2004 mba convention international opportunities panel

DESCRIPTION

2004 MBA Convention International Opportunities Panel. Sponsored by The PMI Group, Inc. 2004 MBA Convention International Opportunities Panel Tony Porter EVP, Managing Director The PMI Group, Inc. Sponsored by The PMI Group, Inc. 2002 Top 10 Mortgage Markets. - PowerPoint PPT PresentationTRANSCRIPT

MBA Logo

2004 MBA ConventionInternational

Opportunities Panel

Sponsored by The PMI Group, Inc.

MBA Logo

2004 MBA ConventionInternational Opportunities Panel

Tony PorterEVP, Managing Director

The PMI Group, Inc.

Sponsored by The PMI Group, Inc.

MBA Logo

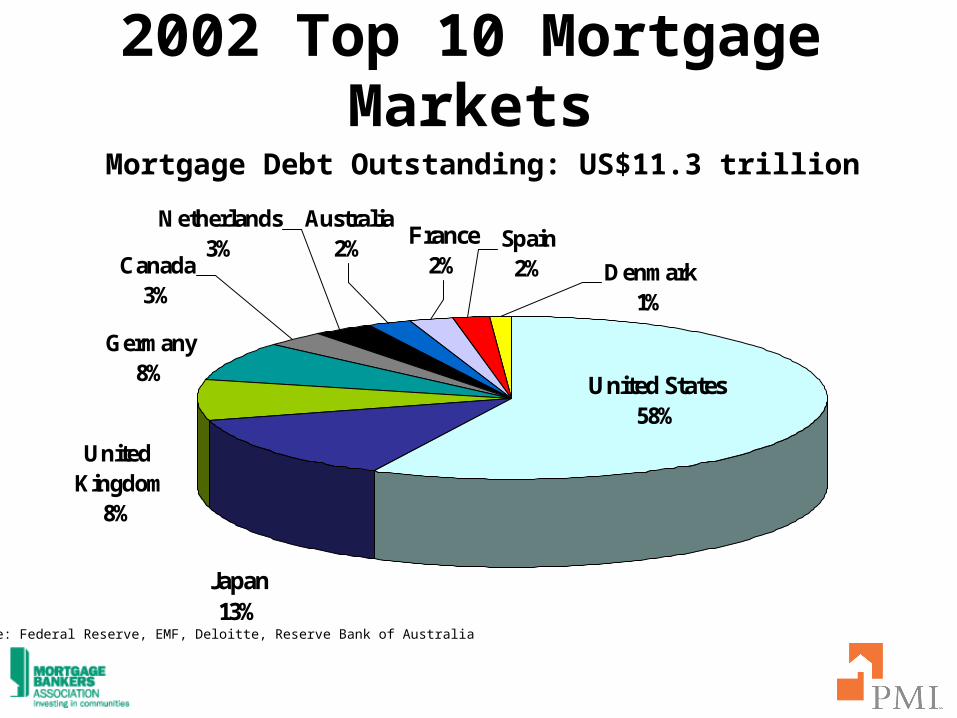

2002 Top 10 Mortgage Markets

Canada3%

Germany8%

United Kingdom

8%

Australia2%

United States58%

Japan13%

France2%

Spain2%

Netherlands3%

Denmark1%

Mortgage Debt Outstanding: US$11.3 trillion

Source: Federal Reserve, EMF, Deloitte, Reserve Bank of Australia

MBA Logo

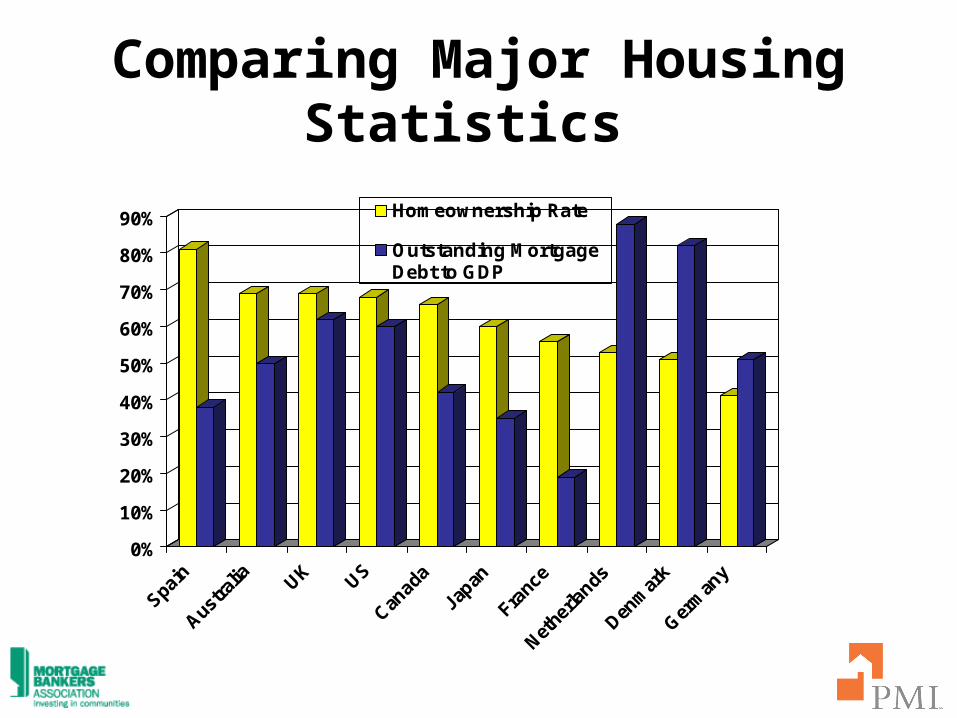

Homeownership Rates

Source: EMF, US Census Bureau, IUHF, CMHC, and internal PMI sources

SpainAustralia

United StatesCanada

JapanFrance

NetherlandsDenmark

Germany

0% 20% 40% 60% 80% 100%

United Kingdom

81%69%69%68%

66%60%

56%53%

51%41%

MBA Logo

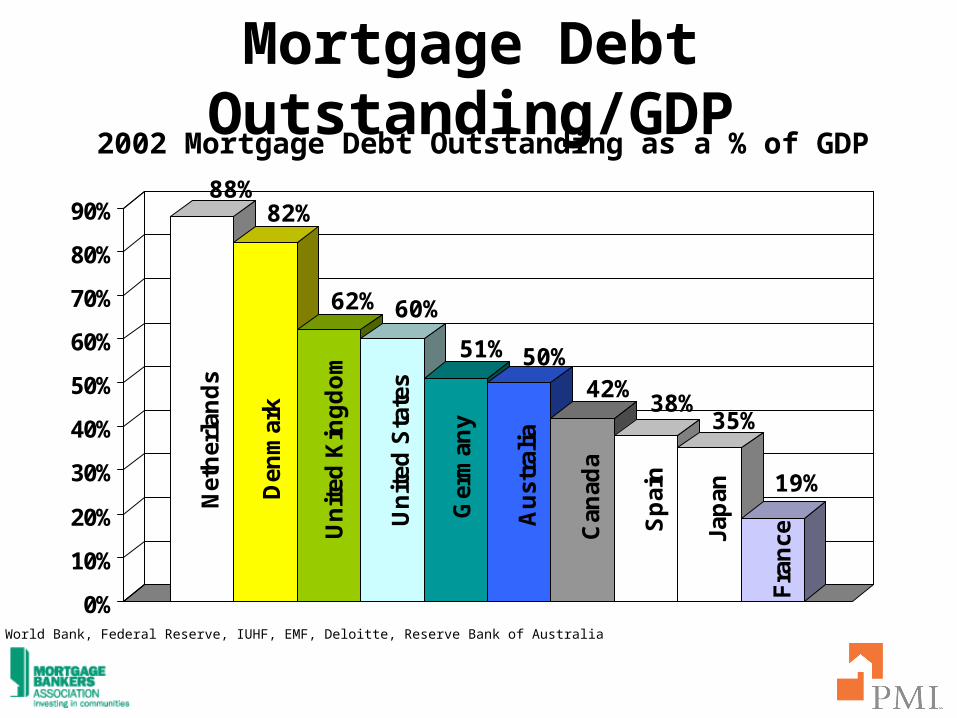

Mortgage Debt Outstanding/GDP

Net

her

lan

ds

Den

mar

k

Un

ited

Kin

gd

om

Un

ited

Sta

tes

Ger

man

y

Au

stra

lia

Can

ada

Sp

ain

Jap

an

Fra

nce

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2002 Mortgage Debt Outstanding as a % of GDP

88%82%

62% 60%

51% 50%42%

38%35%

19%

Source: World Bank, Federal Reserve, IUHF, EMF, Deloitte, Reserve Bank of Australia

MBA Logo

Comparing Major Housing Statistics

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Spain

Austra

lia UK US

Canad

a

Japan

Franc

e

Nethe

rlands

Denm

ark

Ger

man

y

Homeownership Rate

Outstanding MortgageDebt to GDP

MBA Logo

Common Questions

Why should we expand internationally?

Should we look to big markets, where there is more room to find a niche?

Should we look at emerging markets, where we can enter early and define market practices to establish dominance?

Should we focus on transition markets where the market development work is done and business is poised for growth?

Or is the best strategy simply to focus on our home market and compete where we know best?

MBA Logo

What Makes Markets Attractive?

UNATTRACTIVE ATTRACTIVE

Market Size

Growth Rate

Profit Margins

Competition

Legal System

Borrower Quality

Information

Political Stability

Economic Stability

Can my core competencies tilt

the balance?

