) exemptions working in a city with an exemption value of $600, the adjustment is 3 times $11.54, or $34.62.

EXAMPLE: Gross pay is $200.00 per week and the employee is a resident of Grand Rapids with 3 exemptions. The amount from which tax is to be withheld is $200.00 (gross pay) less $34.62 (exemption amount) or $165.38. Apply the 1.5% resident tax rate (.015 times $165.38) and withhold $2.48 from the employee for this week’s compensation.

For bonuses or other taxable earnings paid in addition to regular payroll, do not adjust for exemptions. Withhold the correct tax percentage from the entire bonus or other taxable earnings amount.

COMPUTER PREPARATION OF PAYROLL Since hardware and software used to compute income tax withholding varies, it is impossible to give an actual program with which to compute withholding. The following is a description of the most commonly used method to compute the amount of tax to withhold.

1. Nonresident employee withholding calculation a. Compute the employee’s gross wages from which to withhold:

i. Use gross earnings of the employee for work performed in the nonresident city; or ii. Use total gross earnings for the payroll period multiplied by the percent earned in the

nonresident city; b. Multiply the employee’s number of exemptions by the appropriate exemption value for the

city for the payroll period: c. Subtract the result of Step b from the result of Step a. d. Compute the amount of tax to withhold by multiplying the result from Step c by the

nonresident tax rate for the city.

2. Resident employee withholding calculation a. Compute the employee’s gross earnings for the payroll period. b. Multiply the employee’s number of exemptions by the appropriate exemption value for the

city for the payroll period; c. Subtract the result of Step b from the result of Step a; d. Multiply the result from Step c by the resident tax rate for the city.

e. If the employee worked in another city levying an income tax compute the credit for tax withheld for the other city; (This credit cannot exceed the amount of tax which would be withheld by the resident city using the nonresident tax rate of the resident city on the same amount of gross earnings of the employee for work performed in the nonresident city.)

f. Compute the amount of tax to withhold by subtracting the result of Step e from the result of Step d.

RESIDENT EMPLOYEE WHO WORKS IN ANOTHER CITY LEVYING AN INCOME TAX When an employee who is a resident of a city levying an income tax works at a job in another city levying a city income tax, the employer must withhold separately for both cities. The amount of income tax to withhold for the resident city depends on the credit allowed for the tax withheld for the other city.

If the nonresident tax rate of the other city is less than or equal to the nonresident tax rate of the resident city, the amount to withhold for the resident city is calculated by computing the normal resident city withholding and then subtracting the amount of tax withheld for the other city.

If the nonresident tax rate of the other city is greater than the nonresident tax rate of the employee’s resident city, the amount to withhold for the employee’s resident city is calculated by computing the normal resident city withholding and then subtracting an amount calculated by multiplying gross pay taxable in the other city by the resident city’s nonresident tax rate.

NONRESIDENT – JOB PARTLY IN A CITY LEVYING AN INCOME TAX If a nonresident of the city works less than 100% of the time within the city for an employer, the amount withheld should be based only on wages earned in the city. If gross pay is $200.00 and only 60% of the employee’s work is in city, the gross pay for the city’s tax purposes is 60% of $200.00 or $120.00. In this example, compute the amount to be withheld for the nonresident city as if the employee earned $120.00 gross pay. NONRESIDENT – PREDOMINANT PLACE OF EMPLOYMENT A nonresident of a city levying an income tax is subject to withholding only when the city is the nonresident employee’s predominant place of employment.

The Ordinance defines predominant place of employment as “that city imposing a tax under a uniform city income tax ordinance other than the city of residence, in which the employee estimates he will earn the greatest percentage of his compensation from the employer, which percentage is 25% or more.” See example below.

A city is a nonresident’s predominant place of employment if: 1) The nonresident employee earns a greater percentage of his or her compensation in the city

than any other city levying an income tax, except the employee’s city of residence; and 2) This greater percentage of his or her compensation in the city constitutes 25% or more of the

nonresident employee’s total compensation from the employer.

PAYMENT OF TAX WITHHELD Monthly or quarterly deposit (payment) of the tax withheld may be made in the following ways:

1. Via U.S mail or courier with the filing of a monthly or quarterly withholding tax return form; 2. ACH debit using the city’s withholding tax tool; 3. ACH credit with an addendum file through the employer’s bank. 4. Credit card.

For ACH direct debit payments, instructions are available on the city’s website. For ACH credit payments, registration is required and a set up by the Income Tax Department is necessary. For cities accepting credit card payments, contact the city for instructions. Monthly and quarterly payment forms are available on the city’s website.

Grand Rapids like most cities does not mail withholding forms to employers. If withholding tax forms are needed, contact the Income Tax Dept. Withholding Tax Section. Grand Rapids provides pre-identified withholding tax forms through use of their Withholding Tax Tool. Refer to the city’s website to see if and how to get pre-identified forms. EMPLOYER’S MONTHLY DEPOSIT FOR THE FIRST OR SECOND MONTH OF A QUARTER Many cities require monthly deposit of tax withheld for the first or second month of a quarter in which the tax withheld for the month exceeds $100.00. Employers who make a deposit for a month must use Form GR-501, Employer’s Monthly Deposit. FORM GR-941 - EMPLOYER’S QUARTERLY RETURN Every employer must file a Form GR-941, Employer’s Quarterly Return of Income Tax Withheld, for each calendar quarter. Form GR-941 must be filed even if no tax was withheld during a quarter or when all tax withheld was previously paid on Forms GR-501 for the quarter. The amount to remit with Form GR-941 is the amount tax withheld for the quarter not previously deposited for the first or second month of the quarter. MAILING ADDRESSES FOR MAILING WITHHOLDING TAX RETURNS The City’s mailing address is Grand Rapids Income Tax Dept. PO Box 347, Grand Rapids, MI 49501-037.

All checks, money orders, etc. in payment of withholding taxes should be made payable to City of Grand Rapids. All payments must be submitted with a monthly or quarterly withholding tax form. DUE DATES Each withholding deposit is due on the last day of the month following the month in which the tax withheld exceeds $100. Each quarterly return is due on the last day of the month following the end of the quarter.

Example: GR-501 Monthly Deposit for January is due February 28 (or 29 if a leap year). GR-501 Monthly Deposit for February is due March 31. GR-941 Quarterly Return for 1st calendar quarter is due April 30.

When the due date of a deposit or return falls on a Saturday, Sunday or holiday the due date is automatically extended to the next business day. CORRECTION OF ERRORS OVER OR UNDER REPORTING TAX WITHHELD Employer Errors Employer’s errors over or under withholding of tax or reporting tax withheld should be corrected as follows:

1) If an error is discovered in the same quarter in which it was made, the employer shall make the necessary adjustment in a subsequent withholding payment within the quarter. (Report the corrected amount of tax withheld on the quarterly return.)

2) If an error is discovered in a subsequent quarter of the same calendar year, the employer shall make the necessary adjustment in a subsequent withholding payment and include it as an adjustment on the next quarterly return. (Report the corrected amount of tax withheld on the quarterly return.)

3) If an error is discovered after the end of the year but before W-2 forms are issued to employees, the employer shall make the necessary adjustment when filing Form GR-W-3 and: a) Pay any additional withholding tax due with Form GR-W-3; or b) Report the overpayment of tax withheld on Form GR-W-3 by reporting that the withholding

tax paid is greater than the total tax withheld as reported on the enclosed Forms W-2, and

include a separate written request for refund of the overpayment with a specific explanation of the error(s) causing the overpayment of tax withheld. Overpayments of withholding will not be credited toward tax due in a subsequent year.

