©2007 lincoln national corporation. lcn200712-2011244 12/2007 indexed universal life level 101...

TRANSCRIPT

©2007 Lincoln National Corporation. LCN200712-2011244 12/2007

Indexed Universal Life Level 101

Lincoln LifeElementsSM Indexed UL

Presenter NamePresenter title and organizationApril 19, 2023

Important disclosures

"Standard & Poor's®", "S&P®", "S&P 500®", "Standard & Poor's 500", and "500" are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by Lincoln Variable Insurance Products Trust and its affiliates. The Product is not sponsored, endorsed, sold or promoted by Standard & Poor's and Standard & Poor's makes no representation regarding the advisability of purchasing the Product.

The S&P 500 Index is a price index and does not reflect dividends paid on the underlying stocks.

©2007 Lincoln National Corporation

www.LFG.com

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.

Affiliates are responsible for their own financial and contractual obligations.

Important disclosures. Please read.

Lincoln LifeElementsSM Indexed UL is issued on policy form UL5041 and state variations by the Lincoln National Life Insurance Company, Fort Wayne, IN. The Lincoln National Life Insurance Company is not authorized nor does it solicit business in the state of New York. Product and features subject to state availability. Guarantees are backed by the claims-paying ability of The Lincoln National Life Insurance Company.

Policies sold in New York are issued on policy form UL5041N by Lincoln Life & Annuity Company of New York, Syracuse, NY. The contractual obligations are backed by the claims-paying ability of Lincoln Life & Annuity Company of New York.

In some states, contract terms are set out and coverage may be provided in the form of certificates issued under a group policy issued by The Lincoln National Life Insurance Company to a group life insurance trust.

This material was prepared to support the promotion and marketing of universal life insurance products. Lincoln Financial Group® affiliates, their distributors, and their respective employees, representatives, and/or insurance agents do not provide tax, accounting, or legal advice. Any tax statements contained herein were not intended or written to be used, and cannot be used for the purpose of avoiding U.S. federal, state, or local tax penalties. Please consult your own independent advisor as to any tax, accounting, or legal statements made herein.

Not a depositNot FDIC-insuredNot insured by any federal government agencyNot guaranteed by any bank or savings associationMay go down in value

LCN200712-2011244

Welcome to Indexed UL 101

LCN200712-2011244

Ask yourself…

If I’m not here, will my family still need the income I provide?

Am I concerned about out-living my retirement?

Is continuing to accumulate assets that could provide income important to me?

Am I concerned about market volatility?

Do I need to start saving for my child’s future?

LCN200712-2011244

Life is beautiful

You might consider universal life insurance if

You need to protect your family in case you’re not there.

You need to create wealth to help secure income in retirement

LCN200712-2011244

Life is beautiful

You might consider indexed universal life insurance if

You have a death benefit need.

You need greater growth potential than a fixed rate could offer but are concerned about the impact of market volatility on your assets.

You want flexibility to help pay for college costs, pay for a vacation home, or any surprises life might have for you.

