2015 executive pay outlook for mid- cap ... - bdo usa, llp · 2015 executive pay outlook for...

TRANSCRIPT

1

Page 1

2015 EXECUTIVE PAY OUTLOOK FOR MID-CAP COMPANIES – ARE YOU PREPARED?

MARCH 2015

The presentation will begin shortly.Learn Live Customer Support at:

(888) 228-4188 or [email protected]

BDO USA, LLP, a Delaware limited liability partnership, is the U.S.member of BDO International Limited, a UK company limited byguarantee, and forms part of the international BDO network ofindependent member firms.

Page 2

CPE AND SUPPORT

CPE Participation Requirements ‒ To receive CPE credit for this webcast:• You’ll need to actively participate throughout the program.• Be responsive to at least 75% of the participation pop-ups.

Certificate of Attendance:If you are logged in the entire time and respond to all participation pop-ups, you will be able to print your certificate from the “Participation” section at the end of the webcast. If you log out before printing your certificate:• BDO USA professionals ‒ CPE will automatically be issued in CPE Tracking &

Reporting at the end of every week. A copy of your certificate will be sent after you have been issued credit.

• Clients and Contacts and all other individual participants ‒ You will be emailed instructions on how to access your certificate.

2

Page 3

CPE AND SUPPORT (CONTINUED)Group Participation ‒ To receive credit:• Sign-in sheets must list a Proctor name and CPA license number.• Clients and contacts ‒ Email sign-in sheets to [email protected] within 24 hours of the webcast.• BDO USA professionals ‒ Submit your sign-in sheets using a General Training & Development Request in

BDO Service Now found at: BDOWorld > Applications & Resources > BDO Service Now > Click “Service Catalog” in the left menu, then under Training & Development, “Make a Request”.

• Alliance Firm Members ‒ Should proctor their own group participants. This process is detailed in the LearnLive Participant Guide, which can be found by searching “LearnLive Participant Guide” on the Alliance Portal. Call LearnLive Support below for questions.

• International Firm Members ‒ Unfortunately, we cannot currently support group CPE for International Firms. Those wanting CPE must register and log in on their own computer.

Audio by Teleconference:Dial the teleconference number to listen to webcast audio by phone:• Dial: 1-855-233-5756• Enter Conference Code 78779-47566

Q&A:Submit all questions using the Q&A feature on the lower right corner of the screen. At the end of the presentation, the presenter(s) will review and answer all questions submitted.

Technical Support:If you should have technical issues, please contact LearnLive:• Click on the Live Chat icon under the Support tab, OR call: 1-888-228-4088

Page 4

PRESENTERS

• Mike Conover, Senior Director, Compensation & Benefits Practice, BDO USA, LLP [email protected]

• Peter Klinger, Principal, Compensation & Benefits Practice, BDO USA, LLP [email protected]

• Randy Ramirez, Senior Director, Compensation & Benefits Practice, BDO USA, LLP [email protected]

3

Page 5

AGENDA

• BDO 600 Surveys: Current Trends in Pay Levels and Structures for Corporate Executives and Boards

• PCAOB Auditing Standard No. 18 and Executive Compensation• CEO and Median Employee Pay Ratio

Page 6

LEARNING OBJECTIVES

Upon completion of this module, participants will be able to:• Recognize current trends in pay levels and structures for board members, CEOs

and CFOs for further discussions between boards and executives • Discuss the preparations needed for addressing external auditor inquiries about

executive pay now required under the new PCAOB Auditing Standard No. 18 on related parties

• Understand the pending requirement to disclose CEO vs. median employee pay ratio and the implications to consider with regard to employee, shareholder and public relations

4

Page 7

BDO Competitive Compensation ResourcesBDO 600 Surveys – covering the largest and most dynamic types of companies in the US… highlighting trends and practices unique to these companies

• Published for the past 8 years• Focused on mid-market, publicly-held companies• Seven major industry sectors• Pay practices for:- Board of Directors- Chief Executive Officer- Chief Financial Officer

https://www.bdo.com/insights/assurance/client-advisories/the-bdo-600-2

https://www.bdo.com/insights/assurance/client-advisories/the-bdo-600-1

Page 8

Business Press Focuses on Pay for Mega & Large Cap Companies

10% of Public Companies

$10B + - Large Cap $2B-$10B - Mid Cap $300M-$2B - Small Cap $50M-$300M - Micro Cap <$50M

