2. cost meeting discussion document jun 15

DESCRIPTION

ddTRANSCRIPT

Confidential Document

Cost Review Meeting Discussion Document (Main Slides: 3 - 19)

Cost Management & Review – CS& P

10th Jul’15

Board Room

2 Cost Management & Review Corporate Strategy & Planning 2

Performance: Jun’15 w.r.t ABP

3 3 Cost Management & Review Corporate Strategy & Planning

Production & Sales Performance w.r.t ABP: Jun’15

895 839 825

782 835

771 786

716 600

700

800

900

1000

HM CS WSS Sales

KT

ABP Actual

HM Pooling : ABP 21 KT, Act 32 KT

Hot Metal Crude Steel Saleable Steel & Sales

Main Reasons for variance w.r.t.

ABP

Jun’15:

H Blast Furnace-

Tuyere cooler repair- 15 Kt

Power dip- 10 kt

Lower agglomerate- 7 kt

I Blast Furnace-

Power dip– Impact 12 kt

Lower agglomerate- 5 kt

Rrescheduled MSD -30 kt

Main Reasons for variance w.r.t. ABP:

Jun’15:

Total shortfall 68 Kt:

LD#1 4 Kt

LD#2 44 Kt

LD#3 20 Kt

WOI including power failure: 22 Kt

Plant outages & interruptions: 46 Kt

Main Reasons for shortfall wrt ABP

Rescheduling of shutdown at LD#3.

HSM restricted production (ABP 350 kt act 341

kt) – roughing mill motor issue.

Crude Steel Stock (as on 30.06.15 in Kt):

Slab ABP- 23: Actual - 73

Billet ABP- 109 : Actual – 96

60 kt

39 kt 66 kt

68 kt

4 4 Cost Management & Review Corporate Strategy & Planning

Cost Performance: Jun’ 15 vs. ABP & Target

21489

26885

13561

19503

22489

27885

13497

19374 22031

27353

0

5000

10000

15000

20000

25000

30000

HM CS WSS Despatch

Rs.

/t

Target ABP Actual

129 Rs./t

64 Rs./t

W.r.t target 468 Rs./t

532 Rs./t

W.r.t target 542 Rs./t

458 Rs./t

5 Cost Management & Review Corporate Strategy & Planning 5

Stage wise Prod & cost variance analysis – Jun’15 (ABP vs. Act.)

May'15 Act.

Particulars

Jun'15 ABP Jun'15 Act. Var. (Act over

ABP)

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Raw Materials

1388 1348 OMQ (Total) 1402 1195 1345 1471 -57 276

195 3115 WB (Own Coal) 190 2737 191 2936 1 199

56 12540 Jharia (Own

Coal) 64 8458 55 11477 -9 3019

29 7302 Jharia (BCCL

Coal) 28 7288 31 8654 3 1366

6 Cost Management & Review Corporate Strategy & Planning 6

May'15 Act.

Particulars

Jun'15 ABP Jun'15 Act. Var. (Act over ABP)

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Iron Making

891 12799 Hot Metal 895 13561 835 13497 -60 -65

Steel Making Production & Conversion Cost

285 5654 LD1- Billet 274 5905 271 5418 -4 -487

338 5718 LD2- Slab 349 5683 305 5784 -44 101

213 6011 LD3- Slab 216 6407 196 6657 -20 250

LP - Mills Production & Conversion Cost

36 3374 WRM 32 4142 34 3164 2 -979

37 2571 MM 35 2696 38 2407 2 -289

78 1967 NBM 52 2937 75 2068 23 -869

FP - Mills Production & Conversion Cost

240 2101 HSM - HR (Gross) 350 1937 341 1790 -9 -147

208 2494 TSCR - HR (Gross) 211 2552 192 2514 -18 -38

157 4890 CRM 164 5398 151 5183 -13 -215

Overall Works Saleable Cost

278 19754 LP Saleable 271 20871 266 20233 -5 -638

446 22579 FP Saleable 555 23280 520 22950 -34 -329

725 21494 WSS 825 22489 786 22031 -39 -458

Stage wise Prod & cost variance analysis – Jun’15 (ABP vs. Act.)

