©2015, college for financial planning, all rights reserved. welcome

TRANSCRIPT

©2015, College for Financial Planning, all rights reserved.

Welcome

Expectations of Students

• Time/energy commitment• Read assignments before class• Tested on all LOs • This course will enable you to:

o be eligible to sit for theCFP® Certification Examination

o better serve clients/grow your business

o be successful on the College’s end-of-course examination

1-2

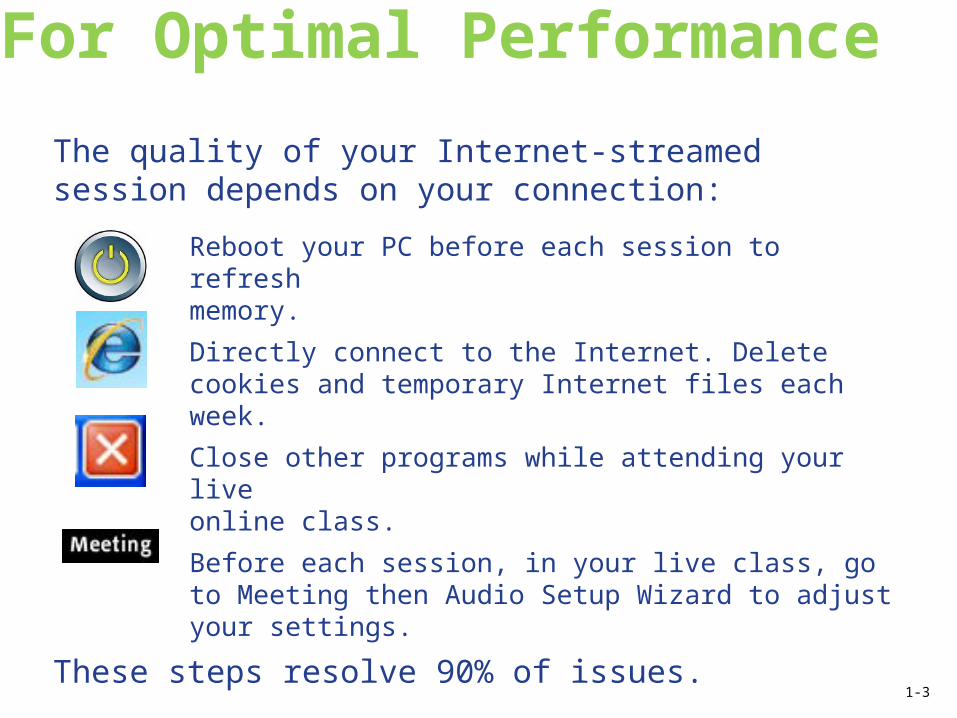

The quality of your Internet-streamed session depends on your connection:

Reboot your PC before each session to refresh memory.

Directly connect to the Internet. Delete cookies and temporary Internet files each week.

Close other programs while attending your live online class.

Before each session, in your live class, go to Meeting then Audio Setup Wizard to adjust your settings.

These steps resolve 90% of issues.