LCN200712-2011244

Challenges to securing your retirement income

Market fluctuationsCost of inflation

LCN200712-2011244

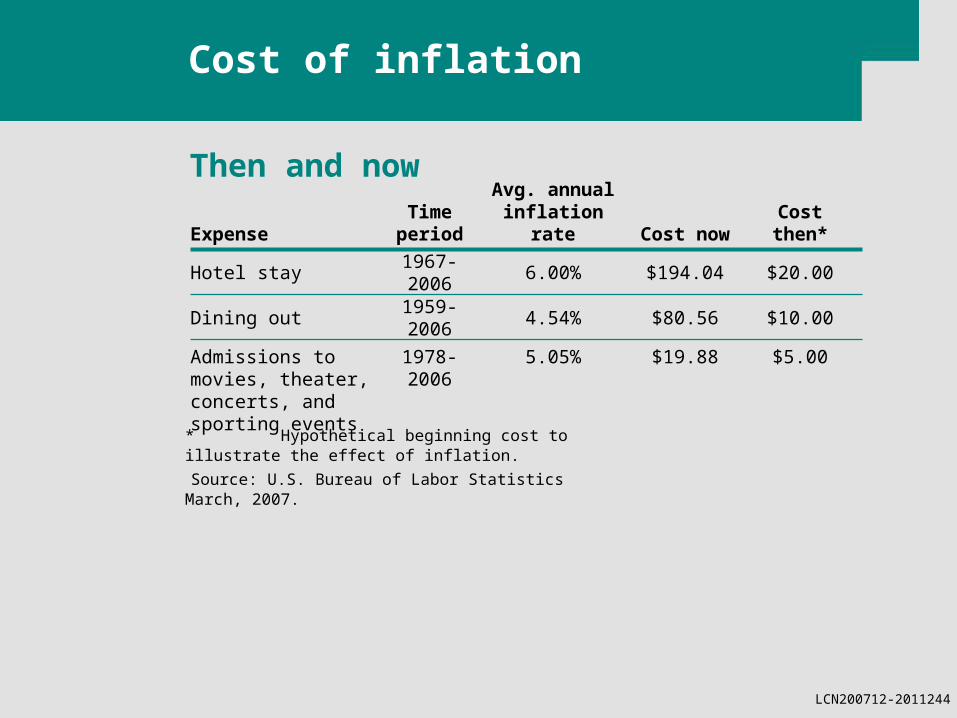

Cost of inflation

Then and now

*Hypothetical beginning cost to illustrate the effect of inflation.Source: U.S. Bureau of Labor Statistics March, 2007.

$5.00

$10.00

$20.00

Cost then*

$19.88

$80.56

$194.04

Cost now

5.05%1978-2006

Admissions to movies, theater, concerts, and sporting events

4.54%1959-2006

Dining out

6.00%1967-2006

Hotel stay

Avg. annual inflation rate

Time periodExpense

LCN200712-2011244

Market volatility

Data source: Ibbotson Associates, March, 2007.

Index past performance is not indicative of future results. The value of securities will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Indexes are unmanaged and unavailable for direct investment. Performance of these indexes does not correspond with any particular investment product and does not represent performance of the insurance product described in this brochure.

Performance of the S&P Index, 1926-2006

LCN200712-2011244

Key benefits

Helps protect your family with a death benefit

Offers opportunities for accumulation

Protects policy values from volatility

Provides a potential source of supplemental income

Indexed Universal Life

LCN200712-2011244

Before jumping in…

Understand the product and potential outcomes

Understand that “Indexed UL” is life insurance

Understand the product components that drive performance:

• caps,• participation rates,• indices,• etc.

Indexed Universal Life

LCN200712-2011244

Indexed Universal Life

Key terms

Cap Maximum growth rate of the indexed interest credited

Spread Amount subtracted from index growth rate

Index The source of values used to determine credited interest rates. (i.e. S&P 500)

Participation Percentage of the index

Crediting Methodology The way in which changes to the index are used to calculate the interest credited.

Guarantee Promised minimum percentage credited to the account

LCN200712-2011244

The markets are as unpredictable as the weather

Lincoln LifeElementsSM Indexed UL protects your family with a reliable death benefit

