2.0 big data full report

TRANSCRIPT

Big Data: Building the nextbusiness platform for telecoms

operatorsJulio Puschel, Kris Szaniawski and Paul Lambert

www.informatandm.com

www.informatandm.com © 2013 Informa Telecoms & Media

Copyright

© 2013 Informa UK Ltd.

All rights reserved.The contents of this publication are protected by international copyright laws, database rights and other intellectualproperty rights. The owner of these rights is Informa UK Ltd, our affiliates or other third party licensors. All product andcompany names and logos contained within or appearing on this publication are the trade marks, service marks or tradingnames of their respective owners, including Informa UK Ltd. This publication may not be:-

(a) copied or reproduced; or(b) lent, resold, hired out or otherwise circulated in any way or form without the prior permission of Informa UK Ltd.

Whilst reasonable efforts have been made to ensure that the information and content of this publication was correct asat the date of first publication, neither Informa UK Ltd nor any person engaged or employed by Informa UK Ltd acceptsany liability for any errors, omissions or other inaccuracies. Readers should independently verify any facts and figures asno liability can be accepted in this regard - readers assume full responsibility and risk accordingly for their use of suchinformation and content. Any views and/or opinions expressed in this publication by individual authors or contributors aretheir personal views and/or opinions and do not necessarily reflect the views and/or opinions of Informa UK Limited

www.informatandm.com © 2013 Informa Telecoms & Media

ContentsTelco Big Data: Building a future business platform...................................................... 1

Fig. 1: What is the strategic priority at your organization for the following areas? (Top two options)..................1

Fig. 2: How would you characterize your company type?......................................................................................................... 2

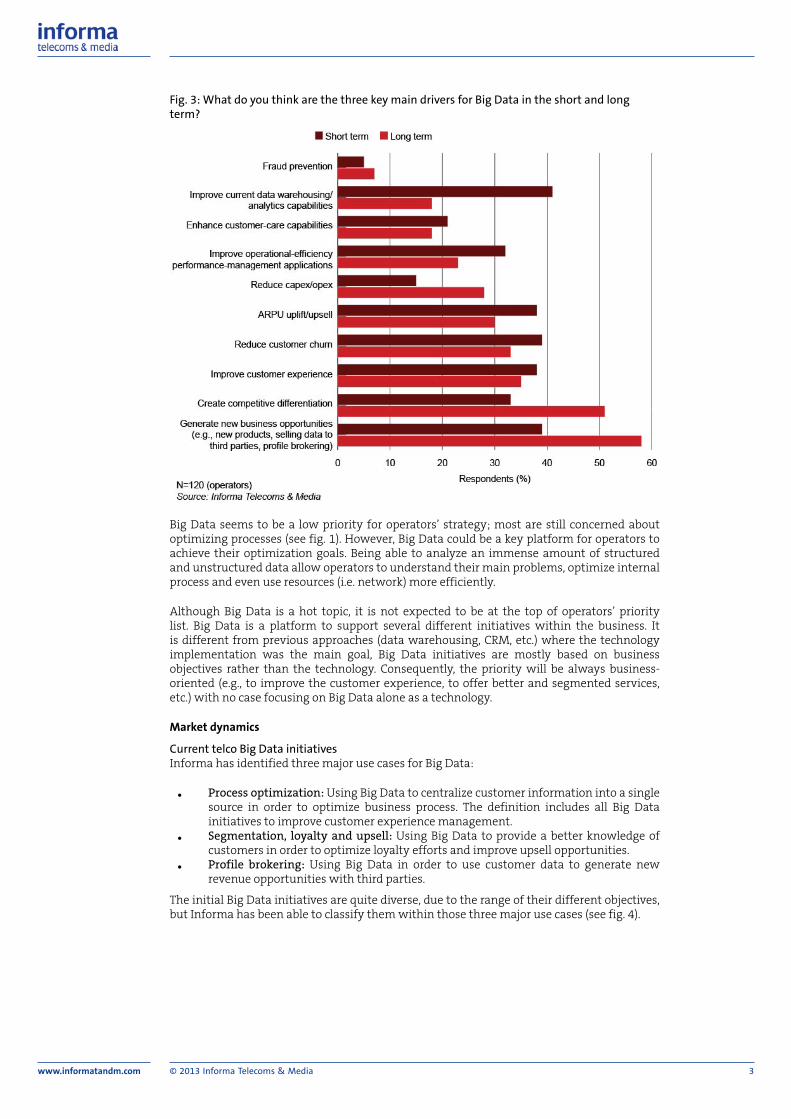

Fig. 3: What do you think are the three key main drivers for Big Data in the short and long term?......................3

Fig. 4: Selected early telco Big Data initiatives................................................................................................................................4

Fig. 5: Is your company currently implementing Big Data?..................................................................................................... 5

Fig. 6: What is the % of your total IT budget is being allocated for Big Data solutions currently, and in threeand five years?................................................................................................................................................................................................ 5

Fig. 7: What type of companies do you believe to be the key partner for operators in Big Dataimplementation?............................................................................................................................................................................................6

Telco Big Data: New tools and strategies........................................................................8

Fig. 1: The 3Vs: The underlying properties that define Big Data............................................................................................ 9

Fig. 2: Potential sources of data...........................................................................................................................................................10

Fig. 3: Big Data analytics use cases....................................................................................................................................................11

Fig. 4: Some of the “Big Data” companies that CSPs claim to be working with currently.........................................14

Fig. 5: Survey question: What type of companies do you believe to be the key partner to operators on BigData................................................................................................................................................................................................................... 15

Telco Big Data: Strategic commitment required before operators can begin to realizethe potential ...................................................................................................................17

Fig. 1: Main approaches to Big Data.................................................................................................................................................18

..............................................................................................................................................................................................................................18

Fig. 2: Types of Big Data..........................................................................................................................................................................18

Fig. 3: What is the main barrier to launching services using Big Data to generate new revenues? (Pleaseselect the top two options)..................................................................................................................................................................... 20

Fig. 4: When do you believe operators will be ready to generate new business opportunities using Big Data?(Please select one option)........................................................................................................................................................................ 21

Fig. 5: What is the most important element to put in place to generate new revenues from Big Data? (Pleaseselect one option)........................................................................................................................................................................................ 22

IT investment: Does it make sense for the CMO to have the power to make thedecisions?.........................................................................................................................24

Who is/are the key influencers and the budget holders/decision makers for Big Data?...........................................24

www.informatandm.com © 2013 Informa Telecoms & Media 1

Telco Big Data: Building a futurebusiness platform02 August 2013Julio Puschel

Executive summary

• The telecoms industry is starting to witness the initial Big Data implementations.Although these first examples are still far from building a solid proposition, they areproviding a good opportunity for operators to test new applications that will influencehow Big Data will evolve in the future.

• Most telco Big Data initiatives are focused on specific business applications, butopportunities in future will demand a broader approach of building a platform forseveral different business needs.

• There is an emerging dynamic vendor competition landscape. The Big Data frameworkis not well defined yet and there are analytics to be found in various areas withinoperators. The expectation is that, as the market evolves, the different vendors willfocus on specific capabilities and collaboration.

Market status

Telecoms operators finally have a good opportunity to generate new business models beyondtraditional connectivity. Internet companies started the concept of Big Data by analyzing anenormous quantity of data in real time to drive business decisions. Telecoms operators alreadycollect thousands of different items of data, including usage, content and location, in theirnetworks and no other industry has its customers interacting with the company 24 hoursa day, seven days a week as telecom operators do with their customers connected to theirnetworks.

However, telecoms operators are still far behind many other industries (e.g., Internet, retailers,etc.) in being able to monetize this opportunity. This is not only due to the complexity of theoperators’ environment relying on various different data sources (e.g., network, BSS/OSS, CRM,customer care, marketing, etc.), but also to their very siloed organization which presents achallenge for an optimized data organization.

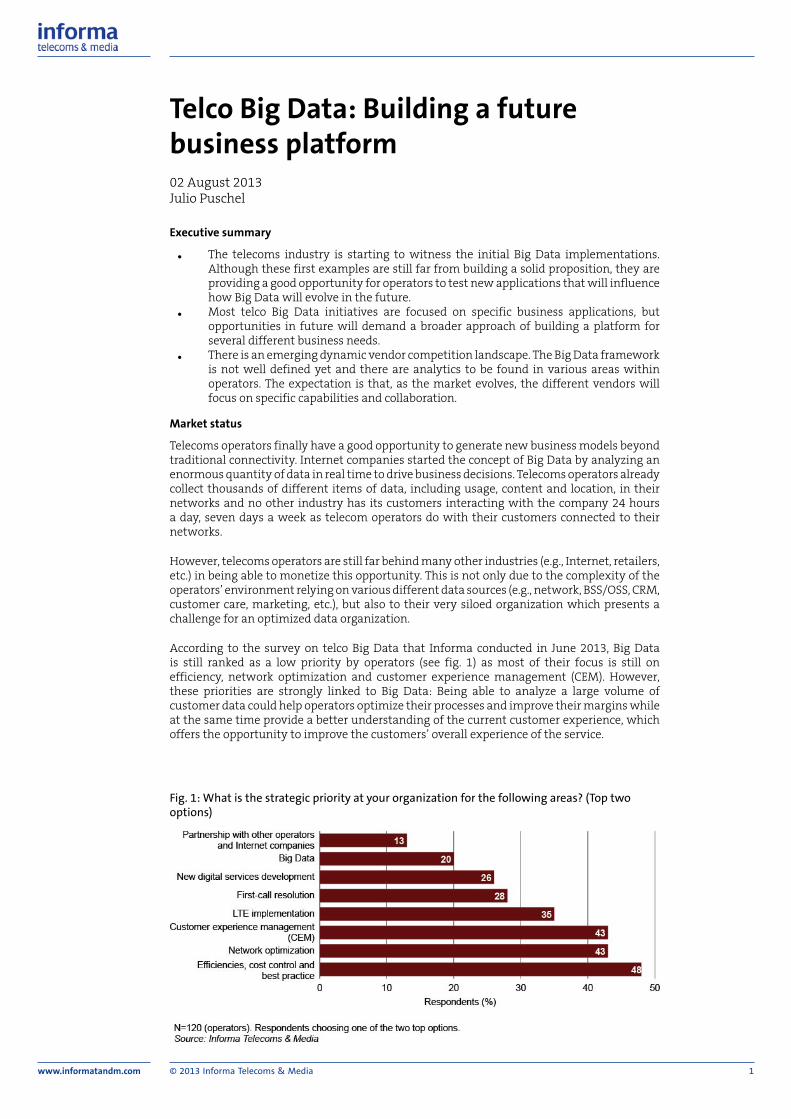

According to the survey on telco Big Data that Informa conducted in June 2013, Big Datais still ranked as a low priority by operators (see fig. 1) as most of their focus is still onefficiency, network optimization and customer experience management (CEM). However,these priorities are strongly linked to Big Data: Being able to analyze a large volume ofcustomer data could help operators optimize their processes and improve their margins whileat the same time provide a better understanding of the current customer experience, whichoffers the opportunity to improve the customers’ overall experience of the service.

