©2013, college for financial planning, all rights reserved. module 4 the federal gift tax certified...

TRANSCRIPT

©2013, College for Financial Planning, all rights reserved.

Module 4The Federal Gift Tax

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMEstate Planning

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-2

Questions to Get Us Warmed Up

4-3

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-4

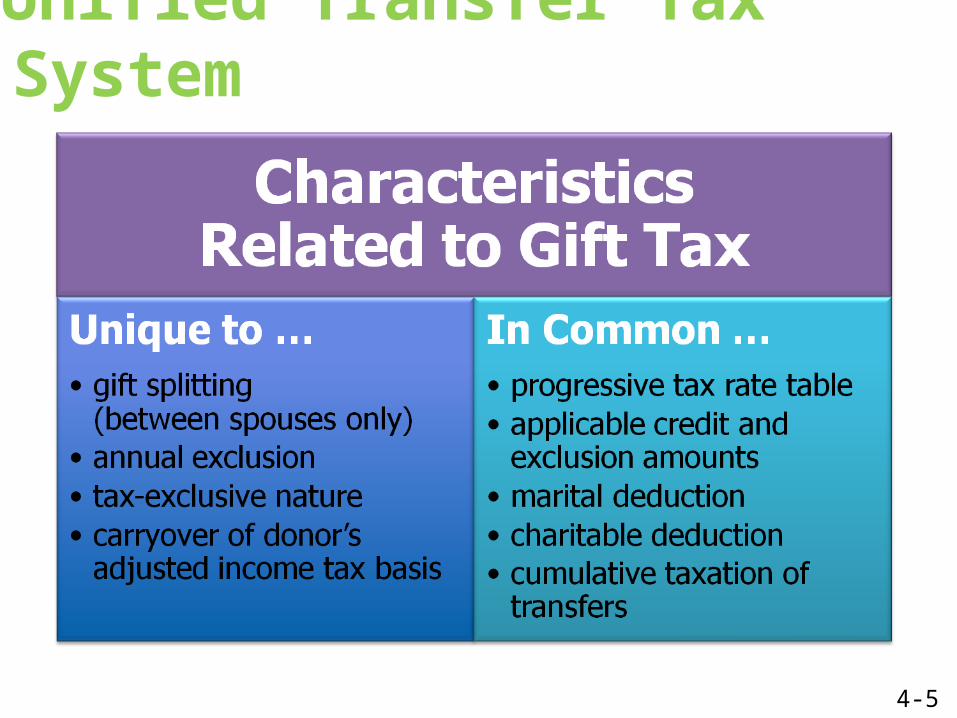

Unified Transfer Tax System

4-5

Gift Tax: Nature & Incidence• tax on transfer of wealth during lifetime• qualifying transfers to a spouse and qualified

charities are wholly deductible• tax on taxable lifetime transfers up to gift tax

exclusion amount are paid by gift tax credit amount

• annual exclusion available for present interest gifts to any donee on an annual basis (limited by indexed amount)

• donor (or estate if donor is deceased) is responsible for reporting and payment

4-6

Gift Tax: Return Requirements• filed on IRS Form 709 on a calendar-year basis

• return is due April 15 of following calendar year, or upon filing of the donor’s estate tax return if earlier

• donor (or donor’s executor) is responsible for filing of return and payment of tax, if any

• valuation date is the date of completion for each gift

• return must be filed if donor has made:o present interest gifts > the maximum annual

exclusion (that do not also qualify automatically for the marital or charitable deduction)

o future interest gifts of any amounto split gifts with spouseo a gift for which the QTIP election is takeno a partial interest charitable gift

4-7

Question 1

Which one of the following situations does not require the filing of a federal gift tax return? a. A donor makes a transfer to one donee of a

present interest valued at less than the annual exclusion, but has used all of his or her applicable credit amount to offset the tax on prior gifts.

b. A donor and spouse agree to split a present interest gift to one donee valued at more than the annual exclusion, but less than twice the annual exclusion amount.

c. A donor transfers to one donee a future interest valued at less than the annual exclusion amount.