Protects your principal from market downturns

Offers opportunity for accumulation

Account value for long-term needs

Riders allow for policy customization

Lincoln LifeElementsSM Indexed UL

LCN200712-2011244

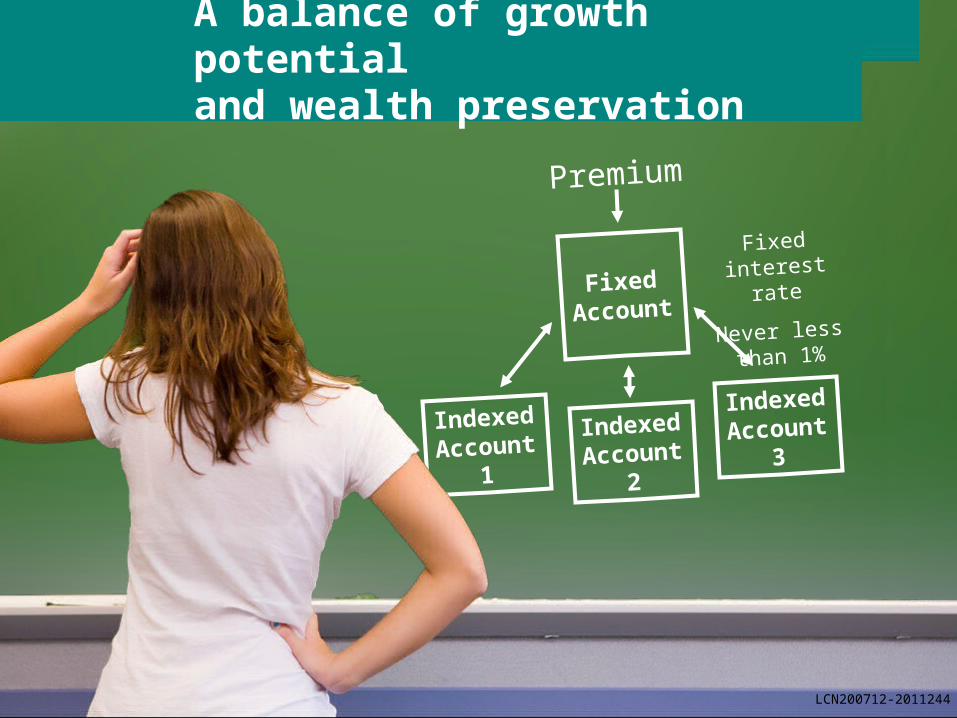

A balance of growth potential and wealth preservation

LCN200709-2007986

Premium

Indexed

Account1

Indexed

Account3

Indexed

Account2

Fixed Account

Fixed

interest rate

Never less

than 1%

LCN200712-2011244

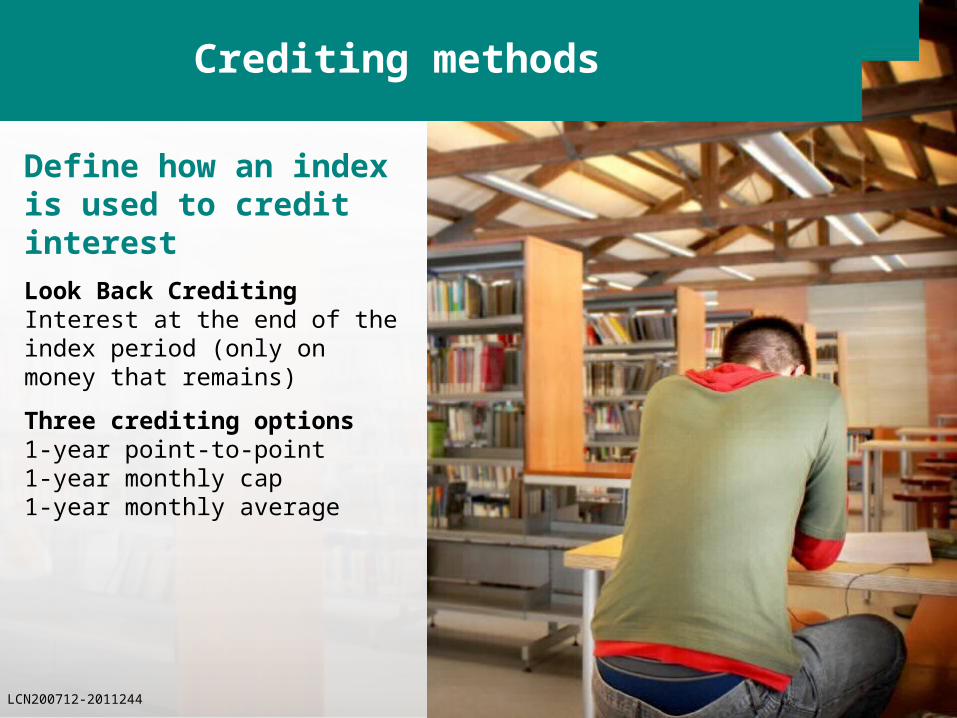

Define how an index is used to credit interest

Look Back CreditingInterest at the end of the index period (only on money that remains)

Three crediting options1-year point-to-point1-year monthly cap1-year monthly average