4) If an error of underreporting tax withheld is discovered in a subsequent year after the issuance of Forms W-2 to employees, the employer shall notify the Income Tax Department of the error by filing an amended GR-W-3, including a copy of the corrected Form(s) W-2C issued to employee(s), and pay any additional withholding tax due with the amended Form GR-W-3.

5) If an error of over reporting tax withheld on a Form W-2 is discovered, the city will not refund the over withheld tax. The employer should seek to recover the over reported tax withheld from their employee.

Employee Errors If an error causing over withholding of tax is due to an employee’s error or any reason other than an employer’s error, the employer shall neither refund the excess tax withheld to the employee nor offset the excess tax withheld by under withholding in a subsequent period.

Example: an employee fails to timely provide employer with a Form GR-W-4. The employer is required to withhold tax from wages to the employee at the resident tax rate. The employee subsequently provides a properly completed form GR-W-4. The employer should start withholding at the correct tax rate from the date the Form GR-W-4 is received from the employee. The employer may not go back and correct the over withholding caused by the employees failure to file a timely Form GR-W-4.

Another example is an employee claiming fewer exemptions than allowed filing a new Form CFW-4 to increase the number of exemptions. The increase number of exemptions may only affect withholding going forward from the date the new Form GR-W-4 was filed. CORRECTION OF FORM W-2 ERRORS OVER OR UNDERREPORTING INCOME An employer is required to file an amended Form GR-W-3 upon issuance of a Form W-2C to an employee correcting the reporting of: Box 1, wages; Box 11, nonqualified plans; or Box 16, wages. A copy of Form(s) W-2C must be submitted with the amended Form GR-W-3.

ANNUAL REPORTS An Employer’s Annual Reconciliation of Income Tax Withheld, Form GR-W-3, is required to be filed by last day of February of the following year. A W-2 form for each employee subject to the city’s income tax withholding must be included with Form GR-W-3. Form GR-W-3 is included in the annual withholding tax booklet and is also available on each city’s website.

A copy of Form W-2 issued to each employee subject to the city’s income tax must be filed whether the tax was withheld or not. The Form W-2 must provide the following information:

1) The name, address and federal identification number of the employer. 2) The name, home address and social security number of the employee. 3) The total gross wages paid the employee for the year even if the total wages did not have the

tax withheld for the city. 4) The total tax withheld for the city for the year. The amount of tax withheld must be clearly

labeled as being the city’s income tax withheld, and the city must be properly identified in the locality name box on the Wage and Tax Statement, Form W-2. Failure to properly and clearly identify the city for which the tax was withheld in the locality box of Form W-2 makes the form unacceptable. An improperly identified city in the locality name box of Form W-2 does not satisfy the withholding tax reporting requirements of the income tax ordinance of the city, and will not be accepted as the basis for a tax payment or refund when attached to an individual’s income tax return for the city.

Employers wishing to purchase one of the commercially available W-2 forms in order to combine the city, state and federal reporting in one operation are permitted to do so, provided one copy is submitted to the city by the employer.

Grand Rapids accepts filing of employer’s Forms W-2 via CD-ROM in lieu of paper Forms W-2. Information and specifications for filing via CD-ROM are available on the city’s website.

SALE OR DISCONTINUANCE OF BUSINESS An employer who sells or discontinues business must file a Notice of Change or Discontinuance. This form is included in the annual withholding tax forms booklet and also available on each city’s website.

An employer who goes out of business or permanently ceases to be an employer must file Forms W-2 and a GR-W-3 by the date the final withholding payment is due.

FORMS, INSTRUCTIONS AND INFORMATION Income tax forms, instructions and additional information are available on the city’s website.

Withholding Tax Tables are available as a separate document on the city’s website.

Each city provides withholding tax assistance on their website and via telephone.

Copies of the Ordinance and the Rules and Regulations adopted by each city are usually available from the City Clerk’s office. Usually a city’s income tax ordinance is available from each city’s website under the City Clerk’s menu item Municipal Code, search for “income tax” to get to the ordinance.

The Michigan Uniform City Income Tax Ordinance (MCL 141.601 et seq.) is available on the Michigan Legislature website at http://www.legislature.mi.gov. Search for “city income tax” under the Michigan Compiled Laws Search, MCL Content, next click on “Act 284 of 1964” (it should be the top item) and then click on Document “284-1964-2” to get to the Michigan Uniform City Income Tax Ordinance. Note that Document “284-1964-3” contains the alternative sections of the ordinance.

DISCLAIMER NOTICE These instructions are interpretations of the Michigan Uniform City Income Tax Ordinance as adopted by the city. The city’s ordinance will prevail in any disagreement between the tax forms, instructions, information, etc. and each city’s ordinance.

ADDRESS SERVICE REQUESTED

2016 CITY OF GRAND RAPIDS 2016 EMPLOYER'S WITHHOLDING TAX

FORMS AND INSTRUCTIONS

ONLINE FILING AND PAYMENT OF WITHHOLDING TAX

SOME CITIES ALLOW ONLINE FILING OF EMPLOYER WITHHOLDING TAX WITH ELECTRONIC DIRECT DEBIT PAYMENT OF TAX DUE. SEE APPENDIX F FOR A LISTING OF THESE CITIES AND, GO TO THEIR WEBSITE FOR INSTRUCTIONS.

WHO IS REQUIRED TO WITHHOLD? Every employer who: 1. Has a location in the city; or 2. Is doing business in the city.

WITHHOLD AT THE FOLLOWING TAX RATE: 1. For a resident of the city withhold at the resident tax rate for an employee who: a. Works in the city; or b. Works outside the city but is not subject to withholding for the city where they work.

2. For a resident of the city working another city levying a city income tax: a. Calculate the amount to withhold at the resident tax rate on all wages paid to the employee; b. Calculate the amount of tax to withhold on the employee’s wages subject to withholding by the

other city; c. Subtract the lesser of the actual tax withheld from the employee in step b or one-half of the tax

calculated in step a from the amount of withholding calculated in step a. d. The amount calculated in step c is the amount to withhold for the employee’s city of residence.

3. For a nonresident of the city withhold at the nonresident tax rate on wages paid to the employee for work performed in the city.

2016 W-2 FORMS WILL BE ACCEPTED VIA ELECTRONIC MEDIA (CD-ROM). FOR SPECIFICATIONS AND INFORMATION REGARDING ELECTRONIC MEDIA FILING, GO TO THE CITY’S WEBSITE FOR INSTRUCTIONS.

QUESTIONS?CALL

(616) 456-4083 OR VISIT

www.grcity.us/taxforms

MAIL TO:

RETURN TO: GRAND RAPIDS INCOME TAX} PO BOX 347 GRAND RAPIDS, MI 49501-0347

City of Grand Rapids Income Tax Department

2016 INCOME TAX WITHHOLDING FORMS AND INSTRUCTIONS

THIS BOOKLET CONTAINS THE FOLLOWING FORMS AND INSTRUCTIONS:

A. Notice of Change or Discontinuance (Form GR-6-IT). B. Employer’s Monthly Deposit of Income Tax Withheld, Form GR-501 (used for making monthly

deposit of tax withheld for the first or second month of a quarter). C. Employer’s Quarterly Return of Income Tax Withheld, Form GR-941 (used to report income tax

withheld during the quarter not previously deposited for the first or second month of the quarter). D. Employers Annual Reconciliation of Income Tax Withheld, Form CFW-3. The reconciliation must

be filed on or before the last day of February of the subsequent tax year. E. Instructions for Form GR-501, Employer’s Monthly Deposit of Income Tax Withheld, and Form

GR-941, Employer’s Quarterly Return of Income Tax Withheld. F. Penalty and Interest Worksheet. The city requires monthly deposit for the first and/or second month of a quarter when the total amount of tax withheld for the city during the month exceeds $100.00 and quarterly deposit of all tax withheld during the quarter not deposited during the first or second month of the quarter.

