2007 annual report -...

TRANSCRIPT

2007 Annual Report

[jumbo loan] [auto loan] [secure loan] [education loan] [equipment loan]11011 Wilcrest drive, suite k, houston, texas 77099 p.o. box 721496, houston, texas 77272-1496

MEMBERS HELPING MEMBERS

CRED

IT U

NION

MUSLIM

Board of Directors 2007

Shaukat AliPresident/CEO

Zulfiqar MohammedVice Chairman

Javaid R DhukaChairman

Asif MarediaTreasurer

Noordin KhojaMember, Supervisory Committee

Rahim MaknojiaSecretary

Sohrab K AliMember, Credit Committee

Zikar MarediaChairman, Supervisory Committee

Ahmedali MominChairman, Credit Committee

Hasan MarediaMember, Marketing Committee

Irfan K AliMember, Credit Committee

Gulbano MohammedLoan Officer

Salma MaknojiaAdministrative Officer

Parveen AliLoan Officer

Ali Ahmed MominAdministrative Assistant

Naeem Charolia Administrative Assistant

Nooruddin MominAccountant

Ambreen MaknojiaCollection Officer

Faiza AliHead Teller/Supervisor

HOUSTON OFFICE

11011 Wilcrest Drive, Suite KHouston, TX 77099

P. O. Box 721496Houston, TX 77272-1496

Telephone (281) 568-6000Fax (281) 568-8054

Toll Free 1-877 OUR PMCU (687-7628)Audio Response (281) 568-8558Email Adress [email protected]

www.pmcuonline.org

OFFICE HOURSMonday - Friday 9:00 am - 5:00 pm

Saturday, Sunday Closed

AUSTIN OFFICE

5555 North Lamar Blvd., Suite C 107Austin, TX 78751

Toll Free 1-877 OUR PMCU (687-7628)Audio Response (281) 568-8558Email Adress [email protected]

OFFICE HOURSMonday - Friday 9:00 am - 3:00 pm

1 hour after Jamat KhanaSaturday, Sunday Closed

Office Staff 2006

Table of Contents

DESCRIPTION PAGE #

Chairman's Report 1

Supervisory & Credit Committee's Report 2

Statement of Financial Position 3

Statement of Operations 4

Statement of Cash Flows 5

Statement of Equity/Key Financial Ratios 6

Notes to Financial Statements 7

Savings, Loans, Membership,

Networth & Assets Bar Charts 11

Chairman's ReportMESSAGE FROM CHAIRMAN, BOARD OF DIRECTORS

As we look back on 2007, we achieved considerable accomplishments that helped strengthen our Credit Union and make it one of the strongest credit unions in the United States. The following numbers speak for themselves.

We have increased total equity by almost 10% to reach the $10 million milestone giving us a top 10% rank as to net worth. Our delinquency is now less than 1%, which improved profitability significantly and helped us achieve top regulatory ratings for Delinquent loans to Total loans. Our loan portfolio increased over 10% by giving out more than $15 million in new loans. We are strengthening our talent across the credit union by improved training of staff and recruitment of new employees. We are continuing to improve our policies and procedures to streamline application processes for loans & new memberships. You have witnessed improvement in our marketing and communication with members via quarterly newsletters and the upgraded PMCU website.

We at People's Pioneer Muslim Credit Union would like to say "thank you" for your loyalty and support and for using your own Credit Union for your financial needs. We realize the decision to conduct your financial business with us is a choice - a choice that is growing in options every week and month as new players enter the field with introductory offers.

Please remember the money experts at PMCU are there to help you with your financial needs. I would like to give a heartfelt thanks to our Board of Directors and Advisory Committee who volunteers their valuable time, talents, and energy for our credit union. Thanks also to our wonderful management and staff for their commitment, devotion, and hard work.

Javaid DhukaChairman of the Board

1

Supervisory Committee's ReportTHE BOARD OF DIRECTORS – PIONEER MUSLIM CREDIT UNION

The Supervisory Committee's major responsibilities are to ensure an independent internal Supervisory audit is performed every month. To carry out its responsibilities, the Supervisory Committee, accountant and independent auditor perform auditing. This includes account verifications, Management reports, Accuracy of the statements, and Suggestions/ Recommendations for improvement in reporting.

