©2009, the mcgraw-hill companies, all rights reserved 3-1 mcgraw-hill/irwin chapter three interest...

TRANSCRIPT

©2009, The McGraw-Hill Companies, All Rights Reserved

3-1McGraw-Hill/Irwin

Chapter ThreeInterest Rates

and Security

Valuation

©2009, The McGraw-Hill Companies, All Rights Reserved

3-2McGraw-Hill/Irwin

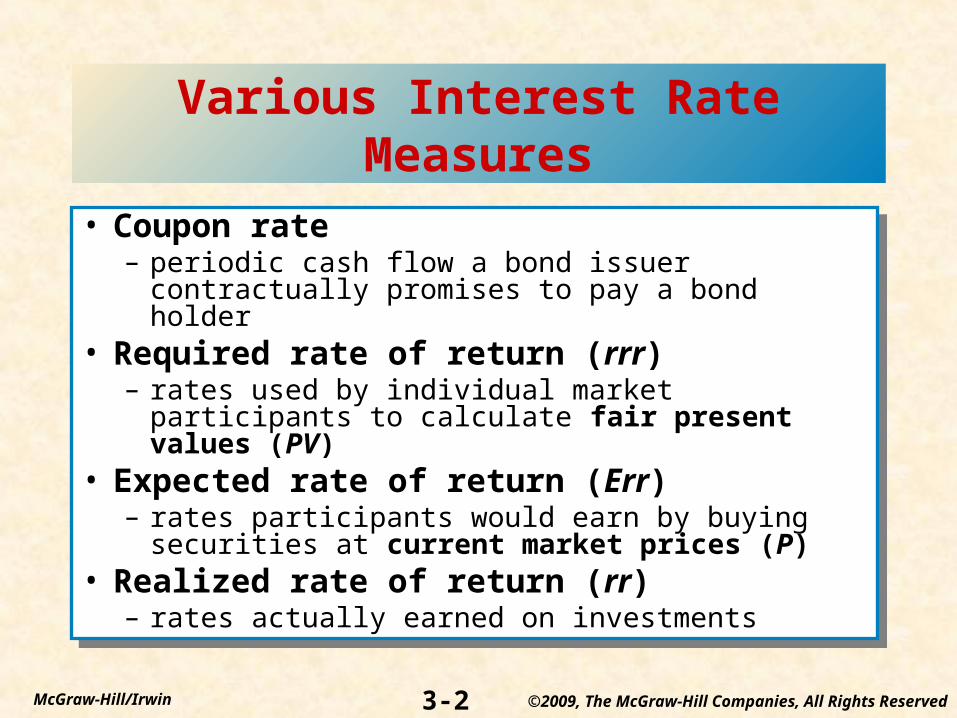

Various Interest Rate Measures

• Coupon rate– periodic cash flow a bond issuer contractually

promises to pay a bond holder• Required rate of return (rrr)

– rates used by individual market participants to calculate fair present values (PV)

• Expected rate of return (Err)– rates participants would earn by buying securities at

current market prices (P)• Realized rate of return (rr)

– rates actually earned on investments

• Coupon rate– periodic cash flow a bond issuer contractually

promises to pay a bond holder• Required rate of return (rrr)

– rates used by individual market participants to calculate fair present values (PV)

• Expected rate of return (Err)– rates participants would earn by buying securities at

current market prices (P)• Realized rate of return (rr)

– rates actually earned on investments

©2009, The McGraw-Hill Companies, All Rights Reserved

3-3McGraw-Hill/Irwin

Required Rate of Return

• The fair present value (PV) of a security is determined using the required rate of return (rrr) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

• The fair present value (PV) of a security is determined using the required rate of return (rrr) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

n

n

rrr

FC

rrr

FC

rrr

FC

rrr

FCPV

)1(

~...

)1(

~

)1(

~

)1(

~

3

3

2

2

1

1

©2009, The McGraw-Hill Companies, All Rights Reserved

3-4McGraw-Hill/Irwin

Expected Rate of Return

• The current market price (P) of a security is determined using the expected rate of return (Err) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

• The current market price (P) of a security is determined using the expected rate of return (Err) as the discount rate

CF1 = cash flow in period t (t = 1, …, n)~ = indicates the projected cash flow is uncertainn = number of periods in the investment horizon

n

n

Err

FC

Err

FC

Err

FC

Err

FCP

)1(

~...