For Optimal Performance

1-3

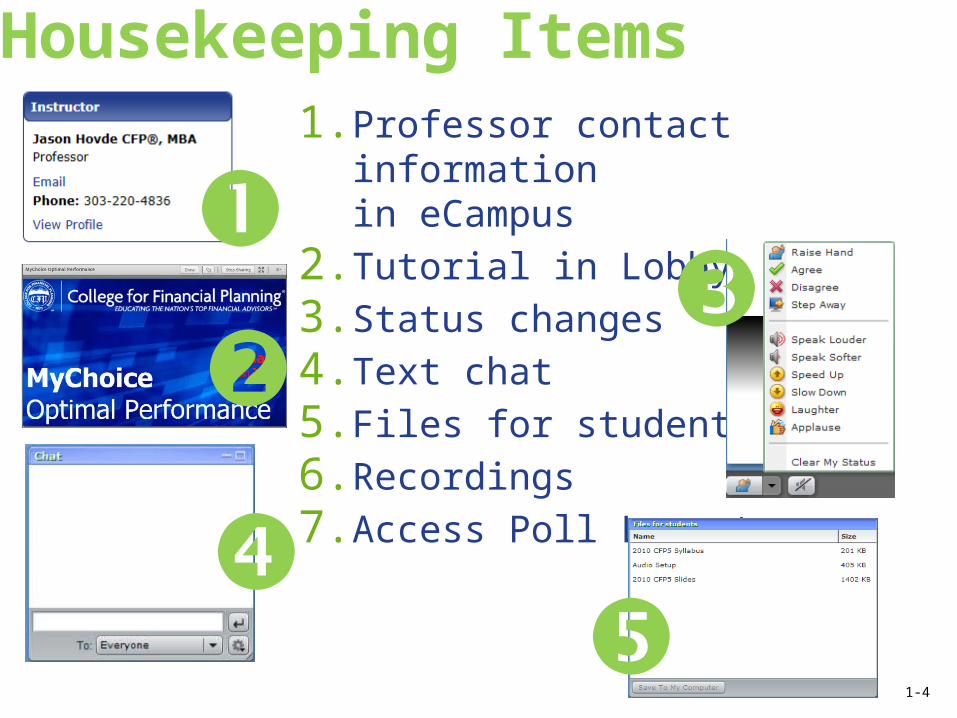

Housekeeping Items1. Professor contact

informationin eCampus

2. Tutorial in Lobby3. Status changes 4. Text chat5. Files for students6. Recordings7. Access Poll Layout

1-4

©2015, College for Financial Planning, all rights reserved.

Session 1Form 1040—Above the Line

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMIncome Tax Planning

Session Details

Module 1

Chapter(s)

1 and 2

LOs 1-1 Describe terms related to income taxation.

1-2 Identify the steps in the tax calculation process.

1-3 Identify items of inclusion, exclusions, deductions, or tax credits.

1-4 Analyze a situation to calculate total income for tax purposes.

1-5 Analyze a situation to calculate adjusted gross income.

