2013 aat accounting qualification specification · 2013 aat accounting qualification specification...

TRANSCRIPT

1

2013 AAT Accounting Qualification specification Published October 2012

2

Level 2 Certificate in Accounting. Qualification number: 60069090 (Level 5 in Scotland)

Title (and reference number) Basic Costing

Level 2 (Level 5 in Scotland)

Credit value 8 (4 knowledge and 4 skills)

Learning outcomes The learner will…

Assessment criteria The learner can…

1 Understand the cost recording system within an organisation

1.1 K Explain the nature of an organisation’s business transactions in relation to its accounting systems

1.2 K Explain the purpose and structure of a costing system within an organisation

1.3 K Identify the relationship between the costing and accounting systems within an organisation

1.4 K Identify sources of income and expenditure information for historic, current and forecast periods

1.5 K Identify types of cost, profit and investment centres

2 Be able to use the cost recording system to record or extract data

2.1 K Explain how materials, labour and expenses are classified and recorded

2.2 K Explain different methods of coding data

2.3 S Classify and code cost information for materials, labour and expenses

2.4 K

Classify different types of inventory as:

Raw materials

Part-finished goods (work in progress)

Finished goods

2.5 S

Calculate inventory valuations and issues of inventory using these methods :

First in first out (FIFO)

Last in first out (LIFO)

Weighted average

2.6 S

Use these methods to calculate payments for labour:

Time rate

Piecework rate

Bonuses

2.7 K Explain the nature of expenses and distinguish between fixed, variable and semi-variable overheads

2.8 S Calculate the direct cost of a product or service

3 Be able to use spreadsheets to provide information on actual and budgeted income and expenditure

3.1 S Enter income and expenditure data into a spreadsheet

3.2 K Explain how spreadsheets can be used to present information on income and expenditure and to facilitate internal reporting

3.3 S Enter budgeted and actual data on income and expenditure into a spreadsheet to provide a comparison of the results and identify differences

3.4 S Use basic spreadsheet functions and formulas

3.5 S Format the spreadsheet to present data in a clear and unambiguous manner and in accordance with organisational requirements

Unit aim(s)

Learners will be able to use cost recording systems to prepare information relating to the income and expenditure of an organisation. They will be able to make comparisons and identify differences between actual and expected figures, and communicate their findings using spreadsheets.

3

Title (and reference number) Computerised Accounting

Level 2 (Level 5 in Scotland)

Credit value 4 (4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Enter accounting data at the beginning of an accounting period

1.1 Set up general ledger accounts, entering opening balances where appropriate

1.2 Set up customer accounts, entering opening balances where appropriate

1.3 Set up supplier accounts, entering opening balances where appropriate

2 Record customer transactions

2.1 Process sales invoices and credit notes, accounting for VAT

2.2 Allocate monies received from customers in partial or full payment of invoices and balances

3 Record supplier transactions

3.1 Process purchase invoices and credit notes, accounting for VAT

3.2 Allocate monies paid to suppliers in full or partial settlement of invoices and balances

4 Record and reconcile bank and cash transactions

4.1 Process receipts and payments for non-credit transactions

4.2 Process recurring receipts and payments

4.3 Process petty cash receipts and payments, accounting for VAT

4.4 Perform a periodic bank reconciliation

5 Be able to use journals to enter accounting transactions

5.1 Process journals for accounting transactions

5.2 Use the journal to correct errors

6 Produce reports

6.1

Produce these routine reports for customers and suppliers:

Day books

Account activity

Aged analysis

Statements or remittance advice notes

6.2

Produce these routine reports from the general ledger:

Trial balance

Audit trail

Account activity

7 Maintain the safety and security of data held in the computerised accounting system

7.1 Make a copy of accounting data using the backup function of the accounting software

7.2 Use a software password to protect accounting information

Unit aim(s)

Learners will be able to use a computerised accounting system to enter accounting transactions, perform a reconciliation, correct errors and produce a range of reports. They will also be able to maintain the security of accounting information using passwords and backup routines.

4

Title (and reference number) Work effectively in accounting and finance

Level 2 (Level 5 in Scotland)

Credit value 5 (3 knowledge and 2 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the accounting or payroll function within an organisation

1.1 K Explain the role of accountancy or payroll functions within an organisation

1.2 K Identify the contribution of those in accounting or payroll functions to maintaining the smooth running, solvency and legal compliance of an organisation

1.3 K Identify appropriate reporting lines within the working environment

1.4 K Identify organisational policies or procedures that affect the workplace

2 Be able to use a range of communication skills

2.1 S Prepare information using effective numeracy and literacy skills

2.2 S

Present information in these formats using organisational house styles/guidelines:

Business report

Letter

Email or memo

3 Work independently or as part of a team

3.1 S Manage work to prioritise routine and non-routine tasks

3.2 K Identify the impact that the completion or non-completion of work can have on colleagues

3.3 K Explain how dissatisfaction can occur within a team and when it is appropriate to refer to a manager

4 Develop skills and knowledge to meet personal and organisational needs

4.1 K Explain the importance of continuing professional development

4.2 S Identify appropriate activities to meet development needs and objectives

5

Understand ethical values and principles

5.1 K Identify the fundamental principles of ethical behaviour

5.2 K Explain the importance of confidentiality

5.3 K Identify situations when a conflict of interest may arise

6 Understand sustainable values

6.1 K Identify organisational initiatives which support sustainability

6.2 K Explain the benefits of sustainable initiatives on an organisation and the environment

Unit aim(s)

The aim of this unit is to ensure that learners can apply the skills of literacy and numeracy in their work and gain skills of self-management and time management. Learners will also gain an appreciation of ethical issues and sustainability.

5

Title (and reference number) Processing bookkeeping transactions

Level 2 (Level 5 in Scotland)

Credit value 9 (3 knowledge and 6 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1

Understand the principles of processing financial transactions

1.1 K

Outline the purpose and content of these business documents:

Petty cash voucher

Invoice

Credit note

Remittance advice

Statement of account

1.2 K Explain the purpose and content of the books of prime entry

1.3 K List the ways in which customers may pay an organisation and an organisation may pay its suppliers

2 Understand the double entry bookkeeping system

2.1 K Explain the accounting equation and how it relates to a double entry bookkeeping system

2.2 K Outline how the books of prime entry integrate with the double entry bookkeeping system

2.3 K Describe the function of a coding system within a double entry bookkeeping system

2.4 K Describe the processing of financial transactions from the books of prime entry into the double entry bookkeeping system

2.5 K Define capital income and capital expenditure

2.6 K Define revenue income and revenue expenditure

3 Understand discounts

3.1 K Explain the difference between settlement, trade and bulk discount

3.2 K Describe the effect that settlement discount has on the sales tax (VAT) charged

4

Prepare and process financial documentation for customers

4.1 S Use source documents to prepare invoices or credit notes

4.2 S

Calculate invoice or credit note amounts reflecting any:

Trade discount

Bulk discount

Settlement discount

Sales tax

4.3 S Enter sales invoices and credit notes into books of prime entry using suitable codes

4.4 S Check the accuracy of receipts from customers against relevant supporting documentation

4.5 S Produce statements of account to send to credit customers

5 Process supplier invoices and credit notes and calculate payments 5.1 S

Check accuracy of supplier invoices and credit notes against these source documents:

Purchase orders

Goods received notes

Delivery notes

5.2 S Enter supplier invoices and credit notes into books of prime entry using suitable codes

5.3 S Reconcile supplier statements to purchase ledger accounts

5.4 S Calculate payments due to suppliers

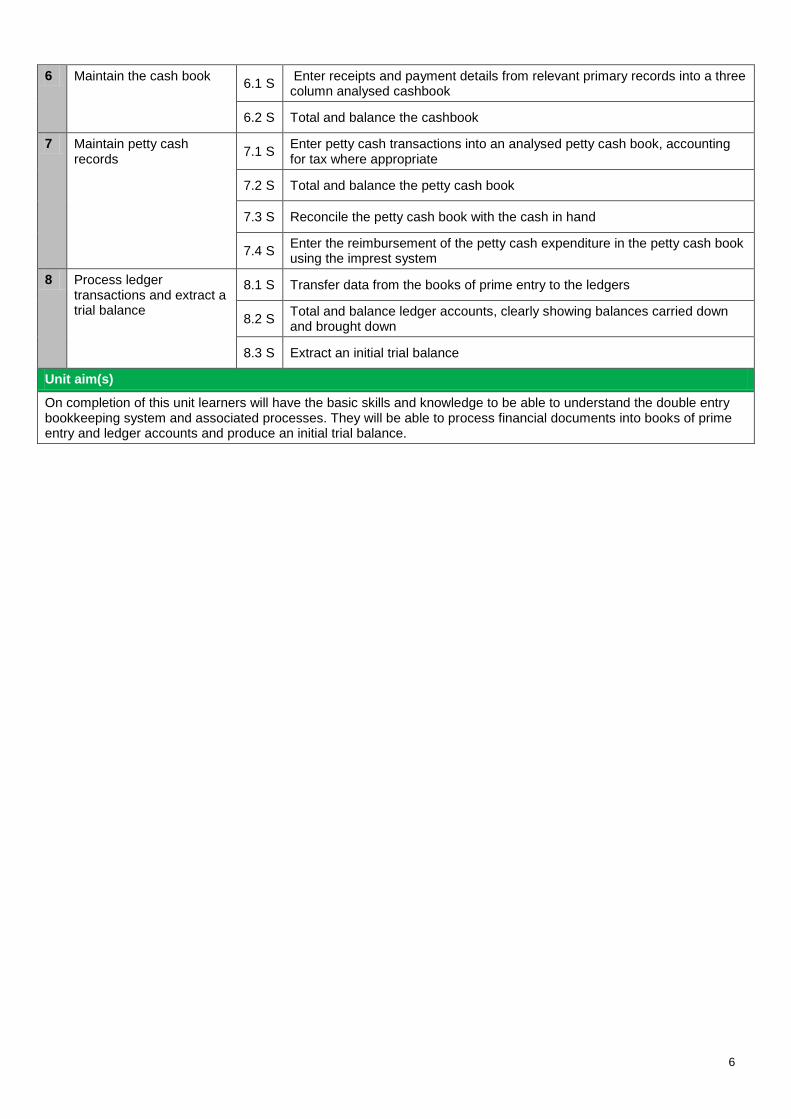

6

6 Maintain the cash book 6.1 S

Enter receipts and payment details from relevant primary records into a three column analysed cashbook

6.2 S Total and balance the cashbook

7 Maintain petty cash records

7.1 S Enter petty cash transactions into an analysed petty cash book, accounting for tax where appropriate

7.2 S Total and balance the petty cash book

7.3 S Reconcile the petty cash book with the cash in hand

7.4 S Enter the reimbursement of the petty cash expenditure in the petty cash book using the imprest system

8 Process ledger transactions and extract a trial balance

8.1 S Transfer data from the books of prime entry to the ledgers

8.2 S Total and balance ledger accounts, clearly showing balances carried down and brought down

8.3 S Extract an initial trial balance

Unit aim(s)

On completion of this unit learners will have the basic skills and knowledge to be able to understand the double entry bookkeeping system and associated processes. They will be able to process financial documents into books of prime entry and ledger accounts and produce an initial trial balance.

