©2012 cliftonlarsonallen llp 1 111 construction tax update: breaking down the repair regulations...

TRANSCRIPT

©2012 CliftonLarsonAllen LLP1 111

©20

12 C

lifton

Lars

onAl

len

LLP

Construction Tax Update:Breaking down the Repair

Regulations and building up Tax Developments

December 4, 2012

©2012 CliftonLarsonAllen LLP2

Presenters

• John Dorn– Partner– Minneapolis, MN

• Jon Olson– Partner– Alexandria, MN

©2012 CliftonLarsonAllen LLP3

Learning Objectives

• Identify the criteria for determining whether an expenditure relating to tangible property is a deductible expense or must be capitalized.

• Identify the “unit of property” used for determining whether an expenditure is deductible or capitalized.

• Understand recent Federal income tax changes resulting from rulings, court cases, and Congressional action.

©2012 CliftonLarsonAllen LLP4

The Fight

• Determining the line for expenditures relating to tangible property between those required to be capitalized under Section 263(a) and those entitled to deduction under Section 162(a).

• Section 263(a) – requires capitalization of amounts paid for new property and improvements or betterments made to increase value of property.

• Section 162(a) – allows deduction for all ordinary and necessary business expenses.– Includes repairs (Treas. Reg. 1.162-4T)

©2012 CliftonLarsonAllen LLP5

Temporary and Proposed Regulations

• Latest of several sets of regulations issued under the two sections

• Issued December 23, 2011• Purpose – from the Preamble of TD 9564:

– “Clarify and expand the standards in the current regulations under sections 162(a) and 263(a) and provide certain bright-line tests for applying these standards.”

• IRS hopes to finalize “early” 2013

©2012 CliftonLarsonAllen LLP6

Clarity? Bright Lines?

• Most rules based on facts and circumstances• Rules “clarified” through examples

– Materials and supplies: 14 examples– De Minimis rules: 4 examples– Unit of Property: 19 examples

◊ Plus 6 more examples on improvement costs– Routine maintenance safe harbor: 10 examples– Betterments: 19 examples– Restorations: 26 examples– Acquired or produced property: 11 examples

◊ Plus 9 more on transaction costs and 3 more on defense of title

©2012 CliftonLarsonAllen LLP7

UNIT OF PROPERTY

©2012 CliftonLarsonAllen LLP8

Unit of Property

• General rule – All components of real or personal property that are functionally interdependent comprise a single Unit of Property (UOP).

• Components are functionally interdependent if the placing in service of one component is dependent on the placing in service of another component.

• However, component must be treated as separate UOP if:– Properly treated as within different class of property under

Section 168(e); or– Properly depreciated using different method.

©2012 CliftonLarsonAllen LLP9

Unit of Property--Building

• General rule – Each building and its structural components is a single UOP– Walls, partitions, floors, ceilings– Permanent coverings– Windows and doors

• However, for application of improvement rules to a building, “building systems” are now treated as separate UOPs from the building structure (roof, walls, windows, floors, ceilings)

• BIG change from the previous regulations!!

