2015 program for vision bank's cle-cpe seminar · past 7 years for cle seminars sponsored by...

TRANSCRIPT

VISION BANK’S ANNUAL CLE/CPE SEMINAR SELECTED SUBJECTS FOR THE GENERAL

PRACTIONER - UPDATE FOR 2015

DATE & Ada, Oklahoma LOCATION: Friday, October 30, 2015 Pontotoc Technology Center 601 W. 33rd St., Ada, Oklahoma 74820 CLE CREDIT: This course as been submitted for approval by the Oklahoma Bar Association Mandatory Continuing Legal Education Commission for approval

of 6 hours of mandatory CLE credit, including 1 hour of ethics. TUITION: FREE COURSE – FREE BREAKFAST AND LUNCH PROGRAM: Program Planner/Moderator M. Keywood Deese, Senior Vice President & Trust Officer for Vision Bank

8:30am – Registration & Continental Breakfast & Introduction of Speakers 9:00am – 9:50am – Every Trust You Have Ever Wanted To Know About And Were Afraid To Ask! by: M. Keywood Deese, Senior Vice President & Trust Officer for Vision Bank, Ada, Oklahoma 9:50am – BREAK 10:00am – 10:50am – How Do You Define An Accounting? Let Me Count The Ways! by: Kara Greuel, J.D., CPA, CFF, CGMA, CFE, Greuel Law Firm, PLLC, Tulsa, Oklahoma 11:00am – 11:50am – It Seemed Like A Good Idea At The Time! by: Kara Greuel, J.D., CPA, CFF, CGMA, CFE, Greuel Law Firm, PLLC, Tulsa, Oklahoma - Ethics

11:50am – 1:00pm – Lunch Provided by Vision Bank Catered by Papa Gjorgio’s Italian Restaurant 1:00pm – 1:50pm – Bankruptcy Basics For The Non-Bankruptcy Practitioner by: Preston Draper, Attorney at Law, Sweeney, Draper & Christopher Law Firm, Ada, Oklahoma 2:00pm – 2:50pm – “I Didn’t Know That” – Selected Topics on Estate Planning & Administration by: James Marshall, Attorney & Partner at Henson & Marshall, PLLC, Shawnee, Oklahoma 2:50pm – BREAK 3:00pm – 3:50pm – Question and Answer Session

BIOGRAPHIES OF SPEAKERS M. Keywood Deese – Senior Vice President & Trust Officer for Vision Bank, Ada, Oklahoma: Ms. Deese has been the Senior Vice President and Trust Officer with the bank since 1987. She graduated from the University of Oklahoma with a Business Administration Degree in 1975. She obtained her Juris Doctor degree from Oklahoma City University in 1979. Before joining the bank she practiced oil and gas law in Oklahoma City, including several years as the senior oil and gas attorney for the Oklahoma Corporation Commission. She is the former Chairman of the Mineral Law Section of the Oklahoma Bar Association. Ms. Deese organized and taught CLE seminars on oil and gas related topics when she practiced law in Oklahoma City. She has been the Program Planner and Moderator for the past 7 years for CLE Seminars sponsored by Vision Bank on a variety of estate and trust issues, business and bankruptcy, real estate and mineral related topics. She is a member of the Oklahoma Bar Association, Texas Bar Association, Pontotoc County Bar Association and the American Bar Association. Kara Greuel, J.D., CPA, CFF, CFMS, CFE at Greuel Law Firm, PLLC in Tulsa, Oklahoma: Ms. Greuel’s foundation in estate and trust planning and administration began as a CPA. With over 17 years of experience in tax planning and preparation, she is able to integrate tax planning strategies in her client’s estate plans, Her experience as an executive with companies in a variety of industries, coupled with extensive experience involving regulatory compliance issues for publicly traded companies, enables her to assist clients who wish to implement business succession and estate planning. Additionally, Kara’s experience as an auditor gives her the ability to analyze and investigate matters that include allegations of fraud and embezzlement. She received Bachelor of Business Administration degrees in both Finance and Accounting from Northeastern State University and Langston University, respectively, and a Juris Doctorate degree from the University of Tulsa, College of Law. Additionally, Kara is a Certified Fraud Examiner and is a CPA with a certification in Financial Forensics. She is also a Chartered Global Management Accountant through the AICPA. Kara is a member of various professional organizations and currently serves as an officer of the Oklahoma Bar Association Estate Planning, Probate and Trust Section and the Bench and Bar Committee for the Tulsa County Bar Association. Additionally, she serves as Treasurer for both Tulsa Artists’ Coalition and the Oaks Indian Mission, Inc. Mr. Preston Draper –Partner, Sweeney, Draper & Christopher, PLLC, Ada, Oklahoma: Mr. Draper founded the Ada firm of Sweeney, Draper & Christopher, PLLC, along with his law partners Kurt Sweeney and Jason Christopher in January 2011. The firm is a full-service law firm handling family law, criminal, bankruptcy, civil suits, He is a 1991 graduate of the United States Navy’s Naval Nuclear Power School; 1999 graduate of Brigham Young University; and 2003 graduate of the University of Oklahoma College of Law in Norman. As a law student, he was the recipient of the prestigious Comfort Scholarship. He began his legal career as an Assistant Attorney General at the Oklahoma Attorney General’s Office. He is admitted to practice law in the state courts of Oklahoma, the tribal courts of the Chickasaw Nation, the federal district courts for the Eastern, Northern, and Western Districts of Oklahoma, the bankruptcy courts for the Easter and Westerns districts of Oklahoma, the United States Court of Appeals for the Tenth Circuit, and the United States Supreme

Court. He previously served two years as president of the Pontotoc County Bar Association. He is currently a member of the Pontotoc County Health Board, a member of the Ada City Council, the Municipal Judge for the Town of Roff, an adjunct professor at East Central University, and Vice President of the Ada Artists Association. James R. Marshall – Attorney at Henson & Marshall, PLLC in Shawnee, Oklahoma: James R. Marshall is a member of the firm of Henson & Marshall, PLLC in Shawnee, Oklahoma. He received a Bachelor of Arts degree from the University of Oklahoma (Phi Beta Kappa) in 1972, a Master of Arts degree (International Relations) from Creighton University in 1976, and a Juris Doctor degree from the University of Oklahoma in 1979. While in law school he served as an editor on the Oklahoma Law Review. From 1972 until 1983, he served on active duty in the United State Air Force, first as an intelligence officer and then, after being sent to law school on an Air Force program, as a Judge Advocate. He served as Chief of Military Justice at Andrews AFB, MD and as Area Defense Counsel at Tinker AFB. After leaving active duty he continued as a Judge Advocate in the Air National Guard. In 1996 he was named the Outstanding Air National Guard Judge Advocate in the United States. He served as the senior Air National Guard Judge Advocate at Air Mobility Command and Air Combat Command responsible, for operational readiness and deployment issues for guard units and personnel in those commands. He retired from the Air National Guard in 2006 at the rank of Brigadier General. He has been in the private practice of law in Shawnee since 1983 with an emphasis throughout his civilian career in the areas of real estate, estate planning, and probate.

VISION BANK’S ANNUAL CLE/CPE SEMINAR 2015 COURSE EVALUATION

OCTOBER 30, 2015 PONTOTOC TECHNOLOGY CENTER

HOW ARE WE DOING? In order to make future sessions more valuable, please submit a critique of today’s seminar. Rate the speakers in the following areas. Please mark one: Excellent (5) – to – Weak (1). Circle one number in each Category.

SPEAKER KNOWLEDGE OF SUBJECT

DELIVERY QUALITY OF MATERIALS

M. Keywood Deese, Senior Vice President & Trust Officer, Vision Bank

5 4 3 2 1 5 4 3 2 1 5 4 3 2 1

Kara Greuel, J.D., CPA, CFF, CGMA, CFE 5 4 3 2 1 5 4 3 2 1 5 4 3 2 1 Preston Draper, Attorney 5 4 3 2 1 5 4 3 2 1 5 4 3 2 1 James Marshall, Attorney 5 4 3 2 1 5 4 3 2 1 5 4 3 2 1

1. Would you like Vision Bank to do another free seminar? ___________________________ 2. What month is most convenient for you to attend Vision Bank’s seminar? ____________ 3. Suggestions for future topics and speakers: ______________________________________ ______________________________________________________________________________ COMMENTS: ________________________________________________________________ ______________________________________________________________________________ ______________________________________________________________________________

VISION BANK

DISCLAIMER

These materials, including the legal research, are the product of

individual contributors, not Vision Bank. Accordingly, any statement,

citation of authority, philosophy or opinion expressed is that of the

individual contributor, and the reader is admonished to check original

citations of authority and to use these materials as a starting point for

individual research.

Vision Bank makes no warranty, express or implied, relating to the

accuracy or content of these materials.

I. EVERY TRUST YOU HAVE EVER WANTED TO KNOW ABOUT AND

WERE AFTRAID TO ASK!

M. Keywood Deese Senior Vice President & Trust Officer

For Vision Bank 101 E. Main St.

P.O. Box 669 Ada, OK 74821

Phone: (580)-436-8311 Fax: (580) 436-8391

1

EVERY TRUST YOU EVER WANTED AND WERE AFRAID TO ASK!

By: M. Keywood Deese – Senior Vice President & Trust Officer, Vision Bank

INTRODUCTION: I have taught or attended estate planning seminars on trusts for over 30

years. Each of these seminars explained the virtues and purposes on a variety of trusts for estate

planning or tax purposes. I decided to take a different approach and try to present a list of all the

trusts I knew of, what their purposes are, who would create them, how to close them, and the key

elements that are unique to each trust.