MBA Logo

2004 MBA ConventionInternational Opportunities Panel

International Expansion: The Case of Countrywide

Michael LeaCardiff Economic Consulting

MBA Logo

Overview of Presentation

Countrywide Financial Corp. – The Leading US Mortgage Lender

Competitive Strengths and Exportable Skills

International Expansion – Rationale, Market Selection and Business Model

UK Market Overview

Making the Business Model Work: Challenges and Solutions

MBA Logo

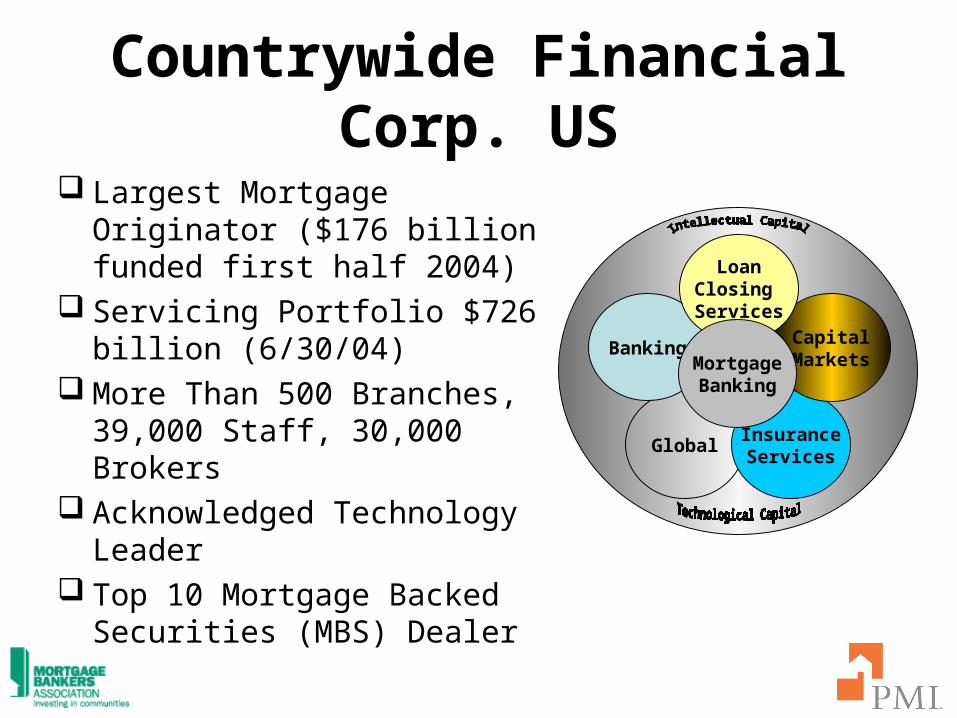

Countrywide Financial Corp. US

Largest Mortgage Originator ($176 billion funded first half 2004)

Servicing Portfolio $726 billion (6/30/04)

More Than 500 Branches, 39,000 Staff, 30,000 Brokers

Acknowledged Technology Leader

Top 10 Mortgage Backed Securities (MBS) Dealer

GlobalInsuranceServices

CapitalMarkets

Banking

LoanClosing Services

MortgageBanking

MBA Logo

CFC Core StrategyTo enable its employees to deliver best-of-class and value-added products and services to its customers through superior technology and processes.

MBA Logo

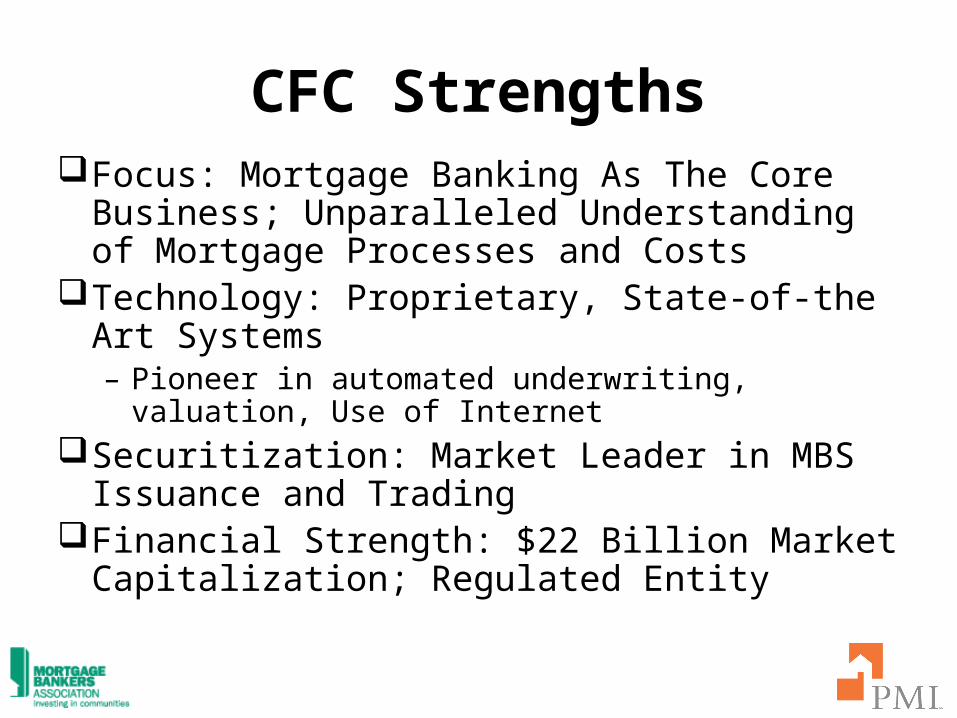

CFC StrengthsFocus: Mortgage Banking As The Core

Business; Unparalleled Understanding of Mortgage Processes and Costs

Technology: Proprietary, State-of-the Art Systems– Pioneer in automated underwriting, valuation, Use of

InternetSecuritization: Market Leader in MBS Issuance

and TradingFinancial Strength: $22 Billion Market

Capitalization; Regulated Entity

MBA Logo

Learning From US Used In Global ArenaFirst Point Of Entry Has Been The UK

– Key attributes: size, language, open competitive market, need for cost reduction and new technology

Three Primary UK Businesses:– Global Home Loans: Market Leading Third Party

Administration– UK Valuation: Market Creator and Leader in

Automated Property Valuation– CFC Technology Solutions: Providers of State of the

Art, End-To-End Mortgage Technology

MBA Logo

GHL in 2000

• over 15,000 applications per

month

• $54 billion servicing portfolio

• over 760,000 loans

GHL in 2003

• over 26,000 applications per month

• $110 billion servicing portfolio

• Nearly 1.2 million loans

• largest end-to-end third party processor in the UK

May 1999

GHL established in venture with

Woolwich

1999

September 2000

Barclays acquired Woolwich

2000

April 2001

GHL facilitated launch of new

Barclays products

2001

November 2002

Barclays transition

2002

Global Home Loans

MBA Logo

Global Technology

CFC Technology Solutions/GHL

Have Developed a Comprehensive

Suite of Mortgage Processing

Systems For UK Market

Systems Based On Leading Edge

Technology Investments Made By

Countrywide In The US

Systems Cover Complete Mortgage

Chain

Designed To ‘Plug And Play’ With

Legacy Systems

Systems Use Proven Technologies

Client Systems

Interfaces

GAP

Origination Servicing

GQS GOS GSS

Workflow / Image

Sales

FSA Mortgage Disclosure Compliance

Payment Processing

Parameters & Rules (Global Tables)

Correspondence on Demand

Customer Contact

Customer Introducer Branch Client Phone Fax Mail Internet Intranet IDTV SMS

Mortgage Track

Multiple "Customers", Multiple Channels

Data warehouse / MI

MBA Logo

UK Market Overview

MBA Logo

The UK Mortgage Market Is the World’s Third

Largest2002 Mortgage Debt Outstanding

6450

1500

890 880

350 325 260 245 230 120

0

1000

2000

3000

4000

5000

6000

7000

US Japan UnitedKingdom

Germany Canada Netherlands Australia France Spain Denmark

Source: Federal Reserve, EMF, Deloitte, Reserve Bank of Australia

$ b

illi

on

MBA Logo

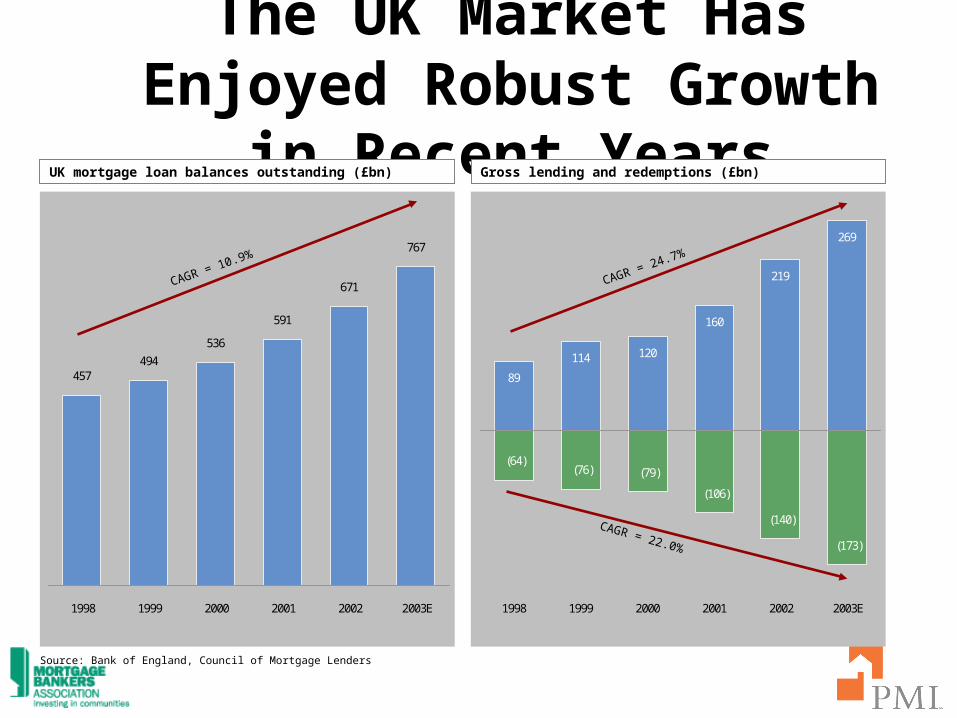

The UK Market Has Enjoyed Robust Growth

in Recent Years

89

114 120

160

219

269

(64)(76) (79)

(106)

(140)

(173)

1998 1999 2000 2001 2002 2003E

457494

536

591

671

767

1998 1999 2000 2001 2002 2003E

Source: Bank of England, Council of Mortgage Lenders

UK mortgage loan balances outstanding (£bn)UK mortgage loan balances outstanding (£bn) Gross lending and redemptions (£bn)Gross lending and redemptions (£bn)