Fig. 1: What is the strategic priority at your organization for the following areas? (Top twooptions)

www.informatandm.com © 2013 Informa Telecoms & Media 2

Telco Big Data is still at a very early stage and operators don’t have a full understanding ofthe business opportunities that it can generate. They will need to work on creating specifictangible applications based on the data they are constantly collecting but not currently usingeffectively. These applications will also need to provide concrete business cases for Big Datainitiatives to justify any future investment.

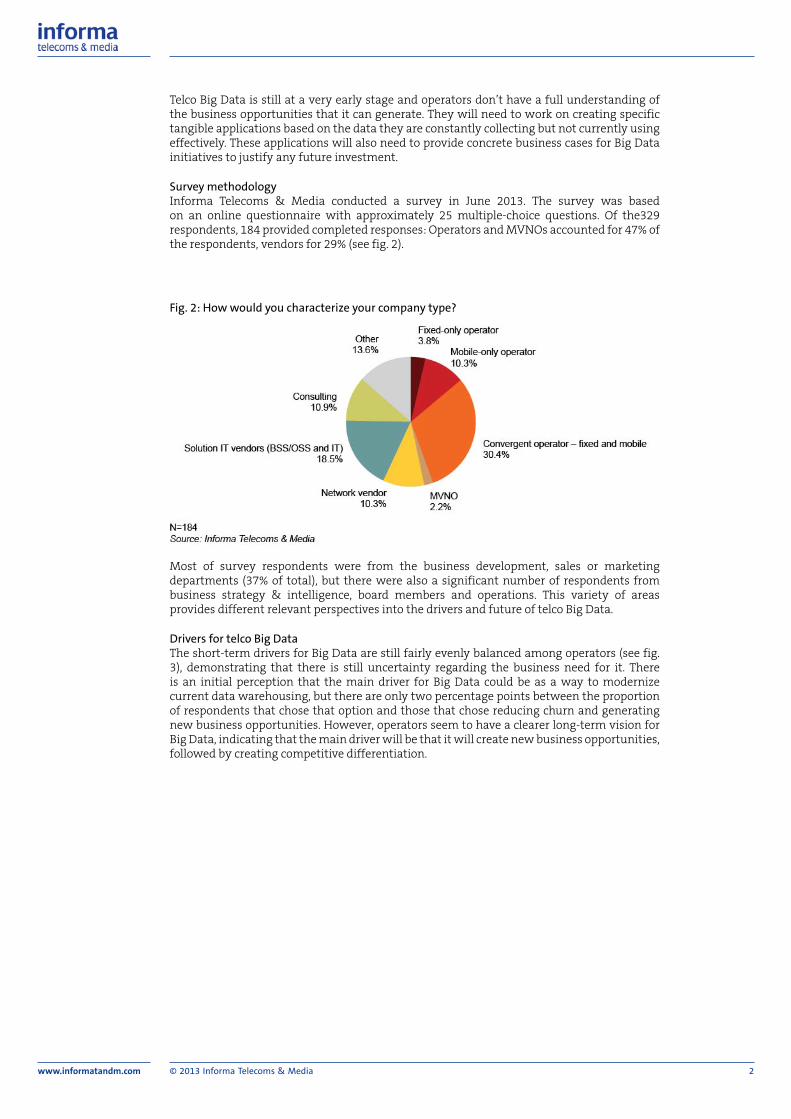

Survey methodologyInforma Telecoms & Media conducted a survey in June 2013. The survey was basedon an online questionnaire with approximately 25 multiple-choice questions. Of the329respondents, 184 provided completed responses: Operators and MVNOs accounted for 47% ofthe respondents, vendors for 29% (see fig. 2).

Fig. 2: How would you characterize your company type?

Most of survey respondents were from the business development, sales or marketingdepartments (37% of total), but there were also a significant number of respondents frombusiness strategy & intelligence, board members and operations. This variety of areasprovides different relevant perspectives into the drivers and future of telco Big Data.

Drivers for telco Big DataThe short-term drivers for Big Data are still fairly evenly balanced among operators (see fig.3), demonstrating that there is still uncertainty regarding the business need for it. Thereis an initial perception that the main driver for Big Data could be as a way to modernizecurrent data warehousing, but there are only two percentage points between the proportionof respondents that chose that option and those that chose reducing churn and generatingnew business opportunities. However, operators seem to have a clearer long-term vision forBig Data, indicating that the main driver will be that it will create new business opportunities,followed by creating competitive differentiation.

www.informatandm.com © 2013 Informa Telecoms & Media 3

Fig. 3: What do you think are the three key main drivers for Big Data in the short and longterm?

Big Data seems to be a low priority for operators’ strategy; most are still concerned aboutoptimizing processes (see fig. 1). However, Big Data could be a key platform for operators toachieve their optimization goals. Being able to analyze an immense amount of structuredand unstructured data allow operators to understand their main problems, optimize internalprocess and even use resources (i.e. network) more efficiently.

Although Big Data is a hot topic, it is not expected to be at the top of operators’ prioritylist. Big Data is a platform to support several different initiatives within the business. Itis different from previous approaches (data warehousing, CRM, etc.) where the technologyimplementation was the main goal, Big Data initiatives are mostly based on businessobjectives rather than the technology. Consequently, the priority will be always business-oriented (e.g., to improve the customer experience, to offer better and segmented services,etc.) with no case focusing on Big Data alone as a technology.

Market dynamics

Current telco Big Data initiativesInforma has identified three major use cases for Big Data:

• Process optimization: Using Big Data to centralize customer information into a singlesource in order to optimize business process. The definition includes all Big Datainitiatives to improve customer experience management.

• Segmentation, loyalty and upsell: Using Big Data to provide a better knowledge ofcustomers in order to optimize loyalty efforts and improve upsell opportunities.

• Profile brokering: Using Big Data in order to use customer data to generate newrevenue opportunities with third parties.

The initial Big Data initiatives are quite diverse, due to the range of their different objectives,but Informa has been able to classify them within those three major use cases (see fig. 4).

www.informatandm.com © 2013 Informa Telecoms & Media 4

Fig. 4: Selected early telco Big Data initiatives

AT&T has started using Big Data to reduce its spending on online advertising. The operatordecided to create its own Demand Side Platform (DSP) to be able to directly negotiate onlineadvertising. With the platform in place, AT&T launched its AdWorks services, which offersan integrated approach (Internet, TV and mobile) for advertising. Therefore, something thatstarted as a way to optimize processes is now a new business area for AT&T.

Furthermore, AT&T is not only investing in the technology to support its AdWorks, but isalso building a platform that can support other future initiatives within its business. Onlineadvertising is just one of many possible Big Data applications and it makes sense to optimizethe investment on a future-proof platform.

Other operators, such as Telefonica, Sprint and Telekom Innovation Laboratories (the centralR&D unit of Telekom), are much more focused on experimenting; they are trying differentbusiness propositions using Big Data. Although these initiatives offer quite relevant examplesof how to generate new opportunities via customer data, they are still far from becominga significant share of operators’ revenues. However, those operators starting now will haveconsiderable advantage by learning the challenges and pitfalls of such initiatives.

Cricket and Telekom Innovation Laboratories are using Big Data to optimize their processesand operations. Telekom Innovation Laboratories is using Big Data to support predictivenetwork capacity modeling while Cricket is using customer usage information to improve thecustomer experience.

Concerns about privacy are present in all the initiatives around the globe, although theycan vary from country to country depending on the regulatory environment. It is still tooearly to say how many of the data privacy challenges will be solved, but operators arefinding alternatives to use anonymized data or offering “opt in” alternatives for some specificcampaigns.

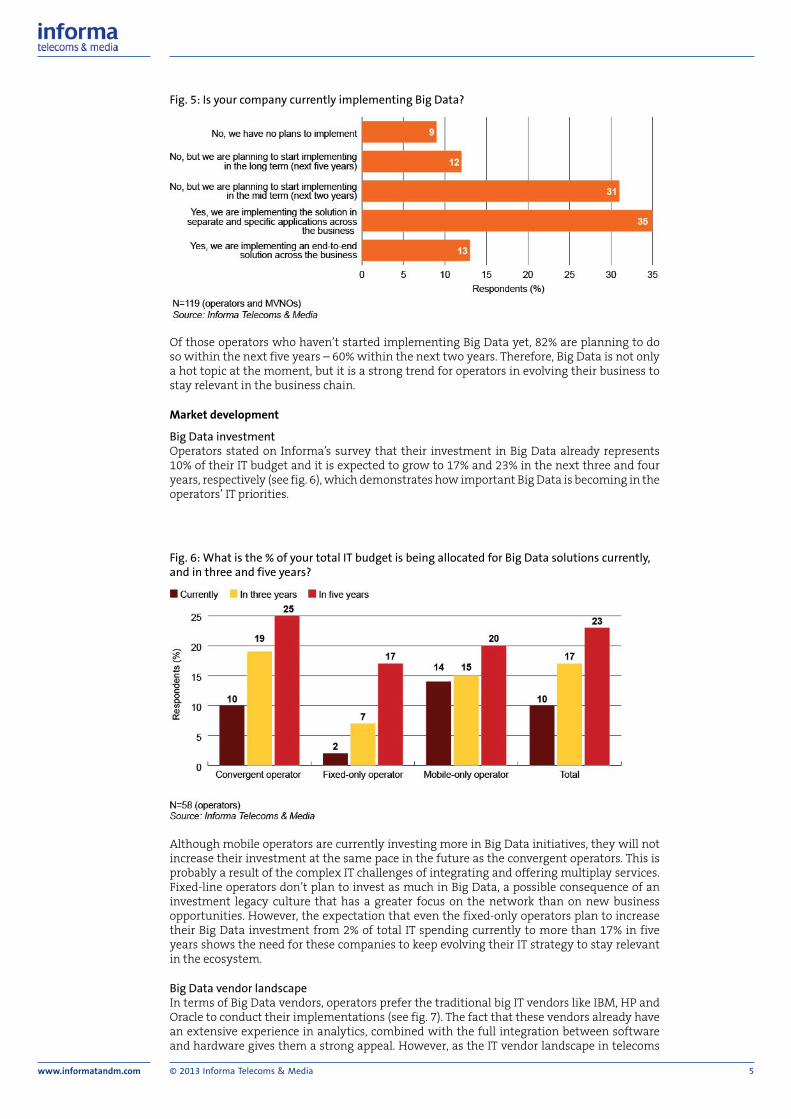

Overall, 48% of operators on our survey are already implementing Big Data (see fig. 5). Of those,72% are implementing separate business applications rather than an end-to-end solution. Asmentioned previously, while it does make sense to focus Big Data implementations on specificbusiness applications, operators also need to consider how they will evolve these initiativesin the future as the business changes.

www.informatandm.com © 2013 Informa Telecoms & Media 5

Fig. 5: Is your company currently implementing Big Data?

Of those operators who haven’t started implementing Big Data yet, 82% are planning to doso within the next five years – 60% within the next two years. Therefore, Big Data is not onlya hot topic at the moment, but it is a strong trend for operators in evolving their business tostay relevant in the business chain.

Market development

Big Data investmentOperators stated on Informa’s survey that their investment in Big Data already represents10% of their IT budget and it is expected to grow to 17% and 23% in the next three and fouryears, respectively (see fig. 6), which demonstrates how important Big Data is becoming in theoperators’ IT priorities.

