2004 canadian telecom summit darren entwistle member of the telus team

TRANSCRIPT

2004 Canadian telecom summit

Darren Entwistlemember of the TELUS Team

2

…to unleash the power of the Internet to deliver the best solutions to Canadians at home, in the workplace and on the move

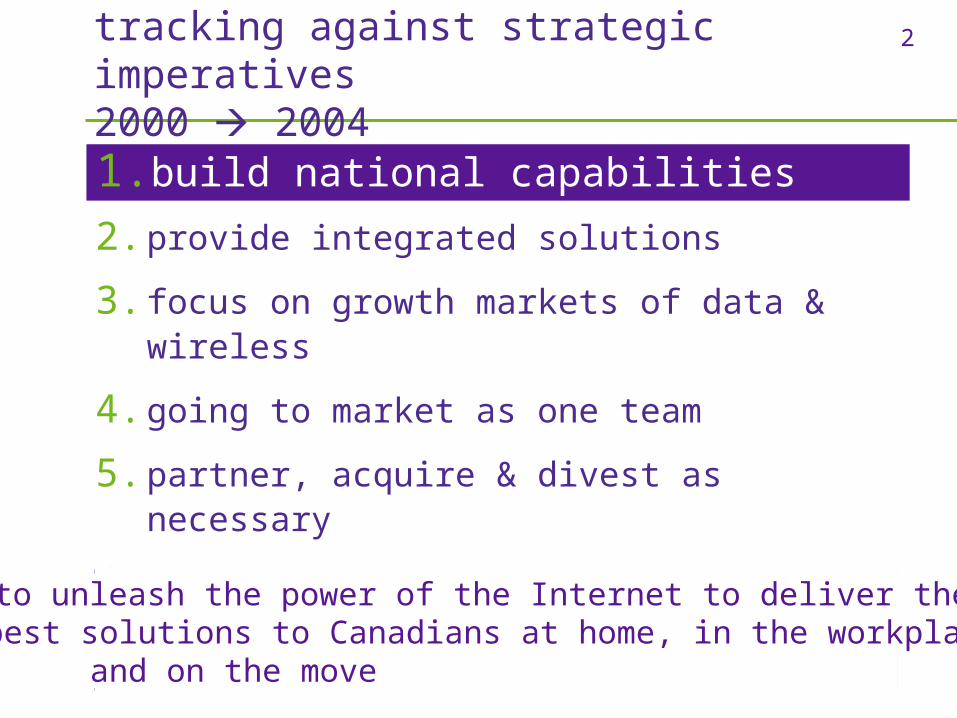

tracking against strategic imperatives2000 2004

1. build national capabilities

2. provide integrated solutions

3. focus on growth markets of data & wireless

4. going to market as one team

5. partner, acquire & divest as necessary

6. invest in internal capabilities

1. build national capabilities

…to unleash the power of the Internet to deliver the best solutions to Canadians at home, in the workplace and on the move

3

383 Ont/Que cities

892 Co-locations

2235 Customer POPs

13,6000 Fibre lit (km)