90% of Public Companies - Under-Reported or Not Covered at All

5

Page 9

Mid-Market Companies –Very Different Sized Companies

S&P 500 Average BDO 600 -Average

BDO "C" - $650M -$1.5B

BDO "B" - $325M -$650M

BDO "A" -$25M -$325M

S&P 500 Average $8.5 Billion Revenue

$600M $825M$440M $175M

$8.5B

Page 10

Mid-Market Directors Paid Less Than S&P 500 Counterparts

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$140,000

$250,000

S&P

BDO 600

6

Page 11

Company Size Impacts Director Pay

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

BDO 600 -Average

C - $650M -$1.5B

B - $325M -$650M

A -$25M - $325M

$145,000

$120,000 $105,000Banking

Technology

Average

Page 12

Mid-Market Directors – More in Cash & Options

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Stock Options

Stock Awards

Committee Retainers andFees

Board Retainers and Fees

S&P 500 BDO 600

7

Page 13

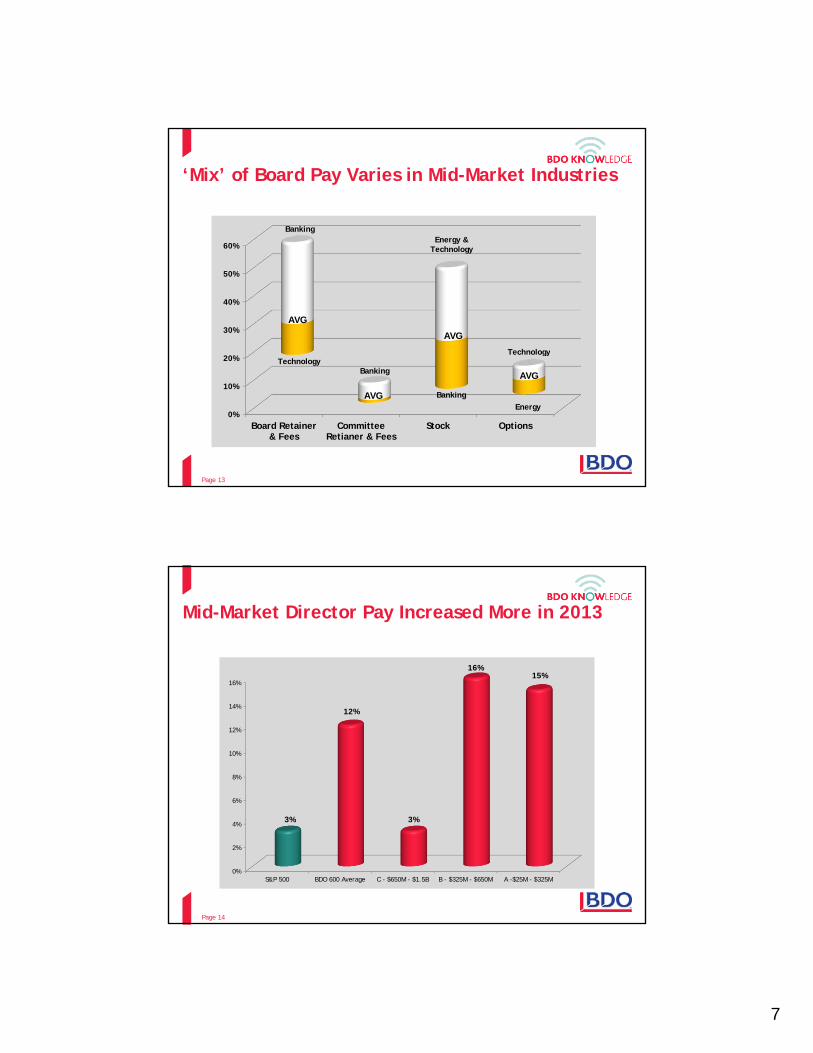

‘Mix’ of Board Pay Varies in Mid-Market Industries

0%

10%

20%

30%

40%

50%

60%

Board Retainer& Fees

CommitteeRetianer & Fees

Stock Options

Technology

Banking

Banking

Energy & Technology

Banking

Technology

Energy

AVG

AVG

AVG

AVG

Page 14

Mid-Market Director Pay Increased More in 2013

0%

2%

4%

6%

8%

10%

12%

14%

16%

S&P 500 BDO 600 Average C - $650M - $1.5B B - $325M - $650M A -$25M - $325M

3%

12%

3%

16%15%

8

Page 15

Mid-Market CEO Pay Vs. S&P 500 CEO

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

S&P 500 BDO 600

$3,000,000

$12,000,000

Page 16

Mid-Market CEOs Saw A Larger Pay Increase in 2013

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

S&P 500 BDO 600

9.8%

12.6%

9

Page 17

Mid-Market CEO Pay ‘Mix’ – Slightly More Cash

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

S&P 500 BDO 600

Other

Equity

Cash

Page 18

Emphasis on Long-Term Incentives for CEO’s Varies by Industry Segment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

