2004 edition world investment prospects - eiugraphics.eiu.com/files/ad_pdfs/wip_2004.pdf2004 edition...

TRANSCRIPT

2004 edition

World investment prospectsThe revival ofglobalisation?

LONDON

15 Regent Street

London

SW1Y 4LR

United Kingdom

Tel: (44.20) 7830 1000

Fax: (44.20) 7499 9767

E-mail: [email protected]

NEW YORK

111 West 57th Street

New York

NY 10019

United States

Tel: (1.212) 554 0600

Fax: (1.212) 586 1181/2

E-mail: [email protected]

HONG KONG

60/F, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: (852) 2585 3888

Fax: (852) 2802 7638

E-mail: [email protected]

For further information: JETRO Invest Japan Business Support Center Akasaka Twin Tower Bldg. • 2-17-22, Akasaka, Minato-ku • Tokyo 107-0052Tel:+81-3-3584-6042 • Fax:+81-3-3584-6024 • E-mail: [email protected]

Visit our web site now!www.investjapan.org

Thinking about Japan?“Japan is a country rich in assets, with ready access to capital, state-of-the-art technology, an excellent infrastructure, government by law, and a dedicated, high-quality work force.”

Carlos Ghosn, President and CEONissan Motor Co., Ltd.

Call on JETRO. In Japan, the manekineko,

beckoning cat, is a symbol that

welcomes customers and brings

good luck in business. JETRO has

been helping businesses for over

forty years, and can be your sym-

bol of welcome in Japan. The

Japan External Trade Organiza-

tion (JETRO) is a Japanese

government-funded organization

that provides a full range of

information and support services

to those who would like to set

up business operations in Japan

through a worldwide network

of 79 overseas offices and 38

local offices.

One of JETRO’s main facili-

ties is the Invest Japan Business

Support Center (IBSC)—a one-

stop service center providing free

investment information and

consulting by English-speaking

specialists. In addition, potential

investors can use free temporary

offices at IBSC which is conven-

iently located in central Tokyo.

Whatever your business needs

are, calling on JETRO is the smart

way to invest in Japan.

© The Economist Intelligence Unit 3

WORLD INVESTMENT PROSPECTS

The editors:

Laza Kekic, Gareth Lofthouse, Dafne Ter-Sakarian,

Philip Whyte

Introduction:

Daniel Franklin, Editorial Director, Economist

Intelligence Unit

Global foreign direct investment: trends and forecasts:

Laza Kekic, Director, Country Forecasting Services,

Economist Intelligence Unit

Global foreign direct investment: the investor

perspective:

Gareth Lofthouse, Director, Executive Services Europe,

Economist Intelligence Unit

This report drew on the work of the Economist

Intelligence Unit’s large team of country economists

and regional specialists, in particular the following

analysts who regularly produce Country Forecast

reports.

North America

Robin Bew Gerard Walsh

Western Europe

Robert O’Daly Jan Friedrich

Ania Thiemann Charles Jenkins

Stefan Wesiak Dan O’Brien

Neil Prothero

Eastern Europe & the former Soviet Union

Leila Butt Stuart Hensel

James Owen Joan Hoey

Mark Katzman Matthew Sherwood

Asia

Leo Abruzzese Kate Allard

Caroline Bain David Webb

Graham Richardson Kilbinder Dosanjh

Robert Ward Paul Cavey

Danny Richards

Latin America & the Caribbean

Justine Thody Robert Wood

John Bowler Mary Stanier

Emily Morris Martin Pickering

Middle East & Africa

David Cowan Ben Faulks

Pratibha Thaker Hania Farhan

Keren Uziyel James Reeve

Neil Partrick

We would also like to thank the following people, all of

whom were instrumental in ensuring that this report

was produced: John Andrew, Mark Bennet, David

Calver, Anwen John, Mike Kenny, Gareth Owen and

Alex Selby-Boothroyd.

The authors

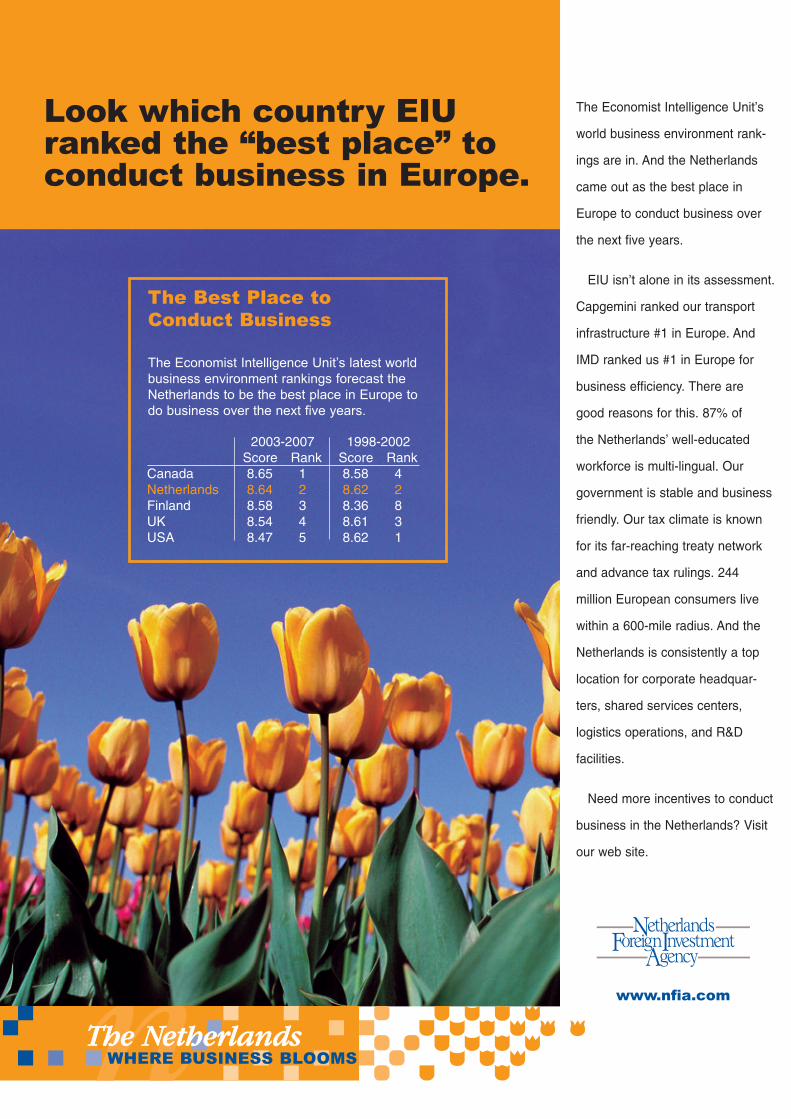

TThe Nhe NetheretherlandslandsWHERE BUSINESS BLOOMS

The Economist Intelligence Unit’s

world business environment rank-

ings are in. And the Netherlands

came out as the best place in

Europe to conduct business over

the next five years.

EIU isn’t alone in its assessment.

Capgemini ranked our transport

infrastructure #1 in Europe. And

IMD ranked us #1 in Europe for

business efficiency. There are

good reasons for this. 87% of

the Netherlands’ well-educated

workforce is multi-lingual. Our

government is stable and business

friendly. Our tax climate is known

for its far-reaching treaty network

and advance tax rulings. 244

million European consumers live

within a 600-mile radius. And the

Netherlands is consistently a top

location for corporate headquar-

ters, shared services centers,

logistics operations, and R&D

facilities.

Need more incentives to conduct

business in the Netherlands? Visit

our web site.

Look which country EIUranked the “best place” toconduct business in Europe.

The Best Place to Conduct Business

The Economist Intelligence Unit’s latest worldbusiness environment rankings forecast theNetherlands to be the best place in Europe todo business over the next five years.

2003-2007 1998-2002Score Rank Score Rank

Canada 8.65 1 8.58 4Netherlands 8.64 2 8.62 2Finland 8.58 3 8.36 8UK 8.54 4 8.61 3USA 8.47 5 8.62 1

www.nfia.com

© The Economist Intelligence Unit 5

WORLD INVESTMENT PROSPECTS

Introduction

By Daniel Franklin, Editorial Director,

Economist Intelligence Unit

This is the fourth edition of the Economist Intelligence

Unit's World investment prospects, and regular

readers will notice a few changes. The report has a

livelier look, thanks to a new design and a fresh cover.

For the first time, it also has advertising, which has

helped to fund an extra layer of research: a global

survey of 500 senior executives, exploring corporate

expectations for foreign direct investment (FDI). This

adds a new dimension to the analysis and provides an

additional fix on future trends.

The tricky business of trying to forecast foreign

investment has become an exercise in triangulation.