©2012 CliftonLarsonAllen LLP10

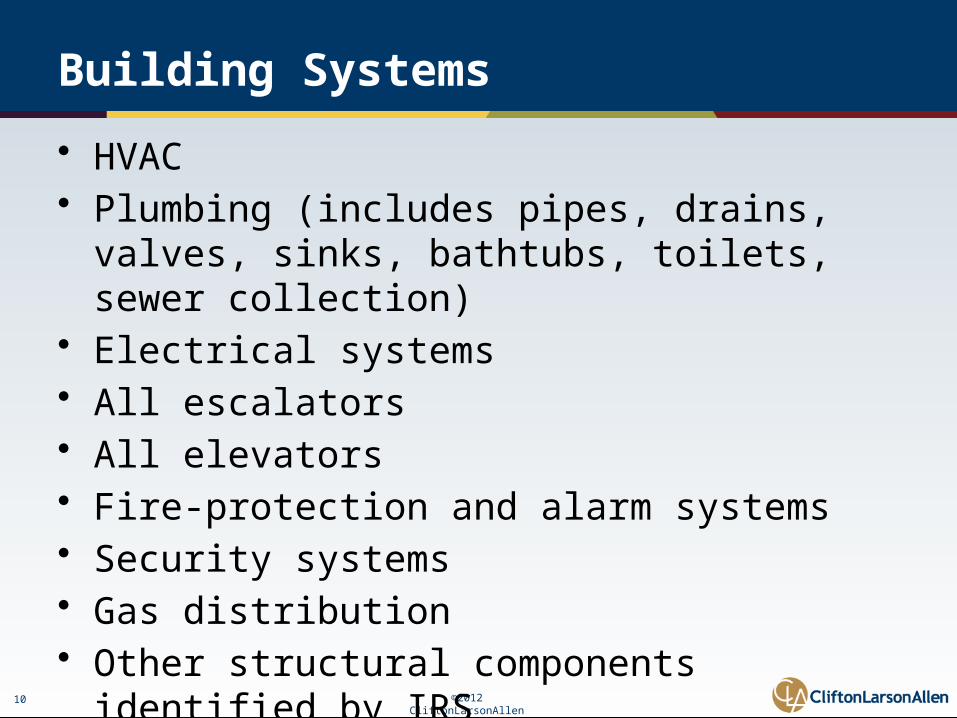

Building Systems

• HVAC• Plumbing (includes pipes, drains, valves, sinks,

bathtubs, toilets, sewer collection)• Electrical systems• All escalators• All elevators• Fire-protection and alarm systems• Security systems• Gas distribution• Other structural components identified by IRS

©2012 CliftonLarsonAllen LLP11

DEDUCTIBLE EXPENSES

©2012 CliftonLarsonAllen LLP12

Materials and Supplies

©2012 CliftonLarsonAllen LLP13

Materials and Supplies

• Incidental– No record of consumption– Deduct when purchased– Example: office supplies

• Non-incidental– Record of consumption is maintained– Not deductible until used or consumed

• Rotable and Temporary Spare Parts– Acquired for installation on a UOP– Default rule is to deduct when disposed of

©2012 CliftonLarsonAllen LLP14

Definition of Materials and Supplies

• Tangible personal property• Used or consumed in taxpayer’s operations• Not inventory• One of the following

– Component to maintain, repair or improve a UOP that itself is not a UOP

– Fuel, lubricants, water, similar items– UOP with economic life ≤ 12 months– UOP with cost ≤ $100, or– Other property identified by IRS as material or supply

©2012 CliftonLarsonAllen LLP15

Elect to Capitalize

• Incidental and non-incidental materials and supplies– May elect to capitalize materials and supplies– Election made by capitalizing and depreciating– Timely filed return for year placed in service

• Rotable and temporary spare parts– Capitalize and depreciate– Elect to deduct when first installed

◊ Capitalize FMV when removed plus cost of repairs◊ Deduct again when later installed◊ Lather, rinse and repeat until disposed of permanently

©2012 CliftonLarsonAllen LLP16

De Minimis Rule

©2012 CliftonLarsonAllen LLP17

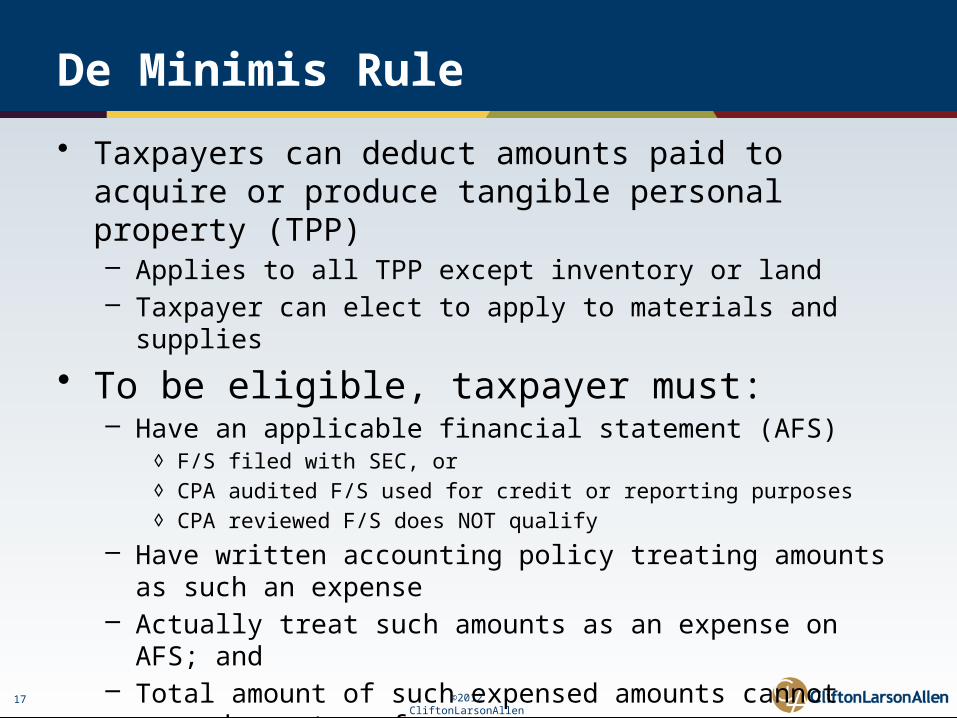

De Minimis Rule

• Taxpayers can deduct amounts paid to acquire or produce tangible personal property (TPP)– Applies to all TPP except inventory or land– Taxpayer can elect to apply to materials and supplies

