2011 kpmg fiduciary management uk market survey

TRANSCRIPT

Investment AdvIsory

2011 KPMG Fiduciary

Management UK Market

Surveynovember 2011

kpmg.co.uk

1 | 2011 KPmG UK Fiduciary management market survey

Executive SummaryKPMG has surveyed the core UK fiduciary management providers to establish a clear picture of the current landscape for fiduciary management (“FM”) within the UK defined benefit pension scheme market. The primary aim of this survey is to define the UK FM market through reliable market statistics and to identify any market trends from this information. We also consider some of the key considerations for Trustees considering a FM solution for their scheme.

We have received responses from the 12 most established fiduciary managers operating in the UK with a combined fiduciary management asset base of over £40bn, servicing over 200 mandates.

We have compiled this survey based on the information supplied by the participating providers. We have liaised with the providers to ensure that we have full understanding of the market data provided, to ensure that our analysis accurately reflects the UK FM market.

2011 KPmG UK Fiduciary management market survey | 2

Key headline trends

We have observed the following highlights and trends from the provider responses to the 2011 KPMG FM UK Market Survey:

• UKpensionschemesmostcommonlyengageinFMtoreducethegovernanceburden that investment management placesupontrustees

• Themostcommonobjectivefor FMclientsisbasedaroundfundinglevel targets

• TheUKFMmarketcurrentlystands inexcessof£40bn,whichequatesto c.4%oftotalUKpensionschemeassets under management (“AUM”)

• Thereareover200UKpensionschememandates within the UK FM market

• TheImplementedConsultancypracticesdominatetheUKFMmarketwithasignificantmarketshareintermsofbothnumberofmandates(c.70%)andAUM(c.60%)

• WithintheUK,asignificantnumber of FM appointments have been madewithoutconsideringalternativeprovidersorconsideringthewidermarket

• UKFMmarketprovidersexpectsignificantgrowthtoemergeinthismarketovertheforthcomingyears –albeitthereissignificantvariability intheexpectationforthisgrowthbetween the market providers

• ThemajorityofFMproviderssurveyedsupported the appointment of a third partyindependentadvisor.Thesurveyresults revealed:

– Independentadvisorsaremostcommonlyengagedunderfullydelegated mandates

– Independentadvisorsaremostlikely to be engaged when the provider is from an investment managementbackground.

• Todate,aconsistentmeasureoffiduciarymanagementtrackrecorddoesnotexist–providerscommonlyuse funding level progress and market-basedperformancemeasurestoillustratetrackrecord

• WhilstthereisnocommonbenchmarkingapproachadoptedwithintheUKFMmarket,therearetwocommonstructures:

– Liability-basedbenchmarkswithaninvestmentoutperformancetarget

– Aschemeobjective-basedbenchmark

• ItisimportanttostructureanFMbenchmarktoensurethatperformancefees,ifapplicable,arenotpayableformarket exposure and/or periods where assets have underperformed

• Allprovidersofferclientsfixedorperformancerelatedfeestructures withthemajorityofprovidersbeingindifferentbetweenwhichstructure is adopted

• Underaperformancerelatedstructure,thesignificantmajorityofprovidersagreed they would offer a high watermarkwithintheperformancefeecalculationandtheywouldconsiderimplementinganannualcaponfees

• TheUKFMindustryexpectfurthergrowth in this market – unsurprisingly allFMmanagerspolledexpectgrowthin their FM assets over the next 3 years throughclientinflows

3 | 2011 KPmG UK Fiduciary management market survey

Introduction

What is Fiduciary Management?Fiduciary management (“Fm”) (also known in the UK as “Implemented Consulting“, “delegated Consulting” or “solvency management”) is a relatively new approach to managing assets of UK defined benefit (“dB”) pension schemes.

Fm is a broad concept with no single definition but usually involves the delegation of some responsibilities to a fiduciary manager (the “provider”) with the aim of better utilising trustees’ limited time and to allow decisions to be taken and implemented more quickly with clear accountability.

the concept of Fm has already taken off in the netherlands and in the Us, albeit in a slightly different structure than the current UK offerings that investment consultants, pensions providers and asset managers are currently marketing.

the proportion of UK pension fund assets under Fm is still relatively small but is growing, with a number of very large schemes having moved to this approach.

2011 KPMG Fiduciary Management UK Market Surveythe UK Fm market has been evolving for a number of years now. However, to date, there has been limited transparency into the size of this market given the difficulties in defining what constitutes Fm and also the manner in which the market has developed - whereby trustees have most commonly entered Fm arrangements with an existing advisor without engaging in a competitive public tender process.

there are now a number of Fm providers within the UK Fm market. each provider’s approach is relatively unique and within each approach, providers offer a range of solutions to meet client objectives. Hence, following the decision to consider Fm, the spectrum of providers and solutions presents clients with important strategic decisions.

Given the lack of market clarity and the wide spectrum of solutions available, many trustees have taken independent advice to gain an understanding of Fm, assess the suitability of Fm for their scheme and objectives and identify the most suitable providers and solutions for their scheme. over the past 3 years, KPmG has consulted with many clients on Fm issues, including areas such as, training and suitability studies, provider selection and appointment structuring. In our experience with clients, there are a number of key areas within the UK Fm market which present questions for clients considering this approach, including:

• What is the current size of the UK Fm market?

• What is Fm and what are the benefits?

• Who is Fm suitable for and is it suitable for the specifics of your scheme and your objectives?

• What are the costs attached to the available solutions?

2011 KPmG UK Fiduciary management market survey | 4

the primary aim of this survey is to accurately define the UK Fm market to present all stakeholders with a reliable representation of the current UK market. We have investigated the primary motivations and objectives for clients engaging in Fm. In terms of suitability, there is no definitive answer here – this should be assessed on a number of factors and should be considered on a scheme- by-scheme basis. there is a wide range of providers and solutions within the UK Fm market, it is therefore important that clients can identify the most appropriate cost/benefit structure for their scheme.

this survey has been complied from market information sourced from the primary UK Fm providers.

5 | 2011 KPmG UK Fiduciary management market survey

Why Fiduciary management?