We can now map FDI’s expected course by the

combined means of the global survey, our five-year

economic forecast and our systematic assessment of

the likely evolution of business environments across

60 countries that collectively account for more than

95% of the world’s GDP and crossborder investment.

Reassuringly, all the indicators point in the same

broad direction: towards a rebound in FDI, after three

years of decline during which the troubles of

recession, terrorism and war took a heavy toll.

In 2003, global FDI of some US$575bn was almost

60% below its dizzy peak of US$1.4trn in 2000.

However, a broad-based economic recovery is now

under way, and, despite protectionist temptations,

business environments around the world will for the

most part become more conducive to foreign

investment over the coming years. Investor

confidence is returning. Our global survey of

executives shows an overwhelming 77% of companies

planning to increase the level of FDI over the next five

years compared with 1999-2003, with more than one

in four expecting the increase to be over 50%. We

forecast that global FDI will bounce back to US$755bn

in 2004, 31% higher than in 2003. By 2008, the end of

our forecast period, we expect the worldwide total to

have climbed back to US$1.2trn, higher than in any

year except top-of-the-boom 2000.

Our benign baseline scenario is, however, subject

to an array of significant risks. Among the many

threats to the resumed vigour of FDI—ranging from US

imbalances to Chinese bubbles, and from terrorist

bombs to anti-globalist bluster—the geopolitical risks

loom largest. After the fall of the Berlin Wall and the

collapse of Soviet communism, international political

co-operation helped to fuel a decade of growth in

foreign investment. The co-operative spirit has wilted

in the aftermath of the Iraq war. The deepening of

globalisation, with FDI to the fore, could be at risk if

the tensions over the Middle East and other arguments

result in a retreat into regionalism or, worse, outright

protectionism.

As it is, many governments’ poor economic policies

already keep FDI well below its full potential, its

benefits unevenly spread around the world. The US, we

predict, will attract about one-fifth of all inward

investment over the next five years. Although our

survey shows enthusiasm among executives about the

prospects for investment into developing countries,

we expect a revival in merger and acquisition (M&A)

activity to boost the developed-country share of

global FDI back above 70%. Among the developing

countries themselves, FDI flows are also highly

concentrated in just a few places. China, Mexico,

Brazil, Russia and India will account for the lion’s (and

the tiger’s) share.

It is no surprise to see China viewed in the executive

survey as the top emerging market for FDI; investment

into China is likely to be some US$58bn in 2004

(roughly half the flow into the US), growing to nearly

US$80bn by 2008. More intriguing is India’s rise up

the scale of attraction for global executives; in

corporate perceptions, other big emerging markets

pale by comparison with the two Asian giants. Yet

© The Economist Intelligence Unit 6

WORLD INVESTMENT PROSPECTS INTRODUCTION

India still has a long way to go: we predict that its

inward FDI will rise from US$5bn last year to US$13bn

in 2008—not in the same league as China, and still

behind Brazil.

Neither the survey nor our own analysis points to a

post-enlargement surge of investment into eastern

Europe. For most of these countries, the EU-related

FDI boom is already behind them, as most of the

benefits of joining the European club are offset by the

costs of membership and a possible slowdown in

reform momentum. FDI into the east European new EU

member countries more than halved in 2003; it is

likely to recover, but not spectacularly. The new EU

members will learn that competition for investment

around the world—not least, from cheaper-labour

places further east in Europe and from Asia—is

intense.

One country that has lately been losing out in the

competition for FDI is the UK. In the 1990s it was

Europe’s star, and it still accounts for nearly one-

quarter of the total stock of FDI in the EU. However,

with the collapse of the M&A boom, flows of

investment into the UK have dwindled—to US$14.5bn

in 2003, just 5% of the EU total and less than went to

Italy. The UK’s share of EU investment has fallen in

every single year since 1999, the year the euro was

launched. According to statistical analysis of the

determinants of FDI by Laza Kekic, this report’s main

editor, staying outside the euro zone may cost EU

members at least one-third of potential annual FDI

flows. Joining the single currency is off the UK’s

agenda for now, and our survey of executives reveals

poor perceptions of the country’s attractiveness for

investors in several vital areas.

So this report should concentrate the minds of

policymakers and investment agencies in the UK, as

well as those in the other 59 countries for which it

provides succinct FDI profiles. For corporate

executives, the report points to where the

opportunities (and problems) lie, and captures the

views of their peers around the world on investment

trends. Those involved in appraising FDI will find an

abundance of fresh data and analysis—valuable inputs

into the risk assessment and rigorous market research

that, our survey suggests, are essential for successful

foreign investment. In short, these pages are for all

those preparing to compete in the coming era of FDI

growth.

© The Economist Intelligence Unit 8

WORLD INVESTMENT PROSPECTS

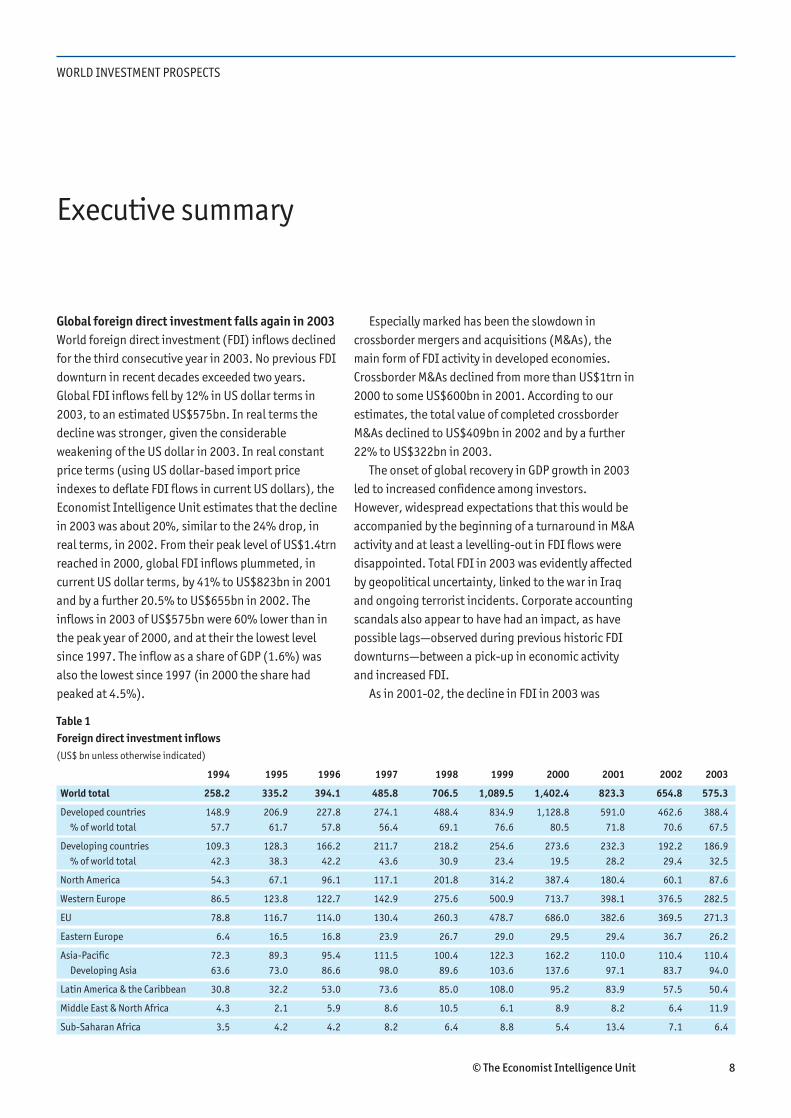

Global foreign direct investment falls again in 2003

World foreign direct investment (FDI) inflows declined

for the third consecutive year in 2003. No previous FDI

downturn in recent decades exceeded two years.

Global FDI inflows fell by 12% in US dollar terms in

2003, to an estimated US$575bn. In real terms the

decline was stronger, given the considerable

weakening of the US dollar in 2003. In real constant

price terms (using US dollar-based import price

indexes to deflate FDI flows in current US dollars), the

Economist Intelligence Unit estimates that the decline

in 2003 was about 20%, similar to the 24% drop, in

real terms, in 2002. From their peak level of US$1.4trn

reached in 2000, global FDI inflows plummeted, in

current US dollar terms, by 41% to US$823bn in 2001

and by a further 20.5% to US$655bn in 2002. The

inflows in 2003 of US$575bn were 60% lower than in

the peak year of 2000, and at their the lowest level

since 1997. The inflow as a share of GDP (1.6%) was

also the lowest since 1997 (in 2000 the share had

peaked at 4.5%).

Especially marked has been the slowdown in

crossborder mergers and acquisitions (M&As), the

main form of FDI activity in developed economies.

Crossborder M&As declined from more than US$1trn in

2000 to some US$600bn in 2001. According to our

estimates, the total value of completed crossborder

M&As declined to US$409bn in 2002 and by a further

22% to US$322bn in 2003.