)1(

~

)1(

~

)1(

~

3

3

2

2

1

1

©2009, The McGraw-Hill Companies, All Rights Reserved

3-5McGraw-Hill/Irwin

Realized Rate of Return

• The realized rate of return (rr) is the discount rate that just equates the actual purchase price ( ) to the present value of the realized cash flows (RCFt) t (t = 1, …, n)

• The realized rate of return (rr) is the discount rate that just equates the actual purchase price ( ) to the present value of the realized cash flows (RCFt) t (t = 1, …, n)P

n

n

rr

RCF

rr

RCF

rr

RCF

rr

RCFP

)1(...

)1()1()1( 3

3

2

2

1

1

©2009, The McGraw-Hill Companies, All Rights Reserved

3-6McGraw-Hill/Irwin

EXAMPLE

• A bond you purchased 2 years ago for $890 is now selling for $925. Coupon payment is $100 per year. You intend to hold the bond for 4 more years and project that you will be able to sell it at the end of year 4 for $960. You also project that the bond will continue paying $100 in interest per year. Given the risk associated with the bond required rate of return is 11.25%. What is its Fair Value?

• Expected rate of return?• Realized rate of return?

©2009, The McGraw-Hill Companies, All Rights Reserved

3-7McGraw-Hill/Irwin

Bond Valuation

• The present value of a bond (Vb) can be written as:

M = the par value of the bond

INT = the annual interest (or coupon) payment

T = the number of years until the bond matures

i = the annual interest rate (often called yield to maturity (ytm))

• The present value of a bond (Vb) can be written as:

M = the par value of the bond

INT = the annual interest (or coupon) payment

T = the number of years until the bond matures

i = the annual interest rate (often called yield to maturity (ytm))

)()(2

)2/1()2/1(

1

2

2,2/2,2/

2

12

TiTi

T

tT

d

t

d

b

ddPFIVMPVIFA

INT

i

M

i

INTV

©2009, The McGraw-Hill Companies, All Rights Reserved

3-8McGraw-Hill/Irwin

EXAMPLE

A bond with a face value of $1000 pays 10%coupon interest rate. Coupon payments are made semiannually. The bond matures in 12 years. If the required rate of return (rrr) is 8%, what is the market value of the bond?What if rrr is 10%What if rrr is 12%

©2009, The McGraw-Hill Companies, All Rights Reserved

3-9McGraw-Hill/Irwin

Bond Valuation

• A premium bond has a coupon rate (INT) greater then the required rate of return (rrr) and the fair present value of the bond (Vb) is greater than the face value (M)

• Discount bond: if INT < rrr, then Vb < M

• Par bond: if INT = rrr, then Vb = M

• A premium bond has a coupon rate (INT) greater then the required rate of return (rrr) and the fair present value of the bond (Vb) is greater than the face value (M)

• Discount bond: if INT < rrr, then Vb < M

• Par bond: if INT = rrr, then Vb = M

©2009, The McGraw-Hill Companies, All Rights Reserved

3-10McGraw-Hill/Irwin

Yield to Maturity

• It is the yield (return) the bondholder will earn on the bond if he or she buys it at its current market price, receives all coupon payments and holds the bond until maturity.

2

22)(b

b

VMTVMINT

AppYTM

©2009, The McGraw-Hill Companies, All Rights Reserved

3-11McGraw-Hill/Irwin

EXAMPLE

• You purchase bond with $1000 face value that pay 11% coupon interest per year. Coupons are paid semiannually. The bond matures in 15 years. If the current market prce of the bond is $931.76

