2011 outlook - e&p and mlp - pipelines - 19 january 2011

TRANSCRIPT

©©

Credit Research | Americas

Contributing Research Analysts

Daniel Volpi, [email protected]

Brock [email protected]

January 19, 2011

See Disclosures Appendix A1 for the Analyst Certification and Other Important Disclosures

Nomura Energy Credit ResearchE&P and MLP/Pipelines

2011 Outlook

Page 2

Table of Contents

Overview Page 3 – 16 Recommendation Changes 3 Picks and Trade Ideas 4 – 7 Recommendations 8 – 9 Key Themes 10 Commodity Prices 11 Inventories 12 – 13 Oil-Gas Ratio 14 Rig Counts 15 – 16

Recommendations Page 17 – 68 Exploration & Production Recommendations 17 – 51 Exploration & Production Comparative Tables 52 – 56 Exploration & Production Hedging Profiles 57

Master Limited Partnerships Recommendations 58 – 68

Disclosures Appendix A1 Page 69 – 71

Recommendation Changes

We are revising our ratings on two E&P names.

Nexen Inc. (NXYCN)

We are revising our rating to BUY from HOLD on NXYCN long bonds. Despite the pending downgrade to Ba1 at Moody’s, we believe that current levels provide a good entry point for longer-term tightening potential of 20 bps on the long end. We believe that a Ba1/BBB-rated Nexen, which is our base case scenario, should trade roughly 10-15 bps through Anadarko Petroleum. We like the lower dollar price NXYCN 5.875% of 2035 at +210bp ($90.85), trading flat on a curve basis to the APC 6.45% of 2036 ($97.00). We also note that there is a reasonable possibility that Nexen management obtains IG ratings from Fitch Ratings, which would keep NXYCN in the major IG credit indices and provide greater upside from our base case scenario. We had moved to a HOLD rating based partially on our concerns over technical selling pressures ahead of the pending Moody’s downgrade. However, year-end 2010 positioning is now behind us, and our sense is that bonds have largely transitioned from would-be forced sellers.

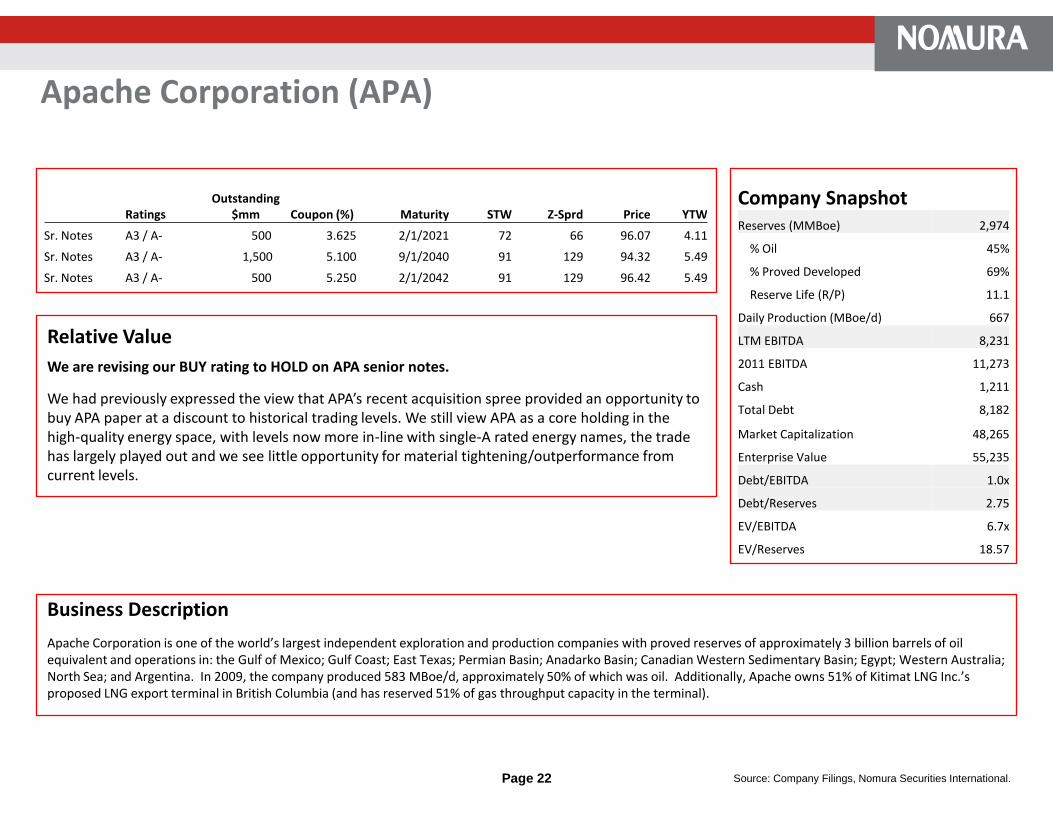

Apache Corp. (APA)

We are revising our BUY rating to HOLD on APA senior notes. We had previously expressed the view that APA’s recent acquisition spree provided an opportunity to buy APA paper at a discount to historical trading levels. We still view APA as a core holding in the high-quality energy space but with levels now more in-line with single-A rated energy names, the trade has largely played out and we see little opportunity for material tightening/outperformance from current levels.

Page 3

Picks and Trade Ideas BUY Nexen (NXYXN) 7.5% senior notes 2039, 6.4% senior notes 2037, 5.875% senior notes 2035

We view current levels as a good entry point for 20bp tightening potential on long bonds. See page 40.

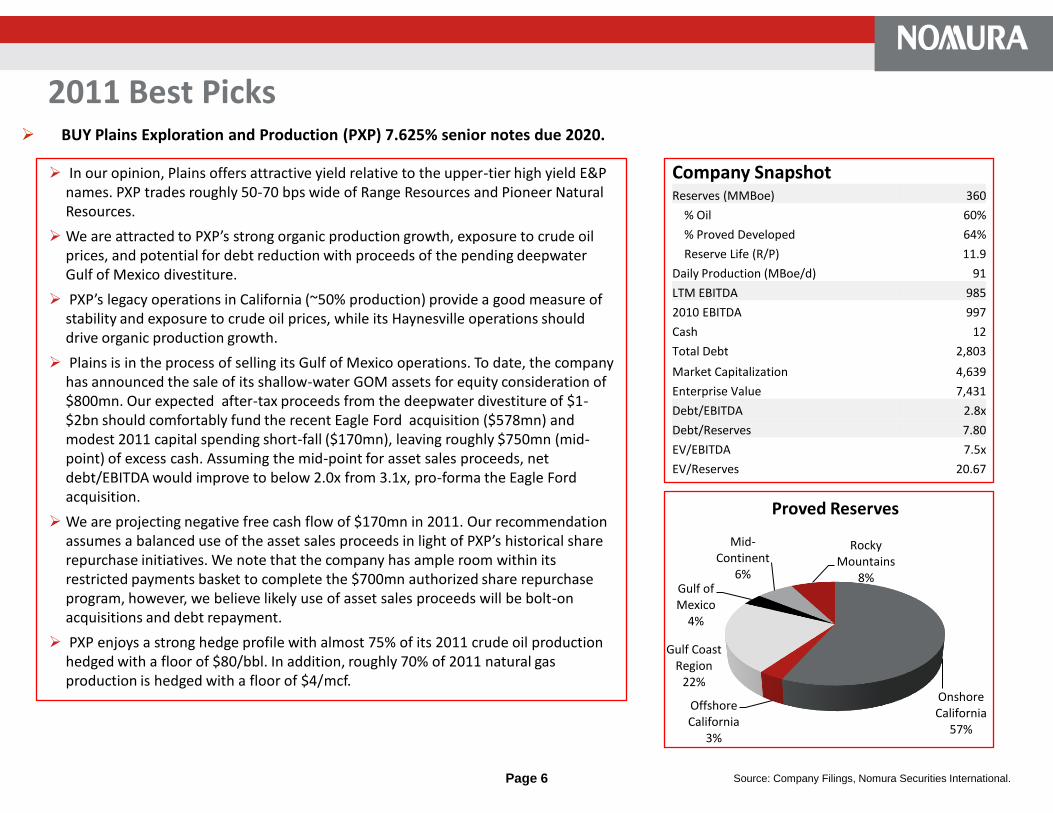

BUY Plains Exploration and Production (PXP) 7.625% senior notes due 2020

PXP offers attractive yield relative to upper-tier HY E&Ps and potential for debt reduction from pending asset sales. See page 46.

BUY Kinder Morgan (KMP) 6.95% senior notes due 2038, 6.5% senior notes due 2039, and 6.55% senior notes due 2040

We view the long end of the senior debt complex as most attractive, with long bonds trading at a roughly 30bp spread to 10-year notes. Note that lower-rated EPD and WPZ 10s-30s curves are flat-10bp. See page 64.

Swap into CNQCN 6.25% of 2038, out of CVECN 6.75% of 2039

The trade allows investors to maintain exposure to crude oil, and take out ~$5 dollar price at even spread to the curve.

Swap into WPZ 4.125% of 2020, out of EPD 5.2% of 2020

While benchmark MLP issuer EPD has greater scale, WPZ offers lower-leverage and less commodity price exposure. The trade allows investors to diversify their MLP holdings with a modest pick up 5bp and take out of $9 dollar price.

Swap into ECACN 5.9% of 2017, out of ECACN 6.5% of 2019

Although we are bearish on natural gas fundamentals, ECACN 2017s appear cheap relative to the ECACN senior notes complex. Investors can shorten 1.5 years in the natural gas producer, take out $4 dollar price and give only 5bp to the curve.

Swap into SLB 4.2% of 2021, out of COP 6.0% of 2020

Recent SLB new issuance provides exposure to premier oilfield services player SLB. The trade allows investors to pick up modestyield and take out $15 dollar price into a par bond.

Page 4

Page 5

Despite the pending downgrade to Ba1 at Moody’s, we believe that current levels provide a good entry point for longer-term tightening potential of 20 bps on the long end.

We believe that a Ba1/BBB- rated Nexen, which is our base case scenario, should trade 10-15 bp through Anadarko Petroleum. We like the lower dollar price NXYCN 5.875% of 2035 at +210bp ($90.85), trading flat to the APC 6.45% of 2036 ($97) on a curve basis.

Moody’s review for downgrade remains focused on Nexen’s leverage metrics, which the agency deems as inconsistent with IG ratings. We have argued, however, that debt/EBITDA of 1.4x (1.1x net basis) has improved from 2.5x (1.8x) in the year-ago period and is comparable with low-BBB rated E&Ps. On a net debt/production basis, leverage stands at C$21k per boe/day compared with C$30K last year following C$1.5bn of debt repayment since year-end 2009.

While we may disagree that NXYCN’s credit profile merits below investment grade ratings, we nevertheless must respect the significance of split rating on valuations. As such, we view APC (rated Ba1/BBB) as the best comparison since APC’s crossover ratings reflect an expectation of increased leverage from the spill liability. Again, we would expect NXYCN to trade roughly flat with APC with Ba1/BBB ratings.

There is also the possibility that NXYCN pursues credit ratings from Fitch Ratings. While management can not comment on the matter, we would point out that an “8 B” energy name would remain in the major IG credit indices, alleviating concerns of forced selling pressure.

From a technical perspective, we remain cognizant of the potential selling pressure following the pending downgrade . That said, our sense is that bonds have already transitioned from would-be forced sellers and year-end 2010 positioning is behind us.

BUY Nexen Inc. (NXYCN) long bonds: 7.5% senior notes 2039; 6.4% senior notes 2037; 5.875% senior notes 2035

Company SnapshotReserves (MMBoe) 920

% Oil 93%

% Proved Developed 55%

Reserve Life (R/P) 11.8

Daily Production (MBoe/d) 213

LTM EBITDAX 3,929

2010 EBITDAX 3,607

Cash 1,210

Total Debt 5,678

Market Capitalization 11,490

Enterprise Value 15,958

Debt/EBITDAX 1.4x

Debt/Reserves 6.18

EV/EBITDAX 4.1x

EV/Reserves 17.36

Long Lake, 32%

Syncrude, 31%

United Kingdom,

19%

Canada, 8%

United States, 5%

Yemen, 1% Other, 4%

Proved Reserves

2011 Best Picks

Source: Company Filings, Nomura Securities International.

