2013 best practices - ccgg · ccgg | introduction 1 2013 best practices for proxy circular...

TRANSCRIPT

2013 Best Practices for Proxy Circular Disclosure

PO Box 22, 3304-20 Queen St W, Toronto, ON M5H 3R3

CCGG | Introduction i

2013 Best Practices for Proxy Circular Disclosure

Table of Contents

Introduction ...................................................................................................................................... 1 Governance Gavel Awards ............................................................................................................... 2 Recommended Tools for Disclosure ................................................................................................. 4 Disclosure of Governance Practices ................................................................................................. 5 Disclosure of Executive Compensation .......................................................................................... 28 Disclosure by Equity Controlled Corporations ............................................................................... 49 Disclosure by Dual Class Share Companies .................................................................................... 52

CCGG | Introduction 1

2013 Best Practices for Proxy Circular Disclosure

Introduction

Since 2004, the Canadian Coalition for Good Governance (CCGG) has prepared best practices documents for

reporting issuers. These documents, including this “2013 Best Practices for Proxy Circular Disclosure”

publication, provide examples of excellent disclosure by Canadian issuers in the area of corporate governance

and executive compensation.

Mission of CCGG The Members of the Canadian Coalition for Good Governance are Canadian institutional investors that together

manage approximately $2 trillion in assets on behalf of pension fund contributors, mutual fund unit holders and

other institutional and individual investors. CCGG promotes good governance practices in Canadian public

companies and the improvement of the regulatory environment to best align the interests of boards and

management with those of their shareholders and to promote the efficiency and effectiveness of the Canadian

capital markets.

A note on terminology In this document, any use of the term “company” refers broadly to any reporting issuer and likewise any use of

the term “share” refers to any form of traded equity.

Why proxy disclosure matters The proxy circular is the primary means for a company to communicate its corporate governance practices to its

shareholders. Shareholders expect the circular to articulate, in plain language, the governance practices and

activities of the board, the qualifications of directors, the issuer’s executive compensation programs and risk

management strategy, including how the company’s compensation plan is linked to the company’s strategy,

objectives and risk management.

How to use this document Issuers should be familiar with and model their policies and behaviours based on the guidelines laid out in

CCGG’s Building High Performance Boards, Executive Compensation Principles and other CCGG publications.

This document gives life to our principles and provides inspiration for crafting and disclosing good corporate

governance practices.

Feedback We value your feedback. Please feel free to send us best practices you have come across or other suggestions

for improvement.

You can reach us at [email protected] or 416-868-3576.

CCGG | Governance Gavel Awards 2

2013 Best Practices for Proxy Circular Disclosure

Governance Gavel Awards

Established in 2005, CCGG’s Governance Gavel Awards recognize excellence in disclosure by issuers through

their annual proxy circular. Awards are given for excellence in disclosure of board governance practices and

director qualifications, and excellence in disclosure of an issuer’s approach to executive compensation. CCGG

also recognizes issuer disclosure in other categories on an ad hoc basis.

Issuers whose governance practices substantially meet all of CCGG’s Building High Performance Boards and

Executive Compensation Principles guidelines and which believe that their disclosure warrants consideration

for a Governance Gavel award are invited to contact us.

Best Disclosure of Board Governance Practices and Director Qualifications In determining the winner of CCGG’s Best Disclosure of Board Governance Practices and Director Qualifications

Gavel award, CCGG considers the alignment between an issuer’s governance practices and the recommended

practices set out in Building High Performance Boards and looks for proxy circular disclosures that allow CCGG

to assess that alignment. CCGG also looks for disclosures that include the following information:

detailed biographies for each director,

a director skills matrix,

the board’s process for identifying and recruiting directors,

the board’s orientation and continuing education programs for directors,

the board’s performance assessment processes, expectations for directors, and the attendance record

of each director at board and committee meetings, and

director compensation and share ownership requirements

2013 Award Winner: BCE Inc.

Best Disclosure of Approach to Executive Compensation In determining the winner of CCGG’s Best Disclosure of Approach to Executive Compensation Gavel award,

CCGG looks for executive compensation disclosure to incorporate substantially all of the best practices outlined

in Executive Compensation Principles and which specifically addresses key areas including:

the links between an issuer’s long-term corporate strategy and its executive compensation programs,

the links between an issuer’s risk management programs and executive compensation,

CCGG | Governance Gavel Awards 3

2013 Best Practices for Proxy Circular Disclosure

a clear and detailed description of the components of the executive compensation program and how

decisions are made,

detailed disclosure of the board’s ability to exercise discretion and whether it has done so,

disclosure of employment contracts, severance agreements and limitations on retirement benefits and

perquisites,

“look-back” tables and charts that show the effectiveness of compensation programs over time,

management biographies, qualifications and a description of their responsibilities, and

no undue reliance on the “competitive harm” exemption.

2013 Award Winner: TELUS Corporation

What do we mean by plain language and what are the benefits of its use? Plain language is a form of communication that allows your intended audience to understand the information

you are trying to convey the first time they read or hear it. In order to achieve effective disclosure, CCGG

recommends that issuers present information in a manner that:

is easy to find,

is easy to understand,

is accurate and complete, and

includes context so that the information has meaning.

Plain language does not mean that issuers should exclude complex information that shareholders require to

make informed investment and proxy voting decisions. Rather, plain language means issuers should disclose all

the information shareholders need in a manner that is understandable and user-friendly, regardless of its

complexity. As the SEC writes in A Plain English Handbook:

Plain English means analyzing and deciding what information investors need to make informed

decisions, before words, sentences, or paragraphs are considered. A plain English document

uses words economically and at a level the audience can understand. Its sentence structure is

tight. Its tone is welcoming and direct. Its design is visually appealing. A plain English document

is easy to read and looks like it’s meant to be read.

CCGG | Recommended Tools for Disclosure 4

2013 Best Practices for Proxy Circular Disclosure

Recommended Tools for Disclosure

Companies should use plain language in their disclosure documents, but other tools also must be employed to

give the document structure, ensure flow and communicate information meaningfully.

Organize for understanding

Organize the document in a manner that supports an understanding of the information it contains. Issuers

should consider whether their disclosure documents are organized in a logical flow so that information

continues to build upon itself, if applicable, and does not jump back and forth between different topics.

Use descriptive headings

Descriptive headings and subheadings allow readers to quickly find the information they are seeking and break

up the document into more manageable pieces.

Draw attention to key ideas

Some effective disclosures by Canadian issuers provide summary overviews of each major section while others

use highlight boxes to draw readers’ attention to the main ideas.

Group related information

Grouping related information helps readers better understand the overall message

being conveyed and reduces redundancies in disclosure documents. Whenever

possible, the reader should not be made to jump around to different sections to

understand a single component of compensation.

Introduce at a high level

For disclosure of executive compensation plans, CCGG recommends that the board

consider including a plain-language introduction to the CD&A section that provides a

high-level overview of the issuer’s compensation programs, the board’s approach to

executive compensation decision-making, a discussion of the decisions made during

the past year and how these decisions link to the issuer’s corporate objectives and

risk management programs.

Employ visual aids

Use charts, tables or images to explain complicated or detailed information wherever appropriate. These visual

aids can explain information more fully and easily than text alone and their use helps to divide the document

into smaller pieces for easier reading.

Avoid industry talk

Avoid jargon that confuses the message. When it is necessary or best to use industry words or technical

information, define or explain terms clearly.

Some issuers use a

highlight box to

summarize main

ideas or highlight

important

information.