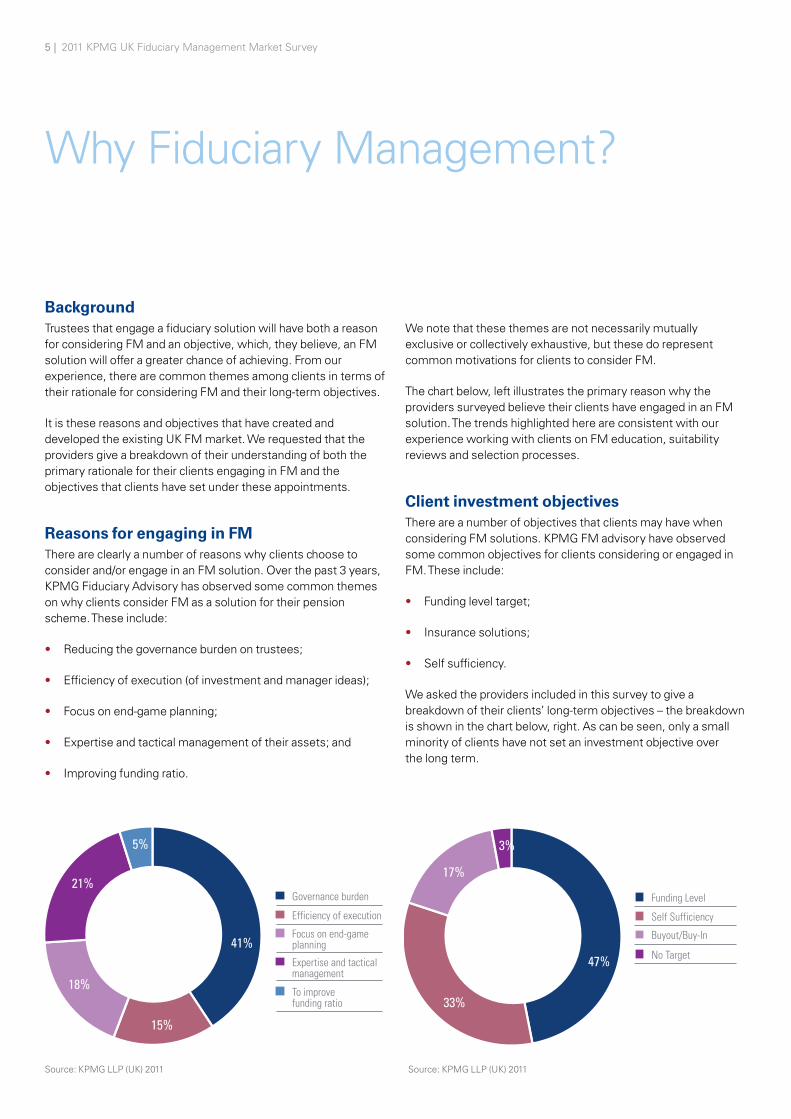

Backgroundtrustees that engage a fiduciary solution will have both a reason for considering Fm and an objective, which, they believe, an Fm solution will offer a greater chance of achieving. From our experience, there are common themes among clients in terms of their rationale for considering Fm and their long-term objectives.

It is these reasons and objectives that have created and developed the existing UK Fm market. We requested that the providers give a breakdown of their understanding of both the primary rationale for their clients engaging in Fm and the objectives that clients have set under these appointments.

Reasons for engaging in FMthere are clearly a number of reasons why clients choose to consider and/or engage in an Fm solution. over the past 3 years, KPmG Fiduciary Advisory has observed some common themes on why clients consider Fm as a solution for their pension scheme. these include:

• reducing the governance burden on trustees;

• efficiency of execution (of investment and manager ideas);

• Focus on end-game planning;

• expertise and tactical management of their assets; and

• Improving funding ratio.

We note that these themes are not necessarily mutually exclusive or collectively exhaustive, but these do represent common motivations for clients to consider Fm.

the chart below, left illustrates the primary reason why the providers surveyed believe their clients have engaged in an Fm solution. the trends highlighted here are consistent with our experience working with clients on Fm education, suitability reviews and selection processes.

Client investment objectivesthere are a number of objectives that clients may have when considering Fm solutions. KPmG Fm advisory have observed some common objectives for clients considering or engaged in Fm. these include:

• Funding level target;

• Insurance solutions;

• self sufficiency.

We asked the providers included in this survey to give a breakdown of their clients’ long-term objectives – the breakdown is shown in the chart below, right. As can be seen, only a small minority of clients have not set an investment objective over the long term.

Governance burden

Efficiency of execution

Focus on end-game planning

Expertise and tactical management

To improve funding ratio

15%

18%

5%

41%

21%Funding Level

Self Sufficiency

Buyout/Buy-In

No Target

33%

3%

47%

17%

source: KPmG LLP (UK) 2011 source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 6

the most common theme in terms of why UK pension schemes engage in Fm is to reduce the governance burden that investment management places upon trustees. the day-to-day investment management of a pension scheme is a significant challenge for trustees – even where an Investment sub-Committee is in place.

the most common client objective set under an Fm mandate is a funding level target – whereby the client engages the fiduciary provider to achieve a specified funding level on a prescribed liability valuation basis. We note that very few Fm mandates are structured without an explicit objective. this highlights that the significant majority of schemes considering Fm have established explicit long-term objectives, which KPmG believe falls under best practice from a pension scheme governance perspective.

7 | 2011 KPmG UK Fiduciary management market survey

the market

Defining the UK FM marketthe UK Fm solutions market (the “market”) for UK occupational dB pension schemes is evolving and there are a variety of providers and solutions. one of the aims of this survey is to provide greater clarity into this market in terms of: client numbers; assets under management (“AUm”); and breadth of providers and solutions available.

there are various headings under which Fm mandates and the market can be subdivided. defining the Fm market consistently is vital in compiling accurate market data. to date, much of the UK Fm market data published has looked largely unrealistic and we attribute this to a lack of consistency in how the UK market is defined and how an Fm mandate is defined within this market. Within this survey, we have framed our market research around the broad definitions that KPmG attach to the UK Fm market: mandate definition (describes the level of delegation) and the type of provider. Whilst we appreciate that these definitions may not be adopted by all market participants, this will serve to set out a framework to establish an accurate representation of the current UK Fm market.

2011 KPmG UK Fiduciary management market survey | 8

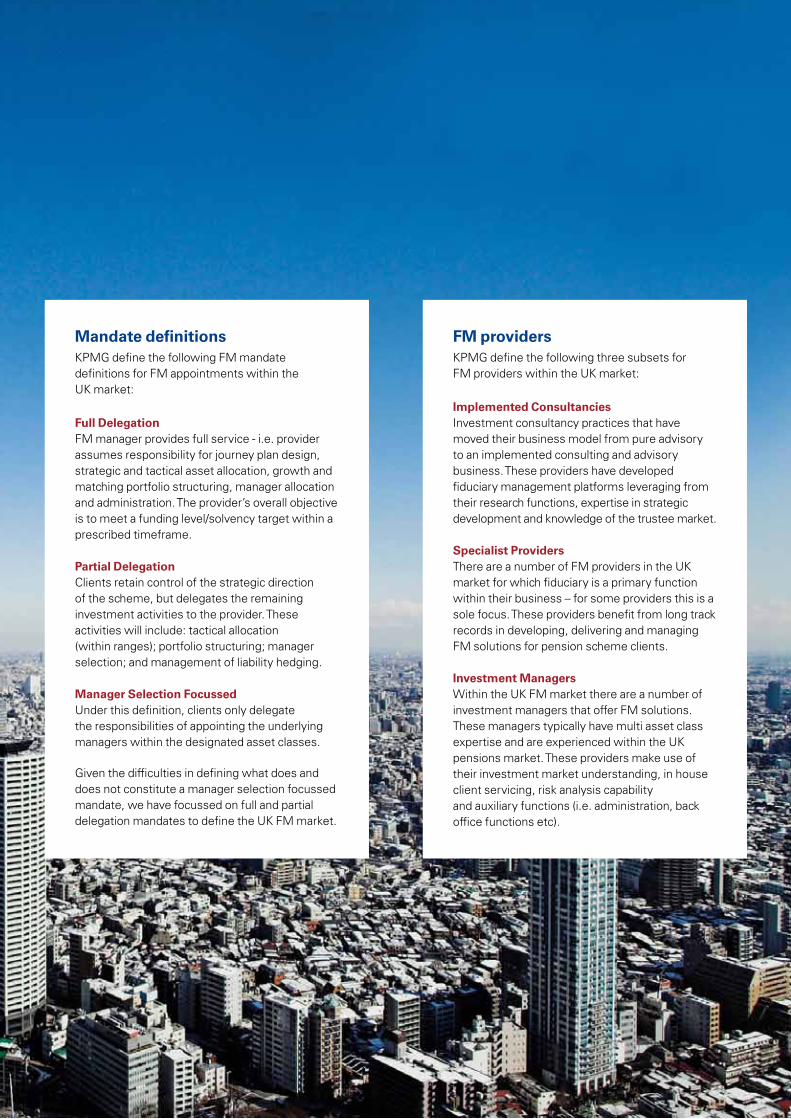

Mandate definitionsKPMG define the following FM mandate definitions for FM appointments within the UK market:

Full DelegationFM manager provides full service - i.e. provider assumes responsibility for journey plan design, strategic and tactical asset allocation, growth and matching portfolio structuring, manager allocation and administration. The provider’s overall objective is to meet a funding level/solvency target within a prescribed timeframe.

Partial DelegationClients retain control of the strategic direction of the scheme, but delegates the remaining investment activities to the provider. These activities will include: tactical allocation (within ranges); portfolio structuring; manager selection; and management of liability hedging.

