2015 06-27 wcce-bielecki_handout

TRANSCRIPT

Introduction Model Scenarios Calibration Results

The shadow of longevity – does social security reformreduce gains from increasing the retirement age?

with Karolina Goraus, Krzysztof Makarski and Joanna Tyrowicz

Marcin Bielecki

Faculty of Economics, University of Warsaw

First World Congress of Comparative EconomicsRome, 25-27 June 2015

1 / 30

Introduction Model Scenarios Calibration Results

Motivation

Major issues in pension economics:increasing old-age dependency ratiomajority of pension systems fail to assure actuarial fairnessin most countries people tend to retire as early as legally allowed

Typical reform proposals

switch to DC systems and strengthen the linkbetween contributions and benefitsraise the social security contribution ratecut government expenditureincrease minimum eligibility retirement age

2 / 30

Introduction Model Scenarios Calibration Results

Effective retirement age in OECD

3 / 30

Introduction Model Scenarios Calibration Results

Participation rates in OECD

4 / 30

Introduction Model Scenarios Calibration Results

Outline

1 Introduction

2 Model

3 Scenarios

4 Calibration

5 Results

5 / 30

Introduction Model Scenarios Calibration Results

Literature reviewTwo streams of literature:

1 Answering the question about optimal retirement ageGruber and Wise (2007), Galasso (2008), Heijdra and Romp (2009)

2 Comparing different pensions system reforms: increasing retirement agevs cut in benefits/privatization of the system/...Auerbach et al. (1989), Hviding and Marette (1998), Fehr (2000),Boersch-Supan and Ludwig (2010), Vogel et al. (2012)

Fehr (2000)Macroeconomic effects of retirement age increase may depend on the existingrelation between contributions and benefits

Remaining gaps in the literature

how the macroeconomic effects differ between various pension systems?

what happens to the welfare of each affected generation and why?

6 / 30

Introduction Model Scenarios Calibration Results

Goals and expectations

GoalAnalyse macroeconomic and welfare implications of retirement ageincrease under DB (defined benefit), NDC (notionally definedcontribution) and FDC (funded defined contribution) systems

Expectations

under DB: leisure ↓, taxes ↓, welfare?under DC: leisure ↓, pensions ↑, welfare?difference between FDC & NDC: pricing of capital?

Why a full model? Labor supply adjustments & GE effects

7 / 30

Introduction Model Scenarios Calibration Results

Model structure: consumers I

”born” at age 20 (j = 1) and live up to 100 years (J = 80)subject to time and cohort dependent survival probability πchoose labor supply l endogenously until exogenousretirement age J̄ (forced to retire)

optimize remaining lifetime utility derived from leisure 1− land consumption c

Uj,t =J−j∑s=0

[δsπj+s,t+sπj,t

u(cj+s,t+s, lj+s,t+s)]

with

u(c, l) = log(cφ(1− l)1−φ)

8 / 30

Introduction Model Scenarios Calibration Results

Model structure: consumers II

receive market clearing wage for laborreceive market clearing interest rate on private savingsreceive pension incomereceive unintentional bequestspay taxes

Subject to the budget constraint

(1 + τ ct )cj,t + sj,t = (1− τ lt )(1− τ ι)wj,tlj,t ← labor income+ (1 + (1− τkt )rt)sj−1,t−1 ← capital income+ (1− τ lt )pιj,t ← pension income+ bj,t ← bequests−Υt ← lump-sum tax

9 / 30

Introduction Model Scenarios Calibration Results

Model structure: producers

perfectly competitive representative firmstandard Cobb-Douglas production function