IF TAX WITHHELD DURING A MONTH EXCEEDS $100 MONTHLY DEPOSITS, FORM GR-501, ARE DUE AS FOLLOWS:

MONTH DUE DATE MONTH DUE DATE

JANUARY 02/28/2016 JULY 08/31/2016FEBRUARY 03/31/2016 AUGUST 09/30/2016

APRIL 05/31/2016 OCTOBER 11/30/2016MAY 06/30/2016 NOVEMBER 12/31/2016

QUARTERLY RETURNS, FORM GR-941, ARE DUE AS FOLLOWS:

QUARTER DUE DATE QUARTER DUE DATE

FIRST 04/30/2016 THIRD 10/31/2016SECOND 07/31/2016 FOURTH 01/31/2017

When the due date of a deposit or return falls on Saturday, Sunday or holiday the due date is automatically extended to the next business day. PREPARING W-2 FORMS – IF FORM W-2, BOX 20 IS LEFT BLANK OR DOES NOT CLEARLY IDENTIFY THE LOCALITY NAME, YOUR EMPLOYEE WILL EXPERIENCE A DELAY IN THE PROCESSING OF THEIR RETURN. THE ABBREVIATION FOR LOCALITY NAME IN BOX 20 IS MIGRR.

GRAND RAPIDS GR-6-IT

Income Tax Department Rev. 11/16/2014

NOTICE OF CHANGE OR DISCONTINUANCE

ACCOUNT NUMBER (FEIN)

CHANGES EFFECTIVE ON (Date)

CURRENT LEGAL NAME

CHANGE LEGAL NAME TO:

DBA

CHANGE DBA TO:

CURRENT LEGAL BUSINESS ADDRESS

CHANGE LEGAL BUSINESS ADDRESS TO:

MAILING ADDRESS

CHANGE MAILING ADDRESS TO:

Instructions: Place an “X” in all boxes that apply. Complete all information for the change. Write any comments or explanations on back of form.

1. The Internal Revenue Service assigned us Federal Employer Identification Number:

2. Our Federal Employer Identification Number is wrong. The correct number is:

3. We have incorporated. Our corporate name is:

4. Our new corporate Federal Employer Identification Number is:

5. Discontinue our withholding tax registration:

a. We no longer have any business activity in the City of GRAND RAPIDS.

b. We closed our business on:

c. We sold our entire business on:

e. We sold our business to:

d. We sold part of our business on:

Their FEIN is:

6. Address and phone number where we may be reached following discontinuance of business:

Contact person Street address City State Zip Code Phone no.

7. Change in ownership. (Please explain on back)

8. Effective , we changed our fiscal year ending from to Month/Year Month Month 9. Other changes. (Please explain on back SIGNATURE OF PREPARER PRINTED NAME OF PREPARER DATE PREPARED PREPARER’S PHONE NUMBER

( ) MAIL TO: GRAND RAPIDS INCOME TAX DPT. PO BOX 347, GRAND RAPIDS, MI 49501-0347

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 01MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » JAN 2016 02/28/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE FIRST MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694101M

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 02MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » FEB 2016 03/31/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE SECOND MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694102M

GR-941 GRAND RAPIDS INCOME TAX DEPARTMENT 941 01QEMPLOYER'S QUARTERLY RETURN OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » 1ST QTR 2016 04/30/2016TAXPAYER QUARTERLY DEPOSIT REQUIRED

FOR BALANCE OF TAX WITHHELD DURING QUARTER THAT WAS NOT DEPOSITED FOR FIRST OR SECOND MONTH OF QUARTER

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694101Q

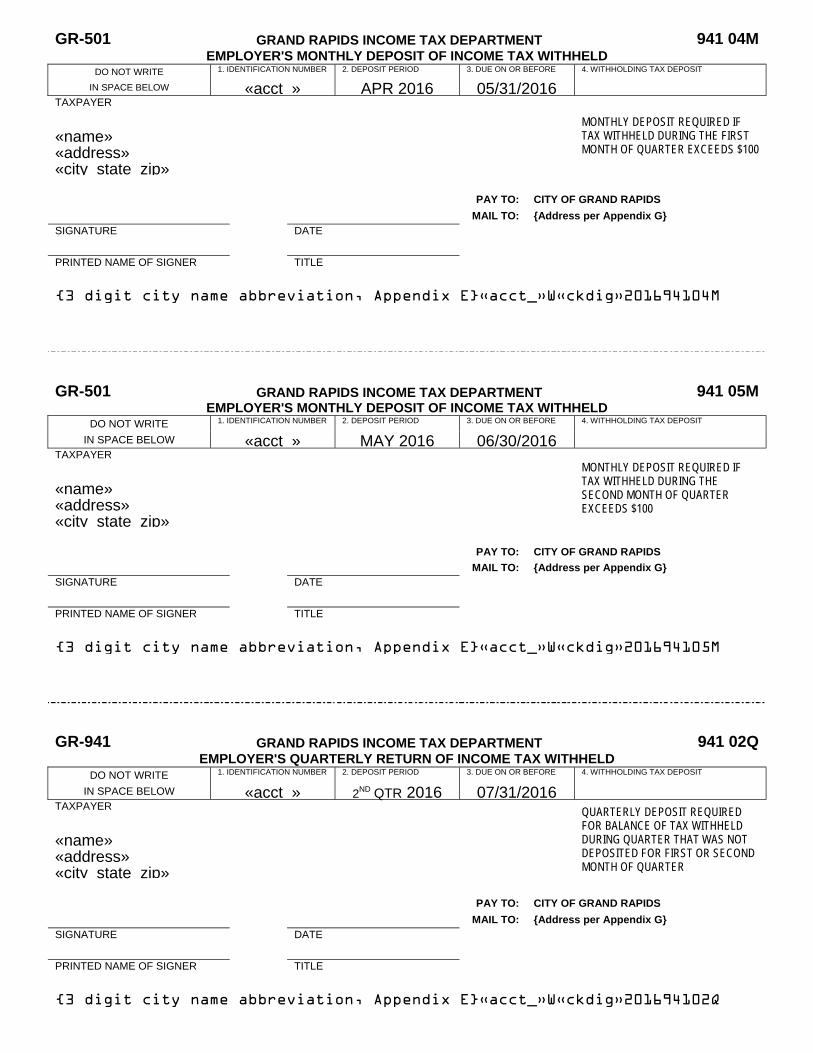

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 04MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » APR 2016 05/31/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE FIRST MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694104M

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 05MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » MAY 2016 06/30/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE SECOND MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G} SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694105M

GR-941 GRAND RAPIDS INCOME TAX DEPARTMENT 941 02QEMPLOYER'S QUARTERLY RETURN OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » 2ND QTR 2016 07/31/2016TAXPAYER QUARTERLY DEPOSIT REQUIRED

FOR BALANCE OF TAX WITHHELD DURING QUARTER THAT WAS NOT DEPOSITED FOR FIRST OR SECOND MONTH OF QUARTER

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694102Q

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 07MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » JUL 2016 08/31/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE FIRST MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694107M

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 08MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » AUG 2016 09/30/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE SECOND MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694108M

GR-941 GRAND RAPIDS INCOME TAX DEPARTMENT 941 03QEMPLOYER'S QUARTERLY RETURN OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » 3RD QTR 2016 10/31/2016TAXPAYER

QUARTERLY DEPOSIT REQUIRED FOR BALANCE OF TAX WITHHELD DURING QUARTER THAT WAS NOT DEPOSITED FOR FIRST OR SECOND MONTH OF QUARTER