The Committee reviews audit reports of our Federal and State Regulators when it conducts its examination on regular basis. The Committee also works with the internal auditor to ensure that the policies and procedures are being followed and that internal controls are in place.

The Committee is pleased to report that PMCU is a financially sound organization dedicated to serving its members. Our Supervisory Annual audit conducted for 2007 was successfully completed. The Supervisory Committee will continue to work with the Board of Directors, CEO and the employees for the 2008 and looks forward to another prosperous year.

Zikar A. Maredia Chairman, Supervisory Committee ___________________________________________________________________________

Credit Committee's ReportTO THE MEMBERS - PIONEER MUSLIM CREDIT UNION

The Credit Committee is appointed by the Board of Directors to review, approve and monitor the loan portfolio. Loan policies and rates are revised by the Board of Directors with the consultation of Credit Committee. During the year 2007 the Credit Union received 561 loan applications and approved 530 loans totaling to $15,379,563.57 setting loan's to share ratio at 98.45 %. The year was of bench mark for loaning out highest number and amount of loans.

Our members receive benefit of our competitive products, which has encouraged them to enhance their credit score and helped them to qualify for the possible lower loan rates offer by Credit Union. The Credit Union not only provides competitive loan rates but also the products which are innovative and saved member's money.

The Credit Committee will continue to provide its vital services to our members by offering quality products for individuals and families.

Ahmedali R. MominChairman,Credit Committee

2

Statement of Financial Position

FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006

ASSETS

Loans (Schedule -1)

MasterCard Loans

Less: Allowance for Loan Loss

Total Loans

Cash at Bank

Investments (Schedule -3)

N.C.U.S.I.F. Deposit

Rent & Utility Deposits

Total Deposits

Prepaid Surety Bond

Prepaid Fees & Membership

Prepaid for AGM

Total Prep. & Def. Expenses

Furniture & Fixtures

Less: Acc. Depreciation

Net Fixed Assets

Accrued Interest on Loans

Accrued Interest on Certificates

Total Accrued Income

Total Assets

LIABILITIES & EQUITY

Payroll Taxes

Other Payables

Total Payables

Members' Shares (Schedule - 2)

Share Drafts

I.R.A. Shares

Total Shares

Regular Reserve

Undivided Earnings

Total Equity

Total Liabilities & Equity

2007 % 2006 % VARIANCE

$25,087,544 65.59 $22,008,631 60.29 $3,078,913

2,370,240 6.20 2,763,938 7.57 (393,698)

(365,571) -0.96 (729,984) -2.00 364,413

27,092,213 70.83 24,042,585 65.86 3,049,628

446,710 1.17 416,125 1.14 30,585

10,093,604 26.39 11,329,633 31.03 (1,236,029)

260,510 0.68 255,988 0.70 4,522

4,249 0.01 4,249 0.01 0

264,759 0.69 260,237 0.71 4,522

10,921 0.03 13,988 0.04 (3,067)

2,183 0.01 1,836 0.01 347

1,7 0 0

14,804 0.04 15,824 0.05 (1,020)

278,653 0.73 204,533 0.56 74,120

(119,577) -0.31 (63,023) -0.17 (56,554)

159,076 0.42 141,510 0.39 17,566

115,367 0.30 144,203 0.40 (28,836)

61,209 0.16 156,352 0.42 (95,143)

176,576 0.46 300,555 0.82 (123,979)

$38,247,742 100.00 $36,506,469 100.00 $1,741,273

$6,102 0.01 $3,715 0.01 $2,387

10,201 0.03 209 0.00 9,992

16,303 0.05 3,924 0.01 12,379

20,835,744 54.48 20,477,734 56.09 358,010

1,974,638 5.16 2,362,005 6.47 (387,367)

