2013 retirement confidence survey mathew greenwald mathew greenwald & associates presented to...

TRANSCRIPT

2013 Retirement Confidence SurveyMathew Greenwald

Mathew Greenwald & Associates

Presented to American Savings Education CouncilWashington, DCApril 10, 2013

2

2013 RCS Methodology

• 23rd annual measure of worker and retiree confidence about retirement

• 1,254 20-minute phone interviews conducted in January 2013 using random-digit dialing with cell phone supplement

• Interviewed Americans ages 25 and over

• Two questionnaire versions- 1,003 interviews with workers (not retired) - 251 interviews with retirees

DECLINING RETIREMENT CONFIDENCE

4

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Very Somewhat Not Too Not At All Don't Know/Refused

Worker Confidence About Having Enough Money for Retirement Resumes Slow, Downward Trend

Overall, how confident are you that you (and your spouse) will have enough money to live comfortably throughout your retirement years? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1993-2013 Retirement Confidence Surveys.

28%

21%

38%

13%

10%

19%

43%

27%

17%

18%

41%

22%

8%

19%

51%

21%

5

Roughly 4 in 10 Workers Believe They Need to Save 20% or More of Their Income to Comfortably Retire

About what percentage of your total household income do you think you (and your spouse) need to save each year from now until you expect to retire so you can live comfortably throughout your retirement? (2013 Workers who plan to retire n=931)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

0% to 9%

10% to 14%

15% to 19%

20% to 29%

30% to 39%

40% to 49%

50% or more

Don't know / Refused

8%

14%

11%

20%

8%

2%

13%

23%

6

One-third of Workers Have Dipped into Savings to Pay for Basic Expenses

In the past 12 months, have you (and your spouse) had to dip into your savings to pay for basic expenses? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1994-2013 Retirement Confidence Surveys.

2011 2012 2013

34% 34%31%

7

6 in 10 Workers Report a Problem With DebtThinking about your current financial situation, how would you describe your level of debt? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2005-2013 Retirement Confidence Surveys.

A Major Problem A Minor Problem Not a problem

20%

39% 40%

20%

42%38%

16%

44%39%

2005 2012 2013

8

Definitely could

Probably could

Probably could not

Definitely could not

50%

20%

12%

16%

Only Half of Workers Are Confident They Could Come Up With $2,000 for Unexpected Need

How confident are you that you could come up with $2,000 if an unexpected need arose within the next month? Do you think you definitely could, probably could, probably could not, or definitely could not come up with the full $2,000? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

9

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

38% 43% 40%25% 25%

49% 41% 42%

49% 45%

9%10% 11%

14%13%

3% 6% 7% 11% 16%

Very Somewhat Not Too Not At All Don't Know/Refused

The Percentage of Workers Not at All Confident About Having Enough for Basic Expenses Continues to Increase

How confident are you that you will have enough money to take care of your basic expenses during your retirement? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1993-2013 Retirement Confidence Surveys.

10

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

17%24% 20%

14%

36%

42% 46%

34%

22%

19% 18%

23%

21%13% 14%

29%

Very Somewhat Not Too Not At All Don't Know/Refused

Worker Confidence About Paying for Medical Expenses in Retirement Continues to Decline

How confident are you that you will have enough money to take care of your medical expenses during your retirement? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1993-2013 Retirement Confidence Surveys.

11

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

15% 17%9% 11%

29%36%

30% 26%

26%23%

27%23%

28%21%

33% 39%

Very Somewhat Not Too Not At All Don't Know/Refused

The Percentage of Workers Not at All Confident About Paying for Long-term Care Reaches New High

How confident are you that you will have enough money to pay for long-term care, such as nursing home or home health care, should you need it during your retirement? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2000-2013 Retirement Confidence Surveys.

12

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

22%31%

24% 26%17%

42%

43%45% 45%

47%

20%14%

15% 15%15%

15% 11% 14% 13%21%

Very Somewhat Not Too Not At All Don't Know/Refused

Worker Confidence About Doing a Good Job Preparing for Retirement Continues Slow Decline

How confident are you that you are doing a good job of preparing financially for your retirement? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1993-2013 Retirement Confidence Surveys.

