2. - unhcr · sr4b: northern, western, central and southern europe albania bulgaria cyprus greece...

TRANSCRIPT

ANNEX 2: BID SUBMISSION DOCUMENTS

The proposal must be prepared in English.

The proposal shall comprise the following documents in two separate envelops:

1. Technical Offer. The technical component of the proposal should be concisely presented and structured in the format specified in Appendix A, Part 1, 2 and 3 of Annex 2.

2. Financial Offer. The financial component of the proposal must be expressed in the format contained in Appendix B of Annex 2.

Proposals not submitted in the specified format will be rejected.

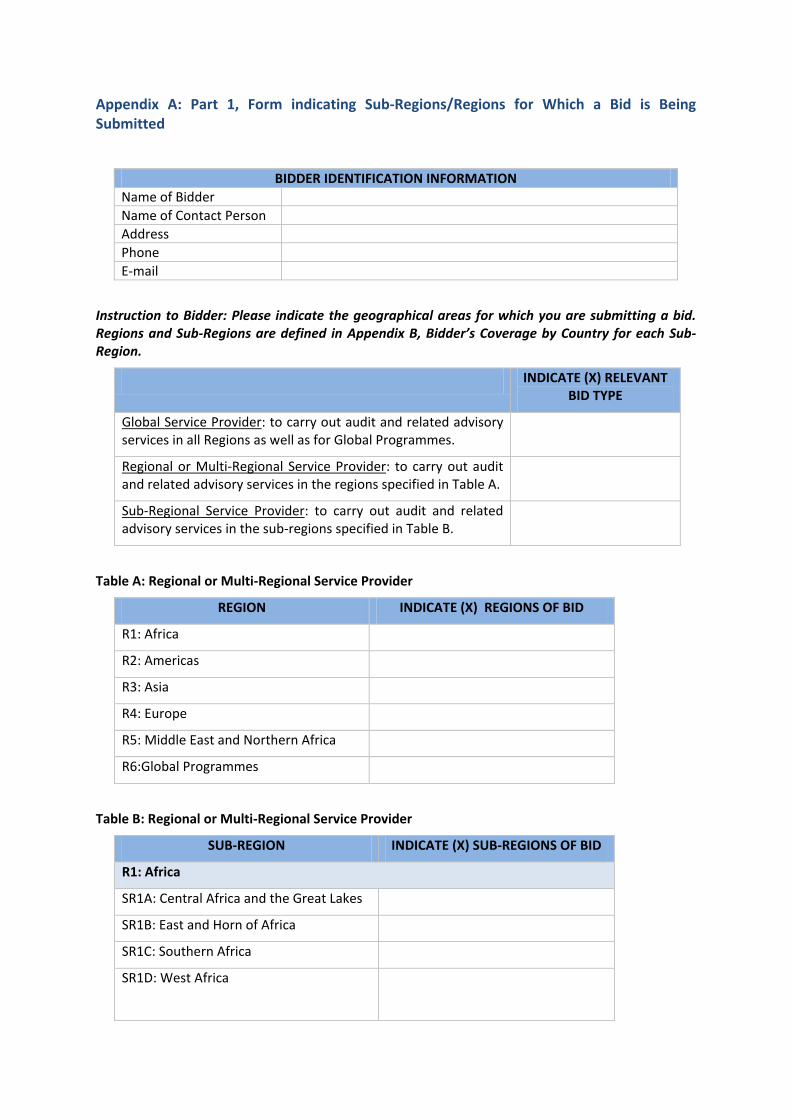

Appendix A: Part 1, Form indicating Sub-Regions/Regions for Which a Bid is Being Submitted

BIDDER IDENTIFICATION INFORMATION Name of Bidder Name of Contact Person Address Phone E-mail

Instruction to Bidder: Please indicate the geographical areas for which you are submitting a bid. Regions and Sub-Regions are defined in Appendix B, Bidder’s Coverage by Country for each Sub-Region.

INDICATE (X) RELEVANT BID TYPE

Global Service Provider: to carry out audit and related advisory services in all Regions as well as for Global Programmes.

Regional or Multi-Regional Service Provider: to carry out audit and related advisory services in the regions specified in Table A.

Sub-Regional Service Provider: to carry out audit and related advisory services in the sub-regions specified in Table B.

Table A: Regional or Multi-Regional Service Provider

REGION INDICATE (X) REGIONS OF BID

R1: Africa

R2: Americas

R3: Asia

R4: Europe

R5: Middle East and Northern Africa

R6:Global Programmes

Table B: Regional or Multi-Regional Service Provider

SUB-REGION INDICATE (X) SUB-REGIONS OF BID

R1: Africa

SR1A: Central Africa and the Great Lakes

SR1B: East and Horn of Africa

SR1C: Southern Africa

SR1D: West Africa

SUB-REGION INDICATE (X) SUB-REGIONS OF BID

R2: Americas

SR1A: Latin America

SR1B: North American and the Caribbean

R3: Asia

SR3A: Central Asia

SR3B: East Asia and the Pacific

SR3C: South-East Asia

SR3D: South-West Asia

R4: Europe

SR4A: Eastern Europe

SR4B: Northern, Western, Central and Southern Europe

SR4C: South-Eastern Europe

R5: Middle East and Northern Africa

SR5A: Middle East

SR5B: North Africa

R6: Global Programmes

SR6A: UNHCR Headquarters

Appendix A: Part 2, Bidder’s Coverage by Country for Each Sub-Region

The following list contains the current locations of UNHCR operations.

Location Specific Bid Qualification Requirement

a) Bidders must be legally registered/ licensed to issue audit opinions in accordance with the applicable rules of each country. UNHCR reserves the right to request proof of registration/ licensing.

b) Bidders must have knowledge of relevant accounting standards of each country.

c) Bidders must have 80% minimum coverage (coverage includes the ability to staff audits with multilingual staff so to undertake the audit work in local language and report in English/French) of countries in each sub-region for which they are submitting a bid.

d) Bidders must have coverage in all sub-regions for each region they are submitting a bid.

e) Bidders must have the ability to undertake audits using multiple audit teams globally to submit a bid for Global Programmes.

f) Bidders who are submitting a bid to be a Global Service Provider must comply with the requirements for all regions and for Global Programmes (points b) and c) above).

For each sub-region applicable to your bid please explain how your organization will cover potential audits in each country of the sub-region. For example, affiliated or member firm presence in the country or the country will be covered by an office from another country etc…

Bidders must use the format below to clearly demonstrate coverage at the country-level.

BIDDER IDENTIFICATION INFORMATION Name of Bidder Name of Contact Person Address Phone E-mail

Description of coverage Coverage of potential audits in

each country. (For example, affiliated or member firm presence in the country or the country will be covered by an office from another country etc…)

Legally registered/ licensed to issue audit opinions in accordance with the applicable rules of the country

Ability to staff audits with multilingual staff so to undertake the audit work in local language and report in English/French

Knowledge of relevant accounting standards in the country

R1: Africa SR1A: Central Africa and the Great Lakes Burundi Cameroon Central African Republic Democratic Republic of the Congo Gabon Republic of the Congo Rwanda United Republic of Tanzania SR1B: East and Horn of Africa Chad Djibouti Eritrea Ethiopia Kenya Somalia

Description of coverage South Sudan Sudan Uganda SR1C: Southern Africa Angola Botswana Malawi Mozambique Namibia South Africa Zambia Zimbabwe SR1D: West Africa Benin Burkina Faso Côte d'Ivoire Ghana Guinea Liberia Mali Niger Nigeria Senegal Sierra Leone Togo R2: Americas SR2A: Latin America Argentina Brazil Colombia Costa Rica Ecuador Mexico

Description of coverage Panama Venezuela SR2B: North America and the Caribbean Dominican Republic Haiti R3: Asia SR3A: Central Asia Kazakhstan Kyrgyzstan Tajikistan Turkmenistan SR3B: East Asia and the Pacific China South Asia India Nepal Sri Lanka SR3C: South-East Asia Bangladesh Indonesia Malaysia Myanmar Philippines Thailand Viet Nam SR3D: South-West Asia Afghanistan Islamic Republic of Iran Pakistan R4: Europe SR4A: Eastern Europe Azerbaijan Belarus