Yt = Kαt (ztLt)1−α

profit maximization implies

wt = zt(1− α)kαtrt = αkα−1

t − d

with k ≡ KzL

10 / 30

Introduction Model Scenarios Calibration Results

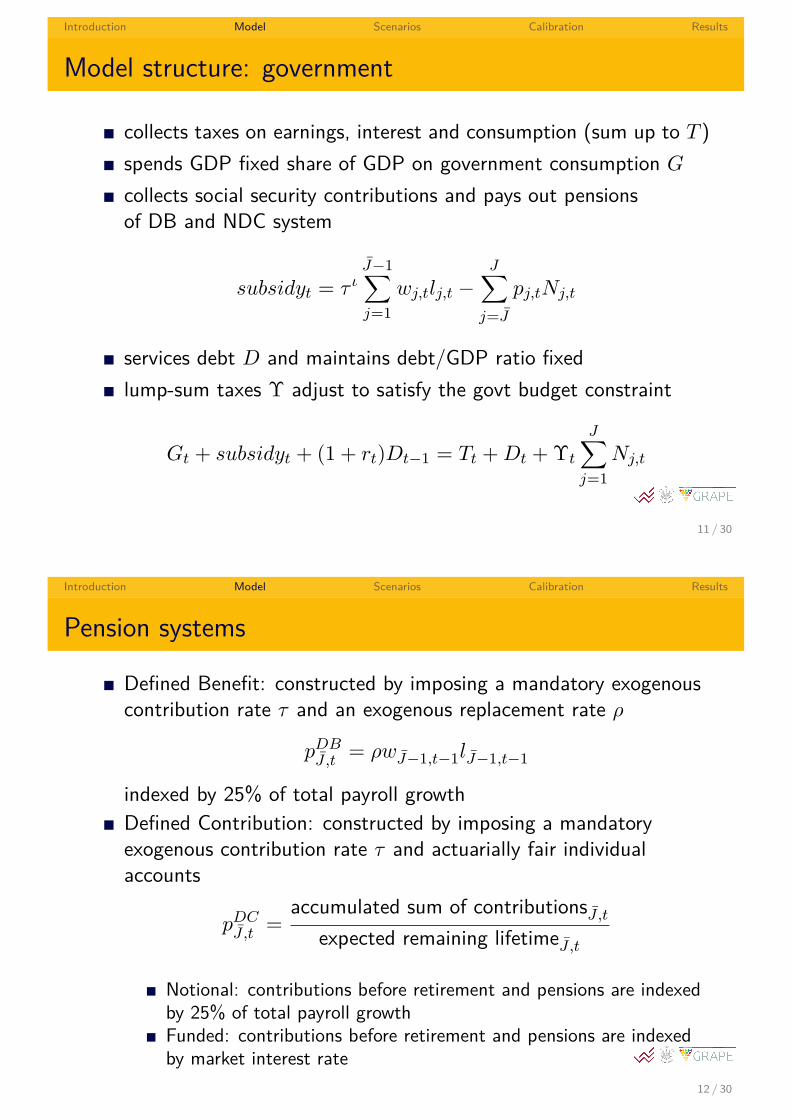

Model structure: government

collects taxes on earnings, interest and consumption (sum up to T )spends GDP fixed share of GDP on government consumption Gcollects social security contributions and pays out pensionsof DB and NDC system

subsidyt = τ ιJ̄−1∑j=1

wj,tlj,t −J∑j=J̄

pj,tNj,t

services debt D and maintains debt/GDP ratio fixedlump-sum taxes Υ adjust to satisfy the govt budget constraint

Gt + subsidyt + (1 + rt)Dt−1 = Tt +Dt + Υt

J∑j=1

Nj,t

11 / 30

Introduction Model Scenarios Calibration Results

Pension systems

Defined Benefit: constructed by imposing a mandatory exogenouscontribution rate τ and an exogenous replacement rate ρ

pDBJ̄,t

= ρwJ̄−1,t−1lJ̄−1,t−1

indexed by 25% of total payroll growthDefined Contribution: constructed by imposing a mandatoryexogenous contribution rate τ and actuarially fair individualaccounts

pDCJ̄,t

=accumulated sum of contributionsJ̄ ,t

expected remaining lifetimeJ̄ ,t

Notional: contributions before retirement and pensions are indexedby 25% of total payroll growthFunded: contributions before retirement and pensions are indexedby market interest rate

12 / 30

Introduction Model Scenarios Calibration Results

What we do

What happens within each experiment?