1-6

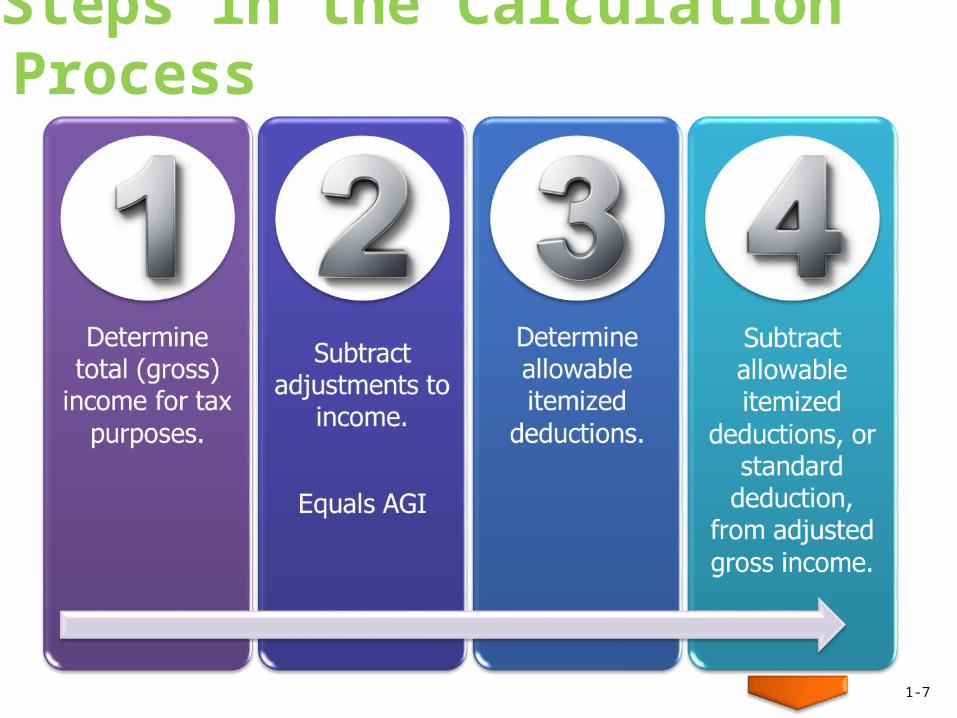

Steps in the Calculation Process

1-7

Steps in the Calculation Process

1-8

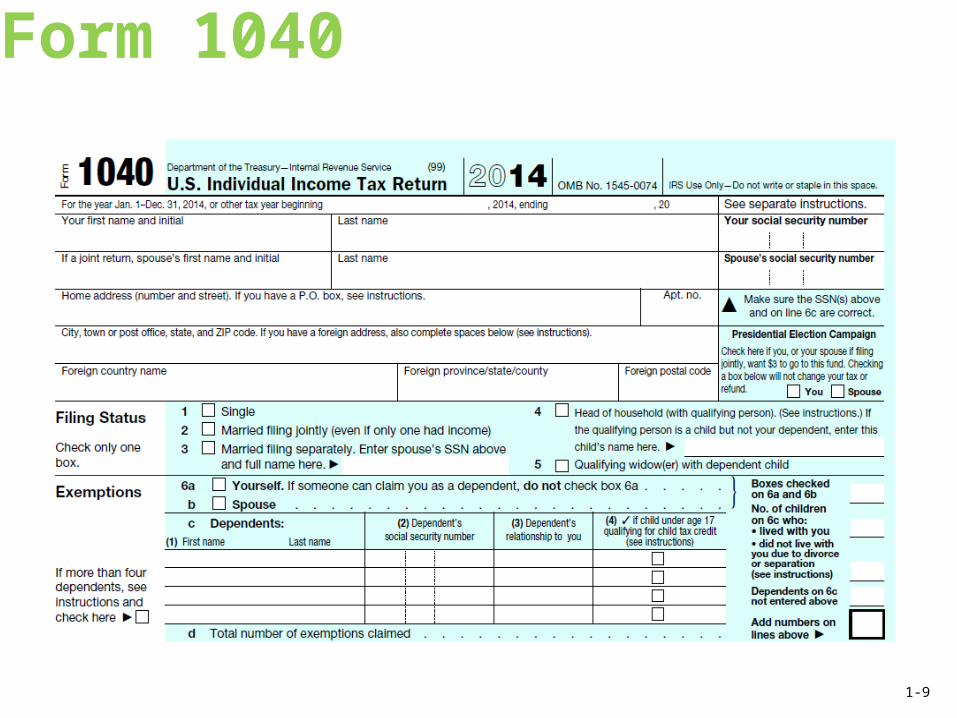

Form 1040

1-9

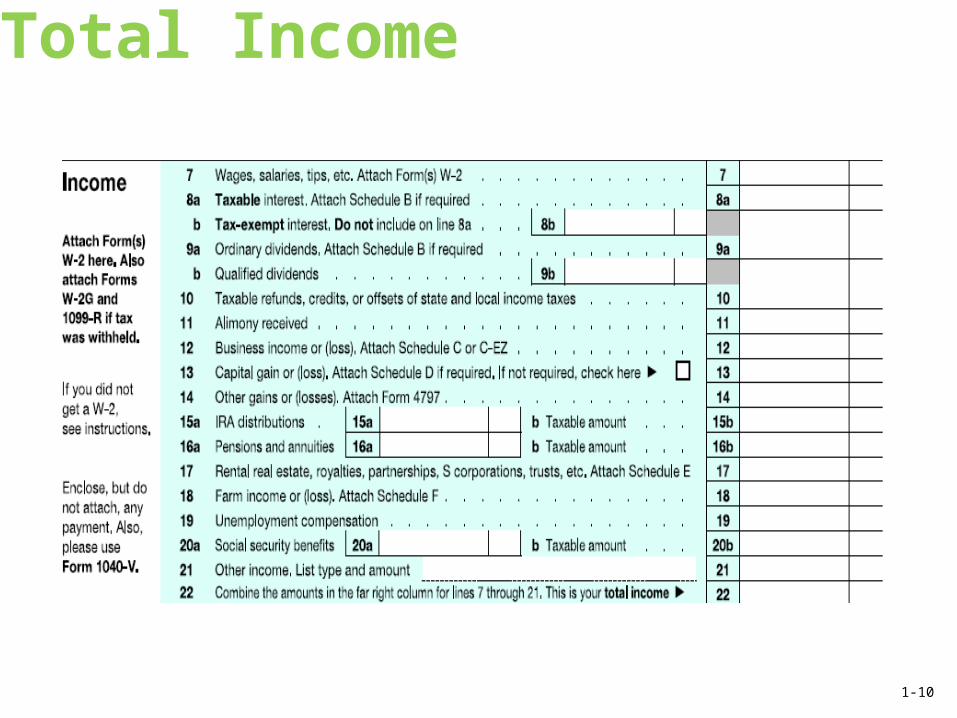

Total Income

1-10

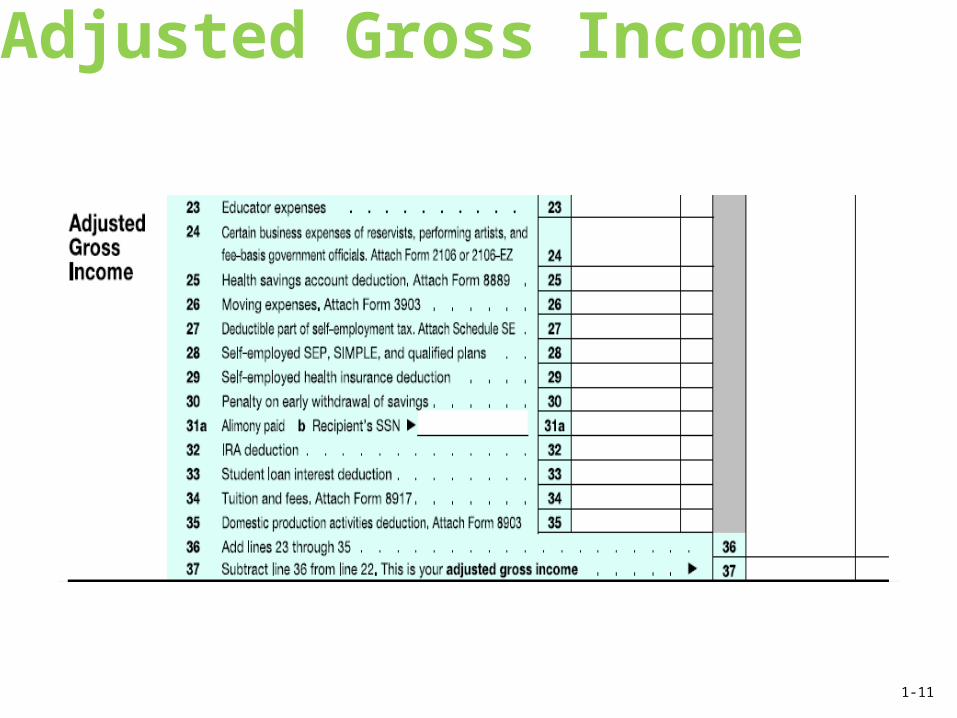

Adjusted Gross Income

1-11

Adjustments to Income• Qualified education (student loan) interest• Educator expense deduction (through 2014)• Tuition and fees deduction (through 2014)• IRA deductions• Keogh contributions (for business owner)• Discrimination lawsuit expenses• Penalty on early withdrawal of savings• Alimony deduction—Module 7• One-half of the self-employment tax—Module