7

Title (and reference number) Control accounts, journals and the banking system

Level 2 (Level 5 in Scotland)

Credit value 8 (2 knowledge and 6 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the purpose and use of control accounts and journals

1.1 K Describe the general purpose of control accounts

1.2 K

Describe the specific purpose of the following control accounts:

Sales ledger

Purchase ledger

Tax (VAT)

1.3 K Explain the importance of reconciling the sales and purchase ledger control accounts regularly

1.4 K Describe the purpose of an aged trade receivables analysis

1.5 K Explain the need to deal with discrepancies quickly and professionally

1.6 K Describe the reasons for maintaining the journal

1.7 K Explain the content and format of the journal

1.8 K Identify errors that are corrected through the journal

2 Maintain and use control accounts

2.1 S

Prepare these control accounts:

Sales ledger

Purchases ledger

Tax (VAT)

2.2 S Reconcile sales and purchase ledger control accounts with the relevant ledgers

2.3 S Verify the balance on the tax control account

3 Maintain and use the journal

3.1 S

Create journal entries to record these transactions:

A new set of double entry bookkeeping records

An irrecoverable debt written off

Wages and salaries

3.2 S Create journal entries to correct errors not disclosed by the trial balance

3.3 S Create journal entries to open a suspense account to balance the trial balance

3.4 S Create journal entries to correct errors disclosed by the trial balance and to clear the suspense account

3.5 S Record journal entries in the ledger accounts

3.6 S Redraft the trial balance following adjustments

4 Reconcile a bank statement with the cash book

4.1 S Identify differences between individual items on the bank statement and in the cashbook

4.2 S Update the cashbook from the bank statement

4.3 S Prepare a bank reconciliation statement

8

5 Understand the banking process

5.1 K Identify the main services offered by banks and building societies

5.2 K Explain when funds banked are cleared and available for use

5.3 K

Identify other forms of payment:

Cash

Cheques

Credit cards

Debit cards

Automated payments

5.4 K

Identify the information required to ensure the following payments are valid:

Cheque

Credit card

Debit card

5.5 K Describe procedures to ensure the security of receipts and payments

5.6 K Describe the effect that different forms of payment will have on an organisation’s bank balance

6 Understand retention and storage requirements relating to banking documents.

6.1 K Explain the importance of a formal document retention policy for an organisation

6.2 K Identify the different types of documents that should be stored securely

Unit aim(s)

On completion of this unit the learner will be able to maintain the journal and control accounts, reconcile balances and make corrections, and redraft the trial balance. They will also understand the banking system.

9

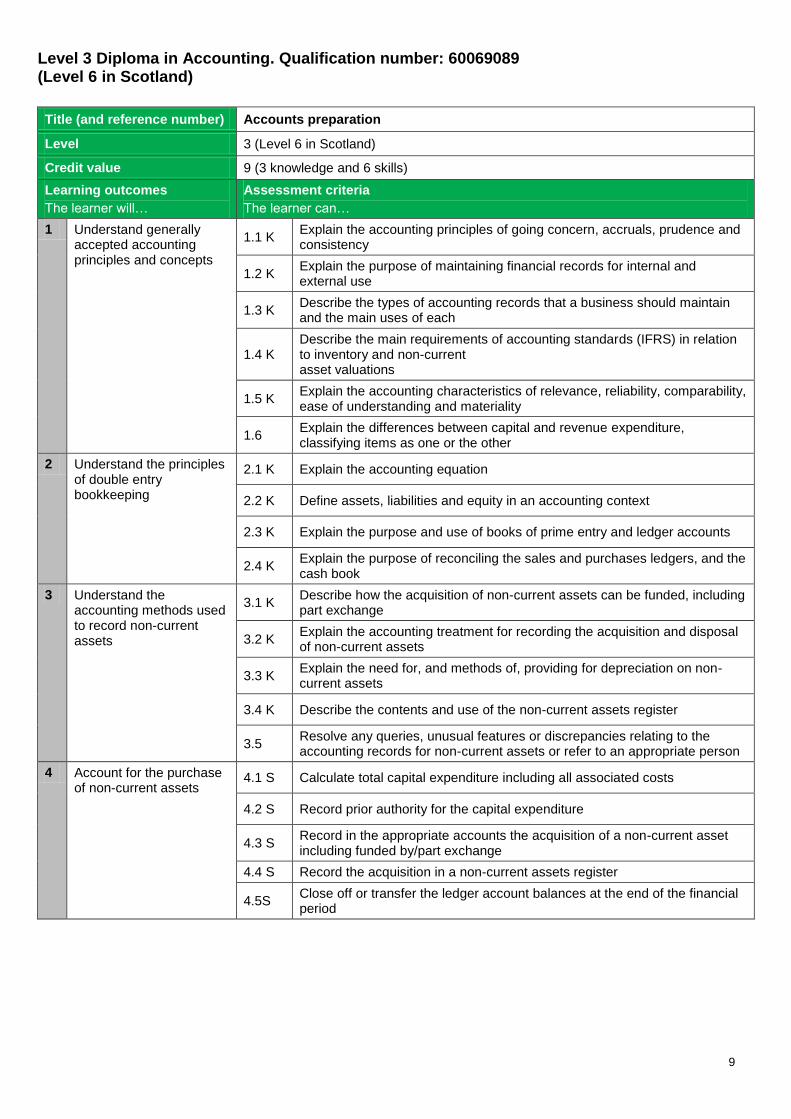

Level 3 Diploma in Accounting. Qualification number: 60069089 (Level 6 in Scotland)

Title (and reference number) Accounts preparation

Level 3 (Level 6 in Scotland)

Credit value 9 (3 knowledge and 6 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand generally accepted accounting principles and concepts

1.1 K Explain the accounting principles of going concern, accruals, prudence and consistency

1.2 K Explain the purpose of maintaining financial records for internal and external use

1.3 K Describe the types of accounting records that a business should maintain and the main uses of each

1.4 K Describe the main requirements of accounting standards (IFRS) in relation to inventory and non-current asset valuations

1.5 K Explain the accounting characteristics of relevance, reliability, comparability, ease of understanding and materiality

1.6 Explain the differences between capital and revenue expenditure, classifying items as one or the other

2 Understand the principles of double entry bookkeeping

2.1 K Explain the accounting equation

2.2 K Define assets, liabilities and equity in an accounting context

2.3 K Explain the purpose and use of books of prime entry and ledger accounts

2.4 K Explain the purpose of reconciling the sales and purchases ledgers, and the cash book

3 Understand the accounting methods used to record non-current assets

3.1 K Describe how the acquisition of non-current assets can be funded, including part exchange

3.2 K Explain the accounting treatment for recording the acquisition and disposal of non-current assets

3.3 K Explain the need for, and methods of, providing for depreciation on non-current assets

3.4 K Describe the contents and use of the non-current assets register

3.5 Resolve any queries, unusual features or discrepancies relating to the accounting records for non-current assets or refer to an appropriate person

4 Account for the purchase of non-current assets

4.1 S Calculate total capital expenditure including all associated costs

4.2 S Record prior authority for the capital expenditure

4.3 S Record in the appropriate accounts the acquisition of a non-current asset including funded by/part exchange

4.4 S Record the acquisition in a non-current assets register

4.5S Close off or transfer the ledger account balances at the end of the financial period

10

5 Account for depreciation

5.1 S

Calculate the depreciation charges for a non-current asset using the:

straight line method

reducing balance method

5.2 S Record the depreciation in the non-current assets register

5.3 S Record depreciation in the appropriate ledger accounts

5.4 S Close off the ledger accounts at the end of the financial period, correctly identifying any transfers to the statement of profit or loss

6 Account for the disposal of non-current assets

6.1 S Identify the correct asset, removing it from the non-current assets register

6.2 S Record the disposal of non-current assets in the appropriate accounts

6.3 S Calculate any gain or loss arising from the disposal, closing off or transferring the account balance

7 Account for adjustments 7.1 K

Explain the accounting treatment of accruals and prepayments to expenses and revenue

7.2 K Explain the reasons for, and method of, accounting for irrecoverable debts and allowances for doubtful debts

7.3 S Record the journal entries for closing inventory

7.4 S Record the journal entries for accrued and prepaid expenses and income

7.5 S Record the journal entries for provision for depreciation, irrecoverable debts and allowances for doubtful debts

7.6 S Record the journal entries to close off revenue accounts in preparation for the transfer of balances to the final accounts

8 Prepare and extend the trial balance

8.1 S Prepare ledger account balances; reconciling them, identifying any discrepancies and taking appropriate action

8.2 S Prepare a trial balance

8.3 S

Account for these adjustments:

Closing inventory

Accruals and prepayments to expenses and income

Provisions for depreciation on non-current assets

Irrecoverable debts

Allowance for doubtful debts

8.4 S Prepare the trial balance after adjustments

8.5 S Check for errors and/or inaccuracies in the trial balance, taking appropriate action

Unit aim(s)

This unit is about learners having the required skills and knowledge to prepare ledger accounts to trial balance stage according to current financial standards, including making any necessary adjustments. Learners will know how to account for the purchase and disposal of non-current assets

11

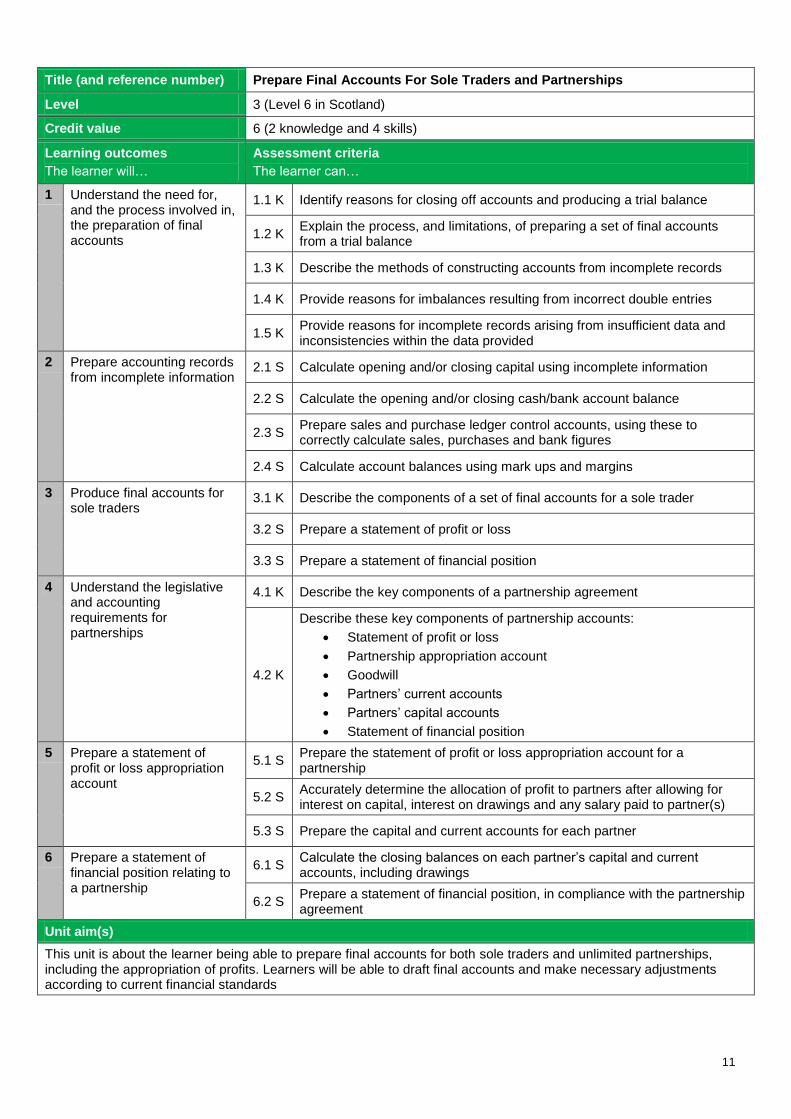

Title (and reference number) Prepare Final Accounts For Sole Traders and Partnerships

