2011 p&sp annual report - grain inspection, packers ... · pdf file2011 packers and...

TRANSCRIPT

2011 P&SP Annual Report

Packers & Stockyards Program

United States Department of Agriculture Grain Inspection, Packers and Stockyards Administration

Our Mission: “To protect fair trade practices, financial integrity, and competitive markets for livestock, meat, and poultry.”

March 2012

2011 Packers and Stockyards Annual Report

i

EXECUTIVE SUMMARY

Overview—The Packers and Stockyards Program (P&SP) operates under the authority of the Packers and Stockyards Act (P&S Act). P&SP is administered by a Deputy Administrator, who reports to the Administrator of the Grain Inspection, Packers and Stockyards Administration (GIPSA) of the U.S. Department of Agriculture (USDA). The Deputy Administrator provides leadership to five program directors—two in the Washington, D.C., headquarters and three in regional offices located in Atlanta, Georgia; Aurora, Colorado; and Des Moines, Iowa.

Each regional office director manages a Business Practices Unit, a Financial Unit, and two Resident Agent Units, which enforce the P&S Act through regulatory actions and investigations. The director also oversees the administrative Program Support Unit, and the Western Regional Office director oversees the Central Reporting Unit, which processes industry entities’ annual reports filed with P&SP.

Unit Level Activities—To ensure compliance with the P&S Act, P&SP agents conduct two broad types of activities: investigative and regulatory. Investigations are carried out when a violation of the Act appears to be occurring. Regulatory activities are monitoring activities to determine if a regulated entity is complying with the P&S Act and result in correction of identified deficiencies.

Program Management—P&SP measures its overall performance by annually measuring the regulated entities’ compliance with the P&S Act. The performance measure encompasses activities P&SP conducts that directly or indirectly influence industry compliance. In 2011, P&SP maintained industry compliance at 76 percent. P&SP measures its efficiency at achieving industry compliance by the number of days it takes to complete the investigative phase (the time from complaint until a decision is made whether to refer the case to the Office of General Counsel (OGC) or the Department of Justice (DOJ) for possible enforcement action) of investigations. The time increased from 98 days in 2010 to 104 days for investigations closed in 2011, including investigative time spent on cases eventually referred to USDA’s OGC and DOJ.

Industry Assessment—P&SP completed the annual assessment of the industries regulated under the P&S Act, which is based on data from the annual reports filed by regulated firms covering the firms’ 2010 fiscal year.

2011 Packers and Stockyards Annual Report

1

CONTENTS

EXECUTIVE SUMMARY i CONTENTS 1 1. OVERVIEW OF THE PACKERS AND STOCKYARDS PROGRAM 2

1.1 Authorities and Responsibilities 2 1.2 Packers and Stockyards Program’s Business Organization 3

2. PACKERS AND STOCKYARDS PROGRAM UNIT-LEVEL ACTIVITIES 7 2.1 Enforcing Business Practice Provisions 9 2.1.1 Competition ............................................................................................... …………..9 2.1.2 Trade Practices ....................................................................................................... 12 2.2 Enforcing Financial Provisions 13

3. PACKERS AND STOCKYARDS PROGRAM MANAGEMENT 18 3.1 Performance and Efficiency Measurement 18 3.1.2 Performance ............................................................................................................ 18 3.1.3 Efficiency ................................................................................................................. 20 3.2 Management Initiatives 24 3.2.1 Custodial Account Special Report .......................................................................... 24 3.2.2 Scale Test Standard Operating Procedures ............................................................ 24 3.2.3 P&SP’s Change Control Working Group (CCWG) ............................................... 25

4. ASSESSMENT OF THE INDUSTRIES 26 4.1 General Economic State of the Industry 28 4.1.1 Cattle—General Economic State of the Industry .................................................... 32 4.1.2 Hogs—General Economic State of the Industry ..................................................... 34 4.1.3 Sheep—General Economic State of the Industry .................................................... 36 4.1.4 Poultry—General Economic State of the Industry .................................................. 38 4.2 Changing Business Practices. 39 4.2.1 Cattle—Changing Business Practices .................................................................... 40 4.2.2 Hogs—Changing Business Practices ...................................................................... 45 4.2.3 Sheep—Changing Business Practices ..................................................................... 48 4.2.4 Poultry—Changing Business Practices .................................................................. 51 4.3 Industry Concerns 53

5. STATUTORY TEXT COMMISSIONING REPORT 55

2

1. OVERVIEW OF THE PACKERS AND STOCKYARDS PROGRAM

This section provides a brief overview of the Packers and Stockyards Program’s (P&SP) authority and responsibilities under the Packers and Stockyards Act of 1921 (P&S Act), P&SP’s position within the organizational structure of the USDA, and P&SP’s own internal organization.

1.1 Authorities and Responsibilities

Under the P&S Act, the Secretary of Agriculture (Secretary) has authority over businesses engaged in the marketing of livestock, wholesale meat, and poultry. The Secretary has delegated this authority to the Packers and Stockyards Program for regulation and enforcement. Regulated business entities include livestock market agencies (which include auction markets), livestock dealers, stockyards, packers, swine contractors, and live poultry dealers (this includes most poultry slaughterers or “poultry integrators”). These businesses assemble and process livestock and poultry, and move their products through the first manufacturing, or meatpacking, phases of the livestock and poultry marketing channel. Livestock producers, feedlots, and poultry growers at the originating or upstream ends of the market channels and most retailers at the opposite downstream end of the market channel are not under P&SP’s jurisdiction.

The P&S Act prohibits unfair, unjustly discriminatory, and deceptive practices. It also prohibits regulated businesses from engaging in specific anti-competitive practices.

In addition to describing unlawful behavior, the P&S Act mandates certain business practices by regulated industries. For example, market agencies and dealers must be registered; market agencies, packers (except those whose average annual livestock purchases do not exceed $500,000), and dealers must be bonded to protect livestock sellers; and buyers must make prompt payment for livestock. To protect unpaid cash sellers of livestock, packers are also subject to trust provisions that require that livestock inventories and receivables or proceeds from meat, meat food products, or livestock products be held in trust for unpaid cash sellers until payment is made in full. A similar provision applies to live poultry dealers.

P&SP uses its statutory authority to investigate alleged violations of the P&S Act and regulations, and prosecutes violations identified through those investigations in administrative actions prosecuted by USDA’s Office of the General Counsel or through referrals to the Department of Justice (DOJ).

Under the Food Security Act of 1985, States may establish central filing systems to pre-notify buyers, commission merchants, and selling agents about security interests against farm products. P&SP administers the section of the statute commonly referred to as the “Clear Title” provision by certifying the filing systems of States that apply to P&SP for certification. P&SP does not have authority to de-certify States unless a State requests such decertification, and it does not have the authority to determine if States are maintaining certification standards.

2011 Packers and Stockyards Annual Report

3

1.2 Packers and Stockyards Program’s Business Organization

The Packers and Stockyards Program is administered by a Deputy Administrator, who reports to the Administrator of the Grain Inspection, Packers and Stockyards Administration (GIPSA). In addition to the P&SP, the GIPSA Administrator oversees the Federal Grain Inspection Service (FGIS). Within the USDA, the GIPSA Administrator reports to the Under Secretary for Marketing and Regulatory Programs (Figure 1). P&SP’s appropriated budget for 2011 was $22.4 million compared to $23.7 million in 2010.

Figure 1. GIPSA Administration Organizational Structure

The Deputy Administrator of the P&SP provides strategic leadership to five program directors— two at headquarters in Washington D.C., and three in regional offices: the Eastern Regional Office in Atlanta, Georgia; the Western Regional Office in Aurora, Colorado; and the Midwestern Regional Office in Des Moines, Iowa (Figure 2). As of October 2011, P&SP had 162 full-time staff.

Each regional director manages an administrative Program Support Unit and four program units: a Business Practices Unit, a Financial Unit, and two Resident Agent Units. The units are organized based on responsibilities under the P&S Act and are designed to capitalize on the tactical advantages of placing staff in the field. Each unit is comprised of 5 to 10 staff members. Each unit has a supervisor who reports to the Regional Director. Staff members supervised in the regional offices are responsible for conducting investigations and regulatory activities such as business audits, weighing verifications, and day-to-day industry monitoring. These activities are described in greater detail in the next section.

4

Each regional office maintains expertise in one or more species of livestock or in poultry. The Eastern Regional Office focuses on poultry, the Midwestern Office on hogs, and the Western Regional Office on cattle and sheep. Fifty resident agents, who report to the regional offices, are located throughout the country to provide core services nationwide (Figure 2). The geographically dispersed resident agents enable P&SP to maintain close contact with the entities that it regulates, which are similarly dispersed throughout the United States (Figures 3 through 5).

Figure 2. P&SP Regional Offices and Resident Agent and Auditor Locations

2011 Packers and Stockyards Annual Report

5

Figure 3. Headquarters Location of Livestock Packers Subject to the P&S Act

Figure 4. Location of Livestock Markets and Firms Selling on Commission Subject to the P&S Act

6

Figure 5. Location of Livestock Dealers Subject to the P&S Act

Figure 6. Headquarters Location of Live Poultry Dealers Subject to the P&S Act

2011 Packers and Stockyards Annual Report

7

2. PACKERS AND STOCKYARDS PROGRAM UNIT-LEVEL ACTIVITIES

P&SP conducts two broad types of activities at the unit level to enforce the P&S Act: investigative and regulatory. Investigations are conducted when there is reason to believe a violation of the P&S Act is occurring or has occurred. Regulatory activities are monitoring activities carried out to determine if a regulated entity is complying with the Act. Agency resident agents, staffed with marketing specialists located in the field, are the agency’s frontline staff who work daily with regulated entities as well as livestock producers and poultry growers. They are typically the first responders for complaints and because of their daily contact with the industry a source of primary market intelligence.