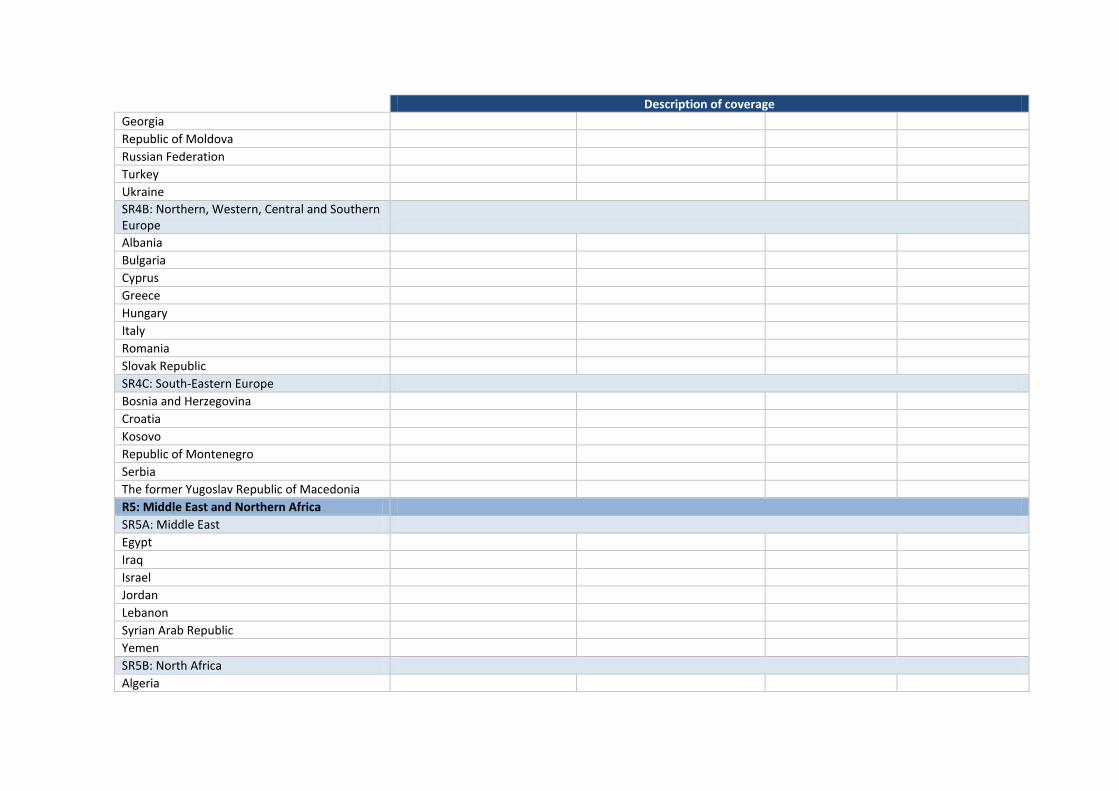

Description of coverage Georgia Republic of Moldova Russian Federation Turkey Ukraine SR4B: Northern, Western, Central and Southern Europe Albania Bulgaria Cyprus Greece Hungary Italy Romania Slovak Republic SR4C: South-Eastern Europe Bosnia and Herzegovina Croatia Kosovo Republic of Montenegro Serbia The former Yugoslav Republic of Macedonia R5: Middle East and Northern Africa SR5A: Middle East Egypt Iraq Israel Jordan Lebanon Syrian Arab Republic Yemen SR5B: North Africa Algeria

Description of coverage Libya Mauritania Morocco Tunisia R6:Global Programmes UNHCR Headquarters

Appendix A: Part 3, Technical Proposal The technical proposal is evaluated and examined to determine its responsiveness and compliance with the requirements specified in this Request for Proposal. Technical proposals must be prepared in the format specified below. Information not provided in this format (or in addition to this format) will not be assessed.

BIDDER IDENTIFICATION INFORMATION Name of Bidder Name of Contact Person Address Phone E-mail

Section I: Expertise and Capability of Bidder

A: General Profile • Provide a brief description of the organization submitting the proposal, including the year and

country of incorporation, types of activities undertaken, and approximate annual billings. • Provide key financial ratio analysis using a table format together with the audited financial

statements (For organizations that are partnerships and do not disclose the audited financial statements, please submit a signed declaration from the organization’s Chief Financial Officer stating figures provided are accurate and complete as well as providing access to the Chief Financial Officer for further enquiry). The financial ratio analysis should cover key financial stability ratios over a 5 year period, including Current Ratio, Quick Ratio and Debt Ratio. (Ratios should be calculated using US $).

B: Litigation and Arbitration • Specify whether there is any ongoing litigation between the organization and any United

Nations agency. • Reference to any history of litigation and arbitration in which the organization has been

involved.

C: General Organizational Capability • Corporate capability for management of arrangement in accordance with the Annex 1, Terms

of Reference. • Outline organization’s global network (presence or organizational partners’ presence in regions

of UNHCR operations). Provide details of partner collaborations, affiliations or licensing arrangement in countries, where Bidder does not have own presence including the duration of partnerships and number of joint projects as partners etc.

• Provide a detailed description of relevant collaborative efforts in which the organizations has participated.

• Demonstrate ability to conduct audits using multilingual staff where and when required.

D: Relevance of Specialized Knowledge and Experience on Similar Projects • Current and ongoing contracts that have a direct relationship to this requirement. • Outline recent experience on projects of a similar nature, including experience with other UN

organizations and other similar public sector international organizations (Regional Development Banks, EU, World Bank, International NGOs etc.).

• Provide evidence of successful completion of at least three similar contracts within the last five years. For each completed contract, include value of each completed contract and contact information for the primary client contract. The examples provided should correspond to the

level at which the Bidder is submitting a bid. That is, a global contract example should be submitted for a bid as a Global Audit Service Provider.

• Demonstrate the number of years of experience the organization has (either by the organization, itself, or through arrangements with affiliates) undertaking audits in the locations for which the bid is submitted.

o For Global audit service provider bids, demonstrate experience for each Region and undertaking multiple site global audits.

o For Regional/Multi-Regional audit service provider bids, demonstrate experience for each region.

o For Sub-Regional audit service provider bids, demonstrate experience at the country level for each sub-region.

E: Quality assurance procedures, risk and mitigation measures • Outline the quality assurance mechanism in place to ensure that all audits undertaken are

consistent with the Detailed Terms of Reference (Annex 1, Appendix A). • Provide certificate (s) for accreditation of quality processes (e.g. International Standard for

Standardization etc.). • Describe the organization’s risk management approach as they relate to the services required. • Describe procedures and protocols in place at the organization related to information/data

security policies and practices for maintaining the confidentiality of audit and auditee data. F: References • Provide at least 3 references for current business that are similar/ relevant to the services

required. If a joint proposal, references must be from sources that are familiar with joint service model. For each reference, provide the following information:

o Name of client organization o Contract value (US $) o Period of project activity (start and end dates) o Description of project o Bidder’s role on project o Reference contact details (Name, title, phone, email)

Section II: Proposed Work Plan and Approach

G: Approach and methodology • Explain your organization’s understandings of:

o UNHCR’s work and its project financial audit and related advisory needs; o UNHCR’s audit environment; and o Partners and their audit expectations.

• Provide a description of the organization's approach, methodology, and timeline for how the organization / firm will achieve the Terms of Reference of the project while meeting or exceeding the stipulations of the terms of reference.

• Description of how the organization would manage and liaise with affiliates to undertake audits in areas where the organization may not have presence.

• Description of the organization’s established and tested audit methodologies relevant to the Detailed Terms of Reference (Annex 1, Appendix A).

• Description of how the organization will address the requirement for the review of compliance with the articles of the Project Partnership Agreement.

• Description of the organization’s policies and protocols for working in countries/areas with security concerns, including a description of how the organization would undertake project financial audits in such areas.

• Identify any gaps in the information provided in this Request for Proposal.