CAGR = 10.9%

CAGR = 24.7%

CAGR = 22.0%

MBA Logo

The UK Market Is Concentrated

2002: Source CML

Total mortgage balances outstanding, end year Gross mortgage lending, in year

Name of Group £ billion

Est.market

share £ billion

Est.market

share

1 (1) HBOS 150.0 22.4% 1 (1) HBOS 56.8 26.0%2 (2) Abbey National 80.1 11.9% 2 (2) Abbey National 22.8 10.4%3 (3) Lloyds TSB 62.5 9.3% 3 (3) Barclays 21.3 9.8%4 (4) Barclays 57.7 8.6% 4 (4) Lloyds TSB 19.0 8.7%5 (5) Nationwide BS 57.2 8.5% 5 (5) Nationwide BS 17.4 8.0%6 (6) The Royal Bank of Scotland 42.1 6.3% 6 (6) The Royal Bank of Scotland3 13.5 6.2%7 (7) Northern Rock 30.0 4.5% 7 (7) Northern Rock 10.5 4.8%8 (8) Alliance & Leicester 23.6 3.5% 8 (9) HSBC Bank 9.4 4.3%9 (9) HSBC Bank 20.3 3.0% 9 (8) Alliance & Leicester 6.4 2.9%10 (10) Bradford & Bingley 16.8 2.5% 10 (11) Britannia BS3 4.3 2.0%

Rank Rank

MBA Logo

UK Mortgage Market Drivers

UK Tenure by Type

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Source: ODPM

% o

f Dw

ellin

gs

Owner-Occupied % of Private Rented % of Housing Association % of Public Rented % of

House Price Trends: UK and Select Regions

-

5.0

10.0

15.0

20.0

25.0

1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: OPDM

% ch

ange

from

pre

vious

year

London South East South West Scotland UK

MBA Logo

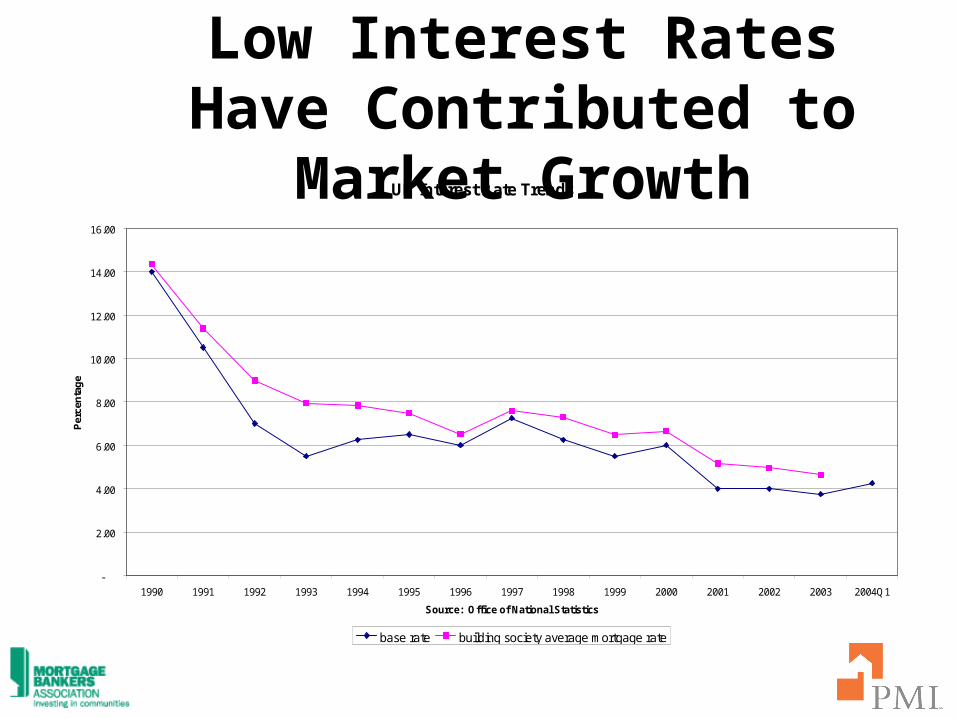

Low Interest Rates Have Contributed to

Market GrowthUK Interest Rate Trends

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004Q1

Source: Office of National Statistics

Per

cen

tag

e

base rate building society average mortgage rate

MBA Logo

Securitization Is Growing

UK Residential Mortgage Securitization

-

10,000

20,000

30,000

40,000

50,000

60,000

1997 1998 1999 2000 2001 2002 2003

Source: Merrill Lynch

Fu

nd

ed T

ran

sact

ion

s (E

uro

mil

lio

n)

0

5

10

15

20

25

30

35

# o

f tr

ansa

ctio

ns

Residential Securitization # of Transactions

MBA Logo

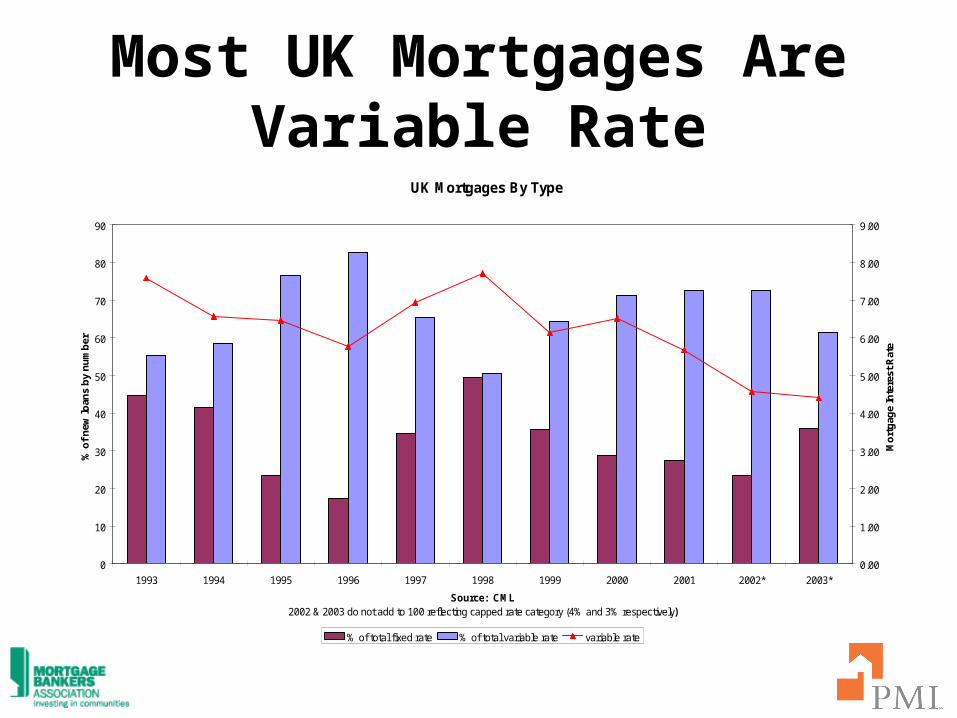

Most UK Mortgages Are Variable Rate

UK Mortgages By Type

0

10

20

30

40

50

60

70

80

90

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002* 2003*

Source: CML2002 & 2003 do not add to 100 reflecting capped rate category (4% and 3% respectively)

% o

f n

ew lo

ans

by

nu

mb

er

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Mo

rtg

age

Inte

rest

Rat

e

% of total fixed rate % of total variable rate variable rate

MBA Logo

The Outsourcing Challenge

Over 30% Of the UK Market Uses Outsourcing– Major lenders have made their decisions

Regulation Has Slowed the Adoption of Outsourcing Lenders Are Seeking a Large Reduction In Cost Which Is

Difficult to Achieve in the UK– Off-shore processing is a way to do this

Opportunities Exist With Component Processing and Smaller Lenders– New products, purchased portfolios– Special servicing, master servicing

European Outsourcing Has Formidable Challenges Labor is a fixed factor of production

MBA Logo

2004 MBA ConventionInternational Opportunities Panel

Tony GillExecutive Director

Macquarie Bank Limited

Sponsored by The PMI Group, Inc.

MBA Logo

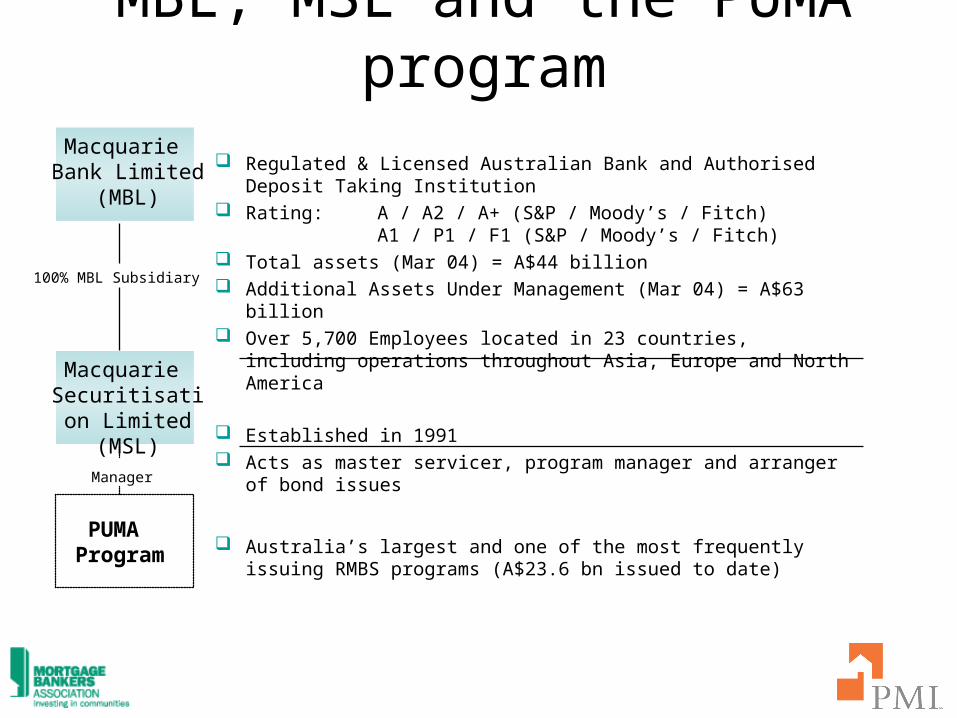

MBL, MSL and the PUMA program

Regulated & Licensed Australian Bank and Authorised Deposit Taking Institution

Rating: A / A2 / A+ (S&P / Moody’s / Fitch) A1 / P1 / F1 (S&P / Moody’s / Fitch)

Total assets (Mar 04) = A$44 billion Additional Assets Under Management (Mar 04) = A$63 billion Over 5,700 Employees located in 23 countries, including

operations throughout Asia, Europe and North America

Established in 1991 Acts as master servicer, program manager and arranger of

bond issues

Australia’s largest and one of the most frequently issuing RMBS programs (A$23.6 bn issued to date)