The onset of global recovery in GDP growth in 2003

led to increased confidence among investors.

However, widespread expectations that this would be

accompanied by the beginning of a turnaround in M&A

activity and at least a levelling-out in FDI flows were

disappointed. Total FDI in 2003 was evidently affected

by geopolitical uncertainty, linked to the war in Iraq

and ongoing terrorist incidents. Corporate accounting

scandals also appear to have had an impact, as have

possible lags—observed during previous historic FDI

downturns—between a pick-up in economic activity

and increased FDI.

As in 2001-02, the decline in FDI in 2003 was

Executive summary

Table 1

Foreign direct investment inflows

(US$ bn unless otherwise indicated)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

World total 258.2 335.2 394.1 485.8 706.5 1,089.5 1,402.4 823.3 654.8 575.3

Developed countries 148.9 206.9 227.8 274.1 488.4 834.9 1,128.8 591.0 462.6 388.4

% of world total 57.7 61.7 57.8 56.4 69.1 76.6 80.5 71.8 70.6 67.5

Developing countries 109.3 128.3 166.2 211.7 218.2 254.6 273.6 232.3 192.2 186.9

% of world total 42.3 38.3 42.2 43.6 30.9 23.4 19.5 28.2 29.4 32.5

North America 54.3 67.1 96.1 117.1 201.8 314.2 387.4 180.4 60.1 87.6

Western Europe 86.5 123.8 122.7 142.9 275.6 500.9 713.7 398.1 376.5 282.5

EU 78.8 116.7 114.0 130.4 260.3 478.7 686.0 382.6 369.5 271.3

Eastern Europe 6.4 16.5 16.8 23.9 26.7 29.0 29.5 29.4 36.7 26.2

Asia-Pacific 72.3 89.3 95.4 111.5 100.4 122.3 162.2 110.0 110.4 110.4

Developing Asia 63.6 73.0 86.6 98.0 89.6 103.6 137.6 97.1 83.7 94.0

Latin America & the Caribbean 30.8 32.2 53.0 73.6 85.0 108.0 95.2 83.9 57.5 50.4

Middle East & North Africa 4.3 2.1 5.9 8.6 10.5 6.1 8.9 8.2 6.4 11.9

Sub-Saharan Africa 3.5 4.2 4.2 8.2 6.4 8.8 5.4 13.4 7.1 6.4

© The Economist Intelligence Unit 9

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

concentrated in the developed world. FDI inflows in

the developed world fell by an estimated 16% in 2003

to US$388bn. The weaker US dollar, as well as strong

GDP growth, led to the expected recovery of FDI into

the US in 2003. By contrast, FDI into the EU fell by

27%, to US$271bn. In the developing world, the

decline in FDI inflows in 2001-03 was more modest—

FDI inflows declined by only 2.8% to US$187bn in

2003, compared with an average annual drop of some

16% in 2001-02. This was thanks to a strong recovery

in FDI into developing Asia in 2003, led by China. Latin

America experienced yet another year of decline, and

FDI into the east European transition economies also

fell, whereas previously it had held up well during the

slump.

FDI is set to recover

Following the sharp post-2000 decline, FDI flows

appear to have reached a nadir in 2003. We expect

global FDI inflows to bounce back by some 30% in US

dollar terms in 2004 (a weak US dollar will mean that

the increase in real terms is less pronounced, just as

the decline in 2003 was understated when expressed

in current US dollar terms). Strengthened economic

growth and a pick-up in fixed capital spending, as well

as improved confidence with regard to M&As, will

underpin a recovery in FDI. After three lean years,

however, the expected recovery in FDI will be modest:

the forecast total in global FDI inflows in 2004 of some

US$755bn will scarcely be much more than half the

total recorded in the peak year of 2000.

Between 2005 and 2008 global FDI inflows are

projected to grow at an average annual rate of 11%.

Despite an array of global risks, on baseline

assumptions the world economic recovery is set to

continue into the medium term, and this will underpin a

robust recovery in global FDI, which will again exceed

the rate of growth in world output and trade. Other

reasons to expect continued growth in FDI over the

medium term include: the ongoing global trend

towards better business environments (as measured by

our cross-country business environment rankings),

including ever more open policies towards FDI; progress

0 50 100 150 200 250

India

Singapore

Russia

Finland

Mexico

Sweden

Hong Kong

Switzerland

Brazil

Italy

Spain

Ireland

Germany

Canada

Netherlands

UK

France

China

USA

Belgium-Lux

Leading FDI recipients, 2004-08 average

US$ bn

Table 2

Foreign direct investment projections

(US$ bn unless otherwise indicated)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

World FDI inflows 1,089.5 1,402.4 823.3 654.8 575.3 754.8 883.7 991.6 1,079.6 1,165.7

Rate of growth (%) 54.2 28.7 -41.3 -20.5 -12.1 31.2 17.1 12.2 8.9 8.0

% of GDP 3.6 4.5 2.6 2.0 1.6 1.8 2.1 2.3 2.4 2.5

FDI inflows to developed countries 834.9 1,128.8 591.0 462.6 388.4 525.2 628.7 710.4 773.8 835.5

Rate of growth (%) 71.0 35.2 -47.6 -21.7 -16.0 35.2 19.7 13.0 8.9 8.0

% of GDP 3.5 4.7 2.5 1.9 1.4 1.7 1.9 2.1 2.3 2.4

% of world total 76.6 80.5 71.8 70.6 67.5 69.6 71.1 71.6 71.7 71.7

FDI inflows to developing countries 254.6 273.6 232.3 192.2 186.9 229.6 255.0 281.2 305.8 330.2

Rate of growth (%) 16.7 7.5 -15.1 -17.3 -2.8 22.8 11.1 10.3 8.7 8.0

% of GDP 3.9 3.8 3.3 2.6 2.3 2.6 2.7 2.8 2.8 2.8

% of world total 23.4 19.5 28.2 29.4 32.5 30.4 28.9 28.4 28.3 28.3

© The Economist Intelligence Unit 10

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

in regional integration; technological change and the

search for competitively priced skills; sharper global

competition pushing companies to seek lower-cost

destinations; and opportunities in emerging markets.

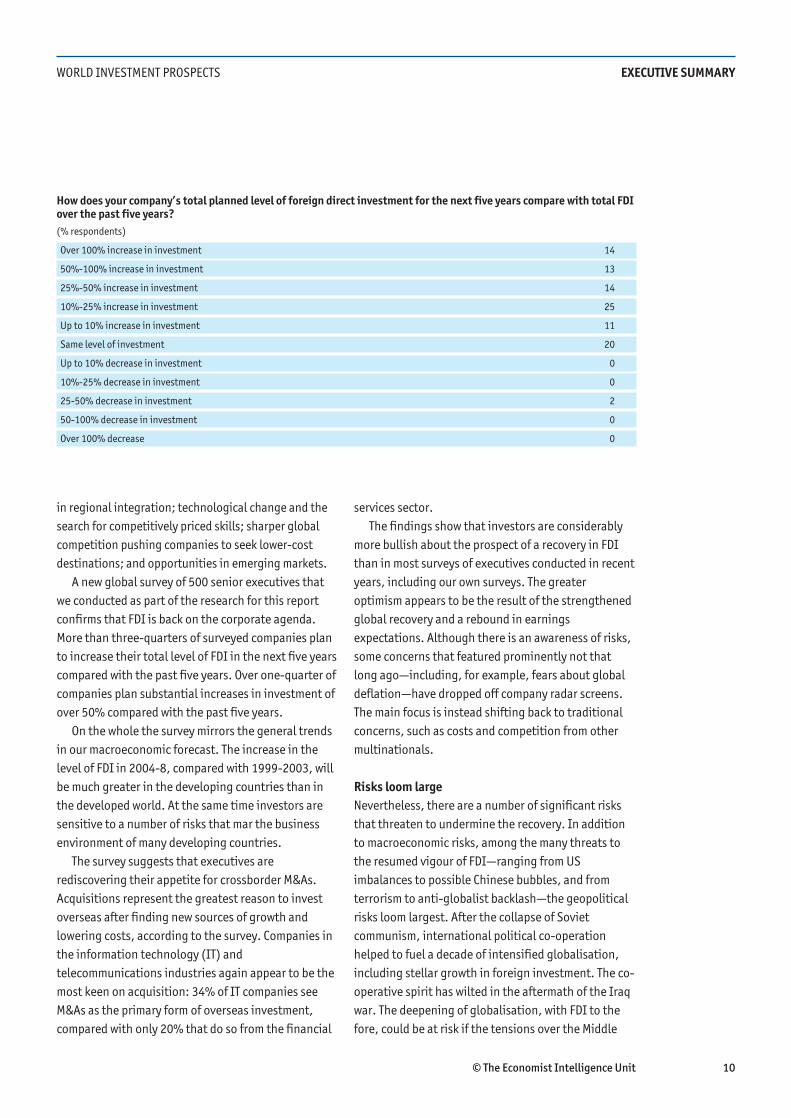

A new global survey of 500 senior executives that

we conducted as part of the research for this report

confirms that FDI is back on the corporate agenda.