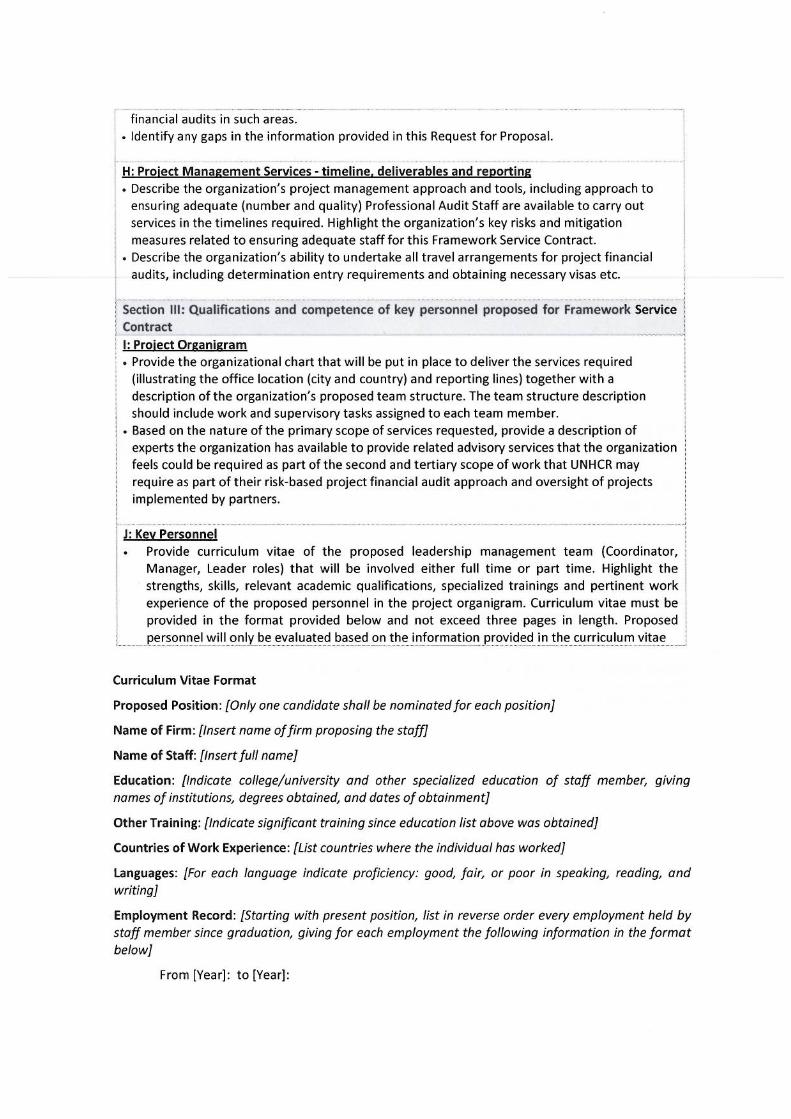

H: Project Management Services - timeline, deliverables and reporting • Describe the organization’s project management approach and tools, including approach to

ensuring adequate (number and quality) Professional Audit Staff are available to carry out services in the timelines required. Highlight the organization’s key risks and mitigation measures related to ensuring adequate staff for this Framework Service Contract.

• Describe the organization’s ability to undertake all travel arrangements for project financial audits, including determination entry requirements and obtaining necessary visas etc.

Section III: Qualifications and competence of key personnel proposed for Framework Service Contract I: Project Organigram • Provide the organizational chart that will be put in place to deliver the services required

(illustrating the office location (city and country) and reporting lines) together with a description of the organization’s proposed team structure. The team structure description should include work and supervisory tasks assigned to each team member.

• Based on the nature of the primary scope of services requested, provide a description of experts the organization has available to provide related advisory services that the organization feels could be required as part of the second and tertiary scope of work that UNHCR may require as part of their risk-based project financial audit approach and oversight of projects implemented by partners.

J: Key Personnel • Provide curriculum vitae of the proposed leadership management team (Coordinator,

Manager, Leader roles) that will be involved either full time or part time. Highlight the strengths, skills, relevant academic qualifications, specialized trainings and pertinent work experience of the proposed personnel in the project organigram. Curriculum vitae must be provided in the format provided below and not exceed three pages in length. Proposed personnel will only be evaluated based on the information provided in the curriculum vitae

Curriculum Vitae Format

Proposed Position: [Only one candidate shall be nominated for each position]

Name of Firm: [Insert name of firm proposing the staff]

Name of Staff: [Insert full name]

Education: [Indicate college/university and other specialized education of staff member, giving names of institutions, degrees obtained, and dates of obtainment]

Other Training: [Indicate significant training since education list above was obtained]

Countries of Work Experience: [List countries where the individual has worked]

Languages: [For each language indicate proficiency: good, fair, or poor in speaking, reading, and writing]

Employment Record: [Starting with present position, list in reverse order every employment held by staff member since graduation, giving for each employment the following information in the format below]

From [Year]: to [Year]:

Employer:

Positions held:

Description of duties/experience:

Certification:

I, the undersigned, certify that to the best of my knowledge and belief, this CV correctly describes myself, my qualifications, and my experience. I understand that any wilful misstatement described herein may lead to my disqualification or dismissal, if engaged.

Date:

[Signature of staff member or authorized representative of the staff] Day/Month/Year

Full name of authorized representative:

Specific information to be provided in the curriculum vitae of the Audit Coordinator (global, regional, sub-regional as appropriate to your bid)

Proven credibility in auditing and oversight mechanisms in complex international organizations and donor/funding agencies

Name of assignment or project:

Year:

Location:

Client:

Main project features:

Positions held:

Activities performed:

[Insert details of all appropriate assignments]

Proven familiarity with project financial auditing and donor/funding agency auditing

Name of assignment or project:

Year:

Location:

Client:

Main project features:

Positions held:

Activities performed:

[Insert details of all appropriate assignments]

Specific information to be provided in the curriculum vitae of the Audit Manager/Leader (regional, sub-regional, country as appropriate to your bid)

Proven credibility auditing the projects of organizations of various sizes and levels of organizational maturity

Name of assignment or project:

Year:

Location:

Client:

Main project features:

Positions held:

Activities performed:

[Insert details of all appropriate assignments]

Proven familiarity with project financial auditing and donor/funding agency auditing

Name of assignment or project:

Year:

Location:

Client:

Main project features:

Positions held:

Activities performed:

[Insert details of all appropriate assignments]

Appendix B: Financial Proposal Format

BIDDER IDENTIFICATION INFORMATION Name of Bidder Name of Contact Person Address Phone E-mail

Professional Fees

Please provide a daily and hourly maximum rate (in US $) for each of the position mentioned below for each of the listed country in the sub-region. Please note that the rates must cover all costs to be borne by your firm for undertaking the assignment including management, coordination, quality assurance and overhead.

Table A: Proposed Rates*

Sub-Regions Coordinator Audit Manager/Leader

Professional Audit Staff

R1: Africa Hourly Rate Hourly Rate Daily Rate* SR1A: Central Africa and the Great Lakes SR1B: East and Horn of Africa SR1C: Southern Africa SR1D: West Africa R2: Americas SR2A: Latin America SR2B: North America and the Caribbean R3: Asia SR3A: Central Asia SR3B: East Asia and the Pacific SR3C: South-East Asia SR3D: South-West Asia R4: Europe SR4A: Eastern Europe SR4B: Northern, Western, Central and Southern Europe

SR4C: South-Eastern Europe R5: Middle East and Northern Africa SR5A: Middle East SR5B: North Africa R6:Global Programmes UNHCR Headquarters

*Rates should be provided for each role proposed in the project organigram outlined in the technical proposal. **Daily rate based on an 8 hour day. Illustrative Audit Budgets

Illustrative audit budgets, as appropriate to the bid (see Table B below), should be prepared and submitted as part of the Bidder’s financial proposal. The reasonableness of the audit budgets will be assessed during the evaluation.

The illustrative audit budgets must be aligned with the approach and methodology described in the technical proposal for the scope of work as per the Detailed Terms of Reference (Annex 1, Appendix A). The illustrative audit budget may provide a general statement of approach, methodology used in

audit, resourcing and costing. Each illustrative audit budget must be presented in the below format. Rates must not exceed the rates quoted in Table A: Proposed Rates for the sub-regions in question.

For each illustrative audit budget provide a table with the following information. Illustrative Audit Budget Sub-Region:

Country:

Professional Fees Audit Team

Member Name

Description of Role/Function

Number Hours/Days

Hourly/Daily Rate Estimated Total Amount

Total Professional Fees Total travel costs (including transport and per diems paid to staff) Other costs (please specify) Total Estimated Audit Budget

For each illustrative project budget, assume an estimated project expenditure of US$ 1 million and that the audit takes place during the period of January – March 2013.