• To be eligible, taxpayer must:– Have an applicable financial statement (AFS)

◊ F/S filed with SEC, or◊ CPA audited F/S used for credit or reporting purposes◊ CPA reviewed F/S does NOT qualify

– Have written accounting policy treating amounts as such an expense– Actually treat such amounts as an expense on AFS; and– Total amount of such expensed amounts cannot exceed greater of:

◊ 0.1% of gross receipts for tax purposes◊ 2% of depreciation and amortization on AFS

©2012 CliftonLarsonAllen LLP18

De Minimis Rule Election

• Made by deducting such amounts in the year paid• Timely filed return• May elect not to treat an otherwise eligible amount

so as to come under the 0.1% gross receipts or 2% of depreciation expense tests

©2012 CliftonLarsonAllen LLP19

De Minimis Rule – Preamble

• Rule is not intended to prevent a taxpayer from reaching an agreement with the IRS revenue agents that, as an administrative matter, based upon risk analysis or materiality, the agents will not review certain items.– Burden on taxpayer that treatment clearly reflects income

©2012 CliftonLarsonAllen LLP20

IRS Update on De Minimis Rule

• Recognition of administrative burden on some companies due to failure to track amounts which would be subject to de minimis limitations– Not much sympathy from IRS Office of Chief Counsel, in

that taxpayers previously were required to capitalize such costs

• One of the topics identified in Notice 2012-73– “may be revised in a manner that might affect, and in

certain cases simplify, taxpayers’ implementation of the rules when the regulations are issued in final form.”

©2012 CliftonLarsonAllen LLP21

Dispositions

©2012 CliftonLarsonAllen LLP22

Dispositions

• Occurs when ownership of an asset is transferred or when an asset is permanently withdrawn from use– Includes sale, retirement, physical abandonment of asset

• Disposition requires recognition of gain or loss• What is the “asset” disposed of?

– Cannot be larger than UOP– Structural components (including all components thereof)

of a building– Improvements or additions

• Does not include a component of personal property

©2012 CliftonLarsonAllen LLP23

Dispositions - Consequences

• Depreciation ends at time of asset’s disposition• If asset disposed of is component of larger asset:

– Must reduce basis and depreciation reserve of larger asset by amount of basis and reserve allocated to component

– Allocate basis to component using any reasonable method• Gain or loss must be recognized