Page 6

In our opinion, Plains offers attractive yield relative to the upper-tier high yield E&P names. PXP trades roughly 50-70 bps wide of Range Resources and Pioneer Natural Resources.

We are attracted to PXP’s strong organic production growth, exposure to crude oil prices, and potential for debt reduction with proceeds of the pending deepwater Gulf of Mexico divestiture.

PXP’s legacy operations in California (~50% production) provide a good measure of stability and exposure to crude oil prices, while its Haynesville operations should drive organic production growth.

Plains is in the process of selling its Gulf of Mexico operations. To date, the company has announced the sale of its shallow-water GOM assets for equity consideration of $800mn. Our expected after-tax proceeds from the deepwater divestiture of $1-$2bn should comfortably fund the recent Eagle Ford acquisition ($578mn) and modest 2011 capital spending short-fall ($170mn), leaving roughly $750mn (mid-point) of excess cash. Assuming the mid-point for asset sales proceeds, net debt/EBITDA would improve to below 2.0x from 3.1x, pro-forma the Eagle Ford acquisition.

We are projecting negative free cash flow of $170mn in 2011. Our recommendation assumes a balanced use of the asset sales proceeds in light of PXP’s historical share repurchase initiatives. We note that the company has ample room within its restricted payments basket to complete the $700mn authorized share repurchase program, however, we believe likely use of asset sales proceeds will be bolt-on acquisitions and debt repayment.

PXP enjoys a strong hedge profile with almost 75% of its 2011 crude oil production hedged with a floor of $80/bbl. In addition, roughly 70% of 2011 natural gas production is hedged with a floor of $4/mcf.

BUY Plains Exploration and Production (PXP) 7.625% senior notes due 2020.

Proved Reserves

Company SnapshotReserves (MMBoe) 360

% Oil 60%

% Proved Developed 64%

Reserve Life (R/P) 11.9

Daily Production (MBoe/d) 91

LTM EBITDA 985

2010 EBITDA 997

Cash 12

Total Debt 2,803

Market Capitalization 4,639

Enterprise Value 7,431

Debt/EBITDA 2.8x

Debt/Reserves 7.80

EV/EBITDA 7.5x

EV/Reserves 20.67

Onshore California

57%

Offshore California

3%

Gulf Coast Region

22%

Gulf of Mexico

4%

Mid-Continent

6%

Rocky Mountains

8%

2011 Best Picks

Source: Company Filings, Nomura Securities International.

Page 7

As one of the largest and most diversified MLPs, we view KMP as a core holding in the high grade MLP space. While the oil production (CO2) segment stands out as atypical to its competitors’ operations, the related hedging program and very high quality, regulated mix of the conventional segments offsets C02’s higher operational risk. We view the long end of the senior debt complex as most attractive, with long bonds trading at a roughly 30bp spread to 10-year notes. We note that lower-rated EPD and WPZ 10s-30s curves are flat-10bp.

Kinder Morgan’s leverage is ~4.6x debt/EBITDA, above the peer average of 4.3x. Over the past 2 years, KMP’s leverage has been above the peer average due to guaranteed joint venture debt. This debt was used to fund construction of new projects (Rockies Express, Midcontinent Express, Fayetteville Express) and once these projects are placed into service, KMP typically terms out the debt at the asset level, thus becoming non-recourse to KMP. Currently, KMP has ~$500mn of guaranteed JV debt, primarily related to the Fayetteville Express Pipeline. FEP was placed into service on December 2nd and we expect the pipeline to issue debt to term out construction costs. This reduction in debt and the increase in EBITDA from the new project should bring leverage closer to the peer average.

Kinder Morgan’s has a well diversified and stable business mix: ~25% of EBITDA from natural gas pipelines; ~25% from refined products pipelines; ~20% from storage terminals; and ~30% from its CO2 business. While the first three segments are primarily stable, fee-based businesses, the CO2 segment’s oil production represents direct commodity price exposure. Approximately 70% of 2011 expected production is currently hedged.

Products Pipelines

21%

Natural Gas Pipelines

25%CO229%

Terminals19%

Kinder Morgan Canada

6%

Segment EBITDA

BUY Kinder Morgan Energy Partners (KMP) 6.95% senior notes due 2038, 6.5% senior notes due 2039, and 6.55% senior notes due 2040.

2011 Best Picks

Source: Company Filings, Nomura Securities International.

Page 8

Company Recommendation Rationale

Anadarko Petroleum Company HOLDWe still see longer-term upside as the Macondo liability is resolved but we view current spreads are somewhat full considering the uncertainty.

Apache Corporation HOLD

We are revising our BUY rating to HOLD on APA senior notes. We had previously expressed the view that APA’s recent acquisition spree provided an opportunity to buy APA paper at a discount to historical trading levels. We still view APA as a core holding in the high-quality energy space, with levels now more in-line with single-A rated energy names, the trade has largely played out and we see little opportunity for material tightening/outperformance from current levels.

Canadian Natural Resources Ltd. BUYAttractive exposure to crude oil pricing (70% of production), low leverage, and good free cash flow profile. We believe that the Horizon incident will likely be resolved in the near-term.

Cenovus Energy Inc. BUY Exposure to oil (~50% of production), free cash flow generation, and best-in-class oil sands operations.

Chesapeake Energy Company HOLDCore holding in high yield energy. Premier assets and consistent production growth offset by risks attendant to recent strategic shift toward liquids production and negative free cash flow.

Devon Energy Company HOLD A high quality, well-diversified portfolio and conservative credit profile are offset by tight trading levels.

EnCana Corporation SELLChallenging fundamentals in the North American natural gas market, relatively tight spreads, and negative free cash flow.

Hess Corporation SELLMinimal hedging policy, high capital requirements for riskier international prospects in Africa and Asia, and sizeable GOM leases.

Marathon Oil Corporation HOLD

While the recently announced plan to spin-off the refining business will be neutral from a financial leverage perspective, the business profile will be diminished by the loss of the high-quality refining operations. However, management plans to reduce debt by $2.5bn (likely through tender offers) and market technicals will likely keep notes from materially widening from current levels, in our opinion.

Newfield Exploration Company HOLD Low relative yields are offset by a strong hedge profile and free cash flow generation.

Nexen Inc. BUY Attractive entry point for 20bp tightening potential in long end of the curve.

Noble Energy, Inc. HOLDSmaller reserve size and nontraditional international development plans are offset by upside potential at the Tamar discovery and competitive cost structure.

Pioneer Natural Resources Company HOLDManagement is pursuing robust production targets while maintaining spending within cash flows. The company has moderate leverage but relatively high finding costs.

Plains Exploration & Production Company BUY PXP offers attractive yield along with organic production growth, exposure to crude oil prices, and the potential for debt reduction from proceeds of the pending deepwater GOM divestiture.

Range Resources Corporation HOLDRelatively low yield and projected free cash flow deficit are offset by strong operational profile, very low cost structure, and moderate leverage.

Talisman Energy Inc. HOLD Wide spreads are merited due to ongoing strategy shifts and cash flow burn, mitigated to an extent by low leverage.

Company Recommendation Rationale

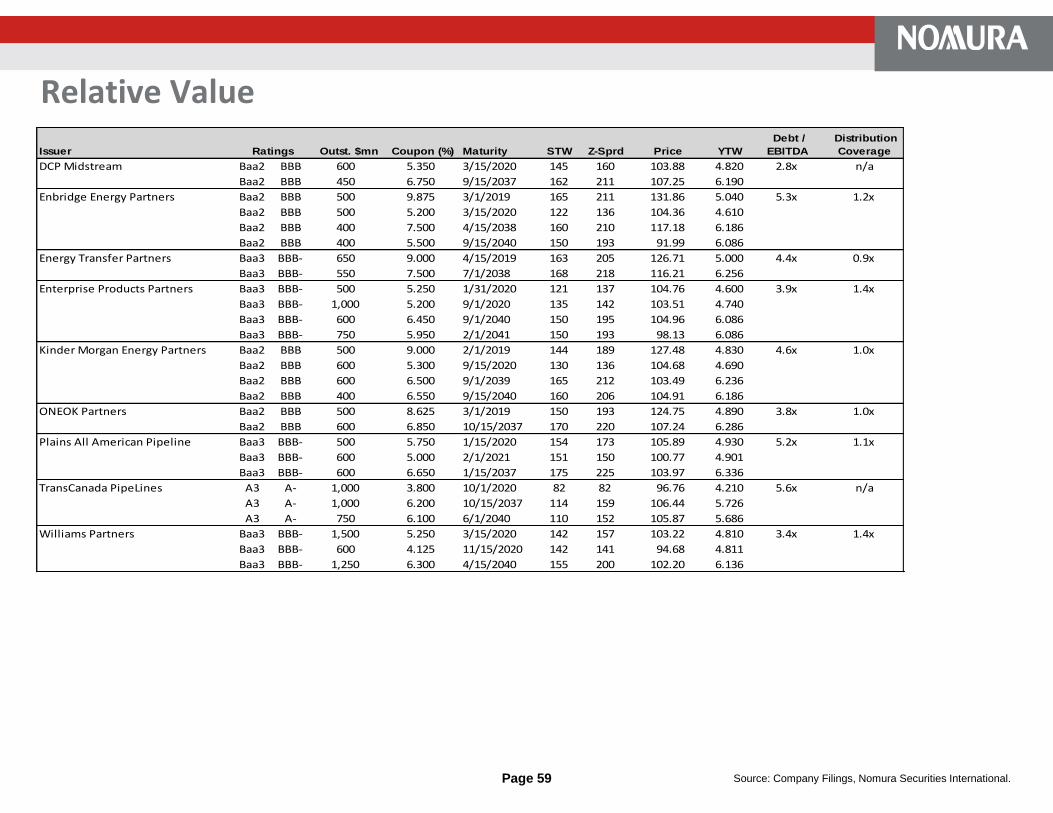

DCP Midstream LLC BUYWe are attracted to the DCMPID’s strong business position in natural gas gathering and processing, conservative leverage, anddemonstrated support from its 50/50 parents ConocoPhillips (A1/A/A) and Spectra Energy (Baa2/BBB). At 15-20bp wide to benchmark MLPs, we view DCPMID (organized as a c-corp.) as excessively wide.

Enbridge Energy Partners, L.P. HOLD

Despite the recent noise surrounding the pipeline spill, we remain comfortable with EEP’s credit profile. We note that EEP enjoys an excellent business position in oil and refined products pipelines and a relatively high percentage of fee-based cash flow. In addition, EEP is strategically important to its general partner and largest unit holder, Enbridge Inc. (Baa1/A-), which in the past has provided financial support to the MLP. Our HOLD rating is based on what we view as full valuations relative to its MLP peers and limited upside.

Energy Transfer Partners, L.P. HOLD

We believe that ETP‘s credit profile has strong positive momentum but the senior notes appear fairly valued, considering the higher dollar price and weaker liquidity in the issues. We are attracted to ETP’s scale and diversification across interstate, intrastate, and midstream natural gas operations. The completion of two large interstate pipelines will improve the business mixby increasing regulated interstate pipeline earnings to nearly 30% from 16%, and reduce the less stable intrastate contribution to 40% from 47%.

Enterprise Products Partners L.P. HOLD

EPD is one of the better-managed midstream companies and enjoys excellent scale, with a significance presence in existing and emerging natural gas producing regions. While EPD does have above-average commodity price exposure given its NGL operations, this is partially offset by conservative financial policies, including a willingness to issue equity units to balance its capital structure.

Kinder Morgan Energy Partners, L.P. BUY

As one of the largest and most diversified MLPs, we view KMP as a core holding in the high grade MLP space. While the oil production (CO2) segment stands out as atypical to its competitors’ operations, the related hedging program and very high quality, regulated mix of the conventional segments offsets the CO2 operational risk . We view the long end of the senior debt complex as most attractive, with long bonds trading at a roughly 30bp spread to 10-year notes. We note that lower-rated EPD and WPZ 10s-30s is roughly flat-10bp.