June over May

Cost Management & Review Corporate Strategy & Planning 7

MAJOR KPIs – PLAN v/s ACTUAL

KPI UNIT FY’15 June ’15 April – June 15

ACT ABP ACT VAR ABP ACT VAR

POWER COST

Rs/Mwh

Rs Cr

3850

1441

3959

133

4014

124

55

9

3996

399

3905

368

91

31

OXYGEN COST Rs/T

Rs Cr

2666

478

2643

45

2623

39

20

6

2661

132

2633

118

28

14

MAINTENANCE

COST

Rs/Tss

Rs Cr

1284

1165

1416

117

1307

103

109

14

1300

308

1232

275

68

33

Power Rate Kwh/tss 406 394 381 13 406 408 2

Specific

Energy

Consumption

Gcal/tcs 6.012 5.915 5.802 0.113 5.876 5.782 0.094

Cost Management & Review Corporate Strategy & Planning

R1: Plant outage / Process disturbance : Crude Steel production loss at LD1 - 4 kt + LD2 - 49 kt = 53kt.

(Including impact of WOI - 22kt) .

R2 : Loss of production at Sinter Plant & Pellet Plant : (SP2) Breakdown in combustion air fan, interlock by

pass leading to belt failure & high nos. of

interruptions (8 kt)

(SP4) primarily due to sinter cooler breakdown (13kt)

(PP) due to voltage dip, gas shortage & dryer #1

discharge belt failure (17kt)

R3 : Demurrage Charges (Rs. 16 Crs.): Vessel: Rs.10.03 crs; Rail: Rs. 3.09 crs; EOL Rs.3.03 Crs.

R4 : Iron ore Mine :

i. Usage of bought out Iron ore : 104 kt - Rs. 49 Crs.

Opportunity loss: Jun’15 Rs. 114 Crs.

Internal factors: - Rs 65 Crs. External Factors

( Raw material ):-Rs 49 Crs.

47 2

16 65

49 114

0

20

40

60

80

100

120

R1 R2 R3 Sub Total R4 Total

Pooling (kt)

ABP : 21 MBP : 10 Act : 32 LD1 LD2 LD3 Total

ABP 274 349 216 839

MBP 274 354 194 822

Actual 271 305 196 771

Gap wrt ABP -4 -44 -20 -68

Gap wrt MBP -4 -49 2 -51

Crude steel prodn.(kt)

Cost Management & Review Corporate Strategy & Planning

Opportunity loss: (Rs. Crs).

72 112

366

480

618

159

85 77 57 56 49

75 45

52

45

53

56

58 55 56 46 65

0

100

200

300

400

500

600

700

800

Aug Sep Oct Nov Dec'14 Jan'15 Feb'15 Mar'15 Apr'15 May'15 Jun'15

External factors Internal factors

Total : 672

Total : 215

Total : 143 Total : 132

Total : 147

Total : 525

Total : 418

Total : 157

Total : 112 Total : 101

1) Total opportunity loss reducing due to

resumption of iron ore mines operation.

2) Opportunity loss due to internal factors

remain unchanged ( Rs. 50-55 Crs pm )

Total : 114

Cost Management & Review Corporate Strategy & Planning 10 Cost Management & Review Corporate Strategy & Planning

Production & Sales Performance: Q1 FY16 vs. ABP & Target

2654 2429 2372 2253

2588 2345 2229 2144

600

1100

1600

2100

2600

3100

HM CS WSS Sales

KT

ABP Actual

HM Pooling : ABP 124 KT, Act 145 KT

Hot Metal Crude Steel Saleable Steel & Sales

Main Reasons for variance w.r.t.

ABP

Jun’15:

Power dip (~15 Kt)

H BF Tuyere cooler repair (15 Kt)

Plant outage & interruptions (36 Kt)

Main Reasons for variance w.r.t. ABP:

Jun’15:

Primarily in LD#2 (Plant outages /

interruptions & WOI)

Main Reasons for shortfall wrt ABP

Lower crude steel (84 Kt).

Break down at HSM

Crude Steel Stock (as on 30.06.15 in Kt):

Slab ABP- 23: Actual - 73

Billet ABP- 109 : Actual - 96

66 kt

143 kt 109 kt 84 kt

Cost Management & Review Corporate Strategy & Planning 11 Cost Management & Review Corporate Strategy & Planning

Cost Performance: Q1 FY16 vs. ABP & Target

21724

26944

13704

19735

22724

27944

13227

19025 21817

26943

0

5000

10000

15000

20000

25000

30000

HM CS WSS Destatch

Rs.

/t

Target ABP Actual

711 Rs./t

477 Rs./t

W.r.t target 93 Rs./t

907 Rs./t

1001 Rs./t

Reached Target

12 12 Cost Management & Review Corporate Strategy & Planning

Projection- Jul’15

13 13 Cost Management & Review Corporate Strategy & Planning

Jul’15 : Production Projection (1/2)

ABP Proj. VAR.