©2012 CliftonLarsonAllen LLP24

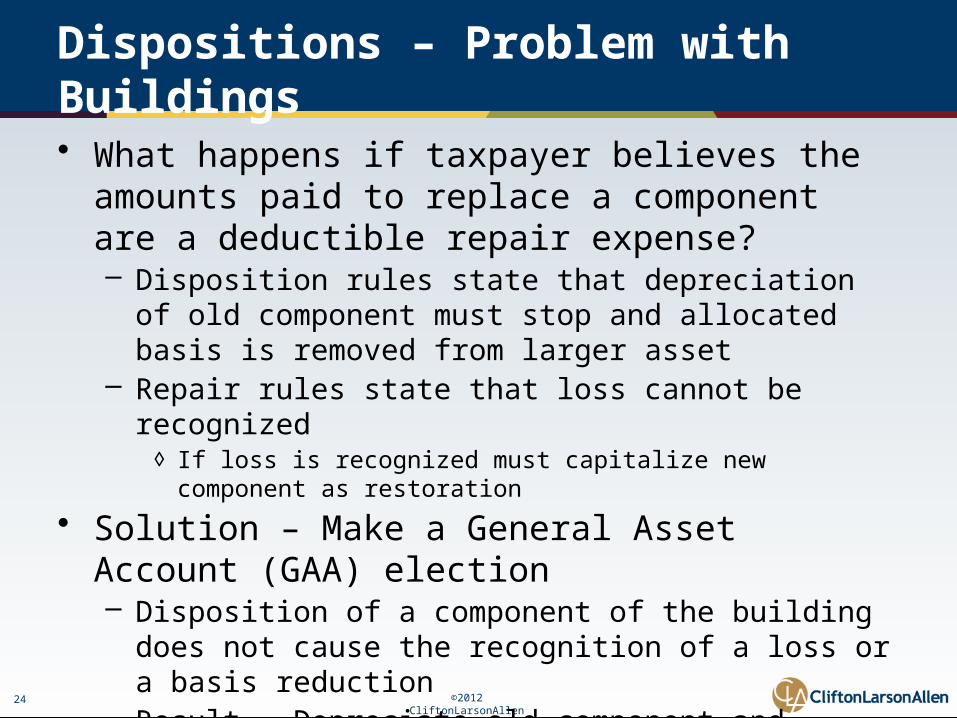

Dispositions – Problem with Buildings

• What happens if taxpayer believes the amounts paid to replace a component are a deductible repair expense?– Disposition rules state that depreciation of old component must

stop and allocated basis is removed from larger asset– Repair rules state that loss cannot be recognized

◊ If loss is recognized must capitalize new component as restoration

• Solution – Make a General Asset Account (GAA) election – Disposition of a component of the building does not cause the

recognition of a loss or a basis reduction– Result – Depreciate old component and deduct new component– Regulations also provide flexibility to elect out of GAA when

taxpayer wants to recognize loss on disposition◊ When “repair” must be capitalized as an improvement

©2012 CliftonLarsonAllen LLP25

IRS Update on Dispositions

• One of the topics identified in Notice 2012-73– May be revised and simplified

• IRS possibly making current GAA treatment for buildings the default treatment for buildings.– Not wanting a 3115 from every taxpayer that owns a

building in a trade or business.

©2012 CliftonLarsonAllen LLP26

DEDUCTIBLE REPAIRS

©2012 CliftonLarsonAllen LLP27

Repairs

• General rule – Taxpayer can deduct amounts not otherwise required to be capitalized.

• Routine maintenance safe harbor– Inspection, cleaning, testing, replacing of parts with

comparable parts of a UOP– Taxpayer reasonably expects such activities will be

performed more than once during the asset’s class life– Includes such activities even when performed after the

expiration of the asset’s class life– Caution: safe harbor no longer applies to buildings or

structural components of buildings– Also a topic identified in Notice 2012-73

◊ Revised? Simplified?

©2012 CliftonLarsonAllen LLP28

CAPITAL EXPENDITURES

©2012 CliftonLarsonAllen LLP29

Acquisitions

• General rule – Must capitalize amounts paid to acquire or produce real or personal property.

• General rule does not affect exceptions– Materials and supplies– De minimis rule

• Amounts paid to acquire or produce include:– Invoice price– Transaction costs– Costs incurred prior to UOP being placed in service– Defense or perfection of title

©2012 CliftonLarsonAllen LLP30

Betterments

©2012 CliftonLarsonAllen LLP31

Betterments

• Corrects a material condition or defect existing prior to acquisition or during the production of a UOP– Applies even if taxpayer was unaware of the condition or defect

• Results in a material addition to the UOP– Enlargement– Expansion– Extension

• Results in material increase in capacity, productivity, efficiency, strength, or quality of UOP or output.

• Buildings – An amount results in a betterment to the UOP if it results in a betterment to either the building structure or any of the nine building systems.