Besides conducting routine regulatory activities, because of their situational awareness the resident agents often are the initiators of more complex investigations and regulatory activities. Support to the resident agents is provided by the regional offices’ Business Practices or Financial units. The Business Practices units include legal specialists, economists, and marketing specialists who focus on competition and trade practice issues. The Financial units are staffed with auditors who investigate and undertake regulatory activities related to enforcing the financial requirements of the Act. Investigations at a firm level may be a follow-up to previously identified violations of the P&S Act. In other instances, investigations may be initiated in response to complaints from industry participants, possible violations found while conducting regulatory activities on a business’s premises, or possible violations found through other monitoring. Investigations may be conducted as rapid response actions to prevent irreparable harm to the regulated industries.

Members of the livestock and poultry industries and the public may report complaints at 1-800-998-3447 or by e-mail at [email protected]. Individuals or firms with complaints about the livestock and poultry industries also are encouraged to call the appropriate regional office to discuss their concerns, anonymously if desired. P&SP responds to all of these external contacts. P&SP also initiates investigations independently, for example, as a result of information obtained from monitoring industry behavior.

Regulatory activities include, but are not limited to, check-weighing; custodial account and prompt payment audits; procurement and marketing business practice reviews; registering market agencies, dealers, and packer buyers who operate subject to the P&S Act; assisting producers in filing bond and trust claims; analyzing trust and bond claims; and conducting orientations for new markets and new packers.

Regulatory activities also include market-level monitoring, which is generally conducted using data that are available in the public domain. Examples include, but are not limited to, monitoring fed cattle and hog prices and analyzing structural changes in the livestock, meat, and poultry industries. Monitoring activities have led to firm-level investigations. Regulatory activity may occur entirely or partially at an entity’s place of business or at a Regional Office.

8

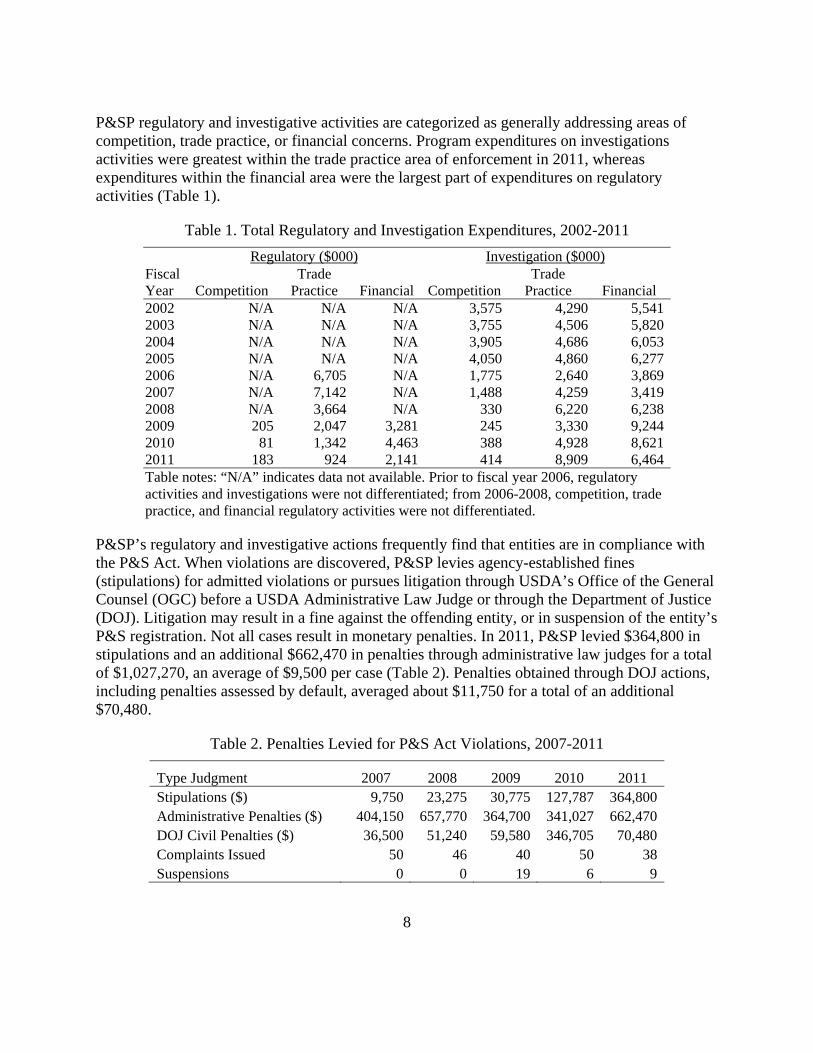

P&SP regulatory and investigative activities are categorized as generally addressing areas of competition, trade practice, or financial concerns. Program expenditures on investigations activities were greatest within the trade practice area of enforcement in 2011, whereas expenditures within the financial area were the largest part of expenditures on regulatory activities (Table 1).

Table 1. Total Regulatory and Investigation Expenditures, 2002-2011

Fiscal Year

Regulatory ($000) Investigation ($000)

Competition Trade

Practice Financial Competition Trade

Practice Financial 2002 N/A N/A N/A 3,575 4,290 5,5412003 N/A N/A N/A 3,755 4,506 5,8202004 N/A N/A N/A 3,905 4,686 6,0532005 N/A N/A N/A 4,050 4,860 6,2772006 N/A 6,705 N/A 1,775 2,640 3,8692007 N/A 7,142 N/A 1,488 4,259 3,4192008 N/A 3,664 N/A 330 6,220 6,2382009 205 2,047 3,281 245 3,330 9,2442010 81 1,342 4,463 388 4,928 8,6212011 183 924 2,141 414 8,909 6,464Table notes: “N/A” indicates data not available. Prior to fiscal year 2006, regulatory activities and investigations were not differentiated; from 2006-2008, competition, trade practice, and financial regulatory activities were not differentiated.

P&SP’s regulatory and investigative actions frequently find that entities are in compliance with the P&S Act. When violations are discovered, P&SP levies agency-established fines (stipulations) for admitted violations or pursues litigation through USDA’s Office of the General Counsel (OGC) before a USDA Administrative Law Judge or through the Department of Justice (DOJ). Litigation may result in a fine against the offending entity, or in suspension of the entity’s P&S registration. Not all cases result in monetary penalties. In 2011, P&SP levied $364,800 in stipulations and an additional $662,470 in penalties through administrative law judges for a total of $1,027,270, an average of $9,500 per case (Table 2). Penalties obtained through DOJ actions, including penalties assessed by default, averaged about $11,750 for a total of an additional $70,480.

Table 2. Penalties Levied for P&S Act Violations, 2007-2011

Type Judgment 2007 2008 2009 2010 2011 Stipulations ($) 9,750 23,275 30,775 127,787 364,800Administrative Penalties ($) 404,150 657,770 364,700 341,027 662,470DOJ Civil Penalties ($) 36,500 51,240 59,580 346,705 70,480Complaints Issued 50 46 40 50 38Suspensions 0 0 19 6 9

2011 Packers and Stockyards Annual Report

9

2.1 Enforcing Business Practice Provisions

The regional business practices units have responsibility for inspections and investigations of trade practice and competition provisions of the P&S Act. Supported by resident agents, the units conduct investigations of alleged anti-competitive practices and unfair and deceptive trade practices by market agencies, livestock dealers and order buyers, slaughtering packers, live poultry dealers, and meat dealers and brokers.

Economists and legal specialists in the units conduct competition investigations and regulatory activities. For example, an economist might monitor market and firm prices for indications of anti-competitive firm behavior. Marketing specialists conduct trade practice investigations and regulatory actions related to inaccurate weighing practices or carcass evaluation instruments and compliance with contracts. The competition and trade practice work conducted by these units is discussed in more detail below.

2.1.1 Competition

Investigations are a central activity of our competition program. P&SP investigates complaints alleging anti-competitive behavior such as attempted restriction of competition, failure to compete, buyers acting in concert to purchase livestock, apportionment of territory, price discrimination, price manipulation, and predatory pricing. P&SP’s economists, legal specialists, and investigative attorneys collaborate with USDA’s OGC on all competition investigations. When the results of an investigation indicate that the evidence and circumstances support legal action, P&SP formally refers the case file to OGC for action.

P&SP conducts many activities that monitor changes in industry behavior in order to understand the nature of and reasons for changes, and to anticipate potential competitive issues that may result from those changes. Details of specific, ongoing individual monitoring efforts are described in the next three sections.

2.1.1.1 Fed Cattle and Hog Market Price Monitoring

The current fed cattle and hog market price monitoring program was first implemented in 2004, but has since evolved into an enhanced program that includes a weekly internal reporting regime based on statistical models, one for the fed cattle markets and the other for hog markets. The statistical models rely on USDA’s Agricultural Marketing Service (AMS) publicly reported price data to assess regional price differences. If a statistically significant price difference is detected, P&SP initiates a regulatory review work plan to determine whether those price differences are caused by an undue or unreasonable preference or disadvantage in violation of section 202 (b) of the Act or by uncontrollable external factors, such as weather or other external macroeconomic conditions.

If the initial regulatory reviews of price differences do not clarify whether they were caused by external market factors, a field investigation is opened into the incident. The fed cattle price

10

monitoring program initiated 11 regulatory activities in 2011, none of which indicated cause for investigation (Table 3). P&SP continues to actively monitor market prices on a weekly basis and initiate timely regulatory reviews and investigations, if necessary, of observed market price anomalies.