Manager Selection FocussedUnder this definition, clients only delegate the responsibilities of appointing the underlying managers within the designated asset classes.

Given the difficulties in defining what does and does not constitute a manager selection focussed mandate, we have focussed on full and partial delegation mandates to define the UK FM market.

FM providersKPMG define the following three subsets for FM providers within the UK market:

Implemented ConsultanciesInvestment consultancy practices that have moved their business model from pure advisory to an implemented consulting and advisory business. These providers have developed fiduciary management platforms leveraging from their research functions, expertise in strategic development and knowledge of the trustee market.

Specialist ProvidersThere are a number of FM providers in the UK market for which fiduciary is a primary function within their business – for some providers this is a sole focus. These providers benefit from long track records in developing, delivering and managing FM solutions for pension scheme clients.

Investment ManagersWithin the UK FM market there are a number of investment managers that offer FM solutions. These managers typically have multi asset class expertise and are experienced within the UK pensions market. These providers make use of their investment market understanding, in house client servicing, risk analysis capability and auxiliary functions (i.e. administration, back office functions etc).

9 | 2011 KPmG UK Fiduciary management market survey

Number of UK FM mandatesthe survey results revealed that there are currently over 200 mandates within the UK Fm market. these mandates are split approximately 70:30 between full (143) and partial (64) delegation.

the charts below illustrate how these mandates are broken down across provider and mandate type. As expected, given their market share, the Implemented Consultancies manage the majority of both full (c. 70%) and partial (c. 80%) delegation mandates.

Full Delegation

Num

ber o

f Man

date

s

Partial Delegation

0

20

40

60

80

100

120

Investment ManagersSpecialist ProvidersImplemented Consultancies

51

101

1824

10 3

The FM market : Number of FM mandates by provider typethe chart below illustrates the proportion of existing UK dB pension scheme Fm mandates under each of these provider structures. Currently, Implemented Consultancy practices dominate the UK Fm market with a market share in excess of 70%. the remaining 30% of the UK Fm market is split between specialist Providers (c. 16%) and Investment managers (c. 10%).

this breakdown is in-line with KPmG’s experience of the market. the Implemented Consultancies have invested heavily in their Fm offerings – winning both internal clients (from their existing client base ) and competitive tenders in external market. Within the specialist Provider and Investment manager classifications there is a mix of established and emerging providers.

Implemented Consultancies

Specialist Providers

Investment Managers152

34

21

source: KPmG LLP (UK) 2011source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 10

The FM market : AUM by provider typeBased on the Fm providers included in this survey, the total AUm within the UK Fm market exceeds £40bn. the chart below, left illustrates the proportion of the AUm within the UK Fm market under each of the provider types.

In line with the number of Fm mandates, Implemented Consultancies manage the significant majority of the AUm in the UK Fm market (c. 60%). the remaining c. 40% of assets are split between specialist providers (c. 24%) and Investment managers (c. 16%).

UK FM AUMthe survey results reveal that AUm for full and partial delegation AUm within the UK Fm market are split broadly equally (50:50) between these two mandate types.

the chart below right illustrates how these mandates are broken down across provider-type. As expected, given their market share, the Implemented Consultancies manage the majority of both full (c. 55%) and partial (c. 67%) delegation mandates.

Full Delegation

AUM

(£bn

)

Partial Delegation

0

2

4

6

8

10

12

14

Investment ManagersSpecialist providersImplemented Consultancies

11.911.0

4.14.9

3.9

2.1

22.9

8.8

6.2

Implemented Consultancies

Specialist Providers

Investment Managers

source: KPmG LLP (UK) 2011 source: KPmG LLP (UK) 2011

there are over 200 UK pension scheme mandates within the UK Fm market, split approximately 70:30

between full and partial delegation. Implemented Consultancy practices dominate the UK Fm market with

over 70% of UK Fm appointments.

In terms of AUm, the UK Fm market currently exceeds £40bn – which equates to c. 4% of total UK pension scheme

AUm (£926bn as at 31 march 2010 – source: 2010 Purple Book). this is split broadly 50:50 between full and partial

delegation mandates. In-line with the number of Fm mandates. Implemented Consultancies dominate the UK Fm market with a

market share of c. 60%.

From this market information, we can deduce that Implemented Consultancies hold the greatest number of Fm mandates within the

UK mandate but given their reduced market share by AUm, specialist providers and investment managers must, on average, hold larger

mandates. similarly, we can deduce the average partial delegation mandate is greater in AUm terms than fully delegated given the greater

number of full delegation mandates against equal market capitalisation.

11 | 2011 KPmG UK Fiduciary management market survey

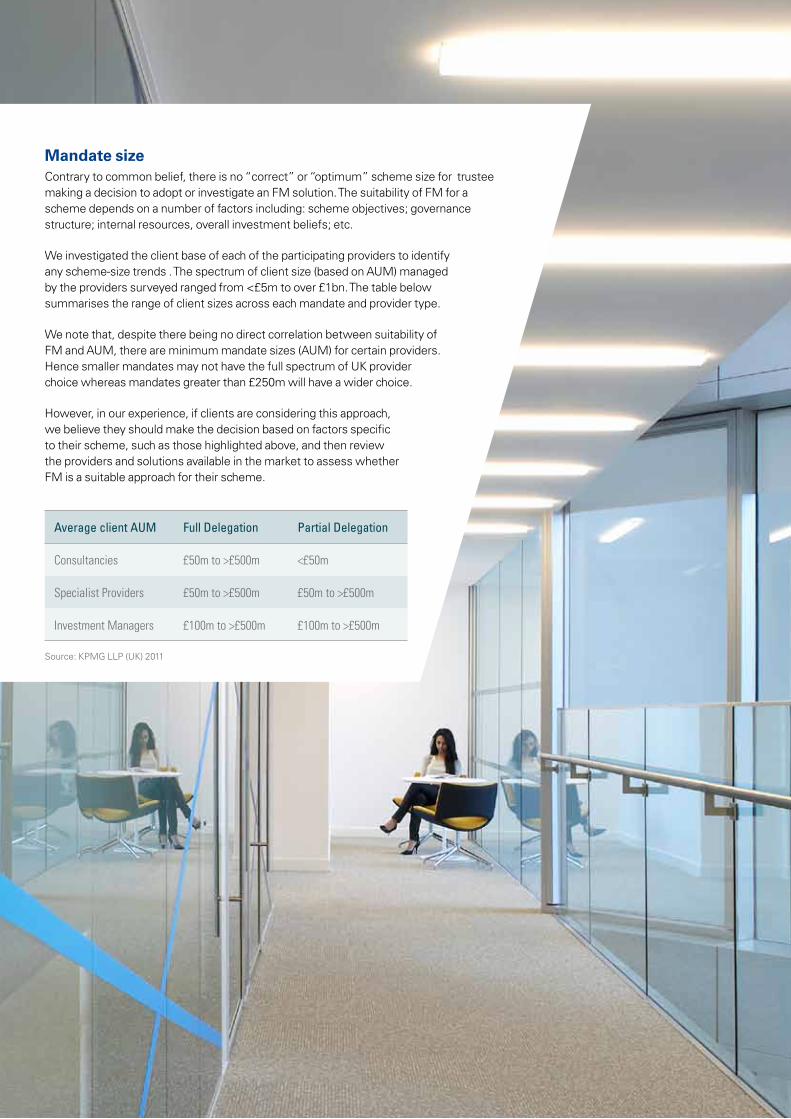

Mandate sizeContrary to common belief, there is no “correct” or “optimum” scheme size for trustee making a decision to adopt or investigate an Fm solution. the suitability of Fm for a scheme depends on a number of factors including: scheme objectives; governance structure; internal resources, overall investment beliefs; etc.

We investigated the client base of each of the participating providers to identify any scheme-size trends . the spectrum of client size (based on AUm) managed by the providers surveyed ranged from <£5m to over £1bn. the table below summarises the range of client sizes across each mandate and provider type.