SAVINGS FOR RETIREMENT STEADY BUT LOW

14

Workers Calculating Retirement Needs Up Slightly in 2013, Steady Since 2000 Peak

Have you (or your spouse) tried to figure out how much money you will need to have saved by the time you retire so that you can live comfortably in retirement? (2013 Workers n=1003, percent yes)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1993-2013 Retirement Confidence Surveys.

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

32% 31% 32%29%

33%

42%45%

51%

39%

32%37%

0.480.53

0.440.38

0.430.420.420.420.430.47

0.440.460.420.42

0.46

Respondent Respondent and/or Spouse

15

Many Workers Guess to Determine Savings Needed for Comfortable Retirement

How did you (or your spouse) determine this amount? Did you…? (2013 Workers giving an amount needed for retirement) (Top mentions, multiple responses accepted)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

Guessed

Did own estimate

Asked a financial advisor

Used an online calculator

Read or heard that is how much needed

45%

18%

18%

8%

8%

12%

40%

33%

17%

6%

73%

0%

5%

0%

10%

Did not do calculation (n=426)Did calculation (n=467)All workers (n=898)

16

The Share of Workers Having Saved for Retirement Holds Steady at About Two-thirds

Not including Social Security taxes or employer-provided money, have you (and/or your spouse) personally saved any money for retirement? These savings could include money you personally put into a retirement plan at work. (2013 Workers n=1003, percent yes)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1994-2013 Retirement Confidence Surveys.

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

57% 58% 60%66%

59%

68%74%

65% 67% 68%

0.730.78

0.69 0.72 0.71 0.68 0.69 0.70.66

0.72 0.750.69 0.68 0.66 0.66

Respondent Respondent and/or Spouse

17

But There Has Been a Severe Decline in Retirement Saving Among Lower-income Workers

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2009-2013 Retirement Confidence Surveys.

49%

80%

93%

35%

74%

93%

24%

76%

94%

2009 2012 2013

Not including Social Security taxes or employer-provided money, have you (and/or your spouse) personally saved any money for retirement? These savings could include money you personally put into a retirement plan at work.

Workers withHousehold Incomes

<$35,000

Workers withHousehold Incomes

$35,000-$74,999

Workers withHousehold Incomes

$75,000+

18

The Percentage of Workers Currently Saving for Retirement Continues Slow Decline

Are you (and/or your spouse) currently saving for retirement? (2013 Workers n=1003, percent yes)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2001-2013 Retirement Confidence Surveys.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

61% 61% 62%58%

62% 64%60%

64% 65%60% 59% 58% 57%

19

Proportion of Workers With Less Than $10,000 of Savings up Ten Percentage Points Since 2008

In total, about how much money would you say you (and your spouse) currently have in savings and investments, not including the value of your primary residence? (2013 Workers n=1003)

2003 2008 2009 2010 2011 2012 2013

Less than $1,000

55%36%

20% 27% 29% 30% 28%

$1,000 - $9,999 19 16 17 18 18

$10,000 - $24,999 13 13 11 10 12 11

$25,000 - $49,999 15 12 11 12 11 10 9

$50,000 - $99,999 11 12 12 11 9 10 10

$100,000 - $249,999 11 15 12 11 14 11 12

$250,000 or more 7 12 12 11 10 10 12

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2003-2013 Retirement Confidence Surveys.

20

Cost of Living and Affordability Predominant Reasons Workers Don’t Contribute More to DC Plan

What is the main reason you are not currently contributing (more) money to the plan? (2013 Workers offered employer-sponsored retirement savings plan n=510)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

Cost of living/day-to-day expenses

Can’t afford to give more

Already contributing plan/legal maximum

Prefer to invest elsewhere/Don’t like plan/investments

Don’t need to save more

Paying off mortgage/housing expenses

Other savings priorities

Paying off other debt

Education expenses

Health costs/health insurance costs

Other

Don't know / Refused

41%

18%

10%

8%

6%

6%

5%

4%

4%

1%

7%

3%

21

6 in 10 Workers—Including Half of Nonsavers—Said They Could Save More for Retirement in 2011 RCS

Do you think it is reasonably possible for you to save $25 a week (more than you are currently saving) for retirement? (2011 Workers n=1004, percent yes)If yes: What would you cut back on or give up to save that (extra) $25 a week? (n=674, top mentions)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2011 Retirement Confidence Survey.