Level 3 (Level 6 in Scotland)

Credit value 6 (2 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the need for, and the process involved in, the preparation of final accounts

1.1 K Identify reasons for closing off accounts and producing a trial balance

1.2 K Explain the process, and limitations, of preparing a set of final accounts from a trial balance

1.3 K Describe the methods of constructing accounts from incomplete records

1.4 K Provide reasons for imbalances resulting from incorrect double entries

1.5 K Provide reasons for incomplete records arising from insufficient data and inconsistencies within the data provided

2 Prepare accounting records from incomplete information

2.1 S Calculate opening and/or closing capital using incomplete information

2.2 S Calculate the opening and/or closing cash/bank account balance

2.3 S Prepare sales and purchase ledger control accounts, using these to correctly calculate sales, purchases and bank figures

2.4 S Calculate account balances using mark ups and margins

3 Produce final accounts for sole traders

3.1 K Describe the components of a set of final accounts for a sole trader

3.2 S Prepare a statement of profit or loss

3.3 S Prepare a statement of financial position

4 Understand the legislative and accounting requirements for partnerships

4.1 K Describe the key components of a partnership agreement

4.2 K

Describe these key components of partnership accounts:

Statement of profit or loss

Partnership appropriation account

Goodwill

Partners’ current accounts

Partners’ capital accounts

Statement of financial position

5 Prepare a statement of profit or loss appropriation account

5.1 S Prepare the statement of profit or loss appropriation account for a partnership

5.2 S Accurately determine the allocation of profit to partners after allowing for interest on capital, interest on drawings and any salary paid to partner(s)

5.3 S Prepare the capital and current accounts for each partner

6 Prepare a statement of financial position relating to a partnership

6.1 S Calculate the closing balances on each partner’s capital and current accounts, including drawings

6.2 S Prepare a statement of financial position, in compliance with the partnership agreement

Unit aim(s)

This unit is about the learner being able to prepare final accounts for both sole traders and unlimited partnerships, including the appropriation of profits. Learners will be able to draft final accounts and make necessary adjustments according to current financial standards

12

Title (and reference number) Costs and Revenues

Level 3 (Level 6 in Scotland)

Credit value 8 (4 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the nature and role of costing systems within an organisation

1.1 K Explain the purpose of internal reporting and providing accurate information to management

1.2 K Explain the relationship between the various costing systems within an organisation

1.3 K Identify the responsibility centres, cost centres, profit centres and investment centres within an organisation

1.4 K Explain the characteristics of different types of cost classifications and their use in costing

1.5 K Explain the differences between marginal and absorption costing

2 Record and analyse cost information

2.1 S Record cost information for material, labour and expenses in accordance with the organisation’s costing procedures

2.2 S Analyse cost information for material, labour and expenses in accordance with the organisation’s costing procedures

2.3 K Define the various stages of inventory

2.4 S

Value inventory using these methods:

First in first out (FIFO)

Last in first out (LIFO)

Weighted average

2.5 K

Describe the behaviour of these costs:

Fixed

Variable

Semi-variable

Stepped

2.6 S

Record cost information using these costing systems:

Job

Batch

Unit

Process

Service

3 Apportion costs according to organisational requirements 3.1 S

Attribute overhead costs to production and service cost centres in accordance with agreed bases of allocation and apportionment:

Direct

Step down

3.2 S

Calculate overhead absorption rates in accordance with suitable bases of absorption:

Machine hours

Labour hours

3.3 S Make adjustments for under or over recovered overhead costs in accordance with established procedures

3.4 S Review methods of allocation, apportionment and absorption at regular intervals, implementing agreed changes to methods

3.5 S Communicate with relevant staff to resolve any queries in overhead cost data

13

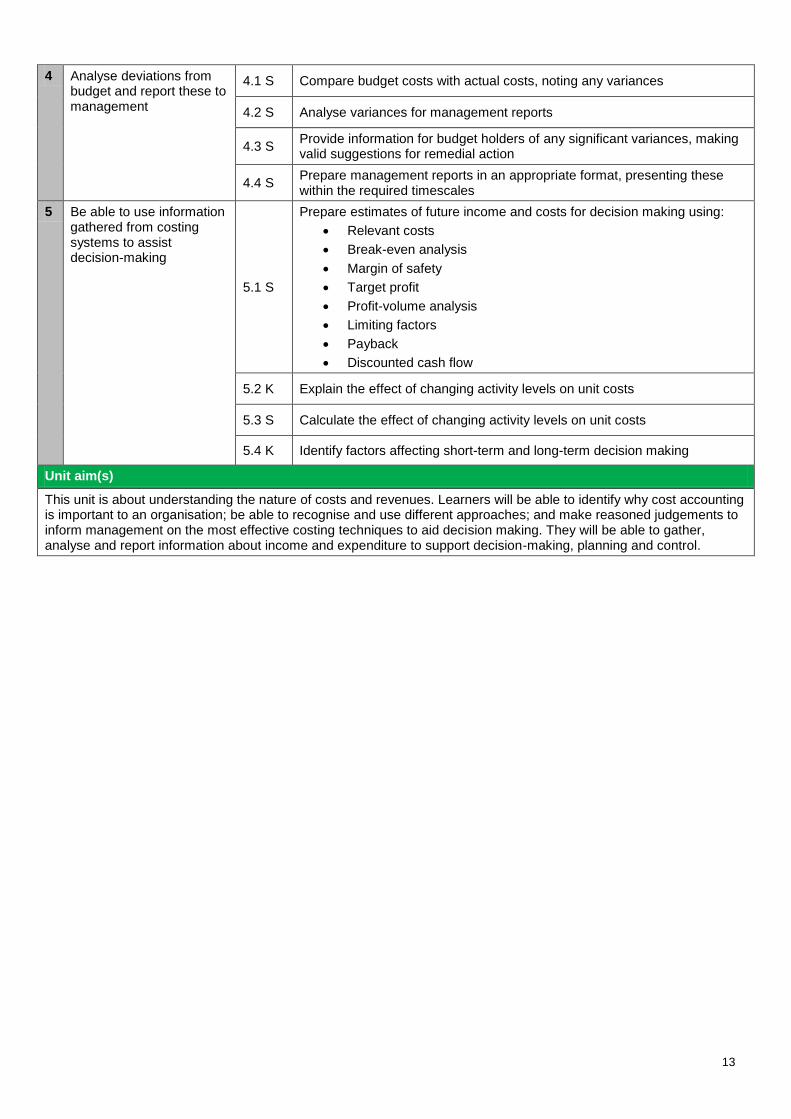

4 Analyse deviations from budget and report these to management

4.1 S Compare budget costs with actual costs, noting any variances

4.2 S Analyse variances for management reports

4.3 S Provide information for budget holders of any significant variances, making valid suggestions for remedial action

4.4 S Prepare management reports in an appropriate format, presenting these within the required timescales

5 Be able to use information gathered from costing systems to assist decision-making

5.1 S

Prepare estimates of future income and costs for decision making using:

Relevant costs

Break-even analysis

Margin of safety

Target profit

Profit-volume analysis

Limiting factors

Payback

Discounted cash flow

5.2 K Explain the effect of changing activity levels on unit costs

5.3 S Calculate the effect of changing activity levels on unit costs

5.4 K Identify factors affecting short-term and long-term decision making

Unit aim(s)

This unit is about understanding the nature of costs and revenues. Learners will be able to identify why cost accounting is important to an organisation; be able to recognise and use different approaches; and make reasoned judgements to inform management on the most effective costing techniques to aid decision making. They will be able to gather, analyse and report information about income and expenditure to support decision-making, planning and control.

14

Title (and reference number) Professional Ethics

Level 3 (Level 6 in Scotland)

Credit value 4 (4 knowledge)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand principles of ethical working

1.1

Explain these fundamental principles of ethical behaviour:

Integrity

Objectivity

Professional and technical competence and due care

Confidentiality

Professional behaviour

1.2 Outline the relevant legal, regulatory and ethical requirements affecting the accounting and finance sector

1.3 Explain the role of professional bodies in relation to the accounting and finance sector

1.4 Explain why individuals, organisations or industry sectors are expected to operate within codes of conduct and practice

1.5 Explain the risks of improper practice to an organisation and the importance of vigilance

1.6 Identify opportunities for maintaining an up to date knowledge of changes to codes of practice, regulation and legislation affecting the accounting and finance sector

2 Understand ethical behaviour when working with internal and external customers

2.1 Explain how to act ethically when working with clients, suppliers, colleagues and others

2.2 Explain the importance of objectivity and maintaining a professional distance between professional duties and personal life at all times

2.3 Explain the importance of adhering to organisational and professional values, codes of practice and regulations

2.4 Explain the importance of adhering to organisational policies for handling clients’ monies

2.5 Identify circumstances when confidential information should be disclosed and who is entitled to the information

2.6 Explain the importance of working within the limits and confines of one’s own professional experience, knowledge and expertise

3 Understand when and how to take appropriate action following any suspected breaches of ethical codes

3.1 Identify the relevant authorities and internal departments to which unethical behaviour, breaches of confidentiality, suspected illegal acts or other malpractice should be reported

3.2 Identify the appropriate action to take in instances when requests for work are beyond the employee’s competence

3.3 Identify inappropriate client behaviour and how to report it

3.4 Explain the internal and external reporting procedures which should be followed if an employee suspects an employer, colleague or client has committed, or may commit, an act which is believed to be illegal or unethical

3.5 Outline strategies that could be used to prevent ethical conflict

4 Understand the ethical responsibility of the finance professional in promoting sustainability

4.1 Explain the importance of an ethical approach to sustainability

4.2 Outline the responsibilities of finance professionals in upholding the principles of sustainability

Unit aim(s)

This unit is about recognising the importance of the learner acting and working in an ethical manner. Learners will be able to work within the ethical code to ensure that the public has a level of confidence in accounting practices or functions, to protect their own and their organisations professional reputation and integrity and ensure they uphold principles of sustainability.