5,078,367 13.28 4,287,039 11.74 791,328

27,888,749 72.92 27,126,778 74.30 761,971

1,250,847 3.27 1,250,847 3.43 0

9,091,843 23.77 8,124,920 22.26 966,923

10,342,690 27.04 9,375,767 25.69 966,923

$38,247,742 100.00 $36,506,469 100.00 $1,741,273

3

4

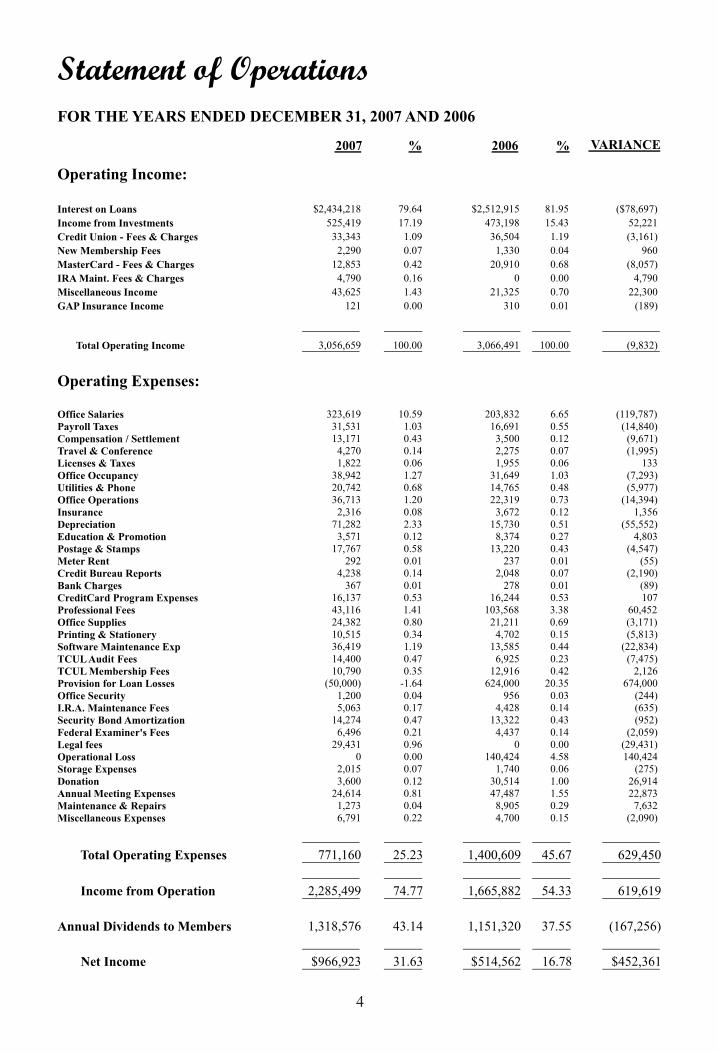

Statement of Operations

FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006

Operating Income:

Interest on Loans

Income from Investments

Credit Union - Fees & Charges

New Membership Fees

MasterCard - Fees & Charges

IRA Maint. Fees & Charges

Miscellaneous Income

GAP Insurance Income

Total Operating Income

Operating Expenses:

Office Salaries Payroll Taxes Compensation / Settlement Travel & Conference Licenses & Taxes Office Occupancy Utilities & Phone Office Operations Insurance Depreciation Education & Promotion Postage & Stamps Meter Rent Credit Bureau Reports Bank Charges CreditCard Program Expenses Professional Fees Office Supplies Printing & Stationery Software Maintenance Exp TCUL Audit Fees TCUL Membership Fees Provision for Loan Losses Office Security I.R.A. Maintenance Fees Security Bond Amortization Federal Examiner's Fees Legal fees Operational Loss Storage Expenses Donation Annual Meeting Expenses Maintenance & Repairs Miscellaneous Expenses

Total Operating Expenses

Income from Operation

Annual Dividends to Members

Net Income

2007 % 2006 %

$2,434,218 79.64 $2,512,91 5 81.95 ($78,697)

525,419 17.19 473,19 8 15.43 52,221

33,343 1.09 36,50 4 1.19 (3,161)

2,290 0.07 1,33 0 0.04 960

12,853 0.42 20,91 0 0.68 (8,057)

4,790 0.16 0 0.00 4,790

43,625 1.43 21,32 5 0.70 22,300

121 0.00 31 0 0.01 (189)

3,056,659 100.00 3,066,49 1 100.00 (9,832)

323,619 10.59 203,83 2 6.65 (119,787) 31,531 1.03 16,69 1 0.55 (14,840) 13,171 0.43 3,50 0 0.12 (9,671)

4,270 0.14 2,27 5 0.07 (1,995) 1,822 0.06 1,95 5 0.06 133

38,942 1.27 31,64 9 1.03 (7,293) 20,742 0.68 14,76 5 0.48 (5,977) 36,713 1.20 22,31 9 0.73 (14,394)