Although there are implied or presumed trusts (see 60 Okla. Stat. §137), today we will be

addressing an expressed trust; that is, a trust created by a written document. The statutory

provisions dealing with trusts is found in Title 60, Oklahoma Statues, §131, set seq., with the

Oklahoma Trust Act appearing at Okla. Stat. Ann. Tit. 60, §175.1, et seq.

1. REVOCABLE LIVING TRUSTS:

Purpose:

A Living Trust comes into operation during the creator’s or grantor’s lifetime. This type

of trust is a private written agreement that is not made a matter of public record, like a

will is when it is filed for probate. The trust agreement will name a Trustee to be in

charge and manage the trust assets, make distributions and investments, etc. The

agreement should also name a Successor Trustee. The Trustee takes custody of

securities, wherever they are held, and performs all the troublesome accounting

paperwork that goes with owning property. Most living trusts today are revocable,

meaning they may be amended or even terminated at any time during the lifetime of the

grantor. This flexibility permits the trust’s creator (grantor) to observe how the trust

operates to meet his needs – and then to make changes accordingly. Often, a husband

and wife, as Co-Grantors, will create a joint living trust. Sometimes, however, the living

trust is made irrevocable – its terms fixed and permanent – after death or incapacity of

2

one of the grantors. The surviving grantor may not be able to amend the trust to leave

assets to his second wife or girlfriend!

Grantor:

Anyone wanting to avoid probate proceedings and keep their estate plans confidential

will find that this type of trust solves many estate planning issues.

Special Provisions:

This type of trust can close at the death of the grantor, only after the medical, funeral or

other bills have been paid. There is no protection from creditors in a living trust. A

creditor can still satisfy a judgement against the grantor of the trust, from the assets of the

trust (60 Okla. Stat. §175.25H). The Trustee will plan how and which assets to distribute

to the next beneficiaries according to the terms of the trust. The Trustee should get

signed releases from each beneficiary, acknowledging the assets they received, agreeing

to the distribution plan presented by the Trustee and acknowledging a final accounting.

The release should place the final income tax liability, for the year the trust closes, on the

beneficiaries receiving the assets.

Helpful Hint on Closing the Living Trust:

(1.) Cost Basis of Distributed Assets - After the original grantor passes away, the Trustee

will be distributing the stocks, bonds, real estate, etc… to the next group of beneficiaries

and close the trust. The trustee should make sure of the cost basis for each type of asset

is provided to each beneficiary in a well organized schedule. This keeps the beneficiary

from calling the Trustee years later, when the beneficiary sells the stock or real estate,

needing to know the cost basis of the asset he sold. This schedule can be provided to the

beneficiary’s broker who received who received his share of the stocks and/or his CPA.

(2.) Closing the Home and Transfer of Contents - It can be a very challenging project to

close the Grantor’s home and distribute his/her personal property to the beneficiaries.

These issues should be reviewed carefully by the Trustee before accepting the trust and

hopefully before the Grantor signs the trust agreement. The more specific the grantor can

be about “which beneficiary is to receive specific pieces of furniture, jewelry, antiques,

3

artwork, or gun collection”, the better it will be for the Trustee at the time of distribution.

If not done well, this can be the first family fight!

Unusual Provisions:

Revocable Living Trusts do not have to completely terminate at the grantor’s death.

Instead, the trust may provide that a new “sub-trust” be created from the remaining trust

assets and be transferred into a new trust. This new trust will have a new name and new

tax id number. These sub-trusts are often for educational trusts for the grandchildren or

special needs trusts for a disabled beneficiary or a charitable trust (See #4, #5 and #6).

Also, even though the actual trust agreement remains private and is not filed of public

record, a Memorandum of Trust is required to be filed. (Title 60, Okla. Stat. § 175.6a)

That document lists the trust name, the date it was created, who the Trustee and

Successor Trustees are and the legal description of the real estate or minerals that have

been transferred into the trust. The private terms on how the trust is to function, who

receives income, and specific gifts or personal family matters are still kept private and

not listed in the Memorandum.

2. TESTAMENTARY TRUSTS:

Purpose:

A trust created by your client’s Last Will and Testament is called a Testamentary Trust,

and can provide asset management for the benefit of his/her family for many years, after

the probate is closed.

Your client may desire that part or all of his/her estate’s assets be placed into trust to

provide professional management of his/her assets to protect the surviving spouse, older

or disabled family members, or until younger family members reach a more mature age

or finish their education. The long range management of assets and invested funds is the

primary responsibility of the Trustee and a corporate trustee should be considered if the

testamentary trust is to last for many years.

4

Creator:

The grantor is the “testator” of the Will.

Unique Features of the Testamentary Trust:

Anyone serving as a Trustee of a testamentary trust needs a certified copy of the deceased

person’s will and the Final Decree in the Probate in order to manage the trust properly.

One of these two documents is not enough. If a codicil to the will was also filed and

probated, be sure the Final Decree implements the provisions in the codicil as well, if it

affects the trust. Often a codicil is used to update and change the Successor Trustee

appointments or to change percentages certain heirs are to receive.

Helpful Hints:

(1.) The Trustee and CPA will have to coordinate obtaining a new tax identification

number, separate from any tax id number used by the deceased on the probate of the

deceased’s estate.

(2.) It may be important to also obtain the estate tax returns of the deceased and the

General Inventory of the deceased filed in the probate (when the Trustee was not the

Executor of the estate as well).

(3.) Transfer notices to stock brokerage accounts and insurance companies for real estate

are essential.

(4.) If minerals are involved, hopefully the attorney on the probate proceedings will write

all the oil companies and provide the Final Decree and request new division orders for all

minerals transferring to the new testamentary trust. Sometimes though the Trustee must

send the notices to the oil companies if the attorney has not done so.

(5.) Be sure to have plenty of death certificates and certified copies of the Final Decree if

there are many assets and producing mineral interest to get transferred into the trust after

the probate closes.

5

3. LIFE INSURANCE TRUSTS:

Purpose:

Life insurance is an asset of ever-increasing importance in the modern estate. Many men

and women today are creating life insurance trusts – a specialized version of the Living

trust – to assure full-time, flexible management of insurance proceeds for the protection

of their families. Instead of securities, life insurance policies now form the principal

asset of the trust. The Trustee collects the proceeds at death and combines those funds

with other assets of the insured, which are added or “poured over” into the trust by terms

of the insured’s Last Will and Testament. This type of trust can also be established as a

separate irrevocable trust during the insured’s lifetime. These are usually created to keep

the insurance proceeds from going outright to the surviving spouse (and her second

husband), and to protect proceeds for the education of the children.

Unique Features:

The life insurance trust offers an ideal way to unify insurance and other estate assets into

a comprehensive family financial plan. It affords many of the tax economies of other

trusts, along with the further benefit of skilled, long-term property management by

professional trustees – a benefit not available when lump-sum insurance proceeds are

paid to an individual beneficiary, who may be too young or inexperienced to manage a

large amount of money.

Helpful Hints on Management of Life Insurance Trusts:

(1.) Education Expense Instructions - Often, this type of trust includes detailed

instructions for the payment of education expenses of college – age beneficiaries. (See

educational trust distribution provisions discussed below in #4.) If it is an irrevocable life

insurance trust created during the insured’s lifetime, they are very difficult to terminate in

case of divorce.

(2.) Premium Payment Bills - The grantor of the trust will need to be notified when

premium payments are due, so he can contribute the funds necessary into the trust

account. Then the Trustee can pay the annual premium to the insurance company.

6

4. EDUCATIONAL TRUSTS:

Purpose:

An educational trust is established usually by the grandparents, parents, or other relative

for the future education of a child. The person creating the trust, called the grantor or

settlor, transfers a certain amount of money, securities or other income producing assets

into the trust for the benefit of the child. Additional contributions to the trust can be

made every year by the Grantor (and Grantor’s spouse) into the trust, so that the pool of

money grows until the child is 18 and ready for college. The annual gift exclusion, which

currently is $14,000 per donor and recipient, is a useful way to provide the funding tax

free for these trusts over a period of years

Grantor:

These types of trusts are often used by parents after a divorce when the grantor is not the

custodial parent of the children. It provides the parent, who will be paying for the future

education, the safeguard of the Trustee being in control of the investments and

distributions, not the custodial parent (who may have remarried or who could misspend

the money).

These types of trusts can be used for the “support, maintenance, and welfare” expenses of

a minor child prior to reaching 18 years of age, as well as their college educational

expenses thereafter. These trusts are commonly created in the settlement of lawsuits

dealing with injury claims of the parents or children.

Special Provisions for Educational Trusts:

The grantor can provide instructions in the terms of the trust agreement regarding what

conditions should exist for the Trustee to make distributions for the child’s benefit. Be

careful of providing insufficient instructions, such as “the net income will be distributed

to the beneficiary”. That will be insufficient guidance to a Trustee for this type of

account! Too often distributions have to cease and the grantor should specify all the

conditions for continuing or delaying the distributions.

7

Examples of Distributions:

a. Distributions for room, board, tuition, and books for college, university, or other

vocational schools.

b. Support and maintenance expenses before college.

c. Transportation expenses – (automobile and car insurance?).

d. Net income distributions after graduation from college. – (until principal distributions

start)

e. Principal distributions at certain times (graduation, one-half at 25th birthday, and one

half at 30th birthday).

f. Distribution instructions can also include guidance to the Trustee on when

distributions should cease (failure to attend college, failure to make satisfactory

progress towards the attainment of a degree, failure to maintain full-time enrollment).

g. Distributions for educational purposes can be for vocational training and not

necessarily limited to college or university classes.

