2014 real estate update - deloitte · · 2018-02-252014 real estate industry update ... jason...

TRANSCRIPT

2014 Real Estate Industry Update Breaking new boundaries: Paving the way for the future Diana Laing

Chief Financial Officer

American Homes 4 Rent

Dr. Richard Green

Director

USC Rusk Center for Real Estate

Lauralee Martin

President & Chief Executive Officer

HCP, Inc.

Bob O'Brien

U.S. and Global Deloitte Real Estate Leader

Deloitte & Touche LLP

Jason Keller

Managing Director

Oaktree Capital Management

2014 Real

Estate Update

Breaking New

Boundaries: Paving

the way for the future

Chris Dubrowski

Industry Professional Practice Director

Deloitte Real Estate

Deloitte & Touche LLP

Johnnie Akin

National Office Senior Manager

Deloitte Real Estate

Deloitte & Touche LLP

3 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Agenda

Standards Setting

Projects Impacting Real Estate

Regulatory Update

4 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• This presentation does not provide official Deloitte & Touche LLP

interpretive accounting guidance

• The views expressed are solely those of the presenter and are not

formal Deloitte & Touche LLP positions

• Check with a qualified advisor before taking any action

• See slides at the end for additional resources available on these topics

Disclaimer

Standards Setting

Where are we and where are we going?

6 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Convergence progress in 2013 and 2014 • Approximately 30 FASB meetings and 20 IASB meetings

• In addition, approximately 10 Joint FASB/IASB meetings

• The majority of the FASB meetings included convergence topics

• The Boards have also held several education sessions and roundtables

• Project Current Path

− Revenue recognition (Issued) Converged

− FI - classification and measurement Diverged

− FI – impairment Diverged

− Leases Partially Converged

− Investment companies (Issued) Substantially Converged

− Consolidation Diverged

7 Copyright © 2014 Deloitte Development LLC. All rights reserved.

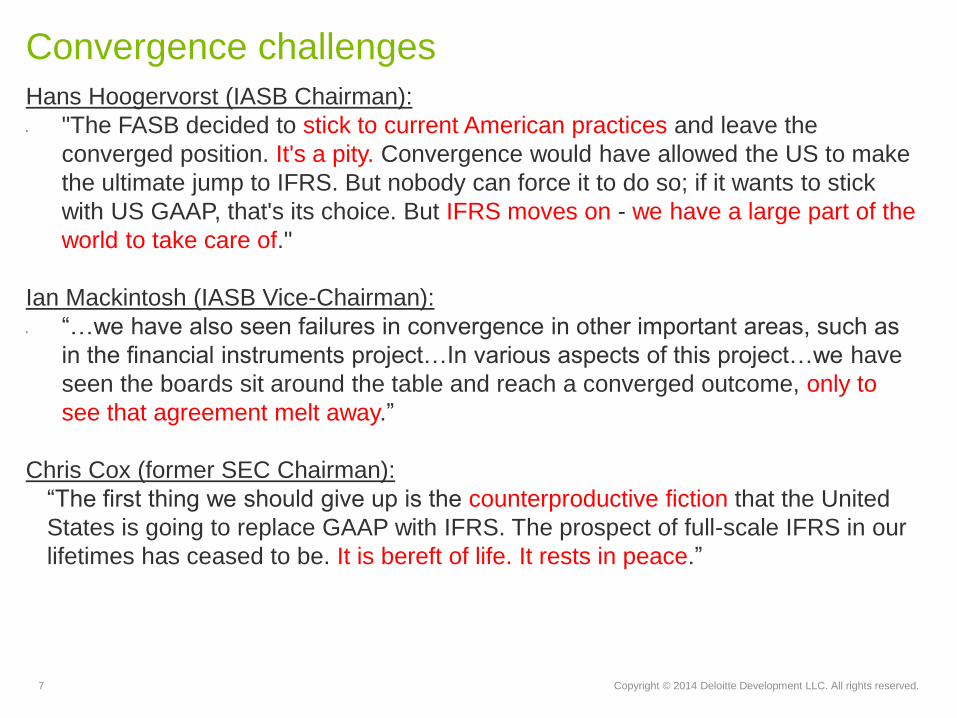

Convergence challenges

Hans Hoogervorst (IASB Chairman):

• "The FASB decided to stick to current American practices and leave the

converged position. It's a pity. Convergence would have allowed the US to make

the ultimate jump to IFRS. But nobody can force it to do so; if it wants to stick

with US GAAP, that's its choice. But IFRS moves on - we have a large part of the

world to take care of."

Ian Mackintosh (IASB Vice-Chairman):

• “…we have also seen failures in convergence in other important areas, such as

in the financial instruments project…In various aspects of this project…we have

seen the boards sit around the table and reach a converged outcome, only to

see that agreement melt away.”

Chris Cox (former SEC Chairman):

“The first thing we should give up is the counterproductive fiction that the United

States is going to replace GAAP with IFRS. The prospect of full-scale IFRS in our

lifetimes has ceased to be. It is bereft of life. It rests in peace.”

8 Copyright © 2014 Deloitte Development LLC. All rights reserved.

FASB member IASB members Staff

Ja

n E

ng

str

om

(Sw

ed

en

)

Ma

rc S

eig

el

Sta

ff

Sta

ff

Sta

ff

Sta

ff

Sta

ff

Pat

Fin

ne

ga

n

(Un

ited

Sta

tes

)

Da

ryl

Bu

ck

Da

rre

l S

co

tt

(So

uth

Afr

ica)

Larry Smith Zhang Wei-Guo

(China)

Martin Edelmann

(Germany)

Steve Cooper

(United Kingdom)

Hal

Schroeder Jim Kroeker

Chungwoo

Suh (Korea)

Mary Tokar

(United States)

Gary Kabureck

(United States) Tom Linsmeier

Sue Lloyd

(Australia / U.K.)

Philippe Danjou

(France)

Ta

ka

tsu

gu

Oc

hi

(Jap

an

)

Am

aro

Go

me

s

(Bra

zil)

FA

SB

Dir

ec

tor

Sta

ff L

ea

d P

M

Ru

ss

Go

lde

n

Ha

ns

Ho

og

erv

ors

t

(Ne

the

rla

nd

s)

Ian

Ma

cin

tos

h

(Au

str

alia)

Sta

ff L

ea

d

IAS

B D

ire

cto

r

IASB and FASB Meeting —

March 18–19, 2014

Why this is so difficult

Projects Impacting the Real Estate Industry Where are we and where are we going?

10 Copyright © 2014 Deloitte Development LLC. All rights reserved.

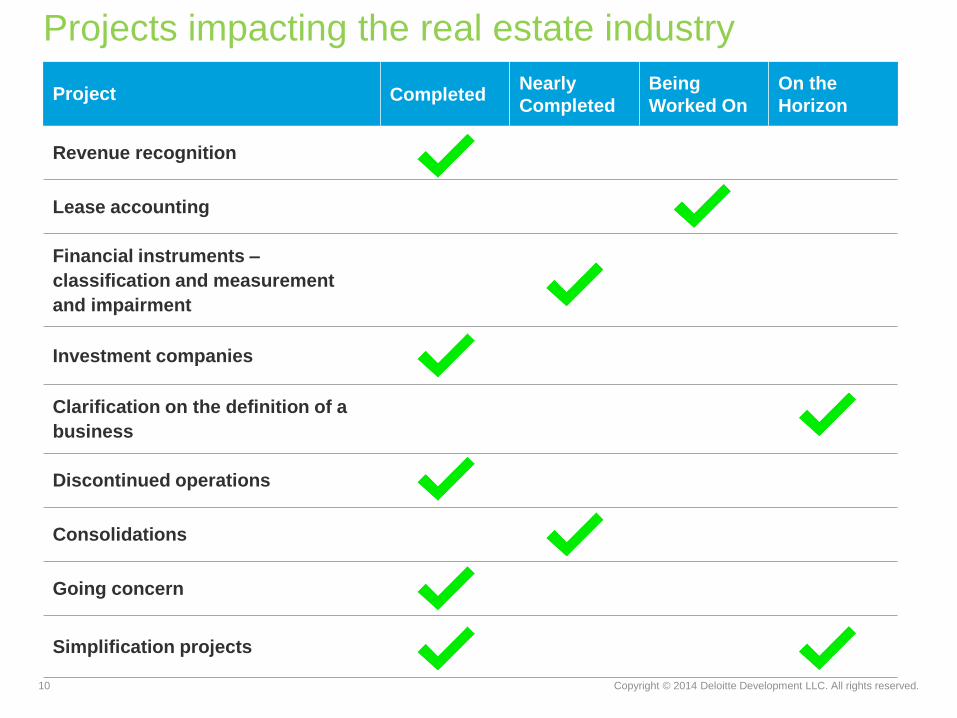

Projects impacting the real estate industry

Project Completed Nearly

Completed

Being

Worked On

On the

Horizon

Revenue recognition

Lease accounting

Financial instruments –

classification and measurement

and impairment

Investment companies

Clarification on the definition of a

business

Discontinued operations

Consolidations

Going concern

Simplification projects

Clarification - the

Definition of a Business

12 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Current GAAP is inconsistent – Commercial property acquisitions are

generally business combinations, but dispositions are treated as sales of

real estate assets

Asset or entity-based guidance

The Real Estate Conundrum

Governing guidance:

ASC 360-20, Real Estate Sales

Based on a “CONTINUING INVOLVEMENT” model

Governing guidance:

ASC 805, Business Combinations

Based on a “CONTROL” model.

Required to assess acquisitions as businesses and sales as assets.

Sales of Real Estate Acquisitions of Real Estate

13 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Summary of other differences

Asset Business

Contingent

Consideration

Not recognized until the

contingency is resolved

Recognized at the acquisition

date fair value while changes in

estimate are trued-up through

earnings after the acquisition

date

Acquisition-related

costs

Capitalized Expensed

Initial measurement Allocated cost on a relative fair

value basis

Measured at fair value

Goodwill N/A Recognized as an asset and

reassessed annually

Bargain purchase

gain

N/A

Recognized immediately in

earnings as a gain

Asset or entity-based guidance

14 Copyright © 2014 Deloitte Development LLC. All rights reserved.

The FASB has added a project that will:

• Determine whether asset-based or business-based accounting literature would apply to

entities that substantially consist of non-financial assets (e.g., in-substance real estate)

• Reassess the definition of a business – project may be narrow or wide ranging

The project will address the existing accounting differences between

asset-based and business-based guidance that include:

• The measurement and timing of gain or loss recognition on sales of assets when

continuing involvement exists, including situations whereby companies sell partial

interests; and

• The measurement of retained interests that occur when a company sells a partial

interest in an asset

For the recently finalized revenue guidance, from whose perspective do

you evaluate “control” in a partial sale? If I sell you a part of an asset and

we now have joint control, I have given up “control” but you haven’t taken

“control”!

Asset or entity-based guidance

15 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Conflict of accounting treatment on partial sales

Transaction ASC 810 (FAS 160) Accounting Treatment

ASC 360-20 (FAS 66) Accounting Treatment

Sell 50% interest and lose control

Gain on the 50% interest sold AND for

the difference between FV and

carrying amount of 50% retained

Business

Gain only on the 50% interest sold; retained interest stays at book value

Asset

16 Copyright © 2014 Deloitte Development LLC. All rights reserved.

REIT has a wholly-owned subsidiary whose sole asset is a building that

has a carrying value of $800 and a fair value of $1,000. REIT agrees

to sell 20% of its interest to an investor for $200. REIT continues to

have a controlling interest and consolidates the subsidiary.

Question: What literature governs REIT’s accounting for this

transaction?

Question: What is REIT’s accounting?

In the case of a partial sale that does not result in deconsolidation, both

ASC 810 and ASC 360-20 would prohibit the derecognition of the asset

and the recognition of the gain at the transaction date.

Partial sale guidance – control retained

17 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Under ASC 810-10, the noncontrolling interest would be initially measured at the

investor’s proportionate share of the subsidiary’s book value with the difference

between the amount paid and the amount recognized for the noncontrolling

interest being recorded to APIC.

The journal entry to record the transaction:

Cash $200

Noncontrolling interest (800 X 20%) $160

Additional paid-in-capital 40

Under ASC 360-20, the sale of in-substance real estate would require the gain on

sale be deferred and recognized on a pro-rata basis over the life of the asset or

when the asset is sold.

The journal entry to record the transaction:

Cash $200

Noncontrolling interest $160

Deferred gain 40

Partial sale guidance – control retained

Revenue Recognition

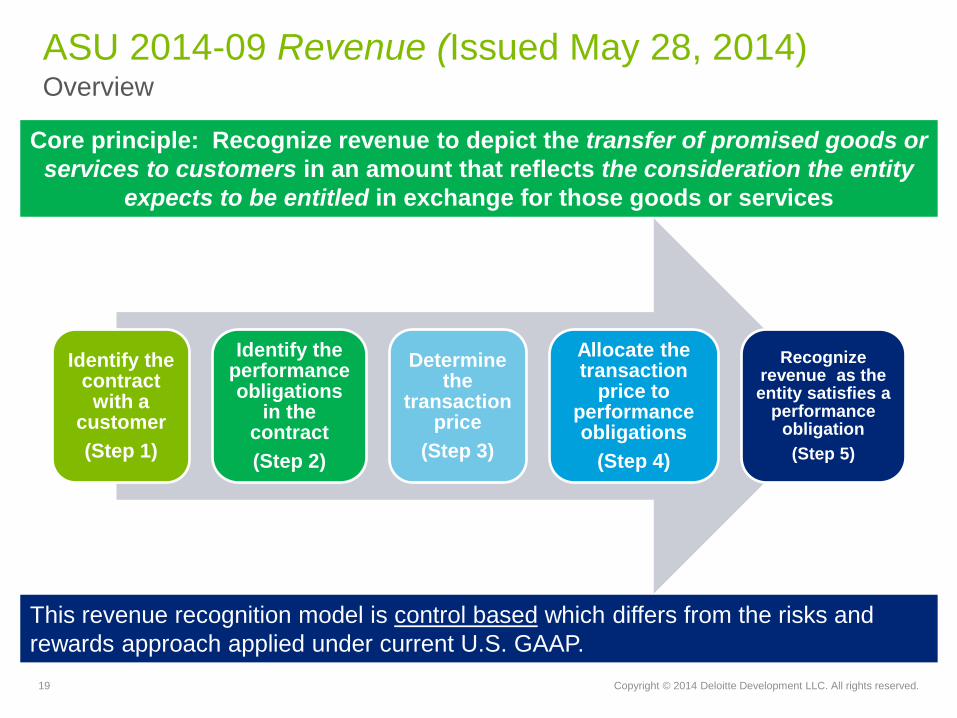

19 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Identify the contract

with a customer

(Step 1)

Identify the performance obligations

in the contract

(Step 2)

Determine the

transaction price

(Step 3)

Allocate the transaction

price to performance obligations

(Step 4)

Recognize revenue as the entity satisfies a

performance obligation

(Step 5)

Overview

ASU 2014-09 Revenue (Issued May 28, 2014)

Core principle: Recognize revenue to depict the transfer of promised goods or

services to customers in an amount that reflects the consideration the entity

expects to be entitled in exchange for those goods or services

This revenue recognition model is control based which differs from the risks and

rewards approach applied under current U.S. GAAP.