835 Hot Metal Kt 887 898 11

271 LD#1 Kt 284 284 0

305 LD#2 Kt 329 347 18

196 LD#3 Kt 231 231 0

34 WRM Kt 28 37 9

38 MM Kt 37 37 1

75 NBM Kt 78 53 -25

341 HSM (Gross) Kt 255 290 35

192 TSCR (Gross) Kt 225 225 0

151 CRM Kt 16 89 72

786 WSS Kt 759 789 30

Jun

ActFacilities UoM

Jul-15

14 14 Cost Management & Review Corporate Strategy & Planning

Jul’15: Projection (Stage wise Incremental Cost) (2/2)

ABP Proj. VAR.

13497 Hot Metal Rs/t 13511 12960 -551

5418 LD#1 Rs/t 5783 5768 -15

5784 LD#2 Rs/t 5939 5517 -422

6657 LD#3 Rs/t 6373 5874 -498

3164 WRM Rs/t 4335 3285 -1050

2407 MM Rs/t 2675 2590 -85

21 NBM Rs/t 2315 3361 1046

1790 HSM (Gross) Rs/t 2283 2121 -162

2514 TSCR (Gross) Rs/t 2469 2348 -121

5183 CRM Rs/t 24489 7932 -16557

22031 WSS Rs/t 22076 21479 -596

Jun

ActFacilities UoM

Jul-15

15 Cost Management & Review Corporate Strategy & Planning 15

Quarter wise Production & Cost Trend

16 Cost Management & Review Corporate Strategy & Planning 16

Production Trend- Q1 FY’16: WSS production is lower by 143 Kt Q2 proj. as per ABP

2528 2676 2654 2588 2650 2661

867 892 895

887 894 869 862 891 835

898 894 869

Q1 FY'15 Q4 FY'15 Q1 ABPFY16

Apr'15 May'15 Jun'15 Q1 FY16 Jul'15 Aug'15 Sept'15 Q2'15ABP

Q2'15Proj

Kt

ABP Act./Proj.

2334 2441 2430 2345 2513 2531

788 802 839

844 870 799 738 836 771

862 870 799

Q1 FY'15 Q4 FY'15 Q1 ABPFY16

Apr'15 May'15 Jun'15 Q1 FY16 Jul'15 Aug'15 Sept'15 Q2'15ABP

Q2'15Proj.

Kt

ABP Act./Proj.

CS

2250 2389 2372 2229 2420 2412

769 778 825

759

854 806

718 725 786

789

818 805

Q1 FY'15 Q4 FY'15 Q1 ABPFY16

Apr'15 May'15 Jun'15 Q1 FY16 Jul'15 Aug'15 Sept'15 Q2'15ABP

Q2'15Proj.

Kt

ABP Act./Proj.

WSS

HM

17 Cost Management & Review Corporate Strategy & Planning 17

WSS Cost Trend –FY’16 Q1 cost lower than ABP Rs. 907, but higher than target by 93/t

22198

21198

22724

21724 21817 22278

21278 21714

22670 23026 22489

22076 22484 22250

21924 21494 22031

21529 21611 22000

FY'16ABP

Fy16Target

Q1FY'16ABP

Q1 FY16Target

Apr'15 May'15 Jun'15 Q1FY'16Act

Jul'15 Aug'15 Sept'15 Q2'15ABP

Q2'15Target

Q2'15Proj.

Rs/

tss

ABP Target

Impact of MMDR act has been included in WSS cost

from Apr’15 onwards

* Does not include DMF impact Rs. 75 crs (~700-800/t), but taken in despatch cost

Actual

18 Cost Management & Review Corporate Strategy & Planning 18

FY16 Operating profit commitment to Board

2000

ABP Additional target Commitment toBoard

Operating Profit (Rs. Crs.)

(Rs. 2000/t)

H1 FY16: Expected shortfall: Rs. 250-300/t Make up target for Q2 to achieve Board commitment: Rs. 500-600/t

H2 FY16: Based on current projection: HRC price drop by $40-50/t New MMDR Act, 2015: ~Rs. 1200/t

Shortfall: ~Rs. 2000/t

1

2

Gap wrt Target

19 Cost Management & Review Corporate Strategy & Planning 19

Key items for discussion: Q2 FY16

Production 1. Plant Availability:

Headroom by 10-15%. 2. Operational efficiency

1

2 Monsoon

Moisture in raw materials Longer recovery time Raw materials supply disruptions Adverse impact on Production & KPIs

3 High Imported Coal stock

Imported coal inventory as on 30th June ‘15 was 1.6 MnT (118 days consumption), significantly higher compared to FY13- FY14 700-800 KT (60-70 days)

Adverse impact on profitability : Rs. 60-80 Crs. p.a.

Counter measures to mitigate the impact

Action plan to be checked. Part of Agenda item.