CCGG | Disclosure of Governance Practices 5

2013 Best Practices for Proxy Circular Disclosure

Disclosure of Governance Practices

Proxy circulars should articulate a company’s governance practices clearly and in a format that allows the reader

to assess them in relation to the guidelines contained in Building High Performance Boards. This section shows

examples of excellent disclosure in the following areas:

Majority Voting ................................................................................................................................. 5 Voting Results ................................................................................................................................... 6 Director Independence ..................................................................................................................... 7 Director Interlocks ............................................................................................................................ 8 Independence of the Board Chair/Lead Director ............................................................................. 9 Director Nominee Profiles .............................................................................................................. 10 Board Succession and Skills Matrix ................................................................................................ 11 Director Continuing Education ....................................................................................................... 13 Board Committee Composition ...................................................................................................... 15 Director Compensation .................................................................................................................. 17 Director Attendance ....................................................................................................................... 20 Director Evaluation ......................................................................................................................... 21 Executive Succession ...................................................................................................................... 23 Strategic Planning Oversight .......................................................................................................... 24 Risk Management Oversight .......................................................................................................... 25 Shareholder Engagement ............................................................................................................... 27

Majority Voting

TELUS Corporation, 2013 Proxy Circular, page 6:

[…]Our majority voting policy applies to this election. Under this policy, a director who is elected

in an uncontested election with more votes withheld than voted in favour of his or her election

will be required to tender his or her resignation to the Board Chair. The resignation will be

effective when accepted by the Board. The Board expects that resignations will be accepted,

unless extenuating circumstances warrant a contrary decision. We will announce the Board’s

decision (including the reason for not accepting any resignation) by news release within 90 days

of the Meeting where the election was held. You can download a copy of our majority voting

policy at telus.com/governance.

Discussion

TELUS discloses a majority voting policy that is very similar to the CCGG model form and that contains all of the

most important elements:

directors with more votes withheld than for must submit resignations promptly,

the board must accept resignations except in special circumstances, and

CCGG | Disclosure of Governance Practices 6

2013 Best Practices for Proxy Circular Disclosure

the board must announce its decision to either accept or reject the resignation in a press release within

90 days, including reasons for not accepting the resignation, if applicable.

Voting Results

First Majestic Silver Corp., 2013 Report of Voting Results:

Discussion

Voting results should be disclosed immediately after a shareholder meeting. The disclosure should include a

detailed breakdown of votes on each motion and each director election. First Majestic discloses the number of

Votes For and Votes Withheld for each matter listed on the proxy and converts them to percentages.

CCGG | Disclosure of Governance Practices 7

2013 Best Practices for Proxy Circular Disclosure

Director Independence

Vermilion, 2013 Proxy Circular, page 36:

Discussion

Vermilion uses a table to identify clearly which directors are independent and which directors are not

independent. It also provides additional details for directors that are not or were previously not independent.

CCGG | Disclosure of Governance Practices 8

2013 Best Practices for Proxy Circular Disclosure

National Bank of Canada, 2013 Proxy Circular, page 20:

To facilitate candid and open discussion, provision is made for the independent members of the

Board and its committees to meet without the Bank’s management being present, at each

Board meeting.

Discussion

National Bank uses a callout box to highlight disclosure of their adoption of a CCGG-recommended best practice:

holding a portion of each board and committee meeting in camera, i.e. with independent directors only.

Director Interlocks

Gildan Activewear Inc., 2013 Proxy Circular, page 49:

No Interlocking Relationships

To maintain director independence and to avoid potential conflicts of interest, the Board has

adopted a policy whereby Board members are prohibited from serving together as directors on

any outside boards of publicly-traded companies, unless authorized by the Board, in its

discretion. None of the director nominees has served together as directors on any outside

boards during the Corporation’s most recently completed fiscal year. The directorships of all

director nominees, which include their directorships on other public companies, are described

under Section 2.1.2 entitled “Nominees” in this Circular.

Discussion

Boards should adopt a policy limiting interlocks. Gildan Activewear discloses such a policy in its circular. It also

discloses the current number of interlocks (zero in this case).

CCGG | Disclosure of Governance Practices 9

2013 Best Practices for Proxy Circular Disclosure

BCE Inc., 2013 Proxy Circular, page 29:

Board Interlocks

The Board’s approach to board interlocks is to the effect that no more than two Board members

may sit on the same public company board.

Common memberships on boards of public companies among our current directors are set out

below. The Board has determined that these board interlocks do not impair the ability of these

directors to exercise independent judgment as members of our Board.

Discussion

BCE discloses both its interlock policy and the names of directors that currently sit together on other boards

(besides the BCE board).

Independence of the Board Chair/Lead Director

Vermilion, 2013 Proxy Circular, pages 54:

Board Chairman

The terms of reference for the Board Chairman address working with management and

managing the board, including meeting processes and the roles and responsibilities of the

directors.

We have had an independent, non-executive Board Chairman since 2003. Keeping our President

and CEO and Board Chairman positions separate allows the board to more effectively oversee

management and enhance accountability. Having an independent Board Chairman fosters

strong leadership, robust discussion and effective decisions, while avoiding potential conflicts of

interest.

Discussion

The position of board Chair should be separate from the CEO. Additionally, the Chair should be chosen by and

from among an issuer’s independent directors. The Chair’s role and responsibilities should be clearly defined.

Vermilion discloses its adoption of all of these recommendations.

CCGG | Disclosure of Governance Practices 10

2013 Best Practices for Proxy Circular Disclosure

Director Nominee Profiles

BCE Inc., 2013 Proxy Circular, page 19:

Discussion

Director nominee profiles permit shareholders to learn detailed information about their representatives on the

board and to compare directors across a range of fields. BCE provides an overview of the director’s experience

and discloses relevant information in an easy to read table.

CCGG | Disclosure of Governance Practices 11

2013 Best Practices for Proxy Circular Disclosure

Board Succession and Skills Matrix

BCE Inc., 2013 Proxy Circular, page 35:

Composition of the Board of Directors and Nomination of Directors

In terms of the composition of BCE’s Board, the objective is to have a sufficient range of skills,

expertise and experience to ensure that the Board can carry out its responsibilities effectively.

Directors are chosen for their ability to contribute to the broad range of issues with which the

Board routinely deals.

The Board reviews each director’s contribution and determines whether the Board’s size allows

it to function efficiently and effectively. The Board believes that a board of directors composed

of 14 members promotes effectiveness and efficiency.

The Governance Committee receives suggestions for Board candidates from individual Board

members, the President and CEO, shareholders and professional search organizations. On a

regular basis, the Governance Committee reviews the current profile of the Board, including

average age and tenure of individual directors and the representation of various areas of

expertise, experience and diversity.

The Board strives to achieve a balance between the need to have a depth of institutional

experience from its members on the one hand and the need for renewal and new perspectives

on the other hand. The Board tenure policy does not impose an arbitrary retirement age limit,

but with respect to term limit, it sets as a guideline that directors serve up to a maximum term

of 12 years, assuming they are re-elected annually and meet applicable legal requirements. The

Board, however, upon recommendation of the Governance Committee, is able to, in certain

circumstances, extend a director’s initial 12-year term limit.

Competency Requirements

We maintain a “competency” matrix where directors indicate their expertise level in areas we

think are required at the Board for a company like ours. Each director has to indicate the degree

to which he/she believes they possess such competency.

The table below lists the top two competencies of our current directors together with their age

range, tenure, linguistic background and residency.