20 Copyright © 2014 Deloitte Development LLC. All rights reserved.

− Applies to an entity’s contracts with customers

− Applies to a transfer or sale of nonfinancial assets (such as real estate)

that do not meet the definition of a business. Also includes “in-

substance assets”

− Partial sales of nonfinancial assets are not addressed

− Does not apply to real estate sale-leaseback transactions (continue to

follow current GAAP)

− Does not apply to:

• Lease contracts (ASC 840),

• Insurance contracts (ASC 944),

• Certain financial instruments and other contractual rights or obligations,

• Guarantees (other than product or service warranties), and

• Nonmonetary exchanges to facilitate a sale to another party

Scope

Revenue ASU

21 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Prescriptive guidance provided by ASC 360-20 (Sales of Real Estate) and

ASC 605 (Construction) will be lost:

− Buyer’s financial commitment - Guarantee buyer return

− Collectibility of transaction price - Partial sales

− Continuing involvement by seller - Condominium sales

− Sales to limited partnerships/joint ventures

• Will likely result in more transactions qualifying as sales of real estate with

gains being accelerated

Example: Consider probability of a conditional repurchase obligation outside the seller’s

control

• Collectibility threshold was changed

Must be probable (not necessarily reasonably assured) that the entity will ultimately

collect the consideration it is entitled to receive

Potential effects on real estate Elimination of bright-line tests

22 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Revenue project Effective date

Early application is

NOT permitted

• Public entities:

‒ Annual reporting periods beginning after December 15, 2016, including interim

reporting periods therein (FY 2017)

‒ Early application not permitted

• Non-public entities:

‒ Annual reporting periods beginning after December 15, 2017, including interim

reporting periods therein (FY 2018)

‒ May elect to adopt earlier under one of two alternatives, which for a calendar

year entity would be:

• The public company effective date

• Fiscal year end 2017, and interim periods during 2018

• At the October 31, 2014 meeting, James Kroeker, the FASB vice

chairman, emphasized that the Board is considering whether to

defer the effective date and noted that a decision will be made no

later than the second quarter of 2015.

23 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Revenue project Transition options

January 1, 2017

Initial Application Year

2017

Current Year

2016

Prior Year 1

2015

Prior Year 2

New contracts New ASU

Existing contracts New ASU + cumulative

catch up

Legacy GAAP Legacy GAAP

Completed contracts Legacy GAAP Legacy GAAP

cumulative catch-up

• Full Retrospective Approach

‒ Restate prior periods in compliance with ASC 250

• Modified Retrospective Approach

‒ Apply revenue standard to contracts not completed as of effective date and

record cumulative catch up

‒ Public entity example:

24 Copyright © 2014 Deloitte Development LLC. All rights reserved.

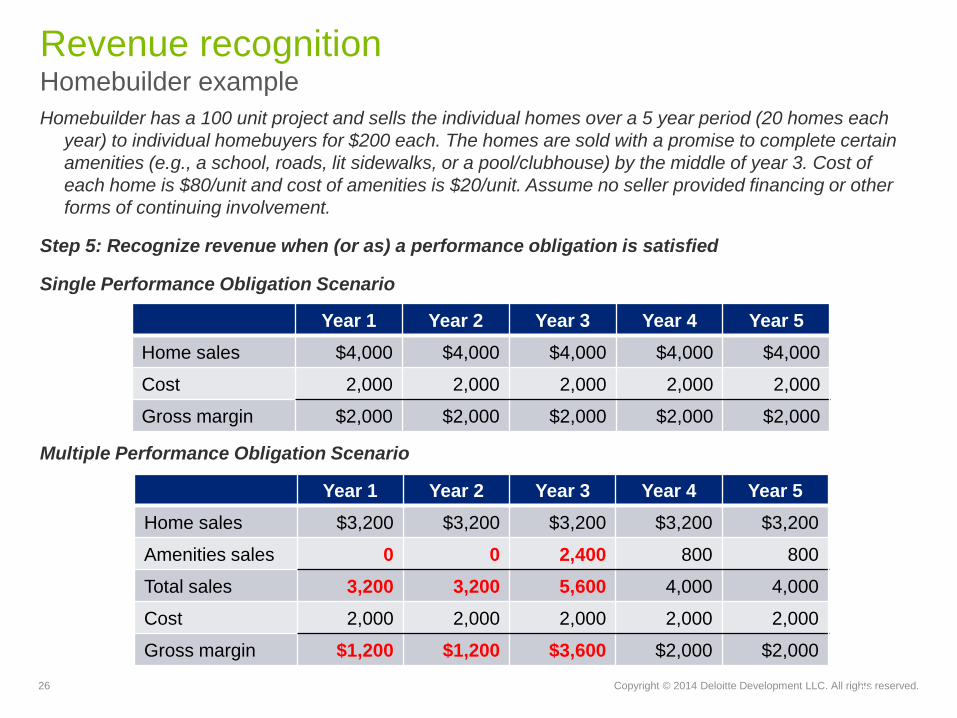

Revenue recognition Homebuilder example

Homebuilder has a 100 unit project and sells the individual homes over a

5 year period (20 homes each year) to individual homebuyers for $200

each. The homes are sold with a promise to complete certain

amenities (e.g., a school, roads, lit sidewalks, or a pool/clubhouse) by

the middle of year 3. Cost of each home is $80/unit and cost of

amenities is $20/unit. Assume no seller provided financing or other

forms of continuing involvement.

Step 1: Identify the contract with the customer

The contracts with the individual homebuyers are the relevant contracts.

Step 2: Identify the performance obligations in the contract

Scenario 1: The only performance obligation is the completion of the individual unit.

Scenario 2: There are two performance obligations. First is the delivery of the individual

unit and second is the delivery of the amenities.

Step 3: Determine the transaction price

Transaction price is $200 per unit or $20,000 in total.

24

25 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Revenue recognition Homebuilder example

Homebuilder has a 100 unit project and sells the individual homes over a 5 year period (20 homes each

year) to individual homebuyers for $200 each. The homes are sold with a promise to complete certain

amenities (e.g., a school, roads, lit sidewalks, or a pool/clubhouse) by the middle of year 3. Cost of

each home is $80/unit and cost of amenities is $20/unit. Assume no seller provided financing or other

forms of continuing involvement.

Step 4: Allocate the transaction price to the performance obligations (Two possible scenarios

based on Step 2)

25

Single Performance

Obligation

Multiple Performance

Obligations

Per Unit Total Per Unit Total

Total cost $100 $10,000 $100 $10,000

Home cost $80 $8,000 $80 $8,000

Amenities cost $20 $2,000 $20 $2,000

Total revenue $200 $20,000 $200 $20,000

Home revenue $200 $20,000 $160 $16,000

Amenities revenue $40 $4,000

26 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Revenue recognition Homebuilder example

Homebuilder has a 100 unit project and sells the individual homes over a 5 year period (20 homes each

year) to individual homebuyers for $200 each. The homes are sold with a promise to complete certain

amenities (e.g., a school, roads, lit sidewalks, or a pool/clubhouse) by the middle of year 3. Cost of

each home is $80/unit and cost of amenities is $20/unit. Assume no seller provided financing or other

forms of continuing involvement.

Step 5: Recognize revenue when (or as) a performance obligation is satisfied

Single Performance Obligation Scenario

Multiple Performance Obligation Scenario

26

Year 1 Year 2 Year 3 Year 4 Year 5

Home sales $4,000 $4,000 $4,000 $4,000 $4,000

Cost 2,000 2,000 2,000 2,000 2,000

Gross margin $2,000 $2,000 $2,000 $2,000 $2,000

Year 1 Year 2 Year 3 Year 4 Year 5

Home sales $3,200 $3,200 $3,200 $3,200 $3,200

Amenities sales 0 0 2,400 800 800

Total sales 3,200 3,200 5,600 4,000 4,000

Cost 2,000 2,000 2,000 2,000 2,000

Gross margin $1,200 $1,200 $3,600 $2,000 $2,000

27 Copyright © 2014 Deloitte Development LLC. All rights reserved.

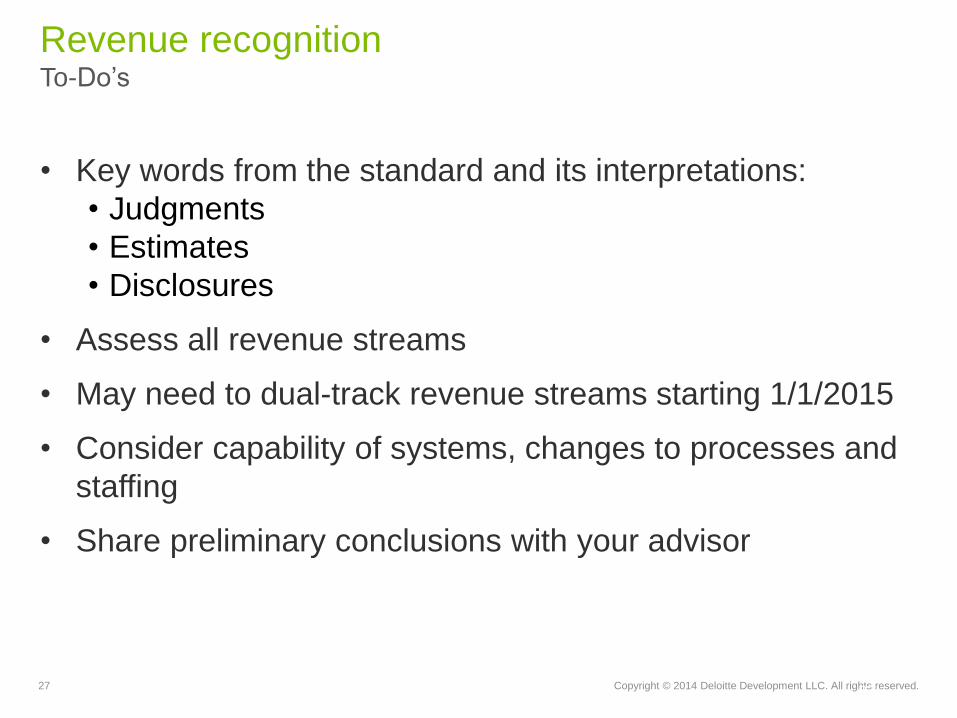

Revenue recognition To-Do’s

• Key words from the standard and its interpretations:

• Judgments

• Estimates

• Disclosures

• Assess all revenue streams

• May need to dual-track revenue streams starting 1/1/2015

• Consider capability of systems, changes to processes and

staffing

• Share preliminary conclusions with your advisor

27

Financial Instruments

29 Copyright © 2014 Deloitte Development LLC. All rights reserved.

FASB classification and measurement

Financial instruments

• Convergence abandoned

• Approach retains existing U.S. GAAP with limited changes

− Equity instruments can no longer be accounted for as available

for sale at fair value through OCI; instead accounted for at FV

through earnings. AFS criteria will only apply to debt

instruments.

• Practicability exception allows measurement of qualifying equity

securities at cost minus impairment, plus/minus changes in

observable prices

− Financial liabilities – fair value option retained with changes in

FV attributable to instrument-specific credit risk recognized in

OCI

• Final ASU anticipated in 2015

30 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Classification and measurement Equity method investments

• A single step impairment model has been discussed for

equity method investments (fair value through net income)

• Would have replaced the other-than-temporary model

currently in place

• However, the FASB recently decided by a close margin that

the OTTI model will be retained; equity method investments

are now scoped out of this project

31 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Impairment

Financial instruments

• Converged approach abandoned

• Current expected credit loss model (CECL) applies to instruments

carried at amortized cost (like loans and H-T-M debt securities)

• Replaces existing impairment models in GAAP, which generally require

that a loss be “incurred” before it is recognized

• Requires impairment to be recorded on existing financial assets on the

basis of the current estimate of contractual cash flows not expected to

be collected at the reporting date

• No impairment allowance is recognized on a financial asset in which the

risk of nonpayment is greater than zero yet the amount of loss would be

zero (i.e. where FV of collateral for a collateral dependent loan is greater

than BV of the loan).

• Final ASU anticipated in 2015

Investment Companies

33 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Definition and typical characteristics of an

investment company – ASU 2013-08

Multiple

investments

Obtains funds from

investor(s) and provides

professional investment

management service

Business purposes &

substantive activities are to

invest funds for returns from

capital appreciation,

investment income, or both

Do not obtain benefits from

their investments that are

either:

• Other than capital

appreciation or investment

income

• Not available to other

noninvestors / not normally

attributable to ownership

interests

Multiple

investors

Equity or

partnership

interests

Manages and

evaluates its

investments on a

fair value basis

Investment

Company

Additional five

characteristics

(Not required to

meet all of these

criteria)

Unrelated

investors

Required Attributes

34 Copyright © 2014 Deloitte Development LLC. All rights reserved.

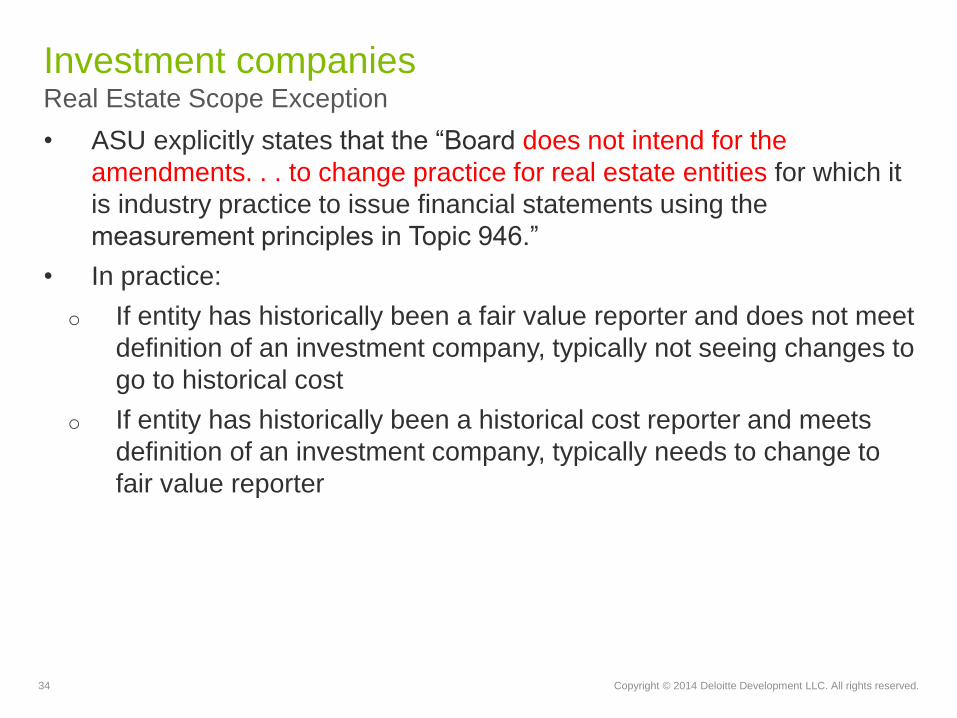

Real Estate Scope Exception

Investment companies

• ASU explicitly states that the “Board does not intend for the

amendments. . . to change practice for real estate entities for which it

is industry practice to issue financial statements using the

measurement principles in Topic 946.”