Current rate of production is not adequate (lower by ~7%) to achieve

2.53 MnT of crude steel production in Q2 FY16

Expediting improvement projects implementation through SHIKHAR 25

20 20 Cost Management & Review Corporate Strategy & Planning

End of main discussion document

Thank you… Back up in subsequent slides

21 Cost Management & Review Corporate Strategy & Planning 21

13561 276 108 102 64 399 215 13497

R1 R2 R3 R4 R5 R6

R1: Higher captive iron ore price (ABP: Rs. 1605/t , Act: Rs. 1845/t)

R2: Impact of lower HM production (ABP : 895 kt , Act : 835 kt)

R3:Higher captive coal price - Jharia: Rs. 2171/t , WB: Rs. 104/t (Jharia - ABP: Rs. 8676/t , Act: Rs. 10727/t ; WB – ABP: Rs. 3318/t, Act: Rs. 3423/t)

R4:Higher flux consumption (ABP: 182 kg/thm, Act: 221 kg/thm)

R5: Lower usage of purchased iron ore (ABP: 146 kt, Act: 104 kt)

R6: Lower requirement of imported coal (ABP: 504 kt, Act: 456 kt)

AB

P

Hot Metal Cost variation (ABP vs Actual): Jun’15 (Rs./thm)

Cost is lower by Rs. 65/thm

Low

er U

sage

of

Pu

rch

ased

Met

allik

s

Hig

her

Cap

tive

C

oal

Pri

ce

AC

TUA

L

Hig

her

Flu

x C

on

sum

pti

on

Hig

her

Cap

tive

Ir

on

Ore

Pri

ce

Imp

act

of

Low

er

pro

du

ctio

n

Low

er R

equ

irem

ent

of

Imp

ort

ed C

oal

22 Cost Management & Review Corporate Strategy & Planning 22

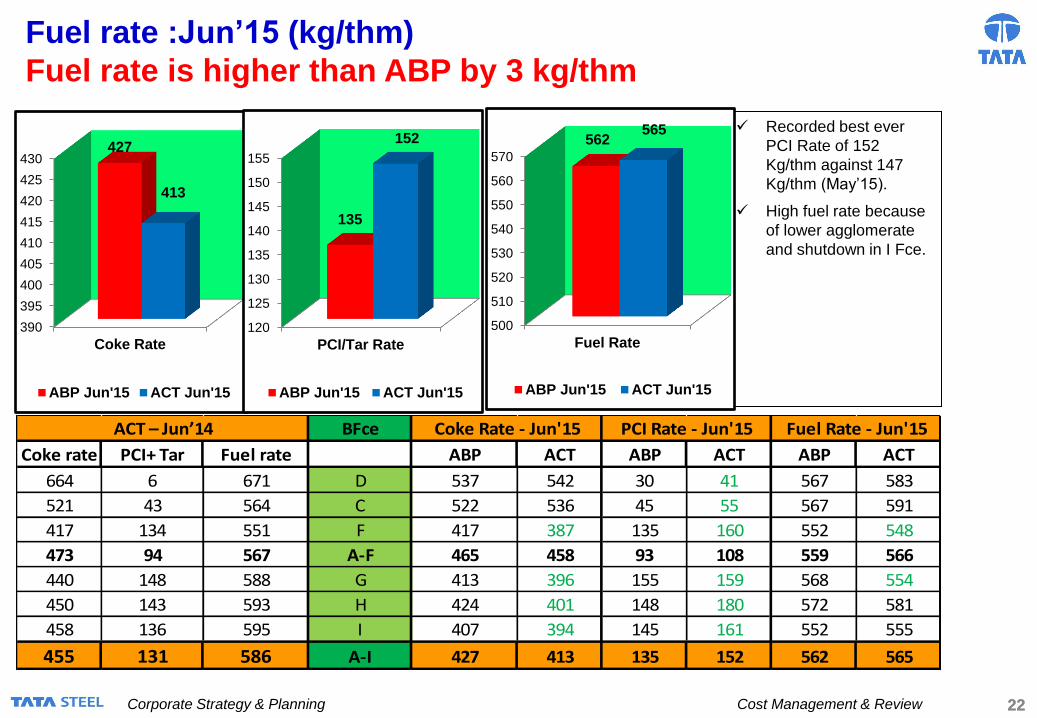

Fuel rate :Jun’15 (kg/thm)

Fuel rate is higher than ABP by 3 kg/thm

Recorded best ever

PCI Rate of 152

Kg/thm against 147

Kg/thm (May’15).

High fuel rate because

of lower agglomerate

and shutdown in I Fce.