«name» «address» «city_state_zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G} SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694103Q

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 10MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » OCT 2016 11/30/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE FIRST MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694110M

GR-501 GRAND RAPIDS INCOME TAX DEPARTMENT 941 11MEMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » NOV 2016 12/31/2016TAXPAYER

MONTHLY DEPOSIT REQUIRED IF TAX WITHHELD DURING THE SECOND MONTH OF QUARTER EXCEEDS $100

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G}

SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694111M

GR-941 GRAND RAPIDS INCOME TAX DEPARTMENT 941 04QEMPLOYER'S QUARTERLY RETURN OF INCOME TAX WITHHELD

DO NOT WRITE 1. IDENTIFICATION NUMBER 2. DEPOSIT PERIOD 3. DUE ON OR BEFORE 4. WITHHOLDING TAX DEPOSIT

IN SPACE BELOW «acct » 4TH QTR 2016 01/31/2017TAXPAYER QUARTERLY DEPOSIT REQUIRED

FOR BALANCE OF TAX WITHHELD DURING QUARTER THAT WAS NOT DEPOSITED FOR FIRST OR SECOND MONTH OF QUARTER

«name» «address» «city state zip»

PAY TO: CITY OF GRAND RAPIDS

MAIL TO: {Address per Appendix G} SIGNATURE DATE

PRINTED NAME OF SIGNER TITLE

{3 digit city name abbreviation, Appendix E}«acct_»W«ckdig»201694104Q

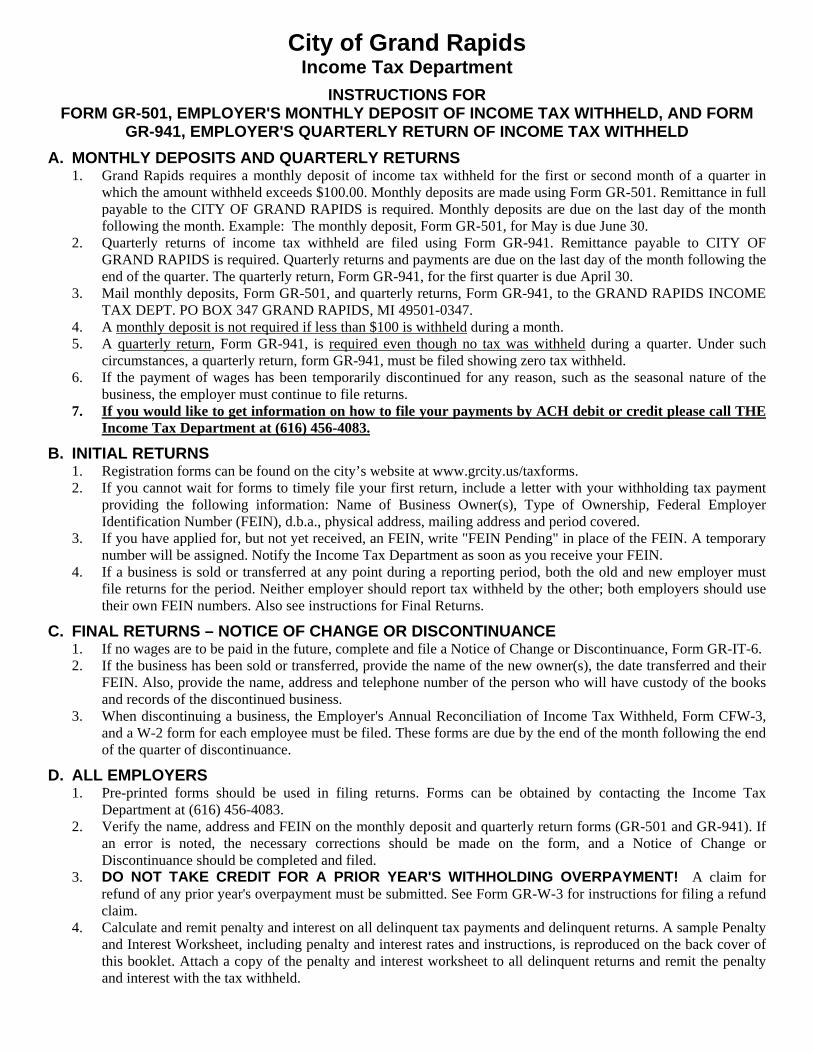

City of Grand Rapids Income Tax Department

INSTRUCTIONS FOR

FORM GR-501, EMPLOYER'S MONTHLY DEPOSIT OF INCOME TAX WITHHELD, AND FORM GR-941, EMPLOYER'S QUARTERLY RETURN OF INCOME TAX WITHHELD

A. MONTHLY DEPOSITS AND QUARTERLY RETURNS 1. Grand Rapids requires a monthly deposit of income tax withheld for the first or second month of a quarter in

which the amount withheld exceeds $100.00. Monthly deposits are made using Form GR-501. Remittance in full payable to the CITY OF GRAND RAPIDS is required. Monthly deposits are due on the last day of the month following the month. Example: The monthly deposit, Form GR-501, for May is due June 30.

2. Quarterly returns of income tax withheld are filed using Form GR-941. Remittance payable to CITY OF GRAND RAPIDS is required. Quarterly returns and payments are due on the last day of the month following the end of the quarter. The quarterly return, Form GR-941, for the first quarter is due April 30.

3. Mail monthly deposits, Form GR-501, and quarterly returns, Form GR-941, to the GRAND RAPIDS INCOME TAX DEPT. PO BOX 347 GRAND RAPIDS, MI 49501-0347.

4. A monthly deposit is not required if less than $100 is withheld during a month. 5. A quarterly return, Form GR-941, is required even though no tax was withheld during a quarter. Under such

circumstances, a quarterly return, form GR-941, must be filed showing zero tax withheld. 6. If the payment of wages has been temporarily discontinued for any reason, such as the seasonal nature of the

business, the employer must continue to file returns. 7. If you would like to get information on how to file your payments by ACH debit or credit please call THE

Income Tax Department at (616) 456-4083. B. INITIAL RETURNS

1. Registration forms can be found on the city’s website at www.grcity.us/taxforms. 2. If you cannot wait for forms to timely file your first return, include a letter with your withholding tax payment

providing the following information: Name of Business Owner(s), Type of Ownership, Federal Employer Identification Number (FEIN), d.b.a., physical address, mailing address and period covered.

3. If you have applied for, but not yet received, an FEIN, write "FEIN Pending" in place of the FEIN. A temporary number will be assigned. Notify the Income Tax Department as soon as you receive your FEIN.

4. If a business is sold or transferred at any point during a reporting period, both the old and new employer must file returns for the period. Neither employer should report tax withheld by the other; both employers should use their own FEIN numbers. Also see instructions for Final Returns.

C. FINAL RETURNS – NOTICE OF CHANGE OR DISCONTINUANCE 1. If no wages are to be paid in the future, complete and file a Notice of Change or Discontinuance, Form GR-IT-6. 2. If the business has been sold or transferred, provide the name of the new owner(s), the date transferred and their

FEIN. Also, provide the name, address and telephone number of the person who will have custody of the books and records of the discontinued business.

3. When discontinuing a business, the Employer's Annual Reconciliation of Income Tax Withheld, Form CFW-3, and a W-2 form for each employee must be filed. These forms are due by the end of the month following the end of the quarter of discontinuance.

D. ALL EMPLOYERS 1. Pre-printed forms should be used in filing returns. Forms can be obtained by contacting the Income Tax

Department at (616) 456-4083. 2. Verify the name, address and FEIN on the monthly deposit and quarterly return forms (GR-501 and GR-941). If

an error is noted, the necessary corrections should be made on the form, and a Notice of Change or Discontinuance should be completed and filed.