More than three-quarters of surveyed companies plan

to increase their total level of FDI in the next five years

compared with the past five years. Over one-quarter of

companies plan substantial increases in investment of

over 50% compared with the past five years.

On the whole the survey mirrors the general trends

in our macroeconomic forecast. The increase in the

level of FDI in 2004-8, compared with 1999-2003, will

be much greater in the developing countries than in

the developed world. At the same time investors are

sensitive to a number of risks that mar the business

environment of many developing countries.

The survey suggests that executives are

rediscovering their appetite for crossborder M&As.

Acquisitions represent the greatest reason to invest

overseas after finding new sources of growth and

lowering costs, according to the survey. Companies in

the information technology (IT) and

telecommunications industries again appear to be the

most keen on acquisition: 34% of IT companies see

M&As as the primary form of overseas investment,

compared with only 20% that do so from the financial

services sector.

The findings show that investors are considerably

more bullish about the prospect of a recovery in FDI

than in most surveys of executives conducted in recent

years, including our own surveys. The greater

optimism appears to be the result of the strengthened

global recovery and a rebound in earnings

expectations. Although there is an awareness of risks,

some concerns that featured prominently not that

long ago—including, for example, fears about global

deflation—have dropped off company radar screens.

The main focus is instead shifting back to traditional

concerns, such as costs and competition from other

multinationals.

Risks loom large

Nevertheless, there are a number of significant risks

that threaten to undermine the recovery. In addition

to macroeconomic risks, among the many threats to

the resumed vigour of FDI—ranging from US

imbalances to possible Chinese bubbles, and from

terrorism to anti-globalist backlash—the geopolitical

risks loom largest. After the collapse of Soviet

communism, international political co-operation

helped to fuel a decade of intensified globalisation,

including stellar growth in foreign investment. The co-

operative spirit has wilted in the aftermath of the Iraq

war. The deepening of globalisation, with FDI to the

fore, could be at risk if the tensions over the Middle

How does your company’s total planned level of foreign direct investment for the next five years compare with total FDIover the past five years?

(% respondents)

Over 100% increase in investment 14

50%-100% increase in investment 13

25%-50% increase in investment 14

10%-25% increase in investment 25

Up to 10% increase in investment 11

Same level of investment 20

Up to 10% decrease in investment 0

10%-25% decrease in investment 0

25-50% decrease in investment 2

50-100% decrease in investment 0

Over 100% decrease 0

© The Economist Intelligence Unit 11

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

East and other disputes sour further the international

climate, and also result in a worsening of trends

towards regionalism and protectionism and away from

globalisation and multilateral liberalisation.

Our central forecast implies robust global growth

over the next five years. However, important risks

stem from large economic imbalances in key countries.

The huge US current-account deficit poses a threat.

The size of private-sector debt in the US, and to a

lesser extent in Europe, is also a cause for concern, as

are public-debt burdens in a number of OECD

countries. Balance sheets look stretched and savings

could increase markedly in many countries. This would

result in declines in spending and an economic

slowdown. A connected threat is that of another

downward turn in the equities market, which would

put paid to any revival in M&As. The widespread

assumption is that the declines in stock prices are

over. Yet the ratio of US stock prices to earnings is still

at least 50% above its historic average.

Three types of, in part inter-related, geopolitical

risks pose a threat to our baseline scenario of robust FDI

recovery: disruptions and costs to business associated

with terrorist attacks and the threat to personal

security; the potential adverse impact on global

business of the unsettled international political climate,

which is linked in large part to the continuing fallout

from the war in Iraq; and the threat to globalisation

from strengthened protectionist sentiment.

With respect to security risks, at present only a

small number of investment projects are being delayed

or cancelled. However, any increase in the intensity

and scope of attacks would have a more serious impact

on business. This would dampen long-term growth

prospects in the worst-affected countries, reducing

businesses' returns on investment, and bias

investment location decisions towards countries or

regions where security risks are perceived to be lower.

The forthcoming US presidential election, the large US

current-account deficit and the perceived

undervaluation of Asian currencies is increasing the

risk of trade protectionism. The prospects for reviving

World Trade Organisation (WTO) negotiations,

following the collapse of talks in Cancun in September

2003, appear very uncertain.

The Asian challenge

Developing Asia bucked the trend of FDI decline in

2003. FDI flows to China increased in 2003 to a record

total of US$53.5bn. High FDI flows to China will be

sustained in the coming years. According to our

survey, in regional terms, Asian countries will be the

Which of the following countries/regions are most attractive as targets for FDI based on the following criteria? Pleasechoose one country/region for each criterion.

(% respondents)

China Euro area Japan Russia USA UK India New EU Brazil

entrants

New consumer markets 49 9 2 5 7 2 9 15 4

Low-cost labour 50 2 0 3 1 0 29 12 3

New partnership possibilities 20 22 5 5 14 4 12 14 3

New corporate markets 23 22 3 5 17 3 7 15 4

Access to highly skilled labour force 6 22 7 3 14 6 30 10 2

New opportunities in outsourcing 16 9 1 3 7 2 46 12 4

Acquisition opportunities 15 20 2 5 13 5 8 22 9

Research and development activities 11 20 5 4 22 7 24 6 3

Greater efficiencies in supply chain 17 26 6 2 22 5 10 9 3

The survey explored the views of investors on the relative strengths and weaknesses of key countries and regions

as targets for FDI. Executives were asked to select the most attractive destination out of a number of key markets

against eight investment criteria, including labour skills and costs, market opportunities, R&D activities, and

outsourcing and acquisition opportunities.

© The Economist Intelligence Unit 12

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

main beneficiaries of the upturn in FDI. The survey

results indicate that China will continue to be the top

emerging market for FDI, but India is also becoming

very attractive to global investors (and not just for

outsourcing).

The survey confirms China as the leading

destination for investment on most criteria, especially

for companies seeking new consumer and corporate

markets and those sensitive to labour costs. China also

rates very well on the criteria of location of research

and development (R&D) activities, partnership (behind

only the euro zone) and outsourcing opportunities

(behind only India). Investor confidence in China

seems undiminished, despite fears that the Chinese

economy is at risk of overheating. China's powerful

attraction reaches across industries: manufacturing

and services sector companies (including IT and

financial services firms) are equally attracted by the

country's rapid growth and low-cost environment.

More surprising is India's performance as one of

the most attractive destinations for FDI based on

several criteria, given that the Indian authorities'

commitment to attract more FDI is yet to be fully

matched by more investment-friendly policies, which

may now be even less likely under the new Congress-

led government. No other country in the survey comes

close as a destination for outsourcing, thanks to the

country's skilled but low-cost English-speaking labour

force. India's technology revolution has also been

noted by investors, with companies from a range of

industries—including IT and financial services—citing

India as the world's top target for R&D investments.

The country offers attractive new consumer markets,

and better opportunities than other large emerging

markets for business partnerships.

The UK is losing its edge

FDI inflows into the UK plummeted in 2003 to

US$14.5bn—half the total of US$29.2bn recorded in

2002, which was in turn less than half the inflows of

US$61.5bn in 2001. Furthermore, the 2001 total was

almost half the peak inflow of US$119.9bn in 2000.

FDI inflows into the UK have now declined as a share of

EU FDI in every year since 1999. The UK's share of

EU15 FDI flows has declined steadily and

precipitously, from 29% in 1998 to 5% in 2003.

We have found strong econometric evidence for the

proposition that the UK's position outside the euro

Table 3

Foreign direct investment inflows in the EU

1998 1999 2000 2001 2002 2003

Inflows (US$ m)

EU15 260,322 478,659 686,012 382,638 369,544 271,285

UK 74,650 89,540 119,940 61,530 29,180 14,542

Sweden 19,413 59,385 22,124 13,084 11,829 3,576

Denmark 6,675 16,076 35,847 10,237 6,411 2,623

% share in EU total

UK 28.7 18.7 17.5 16.1 7.9 5.4

Sweden 7.5 12.4 3.2 3.4 3.2 1.3

Denmark 2.6 3.4 5.2 2.7 1.7 1.0

0

5

10

15

20

25

30

19

98

99

20

00

01

02

03

UK

Sweden

Denmark

Share of total FDI inflows into EU15

%

© The Economist Intelligence Unit 13

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

zone is deterring foreign investors. The survey results

also cast strong doubt on whether the UK can

recapture its lost share of global FDI, with the UK

performing particularly poorly on key measures of

attractiveness as a location to invest. The UK stands

out as the least attractive of the major markets for

offering new consumer and corporate markets, and

only Japan is perceived as having higher labour costs

out of nine key markets assessed by the respondents.