2,316 0.08 3,67 2 0.12 1,356 71,282 2.33 15,73 0 0.51 (55,552)

3,571 0.12 8,37 4 0.27 4,803 17,767 0.58 13,22 0 0.43 (4,547)

292 0.01 23 7 0.01 (55) 4,238 0.14 2,04 8 0.07 (2,190)

367 0.01 27 8 0.01 (89) 16,137 0.53 16,24 4 0.53 107 43,116 1.41 103,56 8 3.38 60,452 24,382 0.80 21,21 1 0.69 (3,171) 10,515 0.34 4,70 2 0.15 (5,813) 36,419 1.19 13,58 5 0.44 (22,834) 14,400 0.47 6,92 5 0.23 (7,475) 10,790 0.35 12,91 6 0.42 2,126

(50,000) -1.64 624,00 0 20.35 674,000 1,200 0.04 95 6 0.03 (244) 5,063 0.17 4,42 8 0.14 (635)

14,274 0.47 13,32 2 0.43 (952) 6,496 0.21 4,43 7 0.14 (2,059)

29,431 0.96 0 0.00 (29,431) 0 0.00 140,42 4 4.58 140,424

2,015 0.07 1,74 0 0.06 (275) 3,600 0.12 30,51 4 1.00 26,914

24,614 0.81 47,48 7 1.55 22,873 1,273 0.04 8,90 5 0.29 7,632 6,791 0.22 4,70 0 0.15 (2,090)

771,160 25.23 1,400,60 9 45.67 629,450

2,285,499 74.77 1,665,88 2 54.33 619,619

1,318,576 43.14 1,151,32 0 37.55 (167,256)

$966,923 31.63 $514,56 2 16.78 $452,361

VARIANCE

5

Statement of Cash Flows

FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006

Cash Flows from Operating Activities:

Net Income for the year

Adjustments to Reconcile Net Income to Net

Cash provided by Operating Activities:

Add: Accumulated Depreciation

Dividends Credited to Members' A/cs

(Increase) Decrease in Accrued Income

Increase (Decrease) in Loan Loss Allowance

Total Adjustments to Net Income

Increase/Decrease in Assets or Liabilities:

(Increase) Decrease in Deposits

(Increase) Decrease in Prepaid & Deferred Exps.

(Increase) Decrease in Furniture & Fixtures

Increase (Decrease) in Payroll Taxes

Net Cash Provided By

Assets or Liabilities:

Net Cash Provided or (Used) By

Operating & Other Activities:

Cash Flows from Investing Activities:

(Increase) Decrease in S.C.F.C.U. A/c

(Increase) Decrease in S.C.F.C.U. Shares

(Increase) Decrease in S.C.F.C.U. Certificates

(Increase) Decrease in United Central Bank

Net Cash Provided or (Used)

By Investment Activities:

Cash Flows from Members' Activities:

Increase (Decrease) in Share Drafts

Increase (Decrease) in Members' Savings

Increase (Decrease) in Members' I.R.A. Savings

(Increase) Decrease in Members' Loans

(Increase) Decrease in MasterCard Loans

Net Cash Provided or (Used)

By Members' Activities:

Net Increase in Cash

Add: Beginning Cash Balance

Ending Cash Balance

2007 2006

$ 9 6 6 , 9 2 3 $514,562

(56,554) (15,458)

1,318,576 1,151,320

(123,979) (84,876)

(364,413) (520,883)

7 7 3 , 6 3 0 530,103

(4,522) (5,301)

(1,020) 189

(74,120) (129,618)

12,379 (1,186)

( 6 7 , 2 8 3 ) (135,916)

1,673,270 908,749

(914,470) (1,030,075)

7,908 0

2,700,000 (3,500,000)

(1,512,879) (1,715,660)

280,559 (6,245,735)

(387,367) (473,569)

358,010 (1,630,578)

791,328 800,779

(3,078,913) 2,901,162

393,698 952,117

(1,923,244) 2,549,911

3 0 , 5 8 5 (2,787,075)

416,125 3,203,200

446,710 416,125

Consolidated Statement of Equity FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006

Regular Reserve

Undivided Earnings

Current Income

Equity (Net Worth)