4-8

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-9

Video

Play Video• CFP 5 Chapter 14• 7 minutes• Play video from

Video Layout

Text chat or other questions

4-10

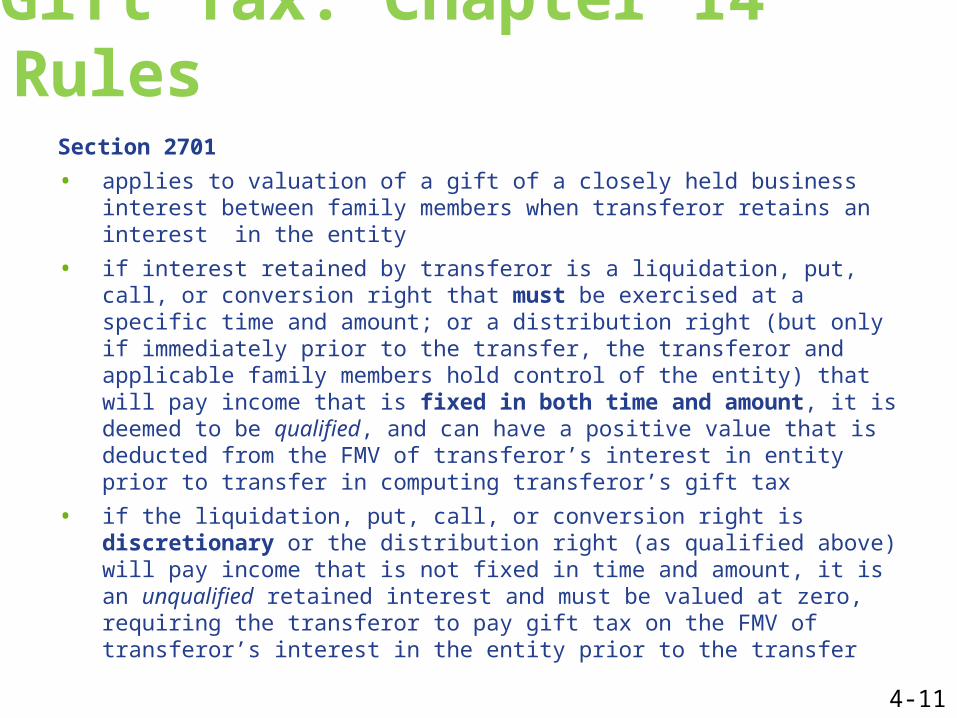

Gift Tax: Chapter 14 Rules

Section 2701

• applies to valuation of a gift of a closely held business interest between family members when transferor retains an interest in the entity

• if interest retained by transferor is a liquidation, put, call, or conversion right that must be exercised at a specific time and amount; or a distribution right (but only if immediately prior to the transfer, the transferor and applicable family members hold control of the entity) that will pay income that is fixed in both time and amount, it is deemed to be qualified, and can have a positive value that is deducted from the FMV of transferor’s interest in entity prior to transfer in computing transferor’s gift tax

• if the liquidation, put, call, or conversion right is discretionary or the distribution right (as qualified above) will pay income that is not fixed in time and amount, it is an unqualified retained interest and must be valued at zero, requiring the transferor to pay gift tax on the FMV of transferor’s interest in the entity prior to the transfer

4-11

Gift Tax: Chapter 14 Rules

Section 2702

• applies to valuation of a transfer of an interest in trust (or equivalent) to a related family member in which transferor retains a beneficial interest

• If interest retained is an annuity, unitrust, or noncontingent remainder interest (where all income interests are annuity or unitrust interests), it is deemed to be qualified, and can have a positive value that is deducted from the FMV of transferor’s interest in trust assets prior to transfer in computing transferor’s gift tax.

• If interest retained is unqualified, it must be valued at zero, requiring transferor to pay gift tax on the FMV of transferor’s interest in the trust assets prior to transfer.

• Exceptions are: QPRT, CRT, PIF, CLT, and QDOT transfers in trust deemed to be for full and adequate consideration in a divorce, and when the remaining interests in the trust are retained by the other spouse.

4-12

Gift Tax: Chapter 14 Rules

Section 2703

• Applies to gift and estate tax valuation of property subject to an agreement, option, or other right to acquire property at less than fair market value, or any restriction on the right to sell or use property.

• Such rights and restrictions are ignored in valuation unless the transaction is

1. a bona fide business arrangement;2. not an attempt to transfer property to family members for less

than full and adequate consideration; and3. similar to an arm’s-length transaction.

• A right or restriction is presumed to meet each of these requirements if more than 50% by value of the property subject to the right or restriction is owned directly or indirectly by individuals who are not members of the transferor’s family