LTI

Annual Cash

10

Page 19

CEO / CFO Pay Relationship Among BDO 600 by Company Size

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

BDO 600 Average C - $650M - $1.5B B - $325M - $650M A -$25M - $325M

$3,000,000

$3,350,000

$2,850,000 $2,825,000

$1,158,664$1,248,338

$1,167,169$1,006,746

CEO

CFO

Page 20

CEO / CFO Pay Relationship Among BDO 600 by Industry Segment

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$5,129,629

$4,553,611

$3,733,496

$2,843,206$2,565,726 $2,552,530

$2,310,889

$1,538,230$1,788,635 $1,687,513 $1,554,541

$960,820 $798,103$1,049,741 $995,817

$631,463

CEO CFO

11

Page 21

PCAOB Auditing Standard No. 18 (AS 18)In general: How might the following categories of transactions, which are specifically identified under AS 18, potentially pose risks of material misstatement in a company’s financial statements?• Related party transactions – “their substance might differ materially from

their form”… “involve difficult measurement and recognition issues”… “an opportunity for management to act in its own interests”

• Transactions outside the normal course of business - “significant unusual transactions… may be entered into to obscure a company's financial position or operating results”

• Companies’ financial relationships and transactions with its executives –“…in a unique position to influence a company's accounting and disclosures… can create incentives and pressures for executive officers to meet financial targets…”

New requirements for FY 2015 are designed to strengthen auditor requirements in these three areas.

Page 22

PCAOB AS 18 – Executive Compensation

How does AS 18 amend and emphasize examination by auditors of executive compensation arrangements that were already in place in PCAOB AS 12?

• Requires the auditor to “perform procedures, as a part of the auditor’s risk assessment, to obtain an understanding of the financial arrangements and transactions with its executive officers” – Previously, auditors were expected to consider

• The change intends to “… heighten the auditor's attention to incentives or pressures for the company to achieve a particular financial position or operating result…”

• Recognizes the role executives play in accounting decisions and financial reporting

12

Page 23

PCAOB AS 18 – How Can We Prepare?What should financial management be doing to prepare for auditor questions in this area?Identify covered executives –• Those individuals in positions of significant responsibility• Consider:- Named executive officers- Executives responsible for major business functions or business units- Any others that may be in a position of significant influence of the company

or its financial statements / reportingIdentify and collect pertinent information for all financial relationships and transactions with covered executives -• Consider: Employment agreements, cash bonus and incentive plans, equity

plans, change-in-control and severance agreements, etc.• Proxy Statements and other relevant SEC filings• Discussions with Compensation Committee Chair & Compensation Consultants• Any other types of arrangements

Page 24

PCAOB AS 18 – How Can We Prepare?

What should financial management be doing to prepare for auditor questions in this area?Collect pertinent information for the policies, procedures and responsible parties establishing, authorizing and administering financial relationships and transactions with covered executives, specifically:• Determination of eligibility• Required review and approvals for implementation• Authorization of any modifications of original terms• Required review and approvals for payment, vesting, etc.

13

Page 25

PCAOB AS 18 – What Should We Look For?

What should financial management be doing to prepare for auditor questions in this area?Examine all financial relationships and transactions with covered executives for conformity to established policies and procedures for their implementation / approval

Conduct further examination of those all financial relationships and transactions with these issues:• Missing required review or approvals• Modified arrangements• Overly complex or extraordinarily large award opportunity of questionable

benefit to the company• Etc.

If necessary, consult with the Compensation Committee

Page 26

PCAOB AS 18 – Timing Issues

• Effective for audits of financial statements for fiscal years beginning on or after December 15, 2014, including reviews of interim financial information within these fiscal years – Q1 2015!