(A) (B) (C) (A+B+C)

Balance at December 31, 2005 $1,250,847 $7,321,630 $288,728 $8,861,205

Account activities during 2006: Transfer of 2005 Current Income 0Statutory transfer to Regular Reserve 0Net Income -2005 0 0Other comprehensive income:

Balance at December 31, 2006 $1,250,847 $7,610,358 $514,562 $9,375,767

Account activities during 2007: Transfer of 2006 Current Income 0 0Statutory transfer to Regular Reserve 0 0 0 0Net Income - 2006 0 0Other comprehensive income:

Balance at December 31, 2007 $1,250,847 $8,124,920 $966,923 $10,342,690

KEY FINANCIAL RATIOS

For the Year 2003 PEER AVGS

% % % % % %Net Worth/Total Assets Delinquent Loans/Total Loans Net Charge-Offs/Avg. Loans Return on Avg. Assets Gross Income/Avg. Assets Cost of Funds/Avg. Assets Operating Exps./Avg. Assets Net Interest Margin/Avg. Assets Operating Exps./Gross Income Net Operating Exps./Average Income Total Loans/Total Shares Total Loans/Total Assets Net Worth Growth Market (Share) Growth Loan Growth Asset Growth Investment Growth

6

288,728 (288,728) 00 00 0

514,562 514,562

514,562 (514,562)

966,923 966,923

The Regular Reserve has been established in accordance with the Statutory Requirements. Under these guidelines, PMCU is required to make transfers from Undivided Earnings to Regular Reserve if Risk Asset Ratio is less than 4% of Gross Income. If required, the transfers can range from 5% to 10% of Gross Income depending on whether the Risk Asset Ratio is less than 4% or less than 6%.

22.971.340.003.479.164.311.264.59

13.751.00

96.2574.1216.3715.3914.1415.6120.56

23.831.480.363.188.473.681.214.15

14.300.75

101.3377.1614.56

4.3014.97

9.21-3.42

23.756.470.000.798.743.871.224.42

13.910.77

100.6876.75

3.373.803.143.70

18.57

25.682.004.271.398.313.122.104.97

25.331.89

91.3267.86

5.81-4.58

-13.46-2.1224.66

27.040.781.202.598.183.532.204.39

26.861.94

98.4571.7910.31

2.8110.84

4.77-10.14

14.461.370.500.647.232.084.214.02

57.353.33

72.5861.43

5.212.362.182.61

12.55

2004 2005 2006 2007

7

Notes To Financial Statements FOR THE YEARS ENDED DECEMBER 31, 2007 AND 2006

1. NATURE OF BUSINESSPioneer Muslim Credit Union (PMCU) was established in 1981. Although the general membership continues to grow at a steady rate, there are many more individuals who are eligible to become members and could benefit from Credit Union's programs. PMCU has managed to achieve these great results in spite of an economy which is constantly under pressure. As a matter of policy and to compete in the market, the credit union has been offering competitive dividend on the shareholders' savings and lower interest rates on the loans. The goal of the PMCU is to help the members in their financial needs through the services and products offered as follows.

LoansCredit Union continues to strive to improve and streamline the loan process by reviewing and revising its loan policies on an ongoing basis. Currently, the credit union offers the following loans:

* 1% above last earning interest rate on Savings with minimum of 5% interest. ** Guarantor / Collateral required depending on Credit Score *** Above rates are subject to Credit Score

Name of Loan Amount of Loan Rate (APR)***

Term Security

Secured Loan Limited by Members' saving 5.00%* 5 Years Members' Saving

Unsecured Advantage loan Up to $20,000 9.99% 5 Years Upto 10% of the Loan Amount** Preferred Members' Loa n $20,001 to $35,000 9.99% 5 Years Upto 10% of the Loan Amount** Jumbo Loan $ 35,001 to $49,000 9.99% 6 Years Upto 10% of the Loan Amount** Auto Loan New Up to $100,000 4.79% 6 Years