Helpful Hints for Educational Trusts:

a. If the trust funds are large enough and the trust is to continue well past the college

education of the beneficiaries, the terms of the agreement can also provide other

instructions to the Trustee on principal distributions. For example, can a certain

amount of money be distributed to help the beneficiary establish or buy a business, or

cover the down payment on a home? Can the trust fund provide a “reasonable

transportation vehicle” – but not a Mercedes-Benz!

b. Medical emergencies allowing invasion of the principal should be considered.

c. Educational trusts like these have several tax advantages and can assist the grantor in

the completion of his or her overall estate plan. Your trust client should consult their

CPA when considering the creation of this type of trust.

d. It is very important to thoroughly consider who should be appointed as Trustee of this

type of trust. It is best to choose a Trustee with experience in managing educational

trusts for young beneficiaries and who is properly equipped to maintain the records

on numerous children or grandchildren’s accounts, each with differing distribution

needs and timeline.

8

e. Choose a Trustee who will not be unduly pressured by family members. Example:

Parents of the beneficiary may try to pressure the Trustee to spend money for a car for

19 year old Johnnie, even though the Grandparents/grantors specified that the trust

was not to buy a car for him!

f. Choose a Trustee who will follow the legal requirements and distribution limitations

specified in the trust agreement. Example: Johnnie must make satisfactory progress

towards the attainment of a degree by making a certain grade point. If he fails to do

so, distributions are to stop and Johnnie can get a job until he is ready to go back to

school.

5. CHARITABLE TRUSTS:

Purpose:

Often when people plan their estate, they want to give money or property to a specific

charity or their church. An attorney should review the choices available when a client

needs assistance in creating a charitable foundation, or leaving assets in trust for the

benefit of a particular charity. The attorney and his client should consult with the client’s

CPA about the creation of the charitable trust.

Special Provisions:

a. A corporate trustee’s professional expertise is often used for management of a

charitable trust’s investments. This situation could arise for a church’s endowment

fund or for any charitable foundation an individual or family created in order to

benefit some type of non-profit project or organization. Our Trust Department has

charitable trusts that have been specifically created by individuals to benefit a local

church or charities or which provide scholarships for local high school students to

attend college.

b. Sometimes the charitable organization, like a church, will have an “Endowment Fund

Committee” that wants to share responsibility with a corporate trustee regarding how

the charity’s money is invested and how the income is spent.

c. Applicable statutes governing professional management of investments for churches

or charitable organization.

9

1. Uniform Management of Institutional Endowment Funds Act (60 O.S. 300.1 et.

seq.) The governing board may contract with investment advisors, investment

counsel or mangers, banks, or trust companies, so to act for the governing board

in investment of institutional endowment funds. 60 O.S. 300.6 (2)

2. Oklahoma Charitable Fiduciary Act (60 O.S. 301.1 et.seq) Any charitable

organization acting as a trustee of charitable trusts in this state may employ and

delegate to investment advisors, investment counselors, state banks in Oklahoma

having trust powers, national banking associations having trust powers, and trust

companies having trust powers the discretion to make specific investment

decisions provided that the charitable organization shall at all times maintain

ultimate control of the management of the common trust fund. 60 O.S. 301.7B (3)

d. Some living trusts for grantors who have no children, grandchildren or other close

heirs, may include a list of chosen charities which are each to receive a certain

percentage of the trust before it is closed. Always include a provision in the trust that

the Trustee should obtain documentation that each charity is a 501(3)c or other IRS

approve charitable organization before distributing the money. In addition, include a

catch-all recipient to receive the amount designated to any specific charity, that by the

time of the distribution, is closed or no longer a qualified organization.

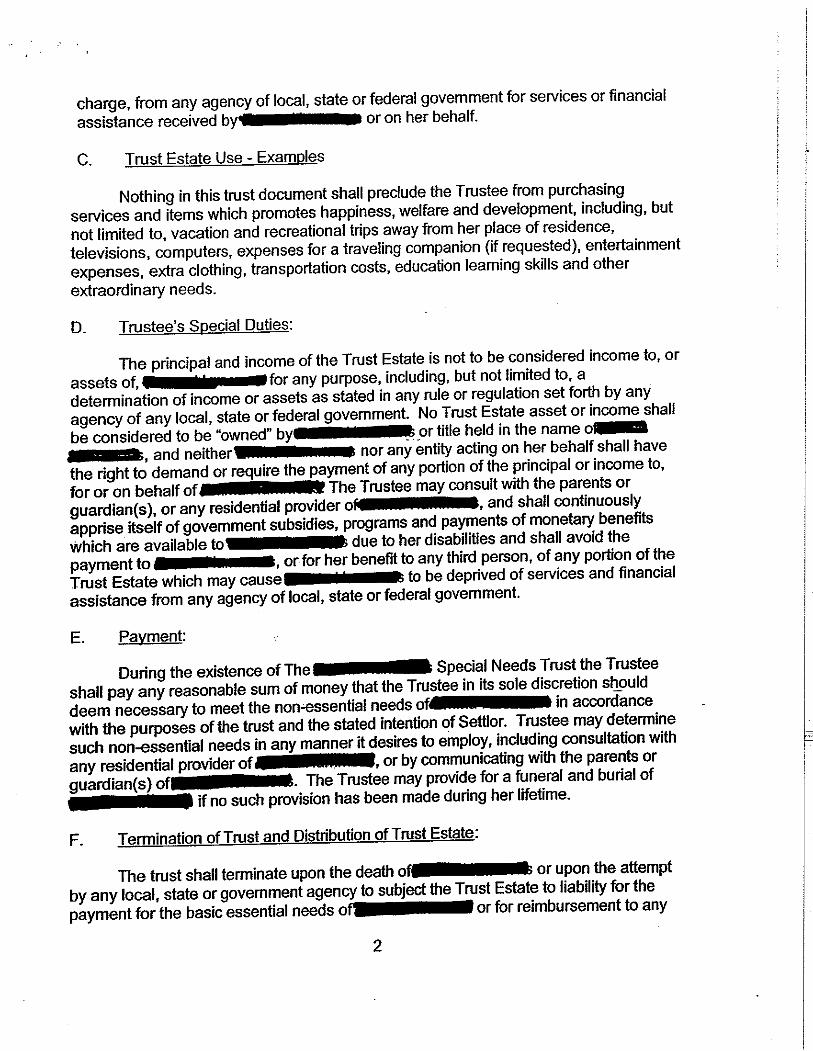

6. SUPPLEMENTAL NEEDS TRUSTS:

Purpose:

The grantor wants to either leave an inheritance in his will, or set aside money in a trust

during his lifetime, to a relative or natural heir who has a disability. For this disabled heir

to receive an inheritance outright, his social security disability benefits or other state

benefits could be jeopardized.

Specific Provisions:

The grantor established a living trust for the benefit of the disabled heir will usually

irrevocably transfer assets into the trust. (An Irrevocable Living Trust) A third party,

such as a corporate trustee or another relative serves as the Trustee. Since the “basic food

and shelter” may be provided by social security, these types of trusts are authorized to

10

pay for the extra items above basic living expenses, such as Christmas and birthday gifts,

vacation, travel and entertainment.

Unusual Features:

Since the funding for the trust comes from the family, the grantor must direct how the

remaining trust funds will be distributed at the disabled beneficiary’s death. Usually,

siblings or other family members are listed as the ultimate beneficiaries. Also, charitable

organizations can be listed to receive a donation (like McCall’s Chapel School Inc. in

Ada, Oklahoma), who may have provided housing for the disabled heir.

Helpful Hints:

The Trustee should know who is the Guardian or Attorney-in-Fact for the disabled heir so

that there is communication about the beneficiary’s health expenses and other permitted

personal distributions the Trustee may be required to make. The Trustee and the

Guardian/Attorney-in-Fact will work closely together for the benefit of their joint client.

7. SPECIAL NEEDS TRUSTS:

Grantor:

If a lawsuit arises from a personal injury situation, whether it is a car wreck or medical

malpractice case, the issue of having a trust created to receive the lump-sum settlement is

a convenient solution for the long term management of the settlement money.

Additionally, if future monthly annuity payments or lump-sum periodic amounts are part

of the settlement, as long as the beneficiary survives, the trust would be there to receive

those funds in the future.

Specific Provisions:

The trust agreement will have to be created and agreed upon by all parties (including the

attorneys representing them and the Trustee) along with the Settlement Agreement to

resolve the litigation. It will take both documents to govern the future of the trust money.

The remaining funds usually revert to the federal or state government at the beneficiary’s

death.

11

Helpful Hints:

(1.) Estimating the life span and future medical needs can be very difficult when the

Settlement Agreement and Trust Agreement are prepared. How often a handicap van

can be purchased, lift equipment installed as well as the insurance and tag for the van

become a major issue. Estimating future surgeries and hospital costs can be

underestimated when the lawsuit settlement is negotiated. The longer the

client/patient lives, the larger wheelchair and van is needed. Lift equipment is very

heavy and the timing for the replacement vehicle and equipment is often

underestimated in the Settlement Agreement.

(2.) In the Trust Agreement, it should be very clear what items or expenses are

considered covered medical expenses. For example, are dental bills and oral

surgeries covered by the trust under “medical expenses”?

(3.) Payroll Issues for the Caregivers:

Parents and relatives of the disabled beneficiary are usually the on-site caregivers.

Settlement Trusts of this nature need to specify the amount, hours or monthly limit

which can be paid to such caregivers and what happens with this payroll if the

beneficiary is temporarily or permanently placed in an assisted living center or

nursing home environment. Temporary trips to the hospital for surgery would be

handled separately.

(4.) Additional Issues that will Confront the Family and the Trust:

Remodeling funds for handicap bathroom and ramps for wheelchair at the home,

inadequate funds for utility bills or lift equipment, keeping the parents on a budget so

the trust funds will last long enough.