Fig. 6: What is the % of your total IT budget is being allocated for Big Data solutions currently,and in three and five years?

Although mobile operators are currently investing more in Big Data initiatives, they will notincrease their investment at the same pace in the future as the convergent operators. This isprobably a result of the complex IT challenges of integrating and offering multiplay services.Fixed-line operators don’t plan to invest as much in Big Data, a possible consequence of aninvestment legacy culture that has a greater focus on the network than on new businessopportunities. However, the expectation that even the fixed-only operators plan to increasetheir Big Data investment from 2% of total IT spending currently to more than 17% in fiveyears shows the need for these companies to keep evolving their IT strategy to stay relevantin the ecosystem.

Big Data vendor landscapeIn terms of Big Data vendors, operators prefer the traditional big IT vendors like IBM, HP andOracle to conduct their implementations (see fig. 7). The fact that these vendors already havean extensive experience in analytics, combined with the full integration between softwareand hardware gives them a strong appeal. However, as the IT vendor landscape in telecoms

www.informatandm.com © 2013 Informa Telecoms & Media 6

is very fragmented, Big Data will offer an opportunity to quite a variety of vendors – not justthe traditional IT companies.

Fig. 7: What type of companies do you believe to be the key partner for operators in Big Dataimplementation?

Specific analytics vendors (e.g., SAS, Microsoft and Teradata) have a significant share of thesurvey respondents as many operators are already using some of these companies for anumber of data analytics initiatives. The competition will increase when traditional telecomsnames start to enter the Big Data competition. The new dynamic will be based on:

• BSS/OSS vendors: These companies have already a strong presence in the operators’IT structure, handling a vast quantity of data generated in billing, CRM, ordermanagement, etc. However, although BSS/OSS solutions already encompass someanalytical capabilities, they still need to evolve these capabilities to be able to deal withreal-time analytics of structured and non-structured data.

• Network vendors: As a significant amount of customer data is generated from theoperators’ networks, it is arguable that these vendors have a role in Big Data. Thereis definitely a value coming from network companies as some of them have madecontinuous investment in evolving the BSS/OSS and network integration.

• Start-up solution providers: A number of companies with specific expertise areas areproving quite successful at supporting particular business applications. Companiesthat are working on network intelligence and traffic management will have a relevantrole in Big Data due to their expertise in some areas.

Although telco Big Data still has a hazy competitive landscape with many different type ofcompanies, it will become more clear as Big Data initiatives evolve. It will be difficult to havea single company responsible for an entire Big Data platform; it is more likely to be severalcompanies with different specialties and backgrounds that will be involved in a single project.For example, it is difficult to imagine network vendors competing with traditional IT vendors;it will be more the case of these two types of company being part of a broader framework.

Conclusions and recommendations

ConclusionsTelco Big Data initiatives are still in their very early stages, but it is better to start now thanlater: Most of the operator Big Data examples are based more on experiments than a solidbusiness proposition. However, as Big Data implementations evolve, those players that havediscovered what the challenges and pitfalls are will be a step ahead of competition.

Big Data is much more than a new trendy IT solution, it is about building a platform tosupport not only operational optimization, but also new business initiatives: There is no sucha thing as a Big Data service, it is more about building a platform that will provide operatorswith the opportunity to deploy several business applications to meet internal challenges, suchas customer experience management, and develop new propositions, such as data/profilebrokering.

Although privacy concerns are still an important barrier for Big Data, they are not slowingdown operators’ plans: Restrictions in the use of customer data vary from country to country,

www.informatandm.com © 2013 Informa Telecoms & Media 7

but the first examples will serve as examples to help mould the regulatory frameworkdiscussions in many countries.

Business applications will drive most Big Data initiatives: Business applications that are moretangible to IT are more likely to get the buy-in from the CEO and CFO rather than just relying ona broad and subjective IT trend. However, operators will need to take into consideration howthese business initiatives will evolve within the company and make sure they are investingin future-proof solutions.

The competitive vendor landscape for Big Data is still not very well defined: It will take sometime to vendors to find their role into Big Data implementations. Various types of company(BSS/OSS and traditional IT companies) are expected to compete with each other at the startbut, in the mid to long term, all these different companies will have a role to play, which willrequire more collaboration.

RecommendationsOperators should take a long-term approach when implementing Big Data in orderto support future business initiatives: Business applications will drive most Big Dataimplementations, but operators need to work towards building a platform that can handleboth the specific applications and also the forthcoming business needs and opportunities.

It is about building a platform: Big Data is not a “magic” solution that is going to solve alloperators’ problems, neither is it a service in itself. Big Data is a platform that will allowoperators to use customer data in order to support internal initiatives (CEM, operationalefficiency, etc.) as well as new business models (digital services, profile brokering, etc).

Don’t underestimate the benefits of being an early starter. The experience acquired at thisexperimental stage will make a difference in the future: These first attempts might notgenerate scale or significant additional revenue, but they will be critical to the future successof business applications based on Big Data.

Vendors should focus on their main areas of expertise rather than trying to address thewhole Big Data requirement: Even within analytics, there will be demand for various differentplayers with specific expertise (network, BSS/OSS, policy control, etc). Entering into the moretraditional analytics solution could be a distraction to the core business.

www.informatandm.com © 2013 Informa Telecoms & Media 8

Telco Big Data: New tools andstrategies06 August 2013Kris Szaniawski

Executive summary

• Advanced real-time Big Data processing and analytics tools will deliver real value tooperators but these technologies will complement and extend the more traditionalrelational database-management-system approaches rather than replace them.

• It is as important to focus on instituting better data-governance practices and betterorganization, integration and management of existing data sources as it is on investingin new technologies

• Operators should beware of creating new data silos. Big Data implementations shouldseek to create a platform that is robust enough to allow future cross-functional andcross-departmental expansion.

• Early Big Data projects have struggled to demonstrate a clear impact on value or delivera strong ROI but initial feedback suggests that this may be as much to do with datasilos, unclear objectives and the shortage of skilled staff as the actual tools.

• It is unrealistic to expect each individual Big Data project to have a stand-alonebusiness case. Each project also needs to be viewed as a building block within a largercustomer-centric strategy.

Market status

DefinitionBig Data has multiple facets and meanings.

At one end of the scale, the term “Big Data” has suffered from so much overuse that it has attimes become synonymous with any type of data processing or analytics, with every operatoror vendor claiming to be pursuing a “Big Data strategy” regardless of the tools or data sourcesinvolved.

At the other end of the scale, the term “Big Data” has been linked solely to the processingof huge volumes of semi-structured and unstructured data that is required for social-mediaanalysis, and is specifically associated with the new generation of data processing andanalytics technologies such as NoSQL databases, Hadoop and MapReduce.

The correct definition falls somewhere between the two and there is a particularly strong logicin the telecoms domain to steering a middle path between these two extremes. Big Data doesindeed require the adoption of new approaches to data processing and analytics because thevolume, velocity and variety of data have outgrown the ability of existing systems to captureand analyze it. But the telecoms vertical, more than other sectors, requires a Big Data strategyto incorporate existing sources of structured data as well as legacy analytics platforms anddata processing tools.

For this reason, Informa’s definition of Big Data in the telecoms domain applies not just tounstructured or semi-structured data derived from Internet data, reports on social-mediaactivity or Web-server logs, but also to transactional and operational data stemming frommore traditional telecoms data sources, such as CDRs and network data captured by sensors,and from mediation, CRM or billing systems.

Big Data for communication service providers (CSPs) needs to be not just about mining andanalyzing new categories of data that have until recently been inaccessible to more traditionalbusiness intelligence (BI) and analytics tools but also about identifying links and associationsbetween CSPs’ more structured transactional and operational data sources.

Big Data also needs to be seen in terms of the underlying data properties which are driving anew breed of data storage, processing and analytics systems and strategies:

• Volume: This is the primary attribute of Big Data with operators seeing exponentialrises in the amount of transactional and operational data they need to process inline with exponential growth in customers’ use of IP applications. The data volumes

www.informatandm.com © 2013 Informa Telecoms & Media 9

involved will increasingly involve not just terabytes but petabytes – or even exabytes– of data.

• Velocity: The rise of real-time reporting and data streaming is gaining increasingtraction and as a consequence operators are no longer just processing batch datauploaded at regular intervals for performance management and other functions.

• Variety: The overwhelming majority of this new data is unstructured or complexand this is expected to continue to grow faster than structured data. Structured data(e.g., CDRs) increasingly needs to be complemented with analysis of unstructureddata (text and human language) and semi-structured data (XML, RSS feeds), althoughmultidimensional data will continue to be drawn from a data warehouse to addcontext.

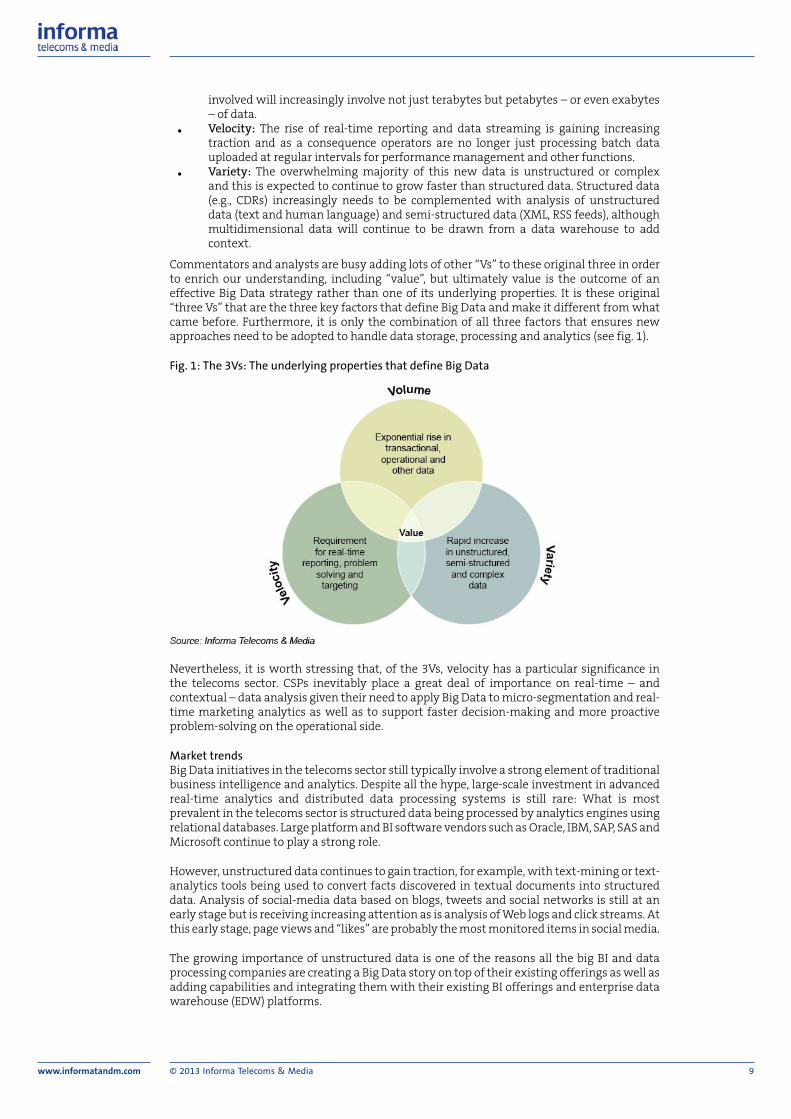

Commentators and analysts are busy adding lots of other “Vs” to these original three in orderto enrich our understanding, including “value”, but ultimately value is the outcome of aneffective Big Data strategy rather than one of its underlying properties. It is these original“three Vs” that are the three key factors that define Big Data and make it different from whatcame before. Furthermore, it is only the combination of all three factors that ensures newapproaches need to be adopted to handle data storage, processing and analytics (see fig. 1).