The UK even fails to impress in areas where

traditionally it would be expected to perform relatively

well, such as skill levels and R&D.

US investors, traditionally an important source of

investment for the UK, rank the country well below the

euro zone for attractiveness on most investment

criteria. The UK also receives a particularly critical

assessment from manufacturing companies. The

survey shows that executives see currency volatility as

one of the greatest risks to their overseas investments.

Asian investors are especially sensitive to this.

In our survey, UK companies appeared especially

bullish about their outward investment—30% said

that they would increase their FDI by over 50% in the

next five years compared with the previous five-year

total, compared with only 11% from euro zone

countries. Combined with the weak prospect for a

strong revovery in inward FDI, this suggests that net

FDI outflows from the UK are to increase.

New EU entrants will struggle to maintain FDI

attractiveness

Contrary to widespread expectations, the EU's

enlargement will not lead to a new surge in FDI into

the eight east European new member states. These

countries have already largely achieved the main

benefits of integration for investment. Further

positive changes to business environments associated

with EU membership will be small. Some possible

further improvement in risk perceptions and the

impact on FDI of fully joining the single market will

largely be offset by the effects of higher wages, the

adoption of business-inhibiting aspects of EU rules,

and the possibility of a post-accession slowdown in

reform momentum.

A sharp decline in FDI inflows to the new EU member

states in 2003 can be seen as the harbinger of a trend

that will lead to a lasting shift in the geographic

distribution of FDI in eastern Europe. FDI inflows over

the medium term into the new EU member states are

expected to recover from those recorded in 2003.

However, the danger of diversion of cost-sensitive

forms of FDI to even cheaper destinations looms larger

than any promise of much more relocation to these

countries of investment from the West.

Average annual FDI inflows into the new EU

members in eastern Europe are forecast at some

US$20bn in 2004-08. FDI inflows are expected to

peak in 2005-06, with the completion of some major

outstanding privatisations. After that investment will

be dominated by re-invested earnings and follow-on

investment by existing FDI ventures. The share of the

new EU members in the east European regional total

is expected to decline to below 50%, compared with

the share of almost two-thirds in the pre-2003

period. Economies in the Balkans and the

Commonwealth of Independent States (CIS), such as

Ukraine and, especially, Russia, will increase their

share of regional FDI.

Our survey results confirm that the prospects for

the new EU entrants appear less promising than is

Which of the following outsourcing activities have you made a direct overseas investment in?

(% respondents)

Already invested Planning to invest No plans to invest

Call centres 17 17 65

Research and development 36 24 40

Distribution and logistics 38 33 29

Treasury and finance 25 18 58

IT 36 29 35

HR/Payroll 19 25 56

© The Economist Intelligence Unit 14

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

often expected. The lure to investors of alternative

destinations in Asia appears to be very strong.

Investors find that the new EU entrants offer attractive

new consumer markets and interesting M&A oppor-

tunities. However, the new EU members compare

badly with Asia on labour costs, and are likely to lose

out on outsourcing opportunities not only to India but

to China as well. The survey offers little support for the

theory that EU enlargement will lead to a new surge of

FDI inflows into the new entrants; if anything, the

results suggest that it will become harder for the

region to attract investment against increasingly

tough competition from Asia, in particular.

There is also no support in the survey for the oft-

repeated proposition that small companies may be

more willing to invest in the region following EU

membership, as opposed to large companies that had

already taken this into account in earlier decision-

making.

Offshoring is here to stay

Offshoring has become an important driver for FDI.

According to our survey, the outsourcing trend is

extending far beyond call centres to affect most areas

of business. In fact, call centres make up a relatively

small proportion of offshoring activity in the survey:

only 17% of companies have overseas call centres,

compared with over one-third that already offshore

R&D, distribution and logistics, and IT, and 25% of

companies that offshore treasury and finance

operations. US companies are the largest investors in

outsourcing and offshoring, and UK companies are

more likely to offshore than companies from other EU

countries.

The offshoring boom looks set to continue, despite

the backlash in countries such as the US. Of

respondents to our survey, 17% are planning future

investments in offshore call centres, 24% plan to

invest in R&D, 33% in distribution and logistics, and

29% in IT.

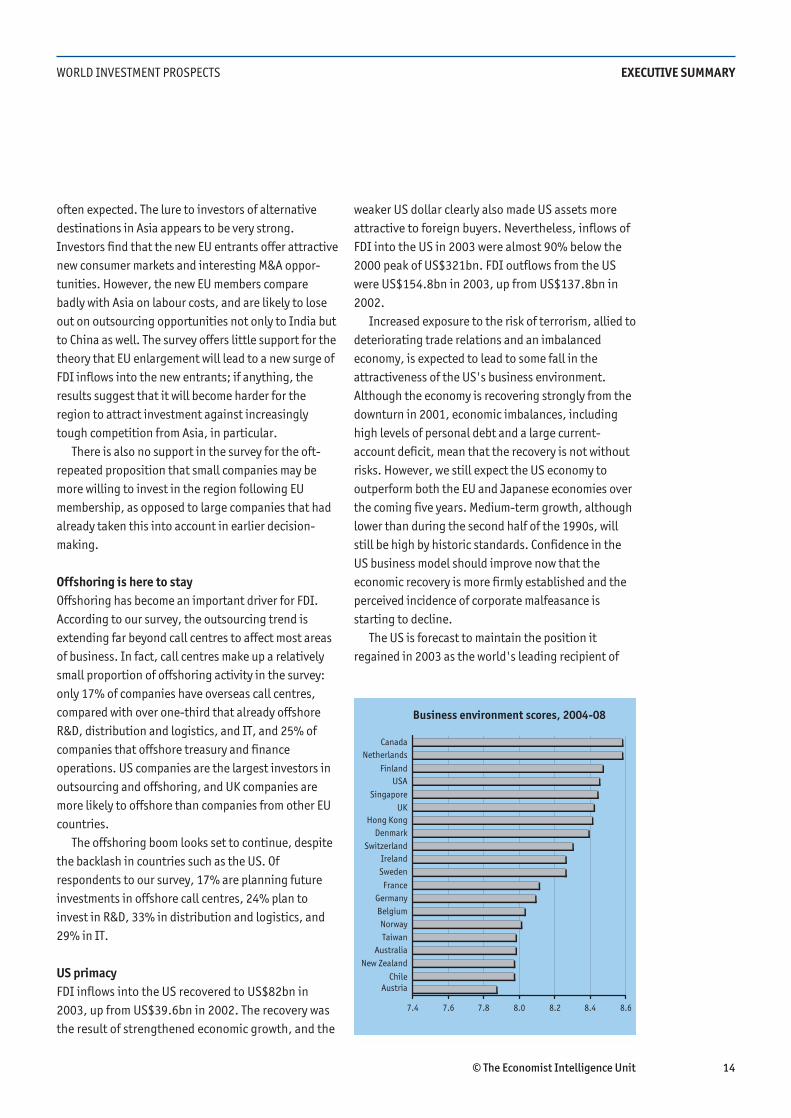

US primacy

FDI inflows into the US recovered to US$82bn in

2003, up from US$39.6bn in 2002. The recovery was

the result of strengthened economic growth, and the

weaker US dollar clearly also made US assets more

attractive to foreign buyers. Nevertheless, inflows of

FDI into the US in 2003 were almost 90% below the

2000 peak of US$321bn. FDI outflows from the US

were US$154.8bn in 2003, up from US$137.8bn in

2002.

Increased exposure to the risk of terrorism, allied to

deteriorating trade relations and an imbalanced

economy, is expected to lead to some fall in the

attractiveness of the US's business environment.

Although the economy is recovering strongly from the

downturn in 2001, economic imbalances, including

high levels of personal debt and a large current-

account deficit, mean that the recovery is not without

risks. However, we still expect the US economy to

outperform both the EU and Japanese economies over

the coming five years. Medium-term growth, although

lower than during the second half of the 1990s, will

still be high by historic standards. Confidence in the

US business model should improve now that the

economic recovery is more firmly established and the

perceived incidence of corporate malfeasance is

starting to decline.

The US is forecast to maintain the position it

regained in 2003 as the world's leading recipient of

7.4 7.6 7.8 8.0 8.2 8.4 8.6

Austria

New Zealand

Chile

Taiwan

Norway

Australia

Belgium

Germany

France

Sweden

Ireland

Denmark

Hong Kong

Switzerland

UK

Singapore

USA

Finland

Netherlands

Canada

Business environment scores, 2004-08

© The Economist Intelligence Unit 15

WORLD INVESTMENT PROSPECTS EXECUTIVE SUMMARY

FDI. Despite some deterioration in its high business

environment rating (it slips to fourth position for

2004-08), the US has clear potential for continued

large-scale inflows in the medium term. In addition to

the appeal of the vast size of the domestic market, the

US is the global technology leader and has

demonstrated an ability to increase productivity much

faster than most other developed countries. Foreign

companies view having operations in the US as a way

of gaining access to the technology and processes that

have made this productivity growth possible, and

subsequently applying them to other operations

around the world.