©2012 CliftonLarsonAllen LLP32

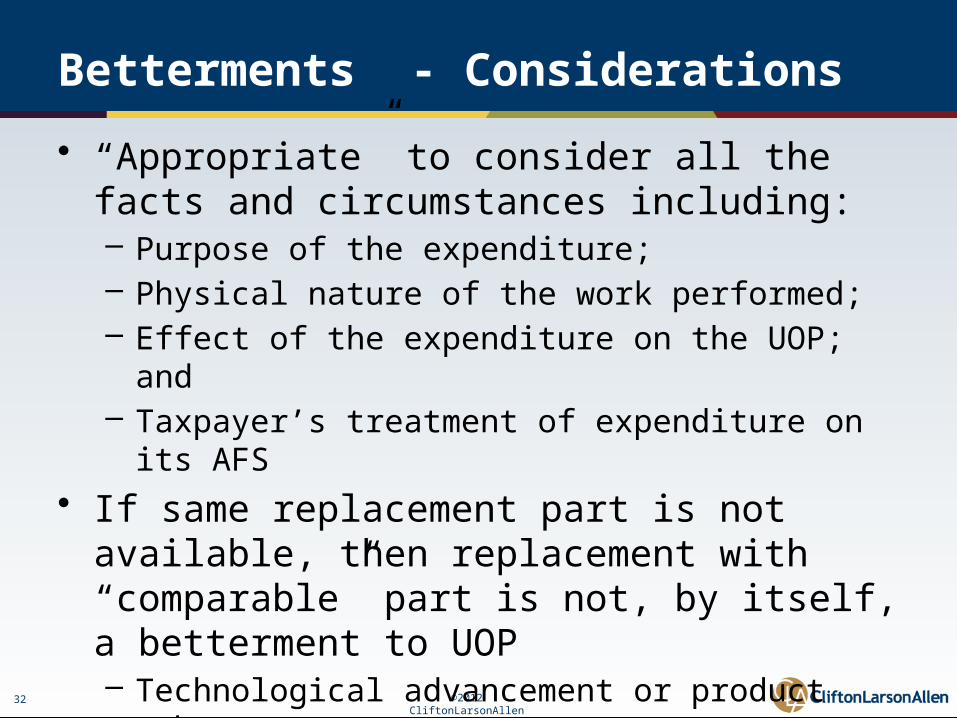

Betterments - Considerations

• “Appropriate” to consider all the facts and circumstances including:– Purpose of the expenditure;– Physical nature of the work performed;– Effect of the expenditure on the UOP; and – Taxpayer’s treatment of expenditure on its AFS

• If same replacement part is not available, then replacement with “comparable” part is not, by itself, a betterment to UOP– Technological advancement or product enhancements

©2012 CliftonLarsonAllen LLP33

Standard of Comparison

• Condition of property before and after expenditure– Compare to condition of property before particular event

necessitating expenditure◊ Example: storm damaging a roof

• Normal wear and tear excepted• Take into account condition of property when placed

in service by taxpayer

©2012 CliftonLarsonAllen LLP34

Restorations

©2012 CliftonLarsonAllen LLP35

Restorations

• An amount paid restores a UOP if it:– Replaces a component of a UOP and taxpayer recognized gain or

loss on old component (disposition)– Repairs damage to a UOP for which taxpayer has taken casualty

loss– Returns UOP to ordinary operating condition after deteriorating

to state where it is no longer functional– Rebuilds UOP to like-new condition after end of class life– Replaces a major component or substantial structural part of

the UOP• Buildings – An amount results in a restoration to the

UOP if it results in a restoration to either the building structure or any of the nine building systems.

©2012 CliftonLarsonAllen LLP36

Restorations (cont.)

• “Major component” or a “substantial structural part”– Must consider all the facts and circumstances including the

quantitative or qualitative significance of the part or combination of parts in relation to the UOP

– Includes a part or combination of parts that: ◊ Comprise a large portion of the physical structure of UOP; or◊ Perform a discrete and critical function in the operation of UOP

• Replacement of a minor component – Even if it affects the function of the UOP, is not supposed

to constitute a major component or substantial structural part (i.e., require capitalization).

©2012 CliftonLarsonAllen LLP37

Adaptations

©2012 CliftonLarsonAllen LLP38

Adaptations

• An amount paid adapts a UOP to a new or different use if the adaptation is not consistent with the taxpayer’s intended use of the property at the time the property was originally placed in service.

• For buildings, the analysis applied to the building structure and each of the nine building systems.