Fig. 1: The 3Vs: The underlying properties that define Big Data

Nevertheless, it is worth stressing that, of the 3Vs, velocity has a particular significance inthe telecoms sector. CSPs inevitably place a great deal of importance on real-time – andcontextual – data analysis given their need to apply Big Data to micro-segmentation and real-time marketing analytics as well as to support faster decision-making and more proactiveproblem-solving on the operational side.

Market trendsBig Data initiatives in the telecoms sector still typically involve a strong element of traditionalbusiness intelligence and analytics. Despite all the hype, large-scale investment in advancedreal-time analytics and distributed data processing systems is still rare: What is mostprevalent in the telecoms sector is structured data being processed by analytics engines usingrelational databases. Large platform and BI software vendors such as Oracle, IBM, SAP, SAS andMicrosoft continue to play a strong role.

However, unstructured data continues to gain traction, for example, with text-mining or text-analytics tools being used to convert facts discovered in textual documents into structureddata. Analysis of social-media data based on blogs, tweets and social networks is still at anearly stage but is receiving increasing attention as is analysis of Web logs and click streams. Atthis early stage, page views and “likes” are probably the most monitored items in social media.

The growing importance of unstructured data is one of the reasons all the big BI and dataprocessing companies are creating a Big Data story on top of their existing offerings as well asadding capabilities and integrating them with their existing BI offerings and enterprise datawarehouse (EDW) platforms.

www.informatandm.com © 2013 Informa Telecoms & Media 10

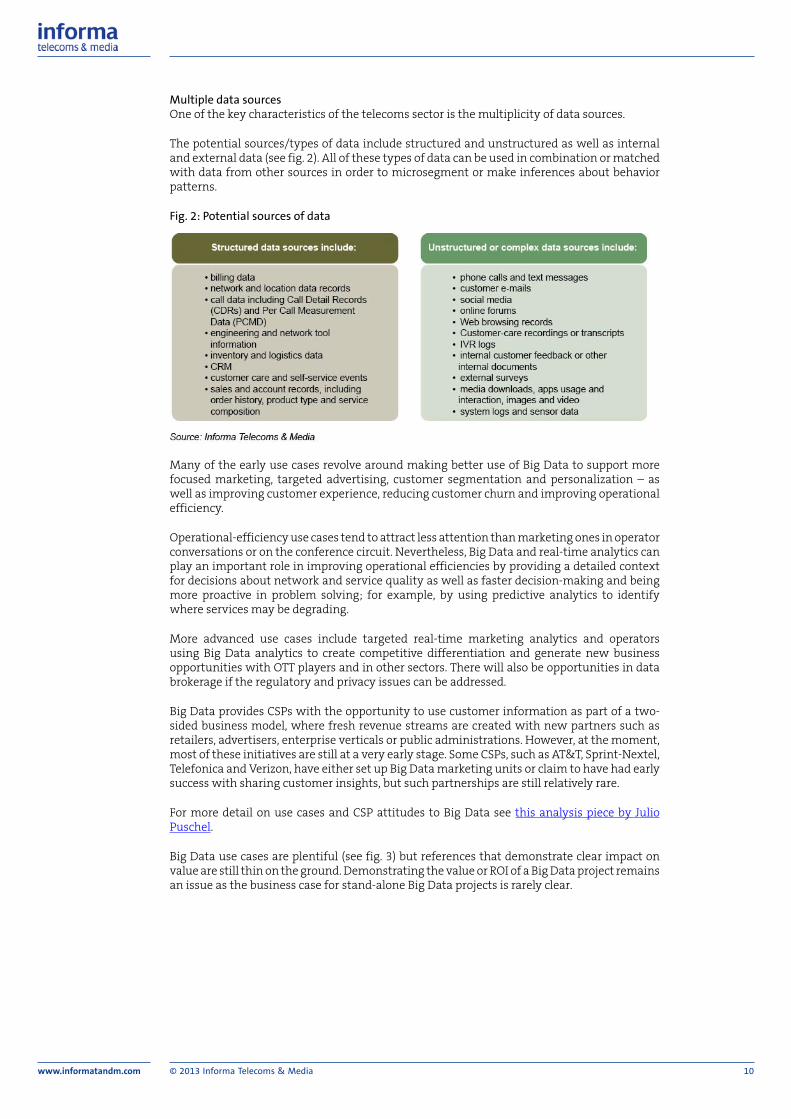

Multiple data sourcesOne of the key characteristics of the telecoms sector is the multiplicity of data sources.

The potential sources/types of data include structured and unstructured as well as internaland external data (see fig. 2). All of these types of data can be used in combination or matchedwith data from other sources in order to microsegment or make inferences about behaviorpatterns.

Fig. 2: Potential sources of data

Many of the early use cases revolve around making better use of Big Data to support morefocused marketing, targeted advertising, customer segmentation and personalization – aswell as improving customer experience, reducing customer churn and improving operationalefficiency.

Operational-efficiency use cases tend to attract less attention than marketing ones in operatorconversations or on the conference circuit. Nevertheless, Big Data and real-time analytics canplay an important role in improving operational efficiencies by providing a detailed contextfor decisions about network and service quality as well as faster decision-making and beingmore proactive in problem solving; for example, by using predictive analytics to identifywhere services may be degrading.

More advanced use cases include targeted real-time marketing analytics and operatorsusing Big Data analytics to create competitive differentiation and generate new businessopportunities with OTT players and in other sectors. There will also be opportunities in databrokerage if the regulatory and privacy issues can be addressed.

Big Data provides CSPs with the opportunity to use customer information as part of a two-sided business model, where fresh revenue streams are created with new partners such asretailers, advertisers, enterprise verticals or public administrations. However, at the moment,most of these initiatives are still at a very early stage. Some CSPs, such as AT&T, Sprint-Nextel,Telefonica and Verizon, have either set up Big Data marketing units or claim to have had earlysuccess with sharing customer insights, but such partnerships are still relatively rare.

For more detail on use cases and CSP attitudes to Big Data see this analysis piece by JulioPuschel.

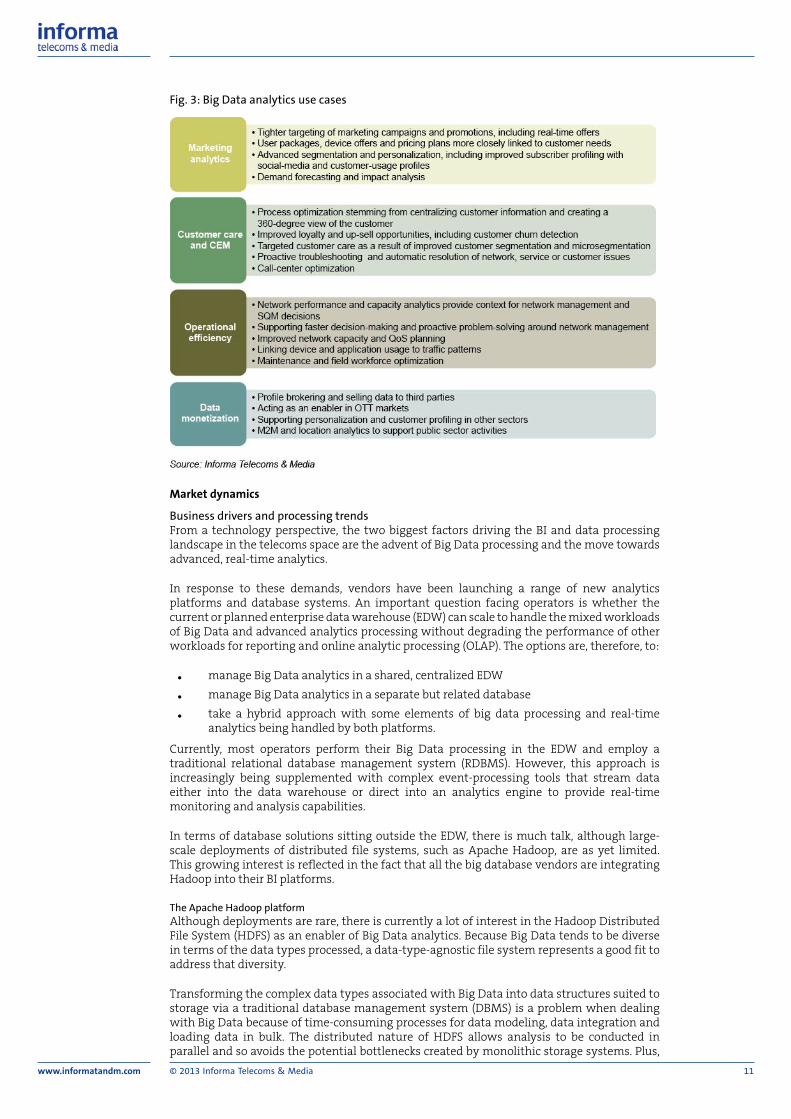

Big Data use cases are plentiful (see fig. 3) but references that demonstrate clear impact onvalue are still thin on the ground. Demonstrating the value or ROI of a Big Data project remainsan issue as the business case for stand-alone Big Data projects is rarely clear.

www.informatandm.com © 2013 Informa Telecoms & Media 11

Fig. 3: Big Data analytics use cases

Market dynamics

Business drivers and processing trendsFrom a technology perspective, the two biggest factors driving the BI and data processinglandscape in the telecoms space are the advent of Big Data processing and the move towardsadvanced, real-time analytics.

In response to these demands, vendors have been launching a range of new analyticsplatforms and database systems. An important question facing operators is whether thecurrent or planned enterprise data warehouse (EDW) can scale to handle the mixed workloadsof Big Data and advanced analytics processing without degrading the performance of otherworkloads for reporting and online analytic processing (OLAP). The options are, therefore, to:

• manage Big Data analytics in a shared, centralized EDW

• manage Big Data analytics in a separate but related database

• take a hybrid approach with some elements of big data processing and real-timeanalytics being handled by both platforms.

Currently, most operators perform their Big Data processing in the EDW and employ atraditional relational database management system (RDBMS). However, this approach isincreasingly being supplemented with complex event-processing tools that stream dataeither into the data warehouse or direct into an analytics engine to provide real-timemonitoring and analysis capabilities.

In terms of database solutions sitting outside the EDW, there is much talk, although large-scale deployments of distributed file systems, such as Apache Hadoop, are as yet limited.This growing interest is reflected in the fact that all the big database vendors are integratingHadoop into their BI platforms.

The Apache Hadoop platformAlthough deployments are rare, there is currently a lot of interest in the Hadoop DistributedFile System (HDFS) as an enabler of Big Data analytics. Because Big Data tends to be diversein terms of the data types processed, a data-type-agnostic file system represents a good fit toaddress that diversity.