8. OKLAHOMA’S FAMILY WEALTH PRESERVATION TRUST ACT:

Purpose:

Title 31, Sections 10 through 18 of the Oklahoma Statues provides the requirements and

specifications for this Act which allows the creator of the trust to shield $1,000,000 of

contributed assets from creditors or future lawsuits. The trust may be created as a

revocable and amendable trust, or as an irrevocable trust.

12

Specific Provisions:

1. Growth in income or appreciation of the value of the contributed assets are still

shielded from creditors. Therefore, if the stocks transferred increase in value, that

increase is still protected.

2. Property owners holding mortgages to property transferred to such a trust will be

considered a “related indebtedness” and will not be shielded from such debt.

Therefore, if a home with an existing mortgage is transferred into the trust, the lender

could still foreclose on the home loan, if the payments are not made.

3. An individual Co-Trustee can serve as long as the other Co-Trustee is an Oklahoma

based bank or Oklahoma based trust company.

4. A majority of the trust assets must be Oklahoma assets in order to qualify. The act

has been expanded to include tangible personal property, jewelry, art, collectibles,

vehicles, inventory, fixtures and equipment located in Oklahoma. Promissory notes

secured by a mortgage in real estate or security interests in tangible personal property,

or both, located in Oklahoma will also qualify.

5. Other publicly traded stocks, U.S. obligations like Treasury bonds, non-Oklahoma

real estate and mutual funds etc… can be included in the minority share of the trust

assets.

6. The trust beneficiaries can include: the creator’s spouse, lineal ancestors or lineal

descendants of the creator or of the creator’s spouse, adopted children under 18, and

qualified charitable organizations. Also, any trust can be a beneficiary of a

preservation trust if it is created solely for the benefit of the person(s) or charity that

separately could qualify as such.

7. A trust like this is not exempt from execution to satisfy a child support judgement

against the creator. Also, a preservation trust remains subject to the Uniform

Fraudulent Transfer Act.

Helpful Hints:

Many professionals or business owners, who are afraid of frivolous or potential lawsuits

due to their business, should consider this type of trust to protect their assets and their

family.

13

9. IRREVOCABLE TRUSTS:

Purpose:

Historically, irrevocable trusts were created for three reasons (1.) for the grantor to

successfully, irrevocably transfer assets out of his/her estate to the children or

grandchildren’s educational trusts and/or (2.) for the grantor to transfer assets to a

charitable trust. (3.) for the creation of an Irrevocable Life Insurance Trust. These trust

transfers are during the grantor’s life and would get the value of these transferred assets

out of this estate for tax purposes. Currently, the federal estate tax exemption is

$5,430,000 with appropriate tax filings and tax elections, married couples may secure a

$10,860,000 exemption regardless of which spouse dies first or how the couple owns

their property (assuming that they both die in 2015). Amounts in excess of the exemption

are taxed at a 40% rate.

Gifts:

The lifetime federal gift tax exemption in 2015 is $5,430,000. Amounts transferred in

excess of the exemption are taxed at the 40% rate. For 2015, the annual exclusion from

the gift tax is $14,000. A gift no larger than $14,000 may be given to each of as many

people as you wish without incurring gift tax or using up your lifetime federal gift tax

exclusion. To qualify for the annual exclusion, the gift must be of a “present interest,”

meaning that the person receiving the gift must have the immediate right to use and enjoy

the gift, without strings attached. Couples may “split” their gifts to secure a $28,000

annual exclusion per recipient.

10. IRA TRUSTS:

Purpose:

For your clients who have IRA accounts naming their children as the beneficiaries at their

death, but would prefer to control what happens later to the money, an IRA Trust may be

an attractive choice. The beneficiaries would receive the required minimum distributions

(RMD), but the Grantor (the deceased parent) could include provisions that would control

any distributions beyond that.

14

Grantor:

Sometimes when a client is receiving a lump sum distribution from an employer

sponsored profit sharing plan or has a regular IRA with a large balance, he or she would

be a good candidate to consider an IRA Trust.

Special Provisions:

1. The forms and paperwork are very specific and not all bank Trust Departments will

agree to serve as Trustee for this kind of trust. The actual trust agreement is an IRA Trust

form.

2. By spreading out the distributions, the regular RMD and limiting amounts above that,

the distributions are spread over many years and the beneficiaries are less likely to cash-

in the balance and all the deferred tax come due in one tax year.

3. The beneficiaries must be “people”, not an estate, charitable organization or another

trust! Those types of beneficiaries do not have life expectancies and the IRS would not

allow spreading the withdrawals out over a period of years.

Helpful Hints:

1. The wording has to comply with the IRS guidelines exactly and the IRA Trust’s

Trustee has to file a copy of the trust documents with the IRA custodian by October 31st

of the year following the IRA original owner’s death.

2. Form 5498 is sent out by January 31st to IRA account holders who will be required to

take a required minimum distribution during the year. Box 11 will be checked if your

client will reach age 70.5 years old during the current year. This box provides a reminder

that your client should begin taking any required minimum distributions no later than

April 1st of the year following the year your turn 70.5.

3. Form 5498 is required to be filed with the IRS by May 31st to report contributions to

IRAs and other tax-preferred savings accounts. Additionally, contributions for the

previous tax year made by April 15th are included on Form 5498 for traditional IRA and

Roth IRA accounts. Accordingly, many IRA account holders receive their Form 5498 in

May.

15

4. The investments will be directed by the Trustee. These are not self-directed IRA

accounts by customers.

5. The documents or the Trustee’s internal policies will dictate if special assets, such as

closely-held family corporations or partnership interest, will be accepted as assets. Also,

real estate and mineral interests may not be accepted as proper assets for the IRA Trusts.

Your client should interview any prospective Trustee and discuss the potential assets the

Trustee is willing to accept and manage in the IRA trust before completing the

paperwork.

11. CHARITABLE REMAINDER TRUSTS:

Purpose:

A Charitable Remainder Trust is a special tax-exempt irrevocable trust arrangement

written to comply with federal tax laws and regulations. Your client transfers cash or

assets (especially appreciated assets) to the trust and may receive income for life or, if he

chooses, a certain term of years (not to exceed 20). In fact, the income can be paid over

his life, his spouse’s life and even their children’s and grandchildren’s lives.

Special Provisions:

IRS code section 664 lists the requirements a trust must meet in order to qualify as a

Charitable Remainder Trust. The Charitable Remainder Trust was made possible by the

Tax Reform Act of 1969.

The minimum payout rate is 5% and the maximum is 50%. The payout rate may be

further limited by a 10% remainder interest requirement, which applies only to Charitable

Remainder Unitrusts. The present value of the remainder interest passing to charity must

equal at least 10% of the value of the gift on the date of contribution.

12. CHARITABLE LEAD TRUSTS:

Purpose:

A charitable lead trust is a philanthropic and estate planning tool. A donor can transfer

assets, such as cash, stocks and artwork, to a trust for a set term of years. This type of

trust is irrevocable. Once your client puts assets or cash into the trust, they cannot get

16

them taken out later. Each year, payments are made from the trust to the donor’s

designated charity/charities. The grantor who creates this type of trust and donates the

assets into the trust can take an up front income tax deduction based on the trust’s

payments to the charity.

Special Provision:

It is called a lead trust because the charities are entitled to the lead (or first) interest in the

trust asset and the non-charitable beneficiary receives the remainder (or second-in-line)

interest. If the trust’s investments fall in value, the amount available to distribute to the

non-charitable beneficiaries (your client’s heirs) may be less, because the trust must make

the charitable payments no matter what the market is doing.

Once the trust’s term expires, what is left goes to the donor’s heirs. Handling assets in

this way can shelter the assets’ appreciation from estate taxes.

Two Types of Charitable Leads Trusts:

Charitable lead trusts are of two types: charitable lead annuity trusts and charitable lead

unitrusts. In the first type, the donor sets a fixed annual gift for the charities named. In

the unitrust, the charities receive a percentage of the trust’s value each year. This means

that those benefits will fluctuate based on the trust’s investment returns or losses.

Conclusion:

For Charitable Remainder Trusts and Charitable Lead Trusts a client really needs an

estate planning attorney well versed in the tax requirements for these highly specialized

trusts. It is always advisable to have the clients confer with their CPA to review all the

provisions before the trust is executed.

II. HOW DO YOU DEFINE AN ACCOUNTING? LET ME COUNT THE

WAYS!

Kara Greuel, J.D., CPA, CFF, CFMA, CFE

Greuel Law Firm, PLLC 5100 East Skelly Drive, Suite 1040

Tulsa, Oklahoma 74135 Phone # 918-728-2699

Fax # 918-491-4708 Email: [email protected]