8• Jury duty fees paid over to employerEquals AGI: THE LINE

1-12

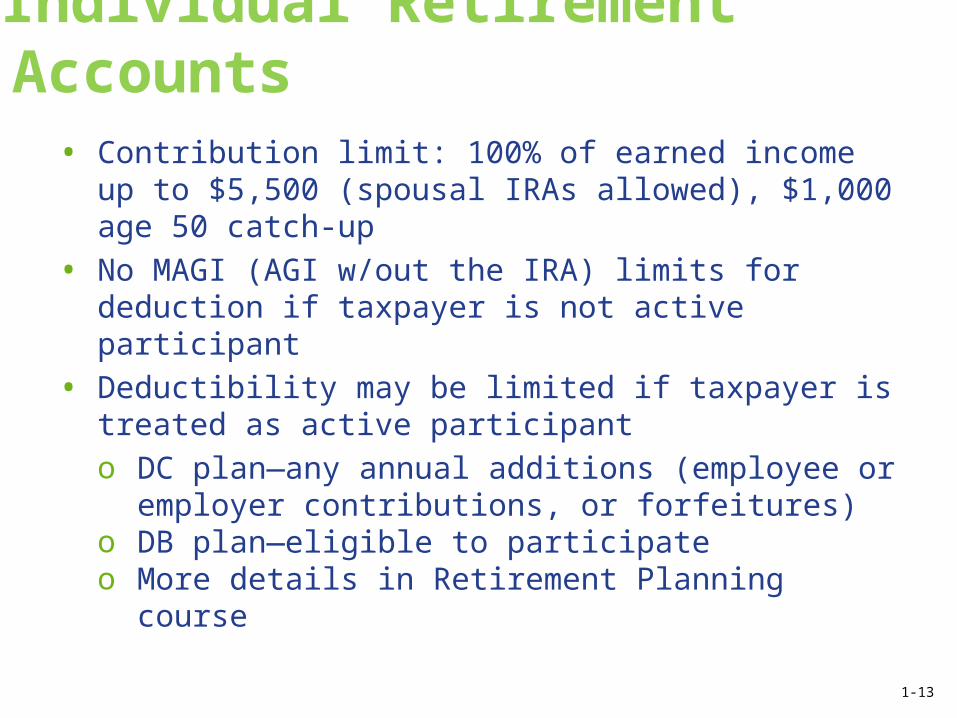

Individual Retirement Accounts

• Contribution limit: 100% of earned income up to $5,500 (spousal IRAs allowed), $1,000 age 50 catch-up

• No MAGI (AGI w/out the IRA) limits for deduction if taxpayer is not active participant

• Deductibility may be limited if taxpayer is treated as active participanto DC plan—any annual additions (employee

or employer contributions, or forfeitures)o DB plan—eligible to participateo More details in Retirement Planning course