• In practice:

o If entity has historically been a fair value reporter and does not meet

definition of an investment company, typically not seeing changes to

go to historical cost

o If entity has historically been a historical cost reporter and meets

definition of an investment company, typically needs to change to

fair value reporter

Leases

36 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Lease project

37 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Lease project

What is wrong with the current lease accounting? – Bright-line tests bring structuring opportunities

– Too many liabilities off-balance sheet

38 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Lease project

Wall Street Journal, September 23, 2004

39 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Joint leases project Timeline

Q3 2010

Exposure Draft (ED)

2011-2013 Re-deliberations

and 2nd ED

2014

Re-deliberations

Q3 2015 ?

Final Standard

39

2014 re-deliberations are focusing on:

• Definition and scope • Subleases

• Lease classification • Measurement

• Lessee accounting • Disclosure

• Lessor accounting • Effective Date

• Sale and leaseback transactions

A final standard is not expected until the second half of 2015 with

effective date no sooner than 2017

FASB and IASB are no longer converged on lessee accounting

40 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Lessor accounting… “And where I did begin, there I shall end” - Shakespeare

40

41 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Classification criteria would be similar to IAS 17

–Type A lease: generally consistent with today’s sales-

type/direct-finance leases

–Type B lease: generally consistent with today’s operating

leases

Lessor accounting model

Existing lessor accounting retained with minimal

changes:

Leases project

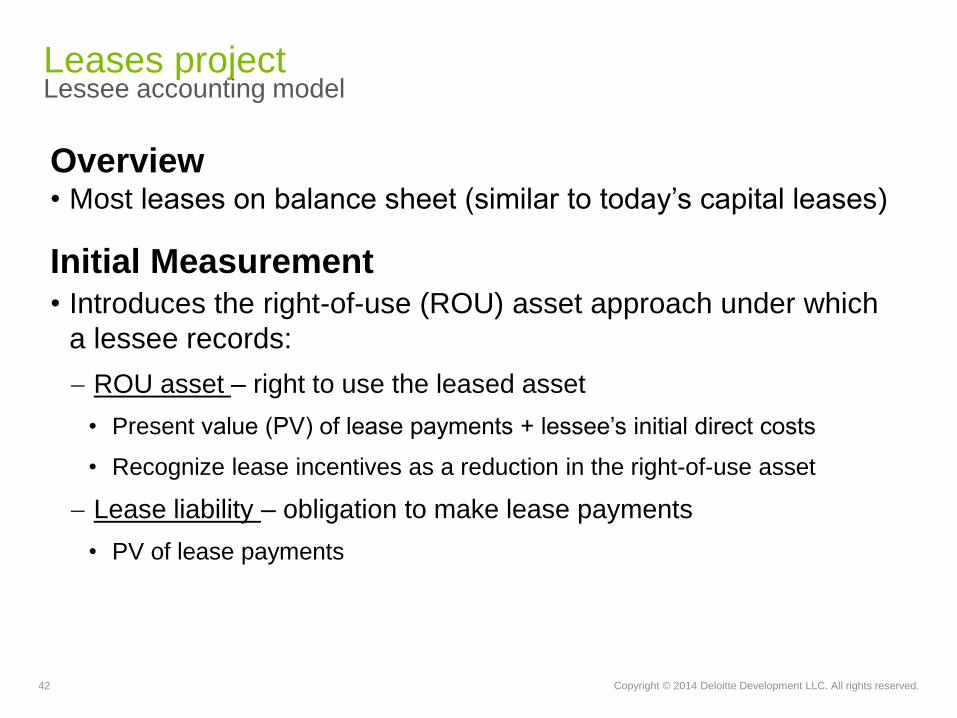

42 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Overview • Most leases on balance sheet (similar to today’s capital leases)

Initial Measurement • Introduces the right-of-use (ROU) asset approach under which

a lessee records:

ROU asset – right to use the leased asset

• Present value (PV) of lease payments + lessee’s initial direct costs

• Recognize lease incentives as a reduction in the right-of-use asset

Lease liability – obligation to make lease payments

• PV of lease payments

Lessee accounting model Leases project

43 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Subsequent Measurement • ROU asset Boards are not converged on the subsequent measurement:

• Lease liability Amortized cost: Use the effective interest method

Leases project

FASB Approach IASB Approach

Dual-model approach – a lessee would

apply guidance similar to IAS 17 when

determining if a lease should be

classified as Type A or Type B

Single-model approach – a lessee

would account for all leases as a

financed purchase of the ROU asset

Type A Lease Type B Lease

Consistent with

today’s capital

leases - expense will

be front-loaded

Expense will be

recorded on a

straight-line basis

Lessee accounting model

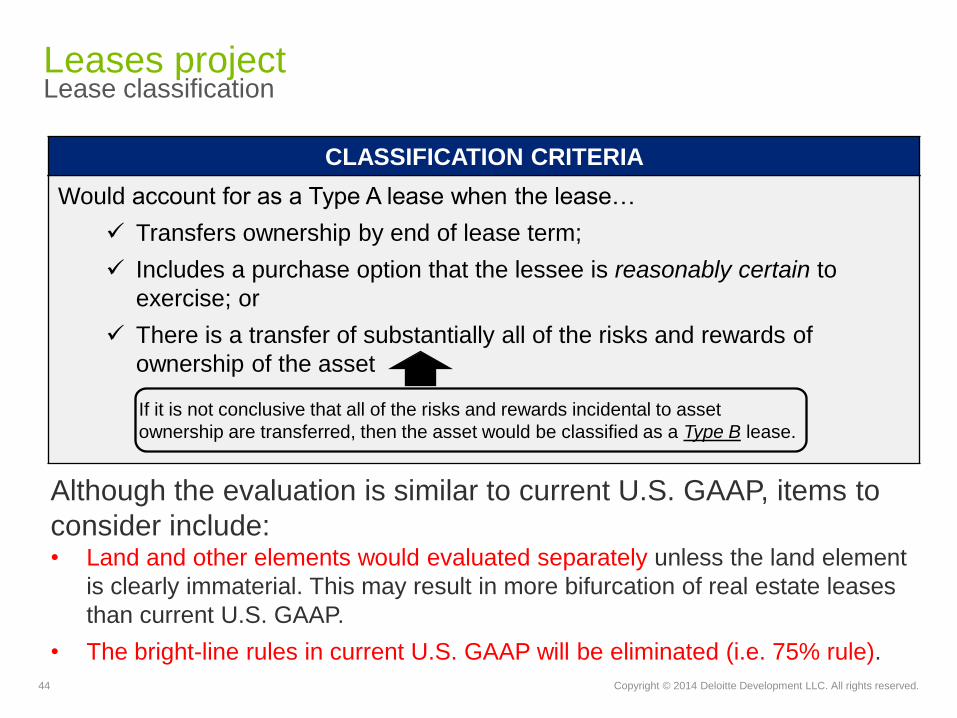

44 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Would account for as a Type A lease when the lease…

Transfers ownership by end of lease term;

Includes a purchase option that the lessee is reasonably certain to

exercise; or

There is a transfer of substantially all of the risks and rewards of

ownership of the asset

If it is not conclusive that all of the risks and rewards incidental to asset

ownership are transferred, then the asset would be classified as a Type B lease.

Lease classification Leases project

Although the evaluation is similar to current U.S. GAAP, items to

consider include: • Land and other elements would evaluated separately unless the land element

is clearly immaterial. This may result in more bifurcation of real estate leases

than current U.S. GAAP.

• The bright-line rules in current U.S. GAAP will be eliminated (i.e. 75% rule).

CLASSIFICATION CRITERIA

45 Copyright © 2014 Deloitte Development LLC. All rights reserved.

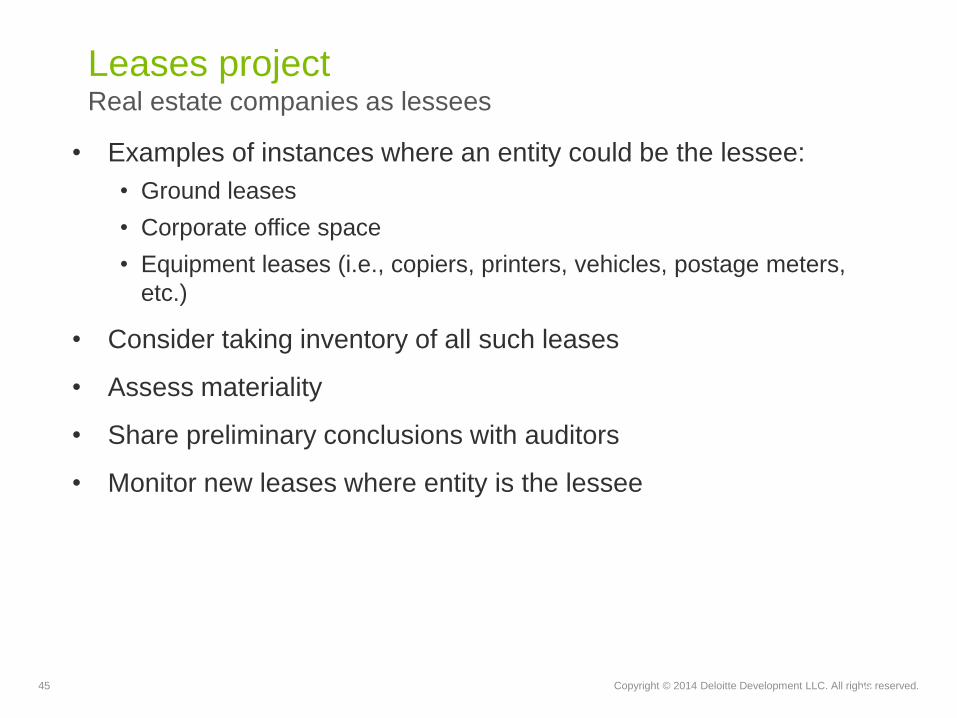

Leases project Real estate companies as lessees

45

• Examples of instances where an entity could be the lessee:

• Ground leases

• Corporate office space

• Equipment leases (i.e., copiers, printers, vehicles, postage meters,

etc.)

• Consider taking inventory of all such leases

• Assess materiality

• Share preliminary conclusions with auditors

• Monitor new leases where entity is the lessee

46 Copyright © 2014 Deloitte Development LLC. All rights reserved.

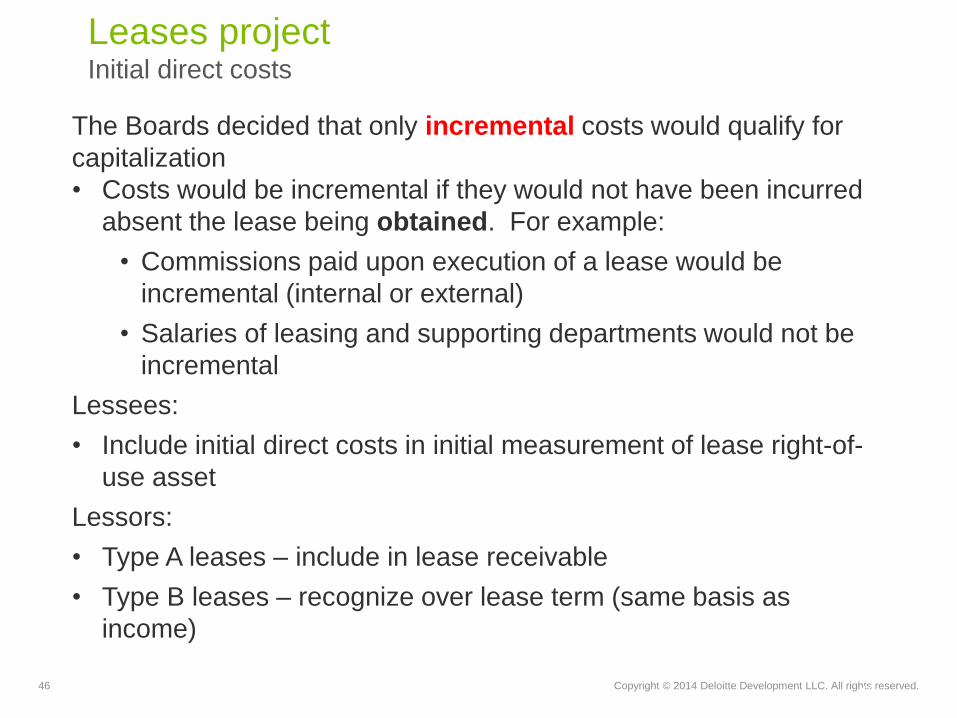

Leases project Initial direct costs

The Boards decided that only incremental costs would qualify for

capitalization

• Costs would be incremental if they would not have been incurred

absent the lease being obtained. For example:

• Commissions paid upon execution of a lease would be

incremental (internal or external)

• Salaries of leasing and supporting departments would not be

incremental

Lessees:

• Include initial direct costs in initial measurement of lease right-of-

use asset

Lessors:

• Type A leases – include in lease receivable

• Type B leases – recognize over lease term (same basis as

income)

46

47 Copyright © 2014 Deloitte Development LLC. All rights reserved.

NAREIT letter to FASB on initial direct costs

• Would be a step backward in reporting the economics of investment property

performance if direct costs of internal leasing staff were accounted for

differently from cost of external leasing resources

• Proposed accounting could force companies to abandon the most effective

leasing structure (internal leasing staff) for an external structure or

dramatically change internal compensation arrangements

• Given the wide diversity in accounting treatment for costs within US GAAP

(e.g. commitment fees, credit card fees and costs, loan syndication fees,

loan origination fees and direct loan origination costs, interest costs, etc.),

recommend FASB forego further evaluation of accounting for initial direct

costs within the leases project

47

48 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Leases project Initial direct costs

NAREIT met with FASB and meeting went something like this…

NAREIT: Requiring entities to expense direct costs of internal leasing

staff would cause our constituents to change the way they currently

do business.

FASB: Your constituents are currently capitalizing internal leasing

cost under current GAAP?

NAREIT: Yes. It’s industry standard to do so and changing current

GAAP would cause our constituents to change the way they currently

do business.

FASB: Wait…Your constituents are currently capitalizing internal

leasing cost under current GAAP?