4-13

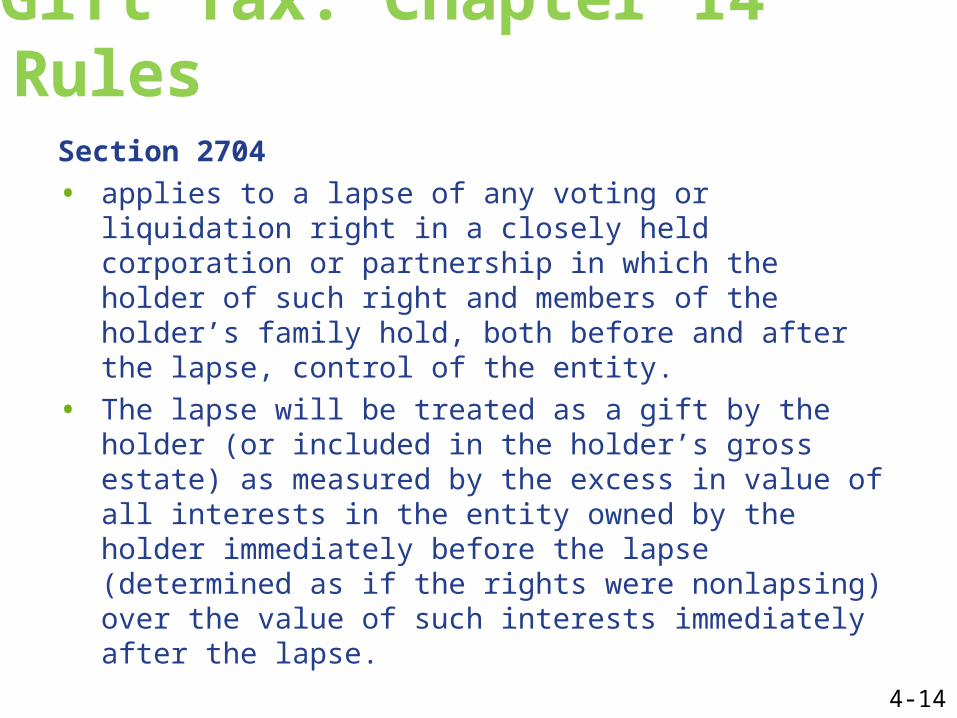

Gift Tax: Chapter 14 Rules

Section 2704

• applies to a lapse of any voting or liquidation right in a closely held corporation or partnership in which the holder of such right and members of the holder’s family hold, both before and after the lapse, control of the entity.

• The lapse will be treated as a gift by the holder (or included in the holder’s gross estate) as measured by the excess in value of all interests in the entity owned by the holder immediately before the lapse (determined as if the rights were nonlapsing) over the value of such interests immediately after the lapse.

4-14

Reserved Powers that Cause a Gift To Be Incomplete

• Power to revoke the transfer• Power to name additional, different, or

alternate donees or beneficiaries• Power to alter the proportionate

shares of the donees or beneficiaries

4-15

Reserved Powers that Will Not Cause a Gift To Be Incomplete

• Power to change the time and manner of a donee’s or beneficiary’s enjoyment of the property

• Power as a fiduciary that is limited by an ascertainable standard

• Power to alter or revoke a gift that can be exercised only with the consent of a party with a substantial adverse interest

4-16

Question 2

Last year, Nate established an irrevocable trust and funded it with his portfolio of income-producing stock valued at $440,000. The trust provides that the trustee is to pay Nate 6.5% of the initial value of the trust annually for a period of 15 years.

After the 15-year term, the trustee is to pay the remaining assets in the trust to Nate’s daughter, Karen.

Which one of the following is a correct statement regarding the gift tax implications of this trust arrangement? a. IRC Chapter 14 does not apply because this is an

intrafamily transfer. b. Nate’s retained interest is not a “qualified” interest for

IRC Chapter 14 purposes. c. Nate will have to pay gift tax only on the present value of

the remainder interest. d. Nate must file a federal gift tax return indicating that he

has made a taxable gift of $440,000 to his daughter, Karen.

4-17

Question 3

Only direct transfers of present interests are completed transfers that are taxable for federal gift tax purposes. True False

4-18

Question 4

Suzie was given a general power of appointment exercisable during the month of December that gives her the right to name the recipients of funds added to an irrevocable trust during the prior eleven months of the year. The trust was created and funded by her father. She will be subject to federal gift tax only if she names someone other than herself to receive the funds during December or renounces her right to exercise the power ever again. TrueFalse

4-19

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-20

Gift Tax: Exempt Transfers

• Political contributions

• Direct and exclusive payment of medical expenses for an individual

• Direct and exclusive payment of tuition expenses for an individualo Medical and tuition payments are

unlimited in amount.o Medical and tuition payments are

also exempt from generation-skipping transfer tax.

o Persons benefited do not have to be related to donor.

o These payments will not lower the amount of annual exclusion gifts that can be made to the party benefited in the year of payment.