©2009, The McGraw-Hill Companies, All Rights Reserved

3-12McGraw-Hill/Irwin

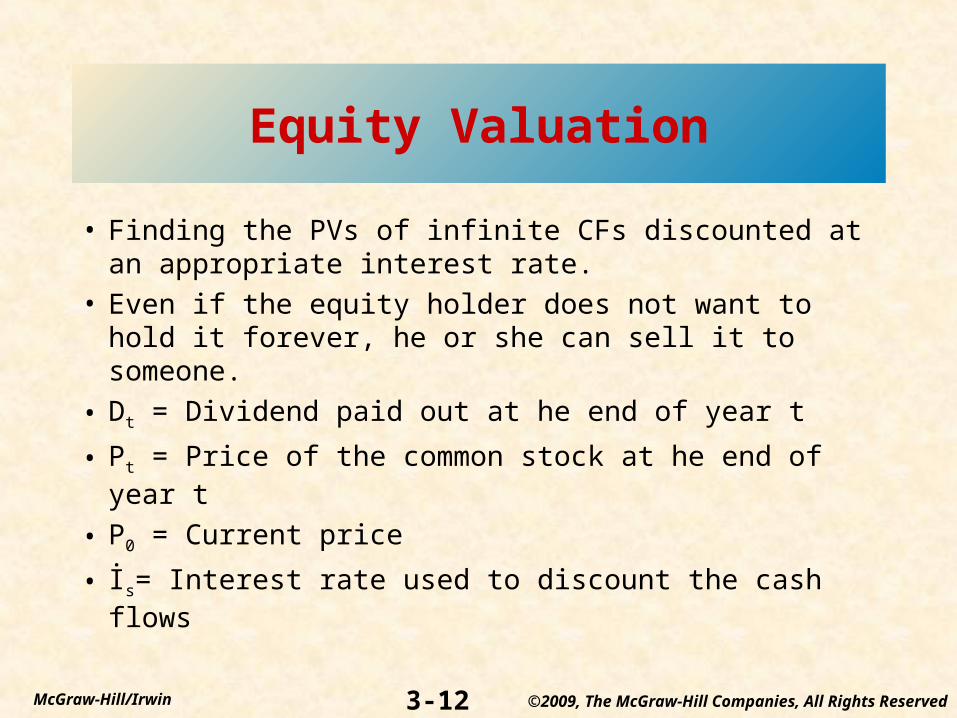

Equity Valuation

• Finding the PVs of infinite CFs discounted at an appropriate interest rate.

• Even if the equity holder does not want to hold it forever, he or she can sell it to someone.

• Dt = Dividend paid out at he end of year t

• Pt = Price of the common stock at he end of year t

• P0 = Current price

• İs= Interest rate used to discount the cash flows

©2009, The McGraw-Hill Companies, All Rights Reserved

3-13McGraw-Hill/Irwin

EXAMPLE

• Suppose you owned a stock for 2 years. You originally bought the stock two years ago for $15 and just sold it for $35. The stock paid an annual dividend of $1 on the last day of each of the past two years. What is the raealized rate of return (rr) on the stock?

©2009, The McGraw-Hill Companies, All Rights Reserved

3-14McGraw-Hill/Irwin

EXAMPLE

• You are considering to purchase the stock that you expect to own for the next 3 years. The current market price is $32 and you expect to sell it for $45 in three years’ time. You also expect the stock to pay an annual dividend of $1.50 on the last day of each of the next 3 years. Calculate the expected rate of return (Err)?