CCGG | Disclosure of Governance Practices 12

2013 Best Practices for Proxy Circular Disclosure

Discussion

Boards should have a plan in place for orderly succession of directors and should maintain an evergreen list of

candidates. Boards also should identify key skills required of directors and use a skills matrix to ensure these

skills are accounted for among current and prospective directors. The skills matrix for current directors should

be disclosed in the proxy circular.

CCGG | Disclosure of Governance Practices 13

2013 Best Practices for Proxy Circular Disclosure

TransCanada Corporation, 2013 Proxy Circular, page 41:

The table below lists the likely retirement dates of the current non-executive directors based on

current age, the Board committees they serve on, their education and their areas of expertise.

The Governance committee considers these factors and others when discussing Board renewal.

Dr. Draper will retire on April 26, 2013 prior to the annual and special meeting.

Discussion

TransCanada provides a table that shows “likely retirement date” for each director, along with his or her primary

areas of expertise. This information is very useful as it highlights the key skill areas the board will need to replace

and when.

Director Continuing Education

Pengrowth Energy Corporation, 2013 Proxy Circular, page 49-50:

Continuing Education

We undertake ongoing education efforts that include meetings among management and the

Board and, where appropriate, outside experts, to discuss regulatory changes, developments in

the industry and market conditions. Continuing education for all members of the Board is also

conducted on an informal basis. As a part of the continuing education of the Directors,

presentations are made at Board meetings by management on new developments which may

affect the Corporation and its business. In connection with almost every Board meeting,

Directors are provided with articles and publications of interest. In addition, Directors receive

periodic one-on-one presentations from management and are provided with the opportunity to

meet with members of senior management outside of formal Board meetings to discuss and

CCGG | Disclosure of Governance Practices 14

2013 Best Practices for Proxy Circular Disclosure

better understand the business. Board members are encouraged to communicate with

management and our auditors to keep themselves current with industry trends and

developments, and to attend related industry seminars. Board members have full access to the

Corporation's records. Pengrowth also facilitates the education of Directors through financing

annual membership in the Institute of Corporate Directors. Directors are provided with

background materials and the information necessary to fulfill their roles as Directors, including

the Corporation’s key corporate policies. Written materials and briefings are extensively used to

ensure that Directors’ knowledge and understanding of the Corporation’s affairs remains

current. In 2012, the Board adopted a policy to conduct at least one field site visit each year and

in August 2012, nine of our Directors toured our Olds gas plant and related properties.

Most of our Directors sit on one or more other boards which enables them to implement the

best practices they observe elsewhere at Pengrowth.

The following table outlines examples of continuing education events held for, or attended by,

all of our Directors in 2012:

CCGG | Disclosure of Governance Practices 15

2013 Best Practices for Proxy Circular Disclosure

Discussion

Directors should undergo education to update their skills and knowledge of the company, its businesses and key

executives and to address ongoing and emerging issues in the functional areas of the board. Issuers should

establish a continuing education program for directors and disclose its components annually. Pengrowth Energy

discloses its continuing education program and specific events attended by directors in the past year.

Board Committee Composition

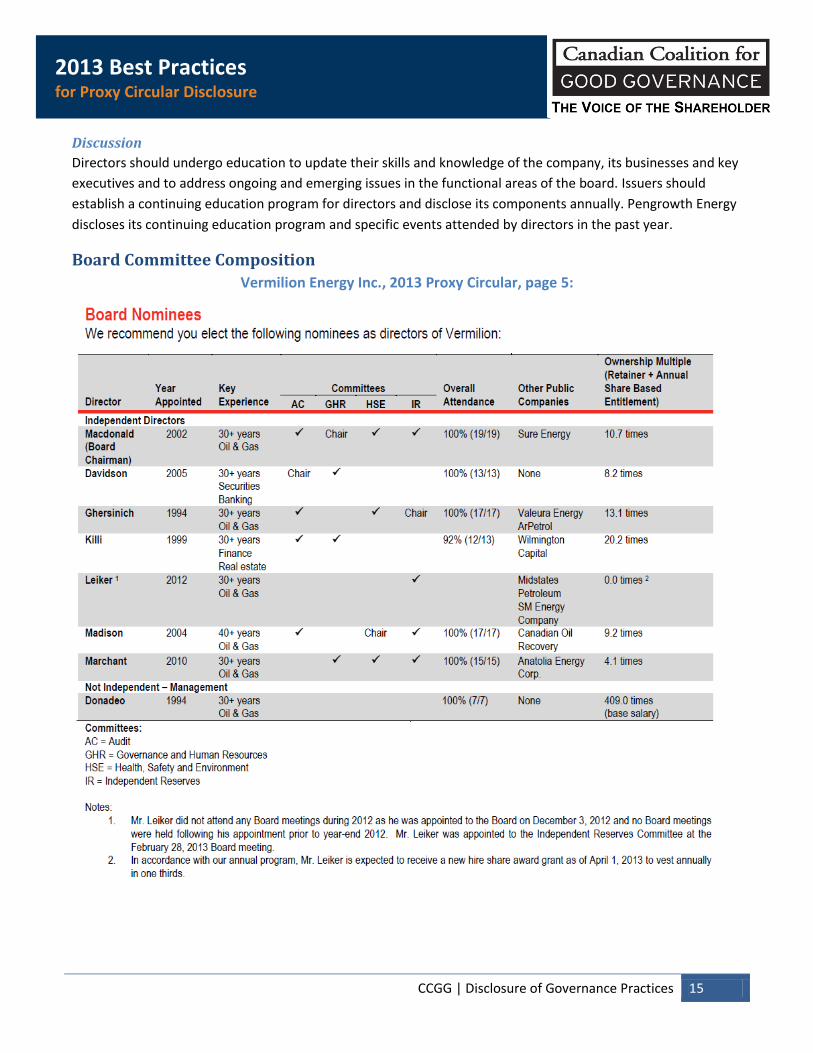

Vermilion Energy Inc., 2013 Proxy Circular, page 5:

CCGG | Disclosure of Governance Practices 16

2013 Best Practices for Proxy Circular Disclosure

Discussion

Vermilion discloses committee memberships and member independence through a clear and comprehensive

table. A snapshot of the director’s area of expertise, attendance record and stock ownership is also provided.

Canadian National Railway Company, 2013 Proxy Circular, page 23:

Human Resources and Compensation Committee

[…] The Board has adopted a policy, which is included in our Corporate Governance Manual,

that no more than one in three members of the Human Resources and Compensation

Committee shall be a sitting CEO of another company, at least one member shall be experienced

in executive compensation, and the President and CEO of the Company shall be excluded from

the Committee member selection process.

Discussion

CN Rail provides shareholders with some insights on how the board selects the composition of its

HR/Compensation committee and makes it clear that the CEO is not involved in the selection process. In the

case of the HR/Compensation committee in particular, CCGG recommends that issuers adopt a policy requiring

that no more than one-third of its members be current CEOs of other issuers.

CCGG | Disclosure of Governance Practices 17

2013 Best Practices for Proxy Circular Disclosure

Director Compensation Sun Life’s disclosure of director compensation is detailed, well-organized and written in plain language. The

disclosure covers several pages and is not reproduced in its entirety here. It begins with the following

explanation of Sun Life’s philosophy, approach and process:

Sun Life Financial Inc., 2013 Proxy Circular, pages 32-36:

CCGG | Disclosure of Governance Practices 18

2013 Best Practices for Proxy Circular Disclosure

It lists the various fees and retainers paid to directors:

It shows what each non-executive director was paid in the fiscal year, broken down by type of fee:

CCGG | Disclosure of Governance Practices 19

2013 Best Practices for Proxy Circular Disclosure

Finally, it also discloses director share ownership requirements and current director share ownership:

CCGG | Disclosure of Governance Practices 20

2013 Best Practices for Proxy Circular Disclosure

Director Attendance

Potash Corporation of Saskatchewan Inc., 2013 Proxy Circular, page 18:

(1) Elected as a member of the Board and a member of the Audit Committee and Safety, Health and Environment Committee on May 17, 2012.