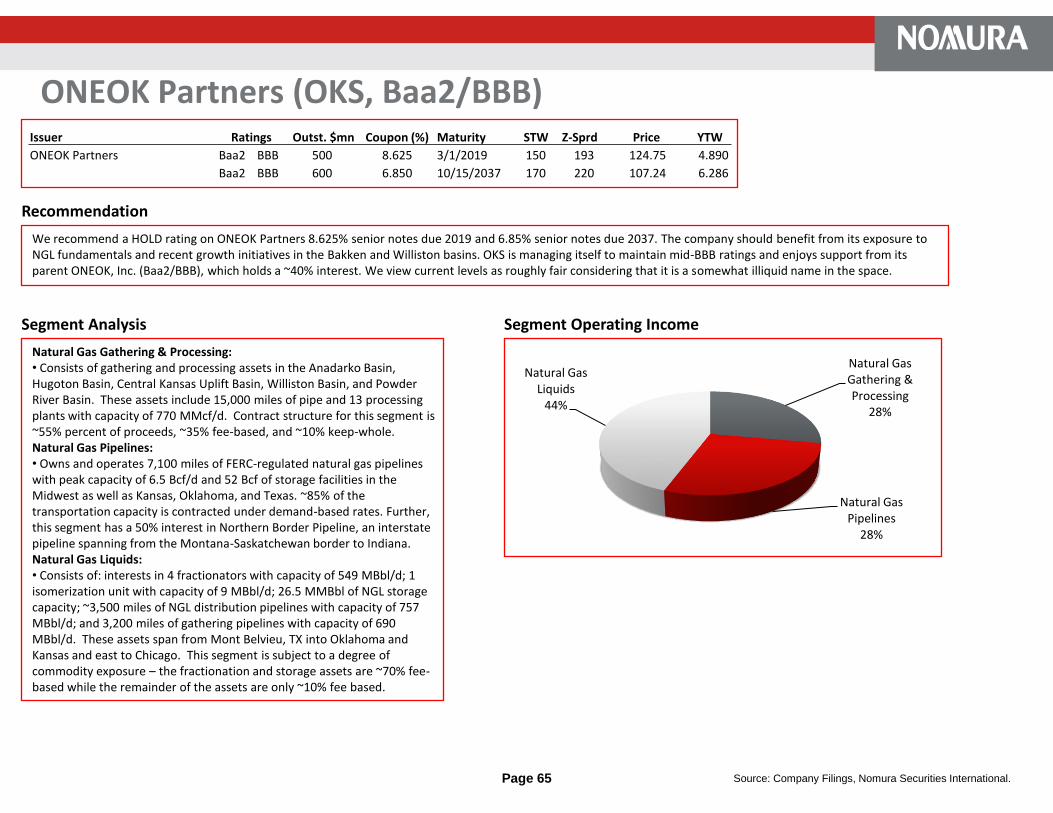

ONEOK Partners, L.P. HOLDONEOK should benefit from its exposure to NGL fundamentals and recent growth initiatives in the Bakken and Williston basins. OKS is managing itself to maintain mid-BBB ratings and enjoys support from its parent ONEOK, Inc.(Baa2/BBB), which holds a ~40% interest. We view current levels as roughly fair considering that it is a somewhat illiquid name in the space.

Plains All American Pipeline, L.P. SELLWe maintain a favorable view on Plains’ largely fee-based crude oil and products pipeline business. However, we believe that current spreads do not compensate for the high leverage of 5.2x debt/EBITDA (high 4x adjusted for oil inventory related debt)and risk inherent to the marketing operations (20-25% of earnings).

TransCanada PipeLines Ltd. SELLRespecting the highly regulated nature of the business mix and the single-A ratings, we view current levels as rich considering the company’s high leverage and negative free cash flow profile. Although the name trades wide for its A ratings, we believe that expectations of steady issuance to finance its cash flow deficit will limit upside from current levels.

Williams Partners, LP HOLD

We are attracted to WPZ’s relatively stable business mix and low leverage compared to its MLP peers. The company owns two major, regulated interstate pipelines and its midstream operations are roughly 50% fee-based. At roughly flat to EPD, we would recommend swapping into WPZ senior notes in order to diversify MLP exposure. While EPD is a larger, better diversified benchmark MLP issuer, WPZ operates with lower leverage (3.8x vs. 4.3x) and less commodity exposure.

Page 9

Page 10

Divergent fundamentals for crude oil and U.S natural gas prices. Global economic activity levels and a balanced inventory picture should maintain supportive pricing for crude oil. The U.S natural gas market, however, remains stubbornly over-supplied. While we would expect a tapering off of natural gas drilling required to hold leases, the implied supply curtailment will likely be insufficient to tighten market conditions in the near- to medium-term. The percentage of hedged production for 2011 is reduced from 2010 levels but nevertheless offers a good degree of downside protection. For 2011 modeling assumptions, we are using $85/bbl WTI and $4.50/mcf Henry Hub.

E&P asset repositioning: more drilling, less land-grab. E&Ps will continue executing the broad strategic shift toward increased liquids – crude oil and NGL – production. We expect that acreage acquisition activity will moderate from the torrid pace of 2010. Intensified development drilling on recently acquired acreage should support increased bookings of proved reserves. An increased use of JVs + drilling carries on developing plays and the divestiture of conventional/non-core assets should offset spending.

Gulf of Mexico: focus will be on the regulatory environment. The administration appears poised to institute a policy response to the Macondo incident rather than aggressively pursuing the involved parties. Macondo will be the platform for a more heavily regulated offshore environment. The involved parties will likely be held liable for damages, but the prospect for severe punitive actions against the involved parties is diminishing. Despite the more burdensome regulatory environment, operating conditions should normalize in the second half of 2011.

Master Limited Partnerships (MLPs) have shifted growth spending toward gathering & processing and NGL operations. The industry is nearing completion of large, long-haul pipeline construction. Broadly speaking, the recently completed projects should improve earnings and cash flow quality. We are expecting the next phase of growth projects to be directed toward the infrastructure build-out in the developing shale plays. 2011 growth spending should yield near- to medium-term earnings contributions since these typical midstream projects are smaller scale and require less lead time. However, the latest MLP growth phase will increase exposure to the more commodity price sensitive segments of the industry.

The MLP acquisition market should remain active. Independent E&Ps and majors will continue divesting infrastructure assets in 2011, providing acquisition opportunities for MLPs. M&A financing is expected to remain largely credit neutral given the traditional balanced debt/equity funding approach.

Key Themes for 2011

Page 11

Oil and Natural Gas Prices

Source: Bloomberg

CommentaryCrude oil, gasoline, and distillate inventories have been running at or near five-year highs for the past 12-24 months (See Page 13). Despite this, WTI prices have recovered from the 2009 lows around $35/Bbl and had established a range of $70-85/Bbl before breaking $90/Bbl in December. With the supply picture essentially unchanged since the beginning of 2009, WTI prices appear to be more closely correlated with broader global commodities. On the demand side, with the prospect of a double dip recession decreasing, emerging markets are expected to drive increased global oil demand. We expect the range to hold in the near-term, as neither the supply nor the demand picture is likely to change dramatically.

Natural gas bottomed in the fall of 2009 at just under $2.00/Mcf with industrial demand reaching its lows and supplies accumulating to record highs. Henry Hub prices received support in the December to March time frame because of higher than normal heating degree days, which resulted in a draw of inventories down towards more normal levels (see Page 12). However, this strength was short-lived and except for a brief flirtation with $5.00/Mcf during an especially hot summer, Henry Hub prices have straddled the $4.00/Mcf level. In 2010, the U.S. gas rig count has increased ~30% and the horizontal rig count (primarily shale gas drilling) is up ~60% (see Pages 15 and 16). Prices should continue the temperature-driven grind upwards over the next few months but with the increasing production profile, we expect a heavy inventory build out of the winter withdrawal season and continued Henry Hub weakness.

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

$7.00

Henry Hub Natural Gas

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

$65.00

$70.00

$75.00

$80.00

$85.00

$90.00

$95.00

WTI Crude Oil

Page 12

Natural Gas Inventories

Source: Department of Energy

Commentary

The second half of 2009 saw a glut of natural gas, with demand from residential customers, industrials, and power producers waning and producers continuing to ramp up production. Beginning in June 2009, natural gas inventories hit 5-year highs as the 2009 summer was cooler than normal throughout the U.S. Inventory levels dropped slightly at the beginning of 2010, with a cold winter spurring heating and electricity demand. But the prevailing theme over the last 24 months has been the mismatch between supply and demand – the unconventional gas boom has increased potential United States gas reserves substantially while industrial demand has weakened. According to the Department of Energy, U.S. proved shale gas reserves increased ~50% from 22 Tcf to 33 Tcf from 2007 to 2008; total U.S. gas reserves were 245 Tcf at the end of 2008. We expect total reserve growth to continue to be driven by shale gas additions over the next decade. Further, U.S. natural gas production increased ~3% in 2009 and ~2% during the first half of 2010. In terms of demand, industrial consumption of natural gas (which represents ~1/3 of total consumption) has remained weak – 2009 consumption was down ~8% versus 2008 and while 2010 levels were better than last year, they are still approximately 4% below H1 2008 levels.

A hotter than normal 2010 summer eased inventories from their 5-year highs and as a result Henry Hub prices topped $5.00/Mcf briefly. However, a legitimate oversupply reapplied pressure to gas prices into year-end and inventories are back to last year’s 5-year highs. Inventory levels during the first quarter of the year may dip based on weather, but we expect continued elevated levels throughout 2011.

3,232

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Natural Gas Inventories (Bcf)

5-Year Range 2009 2010 5-Year Average

Natural Gas Inventories

2010 Inventories Change 2009 Inventories Change 5-Year Avg. Variance

11/19/2010 3,828 (7) 11/20/2009 3,835 2 3,612 216

11/26/2010 3,805 (23) 11/27/2009 3,837 2 3,571 234

12/3/2010 3,716 (89) 12/4/2009 3,773 (64) 3,496 220

12/10/2010 3,552 (164) 12/11/2009 3,566 (207) 3,339 213

12/17/2010 3,368 (184) 12/18/2009 3,400 (166) 3,193 175

12/24/2010 3,232 (136) 12/25/2009 3,276 (124) 3,085 147

Crude Oil and Refined Products Inventories

Page 13 Source: Department of Energy

250,000

270,000

290,000

310,000

330,000

350,000

370,000

390,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Crude Inventories (MBbl)

5-Year Range 2009 2010 5-Year Average

170,000

180,000

190,000

200,000

210,000

220,000

230,000

240,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Gasoline Inventories (MBbl)

5-Year Range 2009 2010 5-Year Average

100,000

110,000

120,000

130,000

140,000

150,000

160,000

170,000

180,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Distillate Inventories (MBbl)

5-Year Range 2009 2010 5-Year Average

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Heating Oil Inventories (MBbl)

5-Year Range 2009 2010 5-Year Average

Oil-Gas Ratio

Page 14 Source: Bloomberg, Nomura Securities International.

CommentaryOver the past 10 years, the oil-gas ratio has averaged approximately 8x. 2009 represented an extreme (average ratio of ~17x) because of the combination of severe natural gas demand erosion and increasing supplies. A new range for the ratio appears to have emerged, however, as the average in 2010 was roughly 19x. Industrial demand has rebounded from the 2009 lows and weather-induced electricity demand has been strong the last 12 months without a large reaction in natural gas prices. Meanwhile, oil prices had been range-bound between $70 and $85/Bbl for much of 2010 before breaking through $90/Bbl in December, correlating with broader global commodities. As a result, several companies have adjusted their capex programs, allocating more capital to oil and liquids-rich projects in order to maximize returns. This is also illustrated in the subsequent rig count data (see Pages 8 and 9) – the U.S. oil rig count has increased over 250% from the June 2009 low, while the U.S. gas rig count is up just under 50%. We expect the oil-gas ratio to remain above historical levels in the near-term, thus continuing to favor oil-weighted producers.

-

5

10

15

20

25

30

35

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Oil-Gas Ratio

5-Year Range 2009 2010 5-Year Average

Rig Counts

Page 15 Source: Baker Hughes Inc.

-

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

U.S. Rig Count

-

250

500

750

1,000

1,250

International Rig Count

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

U.S. Gas Rig Count

-

100

200

300

400

500

600

700

800

900

U.S. Oil Rig Count

Rig Counts

Page 16 Source: Baker Hughes Inc.