Table 3. Regulatory Activities and Investigations Resulting From Statistical Monitoring of Fed Cattle Market Prices Weekly 2007 – 2011 and Hog Market

Prices Daily 2010 – 2011.

Fiscal Regulatory Activities Initiated Investigations Initiated Year Fed Cattle Hogs Fed Cattle Hogs 2007 13 - 0 - 2008 19 - 4 - 2009 25 - 3 - 2010 16 18 0 9 2011 11 19 0 17

The statistical model similar for daily monitoring of hog market prices includes the three AMS barrow and gilt price reporting areas. These AMS market areas include Iowa-Minnesota, the eastern Corn Belt, and the modified western Corn Belt. AMS includes Iowa and Minnesota in its market reports for the western Corn Belt region, but to ensure non-overlapping markets, P&SP modified the territory to remove the Iowa and Minnesota hog transactions and prices from this region. Live and carcass prices are monitored, except in the modified western Corn Belt market, which only reports carcass prices. 19 daily price outliers were detected by the model for these five market areas prices during fiscal year 2011, 17 of these outliers resulted in investigations being opened.

Whether P&SP is monitoring fed cattle or hog prices, when the statistical model reports an outlier, an economist from the Business and Economic Analysis Division in headquarters reviews the suspect price and makes a recommendation report, which is reviewed by an economist in the regional office. Based on the report and reviewer comments, the supervisor either closes the review or opens an investigation and requests individual firm transactions data from AMS.

2.1.1.2 Committed Procurement Review and Audit

P&SP monitors the use of “committed procurement” arrangements, which commit cattle and hogs to a packer more than 14 days prior to delivery. Each year, P&SP economists obtain fed-cattle and hog procurement data for the previous calendar year from the four largest beef packers and four largest hog packers. If the packers change their procurement arrangements with suppliers from previous years, P&SP also collects any new or modified written marketing agreements or contracts. P&SP economists review the contracts and, if necessary, discuss them with the packers to determine how the terms of the agreements relate to committed procurement categories of interest. Economists then classify, review, and tabulate the individual transactions

2011 Packers and Stockyards Annual Report

11

data and calculate the reliance of the top packers on committed procurement methods. Finally, P&SP economists reconcile the calculations based on the detailed transaction data on committed procurement as reported by the packers in their Packer Annual Reports.

If there are significant differences between the transaction data and the Packer Annual Report submissions on committed procurement, the economists contact the packers to identify the cause of the discrepancy. If necessary, P&SP meets with the packers in person to discuss the packers’ procurement methods and explain how they should be reported on the Packer Annual Report. These meetings foster a mutual understanding of the reporting requirements for committed procurement and more reliable reporting and calculation of the packers’ reliance on committed procurement methods.

Relying on written contracts and other information collected during the committed procurement reviews, P&SP agents analyze the various procurement and pricing methods used by hog and fed-cattle packers. Agents obtain and review contracts and agreements as necessary to determine if there have been any competition violations of the Act. The contracts are also used in procurement reviews of the packers to help determine if proper payment practices are being followed.

2.1.1.3 Poultry Contract Compliance Review Process

In FY 2011 P&SP conducted 49 poultry reviews, 31 of these reviews were based on a random sample. These reviews are based on standard operating procedures established in 2009 and are now included as a component of P&SP’s performance measure (see Performance and Efficiency Measurement section). Poultry contract reviews may be initiated based on industry intelligence or complaints in addition to those conducted based on random samples.

The standard operating procedure for conducting poultry contract reviews is electronically documented with links to Packers and Stockyards Automated System (PAS), the P&SP’s automated workflow software. P&SP agents follow these procedures when conducting poultry contract reviews. In general, the agent will collect relevant background information on the firm that is under review prior to conducting a site visit. Once on-site, the agent will conduct an interview and obtain copies of the grower contract being used at the plant location and 3 months of weekly ranking sheets for the contract. These documents are reviewed for consistency and adherence to P&S Act regulations. One week of payment data from the settlement sheet is selected as a random sample for a detailed review for accuracy and completeness. The results are compared to the firm’s ranking sheets, settlement sheets, and payments to the growers to ensure consistency with the contract. If discrepancies are found, an investigation is opened. If the firm’s practices are determined to be free of violation, the agent provides an exit interview indicating this to the firm’s management.

12

2.1.2 Trade Practices

Firms that furnish stockyard services in commerce are required to post a notice that informs the public that the stockyard meets the definition of a stockyard under the P&S Act. Once posted, the stockyard remains posted until it is de-posted through public notice. P&SP meets with new auction market owners and managers as the market begins operations to ensure that market operators understand their fiduciary responsibilities under the P&S Act.

These visits in the early stages of a market’s operation also provide important protection to livestock producers who rely on the market to provide a nondiscriminatory and competitive marketplace. Similarly, P&SP conducts orientations for hog and poultry growout contractors who operate feed mills to ensure they understand the regulatory requirements for feed weights used to calculate producer/grower payments.

P&SP reviews procurement practices to determine if unfair or deceptive trade activities are occurring in the procurement of livestock, meat, and poultry. The reviews assess pricing methods; payment practices; weighing of livestock, carcasses, and poultry; carcass grades used for payment; and accounting issued to sellers.

The P&S Act and regulations require markets, dealers, and packers to test scales at least semi-annually and file scale-test reports as evidence of scale maintenance. State or local government entities and private companies test scales. In addition, P&SP conducts several types of regulatory and investigative inspections to ensure scale operators and firms subject to the P&S Act are properly using their scales and properly recording weights in the purchase and sale of livestock and poultry (Table 4).

Table 4. Weighing Inspections and Violations, 2009-2011

Type 2009 2010 2011 Inspections Market 245 215 223 Dealer 41 61 132 Packer 18 5 35 Carcass 148 242 104 Poultry 74 74 70 Feed 63 74 62

Total 589 671 626 Violations Markets 15 23 33 Dealers 3 6 23 Packers 1 2 15 Carcass 25 30 17 Poultry 11 7 7 Feed 14 9 9

Total 69 77 104

2011 Packers and Stockyards Annual Report

13

These inspections include check weighing plus all other activities conducted by P&SP to ensure accurate weights of livestock, poultry, and poultry feed. Market, dealer, and packer inspections are conducted for scales weighing live animals. Carcass and poultry inspections are conducted on scales that weigh carcasses in slaughter plants, and feed inspections are conducted on scales at feed mills.

A transaction made on false or inaccurate weights, including instances in which a dealer modifies the actual weight of the livestock or fails to pass on a shrink allowance, is an unfair and deceptive practice. Anyone who believes that an action of a stockyard, market agency, or dealer caused personal loss or damage in violation of the P&S Act may file a complaint seeking reparation (damages) with P&SP within 90 days of learning of the action that caused damages. The Act does not provide for reparation complaints to be filed against packers, live poultry dealers, or swine contractors.

2.2 Enforcing Financial Provisions

P&SP’s financial units enforce the financial provisions of the P&S Act and regulations. These enforcement actions support the financial integrity and stability of the livestock, poultry, and meatpacking industries. Enforcement is carried out through reviews of annual and special reports, and onsite financial compliance reviews and investigations. Financial compliance reviews and investigations address solvency issues, payment to livestock sellers and poultry growers, bond claims, trust claims, and maintenance of custodial accounts. When P&SP identifies a potentially serious financial situation that may cause imminent and irreparable harm to livestock producers, rapid response teams are deployed immediately to conduct an investigation.

Under the P&S Act, most regulated entities must be solvent (current assets must exceed current liabilities). P&SP monitors the solvency of regulated entities by reviewing financial data in annual and special reports, and by onsite financial compliance reviews and investigations. P&SP notifies entities of their insolvencies and the immediate need to correct them. P&SP requires special reports from firms whose annual reports disclose insolvencies. In addition, P&SP conducts onsite financial investigations to ensure correction of reported insolvencies or other financial issues. Formal disciplinary action is initiated against firms when appropriate.

Market agencies selling livestock on commission (auction markets) must establish and maintain a bank account designated as a “custodial account for shipper’s proceeds” to hold proceeds from the sale of consigned livestock. The commission firm or auction market acts as a fiduciary depositor to the account, and the funds in the account are trust funds held for the benefit of livestock sellers. P&SP monitors custodial accounts by reviewing annual reports from market agencies, analyzing special custodial account reports, and conducting onsite custodial account audits. When the monitoring reveals shortages in the account, P&SP acts to have the account balance corrected (Table 5).

14

Table 5. Number of Market Reviews and Shortages Corrected Through On-Site Investigations, Fiscal Years 2002-2011

Year Reviews Under Funded

Accounts Corrections ($)

2002 206 97 2,814,439

2003 262 92 2,055,203

2004 272 94 2,144,986

2005 252 102 5,269,525

2006 347 140 7,256,052

2007 296 99 2,037,080

2008 176 62 5,022,966

2009 383 181 2,581,725

2010 297 79 3,402,608

2011 318 96 2,861,471

The P&S Act also establishes a statutory trust on certain assets of packers and live poultry dealers for the benefit of unpaid cash sellers of livestock and unpaid cash sellers or contract growers of live poultry grown for slaughter. Packer trust assets include all livestock purchased in cash sales, inventories, receivables, and proceeds from meat, meat food products, and livestock products derived from the purchase of livestock in cash sales. Poultry trust assets include all poultry obtained by live poultry dealers in cash poultry purchases or by poultry growing arrangements, inventories, receivables, or proceeds from such poultry or poultry products. Valid trust claims come before secured creditor claims in bankruptcy.