©2012 CliftonLarsonAllen LLP39

IMPLEMENTATION

©2012 CliftonLarsonAllen LLP40

Effective Dates

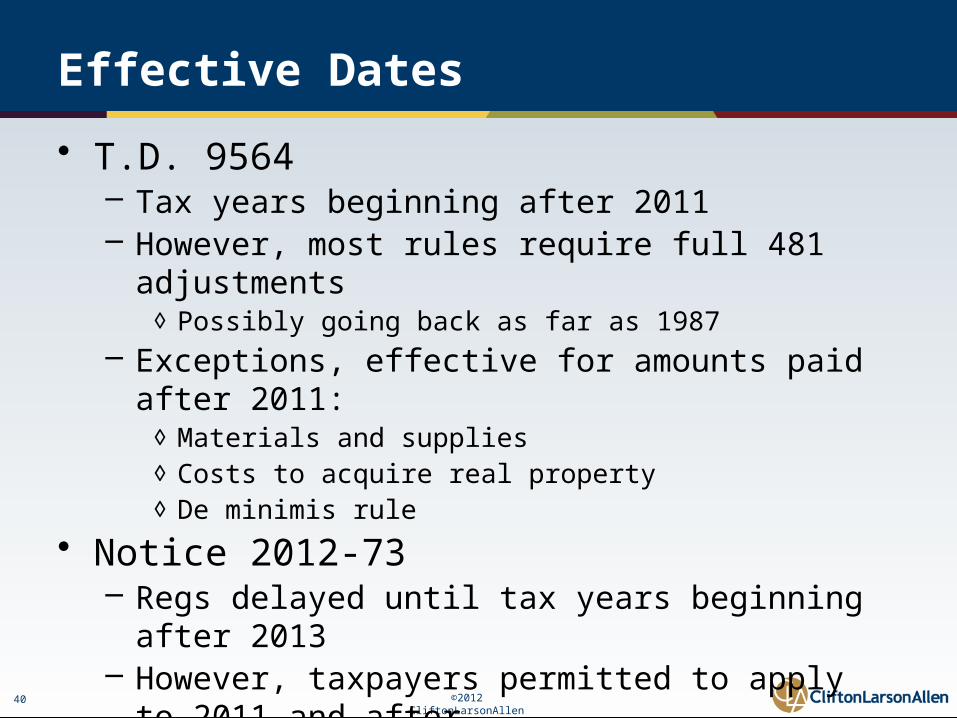

• T.D. 9564– Tax years beginning after 2011– However, most rules require full 481 adjustments

◊ Possibly going back as far as 1987– Exceptions, effective for amounts paid after 2011:

◊ Materials and supplies◊ Costs to acquire real property◊ De minimis rule

• Notice 2012-73– Regs delayed until tax years beginning after 2013– However, taxpayers permitted to apply to 2011 and after– Notified taxpayers of expected changes to de minimis rule,

dispositions, and routine maintenance safe harbor.

©2012 CliftonLarsonAllen LLP41

Changes in Accounting Method

• Accounting method changes – Section 481 adjustment

◊ Positive changes spread over 4 years◊ Negative changes recognized in year of change

– Always open to IRS adjustment– Filing method change provides audit protection

◊ And spreads positive changes over 4 years– Conclusion – File necessary method changes to be

compliant with the new regs! • Guidance arrived March 7, 2012

– Rev. Proc. 2012-19 for materials and supplies, repairs– Rev. Proc. 2012-20 for depreciation changes– New Form 3115 codes for automatic consents (162-180)

©2012 CliftonLarsonAllen LLP42424242

©20

12 C

lifton

Lars

onAl

len

LLP

2012 Federal Income Tax Update

©2012 CliftonLarsonAllen LLP43

Domestic Production Activities Deduction

• Regs allow Section 199 deduction for activities to erect or substantially renovate real property.

• Tax Court allows bridge and road renovation as eligible for Section 199 (Gibson & Assoc.)

©2012 CliftonLarsonAllen LLP44

Gibson & Assoc.

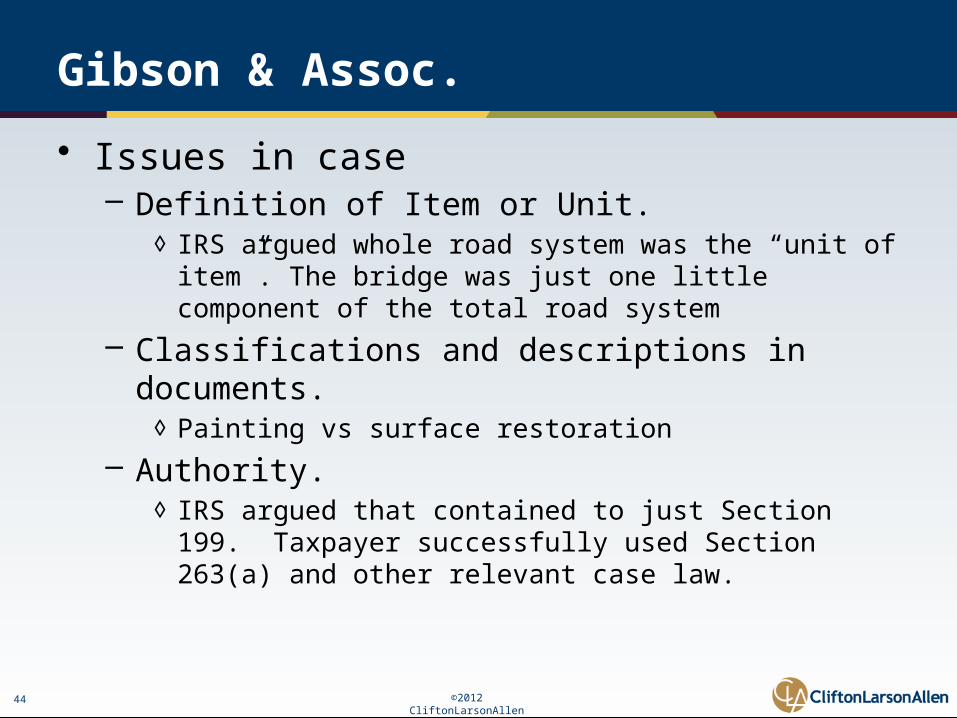

• Issues in case– Definition of Item or Unit.