©2009, The McGraw-Hill Companies, All Rights Reserved

3-15McGraw-Hill/Irwin

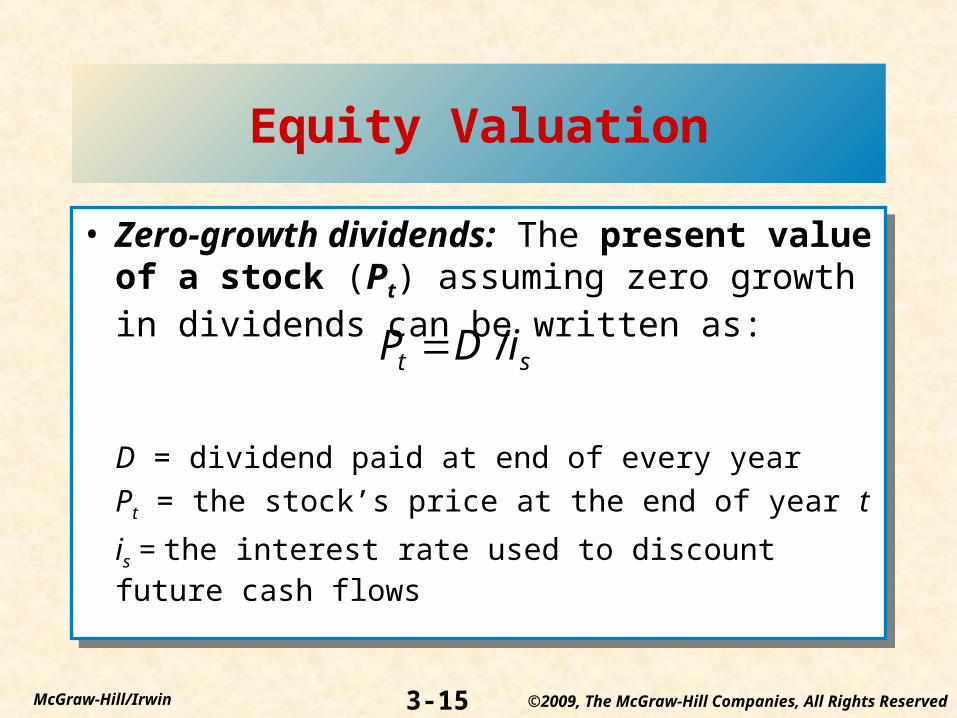

Equity Valuation

• Zero-growth dividends: The present value of a stock (Pt) assuming zero growth in dividends can be written as:

D = dividend paid at end of every year

Pt = the stock’s price at the end of year t

is = the interest rate used to discount future cash flows

• Zero-growth dividends: The present value of a stock (Pt) assuming zero growth in dividends can be written as:

D = dividend paid at end of every year

Pt = the stock’s price at the end of year t

is = the interest rate used to discount future cash flows

st iDP /

©2009, The McGraw-Hill Companies, All Rights Reserved

3-16McGraw-Hill/Irwin

Equity Valuation

• The return on a stock with zero dividend growth, if purchased at price P0, can be written as:

• If the fair market price is applied to this formula, the return we solve for is required rate of return

• If the current market price is applied, the return is expected rate of return.

• In effcient market rrr=Err

• The return on a stock with zero dividend growth, if purchased at price P0, can be written as:

• If the fair market price is applied to this formula, the return we solve for is required rate of return

• If the current market price is applied, the return is expected rate of return.

• In effcient market rrr=Err

0/ PDis

©2009, The McGraw-Hill Companies, All Rights Reserved

3-17McGraw-Hill/Irwin

EXAMPLE

• Suppose the company pays a onstant dividend of $5 per year. What is the current market price of the stock if the expected rate of return is 12%

©2009, The McGraw-Hill Companies, All Rights Reserved

3-18McGraw-Hill/Irwin

Equity Valuation

• Constant growth dividends: The present value of a stock (Pt) assuming constant growth in dividends can be written as:

D0 = current value of dividendsDt = value of dividends at time t = 1, 2, …, ∞g = the constant dividend growth rate

• Constant growth dividends: The present value of a stock (Pt) assuming constant growth in dividends can be written as:

D0 = current value of dividendsDt = value of dividends at time t = 1, 2, …, ∞g = the constant dividend growth rate