(2) In addition to the committees of which he is a member, Mr. Howe, as Board Chair, regularly attends other committee meetings as well. Mr. Howe attended all of the committee meetings held in 2012. At the invitation of applicable committees, Mr. Doyle attended all or a portion of many of the committee meetings held in 2012, including a majority of the Compensation and CG&N committee meetings. In an effort to provide directors with a more complete understanding of the issues facing the Corporation and in line with the Corporation’s core values, directors are encouraged to attend committee meetings of which they are not a member.

(3) Served as a member of the Board, a member of the Compensation Committee and the Chair of the Safety, Health and Environment Committee until his retirement from the Board on May 17, 2012.

CCGG | Disclosure of Governance Practices 21

2013 Best Practices for Proxy Circular Disclosure

(4) Served as a member of the Board and a member of the Safety, Health and Environment Committee until his retirement from the Board on May 17, 2012.

Potash Corporation of Saskatchewan Inc., 2013 Proxy Circular, page A-2:

Director Attendance

Attendance records are fully disclosed in the “Board of Directors— Board Meetings and

Attendance of Directors” section of this Management Proxy Circular. Pursuant to the

“PotashCorp Governance Principles”, directors are expected to attend all meetings of the Board

and Board committees upon which they serve, to come to such meetings fully prepared and to

remain in attendance for the duration of the meetings. Where a director’s absence from a

meeting is unavoidable, the director should, as soon as practicable after the meeting, contact

the Board Chair, the Chief Executive Officer or the Corporate Secretary for a briefing on the

substantive elements of the meeting.

Discussion

PotashCorp discloses attendance at all board and committee meetings in a table that is easy to read. It also

discloses ex-officio and non-voting attendance at committee meetings in a footnote.

Most importantly, PotashCorp expects its directors to attend all meetings.

Director Evaluation

Potash Corporation of Saskatchewan Inc., 2013 Proxy Circular, page 16:

Board, Committee & Director Assessment

Pursuant to the “PotashCorp Governance Principles”, the Board has adopted a 6-part

effectiveness evaluation program for the Board, each Committee and each individual director

which is outlined in Appendix A under “Board Assessments” and summarized in the following

table.

CCGG | Disclosure of Governance Practices 22

2013 Best Practices for Proxy Circular Disclosure

Discussion

PotashCorp presents a tabular summary of its director and board assessment processes.

The table clearly describes by whom annual evaluations are performed, the frequency of assessments and

provides a summary of the “actions” and “outcomes” of a typical evaluation.

CCGG | Disclosure of Governance Practices 23

2013 Best Practices for Proxy Circular Disclosure

Executive Succession

Potash Corporation of Saskatchewan Inc., 2013 Proxy Circular, page 38:

Succession Planning

One major responsibility of the Committee is to oversee our company’s management

succession planning. Twice each year, we review the progress, examine any gaps in

succession plans and discuss ways to improve succession planning. Once each year, we

meet with our CEO to discuss succession plans for our CEO and other senior executive

officers. In addition, the Board regularly interacts with our company’s senior management

team. A number of times each year, the Board has social events at which we are able to meet

a large number of the management employees and build relationships with the people who

represent the future of our company. As a result of this active succession planning process,

in 2012, 80% of senior staff openings were filled by qualified internal candidates who had

been developed for the promotions they received.

EMERA INCORPORATED, 2013 Proxy Circular, page 25:

Board Dinner Sessions

Board dinner sessions are scheduled the evening prior to regularly scheduled Board

meetings. Board dinners are a critical opportunity to accomplish a number of important

governance objectives, including:

• Meeting as independent directors in an atmosphere that is not a board meeting. The Board’s practice is to have one dinner each year at which only the independent Directors attend.

• Meeting in a less formal atmosphere with the Chief Executive Officer, and other senior officers.

• Holding educational sessions on important topics for the Company’s business and strategic direction.

• Meeting high-potential employees in order to advance the succession planning for the Company.

• Strengthening Directors’ collegial working relationship.

The Company’s Board of Directors annually plans a dinner with a number of high-potential

leaders drawn from throughout the Company and its various subsidiary businesses for the

purpose of holding an interactive event in which each high-potential leader is introduced to

each member of the Board of Directors. This is an opportunity for Directors to get to know

the Company’s high-potential leaders and to support and promote the Company’s executive

succession planning and leadership development process.

CCGG | Disclosure of Governance Practices 24

2013 Best Practices for Proxy Circular Disclosure

Discussion

While the CEO is primarily responsible for succession planning, a highly engaged board is involved in the

succession planning process. Both examples shown above demonstrate the board’s involvement in identifying

high potential candidates.

Strategic Planning Oversight Companies should disclose the role of their board in overseeing the determination, execution and monitoring of

the company’s strategic plan.

Cameco Corporation, 2013 Proxy Circular, pages 30-31:

Strategic planning

The board works with management to develop our strategic direction. Our strategic planning

process has four elements:

a) developing a 10-year strategic plan

b) setting annual corporate objectives

c) establishing annual budgets and two-year financial plans

d) reviewing the strategic plan periodically and revising it based on our progress and changing

market conditions.

Management is responsible for preparing information on these four elements and presenting it

to the board for discussion and approval.

The board is actively involved in the strategic planning process and holds several strategic

planning sessions with management every year, including quarterly updates and a multi-day

session in August for more in depth discussion and analysis. Management and the board discuss

the main risks facing our business, strategic issues, competitive developments and corporate

opportunities. At strategic planning sessions in 2012, the board and officers conducted a top-

down review of strategic risks.

While these special meetings focus on strategic planning, management also presents strategic

issues to the board throughout the year based on the business climate and other developments.

The CEO updates the board on execution of our corporate strategy at every regularly-scheduled

board meeting. The board also raises various issues and topics for discussion as part of the

overall process.

CCGG | Disclosure of Governance Practices 25

2013 Best Practices for Proxy Circular Disclosure

Discussion

Cameco’s disclosure of the board’s strategic oversight role goes beyond common boilerplate language found in

appendixes to the circular. The circular provides an overview of the strategic planning process and the board’s

role in strategic planning.

Risk Management Oversight The financial crisis of recent years has heightened shareholders’ focus on risk management and oversight, yet

risk oversight remains an area where disclosure often is lacking among Canadian issuers. Boards should disclose

the processes used that enable them to identify and monitor risk management efforts. Ideally, disclosure should

include:

a perspective from the board of the primary risks facing the company,

a brief explanation of the board’s involvement in defining the company’s risk appetite and overseeing

risk management,

how the board delegates and carries out its risk management oversight responsibilities, and

how the board independently validates and scrutinizes the perspective presented by management on

key risk issues.

Cameco Corporation, 2013 Proxy Circular, page 31:

Risk oversight

Over the last few years, management, the board and board committees have been devoting

more time to the way we identify, manage, report and mitigate risk.