1-13

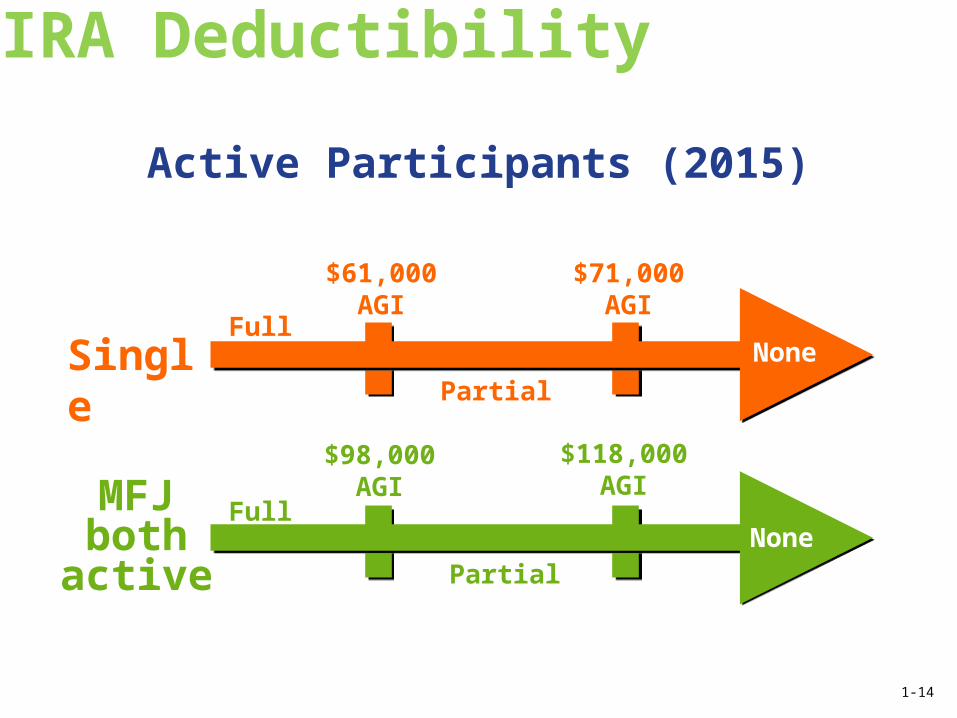

IRA Deductibility

Single

MFJboth

active

Full

$98,000AGI

Full

$61,000AGI

$71,000AGI

$118,000AGI

Partial

Partial

None

None

Active Participants (2015)

1-14

IRA Deductibility

Active Participants (2014)Married Filing Jointly, One Spouse

Active

Active Spous

e

Full

$183,000

AGI Full

$98,000AGI

$118,000AGI

$193,000AGI

Partial

Partial

None

Non-Active Spouse

None

1-15

Basic Tax Planning Techniques

• Tax Avoidanceo Use of exclusions, deductions, and credits

• Tax Deferralo IRAs, pension plans, etc.

• Conversiono Lower rates apply to LTCGs

• Income Shifting (discussed in Module 7)o Allows income to be taxed at potentially

lower rates

1-16

Review Question 1

The following summarizes several financial events in the life of James Grant during the current tax year:o He received a $100,000 inheritance.o He had gambling winnings of $50,000.o He had itemized deductions of $10,000.o He paid student loan interest of $4,200.What is James’ total income for the current tax year?a. $35,800b. $40,000c. $50,000d. $140,000e. $150,000

1-17

Review Question 2

Lowell and Thelma Jordan are married and will file a joint return for the current tax year. They have provided you with the following information:

Based on the information given, what is Lowell and Thelma’s adjusted gross income for the current tax year?

a. $77,000b. $91,200c. $92,000d. $99,200

Lowell’s salaryThelma’s salaryUnemployment compensationNet capital lossPrivate-activity municipal bond interest

$60,000$25,000$10,000$ 8,000$ 4,200

1-18

Review Question 3

Which one of the following is not a step in the tax calculation process?a. Determine total incomeb. Subtract adjustments to income from total