Macquarie Bank Limited

(MBL)

Macquarie Securitisation Limited (MSL)

PUMA Program

100% MBL Subsidiary

Manager

MBA Logo

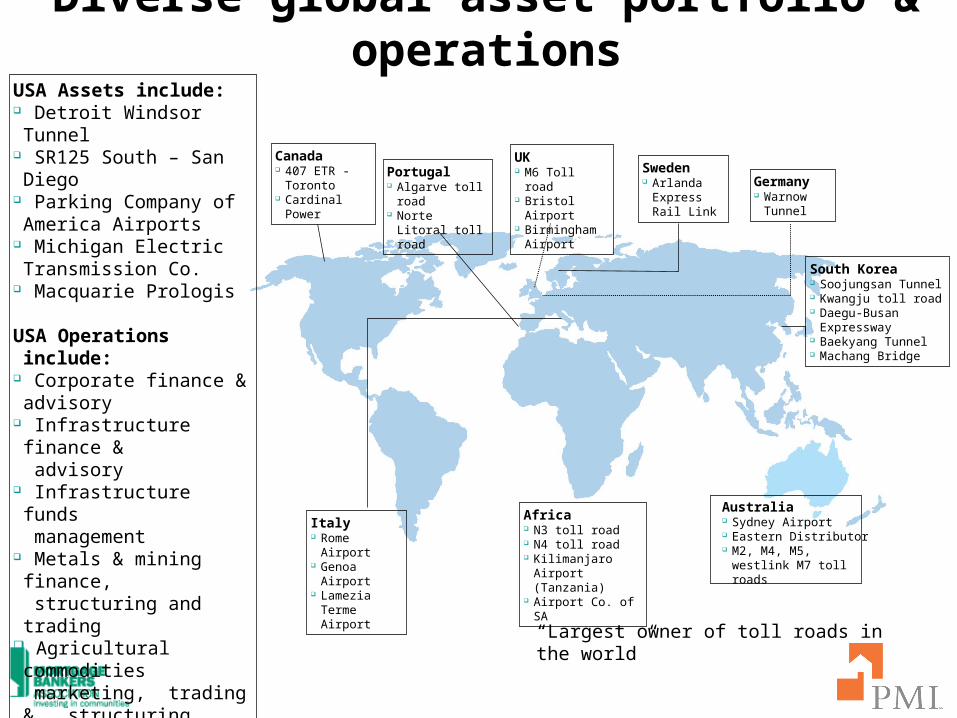

Canada 407 ETR -

Toronto Cardinal Power

USA Assets include: Detroit Windsor Tunnel SR125 South – San Diego Parking Company of America Airports

Michigan Electric Transmission Co.

Macquarie Prologis

USA Operations include: Corporate finance & advisory

Infrastructure finance & advisory

Infrastructure funds management

Metals & mining finance, structuring and trading

Agricultural commodities marketing, trading & structuring

Golf course / residential development

Mortgage origination

Africa N3 toll road N4 toll road Kilimanjaro Airport

(Tanzania) Airport Co. of SA

Italy Rome Airport Genoa Airport Lamezia

Terme Airport

South Korea Soojungsan Tunnel Kwangju toll road Daegu-Busan

Expressway Baekyang Tunnel Machang Bridge

Australia Sydney Airport Eastern Distributor M2, M4, M5,

westlink M7 toll roads

Germany Warnow

Tunnel

Portugal Algarve toll road Norte Litoral toll

road

UK M6 Toll road Bristol Airport Birmingham

Airport

Diverse global asset portfolio & operations

Sweden Arlanda

Express Rail Link

“Largest owner of toll roads in the world”

MBA Logo

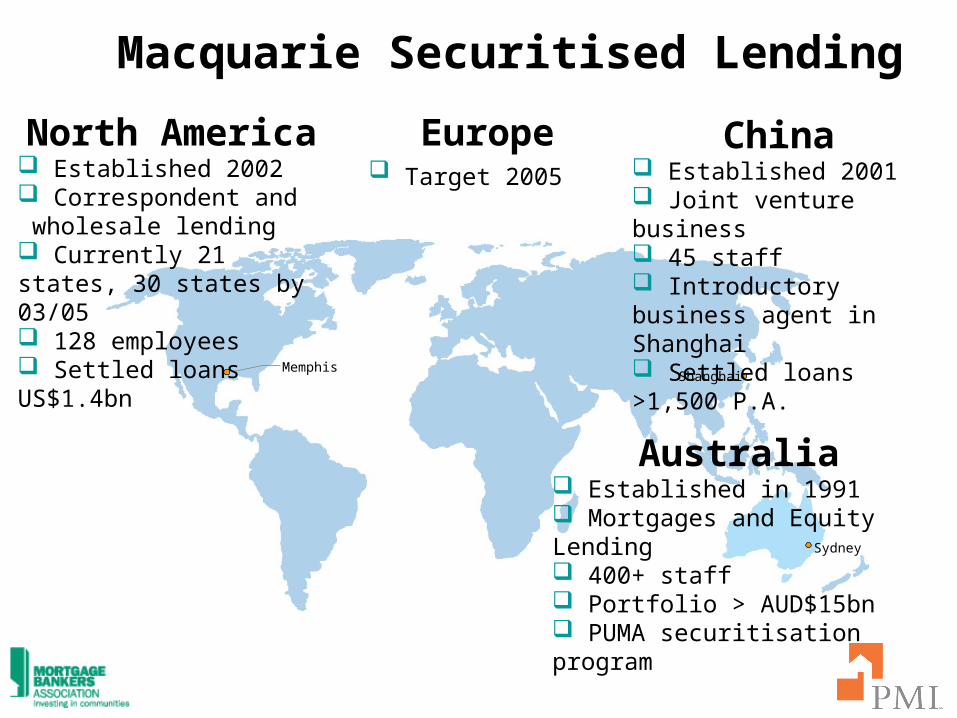

Macquarie Securitised Lending

Shanghai

Sydney

Memphis

North America Established 2002 Correspondent and wholesale lending Currently 21 states, 30 states by 03/05 128 employees Settled loans US$1.4bn

China Established 2001 Joint venture business 45 staff Introductory business agent in Shanghai Settled loans >1,500 P.A.

Australia Established in 1991 Mortgages and Equity Lending 400+ staff Portfolio > AUD$15bn PUMA securitisation program

Europe Target 2005

MBA Logo

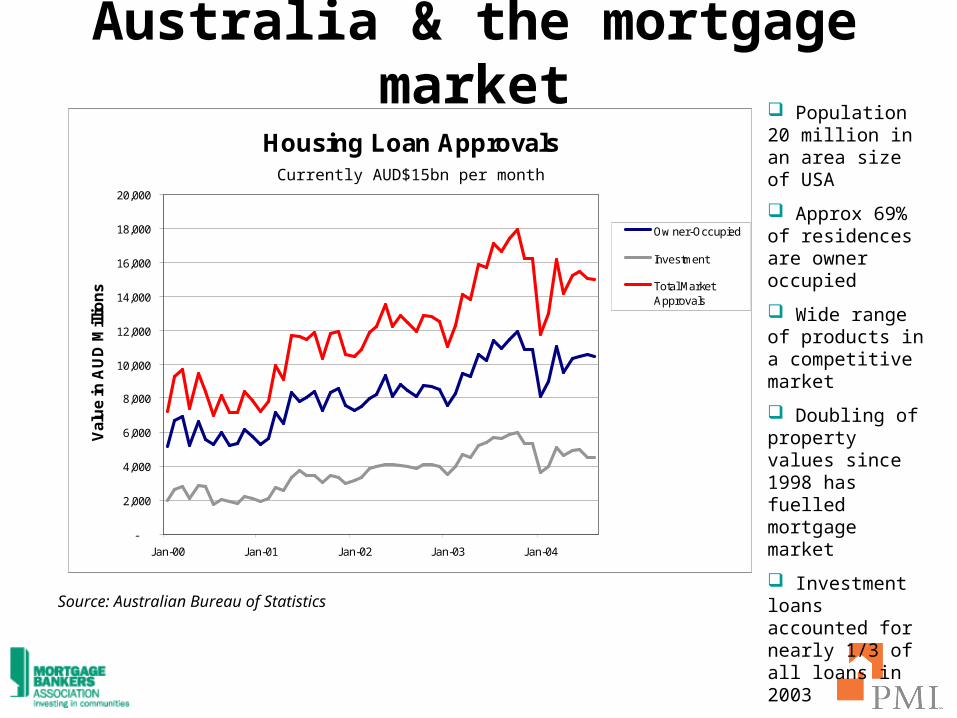

Australia & the mortgage market Population 20 million in an area size of USA

Approx 69% of residences are owner occupied

Wide range of products in a competitive market

Doubling of property values since 1998 has fuelled mortgage market

Investment loans accounted for nearly 1/3 of all loans in 2003

Full recourse to the borrower in event of default

Source: Australian Bureau of Statistics

Housing Loan Approvals

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04

Val

ue

in A

UD

Mill

ions

Ow ner-Occupied

Investment

Total MarketApprovals

Currently AUD$15bn per month

MBA Logo

Low interest rate environment Typical loan is floating rate

Rate is set at lender’s discretion – not linked to any specific index

Fixed rates:

are available for a set period usually 1,3 or 5 years

reverts to variable or re-fix

mark to market prepayment costs are charged to the borrower

Interest paid is tax deductible for investment loans only

MBA Logo

Market still dominated by Major banks

Permanent building societies Banks

78%3%

Wholesale lenders15%

Other lenders4%

Lending sourced by brokers has increased significantly to approx 30% of all new loans