-

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

U.S. On Land Rig Count

-

20

40

60

80

100

120

140

160

180

U.S. Offshore Rig Count

-

100

200

300

400

500

600

700

800

900

1,000

U.S. Horizontal Rig Count

-

100

200

300

400

500

600

700

800

900

1,000

1,100

U.S. Vertical Rig Count

Exploration & Production Recommendations

Page 17

Page 18

Relative Value

Source: Company Filings, Nomura Securities International.

Issuer Ratings

Outst.

$mn

Coupon

(%) Maturity STW Z-Sprd Price YTW

Reserves

(Boe)

LTM

EBITDA(X)

Debt /

EBITDA(X)

Debt /

Boe

Apache Corp. Sr. Notes A3 / A- 500 3.625 2/1/2021 72 66 96.18 4.09 2,974 8,231 1.0x 2.14

A3 / A- 1,500 5.100 9/1/2040 91 129 94.50 5.48

A3 / A- 500 5.250 2/1/2042 91 128 96.61 5.48

Anadarko Petroleum Sr. Notes Ba1 / BBB- 1,750 5.950 9/15/2016 220 181 108.95 4.16 2,304 6,737 2.0x 5.53

Ba1 / BBB- 2,000 6.375 9/15/2017 264 195 110.09 4.60

Ba1 / BBB- 300 6.950 6/15/2019 196 231 110.83 5.33

Ba1 / BBB- 600 8.700 3/15/2019 180 224 123.21 5.17

Ba1 / BBB- 1,750 6.450 9/15/2036 213 265 96.98 6.70

Ba1 / BBB- 750 6.200 3/15/2040 208 256 94.26 6.65

Canadian Natural Res. Sr. Notes Baa1 / BBB 1,100 5.700 5/15/2017 140 79 113.24 3.36 3,557 7,284 1.2x 2.72

Baa1 / BBB 400 5.900 2/1/2018 30 91 113.69 3.67

Baa1 / BBB 1,100 6.250 3/15/2038 107 151 108.46 5.64

Cenovus Energy Sr. Notes Baa2 / BBB+ 1,299 5.700 10/15/2019 60 84 112.64 3.97 1,398 3,024 1.2x 2.62

Baa2 / BBB+ 1,400 6.750 11/15/2039 120 164 113.72 5.77

Devon Energy Sr. Notes Baa1 / BBB+ 700 6.300 1/15/2019 41 81 117.21 3.78 2,624 4,875 1.2x 2.66

Baa1 / BBB+ 1,000 7.950 4/15/2032 95 153 130.20 5.52

EnCana Corp. Sr. Notes Baa2 / BBB+ 700 5.900 12/1/2017 165 89 113.84 3.61 1,920 5,460 1.4x 4.05

Baa2 / BBB+ 500 6.500 5/15/2019 59 93 117.83 3.96

Baa2 / BBB+ 500 6.625 8/15/2037 149 197 107.45 6.06

Baa2 / BBB+ 800 6.500 2/1/2038 150 197 105.72 6.07

Hess Corp. Sr. Notes Baa2 / BBB 1,000 8.125 2/15/2019 88 131 126.21 4.25 1,482 6,574 0.8x 3.11

Baa2 / BBB 750 6.000 1/15/2040 118 160 103.55 5.75

Baa2 / BBB 1,250 5.600 2/15/2041 120 160 97.62 5.77

Marathon Oil Sr. Notes Baa1 /*- / BBB+ /*- 687 7.500 2/15/2019 44 85 125.40 3.81 1,076 7,247 1.1x 7.93

Baa1 /*- / BBB+ /*- 750 6.600 10/1/2037 112 158 112.45 5.69

Nexen Inc. Sr. Notes Baa3 /*- / BBB- 300 6.200 7/30/2019 165 195 108.12 5.02 881 3,929 1.4x 7.89

Baa3 /*- / BBB- 1,250 6.400 5/15/2037 207 258 97.07 6.64

Baa3 /*- / BBB- 700 7.500 7/30/2039 218 270 109.49 6.75

Noble Energy Sr. Notes Baa2 / BBB 1,000 8.250 3/1/2019 110 153 125.46 4.47 841 2,130 1.0x 2.48

Baa2 / BBB 250 8.000 4/1/2027 162 240 118.37 6.19

Talisman Energy Sr. Notes Baa2 / BBB 600 3.750 2/1/2021 115 110 93.81 4.52 1,118 4,441 0.8x 3.18

Baa2 / BBB 600 6.250 2/1/2038 130 175 105.16 5.87

Page 19

Relative Value

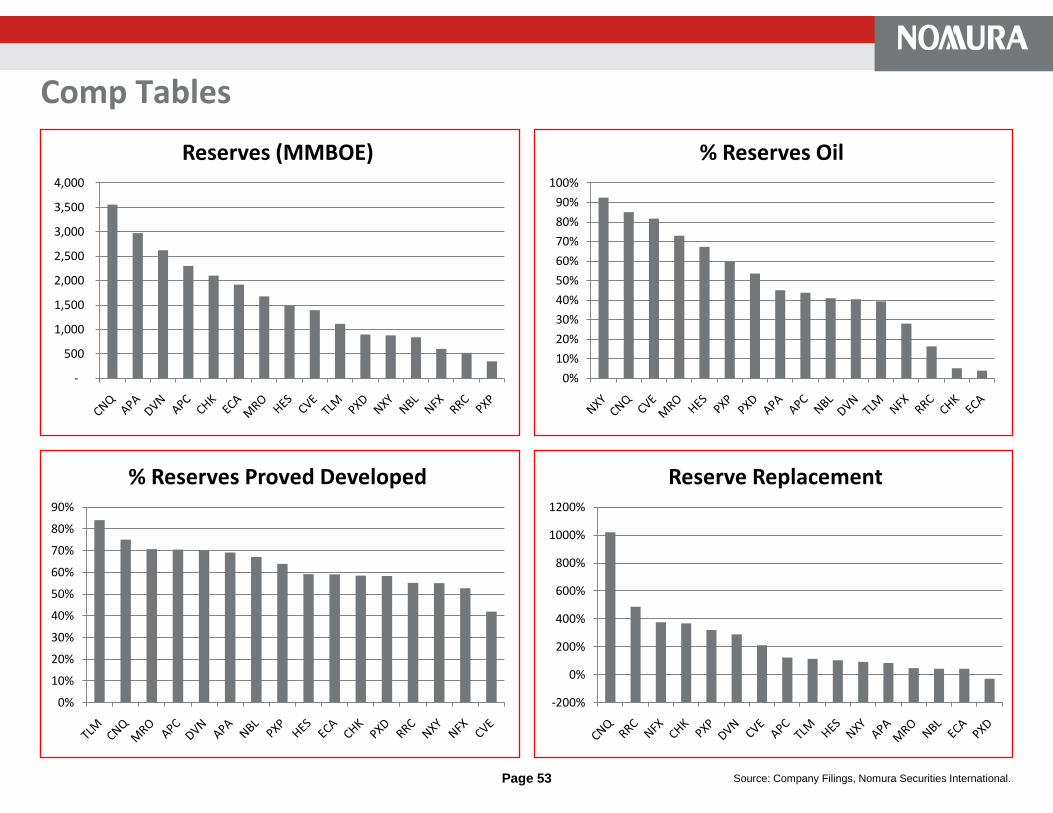

Debt/Proved Reserves metrics for the following companies are typically in $/Mcfe: Chesapeake ($0.86/Mcfe); Newfield ($0.56/Mcfe); and Range Resources ($0.54/Mcfe)

Source: Company Filings, Nomura Securities International.

Issuer Ratings

Outst.

$mn

Coupon

(%) Maturity STW Z-Sprd Price YTW Next Call

Reserves

(Boe)

LTM

EBITDA(X)

Debt /

EBITDA(X)

Debt /

Boe

Chesapeake Energy Sr. Notes Ba3 / BB 1,425 9.500 2/15/2015 312 338 116.00 5.09 2,102 5,099 2.2x 5.18

Ba3 / BB 1,100 6.500 8/15/2017 410 345 102.25 6.08

Ba3 / BB 600 6.875 8/15/2018 268 376 103.75 6.07 8/15/2013

Ba3 / BB 800 7.250 12/15/2018 281 327 106.50 6.20

Ba3 / BB 1,400 6.625 8/15/2020 289 303 102.50 6.27

Ba3 / BB 499 6.875 11/15/2020 307 318 103.00 6.46

Newfield Exploration Sr. Subordinated Ba2 / BB+ 550 6.625 4/15/2016 253 423 103.75 4.50 4/15/2011 603 1,208 1.8x 3.38

Ba2 / BB+ 600 7.125 5/15/2018 173 417 107.50 5.11 5/15/2013

Ba2 / BB+ 700 6.875 2/1/2020 209 376 107.75 5.48 2/1/2015

Pioneer Natural Res. Sr. Notes Ba1 / BB+ 455 5.875 7/15/2016 301 268 104.25 4.98 899 1,248 2.0x 3.07

Ba1 / BB+ 485 6.650 3/15/2017 337 284 106.75 5.35

Ba1 / BB+ 450 6.875 5/1/2018 234 293 106.75 5.73

Ba1 / BB+ 450 7.500 1/15/2020 255 281 110.75 5.94

Ba1 / BB+ 250 7.200 1/15/2028 232 306 103.00 6.90

Plains E&P Sr. Notes B1 / BB- 600 7.750 6/15/2015 269 435 105.00 4.67 6/15/2011 349 985 2.8x 7.37

B1 / BB- 565 10.000 3/1/2016 343 456 113.50 5.41 3/1/2013

B1 / BB- 500 7.000 3/15/2017 405 427 103.50 6.03 3/15/2012

B1 / BB- 400 7.625 6/1/2018 265 507 106.75 6.04 6/1/2013

B1 / BB- 400 8.625 10/15/2019 321 502 110.00 6.59 10/15/2014

B1 / BB- 300 7.625 4/1/2020 272 433 108.50 6.11 4/1/2015

Range Resources Sr. Subordinated Ba3 / BB 150 6.375 3/15/2015 326 474 102.25 5.24 2/18/2011 521 609 3.0x 3.28

Ba3 / BB 250 7.500 5/15/2016 287 455 104.50 4.85 5/15/2011

Ba3 / BB 250 7.500 10/1/2017 388 518 106.00 5.86 10/1/2012

Ba3 / BB 250 7.250 5/1/2018 250 450 106.00 5.89 5/1/2013

Ba3 / BB 300 8.000 5/15/2019 252 451 109.50 5.91 5/15/2014

Ba3 / BB 500 6.750 8/1/2020 269 322 104.00 6.08 8/1/2015

Page 20 Source: Company Filings, Nomura Securities International.

Anadarko Petroleum Company (APC)

Relative Value

We maintain our HOLD recommendation on Anadarko senior notes. We are comfortable holding the APC senior notes at current levels and we still see longer-term upside once the Macondo liability is resolved. However, we view current spreads as somewhat full given our spread targets and the uncertainty/risk still surrounding the situation.

Note that the APC 2019s trade roughly 120 bp through high yield benchmark issuer Chesapeake Energy and roughly 80 bp outside of wider-trading IG names like Talisman Energy. Under our base case scenario where APC is responsible for $5-8bn in spill liabilities, we would expect split-rated (Ba1/BBB-/BBB-) APC to trade roughly 50-75 bp behind TLM.

Business Description

Anadarko Petroleum Corporation is one of the world’s largest independent oil and gas producers, with proved reserves of 2.3 billion barrels of oil equivalent and operations in the United States, Brazil, Africa, China, and Indonesia. In 2009, the company produced 603 MBoe/d of hydrocarbons, approximately 60% of which was natural gas. In addition to its oil and gas operations, Anadarko owns natural gas gathering, processing, treating, and transportation assets in the United States. Anadarko’s major growth projects include the Marcellus, Eagle Ford, and Haynesville shale plays and self-titled “Mega Projects” in the Gulf of Mexico and Africa.