48

Consolidations

50 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Consolidation Projects Overview and Timeline

IASB publishes ED 10

Dec 2008

June 2009

FASB issues FAS 167

FASB & IASB agree to develop single model

Oct 2009

Jan 2010

FASB defers FAS 167 for certain investment funds

Nov 2010

FASB holds public roundtables

FASB votes to converge on some, but not all aspects of IASB model

Jan 2011

Q4 2011

IASB issues Consolidation Standards; FASB exposes principal vs. agent

ExpectedQ1 2015

FASB to issue new consolidation guidance

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Sept 2013

FASB begins to redeliberate certain aspects of the model

51 Copyright © 2014 Deloitte Development LLC. All rights reserved.

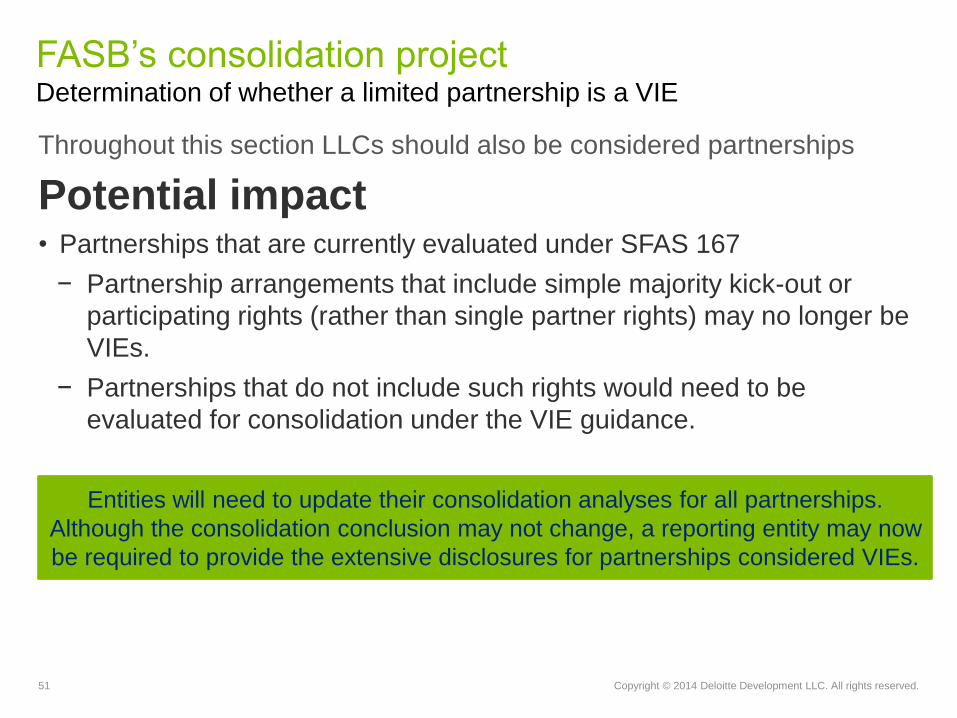

FASB’s consolidation project Determination of whether a limited partnership is a VIE

Throughout this section LLCs should also be considered partnerships

Potential impact • Partnerships that are currently evaluated under SFAS 167

− Partnership arrangements that include simple majority kick-out or

participating rights (rather than single partner rights) may no longer be

VIEs.

− Partnerships that do not include such rights would need to be

evaluated for consolidation under the VIE guidance.

Entities will need to update their consolidation analyses for all partnerships.

Although the consolidation conclusion may not change, a reporting entity may now

be required to provide the extensive disclosures for partnerships considered VIEs.

52 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Facts

• Investors A and B (two unrelated entities)

hold, together, all of the limited partner

interests in a partnership.

• Investor C is the general partner and has

the ability to make the most significant

decisions of partnership. Investor C does

not have significant equity investment at

risk.

• Investor C can be removed by a simple

majority of the limited partners.

Question

• Is the partnership a VIE?

Investor A Investor B

Partnership

Investor C

(GP)

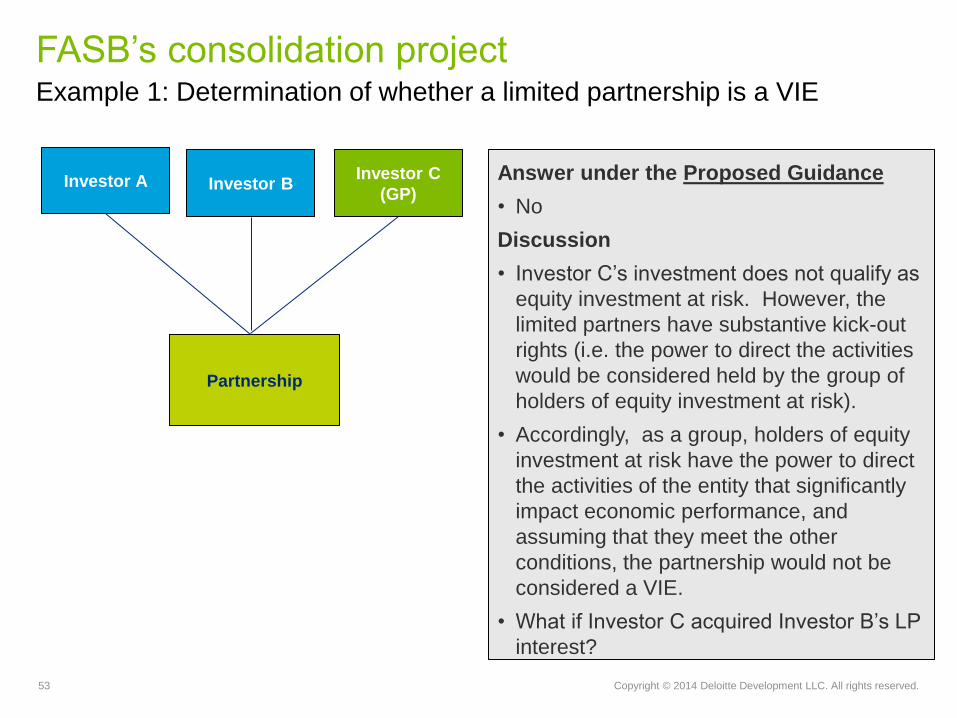

FASB’s consolidation project Example 1: Determination of whether a limited partnership is a VIE

53 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Investor A Investor B

Partnership

Investor C

(GP)

FASB’s consolidation project Example 1: Determination of whether a limited partnership is a VIE

Answer under the Proposed Guidance

• No

Discussion

• Investor C’s investment does not qualify as

equity investment at risk. However, the

limited partners have substantive kick-out

rights (i.e. the power to direct the activities

would be considered held by the group of

holders of equity investment at risk).

• Accordingly, as a group, holders of equity

investment at risk have the power to direct

the activities of the entity that significantly

impact economic performance, and

assuming that they meet the other

conditions, the partnership would not be

considered a VIE.

• What if Investor C acquired Investor B’s LP

interest?

54 Copyright © 2014 Deloitte Development LLC. All rights reserved.

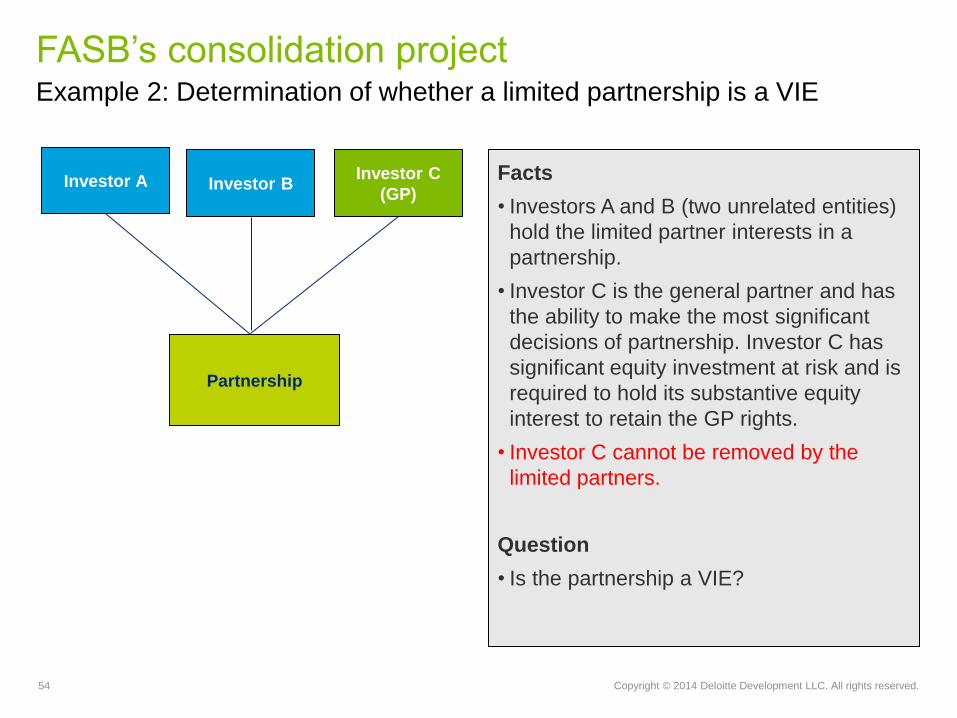

Facts

• Investors A and B (two unrelated entities)

hold the limited partner interests in a

partnership.

• Investor C is the general partner and has

the ability to make the most significant

decisions of partnership. Investor C has

significant equity investment at risk and is

required to hold its substantive equity

interest to retain the GP rights.

• Investor C cannot be removed by the

limited partners.

Question

• Is the partnership a VIE?

Investor A Investor B

Partnership

Investor C

(GP)

FASB’s consolidation project Example 2: Determination of whether a limited partnership is a VIE

55 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Investor A Investor B

Partnership

Investor C

(GP)

FASB’s consolidation project Example 2: Determination of whether a limited partnership is a VIE

Answer under the Proposed Guidance

• Yes

Discussion

• The limited partners cannot remove the

general partner.

• Because the equity investors as a group do

not have kick out or participating rights, the

partnership is a VIE.

• This may be a significant change from the

prior conclusion.

56 Copyright © 2014 Deloitte Development LLC. All rights reserved.

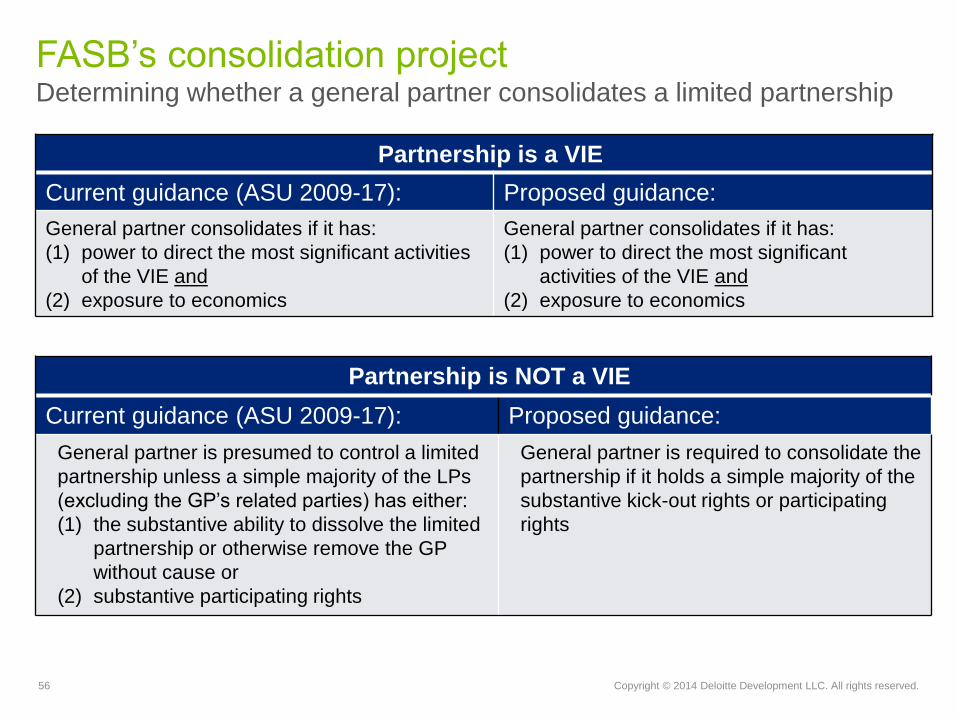

FASB’s consolidation project Determining whether a general partner consolidates a limited partnership

Partnership is NOT a VIE

Current guidance (ASU 2009-17): Proposed guidance:

General partner is presumed to control a limited

partnership unless a simple majority of the LPs

(excluding the GP’s related parties) has either:

(1) the substantive ability to dissolve the limited

partnership or otherwise remove the GP

without cause or

(2) substantive participating rights

General partner is required to consolidate the

partnership if it holds a simple majority of the

substantive kick-out rights or participating

rights

Partnership is a VIE

Current guidance (ASU 2009-17): Proposed guidance:

General partner consolidates if it has:

(1) power to direct the most significant activities

of the VIE and

(2) exposure to economics

General partner consolidates if it has:

(1) power to direct the most significant

activities of the VIE and

(2) exposure to economics

57 Copyright © 2014 Deloitte Development LLC. All rights reserved.

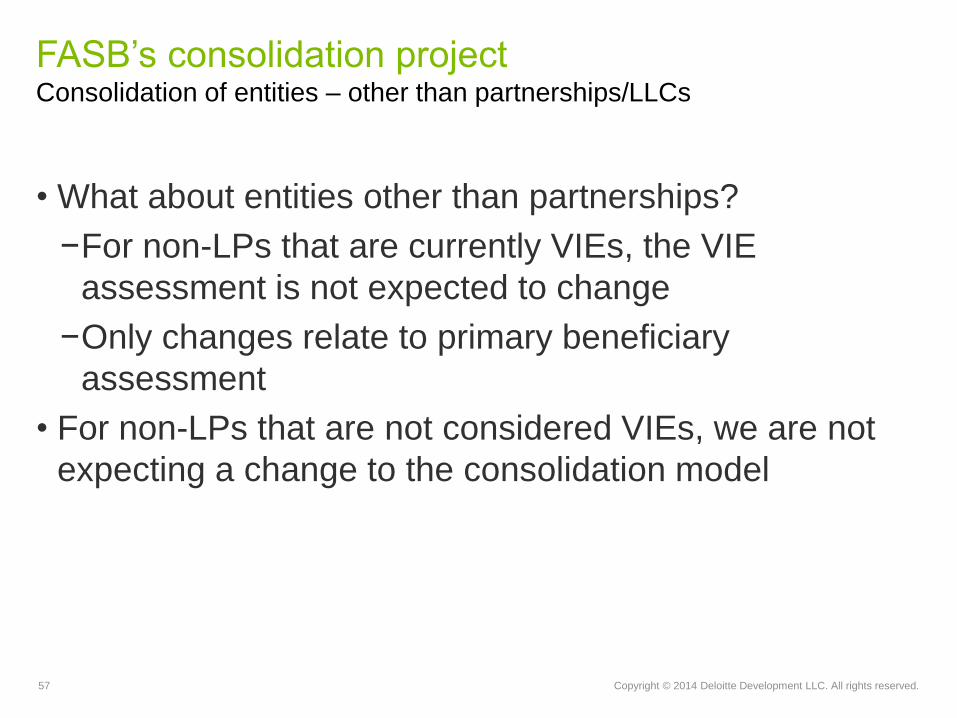

FASB’s consolidation project Consolidation of entities – other than partnerships/LLCs

• What about entities other than partnerships?