Crediting methods

LCN200712-2011244

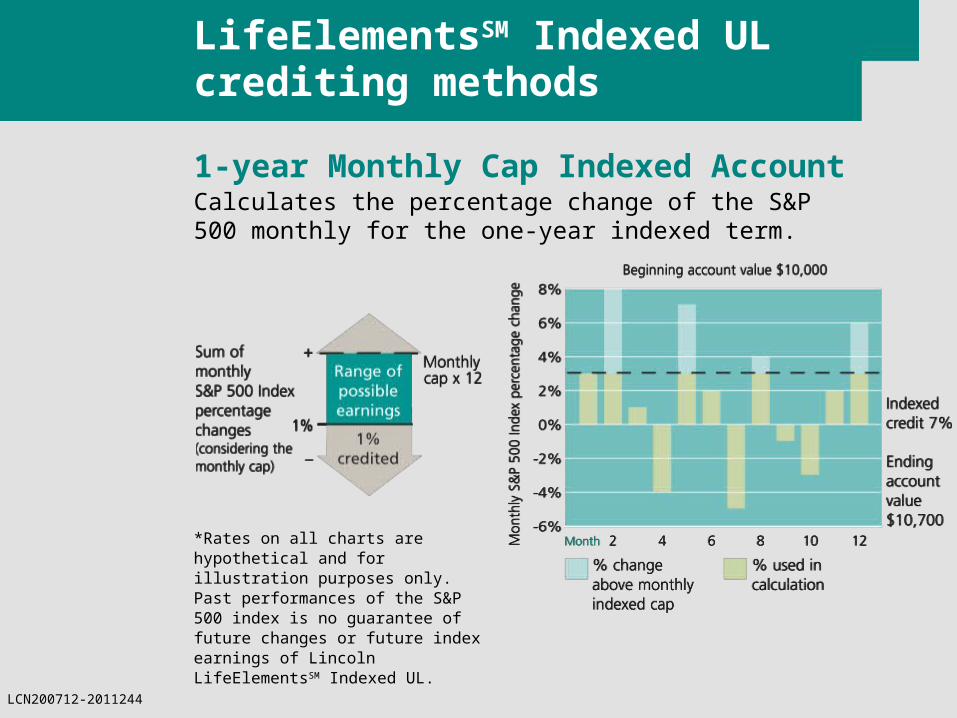

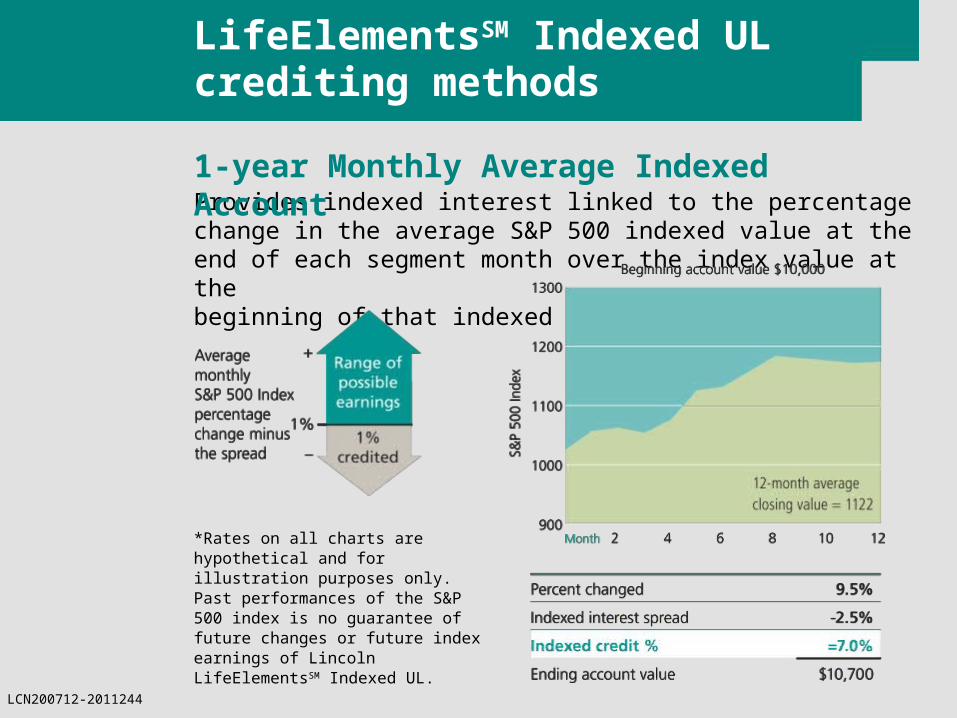

LifeElementsSM Indexed UL crediting methods

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL.