Challenges for the US emerging from our survey of

investors include concerns over currency volatility, in

the light of the weakening of the US dollar, and the

US's macroeconomic imbalances.

Investor motives and concerns

In developed countries, high costs present the

greatest risk to investments. Sluggish market growth

and currency volatility follow closely behind. In

emerging markets, foremost among the perceived

risks are political instability and corruption. Red tape

and the lack of rule of law serve to hamper business

further and increase uncertainty.

UK investors and those from other EU countries

register higher levels of concern about risks in

developing countries than their US counterparts,

whereas the situation is reversed when assessing risk

in developed countries.

The survey confirms that our ten categories of the

business environment are all highly rated as important

for investment. This means that countries need to

satisfy across the full range of business environment

issues. This is also the reason why developed countries

have the best business environments—taking into

account their performance across the board.

Specific policies towards foreign investment have a

moderately high influence on executive decisions, but

again less so than the broad business climate in a

country. Specific pro-FDI policies can have a

significant but rarely decisive influence on companies'

decisions to invest in a country.

As far as particular factors are concerned, the

survey confirms some well-known findings. Special tax

incentives are considered much less important than

other features of the investment climate; local

financing opportunities are of low importance for

direct investors.

© The Economist Intelligence Unit 17

WORLD INVESTMENT PROSPECTS

Business survey results

Section 1: Demographics

Which of the following titles best describes your job?

(% respondents)

Manager 35

CEO/COO/Chief executive/Managing director 22

SVP/VP 18

CFO/Treasurer/Comptroller 6

CKO/CIO/Technology director 3

Board member 3

Other 13

UK 12

Other developed 6

Where is your company located?

(% respondents)

EU 21

Asia 14

Eastern Europe 5

Other developing 13

US 29

© The Economist Intelligence Unit 18

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

What industry are you in?

(% respondents)

Automotive 7

Chemicals 4

Consumer goods (includes also consumer durables and retailing) 12

Healthcare, pharmaceuticals and biotechnology 3

Manufacturing (heavy equipment) 4

Other (includes aerospace, agribusiness, and "other") 12

Energy 3

Construction and real estate 4

Entertainment, media and publishing 3

Financial services (non-insurance plus insurance) 16

IT services 4

Professional services 14

Technology 4

Telecoms 4

Travel, tourism and transport 3

Government public sector 3

What is your organisation’s annual turnover?

(% respondents)

Under US$250m 48

US$250m – US$500m 10

US$500m – US$1bn 9

US$1bn – US$8bn 17

Over US$8bn 16

What percentage of your organisation’s total revenues comes from its home market

and what percentage comes from overseas markets?

(% respondents)

Overseas market 40

Home market 60

© The Economist Intelligence Unit 19

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

Section 2: FDI trends

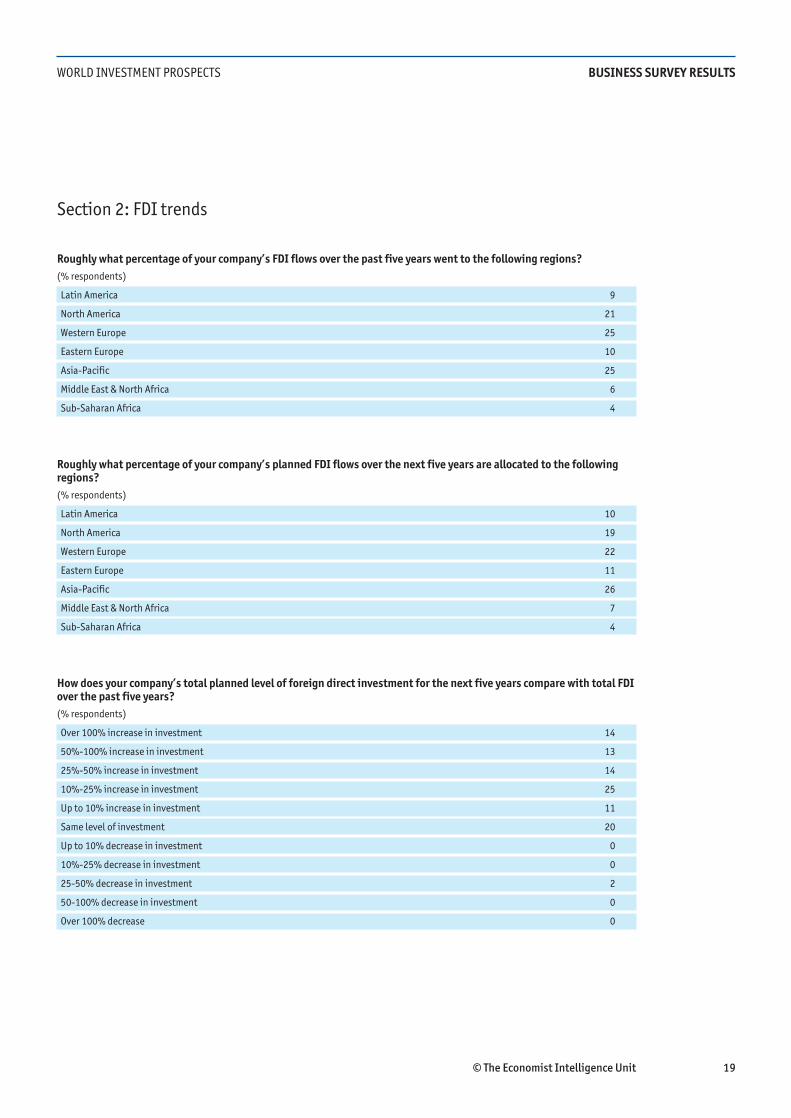

Roughly what percentage of your company’s FDI flows over the past five years went to the following regions?

(% respondents)

Latin America 9

North America 21

Western Europe 25

Eastern Europe 10

Asia-Pacific 25

Middle East & North Africa 6

Sub-Saharan Africa 4

Roughly what percentage of your company’s planned FDI flows over the next five years are allocated to the followingregions?

(% respondents)

Latin America 10

North America 19

Western Europe 22

Eastern Europe 11

Asia-Pacific 26

Middle East & North Africa 7

Sub-Saharan Africa 4

How does your company’s total planned level of foreign direct investment for the next five years compare with total FDIover the past five years?

(% respondents)

Over 100% increase in investment 14

50%-100% increase in investment 13

25%-50% increase in investment 14

10%-25% increase in investment 25

Up to 10% increase in investment 11

Same level of investment 20

Up to 10% decrease in investment 0

10%-25% decrease in investment 0

25-50% decrease in investment 2

50-100% decrease in investment 0

Over 100% decrease 0

© The Economist Intelligence Unit 20

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

Sales operation 29

Outsourcing/

offshoring 12

What percentage of your company’s planned FDI flows over the next five years

are allocated to the following activities?

(% respondents)

Research and development 13

Supply-chain management

and logistics 11

Regional headquarters 8

Other 5

Production and manufacturing activities 21

Which of the following outsourcing activities have you made a direct overseas investment in?

(% respondents)

Already invested Planning to invest No plans to invest

Call centres 17 17 65

Research and development 36 24 40

Distribution and logistics 38 33 29

Treasury and finance 25 18 58

IT 36 29 35

HR/Payroll 19 25 56

Which will be the main forms of investment activity for your company in the next five years? Please rank each in order,1 being the primary form of activity.

(% respondents)

1 2 3 4 5

Follow-on investment in existing operations 42 21 15 14 9

Joint ventures 21 37 26 13 2

Mergers and acquisitions 18 21 32 19 10

Greenfield investment 15 14 14 31 27

Franchising 4 7 14 23 52

© The Economist Intelligence Unit 21

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

Which of the following countries/regions are most attractive as targets for FDI based on the following criteria? Pleasechoose one country/region for each criterion.