We note that, despite there being no direct correlation between suitability of Fm and AUm, there are minimum mandate sizes (AUm) for certain providers. Hence smaller mandates may not have the full spectrum of UK provider choice whereas mandates greater than £250m will have a wider choice.

However, in our experience, if clients are considering this approach, we believe they should make the decision based on factors specific to their scheme, such as those highlighted above, and then review the providers and solutions available in the market to assess whether Fm is a suitable approach for their scheme.

Average client AUM Full Delegation Partial Delegation

Consultancies £50m to >£500m <£50m

Specialist Providers £50m to >£500m £50m to >£500m

Investment Managers £100m to >£500m £100m to >£500m

source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 12

UK FM market: Current positionone of the primary reasons for carrying out this market survey was to gain a clear picture of the size of the UK Fm market. While there has been more transparency in this market recently, with well-publicised competitive tenders, there has been a number of years where this market has been developing with little transparency. the result being that providers and participants in this market have been unsure of both the market size and the growth within this market over the last 3-5 years.

to measure the providers perception of the UK market, we asked all participating providers to disclose their expectations of the size of the current UK Fm market (£bn). the range of estimates provided was £15bn - £100bn. As above, we estimate (from the information provided) that the actual UK Fm market size is c. £40bn across the various providers and mandate types.

Selection processGiven the recent growth in the Fm market and the diversity of clients and solutions, we have observed different growth strategies and channels across the different types of providers. Implemented Consultancies have been highly successful at converting traditional advisory clients into fiduciary appointments – leveraging their existing client relationships and offering their delegated service where suitable. Whereas Investment managers and specialist Providers have typically been engaging in competitive tender processes, more in line with typical pension scheme provider appointments.

Within the Implemented Consultancy client space, over 50% of Fm appointments are made without consulting an alternative provider. Within the Investment managers and specialist Provider space the majority of providers have won 100% of appointments via competitive tender – whereby clients consider alternative providers.

Market activityto build up a picture of recent market activity within the UK Fm market, the providers submitted information on the time since their most recent appointment.

Within full delegation, there have been appointments within the last 3 months for all of the providers surveyed that currently participate in this area. We note that the activity was not as recent for partial delegation.

the majority of providers noted that of their existing client base, over 50% of the mandates have been won in the last 3 years – with the exception of those providers with a relatively long-track record.

We asked the providers about turnover within their UK Fm clients base – no full or partial delegation mandate termination cases were disclosed.

UK FM market summaryWe have observed the following UK Fm market highlights and trends from the provider responses to the 2011 KPmG UK Fm market survey:

• TheUKFMmarketcurrentlystandsinexcessof£40bn,which equates to c. 4% of total UK pension scheme AUm (£926m as at 31 march 2010 - source: 2010 Purple Book).

• Thereareover200UKpensionschememandateswithinthe UK Fm market.

• Therearecurrentlyover140fullydelegatedFMmandatesin the UK representing an AUm of c. £20bn.

• Therearecurrentlyover60partiallydelegatedFMmandates in the UK representing an AUm of c. £18bn.

• Thereisalsoasignificantvolumeof‘managerselection’fiduciary mandates in existence – whereby clients only delegate investment manager appointments.

• ImplementedConsultancypracticesdominatetheUKFMmarket with a significant market share majority in terms of both number of mandates (c. 70%) AUm (c. 60%).

• ImplementedConsultanciesholdthegreatestnumber of Fm mandates within the UK mandate but given their reduced market share by AUm, specialist providers and investment managers must, on average, hold larger mandates.

• Thereisno“correct”or“optimum”schemesizefortrustees making a decision to adopt or investigate a fiduciary management solution.

• Certainprovidersdohaveaminimummandatesizeinterms of AUm.

•WithintheUK,asignificantnumberofFMappointmentshave been made without consulting alternative providers or considering the wider market.

• Fromtheinformationprovidedweunderstandtherehavebeen no mandate terminations in full or partial delegation mandates.

13 | 2011 KPmG UK Fiduciary management market survey

roles and responsibilities

BackgroundUnder a fiduciary management arrangement there is no actual transfer of responsibility. By appointing a fiduciary manager trustees do not give up their responsibilities to their scheme – from both a regulatory and legal perspective. Under Fm, there is a delegation of duty to perform certain roles (i.e. strategy setting, manager selection, reporting, etc). However, while the delegated party is accountable to the trustees, the trustees retain the ultimate responsibility for the scheme.

there can be various stakeholders involved in an Fm appointment beyond the trustees and fiduciary manager. In this section we cover the approaches taken in this respect and the providers’ experience in managing UK fiduciary mandates.

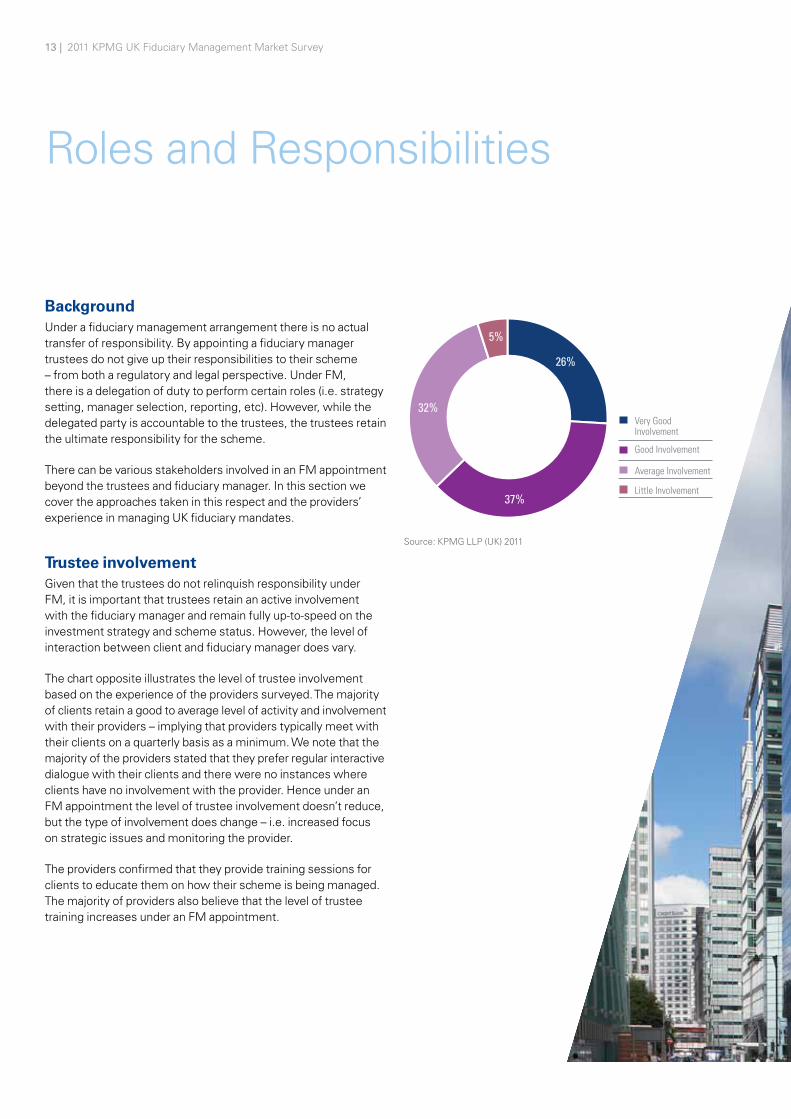

Trustee involvementGiven that the trustees do not relinquish responsibility under Fm, it is important that trustees retain an active involvement with the fiduciary manager and remain fully up-to-speed on the investment strategy and scheme status. However, the level of interaction between client and fiduciary manager does vary.

the chart opposite illustrates the level of trustee involvement based on the experience of the providers surveyed. the majority of clients retain a good to average level of activity and involvement with their providers – implying that providers typically meet with their clients on a quarterly basis as a minimum. We note that the majority of the providers stated that they prefer regular interactive dialogue with their clients and there were no instances where clients have no involvement with the provider. Hence under an Fm appointment the level of trustee involvement doesn’t reduce, but the type of involvement does change – i.e. increased focus on strategic issues and monitoring the provider.

the providers confirmed that they provide training sessions for clients to educate them on how their scheme is being managed. the majority of providers also believe that the level of trustee training increases under an Fm appointment.