Company SnapshotReserves (MMBoe) 2,304

% Oil 44%

% Proved Developed 70%

Reserve Life (R/P) 10.5

Daily Production (MBoe/d) 629

LTM EBITDAX 6,737

2011 EBITDAX 7,374

Cash 4,218

Total Debt 13,471

Market Capitalization 37,566

Enterprise Value 46,819

Debt/EBITDAX 2.0x

Debt/Reserves 5.85

EV/EBITDAX 6.9x

EV/Reserves 20.32

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Ba1 / BBB- 1,750 5.950 9/15/2016 220 181 108.79 4.19

Sr. Notes Ba1 / BBB- 2,000 6.375 9/15/2017 264 196 109.97 4.62

Sr. Notes Ba1 / BBB- 300 6.950 6/15/2019 196 230 110.71 5.35

Sr. Notes Ba1 / BBB- 600 8.700 3/15/2019 180 223 123.10 5.19

Sr. Notes Ba1 / BBB- 1,750 6.450 9/15/2036 213 265 96.76 6.72

Sr. Notes Ba1 / BBB- 750 6.200 3/15/2040 208 256 94.03 6.67

Anadarko Petroleum Company (APC)

Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

U.S. Onshore75%

Deepwater GOM12%

International13%

2010 Capital Expenditures

U.S. Onshore44%

International30%

Gulf of Mexico16%

Midstream/ Other12%

Financial Summary

2008 2009 2010E 2011E

EBITDAX 9,304 4,341 6,659 7,374

Operating Cash Flow 6,464 3,926 5,159 5,533

Capital Expenditures (4,801) (4,352) (5,013) (5,400)

Dividends (171) (176) (182) (184)

Free Cash Flow 1,492 (602) (36) (51)

Divestitures 2,455 176 44 -

Share Repurchases (676) (35) (35) -

Adjusted Cash Flow 3,271 (461) (27) (51)

Cash 2,360 3,531 2,917 2,581

Debt/EBITDAX 1.3x 2.9x 1.8x 1.6x

Net Debt/EBITDAX 1.1x 2.1x 1.3x 1.2x

Operations Summary

2008 2009 2010E 2011E

Production (MBoe/d) 563 603 649 693

Realized Price ($/Boe) 60.97 33.96 42.52 44.32

Lease Operating Expenses 8.04 6.92 6.76 6.95

Production Taxes 7.05 3.39 4.70 5.36

G&A 4.20 4.47 3.94 3.73

Interest 3.55 3.19 3.45 3.01

Cash Costs 22.84 17.97 18.84 19.04

F&D Costs 24.37 16.93

Full Cycle Costs 47.21 34.90

Recycle Ratio 1.56 0.94

Page 21

Page 22 Source: Company Filings, Nomura Securities International.

Relative Value

We are revising our BUY rating to HOLD on APA senior notes.

We had previously expressed the view that APA’s recent acquisition spree provided an opportunity to buy APA paper at a discount to historical trading levels. We still view APA as a core holding in the high-quality energy space, with levels now more in-line with single-A rated energy names, the trade has largely played out and we see little opportunity for material tightening/outperformance from current levels.

Apache Corporation (APA)

Business Description

Apache Corporation is one of the world’s largest independent exploration and production companies with proved reserves of approximately 3 billion barrels of oil equivalent and operations in: the Gulf of Mexico; Gulf Coast; East Texas; Permian Basin; Anadarko Basin; Canadian Western Sedimentary Basin; Egypt; Western Australia; North Sea; and Argentina. In 2009, the company produced 583 MBoe/d, approximately 50% of which was oil. Additionally, Apache owns 51% of Kitimat LNG Inc.’s proposed LNG export terminal in British Columbia (and has reserved 51% of gas throughput capacity in the terminal).

Company SnapshotReserves (MMBoe) 2,974

% Oil 45%

% Proved Developed 69%

Reserve Life (R/P) 11.1

Daily Production (MBoe/d) 667

LTM EBITDA 8,231

2011 EBITDA 11,273

Cash 1,211

Total Debt 8,182

Market Capitalization 48,265

Enterprise Value 55,235

Debt/EBITDA 1.0x

Debt/Reserves 2.75

EV/EBITDA 6.7x

EV/Reserves 18.57

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes A3 / A- 500 3.625 2/1/2021 72 66 96.07 4.11

Sr. Notes A3 / A- 1,500 5.100 9/1/2040 91 129 94.32 5.49

Sr. Notes A3 / A- 500 5.250 2/1/2042 91 129 96.42 5.49

Page 23 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Pro Forma Production

Gulf Coast, 13%

Central U.S., 27%

Canada, 22%

Egypt, 13%

Australia, 13%

North Sea, 7% Argentina, 5%

Egypt, 22%

Canada, 15%

GOM DW, 2%GOM Shelf, 17%Gulf Coast

Onshore, 2%

Central U.S., 5%

Permian, 12%

Argentina, 6%

Australia, 12%North Sea, 7%

Apache Corporation (APA)

Financial Summary

2008 2009 2010E 2011E

EBITDA 8,988 5,846 8,831 11,273

Operating Cash Flow 7,065 4,224 6,748 8,937

Capital Expenditures (5,823) (3,631) (5,019) (7,200)

Dividends (239) (209) (203) (204)

Free Cash Flow 1,003 384 1,527 1,533

Acquisitions (150) (310) (7,450) -

Divestitures 308 2 - -

Share Repurchases - - - -

Adjusted Cash Flow 1,161 76 (5,924) 1,533

Cash 1,181 2,048 1,165 2,698

Debt/EBITDA 0.5x 0.9x 0.9x 0.7x

Net Debt/EBITDA 0.4x 0.5x 0.8x 0.5x

Operations Summary

2008 2009 2010E 2011E

Production (MBoe/d) 534 583 672 823

Realized Price ($/Boe) 63.04 40.27 49.39 51.11

Lease Operating Expenses 9.76 7.81 8.04 8.10

Production Taxes 5.03 2.72 2.95 3.25

G&A 1.48 1.62 1.60 1.66

Interest 0.85 1.14 1.14 1.45

Cash Costs 17.12 13.28 13.73 14.46

F&D Costs 25.97 17.95

Full Cycle Costs 43.09 31.23

Recycle Ratio 1.77 1.50

Page 24 Source: Company Filings, Nomura Securities International.

Canadian Natural Resources Ltd. (CNQ)

Relative Value

We are maintaining our BUY recommendation on Canadian Natural Resources (CNQ) senior notes. We are attracted to CNQ’s exposure to crude oil pricing (70% of production), low leverage, and free cash flow profile. We view the company as a core holding in the large independent E&P universe.

From a tactical perspective, we are cognizant that the company may access the debt markets to refinance recent and pending maturities (C$400mn 12/2010 and $400mn 7/2011) and its outstanding revolver draws (C$1.4B at 9/30/10). We believe that new issuance may provide an attractive opportunity to establish or add to existing positions.

We are monitoring the recent (January 2011) damage to the Horizon oil sands project (15% production). Our initial impression is that the damage will be disruptive in the short-term but likely prove to be manageable based on the industry’s historical experience with oil sands accidents. There remains little information available on Horizon, but typical incidents at competitor Suncor have resulted in 2-6 months of downtime. CNQ maintains a C$2bn umbrella policy that covers business interruptions after 90 days.

Business Description

Canadian Natural Resources Ltd. is one of the world’s largest independent exploration and production companies, with approximately 3.6 billion barrels of oil equivalent of proved reserves. With 90% of its production and reserves located in North America, CNQ is the largest heavy oil producer in Canada and 2nd largest independent natural gas producer in Canada. Canadian Natural’s Horizon Oil Sands began development in 2005 and are estimated to contain 16 billion barrels of oil in place and 6-8 billion barrels of mineable reserves and contingent resources. In addition to its North American assets, CNQ has reserves in the North Sea and Offshore West Africa.

Company SnapshotReserves (MMBoe) 3,557

% Oil 85%

% Proved Developed 75%

Reserve Life (R/P) 17.0

Daily Production (MBoe/d) 621

LTM EBITDA 7,284

2011 EBITDA 8,685

Cash 27

Total Debt 8,490

Market Capitalization 45,263

Enterprise Value 53,726

Debt/EBITDA 1.2x

Debt/Reserves 2.39

EV/EBITDA 7.4x

EV/Reserves 15.10

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa1 / BBB 1,100 5.700 5/15/2017 140 79 113.12 3.38

Sr. Notes Baa1 / BBB 400 5.900 2/1/2018 30 90 113.60 3.69

Sr. Notes Baa1 / BBB 1,100 6.250 3/15/2038 107 151 108.27 5.65

Canadian Natural Resources Ltd. (CNQ)

Page 25 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

North America89%

North Sea7%

West Africa4%

North America Conventional

68%

North Sea6%

West Africa7%

Horizon19%

Financial Summary

2008 2009 2010E 2011E

EBITDA 9,520 5,741 7,455 8,685

Operating Cash Flow 6,767 5,812 6,299 6,643

Capital Expenditures (7,433) (2,985) (4,963) (5,800)

Dividends (208) (225) (301) (324)

Free Cash Flow (874) 2,602 1,035 519

Acquisitions - - - -

Divestitures 20 36 3 -

Share Repurchases - - - -

Adjusted Cash Flow (854) 2,638 1,038 519

Cash 27 13 109 228

Debt/EBITDA 1.4x 1.7x 1.2x 1.0x

Net Debt/EBITDA 1.4x 1.7x 1.2x 1.0x

Operations Summary

2008 2009 2010E 2011E

Production (MBoe/d) 565 575 631 676

Realized Price ($/Boe) 68.26 44.15 52.98 59.76

Lease Operating Expenses 21.22 20.05 22.31 20.50

Production Taxes 0.86 0.51 0.59 0.65

G&A 0.87 0.86 0.93 0.95

Interest 0.62 1.95 1.95 2.05

Cash Costs 23.57 23.37 25.78 24.15

F&D Costs 18.81 1.48

Full Cycle Costs 42.38 24.85

Recycle Ratio 2.38 14.01

Page 26 Source: Company Filings, Nomura Securities International.

Cenovus Energy Inc. (CVE)

Relative Value

We are affirming our BUY recommendation on Cenovus Energy senior notes. We still recommend swapping out of EnCana 6.5% of 2019 into Cenovus 5.7% of 2019 for roughly flat spread and a take-out of $5 in dollar price. We prefer CVE’s exposure to crude oil pricing (~50% liquids volumes compared with EnCana’s pure-play natural gas) and superior free cash flow profile (we expect EnCana to generate negative free cash flow in 2011).

We are attracted to the longer-term potential of Cenovus’s best in class oil sands operations at Christina Lake and Foster Creek. While oil sands production currently accounts for ~20% of volumes, CVE plans to steadily ramp up production to 200 MBbl/d by 2018 with staged expansion programs. The conventional natural gas (50% production) and liquids (30% production) operations provide a good measure of stability, generating $1-1.5bn of annual free cash flow. With company-wide capital expenditures peaking in 2010, CVE should generate roughly $300mn in free cash flow in 2011.

Business Description

Cenovus Energy Inc. is an integrated oil company headquartered in Calgary, Alberta. Its operations include enhanced oil recovery properties and established oil and natural gas production in Alberta and Saskatchewan. Cenovus has approximately 1.4 billion barrels of oil equivalent of proven reserves, 80% of which are oil. CVE began independent operations on December 1, 2009 following the arrangement with EnCana Corporation in which two independent publicly traded companies (Cenovus and EnCana) were created. Cenovus’s enhanced oil recovery projects include Foster Lake, Christina Lake, and Pelican Lake, located in the Athabasca region in northeast Alberta. In addition to its upstream assets, Cenovus owns a 50% stake in two refineries in the United States: Wood River in Illinois and Borger in Texas (ConocoPhillips is the other 50% owner and the operator of both refineries).

Company SnapshotReserves (MMBoe) 1,398

% Oil 82%

% Proved Developed 42%

Reserve Life (R/P) 14.6

Daily Production (MBoe/d) 251

LTM EBITDA 3,024

2011 EBITDA 3,669

Cash 464

Total Debt 3,574

Market Capitalization 24,234

Enterprise Value 27,344

Debt/EBITDA 1.2x

Debt/Reserves 2.56

EV/EBITDA 9.0x

EV/Reserves 19.56

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa2 / BBB+ 1,299 5.700 10/15/2019 60 83 112.53 3.99

Sr. Notes Baa2 / BBB+ 1,400 6.750 11/15/2039 120 165 113.35 5.79

Page 27 Source: Company Filings, Nomura Securities International.