All Workers Savers Nonsavers

62%68%

48%

Dining out

Entertainment/Leisure

Smoking/Cigarettes

Groceries

Impulse buying

Bills

Clothing

Nothing

33%

21%

10%

10%

9%

6%

6%

9%

22

Most Not Offered DC Plan Would Continue Contribution Even if 6% Withheld Through Auto-Enrollment

Suppose your employer automatically enrolled you into a retirement savings plan, withholding 3%/6% of your pay each pay period to contribute to your account. Do you think you would be most likely to… ? (2013 Workers not offered plan n=162)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

Increase the contribution

Leave the contribution as it is

Continue the contribution, but decrease the amount

Cancel the contribution

Don't know / Refused

35%

42%

7%

11%

5%

11%

44%

24%

16%

5%6% Deferral3% Deferral

EXPECTATIONS ABOUT RETIREMENT: REALISTIC OR NOT?

24

Before 60 60-64 65 66-69 70 or older Never retire Don't know

19%

31%34%

2%

9%

0%

5%

24% 25% 25%

2%

7%9% 8%

16%

21%25%

7%

17%

6%9%

11%

21%24%

9%

20%

6% 7%8%

16%

26%

11%

26%

7%5%

9%

14%

25%

10%

26%

7%9%

1991 1998 2003 2008 2012 2013

The Age at which Workers Expect to Retire Has Increased Steadily Since 1991

Realistically, at what age do you expect to retire? (2013 Workers n=1003)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

25

Under 55 55-59 60-64 65 66-69 70 or older Never retire Don't know

3%6%

14%

25%

10%

26%

7% 8%

21%

16%

32%

11%8%

6%

1% 1%

Workers (n=1003) Retirees (n=251)

More than One-third of Workers Expect to Retire After Age 65; Just 1 in 7 Retirees Retired Then

Realistically, at what age do you expect to retire?/How old were you when you retired?

MedianWorkers 65Retirees 62

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

26

Nearly Half of Retirees Indicate Their Retirement Occurred Earlier Than Planned

Did you retire earlier than you planned, later than you planned, or about when you planned? (2013 Retirees n=251)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1991-2013 Retirement Confidence Surveys.

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

52%

40%

48% 49%45%

40%36%

39%

45%

39% 37%40% 38% 37%

51%47%

41%45%

50%47%

43%

53%

42%39%

42%

48%52%

48% 47% 48%52% 50% 52%

55%

40% 42%

49%46%

37%

43%

3% 3%7% 7% 5% 5% 6% 5% 5% 5% 6% 5% 5% 5% 4%

7%4% 3%

9%6%

Earlier Than Planned About When Planned Later Than Planned

27

People Retire Early for a Variety of Reasons, Though Over Half of Retirees Cite Health Problems as a Factor

Why did you retire earlier than you had planned? (2013 Retirees retiring earlier than planned n=127)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

You had a health problem or disability

You could afford to retire earlier

You had to care for a spouse or another family member

Changes at your company

You had another work-related reason

You wanted to do something else

Changes in the skills required for your job

55%

32%

23%

20%

20%

19%

9%

28

Workers Are Much More Likely to Think They Will Work in Retirement Than Retirees Actually Worked

Do you think you will do any work for pay after you retire?/Have you worked for pay since you retired? (2013 Workers expecting to retire n=931, Retirees n=251)

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 1994-2013 Retirement Confidence Surveys.