390

395

400

405

410

415

420

425

430

Coke Rate

427

413

ABP Jun'15 ACT Jun'15

120

125

130

135

140

145

150

155

PCI/Tar Rate

135

152

ABP Jun'15 ACT Jun'15

500

510

520

530

540

550

560

570

Fuel Rate

562 565

ABP Jun'15 ACT Jun'15

BFce

Coke rate PCI+ Tar Fuel rate ABP ACT ABP ACT ABP ACT

664 6 671 D 537 542 30 41 567 583

521 43 564 C 522 536 45 55 567 591

417 134 551 F 417 387 135 160 552 548

473 94 567 A-F 465 458 93 108 559 566

440 148 588 G 413 396 155 159 568 554

450 143 593 H 424 401 148 180 572 581

458 136 595 I 407 394 145 161 552 555

455 131 586 A-I 427 413 135 152 562 565

Fuel Rate - Jun'15ACT – Jun’14 Coke Rate - Jun'15 PCI Rate - Jun'15

23 23 Cost Management & Review Corporate Strategy & Planning

Coke Cost Jsr Plant : June’15 (Rs.828/t lower than ABP)

Lower cost due to favorable domestic coal blend (ABP : 38%, ACT :47%)

Coke Yield (BF+Nut)

Prod'n Tons Coal Tar (631) (682) (51) ABP 68.9%

ABP 269480 Coke Breeze (605) (637) (32) Act 68.7%

Act 264676 CO gas credit (2425) (2629) (204) Impact 29

Impact 39 Total -3,660 -3,947 -286

Rs./ton

ABP - June'15 10,727

ACT - June'15 9,898

Adv/Fav() -828

variance variance Coal Mix (748)

Wages 43 Fuel cost -149 Coal Price 253Stores & Refactory 38 Utilities 15 Coal H'ndlng (8)

Maint -86 Misc exps 32 Total -503

Total Impact -5 Total Impact -102

Coal

BlendABP % Act %

ABP

Price/t

Act

Price/t

Price

Var'nce

Mix

VariancJamadoba Coal 8% 8% 9,448 12,208 300 46W Bokaro Coal 30% 39% 3,587 3,756 96 461Imp Semi Soft 35% 26% 9,460 9,333 -54 -1,278HCC 27% 27% 9,975 9,750 -88 22

100% 100% 7835 7510 253 -748

Prod'n Impact(BF+Nut)

Coal CostFixed cost Fuel & Utilities

Credits

24 24 Cost Management & Review Corporate Strategy & Planning

HMC Gross Coke cost : Jun’15 (Rs.1003/t higher than ABP)

Higher cost mainly due to higher imported coal in blend.

25 25 Cost Management & Review Corporate Strategy & Planning

Change

Qty (kt) Blend % Qty (kt) Blend % Blend %

Jharia 87 11% 69 10% -2%

West Bokaro 174 23% 198 27% 5%

Total Captive (A) 261 34% 267 37% 3%

SS (Imported) 170 22% 140 19% -3%

HCC (Imported) 202 26% 178 25% -2%

Total Imported Coking Coal (B) 372 49% 318 44% -5%

PCI 132 17% 137 19% 2%

Total Imported non-Coking Coal (C) 132 17% 137 19% 2%

Total Imported Coal (B+C) 504 66% 456 63% -3%

Total Coal (A+B+C) 765 100% 723 100% 0%

Wet CoalABP-Jun'15 ACT-Jun'15

# Jharia coal supply was lower by 5 kt (ABP : 92 kt, Act :87 kt),

W Bokaro coal supply higher by 5 kt (ABP : 190 kt, Act :195 kt).

#

Coal Blend : Jun’15 Favorable coal blend : Higher Captive coal availability.

26 26 Cost Management & Review Corporate Strategy & Planning

Sinter Cost variation : Jun’15 (ABP vs ACT) (Lower than plan by Rs. 153/tns)

*Use of purchased

iron ore –

ABP:146 kt,

Act:101 kt

*

27 27 Cost Management & Review Corporate Strategy & Planning

Pellet Cost variation : Jun’15 (ABP vs ACT) (Lower than plan by Rs.82/t)

Cons Rate Cons Rate Cons Rate Cons Rate

kg/t Rs/t kg/t Rs/t GCL/t Rs/GCL Kg/t Rs/t

ABP 1135 1699 31 1300 48 1680 73 4358

Act. 1066 1838 21 1300 58 1578 73 4178

Impact (Rs/t) -116 149 13 0 16 (6) (1) (13)

Net Impact (Rs/t) 33 13 10 (14) (82)