To be eligible for payment under the trust, a seller must file a claim with the packer or live poultry dealer and the Secretary within 30 days of the unpaid transaction. When a trust claim is filed, P&SP and OGC analyze the claim to assess whether it is timely and supported by adequate documentation. P&SP then makes the analysis available to the packer or live poultry dealer (the statutory trustee) and to trust claimants so that they can take any necessary action.

Additionally, all market agencies, dealers, and slaughtering packers purchasing over $500,000 of livestock annually are required to file and maintain bonds or bond equivalents for the protection of livestock sellers. To be eligible to receive payment under the bond, a seller (cash or credit) who does not receive payment for a transaction must file a bond claim within 60 days of the transaction. P&SP analyzes the claim to ensure it was filed within the timeline and supported by adequate documentation. P&SP provides its analysis to the principal and to the bond surety or trustee on a bond equivalent. In some instances the analysis is made available to all claimants to

2011 Packers and Stockyards Annual Report

15

facilitate joint legal action. In some cases, claims may be made against and paid by both bond and trust assets.

Bonding requirements usually do not cover the entire loss sustained when a firm fails financially. Further, livestock sellers do not always determine the current bond status of smaller packers, dealers, and market agencies before selling livestock to them, making those sellers vulnerable to insufficient bond protection if the smaller firms fail. A large packer’s failure may impact auction markets and dealers from whom it purchased livestock and failed to pay.

Since 2002, an average of 13 dealers failed each year, with a range of 1 to 31 failures per year. During that same time period, producers received an average 19 percent payment of amounts owed to them, with recovery ranging from 0 to 56 percent (Table 6).

Table 6. Total Dealer Financial Failures and Restitution, 2002-2011

Open Closed Restitution on Closed Cases

Year No. Owed ($) No. Owed ($) Bonds ($) Other ($) Return (%)

2002 NA NA 11 3,271,962 618,764 60,000 21

2003 NA NA 5 1,805,600 112,281 28,923 8

2004 NA NA 3 770,860 95,000 0 12

2005 NA NA 1 2,993,990 0 0 0

2006 NA NA 13 3,018,131 134,936 26,856 5

2007 NA NA 31 6,941,930 257,634 549,303 12

2008 NA NA 20 2,054,647 843,682 301,916 56

2009 NA NA 25 3,134,145 348,018 411,133 24

2010 2 NA 7 213,332 20,000 0 9

2011 6 23,632,101 14 878,620 407,105 4,479 47

Starting in 2010 entries show the number of firms that have claims open at year-end and those cases that have closed at year-end; for past years, only total number of failures is shown. Dollar amounts for all years are for failures with claims closed as of most recent year-end, so historical data may have been updated to reflect any settlements after the year the failure occurred. Although bond claims processing by P&SP is generally complete in the 2011 Eastern Livestock Market failure, it is being classified as open pending final outcome of proceedings in bankruptcy court.

Auction markets may be especially vulnerable to a domino effect from dealer failures since many dealers purchase livestock from auction markets. The failure of a large dealer may impact every auction market that it failed to pay. Since 2002, an average of 6 auction markets failed per year. Consignors received average restitution of 47 percent payment of amounts owed to them, with a range of 22 to 98 percent (Table 7). Starting in 2010 table entries show the number of firms that

16

have claims open at year-end and those cases that have closed at year-end; for past years, only total number of failures is shown. Dollar amounts for all years are for failures with claims closed as of most recent year-end, so historical data may have been updated to reflect any settlements after the year the failure occurred.

Table 7. Total Auction Market Financial Failures and Restitution, 2002-2011

Open Closed Restitution on Closed Cases

Year No. Owed ($) No. Owed ($) Bonds ($) Other ($) Return (%)

2002 NA NA 6 1,082,034 378,610 0 35

2003 NA NA 6 1,187,979 211,464 138,848 29

2004 NA NA 2 145,772 60,000 16,649 53

2005 NA NA 3 336,006 85,000 201,840 85

2006 NA NA 9 979,543 267,174 19,380 29

2007 NA NA 11 511,704 37,252 155,890 38

2008 NA NA 6 602,100 237,734 352,111 98

2009 NA NA 7 981,189 261,498 1,365 27

2010 1 NA 4 20,901 4,547 0 22

2011 0 0 4 158,279 0 89,586 57

To maximize recovery, bond claims filed against packers are normally paid after claims made against the packer trust are dispensed. On average, in any one year, 5 packers will suffer financial failures owing livestock sellers an average of $5,726,261 (Table 8).

Table 8. Total Packer Financial Failures, Bond Payout, and Payout From Other Sources, 2002-2011

Open Closed Restitution on Closed Cases Year No. Owed ($) No. Owed ($) Bonds ($) Other ($) Return (%)

2002 NA NA 3 17,007,170 6,394,489 5,838,750 72 2003 NA NA 3 2,508,633 225,952 1,238,772 58 2004 NA NA 3 2,056,869 142,752 369,507 25 2005 NA NA 1 5,032,018 55,000 1,977,761 40 2006 NA NA 13 755,550 35,267 683,834 95 2007 NA NA 31 4,118,456 40,000 4,083,946 100 2008 NA NA 20 3,498,895 0 1,588,620 45 2009 NA NA 25 15,676,349 196,208 9,999,228 65 2010 5 NA 7 5,960,684 748,435 3,825,518 77 2011 1 80,000 10 647,986 0 62,195 10

2011 Packers and Stockyards Annual Report

17

The bond payout for packers was, on average, $783,810 or 14 percent of the valid bond claims. Additional restitution from packer trust assets and other sources bring the average recovery to 59 percent of total amounts owed, with a standard deviation range of 30 to 89 percent.

As the livestock and meat industries evolve, P&SP continues to examine alternate ways to effectively regulate and monitor the industries and to effectively allocate its resources for planning and conducting regulatory compliance reviews. Most recently, P&SP adopted a statistical model to identify characteristics that place a livestock dealer, market, or packer at risk of financial failure. The characteristics identified are used, along with other firm information and market intelligence, to assess the need for financial audits.

18

3. PACKERS AND STOCKYARDS PROGRAM MANAGEMENT

The P&SP executes its management function through strategic, broad, multi-year goals and shorter term tactical annual objectives and activities. The next section addresses how P&SP improves its performance and efficiency, and the results P&SP is demonstrating.

3.1 Performance and Efficiency Measurement

P&SP measures its overall performance by annually measuring the regulated entities’ compliance with the P&S Act. The performance measure encompasses activities P&SP conducts that directly or indirectly influence industry compliance. P&SP calculates the percent of industry entities in compliance using random samples designed to provide an estimate of compliance with a 90-percent confidence level. In 2011, P&SP maintained industry compliance at 76 percent.

P&SP measures its efficiency at achieving industry compliance by the number of days it takes to complete the investigative phase (the time from complaint until the investigation is closed by P&SP or a decision is made whether to refer the case to OGC or DOJ for possible enforcement action) of investigations. The time increased from 98 days in 2010 to 104 days for investigations closed in 2011. The time to conduct the investigative phase is only one measurement in the complex process of conducting an investigation. Additional information about efficiency measures follows the performance section.

3.1.2 Performance

P&SP’s overall performance rate is a composite index of five program wide audit and inspection activities based on a scientifically-drawn random sample of subject entities. Note that this sampling approach provides estimates of industry-wide compliance among all subject entities, which will generally differ from simple ratios of number of violations found to number of entities investigated or inspected as illustrated in some previous tables in this report.

In 2011 the index included: 1) the financial components of the poultry contract compliance; 2) financial reviews of custodial accounts; 3) financial reviews of prompt payments of a random sample of firms; 4) inspection of scales and weighing practices at markets, dealers, and poultry integrators, and 5) inspection of all carcass evaluation devices and carcass evaluation practices for packing plants purchasing more than 1,000 head per year.

The sampling process is designed to yield 90-percent confidence for the estimated population compliance. The compliance rate declined to 76 percent last year after remaining steady for the last 3 prior reporting years at 80 percent (Figure 7).

2011 Packers and Stockyards Annual Report

19

Figure 7. Aggregated Industry Compliance 2008-2011

Financial reviews are conducted and overseen by P&SP staff auditors and supervisors, many of whom are licensed Certified Public Accountants. The reviews are carried out in accordance with general accounting standards. Business practice inspections of scales and weighing practices are conducted based on standards established by the National Institute of Standards and Technology and supervised by staff trained in inspection procedures.

P&SP validates reviews and inspections through internal compliance reviews, which were designed in conjunction with a private consultant, and adhere to the P&SP Standard Operating Procedures manual published on an internal GIPSA Web page.

While additional focus on activities to achieve industry compliance has been made, general economic conditions within the industry also affect year-to-year compliance. Weak economic conditions may increase the incentive for industry non-compliance in the financial components to a larger degree than in the business practice enforcement areas. The full effect of these external conditions on the compliance rate are not known, and to the degree that this measure only has a 4-year history, understanding the interaction of these variables on the overall compliance rate will be a challenge GIPSA confronts in future years. Additionally, GIPSA is just beginning to be able to use the data to make internal adjustments to ensure resources are effectively deployed to meet changing industry conditions due to external factors such as liquidity concerns.

The results of the individual component inspections and audits that comprise the aggregate index showed a year-to-year decline in compliance rates in 2011 for four of the five areas reviewed. The poultry payment review continues to show improvement, increasing from the initial rate of 60 percent in 2009 and 67 percent in 2010 to 69 percent in 2011. (Figure 8).