(% respondents)

China Euro area Japan Russia USA UK India New EU Brazil

entrants

New consumer markets 49 9 2 5 7 2 9 15 4

Low-cost labour 50 2 0 3 1 0 29 12 3

New partnership possibilities 20 22 5 5 14 4 12 14 3

New corporate markets 23 22 3 5 17 3 7 15 4

Access to highly skilled labour force 6 22 7 3 14 6 30 10 2

New opportunities in outsourcing 16 9 1 3 7 2 46 12 4

Acquisition opportunities 15 20 2 5 13 5 8 22 9

Research and development activities 11 20 5 4 22 7 24 6 3

Greater efficiencies in supply chain 17 26 6 2 22 5 10 9 3

© The Economist Intelligence Unit 22

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

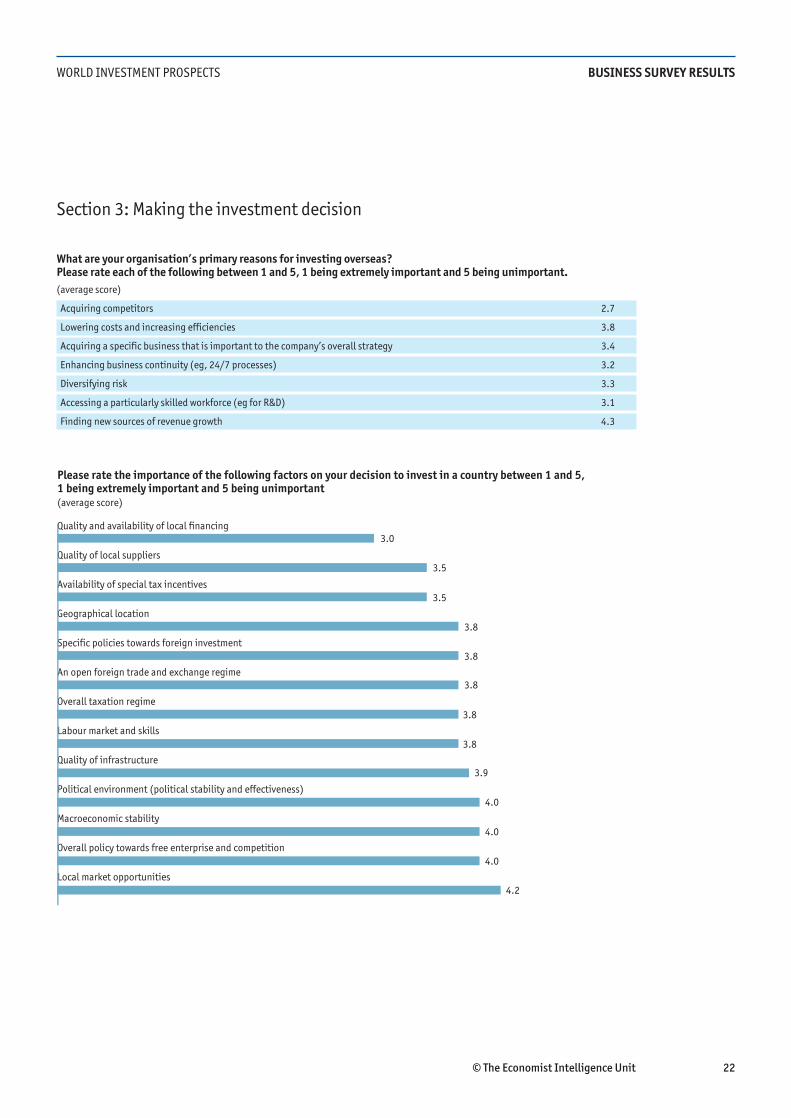

Section 3: Making the investment decision

What are your organisation’s primary reasons for investing overseas? Please rate each of the following between 1 and 5, 1 being extremely important and 5 being unimportant.

(average score)

Acquiring competitors 2.7

Lowering costs and increasing efficiencies 3.8

Acquiring a specific business that is important to the company’s overall strategy 3.4

Enhancing business continuity (eg, 24/7 processes) 3.2

Diversifying risk 3.3

Accessing a particularly skilled workforce (eg for R&D) 3.1

Finding new sources of revenue growth 4.3

Please rate the importance of the following factors on your decision to invest in a country between 1 and 5, 1 being extremely important and 5 being unimportant

Quality and availability of local financing

Quality of local suppliers

Availability of special tax incentives

Geographical location

Specific policies towards foreign investment

An open foreign trade and exchange regime

Overall taxation regime

Labour market and skills

Quality of infrastructure

Political environment (political stability and effectiveness)

Macroeconomic stability

Overall policy towards free enterprise and competition

Local market opportunities

(average score)

3.0

3.5

3.5

3.8

3.8

3.8

3.8

3.8

3.9

4.0

4.0

4.0

4.2

© The Economist Intelligence Unit 23

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

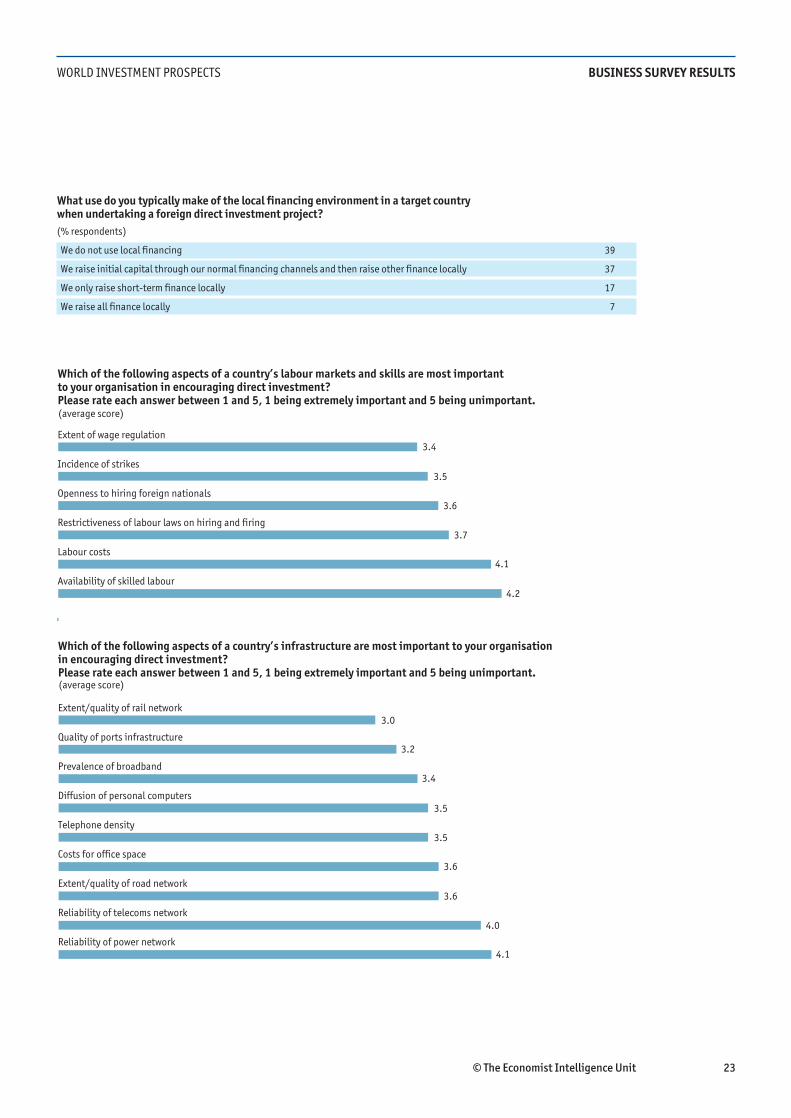

Which of the following aspects of a country’s labour markets and skills are most important to your organisation in encouraging direct investment? Please rate each answer between 1 and 5, 1 being extremely important and 5 being unimportant.

Extent of wage regulation

Incidence of strikes

Openness to hiring foreign nationals

Restrictiveness of labour laws on hiring and firing

Labour costs

Availability of skilled labour

(average score)

3.4

3.5

3.6

3.7

4.1

4.2

Which of the following aspects of a country’s infrastructure are most important to your organisation in encouraging direct investment? Please rate each answer between 1 and 5, 1 being extremely important and 5 being unimportant.

Extent/quality of rail network

Quality of ports infrastructure

Prevalence of broadband

Diffusion of personal computers

Telephone density

Costs for office space

Extent/quality of road network

Reliability of telecoms network

Reliability of power network

(average score)

3.0

3.2

3.4

3.5

3.5

3.6

3.6

4.0

4.1

What use do you typically make of the local financing environment in a target country when undertaking a foreign direct investment project?