2009 Production

2010 Capital Expenditures

Foster Creek15%

Christina Lake3%

Athabasca3%

Other Bitumen1%

Weyburn6%

Pelican Lake8%

Southern Alberta

59%

Other Canadian

Plains5%

Cenovus Energy Inc. (CVE)

Financial Summary

Operations Summary

Foster Creek15%

Christina Lake14%

Pelican Lake, Other Oil

28%

Natural Gas10%

Refining33%

Financial Summary2008 2009 2010E 2011E

EBITDA 4,665 3,280 3,146 3,669

Operating Cash Flow 2,845 3,039 2,628 3,089

Capital Expenditures (2,046) (2,165) (2,104) (2,200)

Dividends - (159) (600) (600)

Free Cash Flow 799 715 (76) 289

Acquisitions - - - -

Divestitures 47 222 312 -

Share Repurchases - - - -

Adjusted Cash Flow 846 937 236 289

Cash 188 155 356 645

Debt/EBITDA 0.8x 1.1x 1.1x 1.0x

Net Debt/EBITDA 0.8x 1.1x 1.0x 0.8x

2008 2009 2010E 2011E

Production (MBoe/d) 271 262 253 243

Realized Price ($/Boe) 57.89 52.07 48.37 55.17

Lease Operating Expenses 23.30 21.71 25.89 26.50

Production Taxes 0.81 0.46 0.36 0.30

G&A 1.72 2.21 2.41 2.80

Interest 2.35 2.56 2.98 2.85

Cash Costs 28.17 26.94 31.63 32.45

F&D Costs 28.39 4.76 4.76 4.76

Full Cycle Costs 56.56 31.70 36.40 37.21

Recycle Ratio 1.05 5.28 3.51 4.77

Page 28 Source: Company Filings, Nomura Securities International.

Chesapeake Energy Corporation (CHK)

Relative ValueWe are affirming our HOLD recommendation on Chesapeake Energy senior notes. We view benchmark issuer Chesapeake as a core holding in the HY energy space. CHK has assembled a well diversified, premier-quality asset base in key North American plays. Further, the company continues to post strong organic production and reserve growth.

We view the recent strategic shift toward liquids production (25% production volume target by 2015) as positive, but we remain cognizant of the attendant risks. We acknowledge Chesapeake’s demonstrated success in executing large-scale development of unconventional resource plays. That said, transforming one of the largest natural gas producers toward liquids production carries a measure of operational risk. Management recently (Jan 2011) announced the so-called “25/25” plan, which aims to dial back growth over the next 2 years to 25% from its previous targeted of 30-40%, and to reduce debt by 25% over the same period. CHK plans to achieve these goals through reduced acreage acquisitions and additional asset monetizations. After +$4.5bn of acreage acquisitions in 2010, we view the plan as conservative but we note that CHK will remain free cash flow negative and reliant on asset sales/monetization to make up cash short-falls.

Business Description

Chesapeake Energy Corporation is one of the largest independent exploration and production companies in the world. Chesapeake has approximately 13 trillion cubic feet equivalent of proved reserves and current production of 2.8 Bcfe/d, 90% of which is natural gas. Its core holdings are in the “Big 6” natural gas shale plays: Barnett; Bossier; Fayetteville; Eagle Ford; Haynesville; and Marcellus. In addition to its substantial E&P assets, Chesapeake owns 50% of the General Partner, the associated Incentive Distribution Rights, and approximately 41% of the limited partner units of Chesapeake Midstream Partners (CHKM), a master limited partnership with 2,800 miles of gathering pipelines and approximately 1.5 Bcf/d of natural gas gathering capacity.

Company SnapshotReserves (Bcfe) 16,900

% Gas 95%

% Proved Developed 58%

Reserve Life (R/P) 15.7

Daily Production (MMcfe/d) 3,043

LTM EBITDA(X) 5,099

2011 EBITDA(X) 5,257

Cash 609

Total Debt 11,445

Market Capitalization 18,064

Enterprise Value 31,965

Debt/EBITDAX 2.2x

Debt/Reserves 0.68

EV/EBITDA(X) 6.3x

EV/Reserves 1.89

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Ba3 / BB 1,425 9.500 2/15/2015 312 338 116.00 5.09

Sr. Notes Ba3 / BB 1,100 6.500 8/15/2017 410 345 102.25 6.08

Sr. Notes Ba3 / BB 600 6.875 8/15/2018 268 376 103.75 6.07

Sr. Notes Ba3 / BB 800 7.25 12/15/2018 281 327 106.50 6.20

Sr. Notes Ba3 / BB 499 6.875 11/15/2020 307 318 103.00 6.46

Sr. Notes Ba3 / BB 1,400 6.625 8/15/2020 289 303 102.50 6.27

Chesapeake Energy Corporation (CHK)

Page 29 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2009 Capital Expenditures

Barnett Shale, 24%

Fayetteville Shale, 15%

Haynesville Shale, 13%

Marcellus Shale, 2%

Mid-Continent, 29%

Permian & Delaware Basins, 5%

S. Texas/Gulf/Ark-

La-Tex, 4%

Appalachian Basin, 8%

Barnett Shale34%

Fayetteville Shale

5%

Haynesville Shale21%

Marcellus Shale4%

Mid-Continent20%

Permian & Delaware Basins

9%

S. Texas/Gulf/Ark-

La-Tex6%

Appalachian Basin

1%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

Production (MMcfe/d) 2,303 2,481 2,797 3,315

Realized Price ($/Mcfe) 8.38 6.22 4.38 6.62

Lease Operating Expenses 1.05 0.97 0.90 0.90

Production Taxes 0.34 0.12 0.28 0.30

G&A 0.45 0.39 0.35 0.35

Interest 0.82 0.91 0.83 0.85

Cash Costs 2.65 2.38 2.36 2.40

F&D Costs 2.41 1.07

Full Cycle Costs 5.06 3.46

Recycle Ratio 2.38 3.58

2008 2009 2010E 2011E

EBITDAX 5,851 4,509 4,914 5,257

Operating Cash Flow 5,236 4,356 4,766 4,563

Capital Expenditures (9,177) (5,226) (6,785) (6,600)

Dividends (183) (204) (278) (352)

Free Cash Flow (4,124) (1,074) (2,297) (2,389)

Acquisitions (8,472) (2,298) (4,568) (1,000)

Divestitures 7,670 1,926 4,555 3,200

Share Repurchases (5) (7) - -

Adjusted Cash Flow (4,931) (1,453) (2,310) (189)

Cash 1,749 307 609 925

Debt/EBITDAX 2.3x 2.7x 2.4x 2.3x

Net Debt/EBITDAX 2.0x 2.7x 2.3x 2.1x

Page 30 Source: Company Filings, Nomura Securities International.

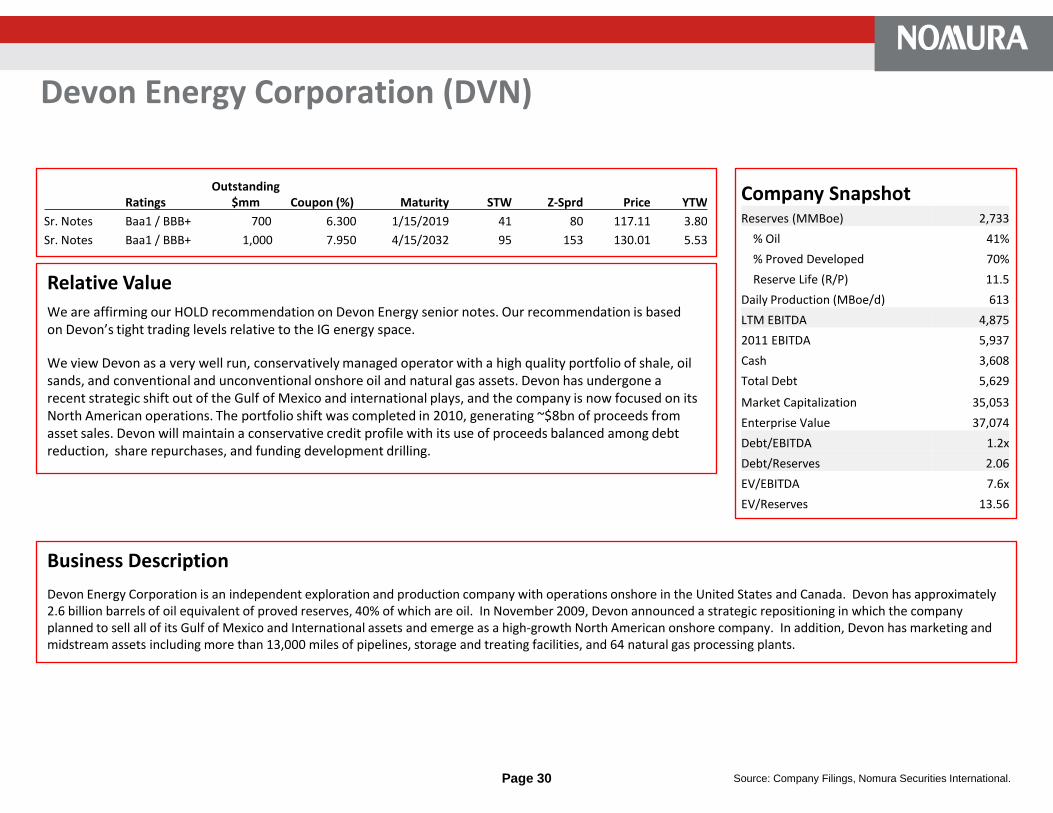

Devon Energy Corporation (DVN)

Relative Value

We are affirming our HOLD recommendation on Devon Energy senior notes. Our recommendation is based on Devon’s tight trading levels relative to the IG energy space.

We view Devon as a very well run, conservatively managed operator with a high quality portfolio of shale, oil sands, and conventional and unconventional onshore oil and natural gas assets. Devon has undergone a recent strategic shift out of the Gulf of Mexico and international plays, and the company is now focused on its North American operations. The portfolio shift was completed in 2010, generating ~$8bn of proceeds from asset sales. Devon will maintain a conservative credit profile with its use of proceeds balanced among debt reduction, share repurchases, and funding development drilling.

Business Description

Devon Energy Corporation is an independent exploration and production company with operations onshore in the United States and Canada. Devon has approximately 2.6 billion barrels of oil equivalent of proved reserves, 40% of which are oil. In November 2009, Devon announced a strategic repositioning in which the company planned to sell all of its Gulf of Mexico and International assets and emerge as a high-growth North American onshore company. In addition, Devon has marketing and midstream assets including more than 13,000 miles of pipelines, storage and treating facilities, and 64 natural gas processing plants.

Company SnapshotReserves (MMBoe) 2,733

% Oil 41%

% Proved Developed 70%

Reserve Life (R/P) 11.5

Daily Production (MBoe/d) 613

LTM EBITDA 4,875

2011 EBITDA 5,937

Cash 3,608

Total Debt 5,629

Market Capitalization 35,053

Enterprise Value 37,074

Debt/EBITDA 1.2x

Debt/Reserves 2.06

EV/EBITDA 7.6x

EV/Reserves 13.56

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa1 / BBB+ 700 6.300 1/15/2019 41 80 117.11 3.80

Sr. Notes Baa1 / BBB+ 1,000 7.950 4/15/2032 95 153 130.01 5.53

Devon Energy Corporation (DVN)

Page 31 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

Shale Plays, 47%

Oil Sands, 12%

Conventional Plays, 23%

Other Unconventional,

18%

Barnett39%

Carthage7%Permian

5%Washakie

3%Cana-Woodford

3%

Arkoma-Woodford

2%

Groesbeck2%

Other U.S.11%

Jackfish15%

Northwest4%

Lloydminster3%

Deep Basin2%

Other Canada4%

Financial Summary

2008 2009 2010E 2011E

EBITDA 9,429 3,977 5,288 5,941

Operating Cash Flow 9,408 4,737 5,475 4,920

Capital Expenditures (8,843) (4,879) (6,043) (5,200)

Dividends (289) (284) (283) (288)

Free Cash Flow 276 (426) (851) (568)

Acquisitions - - (500) -

Divestitures 117 34 8,391 -

Share Repurchases (665) - (1,679) (1,500)

Adjusted Cash Flow (272) (392) 5,361 (2,068)

Cash 195 646 6,535 2,717

Debt/EBITDA 0.6x 1.8x 0.7x 0.6x

Net Debt/EBITDA 0.6x 1.7x -0.5x 0.2x

Operations Summary

2008 2009 2010E 2011E

Production (MBoe/d) 610 649 626 652

Realized Price ($/Boe) 52.23 34.54 37.04 34.17

Lease Operating Expenses 7.90 7.05 7.40 7.25

Production Taxes 2.03 1.32 1.59 1.28

G&A 2.75 2.73 2.40 2.70

Interest 1.40 1.47 1.66 1.66

Cash Costs 14.08 12.58

F&D Costs 79.24 5.83

Full Cycle Costs 93.33 18.41

Recycle Ratio 0.48 3.77

Page 32 Source: Company Filings, Nomura Securities International.