−For non-LPs that are currently VIEs, the VIE

assessment is not expected to change

−Only changes relate to primary beneficiary

assessment

• For non-LPs that are not considered VIEs, we are not

expecting a change to the consolidation model

58 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Other areas affected by the proposed guidance include:

• Related party tie breaker test

• Whether fees paid to a decision maker or a service

provider should be considered when evaluating a

reporting entity’s economic exposure to a VIE

• Whether fees paid to a decision maker or service

provider represent a variable interest

• Effective for public companies for annual and interim

periods beginning after December 15, 2015 (FY2016

for calendar YE). Non public is FY 2017 for calendar YE

• FASB will allow early adoption for all entities

FASB’s consolidations project

59 Copyright © 2014 Deloitte Development LLC. All rights reserved.

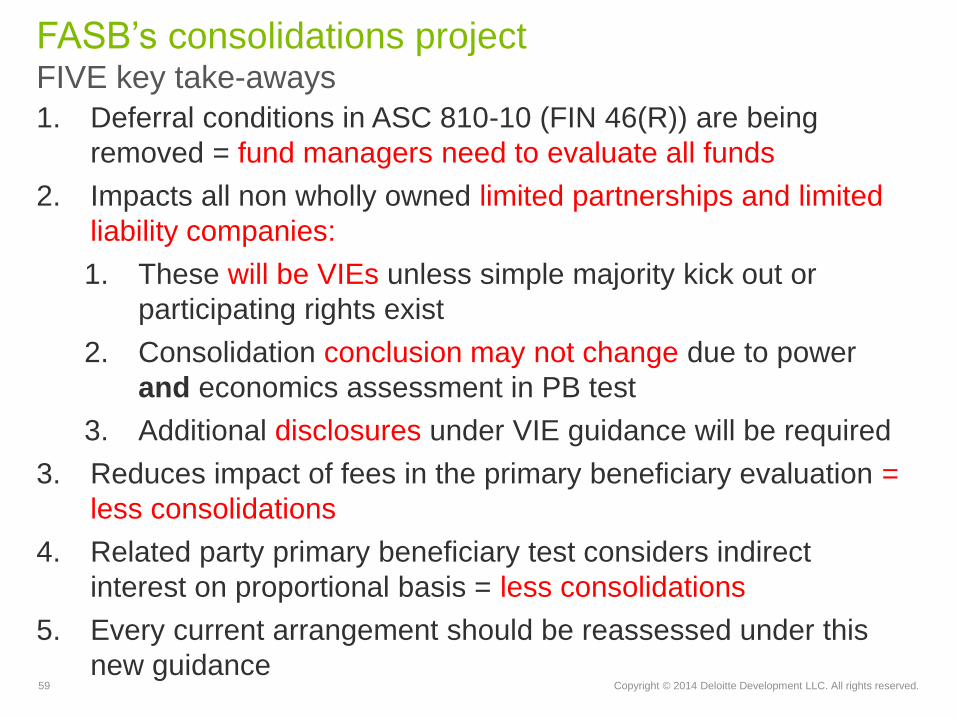

1. Deferral conditions in ASC 810-10 (FIN 46(R)) are being

removed = fund managers need to evaluate all funds

2. Impacts all non wholly owned limited partnerships and limited

liability companies:

1. These will be VIEs unless simple majority kick out or

participating rights exist

2. Consolidation conclusion may not change due to power

and economics assessment in PB test

3. Additional disclosures under VIE guidance will be required

3. Reduces impact of fees in the primary beneficiary evaluation =

less consolidations

4. Related party primary beneficiary test considers indirect

interest on proportional basis = less consolidations

5. Every current arrangement should be reassessed under this

new guidance

FASB’s consolidations project FIVE key take-aways

Discontinued

Operations

61 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Discontinued operations

• ASU 2014-8 raises the threshold for reporting discops and aligns with

IFRS

– Represents a strategic shift that has (or will have) a major effect on

an entity’s operations and financial results

– Examples include:

– Disposal of a major geographical area

– A major line of business

– A major equity method investment (scope exception removed)

– Other major parts of an entity

• Disclosure requirements for significant component disposals that do

not meet discops requirements include:

• Pre-tax income for all periods presented for public companies

• Current period pre-tax income for private companies

62 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Discontinued operations

Transition and timing –

– Prospective application required

– Standard was issued April 10, 2014 and is effective on January 1, 2015 for

public companies and January 1, 2016 for private companies

– Early adoption permitted for disposals (or classifications as held for

sale) that have not been reported in financial statements previously issued

or available for issuance

Presentation of gains and losses on disposals that are not discontinued

operations:

– SEC Rule S-X 3-15 – Gain or loss on a sale or disposal by a REIT that does

not qualify as a discontinued operation is reported below Income from

discontinued operations

– ASC 360-10-45-5 – A gain or loss recognized on the sale of a long-lived

asset that is not a discontinued operation shall be included in income from

continuing operations before income taxes in the income statement of a

business entity. If a subtotal such as income from operations is presented, it

shall include the amounts of those gains or losses.

63 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Discontinued operations

Per ASC 360-10-45-5: SEC Rule S-X 3-15

Income from continuing operations

before gain on sale of real estate XXXXX

Income from continuing operations

before gain on sale of real estate XXXXX

Gain on sale of real estate XXX

Income from continuing operations XXXXX Discontinued operations: Income from discontinued

Discontinued operations: operations XXX Income from discontinued Gain on sale of real estate in operations XXX discontinued operations XX Gain on sale of real estate in discontinued operations XX Income from discontinued XXXIncome from discontinued XXX operations

Gain on sale of real estate XXX

Net income XXXXXNet income XXXXX

Going Concern

65 Copyright © 2014 Deloitte Development LLC. All rights reserved.

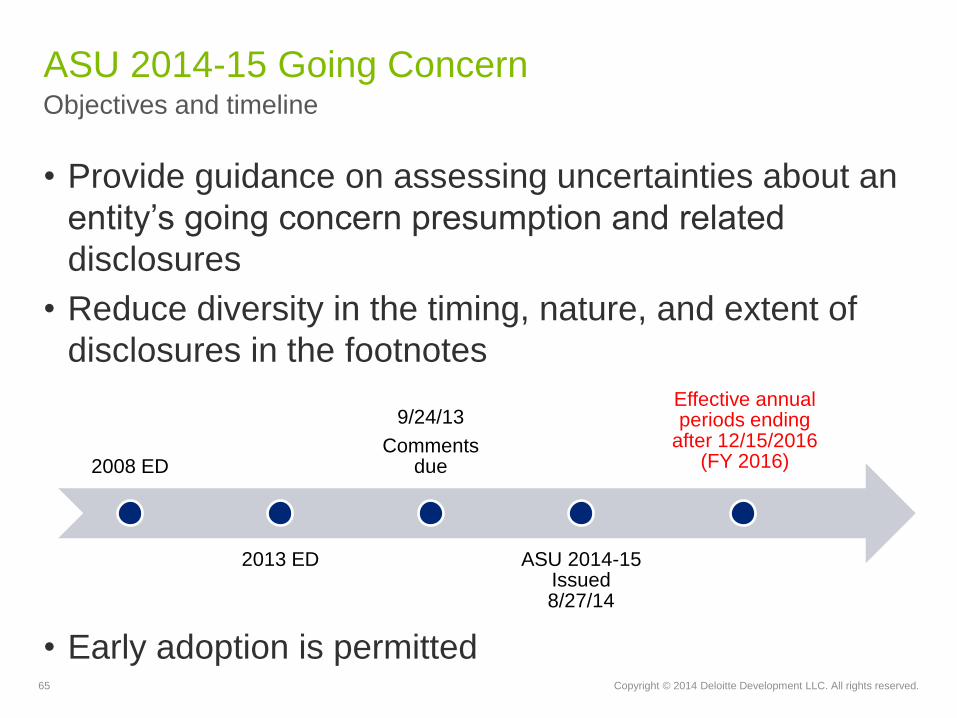

• Provide guidance on assessing uncertainties about an

entity’s going concern presumption and related

disclosures

• Reduce diversity in the timing, nature, and extent of

disclosures in the footnotes

• Early adoption is permitted

ASU 2014-15 Going Concern Objectives and timeline

2008 ED

2013 ED

9/24/13

Comments due

ASU 2014-15 Issued 8/27/14

Effective annual periods ending

after 12/15/2016 (FY 2016)

66 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Substantial doubt Liquidation is imminent

Going concern ASU Background

• Going concern presumed until liquidation deemed imminent

• May have uncertainties about continuing as a going concern before

liquidation deemed imminent

• Previously no guidance in U.S. GAAP (only auditing standards)

• ASU extends going concern assessment to management. Entities

may need to implement and document their processes and controls

• Liquidation basis does not apply when liquidation follows a plan for

liquidation that was specified in the entity’s governing documents at

the entity’s inception (common in partnerships)

• Assessment period is 12 month from issuance date

Going concern disclosures required Liquidation basis of

accounting

FASB and SEC

Simplification Projects

68 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• SEC’s disclosure effectiveness project

• FASB's limited-scope projects to simplify U.S. GAAP in the

near term

Simplification projects Background and objectives

69 Copyright © 2014 Deloitte Development LLC. All rights reserved.

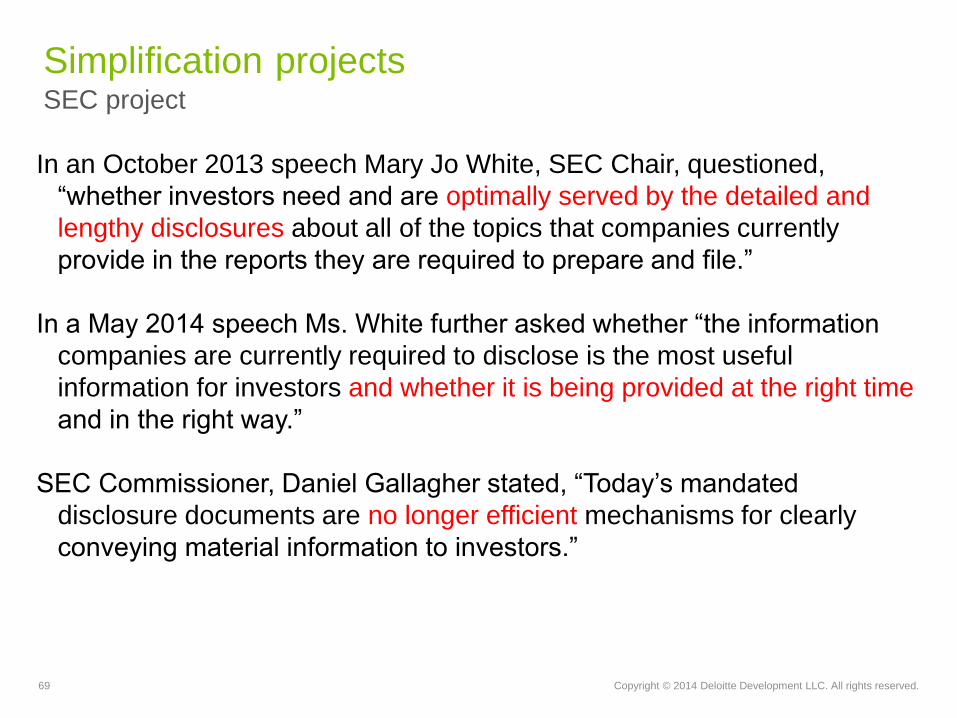

In an October 2013 speech Mary Jo White, SEC Chair, questioned,

“whether investors need and are optimally served by the detailed and

lengthy disclosures about all of the topics that companies currently

provide in the reports they are required to prepare and file.”

In a May 2014 speech Ms. White further asked whether “the information

companies are currently required to disclose is the most useful

information for investors and whether it is being provided at the right time

and in the right way.”

SEC Commissioner, Daniel Gallagher stated, “Today’s mandated

disclosure documents are no longer efficient mechanisms for clearly

conveying material information to investors.”

Simplification projects SEC project

70 Copyright © 2014 Deloitte Development LLC. All rights reserved.

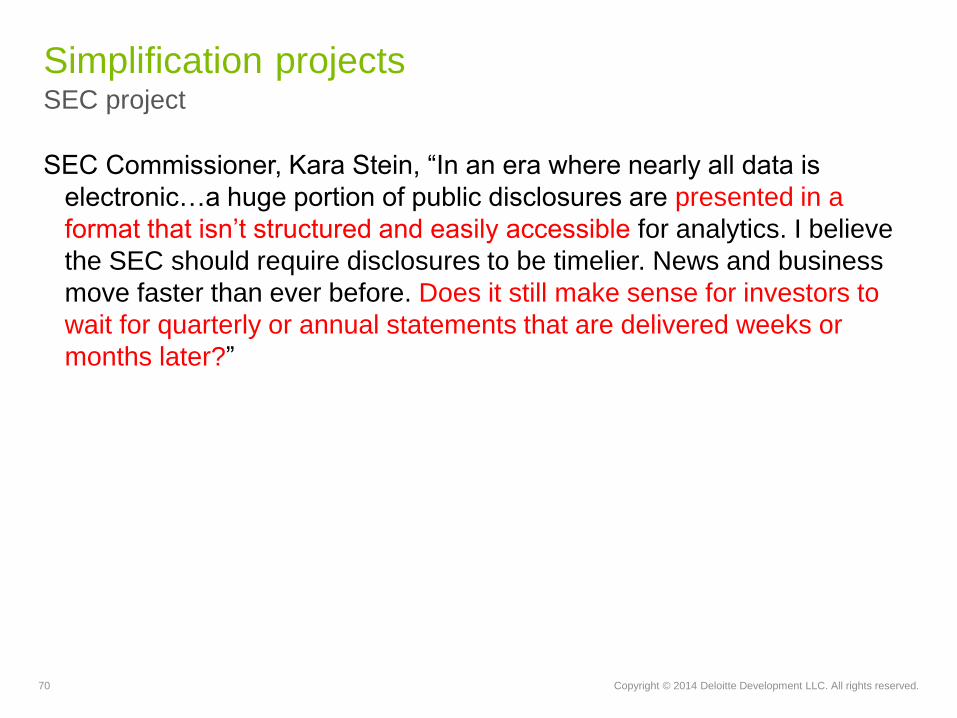

SEC Commissioner, Kara Stein, “In an era where nearly all data is

electronic…a huge portion of public disclosures are presented in a

format that isn’t structured and easily accessible for analytics. I believe

the SEC should require disclosures to be timelier. News and business

move faster than ever before. Does it still make sense for investors to

wait for quarterly or annual statements that are delivered weeks or

months later?”

Simplification projects SEC project

71 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• SEC project to focus on identifying ways to improve disclosure

requirements in Regulations S-K and S-X

• Focus on business and financial disclosures that flow into Forms 10-

K, 10-Q, and 8-K and ultimately make their way into transactional

filings

• Staff will consider eliminating disclosure requirements that were

originally created to fill a void in US GAAP

• Project could incorporate increased disclosure into audit committee

activities

Simplification projects SEC project

72 Copyright © 2014 Deloitte Development LLC. All rights reserved.

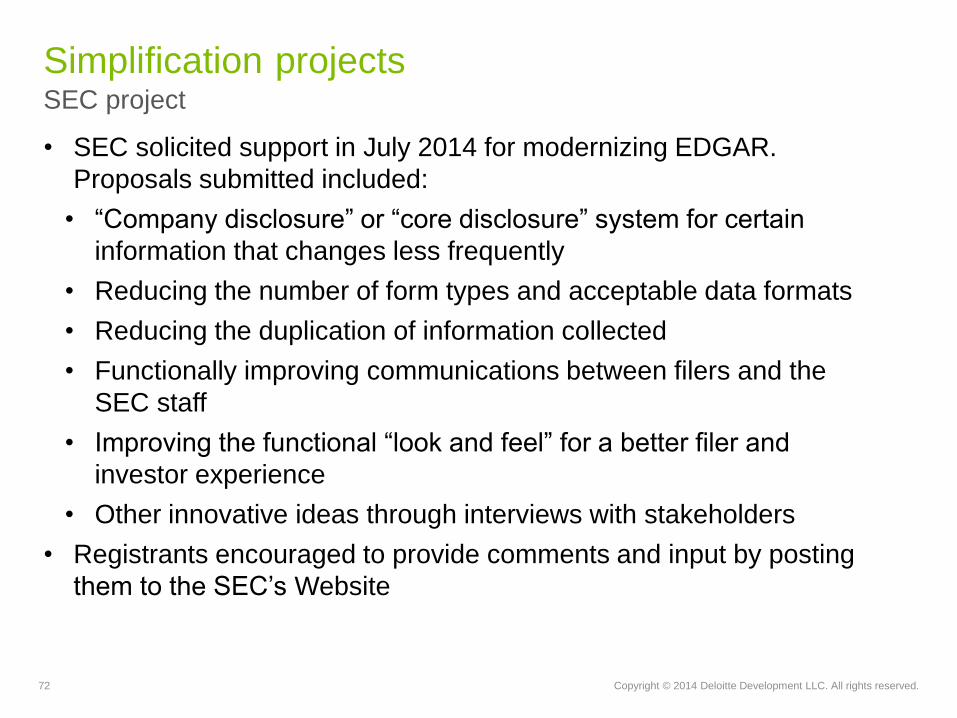

• SEC solicited support in July 2014 for modernizing EDGAR.