Very Good Involvement

Little Involvement

Average Involvement

Good Involvement

5%

37%

26%

32%

source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 14

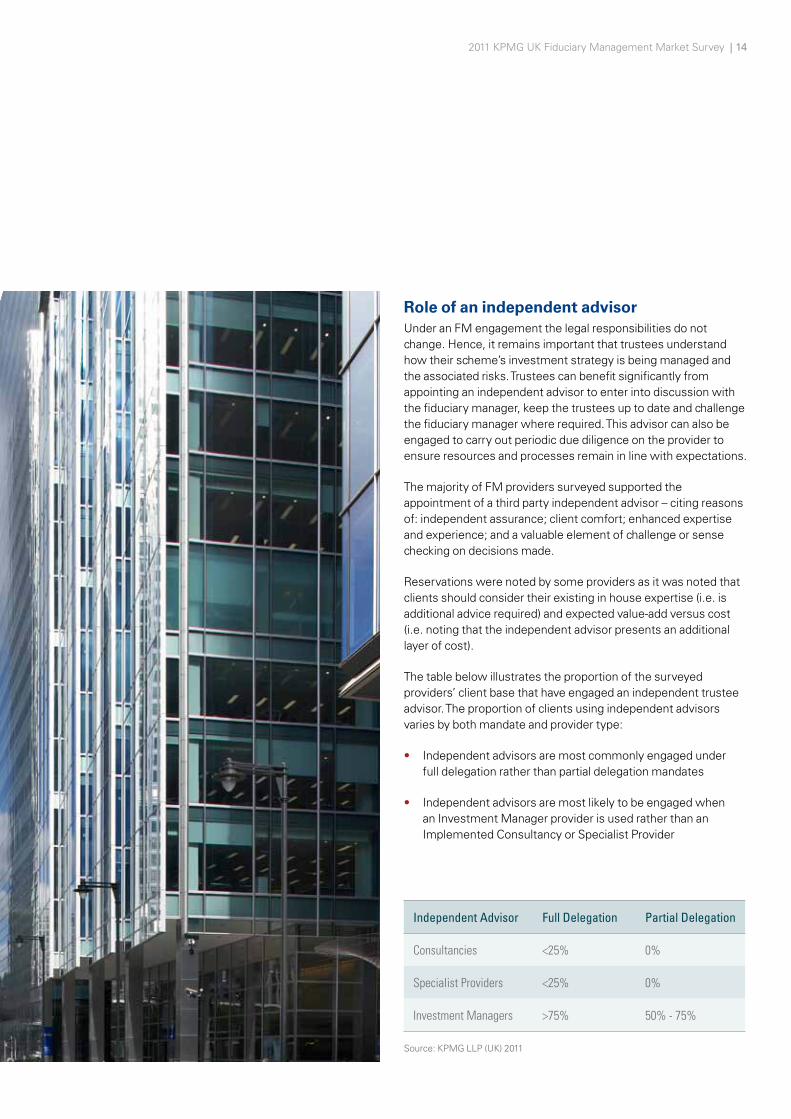

Role of an independent advisorUnder an Fm engagement the legal responsibilities do not change. Hence, it remains important that trustees understand how their scheme’s investment strategy is being managed and the associated risks. trustees can benefit significantly from appointing an independent advisor to enter into discussion with the fiduciary manager, keep the trustees up to date and challenge the fiduciary manager where required. this advisor can also be engaged to carry out periodic due diligence on the provider to ensure resources and processes remain in line with expectations.

the majority of Fm providers surveyed supported the appointment of a third party independent advisor – citing reasons of: independent assurance; client comfort; enhanced expertise and experience; and a valuable element of challenge or sense checking on decisions made.

reservations were noted by some providers as it was noted that clients should consider their existing in house expertise (i.e. is additional advice required) and expected value-add versus cost (i.e. noting that the independent advisor presents an additional layer of cost).

the table below illustrates the proportion of the surveyed providers’ client base that have engaged an independent trustee advisor. the proportion of clients using independent advisors varies by both mandate and provider type:

• Independent advisors are most commonly engaged under full delegation rather than partial delegation mandates

• Independent advisors are most likely to be engaged when an Investment manager provider is used rather than an Implemented Consultancy or specialist Provider

Independent Advisor Full Delegation Partial Delegation

Consultancies <25% 0%

Specialist Providers <25% 0%

Investment Managers >75% 50% - 75%

source: KPmG LLP (UK) 2011

15 | 2011 KPmG UK Fiduciary management market survey

External servicesUnder an Fm appointment there are a number of external services that clients may still have to engage. the level and detail of these services will depend on the client’s preference, Fm structure and the provider service level. each of the providers surveyed submitted details of their service level offering for: custody; performance reporting; and management of liability hedging.

Independent custody and performance reportingAll providers surveyed provide client reporting. However, as with any investment management appointment, it is generally considered good practice to engage an independent custodian and performance measurer.

the majority of the providers do encourage clients to engage an external custodian and performance measurer for reasons of independence. A number of the providers surveyed have preferred providers for these services and/or will make arrangements for clients in this respect.

Liability hedgingLiability hedging expertise is a significant element within each Fm providers’ service offering. From our experience working with the UK Fm managers we noted that there are varying approaches to managing liability hedging – typically this is managed through in-house functions or outsourcing to a specialist provider. We asked the providers how they approached liability hedging:

• Implemented Consultancy providers typically design liability hedging in-house and outsource the execution of the strategy to their preferred provider(s)

• specialist Providers typically manage liability hedging design and execution in house

• Investment manager providers typically offer clients the choice of the in-house management or an outsourced solution

FM appointment contractsthe appointment contract under Fm, typically takes the form of an Investment management Agreement (“ImA”) or a Fiduciary management Agreement (“FmA”). We note that ImAs are more commonly used but in KPmG’s experience there is little difference between these documents.

each of the providers stated that they offer clients “standardised” appointment documentation. However, these documents contain a material volume of appointment specific detail (i.e. objectives, guidelines, benchmarking, fee structure, etc) which results in significant customisation. the majority of providers also stated that they offer clients bespoke appointment documentation where requested.

From our experience, appointment contract negotiation is a detailed, time-consuming process. even with a degree of standardisation, clients will require professional advice from both a legal and investment perspective to finalise these agreements.

2011 KPmG UK Fiduciary management market survey | 16

the fiduciary manager is accountable to the trustees for the services they were engaged to fulfil, but the trustees retain ultimate responsibility for their pension scheme. therefore It remains important for the trustees to remain involved with the fiduciary manager – the majority of clients retain a better level of involvement with their fiduciary manager. there may be other parties accountable to either the trustees or the fiduciary manager. It is important for the trustees to understand who is accountable to them and for which services and that the trustees are satisfied that these roles and responsibilities are captured accurately within the Fm appointment contract.

to manage this responsibility, trustees may appoint an independent advisor to challenge and monitor the fiduciary manager. the majority of providers surveyed supported the appointment of a third party independent advisor on grounds of: independent assurance; client comfort; enhanced expertise and experience; and a valuable element of challenge or sense check on decisions made. However, we note that the significant majority of Fm appointments do not currently engage an independent trustee advisor.

17 | 2011 KPmG UK Fiduciary management market survey

track record measurement

FM provider track recordA common theme KPmG have observed in our role as independent advisor to clients considering Fm, is how best to compare Fm providers and/or solutions. much of the difficulty here stems from the significant difference between the Fm solutions offered as well as the relatively short time-frames over which many of the providers have had their solutions implemented.