Table B: Illustrative Project Budget Required by Type of Bid Global Audit Service Providers Democratic Republic of the Congo, South Sudan, Myanmar,

Colombia, Pakistan, Turkey, Lebanon, Switzerland Regional Audit Service Providers Case study for each Sub-Region for the Region (s) you are

submitting a bid. Sub-Regional Audit Service Providers Case study for both countries for each sub-region you are

submitting a bid. Africa Regional Bid

First country for Sub-Regional Bids

Second country for Sub-Regional Bids

Central Africa and the Great Lakes Democratic Republic of the Congo

Burundi

East and Horn of Africa South Sudan Ethiopia Southern Africa South Africa Namibia West Africa Burkina Faso Niger

Americas Latin America Colombia Ecuador North America and the Caribbean Dominican Republic Haiti

Asia Central Asia Kazakhstan Tajikistan East Asia and the Pacific Nepal India South-East Asia Myanmar Thailand South-West Asia Pakistan Afghanistan

Europe Eastern Europe Turkey Russian Federation Northern, Western, Central and Southern

Europe Greece Slovak Republic

South-Eastern Europe Serbia Republic of Montenegro MENA

Middle East Lebanon Iraq North Africa Algeria Mauritania

Global Programmes UNHCR Headquarters Switzerland Japan

Other innovative pricing proposals

UNHCR is looking to establish Framework Service Contracts with audit service providers that can effectively and efficiently deliver the required audit services as well as bring forward innovative solutions. With this in mind, Bidder’s may propose an alternative pricing arrangement for UNHCR’s consideration. However, the information requested in Table A and the illustrative project budgets must still be submitted with the Bidder’s financial proposal.

Page 1 of 23

Suppliers’ Conference RFP/2013/550: Audit and Advisory Services

Teleconference

Date / Time: Tuesday, September 3, 2013, 3:00pm CET Agenda: 1) Welcome and Introductions 2) Opening Remarks by Procurement Management and Contracting Service (PMCS) 3) Opening Remarks by Implementing Partner Management Service (IPMS) 4) Questions and Answers 5) Wrap-up

UNHCR Attendees: Fatima Sherif-Nor, Head, IPMS Isaac Mcekeni, Chief of Section, Procurement of Services, PMCS Andrea Suley, Special Advisor, Risk Management, IPMS Sofia van Dijk, Supply Associate, PMCS Beverly Osborn, Intern, PMCS Items Discussed: Welcome, Introductions and Opening Remarks:

1. Isaac Mcekeni welcomed the attending suppliers. Procurement personnel involved in the tender were introduced. Fatima Sherif-Nor introduced the technical experts.

2. Isaac Mcekeni introduced the tender and purpose of the Suppliers’ Conference. The conference objective was that all potential suppliers should have a clear understanding of UNHCR’s requirements and thereby be able to submit a clear and complete proposal to meet those requirements.

3. Isaac Mcekeni gave an overview of the conference agenda.

4. Fatima Sherif-Nor introduced the tender from a technical perspective. She noted that it encompasses all audits of implementing partners, excluding any and UN entities. Fatima Sherif-Nor also noted that in the past audits have been procured on a local level, but now there is a desire to achieve efficiencies through centralized global procurement.

Page 2 of 23

Questions and Answers:

EXPECTED NUMBER OF SUCCESSFUL BIDDERS

1.

Question: Would it be possible to know how many contractors you intend to appoint?

Answer: We do not have any predetermined number. We could have one global provider, or we could have several regional service providers.

2.

Question: If more than one contractor is appointed, will the contractors enter into competition for each Purchase Order (e.g. submit a budget and CVs) or will you specifically assign the work to one contractor?

Answer: If we chose, say, one contractor for one region, we will remain with that one contractor for that one region for the given time. However, if that contractor does not give us the value that we expected based on the selection process, we may go to another contractor.

Clarification: In other words, performance will be a key driver in the vendor selection for different regions?

Response: Exactly.

3.

Question: Is UNHCR leaving open the number and type of audit service providers that it chooses to appoint until it has reviewed the tender submissions?

Answer: Yes.

4.

Question: Could you please confirm if you are looking for a single partner or multiple suppliers? If a single partner, is that partner required to cover all locations and regions?

Answer: We are looking for both. If a single partner is more cost-effective, and also provides quality, we will use a single supplier for everything. If multiple suppliers are most cost-effective, then multiple suppliers will be used.

COMPETITION AMONG SUCCESSFUL BIDDERS

5.

Question: How will work be divided among winning contractors?

Page 3 of 23

Answer: Again, it depends on the value of the tender. If the contractor was selected for the region, based on the points, then that contractor will perform the work. Unless the contractor cannot then perform that best offer.

6.

Question: Will UNHCR choose the audit service provider for each country, sub-region or region from among the framework contractors based on the primary tender submission or will the framework contractors engage in secondary competition in order to be appointed?

Answer: What we are saying is that we will select the audit service provider based on the quality of the proposals. We will then engage into framework agreements based on those proposals. If the audit service provider adheres to the proposed services, then it will continue. If it does not adhere to what it has proposed then we will go to another.

Clarification: This cannot be answered definitively without knowing the quantity of the bids submitted.

Response: And the quality also.

7.

Question: If multiple suppliers appointed, will this work by rotational selection, primary/secondary proposal, or on a lowest fee basis?

Answer: It’s the same answer. (Please refer to the questions and answers to questions 2, 5, and 6).

8.

Question: Does UNHCR envisage appointing global service providers, regional service providers and sub-regional service providers who will compete with each other in each sub-region?

Answer: It’s the same answer. (Please refer to the questions and answers to questions 2, 5, and 6).

9.

Question: If secondary competition among framework contractors will be required, will it be conducted on a country, sub-regional, regional or global basis?

Answer: It’s the same answer. Secondary competition will only be used if the quality delivered with the originally selected bidder declines or is not as was set forth in the proposal. (Please also refer to the questions and answers to questions 2, 5, and 6).

10.

Question: If secondary competition will be required, how will framework contractors be assessed, marked and compared in order to decide which one will be appointed?

Answer: Response made in conjunction with response to question 9 above.

Page 4 of 23

FINANCIAL PROPOSAL AND EVALUATION

11.

Question: The TORs state that the proposed rates quoted in Table A must be all-inclusive, but it is not too clear whether they must cover travel, transport and per diem costs. The format of the “Illustrative Project Budgets” seems to imply that travel costs will be billed separately, but this is not fully clear from the phrasing of the ToRs. Could you clarify that travel, transport and per diems costs will be billed separate and not as part of the proposed rates of Table A?

Answer:

The proposed rates quoted in Table A should exclude travel related costs. Travel will be budgeted and billed separate from professional fees.

With regards to travel: Travel is exclusive, because travel will be covered in accordance by the UN Policy on travel. This policy can be provided in the response and clarifications.

With regards to per diem: That’s the cost we expect a partner to bring forward in the Illustrative Project Budgets, part of the cost of the service. They should show whether the cost is per diem, or otherwise. The decision will be based on the bottom line. We want to see the proposal all-inclusive, but broken-down.

12.

Question: The financial proposal will be scored based on the total price of the financial offer. For the purposes of this calculation what is the total price of a financial offer?

Answer: The financial proposal should be provided in accordance with the pricing proposal provided for the rates, as well as the other pricing tables provided for the illustrative budget. It should be provided as per Table A and Table B. The partner that gives us more information, the better for us to understand.

Clarification: But the financial proposal must be submitted in accordance with the format provided.

Response: Yes.

13.

Question: The financial proposal requires hourly or daily rates per sub-region. From these, how is the total price of an offer assessed and compared with other offers?

Answer: From Table A there will be a calculation of the rates provided, which is the one part and the second part will be the calculation of the illustrative project budget with the assumptions as provided in this particular table. From this information a comparison will be made between the vendors to determine the most responsive proposal to our requirement.

14.

Page 5 of 23

Question: How is the financial offer of a global service provider assessed and marked in comparison with that from a regional or a sub-regional service provider?

Answer: Please refer to the answer to question 13.

15.

Question: Are the illustrative audit budgets included in the total price of an offer?

Answer: Yes.

16.

Question: How do the hourly/daily rates per sub-region and illustrative budgets combine to arrive at the total price of an offer?

Answer: The rates will be compared to the rates on a like for like basis. The rates in the illustrative project budget will also be compared on a like for like basis to arrive at the most responsive offers.

17.

Question: Travel costs – does UNHCR expect teams to travel to/from different locations? If so, is there a travel cost cap or restriction?