80 80 80 7650556065707580859095

100

2008 2009 2010 2011

Percent in Compliance

Year

20

Figure 8. Performance Measure Component Compliance 2008 – 2011.

3.1.3 Efficiency

P&SP measures its efficiency as the time from initiating an investigation to closing it in P&SP, or until the investigation case file is referred to OGC. After referral, P&SP and OGC typically work together to develop adequacy and quality of evidence, determine witness availability, and complete final case preparation. The average days to conduct an investigation and close the case increased in 2011, after decreasing in 2010 (Figure 9).

Figure 9. Average Days to Conduct Investigation from Opening to Closing or Referral to OGC, 2009 – 2011

0

20

40

60

80

100

Prompt Pay Custodial Account

Weighing Practices

Carcass Eval. Accuracy

Poultry Payment

2008 2009 2010 2011

114 98 1040

20

40

60

80

100

120

140

2009 2010 2011

Days

2011 Packers and Stockyards Annual Report

21

The data in Table 9 show total days to completion of investigative activity in regional offices, averaged across investigations completed by P&SP in the regional offices. Data in Table 9 do not include additional time spent on case development and processing for any investigative files forwarded to Headquarters. The total number of both types of actions that P&SP worked on during the year increased about 37 percent, from 5,525 in 2010 to 7,384 in 2011. Field activities are conducted at the location of the regulated business entity. Office activities are conducted in GIPSA offices and are typically filing violations, e.g., failure to submit required documentation. Data do not include time spent at Headquarters.

Table 9. Field and Office Investigations and Regulatory Activities Closed and Activities Open at End of the Fiscal Year, Fiscal Year 2011

Field Activities Office Activities

Type No. Avg. Days

Open No. Avg. Days

Open

Closed during year 715 147 1429 66 Open end of year 26 206 681 136 Regulatory Activities Closed during year 1129 18 1061 20 Open end of year 10 47 103 95

Investigations address a broad range of potential violations under the P&S Act and are grouped into three categories of competition, trade practice, or financial violations.

Competition violations often involve preferential treatment or restriction of competition, such as through apportionment of territory. Examples of trade practice violations include offenses such as unfair or deceptive practices, failure to register properly, tariff misrepresentation, and misuse of scales and improper weighing practices, including at any location where scales are used to weigh feed when feed is a factor affecting payment to livestock producers or poultry growers. Examples of financial violations include misuse of custodial accounts, failure to pay, and failure to pay when due (Table 10).

22

Table 10. Number of Investigations Closed at Regional Level in 2011 by Investigative Category

Investigative Category Number

Competition Restriction of Competition 14 Preferential Treatment 6 Concentration/Industry Structure 1 Financial

Bond Activities 609 Failure to Pay/Pay When Due 194 Custodial Accounts 128 Solvency 121 Annual Report 15 Packer/Poultry Trust 9

Trade Practice Registration/Jurisdiction 645 Weighing Practices and Scales 189 Unfair/Deceptive Practices 121 Contract Poultry Arrangements 44 Inadequate or False Records 17 Grower Termination 15 Procurement or Sales Review 10 Reparations 4 Merchandising 1 Tariff 1

Total 2,144 Table Note: Includes investigations for which regional-level work was completed in 2011and the cases were referred to headquarters, but may have remained open at headquarters at year-end. Thus the total differs from the total in Table 11.

P&SP’s regulatory and investigative actions often find that entities are in compliance with the P&S Act. When non-compliance is identified, P&SP either assesses fines or stipulations for admitted violations or pursues enforcement litigation with OGC. After referral but before filing, OGC works with P&SP to prepare the referred cases for filing and litigation before a USDA Administrative Law Judge or for referral to DOJ.

In fiscal year 2011, P&SP opened 2,780 cases, of which 2,678 were alleged violations for financial or trade practice behaviors. During the fiscal year, P&SP closed 2,053 cases without referring them to OGC (Table 11). An additional 78 cases were closed after referral to OGC, including 16 that OGC referred to DOJ.

2011 Packers and Stockyards Annual Report

23

Table 11. Number of Investigations Opened and Closed by Category and Enforcement Action, with Average Days to Complete Stages for Closed Cases, Fiscal Year 2011

Average Days

Status & Type

In P&SP

Referral to Filing

Filing to Resolution

Start to Resolution

Number

A. Total Investigations Opened Livestock Competition 10 Financial 1,411 Trade Practice 1,219Poultry Competition 2 Financial 16 Trade Practice 122Total Opened 2,780B. Total Investigations Resolved and Closed by P&SP Livestock Competition 238 238 20 Financial 81 81 1,014 Trade Practices 97 97 884Poultry Competition 175 175 3 Financial 153 153 8 Trade Practices 226 226 124Weighted Averages & Sub Total 98 98 2,053C. Total Referred to OGC and Closed Livestock Competition w/o Admin Action 298 492 5 Financial w Enforcement Action 190 882 29 Financial w/o Admin Action 248 254 438 674 11 Trade Practice w/ Enforcement Action 352 960 7 Trade Practice w/o Admin Action 326 276 333 613 7Poultry Trade Practice w/o Admin Action 370 535 3Weighted Averages & Sub Total 252 262 397 775 62D. Total Referred to DOJ and Closed Livestock Financial w/o Civil Action 211 519 1,014 4 Financial w/ Enforcement Action 149 704 1,061 7Poultry Trade Practice w/o Admin Action 379 122 658 5Weighted Averages & Sub Total 236 476 923 16

Overall Weighted Averages and Total 104 262 622 124 2,131

Table Note: Investigations opened during the fiscal year are not necessarily closed by year end. The number of days per stage applies only to cases closed during the fiscal year. Typically some closed cases were opened in prior years. Cases closed by P&SP after referral to OGC without a formal administrative action are indicated by “w/o Admin Action.” The “Referral to Filing” column in section C is the time that the case is in OGC prior to filing. The “Filing to Resolution” is the time from when a complaint is formally filed with the court clerk until a judicial decision. All cases closed after referral to DOJ in FY 2011 were settled without filing a complaint.

24

Investigations resolved by P&SP are closed either through a finding of no violation, a Notice of Violation letter issued to the entity, or a stipulation settlement in which the respondent admits the violation and voluntarily agrees to a penalty. P&SP closed these cases within an average of 98 days.

Another 62 cases were resolved that had been referred to OGC. Cases are referred to OGC when P&SP determines that the investigation requires cooperation with OGC. Frequently in competition and cases involving large financial failures, OGC and P&SP continue to develop evidence with the goal of filing a complaint. The average number of days for cases referred to OGC is calculated based on whether the cases were referred to DOJ for prosecution. Cases not referred to DOJ required an average of 252 days in P&SP; cases referred to DOJ required an average of 236 days in P&SP.

Table 11 represents only cases that were closed in 2011, and includes some cases that were initiated in years prior to 2011. As a result of referrals from P&SP, 36 administrative actions that had been filed by OGC were closed in 2011, and OGC closed an additional 26 cases after determining that evidence did not support formal administrative action. DOJ closed, without formal civil action, 9 cases that OGC had referred to DOJ, and closed 7 cases with formal action.

3.2 Management Initiatives

P&SP’s management team supports achieving higher performance and efficiency through various management initiatives. Central to the management initiatives has been the core recognition that the people in P&SP are its primary resource and strength in achieving its mission. In 2011, there were three special initiatives.

3.2.1 Custodial Account Special Report

P&SP management team selected six employees from the region to establish a standard operating procedure for handling custodial account special report requests. The team included some auditors, program support staff, and a Financial Unit supervisor. The team met by teleconferences over a couple of weeks and developed general instructions to follow when the agency requests these special reports from the industry. The standard operating procedures were reviewed and approved by the management team. A copy of the document has been published in the Employee Library and will be used to create a workflow in the Packers and Stockyard’s Automated System (PAS).

3.2.2 Scale Test Standard Operating Procedures

P&SP implemented the Packers and Stockyards Automated System (PAS) roughly 2 years ago. PAS is an automated management information system to manage workflows and capture data including data for case file management. PAS was implemented in two phases with phase 1

2011 Packers and Stockyards Annual Report

25

including higher priority standard procedures and phase 2 incorporating remaining standard procedures such as scale tests. The P&SP management team solicited several subject matter experts from each region to focus on updating the standard operating procedure for scale test and work with PAS developers to design a workflow to automate the process. A new Standard Operating Procedure workflow was developed and implemented. The new workflow has been implemented.

3.2.3 P&SP’s Change Control Working Group (CCWG)

In an effort to promote efficiency and adjustments for current industry changes, the P&SP management team established a team to focus on vetting change requests submitted from agency staff. The team is made up of voting members and non-voting members with representation from the regional and headquarter staff. The team is responsible for vetting change requests regarding agency activities, standard procedures, and PAS. The team forwards all change requests to the management team for final decision. This enables the management team to have an idea of issues of concern to staff. The CCWG is into its third year and has reviewed close to 200 change requests with 43 being approved by management.

26

4. ASSESSMENT OF THE INDUSTRIES

This section contains an assessment of the industries that P&SP regulates as requested by Congress. The first subsection provides an assessment of the general economic state of the regulated industries, including trends in the number of firms, financial conditions, and the percentage of the market held by the four largest firms of a particular sector (market concentration). The second subsection examines changing business practices of firms in the regulated industries, including pricing methods, and particularly pricing on live weight versus carcass weight; procurement methods, with a focus on commitments to procure more than 14 days before slaughter versus transactions conducted on a cash-carry or spot basis; and trends related to the volume marketed through market agencies via commissions versus direct purchases. Finally, this section outlines specific concerns about the behavior or conduct of the entities regulated under the P&S Act and P&SP’s actions to address those concerns.