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

56%

66% 63% 61%66%

70% 68% 66% 67% 66% 63%

72% 70%74%

70% 69%

22%27%

22%26% 24%

28%32%

26% 27%

37%

25%

34%

23% 23%27% 25%

Workers Retirees

29

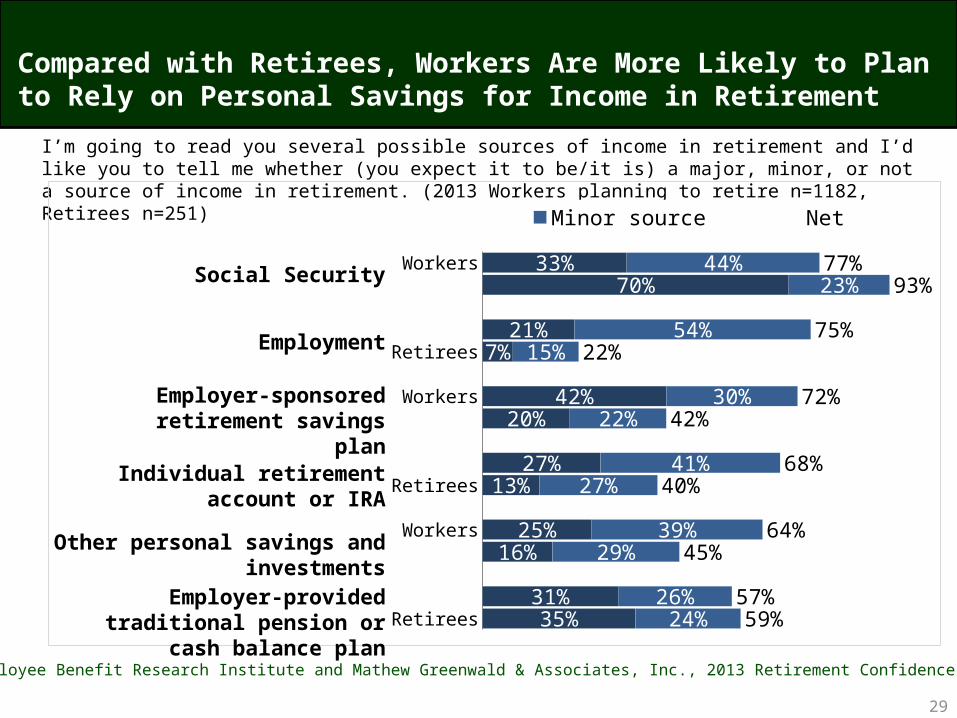

Compared with Retirees, Workers Are More Likely to Plan to Rely on Personal Savings for Income in Retirement

I’m going to read you several possible sources of income in retirement and I’d like you to tell me whether (you expect it to be/it is) a major, minor, or not a source of income in retirement. (2013 Workers planning to retire n=1182, Retirees n=251)

WorkersRetirees

WorkersRetirees

WorkersRetirees

WorkersRetirees

WorkersRetirees

WorkersRetirees

33%70%

21%7%

42%20%

27%13%

25%16%

31%35%

44%23%

54%15%

30%22%

41%27%

39%29%

26%24%

77%93%

75%22%

72%42%

68%40%

64%45%

57%59%

Minor source Net

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2013 Retirement Confidence Survey.

Employer-sponsored retirement savings plan

Other personal savings and investments

Social Security

Individual retirement account or IRA

Employer-provided traditional pension or cash balance plan

Employment

30

Interpretive Comments

• A grim picture, but heartening evidence we have learned

– Found that defaults work

– Evidence of more realism on savings from workers, hopefully a first step

• Now, focus on more defaults and more effective defaults

– Auto enroll at 5%-6%, auto escalate for five years

– More use of commitment devices

31

Interpretive Comments

• Focus on more effective use of accumulations

– Gamma can produce 29% more retirement income

• Focus on more effective Social Security claiming

• Don’t let expectation of longer work forgive need for accumulation

– Two targets, one at age 60 the other at target retirement age

• Need more effective mileposts for on-track accumulation

• Culture of spending should be addressed

• “Hyper-discounting” should be addressed