Answer: Travel costs will be covered in accordance with the UNHCR travel policy, which will be provided in our response and clarifications.

Clarification after suppliers’ conference: When travel is required during the course of the Contract by UNHCR, travel is subject to the UN travel rules. All air transport to/from any destination will be at the cheapest economic fare available as determined by UNHCR travel unit. Please refer to answer of question 11 on per diem costs.

CONTENT OF TECHNICAL OFFER

18.

Question: With regards to Appendix A, Section C: We will provide an outline of our international network. As we are one multinational firm, we understand no details of partner collaborations, affiliations, etc. is needed. Would this be your understanding as well?

Answer: Yes, as far as it is demonstrated that performance would be effective, and UNHCR would receive the quality without any problematic collaborations, then that is fine.

19.

Question: What is approach to be adopted by a network, when bidding under this RFP? Specifically, the RFP requires certain information about the entity bidding – Vendor registration form, licensing issues, technical and organization capacity (financial analysis, ratios, etc.). How should this information be presented, if the entities in each country are

Page 6 of 23

separate legal entities, although they are member firms of one network? Will cooperation between an assigned lead firm for region/sub-region with the member firms in country deem to be approved subcontracting according Article 5, if we include this cooperation in our proposal, or will this need to be approved separately according to Article 5?

Answer: Working with affiliates in different countries is an acceptable arrangement. However, the bidding firm becomes the lead entity and is expected to manage the entire arrangement and must therefore coordinate the arrangements with the various affiliates in all the operating countries.

As per the response to question 18. The contracting partner is the one that submits the offer, and we expect them then to be effective, and the collaboration effective. We need to see demonstration that such a collaboration is not a hindrance to performance.

We expect full disclosure from the vendor community. If you have an affiliate in one country and that country office operates with the United Nations and there have been issues there, we expect full disclosure on those entities. However, we expect that the main office is coordinating activities for the other affiliate offices.

20.

Question: Section D: We need to demonstrate ability to conduct audits using multilingual staff. Will the description of our network and submission of CVs be sufficient? If not, what other type of evidence do you expect?

Answer: The description in the submission and CVs will be sufficient. If we were later to discover that skills were inadequate, then this would be a lack of disclosure and we would act accordingly.

A description of your staff’s multilingual skill competencies relevant to the geographical scope of bid would suffice as well as established approaches to ensure high quality English or French in reports when audit work is undertaken in a different language.

21.

Question: Other than internal audit skills, are there any other technical skills required, such as IT or forensics?

Answer: Yes, the more you tell us, the better it is. The more skills, the better performance, and we may choose you on that basis. Bidders are encouraged to detail their complementary service offerings/ expertise to the primary scope of work.

22.

Question: Is UNHCR expecting CVs and detailed team structure from Partner to Associate, or only the leadership team of the core and/or regional teams?

Answer: We expect CVs and detailed team structure only for the leadership teams. If a sub-regional bid, then the sub-regional leadership. If a regional bid, then the regional leadership. We do not expect the CVs of specific teams of associates (professional audit staff).

Page 7 of 23

For Purposes of Section J (Annex 2, Appendix A, Part 3), UNHCR is expecting CVs of the leadership team. CVs of Professional Audit Staff are not required. (Please refer to Annex 1, Appendix D for our use of the term ‘Professional Audit Staff’).

For purposes of Section I (Annex 2, Appendix A, Part 3), UNHCR is expecting a detailed team structure with specific duties assigned to each role and reporting lines. While specific individuals do not have to be specified for the Professional Audit Staff role (s, it is expected that a description of tasks undertaken and reporting lines of Professional Audit Staff will be included.

23.

Question: Section F References of current business: We will provide the information requested and we understand no additional documents are needed, is this correct?

Answer: We just need the information requested and we will do reference checks. If we ask further questions at the time you are selected, then it will be of value to you to provide the requested information.

24.

Question: Would a Declaration of Honor be sufficient to prove knowledge of relevant accounting standards?

Answer: With respect to multilingual skills and knowledge of accounting standards, please indicate your firm’s competency in the appendix A part 2 for each country. No Declaration of Honour is required. We will assume that you are submitting true information and will move forward on that basis.

TECHNICAL IMPLEMENTATION

25.

Question: It is mentioned bidder must be legally registered/licensed to issue audit opinions in accordance with the applicable rules of each country. We intend to cover the work in one country with an office in another country, and therefore the license of the country performing the work will apply to the other one. Would this be also acceptable for you and does this meet your expectations?

Answer: It depends on the applicable public accounting rules of each country. If it is allowed in that jurisdiction then it is allowed for UNHCR, if not, then not.

Whether this arrangement would be acceptable to UNHCR is dependent on the applicable public accounting regulations in each country/jurisdiction.

An illustrative example that would be acceptable to UNHCR:

The Public Accounting Act of Country A allows for a firm licensed under the Public Accounting Act of Country B to provide opinions on assurance engagements within the jurisdiction of Country A.

Page 8 of 23

26.

Question: Is being ISA compliant sufficient for you or do you expect to have the audit reports signed by a regional Audit Partner?

Answer: In addition to being ISA compliant, we also expect you to be compliant with public accounting rules in the given jurisdiction. If the jurisdiction requires that the local audit manager signs off on it then that is what we would require as well. Where no public accounting laws exist then only the ISA applies.

27.

Question: In the tender, only two types of audit opinion are mentioned (unqualified and qualified). Nevertheless, we read in the tender documentation that we can mutually agree to a specific report format. As a consequence, we suppose that we may suggest two additional audit opinions, which are a disclaimer and negative opinion. Could you please confirm?

Answer: Yes, this is acceptable. Disclaimer of opinion and adverse opinion are permitted. However, in negotiating the framework agreement, detailed escalation protocols will be established that UNHCR will expect the auditor to follow prior to issuance of a disclaimer of opinion or adverse opinion.

28.

Question: Could you please clarify who would be responsible for the completion of the Checklist? It is our understanding we will provide the document to the auditee and follow-up on its proper completion, but it would be the Auditee himself that would complete it. Is this correct?

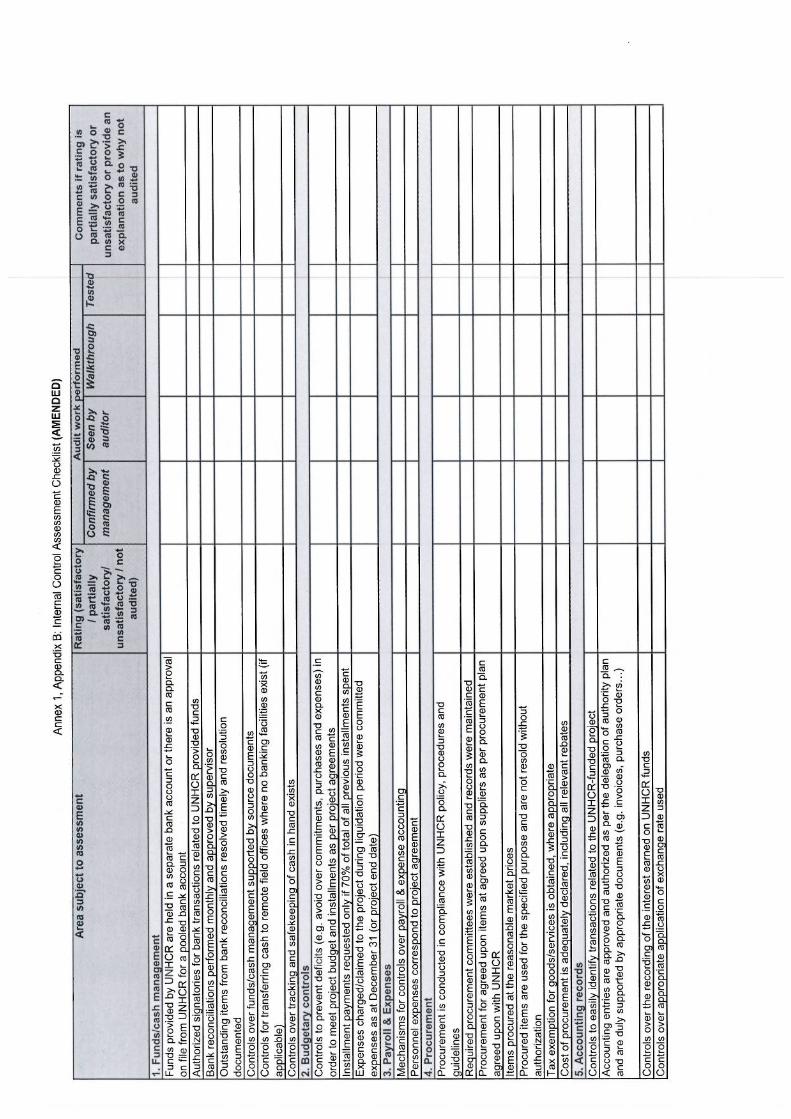

Answer: No. We auditor is to complete the Internal Control Assessment Checklist.