gi

D

gi

gDP

s

t

s

t

t

10 )1(

©2009, The McGraw-Hill Companies, All Rights Reserved

3-19McGraw-Hill/Irwin

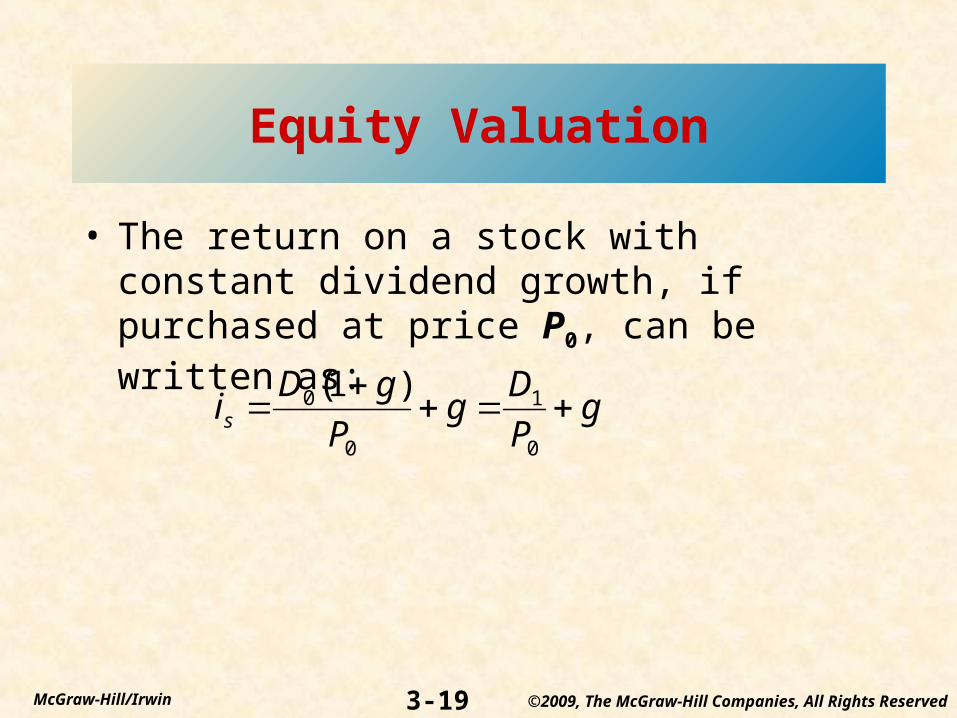

Equity Valuation

• The return on a stock with constant dividend growth, if purchased at price P0, can be written as:

gP

Dg

P

gDis

0

1

0

0 )1(

©2009, The McGraw-Hill Companies, All Rights Reserved

3-20McGraw-Hill/Irwin

EXAMPLE

• You are evaluating a stock paid a dividend at the end of last year of $3.5. Dividend has grown at a constant rate of 2% per year over the last 20 years, this constant growth is expected to continue. The required rate of return is 10%. Calculate the fair value of the stock

©2009, The McGraw-Hill Companies, All Rights Reserved

3-21McGraw-Hill/Irwin

EXAMPLE

• A stock you are evaluating paid a dividend at the nd of the last year of $4.80. Dividends have grown at a constant rate of 1.75 over the last 15 years. And this growth rate is expected to continue into the future. The stock is currently selling for $52 per share. What is the expected rate of return?

©2009, The McGraw-Hill Companies, All Rights Reserved

3-22McGraw-Hill/Irwin

Equity Valuation

• Supernormal or Non-constant Growth in Dividends: Firms ofteh experience periods of supernormal or non-constnt dividend growth. Dividends during the periods of supernormal must be evaluated individually.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-23McGraw-Hill/Irwin

Equity Valuation

• Step 1: Find the PV of dividends during the supernormal period.

• Step 2: Find the price of the stock at the end of the supernormal growth using constant growth model.

• Step 3: Add the two components of the stock price together.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-24McGraw-Hill/Irwin

EXAMPLE

• A stock is expected to experience supernormal growth in dividends of 10% over the next 5 years. Following this period, dividends are expected to grow at a constant rate of 4%. The stock is paid a dividend of $4 last year and the required rate of return is 15%. Calculate the fair value of the stock.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-25McGraw-Hill/Irwin

Relation between InterestRates and Bond Values

Interest Rate

Bond Value

Interest Rate

Bond Value

12%

10%

8%

874.50 1,000 1,152.47

©2009, The McGraw-Hill Companies, All Rights Reserved

3-26McGraw-Hill/Irwin

Impact of Maturity onInterest Rate Sensitivity

Absolute Value of Percent Change in aBond’s Price for aGiven Change inInterest Rates

Absolute Value of Percent Change in aBond’s Price for aGiven Change inInterest Rates

Time to Maturity

©2009, The McGraw-Hill Companies, All Rights Reserved

3-27McGraw-Hill/Irwin

Impact of Coupon Rates onInterest Rate Sensitivity

Bond Value

Bond Value

Interest Rate

Low-Coupon Bond

High-Coupon Bond

©2009, The McGraw-Hill Companies, All Rights Reserved

3-28McGraw-Hill/Irwin

Duration

• Duration is the weighted-average time to maturity (measured in years) on a financial security

• Duration measures the sensitivity (or elasticity) of a fixed-income security’s (bond) price to small interest rate changes

• Duration is the weighted-average time to maturity (measured in years) on a financial security

• Duration measures the sensitivity (or elasticity) of a fixed-income security’s (bond) price to small interest rate changes

©2009, The McGraw-Hill Companies, All Rights Reserved

3-29McGraw-Hill/Irwin

Duration

• Macauley’s Duration

• For investors and financial managers duration is a tool that can be used to estimate the change in the value of a portfolio of securities or even firm value for a given change in interest rates.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-30McGraw-Hill/Irwin

EXAMPLE

• Consider a bond 1 year remaining to maturity, $1000 face value, 8% coupon rate (paid semiannually) and an interest rate of 10%. Calculate duration?