We implemented a new risk policy and process in 2011 that involves a broad, systematic

approach to identifying, assessing, reporting and managing the significant risks we face in our

business and operations. We consider any risk that has the potential to significantly affect our

ability to achieve our corporate objectives or strategic plan as an enterprise risk, and we assess

all risks against our four measures of success. See Measuring performance on page 63 for our

four measures of success.

Our risk management program follows the guidance of ISO 31000:2009, and the board works

with management to ensure our system is robust. The policy establishes clear accountabilities

and we use a common risk matrix throughout the company.

We manage risk in six broad categories:

a) financial

b) human capital

c) infrastructure and security

CCGG | Disclosure of Governance Practices 26

2013 Best Practices for Proxy Circular Disclosure

d) operational

e) social, governance and compliance

f) strategic

We manage risks in three tiers based on their severity or level of risk, and incorporate the risks

into the strategic planning and budgeting process as part of our management discipline. Risks in

the top tier are assigned to the board or board committees for ongoing oversight.

Employees “own” the risks and are responsible for developing and implementing controls to

mitigate risk and for ongoing risk assessments. The chair of the board and each committee chair

met in 2012 to discuss the risk oversight process.

Our management committee receives quarterly reports to review our progress in managing

these risks and identify any emerging risks. Management reports quarterly to the nominating,

corporate governance and risk committee on the risk management process and provides a risk

management report to the board annually.

The table below shows how the board and committees monitor risk across the organization. You

can read about the board committees on page 34 and compensation risk on page 41

Discussion

Cameco’s disclosure is excellent compared to most Canadian issuers. One suggestion for improvement would be

a discussion of how the board independently verifies management’s assessment of risk.

CCGG | Disclosure of Governance Practices 27

2013 Best Practices for Proxy Circular Disclosure

Royal Bank of Canada, 2013 Proxy Circular, page 18-19:

Discussion

Some boards have established a separate committee that oversees risk. The RBC risk committee approves the

Bank’s risk appetite every year. The risk committee writes a report to shareholders each year that is included in

the circular.

Shareholder Engagement There is a growing emphasis on shareholder engagement and best practices continue to evolve. CCGG

recognizes that while boards may be able to meet with their largest institutional shareholders and groups like

the CCGG, in-person meetings are not a practical forum for boards to engage with all shareholders. At the very

least a company’s investor relations page should be used to engage with non-institutional shareholders. The

page should be regularly updated and should include all the major public documents (including but not limited

to the latest annual reports, proxy circulars, annual information forms and earnings conference call transcripts,

slideshows and webcasts). PotashCorp’s investor website is a good example.

CCGG | Disclosure of Executive Compensation 28

2013 Best Practices for Proxy Circular Disclosure

Disclosure of Executive Compensation

Compensation is one of the most powerful tools that boards have at their disposal for shaping the behaviour of

company management. While CCGG recognizes that the amount and design of executive compensation

packages is the responsibility of the board, compensation plans should reward performance and be aligned with

CCGG’s Executive Compensation Principles.

Disclosure of a company’s compensation plan should describe clearly how it is linked to the company’s strategy,

objectives and risk management. Compensation disclosure also should communicate the role of the board in

designing and determining executive compensation, key factors considered by the board, the ability of the

board to exercise discretion when making compensation decisions and whether discretion actually has been

used, and the rationale for the board’s decisions. This section shows examples of excellent disclosure of the

following practices:

Linkages between Executive Compensation and Corporate Strategy ........................................... 28 Linkages between Executive Compensation and Risk Management ............................................. 30 Variable Compensation .................................................................................................................. 34 Effectiveness of the Compensation Program over Time ................................................................ 37 Management Biographies and Performance Assessment ............................................................. 40 Termination and Change of Control Benefits ................................................................................. 41 Executive Share Ownership Requirements .................................................................................... 43 Use and Limits of Retirement Benefits and Perquisites ................................................................. 45 Use, Policies and Limits for Discretion ........................................................................................... 45 Compensation Consultants and Benchmarking ............................................................................. 46

Linkages between Executive Compensation and Corporate Strategy It is not sufficient merely to state how an issuer compensates its executive officers. CCGG expects issuers to

explain the link between its long-term corporate objectives and the compensation mix. We expect the

performance measures used in determining executive compensation to be linked to corporate strategy.

A common shortfall of compensation disclosure is the failure to explain why the key performance metrics

identified were chosen.

Sun Life Financial, 2013 Proxy Circular, page 38:

Letter to shareholders

In 2012, we began to execute on our strategic plan to accelerate growth, improve return on

equity and reduce volatility by concentrating on four key pillars:

a) Continuing to build on our leadership position in Canada in insurance, wealth

management and employee benefits

CCGG | Disclosure of Executive Compensation 29

2013 Best Practices for Proxy Circular Disclosure

b) Becoming a leader in group insurance and voluntary benefits in the U.S.

c) Supporting continued growth in MFS Investment Management (MFS) and broadening

our other asset management businesses around the world

d) Strengthening our competitive position in Asia.

We believe our current compensation programs are structured to support the achievement

of these strategic objectives. The performance targets used in our annual incentive plan

(AIP) reflect financial and non-financial objectives that are aligned to the annual business

plan approved by the board based on this strategy. Our long-term success on these strategic

pillars will be reflected in both our absolute and relative share price performance, which

are the key measures used in our long-term incentives and represent a significant portion of

pay for our most senior leaders. In addition to incentives, providing competitive salaries

and other pension and benefit programs ensures we attract and retain the talent needed to

execute on our strategy.

Discussion

Sun Life’s circular describes the organization’s strategic initiatives. It then describes how the chosen long term

performance measures link to these strategic initiatives.

Sun Life also states that short term performance measures link to the company’s strategic initiatives. Later on in

the circular, Sun Life provides more details regarding these short term measures:

Sun Life Financial, 2013 Proxy Circular, page 54

CCGG | Disclosure of Executive Compensation 30

2013 Best Practices for Proxy Circular Disclosure

Tim Hortons Inc., 2013 Proxy Circular, page 57

Short-Term Incentives (or Annual Cash Bonus)—the Executive Annual Performance Plan

Our short-term (annual) incentive compensation program for executive officers is known as the

Executive Annual Performance Plan (“EAPP”). Awards under the EAPP are “at risk” because the

corporation must achieve annual financial performance objectives established by the HRCC in

order for the executive officers to receive any payments under the EAPP. The HRCC believes that

the annual cash incentive award should constitute a substantial portion of executive

compensation to support our “pay-for-performance” philosophy and because our business

tends to work on shorter performance cycles, thus making annual incentive awards effective at

matching compensation to our performance. Additionally, given the relatively low level of our

executive base salaries, we believe that strong short-term cash incentive compensation assists

us to retain, motivate, and attract talented executives.

The two performance objectives established under the EAPP in 2012 were operating income, or

EBIT, as to 75% of the award, and Net Income, as to 25% of the award. The HRCC believed that

EBIT best reflects the financial health and performance of our business and also is a key

performance measure used by other quick service restaurant companies, which allows for

general comparability of performance. The HRCC also believed that Net Income was an

appropriate measure as it reflected overall earnings performance and requires management to

be responsible for, and manage every line item on, our Consolidated Statement of Operations.

[…]

Discussion

Tim Hortons explains how the design of the compensation plan, in this case the compensation mix, aligns with

the company’s particular business environment. As a retail business, Tim Hortons discloses that it operates on a

short performance cycle and, accordingly, the board has placed greater emphasis on compensation awards that

it believes best match this time horizon.

Linkages between Executive Compensation and Risk Management Closely related to the link between compensation and strategy is the link between compensation and risk.