In answering this question, we assume the question refers to the Internal Control Assessment Checklist (Annex 1, Appendix B).

29.

Question: Engagement Operating Model – does UNHCR expect a central team in Geneva to manage the overall engagement with a core team that identifies local resources, reviews work performed and submits the final report? Or is UNHCR expecting a central team with regional leaders that work with local country offices?

Answer: We have no specific expectation of where the management team should be placed, provided we have direct and easy communication, and no time difference problems.

TECHNICAL EVALUATION CRITERIA

30.

Question: Is there a marking scheme for the technical proposal, i.e. a breakdown of the marks for each section and sub-section of the proposal?

Page 9 of 23

Answer: Yes, we have a rating scale, but that is internal. We will use this to rate vendors according to the proposals provided. The reason is simply that we want to make sure that whatever offers are provided are rated in such a way that it is objective and that there is a structure to the way that offers are evaluated in relation to the technical criteria which were provided externally.

31.

Question: In the technical proposal how will a tender from a global service provider be assessed and marked in comparison with a tender from a regional or a sub-regional service provider?

Answer: We will look at the compatible points between regions as well as combinations of various regional providers compared to one global provider.

Clarification: These will be compared like to like?

Response: Yes.

PAST EXPERIENCE OF UNHCR WITH PROJECT AUDITS

32.

Question: Who has done the UNHCR project audits in the past and how have they been tendered?

Answer: Audit service providers were contracted by UNHCR field offices according to a standard terms of reference. The difference now is that contracting and management of audit service providers will be done collectively at a global level.

33.

Question: What aspects of the current system of managing project audits would UNHCR most like to see improved by the new centrally managed approach that is the subject of this tender?

Answer: Three things: quality; timeliness of submission of reports; and cost.

34.

Question: Are project audit reports for 2012 and earlier published?

Answer: Not publicly. The reports are issued to UNHCR and given to the implementing partner (the auditee).. However, UNHCR reserves the right to publish audit reports at any point.

Clarification: For those that are done in the future and the current ones?

Page 10 of 23

Response: Yes, because the rules could change.

TIMELINE

35.

Question: Timeline Example (2013): We understand the list of audits to be performed will be communicated end of December 2013 and finalized sometime between end of February – April 2014. Once Task Authorizations have been provided, we will start executing the audits but we would need to submit all audit reports by April 2015. Could you please confirm this is correct?

Answer: The understanding of the timelines is not correct.

UNHCR has a 31 December year-end. The completion date of each Project Partnership Agreement cannot extend past 31 December of each year. Audit of Project Partnership Agreements with completion date 31 December 2013 must be submitted by 30 April 2014.

Annex 1 describes the Task Authorization schedule and arrangement that will be put in place. To complement this description and further clarify, a brief illustrative example for Project Partnership Agreements with completion date of 31 December 2014 is provided below:

a) 30 June 2014 - UNHCR communicates the bulk of the project audit requirement to the audit service provider

b) 18 July 2014 – latest date that audit service providers can provide UNHCR with a written commitment as to whether they are able to perform the requested audits and confirming that undertaking any of the audits does not give rise to a conflict of interest

c) 07 August 2014 – latest due date for submission of proposed budgets for each audit for committed audits in b).

d) UNHCR will issue Task Authorizations no later than 30 working days after agreement.

e) 30 September 2014 – the audit sample will be finalized through consideration of any new information and any additional requirements communicated to audit service providers. The process detailed in b) c) and d) will be compressed and completed by 11 November 104.

f) 30 April 2015 – audit service providers submit final reports.

Annex 1 also notes that a transitional arrangement will be put in place for services required for the audit of 2013 projects (that is Project Partnership Agreements with end date of 31 December 2013). The terms of a transitional arrangement will be negotiated with each audit service provider for which a Framework Services Contract will be established.

SPECIFIC SITUATIONS

36.

Question: We are a registered audit firm under the laws of the United Arab Emirates. To which region can we provide service?

Page 11 of 23

Answer: Any sub-region you may choose. Wherever you are based, or wherever you are registered, you may bid on any geographical area for which you meet all the requirements listed in Appendix A: Part 2 (Annex 2).

37.

Question: We are intending to submit our RFP for one region and another sub-region, e.g., MENA and Central Asia. Is this acceptable? If yes, then what are the eligibility requirements for this arrangement?

Answer: The same answer as number 36.

38.

Question: We intend to submit a bid as Global Audit Provider. We have taken good note of your indicate organizational structure but we would like to propose a slightly different one. Do we have any flexibility in this regard?

Answer: Yes. First we expect you to quote according to our requirement, and then you can submit other scenarios that you think are more appropriate.

39.

Question: We are comfortable to handle only some specific countries with some regions; can we bid per country in these regions?

Answer: No. We would like to see sub-regions and not countries, thereafter during the framework agreement if there are any exceptional situations those will be dealt with case by case. However, we expect to see bidders with at least 80% coverage of the sub-regional groupings we have given. Refer to Appendix 2 Location Specific Bid Requirements.

OTHER/GENERAL

40.

Question: Is our acceptance of point 50 of the Vendor Registration Form sufficient to acknowledge your General Conditions of Contract, or is something else required?

Answer: Confirmed. This is acceptable.

41.

Question: We understand our bid needs to be concise, but is there any page limit?

Answer: There is no page limit, but we expect you to maintain the same format so that we are able to compare with others.

Clarification: And if they are submitting proposals that are slightly different than those we have requested, that would be more pages?

Page 12 of 23

Response: We will clarify this in further detail in the written response after looking again at the submission forms.

Clarification after suppliers’ conference: Please provide any alternative pricing proposals in the indicated section of Annex 2, Appendix B: Financial Proposal Format. When providing an alternate pricing proposal, the bidder is still required to provide the information requested in Table A and the illustrative project budgets.

For bidders that wish to suggest alternative engagement operating model (other than that proposed in Annex 1, Appendix D), please describe the alternative engagement operating model in I: Project Organigram of Annex 1, Appendix A: Part 3, Technical Proposal.

42.

Question: It is mentioned that our bid needs to be submitted by email only, but there it also mention that the technical offer and financial offer should be submitted in 2 different envelopes. Could you please clarify this point?

Answer: The submission should be in two separate emails. The technical proposal should be separate from the financial proposal. The reason is that in an RFP we have to open the technical proposal first, and that has to be evaluated, and only once we have completed the technical evaluation do we open the financial proposal of only those vendors who are deemed technically compliant. That is why we have a two email, or a two envelope, system of submitting an RFP.

Questions Submitted after the First Deadline 1.

Question: Can you confirm whether it is acceptable to bid on a country-by-country basis in the various regions or sub-regions.

Answer: Please refer to the question 39 above.

2.

Question: The table provides details of the various regions and sub-regions, and also includes Global Programmes. Please can you confirm whether it is acceptable to bid purely for the audit of projects that fall under the Global Programmes category (i.e. the firm does not bid for any of the other regions/sub-regional categories).

Answer: Yes, this is acceptable.. Global Programmes are HQ projects and considered a region. This possibility is allowed for by the bid submission formats in Annex 2.

3.

Question: Please can you confirm whether all audits for global programmes will be performed at UNHCR HQ in Geneva/Switzerland. If this is not the case, please can you provide details on the general geographical split of projects to be audited under Global

Page 13 of 23

Programmes category (for example, percentage that are expected to be audited in Geneva, percentage in Budapest, and any other countries where applicable). We fully appreciate that this would only be an indicative percentage and would not reflect an exact percentage of audits to be conducted per geographical location for global programmes.

Answer: No further information will be provided other than what is available in Annex 1, Appendix C. It should not be assumed that all Global Programme projects are based in Geneva as the location is project dependent.

4.