Production(KT) Rs/t

ABP 520 ABP 3368

Act. 443 Act. 3285

Production

variance(77) Adv(+)/Fav(-) (82)

3 0 (45)

Stores&

RefractoryMaint

Fixed Cost-

Price

Impact

Fixed Cost-

Qty Impact

Cons Rate Cons Rate

KWH/t Rs/KWH Rs/tnp Rs/tnp Rs/tnp Rs/tnp kg/t Rs/t

ABP 49.0 3971 45 230 315 268 103 3341

Act. 49.2 4014 31 163 270 315 90 3276

Impact (Rs/t) 1 2 (14) (67) (45) 47 (42) (6)

Net Impact (Rs/t) 3 2 (48)

PowerSolid Fuel + Coal

Tar+Others

Fe Bearing Material Return Fines CO Gas Flux

28 28 Cost Management & Review Corporate Strategy & Planning

A-I Blast Fce Cost variation : Jun’15 (ABP vs ACT) (Lower than plan by Rs.65/thm)

Prices ABP Act

Power Utility Sinter 4269 4075

Rate Rate Cons Rate Cons Rate Cons Rate Pellet 3368 3287

Rs./thm Rs./thm Kg/t Rs./t GCL/t Rs./GCL Kg/t Rs./t Sz Ore 1763 2333

ABP 140 416 172 1,651 0.50 350 1,576 3,491

Act 113 423 135 2,426 0.48 339 1,604 3,404 Cons(Kg/thm) ABP Act

(61) 105 (6) (5) 95 (140) Sinter 724 653

Net Impact (27) 7 44 (12) (46) Pellet 567 583

Lump ore 285 368

Total 1576 1604

Rs./thm

ABP 895 ABP 13,561

ACT 835 ACT 13,497

Production

variance 60 Adv(+)/Fav(-) (65)

Lower fixed cost 36

Rs./thm Rs./thm Rs./thm Cons Rate Cons Rate Prices ABP Act

Kg/t Rs./t Kg/t Rs./t

ABP (389) ABP 440 ABP 363 ABP 16 2,582 562 11,183 Coke 11920 11390

Act (377) Act 426 Act 439 Act 40 2,678 565 10,768 PCI 8692 8865

61 4 28 (234) Tar 17250 17400

12 Net Impact (15) 76 65 (206) Total 11183 10768

Rs./t

Rs./t

Industrial Gases Gaseous Fuel Fe Bearing Mat

Production Impact (KT)

Stores & Refractory + SS Maint. FuelFluxBF Gas Credit

Plan Act

Sinter 46% 40.72%

Lump 18% 20%

Pellet 36% 36%

Agglomerate 82% 77%

Kg/t ABP ACT

Coke Rate 427 413

PCI+Tar 135 152

Fuel Rate 562 565

29 29 Cost Management & Review Corporate Strategy & Planning

LD#1: Cost Analysis Jun’15 (ABP vs. Actual)

(13) (81) (26)

274

Cons

(kg/t)

Rate

(Rs/t)

Cons

(kg/t)

Cons

(kg/t)

Cons

(kg/t)

Rate

(Rs/t)271

ABP 1040 13561 65 76 20.0 53982

Actual 1043 13497 54 71 19.4 42048

Impact

(Rs/t)38 (51) (144) (44) (35) (9)

Net Impact

(Rs/t)(13) (26)

HM+Scrap Consn.(kg/t)

ABP 1105

Actual 1097 Rs/t

19466

18914

(551)

(67) (176) 4 (41) (10) 18 81 18

Stores R&M PowerFuel &

Gases

LS from

LD 3Others

Scrap

Credit

Fixed

CostRs. Cr.

Cons

(kg/t)

Rate

(Rs/t)Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t

ABP 6.80 66912 329 335 373 348 430 -590 710 19 5905

Actual 6.42 66130 262 159 378 307 401 -510 729 20 5418

Impact

(Rs/t)-25 (5) (67) (176) 4 (41) (10) (29) 81 18 0.03 (487)

Major Reasons in detail :

Consn. -301

R1: Credit for Muck returned to IBMD, which was booked as scrap cons in earlier months: 3.5 Kg/tcs Price -201 Lower HM Si - 1.5 Kg/tcs ( Pan - 0.92, Act 0.87 ) Volume 15 Scrap : Lower Scrp cons in overall mix : HM has higher Fe than Scrap - 1 Kg/tcs , Lower Slag Fe - 0.5 Kg/tcs Total -487

R3: Lower HM Si by 0.05 ^% - 3.5 Kg/tcs, Usage of LF Slag - Net Lime cons lower by 0.5 Kg/tcs