5 Years

Vehicle

Auto Loan Used 6.79% Vehicle

Education Loan Up to $40,000 5.99% 4 Years

Up to $65,000

Schedule - 1: Classification of Loans

Opening Balance New Loans Loans Paid Ending Balance

Type of Loans # Amount # Amount # Amount # Amount

Unsecured 749 $15,143,99 0 397 $12,076,304 297 $9,128,36 9 849 $18,091,925

Secured 22 467,81 0 20 572,550 15 469,48 1 27 570,879

Business 30 2,991,08 0 0 0 4 894,84 3 26 2,096,238

Equipment 2 52,28 9 0 0 1 47,28 9 1 5,000

Automobiles 205 2,650,00 4 101 2,673,218 57 1,584,44 5 249 3,738,777

Education 52 703,45 8 12 57,491 19 176,22 3 45 584,726

Totals 1060 $22,008,63 1 530 $15,379,563 393 $12,300,65 0 1197 $25,087,544

Average Loans $20,763 $29,018 $31,299 $20,959

8

Master Card

During the year 2007, approximately, $2,370,240 was loaned out to the members through Master Card program compared to $2,763,938 in the year 2006. The details of the total accounts and the activities are as below:

Classic

522

339

Accounts on file

Active Accounts

Percent Active 65%

Allowance for Loan Losses A/c (ALLL)

Gold Platinum Total

111

71

64%

228

165

72%

861

575

67%

No. of Year

Charge-off 2007

$365,571

Amount

$729,984-$50,000

$679,984

$204,498$201,243

$0

$405,741

$274,243

$91,328

09120

21

No. of Year

Charge-off 2006

$729,984

Amount

$1,250,867$642,000

$1,874,867

$844,208$408,228

$4,297

$1,256,733

$618,134

$111,850

443301

78

No. of Year

Charge-off 2005

$1,250,867

Amount

$185,867$1,065,000

$1,250,867

$0

$0

$1,250,867

$0

00

00

$0

No. of Year

Charge-off 2004

$185,867

Amount

$204,631$73,440

$278,071

$92,204

$92,204

$185,867

$0

08

08

Description

Opening Balance Add new fund for ALLL Balance Aavilable

Less : Loan Charge Off Master Card Charge-Off Other Charge Off

Total amount Charge off

Balance After Charge Off

Add Recovery from Charge off Loan and Master Card

Balance end of the year

Schedule - 2: Members' Shares

Membership Count

Opening Members

New

Members Accounts

Closed

Ending Members

Membership 4,385 229

Members' Shares

Opening Balance

Add:

Deposits

Less: Withdrawals

Ending Balance

Savings/Shares $20,477,734 $2,099,826 I.R.A. Shares 4,287,039 896,608

Totals $24,764,773 $2,996,434

Average Balance of a Member’s Share = $5,705

72 4542

$1,741,816$105,280

$20,835,7445,078,367

$1,847,096 $25,914,111

Members' Savings

Members' savings continue to grow, at a rate comparable to previous years. On occasions, members' ability to save money was limited to maintain the Credit Union's Cash to Assets Ratio in compliance with our Asset/Liability Management policy. This also enables the credit union to declare higher dividends on savings. The IRA portfolio is growing steadily ever since. Saving money into IRA account will help members' in their retirement and tax planning. Members can

th open an IRA account before 15 April and the contribution can still be applied to year 2007 for tax purposes.