Question: In the case of Global programmes, which audit licence would be required? Would an audit licence from the bidders country of registration be sufficient, or would there be a requirement to have a Swiss audit licence (if the audits are being performed at HQ in Geneva) or a Hungarian licence (if the audits are being performed at UNHCR in Budapest) etc.

Answer: Going back to the earlier question, it is not safe to assume that these projects will take place in Geneva. The requirements will depend on where the audit is being executed. To give you an idea, global projects are mainly headquartered in New York, Geneva, and London. They are not generally in Budapest.

5.

Question: Can you provide a breakdown of the type of projects and $ values within Global Programmes category, in particular within the Division of external relations (these have a budget of US$ 34, 534,094). If it is possible to obtain similar information for projects in Europe, this would also be very helpful.

Answer: Information beyond that provided in Annex 1, Appendix C will not be provided.

6.

Question: Has UNHCR previously launched a similar framework contract for conducting these audits, particularly for projects that fall within Global Programmes. If these audits were not performed through a similar framework contract, please could you provide details of how these audits have previously been undertaken.

Answer: Refer to previous response. Audits were contracted at the country or unit level. This will be the first global tender for these services.

7.

Question: Will UNHCR facilitate travel to/in remote locations where commercial planes do not fly?

Answer: For remote locations we do not provide explicit support, however if it happens that in one location we have transport already we can provide this on a cost-reimbursable as-available basis. However, we do not make this commitment. We assist only when we can, when these resources are available.

8.

Page 14 of 23

Question: Will UNHCR facilitate accommodation while auditors work in remote locations, e.g., camp locations?

Answer: On a needs-available basis. If there is a spare room in a local office this may be provided, but the vendor is generally expected to be self-sustaining. Advice is likely to be provided, however this is also something that UNHCR will not make a commitment to.

9.

Question: Would UNHCR consider an alternative approach where for certain low risk projects required audits are conducted via electronic exchange of books and records, including electronic file interrogation of the Project Partners’ records, teleconferences, video conferences and other electronic approaches without actual on site presence? This approach would logically only be used in locations that are both low dollar value and low risk.

Answer: No. These approaches are not acceptable to UNHCR.

10.

Question: Would the UNHCR Audit Programme Coordinator(s) be based in Geneva, Budapest, NY, or elsewhere?

Answer: UNHCR program coordinators location is described in Annex 1, Appendix D.

11.

Question: Would UNHCR consider a bid that identifies the selected provider as “Primary” with respect to all audit projects, such that the provider can (while not guaranteed) reasonably determine that they will receive a substantial portion of the audit engagement in return for discounted pricing? As there are no volume guarantees within the RFP, the audit firm would otherwise not know if they were to be awarded 9 projects or 900 projects, making pricing difficult.

Answer: We have given indicative tables and subgroupings, and this would give an idea of the volume of UNHCR’s requirement. The volumes provided are, however, indicative only as situations and programs are subject to change. Vendors should be well-informed that UNHCR works on an as-required basis and will make no guarantees to minimum order quantities.

12.

Question: As an alternative, would UNHCR contemplate a volume discount arrangement whereby for volumes of audit project assignments, over and above certain thresholds, the rates tendered would be further discounted?

Answer: Yes, UNHCR would consider volumetric discounts. However pricing should be provided as is, as well as with potential price discounts. Arrangements such as this should be described as per the “Other innovative pricing proposals” section of Annex 2, Appendix D, as should any other innovative or best-value suggestions.

13.

Page 15 of 23

Question: Please confirm our understanding that the least acceptable bid is for a sub-region and not for a country.

Answer: Confirmed.

14.

Question: The scope of the assignment defined in Appendix A states that the audit opinion reporting framework should be under ISA 700 / 705 which in our view is for GAAP reporting (Normally IFRS or other GAAP authorised in each country). As the opinion is on cash basis and terms of agreements between UNHCR and partner we feel that the opinion should be based on ISA 800/805 instead. We would like this matter to be discussed and any concern with UNHCR communicated for resolution.

Answer: Both ISA 800 and 805 apply. It is important to note that para. 11 of ISA 800 states that “When forming an opinion and reporting on special purpose financial statements, the auditor shall apply the requirements in ISA 700.”

The format and content of the Auditor’s Report is to be in conformity with ISA 800 and 705.

Additional Questions Attendees were invited to ask additional questions at this time. 1.

Question: Will a list of attendees be provided? (Lynn Boston, of LubbockFine)

Answer: we can provide a list of companies which indicated an intention to attend, but have been unable to track the presence of actual people on the line.

Response after conference: Companies expressing interest to attend suppliers’ conference:

1. Asad Abbas & Co.

2. Baker Tilly Berk N.V.

3. CGIC Afrique International

4. Deloitte

5. Ernst & Young

6. Grant Thornton

7. INTERAUDITOR Neuner + Henzl

8. KPMG SA

9. LBC International

10. Lochan Co

11. LubbockFine

12. Moore Stephens

13. Nexia – Eurostatus Certified Auditors S.A.

14. PwC

15. REVIK d.o.o. SARAJEVO

16. RSM Tenon

Page 16 of 23

17. UHY Moreira Auditores

Page 17 of 23

Closing Remarks

Fatima Sherif-Nor thanked all the bidders for their interest, and noted that UNHCR will answer their further questions should they be provided by the deadlines. Please refer to the RFP/2013/550 Cover Letter for deadlines.

Isaac Mcekeni expressed appreciation for the vendors’ attendance at the conference, and their interest in working with UNHCR. Isaac Mcekeni also expressed an expectation that proposals would be received from the attending vendors.

Page 18 of 23

Questions received after suppliers’ conference and before September 5th 23:59 CET

1.

Question: Please send us Appendix, Part 1 through Appendix B of the RFP in WORD. We

need those pages in word to prepare our firm proposal faster.

Answer: Annex 2 is now provided in Word version.

2.

Question: The Project Partnership Agreement (PPA) is a standard contract, although

authorized amendments are permitted. How many of the PPA's are amended in this way. Is a

complete list of emended PPA's kept and is this available centrally? Specifically, regarding

paragraph 2.14.1 of the PPA, What is the percentage of respondents who ticked the first box

and the second box.

Answer: Amendments to the general articles of the PPA are rare and require the approval of

the UNHCR Controller and therefore a complete list of amended PPAs are maintained.

Regarding paragraph 2.14.1 of the PPA, the applicable box is ‘ticked’ by UNHCR. The use

of a pooled account is the exception and requires the advance approval of the UNHCR

Controller. The use of a pooled account may be is granted to partners who apply to the

UNHCR Controller for approval and have a strong history performance on UNHCR projects;

sound financial management framework and internal controls; and strong financial health at

the entity level for which the approval is being sought.

3.

Question: Does the UNHCR have its own definition of "conflict of interest" or any

expectations in this regard?

Answer: In answering this question, we assume that you are referring to the requirement of

the audit service provider to declare whether it has a conflict of interest with an auditee.

UNHCR does not have an internal “conflict of interest” definition that would be applicable to

Page 19 of 23

the provision of audit services. It is the expectation of UNHCR that audit service providers

would have their own definition used by firms to guide the work they accepted which was

aligned with professional ethical considerations. Details of the bidder’s approach to

identification of conflict of interest and supporting processes should be provided in E: Quality

assurance procedures, risk and mitigation measures Appendix A: Part 3, Technical Proposal.

4.

Question: Approximately what percentage of 2012 audit reports were clean/modified?

Answer: The majority of audit reports received unmodified opinions in 2012. UNHCR will

not provide further detail at this time.

5.