1-year Point-To-Point Indexed AccountThe value at the end of the one-year indexed term is compared to the value at the beginning of the term.

LCN200712-2011244

LifeElementsSM Indexed UL crediting methods

Calculates the percentage change of the S&P 500 monthly for the one-year indexed term.

1-year Monthly Cap Indexed Account

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL.

LCN200712-2011244

LifeElementsSM Indexed UL crediting methods

Provides indexed interest linked to the percentage change in the average S&P 500 indexed value at the end of each segment month over the index value at the beginning of that indexed term.

1-year Monthly Average Indexed Account

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL.

LCN200712-2011244

How’s the market?

LCN200712-2011244

The volatile market

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL. LCN200712-2011244

The bear market

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL. LCN200712-2011244

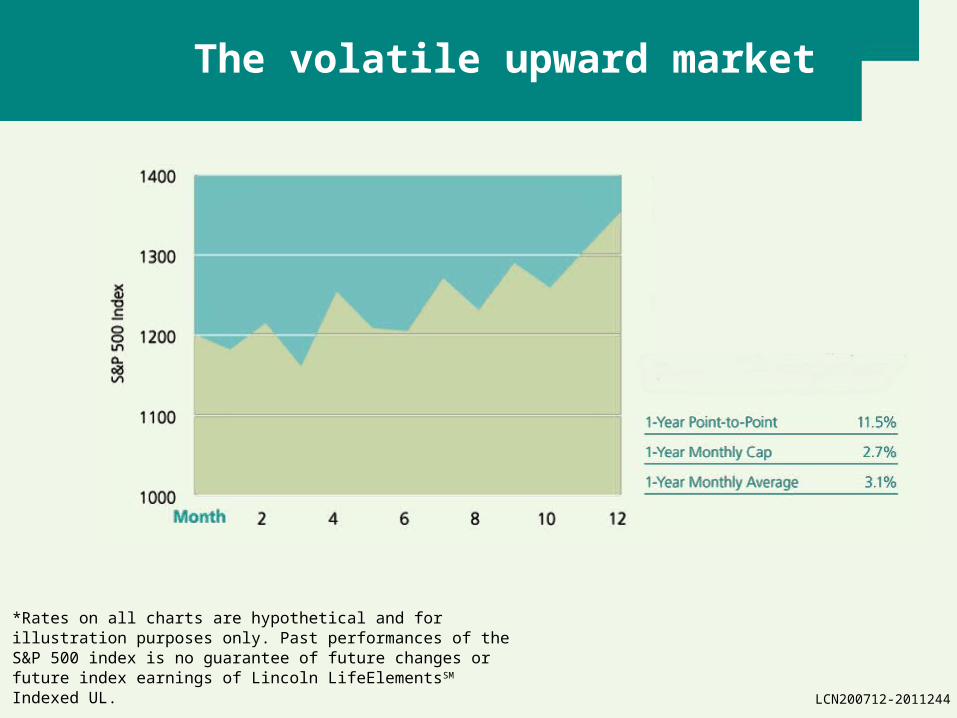

The volatile upward market

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL. LCN200712-2011244

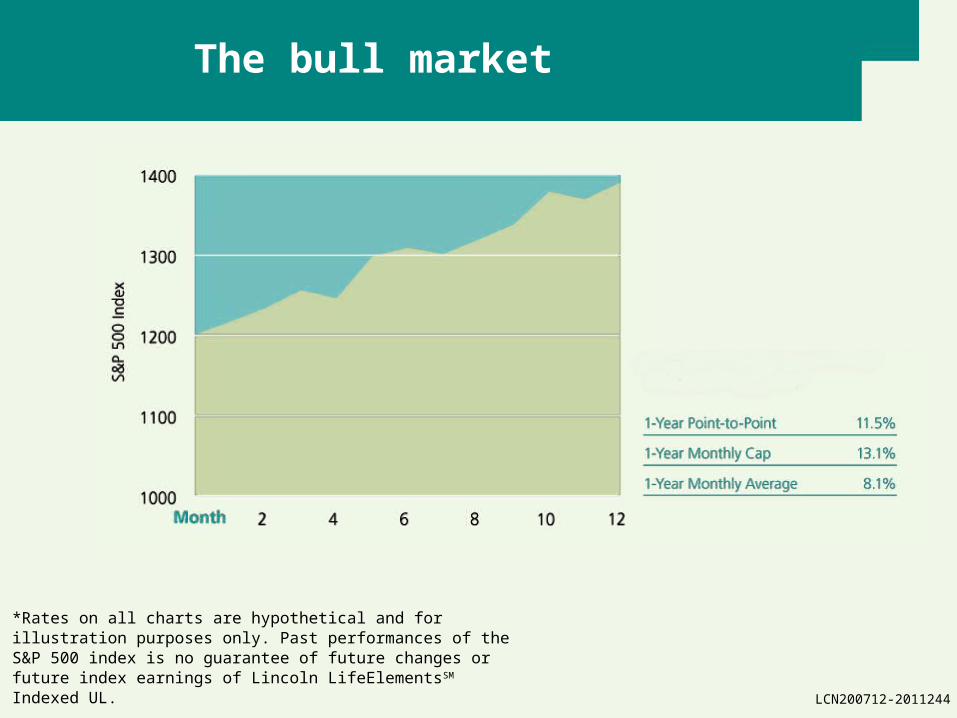

The bull market

*Rates on all charts are hypothetical and for illustration purposes only. Past performances of the S&P 500 index is no guarantee of future changes or future index earnings of Lincoln LifeElementsSM Indexed UL. LCN200712-2011244

Withdrawals

Minimum withdrawal

Possible tax implications

Transaction fee

100% of cash surrender value

Withdrawal limitations

Loans and withdrawals will reduce account value and death benefit LCN200712-2011244

Loans

Your funds continue to work

Borrow up to 100% of cash surrender value

Loan accrues interest

Loans from the Fixed Account add flexibility

Loans and withdrawals will reduce account value and death benefit LCN200712-2011244