Companies should disclose details of its executive compensation scheme through a risk oversight lens. The

disclosure should explain how the design of the compensation plan and use of board discretion serves to

discourage or dis-incent risk-taking beyond the company’s acceptable risk appetite, including the use of:

caps on payouts,

board discretion on payouts,

performance thresholds and vesting provisions,

deferring payouts beyond the term of greatest risk exposure, and

CCGG | Disclosure of Executive Compensation 31

2013 Best Practices for Proxy Circular Disclosure

a “clawback” policy that permits the company to recoup compensation already awarded in certain

circumstances.

TransAlta Corporation, 2013 Proxy Circular, pages 66-67:

ANNUAL COMPENSATION RISK REVIEW PROCESS

The Board believes that our executive compensation program should not raise the Company’s

risk profile. Accordingly, the HRC undertakes a comprehensive annual compensation risk review

as part of our Compensation Strategy. The focus of this review is to ensure that safeguards are

in place to identify and mitigate compensation-related risks. We also ensure our mitigation

measures are effective by conducting an annual audit through our Enterprise Risk Management

process.

We believe that this risk review process is an effective vehicle for examining compensation risk

and mitigation strategies. The review considers the major risks of our business, which include

equipment/maintenance, long-term contracting, market competition and pricing, energy

marketing, growth opportunities, construction and regulatory impact. In addition, our review

takes into consideration our compensation philosophy, pay mix balance, incentives and

performance measures, stock-based compensation and ownership requirements. The mix and

balance of these various measures including the limits to our variable compensation plans are

also reviewed. Our plans are also based on Company-wide financial metrics and payouts are

based on a combination of absolute and relative measures. In addition, the HRC receives

management’s analysis and stress testing of the factors included in the annual budget which is

the basis for establishing the Company’s various targets. This results in targets which are set

within our risk appetite and which provide sufficient incentive for our executives to pursue our

corporate objectives.

To further enhance our risk management strategy, we have adopted policies that limit

independent decision-making for transactions over certain financial thresholds thereby

incorporating a check and balance system to financial decision-making. Together, these

measures help minimize compensation risk-taking. These processes are evaluated yearly and are

designed to evolve over time in order to reflect developments and best practices in risk

governance. A comprehensive compensation-related risk assessment was undertaken by Towers

Watson in January 2012, and subsequently updated in October 2012 to include the changes to

the 2013 executive incentive plans. Following a review of this assessment by Meridian, the HRC

concluded that our pay programs and policies were not reasonably likely to have a material

adverse effect on TransAlta, our business and our value.

CCGG | Disclosure of Executive Compensation 32

2013 Best Practices for Proxy Circular Disclosure

Safeguards to mitigate compensation risks

Our compensation programs are designed to mitigate compensation risks. We believe the

following measures impose appropriate limits to avoid excessive or inappropriate risk-taking or

payments:

Compensation payments are capped to provide upper payout boundaries;

Milestones achieved must be maintained over a period of time prior to being paid or

awarded. This is achieved through vesting provisions built into our medium and long-term

incentive plans;

Annual review of our medium and long-term incentive plans targets and milestones to

ensure continued relevance and applicability;

Evaluation of variable compensation plan metrics to confirm balance of objectives between

plans thereby mitigating by design excessive risk-taking;

Clawback policy, which applies to all variable compensation plans. […]

Anti-hedging policy which, in addition to our insider trading policy, ensures that Executives

and directors cannot participate in speculative activity related to our shares. […]

Policies which limit authority on expenditures. The Board has put in place policies that limit

the expenditures which can be made at different levels of the organization.

Discussion

TransAlta provides detailed disclosure of how its Human Resources Committee actively considers risk

management when making compensation decisions. The disclosure also provides a summary of the actual

safeguards built into the compensation scheme.

Canadian National Railway Company, 2013 Proxy Circular, pages 39:

RISK MITIGATION IN OUR COMPENSATION PROGRAM

The Company has a formalized compensation philosophy to guide compensation program

design and decisions. Many of the characteristics inherent in the Company’s executive

compensation program encourage the right behaviours, thus mitigating risks and aligning long-

term results with shareholder interests. The following are examples of such characteristics:

• Appropriate balance between fixed and variable pay, as well as short- and long-term

incentives;

• Multiple performance metrics are to be met or exceeded in the AIBP;

CCGG | Disclosure of Executive Compensation 33

2013 Best Practices for Proxy Circular Disclosure

• Incentive payout opportunities are capped and do not have a guaranteed minimum payout;

• Executive compensation clawback policy is in place;

• Stock ownership guidelines apply to executives and senior management employees

(approximately 200 individuals).

A complete list and description of these risk-mitigating features is available on pages 49 and 50.

In 2012, CN requested that Towers Watson review the actions taken by CN since the 2011 Risk

Assessment and comment on any potential risks. Towers Watson considered the actions taken

by CN and consistent with their 2011 assessment, confirmed that “overall, there does not

appear to be significant risks arising from CN’s compensation programs that are reasonably

likely to have a material adverse effect on the Company”. The Committee strongly supports the

conclusions from Towers Watson’s risk assessment report and in its own assessment

determined that proper risk mitigation features are in place within the Company’s

compensation program.

Discussion

CN Rail presents a summary on risk mitigation towards the beginning of its compensation discussion. CN refers

the reader to a more detailed disclosure within the document.

Loblaw Companies Limited, 2013 Proxy Circular, pages 25-26:

Clawback Policies

In 2011, the Governance Committee introduced a clawback policy on STIP and LTIP payments for

senior executives including the NEOs when (i) an executive engages in conduct that results in

the need for the correction or restatement of financial results, (ii) the executive receives an

award calculated on the achievement of those financial results, and (iii) the award received

would have been lower had the financial results been properly reported. The clawback policy

also provides that a clawback may be triggered if an executive commits a material breach of the

Corporation’s Code of Conduct. The policy requires that when the clawback is triggered, the

executive must repay all of the incentive payments received over the two-year period preceding

the triggering event.

In 2011, the Corporation also introduced a data quality clawback mechanism that may reduce

STIP awards for data inaccuracies occurring as part of the Corporation’s IT systems

implementation. In 2012, the Corporation did not achieve 100% of its data accuracy and

completeness targets and, as a result, executives’ 2012 STIP payouts were reduced by 2.3%.

CCGG | Disclosure of Executive Compensation 34

2013 Best Practices for Proxy Circular Disclosure

Discussion

In its risk mitigation practices, Loblaw lists and explains its Clawback polices. The section demonstrates a good

example of clawback policies that go beyond financial restatement.

Variable Compensation Many compensation disclosures will state what percentage of named executive officer (NEO) compensation is

comprised of variable or “at-risk” elements, but there are many factors that can affect the degree of variability

in compensation outcomes. In assessing the degree to which executive compensation is truly at-risk, CCGG looks

for a company’s disclosure to answer the following questions:

What proportion of target total compensation is variable?

What is the range of potential payments under each variable compensation payment?

Are there specific vesting provisions tied to variable compensation? If so, do they include both time- and

performance-vesting provisions?

Further, when discussing performance targets and performance vesting conditions, compensation disclosure

should provide context so that shareholders have an appreciation for the degree of challenge or “stretch”

incorporated into “target performance” metrics. This may be done by providing historical performance results

for the metrics being used.

Bank of Nova Scotia, 2013 Proxy Circular, pages 27-28:

CCGG | Disclosure of Executive Compensation 35

2013 Best Practices for Proxy Circular Disclosure

Discussion

BNS’ disclosure clearly illustrates each general component of compensation and each component’s:

purpose,

performance period, if any,

relative risk of payout, and

proportion of target total direct compensation.