Data in this section are generally from regulated industry annual reports to P&SP, and those reports for the 2011 reporting year are not due until April 15, 2012. Hence most statistics in this section are for 2010. Exceptions are statistics on firms currently bonded and/or registered as recorded in P&SP databases and market share (concentration) statistics.

The number of entities subject to the P&S Act shows some sign of stabilizing, with a small increase in number of entities of each type.

The four largest slaughter firms’ share of the total value of livestock purchases (i.e., aggregate industry concentration) declined nearly three percentage points in 2010 after increasing for the previous three years. Patterns of concentration in the purchase of different types of livestock, however, have exhibited varying trends.

Concentration in poultry slaughter has trended upward since 2000. The four-firm concentration ratio by volume of steer and heifer slaughter has been relatively stable in recent years, but increased by four percentage points in 2010. Cow and bull slaughter concentration increased from 1999 to 2007 then declined slightly for the last three years.

Concentration in hog slaughter increased sharply in 2003, declined in 2006, increased in 2007 and remained essentially steady since. Concentration in sheep slaughter declined in the first half of the decade then increased in 2005 and remained steady through 2009, but declined by five percentage points in 2010.

In general, increases in industry concentration from declining firm numbers reflect efforts by firms to increase net incomes. Agriculture firms in particular have tended to focus on cost minimization to increase net incomes. To achieve this objective, firms have adopted cost-saving technologies (frequently replacing labor with machines) that fostered larger capacities. Low interest rates throughout 2011 provided additional incentives for firms to replace labor with

2011 Packers and Stockyards Annual Report

27

capital assets. At the processor level increased worker productivity appears to be responsible in part for better income margins.

Some business practice trends are stabilizing. For example, carcass-basis purchases of cattle were 19.5 million head in 2010, near the average for the previous 10 years of 19 million. Carcass based purchases of hogs were 85 million in 2010 with the previous 10 years averaging 79 million. Carcass-based purchases reflect a trend by packers to pay livestock sellers for quality or grade characteristics tied to product values using contractual arrangements.

Carcass-basis pricing tends to correlate with trends in increased contracting for procurement and reductions in the volume of transactions through market agencies. These trends started over 10 years ago in the livestock/meat sector and will be resistant to change, even in the face of economically stressful conditions since they are related to cost-saving motives for increased coordination of livestock, poultry, and meat production and marketing.

The use of formula pricing methods and forward contracting for fed cattle increased in 2010, as the use of negotiated pricing declined. Packer feeding remained relatively constant. Packer feeding and forward contracting represent about 5 percent and 12 percent, respectively, of total fed cattle procurement. Patterns of use of alternative procurement and pricing methods for hogs were relatively unchanged in 2010, with about 68 percent purchased through various types of marketing arrangements, about 28 percent fed by packers, and the balance of just under five percent purchased on the negotiated spot market.

Unlike the livestock industry, which relies on contract procurement to coordinate the market supply channel, the poultry industry has been almost completely vertically integrated for several decades. As a result, the use of spot markets for poultry is virtually nonexistent.

28

4.1 General Economic State of the Industry

At the end of fiscal year 2011, there were 258 bonded livestock slaughter firms, 136 live poultry dealers, 4,572 registered dealers, and 1,220 market agencies were subject to the P&S Act (Table 12). There were also 1,218 posted stockyards. Entities subject to the Act are:

Bonded slaughter firms include firms operating Federally inspected plants as well as some firms operating plants that are not Federally inspected. Some firms with smaller volume purchases voluntarily bond but do not file annual reports. All packers operating in interstate commerce are subject to the P&S Act, which requires firms that purchase $500,000 or more of livestock for slaughter to be bonded and to file annual reports.

Livestock dealers purchase livestock for resale on their own accounts and take title to the animals. They may also purchase or sell as the agent or vendor of another entity.

Market agencies are entities engaged in the business of buying or selling livestock in commerce on a commission basis, furnishing stockyard services, or, in rare cases, an entity providing State brand inspection services.

Live poultry dealers, commonly called poultry integrators, contract with producers for grower services to raise chicks to slaughter size and weight. The integrator slaughters and further processes the poultry.

Table 12. Number of Slaughterers, Live Poultry Dealers, Bonded Dealers, Bonded Market Agencies, and Posted Stockyards Subject to the P&S Act, 2000-2011

Year

Bonded slaughter

firms

Live poultry dealers

Bonded dealers

Bonded market

agencies Posted

stockyards

2000 359 NA 4,772 1,608 1,519

2001 338 NA 4,675 1,575 1,525

2002 335 NA 4,480 1,544 1,510

2003 338 NA 4,675 1,575 1,429

2004 314 NA 4,152 1,457 1,443

2005 312 NA 4,100 1,447 1,426

2006 304 NA 3,984 1,433 1,400

2007 296 NA 3,883 1,410 1,413

2008 281 126 4,685 1,326 1,392

2009 284 125 4,529 1,225 1,170

2010 233 117 4,468 1,205 1,209

2011 258 136 4,572 1,220 1,218

2011 Packers and Stockyards Annual Report

29

Posted stockyards are physical facilities and are not necessarily separate businesses. For example, a county fairground may be registered as a posted stockyard. Terminal market agencies and auction market agencies are located at posted stockyards, but may or may not be the same entities that own and operate the stockyards.

In 2008, P&SP began transitioning from multiple older databases to a new single database. In the process, data was manually re-entered into the new system after field verification, except for information about posted stockyards, which do not report annually. In 2008, P&SP re-posted 864 known stockyards and in 2009 began de-posting any stockyards that do not respond to a request seeking applicants for re-posting. P&SP did not maintain statistics on live poultry dealers prior to 2008.

The volume of business of packers trended upward from 2006 through 2008, dropped in 2009, then returned to slightly more that the 2008 level at just over $50 billion in 2010. Similarly, dollar volume for firms selling on commission and for firms operating as dealers or purchasing on commission basis was relatively constant from 2004 through 2007, dropped in 2009, then increased in 2010. The decline in these measures in 2009 may reflect a changeover in GIPSA’s data tracking system (Figure 10).

Figure 10. Dollar Volume of Slaughter Firms, Dealers, and Market Agencies Selling and Buying on Commission Subject to P&S Act,

2000-2011.

The value of bonds held by subject firms has been relatively constant, although packing firms have shown some increase (Figure 10). The total value of bonds held by subject firms should continue to follow the same trend as the total dollar business volume of these firms.

15

20

25

30

35

40

45

50

55

60

65

2000 2002 2004 2006 2008 2010

Billion Dollars

Year

Packer Purchases

Commision Sales Value of livestock

Dealer and Commission Purchase Total Value

30

Figure 11 Value of Bonds Held in Accordance With P&S Act by Slaughter Firms, Market Agencies Selling on Commission, and Dealers and Market Agencies Purchasing on Commission,

2000-2010

The four largest slaughter firms’ share of total industry expenditures on livestock for slaughter dropped to 67 percent, about the same as the 2008 level after an increase in 2009 to about 70 percent (Figure 12).

Figure 12. Share of Total Industry Livestock Procurement Expenditures for the Four Largest Slaughter Firms, Ranked by Total Livestock Procurement Expenditure, 2000-2010

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010

Million Dollars

Year

Reporting Packers

Firms Selling on Commission

Firms Purchasing on Commission and Dealers

50

55

60

65

70

75

80

85

2000 2002 2004 2006 2008 2010

Percentage

Year

2011 Packers and Stockyards Annual Report

31

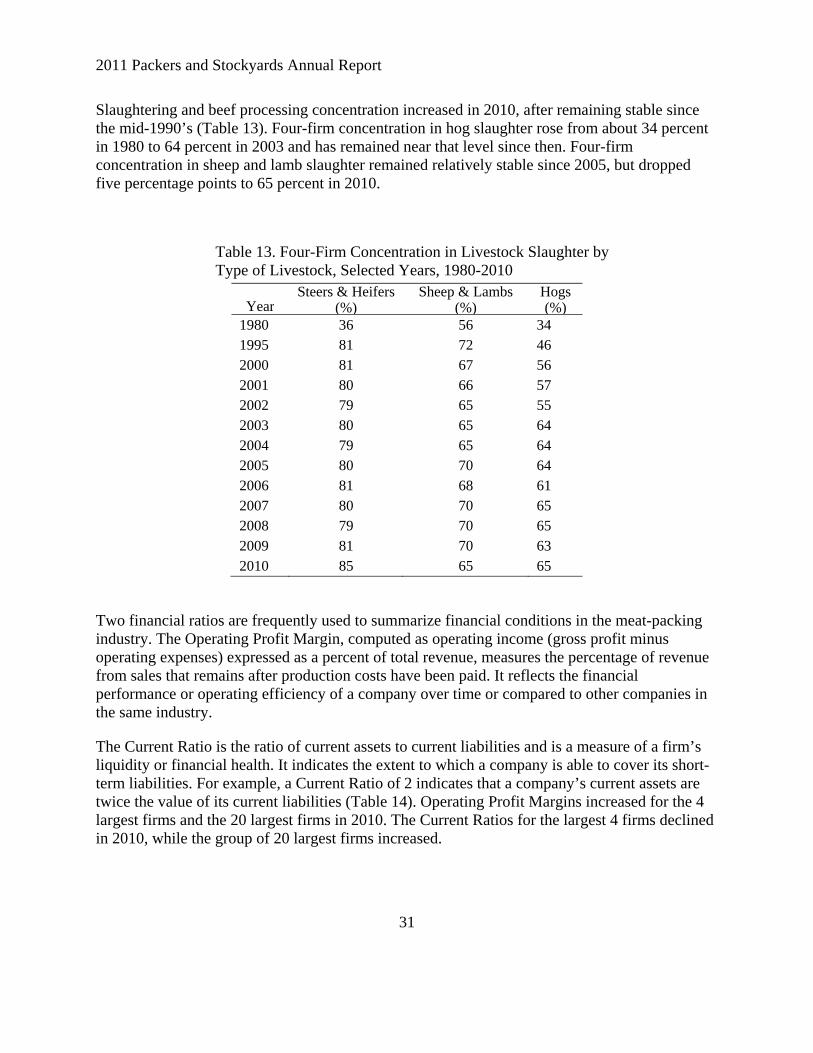

Slaughtering and beef processing concentration increased in 2010, after remaining stable since the mid-1990’s (Table 13). Four-firm concentration in hog slaughter rose from about 34 percent in 1980 to 64 percent in 2003 and has remained near that level since then. Four-firm concentration in sheep and lamb slaughter remained relatively stable since 2005, but dropped five percentage points to 65 percent in 2010.