Proposals submitted included:

• “Company disclosure” or “core disclosure” system for certain

information that changes less frequently

• Reducing the number of form types and acceptable data formats

• Reducing the duplication of information collected

• Functionally improving communications between filers and the

SEC staff

• Improving the functional “look and feel” for a better filer and

investor experience

• Other innovative ideas through interviews with stakeholders

• Registrants encouraged to provide comments and input by posting

them to the SEC’s Website

Simplification projects SEC project

73 Copyright © 2014 Deloitte Development LLC. All rights reserved.

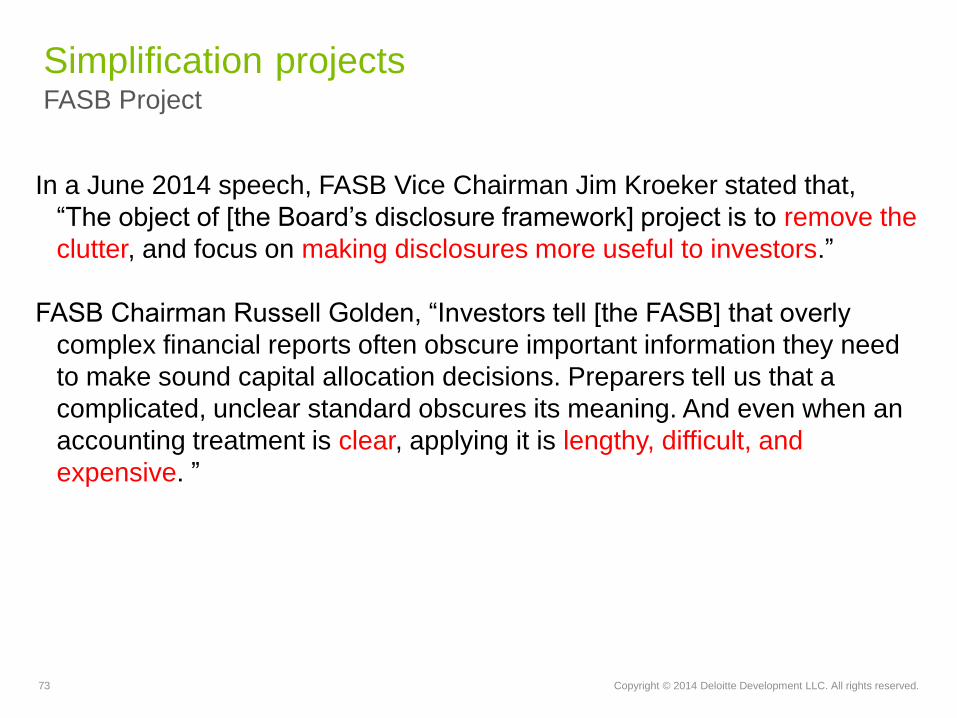

In a June 2014 speech, FASB Vice Chairman Jim Kroeker stated that,

“The object of [the Board’s disclosure framework] project is to remove the

clutter, and focus on making disclosures more useful to investors.”

FASB Chairman Russell Golden, “Investors tell [the FASB] that overly

complex financial reports often obscure important information they need

to make sound capital allocation decisions. Preparers tell us that a

complicated, unclear standard obscures its meaning. And even when an

accounting treatment is clear, applying it is lengthy, difficult, and

expensive. ”

Simplification projects FASB Project

74 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• FASB released an exposure draft in March 2014 on its decision

process for determining disclosure required in footnotes

• Comment period ended in July 2014 and FASB has begun

redeliberations

• Board has been considering a decision making framework for

financial statement preparers

• Intends to evaluate whether simplified accounting alternatives

available to private companies could be extended to public

companies

Simplification projects FASB Project

75 Copyright © 2014 Deloitte Development LLC. All rights reserved.

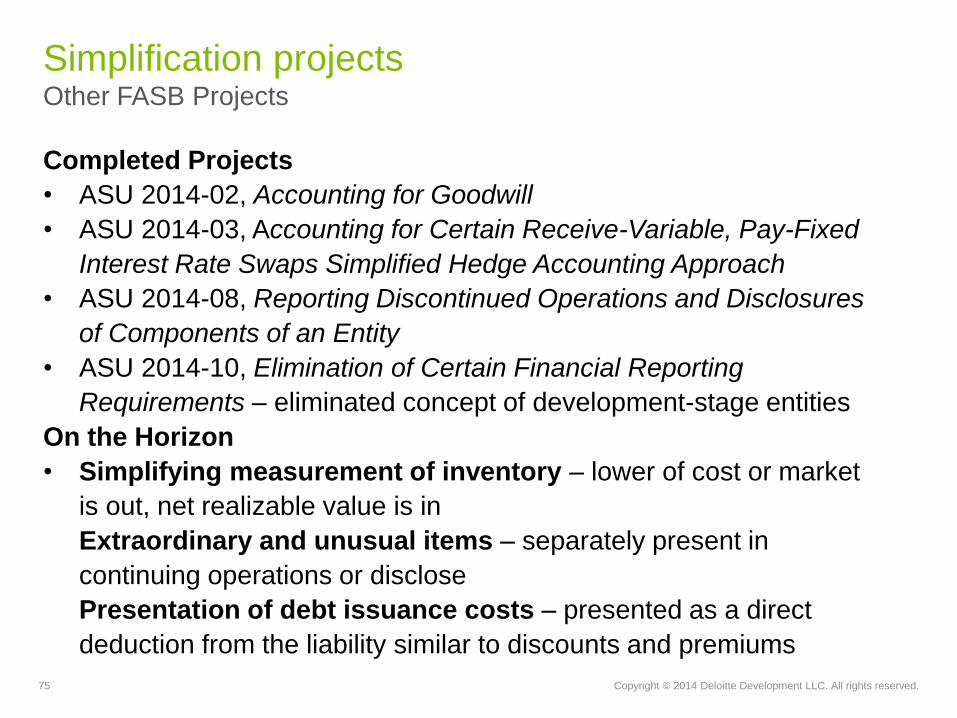

Completed Projects

• ASU 2014-02, Accounting for Goodwill

• ASU 2014-03, Accounting for Certain Receive-Variable, Pay-Fixed

Interest Rate Swaps Simplified Hedge Accounting Approach

• ASU 2014-08, Reporting Discontinued Operations and Disclosures

of Components of an Entity

• ASU 2014-10, Elimination of Certain Financial Reporting

Requirements – eliminated concept of development-stage entities

On the Horizon

• Simplifying measurement of inventory – lower of cost or market

is out, net realizable value is in

Extraordinary and unusual items – separately present in

continuing operations or disclose

Presentation of debt issuance costs – presented as a direct

deduction from the liability similar to discounts and premiums

Simplification projects Other FASB Projects

Regulatory Update – PCAOB and SEC

PCAOB Update

78 Copyright © 2014 Deloitte Development LLC. All rights reserved.

PCAOB update Staff consultation paper on auditing accounting estimates and FV

measurements

Overview

Staff consultation paper issued August 19

‒ Area of many inspection findings

‒ Existing standards related to auditing estimates and fair value measurements

are:

Simplifying the Classification of Debt

“The PCAOB and foreign audit regulators have identified compliance with auditing

requirements related to fair value measurements as an area of continued concern,

and I support the staff's outreach efforts in this important area.”

- James R. Doty, PCAOB Chairman

• Auditing Fair Value Measurements and Disclosures

PCAOB AU Sec. 328

Orig. Issued January 2003

• Auditing Derivative Instruments, Hedging Activities, and Investments in Securities

PCAOB AU Sec. 332

Orig. Issued September 2000

• Auditing Accounting Estimates PCAOB AU Sec. 342

Orig. Issued April 1988

79 Copyright © 2014 Deloitte Development LLC. All rights reserved.

PCAOB update Staff consultation paper on auditing accounting estimates and FV measurements

• The staff paper suggests expanding the scope of audit work when

management uses a third party specialist or pricing services (i.e.

appraisals used in fair value estimates)

• Could require the auditor to “test the information provided by the

specialist as if it were produced by the company” or to “evaluate the

audit evidence obtained [from the third-party source] as if it were

produced by the company.”

• By suggesting that the auditor treat third party specialists as part of the

entity that they are auditing, the staff paper seems to be requiring

management to understand and evaluate the operating effectiveness

and sufficiency of controls at third party vendors.

• Simplifying the Classification of Debt

80 Copyright © 2014 Deloitte Development LLC. All rights reserved.

NAREIT’s response Staff consultation paper on auditing accounting estimates and FV measurements

“NAREIT’s member companies observe that external auditors currently

perform a significant amount of audit work surrounding estimates

pursuant to existing audit standards.”

“The suggestions in the Staff Paper would only expand the work that

auditors perform today, with no increase in the reliability or credibility of

the audited financial statements. Further, as discussed below, there is no

evidence that the existing auditing standards related to auditing

estimates fail to detect significant errors in financial statements.”

“While NAREIT understands the importance of auditing estimates, we

have to wonder whether the Staff Paper is attempting to reach a level of

precision via the audit process that contradicts the inherent nature of the

subject being audited.”

• Simplifying the Classification of Debt

81 Copyright © 2014 Deloitte Development LLC. All rights reserved.

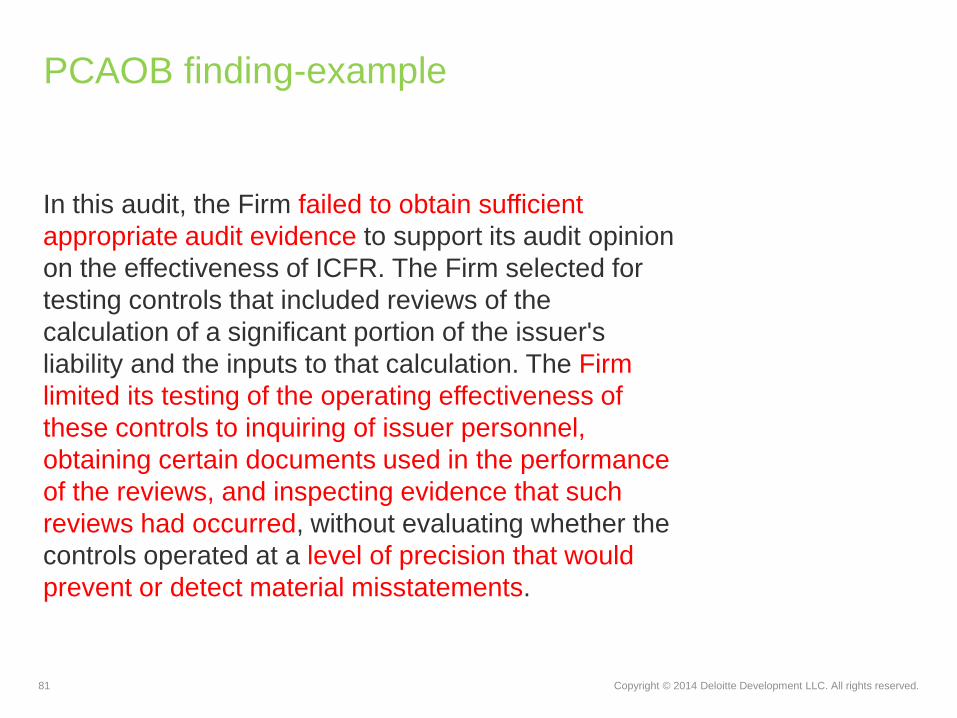

PCAOB finding-example

In this audit, the Firm failed to obtain sufficient

appropriate audit evidence to support its audit opinion

on the effectiveness of ICFR. The Firm selected for

testing controls that included reviews of the

calculation of a significant portion of the issuer's

liability and the inputs to that calculation. The Firm

limited its testing of the operating effectiveness of

these controls to inquiring of issuer personnel,

obtaining certain documents used in the performance

of the reviews, and inspecting evidence that such

reviews had occurred, without evaluating whether the

controls operated at a level of precision that would

prevent or detect material misstatements.

82 Copyright © 2014 Deloitte Development LLC. All rights reserved.

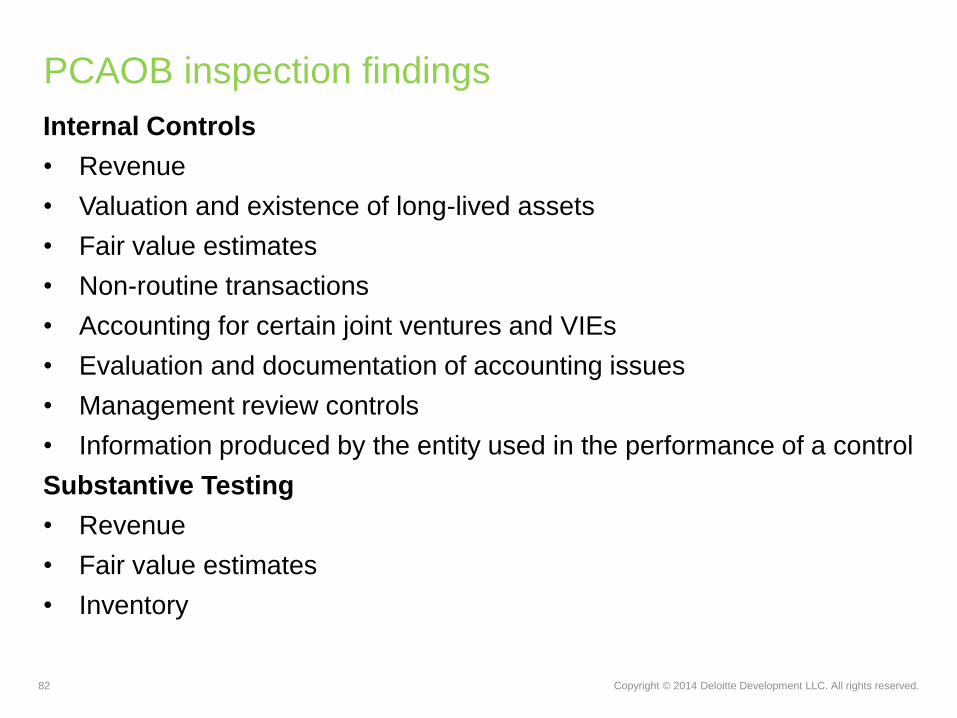

PCAOB inspection findings

Internal Controls

• Revenue

• Valuation and existence of long-lived assets

• Fair value estimates

• Non-routine transactions

• Accounting for certain joint ventures and VIEs

• Evaluation and documentation of accounting issues

• Management review controls

• Information produced by the entity used in the performance of a control

Substantive Testing

• Revenue

• Fair value estimates

• Inventory

SEC Comments on

Real Estate Companies

84 Copyright © 2014 Deloitte Development LLC. All rights reserved.

SEC review process

About 9,000 registrants

• Focus on 2,500 registrants that comprise 98% of market cap

All issuers reviewed at least every three years

Percentage of issuers reviewed:

Continuous reviews of large financial services registrants

Use of data analytics in the review of filings

Staff is listening to analyst/earnings calls, reviewing press releases and

websites and issuing comments

Comments are posted to EDGAR 20 days after completion of review (was 45

days)

FY08 FY09 FY10 FY11 FY12 FY13

38% 40% 44% 48% 48% 52%

85 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Fewer preclearances with the Office of the Chief Accountant

• 40% lower in 2013 compared to 2012; lowest level in 10 years

• Most common:

◦ Business combinations, consolidations, financial instruments, revenue recognition

• No compensation, leasing/RE, income taxes or miscellaneous

Concerned about accounting firms’ audit / internal control skillset versus the accounting skillset

• Each should be at the same level of prominence

• Careful that the pendulum hasn’t swung too far away from accounting

Dan Murdock, Deputy Chief Accountant

2013 AICPA SEC Conference

86 Copyright © 2014 Deloitte Development LLC. All rights reserved.

“We note your disclosure of operating statistics for your same store

property portfolio on page XX. In future Exchange Act periodic reports,

please expand your analysis in the MD&A section to address any material

period to period changes in same- store performance, including the

relative impact of occupancy and rental rate changes, or advise.”