◊ IRS argued whole road system was the “unit of item”. The bridge was just one little component of the total road system

– Classifications and descriptions in documents.◊ Painting vs surface restoration

– Authority.◊ IRS argued that contained to just Section 199. Taxpayer

successfully used Section 263(a) and other relevant case law.

©2012 CliftonLarsonAllen LLP45

15

Investment Income Tax in 2013

• 3.8% surtax on net investment income of individuals effective in 2013, computed as the lesser of:– Net investment income, or– Excess of modified AGI over $200K single/$250K jt.– Example

• Definition of net investment income– Interest, div., annuities, royalties, rents– Passive business income and trading– Gains from property (except active business)

©2012 CliftonLarsonAllen LLP46

18

• Present employee FICA payroll tax: 6.2% OASDI on first $110,100; 1.45% Medicare tax on all earnings

• Effective in 2013, Medicare tax up .9% to 2.35% on higher income earners [IRC Sec. 3101(b)(2)]:– Single earned income over $200,000– Joint earned income over $250,000– Assessed on employee share only, but employer withholds– If W/H inadequate, remit in 1040– Income tax deduction for ½ SE tax remains the same

High Earner Medicare Tax

©2012 CliftonLarsonAllen LLP47

19

Accrual of Bonuses

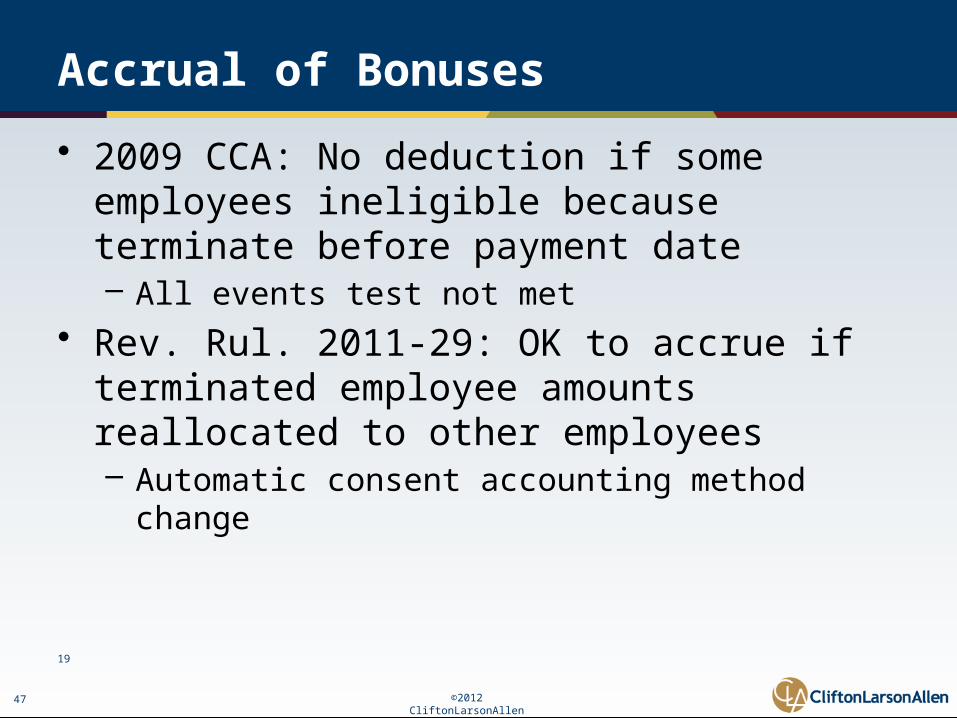

• 2009 CCA: No deduction if some employees ineligible because terminate before payment date– All events test not met

• Rev. Rul. 2011-29: OK to accrue if terminated employee amounts reallocated to other employees– Automatic consent accounting method change