Table 13. Four-Firm Concentration in Livestock Slaughter by Type of Livestock, Selected Years, 1980-2010

Year Steers & Heifers

(%)Sheep & Lambs

(%)Hogs (%)

1980 36 56 34 1995 81 72 46 2000 81 67 56 2001 80 66 57 2002 79 65 55 2003 80 65 64 2004 79 65 64 2005 80 70 64 2006 81 68 61 2007 80 70 65 2008 79 70 65 2009 81 70 63 2010 85 65 65

Two financial ratios are frequently used to summarize financial conditions in the meat-packing industry. The Operating Profit Margin, computed as operating income (gross profit minus operating expenses) expressed as a percent of total revenue, measures the percentage of revenue from sales that remains after production costs have been paid. It reflects the financial performance or operating efficiency of a company over time or compared to other companies in the same industry.

The Current Ratio is the ratio of current assets to current liabilities and is a measure of a firm’s liquidity or financial health. It indicates the extent to which a company is able to cover its short-term liabilities. For example, a Current Ratio of 2 indicates that a company’s current assets are twice the value of its current liabilities (Table 14). Operating Profit Margins increased for the 4 largest firms and the 20 largest firms in 2010. The Current Ratios for the largest 4 firms declined in 2010, while the group of 20 largest firms increased.

32

Table 14. Average Operating Profit Margin and Current Ratios for the Top 4 and the Top 20 Firms, 2006 - 2010

Operating Profit

Margin (%) Current RatioYear Top 4 Top 20 Top 4 Top 20

2006 -0.2 0.8 1.9 1.32007 1.0 1.7 1.9 1.62008 1.0 2.0 2.9 1.92009 2.0 2.0 3.5 2.32010 4.5 5.0 3.4 3.1

These financial data are averaged across a wide variety of types of firms. The size rankings are based on total livestock procurement expenditures. There are differences both across and within size groups in combinations of species slaughtered (beef, pork, sheep, and poultry) by the included firms. Within beef slaughter firms, the larger packers all slaughter a large proportion of steers and heifers in their total slaughter mix. Many smaller packers specialize in cow and bull slaughter and almost no steers and heifers.

Financial data reported to P&SP by some firms may include information on operations other than meat packing and processing. Variation in other types of non-meat activities included in the data from some firms occasionally leads to large swings in some of the ratios, especially for the group of smaller firms.

4.1.1 Cattle -- General Economic State of the Industry

The volume of cattle slaughtered by firms reporting to P&SP (firms with livestock purchases equal to or exceeding $500,000 per year) fluctuates with the cattle cycle. Total cattle slaughter by firms reporting to P&SP trended downward from 2000 through 2005 then increased in 2006, but has remained within a 1 million head band since (Figure 13). Total cattle includes steers and heifers (often collectively called “fed cattle”), cows, and bulls, but excludes calves. In most but not all cases, individual plants operated by firms that report to P&SP tend to slaughter either fed cattle or cows and bulls.

2011 Packers and Stockyards Annual Report

33

Figure 13. Total Slaughter Cattle Purchases for Firms Reporting to P&SP, 2000-2010

The number of cattle slaughter plants reporting to P&SP declined by approximately 60, or 27 percent, from 1998 through 2003, as plant sizes increased and smaller plants closed (Figure 14). The number of slaughter plants then remained stable until 2008, when there was a decline of 30 plants. The number of plants has remained relatively stable through 2010, but a gradual reduction in total numbers is expected as financial conditions make larger firms look for ways to reduce costs and operate more efficiently.

Figure 14. Number of Cattle Slaughter Plants for Firms Reporting to P&SP, 2000-2010

28,000

29,000

30,000

31,000

32,000

33,000

34,000

35,000

36,000

37,000

38,000

2000 2002 2004 2006 2008 2010

Head

(000)

Year

80

100

120

140

160

180

200

220

240

260

2000 2002 2004 2006 2008 2010

Number

Year

34

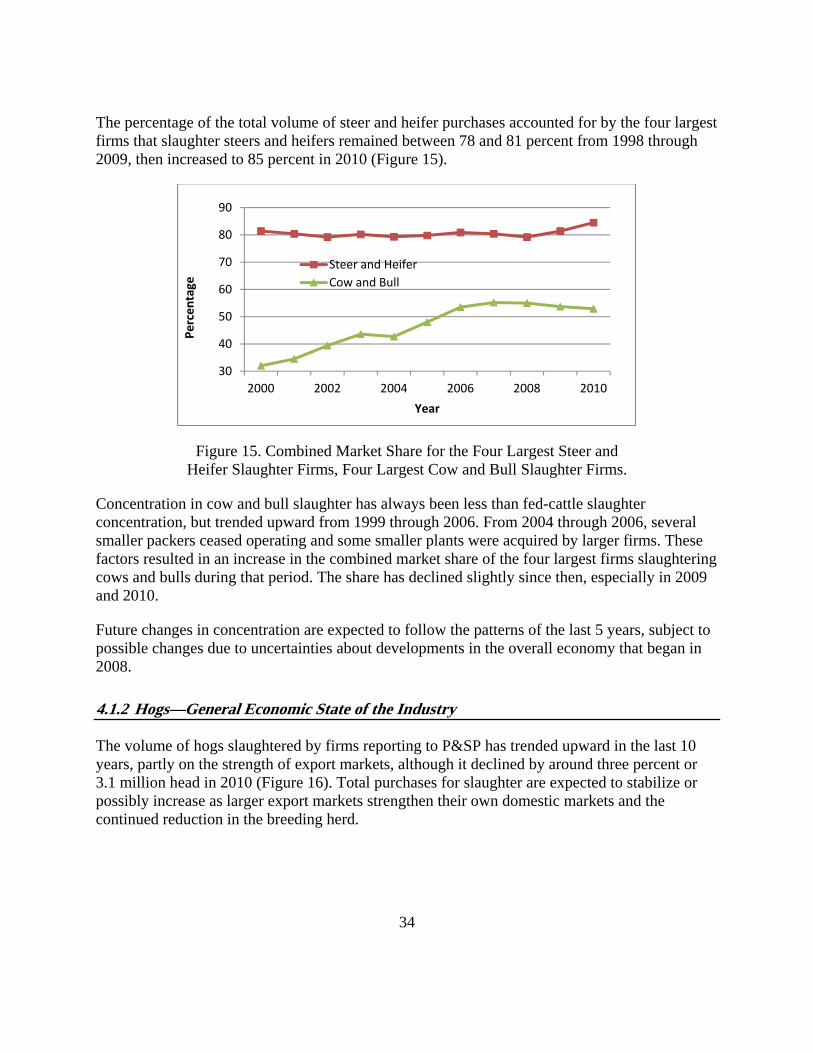

The percentage of the total volume of steer and heifer purchases accounted for by the four largest firms that slaughter steers and heifers remained between 78 and 81 percent from 1998 through 2009, then increased to 85 percent in 2010 (Figure 15).

Figure 15. Combined Market Share for the Four Largest Steer and Heifer Slaughter Firms, Four Largest Cow and Bull Slaughter Firms.

Concentration in cow and bull slaughter has always been less than fed-cattle slaughter concentration, but trended upward from 1999 through 2006. From 2004 through 2006, several smaller packers ceased operating and some smaller plants were acquired by larger firms. These factors resulted in an increase in the combined market share of the four largest firms slaughtering cows and bulls during that period. The share has declined slightly since then, especially in 2009 and 2010.

Future changes in concentration are expected to follow the patterns of the last 5 years, subject to possible changes due to uncertainties about developments in the overall economy that began in 2008.