Non-traditional REITs also receive typical real estate

comments

87 Copyright © 2014 Deloitte Development LLC. All rights reserved.

“In future Exchange Act periodic reports, with respect to leases expiring in

the next 12 months, please discuss any known trends regarding the

relationship between contractual rents on these expiring leases and

market rents.”

Lease expirations

88 Copyright © 2014 Deloitte Development LLC. All rights reserved.

“We note that throughout MD&A, you oftentimes do not quantify the

absolute impact of the factors that have been cited as contributors to the

variances in your results. In certain circumstances, you cite offsetting

factors without quantification of their relative impact. We believe that the

quantification of all material factors on an absolute basis would provide

readers with a more complete understanding of the variances in your

reports results, as well as provide additional transparency with regard to

the impacts of offsetting factors.”

MD&A - analytics

89 Copyright © 2014 Deloitte Development LLC. All rights reserved.

“We note that your discussion of cash flows from operating activities

primarily recites the information seen on the face of your cash flow

statement. Revise to disclose the underlying reasons for material changes

in your operating cash flows from operating assets and liabilities to better

explain the variability in your cash flows. Please refer to the guidance of

Section IV of SEC Release No. 33−8350.”

MD&A – liquidity and capital resources

90 Copyright © 2014 Deloitte Development LLC. All rights reserved.

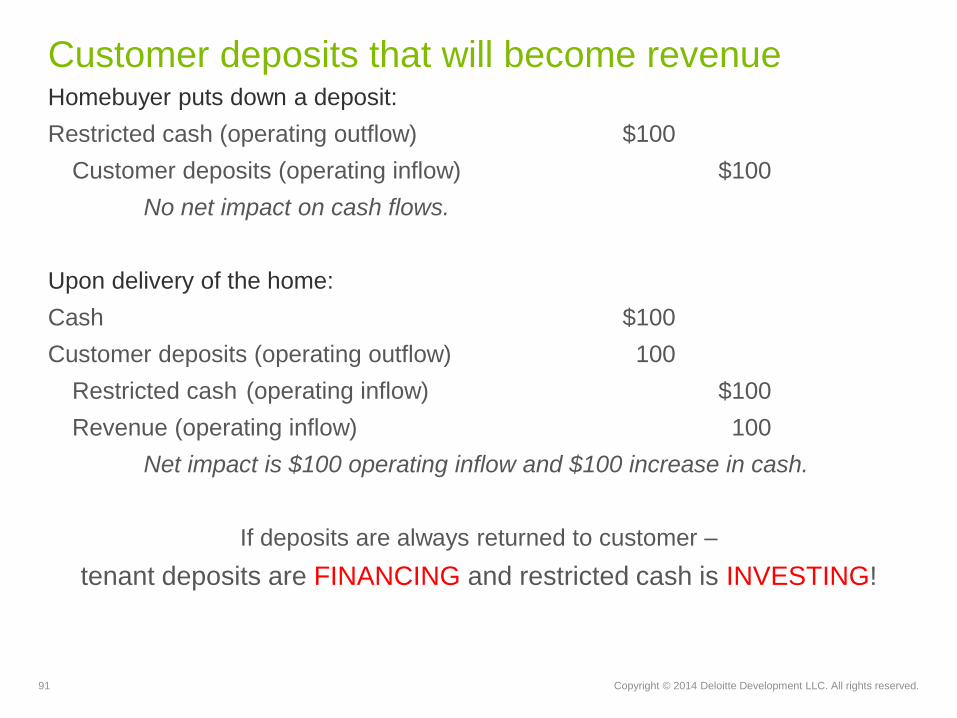

“You indicate that you classified the changes in restricted cash and

security deposits within cash flows from operating activities, based on the

fact that the cash flows associated with your security deposits are

predominantly operating in nature as they are directly related to your core

revenue generating activity. To the extent a majority of the security

deposits are returned to your lessees, please reassess your basis for

reflecting these activities within operating cash flows.”

Cash flow statement – restricted cash

91 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Homebuyer puts down a deposit:

Restricted cash (operating outflow) $100

Customer deposits (operating inflow) $100

No net impact on cash flows.

Upon delivery of the home:

Cash $100

Customer deposits (operating outflow) 100

Restricted cash (operating inflow) $100

Revenue (operating inflow) 100

Net impact is $100 operating inflow and $100 increase in cash.

If deposits are always returned to customer –

tenant deposits are FINANCING and restricted cash is INVESTING!

Customer deposits that will become revenue

92 Copyright © 2014 Deloitte Development LLC. All rights reserved.

“Please supplement your disclosure in this section to clarify whether you

are currently in compliance with all covenants and also include a general

discussion of how failure to comply could impact your current business.

Please also include disclosure analyzing how the financial covenants in

your indebtedness may restrict your ability to incur additional debt to

finance your uses.”

Debt covenants

93 Copyright © 2014 Deloitte Development LLC. All rights reserved.

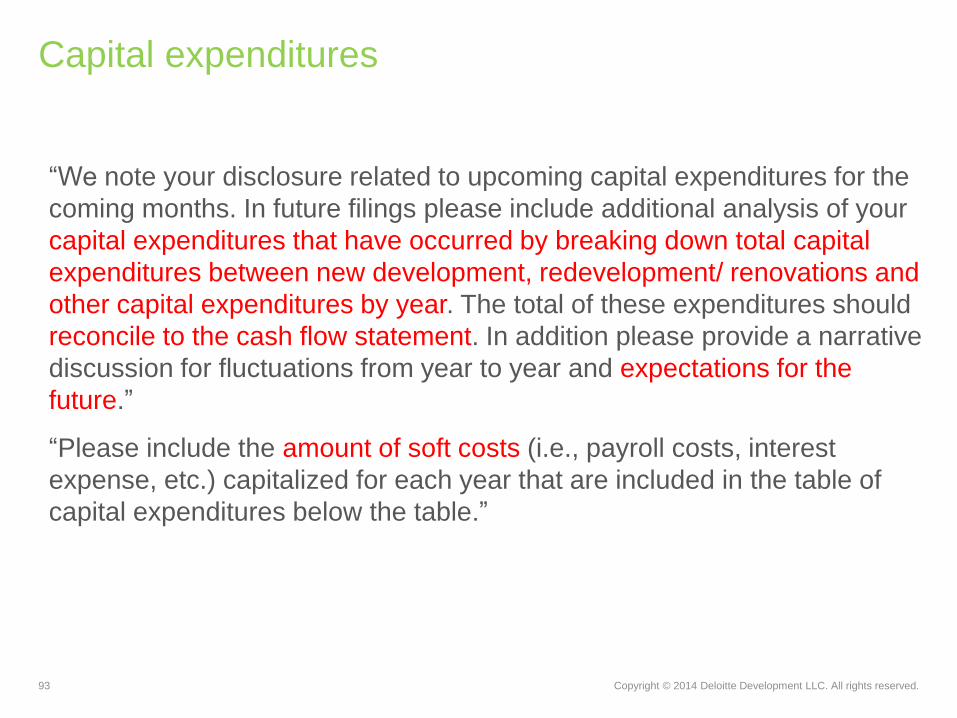

“We note your disclosure related to upcoming capital expenditures for the

coming months. In future filings please include additional analysis of your

capital expenditures that have occurred by breaking down total capital

expenditures between new development, redevelopment/ renovations and

other capital expenditures by year. The total of these expenditures should

reconcile to the cash flow statement. In addition please provide a narrative

discussion for fluctuations from year to year and expectations for the

future.”

“Please include the amount of soft costs (i.e., payroll costs, interest

expense, etc.) capitalized for each year that are included in the table of

capital expenditures below the table.”

Capital expenditures

94 Copyright © 2014 Deloitte Development LLC. All rights reserved.

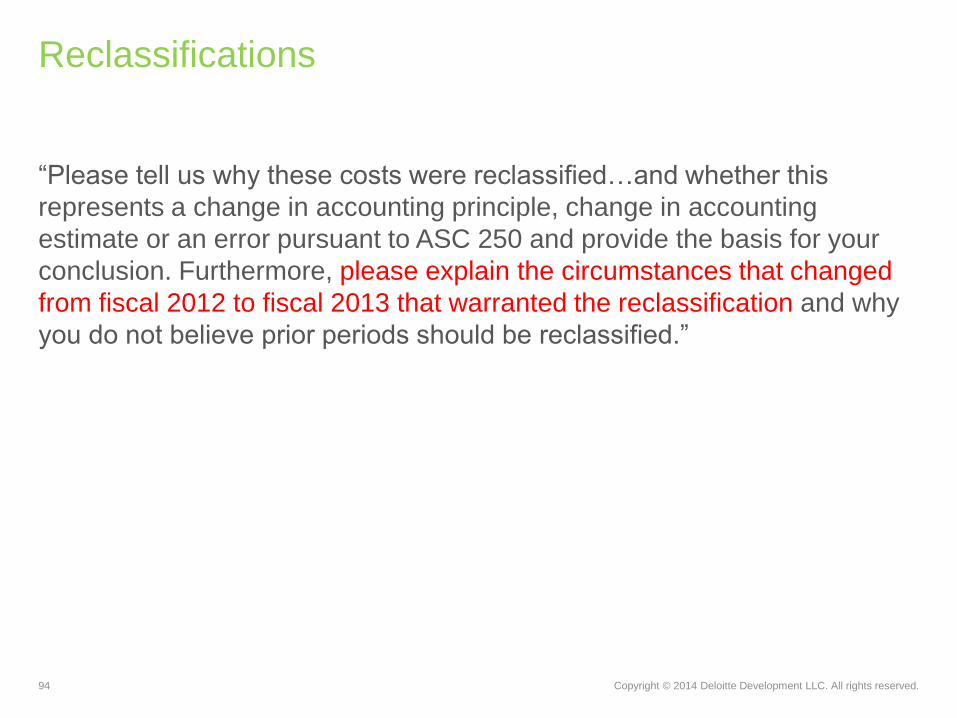

“Please tell us why these costs were reclassified…and whether this

represents a change in accounting principle, change in accounting

estimate or an error pursuant to ASC 250 and provide the basis for your

conclusion. Furthermore, please explain the circumstances that changed

from fiscal 2012 to fiscal 2013 that warranted the reclassification and why

you do not believe prior periods should be reclassified.”

Reclassifications

95 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Deloitte Publications and Resources

• Subscribe to free publications:

− Heads Up – periodic updates of accounting developments

− Accounting Roundup – monthly summary of standard-setting and

regulatory projects

− Roadmap – interpretive accounting manual on particular accounting

topics

− Numerous other publications at www.deloitte.com/us/subscriptions

• Register to receive notifications for free Dbriefs webcasts

(eligible for CPE)

− Register at www.deloitte.com/us/dbriefs

• Subscribe to our online library of accounting and financial disclosure

literature (Technical Library: The Deloitte Accounting Research Tool)

− See more information at www.deloitte.com/us/techlibrary

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities.

DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte

LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2014 Deloitte Development LLC. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited

2014 Real

Estate Update

Breaking New

Boundaries:

Paving the way

for the future Larry Varellas

Deloitte Tax LLP

Jim deBree

Deloitte Tax LLP

Todd LaBelle

Deloitte Tax LLP

98 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Tax Agenda

• Legislative Overview

• Inversions 101

• Tangible Property Regs.—Stretch Run

• What’s Really Real Estate?

• Marketplace Structures—”What’s Out There”?

• Other Hot Topics: What Are We Seeing?

Legislative Overview

100 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Where we are now…

Tax Item 2012 2013/2014

Ordinary income 35% 39.6% for singles earning more than $400K

($450K for couples)

Capital gains & qualified dividends 15% 20% for singles earning more than $400K ($450K

for couples)

Health care reform increases None 0.9% Medicare tax on “earned” income over

$200K for singles ($250K for couples)

3.8% tax on investment income over $200K for

singles ($250K for couples)

Bonus depreciation 50% of cost basis for eligible property 50% of cost basis in 2013

Expired in 2014 unless extended by

Congressional action

Estate and Gift tax 35% top rate;

$5 million exemption

(indexed for inflation)

40% top rate;

$5 million exemption

(indexed for inflation)

Selected Items

101 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Key real estate provisions include, among many others:

− 15 year recovery period for leasehold improvements

− Bonus deprecation

− New Markets Tax Credit

− Several charitable and S corporation related extenders

• Permanent and 2 year deal dropped off the table.