As part of this survey, we wanted to identify how Fm track records are being communicated to clients and investigate each providers view on how they believe Fm track records should be measured. Further to this, we explored the possibility of introducing a consistent approach to measure Fm provider track records with the aim of enabling clients to make a consistent comparison across providers.

2011 KPmG UK Fiduciary management market survey | 18

Current approach to track record measurement?each of the providers surveyed provided details of how they currently illustrate their Fm track record to clients. though there were differences in the approaches taken to track record measurement, there were two common themes described:

1. Funding level objectives – track record can be illustrated based on progression towards achieving a client’s overall funding level objectives. this is commonly illustrated through references and case studies

2. market benchmarks - analytical measures of funding level against target, matching portfolio against liabilities, growth portfolio against market benchmark, etc

We note that although there were some common themes, many of the providers highlighted that track record illustration would vary by client and be based on objectives and level of delegation afforded. It was also noted that for the majority of providers, track records are relatively short compared with the timeframe in which client objectives are set – hence short-term track records relative to long-term objectives may lack credibility.

Can a consistent approach to FM track record measurement be achieved?For the majority of investment management appointments that trustees make on behalf of their schemes, a consistent comparison of providers’ track record can be observed. While this is not a direct guide to the suitability of a provider or a guide to what they will deliver in the future, it does give clients the opportunity to compare what a provider has achieved relative to what they state they aim to do and relative to other considered providers.

Within the UK Fm market, we have observed that clients do not have a clear relative comparison available to assess prospective providers. We asked the providers surveyed if such a consistent comparison could be established within the UK Fm provider market.

• the majority of providers did not feel that a universal track record could be established for two core reasons:

1. Providers noted that pension scheme objectives will always differ in some form and are generally unique in terms of return objective, risk budgets, etc. to be of use, analysis of track records should ideally relate to the scheme objectives. A possible solution is to analyse a company’s track record in case studies with similar scheme objectives. However, these examples may not always exist and may lack credibility.

2. there are many different areas within Fiduciary management that may be measured – i.e. growth asset management, liability matching, liability hedging, risk management and progress towards funding level targets. A Fiduciary manager may not be involved in all these areas as this will depend on the degree of delegation and mandate specifics. therefore a uniform measure for track record would be hard to define.

• However, a number of the providers believed there were aspects of a providers’ track record that could be measured consistently – e.g. funding level progression and/or investment growth achieved relative to target and value added through manager selection.

As with any trustee or pension scheme appointment, track record is an important measurement to illustrate past success and provide an objective measure on which to compare providers. to date, a consistent measure of fiduciary management track record does not exist. the majority of the UK Fm providers believe that unique client objectives, scheme position and the distinct elements that make up a fiduciary mandate do not offer a basis for a consistent means of track record comparison.

two common approaches that providers adopt to illustrate their respective track records are: progress towards achieving fund level objectives; and a market-based measure for investment performance. While these measures may not offer a consistent platform for comparison, given the unique nature of the mandates involved, this information does offer an insight into provider experience. KPmG use this approach and also believe client references offer powerful insight into client Fm and provider experience.

19 | 2011 KPmG UK Fiduciary management market survey

Benchmarking

Benchmark considerationsAs with the other appointments that trustees make on behalf of their pension funds, the benchmark to which an Fm appointment is to be measured against is the key indicator of the success and/or performance of the appointed provider. Under an Fm appointment there are two significant benchmark considerations:

1. there is no established structure for benchmarking an Fm mandate; and

2. Where a performance related fee structure is adopted, the benchmark may form the framework on which performance related fees are calculated.

Benchmark structureWe asked the providers if a consistent benchmarking structure could be established within the UK Fm market. the significant majority of providers did not believe a consistent benchmarking approach would be possible or suitable. the providers noted that given the variability of clients’ objectives and the spectrum of providers and solutions available within the UK Fm market, benchmarking Fm mandates on a consistent basis is not realistic. It was noted that there are a number of approaches that can be considered when agreeing the benchmark for an Fm appointment – the approach will be driven by a combination of the client, the solution and the provider.

Performance related benchmark structureWe requested that the providers give details of how they would construct a benchmark for a performance related Fm mandate. the most common approach from the providers surveyed is to adopt an agreed liability benchmark with an investment outperformance target (e.g. liabilities on a funding basis +2% p.a.). there was also a common theme of focussing on clients long-term investment objectives and basing a benchmark measure around this.

Under a performance-related benchmark structure the benchmark will have profound implications on the fiduciary management fees payable. Whilst there is no common approach adopted within the UK Fm market, there are two common structures:

1. Liability-based benchmark with an investment outperformance target ; or

2. A scheme objective-based benchmark.

If the benchmark is not established appropriately, under a liability plus benchmark, performance fees could be payable for beta (i.e. market exposure) rather than manager skill and similarly, under an objective-based benchmark, performance fees may be payable where assets have underperformed but liabilities have underperformed further due to market movements.

As such, the benchmark structuring process is very important under a fiduciary management appointment. therefore, clients should consider taking advice on the benchmark structure being proposed and/or clients should engage in a competitive tender to compare and contrast benchmark approaches offered.

2011 KPmG UK Fiduciary management market survey | 20

Under a performance-related benchmark structure the benchmark will have profound implications on the fiduciary management fees payable. Whilst there is no common approach adopted within the UK Fm market, there are two common structures:

1. Liability-based benchmark with an investment outperformance target ; or

2. A scheme objective-based benchmark.

If the benchmark is not established appropriately, under a liability plus benchmark, performance fees could be payable for beta (i.e. market exposure) rather than manager skill and similarly, under an objective-based benchmark, performance fees may be payable where assets have underperformed but liabilities have underperformed further due to market movements.

As such, the benchmark structuring process is very important under a fiduciary management appointment. therefore, clients should consider taking advice on the benchmark structure being proposed and/or clients should engage in a competitive tender to compare and contrast benchmark approaches offered.

21 | 2011 KPmG UK Fiduciary management market survey

Fee structuring

FM Fee structuringWithin the UK Fm market there are a variety of providers, each with a range or service levels and fee structures available. With this variability across provider, service level and structure there is significant variance in the proposed fee scales that clients are offered. therefore, clients appointing a fiduciary manager will generally be faced with a choice of fee structure and scale and an associated level of service.

Fee structures under Fm mandates are generally fixed or performance-related in nature. As part of this survey we explore the general consensus within the provider market as to which of these fee structures (if either) is preferable. A further consideration is the measure used to determine the outperformance that will attract performance fees under a performance-related fee arrangement – i.e. to ensure that clients are treated fairly, whilst providers are rewarded appropriately as experience develops.

Provider fee offeringsIn practice the majority of providers offer clients both fixed and performance related fee structures. Generally each provider has a preferred fee structure that they feel is best suited to their solution, their business and their clients. the chart below illustrates the providers preferences in this respect:

the survey highlighted that the majority of providers are indifferent to which fee structure is adopted. In practice, performance related fee structures are commonly structured with both a fixed fee element and a performance related element.

the aggregate position across the client base of the providers surveyed – both in terms of number of mandates and AUm – is split approximately 50:50 between fixed and performance related fee structures.

each of the providers stated that where they offer both fixed and performance related fee structures they aim to position these as equally competitive.

Fixed or flat fee structuresUnder a fixed fee structure clients pay a fixed monetary amount with defined progression (i.e. £1m p.a. with increases linked to inflation) or a percentage of total assets (i.e. 25bps based on AUm). Fixed fee scales have the advantage of being transparent and simple to understand. However, fixed fee scales do not offer direct alignment of interest between client and provider and clients could pay significant fees over periods where the provider has underperformed relative to the objectives set.