©2012 CliftonLarsonAllen LLP48

Section 179 Provisions

Sec. 179 Asset Addn.Tax yr. beginning in Limit Phase-out Range

2009 $250,000 $800K - $1.05M2010 $500,000 $2M - $2.5M2011 $500,000 $2M - $2.5M2012 $139,000 $560K - $699K2013 $25,000 $200K - $225K

©2012 CliftonLarsonAllen LLP49

28

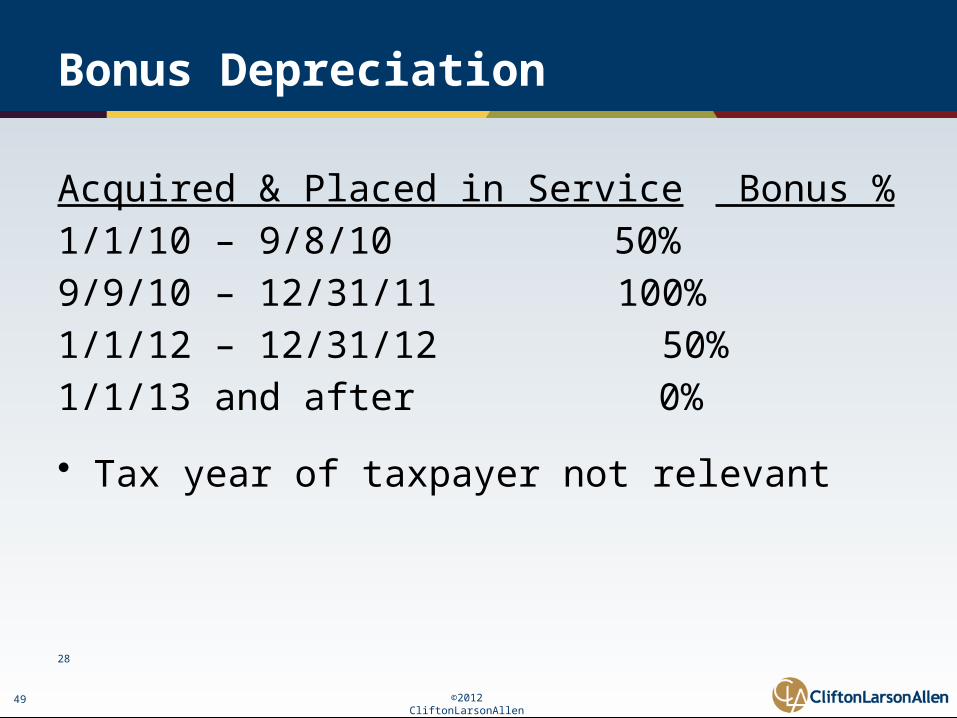

Bonus Depreciation

Acquired & Placed in Service Bonus %1/1/10 – 9/8/10 50%9/9/10 – 12/31/11 100%1/1/12 – 12/31/12 50%1/1/13 and after 0%

• Tax year of taxpayer not relevant

©2012 CliftonLarsonAllen LLP50

29

Bonus Depreciation

• Overview of eligibility– Original use with taxpayer (i.e., new not used)– Qualified property (< 20 yr. recovery period)– Acquired & placed in service in eligible period

• Ordering: Sec. 179 first; 50% bonus second

©2012 CliftonLarsonAllen LLP51

35

• WOTC generally 40% of first $6,000 of wages = $2,400 credit

• An extender: Expired 12-31-11• Certification: Prescreening notice (Form 8850) within

28 days of employment• Veteran-hire WOTC extended thru 2012

– Expanded categories and credit amts. if hired after 11-21-11

WOTC Veteran Hires

©2012 CliftonLarsonAllen LLP52

36

Maximum credit: Qual. Vet. category Old New1. Food stamp family $2,400 $2,4002. Disabled and - w/in 1 yr. of active duty $4,800 $4,800 - unempl. >6 mo. of last 12 $4,800 $9,6003. Unempl. >4 wks. prior 12 mo. -

$2,4004. Unempl. >6 mo. prior 12 mo. - $5,600

WOTC for Hiring Qualified Veterans

©2012 CliftonLarsonAllen LLP53

37

• Veteran: > 180 days active duty– 4 of 5 categories do not require recent active duty

• Tax-exempt employers: Credit allowed, limited to employer’s 6.2% Soc. Sec. tax on all employees for 12 mos. after hire– Credit at 26%, not 40% of wages– Lower maximums (65% of for-profit)

WOTC for Hiring Qualified Veterans

©2012 CliftonLarsonAllen LLP54

Questions?

©2012 CliftonLarsonAllen LLP55555555

©20

12 C

lifton

Lars

onAl

len

LLP

Thank You