Transforming the complex data types associated with Big Data into data structures suited tostorage via a traditional database management system (DBMS) is a problem when dealingwith Big Data because of time-consuming processes for data modeling, data integration andloading data in bulk. The distributed nature of HDFS allows analysis to be conducted inparallel and so avoids the potential bottlenecks created by monolithic storage systems. Plus,

www.informatandm.com © 2013 Informa Telecoms & Media 12

transforming data into structures suitable for storage via traditional DBMS could potentiallylose the data details and anomalies that fuel some forms of analytics.

Nevertheless, a number of deployment models are currently being considered. One involvesusing Hadoop as a separate database from the EDW to process and run analytics onunstructured data from social media and Web logs while the EDW is used to process structureddata from traditional mediation platforms. The issue here is that this approach creates silosof data with multiple versions of the truth. Another approach is to use Hadoop as a staginglayer where it performs preprocessing, filtering and transforming of semi-structured andunstructured data for loading into a data warehouse.

Although Hadoop can be used on both structured and unstructured data, at the moment it isnot typically being used for analyzing conventional structured data such as transaction data,customer information and call records, where traditional RDBMS tools are still better adapted.Instead, Hadoop currently appears to be used mainly for storage or as a staging layer; forexample, being used as “Hadoop ETL” (Extract, Transform and Load) to preprocess, filter andtransform vast quantities of semi-structured and unstructured data for loading into a datawarehouse.

Distributed file systems such as Hadoop should not be viewed as a substitute but rather as acomplement to traditional RDBMS platforms as they are particularly suited to processing theunstructured data required in social-media analysis.

HDFS is particularly valuable in that it is scalable and fault-tolerant. In a distributed filesystem, if one node goes down, then other nodes in the cluster can be used. The scalability andresilience comes from the combination of the clustered storage capabilities of HDFS and thefault-tolerant distributed processing of MapReduce, a programming model closely associatedwith distributed file systems like Hadoop and designed to process large datasets stored inclusters.

Operator challenges and Big Data inhibitorsDepending on their existing infrastructure, operators are faced with either optimizing andupgrading their current architecture or investing in new technology such as the Hadoop-based systems mentioned above.

There are potential drawbacks to either approach.

Legacy BI and EDW assets have the advantage of scalability and processing speed, but inmany organizations these technologies have been designed and optimized for reporting,performance management and OLAP. This optimization is invaluable for big-picture orenterprise-wide reports but is often less well-suited to advanced analytics and Big Dataprocesses.

New technologies that are based on distributed file systems and which sit outside of theEDW are better-suited for processing unstructured or semi-structured data. But they also havepotential drawbacks – not just the lack of a compelling business case (as mentioned earlier),but also:

• human/organizational issues

• time and cost concerns

• integration issues.

Other concerns, such as those around security, privacy and regulatory issues, straddle bothapproaches.

Human/organizational issuesPeople and process are typically quoted as contributors when major data projects have failedto deliver. Big Data, and the value around it, is not just about technology. If projects focus onlyon new technology, they are unlikely to deliver significant change.

CSPs that have undergone Big Data projects stress the importance of the human aspect ofthe projects and the need to reorganize and restructure the business, IT, customer care andmarketing teams. New processes and structures are as important as the technology.

A lack of sufficiently skilled IT and analytics staff is also an issue given the novel natureof Big Data and the fact that so many disparate sectors suddenly want to hire people with

www.informatandm.com © 2013 Informa Telecoms & Media 13

data analytics expertise. Skills shortages have been an issue with regards to data scientists,programmers, modelers and analysts. However, some of this pressure may ease as moreautomation and simpler user interfaces are introduced.

Time and cost concernsSetting up Hadoop can be complex and time-consuming. Although this is not always the case,the length of time it takes to implement an individual Hadoop project can vary from a fewweeks to several months or more, depending on the complexity of the project. There herehave been implementation failures and as is the case with all new technologies there is thepotential a backlash.

Big Data projects are also rarely a one-off investment with a fixed start and end point. Giventhe nature of such projects, involving multiple data sources and cross-organizational groups, itis inevitable that such projects proceed on a step-by-step basis. However, such an incrementalapproach, using a Big Data platform to support multiple initiatives, can make it difficultto convince senior management given that they typically demand a clear and immediatebusiness case.

Integration issuesData quality and integration issues are also a key concern. As a consequence data integrationis one of the big challenges when it comes to achieving success with Big Data and analyticsimplementations.

The data integration capabilities of vendors are typically cited as important criteria whendeciding who to go with for an implementation. CSPs typically have a legacy of multiplesystems and databases serving different departments and functions and supporting multipleproducts and services. Addressing these fragmented data sources and structures is far fromeasy. As a consequence it is not just the integration tools that large IT providers offer that areattractive but also their data integration and management skills.

There may be low-hanging fruit that can be targeted with a Big Data implementation but togain maximum value from Big Data it is better to deal with data in an integrated and holisticmanner rather than risk creating yet more data silos. A single view of the customer is crucial.For more on this, see this analysis piece on CEM.

Market development

As mentioned earlier, the adoption of Big Data processing and advanced real-time analyticsin the telecoms sector is still not that common. For example, at Big Data conferences andevents focused on the telecoms sector, the case studies and projects discussed by delegatestypically focus on more traditional BI or analytics approaches rather than on Apache Hadoopimplementation.

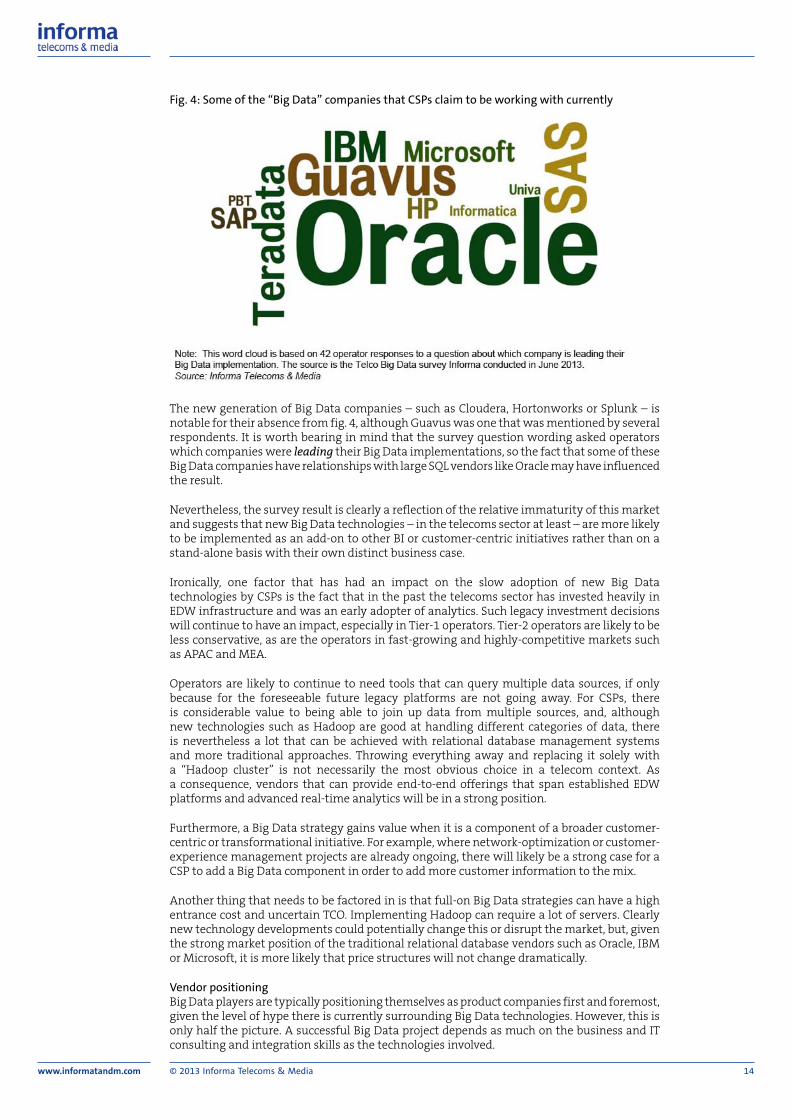

A global Telco Big Data survey that Informa conducted in June 2013 also reinforces thismessage. Just under half of the 159 operator respondents claimed to be implementing a BigData solution currently. Furthermore, the types of companies survey respondents claimedto be working with currently (see fig. 4) suggests that what operators label as “Big Data”implementations are as often as not variations on traditional BI and data-warehousingstrategies rather than a full-on adoption of a Big Data strategy based on distributed filesystems and advanced real-time analytics.

www.informatandm.com © 2013 Informa Telecoms & Media 14

Fig. 4: Some of the “Big Data” companies that CSPs claim to be working with currently

The new generation of Big Data companies – such as Cloudera, Hortonworks or Splunk – isnotable for their absence from fig. 4, although Guavus was one that was mentioned by severalrespondents. It is worth bearing in mind that the survey question wording asked operatorswhich companies were leading their Big Data implementations, so the fact that some of theseBig Data companies have relationships with large SQL vendors like Oracle may have influencedthe result.

Nevertheless, the survey result is clearly a reflection of the relative immaturity of this marketand suggests that new Big Data technologies – in the telecoms sector at least – are more likelyto be implemented as an add-on to other BI or customer-centric initiatives rather than on astand-alone basis with their own distinct business case.

Ironically, one factor that has had an impact on the slow adoption of new Big Datatechnologies by CSPs is the fact that in the past the telecoms sector has invested heavily inEDW infrastructure and was an early adopter of analytics. Such legacy investment decisionswill continue to have an impact, especially in Tier-1 operators. Tier-2 operators are likely to beless conservative, as are the operators in fast-growing and highly-competitive markets suchas APAC and MEA.

Operators are likely to continue to need tools that can query multiple data sources, if onlybecause for the foreseeable future legacy platforms are not going away. For CSPs, thereis considerable value to being able to join up data from multiple sources, and, althoughnew technologies such as Hadoop are good at handling different categories of data, thereis nevertheless a lot that can be achieved with relational database management systemsand more traditional approaches. Throwing everything away and replacing it solely witha “Hadoop cluster” is not necessarily the most obvious choice in a telecom context. Asa consequence, vendors that can provide end-to-end offerings that span established EDWplatforms and advanced real-time analytics will be in a strong position.

Furthermore, a Big Data strategy gains value when it is a component of a broader customer-centric or transformational initiative. For example, where network-optimization or customer-experience management projects are already ongoing, there will likely be a strong case for aCSP to add a Big Data component in order to add more customer information to the mix.

Another thing that needs to be factored in is that full-on Big Data strategies can have a highentrance cost and uncertain TCO. Implementing Hadoop can require a lot of servers. Clearlynew technology developments could potentially change this or disrupt the market, but, giventhe strong market position of the traditional relational database vendors such as Oracle, IBMor Microsoft, it is more likely that price structures will not change dramatically.