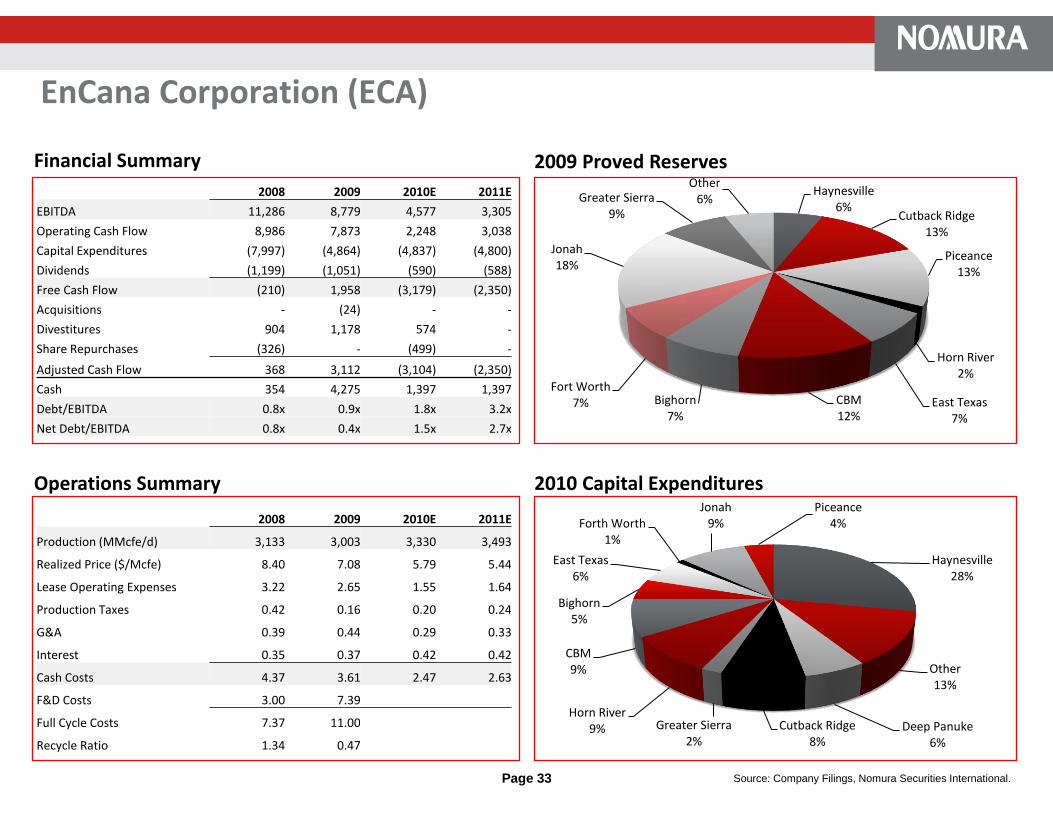

EnCana Corporation (ECA)

Relative Value

We are affirming our SELL recommendation on EnCana Corporation senior notes. Given the more challenging fundamentals in North American natural gas and relatively tight spread range of the IG E&P peer group, we prefer exposure to the more oil-weighted names such as Canadian Natural Resources and Cenovus Energy. With the recent spin-off of Cenovus, EnCana is a pure-play natural gas producer with top-tier North American properties, including considerable acreage in high-potential plays. While we acknowledge the high asset quality and very competitive cost structure, we expect that high development spending and weaker natural gas prices will result in negative free cash flow of $2.3bn in 2011.

Business Description

EnCana Corporation is an independent exploration and production company with operations in North America, stretching from Louisiana to northeast British Columbia. EnCana has approximately 11.5 trillion cubic feet equivalent of proved reserves, 95% of which are natural gas. On November 30, 2009, EnCana completed its corporate reorganization to split into two independent companies – EnCana Corporation, a natural gas company, and Cenovus Energy, Inc., an integrated oil company. EnCana’s major development areas include: the Haynesville Shale; the Horn River Basin; the Montney shale; the Maverick Basin in South Texas; and the Piceance Basin.

Company SnapshotReserves (Bcfe) 11,522

% Gas 96%

% Proved Developed 59%

Reserve Life (R/P) 10.5

Daily Production (MMcfe/d) 3,319

LTM EBITDA 5,460

2011 EBITDA 3,305

Cash 1,397

Total Debt 7,586

Market Capitalization 22,537

Enterprise Value 28,726

Debt/EBITDA 1.4x

Debt/Reserves 0.66

EV/EBITDA 5.3x

EV/Reserves 2.49

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa2 / BBB+ 700 5.900 12/1/2017 165 89 113.70 3.63

Sr. Notes Baa2 / BBB+ 500 6.500 5/15/2019 59 92 117.72 3.98

Sr. Notes Baa2 / BBB+ 500 6.625 8/15/2037 149 197 107.27 6.07

Sr. Notes Baa2 / BBB+ 800 6.500 2/1/2038 150 197 105.54 6.08

EnCana Corporation (ECA)

Page 33 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

Haynesville28%

Other13%

Deep Panuke6%

Cutback Ridge8%

Greater Sierra2%

Horn River9%

CBM9%

Bighorn5%

East Texas6%

Forth Worth1%

Jonah9%

Piceance4%

Haynesville6%

Cutback Ridge13%

Piceance13%

Horn River2%

East Texas7%

CBM12%

Bighorn7%

Fort Worth7%

Jonah18%

Greater Sierra9%

Other6%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

EBITDA 11,286 8,779 4,577 3,305

Operating Cash Flow 8,986 7,873 2,248 3,038

Capital Expenditures (7,997) (4,864) (4,837) (4,800)

Dividends (1,199) (1,051) (590) (588)

Free Cash Flow (210) 1,958 (3,179) (2,350)

Acquisitions - (24) - -

Divestitures 904 1,178 574 -

Share Repurchases (326) - (499) -

Adjusted Cash Flow 368 3,112 (3,104) (2,350)

Cash 354 4,275 1,397 1,397

Debt/EBITDA 0.8x 0.9x 1.8x 3.2x

Net Debt/EBITDA 0.8x 0.4x 1.5x 2.7x

2008 2009 2010E 2011E

Production (MMcfe/d) 3,133 3,003 3,330 3,493

Realized Price ($/Mcfe) 8.40 7.08 5.79 5.44

Lease Operating Expenses 3.22 2.65 1.55 1.64

Production Taxes 0.42 0.16 0.20 0.24

G&A 0.39 0.44 0.29 0.33

Interest 0.35 0.37 0.42 0.42

Cash Costs 4.37 3.61 2.47 2.63

F&D Costs 3.00 7.39

Full Cycle Costs 7.37 11.00

Recycle Ratio 1.34 0.47

Page 34 Source: Company Filings, Nomura Securities International.

Hess Corporation (HES)

Relative Value

We are affirming our SELL recommendation on Hess Corporation senior notes. HES has one of the highest leverage to oil prices given its production mix (~70% liquids) and minimal hedging policy. In addition, HES has amassed a strong position in the very attractive, liquid-rich Bakken shale. Although the area accounts for ~5% of current production, the basin should support longer-term production growth in the US onshore. That said, we note that roughly half of the company’s production is from Africa (Equatorial Guinea, Libya, Algeria, Gabon) and Asia (Malaysia, Thailand, Indonesia) and the company will direct significant capital to higher-risk international prospects. While the current GOM drilling ban will likely not have a material near-term effect on HES’ production profile (~15% volumes), the company does hold significant leases in the Gulf of Mexico and the area remains a key contributor to longer-term production and reserves growth.

Business Description

Hess Corporation is an integrated energy company with operations in Africa, Europe, Russia, South America, Southeast Asia, the United Kingdom, and the United States. Hess has approximately 1.4 billion barrels of oil equivalent of proved reserves, 65% of which are oil. In addition, Hess owns a 50% interest in HOVENSA L.L.C, a refining joint venture in the U.S. Virgin Islands with PDVSA, and a refinery in Port Reading, New Jersey. The company markets refined products, natural gas and electricity in the United States though its 1,357 HESS gasoline stations, 21 storage terminals, and 50% interest in Bayonne Energy Center, LLC.

Company SnapshotReserves (MMBoe) 1,437

% Oil 67%

% Proved Developed 59%

Reserve Life (R/P) 9.7

Daily Production (MBoe/d) 413

LTM EBITDAX 6,574

2011 EBITDAX 6,537

Cash 2,353

Total Debt 5,584

Market Capitalization 27,012

Enterprise Value 30,243

Debt/EBITDAX 0.8x

Debt/Reserves 3.89

EV/EBITDAX 4.6x

EV/Reserves 21.04

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa2 / BBB 1,000 8.125 2/15/2019 88 130 126.10 4.27

Sr. Notes Baa2 / BBB 750 6.000 1/15/2040 118 160 103.36 5.76

Sr. Notes Baa2 / BBB 1,250 5.600 2/15/2041 120 161 97.44 5.78

Hess Corporation (HES)

Page 35 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2009 Capital Expenditures

United States21%

Europe30%

Africa23%

Asia and Other26%

United States E&P37%

International E&P59%

Refining and Marketing

4%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

EBITDAX 7,789 5,010 6,397 6,537

Operating Cash Flow 4,688 3,046 4,053 4,391

Capital Expenditures (4,438) (2,918) (4,451) (4,200)

Dividends (130) (131) (164) (139)

Free Cash Flow 120 (3) (562) 53

Acquisitions - - (1,546) -

Divestitures - - 183 -

Share Repurchases - - - -

Adjusted Cash Flow 120 (3) (1,925) 53

Cash 908 1,362 2,353 2,406

Debt/EBITDAX 0.5x 0.9x 1.2x 1.1x

Net Debt/EBITDAX 0.4x 0.6x 0.8x 0.8x

2008 2009 2010E 2011E

Production (MBoe/d) 381 408 414 421

Realized Price ($/Boe) 69.74 44.82 55.94 59.36

Lease Operating Expenses 13.43 12.12 12.50 12.65

G&A 2.17 1.71 1.72 1.75

Interest 1.92 2.42 2.29 2.21

Cash Costs 17.51 16.25 16.51 16.61

F&D Costs 16.48 20.35

Full Cycle Costs 33.99 36.60

Recycle Ratio 3.17 1.40

Page 36 Source: Company Filings, Nomura Securities International.

Marathon Oil Corporation (MRO)

Relative ValueWe are affirming our HOLD recommendation on Marathon Oil senior notes. While the recently announced plan to spin-off the refining business will be neutral from a financial leverage perspective, the business profile will be diminished by the loss of the high-quality refining operations, in our opinion. However, management plans to reduce debt by $2.5bn (likely through tender offers) and market technicals will likely keep the notes from materially widening from current levels, in our opinion.

Marathon recently (Jan 2010) announced a plan to spin off the downstream business, creating an independent E&P and independent refiner. MRO plans to reduce existing debt by $2.5bn from cash on hand ($1.6bn) and distributions from the spin-co, which will raise $2.5-3bn of debt and maintain cash on hand at about $750mn. We estimate that leverage at post-spin MRO will be roughly unchanged at 1.0x debt/EBITDA (0.7x net) and the refining entity, MPE, will be levered at roughly 1.9x debt/EBITDA (1.4x net). S&P and Moody’s have indicated that both entities likely will be rated Baa2/BBB.