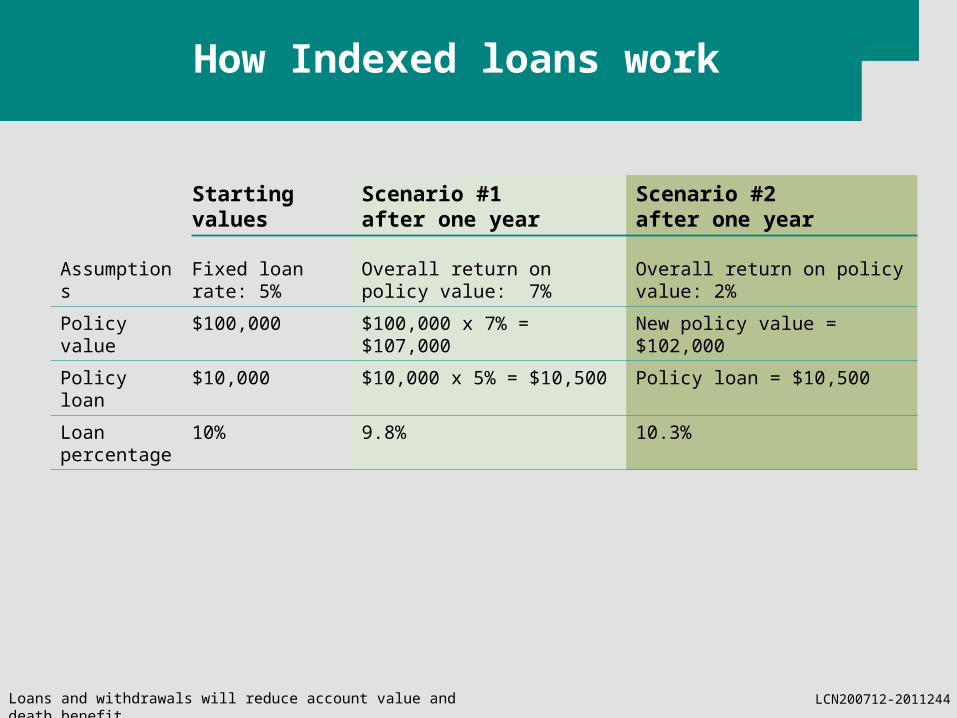

How Indexed loans work

Starting values

Scenario #1 after one year

Scenario #2 after one year

AssumptionsFixed loan rate: 5%

Overall return on policy value: 7%

Overall return on policy value: 2%

Policy value $100,000 $100,000 x 7% = $107,000 New policy value = $102,000

Policy loan $10,000 $10,000 x 5% = $10,500 Policy loan = $10,500

Loan percentage

10% 9.8% 10.3%

Loans and withdrawals will reduce account value and death benefit LCN200712-2011244

Why Lincoln LifeElementsSM Indexed UL?

Optional riders & benefits• Overloan Protection Endorsement

• Supplemental Term Insurance Rider on Primary Insured

• Supplemental Term Insurance Rider on Other Insured

• Accidental Death Benefit Rider

• Children’s Insurance Rider

• Guaranteed Insurability Rider

• Disability Waiver of Monthly Deductions Benefit

• Disability Waiver of Specified Premium

• Accelerated Benefits Rider

• Disability Income Rider

• Non-working Spouse Disability Income RiderOptional riders and benefits are available at an additional cost.

Availability of benefits, riders, and features may vary by state. LCN200712-2011244

John and Maria

Over the years, John and Maria have created a fairly aggressive portfolio to prepare for their retirement. As they are getting closer to retirement, they are concerned about having a significant percentage of their assets exposed to the market.

To balance out their portfolio risk, they want assets that are still able to increase over time as they are still preparing for retirement, but they want more assets protected from market downturns.

How it can work for you

LCN200712-2011244

John and Maria

And for those assets not needed for income, they also want to make sure that they have both the protection of life insurance and its tax efficiency for creating a legacy for their family.

How it can work for you

LCN200712-2011244

Goals

Creating a tax-efficient legacy for their family through death benefit protection

Protecting assets

Flexibility in their retirement income

Increasing long-term purchasing power

How it can work for you

LCN200712-2011244

Why a LifeElementsSM Indexed UL policy might be the right choice

Death benefit creates a tax-efficient legacy for their family

Protection from volatility

The flexibility to use the account value for supplementing their income

The opportunity to increase their assets

How it can work for you