Vendor positioningBig Data players are typically positioning themselves as product companies first and foremost,given the level of hype there is currently surrounding Big Data technologies. However, this isonly half the picture. A successful Big Data project depends as much on the business and ITconsulting and integration skills as the technologies involved.

www.informatandm.com © 2013 Informa Telecoms & Media 15

It is on the services side that much of the business value and cost will reside, as is often thecase when complex software is involved. Given the importance of the data-integration issuesmentioned earlier, as well as the incremental and ongoing nature of Big Data projects, it isinevitable that strong consulting, business process and integration capabilities, as well as theability to provide different types of data-related services and support, will all be importantdifferentiators for vendors.

For this reason, big IT solution providers such as IBM, Microsoft and Oracle are well-positionedto maintain a strong position in this space, as are any companies that can combine IT andanalytics expertise with strong consulting and transformational skills.

This message is driven home by the answer to a partnership question asked in the Telco BigData survey (see fig. 5).

Fig. 5: Survey question: What type of companies do you believe to be the key partner tooperators on Big Data

When asked which companies they believed were the strongest partners for a Big Dataimplementation, the largest number of CSP respondents (37%) chose big IT solution providers,such as IBM, HP, Microsoft or Oracle. The second most popular category (24%) was specificanalytics providers, such as SAS, Microsoft or Teradata. The third most popular category (17%)was start up solution providers such as Guavus or Hadapt. Network and support systemvendors scored lower.

However, it is worth pointing out that the survey question was a broad-brush one as itasked respondents what single category of company would play the key role in a Big Dataengagement. In the real world, the picture will be a more complicated one with CSPsworking with multiple suppliers and opportunities for companies from different parts of theecosystem to work with each other.

One example of this type of arrangement is the recently-announced relationship betweenIBM and China-based telecom IT provider AsiaInfo-Linkage. The latter’s Big Data offering,Veris Convergent Context-awareness Center (C³), has IBM’s Netezza-powered PureData forAnalytics technology embedded in it and is already being deployed by China Mobile fortargeted marketing and customer insight purposes.

Conclusions and recommendations

Conclusions

The telecoms Big Data market is still relatively immature and CSP goals need to reflect thisThe telecoms Big Data market is still relatively immature and, although everyone is talkingabout “Big Data”, the typical reality on the ground is structured data being processedby analytics engines using more traditional relational databases rather than Big Datatechnologies such as Hadoop. Hence, the initial steps need to be as much around institutingbetter data-governance practices and better organization, integration and management ofexisting data sources. In the medium to long term, advanced Big Data processing and analyticstools will be required if operators are to get to grips with disparate data sources and usethem fully but Big Data technologies will complement and extend more traditional relationaldatabase management system (RDMS) approaches rather than replace them.

www.informatandm.com © 2013 Informa Telecoms & Media 16

Beware of creating new silosIn an ideal world, Big Data projects would be implemented as one component within abroader transformational or customer-centric project because there are clear synergies withany strategies that seek to improve agility, optimization or customer experience management.But the reality is that the majority of Big Data project implementations are – and willcontinue to be – driven by specific business needs and applications. Stand-alone Big Dataimplementations may predominate initially but that should be no excuse for creating yetanother set of data silos. Big Data implementations should seek to create a platform that isscalable, extensible and future-proofed as much as possible as well as robust enough to allowfuture cross-functional and cross-departmental expansion.

Big Data is as much about processes and organizational issues as it is about technologyBig Data is as much about people and processes as it is about technology and it is theseorganizational issues that need to be sorted out in the first instance. Some of the early Big Dataprojects have struggled to demonstrate a clear impact on value or deliver a strong return oninvestment (ROI) but initial feedback suggests that this may be as much to do with data silosand the shortage of skilled staff as the actual tools. With this in mind, CSPs need to put theirown house in order before pushing ahead with more sophisticated business models involvingthird parties.

Recommendations

CSPs should not get too hung up about quantifying the value of stand-alone projectsIt can be counterproductive to focus exclusively on the ROI on individual Big Data projectswithout taking into account the bigger picture. An incremental approach to Big Dataclearly still requires each individual project to deliver a measurable outcome, however small,otherwise no project would ever get approved. But it is unrealistic to expect each individual BigData project to have a stand-alone business case. Each individual project needs to be seen asa building block within a larger customer-centric strategy and it is this which will ultimatelydeliver ROI.

Start with simple analysis and get that right first before moving onTo achieve success, CSPs need to keep their project goals focused on relatively straightforwardbusiness requirements. CSPs should take an incremental approach both to projects andimplementation and also to what they are seeking to achieve. It makes sense to start withsimple analysis to investigate key usage trends or understand critical demographic segmentsbefore moving on to advanced modelling or predictive analytics. Given most CSPs’ relativelylow starting-point, a lot can be achieved by applying simple experiments to customer care,revenue management or segmentation. It makes more sense for CSPs to refine and build onsuch achievements gradually rather than experiment blindly.

Technology can only provide a temporary competitive advantage for vendorsVendors need to focus on creating strong professional services, integration and processcapabilities if they wish to succeed in the Big Data space. Much of the revenue opportunityin this space is around services rather than just products and this is also where a lot ofthe differentiation will reside. Collaboration and partnership – or acquisition – can deliveradditional components of a BI and data-analytics offering, whereas strong professionalservices, integration and process capabilities are more difficult to match.

Further reading

• Telco Big Data: Building a future business platform

• Why operators need CEM, customer intelligence and analytics

www.informatandm.com © 2013 Informa Telecoms & Media 17

Telco Big Data: Strategic commitmentrequired before operators can begin torealize the potential09 August 2013Paul Lambert

Executive summary

• A handful of operators are in the early stages of exploring the business opportunitiesaround Big Data, in particular high-velocity, real-time data use. The market is not neara tipping point, but when an operator sees tangible benefit from an initiative that usesBig Data, the market will follow.

• Operators need a genuine C-level commitment to Big Data if they want to begin toexplore the opportunity in a coherent manner. Vendors are pitching the maturity ofthe technologies that will enable Big Data projects, but operators in general are not yetready to commit to make the necessary investments in the absence of proven ROI.

• Because the business case has yet to be proven, the vast majority of operatorshave a wait-and-see approach to Big Data, despite the fact that operators are underpressure to create new revenue from other sources. The main questions for an operatorcommitted to monetizing Big Data are: what are the main areas ripe for investmentand strategic commitment; and who will maximize opportunities around it?

• Operators lack vertical-industry knowledge. So they need to form partnerships to gainaccess to the specific vertical-industry expertise that they need to build the necessaryinfrastructure to use their Big Data assets. In creating partnerships, operators needto prove that they are effective partners and that their Big Data assets will createnew value to companies in other sectors as they will often be new to partnering withtelecoms companies.

• Regulation covering Big Data is hampering operators in two ways: regulation on amarket-by-market basis is often out of step with the operators’ technical capabilityand strategic intent; and inconsistent regulation between countries and withinregions.

• Regulation needs to evolve to meet consumers’ expectations on privacy and use ofdata, and also provide operators with a clearly defined framework within which theycan explore the Big Data opportunity.

Market status

It’s a widely held view that operators have more information about their subscribers thanInternet companies do but Internet companies are better placed to monetize this informationthan operators. While Internet companies are not necessarily uniquely positioned in the areaof Big Data, they are 100% focused on creating value from its data. Although this is certainlythe case at the moment, operators are now beginning to explore ways they can use the datatheir subscribers generate in conjunction with their direct-billing relationships as an asset tocreate new revenues away from their core voice and data-access revenues.

But as operators eye this new metric, average revenue from other sources (AROS), thechallenges they face touch the core strategic challenges they face in general: identifying newbusiness opportunities with an entrepreneurial mindset and positioning themselves to takeadvantage of them, often through partnerships.

While there are clearly defined opportunities in the area of “Big Data”, how these opportunitiescan be realized in practice remains unclear. Regulatory hurdles, questions over end-useracceptance of allowing their data to be used in new ways, and the current lack of a clear visionof the concrete business opportunities available to operators in this area mean that Big Datais very much uncharted territory. However, some operators are focused on exploring theseopportunities, despite these uncertainties, and are exploring different emerging businessmodels to begin to capitalize on the potential of Big Data.

A growing number of operators, in particular the large multinational players, are looking attheir data assets in the following ways:

• How can we store and structure it?

www.informatandm.com © 2013 Informa Telecoms & Media 18

• How can we investigate the value of it?

• How can we use it to improve customer experience and to optimize customerinteractions?

• How can we use Big Data to drive AROS?

An analysis of the technical-strategic considerations related to these finds that Big Dataimplementations should seek to create a platform that is scalable, extensible and future-proofed as much as possible – as well as robust enough to allow future cross-functional andcross-departmental expansion.

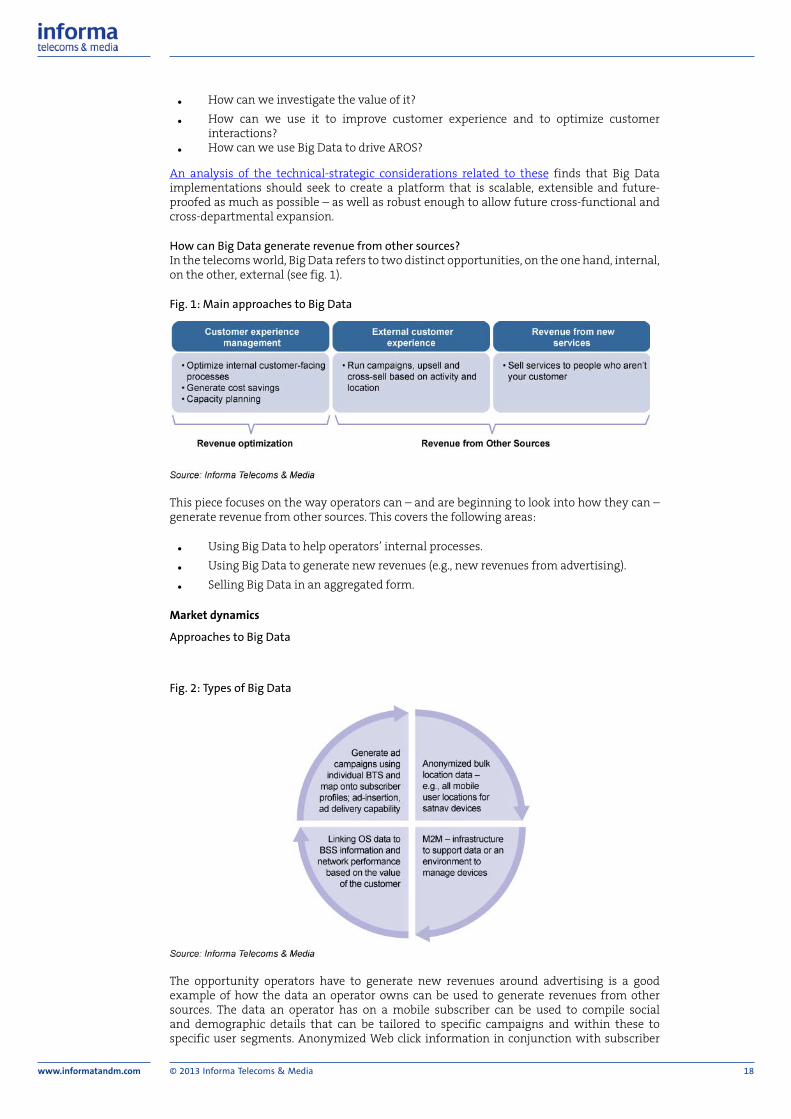

How can Big Data generate revenue from other sources?In the telecoms world, Big Data refers to two distinct opportunities, on the one hand, internal,on the other, external (see fig. 1).