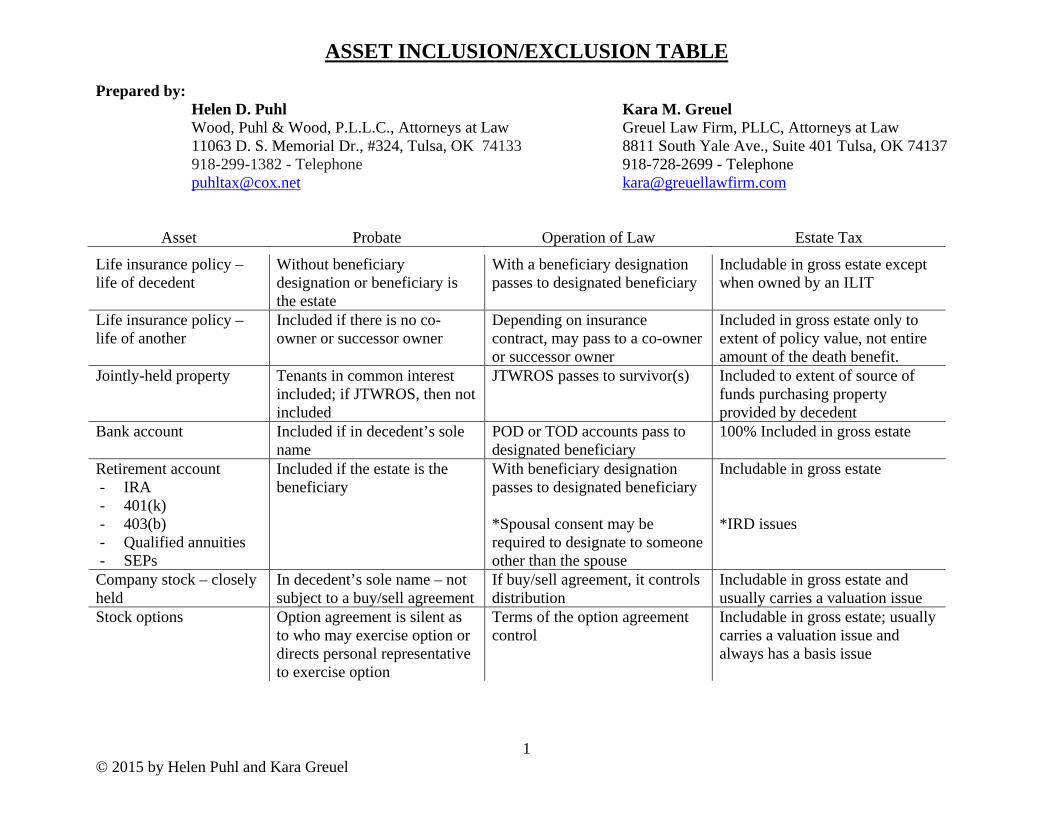

ASSET INCLUSION/EXCLUSION TABLE Prepared by: Helen D. Puhl Kara M. Greuel Wood, Puhl & Wood, P.L.L.C., Attorneys at Law Greuel Law Firm, PLLC, Attorneys at Law 11063 D. S. Memorial Dr., #324, Tulsa, OK 74133 8811 South Yale Ave., Suite 401 Tulsa, OK 74137 918-299-1382 - Telephone 918-728-2699 - Telephone [email protected] [email protected]

Asset Probate Operation of Law Estate Tax

1

© 2015 by Helen Puhl and Kara Greuel

Life insurance policy – life of decedent

Without beneficiary designation or beneficiary is the estate

With a beneficiary designation passes to designated beneficiary

Includable in gross estate except when owned by an ILIT

Life insurance policy –life of another

Included if there is no co-owner or successor owner

Depending on insurance contract, may pass to a co-owner or successor owner

Included in gross estate only to extent of policy value, not entire amount of the death benefit.

Jointly-held property Tenants in common interest included; if JTWROS, then not included

JTWROS passes to survivor(s) Included to extent of source of funds purchasing property provided by decedent

Bank account Included if in decedent’s sole name

POD or TOD accounts pass to designated beneficiary

100% Included in gross estate

Retirement account - IRA - 401(k) - 403(b) - Qualified annuities - SEPs

Included if the estate is the beneficiary

With beneficiary designation passes to designated beneficiary *Spousal consent may be required to designate to someone other than the spouse

Includable in gross estate *IRD issues

Company stock – closely held

In decedent’s sole name – not subject to a buy/sell agreement

If buy/sell agreement, it controls distribution

Includable in gross estate and usually carries a valuation issue

Stock options Option agreement is silent as to who may exercise option or directs personal representative to exercise option

Terms of the option agreement control

Includable in gross estate; usually carries a valuation issue and always has a basis issue

ASSET INCLUSION/EXCLUSION TABLE

Asset Probate Operation of Law Estate Tax

2 © 2015 by Helen Puhl and Kara Greuel

Stocks/Bonds Included if in decedent’s sole name

Exceptions: where company allows for beneficiary designation

Includable in gross estate; value based on stock price on date of death

Vehicles Included if in decedent’s sole name; or, if the title designates “and,” then treated like TIC

If title designates “or,” then passes to the joint title holder

Included in gross estate

Personal property

Included in the estate Finder’s keepers Includable in gross estate

Rental income/ Leaseholds

Included if rental agreement is solely in name of decedent *Personal Representative has responsibility to collect decedent’s share of accrued rents

If rental agreement is in name of decedent and survivor *Decedent’s portion could be collected by the Personal Representative

Includable in gross estate *IRD Issues

Tax refunds Included if solely in the name of the decedent; if shared with surviving spouse, then based on actual tax liability (if any) and the amounts paid by the decedent

If joint refund with surviving spouse, the surviving spouse’s portion based on actual tax liability and amounts paid by the surviving spouse

Decedent’s Portion includable in gross estate

Deferred comp and other types of IRD

Most IRD (except deferred comp) is included since it is a type of personal property

Often, the deferred compensation agreement has an internal distribution order or refers to pension beneficiary designations

All included on estate tax return. For cash basis taxpayers most IRD is shown on the estate’s or beneficiaries’ income tax returns; for accrual basis taxpayers most IRD shown on the decedent’s final income tax return

ASSET INCLUSION/EXCLUSION TABLE

Asset Probate Operation of Law Estate Tax

3 © 2015 by Helen Puhl and Kara Greuel

Dividends payable Includable if decedent or the estate was the sole holder of record on the declaration date

In some rare instances may pass with a beneficiary designation to a designated beneficiary

All included on estate tax return. For cash basis taxpayers most IRD is shown on the estate’s or beneficiaries’ income tax returns; for accrual basis taxpayers most IRD shown on the decedent’s final income tax return

Mortgages/ Notes/ Accounts payable

Includable in probate estate (except for assignment)

Possibility of non-inclusion in probate if properly assigned to an entity such as a revocable trust or an LLC

Principal and accrued interest included in the gross estate; Interest included on the estate’s income tax return (if cash basis tax payer); if accrual basis tax payer, interest includable on the decedent’s final income tax return.

LLC/ FLPS/ Partnership Only if in decedent’s sole name and operating agreement or partnership agreement are silent as to distribution

Many operating agreements and partnership agreements have strict restrictions on the transfer of the ownership; a distribution order is often built into the document

Full Value of ownership percentage is included; if anything less than the full value is included, any discounts or reductions in the value must be explained in detail on the return

Chose in action / Judgments

Typically any type of suit must be filed or continued by the Personal Representative of an estate; proceeds are includable in the probate estate; may require a probate to stay open for a long period of time

Certain wrongful death actions may be brought by a surviving spouse, surviving children or next of kin without involving a personal representative

Includable but valuation is an issue; may require an amendment of the estate tax return upon payment of the judgment. Adjustments may need to be made for indemnified amounts repaid to social security, Medicare or private insurer.

MSA/HSA Rarely; usually has a designated beneficiary

Beneficiary designation controls Included unless such interest passes to a surviving spouse

ASSET INCLUSION/EXCLUSION TABLE

Asset Probate Operation of Law Estate Tax

4 © 2015 by Helen Puhl and Kara Greuel

Custodial accounts Rarely included; decedent usually owns such accounts as a custodian (a fiduciary role)

A beneficiary designation usually controls the distribution of such custodial accounts; if the child for whom the account has been created dies, the custodian names a new beneficiary

Not included in the gross estate

Revocable Trust Assets Assets transferred are not included in probate estate

Distribution of assets are made pursuant to terms of the trust

All assets trust assets are includable in the gross estate; indicate transfers of assets on Schedule G

Other interest held as a fiduciary / trust protector

Not included in probate estate Obligation to hold as fiduciary passes to successor fiduciary

Not included in the gross estate (unless deemed to have a general power of appointment due to broadness of powers)

Intellectual property / Royalties

Includable in probate estate (unless controlled by royalty agreement)

Royalty agreement may control distribution

Includable in gross estate (huge valuation issues)

Cloud assets/ social media

Not included in the probate estate – unless agreement specifies transfer can occur on death

Can be managed by fiduciary after death if allowed by license agreement with individual sites

Not included in the gross estate

Annuities Unlikely if annuitant is decedent; more likely if annuitant is a third party

Beneficiary designation controls or successor owner if annuity is not on life of the decedent

Annuity on decedent’s life – full value (to extent decedent contributed to the purchase price) is included; annuity on third party’s life not includable

ASSET INCLUSION/EXCLUSION TABLE

Asset Probate Operation of Law Estate Tax

5 © 2015 by Helen Puhl and Kara Greuel

Tribal property / Trust land

If held in name of decedent alone, included; if trust land or headright, will must be approved by the tribe before transfer can occur; after approval, probate process in district court using Oklahoma Statutes governs transfer

Use of a beneficiary deed or joint title may affect these rights and be nullified if not approved by tribe or property may lose its status as tribal property or trust land.

If included in the Indian General Allotment Act, not included in gross estate (exempt from federal estate tax); includes trust lands acquired either in the original allotment or by inheritance, original and inherited headrights, mineral headright income derived from royalties held in trust by the U.S. Government and trust-fund cash directly derived from allotted lands.