Performance related feesUnder a performance related fee structure, clients pay fee levels linked to the level of performance achieved by the fiduciary manager (i.e. under a 20% performance fee, if the manager outperforms the agreed benchmark by 1% they receive 0.2% of AUm in fees) – similar to active management fees under a traditional investment manager appointment.

Performance related fee scales are more complex and less transparent than the fixed equivalent. However, under an Fm engagement, clients often seek to align the provider’s interests with their own. many clients pursue a performance related fee option under the belief that this fee structure offers greater alignment of interest.

Fixed Fee Preference

Performance Related Fee Preference

Indifferent

3

2

6

source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 22

Performance related fee structuresthe majority of the providers agreed that performance related fee structures were helpful for clients and suitable for an Fm mandate – with no provider stating that performance fees were inappropriate. However there were a number of considerations noted by the providers:

• An appropriate performance benchmark should be selected to ensure that performance is fairly rewarded

• Clients should consider the total potential fees payable and whether a fee cap should be applied

• Clients should understand the performance fee structure

• Clients should ensure a long-term focus is retained to match the long-term nature of their objectives (i.e. performance measured relative to funding level)

• Benchmarks can be structured relative to measures based not only on the growth assets, but also on components such as liabilities or funding level

• Fee structures and benchmarks should be flexible with client input to align with long-term objectives

the considerations noted above, and those beyond, and the complexity of understanding and quantifying the various fee options clients will be presented with, illustrate the importance of clear advice at the point of engagement. A key aspect of the competitive tender process and/or independent advice should focus on assessing the various fee structures proposed and available.

23 | 2011 KPmG UK Fiduciary management market survey

Performance fee benchmark or hurdle rateUnder a performance based fee, the fee rate is applied to any outperformance above a agreed level or metric (i.e. 20% of outperformance). Using equity markets as an example, most active equity managers are paid performance related fees on the margin above the set benchmark (i.e. the Ftse All share). Under an Fm mandate there is no market or peer benchmark to measure performance against. the Fm providers within the UK market adopt a range of performance benchmarking approaches – with the majority of providers offering more than one option to clients.

2011 KPmG UK Fiduciary management market survey | 24

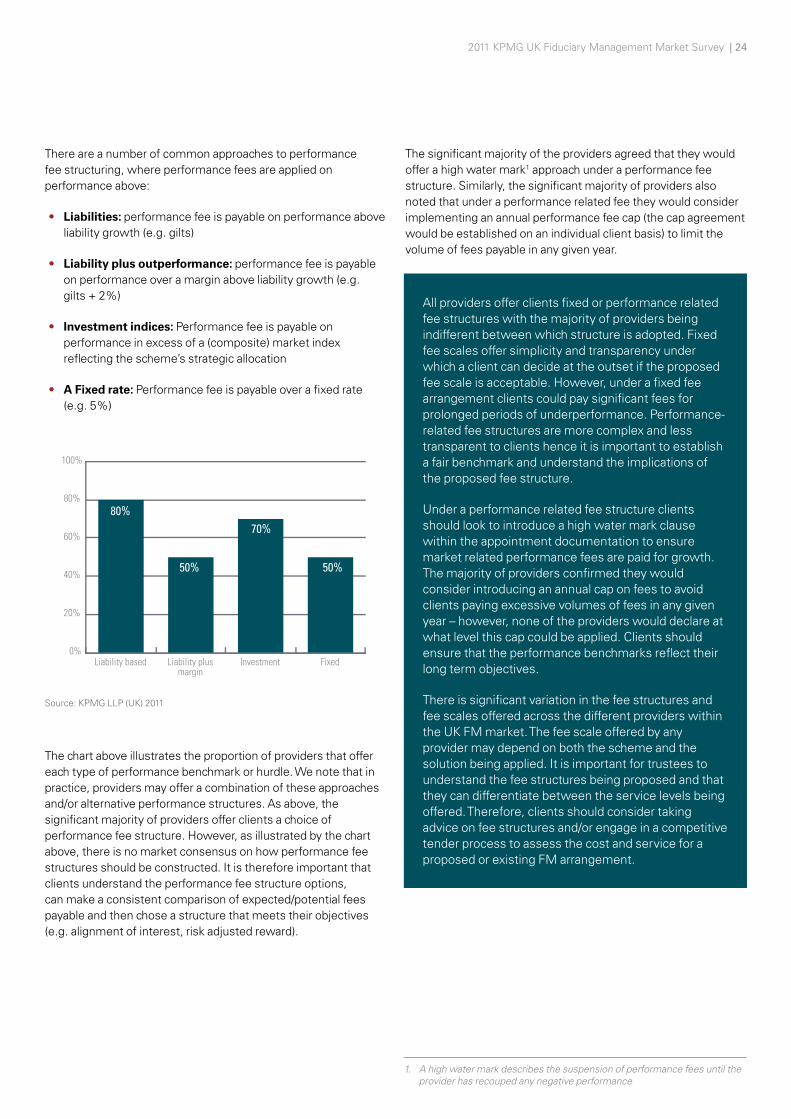

there are a number of common approaches to performance fee structuring, where performance fees are applied on performance above:

• Liabilities: performance fee is payable on performance above liability growth (e.g. gilts)

• Liability plus outperformance: performance fee is payable on performance over a margin above liability growth (e.g. gilts + 2%)

• Investment indices: Performance fee is payable on performance in excess of a (composite) market index reflecting the scheme’s strategic allocation

• A Fixed rate: Performance fee is payable over a fixed rate (e.g. 5%)

the chart above illustrates the proportion of providers that offer each type of performance benchmark or hurdle. We note that in practice, providers may offer a combination of these approaches and/or alternative performance structures. As above, the significant majority of providers offer clients a choice of performance fee structure. However, as illustrated by the chart above, there is no market consensus on how performance fee structures should be constructed. It is therefore important that clients understand the performance fee structure options, can make a consistent comparison of expected/potential fees payable and then chose a structure that meets their objectives (e.g. alignment of interest, risk adjusted reward).

the significant majority of the providers agreed that they would offer a high water mark1 approach under a performance fee structure. similarly, the significant majority of providers also noted that under a performance related fee they would consider implementing an annual performance fee cap (the cap agreement would be established on an individual client basis) to limit the volume of fees payable in any given year.

0%

20%

40%

60%

80%

100%

FixedInvestmentLiability plusmargin

Liability based

80%

50%50%

70%

source: KPmG LLP (UK) 2011

1. A high water mark describes the suspension of performance fees until the provider has recouped any negative performance

All providers offer clients fixed or performance related fee structures with the majority of providers being indifferent between which structure is adopted. Fixed fee scales offer simplicity and transparency under which a client can decide at the outset if the proposed fee scale is acceptable. However, under a fixed fee arrangement clients could pay significant fees for prolonged periods of underperformance. Performance-related fee structures are more complex and less transparent to clients hence it is important to establish a fair benchmark and understand the implications of the proposed fee structure.

Under a performance related fee structure clients should look to introduce a high water mark clause within the appointment documentation to ensure market related performance fees are paid for growth. the majority of providers confirmed they would consider introducing an annual cap on fees to avoid clients paying excessive volumes of fees in any given year – however, none of the providers would declare at what level this cap could be applied. Clients should ensure that the performance benchmarks reflect their long term objectives.

there is significant variation in the fee structures and fee scales offered across the different providers within the UK Fm market. the fee scale offered by any provider may depend on both the scheme and the solution being applied. It is important for trustees to understand the fee structures being proposed and that they can differentiate between the service levels being offered. therefore, clients should consider taking advice on fee structures and/or engage in a competitive tender process to assess the cost and service for a proposed or existing Fm arrangement.

25 | 2011 KPmG UK Fiduciary management market survey

the Future of Fiduciary management in the UK

BackgroundGiven the relative infancy of Fm in the UK market, the future for Fm is not clear. What is clear, is the investment in infrastructure and resource made by the primary UK Fm providers – these firms are experts in their respective fields, understand the UK pensions market explicitly and are clearly anticipating significant growth in the UK Fm market which has yet to materialise.