15

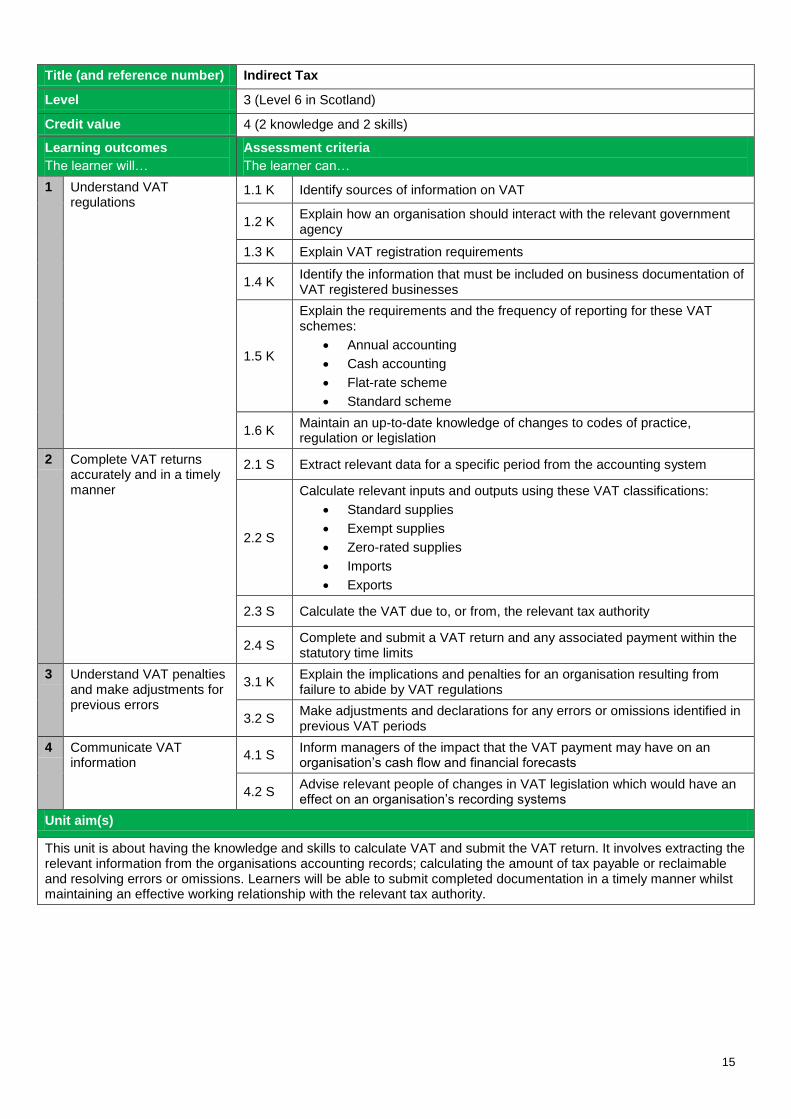

Title (and reference number) Indirect Tax

Level 3 (Level 6 in Scotland)

Credit value 4 (2 knowledge and 2 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand VAT regulations

1.1 K Identify sources of information on VAT

1.2 K Explain how an organisation should interact with the relevant government agency

1.3 K Explain VAT registration requirements

1.4 K Identify the information that must be included on business documentation of VAT registered businesses

1.5 K

Explain the requirements and the frequency of reporting for these VAT schemes:

Annual accounting

Cash accounting

Flat-rate scheme

Standard scheme

1.6 K Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

2 Complete VAT returns accurately and in a timely manner

2.1 S Extract relevant data for a specific period from the accounting system

2.2 S

Calculate relevant inputs and outputs using these VAT classifications:

Standard supplies

Exempt supplies

Zero-rated supplies

Imports

Exports

2.3 S Calculate the VAT due to, or from, the relevant tax authority

2.4 S Complete and submit a VAT return and any associated payment within the statutory time limits

3 Understand VAT penalties and make adjustments for previous errors

3.1 K Explain the implications and penalties for an organisation resulting from failure to abide by VAT regulations

3.2 S Make adjustments and declarations for any errors or omissions identified in previous VAT periods

4 Communicate VAT information

4.1 S Inform managers of the impact that the VAT payment may have on an organisation’s cash flow and financial forecasts

4.2 S Advise relevant people of changes in VAT legislation which would have an effect on an organisation’s recording systems

Unit aim(s)

This unit is about having the knowledge and skills to calculate VAT and submit the VAT return. It involves extracting the relevant information from the organisations accounting records; calculating the amount of tax payable or reclaimable and resolving errors or omissions. Learners will be able to submit completed documentation in a timely manner whilst maintaining an effective working relationship with the relevant tax authority.

16

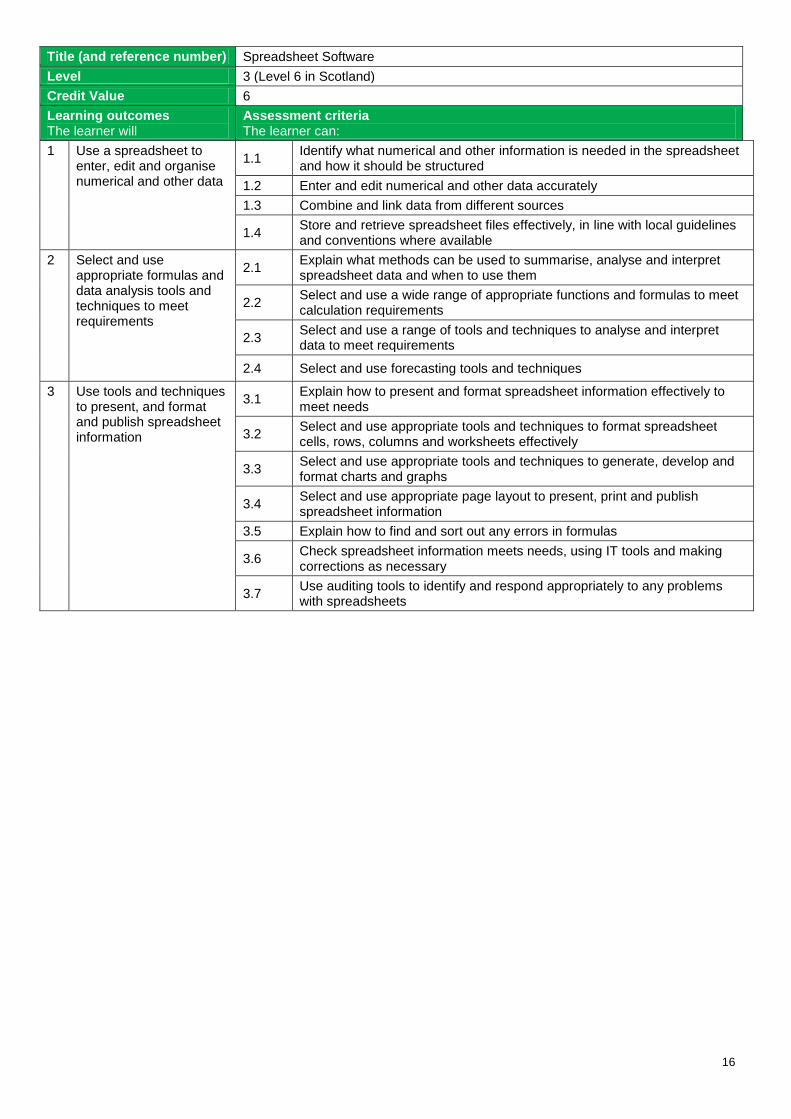

Title (and reference number) Spreadsheet Software

Level 3 (Level 6 in Scotland)

Credit Value 6

Learning outcomes The learner will

Assessment criteria The learner can:

1 Use a spreadsheet to enter, edit and organise numerical and other data

1.1 Identify what numerical and other information is needed in the spreadsheet and how it should be structured

1.2 Enter and edit numerical and other data accurately

1.3 Combine and link data from different sources

1.4 Store and retrieve spreadsheet files effectively, in line with local guidelines and conventions where available

2 Select and use appropriate formulas and data analysis tools and techniques to meet requirements

2.1 Explain what methods can be used to summarise, analyse and interpret spreadsheet data and when to use them

2.2 Select and use a wide range of appropriate functions and formulas to meet calculation requirements

2.3 Select and use a range of tools and techniques to analyse and interpret data to meet requirements

2.4 Select and use forecasting tools and techniques

3 Use tools and techniques to present, and format and publish spreadsheet information

3.1 Explain how to present and format spreadsheet information effectively to meet needs

3.2 Select and use appropriate tools and techniques to format spreadsheet cells, rows, columns and worksheets effectively

3.3 Select and use appropriate tools and techniques to generate, develop and format charts and graphs

3.4 Select and use appropriate page layout to present, print and publish spreadsheet information

3.5 Explain how to find and sort out any errors in formulas

3.6 Check spreadsheet information meets needs, using IT tools and making corrections as necessary

3.7 Use auditing tools to identify and respond appropriately to any problems with spreadsheets

17

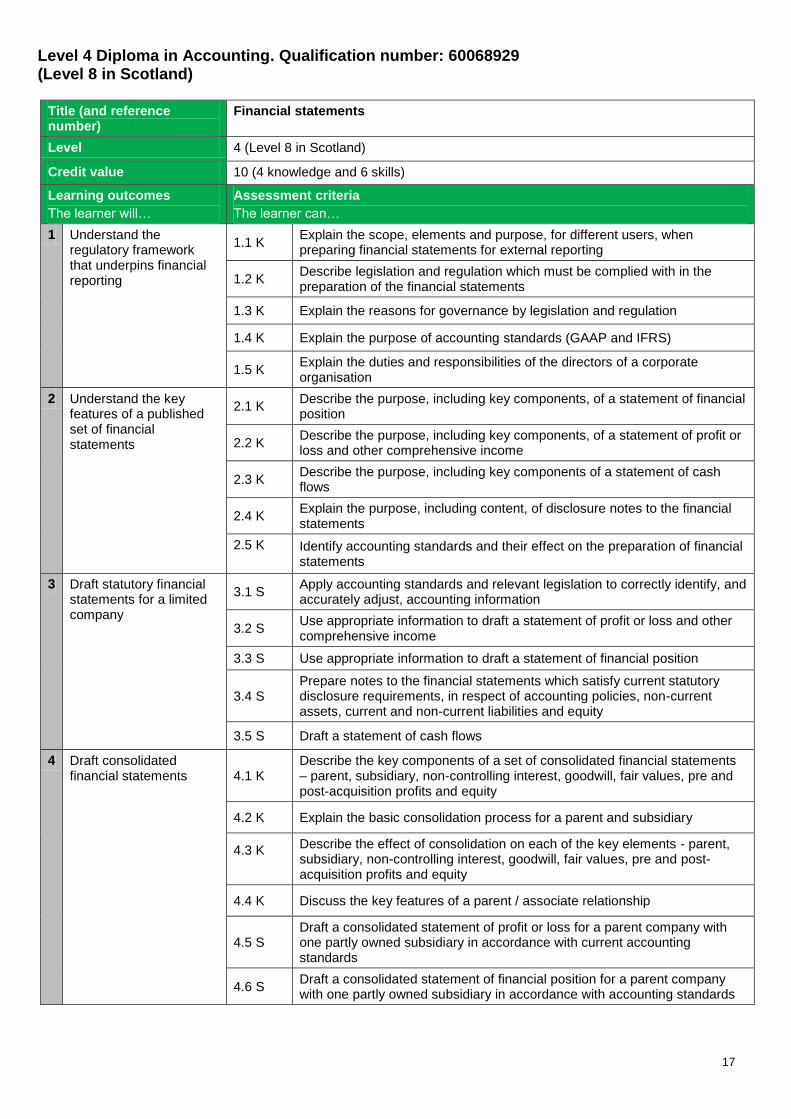

Level 4 Diploma in Accounting. Qualification number: 60068929 (Level 8 in Scotland)

Title (and reference number)

Financial statements

Level 4 (Level 8 in Scotland)

Credit value 10 (4 knowledge and 6 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the regulatory framework that underpins financial reporting

1.1 K Explain the scope, elements and purpose, for different users, when preparing financial statements for external reporting

1.2 K Describe legislation and regulation which must be complied with in the preparation of the financial statements

1.3 K Explain the reasons for governance by legislation and regulation

1.4 K Explain the purpose of accounting standards (GAAP and IFRS)

1.5 K Explain the duties and responsibilities of the directors of a corporate organisation

2 Understand the key features of a published set of financial statements

2.1 K Describe the purpose, including key components, of a statement of financial position

2.2 K Describe the purpose, including key components, of a statement of profit or loss and other comprehensive income

2.3 K Describe the purpose, including key components of a statement of cash flows

2.4 K Explain the purpose, including content, of disclosure notes to the financial statements

2.5 K

Identify accounting standards and their effect on the preparation of financial statements

3 Draft statutory financial statements for a limited company

3.1 S Apply accounting standards and relevant legislation to correctly identify, and accurately adjust, accounting information

3.2 S Use appropriate information to draft a statement of profit or loss and other comprehensive income

3.3 S Use appropriate information to draft a statement of financial position

3.4 S Prepare notes to the financial statements which satisfy current statutory disclosure requirements, in respect of accounting policies, non-current assets, current and non-current liabilities and equity

3.5 S Draft a statement of cash flows

4 Draft consolidated financial statements

4.1 K Describe the key components of a set of consolidated financial statements – parent, subsidiary, non-controlling interest, goodwill, fair values, pre and post-acquisition profits and equity

4.2 K Explain the basic consolidation process for a parent and subsidiary

4.3 K

Describe the effect of consolidation on each of the key elements - parent, subsidiary, non-controlling interest, goodwill, fair values, pre and post-acquisition profits and equity

4.4 K Discuss the key features of a parent / associate relationship

4.5 S Draft a consolidated statement of profit or loss for a parent company with one partly owned subsidiary in accordance with current accounting standards

4.6 S Draft a consolidated statement of financial position for a parent company with one partly owned subsidiary in accordance with accounting standards

18

5 Interpret financial statements using ratio analysis

5.1 K Explain the relationship between elements of the financial statements – assets, liabilities, equity, income, expenses, contributions from owners and distributions to owners

5.2 K Discuss the purpose of interpreting ratios in a business environment

5.3 S Use accounting ratios to calculate and interpret the relationship between elements of the financial statements with regard to profitability, liquidity, efficient use of resources and financial position

5.4 S Draw valid conclusions from the information contained within the financial statements

5.5 S Present clearly and concisely issues, analysis and conclusions to the appropriate people

Unit aim(s)

This unit is about the learner having the skills and knowledge to prepare financial statements for limited companies, and prepare consolidated financial statements for simple groups. Learners will also be able to use ratio analysis to analyse financial statements and gain a good understanding of current accounting standards.