• Has your auditor talked to you yet?• What are the potential consequences of having such discussions at the end of

the year?

14

Page 27

SEC’s CEO Pay Ratio

• One of the remaining requirements of the Dodd-Frank legislation is the SEC’s announcement of the implementation of the ratio of the company’s Chief Executive Officer to the company’s median employee ranked on the basis of compensation for ALL company employees excluding the CEO

• The SEC’s previously announced deadline for the final regulations was October 2014

• In November of 2014, the date was revised to “on or before October 2015”• This ratio and the delay in its implementation have strong proponents and

detractors

Page 28

SEC’s CEO Pay Ratio – What Are The Benefits?

SEC comments:

“… neither the statute nor the related legislative history directly states the objectives or intended benefits of the provision.”

“… the lack of a specific market failure identified as motivating the enactment of this provision poses significant challenges in quantifying potential economic benefits, if any, from the pay ratio disclosure.”

15

Page 29

SEC’s CEO Pay Ratio – How Is It Determined?

Principal Executive Officer Annual Compensation:

(Salary + Bonus + Stock Awards + Option Awards + Non-Equity Incentive Plans + Change in pension value and nonqualified deferred compensation earnings + All Other Compensation)

Median Employee Compensation:(Salary + Bonus + Stock Awards + Option Awards + Non-Equity Incentive Plans + Change in pension value and nonqualified deferred compensation earnings + All Other Compensation)

Page 30

SEC’s CEO Pay Ratio –Who Is The Median Employee?

CEO

?

Highest Pay

Lowest Pay

• Part-Time Employee?• Non US Employee?• Seasonal Employee?• Subsidiary Employee?

16

Page 31

SEC’s CEO Pay Ratio –What is Median Employee Pay?

Actual annual pay:• Full time equivalent adjustments for part-time or seasonal employees are NOT

allowed• Adjustments for cost-of-living for non-U.S. workers are NOT allowed• For the identified median employee:

- Employee’s compensation to be calculated according to 402(c)(2)(x) - Employee compensation for the last completed fiscal year to be used NOT the annual period used

in the payroll or tax records

• Use of reasonable estimates is permitted in determining total compensation of employees other than the PEO under Item 402(c)(2)(x)

Page 32

SEC’s CEO Pay Ratio – What Are The Options?

Regulations allow some ‘flexibility’ in terms of the methods used to:• Select the compensation used to ‘rank’ all employees, excluding the CEO• Identify the ‘median employee’• Estimate the total compensation of the ‘median employee’ according to

402(c)(2)(x)You will be required to disclose your methodology

“… the methodology and material assumptions, adjustments and estimates used should provide sufficient information for a reader to be

able to evaluate the appropriateness of the estimates.”

17

Page 33

SEC’s CEO Pay Ratio – What Are Next Steps?

• Companies would be well-advised to undertake this analysis and finalize an approach in advance of the regulations becoming effective.

• The CEO pay ratio will have virtually no value for company-to-company comparisons or year-to-year comparisons for the same company- Different approaches and assumptions used by companies- Fluctuations in company compensation for the CEO (e.g. multi-year vs.

annual grants of equity-based incentives)• However, companies should anticipate and address the implications of the CEO

pay ratio in terms of employee, shareholder and customer perceptions.• Once utilized, any future changes to the methodology must be explained and

the effects of the change disclosed.

Page 34

EVALUATION

We continually try and improve our programming and appreciate constructive feedback.

Following the program, we will be sending out a thank you e-mail that contains a link to a brief evaluation.

Thank you in advance for your participation!

18

Page 35

CONCLUSIONThank you for your participation!Certificate Availability – If you participated the entire time and responded to at least 75% of the polling questions, click the “Participation” tab to access the print certificate button.

Group Participation Reminder – to receive credit:• Sign-in sheets must list a Proctor name and CPA license number.• Clients and Contacts – email sign-in sheets to [email protected] within 24 hours of the webcast.• BDO USA professionals ‒ Submit your sign-in sheets using BDO Service Now.• Alliance Firm Members – Should proctor their own group participants. This process is detailed in the LearnLive Participant Guide on Alliance Portal > Resource Center. Call LearnLive Support for questions – 1-888-228-4088.• International Firm Members - Unfortunately, we cannot currently support group CPE for International Firms. Those requesting CPE must have registered and participated from their own computer.

Please exit the interface by clicking the red “X” in the upper right hand corner of your screen.