3. DO NOT TAKE CREDIT FOR A PRIOR YEAR'S WITHHOLDING OVERPAYMENT! A claim for refund of any prior year's overpayment must be submitted. See Form GR-W-3 for instructions for filing a refund claim.

4. Calculate and remit penalty and interest on all delinquent tax payments and delinquent returns. A sample Penalty and Interest Worksheet, including penalty and interest rates and instructions, is reproduced on the back cover of this booklet. Attach a copy of the penalty and interest worksheet to all delinquent returns and remit the penalty and interest with the tax withheld.

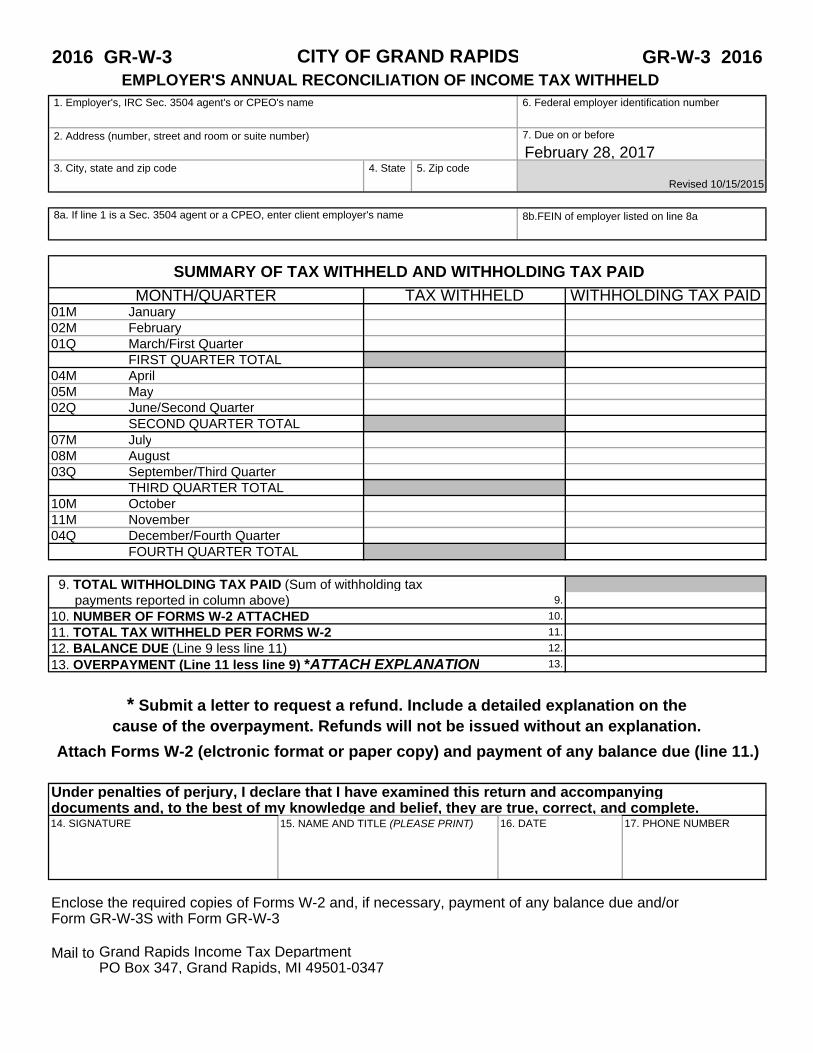

2016 GR-W-3 GR-W-3 2016

1. Employer's, IRC Sec. 3504 agent's or CPEO's name 6. Federal employer identification number

2. Address (number, street and room or suite number) 7. Due on or before

February 28, 2017 3. City, state and zip code 4. State 5. Zip code

Revised 10/15/2015

8a. If line 1 is a Sec. 3504 agent or a CPEO, enter client employer's name 8b.FEIN of employer listed on line 8a

01M January 02M February01Q March/First Quarter

FIRST QUARTER TOTAL04M April05M May02Q June/Second Quarter

SECOND QUARTER TOTAL 07M July08M August03Q September/Third Quarter

THIRD QUARTER TOTAL10M October11M November04Q December/Fourth Quarter

FOURTH QUARTER TOTAL

9. TOTAL WITHHOLDING TAX PAID (Sum of withholding tax X payments reported in column above) 9.

10. NUMBER OF FORMS W-2 ATTACHED 10.

11. TOTAL TAX WITHHELD PER FORMS W-2 11.

12. BALANCE DUE (Line 9 less line 11) 12.

13. OVERPAYMENT (Line 11 less line 9) *ATTACH EXPLANATION 13.

Under penalties of perjury, I declare that I have examined this return and accompanying documents and, to the best of my knowledge and belief, they are true, correct, and complete.14. SIGNATURE 15. NAME AND TITLE (PLEASE PRINT) 16. DATE 17. PHONE NUMBER

Enclose the required copies of Forms W-2 and, if necessary, payment of any balance due and/or Form GR-W-3S with Form GR-W-3

Mail to Grand Rapids Income Tax DepartmentPO Box 347, Grand Rapids, MI 49501-0347

EMPLOYER'S ANNUAL RECONCILIATION OF INCOME TAX WITHHELD

SUMMARY OF TAX WITHHELD AND WITHHOLDING TAX PAID

Attach Forms W-2 (elctronic format or paper copy) and payment of any balance due (line 11.)

CITY OF GRAND RAPIDS

WITHHOLDING TAX PAIDTAX WITHHELDMONTH/QUARTER

* Submit a letter to request a refund. Include a detailed explanation on the cause of the overpayment. Refunds will not be issued without an explanation.