Expected to increase to 50% within next 3 years

Asset retention due to churn is a key challenge

MBA Logo

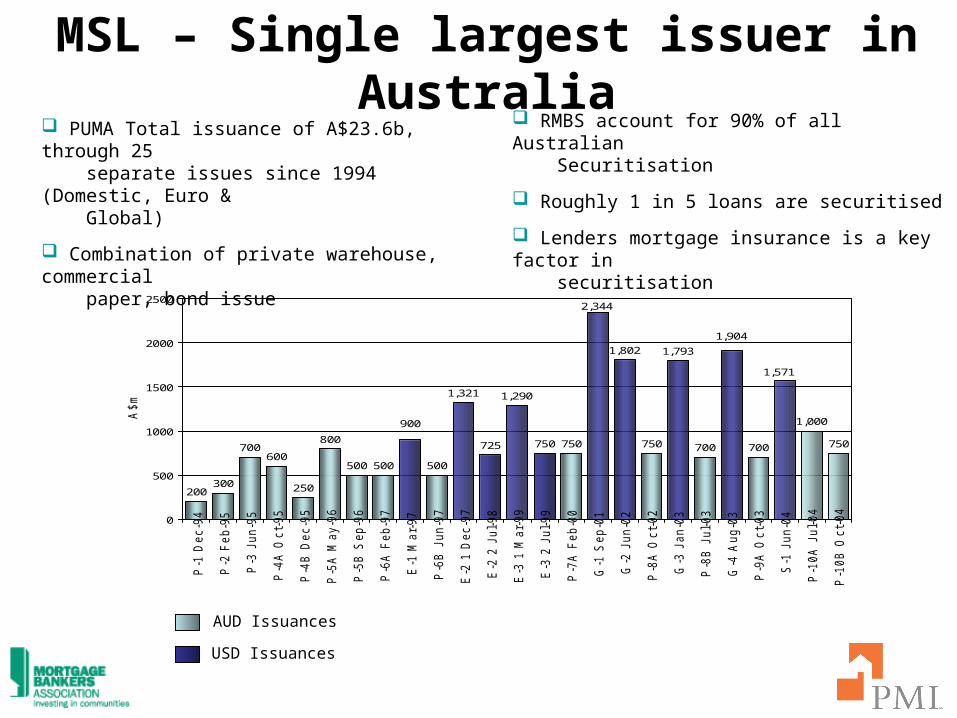

PUMA Total issuance of A$23.6b, through 25 separate issues since 1994 (Domestic, Euro & Global)

Combination of private warehouse, commercial paper, bond issue

MSL – Single largest issuer in Australia RMBS account for 90% of all Australian Securitisation

Roughly 1 in 5 loans are securitised

Lenders mortgage insurance is a key factor in securitisation

200300

700600

250

800

500 500 500

1,321

725

1,290

750 750

1,802

750

1,793

700 700

1,000

750

2,344

1,904

900

1,571

0

500

1000

1500

2000

2500

P-1

Dec-9

4

P-2

Feb-9

5

P-3

Jun-9

5

P-4

A O

ct-

95

P-4

B D

ec-9

5

P-5

A M

ay-9

6

P-5

B S

ep-9

6

P-6

A F

eb-9

7

E-1

Mar-

97

P-6

B J

un-9

7

E-2

1 D

ec-9

7

E-2

2 J

ul-98

E-3

1 M

ar-

99

E-3

2 J

ul-99

P-7

A F

eb-0

0

G-1

Sep-0

1

G-2

Jun-0

2

P-8

A O

ct-

02

G-3

Jan-0

3

P-8

B J

ul-03

G-4

Aug-0

3

P-9

A O

ct-

03

S-1

Jun-0

4

P-1

0A

Jul-04

P-1

0B

Oct-

04

A$m

AUD Issuances

USD Issuances

MBA Logo

MSL – Key success factors

-

100

200

300

400

500

600

Jan.

00

Mar

.00

May

.00

Jul.0

0

Sep.0

0

Nov.0

0

Jan.

01

Mar

.01

May

.01

Jul.0

1

Sep.0

1

Nov.0

1

Jan.

02

Mar

.02

May

.02

Jul.0

2

Sep.0

2

Nov.0

2

Jan.

03

Mar

.03

May

.03

Jul.0

3

Macquarie

Market

Growth in monthly approvals as percentage of January 00

%

Core competencies

Product Innovation

Distribution expertise

End-to-end service provider

Flexible business philosophy

Servicing of brokers & borrowers. Rated the No. 2 service provider by the Australian mortgage broking industry

MBA Logo

International expansion criteria

Funding/Securitisation Supportive regulatory framework

Risk Management Good title

Acceptable credit data

Housing & Mortgage Market Size

Mortgages vs. GDP

Ease of entry & exit

Market Structure Niche opportunities in established market

Changing regulatory environment

Lenders mortgage insuranceProduct & Distribution Product types/range

Distribution networks

Opportunity to innovate

MBA Logo

MSL expansion into US market

Market Structure

Risk Management

Niche opportunities in established market

Changing regulatory environment

Lenders mortgage insurance Housing & Mortgage Market Size

Mortgages vs. GDP

Ease of entry & exit

Good title

Acceptable credit data

Funding/Securitisation Supportive regulatory framework

Product & Distribution Product types/range

Distribution networks

Opportunity to innovate

Risk Management

MBA Logo

China & the mortgage market

Heavily regulated – products, interest rates, lenders, repayment terms

Mortgage market established 1999

Outstanding mortgage balance at 2003 RMB 1.2 trillion (USD 145bn)

No concept of non bank lending

Risk management framework still developing

21 independent title registration offices in Shanghai alone

No formal credit data

Securitisation non-existent

0

5

10

15

20

25

Australia Shanghai Beijing

Pop

ulat

ion

(mill

ion)

Key data

Pop. China = 1.2 billion

Pop. USA = 294 million

Several “tier 2” cities with population of 8 to 10 million

Shift from government to private home ownership

MBA Logo

Two tier market

Chinese Banks Foreign Lenders

Type of borrower Local & Overseas Overseas passport holders only

Product Standard for all borrowers20 yr fixed termMinimal features

Standard for all borrowers 20-30 yr fixed term Minimal features

Currency RMB only HKD or USD only

Interest rates Fixed 5.04% all lenders Variable based on Customer quality Size of deposit Currently 2.75 – 4% for USD loans

MBA Logo

Property values are fuelling market growth

Recent share market losses mean investors favouring property

Capital growth over the last 3 years ranged from 20-50% P.A.

Not uncommon for investors to purchase property purely for capital growth. Properties remain unoccupied

Greater than 10% year to date growth despite government policy to introduce more controlled growth

Government imposed restrictions to limit growth to 15-18% in Shanghai market

MBA Logo

MSL in China

Niche opportunities in established market

Changing regulatory environment – WTO 2007

Lenders mortgage insurance

Product types/range

Distribution networks

Opportunity to innovate

Supportive regulatory framework Good title

Acceptable credit data

Size

Mortgages vs. GDP

Ease of entry & exit

?X

??

X

?

Market Structure

Product & Distribution

Housing & Mortgage Market

Risk ManagementFunding/Securitisation

MBA Logo

US Controlled growth through geographical expansion and product innovation

Where next?

Europe Commence operations by 2005

Further expansion

“Horizon scanning” for opportunities that match exportable core competencies

Australia

Client service, client service, client service

Continued focus on quality brokers and originators

Product diversification

China

Continually assess changing market for opportunities in preparation for entry into WTO in 2007

MBA Logo

GMAC-RFCBusiness Overview

Prepared for:International Panel - MBA Convention

Chris Nordeen – President, International Business Group

MBA Logo

A Member of the General Motors Family

MBA Logo

What We Do

A Global Provider of Capital and Liquidity Solutions

Residential Mortgage Finance

We originate, purchase, service and securitize a full range ofresidential mortgage loan products to make affordable capitalavailable in support of homeownership

Business-to-Business LendingWe provide a wide range of liquidity solutions including

constructionloans, subordinated debt-type financing, receivables financing andterm loans to residential developers/builders, timeshare resortdevelopers and healthcare enterprises

We are committed to expanding the availability of capital in key real estate finance markets worldwide.

MBA Logo

A Values-Based Company

We have a strong, vibrant culture focused on people and markets.

MBA Logo

We move capital between businesses and investors in select markets worldwide.

Our Business Model

MBA Logo

Our Business Strategy

Our strategy is to diversify our business and grow organically.

MBA Logo

A Market Leader

We have a strong business-to-business brand presence in U.S. and international markets.

MBA Logo

Mexico Market

MBA Logo

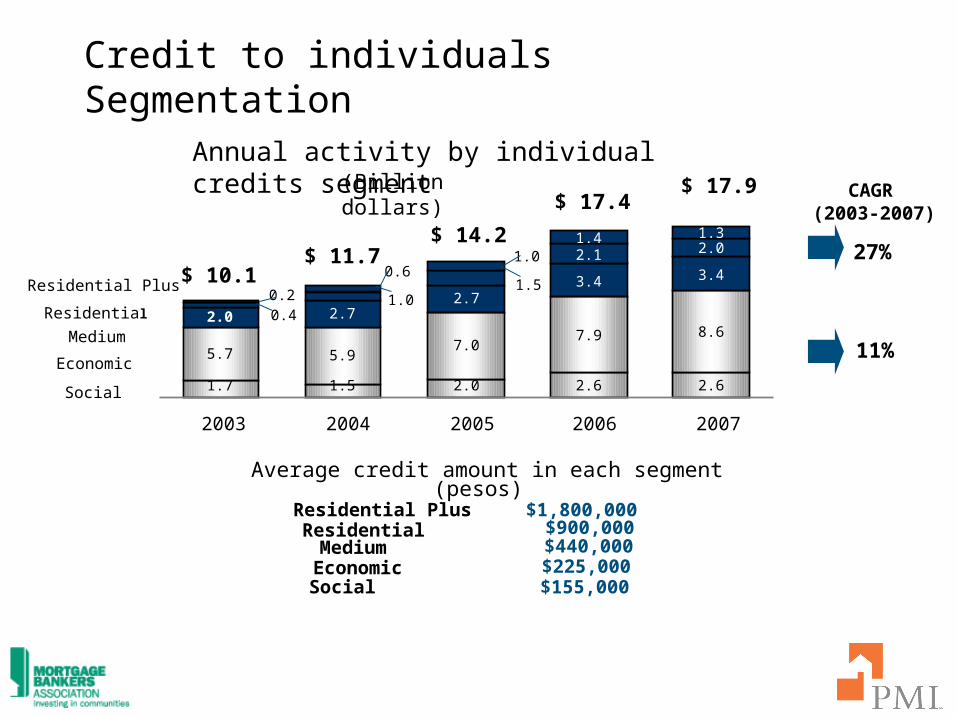

1.7 1.5 2.6 2.6

5.7 5.97.9 8.6

2.72.7

3.4 3.4

2.0

7.0

2.0

2.1

1.5

2.0

1.00.4

1.31.41.0

0.2

0.6$ 10.1$ 11.7

$ 17.4$ 17.9

2003 2004 2005 2006 2007

Medium

Residential Plus

Economic

Social

Residential

CAGR (2003-2007)