UK FM market: Growth expectationsthere has been a significant investment in the infrastructure and resource required to offer a formal fiduciary management platform from the 12 high profile providers featuring in this survey and a number of additional providers who are yet to win their first UK dB pension scheme Fm mandate. this signifies that market providers expected significant revenue to be generated from the UK Fm market and also significant growth to emerge in this market over the forthcoming years.

to gauge this growth expectation we surveyed the providers’ expectations of client growth within their own businesses over the short to medium term.

2011the majority of providers surveyed targeted up to 5 new Fm clients within each mandate type over 2011 – reflecting the view that while significant growth is expected, the market believes that this will continue to emerge relatively slowly over 2011. We note that some providers are targeting over 10 new clients this year.

2015over the short to medium term (i.e. 3-5 years), there are mixed beliefs between the providers regarding the pace of expected growth in the UK Fm market – with increases in client lists ranging from 10-50 new clients within each mandate type by 2015.

to measure the providers’ expectation of medium term growth within the UK Fm market, we asked all participating providers to disclose their expectations of the size of the UK Fm market (£bn) in 3 years time. the range of estimates provided was £15bn – £100bn. this signifies expected growth within this market together with a wide range on this expectation.

UK FM market: The futureWe asked the providers what their long-run expectations were for UK defined benefit pensions schemes’ take up of fiduciary management. the table below illustrates the responses across the various mandate types and providers.

From the responses received, it is clear that each provider, regardless of type, has their own view on the future of Fm. It is also clear that each of the managers engaged in providing fiduciary management solutions for UK pension scheme clients expects growth within the UK Fm market – the question will be how much of these growth expectations are realised.

Expected proportion of UK pension schemes engaging in an FM solution over the long-term

Consultancies 25% to 50%

Specialist Providers 10% to 75%

Investment Managers 10% to 50%

source: KPmG LLP (UK) 2011

2011 KPmG UK Fiduciary management market survey | 26

KPmG expect that for the subset of UK pension schemes for which Fm presents a suitable solution a number of these clients will engage a fiduciary manager where the benefits of doing so can be clearly identified. As such, we expect further growth in this market. this view is shared by the UK fiduciary management industry, as all Fm managers polled expect growth in their Fm assets over the next 3 years through client inflows – albeit we note that the providers have very divergent expectations on the level of this growth.

27 | 2011 KPmG UK Fiduciary management market survey

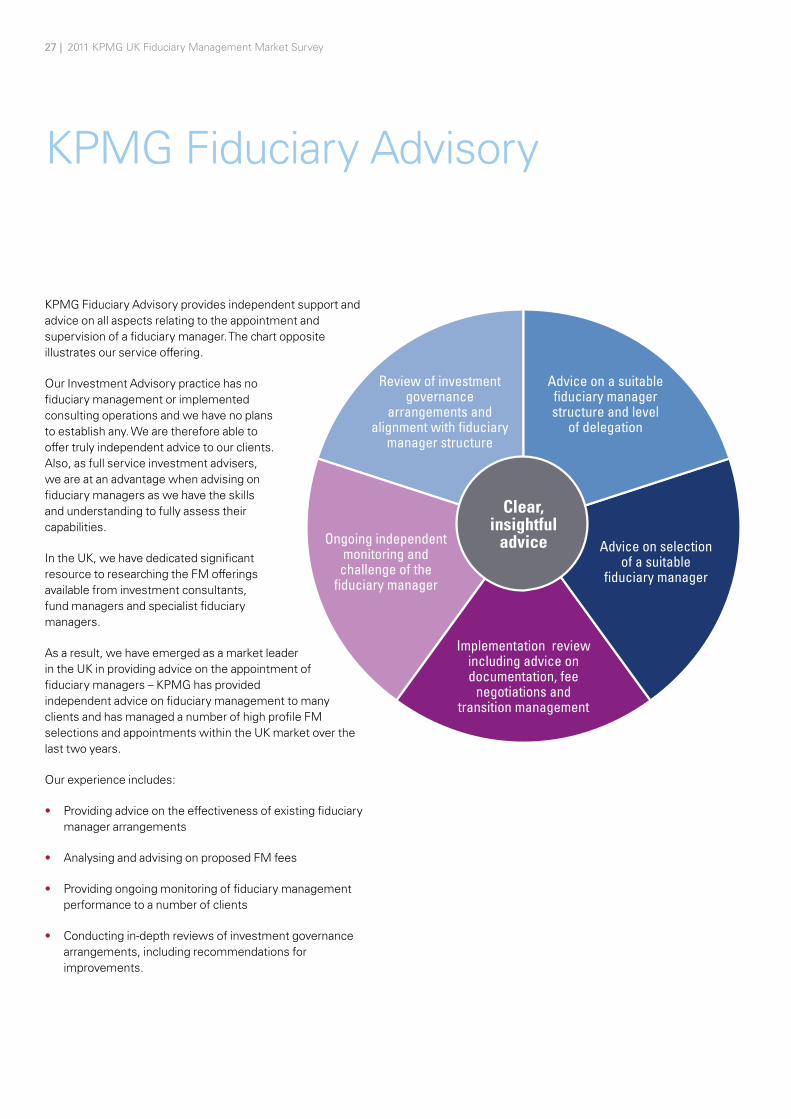

KPmG Fiduciary Advisory provides independent support and advice on all aspects relating to the appointment and supervision of a fiduciary manager. the chart opposite illustrates our service offering.

our Investment Advisory practice has no fiduciary management or implemented consulting operations and we have no plans to establish any. We are therefore able to offer truly independent advice to our clients. Also, as full service investment advisers, we are at an advantage when advising on fiduciary managers as we have the skills and understanding to fully assess their capabilities.

In the UK, we have dedicated significant resource to researching the Fm offerings available from investment consultants, fund managers and specialist fiduciary managers.

As a result, we have emerged as a market leader in the UK in providing advice on the appointment of fiduciary managers – KPmG has provided independent advice on fiduciary management to many clients and has managed a number of high profile Fm selections and appointments within the UK market over the last two years.

our experience includes:

• Providing advice on the effectiveness of existing fiduciary manager arrangements

• Analysing and advising on proposed Fm fees

• Providing ongoing monitoring of fiduciary management performance to a number of clients

• Conducting in-depth reviews of investment governance arrangements, including recommendations for improvements.

Review of investment governance

arrangements and alignment with fiduciary

manager structure

Advice on a suitable fiduciary manager structure and level

of delegation

Clear, insightful

adviceOngoing independent monitoring and

challenge of the fiduciary manager

Advice on selection of a suitable

fiduciary manager

Implementation �review including advice on documentation, fee

negotiations and transition management

KPmG Fiduciary Advisory

2011 KPmG UK Fiduciary management market survey | 28

29 | 2011 KPmG UK Fiduciary management market survey

Acknowledgements

KPmG would like to thank the following providers for their participation in the 2011 KPmG Fiduciary management UK market survey:

• AonHewitt Ltd

• Blackrock

• Cardano

• Goldman sachs Asset management

• Henderson Global Investors

• mercer

• mn services Investment management UK

• P-solve

• russell Investments

• seI

• towers Watson

• UBs

the KPmG 2011 Fm survey has been conducted using information provided by third parties. KPmG does not accept responsibility for the accuracy of the data or information provided herein.

the information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. no one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2011 KPmG LLP, a UK limited liability partnership, is a subsidiary of KPmG europe LLP and a member firm of the KPmG network of independent member firms affiliated with KPmG International Cooperative, a swiss entity. All rights reserved. Printed in the United Kingdom.

the KPmG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPmG International.

rr donnelley | rrd-261044 | november 2011 | Printed on recycled material.

Contact us

Patrick McCoy T: +44 (0)20 7311 2393 E: [email protected]

Calum Brunton Smith T: +44 (0)141 300 5629 E: [email protected]

www.kpmg.co.uk