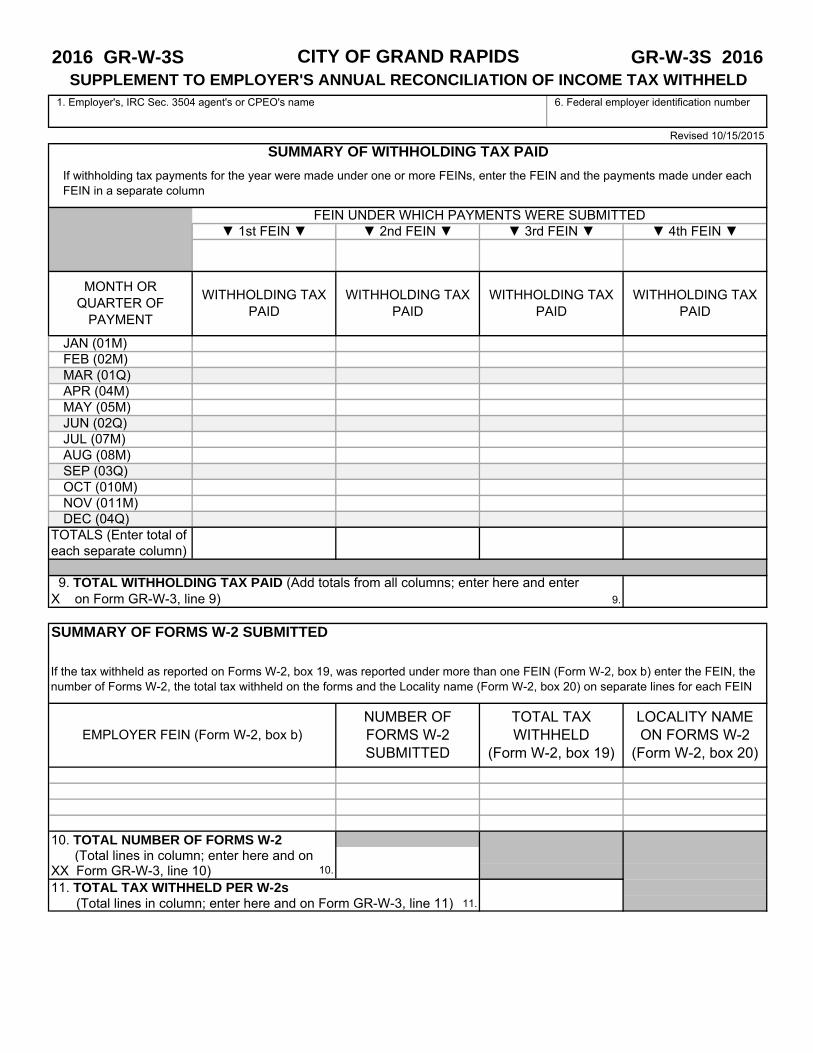

2016 GR-W-3S GR-W-3S 2016

1. Employer's, IRC Sec. 3504 agent's or CPEO's name 6. Federal employer identification number

Revised 10/15/2015

9. TOTAL WITHHOLDING TAX PAID (Add totals from all columns; enter here and enter X on Form GR-W-3, line 9) 9.

SUMMARY OF FORMS W-2 SUBMITTED

10. TOTAL NUMBER OF FORMS W-2 X (Total lines in column; enter here and on XX Form GR-W-3, line 10) 10.

11. TOTAL TAX WITHHELD PER W-2sXX (Total lines in column; enter here and on Form GR-W-3, line 11) 11.

EMPLOYER FEIN (Form W-2, box b)

CITY OF GRAND RAPIDSSUPPLEMENT TO EMPLOYER'S ANNUAL RECONCILIATION OF INCOME TAX WITHHELD

SUMMARY OF WITHHOLDING TAX PAID

If withholding tax payments for the year were made under one or more FEINs, enter the FEIN and the payments made under each FEIN in a separate column

FEIN UNDER WHICH PAYMENTS WERE SUBMITTED ▼ 3rd FEIN ▼ ▼ 4th FEIN ▼▼ 1st FEIN ▼ ▼ 2nd FEIN ▼

MONTH OR QUARTER OF

PAYMENT

WITHHOLDING TAX PAID

WITHHOLDING TAX PAID

WITHHOLDING TAX PAID

WITHHOLDING TAX PAID

JAN (01M)FEB (02M)MAR (01Q)APR (04M)MAY (05M)JUN (02Q)JUL (07M)AUG (08M)SEP (03Q)OCT (010M)NOV (011M)DEC (04Q)

TOTALS (Enter total of each separate column)

NUMBER OF FORMS W-2 SUBMITTED

TOTAL TAX WITHHELD

(Form W-2, box 19)

LOCALITY NAME ON FORMS W-2

(Form W-2, box 20)

If the tax withheld as reported on Forms W-2, box 19, was reported under more than one FEIN (Form W-2, box b) enter the FEIN, the number of Forms W-2, the total tax withheld on the forms and the Locality name (Form W-2, box 20) on separate lines for each FEIN

CITY OF GRAND RAPIDS INCOME TAX DEPARTMENT INSTRUCTIONS FOR

FORM GR-W-3, EMPLOYERS ANNUAL RECONCILIATION OF INCOME TAX WITHHELD AND FORM GR-W-3S, SUPPLEMENT TO EMPLOYERS ANNUAL RECONCILIATION OF INCOME TAX WITHHELD

Revised 10/15/2015

Page 1 of 2

GENERAL INSTRUCTIONS Employers withholding city income tax are required to annually reconcile the city income tax withheld to the city income tax withholding paid. Form GR-W-3, Employer’s Annual Reconciliation of Income Tax Withheld, is the form used to make this reconciliation. A copy of each Form W-2 issued by the employer is required to be filed with Form GR-W-3. Electronic filing of Forms W-2 via CD-ROM or DVD is allowed by some cities. Refer to the city’s website for information about acceptance of electronic filing of Forms W-2 and the Form W-2 file formats accepted by the city. Forms W-2 cannot be submitted in PDF format.

IRC Sec. 3405 Agent An employer’s withholding agent under Internal Revenue Code (IRC) Sec. 3405 must also become the employer’s withholding agent for the city. This is accomplished by the Employer and the IRC Sec. 3405 withholding agent filing Form GR-2678, Employer/Payor Appointment of Agent with the city. This type of withholding agent files city income tax Form GR-W-3 and the associated Forms W-2 under the withholding agent’s federal employer identification number (FEIN). When filing Form GR-W-3 with the city, the reporting agent shall report the employer’s name and FEIN on Form GR-W-3. A non-certified professional employer organization (PEO) may be an IRC Sec. 3405 reporting agent.

Certified Professional Employer Organization (CPEO) Starting in year 2016, a PEO may be certified under IRC Sec. 3511(a)(1). A CPEO becomes the co-employer of record responsible for city income tax withholding and must register with the city by filing Form GR-SS-4, Employer’s Withholding Registration. The CPEO must file Form GR-W-3 and associated Forms W-2 under their FEIN. When filing Form GR-W-3 with the city, the CPEO shall report the employer’s name and FEIN on Form GR-W-3.

Common Paymaster A common paymaster must file Form GR-W-3 and associated Forms W-2 under the same FEIN as the one used on the federal Forms W-3 and W-2.

Filing Form GR-W-3 Withholding Payments Made Under More Than One FEIN. When withholding tax paid was reported to the city under more than one FEIN, Form GR-W-3S, Employer’s Annual Reconciliation of Income Tax Withheld, must be filed with Form GR-W-3. Form GR-W-3S, Summary of Withholding Tax Paid section identifies all FEIN’s under which withholding tax payments were made and the month or quarter of each payment. The form totals the withholding tax payments made under each FEIN and

the totals all of the withholding tax payments made on line 9, The total of all withholding tax payments are also entered on Form GR-W-3, line 9.

Tax Withheld on Forms W-2, Box 19, Reported under More Than One FEIN (Form W-2, box b) When the Forms W-2 filed with Form GR-W-3 report more than one employer FEIN in Form W-2, box b, Form GR-W-3S must be filed with Form GR-W-3. Form GR-W-3S identifies all FEINs under which Forms W-2 were filed, the number of Forms W-2 filed under each FEIN and the locality name reported, Forms W-2, box 20.

SPECIFIC INSTRUCTIONS FOR FORM GR-W-3 Line 1. Enter the name of the employer, IRC Sec. 3504 agent or CPEO.

Line 2. Enter the street address including suite or room number of the person named on line 1.

Lines 3, 4 and 5. Enter the city, state and zip code under the respective line number.

Line 6. Enter FEIN of the person named on line 1.

Line 7. Enter the due date if not already preprinted.

Line 8. If the entry on line 1 is an IRS Sec. 3504 agent or a CPEO, enter the employer’s or co-employer’s FEIN

Summary of withholding tax paid section. Under this section report the actual tax withheld each month and the withholding tax deposits and payment made each month or quarter. If withholding tax payments were made under FEIN’s in addition to the one reported on line 6, write across this section “SEE FORM GR-W-3S and complete the Summary of Withholding Tax Paid section of Form GR-W-3S.

Line 9. Enter the total withholding tax paid from the lines above or if withholding tax was paid under more than one number, the total from form GR-W-3S, line 9.

Line 10. Enter the number of Forms W-2 attached to this form or if Forms W-2 were filed under more than one FEIN, enter the total from Form GR-W-3S, line 11.