19

Title (and reference number)

Budgeting

Level 4 (Level 8 in Scotland)

Credit value 7 (3 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Prepare forecasts of income and expenditure

1.1 K Explain responsibility centres and the relationships between departments and functions

1.2 S Code, classify and allocate cost and revenue data to responsibility centres

1.3 K Identify internal and external sources of information on costs, prices, demand, availability of resources and cost of finance which can be used to forecast income and expenditure

1.4 K

Demonstrate the use of these techniques to forecast income and expenditure:

Indexing

Sampling

Moving averages

Linear regression

Seasonal trends

1.5 K Describe the internal charges made to attribute indirect costs to production

1.6 K Explain the principles and application of standard costing within the context of a budgetary control system

1.7 S Describe the purpose of income and expenditure forecasts and their link to budgets

1.8 K Forecast income and expenditure, using internal and external information

2 Prepare budgets 2.1 K

Identify the sources of data and planning assumptions used in budget proposals

2.2 S

Calculate these different types of costs:

Direct or indirect

Fixed, variable, semi-variable or stepped

Capital or revenue

2.3 S Schedule materials, labour and production resources to meet forecasts

2.4 S Prepare relevant draft budgets for consecutive time periods from forecast data

2.5 S Prepare cash flow forecasts to facilitate the achievement of organisational objectives

3 Assess the impact of internal and external factors on budgets

3.1 K

Describe the impact of the external environment and any specific external costs on budgets

3.2 S Analyse critical factors affecting costs and revenues, drawing conclusions

3.3 S Calculate the effect that variations in production and sales constraints will have on budgeted costs and revenues

3.4 S Review and revise the validity of budgets in light of any anticipated changes

20

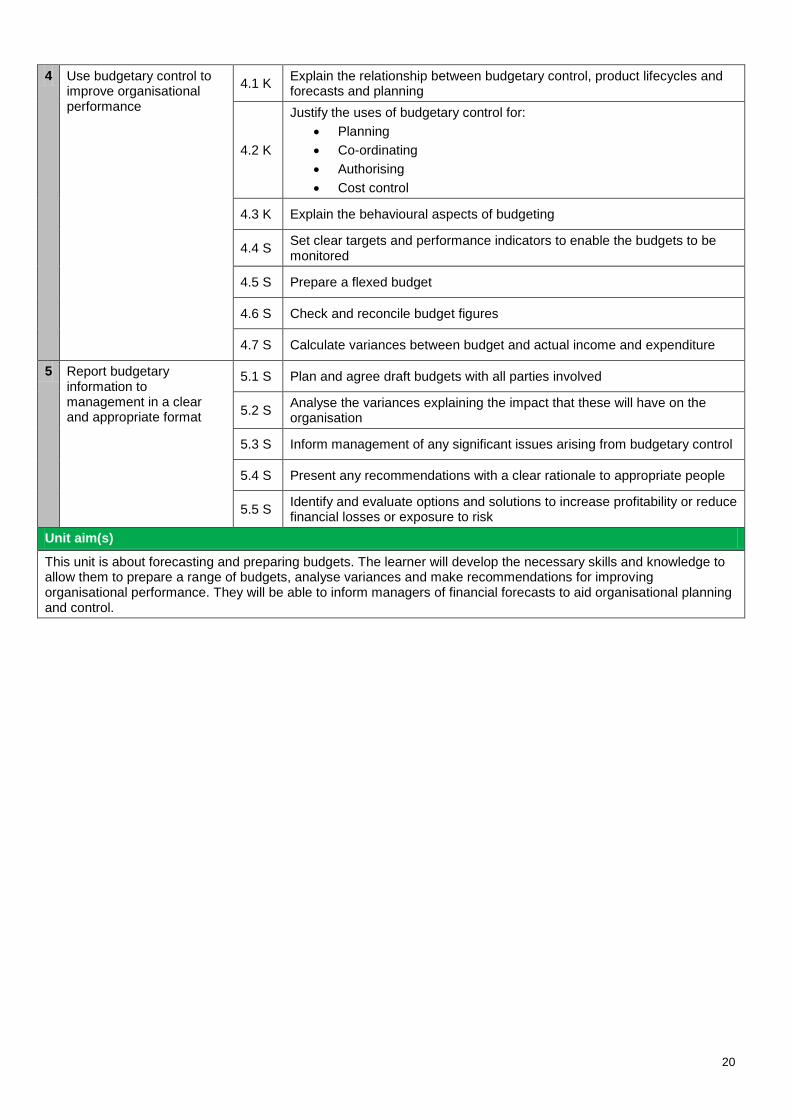

4 Use budgetary control to improve organisational performance

4.1 K Explain the relationship between budgetary control, product lifecycles and forecasts and planning

4.2 K

Justify the uses of budgetary control for:

Planning

Co-ordinating

Authorising

Cost control

4.3 K Explain the behavioural aspects of budgeting

4.4 S Set clear targets and performance indicators to enable the budgets to be monitored

4.5 S Prepare a flexed budget

4.6 S Check and reconcile budget figures

4.7 S Calculate variances between budget and actual income and expenditure

5 Report budgetary information to management in a clear and appropriate format

5.1 S Plan and agree draft budgets with all parties involved

5.2 S Analyse the variances explaining the impact that these will have on the organisation

5.3 S Inform management of any significant issues arising from budgetary control

5.4 S Present any recommendations with a clear rationale to appropriate people

5.5 S Identify and evaluate options and solutions to increase profitability or reduce financial losses or exposure to risk

Unit aim(s)

This unit is about forecasting and preparing budgets. The learner will develop the necessary skills and knowledge to allow them to prepare a range of budgets, analyse variances and make recommendations for improving organisational performance. They will be able to inform managers of financial forecasts to aid organisational planning and control.

21

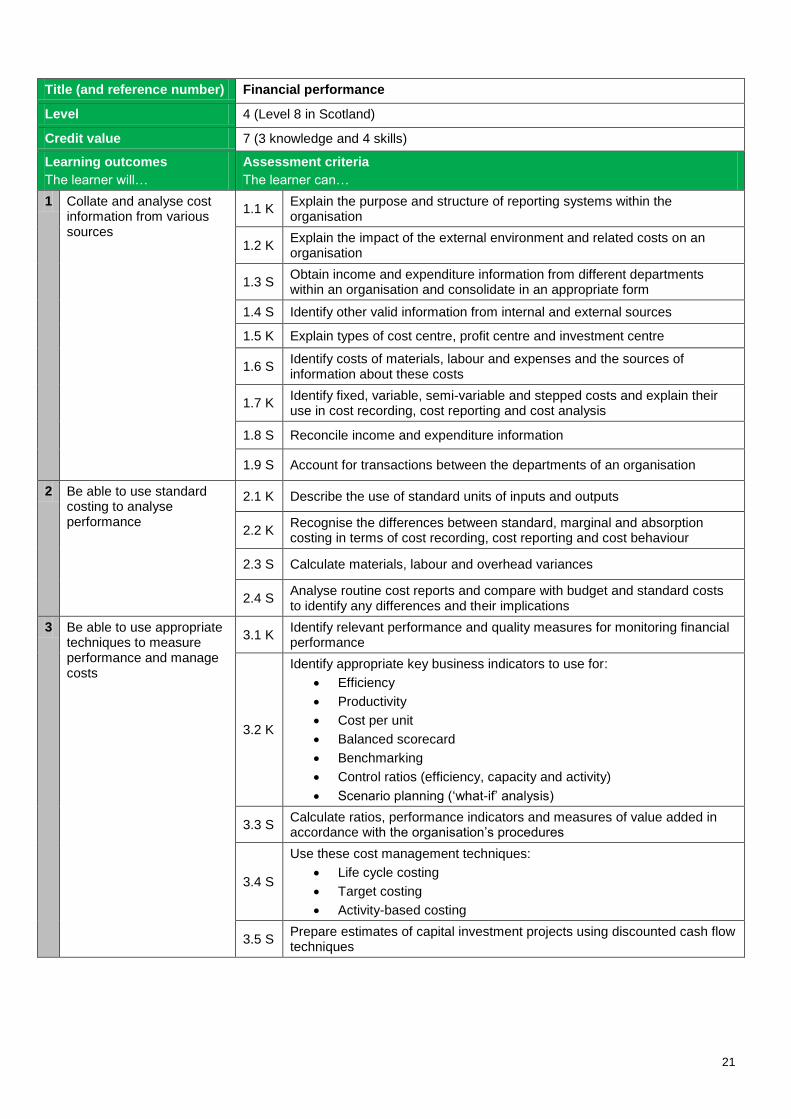

Title (and reference number) Financial performance

Level 4 (Level 8 in Scotland)

Credit value 7 (3 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Collate and analyse cost information from various sources

1.1 K Explain the purpose and structure of reporting systems within the organisation

1.2 K Explain the impact of the external environment and related costs on an organisation

1.3 S Obtain income and expenditure information from different departments within an organisation and consolidate in an appropriate form

1.4 S Identify other valid information from internal and external sources

1.5 K Explain types of cost centre, profit centre and investment centre

1.6 S Identify costs of materials, labour and expenses and the sources of information about these costs

1.7 K Identify fixed, variable, semi-variable and stepped costs and explain their use in cost recording, cost reporting and cost analysis

1.8 S Reconcile income and expenditure information

1.9 S Account for transactions between the departments of an organisation

2 Be able to use standard costing to analyse performance

2.1 K Describe the use of standard units of inputs and outputs

2.2 K Recognise the differences between standard, marginal and absorption costing in terms of cost recording, cost reporting and cost behaviour

2.3 S Calculate materials, labour and overhead variances

2.4 S Analyse routine cost reports and compare with budget and standard costs to identify any differences and their implications

3 Be able to use appropriate techniques to measure performance and manage costs

3.1 K Identify relevant performance and quality measures for monitoring financial performance

3.2 K

Identify appropriate key business indicators to use for:

Efficiency

Productivity

Cost per unit

Balanced scorecard

Benchmarking

Control ratios (efficiency, capacity and activity)

Scenario planning (‘what-if’ analysis)

3.3 S Calculate ratios, performance indicators and measures of value added in accordance with the organisation’s procedures

3.4 S

Use these cost management techniques:

Life cycle costing

Target costing

Activity-based costing

3.5 S Prepare estimates of capital investment projects using discounted cash flow techniques

22

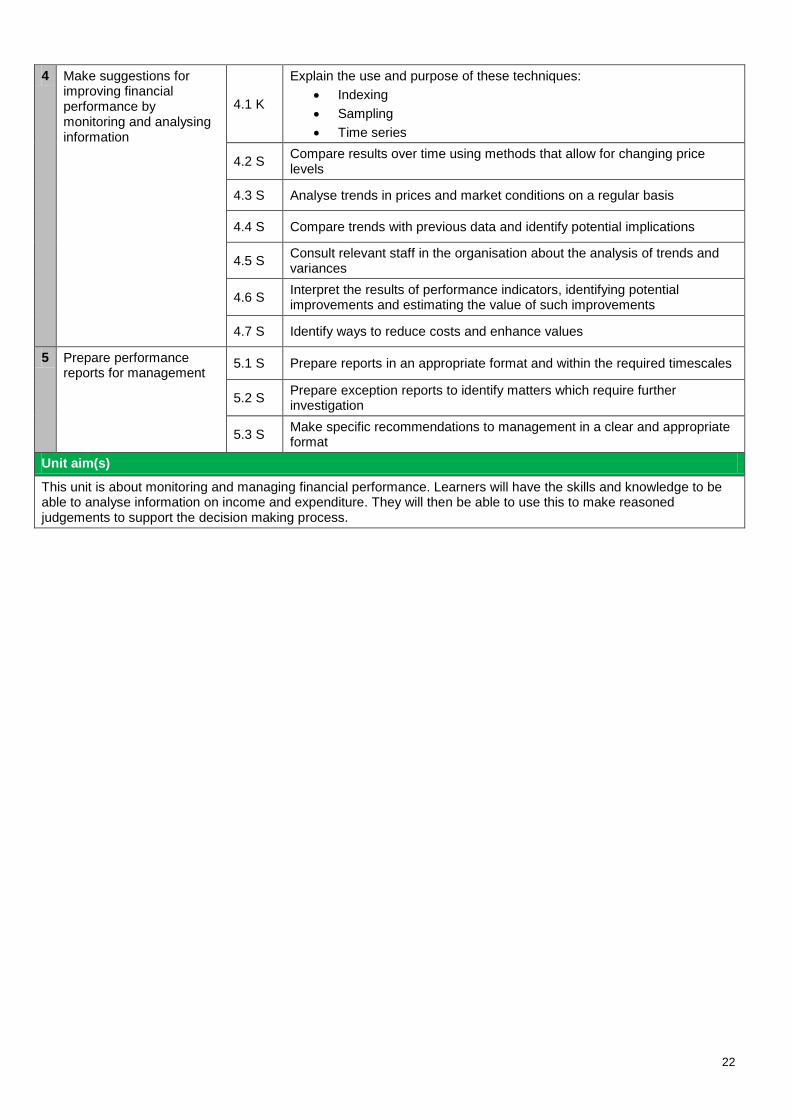

4 Make suggestions for improving financial performance by monitoring and analysing information

4.1 K

Explain the use and purpose of these techniques:

Indexing

Sampling

Time series

4.2 S Compare results over time using methods that allow for changing price levels

4.3 S Analyse trends in prices and market conditions on a regular basis

4.4 S Compare trends with previous data and identify potential implications

4.5 S Consult relevant staff in the organisation about the analysis of trends and variances

4.6 S Interpret the results of performance indicators, identifying potential improvements and estimating the value of such improvements

4.7 S Identify ways to reduce costs and enhance values

5 Prepare performance reports for management

5.1 S Prepare reports in an appropriate format and within the required timescales

5.2 S Prepare exception reports to identify matters which require further investigation

5.3 S Make specific recommendations to management in a clear and appropriate format

Unit aim(s)

This unit is about monitoring and managing financial performance. Learners will have the skills and knowledge to be able to analyse information on income and expenditure. They will then be able to use this to make reasoned judgements to support the decision making process.

23

Title (and reference number) Internal control and accounting systems

Level 4 (Level 8 in Scotland)

Credit value 8 (4 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the role of accounting within an organisation

1.1 K Describe the purpose, structure and organisation of the accounting function and its relationships with other functions within the organisation

1.2 K Explain the various business purposes for which the following financial information is required:

Statement of profit or loss

Statement of cash flows

Statement of financial position

1.3 K Give an overview of the organisation’s business and its critical external relationships with stakeholders

1.4 K Explain how the accounting systems are affected by the organisational structure, systems, procedures and business transactions

1.5 K Explain the effect on users of changes to accounting systems caused by:

External regulations

Organisational policies and procedures

2

Understand the importance and use of internal control systems

2.1 K Identify the external regulations that affect accounting practice

2.2 K Describe the causes of, and common types of, fraud and their impact of this on an organisation

2.3 K Explain methods that can be used to detect fraud within an accounting system

2.4 K Explain the types of controls that can be put in place to ensure compliance with statutory or organisational requirements

2.5 K Explain how an internal control system can support the accounting function

3 Evaluate the accounting system and identify areas for improvement

3.1 S Identify an organisation’s accounting system requirements including hardware and software packages

3.2 S Review record keeping systems to confirm whether they meet an organisation’s requirements

3.3 S Identify weaknesses in and the potential for improvements to, the accounting system and consider the impact on the operation of an organisation

3.4 S Identify potential areas of fraud arising from lack of control within the accounting system evaluating the risk

3.5 S Review methods of operating for cost effectiveness, reliability and speed

4 Conduct an ethical evaluation of the accounting systems

4.1 S Evaluate the accounting system against ethical principles

4.2 S Identify actual or possible breaches of professional ethics

5 Conduct a sustainability evaluation of the accounting system

5.1 Evaluate the accounting system against sustainable principles

5.2 Identify where improvements could be made to improve sustainability

24

6 Make recommendations to

improve the accounting system

6.1 S Make recommendations for changes to the accounting system, including ethical and sustainability considerations, with a clear rationale and an explanation of any assumptions made

6.2 S Identify the effects that any recommended changes would have on the users of the system

6.3 K Enable individuals to understand how to use the accounting system by use of:

Training

Manuals

Written information

Help menus

6.4 S Identify the implications of recommended changes in terms of time, financial costs, benefits and operating procedures

Unit aim(s)

The aim of this unit is to ensure that the learner will be able to make a considered evaluation of an accounting system, with particular reference to internal controls, ethical considerations and the prevention of fraud. They will be able to make recommendations for improvements supported by a clear rationale of the impact upon the organisation and a cost benefit analysis.

25

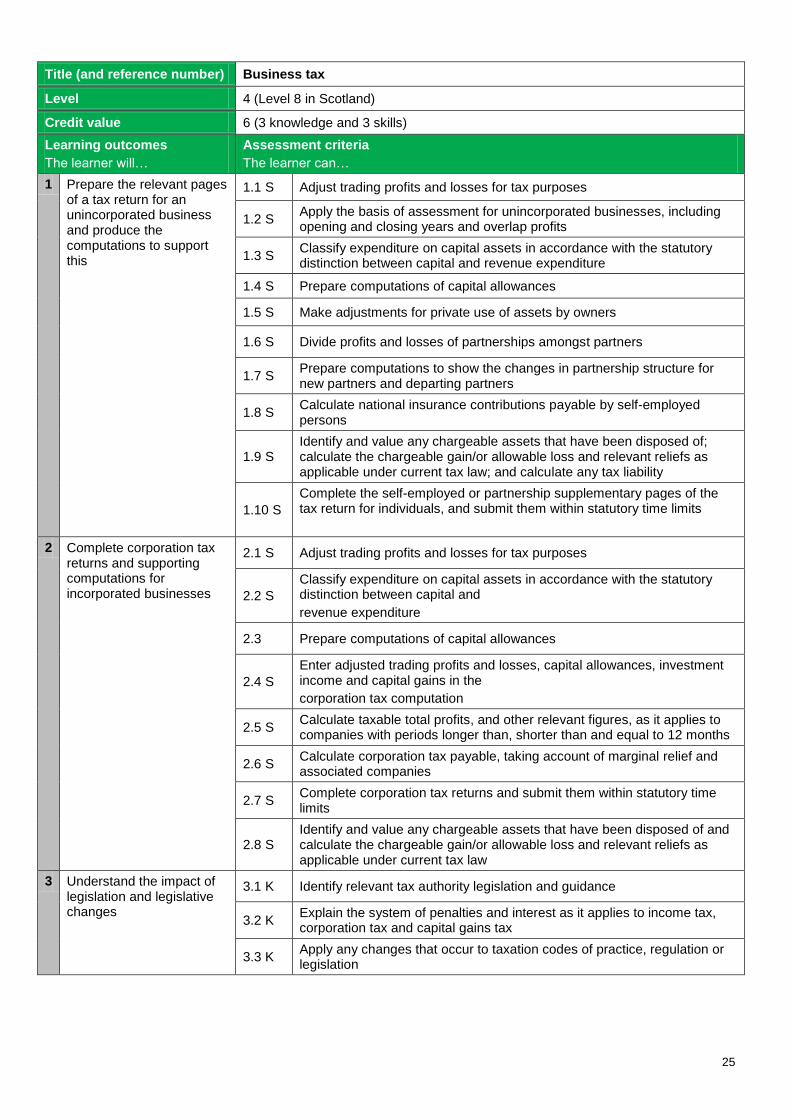

Title (and reference number) Business tax

Level 4 (Level 8 in Scotland)

Credit value 6 (3 knowledge and 3 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Prepare the relevant pages of a tax return for an unincorporated business and produce the computations to support this

1.1 S Adjust trading profits and losses for tax purposes

1.2 S Apply the basis of assessment for unincorporated businesses, including opening and closing years and overlap profits

1.3 S Classify expenditure on capital assets in accordance with the statutory distinction between capital and revenue expenditure

1.4 S Prepare computations of capital allowances

1.5 S Make adjustments for private use of assets by owners

1.6 S Divide profits and losses of partnerships amongst partners

1.7 S Prepare computations to show the changes in partnership structure for new partners and departing partners

1.8 S Calculate national insurance contributions payable by self-employed persons

1.9 S Identify and value any chargeable assets that have been disposed of; calculate the chargeable gain/or allowable loss and relevant reliefs as applicable under current tax law; and calculate any tax liability

1.10 S

Complete the self-employed or partnership supplementary pages of the tax return for individuals, and submit them within statutory time limits

2 Complete corporation tax returns and supporting computations for incorporated businesses

2.1 S Adjust trading profits and losses for tax purposes

2.2 S

Classify expenditure on capital assets in accordance with the statutory distinction between capital and

revenue expenditure

2.3 Prepare computations of capital allowances

2.4 S

Enter adjusted trading profits and losses, capital allowances, investment income and capital gains in the

corporation tax computation

2.5 S Calculate taxable total profits, and other relevant figures, as it applies to companies with periods longer than, shorter than and equal to 12 months

2.6 S Calculate corporation tax payable, taking account of marginal relief and associated companies

2.7 S Complete corporation tax returns and submit them within statutory time limits

2.8 S Identify and value any chargeable assets that have been disposed of and calculate the chargeable gain/or allowable loss and relevant reliefs as applicable under current tax law

3 Understand the impact of legislation and legislative changes

3.1 K Identify relevant tax authority legislation and guidance

3.2 K Explain the system of penalties and interest as it applies to income tax, corporation tax and capital gains tax

3.3 K Apply any changes that occur to taxation codes of practice, regulation or legislation

26

4 Understand tax law and its implications for unincorporated businesses

4.1 K Describe the main regulations relating to disallowed expenditure

4.2 K Explain the basis of assessment for unincorporated businesses

4.3 K Explain the availability and types of capital allowances

4.4 K Identify alternative loss reliefs, demonstrating how best to utilise that relief

4.5 K Explain the basic allocation of trading profits between partners

4.6 K Explain the self-assessment process including payment of tax and filing of returns for unincorporated businesses

4.7 K Identify due dates of payments, including payments on account

5 Understand tax law and its implications for incorporated businesses

5.1 K Explain the calculation of corporation tax payable by different sizes of companies including those with associated companies

5.2 K Identify alternative loss reliefs for trading losses, describing how best to utilise that relief

5.3 K Identify corporation tax payable and the due dates of payment, including instalments

6 Understand how to treat capital assets

6.1 K Identify capital gains exemptions and reliefs on assets

6.2 K Identify methods by which chargeable assets can be disposed of

6.3 K Identify the rate of tax payable on gains on capital assets disposed of by individuals and entitlement to relevant reliefs

Unit aim(s)

This unit is about the learner being able to prepare tax returns for sole traders, partnerships and incorporated businesses, and understand all relevant regulations and guidance for this. The learner will be able to recognise trading profits, make adjustments and apply current relevant legislation to accurately prepare the required computations to support the completion of the tax returns to the statutory authorities.