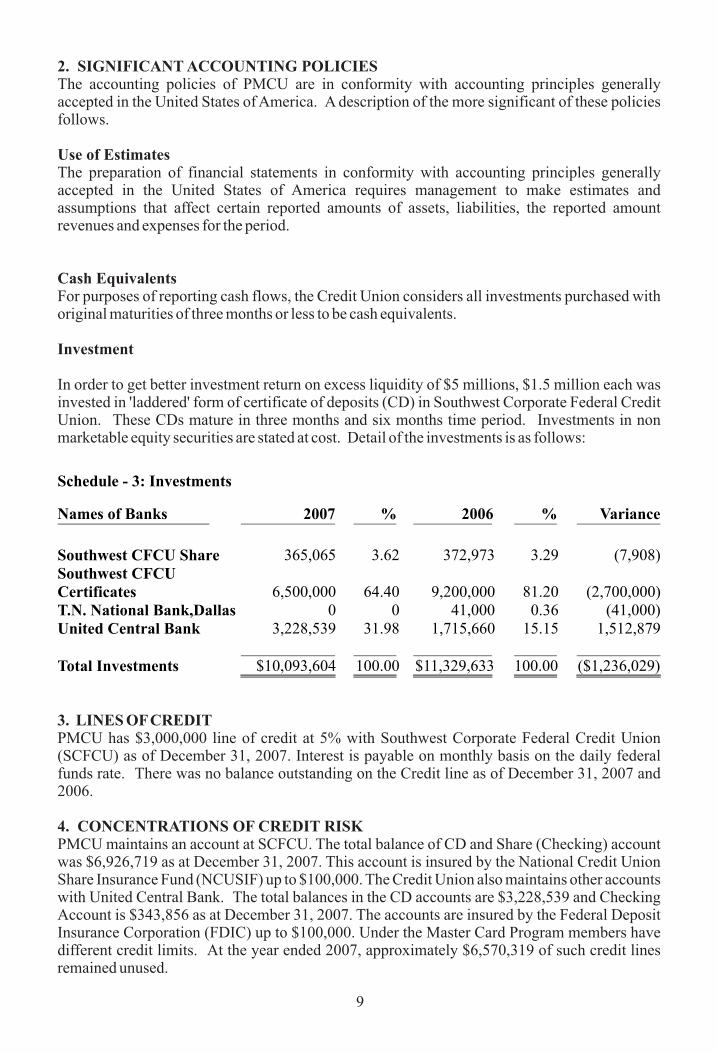

2. SIGNIFICANT ACCOUNTING POLICIESThe accounting policies of PMCU are in conformity with accounting principles generally accepted in the United States of America. A description of the more significant of these policies follows.

Use of EstimatesThe preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect certain reported amounts of assets, liabilities, the reported amount revenues and expenses for the period.

Cash EquivalentsFor purposes of reporting cash flows, the Credit Union considers all investments purchased with original maturities of three months or less to be cash equivalents.

Investment

In order to get better investment return on excess liquidity of $5 millions, $1.5 million each was invested in 'laddered' form of certificate of deposits (CD) in Southwest Corporate Federal Credit Union. These CDs mature in three months and six months time period. Investments in non marketable equity securities are stated at cost. Detail of the investments is as follows:

3. LINES OF CREDITPMCU has $3,000,000 line of credit at 5% with Southwest Corporate Federal Credit Union (SCFCU) as of December 31, 2007. Interest is payable on monthly basis on the daily federal funds rate. There was no balance outstanding on the Credit line as of December 31, 2007 and 2006.

4. CONCENTRATIONS OF CREDIT RISKPMCU maintains an account at SCFCU. The total balance of CD and Share (Checking) account was $6,926,719 as at December 31, 2007. This account is insured by the National Credit Union Share Insurance Fund (NCUSIF) up to $100,000. The Credit Union also maintains other accounts with United Central Bank. The total balances in the CD accounts are $3,228,539 and Checking Account is $343,856 as at December 31, 2007. The accounts are insured by the Federal Deposit Insurance Corporation (FDIC) up to $100,000. Under the Master Card Program members have different credit limits. At the year ended 2007, approximately $6,570,319 of such credit lines remained unused.

9

Schedule - 3: Investments Names of Banks 2007

Southwest CFCU Share 365,065 3.62 372,973 3.29 (7,908)Southwest CFCU Certificates 6,500,000 64.40 9,200,000 81.20 (2,700,000)T.N. National Bank,Dallas 0 0 41,000 0.36 (41,000)United Central Bank 3,228,539 31.98 1,715,660 15.15 1,512,879 Total Investments $10,093,604 100.00 $11,329,633 100.00 ($1,236,029)

% 2006 % Variance

Loans to membersLoans to members are stated at the current principal amount outstanding. Interest on loans is accrued monthly basis on the amount of principal outstanding. Premises and EquipmentThe Credit Union occupies the Houston premises of approximately 3,000 square feet for $2,325 and Austin premises of approximately 1017 square feet for $1,035 monthly rent. The equipment is carried at cost less accumulated depreciation. Provisions for depreciation are computed using the straight-line method. Average useful lives used for depreciation with respect to major classifications of property are as follows:

Furniture and equipment 3 to 10 yearsComputer and Software 2 to 5 years

Expenses for maintenance and repairs are charged against operations. Assets and related amounts are removed from the accounts upon retirement or other disposition and any resulting gains or losses are recorded in the statement of activities.