Oil and gas royalties Included if in decedent’s sole name; use of 58 O.S. 393 directs payments only, does not affect the title to the underlying mineral interest

JTWROS passes to survivor(s) Includable – valuation is not as much of an issue since no longer have Oklahoma Estate Tax

Reversionary or remainder interests

Typically not included – except on case by case basis when gap of time between allocation and distribution

Terms creating reversionary or remainder interest generally apply

Typically not included – except on case by case basis when gap of time between allocation and distribution

Insurance claims Included; use of 58 O.S. 393 can avoid probate if under $20,000

Even if there is a joint policy holder, claim payments are usually made to both parties; no way to designate a beneficiary; some insurance companies will allow you to hold insurance in name of a revocable trust - but, this creates an issue with regards to payments from government entities on types of crop insurance and crop subsidies

Includable if asset for which claim was paid was not included on estate tax return

ASSET INCLUSION/EXCLUSION TABLE

Asset Probate Operation of Law Estate Tax

6 © 2015 by Helen Puhl and Kara Greuel

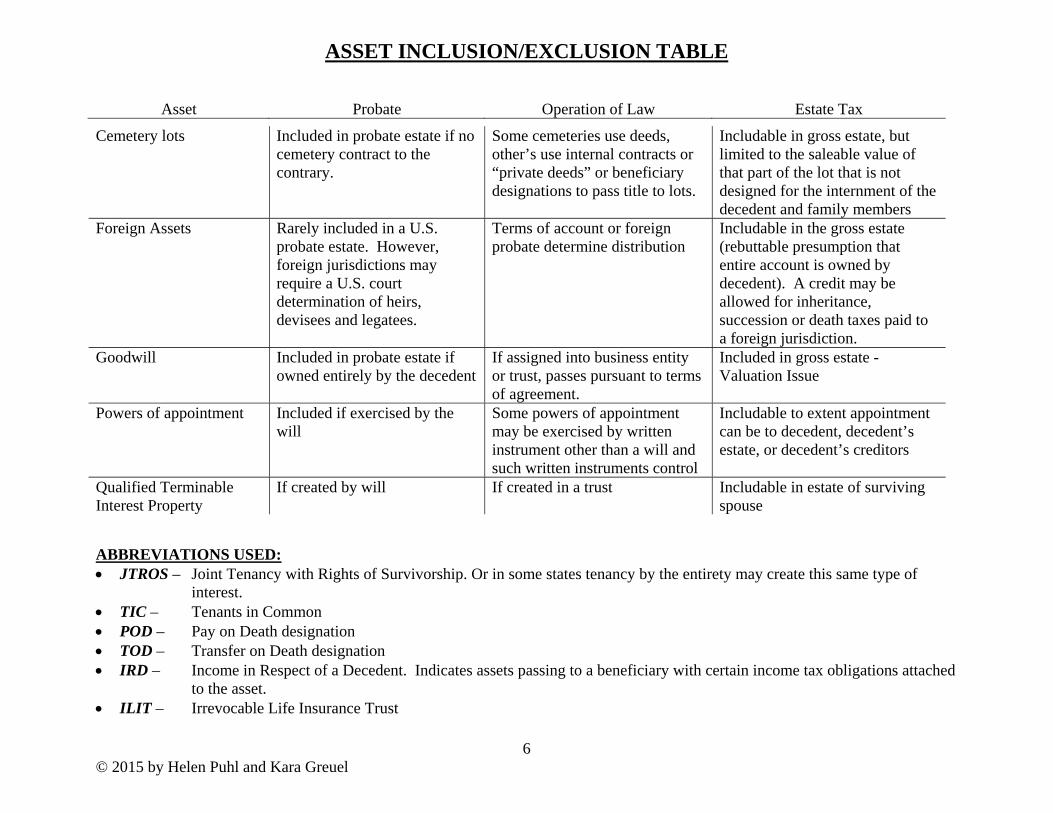

Cemetery lots Included in probate estate if no cemetery contract to the contrary.

Some cemeteries use deeds, other’s use internal contracts or “private deeds” or beneficiary designations to pass title to lots.

Includable in gross estate, but limited to the saleable value of that part of the lot that is not designed for the internment of the decedent and family members

Foreign Assets Rarely included in a U.S. probate estate. However, foreign jurisdictions may require a U.S. court determination of heirs, devisees and legatees.

Terms of account or foreign probate determine distribution

Includable in the gross estate (rebuttable presumption that entire account is owned by decedent). A credit may be allowed for inheritance, succession or death taxes paid to a foreign jurisdiction.

Goodwill Included in probate estate if owned entirely by the decedent

If assigned into business entity or trust, passes pursuant to terms of agreement.

Included in gross estate - Valuation Issue

Powers of appointment Included if exercised by the will

Some powers of appointment may be exercised by written instrument other than a will and such written instruments control

Includable to extent appointment can be to decedent, decedent’s estate, or decedent’s creditors

Qualified Terminable Interest Property

If created by will If created in a trust Includable in estate of surviving spouse

ABBREVIATIONS USED: JTROS – Joint Tenancy with Rights of Survivorship. Or in some states tenancy by the entirety may create this same type of

interest. TIC – Tenants in Common POD – Pay on Death designation TOD – Transfer on Death designation IRD – Income in Respect of a Decedent. Indicates assets passing to a beneficiary with certain income tax obligations attached

to the asset. ILIT – Irrevocable Life Insurance Trust

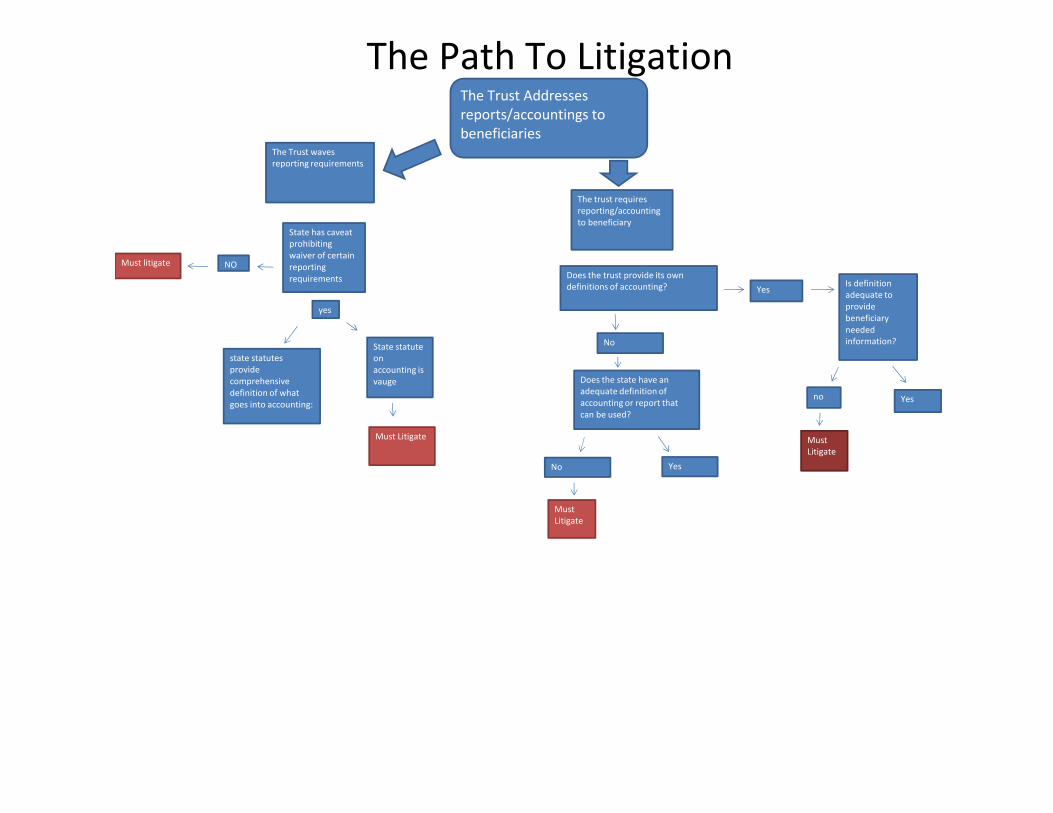

The Path To LitigationThe Trust Addresses reports/accountings to beneficiaries

The Trust waves reporting requirements

The trust requires reporting/accountingto beneficiary

Does the trust provide its own definitions of accounting?

Does the state have an adequate definition of accounting or report that can be used?

State has caveat prohibitingwaiver of certain reporting requirements

state statutes provide comprehensive definition of what goes into accounting:

State statuteon accounting is vauge

Must litigate

No

Yes

No Yes

Must Litigate

Is definition adequate to provide beneficiary needed information?

no Yes

Must Litigate

Must Litigate

NO

yes

The Path To LitigationThe Trust is silent about providing an accounting.

Is there a state statute on accountings/reports/ or providing some sort of information to trust

No

Yes

Does it only provide for relevant informationor other vauge terminology which does not reaveal what is happening with trust

Beneficiaries must make reasonable request because report is not mandatory?

Is reportautomatically provided to beneficiaries?

Do state statutesonly address ct ordered accountings?

Does statute provide descriptionof what must go into accounting?

Yes No

Must litigate

Must Litigate

Must Litigate

Must litigateto for more comprehensive information

Must Litigate

NO

Yes

III. IT SEEMED LIKE A GOOD IDEA AT THE TIME!

ETHICS BY: Kara Greuel,

J.D., CPA, CFF, CFMA, CFE Greuel Law Firm, PLLC

5100 East Skelly Drive, Suite 1040 Tulsa, Oklahoma 74135

Phone # 918-728-2699 Fax # 918-491-4708

Email: [email protected]

IT SEEMED LIKE A GOOD IDEA AT THE TIME…

OR Why You May Not Want to Serve

As A Trustee For The Trusts You Create

By Kara M. Greuel, J.D., CPA/CFF/CGMA, CFE

Greuel Law Firm, PLLC 8811 S. Yale Ave., Suite 401

Tulsa, OK 74137 918-728-2699

1

Have you been there? Surely, you have…

You meet with a client and begin the estate planning process. During discussions

regarding the design of the plan, the client poses a question “Can you serve as my trustee?”

There are some attorneys who routinely say yes. Others always refuse. So, the real question

becomes this – Can we? Is it allowed? Is agreeing to serve a violation of some rule of

professional responsibility? As with all good legal analysis, the answer is – it depends.