1 Run the no policy change scenario ⇒ baseline2 Run the policy change scenario ⇒ reform3 For each cohort compare utility, compensate the losers from the

winners4 If net effect positive ⇒ reform efficient

Welfare analysis – like Nishiyama & Smetters (2007)Macroeconomic analysis

13 / 30

Introduction Model Scenarios Calibration Results

Reforms

Three experiments:

1 DB with flat retirement age → DB with increasing retirement age

2 NDC with flat retirement age → NDC with increasing retirement age

3 FDC with flat retirement age → FDC with increasing retirement age

Increasing retirement age

14 / 30

Introduction Model Scenarios Calibration Results

Robustness: age-productivity profile

Heterogeneity between cohorts due to age-specific productivity: wj,t = ωjwt

Deaton (1997) decomposition on Polish LFS data15 / 30

Introduction Model Scenarios Calibration Results

Calibration to replicate 1999 economy of Poland

Preference for leisure (φ) chosen to match participation rate of 56.8%

Impatience (δ) chosen to match interest rate of 7.4%

Replacement rate (ρ) chosen to match benefits/GDP ratio of 5%

Contributions rate (τ) chosen to match SIF deficit/GDP ratio of 0.8%

Labor income tax (τ l) set to match PIT/GDP ratio

Consumption tax (τ c) set to match VAT/GDP ratio

Capital income tax (τk) set de iure = de facto

16 / 30

Introduction Model Scenarios Calibration Results

Calibrated parameters

Age-productivity profileω – D97 ω = 1

α capital share 0.31 0.31τ l labor income tax 0.11 0.11τ c consumption tax 0.11 0.11τk capital income tax 0.19 0.19φ leisure-consumption preference 0.578 0.526δ discounting rate 0.998 0.979d depreciation rate 0.045 0.045τ social security contribution 0.060 0.060ρ replacement rate 0.138 0.227

resulting(dk)/y investment rate 21 21r interest rate 7.4 7.4

17 / 30

Introduction Model Scenarios Calibration Results

Exogenous processes in the model I

Demographic projection until 2060, after that 80 years, and afterthat “new steady state”“Births” of 20-year olds from the projection, constant afterwardsMortality rates from the projection, constant afterwards

18 / 30

Introduction Model Scenarios Calibration Results

Exogenous processes in the model II

Productivity growth

Labor augmenting productivity parameter zProjection from AWG, after that “new steady state”, 1.7%

19 / 30

Introduction Model Scenarios Calibration Results

Is the reform efficient?

Yes!

Net consumption equivalent ω – D97 ω = 1DB 9.88% 3.70%Transition to NDC 11.31% 4.41%Transition to FDC 11.81% 4.70%

20 / 30

Introduction Model Scenarios Calibration Results

Everybody gains

21 / 30

Introduction Model Scenarios Calibration Results

Why they gain? Benefits under DC systems ...

22 / 30

Introduction Model Scenarios Calibration Results

... and taxes under DB system

SIF deficit

Lump-sum taxes

23 / 30

Introduction Model Scenarios Calibration Results

Is there any behavioral response? Of course!

24 / 30

Introduction Model Scenarios Calibration Results

Labor supply in the final steady state

Labor supply Labor supply with MERA increase(no reform) j < 60 j ≥ 60 Total

Average Average Aggregate Average Aggregate(base=100%) (base=100%)

DB 63.2% 59.6% 94.4% 71.8% 113.7%NDC 62.0% 58.8% 94.8% 72.3% 114.7%FDC 61.7% 59.0% 95.5% 72.2% 115.4%

25 / 30

Introduction Model Scenarios Calibration Results

Aggregate labor supply (in millions of individuals)

26 / 30

Introduction Model Scenarios Calibration Results

Capital per effective unit of labor decreases ...

27 / 30

Introduction Model Scenarios Calibration Results

... but mostly due to decrease in “precautionary savings”

28 / 30

Introduction Model Scenarios Calibration Results

Conclusions

extending the retirement age is universally welfare enhancingsome downward adjustment in individual labor supply,but the aggregate labor supply increaseseffects on capital are “overstated”

29 / 30

Introduction Model Scenarios Calibration Results

Thank you for your attention!

Questions or suggestions?

30 / 30