©2009, The McGraw-Hill Companies, All Rights Reserved

3-31McGraw-Hill/Irwin

Duration

• Duration (D) for a fixed-income security that pays interest annually can be written as:

t = 1 to T, the period in which a cash flow is receivedT = the number of years to maturity

CFt = cash flow received at end of period tR = yield to maturity or required rate of return

PVt = present value of cash flow received at end of period t

• Duration (D) for a fixed-income security that pays interest annually can be written as:

t = 1 to T, the period in which a cash flow is receivedT = the number of years to maturity

CFt = cash flow received at end of period tR = yield to maturity or required rate of return

PVt = present value of cash flow received at end of period t

T

tt

T

tt

T

tt

t

T

tt

t

PV

tPV

RCF

RtCF

D

1

1

1

1

)1(

)1(

©2009, The McGraw-Hill Companies, All Rights Reserved

3-32McGraw-Hill/Irwin

Duration

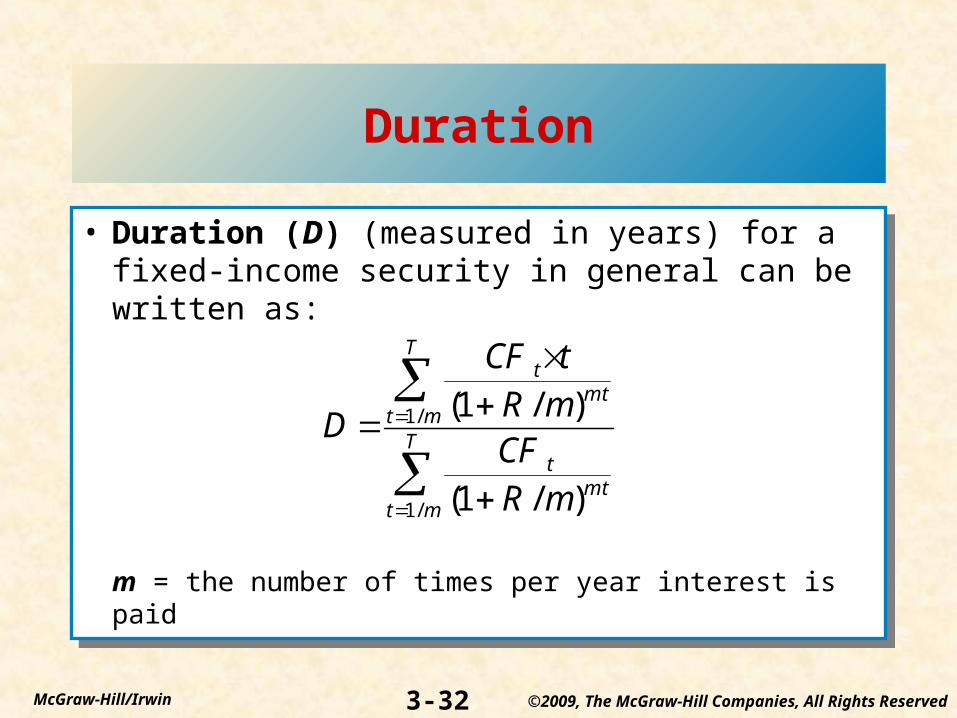

• Duration (D) (measured in years) for a fixed-income security in general can be written as:

m = the number of times per year interest is paid

• Duration (D) (measured in years) for a fixed-income security in general can be written as:

m = the number of times per year interest is paid

T

mtmt

t

T

mtmt

t

mR

CFmR

tCF

D

/1

/1

)/1(

)/1(

©2009, The McGraw-Hill Companies, All Rights Reserved

3-33McGraw-Hill/Irwin

EXAMPLE

• Suppose that you have a bond that offers a coupon rate of 10% paid semiannually. Face value is $1000, it matures in 4 years, its current yield to maturity is 8%. Calculate duration.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-34McGraw-Hill/Irwin

Duration

• The Duration of Zero-coupon Bond: Zero-coupon bonds sell at discount from face value on issue and pay their face value on maturity.