Logically speaking, the drafting lawyer would appear to be an excellent choice to serve

as fiduciary. He or she would have a particular familiarity with the client’s intent and the

circumstances surrounding familial relationships. However, if we continue the thought process

using the adage of “what could go wrong, will,” there are several issues to consider. For

example, questions may arise as to whether or not the client has exercised his or her independent

judgment regarding the appointment of the lawyer as fiduciary - especially when the attorney

may not be the best choice to serve. Further, should there be after- death contests by family

members or other beneficiaries and claims made against the fiduciary, the attorney who serves in

both capacities winds up being in a compromising position. The conflict of serving in both roles

never goes away.

The ABA, in Formal Ethics Opinion 02-426 (May 31, 2002) allows for a lawyer to serve

as a fiduciary if his or her obligations are met under Model Rules 1.4(b) and 1.7(b). These

Model Rules are reiterated in our Oklahoma Rules of Professional Conduct Section Rules 1.4(b)

and Rule 1.7(b) under Title 5, Appendix 3-A, of our Oklahoma Statutes.

Rule 1.4(b) states that “A lawyer shall explain a matter to the extent reasonably necessary

to permit the client to make informed decisions regarding the representation.” This means that

the lawyer must discuss options that the client has with regard to appointing a fiduciary and

2

particularly, an individual fiduciary. This doesn’t mean that the attorney can not also discuss

with the client his or her ability to serve as a fiduciary. However, the lawyer cannot allow self-

interest and desire to prevail against the independent professional duty the lawyer owes to the

client. The lawyer’s responsibility to the client includes providing the client with information

regarding the tasks that the fiduciary will need to perform, what skills would be ideal for being

able to perform the designated tasks and the costs and benefits of the different types of

fiduciaries – individual or corporate. A good place to start with regard to discussing the role of

the fiduciary is to review the requirements with the client. Often times the client only has a

vague idea as to the tasks that the fiduciary will have to accomplish. Reviewing a document that

would typically only be reviewed after the client’s death, may prove very beneficial. The

American Bar Association has a client brochure entitled “You Are The Fiduciary.” It’s a

handbook for those individuals who are serving as a fiduciary and an inexpensive resource for

education of your client.

Continuing in numerical order, Rule 1.7(b) states that as long as certain requirements are

met, a lawyer may serve as a fiduciary even if a conflict of interest exists under 1.7(a). Conflicts

include the representation of one client who will be directly adverse to another client, or a

circumstance in which there is a significant risk that the representation of one or more clients

will be materially limited by the lawyer’s responsibilities to another client, a former client or a

third person or by the lawyer’s own personal interest. Even so, if certain requirements are met,

the lawyer may go forward with the representation. These requirements include that the lawyer

reasonably believes he or she will be able to provide competent and diligent representation to

each affected client.

3

With regard to self-appointment, Ethics Opinion 02-426 provides that in the case of a

lawyer naming himself or herself as fiduciary, or naming his or her firm as counsel for the

fiduciary, the Model Rules allow for a fiduciary to appoint himself or his firm as the attorney to

provide services during the administration of an estate or trust. Even though these are dual roles,

there is no conflict of interest because the obligations of an attorney and a fiduciary do not differ.

The ethics opinion points out that the principal responsibility of the lawyer for a fiduciary is to

advise the fiduciary in properly performing his or her fiduciary duties. Likewise, because the

fiduciary is to act in the best interest of the beneficiaries while serving, the attorney assisting can

not advise the fiduciary to act or assist the fiduciary in acting against the interest of the

beneficiaries. The ethics opinion takes the position that the attorney for a fiduciary only owes a

limited duty of care to the legatees, devisees and creditors of an estate or to the beneficiaries of a

trust. However, regardless of what capacity an attorney is serving, the fees that are charged for a

dual representation must be reasonable.

The ACTEC Commentary to Model Rule 1.7 expressly discusses application of the rule

to appointment of a scrivener as fiduciary. The commentary reads,

An individual is generally free to select and appoint whomever he or she wishes to a fiduciary office (e.g., trustee, executor, and attorney-in-fact). None of the provisions of the MRPC deals explicitly with the propriety of a lawyer preparing for a client a will or other document that appoints the lawyer to a fiduciary office. As a general proposition, lawyers should be permitted to assist adequately informed clients who wish to appoint their lawyers as fiduciaries. Accordingly, a lawyer should be free to prepare a document that appoints the lawyer to a fiduciary office so long as the client is properly informed, the appointment does not violate the conflict of interest rules of MRPC 1.7, and the appointment is not the product of undue influence or improper solicitation by the lawyer.

For purposes of the ACTEC Commentary, a client is properly informed if the client is

provided with information:

Regarding the role and duties of a fiduciary;

4

Regarding the ability of a layperson to serve as fiduciary with legal and other professional assistance; and

The comparative costs of appointing the lawyer or another person or institution as fiduciary.

The information provided should always inform the client of conflicts of interest

including any significant lawyer-client relationship that exists between the lawyer or the lawyer’s

firm and a corporate fiduciary under consideration for appointment as fiduciary.

If you don’t make the necessary disclosures, it can result in liability for potentially

significant damages. It’s often said, “If you can’t be a good example, be a horrible warning,” To

illustrate that adage, , consider a recent case where conflicts were not disclosed and it ended

badly for the law firm. In Gunster, Yoakley & Stewart v. McAdam, a law firm was held liable for

$1,043,430 in damages because, it “wrongfully procured” an appointment of a corporate

fiduciary which caused the estate administration to be more expensive. The underlying case

reveals that the law firm had a referral relationship with the corporate fiduciary and the lack of

disclosure of the relationship caused the plaintiffs to seek recompense for all “avoidable probate

expenses.”1

Some states have enacted specific statutes relating to the issue of the appointment of the

scrivener as fiduciary. For example, New York State has addressed the issue of naming the

lawyer as executor by statute.2

These statutes permit a lawyer to prepare a will and be designated as executor as long as

the testator is informed of the following points before the execution of the will:

Any person, including a lawyer, is eligible to serve as an executor.

1 965 So.2d 182 (Fl. Dist. Ct. of App. 2007) 2 See McKinney’s SCPA §2307-A.

5

Absent an agreement to the contrary, any person, including a lawyer, who serves as an

executor is entitled to receive the statutory commission.

If the lawyer or an affiliated lawyer renders legal services in connection with the

executor’s official duties, such lawyer or the affiliated lawyer is entitled to receive

reasonable compensation in addition to the statutory commission.

To ensure that this information is provided, the testator must provide written acknowledgement

of the disclosures and the disclosure must be witnessed by someone other than the designated

executor. And although the disclosures are separate from the will itself, they may be annexed to

it. Although Oklahoma does not require it, as a measure of protection for those drafting

attorneys who are also serving as fiduciaries, I have provided a comprehensive sample

Acknowledgment and Disclosure form to this paper. Please use it, or not, as you see fit.

Another state that has addressed this issue is California. It has enacted legislation to

specifically address the appointment of a client’s lawyer as the named fiduciary. Any individual

who drafts, transcribes, or causes to be drafted any instrument of transfer, is defined as a

“disqualified person,” unless that person is related by blood, marriage or is a cohabitant.

Alternatively, an “independent” attorney can certify that the transfer was not the product of

fraud, menace, duress or undue influence. Regardless, this provision can not be

waived.3However, all is not lost should a disqualified person be named as the sole trustee. If the

court, based on the facts and circumstances, finds that “it is consistent with the settlor’s intent

that the trustee continue to serve and that this intent was not the product of fraud or undue

influence,” the disqualified person may be allowed to continue serving.4

3 Cal. Proc. C. §15642(b)(6) 4 Id.

6

Further, should an attorney also be named as a personal representative, he or she may

receive payment or fees for serving as the personal representative, but will not also receive

payment for serving as the attorney unless the court approves it. However, the court must

approve the arrangement in advance and find that the arrangement is to the advantage, benefit

and best interest of the decedent’s estate.5

Other states have adopted ethical rules that address the propriety of the scrivener serving

as fiduciary and place emphasis on slightly different ethical principles.

New Jersey ethical rules allow services, but with the disclosure and consultation

requirements of MRPC 1.7(b)(2).6

South Carolina allows for such service but subject to MRPC 1.8(c) regarding the

prohibition on lawyers soliciting gifts from clients.7

Georgia issued a Form Advisory Opinion which held:

It is not ethically improper for a lawyer to be named executor or trustee in a will or trustee he or she has prepared when the lawyer does not consciously influence the client in the decision to name him or her executor or trustee, so long as he or she obtains the client’s written consent in some form or gives the client written notice in some form after a full disclosure of all the possible conflicts of interest. In addition, the total combined attorney’s fee and executor or trustee fee or commission must be reasonable and procedures used in obtaining this fee should be in accord with Georgia law.8

The opinion held that the following items need to be disclosed to the client:

o All potential choices of executor or trustee, their relative abilities, competence, safety and integrity, and their fee structure;

o The nature of the representation and service that will result if the client wishes to name the attorney as executor or trustee (i.e., what

5 Cal. Prob. C. §10804 6 New Jersey, Eth. Op. 683 (1996). 7 SC. Op. 91-07 (1991). 8 Formal Advisory Opinion No. 91-1 (September 13, 1991).

7

the exact role of the lawyer as fiduciary will be, what the lawyer’s fee structure will be as a lawyer/fiduciary, etc.);

o The potential for the attorney executor or trustee hiring him or herself or his or her firm to represent the estate or trustee, and the fee arrangement anticipated; and

o An explanation of the potential advantages to the client of seeking independent legal advice.

These disclosures can be made orally. However, the acknowledgement and

consent by the client should be in writing.

Conventional wisdom says that rules were created because someone did something

stupid which caused the need for the rule. We’ve discussed at length some examples of state-

imposed rules for attorneys and now we’ll look at a couple of cases. Neither are Oklahoma cases.