R6: Charging for 90 tons of tundish material not charged in June as MR was put up late : 0.32 Kg/tcs

R7: Electrodes could not be charged - as reservation was made late : 17 Rs/t. Will be a cost spillover to July

R8: Lower Vol- 4 Rs/t F , Exp - 180 Rs/t A - R & M Exp of 4.80 crs deferred to Sep 15 (B scheme of ID fan impeller of Rs 3.40 Crs

and normal expenditure of Rs 1.40 Crs )

R13: Better Yield

R14: Lower volume - 10 Rs/t , Higher exp ( GW )- 8 Rs.t

Cons

(kg/t)

(154)

9283

(27) (81)

(10) 17

0.80

1.10

Production (Kt)

DS Compound

Actual

Actual

Actual

ABP

ABP

LD 1 Billet

Works Cost

Var.

(17)

(154) (27)

Rate

(Rs/t)

Rate

(Rs/t)

Rate

(Rs/t)

592361549315311

Hot Metal Scrap Consumed Lime Ferro Alloys ABP

9047 61039

(551)

(47)

(5) (487)

Refractories

Var.

LD 1 Billet

Conversion Cost

R1 R2 R3 R4

R6 R7 R8 R9 R10 R11 R13R12 R14

R5

30 30 Cost Management & Review Corporate Strategy & Planning

LD#2 & SC: Cost Analysis Jun’15 (ABP vs. Actual)

88 56 (169) (139)

Scrap Credit Prodn :

ABP 349

Act. 305

ABP 1039 13561 70 66 10.18 125573 -442 -44

Act. 1051 13497 71 75 9.52 116439 -581

Impact (Rs/t) 155 (67) 22 88 (82) (87)

Net Impact

(Rs/t)88 (169) (139)

Yield Impact (3)

HM + Scrap:-

ABP 1109

Act. 1122 Rs/t

19244

19281

36

38 15 35 (49) 97

Stores R&M PowerFuel &

GasesFixed Cost

Cons

(kg/t)

Rate

(Rs/t)Rs/t Rs/t Rs/t Rs/t Rs/t Rs cr Rs/t

ABP 5.65 75823 207 195 223 374 568 20 5683

Act. 6.28 70469 245 210 258 326 666 20 5784

Impact (Rs/t) 14 38 15 35 (49) 97 0 101

Major Reasons in detail :

Cons 125

Vol 124

Price/ Exp (148)

R7 Rs 1.5 Crs was spend more than plan in June, however YTD cost is lower than plan (ABP Rs 21 Crs Act : Rs 20 Crs) Total 101

R9 & R12 Higher due to lower Vol Impact

HM Scrap

94

(45)

Rate

(Rs/t)

94

Rate

(Rs/t)

Cons

(kg/t)

Rate

(Rs/t)

Lime Ferro Alloys

LD 2 Slab

Works Cost

16053

16533

34

56

9834

9914

Rate

(Rs/t)

Cons

(kg/t)

Rate

(Rs/t)

Cons

(kg/t)

Cons

(kg/t)

6

14

36

RefractoriesLD 2 Slab

Conversion Cost

ABP

Var.

Others

Rs/t

(45)Act.

Var.

ABP

Act.

101

R3 Impact of higher HM P (20% increase in HM P >0.18) : 2.5 kg/tcs, Higher HM Si (0.78%): 1 kg/tcs, Capoff 0.5 kg/tcs,

V1 high life 1.5kg/t

R6 0.55 Kg/tcs :Vessel Relining bricks & Ladle bricks excess drwan in June'15 to be set off with July'15

0.08 Kg/tcs :a) Increase in DS lance Consumption due to increase in chokage of lances : 0.01 Kg/tcs

b) Increase in LF bush & lances Consumption due increase in LF failures : 0.03 Kg/tcs

c) Increase in Vessel Maintenance due to vessel #1 (running at 4450 Heats) : 0.04 Kg/tcs

R8 Lower Vol Impact Rs28/t (A) & Expenditure by Rs13/t (F) (R & M B scheme of Vessel # 1 Hood of Rs 0.80 Crs not charged

due to deferement of hood change to Jan'16

506

551

R1 R2 R3 R4 R5

R6 R7 R8 R9 R10 R11 R12

31 31 Cost Management & Review Corporate Strategy & Planning

LD#3 & TSC: Cost Analysis Jun’15 (ABP vs. Actual)

(483) (89) 227

Scrap Credit Prodn :

Cons

(kg/t)

Rate

(Rs/t)

Cons

(kg/t)

Cons

(kg/t)

Cons

(kg/t)