Question: Appendix B. of the financial proposal: The illustrative audit budget appears to be

a very critical element of the proposal and weighing. The time estimate, however, is heavily

dependent on the risk assessment and the type of expenditure (eg own payroll vs external

consultants) and the number of transactions. In order to ensure more comparability, the

UNHCR may like to expand on the guidance around the hypothetical project and also the

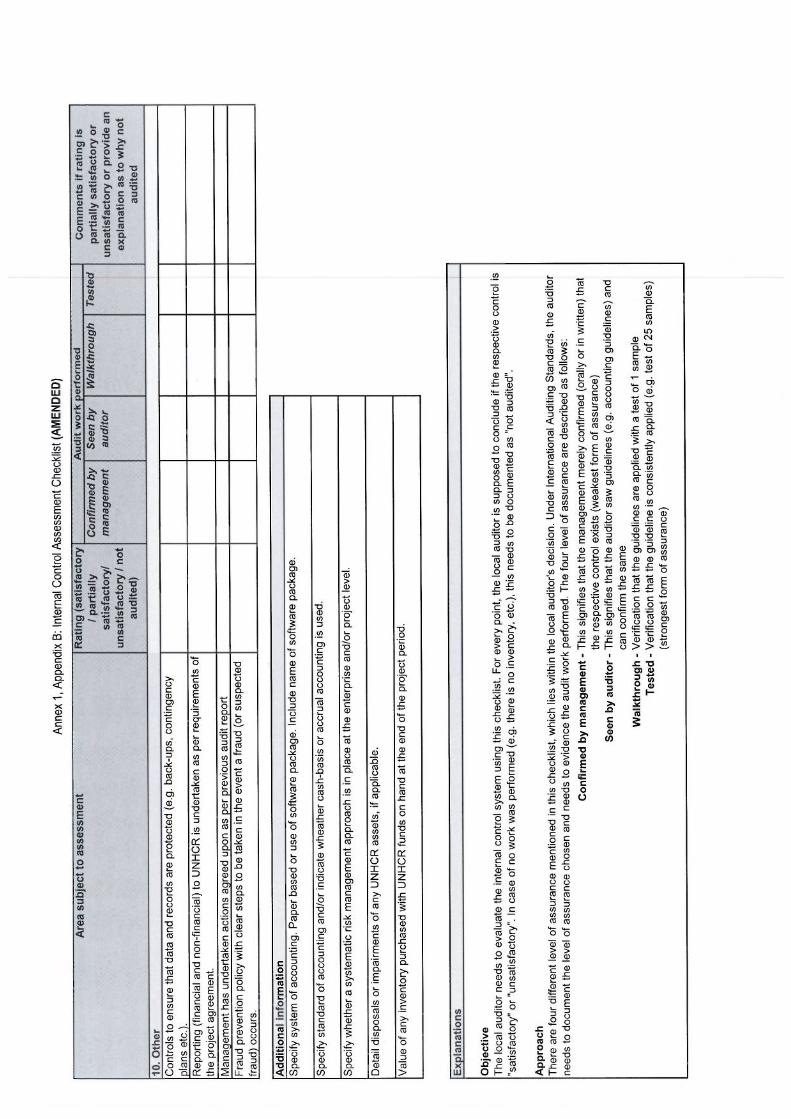

level of work expected on the ICS ("Confirmed by management /Seen by

Auditor/Walkthrough/Testing") and also confirm if coordination hours should be included in

such a budget.

Answer: Any and all costs associated (including coordination costs) should be included in the

illustrative audit budget. The more detail you provide, the better we are able to understand the

illustrative audit budget. Therefore, you may outline any assumptions you have made in

building the budget.

Please assume the following when building the illustrative audit budget:

- The auditee uses a separate bank account for all remittances and disbursements related to the

PPA.

- The auditee uses a standard off-the shelf accounting package.

- The auditee undergoes an annual external financial statement audit which has not been

qualified in the past three years.

Page 20 of 23

- UNHCR has not provided the auditee with inventory to distribute to persons of concern.

- UNHCR has not provided the auditee with assets on loan to carry out the project.

- Please use the following simple mock project budget to build your illustrative audit budget:

Description Budget (USD)

Fuel 40,000

Office rental 25,000

Personnel costs (salaries and benefits)

795,000

Travel costs 30,000

Training costs 15,000

Utilities (water, heat, electricity etc..)

12,000

Insurance 6,000

Bank fees 2,000

Transport contract 25,000

Maintenance Repair (equipment)

25,000

Other expendable office costs 25,000

Total budget 1,000,000

6.

Question: Appendix B. Table A. The preamble states that the rates should cover all costs

including coordination. The table however requests an hourly rate for the coordinator. Does

the UNHCR envisage a separate time budget for a global/regional coordinator or is it

expected that the costs for the coordination function are recovered through the field visits?

Answer: Any costs associated with the coordination function should be recovered through

each project audit budget.

7.

Question: In conjunction with other firms in various jurisdictions, we are considering

submitting a bid for a number of regions. The firm and other fellow bidders have audit

licenses that cover many countries, but not for every country in the various regions. Is it

acceptable for the other countries audits (those countries where lead firm and other members

Page 21 of 23

of the consortium do not have an audit license) to be covered by affiliates and subcontractors

that we would propose to include (and name) in our proposal.

Answer: Yes.

8.

Question: We would like to clarify whether UNHCR would expect audit firms with the local

license to provide audit opinions or whether it will always be the lead contractor that would

be required to sign off on individual audits with local firms with a license participating in the

audit?

Answer: We expect that lead contractor will be responsible for the overall quality delivery of

all services; however, the lead contractor does not necessarily have to sign-off on individual

audits. The signature on the audit report is dependent on the firm’s internal practices and that

which is required by the applicable jurisdictions.

9.

Question: Based on the teleconference and the ToR, we assume that the audit of any of the

projects in any of the regions would generally require an audit to be performed at the field

office in the respective country where the project is being implemented. However, we would

like to clarify whether the audit might also include work that would be required to be

performed at the HQ of the International NGO (wherever in the world this HQ might be

located). For example, for a project being implemented in Sudan – we assume the majority of

the audit would be performed at the field office in Sudan. However, please can you clarify

whether there would also be a requirement to perform some of the audit work for this project

at the International NGO HQ.

Answer: The audit work is generally performed at the field level – site of project

implementation and/or local office of an international NGO.

10.

Question: We would like to clarify whether there is always a requirement for the contractor

to have an audit license for the country in which the audit is to be performed. For example, if

a firm is awarded the contract, and an audit is required for a project being implemented in

Mauritania (which may include a field visit to the field office in Mauritania to perform part of

Page 22 of 23

the audit), but the International NGO for that project is in the UK (which may include a site

visit to the International NGO HQ in the UK to perform part of the audit) please can you

clarify whether:

a) a Mauritanian audit licence would be required by the firm?

b) a UK audit licence would be required by the firm?

Answer: Audits of projects implemented by international NGOs are typically performed in

the country of project implementation. In cases where projects are implemented in multiple

countries, UNHCR and the audit service provider will determine on a case-by-case basis the

appropriate approach.

11.

Question: With respect to Global Programmes, no specific locations for projects are

provided, but we understand from the teleconference that this category should also be treated

as a ‘region’. Please can you clarify, if the location of a project audit within this ‘region’ is

London, would the firm be required to have a UK audit licence?

Answer: Generally, this would be the case. However, in cases where projects are

implemented in multiple countries, UNHCR and the audit service provider will determine on

a case-by-case basis the appropriate approach.

12.

Question: Can a tenderer submitting a tender to be a global service provider be selected as

service provider for an individual region or sub-region if their tender is evaluated as the best

for that region / sub-region?

Answer: Yes.

13.

Question: When selecting contractors for a frame agreement it is common practice for

those contractors to be asked to engage in “secondary competition” before being awarded

individual purchase orders. In the suppliers’ conference you said that suppliers will be

appointed as auditors for regions or sub-regions based on their primary tender submission

and that there will be no secondary competition unless the appointed supplier does not

Page 23 of 23

perform adequately. Please can you reconfirm that this understanding is correct and that

there will be no secondary competition unless the supplier’s performance is inadequate?

Answer: Please refer to the written answers questions posed during the supplier’s conference

above.

14.

Question: Section 2.5.2. of the request for proposal states that for the financial evaluation

“the maximum number of points will be allotted to the lowest price offer…”. Following the

suppliers’ conference it still seems to be unclear how the price of each offer is calculated in

order to decide which is the lowest price offer. The issue is that the financial offer is made

up of two distinct components: the proposed rates and the illustrative budgets. It is not clear

how the evaluators will calculate the overall price of an offer from the proposed rates and

illustrative budgets. Is it possible to provide a worked example of how the financial proposal

will be scored?

Answer: Financial proposals shall be evaluated based on the following:

1. A pre-assigned scoring weight for proposed professional fees for key personnel

2. A pre-assigned scoring weight for the Illustrative audit project budgets

While UNHCR is not disclosing the exact weight given to each of those two components,

there is a heavier scoring weight given to the proposed professional fees (Table A). The

combination of these two components will be used to determine the lowest price offer.

The assessment of professional fees will be compared on a like-to-like basis with other

bidders.

The assessment of the illustrative audit project budgets will take into account bidders

proposed methodology contained in the technical proposal considering the best value for

money.