The disclosure also notes that more senior employees have greater ability to affect results over the long-term

and accordingly a greater proportion of their compensation is variable.

CCGG | Disclosure of Executive Compensation 36

2013 Best Practices for Proxy Circular Disclosure

TransAlta Corporation, 2013 Proxy Circular, pages 59:

Discussion

TransAlta’s circular provides a table that shows the following important details regarding each component of

executive compensation:

a) Component’s Purpose

b) Measurement (vesting criteria)

c) Target and Range

d) Form of payment

e) Performance Period

CCGG | Disclosure of Executive Compensation 37

2013 Best Practices for Proxy Circular Disclosure

Potash Corporation of Saskatchewan, 2013 Proxy Circular, page 45:

The following table sets forth the percentage of stock options granted under the 2008 POP, the

2009 POP and the 2010 POP that vested for the three-year performance periods ended

December 31, 2010, December 31, 2011 and December 31, 2012, respectively.

[…]The Compensation Committee believes that 100% vesting under our POP requires superior

performance during the applicable performance period and believes that our POP vesting

schedule appropriately links vesting of stock options to our performance relative to our peers.

Discussion

PotashCorp’s circular provides shareholders with a performance vesting schedule for the company’s annual

option grant. Furthermore, the company provides a table illustrating its performance during the vesting period

of the three most recently vested option grants, providing shareholders with some useful context.

This disclosure also merits inclusion as a best practice because it is an example of an option program that

includes performance-vesting conditions rather than merely time-vesting conditions.

Effectiveness of the Compensation Program over Time In order to truly understand the effectiveness of an issuer’s compensation program, shareholders need to know

not only the grant date value of compensation awards, which reflects how the board intended to compensate

management, but also how effective the compensation program has actually been in aligning management’s

interests with shareholders. Compensation disclosure should include:

an explicit discussion of whether and how a board considers outstanding and realized equity awards

when considering further such awards,

a “look back” table or chart showing the realized value of past compensation awards,

a chart comparing compensation awards against the actual results of key performance metrics used in

the compensation plan, and

CCGG | Disclosure of Executive Compensation 38

2013 Best Practices for Proxy Circular Disclosure

affirmation of any forward-looking stress tests the board may have conducted when making

compensation decisions and the results of those tests.

The Toronto-Dominion Bank, 2013 Proxy Circular, pages 39:

CEO Performance Compensation During Tenure

The following table compares the grant date value of compensation awarded to Mr. Clark in

respect of his performance as CEO with the actual value that he has received from his

compensation awards during his tenure. The actual compensation that he has received includes

salary and cash incentive payments, as well as the value at maturity of share units granted (or

current value for units that are outstanding), the value of stock options exercised during the

period, and the in-the-money value of stock options that remain outstanding. This analysis

allows the committee to consider compensation outcomes for the CEO when determining new

awards.

Discussion

Some issuers have included in their circulars the realizable value of Options and PSUs based on year end stock

prices. Disclosing realizable value of options and PSUs is a good practice but this value does not reflect the actual

compensation that is realized by the executive.

CCGG | Disclosure of Executive Compensation 39

2013 Best Practices for Proxy Circular Disclosure

TD’s circular includes an innovative look-back table which shows the grant date values of the CEO’s

compensation for each year of his tenure and the sum of the realized value and the value of any awards still

outstanding as of the most recent year-end. The table also compares the actual compensation the CEO received

to the value of a $100 shareholder investment in each of those years.

Potash Corporation of Saskatchewan, 2013 Proxy Circular, page 68:

The above chart compares the total annual compensation, which is comprised of fixed

compensation, equity compensation and awards under the Short-Term Incentive Plan earned by

the Corporation’s Named Executive Officers from 2005 through 2012 to PotashCorp’s annual

CFROI-WACC during the same period.

CFROI-WACC is the performance metric used to determine vesting of performance options

granted under the POP and is correlated with total shareholder return. While total Named

Executive Officer compensation was not directly correlated to CFROI-WACC between 2005 and

2012, the general trend in total Named Executive Officer compensation was consistent with the

general trend in CFROI-WACC. Because awards under PotashCorp’s incentive plans are capped

at certain maximum performance levels, there was a substantial increase in CFROI-WACC

between 2006 and 2008 while levels of total Named Executive Officer compensation during the

same period were relatively stable. In 2009, because the Corporation failed to achieve the

minimum corporate financial performance required under STIP, no STIP awards were earned by

PotashCorp’s Named Executive Officers. Furthermore, the equity compensation levels in 2006,

CCGG | Disclosure of Executive Compensation 40

2013 Best Practices for Proxy Circular Disclosure

2009 and 2012 reflect the payout of a multi-year award under the Medium- Term Incentive Plan,

reflecting performance in each respective prior three-year period.

For purposes of the above chart, fixed compensation includes base salary and other

compensation, which includes perquisites and personal benefits. Equity compensation includes

the grant-date fair value of awards under the Medium-Term Incentive Plan and annual

Performance Option Plans.

Discussion

PotashCorp discloses a chart that shows the grant date value of each of its compensation awards relative to

performance under one of the company’s primary performance metrics (the spread between CFROI and WACC).

This disclosure provides shareholders with some context to understand how closely the grant date value of

executive compensation tracks performance.

Management Biographies and Performance Assessment To understand the appropriateness of a company’s executive compensation plan and its compensation

decisions, shareholders need to have some understanding of the roles and responsibilities of all NEOs, their

qualifications, and how their performance was assessed.

Royal Bank of Canada, 2013 Proxy Circular, pages 40-44:

CCGG | Disclosure of Executive Compensation 41

2013 Best Practices for Proxy Circular Disclosure

Discussion

RBC’s circular provides an excellent overview of the preceding year’s compensation for each NEO.

Termination and Change of Control Benefits In seeking to understand the employment agreements between an issuer and its NEOs, including their minimum

share ownership requirements, CCGG looks for compensation disclosure to answer the following questions:

Does the company have employment agreements with its NEOs? What are the material terms of the

agreements?

What payment, if any, is awarded…

o …if a NEO resigns?

o …if a NEO is terminated without cause?

o …if a NEO is terminated without cause after a change of control occurs?

o …if a change of control occurs but a NEO is not terminated?

How is a change of control defined?

Has the board resolved to discontinue/introduce contract provisions in future that differ from those

currently in place (e.g. will a future CEO’s severance payments be subject to double trigger provisions)?

What payments would be made to NEOs under each termination scenario if their employment had been

terminated at year-end?

CCGG | Disclosure of Executive Compensation 42

2013 Best Practices for Proxy Circular Disclosure

Canadian National Railway Company, 2013 Proxy Circular, pages 48-49:

CHANGE OF CONTROL PROVISIONS

The Management Long-Term Incentive Plan and the RSU Plan were amended effective March 4,

2008 to include “double trigger provisions”. Pursuant to such provisions, the vesting of non-

performance options or RSUs awarded after that date and held by a participant would not

accelerate upon a Change of Control, unless the participant is terminated without cause or

resigns for good reason. A Change of Control means any of the following events:

a) in the event the ownership restrictions in the CN Commercialization Act are repealed, a

formal bid for a majority of the Company’s outstanding common shares;

b) approval by the Company’s shareholders of an amalgamation, merger or consolidation of the

Company with or into another corporation, unless the definitive agreement of such transaction

provides that at least 51% of the directors of the surviving or resulting corporation immediately

after the transaction are the individuals who, at the time of such transaction, constitute the

Board and that, in fact, these individuals continue to constitute at least 51% of the board of

directors of the surviving or resulting corporation during a period of two consecutive years; or

c) approval by the Company’s shareholders of a plan of liquidation or dissolution of the

Company.