Next Generation (NGN)Circuit-based Network

TELUSStentor Platform

Mar 2004Jan 2000Communications

NGN delivers enhanced customer data & IP services and operational cost savings

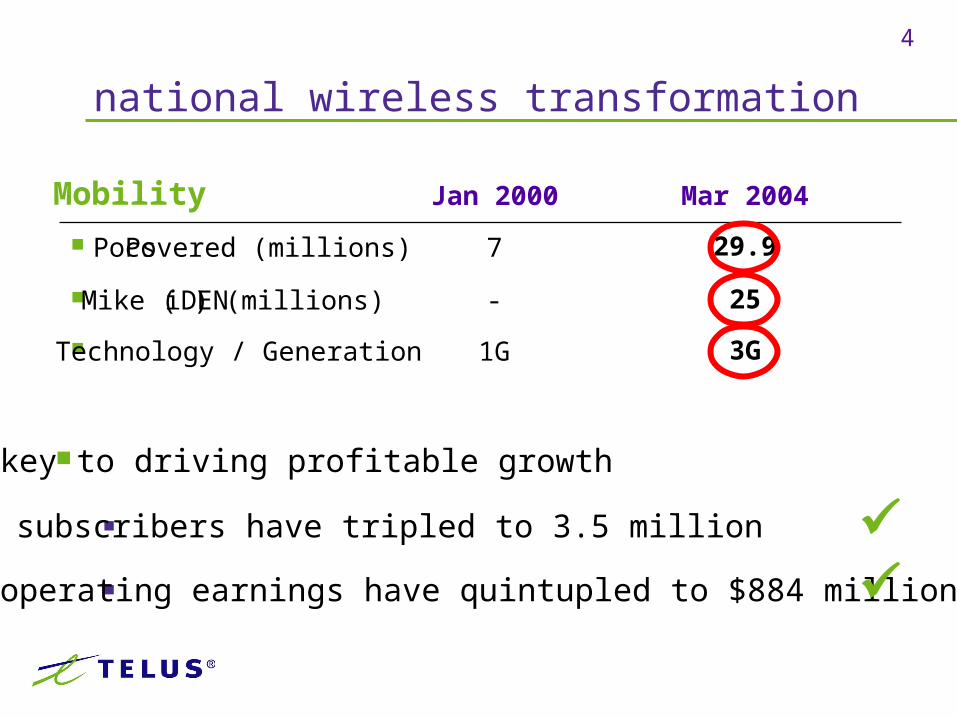

national transformation

4

29.97 PoPs covered (millions)

3G1G Technology / Generation

25- Mike (iDEN) (millions)

Mar 2004Jan 2000Mobility

key to driving profitable growth

subscribers have tripled to 3.5 million operating earnings have quintupled to $884 million

national wireless transformation

5

(18)

21

16

13

8

(2)(3)

(5)(6)

(14)

(2)

1314

2 1

(0.3)

3

Telia FT DT KPN TELUS MTS Telstra Nippon BCE

As at March 1, 2004

Notes: 1 Excluding restructuring TELUS data based on 2002 & 2003 resultsOther results provided by Bloomberg, company, and analyst reports

EBITDA1 % growth rates

BT PSSW Sprint Aliant BLS VZ SBC AT&T

2003 global telecom performance

6

(24)

94

63

29

19 17

4 4 3

(4)

(16)

(0.1)

1 1

20

7

46

TELUS FT Telia DT MTS FON BCE KPN Aliant Nippon BLS Telstra PCCW

Cash Flow (EBITDA1 - Capex) % growth rates

As at March 1, 2004

Notes: 1 Excluding restructuring TELUS data based on 2002 & 2003 resultsOther results provided by Bloomberg, company, and analyst reports

AT&TVZBT

Sprint

SBC

2003 global telecom performance

7

7 7

4 4 3 3

(1)

(6)

(8)

(20)

123

6

0.4

(0.4) (1)TELUS FT DT MTS Sprint Aliant Telstra BCE BT Nippon Telia

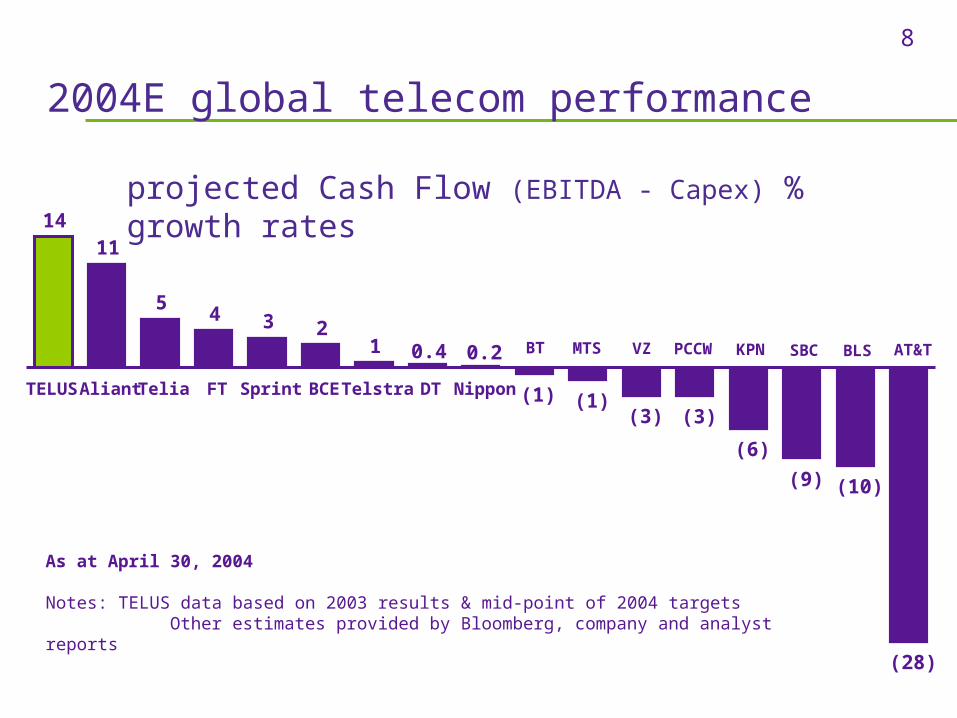

2004E global telecom performance

AT&TBLSSBCPCCWVZ KPN

As at April 30, 2004

Notes: TELUS data based on 2003 results & mid-point of 2004 targets Other estimates provided by Bloomberg, company and analyst reports