27%

Annual activity by individual credits segment (Billion dollars)

11%

Average credit amount in each segment(pesos)

Medium

Residential Plus

EconomicSocial

Residential

$155,000$225,000$440,000$900,000

$1,800,000

$ 14.2

Credit to individuals Segmentation

MBA Logo

2005-2007 Business Plan

Large developers in Mexico (December 2003) Large developers in Mexico

2%2%

2%

3%

4%

7%

4%

5%

2%

1%1%

Medium and SmallDevelopers

67.2%

GEOURBI

100%= 400,000 homes

ARA

SADASI

HOMEX

PULTE

BETA

SARE

RUBA

METTAHOGAR

DEMET

•Grupo GEO•URBI•Consorcio ARA•Grupo SADASI•HOMEX•PULTE•BETA•SARE•RUBA•Grupo METTA•Consorcio HOGAR•DEMET

32.8% of the market

131,558 homes sold

Developers in the Mexican housing market

MBA Logo

2002

BillIions of USD

2000 2003

Mortgage sofoles credit portfolio evolution

CAGR37.8%

2001

$2.9

Market Share of the Mortgage Sofoles in the Total Credit Portfolio

3%3%3%

5%

15%

31% 7%

19%

5%

2.4%

3%

1.1%1%

2%

Hipotecaria Nacional

Hipotecaria su Casita Hipotecaria Crédito

y Casa

Crédito Inmobiliario

Patrimonio

General Hipotecaria

Hipotecaria Comercial América

Ficansa Hipotecaria

Terras Hipotecaria

Hipotecaria México

GMAC Financiera

Hipotecaria Vanguardia

GMAC Hipotecaria

Rest

100%= US$ 7.6 billions

$4.3

$6.3

$7.6

The total credit portfolios of the Sofoles has shown important growth, reaching US $7.6 billion in 2003

Sofoles Credit Portfolio

MBA Logo

Market Trends

• The Mexican mortgage industry has experienced an important growth rate in the past 5 years, mainly through the Sofoles

• According to the governmental housing programs, the mortgage industry is expected to continue with high growth rates

• Sociedad Hipotecaria Federal (“SHF”) is changing from being a direct lender to a provider of credit enhancements to Sofoles

• To keep up with the growth it is important to develop alternative sources of funding for the industry

• Sofoles and other industry participants are looking at the capital markets as an alternative source of funds

MBA Logo

Investors/Capital Market

• Institutional Investors in Mexico:– Mutual Funds: USD $32.2 billion.– Afores (private pension funds): USD $37.5 billion.– Insurance Companies: USD $10.8 billion.– Annuities: USD $ 6.3 billion.

Total USD $86.8 billion.

• The average maturity for corporate debt issues has recently increased from 5.7 years in 2002 to 6.2 years in 2003

•Mutual Funds

•Insurance Co.

•Afores

•Private Funds

•Insurance Co.

•Afores

•Private Funds

•Annuities

•Insurance Co.

•Afores

•Annuities

1–5 years

6–9 years

Investment Preferences

10-20 years

MBA Logo

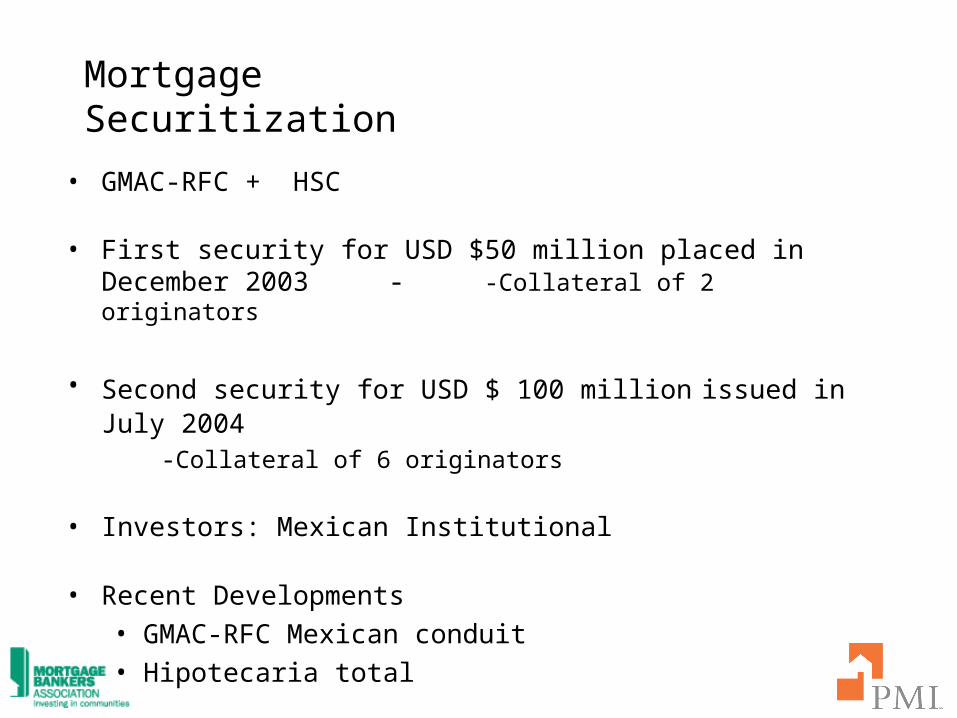

• GMAC-RFC + HSC

• First security for USD $50 million placed in December 2003 - -Collateral of 2 originators

• Second security for USD $ 100 million issued in July 2004

-Collateral of 6 originators

• Investors: Mexican Institutional

• Recent Developments• GMAC-RFC Mexican conduit• Hipotecaria total

Mortgage Securitization

MBA Logo

Conclusion

GMAC-RFC is becoming a global leader in real estate finance

• Leveraging skills from market to market

• Finding trusted local partners to interpret our business model

• Taking selected risks to help transform international markets

• Delivering sustainable growth to our shareholders

MBA Logo

2004 MBA ConventionInternational Opportunities Panel

Markus BolderHead of Credit Treasury

DG HYP AG

Sponsored by The PMI Group, Inc.

MBA Logo

Agenda Overview of DG HYP

Germany Primary Market Overview- Key Challenges and Opportunities- Borrowers, Mortgage Products and Product Development

Considerations- Distribution Channels - Servicing Requirements and Issues

Prospects for a Pan-European Mortgage Market

International Expansion Rationale, Market Selection Criteria, Outlook

MBA Logo

Overview of DG HYP

Size and Quality of the Cooperative Banking Sector:

- 1,400 primary banks covering 30 million German citizens

- Retail customers Small and mid-cap enterprises

- Broadly based distribution network Placement power Direct client share

Mission of DG HYP:Supplying German cooperative banks with:

- Private housing loans

- Commercial mortgage loans

- Public sector financing

- Services based around core products / portfolio management for real estate

The Cooperative Banking Context

Key figures 2003: Balance sheet:

69 bn EUR 1. Real estate lending:

25 bn EUR 2. Public sector lending:

37 bn EUR 3. Investements in MBS:

2 bn EUR

CIR: 58% ROE: 7%

Brokerageof

real estateloansand

portfolios

MBA Logo

DG HYP is one of the leading players in the German mortgage banking market:

No. 1 in the cooperative sector No. 2 in the segment of medium-sized mortgage banks Among the five biggest players in the German mortgage

lending market (incl. the two large mortgage banks HVB and Eurohypo)

average gross margins increasing substantially, in 2003 from 80 BP (2002) to 92 BP

slight decrease of loan to value for business in 2003 improvement of diversification of the real estate related loan

book … strengthens DG HYP‘s favourable market position with

… growth potential in net interest income and improvement of the risk/return profile of the loan portfolio

Strong growth rates in real estate lending and new MBS business over the last few years with …

Overview of DG HYPMarket Position / New Business

Development

MBA Logo

Total mortgage loan volume of medium-sized mortgage banks at the end of the financial year 2002 (in Euro bn)

Source: VDH (Association of German Mortgage Banks), companies‘ Annual Reports * Member of the cooperative sector

New Business in Real Estate Lending and MBS Investments (in Euro m)

Overview of DG HYPMarket Position / New Business

Development

0 5 10 15 20 25 30 35 40

WL-Bank*

Deutsche Hypo

Westhyp

Württ. Hypo

MHB*

Berlin Hyp

AHBR

Aareal Bank

DG HYP*

Hypo Real Estate

2,703

3,377

3,946

4,642

0

1.000

2.000

3.000

4.000

5.000

2000 2001 2002 2003

Retail Clients Commercial Clients MBS investments

MBA Logo

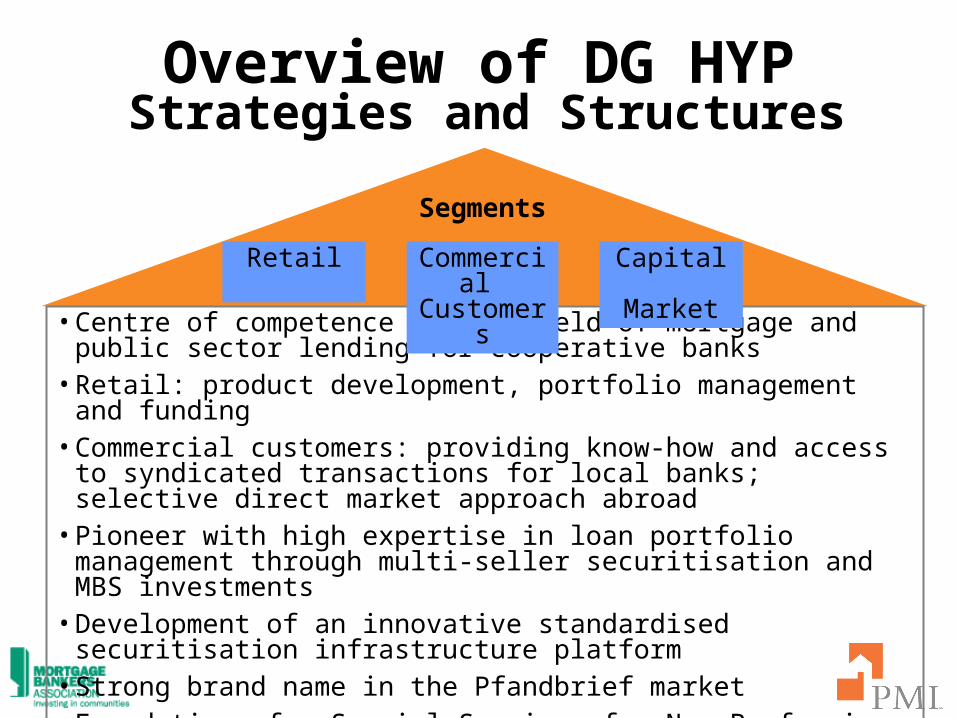

•Centre of competence in the field of mortgage and public sector lending for cooperative banks