4.1.2 Hogs—General Economic State of the Industry

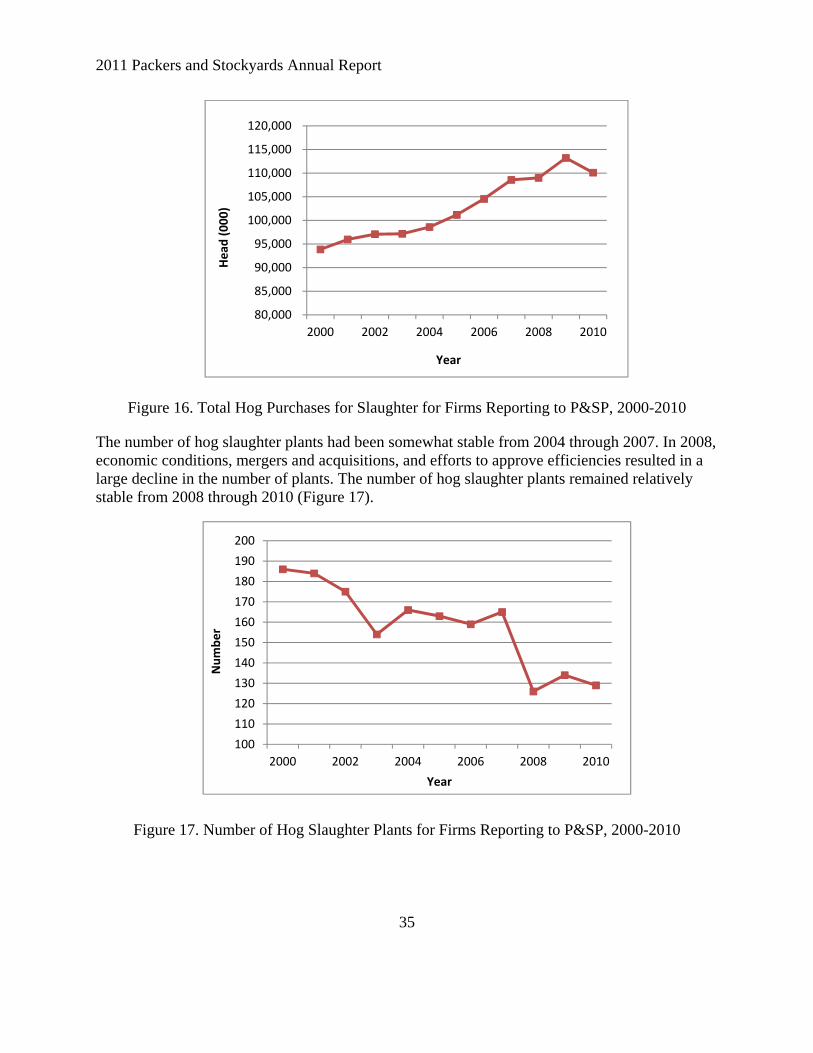

The volume of hogs slaughtered by firms reporting to P&SP has trended upward in the last 10 years, partly on the strength of export markets, although it declined by around three percent or 3.1 million head in 2010 (Figure 16). Total purchases for slaughter are expected to stabilize or possibly increase as larger export markets strengthen their own domestic markets and the continued reduction in the breeding herd.

30

40

50

60

70

80

90

2000 2002 2004 2006 2008 2010

Percentage

Year

Steer and Heifer

Cow and Bull

2011 Packers and Stockyards Annual Report

35

Figure 16. Total Hog Purchases for Slaughter for Firms Reporting to P&SP, 2000-2010

The number of hog slaughter plants had been somewhat stable from 2004 through 2007. In 2008, economic conditions, mergers and acquisitions, and efforts to approve efficiencies resulted in a large decline in the number of plants. The number of hog slaughter plants remained relatively stable from 2008 through 2010 (Figure 17).

Figure 17. Number of Hog Slaughter Plants for Firms Reporting to P&SP, 2000-2010

80,000

85,000

90,000

95,000

100,000

105,000

110,000

115,000

120,000

2000 2002 2004 2006 2008 2010

Head

(000)

Year

100

110

120

130

140

150

160

170

180

190

200

2000 2002 2004 2006 2008 2010

Number

Year

36

The four-firm concentration ratio for hog slaughterers was roughly 56 percent in the late 1990s and then increased to near 65 percent in 2003, where it remained in the mid 60’s range through 2010 (Figure 18).

Figure 18. Combined Market Share for the Four Largest Hog Slaughter Firms, 2000-2010

4.1.3 Sheep—General Economic State of the Industry

The volume of sheep and lambs slaughtered by packers reporting to P&SP declined in every year but three between 1998 and 2007, with the sharpest single year decline between 2007 and 2008. The volume has remained relatively constant since, with total slaughter of just over 1.9 million head in 2010 (Figure 19).

Figure 19. Total Slaughter Sheep and Lamb Purchases for Firms Reporting to P&SP, 2000-2010

50

55

60

65

70

75

2000 2002 2004 2006 2008 2010

Percentage

Year

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

2000 2002 2004 2006 2008 2010

Head

(000)

Year

2011 Packers and Stockyards Annual Report

37

The number of plants slaughtering sheep and lambs has been relatively constant since 2002, with a small decline from 2005 through 2008 offset by an equal increase since then (Figure 20). Many of these are small multispecies plants that slaughter only a few sheep and lambs, with fewer than two dozen plants averaging over 100 head per week in 2010.

Figure 20. Number of Sheep and Lamb Slaughter Plants for Firms Reporting to P&SP, 2000-2010

The combined market share of the four largest sheep and lamb slaughter firms trended steadily downward from 1998 through 2004, as the largest plants in the industry decreased slaughter faster than total industry slaughter declined (Figure 21).

Due to the small total slaughter volume of the industry, relatively moderate volume adjustments by any of the largest four firms result in relatively large changes in the percent of total industry slaughter accounted for by those firms. The long-term decline in share reversed in 2005, when one of the four largest firms exited and the remaining three large firms increased their combined volume by an amount equal to the output of the exiting firm. An additional firm then entered the group of four largest, causing a net increase in total slaughter of the four largest firms and in their share of total industry slaughter.

20

30

40

50

60

70

80

2000 2002 2004 2006 2008 2010

Number

Year

38

Figure 21. Combined Market Share for the Four Largest Sheep and Lamb Slaughter Firms, 2000-2010

The share of the four largest lamb packers then declined in 2006, returned to 2005 levels in 2007 through 2009, but decreased by five percentage points in 2010. But, as in previous years, these changes in shares represented only a few thousand head of slaughter lambs. Future changes in sheep slaughter concentration will continue to be variable due to adjustments among the four largest firms, but will likely remain in the 65-70 percent range.

4.1.4 Poultry—General Economic State of the Industry

This section addresses slaughter volume, industry concentration, and two measures of live poultry dealer financial health (the Operating Profit Margin and Current Ratio) obtained from annual reports filed by the industry with P&SP.

In 2010, poultry processors reporting to P&SP slaughtered an estimated 48.4 billion pounds of chickens. By comparison, in 2010, the federally inspected (FI) volume was 50.1 billion pounds. This continues to reflect an upward trend in poultry slaughter since 1996, when FI volume was approximately 26 billion pounds. Turkey slaughter increased to an estimated 7.2 billion pounds by firms reporting to P&SP for 2010. This was actually slightly more than the reported FI volume of 7.1 billion pounds for 2010, in part due to the fact that the reporting years for some P&SP firms are not the same as the calendar year represented by the FI statistics.

Concentration in broiler and turkey slaughter trended upwards from 2000 through 2008, but in 2009, the four largest broiler slaughterers posted a 4 percent decline to 53 percent of the market share compared to 57 percent in 2008, and their share decreased another 2 points to 51 percent in 2010. The four largest turkey slaughterers also posted a decrease of 2 percentage points to a 58 percent market share. Concentration in poultry slaughter is expected to remain relatively stable when data for 2011 are available.

50

55

60

65

70

75

2000 2002 2004 2006 2008 2010

Percentage

Year

2011 Packers and Stockyards Annual Report

39

In 2010, the Operating Profit Margin (the percentage of revenue from sales that remains after production costs have been paid) of the 20 largest broiler companies averaged 2.3 percent, an improvement over the 1.3 percent in 2009 (Table 15). Profits for the four largest broiler firms averaged considerably higher than profits for the entire group of 20 largest broiler firms, increasing to an average of 5.2 percent. The average profit margin for the four largest turkey processing companies was also higher than that of the 20 largest, at 5.4 percent versus 1.7 percent, respectively. The largest four firms for both types of poultry had a higher average Current Ratio than the group of the 20 largest firms.

Table 15. Poultry Industry Market Share, Operating Profit Margin, and Current Ratio, 2008 - 2010

Market Operating Profit

Margin (%) Current Ratio Type and Year Share (%) Top 4 Top 20 Top 4 Top 20

Broiler 2008 57 -5.4 -1.2 1.9 2.1 Broiler 2009 53 0.0 1.3 2.4 2.2 Broiler 2010 51 5.2 2.3 2.3 2.1 Turkey 2008 51 1.8 2.4 1.8 2.4 Turkey 2009 58 1.8 -1.6 2.0 2.5 Turkey 2010 56 5.4 1.7 2.9 2.4

4.2 Changing Business Practices.

The long-term decline in the number of livestock slaughter firms reporting to P&SP reported in the previous section has been accompanied by a trend toward increased specialization in slaughter. This has been illustrated by a greater decline from 1997 through 2006 in the number of firms slaughtering two or more classes of livestock than in the number of firms slaughtering a single class (Figure 22). For purposes of this comparison, the separate classes of livestock are steers and heifers; cows and bulls; calves; sheep and lambs; and hogs. While the number slaughtering two or more classes increased in 2007, it has declined since 2008 as the number slaughtering only one class stayed about the same.

40

Figure 22. Number of Firms Slaughtering One Class and Number of Firms Slaughtering Two or More Classes of Livestock, 2000-2010.

4.2.1 Cattle—Changing Business Practices

The pricing method that sellers and purchasers agree to use for a transaction is a fundamental characteristic of any market transaction. For livestock and for cattle transactions in particular, pricing methods are most often divided into two categories: live-weight and carcass pricing methods.

In live-weight purchasing of livestock, the price is quoted and the final payment is determined based on the weight of the live animal. Transactions that use some variation of live-weight purchasing are usually on an “as-is” basis with a single price per pound for all animals in the entire transaction.