Line 11. Enter the total tax withheld as reported on the attached Forms W-2 or if Forms W-2 were filed under FEINs other than the one reported on line 6, enter the total from Form GR-W-3S, line 11.

Forms W-2 must be submitted with Form GR-W-3. The preferred format is the federal EFW2 format. The city tax proprietary (CTP) format may also be used. Electronic format Form W-2 data must be submitted on CD-ROM or DVD. See Appendix K for specifications. Forms W-2 cannot be submitted in PDF format. Paper copies of the actual Forms W-2 are acceptable. A listing, summary or printout of Form W-2 data will not be accepted.

CITY OF GRAND RAPIDS INCOME TAX DEPARTMENT INSTRUCTIONS FOR

FORM GR-W-3, EMPLOYERS ANNUAL RECONCILIATION OF INCOME TAX WITHHELD AND FORM GR-W-3S, SUPPLEMENT TO EMPLOYERS ANNUAL RECONCILIATION OF INCOME TAX WITHHELD

Revised 10/15/2015

Page 2 of 2

Submit only Forms W-2 for employees subject to the city’s income tax and Forms W-2 reporting city tax withheld for the city. Form W-2, box 20, data should only be an authorized locality name abbreviation. See Appendix D for a listing of authorized locality name abbreviations.

Line 12. Enter the balance due, line 9 less line 11. If no balance due enter a zero (0). The balance due must be paid full with Form GR-W-3.

Line 13. Enter any overpayment, line11 less line 9. If no overpayment, enter a zero (0). A refund of any overpayment will not be made unless a letter explaining the overpayment and requesting the refund is submitted with Form GR-W-3.

Line 14. Have the individual responsible for preparing Form GR-W-3 sign the return on line 14.

Line 15. Type or print the name and title of the individual signing the return on line 14.

Line 16. Enter the date the reconciliation was signed.

Line 17. Enter the phone number of the individual signing the return.

After Form GR-W-3 is completed, please double check the entries on lines 1 through 6. Also, if Form GR-W-3 is submitted by a Sec 3504 agent or a CPEO, check the employer’s name and FEIN reported for the employer on lines 8a and 8b.

Filing Form GR-W-3 Mail the completed Form GR-W-3 along with the Forms W-2, payment of any tax due, a letter explaining any overpayment and requesting a refund if necessary and Form GR-W-3S if necessary to: Grand Rapids Income Tax Department PO Box 347, Grand Rapids, MI 49501-0347

SPECIFIC INSTRUCTIONS FOR FORM GR-W-3S Line 1. On line one, enter the name as stated on Form GR-W-3 line 1.

Line 6. Enter the FEIN of the person named on line 1.

Summary of Withholding Tax Paid Complete this section only when withholding tax was paid to the city under more than one FEIN. Use a separate column to report withholding tax paid under each FEIN by listing the FEIN of the payor and the payments on the line for the corresponding month or quarter. Enter the total withholding tax paid under each FEIN on the totals line of the column. On line 9 enter the grand total of withholding tax paid under all FEINs. Also enter the total tax withheld on Form GR-W-3, line 9.

Summary of Forms W-2 submitted Complete this section only when Forms W-2, filed with Form GR-W-3, report more than one FEIN in box b. Use a separate line for each FEIN reported on Form W-2, box b. In the related column for each line enter the FEIN, the number of Forms W-2 filed under the FEIN, the total tax withheld under the FEIN and the abbreviation for the locality name of the city which for Grand Rapids is MIGRR. The abbreviation of MI-GRR is also acceptable for printed paeer W-2 forms only.

Line 10. Total the number of forms W-2 listed in this column and enter the total on line 10. Also enter this total on Form GR-W-3, line 10.

Line 11. Total the amount of tax withheld listed in this column and enter the total on line 11. Also enter this total on Form GR-W-3, line 11.

Complete the reconciliation process by completing Form GR-W-3, lines 12 through 17. Submit this Form GR-W-3 along with Form GR-W-3 and the related forms W-2.

DISCLAIMER NOTICE These instructions are interpretations of the Uniform City Income Tax Ordinance, MCLA 141.601 et seq. The Grand Rapids Income Tax Ordinance will prevail in any disagreement between these instructions and the ordinance.

CITY OF GRAND RAPIDS INCOME TAX DEPARTMENT

PENALTY AND INTEREST WORKSHEET

FOR DELINQUENT WITHHOLDING TAX RETURNS

RETURN PERIOD DUE DATE TAX DUE INTEREST PENALTY MINIMUM P & I TOTAL DUE

Attach a copy of completed worksheet to each delinquent return. INTEREST CALCULATION INSTRUCTIONS: Interest is due from the due date of a return until the tax is paid. Interest Rates: For period 1/1/2012 through 12/31/2012 the interest rate is 4.25% per year or 0.0001161 per day. For period 1/1/2013 through 12/31/2013 the interest rate is 4.25% per year or 0.0001164 per day. For period 1/1/2014 through 12/30/2014 the interest rate is 4.25% per year or 0.0001164 per day. For period 1/1/2015 through 12/31/2015 the interest rate is 4.25% per year or 0.0001164 per day. For period 1/1/2016 through 12/31/2016 use the interest rate listed for 2015 or the city for rate. Interest rates are set by the Michigan Department of Treasury. The interest rate changes every six months. Interest

rates for current or past periods are found on the Michigan Department of Treasury web site, http://www.michigan.gov/treasury under Revenue Administrative Bulletins. Look for the most recent interest rate bulletin.

Interest Computation: For Interest Rate Period: 1/1/2012 to 12/31/2012: Number of days after due date: _____ times 0.0001161 times tax due = $_________ 1/1/2013 to 12/31/2013: Number of days after due date: _____ times 0.0001164 times tax due = $_________ 1/1/2014 to 12/31/2014: Number of days after due date: _____ times 0.0001164 times tax due = $_________ 1/1/2015 to 12/31/2015: Number of days after due date: _____ times 0.0001164 times tax due = $_________ 1/1/2016 to 12/31/2016: Number of days after due date: _____ times 0.0001164 times tax due = $_________ Total interest. Add the interest calculated on the lines above and Enter on the INTEREST line of the worksheet. Total Interest $_________ PENALTY CALCULATION INSTRUCTIONS: Penalty is due upon failure to timely file a return or failure to timely pay tax due. Penalty Rate: One percent (1%) of the tax due per month (or portion thereof) per return. A penalty of one percent of the tax due is applied on the first day after the due date of the return. An additional penalty of one percent of the tax due is added on the first day of each subsequent month. Maximum penalty is 25% of the tax due per return. Penalty Computation: Number of months delinquent times 1% (.01) times the tax due = $_________ Enter the penalty calculated on the PENALTY line of the worksheet. MINIMUM PENALTY AND INTEREST CALCULATION: The minimum amount of penalty and interest combined is $2.00 per return. Calculation of minimum penalty and interest: If total penalty and interest is greater than $2.00 minimum does not apply. If total penalty and interest is less than $2.00, enter $2.00 on the MINIMUM P & I line of the worksheet.

Part I. Identification and addresses of employer or certified professional employer organization 1. Employer application 2. Certified professional employer organization (CPEO) co-employer application

3. Complete company name (include, if applicable, Corp., Inc., LLC, etc.) 4. Federal Employer Identification Number

5. Business name, assumed name or DBA (if used) 6. Business phone number

7. Enter street number and name (include apartment or suite number after street name)

8. Enter Address Line 2:

9. City 10. State 11. Zip Code

12. Enter street number and name (include apartment or suite number after street name)

13. Enter Address Line 2:

14. City 15. State 16. Zip Code

17. Enter street number and name (include apartment or suite number after street name)

18. Enter Address Line 2:

19. City 20. State 21. Zip Code

Part II. General information 1. Date first wages subject to city withholding paid 1a. 7. Reinstated old business; enter old FEIN7a.