projected EBITDA % growth rates

8

1411

4 3 21

(3) (3)

(6)

(9) (10)

(28)

0.2

(1)(1)

0.4

5

TELUS Aliant Telia FT Sprint BCE Telstra DT Nippon

2004E global telecom performance

projected Cash Flow (EBITDA - Capex) % growth rates

As at April 30, 2004

Notes: TELUS data based on 2003 results & mid-point of 2004 targets Other estimates provided by Bloomberg, company and analyst reports

AT&TBLSSBCPCCWVZ KPNMTSBT

9

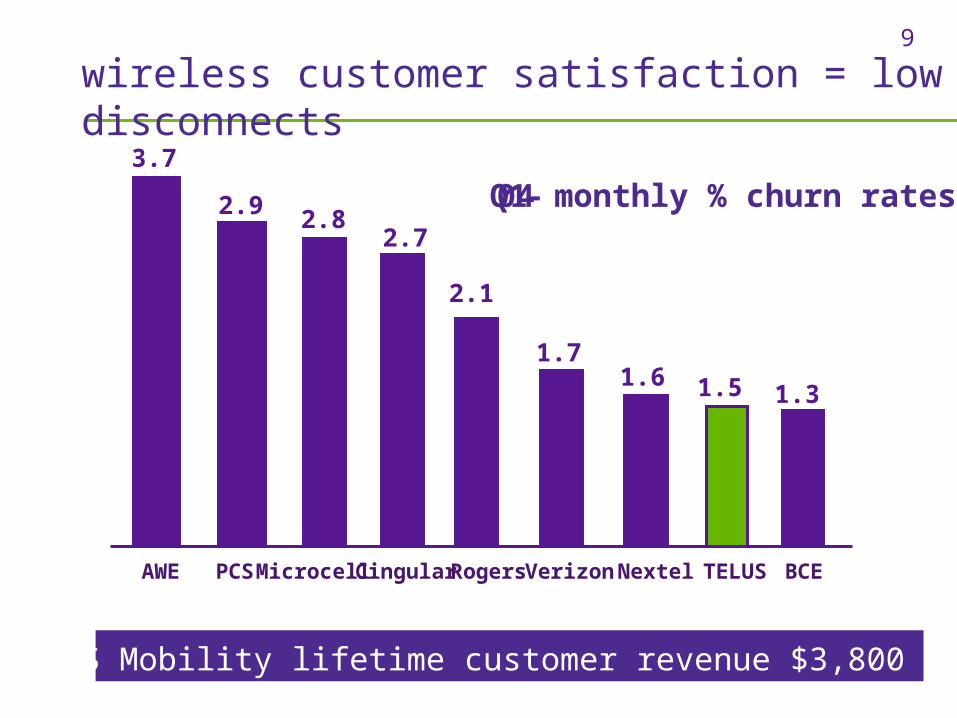

PCS

2.82.7

1.6

2.1

1.71.5 1.3

BCEVerizonCingular Rogers Nextel

3.7

2.9

AWE TELUSMicrocell

TELUS Mobility lifetime customer revenue $3,800

Q1-04 monthly % churn rates

wireless customer satisfaction = low disconnects

10

Exceeded CRTC standard1Service Indicators

Complaints

Directory Services

Local Service

Repair Service

Service Provisioning

1company report on 19 CRTC quality of service indicators and standards for March 2004