income to get adjusted gross incomec. Deduct the greater of itemized deductions

or the standard deduction from AGId. Determine the personal exemption

amount that can be deductede. Subtract credits from taxable income to

compute net tax due

1-19

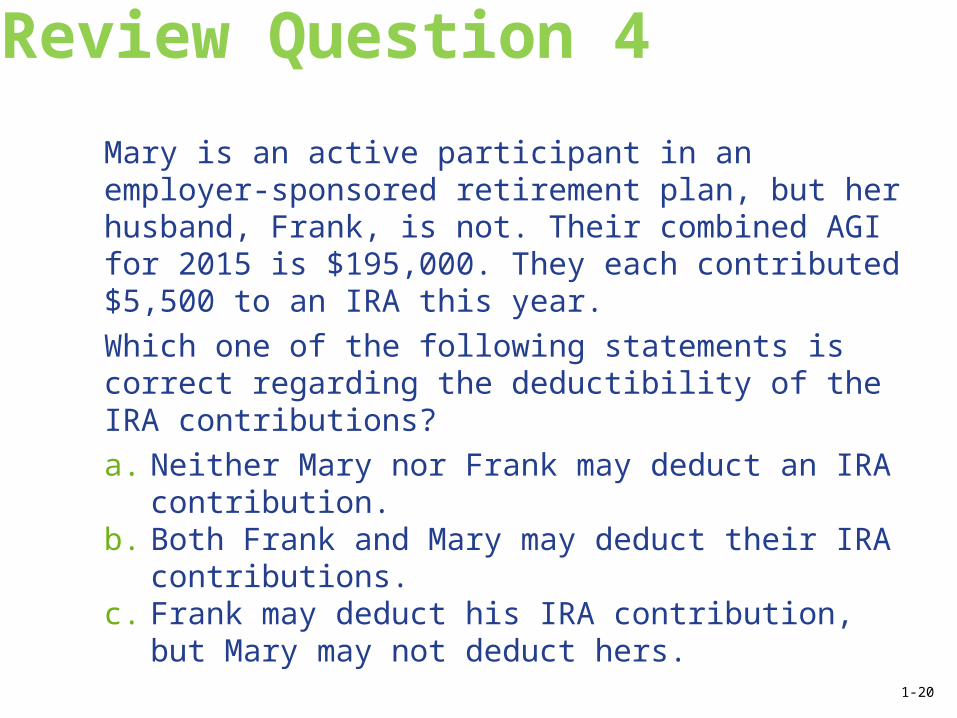

Review Question 4

Mary is an active participant in an employer-sponsored retirement plan, but her husband, Frank, is not. Their combined AGI for 2015 is $195,000. They each contributed $5,500 to an IRA this year. Which one of the following statements is correct regarding the deductibility of the IRA contributions?a. Neither Mary nor Frank may deduct an IRA

contribution.b. Both Frank and Mary may deduct their IRA

contributions.c. Frank may deduct his IRA contribution, but

Mary may not deduct hers. 1-20

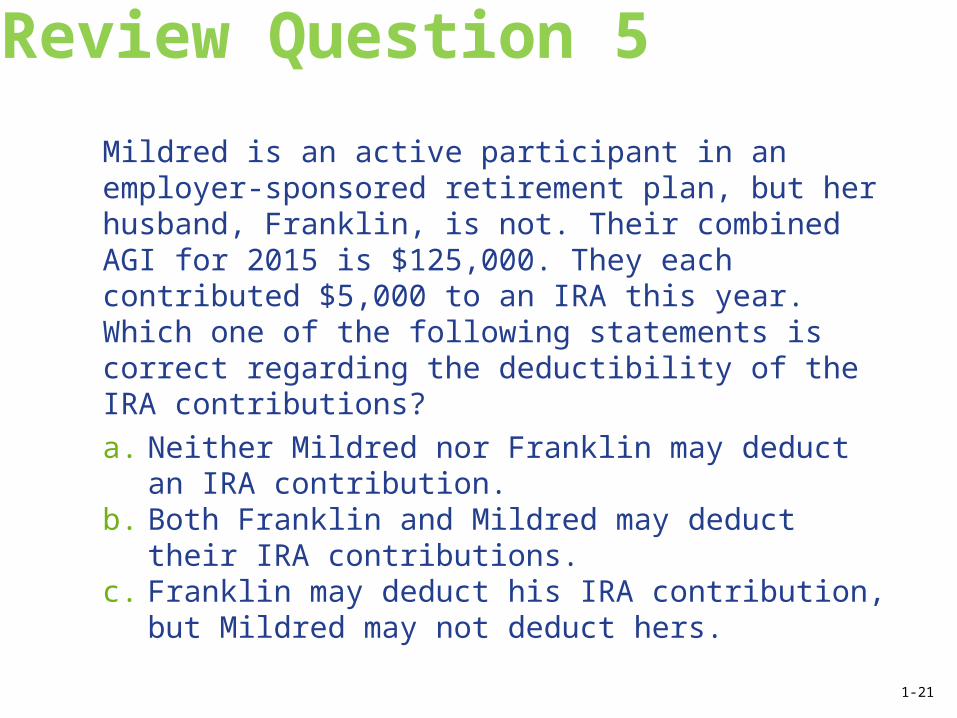

Review Question 5

Mildred is an active participant in an employer-sponsored retirement plan, but her husband, Franklin, is not. Their combined AGI for 2015 is $125,000. They each contributed $5,000 to an IRA this year. Which one of the following statements is correct regarding the deductibility of the IRA contributions?a. Neither Mildred nor Franklin may deduct an

IRA contribution.b. Both Franklin and Mildred may deduct their

IRA contributions.c. Franklin may deduct his IRA contribution, but

Mildred may not deduct hers.

1-21

©2015, College for Financial Planning, all rights reserved.

Session 1End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMIncome Tax Planning