Business Description

Marathon Oil Corporation is an integrated energy company with operations in Africa, Europe, North America, and Southeast Asia. Marathon has proved reserves of approximately 1.7 billion barrels of oil equivalent, 70% of which are oil. Additionally, the company’s integrated gas segment markets and transports products manufactured from natural gas, such as LNG and methanol. In its refining, marketing, and transportation segment, Marathon owns and operates six refineries in the United States with aggregate refining capacity of 1.1 million barrels per day and distributes refined products through approximately 5,100 Marathon-branded retail outlets. Marathon also owns a product transportation system including terminals, pipelines, inland waterway tow boats and barges, tractor-trailer units, and rail cars.

Company SnapshotReserves (MMBoe) 1,679

% Oil 73%

% Proved Developed 71%

Reserve Life (R/P) 11.6

Daily Production (MBoe/d) 386

LTM EBITDA 6,636

2011 EBITDA 9,959

Cash 2,062

Total Debt 7,930

Market Capitalization 30,335

Enterprise Value 36,203

Debt/EBITDA 1.2x

Debt/Reserves 4.72

EV/EBITDA 5.5x

EV/Reserves 21.56

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa1 /*- / BBB+ /*- 687 7.500 2/15/2019 44 84 125.29 3.83

Sr. Notes Baa1 /*- / BBB+ /*- 750 6.600 10/1/2037 112 158 112.26 5.70

Marathon Oil Corporation (MRO)

Page 37 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

United States18%

Canada36%

Africa39%

Europe7%

E&P, 56% Oil Sands Mining, 9%

Refining, Marketing and Transportation,

25%

Corporate and Other, 10%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

EBITDA 9,433 5,851 7,868 9,959

Operating Cash Flow 6,752 5,268 5,086 6,560

Capital Expenditures (6,989) (6,231) (4,869) (5,080)

Dividends (681) (679) (706) (712)

Free Cash Flow (918) (1,642) (489) 768

Acquisitions - - - -

Divestitures 999 865 1,361 -

Share Repurchases (402) - - -

Adjusted Cash Flow (321) (777) 872 768

Cash 1,285 2,057 2,301 3,069

Debt/EBITDA 0.8x 1.5x 1.0x 0.8x

Net Debt/EBITDA 0.6x 1.1x 0.7x 0.5x

2008 2009 2010E 2011E

Production (MBoe/d) 363 396 394 414

Realized Price ($/Boe) 62.64 41.46 52.08 57.55

Lease Operating Expenses 9.96 11.02 11.30 11.50

G&A 0.89 0.82 0.82 0.82

Interest 0.21 1.03 0.70 0.74

Cash Costs 11.05 12.86 12.82 13.06

F&D Costs 26.63 48.58

Full Cycle Costs 37.68 61.44

Recycle Ratio 1.94 0.59

Page 38 Source: Company Filings, Nomura Securities International.

Newfield Exploration Company (NFX)

Relative Value

We are affirming our HOLD recommendation on Newfield Exploration senior subordinated notes. With the sub notes trading 20-40 bp inside of Pioneer and Chesapeake Energy, NFX is one of the tightest trading high yield energy names. Newfield’s operations are performing well and management is directing capital toward development of its liquids plays. We expect the company to generate free cash flow in 2011, protected by significant (60-65%) hedges on its natural gas production at attractive prices ($6.35/Mcf).

Business Description

Newfield Exploration Company is an independent oil and gas company with operations in the U.S. in the Anadarko Basin, Arkoma Basin, Rocky Mountains, onshore Texas, and Gulf of Mexico and internationally in Malaysia and China. In 2009, Newfield signed a joint exploration agreement with Hess Corporation covering up to 140,000 gross acres in Marcellus shale play. Newfield has proved reserves of approximately 3.6 trillion cubic feet equivalent, 30% of which are oil. The company’s strategy is to focus on domestic, unconventional resource plays, which represent approximately 80% of proved reserves.

Company SnapshotReserves (Bcfe) 3,619

% Oil 28%

% Proved Developed 53%

Reserve Life (R/P) 14.3

Daily Production (MMcfe/d) 763

LTM EBITDA 1,208

2011 EBITDA 1,692

Cash 128

Total Debt 2,169

Market Capitalization 9,473

Enterprise Value 11,514

Debt/EBITDA 1.8x

Debt/Reserves 0.60

EV/EBITDA 9.5x

EV/Reserves 3.18

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW Next Call

Sr. Subordinated Ba2 / BB+ 550 6.625 4/15/2016 253 423 103.75 4.50 4/15/2011

Sr. Subordinated Ba2 / BB+ 600 7.125 5/15/2018 173 417 107.50 5.11 5/15/2013

Sr. Subordinated Ba2 / BB+ 700 6.875 2/1/2020 209 376 107.75 5.48 2/1/2015

Newfield Exploration Company (NFX)

Page 39 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

Mid-Continent, 55%

Rocky Mountains, 26%

Gulf of Mexico, 5%

Onshore Texas, 9%

International, 5%

Mid-Continent40%

Rocky Mountains

23%

Gulf of Mexico14%

Onshore Texas10%

International13%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

EBITDA 1,662 872 1,275 1,692

Operating Cash Flow 854 1,578 1,732 1,974

Capital Expenditures (2,067) (1,392) (1,637) (1,680)

Dividends - - - -

Free Cash Flow (1,213) 186 95 294

Acquisitions (223) (9) (209) -

Divestitures 9 33 14 -

Share Repurchases - (1) (14) -

Adjusted Cash Flow (1,427) 209 (114) 294

Cash 24 78 118 412

Debt/EBITDA 1.3x 2.3x 1.7x 1.3x

Net Debt/EBITDA 1.3x 2.2x 1.6x 1.0x

2008 2009 2010E 2011E

Production (MMcfe/d) 646 694 783 887

Realized Price ($/Mcfe) 8.30 8.64 8.13 8.09

Lease Operating Expenses 1.12 1.02 1.15 1.15

Production Taxes 0.66 0.25 0.41 0.40

G&A 0.60 0.57 0.54 0.55

Interest 0.47 0.50 0.55 0.54

Cash Costs 2.86 2.34 2.66 2.64

F&D Costs 2.89 1.35

Full Cycle Costs 5.75 3.69

Recycle Ratio 1.88 4.67

Page 40 Source: Company Filings, Nomura Securities International.

Nexen Inc. (NXY)

Relative Value

We have revised our rating on Nexen long bonds to BUY from HOLD. Despite the pending downgrade to Ba1 at Moody’s, we believe that current levels provide a good entry point for longer-term tightening potential of 20bp on the long end. We believe that a Ba1/BBB- rated Nexen, which is our base case scenario, should trade 10-15bp through Anadarko Petroleum. We like the lower dollar price NXYCN 5.875% of 2035 at +210bp ($90.80), trading flat on a curve basis of the APC 6.45% of 2036 ($97). We also note that there is a reasonable possibility that Nexen management obtains IG ratings from Fitch Ratings, which would keep NXYCN in the major IG credit indices and provide greater upside to our base case scenario. We had moved to a HOLD rating based partially on our concerns over technical selling pressures ahead of the pending Moody’s downgrade. However, year-end 2010 positioning is now behind us and our sense is that bonds have largely transitioned from would-be forced sellers.

Business Description

Nexen Inc. is an independent, Canadian-based global energy company with 3 operating segments: oil sands, which includes a 65% operated interest in the Long Lake project and a 7.23% participating interest in Syncrude; conventional oil and gas, which includes properties in Canada, the Gulf of Mexico, the North Sea, offshore West Africa, and Yemen; and unconventional gas production in the Horn River Basin in northeastern British Columbia. Nexen has approximately 900 million barrels of oil equivalent of proved reserves, 93% of which are oil. In addition, the company has oil and gas marketing operations in North America as well as legacy power and chemicals businesses.

Company SnapshotReserves (MMBoe) 920

% Oil 93%

% Proved Developed 55%

Reserve Life (R/P) 11.8

Daily Production (MBoe/d) 213

LTM EBITDAX 3,929

2011 EBITDAX 4,122

Cash 1,210

Total Debt 5,678

Market Capitalization 12,562

Enterprise Value 17,030

Debt/EBITDAX 1.4x

Debt/Reserves 6.18

EV/EBITDAX 4.3x

EV/Reserves 18.52

RatingsOutstanding

$mm Coupon (%) Maturity STW Z-Sprd Price YTW

Sr. Notes Baa3 /*- / BBB- 300 6.200 7/30/2019 175 205 107.27 5.14

Sr. Notes Baa3 /*- / BBB- 1,250 6.400 5/15/2037 220 272 95.35 6.78

Sr. Notes Baa3 /*- / BBB- 700 7.500 7/30/2039 225 278 108.36 6.83

Nexen Inc. (NXY)

Page 41 Source: Company Filings, Nomura Securities International.

2009 Proved Reserves

2010 Capital Expenditures

Long Lake, 32%

Syncrude, 31%

United Kingdom, 19%

Canada, 8%

United States, 5%

Yemen, 1% Other, 4%

Financial Summary

Operations Summary

2008 2009 2010E 2011E

EBITDAX 5,678 3,232 3,607 4,122

Operating Cash Flow 4,354 1,886 2,665 3,079

Capital Expenditures (3,044) (2,742) (2,760) (2,700)

Dividends (92) (104) (104) (104)

Free Cash Flow 1,218 (960) (199) 275

Acquisitions (22) (755) - -

Divestitures 6 17 1,256 -

Adjusted Cash Flow 1,202 (1,698) 1,057 275

Cash 2,003 1,700 1,288 1,563

Debt/EBITDAX 1.2x 2.2x 1.6x 1.4x

Net Debt/EBITDAX 0.8x 1.7x 1.2x 1.0x

2008 2009 2010E 2011E

Production (MBoe/d) 210 213 218 236

Realized Price ($/Boe) 89.84 59.94 68.53 72.05

Lease Operating Expenses 11.04 11.66 15.00 15.50

G&A 3.34 6.39 5.16 4.50

Interest 1.22 4.01 4.00 4.00

Cash Costs 15.60 22.05 24.16 24.00

F&D Costs 30.03 NM

Full Cycle Costs 45.64 NM

Recycle Ratio 2.47 NM

North Sea33%

Gulf of Mexico7%

West Africa25%

Canada24%

Other Countries7%

Chemicals4%

Page 42 Source: Company Filings, Nomura Securities International.

Noble Energy, Inc. (NBL)

Relative Value

We are affirming our HOLD recommendation on Noble Energy senior notes. Noble is a smaller independent energy company with sizeable non-traditional international development projects. Its recent discovery, Tamar in offshore Israel, has significant upside potential over the next 2-3 years. We note that the company’s far flung operations and acreage positions may appear somewhat unfocused, and we have some concern over the development capital requirements relative to Noble’s smaller size. Still, Noble has to date successfully managed its sizeable development projects, maintaining a competitive cost structure and low financial leverage. We believe that Noble may need to access the capital markets to term out its credit facility and/or fund development spending. We believe that an issuance could provide an interesting entry point.

Business Description

Noble Energy, Inc. is an independent energy company with U.S. operations in the Rocky Mountains, Mid-continent, and deepwater GOM and international operations in West Africa, China, Ecuador, Israel, and the North Sea. Noble has proved reserves of 841 million barrels of oil equivalent, 67% of which are oil. In 2009, Noble produced 210 MBoe/d of hydrocarbons, with natural gas constituting approximately 60%. Noble’s major development projects are: Galapagos and Gunflint (deepwater Gulf of Mexico); Tamar (offshore Israel); and Aseng, Belinda and Diega/Carmen (offshore West Africa).

Company SnapshotReserves (MMBoe) 820

% Oil 41%

% Proved Developed 67%

Reserve Life (R/P) 10.7

Daily Production (MBoe/d) 229

LTM EBITDAX 2,130

2011 EBITDAX 2,582

Cash 1,149

Total Debt 2,194

Market Capitalization 14,547