Fig. 1: Main approaches to Big Data

This piece focuses on the way operators can – and are beginning to look into how they can –generate revenue from other sources. This covers the following areas:

• Using Big Data to help operators’ internal processes.

• Using Big Data to generate new revenues (e.g., new revenues from advertising).

• Selling Big Data in an aggregated form.

Market dynamics

Approaches to Big Data

Fig. 2: Types of Big Data

The opportunity operators have to generate new revenues around advertising is a goodexample of how the data an operator owns can be used to generate revenues from othersources. The data an operator has on a mobile subscriber can be used to compile socialand demographic details that can be tailored to specific campaigns and within these tospecific user segments. Anonymized Web click information in conjunction with subscriber

www.informatandm.com © 2013 Informa Telecoms & Media 19

data can create targeted segmentation information about, for instance, a typical car ownerthat advertisers can use to target an ad-insertion campaign more effectively.

While Big Data initiatives are very much in their infancy, some operators are taking early leadson experimenting with initiatives that use Big Data assets. We cover a few in the followingsections.

AT&T AdWorksAT&T AdWorks is a unit within AT&T covering its mobile, fixed and TV assets that offersadvertising based on AT&T subscribers’ usage patterns and identity data. AdWorks aims toplace adverts on PC, mobile and TV devices that are targeted to individual users based onthe information it has on subscriber usage patterns that are mapped onto sociodemographicinformation.

This is a good example of an operator’s Big Data initiative at this stage of the market becauseit encompasses both technical and organizational commitments to realize the Big Dataopportunity. In terms of technical capability, AT&T is implementing a new Demand SidePlatform (DSP) for advertising, and, on the organizational side, it is implementing a centralizedBig Data approach.

Telefonica SmartstepsThe Telefonica Digital unit of Telefonica has launched Telefonica Smartsteps to offeranonymized customer traffic information to high-street retailers. Smartsteps represents aclear organizational commitment to positioning for the Big Data opportunity. Not only hasTelefonica created a separate unit within Telefonica Digital with the specific aim of generatingrevenues from new sources, the operator has also partnered with a company in an adjacentsector, market research company GFK, to explore this opportunity.

Telekom Innovation LaboratoriesTelekom Innovation Laboratories, the central R&D unit of Telekom, launched a series of real-time insurance services based on demographic and location-based data this year. TelekomInnovation Laboratories says it positions itself as a secure and a trusted service provider andbelieves that it can generate new revenues from real-time insurance by being a businessenabler for insurers.

The first product Telekom Innovation Laboratories launched was a third-party-branded real-time insurance product targeted at young skiers. The service uses a mix of data: CRM; location-based; third-party and insurer; and behavioral. Telekom Innovation Laboratories carried outthe platform development, front-end and back-end operations and provided the billing andaccounting capability. It shares responsibilities for marketing and communication with theinsurance third party while the app is also promoted using other Telekom channels, theTelekom brand and the Telekom customer-support capability.

Telekom Innovation Laboratories offered a range of services: insurance price comparisonproducts; multiple payment offers; context-enriched insurance offers; and opt-in based pre-filling of customer information. The opt-in service is delivered via a smartphone app thatidentifies when someone fitting a particular profile arrives at a relevant airport or ski resortand targets them with personalized alerts and reminders to pitch tailored insurance offersto them. Telekom and its insurance partner agreed a revenue-share model based on usage:Telekom acts as an agent for the insurance company, but takes a higher revenue share. Theinsurance premium is paid for via Telekom users’ monthly bills rather than direct to theinsurer. Again, this initiative shows the importance of:

• identifying the opportunity

• targeting clearly-defined segments

• enabling the technical capability

• partnering with the right company to augment core capability, Telekom is also opento partnering with other operators to launch the service.

www.informatandm.com © 2013 Informa Telecoms & Media 20

SprintUS operator Sprint has partnered with a market research company for access to insightsderived from anonymized user data to understand consumer behavior and movements.Sprint uses a mix of structured (call records and logs) and unstructured data (Web browsing,app usage) to create Big Data insights centered on anonymized consumer profiles. Sprintsees retailers, financial services, healthcare, entertainment, transport, hospitality and marketresearch as potential industries that would benefit from its Big Data insights.

Sprint’s Big Data initiative is in an early experimental phase. It believes there are technical andinstitutional challenges to monetizing Big Data effectively, ranging from a top-level strategiccommitment to realizing the Big Data opportunity to ensuring that the data insights it canoffer third parties is reliable and valuable to them in the specific ways that they will want touse the data.

Sprint is understood to generate single-digit millions of dollars from its Big Data partnershipsat present.

Barriers to Big DataVendors and operators no longer see technical capabilities as the major barrier to exploring theBig Data opportunity – it is more a question of how and if to deploy the technology available,both from vendors and in-house development.

The main barriers to deploying the necessary technology to explore Big Data initiatives arestrategic – particularly the absence of a clear business case. Of the main operator initiativesaround Big Data, Telefonica, AT&T and Telekom’s are underpinned by the strongest strategiccommitment. In the case of Telefonica, it has set up a whole new unit to explore opportunitiesfor revenue from other sources. The decisions these operators have taken to address the BigData opportunity have resulted in distinct teams or units within companies to integrate theseparate components that need to be in place to approach Big Data.

A strategic barrier to launching Big Data initiatives is the lack of expertise within operators.Using Big Data to generate new revenues requires expertise about other sectors, such asadvertising and insurance. This means that operators need to partner with companies that canbring this expertise to the project, something that can only be done if there is C-level strategiccommitment to Big Data in the first place. This gives rise to a vicious circle: operators need tocommit to Big Data in the absence of clear ROI but a clear ROI is absent without the expertiseto identify it.

According to Informa Telecoms & Media’s Telco Big Data survey, the major barriers tolaunching services using Big Data to generate new revenues are the lack of a clear businesscase and that the organizational barriers are too high (see fig. 3).

Fig. 3: What is the main barrier to launching services using Big Data to generate newrevenues? (Please select the top two options)

End users’ willingness to accept the use of their data is also a barrier to operator commitmentto Big Data. If an operator uses subscriber data, will it fall foul of regulation? What are theregulatory limits to using Big Data? Are there any best-practice guidelines to using subscriberdata, both internally and in partnership? Operators don’t yet know the answer to these

www.informatandm.com © 2013 Informa Telecoms & Media 21

questions with a sufficient degree of certainty to feel comfortable committing to Big Data,especially given the often punitive, and retroactive, fines that regulators impose for perceivedbreaches of consumer privacy.

A working approach that operators are relying on to avoid regulatory censure is anonymizingsubscriber data, as in the case of Sprint’s profile-brokering initiative. However, regulationaround anonymization of subscriber data is also still uncertain, as is regulation betweencountries and regions. For instance, in the European Union, consent to using subscriber datahas to be opt-in on the basis of “informed consent”. In the US, by contrast, the requirementsare that there is only some consent, either opt-in or opt-out.

Market development

While advertising and insurance are two of the main examples of using Big Data to generatenew revenues, there are innumerable areas where Big Data could potentially be used.However, in the near term at least, the extent of operator commitment to using Big Data asa way to generate revenue from new sources will largely be determined by the success of theinitial deployments. Operators will look to these early deployments to gauge if and how theypursue Big Data strategies. Gauging the success of these deployments is challenging to assessreliably because they are in such uncharted territory.

Although there are more questions than reliable answers about the development of themarket, the questions do point to some of the areas where the future of the market will beplayed out.

Can mobile operators offer better end-user insights than established mobile-advertisingplayers? Can advertisers and operators charge more for adverts in this way? How big canthe premium be? Can operators demonstrate any improvement on insights provided byestablished players? Can operators catch up with established players in other sectors (e.g.,insurance, advertising)? If the early-running operators prove the potential of Big Data togenerate new revenues, how will competition in this space among operators play out?

While Big Data is a clear opportunity for operators to generate new revenues from othersources, the progress of the early Big Data deployments over the next 12 months will be crucialin determining the extent and speed at which other operators commit. It is likely that themajority of operators will adopt a wait-and-see approach and look to deploy key findings fromthe Big Data front-runners. According to Informa’s Telco Big Data survey, almost half (48.3%)expect to generate new business opportunities using Big Data in the next 1-2 years, while 42.%expect to generate new business opportunities using Big Data in the next 3-4 years (see fig. 4).

Fig. 4: When do you believe operators will be ready to generate new business opportunitiesusing Big Data? (Please select one option)

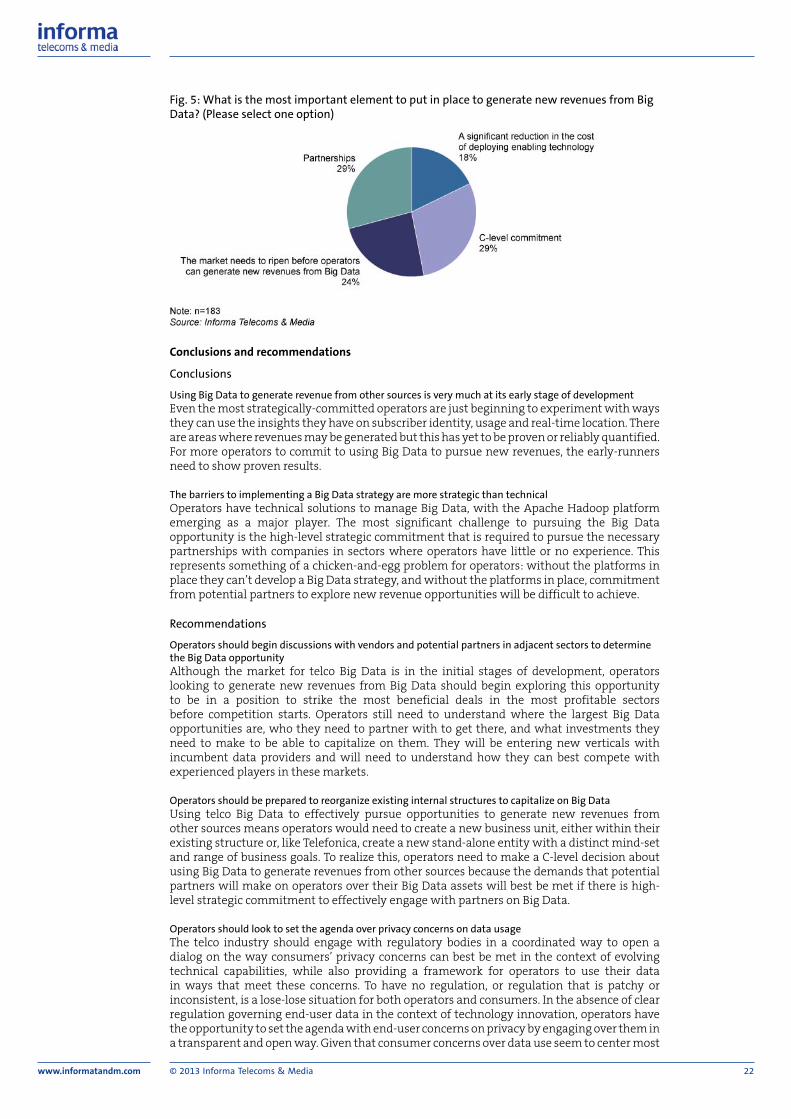

The most important elements to put in place to generate new revenues from Big Dataaccording to the survey are partnerships, C-level commitment and a proven market (see fig. 5).

www.informatandm.com © 2013 Informa Telecoms & Media 22

Fig. 5: What is the most important element to put in place to generate new revenues from BigData? (Please select one option)

Conclusions and recommendations

Conclusions

Using Big Data to generate revenue from other sources is very much at its early stage of developmentEven the most strategically-committed operators are just beginning to experiment with waysthey can use the insights they have on subscriber identity, usage and real-time location. Thereare areas where revenues may be generated but this has yet to be proven or reliably quantified.For more operators to commit to using Big Data to pursue new revenues, the early-runnersneed to show proven results.