• P = 1000/(1+R/2)T

©2009, The McGraw-Hill Companies, All Rights Reserved

3-35McGraw-Hill/Irwin

EXAMPLE

• Suppose that you have a zero-coupon bond with a face value of $1000, a maturity of 4 years, current yield to maturity of 8% compounded semiannually.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-36McGraw-Hill/Irwin

Duration

• Duration and coupon interest– the higher the coupon payment, the lower the bond’s

duration

• Duration and yield to maturity– the higher the yield to maturity, the lower the bond’s

duration

• Duration and maturity– duration increases with maturity at a decreasing rate

• Duration and coupon interest– the higher the coupon payment, the lower the bond’s

duration

• Duration and yield to maturity– the higher the yield to maturity, the lower the bond’s

duration

• Duration and maturity– duration increases with maturity at a decreasing rate

©2009, The McGraw-Hill Companies, All Rights Reserved

3-37McGraw-Hill/Irwin

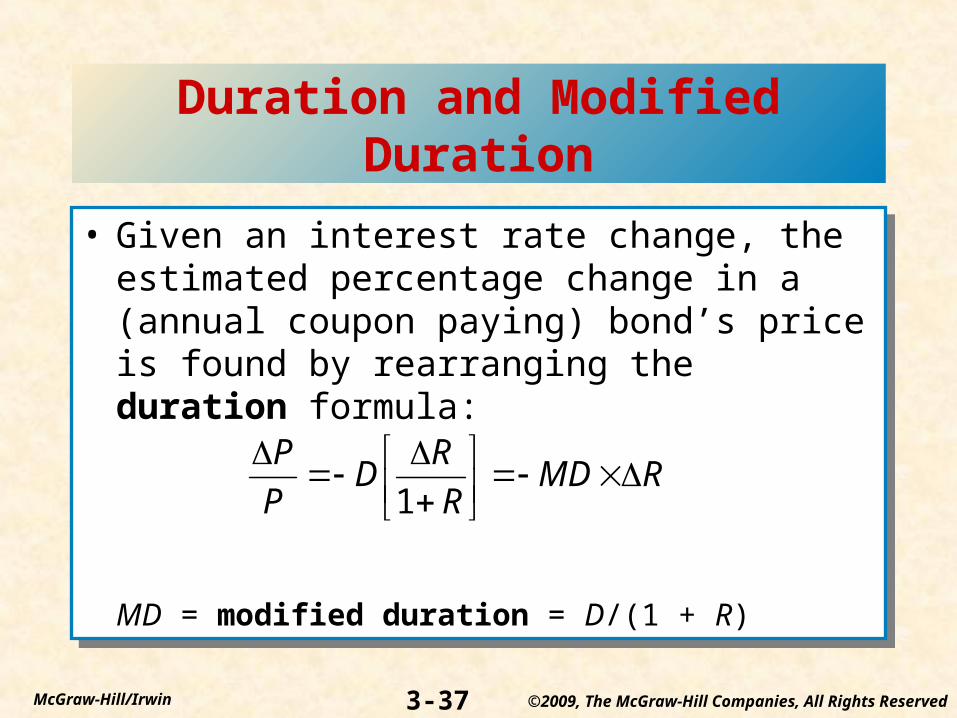

Duration and Modified Duration

• Given an interest rate change, the estimated percentage change in a (annual coupon paying) bond’s price is found by rearranging the duration formula:

MD = modified duration = D/(1 + R)

• Given an interest rate change, the estimated percentage change in a (annual coupon paying) bond’s price is found by rearranging the duration formula:

MD = modified duration = D/(1 + R)

RMDR

RD

P

P

1

©2009, The McGraw-Hill Companies, All Rights Reserved

3-38McGraw-Hill/Irwin

EXAMPLE

• Four-year bond 10% coupon paid semiannually. YTM is 8%. Duration (D)= 3.42 years.

• At 8%, Bond Value =$1067.34 • Suppose that YTM increase by 10 basis points

(1/10 of 1%) from 8% to 8.10%. Bond Value =$1063.83.

• Calculate the sensitivity of bond price to changes in interest rate.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-39McGraw-Hill/Irwin

EXAMPLE

• Four-year bond 6% coupon paid semiannually. YTM is 8%. Duration (D)= 3.6 years.

• At 8%, Bond Value =$932.68 • Suppose that YTM increase by 10 basis points

(1/10 of 1%) from 8% to 8.10%. Bond Value =$929.45.

• Calculate the sensitivity of bond price to changes in interest rate.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-40McGraw-Hill/Irwin

Duration

• The higher the coupon rate, the shorter the duration and the smaller the % decrease in bond’s price.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-41McGraw-Hill/Irwin

Duration

• Duration accurately measures the price sensitivity of financial securities only for small changes in interest rates.

• For large interest rate increases, duration overpredicts the fall in price.