Loans and withdrawals will reduce account value and death benefit

LCN200712-2011244

Dave and Tanya

The last of Dave and Tanya’s three children just graduated from college, and they want to make up for lost time. Their chief concern for their overall portfolio is not having enough saved for retirement.

With that issue in mind, they want to make sure more of their portfolio works harder. At the same time, they want to somehow protect the assets they do have, so they don’t lose any ground toward their retirement goals.

How it can work for you

LCN200712-2011244

Dave and Tanya

They know they still need the protection that life insurance offers in case something happens to one of them, but they also want it to be flexible enough. Dave and Christine both work full time and earn substantial salaries, allowing them to maximize their premiums to a policy.

How it can work for you

LCN200712-2011244

Goals

Death benefit protection for their family

Making up for lost time with their retirement savings

Increasing long-term purchasing power

Protecting assets

How it can work for you

LCN200712-2011244

Why a LifeElementsSM Indexed UL policy might be the right choice

Solve two needs with one product: the protection of life insurance combined with the opportunity to increase assets

Multiple index accounts allow them to create a portfolio that can take advantage of different market environments

Protection from volatility with a guaranteed minimum of 1%

Flexibility to use the account value for supplementing their income

How it can work for you

Loans and withdrawals will reduce account value and death benefit LCN200712-2011244

Final exam

LCN200712-2011244

Contact information

Securities and investment advisory services distributed by Lincoln Financial Distributors, Inc., a broker/dealer and registered investment advisor. Insurance offered through Lincoln affiliates. Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates.

Presenter NamePresenter Title and Organization(888) [email protected]

Second Presenter NamePresenter Title and Organization(888) [email protected]

Third Presenter NamePresenter Title and Organization(888) [email protected]

Presenter NamePresenter Title and Organization(888) [email protected]

Second Presenter NamePresenter Title and Organization(888) [email protected]

Third Presenter NamePresenter Title and Organization(888) [email protected]

LCN200712-2011244