Income Taxes

PMCU is generally exempt from federal income taxes under Internal Revenue Code section 501(c) 6).

Checking & Automatic Clearing House (ACH)

PMCU has ACH services that enable the members to directly debit or credit their account.

Newsletter

In order to establish and maintain a continuous channel of communication with members, a quarterly newsletter has been started again in the year 2007. The goal of this newsletter is to communicate current events, ongoing activities, future programs, and other important financial information to the members. We also hope to use this newsletter as a tool to obtain feedback and input from the members to improve the quality and easy means of communications.

Other Programs to be Introduced Soon· Member's Business Loan

· Home Banking

· Audio Response

10

11

Graphs

$24,1

39,1

74

$27,7

53,0

22

$28,3

23,0

95

$24,7

72,5

69

$27,4

57,7

84

$22,0

00,0

00

$23,0

00,0

00

$24,0

00,0

00

$25,0

00,0

00

$26,0

00,0

00

$27,0

00,0

00

$28,0

00,0

00

$29,0

00,0

00

2003

2004

2005

2006

2007

LO

AN

S

$25,0

80,0

93

$27,3

89,8

37

$28,4

30,1

45

$27,1

26,7

78

$27,8

88,7

49

$23,0

00,0

00

$24,0

00,0

00

$25,0

00,0

00

$26,0

00,0

00

$27,0

00,0

00

$28,0

00,0

00

$29,0

00,0

00

2003

2004

2005

2006

2007

SA

VIN

GS

$7,4

82,6

67

$32,5

65,9

21 $8,5

72,4

77

$35,9

66,1

22 $

8,6

94,2

78

$37,2

96,4

60 $

9,3

75,7

66

$36,5

06,4

69 $10,3

42,6

90

$38,2

47,7

42

$5,0

00,0

00

$10,0

00,0

00

$15,0

00,0

00

$20,0

00,0

00

$25,0

00,0

00

$30,0

00,0

00

$35,0

00,0

00

$40,0

00,0

00

2003

2004

2005

2006

2007

NE

T W

OR

TH

AS

SE

TS

3,7

72

4,0

84

4,2

91

4,3

85

4,5

42

0

500

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

3,5

00

4,0

00

4,5

00

5,0

00

2003

2004

2005

2006

2007

ME

MB

ER

SH

IP

0

Board of Directors 2007

Shaukat AliPresident/CEO

Zulfiqar MohammedVice Chairman

Javaid R DhukaChairman

Asif MarediaTreasurer

Noordin KhojaMember, Supervisory Committee

Rahim MaknojiaSecretary

Sohrab K AliMember, Credit Committee

Zikar MarediaChairman, Supervisory Committee

Ahmedali MominChairman, Credit Committee

Hasan MarediaMember, Marketing Committee

Irfan K AliMember, Credit Committee

Gulbano MohammedLoan Officer

Salma MaknojiaAdministrative Officer

Parveen AliLoan Officer

Ali Ahmed MominAdministrative Assistant

Naeem Charolia Administrative Assistant

Nooruddin MominAccountant

Ambreen MaknojiaCollection Officer

Faiza AliHead Teller/Supervisor

HOUSTON OFFICE

11011 Wilcrest Drive, Suite KHouston, TX 77099

P. O. Box 721496Houston, TX 77272-1496

Telephone (281) 568-6000Fax (281) 568-8054

Toll Free 1-877 OUR PMCU (687-7628)Audio Response (281) 568-8558Email Adress [email protected]

www.pmcuonline.org

OFFICE HOURSMonday - Friday 9:00 am - 5:00 pm

Saturday, Sunday Closed

AUSTIN OFFICE

5555 North Lamar Blvd., Suite C 107Austin, TX 78751

Toll Free 1-877 OUR PMCU (687-7628)Audio Response (281) 568-8558Email Adress [email protected]

OFFICE HOURSMonday - Friday 9:00 am - 3:00 pm

1 hour after Jamat KhanaSaturday, Sunday Closed

Office Staff 2006

2007 Annual Report

[jumbo loan] [auto loan] [secure loan] [education loan] [equipment loan]11011 Wilcrest drive, suite k, houston, texas 77099 p.o. box 721496, houston, texas 77272-1496

MEMBERS HELPING MEMBERS

CRED

IT U

NION

MUSLIM