There is only one Oklahoma case in which the issue has come up (Oklahoma Bar Association v.

Kenneth E. Bradley)9 and in that instance, the Court only concerned itself with the

mismanagement of assets that resulted while the attorney was serving as trustee. It never dealt

with whether or not his drafting of four trusts and naming himself as trustee was an ethics

violation. In the cases we will look at, one caused the need for the rules we have reviewed

above, and one supports the ability of a drafting attorney to name himself as a fiduciary.

The case of In Re Estate of Weinstock,10 along with others, resulted in the creation of

SCPA §2307-A for New York (discussed above). This matter involved two attorneys who were

father and son. They met with an 82 year old elderly man (the decedent) who was physically

disabled and had reduced mental abilities. During the first meeting between the man and the

attorneys, he indicated that the bank, which was set to serve as the executor of the estate, would

charge too much money and so he wanted to change his previous designation. During this

discussion, he talked about appointing his daughter and son-in-law.

9 746 P.2d 1130 (Okla. 1987) 10 351 N.E. 2d 647 (N.Y. 1976).

8

Also discussed during this meeting was the possible appointment of both of the attorneys

and the elderly man’s accountant. At some point during the meeting, the man agreed and the

attorneys drafted a new will. The man never had an opportunity to review the will prior to

signing and the attorneys never disclosed to the man that each person serving – attorneys and

accountant – would receive compensation for doing so.

The surrogate determined that along with over-reaching, the father and son team had

committed constructive fraud and that they should be prohibited from serving as executors under

the will. The court additionally stated that is was ok to choose the drafting attorney to serve as

the executor and doing so would not create a presumption or inference of wrong-doing. One of

the deciding factors in this case had to do with the fact that neither of the attorneys had ever met

the elderly man prior to their initial meeting and subsequent appointment as executors.

In Petty v. Privett,11 the executor of the estate brought suit against the attorney retained

by the former executor (this attorney also was involved in the drafting of the decedent’s will) and

alleged failures to account, to disperse assets and excessive and unauthorized payments. The

attorney used the exculpatory clause in the will as a defense and the trial court held that the

clause was void as against public policy.

On appeal, the Court concluded that the attorney was not barred from depending on the

exculpatory clause if the attorney proves that there is no overreaching, undue influence or abuse

of fiduciary relationship. The Court of Appeals remanded it back to the trial court to determine

those three issues.

There are many landmines to avoid when choosing how to assist your clients. Attorneys

who consistently agree to serve as trustee for clients whose trusts they draft are setting

11 818 S.W. 2d 743 (Tenn. Ct. App. 1989).

9

themselves up for problems later on. All attorneys should be aware of the statutory, ethical and

legal restrictions regarding this type of service. Additionally, they should make their clients

aware of the choices available to them in selecting a fiduciary and obtain a written

acknowledgment from the client.

Acknowledgment of Disclosure

I, _________________, (“Client”) am a current client of _______________________, attorney

at law (“my attorney”) who is associated with the firm of ___________________ and said

attorney has been engaged to perform estate planning services for me. As part of the

engagement, I have requested that my attorney serve in a fiduciary capacity with regard to my

estate and trust after my death. I have made this request after discussion with my attorney and

with full knowledge and awareness regarding important considerations. As such, I state the

following:

I understand the role and duties of a fiduciary.

I understand that any person, including a lawyer, is eligible to serve as a fiduciary.

I understand that absent an agreement to the contrary, any person, including a lawyer,

who serves as an executor is entitled to receive the statutory commission.

I understand that a layperson who obtains legal and other professional assistance may be

perfectly capable of serving as a fiduciary.

I understand and my attorney has discussed with me potential choices of executor or

trustee, their relative abilities, competence, safety and integrity and the comparative costs

of appointing a lawyer or another person or institution as fiduciary.

I understand that if my attorney or an affiliated attorney renders legal services in

connection with the official duties of the fiduciary (whether or not my attorney is serving

as my fiduciary), my attorney or the affiliated attorney is entitled to receive reasonable

compensation in addition to the statutory commission.

I understand, and my attorney has disclosed to me, any known significant lawyer-client

relationship that exists between my attorney or my attorney’s firm and a corporate

fiduciary under consideration for appointment.

I understand there are advantages of seeking independent legal advice regarding the

appointment of my attorney to serve in a fiduciary capacity for my estate planning

documents. I assert that I have either sought independent legal advice or have chosen not

to do so.

I am executing this Acknowledgment and Disclosure for use in conjunction with my existing or

newly- created estate planning documents and any amendments to those documents subsequent

to this date, unless such amendments make a change to the fiduciary succession.

Dated: ______________ __________________________________ CLIENT, Client

STATE OF OKLAHOMA ) ) ss.

COUNTY OF TULSA ) Before me, the undersigned, a Notary Public in and for said County and State, on ________________, 2015, personally appeared CLIENT, to me known to be the identical person who executed the within and foregoing Acknowledgment of Disclosure and acknowledged to me that the same was executed as a free and voluntary act and deed for the uses and purposes therein set forth.

IN WITNESS WHEREOF, I hereunto set my official signature and affixed my notarial seal the day and year last above written.

My Commission Expires: ____________________ _____________________________ Notary Public Commission No.: __________________________

WITNESS ATTESTATION STATE OF OKLAHOMA ) ) ss. COUNTY OF TULSA )

The Client is personally known to me and I believe the Client to be of sound mind. I am eighteen (18) years of age or older. I am not related to the Client by blood or marriage. The Client have declared to me that this instrument is their Acknowledgment of Disclosure and that he or she has willingly made and executed it as his or her free and voluntary act for the purposes herein expressed.

________________________________________ Witness

________________________________________ Witness

STATE OF OKLAHOMA ) ) ss: COUNTY OF TULSA )

Before me, the undersigned, a Notary Public in and for said County and State, on ___________________, 2015, personally appeared _____________________ and ______________________, witnesses, to me known to be the identical persons who executed the within and foregoing instrument, and acknowledged to me that they executed the same as their free and voluntary act and deed for the uses and purposes therein set forth. IN WITNESS WHEREOF, I hereunto set my official signature and affixed my notarial seal the day and year last above written. My Commission Expires: ___________________ ___________________________ Notary Public My Commission No.: ______________________ [S E A L]

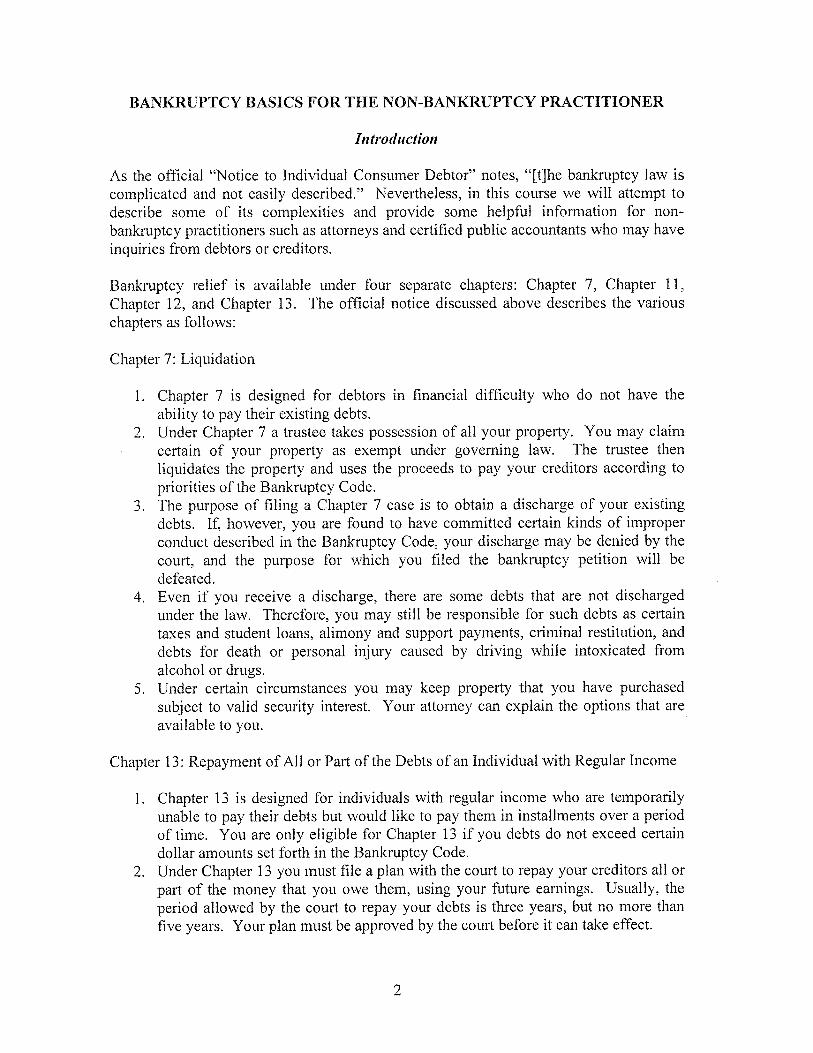

IV. BANKRUPTCY BASICS FOR THE NON-BANKRUPTCY PRACTITIONER

Preston Draper, Attorney

Sweeney, Draper & Christopher Law Firm PO Box 190

1320 Stone Bridge Ada, OK 74820

PHONE: 580-332-7200 EMAIL: [email protected]

V. “I DIDN’T KNOW THAT” – SELECTED TOPICS ON ESTATE PLANNING & ADMINISTRATION

James R. Marshall, Attorney & Partner Henson & Marshall, PLLC

101 W. 9th P.O. Box 3488

Shawnee, OK 74802-3488 Phone # (405) 275-2550