The amended provisions state that acceleration of vesting would not occur if a proper substitute

to the original options or units is granted to the participant. If such substitute is granted and a

participant is terminated without cause or submits a resignation for good reason within 24

calendar months after a Change of Control, all outstanding substitute options or units which are

not then exercisable shall vest and become exercisable or payable in full upon such termination

or resignation. Substitute options that are vested and exercisable shall remain exercisable for a

period of 24 calendar months from the date of such termination or resignation and units shall

be paid within 30 days. These amended provisions only affect grants made after March 4, 2008,

and discretion is left to the Board of Directors to take into account special circumstances.

Canadian National Railway Company, 2013 Proxy Circular, pages 69-70:

TERMINATION AND CHANGE OF CONTROL BENEFITS

The Company does not have contractual arrangements or other agreements with NEOs in

connection with termination, resignation, retirement, change of control or a change in

responsibilities, other than the conditions provided in the compensation plans, and summarized

as follows:

CCGG | Disclosure of Executive Compensation 43

2013 Best Practices for Proxy Circular Disclosure

CHANGE OF CONTROL

The following table shows the incremental benefits that NEOs would have been entitled to had

there been a change of control on December 31, 2012.

Discussion

CN Rail’s circular includes all the information discussed above.

Executive Share Ownership Requirements Companies should consider adopting share ownership requirements for its NEOs to enhance alignment of

interests with the company’s shareholders. Additionally, disclosure should answer the following questions:

What are the minimum share ownership requirements that each NEO must meet?

Are NEOs required to maintain minimum share ownership levels for any period of time after leaving the

company?

Has the company adopted an anti-monetization and/or an anti-hedging policy?

What are each NEO’s current shareholdings relative to the required holdings level?

What is the basis used for valuing NEO shareholdings?

Do in-the-money option grants and unvested equity grants count towards an NEO’s minimum ownership

requirements?

CCGG | Disclosure of Executive Compensation 44

2013 Best Practices for Proxy Circular Disclosure

Bank of Nova Scotia, 2013 Proxy Circular, pages 32-33:

Executive Share Ownership Guidelines

In support of our goal of aligning executive and shareholder interests and discouraging undue

and excessive risk taking, all of our executives must meet minimum share ownership

requirements. In addition, the CEO and his direct reports are subject to postretirement

retention requirements. The required holdings reflect the executive’s compensation and level,

and may be satisfied through holdings of common shares, as well as any outstanding DSUs,

RSUs, PSUs and DPP units and holdings in our Employee Share Ownership Plan. New and

promoted executives have three years to meet the share ownership requirements.

The table below summarizes the minimum ownership requirements by level:

All of the NEOs have exceeded the minimum share ownership guidelines, as outlined in the

following table:

CCGG | Disclosure of Executive Compensation 45

2013 Best Practices for Proxy Circular Disclosure

Note on Trading Restrictions:

Effective with the December 2010 grants, to be eligible to receive equity-based awards

executives must attest that they do not use personal hedging strategies or compensation-

related insurance to undermine the risk alignment effects embedded in our compensation plans.

All of our employees, including executive officers are prohibited from entering into short sales,

calls and puts with respect to any of our securities. These restrictions are prohibited under the

Bank Act, and are enforced through our compliance programs. In addition, executive officers are

required to seek pre-clearance from our compliance department prior to buying or selling any of

our publicly-traded securities, including stock options.

Discussion

BNS’ disclosure with respect to NEO share ownership meets all of our best practices.

Use and Limits of Retirement Benefits and Perquisites In reviewing the use of executive perquisite and retirement benefit programs, CCGG looks for compensation

disclosure to answer the following questions:

Has the company granted an NEO bonus years of pension service beyond those years actually worked?

Does the company have a policy on whether it will do so in the future?

Does the company have caps, either hard-dollar or otherwise, on pension benefits?

Does the company have any policies governing the use of perquisites for executives, particularly for

controversial perquisites such as personal use of corporate aircraft or tax-gross ups?

Canadian National Railway Company, 2012 Proxy Circular, page 42:

Discussion

CN Rail discloses explicitly that it does not provide tax gross-ups and that executives may use corporate aircraft

only for business matters.

Use, Policies and Limits for Discretion The use of board discretion is an important consideration for many shareholders when assessing executive

compensation disclosure. Situations may arise in which unforeseen circumstances cause formula-driven

compensation decisions to be inappropriate, but the use of discretion to increase compensation awards in years

CCGG | Disclosure of Executive Compensation 46

2013 Best Practices for Proxy Circular Disclosure

of poor performance may prompt shareholder concern that discretion is being used inappropriately. In order to

mitigate these concerns, compensation disclosure should:

fully explain under what circumstances the board might reasonably expect to exercise discretion,

state whether discretion was used to adjust awards during the current year or in the recent past, and if

so, why,

state the degree to which the use of discretion (if applicable) affected actual compensation awards and

if it would be exercised in the inverse situation to an equal but opposite degree, and

state if there are any limits or rules governing the use of board discretion.

Sun Life Financial, 2013 Proxy Circular, page 50:

Use of discretion

The board has discretion to increase or decrease awards under the AIP based on its assessment

of risk management and the impact on our financial results, and other factors that may have had

an effect on performance. The board has discretion to lower or zero out AIP or IIP awards, and

to lower or not grant new LTI awards for individuals or groups, if it concludes that results were

achieved by taking risks outside of board approved risk appetite levels. Under the Sun Share

plan, the board has discretion to cancel all outstanding awards if it determines that payment

would seriously jeopardize the capital position or solvency of the organization.

Discussion

Sun Life discloses that its board has the right to use discretion, gives a broad sense of what the circumstances

are under which discretion would be applied (discretion is primarily used for “risk mitigation” by Sun Life), and

discloses in its circular where discretion was used (not shown in the above quote).

Compensation Consultants and Benchmarking Compensation structure is often complicated and many boards seek outside advice to help design compensation

plans. Boards also commonly benchmark compensation against peers to ensure the company pays in a manner

that is competitive. We caution that the practice of benchmarking against peers should not be overly relied

upon at the expense of a robust, independent analysis.

When external consultants are retained by the board, the board, as a governance best practice, should ensure

that the consultant is independent of management. In any event, while the input received from independent

compensation consultants may provide valuable assistance to the board, it does not necessarily validate the

approach to executive compensation nor does it reduce the board’s responsibility to ensure that compensation

decisions are appropriate and closely aligned with performance.

Boards should disclose answers to the following questions:

Does the compensation committee make use of an independent compensation consultant?

CCGG | Disclosure of Executive Compensation 47

2013 Best Practices for Proxy Circular Disclosure

If management retains the same compensation consultant as the committee, must the committee first

give its approval? If so, what portion of the consultant’s total fees was attributable to work done for

management?

To the extent peer group benchmarking is used, does it serve solely to inform the board or does the

board target a specific range or percentile level for compensation relative to its chosen peer group?

What companies comprise the peer benchmarking group and what is the rationale for including the

peers that were chosen?

The Toronto-Dominion Bank, 2013 Proxy Circular, page 26:

Discussion

Like most companies, TD discloses its peer selection criteria and the selected peers. What sets TD apart is the