(% respondents)

We do not use local financing 39

We raise initial capital through our normal financing channels and then raise other finance locally 37

We only raise short-term finance locally 17

We raise all finance locally 7

© The Economist Intelligence Unit 24

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

Section 4: Managing overseas investments

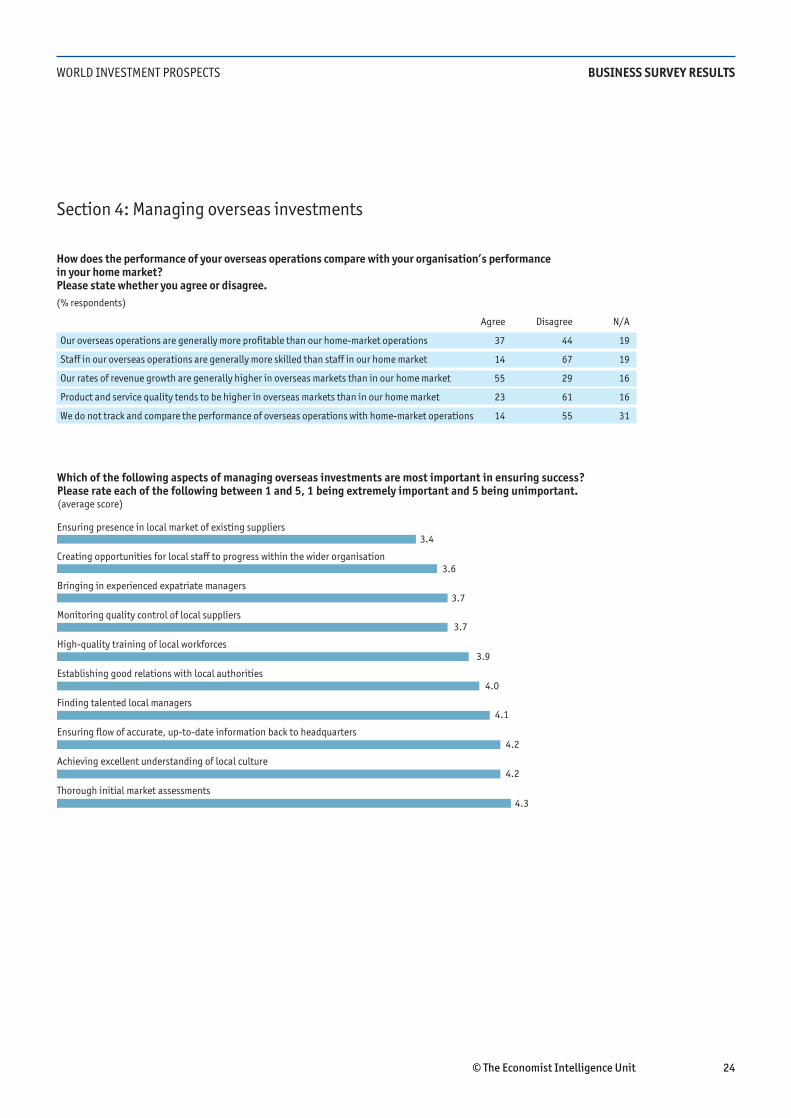

How does the performance of your overseas operations compare with your organisation’s performance in your home market? Please state whether you agree or disagree.

(% respondents)

Agree Disagree N/A

Our overseas operations are generally more profitable than our home-market operations 37 44 19

Staff in our overseas operations are generally more skilled than staff in our home market 14 67 19

Our rates of revenue growth are generally higher in overseas markets than in our home market 55 29 16

Product and service quality tends to be higher in overseas markets than in our home market 23 61 16

We do not track and compare the performance of overseas operations with home-market operations 14 55 31

Which of the following aspects of managing overseas investments are most important in ensuring success? Please rate each of the following between 1 and 5, 1 being extremely important and 5 being unimportant.

Ensuring presence in local market of existing suppliers

Creating opportunities for local staff to progress within the wider organisation

Bringing in experienced expatriate managers

Monitoring quality control of local suppliers

High-quality training of local workforces

Establishing good relations with local authorities

Finding talented local managers

Ensuring flow of accurate, up-to-date information back to headquarters

Achieving excellent understanding of local culture

Thorough initial market assessments

(average score)

3.4

3.6

3.7

3.7

3.9

4.0

4.1

4.2

4.2

4.3

© The Economist Intelligence Unit 25

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

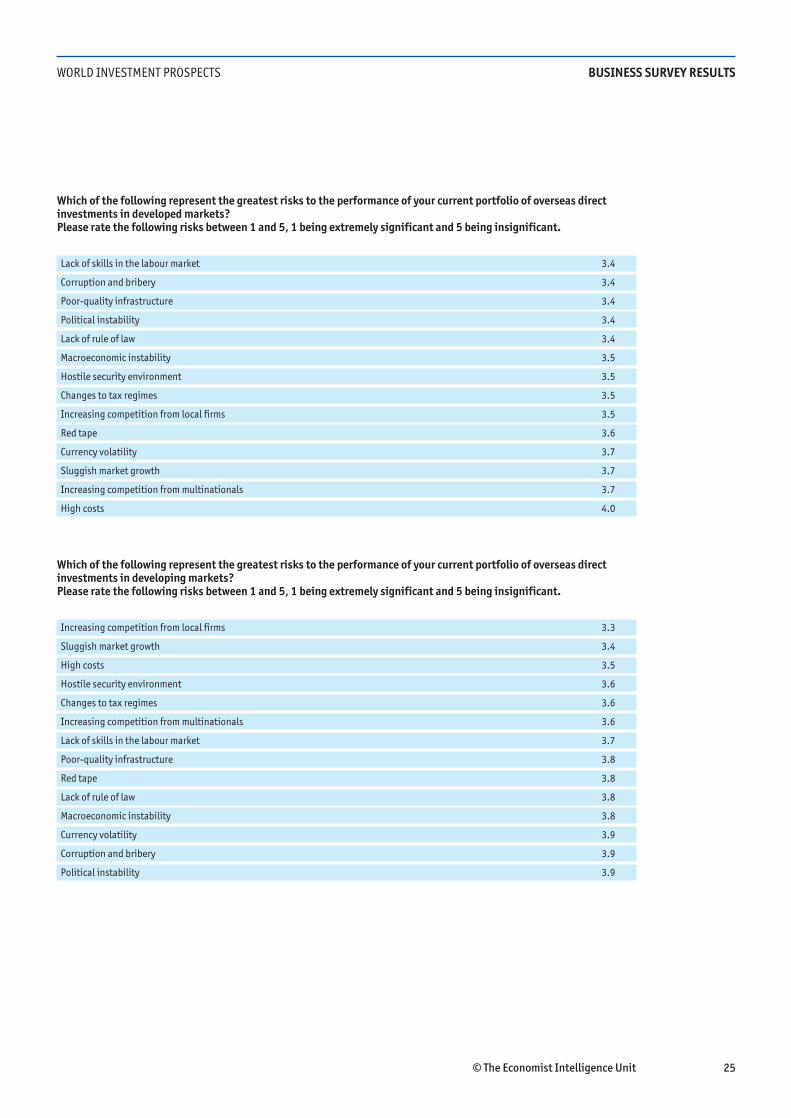

Which of the following represent the greatest risks to the performance of your current portfolio of overseas directinvestments in developed markets? Please rate the following risks between 1 and 5, 1 being extremely significant and 5 being insignificant.

Lack of skills in the labour market 3.4

Corruption and bribery 3.4

Poor-quality infrastructure 3.4

Political instability 3.4

Lack of rule of law 3.4

Macroeconomic instability 3.5

Hostile security environment 3.5

Changes to tax regimes 3.5

Increasing competition from local firms 3.5

Red tape 3.6

Currency volatility 3.7

Sluggish market growth 3.7

Increasing competition from multinationals 3.7

High costs 4.0

Which of the following represent the greatest risks to the performance of your current portfolio of overseas directinvestments in developing markets? Please rate the following risks between 1 and 5, 1 being extremely significant and 5 being insignificant.

Increasing competition from local firms 3.3

Sluggish market growth 3.4

High costs 3.5

Hostile security environment 3.6

Changes to tax regimes 3.6

Increasing competition from multinationals 3.6

Lack of skills in the labour market 3.7

Poor-quality infrastructure 3.8

Red tape 3.8

Lack of rule of law 3.8

Macroeconomic instability 3.8

Currency volatility 3.9

Corruption and bribery 3.9

Political instability 3.9

© The Economist Intelligence Unit 26

WORLD INVESTMENT PROSPECTS BUSINESS SURVEY RESULTS

How reliant is your organisation on local suppliers in your overseas investments?

Please choose the statement with which you most agree.

(% respondents)

Other 13.8

We rely on a mixture of local suppliers

and international suppliers,

depending on the country 57.9We rely on local

suppliers 16.6

We rely on

international

suppliers 11.7

What proportion of your organisation’s new products and services are developed overseas?

None 17.8

Under 10% 28.3

Between 10 and 25% 26.7

Between 25% and 50%

13.6

Between 50% and 75%

8.0

Over 75% 4.0

All of it 1.6

2004 edition

World investment prospectsThe revival ofglobalisation?

LONDON

15 Regent Street

London

SW1Y 4LR

United Kingdom

Tel: (44.20) 7830 1000

Fax: (44.20) 7499 9767

E-mail: [email protected]

NEW YORK

111 West 57th Street

New York

NY 10019

United States

Tel: (1.212) 554 0600

Fax: (1.212) 586 1181/2

E-mail: [email protected]

HONG KONG

60/F, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: (852) 2585 3888

Fax: (852) 2802 7638

E-mail: [email protected]