TELUS setting new historical records in customer service

customer service improvements

11

challenges in the marketplace

timeliness of decisions market is changing at incredible pace

customers demand benefits of new technologies - like IP - instantly

ability to deliver innovative services tied to timely regulatory decisions

competitors are largely unregulated

turnaround time for decisions must improve

12

challenges in the marketplace

consistent application of policies TELUS & other ILECs invested in infrastructure

based on facilities-based competition policy

subsequent regulatory actions create uncertainty

need to set policy, then stay the course

13

challenges in the marketplace

lost opportunities delay and indecision have a price

deferral account example:

roughly $800 million nationally

CRTC process could add two more years

Broadband Task Force = $1billion to bridge digital divide

TELUS proposal addresses divide

industry & CRTC must work together to change

14

challenges in the marketplace

disruptive nature of VoIP technology VoIP more than new way to deliver POTS

decouples service from underlying transport

multiple VoIP flavours challenge traditional regulatory approaches

business challenge – deliver promise of IP

regulatory challenge – treat all competitors equally

15

a transformation strategy

key performance indicators

focus on essentials

compliance and enforcement

don’t favour or disadvantage particular competitors

adapt to disruptive change

16

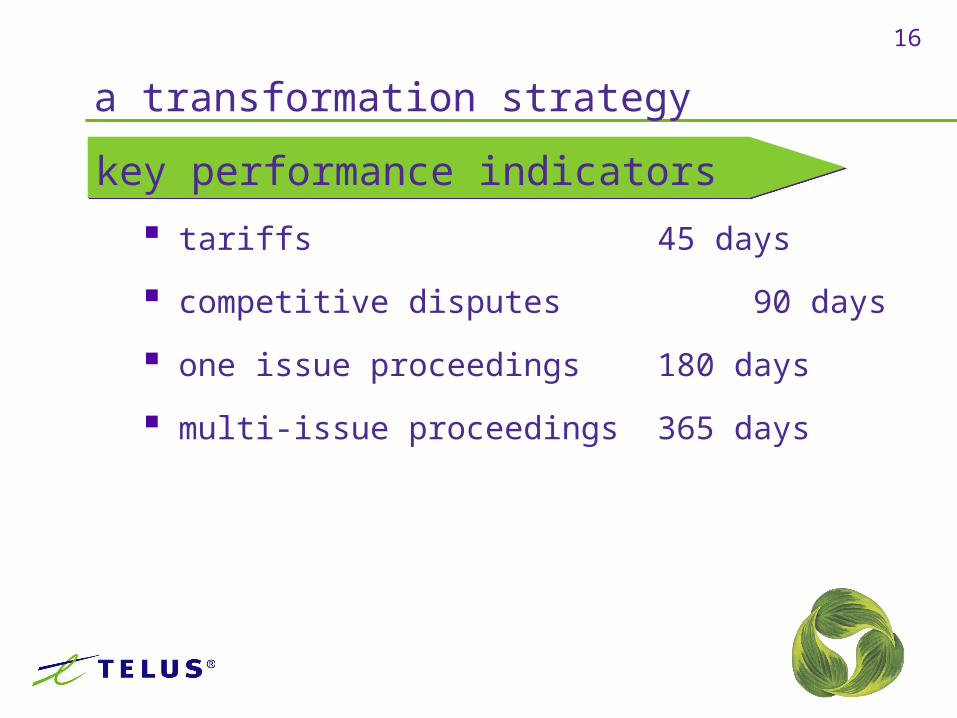

a transformation strategy

key performance indicators