• For large interest rate decreases, duration underpredicts the increase in price.

• Bond price and interest rate relationship exibiting a property called convexity.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-42McGraw-Hill/Irwin

Figure 3-7

©2009, The McGraw-Hill Companies, All Rights Reserved

3-43McGraw-Hill/Irwin

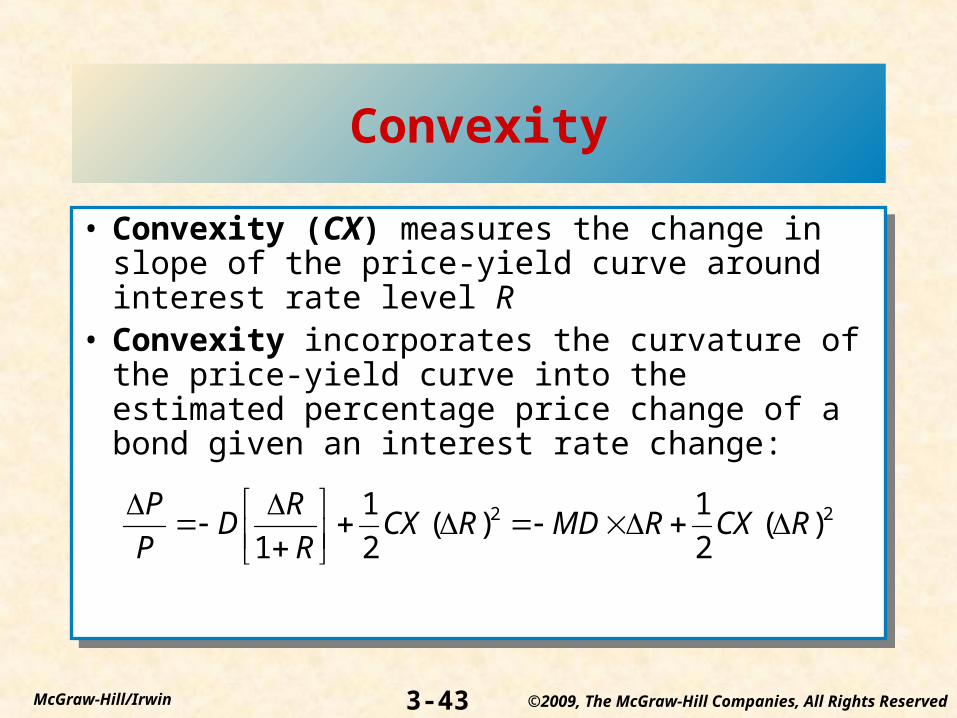

Convexity

• Convexity (CX) measures the change in slope of the price-yield curve around interest rate level R

• Convexity incorporates the curvature of the price-yield curve into the estimated percentage price change of a bond given an interest rate change:

• Convexity (CX) measures the change in slope of the price-yield curve around interest rate level R

• Convexity incorporates the curvature of the price-yield curve into the estimated percentage price change of a bond given an interest rate change:

22 )(2

1)(

2

1

1RCXRMDRCX

R

RD

P

P

©2009, The McGraw-Hill Companies, All Rights Reserved

3-44McGraw-Hill/Irwin

EXAMPLE

• 4 year bond, $1000 face value with 10% coupon paid semiannually and a 8% yield. D= 3.42 years

• Current price = $1067.34 at 8% yield.• What will be the bond value if yield increase from

8% to 10% according to the duration model?• What will be the exact change in price after yield

increase to 10%

©2009, The McGraw-Hill Companies, All Rights Reserved

3-45McGraw-Hill/Irwin

EXAMPLE

• What will be the bond value if yield decrease from 8% to 6% according to the duration model?

• What will be the exact change in price after yield decrease to 6%

©2009, The McGraw-Hill Companies, All Rights Reserved

3-46McGraw-Hill/Irwin

Convexity

• Imp. Question for investors and FI is whether the error in the duration equation is big enough to be concerned about. It depends on the size of interest rate change and size of their portfolios.

• High convexity means that for equally large changes of int. rates, (up and down 2%), the capital gain effect of a rate decrease is more than the capital loss effect of a rate increase.

©2009, The McGraw-Hill Companies, All Rights Reserved

3-47McGraw-Hill/Irwin

• 1) Convexity is desirable.

• 2) Convexity diminishes the error in duration.

• 3) All-fixed income securities are convex.