2. Number of employees subject to city withholding 2a. 8. Started "doing business" in city; enter date 8a.

3. Reasons for filing withholding registration 9. CPEO with new client in the city. Enter client's FEIN on line 11a and

4. Started a new business; enter date 4a. complete items 11 and 12 below 9a.

5. Incorporated an existing busines 10. Other (explain) 10a.

6. Purchased a going business (complete items 11 and 12 below)

11. Name of previous owner or PEO's client 12. Will the previous owner or PEO's client continue to 12a. Yes

x have employees subject to city income tax withholding 12b. No

13. Does your tax year end in December 31

13a. Yes 13b. No If no, provide the fiscal year end month and day 13c.

Part. III. Income tax withholding - Filing and payment of income tax withheld Check box below to indicate how withholding tax returns are prepared and filed

1. Our withholding tax returns are prepared in house, filed and paid 5. An IRC Section 3504 agent is authorized to prepare, file and pay

X and all returns and Forms W-2 are filed and paid under our FEIN X our withholding tax returns and Forms W-2; all withholding tax

2. A common paymaster prepares our withholding tax returns: X returns and Forms W-2 are filed under the agents FEIN. Attach a

X Withholding tax is paid under FEIN 2a. X copy of federal Form 2678. ATTACH A COMPLETED FORM

X Forms W-2 are filed under FEIN 2b. X CF-2678 AS A PART OF THIS REGISTRATION

3. A payroll services provider prepares our withholding tax returns 6. A professional employer organization is authorized under a PEO

X and Forms W-2. Returns and Forms W-2 are filed and paid under X agreement to prepare, file and pay our withholding tax returns

X our FEIN X and Forms W-2 under their FEIN. Attach a copy of the PEO

4. A payroll reporting agent is authorized to prepare our withholding X agreement. A certified PEO must be registered with the city as a

X tax returns and Forms W-2 which are filed and paid by the agent X co-employer liable for filing and payment of withholding tax

X under our FEIN. Attach a copy of Form 8655 filed with the IRS. 7. We are a CPEO preparing, filing and paying or clients city

X ATTACH A COMPLETED FORM CF-8655 AS PART OF THIS X withholding tax under our FEIN. Attach a copy of the IRS

X REGISTRATION X certification.

Month (MM) Day (DD)

PHYSICAL ADDRESS OF PROJECT OR

ACTIVITY IN CITY

LEGAL ADDRESS

MAILING ADDRESS

Employer’s Withholding Registration

GR-SS-4

PLEASE TYPE OR PRINT

GR-SS-4

PLEASE TYPE OR PRINT

INCOME TAX DEPARTMENTCity of Grand Rapids

Complete company name (include, if applicable, Corp., Inc., LLC, etc.) Federal Employer Identification Number

Part IV. Type of business ownership (Check all boxes that apply) 1. Individual/Sole Proprietorship (Identify owner in 8. Michigan Corporation (Identify all corporation officers in X Part III below) X Part III below) 2. General Partnership 8a. Michigan Subchapter S Corporation X (Identify all partners in Part III below) 8b. Michigan Professional Corporation 3. Limited Partnership (LP) 9. Foreign (Non-Michigan) Corporation (Identify all corporation X (Identify general partners in Part III below) X officers in Part III below) 4. Professional Limited Liability 9a.Foreign Subchapter S Corporation 5. Partnership (LLP) (Identify all 10. Nonprofit Corporation (Identify all corporation officers in X General Partners in Part III below) X Part III below) 6. Limited Liability Company (LLC) 11. Government X (Identify all members in Part III below) 12. Estate (Identify estate administrator or personal 7. Professional Limited Liability Company (PLLC) X representative in Part III below)X (Identify all members in Part III below) 13. Trust (Identify trustee in Part III below)

14. Other (explain)

Part V. Identification of each owner, partner, member or corporate officer (Attach Part VII if more than 2) 1a. Name (last, first middle, suffix) 1g. Home Telephone Number

1b. Business Title 1h. Date of Birth

1c. Residence Address (street number and name including apartment number after street name) 1i. Social Security Number

1d. City 1e. State 1f. Zip Code 1j. Drivers License Number/ ST ID Number

2a. Name (last, first middle, suffix) 2g. Home Telephone Number

2b. Business Title 2h. Date of Birth

2c. Residence Address (street number and name including apartment number after street name) 2i. Social Security Number

2d. City 2e. State 2f. Zip Code 2j. Drivers License Number/ ST ID Number

Part VI. Contact information 1. Contact person for withholding tax questions 2. E-mail address of contact person

3. Phone number for contact person above. 4a.

Part VII. Signature area Under penalties of perjury, I declare that I have examined this application, and to the best of my knowledge and belief, it is true, correct, and complete. 1a. Signature (owner, member or officer who controls or is responsible for 1b. Title

X filing withholding tax returns and paying the income tax withheld)

1c. Type or print name of person signing above 1d. Date

Mail to: Grand Rapids Income Tax Dept. PO Box 347 Grand Rapids, MI 49501-0347 Form GR-SS-4, page 2, revised 11/19/2015

GR-SS-4 Questions about this application? Call the Income Tax Department at (616) 456-3415.

Information collected on this form is confidential pursuant to MCL 141.674(1), Michigan Uniform City Income Tax Ordinance; Sec.74(1). Information gained by the administrator, city treasurer or any other city official, agent or employee as a result of a return, investigation, hearing or verification required or authorized by this ordinance is confidential, except for official purposes in connection with the administration of the ordinance and except in accordance with a proper judicial order.

Complete company name (include, if applicable, Corp., Inc., LLC, etc.) Federal Employer Identification Number

Part VII. Identification of each owner, partner, member or corporate officer (Part V Continued) 3a. Name (last, first middle, suffix) 3g. Home Telephone Number

3b. Business Title 3h. Date of Birth

3c. Residence Address (street number and name including apartment number after street name) 3i. Social Security Number

3d. City 3e. State 34f. Zip Code 3j. Drivers License Number/ ST ID Number

4a. Name (last, first middle, suffix) 4g. Home Telephone Number

4b. Business Title 4h. Date of Birth

4c. Residence Address (street number and name including apartment number after street name) 4i. Social Security Number

4d. City 4e. State 4f. Zip Code 4j. Drivers License Number/ ST ID Number

5a. Name (last, first middle, suffix) 5g. Home Telephone Number

5b. Business Title 5h. Date of Birth

5c. Residence Address (street number and name including apartment number after street name) 5i. Social Security Number

5d. City 5e. State 5f. Zip Code 5j. Drivers License Number/ ST ID Number

6a. Name (last, first middle, suffix) 6g. Home Telephone Number

6b. Business Title 6h. Date of Birth

6c. Residence Address (street number and name including apartment number after street name) 6i. Social Security Number

6d. City 6e. State 6f. Zip Code 6j. Drivers License Number/ ST ID Number

7a. Name (last, first middle, suffix) 7g. Home Telephone Number

7b. Business Title 7h. Date of Birth

7c. Residence Address (street number and name including apartment number after street name) 7i. Social Security Number

7d. City 7e. State 7f. Zip Code 7j. Drivers License Number/ ST ID Number

8a. Name (last, first middle, suffix) 8g. Home Telephone Number

8b. Business Title 8h. Date of Birth

8c. Residence Address (street number and name including apartment number after street name) 8i. Social Security Number

8d. City 8e. State 8f. Zip Code 8j. Drivers License Number/ ST ID Number

Form GR-SS-4, page 3, revised 09/29/2015