•Retail: product development, portfolio management and funding

•Commercial customers: providing know-how and access to syndicated transactions for local banks; selective direct market approach abroad

•Pioneer with high expertise in loan portfolio management through multi-seller securitisation and MBS investments

•Development of an innovative standardised securitisation infrastructure platform

•Strong brand name in the Pfandbrief market•Foundation of a Special Servicer for Non Performing Loans

Overview of DG HYPStrategies and Structures

Retail

Segments

Commercial

Customers

Capital Market

MBA Logo

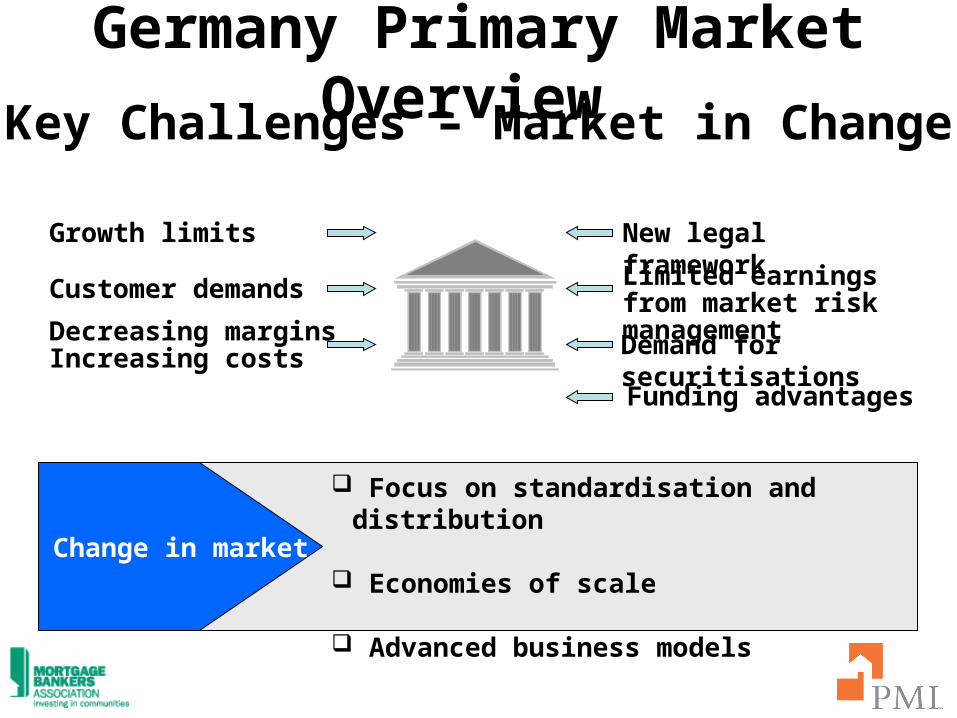

Germany Primary Market Overview Key Challenges – Market in Change

Change in market

Customer demands

Growth limits

Decreasing marginsIncreasing costs Demand for

securitisations

New legal frameworkLimited earnings from market risk management

Funding advantages

Focus on standardisation and distribution

Economies of scale

Advanced business models

MBA Logo

Germany Primary Market Overview

Rati

ng

AAA AA A BBB

Available for Mortgage Backed SecuritiesCollateral Pool for Covered Bonds

Bank PortfolioTarget Clients

Investors

AAA A

Mortgage Backed Securities

AAA AA A

Covered Bonds (Pfandbrief)

SecuritisationVolume

Mortgage ProductsPortfolio Management/Product

Development

MBA Logo

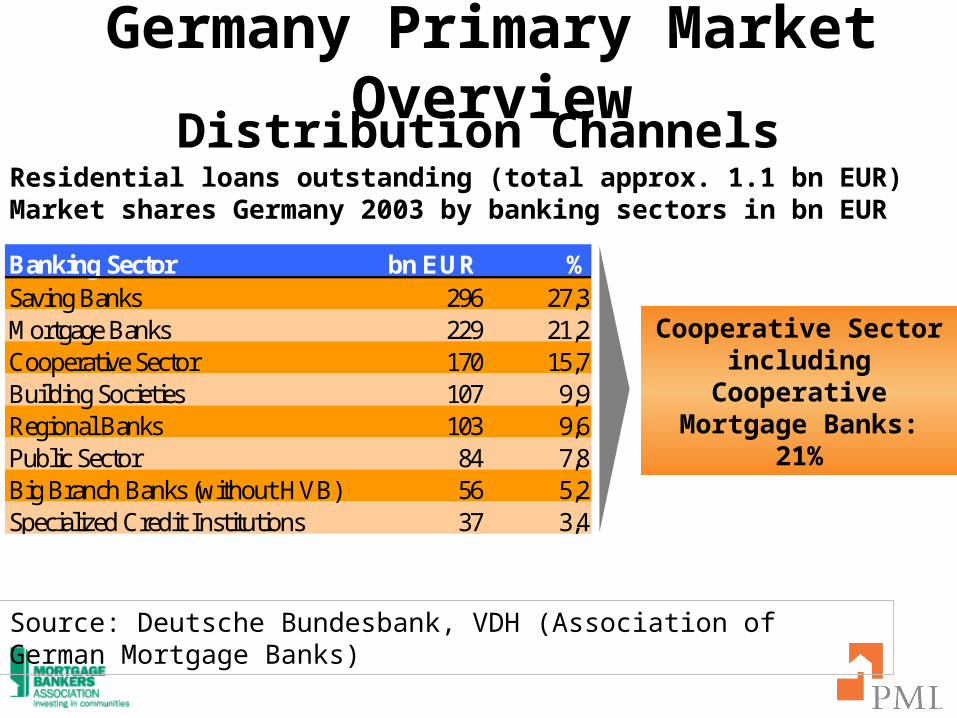

Residential loans outstanding (total approx. 1.1 bn EUR) Market shares Germany 2003 by banking sectors in bn EUR

Germany Primary Market Overview

Distribution Channels

Cooperative Sectorincluding

Cooperative Mortgage Banks:

21%

Source: Deutsche Bundesbank, VDH (Association of German Mortgage Banks)

Banking Sector bn EUR %Saving Banks 296 27,3Mortgage Banks 229 21,2Cooperative Sector 170 15,7Building Societies 107 9,9Regional Banks 103 9,6Public Sector 84 7,8Big Branch Banks (without HVB) 56 5,2Specialized Credit Institutions 37 3,4

MBA Logo

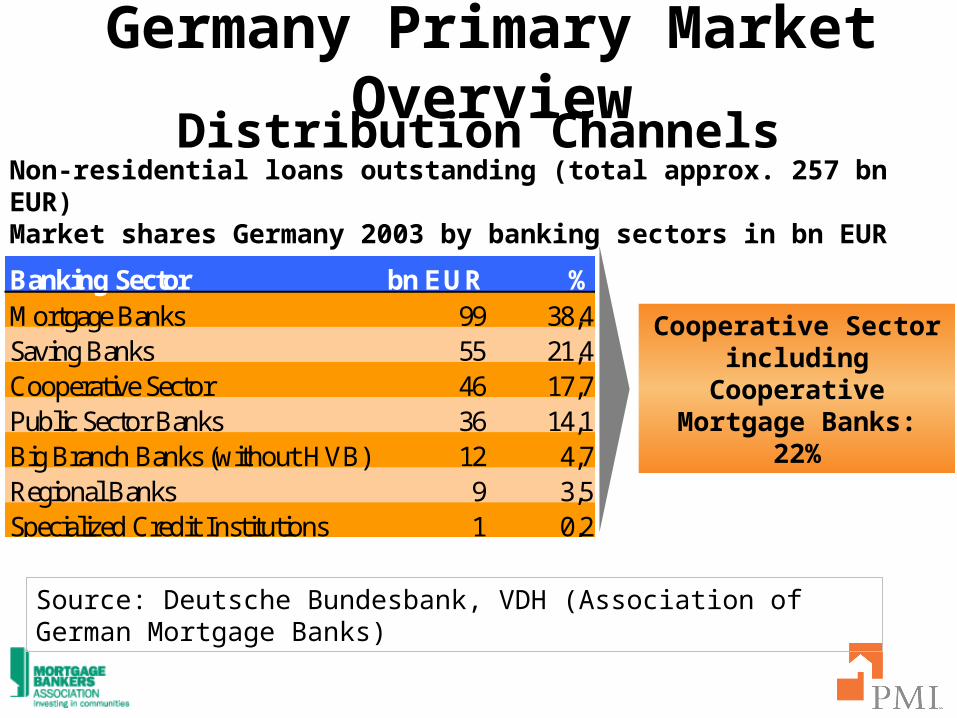

Non-residential loans outstanding (total approx. 257 bn EUR) Market shares Germany 2003 by banking sectors in bn EUR

Germany Primary Market Overview

Distribution Channels

Cooperative Sectorincluding

Cooperative Mortgage Banks:

22%

Source: Deutsche Bundesbank, VDH (Association of German Mortgage Banks)

Banking Sector bn EUR %Mortgage Banks 99 38,4Saving Banks 55 21,4Cooperative Sector 46 17,7Public Sector Banks 36 14,1Big Branch Banks (without HVB) 12 4,7Regional Banks 9 3,5Specialized Credit Institutions 1 0,2

MBA Logo

Germany Primary Market Overview

Benefits for Local Cooperative Banks Retail Customers:

- ‘Combined support’ for cooperative banks in sales and marketing via sales force of a home loan and savings association (BSH, No. 1 in Germany)

- ‘One-stop shopping’ for real estate financing customers based on a standardised product portfolio, where the products fit to each other

- Consulting and processing support with a uniform and efficient software Increased income through higher market penetration

Commercial Customers: - Access to ‘big ticket business’ in alliance with DG HYP - Loan syndications of DG HYP together with cooperative

banks leads to new business potential and active management of the loan book

- Know-how transfer from DG HYP regional real property financing offices

MBA Logo

Germany Primary Market Overview

Benefits for Local Cooperative Banks Capital Markets:

- Reducing ‘concentration risks’ by risk transfer / securitisation - Introducing new income opportunities by usage of secondary loan market - Increase of flexibility due to richer refinancing possibilities - Improvement of risk / return profile - Capital relief due to securitisation Processing: - Industrial production (advantages through outsourcing

regarding time and price) - Using a processing norm with system advantages e.g. via

scoring when checking creditworthiness

- Economies of scale due to increased processing quantities - Relieving the local back offices in order to be able to

concentrate on sophisticated processing and on sales

MBA Logo

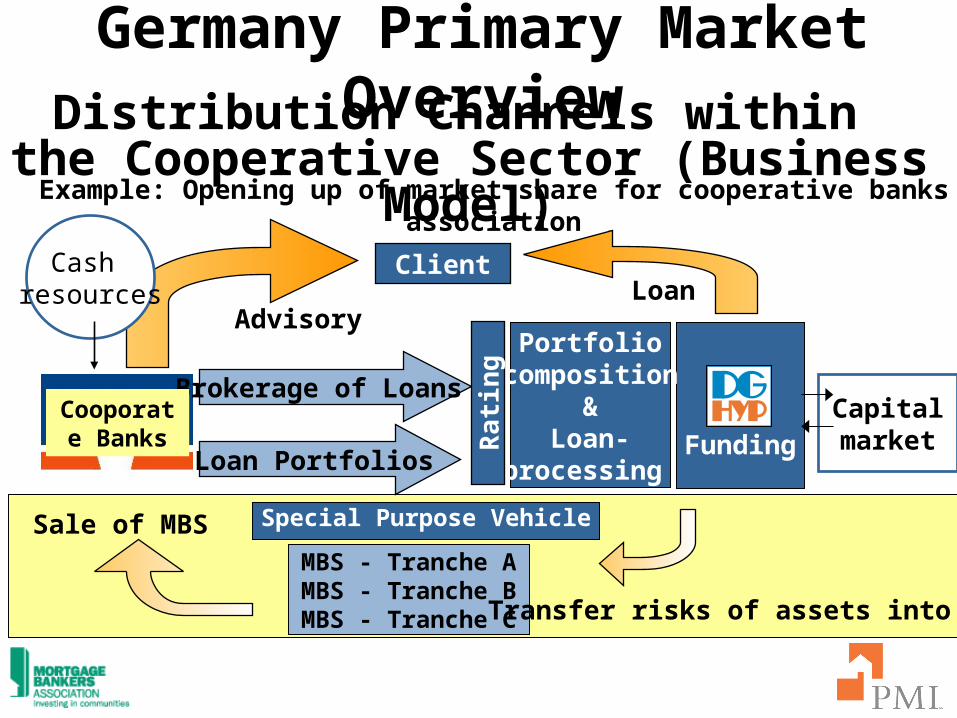

Funding

Example: Opening up of market share for cooperative banks association

Special Purpose Vehicle

Cash resources

MBS - Tranche AMBS - Tranche BMBS - Tranche C

Client

Brokerage of Loans

Transfer risks of assets into MBS

AdvisoryLoan

Capitalmarket

Portfoliocomposition

&Loan-

processing

Sale of MBSR

ati

ng

Loan Portfolios

Germany Primary Market Overview

Cooporate Banks

Distribution Channels within the Cooperative Sector (Business

Model)

MBA Logo

European ABS Market by Assets 2003/2004

Source: HSBC

Volume: 224 bn USD (funded)

Lease2%

Credit Cards

4%

Con.Loans

4%

RMBS56%

Auto2%

Other16%

CMBS5%

CDO11%

Credit Cards

5%

Lease3%

WBS4%

RMBS55%

Auto2%

Other17%

CMBS6%

CDO9%

Volume: 163 bn USD (funded)

2003

2004 (as of 06/2004)

Germany Primary Market Overview

MBS-Volume: 61% MBS-Volume: 61%

MBA Logo

Germany Primary Market Overview

Outsourcing: - DG HYP VR kreditwerk (retail servicer): 07/2000

- Mortgage Servicing Standards

Drivers: - Economics Cost Efficiency - center of competence Factory Process,

Value-Added Chain - Rating Advantages needed

(Basle II)

Developments: - Separation of a) Special Servicerb) MBS-Administrationc) Production Chain: Originator / Underwriter /

Servicer

Servicing Requirements and Issues

MBA Logo

Production Chain

Current setting: - Different jurisdictions

- Property valuation - Non Performing Loans work out/Enforcement - Securitisation regime (Synthetic vs.True Sale)

But: - Process Standardisation

- Transparency (regulatory and investor driven) - Harmonisation of funding and risk hedging

ALIGNMENT

Prospects for a Pan-European Mortgage Market

MBA Logo

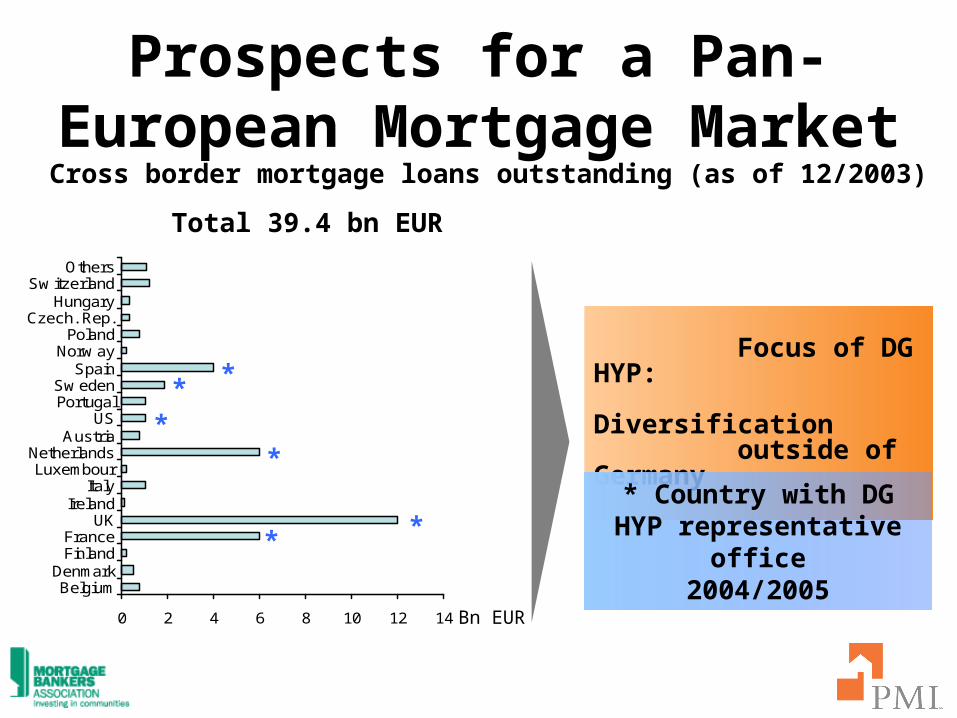

Total 39.4 bn EUR

Cross border mortgage loans outstanding (as of 12/2003)

Prospects for a Pan-European Mortgage

Market

Focus of DG HYP: Diversification outside of Germany

* Country with DG HYP representative

office2004/2005

0 2 4 6 8 10 12 14

BelgiumDenmark

FinlandFrance

UKIreland

ItalyLuxembour

NetherlandsAustria

USPortugalSw eden

SpainNorw ay

PolandCzech. Rep.

HungarySw itzerland

Others

Bn EUR

* *

*

*

*

*

MBA Logo

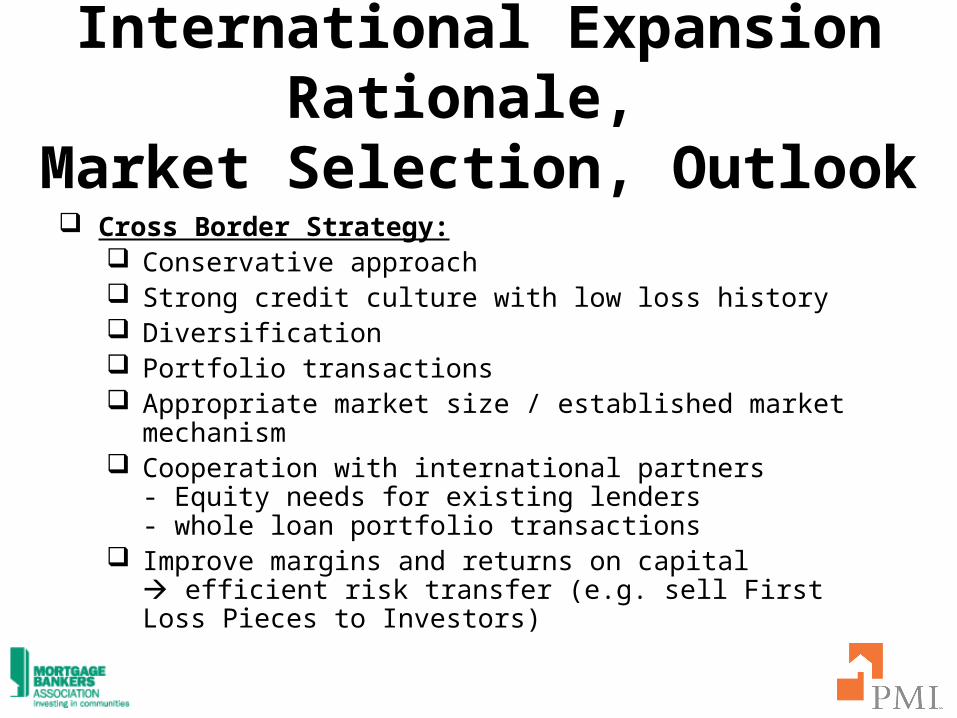

Cross Border Strategy: Conservative approach Strong credit culture with low loss history Diversification Portfolio transactions Appropriate market size / established market

mechanism Cooperation with international partners

- Equity needs for existing lenders- whole loan portfolio transactions

Improve margins and returns on capital efficient risk transfer (e.g. sell First Loss Pieces to Investors)

International Expansion Rationale,

Market Selection, Outlook

MBA Logo

Markus BolderHead of Credit TreasuryDeutsche Genossenschafts-Hypothekenbank AGRosenstraße 2 20095 Hamburg Germany

Phone: # 49 (40) 33 34 – 36 14Fax: # 49 (40) 33 34 11 71Email: [email protected]

Ladies and Gentlemen,Thank you very much for your

attention!