27

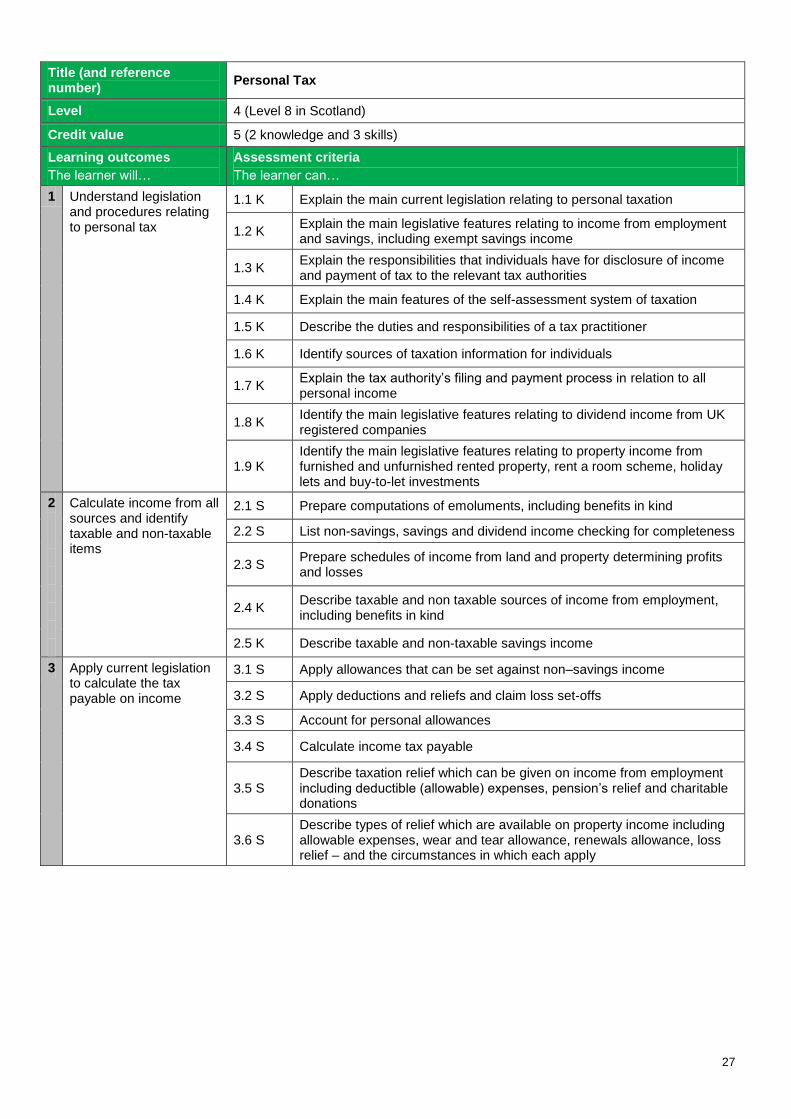

Title (and reference number)

Personal Tax

Level 4 (Level 8 in Scotland)

Credit value 5 (2 knowledge and 3 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand legislation and procedures relating to personal tax

1.1 K Explain the main current legislation relating to personal taxation

1.2 K Explain the main legislative features relating to income from employment and savings, including exempt savings income

1.3 K Explain the responsibilities that individuals have for disclosure of income and payment of tax to the relevant tax authorities

1.4 K Explain the main features of the self-assessment system of taxation

1.5 K Describe the duties and responsibilities of a tax practitioner

1.6 K Identify sources of taxation information for individuals

1.7 K Explain the tax authority’s filing and payment process in relation to all personal income

1.8 K Identify the main legislative features relating to dividend income from UK registered companies

1.9 K Identify the main legislative features relating to property income from furnished and unfurnished rented property, rent a room scheme, holiday lets and buy-to-let investments

2

Calculate income from all sources and identify taxable and non-taxable items

2.1 S Prepare computations of emoluments, including benefits in kind

2.2 S List non-savings, savings and dividend income checking for completeness

2.3 S Prepare schedules of income from land and property determining profits and losses

2.4 K Describe taxable and non taxable sources of income from employment, including benefits in kind

2.5 K Describe taxable and non-taxable savings income

3 Apply current legislation to calculate the tax payable on income

3.1 S Apply allowances that can be set against non–savings income

3.2 S Apply deductions and reliefs and claim loss set-offs

3.3 S Account for personal allowances

3.4 S Calculate income tax payable

3.5 S Describe taxation relief which can be given on income from employment including deductible (allowable) expenses, pension’s relief and charitable donations

3.6 S Describe types of relief which are available on property income including allowable expenses, wear and tear allowance, renewals allowance, loss relief – and the circumstances in which each apply

28

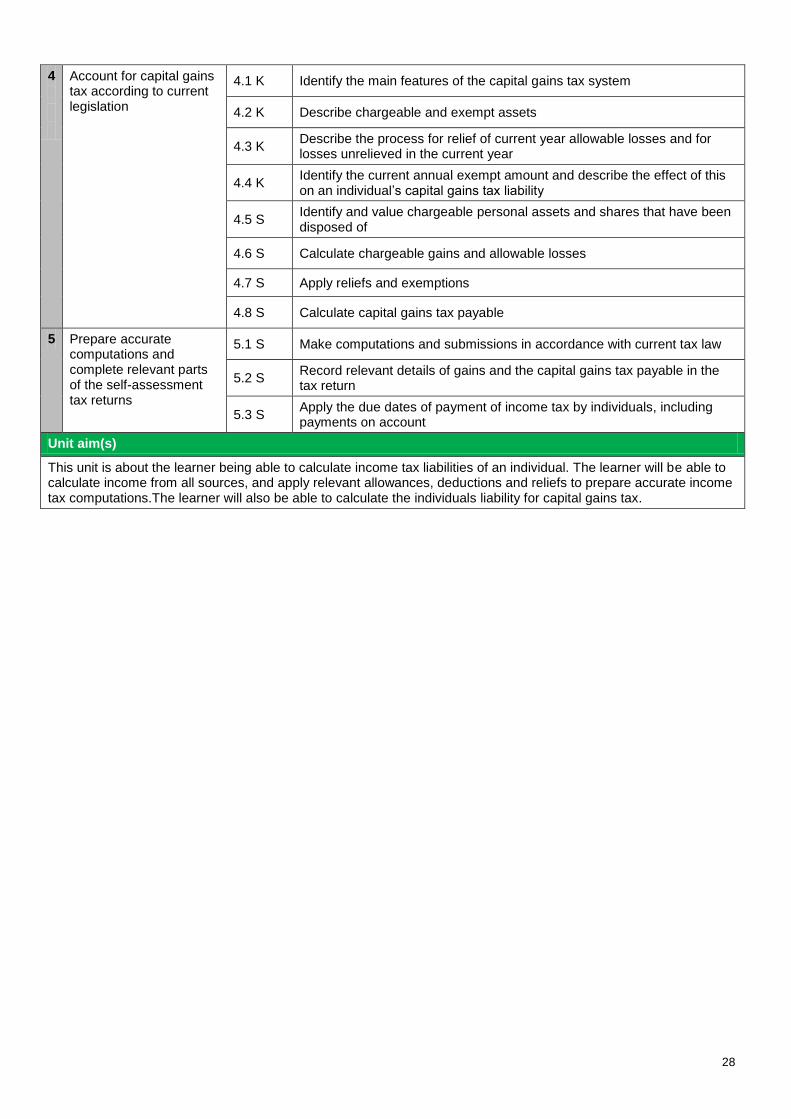

4

Account for capital gains tax according to current legislation

4.1 K Identify the main features of the capital gains tax system

4.2 K Describe chargeable and exempt assets

4.3 K Describe the process for relief of current year allowable losses and for losses unrelieved in the current year

4.4 K Identify the current annual exempt amount and describe the effect of this on an individual’s capital gains tax liability

4.5 S Identify and value chargeable personal assets and shares that have been disposed of

4.6 S Calculate chargeable gains and allowable losses

4.7 S Apply reliefs and exemptions

4.8 S Calculate capital gains tax payable

5 Prepare accurate computations and complete relevant parts of the self-assessment tax returns

5.1 S Make computations and submissions in accordance with current tax law

5.2 S Record relevant details of gains and the capital gains tax payable in the tax return

5.3 S Apply the due dates of payment of income tax by individuals, including payments on account

Unit aim(s)

This unit is about the learner being able to calculate income tax liabilities of an individual. The learner will be able to calculate income from all sources, and apply relevant allowances, deductions and reliefs to prepare accurate income tax computations.The learner will also be able to calculate the individuals liability for capital gains tax.

29

Title (and reference number) External auditing

Level 4 (Level 8 in Scotland)

Credit value 8 (4 knowledge and 4 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand the organisation’s systems and the external auditing procedures

1.1 K Describe the accounting systems relevant to the external audit

1.2 K Describe the features of an accounting system

1.3 K

Identify these principles of control and when they should be used:

separation of functions

authorisation

recording custody

vouching

verification

1.4 S Explain the concept of assurance and why an organisation needs to be audited

2 Plan an audit identifying areas to be verified and any associated risks

2.1 K Identify the accounting systems under review and accurately record them on appropriate working papers

2.2 K Identify the control framework

2.3 S Assess risks associated with the accounting system and its controls

2.4 S Record significant weaknesses in control

2.5 K Identify account balances to be verified and the associated risks

2.6 K

Explain these different sampling techniques selecting a sample for a specific situation:

confidence levels

random numbers

interval sampling

stratified sampling

2.7 K Explain tests of control and substantive procedures and their links to the audit objective

2.8 S Select or devise tests in accordance with the auditing principles and agree them with the audit supervisor

2.9 S Provide clear information and recommendations for the proposed audit plan for submission to the appropriate person for consideration