tariffs 45 days

competitive disputes 90 days

one issue proceedings 180 days

multi-issue proceedings 365 days

17

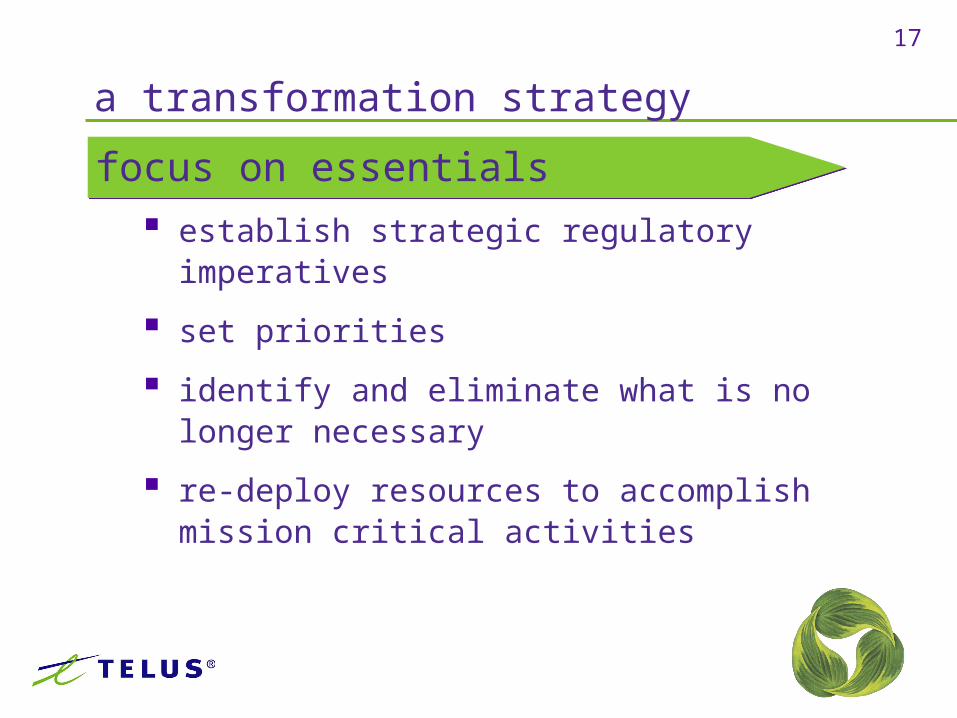

a transformation strategy

focus on essentials

establish strategic regulatory imperatives

set priorities

identify and eliminate what is no longer necessary

re-deploy resources to accomplish mission critical activities

18

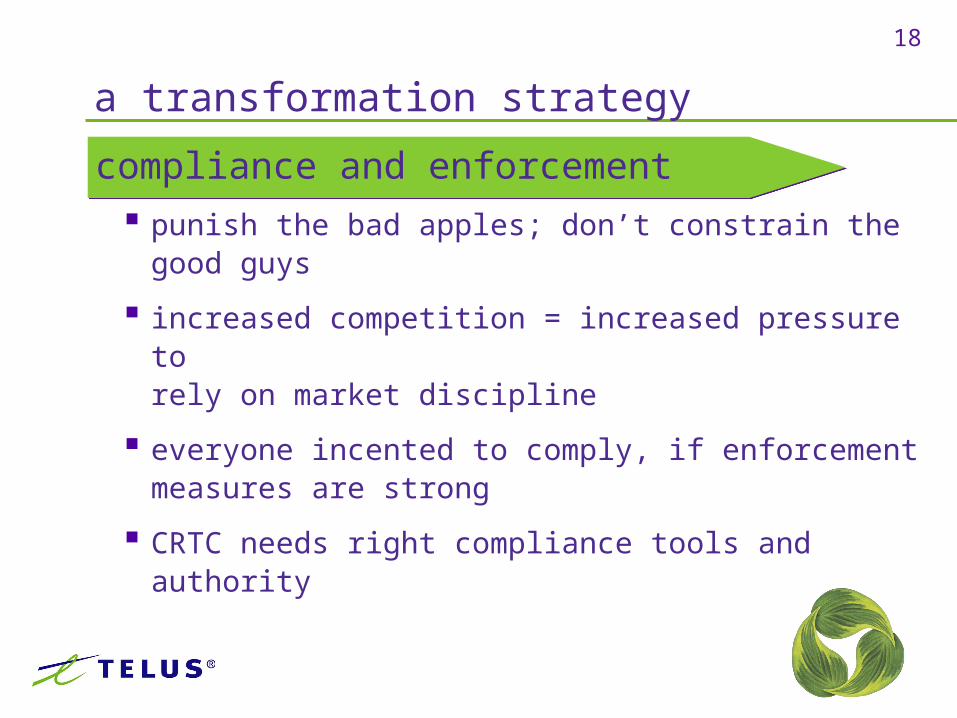

a transformation strategy

compliance and enforcement

punish the bad apples; don’t constrain the good guys

increased competition = increased pressure to rely on market discipline

everyone incented to comply, if enforcement measures are strong

CRTC needs right compliance tools and authority

19

a transformation strategy

don’t favour or disadvantage particular competitors

trend to favour competitors, not competition

undermines sustainable competition

regulatory objective should not be generating regulated margin for our competitors

CLECs don’t need TELUS customers to finance their growth

20

a transformation strategy

adapting to disruptive change

VoIP regulatory framework

VoIP services don’t fit traditional regulatory boxes

CRTC should use wireless approach … did not regulate providers in nascent marketplace

TELUS should be able to compete in VoIP on equal footing with others

21

a transformation strategy

adapting to disruptive change

local market forbearance

time for clarity

what is target market share loss?

consider local telephone service substitutes

competition increasing rapidly; need regulator ready to act

thank you