The barriers to implementing a Big Data strategy are more strategic than technicalOperators have technical solutions to manage Big Data, with the Apache Hadoop platformemerging as a major player. The most significant challenge to pursuing the Big Dataopportunity is the high-level strategic commitment that is required to pursue the necessarypartnerships with companies in sectors where operators have little or no experience. Thisrepresents something of a chicken-and-egg problem for operators: without the platforms inplace they can’t develop a Big Data strategy, and without the platforms in place, commitmentfrom potential partners to explore new revenue opportunities will be difficult to achieve.

Recommendations

Operators should begin discussions with vendors and potential partners in adjacent sectors to determinethe Big Data opportunityAlthough the market for telco Big Data is in the initial stages of development, operatorslooking to generate new revenues from Big Data should begin exploring this opportunityto be in a position to strike the most beneficial deals in the most profitable sectorsbefore competition starts. Operators still need to understand where the largest Big Dataopportunities are, who they need to partner with to get there, and what investments theyneed to make to be able to capitalize on them. They will be entering new verticals withincumbent data providers and will need to understand how they can best compete withexperienced players in these markets.

Operators should be prepared to reorganize existing internal structures to capitalize on Big DataUsing telco Big Data to effectively pursue opportunities to generate new revenues fromother sources means operators would need to create a new business unit, either within theirexisting structure or, like Telefonica, create a new stand-alone entity with a distinct mind-setand range of business goals. To realize this, operators need to make a C-level decision aboutusing Big Data to generate revenues from other sources because the demands that potentialpartners will make on operators over their Big Data assets will best be met if there is high-level strategic commitment to effectively engage with partners on Big Data.

Operators should look to set the agenda over privacy concerns on data usageThe telco industry should engage with regulatory bodies in a coordinated way to open adialog on the way consumers’ privacy concerns can best be met in the context of evolvingtechnical capabilities, while also providing a framework for operators to use their datain ways that meet these concerns. To have no regulation, or regulation that is patchy orinconsistent, is a lose-lose situation for both operators and consumers. In the absence of clearregulation governing end-user data in the context of technology innovation, operators havethe opportunity to set the agenda with end-user concerns on privacy by engaging over them ina transparent and open way. Given that consumer concerns over data use seem to center most

www.informatandm.com © 2013 Informa Telecoms & Media 23

on unwarranted use of their data, then operators should explore ways to effectively informthem about how their data will be used and provide a simple way to opt out.

Further reading

• Telco Big Data: New tools and strategies

• Telco Big Data: Building a future business platform

www.informatandm.com © 2013 Informa Telecoms & Media 24

IT investment: Does it make sense forthe CMO to have the power to makethe decisions?10 July 2013Julio Puschel

What’s happened?

The telecoms industry has been arguing about whether or not IT decisions are being shiftedaway from the CIO to the CMO. Most of this perception is based on the way that, in manycases, technology is not able to keep up with marketing needs due to the market dynamics.The CMO still faces limitations in the IT even for simple tasks such as creating a new productor changing a plan price. Ordinary tasks like this can take weeks or even months in some cases.

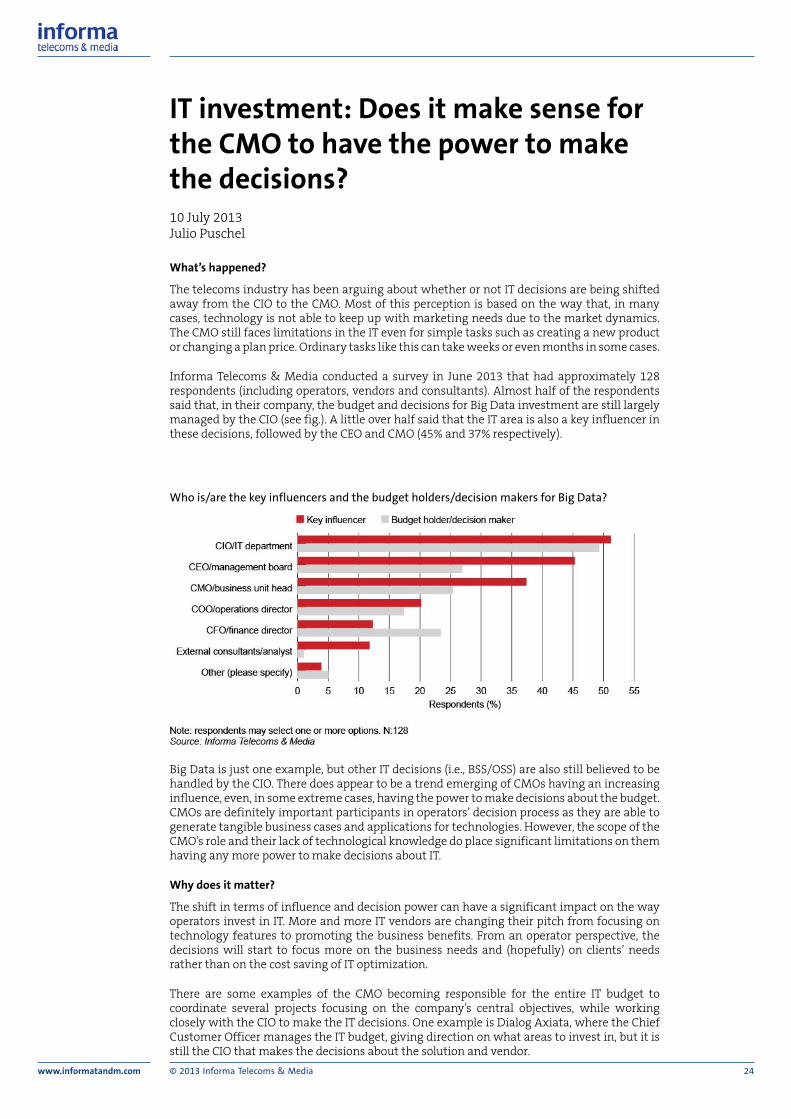

Informa Telecoms & Media conducted a survey in June 2013 that had approximately 128respondents (including operators, vendors and consultants). Almost half of the respondentssaid that, in their company, the budget and decisions for Big Data investment are still largelymanaged by the CIO (see fig.). A little over half said that the IT area is also a key influencer inthese decisions, followed by the CEO and CMO (45% and 37% respectively).

Who is/are the key influencers and the budget holders/decision makers for Big Data?

Big Data is just one example, but other IT decisions (i.e., BSS/OSS) are also still believed to behandled by the CIO. There does appear to be a trend emerging of CMOs having an increasinginfluence, even, in some extreme cases, having the power to make decisions about the budget.CMOs are definitely important participants in operators’ decision process as they are able togenerate tangible business cases and applications for technologies. However, the scope of theCMO’s role and their lack of technological knowledge do place significant limitations on themhaving any more power to make decisions about IT.

Why does it matter?

The shift in terms of influence and decision power can have a significant impact on the wayoperators invest in IT. More and more IT vendors are changing their pitch from focusing ontechnology features to promoting the business benefits. From an operator perspective, thedecisions will start to focus more on the business needs and (hopefully) on clients’ needsrather than on the cost saving of IT optimization.

There are some examples of the CMO becoming responsible for the entire IT budget tocoordinate several projects focusing on the company’s central objectives, while workingclosely with the CIO to make the IT decisions. One example is Dialog Axiata, where the ChiefCustomer Officer manages the IT budget, giving direction on what areas to invest in, but it isstill the CIO that makes the decisions about the solution and vendor.

www.informatandm.com © 2013 Informa Telecoms & Media 25

Of course, with power comes responsibility. Although the CMO definitely plays a key rolein decisions about IT, it is questionable whether the final say should move entirely tothe marketing area. IT still demands significant technical knowledge to understand howtechnologies are evolving in order to make the decision that will optimize the company’sinvestment in the long term. Otherwise technical solutions that make sense to the CMO todaymight be siloed if they do not evolve in the same way as the other IT solutions the operatorrelies on. Additionally, the CIO is in a position to plan for solutions that can support not onlyone business need but several other applications across the business.

Some CMOs may argue that they need to start hiring technical people so they have moresupport to make the right decisions. But if there is already an entire area just looking at IT, isthere a case for creating redundant positions?

Marketing’s attempt to have bigger role in IT decision-making is not just about strategicpriorities, but much more to do with the frustration of not having most of its demandsfulfilled. In the CTOs’ defense, the complexity of modernizing immense legacy systems andthe pressure to optimize technologies and processes has resulted in priority being given tospecific issues within one area before they are able to have more effective collaboration withother areas.

What’s next?

Marketing’s IT requirements are becoming much more complex and are demandingsignificant integration and collaboration. As customer experience management (CEM) andBig Data are becoming a top priority in operators’ agenda, IT decisions will need to be in linewith the business cases and applications. Those areas demand integration and collaborationto allow decisions to be made based on real-time analytics of customer data (structured andunstructured) generated in different parts in the organization.

This is different from the old CRM approach, where operators invested a significant amountof money in solutions without having a clear business case use for them – CEM and Big Datainvestment are being driven by specific business applications. Therefore, investment is nownot focused on buying a solution and then finding an application for it, but on finding asolution that will support a range of business demands.

What should you do?

Operators should to start allocating their budget by business proposition rather than by thearea of the organization. The investment needs to be driven by strategic projects that involvedifferent areas across the organization. The decision-making process needs to be orchestratedby the CEO, so all the initiatives are in line with the company’s strategic goals. The businessinvestment priorities should be decided by a committee formed of all the C-level executivesin the organization (CEO, CMO, CIO, CTO, CFO, etc).

The CIO should still be the main decision-maker for IT investment. The CIO has the requisiteexpertise to choose the right solution and vendors to have a future-proof IT roadmap andoptimize the investment in the long term. However, this decision should be driven by abroader strategy, which aims to support the overall strategic goals of the company rather thanthe goals of one department.

Related analysis

• CEM 2.0: Evolution path for the ultimate customer experience

• CEM will enable operators to differentiate their offerings and innovate better

• Why operators need CEM, customer intelligence and analytics

www.informatandm.com © 2013 Informa Telecoms & Media

Contact us:Informa Telecoms & MediaMortimer House37-41 Mortimer HouseLondon, W1T 3JHUK

Phone: +44 (0) 207 017 4994Fax: +44 (0) 207 017 4783Email: [email protected]