2.10 K

Describe these verification techniques and their uses:

physical examination

reperformance

third party confirmation

vouching

documentary evidence

identification of unusual items

2.11 K Explain the auditing techniques that could be used in an IT environment

2.12 K Explain how management feedback can be used when planning an audit

30

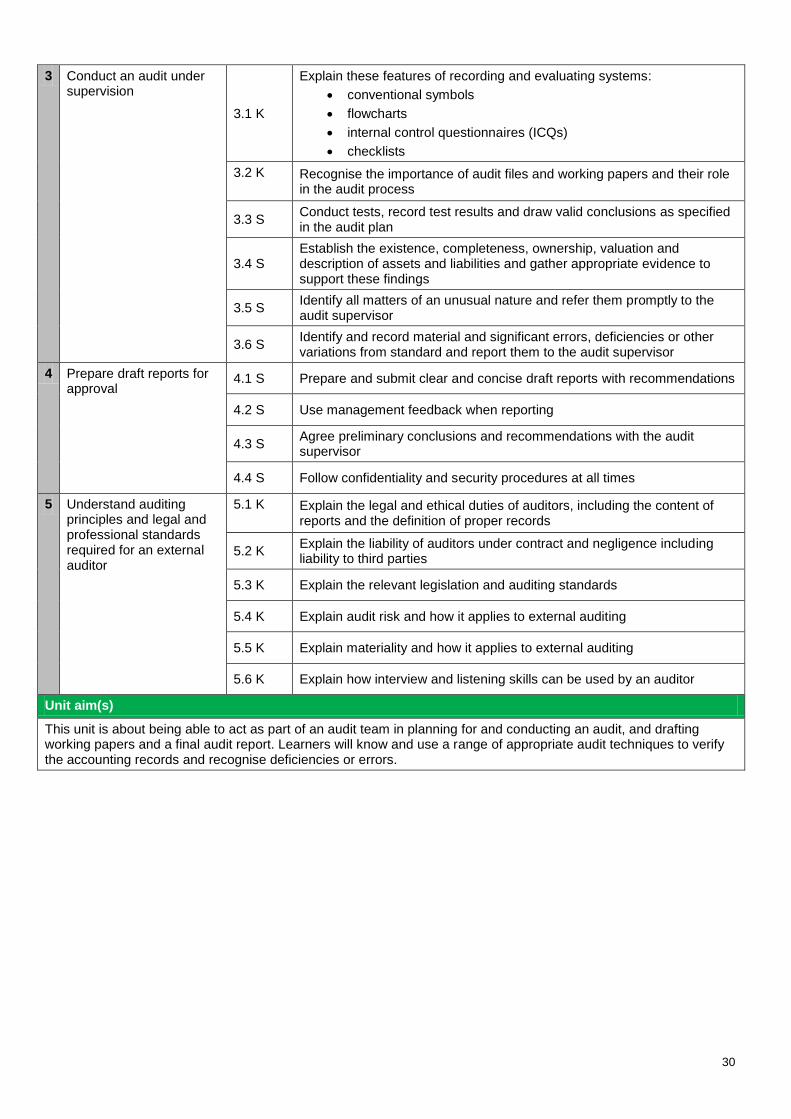

3 Conduct an audit under supervision

3.1 K

Explain these features of recording and evaluating systems:

conventional symbols

flowcharts

internal control questionnaires (ICQs)

checklists

3.2 K

Recognise the importance of audit files and working papers and their role in the audit process

3.3 S Conduct tests, record test results and draw valid conclusions as specified in the audit plan

3.4 S Establish the existence, completeness, ownership, valuation and description of assets and liabilities and gather appropriate evidence to support these findings

3.5 S Identify all matters of an unusual nature and refer them promptly to the audit supervisor

3.6 S Identify and record material and significant errors, deficiencies or other variations from standard and report them to the audit supervisor

4 Prepare draft reports for approval

4.1 S Prepare and submit clear and concise draft reports with recommendations

4.2 S Use management feedback when reporting

4.3 S Agree preliminary conclusions and recommendations with the audit supervisor

4.4 S Follow confidentiality and security procedures at all times

5 Understand auditing principles and legal and professional standards required for an external auditor

5.1 K

Explain the legal and ethical duties of auditors, including the content of reports and the definition of proper records

5.2 K Explain the liability of auditors under contract and negligence including liability to third parties

5.3 K Explain the relevant legislation and auditing standards

5.4 K Explain audit risk and how it applies to external auditing

5.5 K Explain materiality and how it applies to external auditing

5.6 K Explain how interview and listening skills can be used by an auditor

Unit aim(s)

This unit is about being able to act as part of an audit team in planning for and conducting an audit, and drafting working papers and a final audit report. Learners will know and use a range of appropriate audit techniques to verify the accounting records and recognise deficiencies or errors.

31

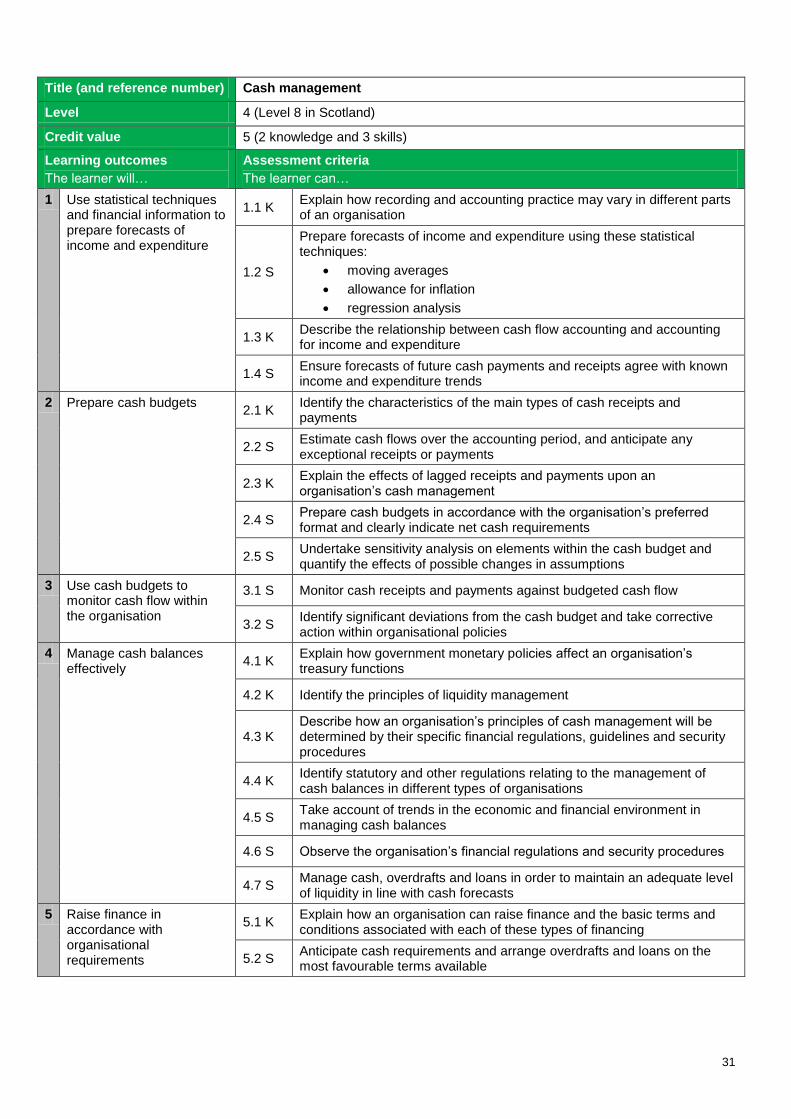

Title (and reference number) Cash management

Level 4 (Level 8 in Scotland)

Credit value 5 (2 knowledge and 3 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Use statistical techniques and financial information to prepare forecasts of income and expenditure

1.1 K Explain how recording and accounting practice may vary in different parts of an organisation

1.2 S

Prepare forecasts of income and expenditure using these statistical techniques:

moving averages

allowance for inflation

regression analysis

1.3 K Describe the relationship between cash flow accounting and accounting for income and expenditure

1.4 S Ensure forecasts of future cash payments and receipts agree with known income and expenditure trends

2 Prepare cash budgets 2.1 K

Identify the characteristics of the main types of cash receipts and payments

2.2 S Estimate cash flows over the accounting period, and anticipate any exceptional receipts or payments

2.3 K Explain the effects of lagged receipts and payments upon an organisation’s cash management

2.4 S Prepare cash budgets in accordance with the organisation’s preferred format and clearly indicate net cash requirements

2.5 S Undertake sensitivity analysis on elements within the cash budget and quantify the effects of possible changes in assumptions

3 Use cash budgets to monitor cash flow within the organisation

3.1 S Monitor cash receipts and payments against budgeted cash flow

3.2 S Identify significant deviations from the cash budget and take corrective action within organisational policies

4 Manage cash balances effectively

4.1 K Explain how government monetary policies affect an organisation’s treasury functions

4.2 K Identify the principles of liquidity management

4.3 K Describe how an organisation’s principles of cash management will be determined by their specific financial regulations, guidelines and security procedures

4.4 K Identify statutory and other regulations relating to the management of cash balances in different types of organisations

4.5 S Take account of trends in the economic and financial environment in managing cash balances

4.6 S Observe the organisation’s financial regulations and security procedures

4.7 S Manage cash, overdrafts and loans in order to maintain an adequate level of liquidity in line with cash forecasts

5 Raise finance in accordance with organisational requirements

5.1 K Explain how an organisation can raise finance and the basic terms and conditions associated with each of these types of financing

5.2 S Anticipate cash requirements and arrange overdrafts and loans on the most favourable terms available

32

6 Invest surplus funds observing organisational policies

6.1 S Assess different types of investment and the risks, terms and conditions associated with them

6.2 S Analyse ways to manage risk when investing, to minimise potential losses to the organisation

6.3 S Invest surplus funds according to organisational policy and within defined authorisation limits

Unit aim(s)

This unit is about managing cash balances to ensure the ongoing liquidity of an organisation. The learner will have the knowledge and skills to be able to make informed decisions regarding borrowing and investing surplus funds without affecting the day to day liquidity of the organisation. They will be able to prepare and use cash budgets to assist with the treasury function of the organisation.

33

Title (and reference number) Credit Control

Level 4 (Level 8 in Scotland)

Credit value 5 (2 knowledge and 3 skills)

Learning outcomes

The learner will…

Assessment criteria

The learner can…

1 Understand relevant legislation that impacts upon credit management

1.1 K Explain how the main features of contract law are applied in relation to the credit an organisation offers its customers

1.2 K Describe remedies for breach of contract

1.3 K Define the terms and conditions associated with contracts relating to the grant of credit

1.4 K Explain the importance of data protection legislation and its application to credit management

2 Use information from a variety of sources to grant credit to customers within organisational guidelines

2.1 K Identify sources of credit status and related information used to assess the risk of granting credit

2.2 K Explain methods of assessing credit control information

2.3 S Assess the current credit status of customers and potential customers

2.4 S Agree credit terms with new customers or changes to credit terms with existing customers

2.5 S Communicate tactfully the reasons for refusing or extending credit with customers

3 Use a range of techniques for the collection of debts

3.1 K Explain legal and administrative procedures for the collection of debts

3.2 K Evaluate a range of methods for the collection and management of debts

3.3 S Select debt recovery methods appropriate to individual outstanding debtors

3.4 S Explain the reasons for offering discounts for prompt payment and the effects on the organisation of offering such a discount

4 Monitor and control the supply of credit

4.1 K Explain the importance of liquidity management

4.2 K Explain the effect on organisations following bankruptcy or insolvency of credit customers

4.3 S Regularly analyse information relating to debtors’ accounts

4.4 S Negotiate the payment of outstanding debts in a courteous and professional manner and record the outcome

4.5 S Promptly send information regarding significant outstanding amounts and potential irrecoverable debts to relevant individuals within the organisation

4.6 S Make recommendations to write off irrecoverable debts and make provisions for doubtful debts based upon a realistic analysis of all known factors

Unit aim(s)

This unit is about applying the principles of credit management in an organisation. The learner will have the skills and knowledge to be able to assess the risk of offering credit to customers, monitor and control the collection of debts.