4-21

Question 5

Which one of the following transfers that would otherwise be a gift for federal gift tax purposes is exempted on public policy grounds? a. a check for $14,500 payable to your

nephew so he will have funds to pay his book fees and tuition

b. a payment of $15,000 to a special fund set up to pay the doctors and hospital for a neighbor’s rehabilitative surgery

c. a contribution of $300 to a political partyd. an outright gift of $30,000 to your

spouse4-22

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-23

Federal Gift Tax Worksheet(1) Total calendar-year gifts

(a) Gifts made by the donor $(b) One-half of gifts split with spouse(c) Adjusted gifts of donor (line 1a minus line 1b)(d) One-half of gifts spouse split with donor(e) Total calendar-year gifts (line 1c plus line 1d) $

(2) Subtractions (exclusions and deductions)(a) Annual exclusions allowable $(b) Marital deduction (after annual exclusion)(c) Charitable deduction (after annual exclusion)(d) Total subtractions (line 2a plus lines 2b and 2c) $

(3) Taxable gifts for the calendar year (line 1e minus line 2d)(4) Prior taxable gifts(5) Total taxable gifts (line 3 plus line 4)(6) Total tentative tax (tax computed on line 5)(7) Prior tentative tax (tax computed on line 4)(8) Current tentative tax (line 6 minus line 7) $(9) Available applicable credit

(a) Maximum applicable credit for current year $(b) Applicable credit used in prior years(c) Applicable credit available (line 9a minus 9b)

(10) Net federal gift tax for the calendar year (line 8 less line 9c) $

4-24

Gift Tax: Gift Splitting

Prerequisites

• At time of gift, each spouse must be a U.S. citizen or resident alien.

• Spouses must be married at time of completion of the gift, and, if subsequently divorced, must not remarry during remainder of calendar year.

• Each spouse must consent to gift splitting for all gifts made during the calendar year by either spouse to third parties while married to the other.

4-25

Question 6

“Gift splitting” means that spouses may file a joint gift tax return. TrueFalse

4-26

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-27

Gift Tax: Annual Exclusion

• Donee must be able to immediately use, possess, or enjoy what has been given.

• In a trust, only income beneficiaries can possibly have a present interest.

• Three ways in which trust income beneficiaries can be deemed to have a present interest are if1. income is payable on a mandatory basis at least

annually (Section 2503(b) Mandatory Income Trust),

2. the beneficiary holds a Crummey power (Crummey Trust), or

3. an annual exclusion is awarded by statute (Section 2503(c) Minor’s Trust; Section 529 plan accounts; Coverdell Education Savings Accounts; UTMA; UGMA).

4-28

Gift Tax: Marital Deduction

Prerequisites

• Spouses must be married at completion of gift.

• Donee spouse must be a U.S. citizen.

• The gift must be included in the donor’s total calendar year gifts.

• The donee spouse must not be given a terminable interest, or must receive a terminable interest that is deductible such as an interest that is eligible for the QTIP election (and the election is made).

4-29

Question 7

Which one of the following correctly describes the federal gift tax annual exclusion? a. It is the maximum amount of present

interest gifts allowed per donee per year or the actual amount given to the donee, whichever is less.

b. It applies to completed gifts of whole or partial interests and present or future interests.

c. It allows a donor to completely avoid tax liability on a qualifying transfer of any amount.

d. It is available only to gifts made by married donors.

4-30

Question 8

Which one of the following gifts will not qualify for the federal annual gift tax exclusion? a. a gift of securities valued at $50,000 to an

irrevocable trust for the benefit of your minor child, with trust provisions that allow either trust income or corpus to be used at the trustee’s discretion for the benefit of the child prior to age 21, and that entitle your child to both accumulated income and corpus at that age.

b. an outright gift to your spouse of a $20,000 certificate of deposit

c. a gift to your two nieces of a $42,000 remainder interest in a Section 2503(b) trust

d. the transfer to a minor child of a life insurance policy with an existing cash value, pursuant to the Uniform Transfers to Minors Act (UTMA)

4-31

Question 9

Which one of the following does not qualify for a federal gift tax marital deduction? a. a gift to your spouse of a joint tenancy interest in

property you previously held solely in your nameb. a lifetime transfer of income-producing securities to

an irrevocable trust, with all income going annually to your spouse for 10 years, and the remainder going to your two children equally

c. a lifetime transfer of income-producing securities to an irrevocable trust, with all income going annually to your two adult children equally for five years, and the remainder going to your spouse

d. a lifetime transfer of non-income-producing property to an irrevocable trust with no mandatory payment of income to your spouse during life, but with accumulated income and corpus payable to your spouse’s estate

4-32

Learning Objectives

4–1 Describe the basic features of the federal gift tax.4–2 Describe the purpose and basic features of the

special valuation rules under IRC Chapter 14.4–3 Analyze a situation to identify factors that would be

relevant in determining the value of gifted assets.4–4 Analyze a situation to identify transfers included in

total gifts, and/or deductions that are available in calculating taxable gifts.