Extenders Package-Retroactive and for

2014 Only

102 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Comparison of Real Estate Provisions in Leading Tax Reform Plans

Proposal Rates Expenditures Repealed Other Changes

White House

“Framework”

(corporate only)

• Corporate: 28%,

• Individual: N/A

• Many corporate tax

expenditures (limited detail)

• Lengthen depreciation schedules (no details)

• Ordinary treatment for carried interest

Camp (House) Proposal

• Corporate:25%

• Individual:

10%/25%/35% (high-

income taxpayers

subject to phase-out of

10% bracket)

• Many corporate and

individual tax expenditures;

• Deduction for real estate

taxes;

• Like-kind exchanges;

• Current law depreciation

rules (replacement similar to

ADS);

• Special rules for timber

(REITs)

• Limit mortgage interest deduction to $500k of

indebtedness, no deduction for home equity

loans;

• Phase-out of gain exclusion for sale of

principal residence;

• FIRPTA relief for REITs and RICs;

• Limit taxable subsidiaries of total REIT

assets to 20%

• LIHTC changes

• Ordinary treatment for some carried interest

Baucus (Senate)

Discussion Drafts Drafts do not address rates

• Like-kind exchanges;

• Current-law depreciation

rules

• 43-year depreciable life for real property

(pooling method for other property)

• Modify FIRPTA rules

Wyden-Coats (Senate)

• Corporate:24%

• Individual:

15%/25%/35%

• Many domestic tax

expenditures • Retain current mortgage interest deduction

Bowles-Simpson

(Commission on Fiscal

Responsibility and

Reform)

• Corporate: 1 bracket no

higher than 29%

• Individual: 3 brackets,

top rate no higher than

29%

• Almost all tax expenditures;

• Buy back tax expenditures by

increasing the rate

• 12% tax credit for all taxpayers ($500k

mortgage limit; no second homes)

103 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Bipartisan agreement that FIRPTA rules should be relaxed and

several proposals

• Sen. Robert Menendez, D-N.J., and Rep. Kevin Brady, R-Tex.,

introduced the Real Estate Investment Act (S. 1181; H.R. 2870) in July

2013

− Companion bills would exempt certain REIT stock from FIRPTA

• Obama Administration’s last two budget blueprints have proposed

exempting foreign pension funds from FIRPTA

• Both tax reform draft proposals from Camp and Baucus include

FIRPTA reforms to increase foreign investment in United States

Proposed Changes to FIRPTA Rules

104 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• November elections are now the focus of the political narrative in

Washington with both parties staking their turf

• Camp draft changes the debate from running for office on the merits of tax

reform to defending the details of tax reform

• White House not engaged on details of comprehensive tax reform

• Two sides still far apart on revenue neutral versus revenue-raising tax

reform and distributional impact of reform

Tax Reform Remains a Heavy Lift

105 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Despite the strong headwinds facing the taxwriters, conceptually everyone

still agrees that tax reform is necessary

• Tax reform is likely to be on the agenda until it is actually enacted; work

being done by the committees now is likely to form the basis of future

reform efforts

• Perhaps there is a window to work with a president looking to build a

legacy in last two years of his term

• If Congress does not enact comprehensive reform, focus may turn back to

“loophole closers” not tied to rate reduction, and Camp’s draft arguably

creates a ready-made list from which to choose

However, Ignoring Tax Reform Could Be a

Mistake

Inversions 101

107 Copyright © 2014 Deloitte Development LLC. All rights reserved.

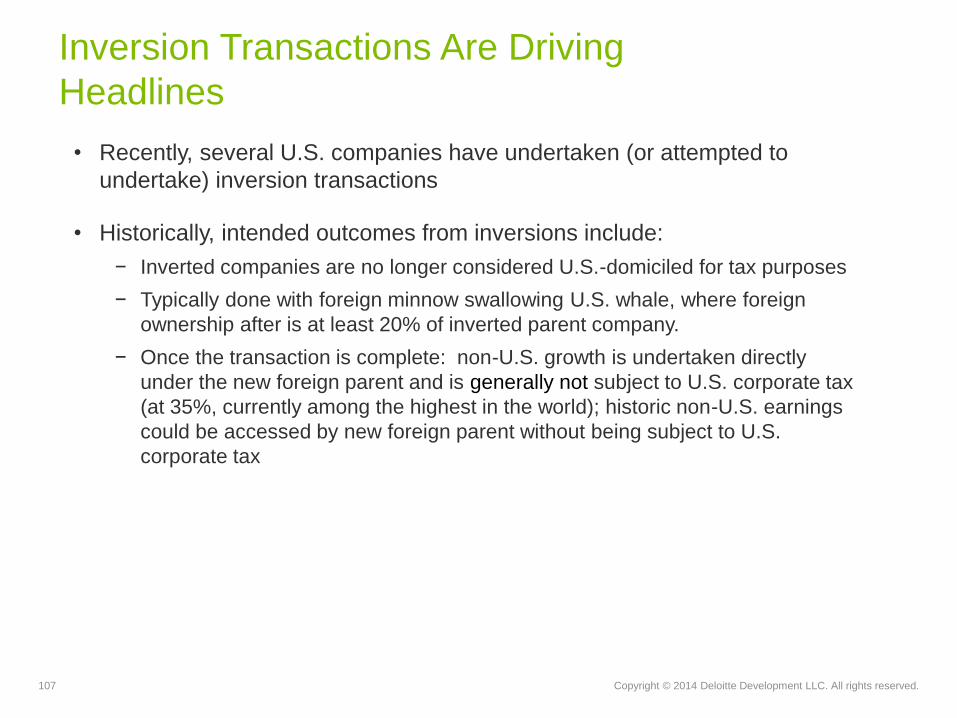

• Recently, several U.S. companies have undertaken (or attempted to

undertake) inversion transactions

• Historically, intended outcomes from inversions include:

− Inverted companies are no longer considered U.S.-domiciled for tax purposes

− Typically done with foreign minnow swallowing U.S. whale, where foreign

ownership after is at least 20% of inverted parent company.

− Once the transaction is complete: non-U.S. growth is undertaken directly

under the new foreign parent and is generally not subject to U.S. corporate tax

(at 35%, currently among the highest in the world); historic non-U.S. earnings

could be accessed by new foreign parent without being subject to U.S.

corporate tax

Inversion Transactions Are Driving

Headlines

108 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Treasury recently released guidance (Notice 2014-52) designed to curtail or

limit the benefit of inversions, in part by making it more difficult to reach the

20% foreign ownership threshold, and to access non-U.S. cash held under

the legacy U.S. parent, among other rules

• Legislation may be required in order to more effectively curtail inversions

• Key takeaway—the inversion discussion and debate illuminates a U.S.

corporate tax rate that is high compared to many countries, and may

stimulate progress toward tax reform for corporations and possibly pass-

throughs and individuals

Inversion Transactions, cont’d

Tangible Property

Regs.—Stretch Run

110 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• The recently finalized tangible property regulations will likely have a significant

impact on virtually every real estate company.

• At a minimum, some clients will have significant compliance requirements for 2014,

including several method changes and current year elections to consider.

• Limited number of companies implemented portion of regulations in 2012 and 2013

• The regulations are effective for tax years beginning on or after 1/1/14 and therefore

need to be adopted on 2014 tax returns. Note that for short tax years this may

apply for tax years ending before 12/31/14.

Background

111 Copyright © 2014 Deloitte Development LLC. All rights reserved.

1. Materials and supplies definitions

− Regulations define what constitute a material and supply. Cost recovery depends on

whether the material and supply is considered incidental (deduct as incurred) or non

incidental (deduct as used/consumed).

− Entities may be over deducting under their capitalization policy

− De minimis safe harbor election may help deal with accounting issues

2. Minimum capitalization threshold (de minimis safe harbor)

− An annual, irrevocable election for taxpayers with applicable financial statements (“AFS”)

and written capitalization policies to expense property in accordance with policies with a

ceiling of $5,000 (without AFS - $500 ceiling limit)

− Intended to provide for deductions consistent with the financial accounting capitalization

dollar threshold (allows for book/tax conformity)

− Consolidated groups may use consolidated AFS and/or written policies

Five focus areas for real estate

112 Copyright © 2014 Deloitte Development LLC. All rights reserved.

3. Capitalization versus repairs

− Unit of property defined as building and its structural components, and separate

building systems

◦ Many examples in the regulations

− Must capitalize amounts that improve a property

◦ Betterment

◦ Restoration

◦ Adaptation

− May apply de minimis safe harbor where applicable

− Annual election to follow book capitalization for amounts otherwise considered

deductible tax repairs

− Will likely need analysis

◦ If prior repair studies, to be reevaluated for additional capitalization

◦ If no prior repair studies, opportunities for additional deductions

◦ Can elect out annually, but only for balance sheet activities

Five focus areas for real estate

113 Copyright © 2014 Deloitte Development LLC. All rights reserved.

4. Routine Maintenance Safe Harbor

− The RMSH allows taxpayers to deduct certain costs that may otherwise be considered

“restorations” if the taxpayer reasonably expects to incur these costs more than once

during an asset’s ADS life

− Requires taxpayers maintain documentation supporting reasonable expectation of

performing activity more than once during ADS life

◦ For buildings and structural components thereof must reasonably expect to perform

activities more than once during 10 year period from Placed in Service date

5. Loss on Dispositions

− May elect to treat partial disposition as disposition of an asset (and thereby recognize gain

or loss); mandatory in certain circumstances

− By recognizing the loss, taxpayer must capitalize any related repair

− Deemed election; simply report on Form 4797

Five focus areas for real estate

114 Copyright © 2014 Deloitte Development LLC. All rights reserved.

Considerations

• At a minimum, compliance with the regulations will likely require significant analysis of current

and prior year information

Potential planning

• The de minimis election will likely be made by most taxpayers

• Many of our clients are surfacing significant deductions via the partial disposition rules

discussed in area 5 above.

• Many real estate taxpayers may want to consider the book capitalization election as well; note

it only covers balance sheet activities (anything capitalized for book purposes)

• As noted, method changes are made entity by entity, and method by method, providing great

flexibility to taxpayers

Potential action steps for 2015

• If election has not yet been made, need to complete by filing of 2014 tax returns

• Generally, most taxpayers that own tangible property should expect to file Form 3115 with

their 2014 tax returns if election was not made under the early adoption regimes in 2012 or

2013

Observations and analysis

What’s Really Real

Estate?

116 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Multiple public company REIT conversions in past 3 years.

• Non-traditional asset classes proliferate

− Data centers, cell towers, billboard advertising, electrical transmission, pipelines, prisons,

document storage, casinos

• Proliferation of private letter rulings concluding various assets qualify as real estate

• Extensive press coverage leads to congressional saber-rattling

• IRS convenes working group to consider what constitutes real estate

Market Trends

117 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Proposed regs (§ 1.856-10) issued May 2014 clarify guidance on the definition of

"real property" for REIT asset test purposes

• The proposed regulations define real property to include:

− Land (including water and air space adjacent to land, and natural products and deposits)

− Inherently permanent structures (IPS)

◦ Buildings

◦ Other IPS

− Structural components

− Intangibles

New Proposed Regs.

118 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Safe harbor lists of assets that qualify as real estate

− Buildings: houses, apartments, hotels, factory and office buildings; warehouses, barns,

enclosed garages, enclosed transportation stations and terminals, and stores.

− Other IPS: microwave transmission, cell, and broadcast towers, telephone poles, parking

facilities, bridges, tunnels, roadbeds, railroad tracks, transmission lines, pipelines, fences,

in-ground pools, offshore drilling platforms, storage structures (silos, O&G storage tanks),

stationary wharves and docks, outdoor advertising displays.

− Structural components: wiring, plumbing, heating/air, elevators/escalators, walls, floors,

ceilings, windows, doors, insulation, fire suppression systems, central refrigeration,

security systems, & humidity control

Safe Harbors

119 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Assets not listed under the safe harbor provision must undergo a facts and

circumstances determination; factors include:

− The manner in which the asset is affixed to the property;

− Whether the asset is designed to remain in place indefinitely;

− Any damage the removal of the asset would cause to the asset or related real property;

− Any circumstances that suggest an other-than-indefinite period of being affixed;

− The time and expense required to remove the asset.

Facts & Circumstances

120 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• Recent proposed regulation defines real property ONLY for REIT qualification

purposes.

− No impact on depreciation, FIRPTA, etc.

• Adopts rules generally consistent with existing law.

− Clarify existing rules, rather than expand definitions.

− Unlikely to result in re-classifications of property.

• May help alleviate the need for REITs to obtain private letter rulings.

• Little impact on REIT quarterly compliance.

− Consider need for addition documentation for assets not on safe harbor list.

− Auditors may require additional work around “facts & circumstances” determinations.

Implications

Marketplace Structures

“What’s Out There?”

122 Copyright © 2014 Deloitte Development LLC. All rights reserved.

REIT Structures

Op Co / Prop Co--Birth and Spinoff of

REIT/Lessor REIT Conversion--Reduce Corporate Tax

• Corp contributions property to

newly-formed REIT and

establishes lease arrangement with

Op Co

• REIT shares distributed to

shareholders

• Ownership test concerns and other

benefits/complexities with REIT in

structure

• Corp makes a REIT election and

benefits from dividends-paid

deduction

• TRS is subsidiary of REIT − TRS established to hold non-

qualifying operations or to

provide services to customers

• Considerations around transfer

pricing, E&P distribution, and

built-in gain tax/period

123 Copyright © 2014 Deloitte Development LLC. All rights reserved.

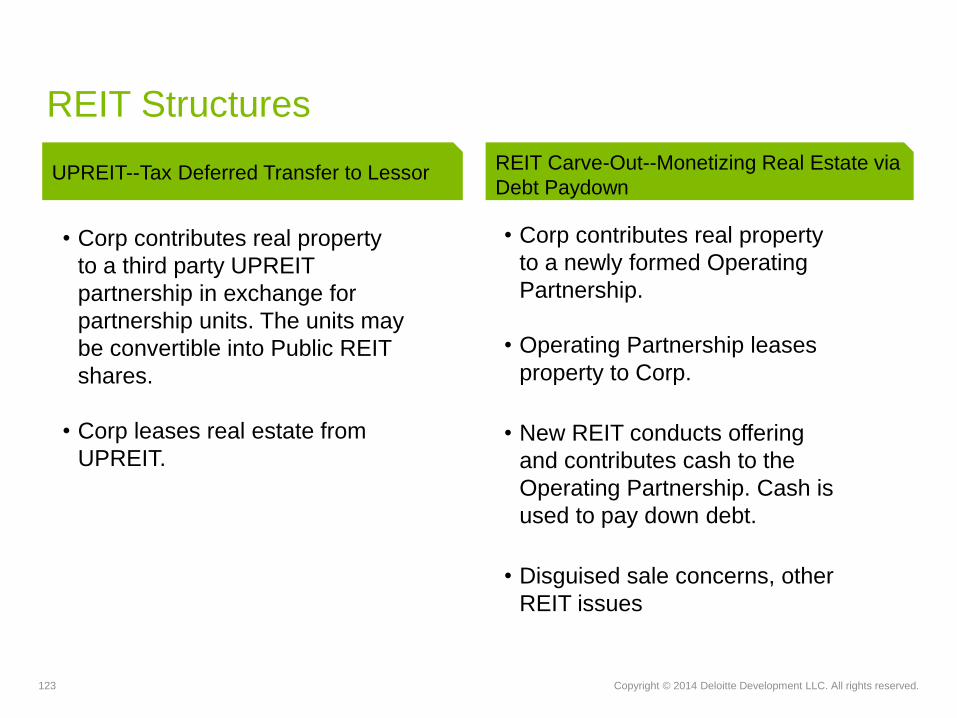

REIT Structures

• Corp contributes real property

to a newly formed Operating

Partnership.

• Operating Partnership leases

property to Corp.

• New REIT conducts offering

and contributes cash to the

Operating Partnership. Cash is

used to pay down debt.

• Disguised sale concerns, other

REIT issues

REIT Carve-Out--Monetizing Real Estate via

Debt Paydown UPREIT--Tax Deferred Transfer to Lessor

• Corp contributes real property

to a third party UPREIT

partnership in exchange for

partnership units. The units may

be convertible into Public REIT

shares.

• Corp leases real estate from

UPREIT.

Other Hot Topics: What

Are We Seeing?

125 Copyright © 2014 Deloitte Development LLC. All rights reserved.

• LTIPs and profits interests, generally

• Debt allocation planning

− Proposed regulations limiting the use of bottom-dollar guarantees

− The current rules do not explicitly require that a partner/member’s net worth be

considered in evaluating whether the debt is allocable to the partner/member

− Proposed regulations fundamentally change how economic risk of loss is determined

under Treas. Reg. § 1.752-2

• Like-kind exchanges and the like

• Tax rate planning focus

− Rates are the highest in years

Other Hot Topics: What Are We Seeing?

About Deloitte