4–5 Analyze a situation to calculate the federal gift tax.4–6 Analyze a situation to determine the tax impact of

lifetime transfers on subsequent lifetime transfers by the donor, and on a donee spouse’s potential estate tax liability.

4-33

Gift Tax: Charitable Deduction

Prerequisites• gift must be of cash or property• deduction only for excess of value of what

is given over value of what is received• transfer cannot be of a partial interest

unless it is in a form authorized by the Code

• property must be included in donor’s calendar year gifts

4-34

Gift Tax: Charitable Techniques• outright charitable gift• charitable bargain sale• charitable stock bailout• charitable gift annuity• remainder interest in

a farm or personal residence

• charitable lead trusts• charitable remainder trusts• pooled income funds

4-35

Gift Tax: Charitable Bargain Sale• donor sells asset to qualified charity

for less than fair market value• donor receives charitable gift tax

deduction for difference between the sale price and the asset’s fair market value (less the annual exclusion)

• donor may recognize gain on sale portion

• asset is removed from donor’s gross estate

4-36

Gift Tax: Charitable Stock Bailout• donor gives highly

appreciated closely held stock to charity

• donor receives charitable gift tax deduction for FMV of stock (less annual exclusion)

• corporation redeems stock from charity (the corporation must not be under a legal obligation to redeem)

• remaining corporate shareholders own larger share of corporation after redemption as redeemed shares are retired and not reissued

4-37

Gift Tax: Charitable Gift Annuity• donor transfers cash or property to charity in

exchange for charity’s promise to pay an annual annuity amount to donor, or someone designated by donor, during that person’s lifetime

• donor receives a charitable gift tax deduction for difference in value of property given to charity, and present value of annuity payments (less the annual exclusion only if immediate annuity)

• if annuity interest is given to anyone other than the donor or the donor’s spouse, gift tax will usually result

4-38

Gift Tax: Pooled Income Funds• can be established only by 50% charities

• donor transfers property to the fund, but retains a life income interest for one or more living individuals; a noncontingent remainder interest is given to the charity

• fund managed by the charity

• income beneficiary gets proportionate share of net income of the fund annually until death

• if income interest is given solely to donor’s spouse, QTIP election can be made to gain marital deduction

• if income interest is given to someone other than donor’s spouse, gift tax will result

4-39

Question 10

The following is a complete list of all the gratuitous transfers made by Jim Tuckle in the current year: o contributed $1,000 to the Republican Party o gave his wife the sole income interest in a Section 2503(b)

trust for 10 years (valued at $82,000) o gave $14,000 in cash to his brother o established and funded a revocable trust with $100,000 in

cash, naming himself as trustee.

He distributed $17,000 of property to his mother from this revocable trust. Jim had taxable transfers in prior years of $100,000.

What is Jim's gift tax liability for the current year before application of the gift tax applicable credit amount? Use the United Federal Estate and Gift Tax Rates table. a. $0b. $21,720c. $23,800d. $46,800

4-40

Jim Tuckle Gift Tax Calculation

(1) Total calendar-year gifts(a) Gifts made by the donor $113,000(b) One-half of gifts split with spouse(c) Adjusted gifts of donor (line 1a minus line 1b) 113,000(d) One-half of gifts spouse split with donor(e) Total calendar-year gifts (line 1c plus line 1d) $113,000

(2) Subtractions (exclusions and deductions)(a) Annual exclusions allowable $42,000(b) Marital deduction (after annual exclusion)(c) Charitable deduction (after annual exclusion)(d) Total subtractions (line 2a plus lines 2b and 2c) $42,000

(3) Taxable gifts for the calendar year (line 1e minus line 2d) 71,000(4) Prior taxable gifts 100,000(5) Total taxable gifts (line 3 plus line 4) 171,000(6) Total tentative tax (tax computed on line 5) 45,520(7) Prior tentative tax (tax computed on line 4) 23,800(8) Current tentative tax (line 6 minus line 7) $21,720(9) Available applicable credit

(a) Maximum applicable credit for current year $(b) Applicable credit used in prior years(c) Applicable credit available (line 9a minus 9b)

(10) Foreign gift tax credit(11) Net federal gift tax for the calendar year (line 8 less lines 9c and 10)

4-41

Unified Federal Estate & Gift Tax Rates for 2013

4-42

©2013, College for Financial Planning, all rights reserved.

Module 4End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMEstate Planning