Rate

(Rs/t)Rs/t ABP 216

ABP 1048 13561 70 81 10.21 132617 -599 Act. 196

Act. 1018 13497 99 77 10.25 123405 -372 Gap -20

Impact (Rs/t) (418) (65) 462 (37) 6 (94)

Net Impact (Rs/t) (483) (89) 227

Yield Impact (1)

HM + Scrap:-

ABP 1118

Act. 1117 Rs/t

19968

20154

185

75 90 40 (31) 127

Stores R&M PowerFuel &

GasesFixed Cost Rs cr

Cons

(kg/t)

Rate

(Rs/t)Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t

ABP 5.97 79664 420 319 298 335 651 14 6407

Act. 5.91 74516 496 409 338 304 778 15 6657

Impact (Rs/t) (35) 75 90 40 (31) 127 1.2 250

Major Reasons in detail :

R3 Due to low HM Si lead to lower consumotion of lime. Operating at lower basicity as vessels are new lead to lower consumption of lime Cons 223

R7 Mould woth Rs 1.5 Crs planned for May has been changed in June'15 Vol 106

Price/ Exp (79)

Total 250

R9 Due to consumption Rs 36/t (A) & due to rate Rs 4/t(A)

R12 Due to higher expenditure Rs 61/t & due to lower voluume Rs 65/t

(115)

Ferro Alloys

Rs/t

607

491

ABP

R8 Mech -Expenditure related to operation of 1.07 Crs was wrongly charged in mechanical , which will be reversed in July

IEM - Preponement of R & M B scheme of Crane drive fan, FDA revival spare , Fire coating & WCC Hose of Rs 0.38 Crs and

higher normal expenditure of Rs 0.11 Crs due to charging of Crane servise (track rail & DSL) & Rope which was not in plan

Var.

HM Scrap Lime

(35)

Refractories

Rate

(Rs/t)

Rate

(Rs/t)

(1) (44)

(81)

Others

(115)

(81)461

ABP

Act.

Act.

Var.

15570 9950

15559 9379

250

LD 3 Slab

Conversion Cost

461

185

LD 3 Slab Works Cost

R1 R2 R3 R4 R5

R6 R7 R8 R9 R10 R11 R12

32 32 Cost Management & Review Corporate Strategy & Planning

WRM(E): Cost Analysis Jun’15 (ABP vs. Actual)

(22)

ABP 32.0

Yield %Cons

(kwh/t)Actual 34.4

ABP 97.52% 121

Actual 97.52% 121

Impact(Rs/T) 0 (1)Net Impact

(Rs/T)

Rs/t

25008

23575

(1433)

(11) (797) (23) (64)

Stores R&MFuel &

GasesOthers Rs Cr.

Rs/t (Rs/t) Rs/t Rs/t Rs/t

ABP 290 1172 339 481 4.1 4142

Actual 279 375 316 417 4.2 3164

Impact

(Rs/T)(11) (797) (23) (64) 0.11 (979)

Major Reasons in detail :

Consn. 10

R5: Higher Vol 81 Rs/t F , Lower Spend 715 F ( R & M B schemes of Electrical and Price -819

maintenance not carried out due to deferment of MSD - 1.70 crs) Volume -170

R8: Higher Volume - 88 Rs/t F , Higher Exp 33 A Total -979

ABP

(466) 5

(55) (979)

Actual

Rate

(Rs/t)

Rate

(Rs/KWh)

Var.

(465) 5 (22)

(1433)

Rs/t

WRM Works Cost

20866 3.97 -425

20411 4.01 -447

(465) 5 Production (Kt)

Power Scrap Credits

(55) Var.

Fixed Cost WRM Conversion Cost

1274 ABP

1219 Actual

Rs/t

R5 R6 R7 R8

R2R1 R3

R4

33 33 Cost Management & Review Corporate Strategy & Planning

MM: Cost Analysis Jun’15 (ABP vs. Actual)

27

ABP 35

Yield %Cons

(kwh/t)Actual 38

ABP 97.26% 61Actual 97.27% 45Impact (Rs/T) (3) (62)Net Impact

(Rs/T)

Rs/t2166120800

(861)

(62) (22) (46) (46)

Stores R&M Fuel &

GasesOthers Rs Cr.

Rs/t Rs/t Rs/t Rs/t Rs/tABP 165 344 534 358 3.3 2696Actual 103 322 488 312 3.3 2407

Impact (62) (22) (46) (46) 0.0 (289)

Major Reasons in detail :

Cons -65

R2: Reversal of excess energy consmption, wrongly booked last month. Price -141

R4: Extra charging of packaging bills of last month , reversed : 30 Rs/t F Volume -84

R5 / R 8 : Favourable Volume impact Total -289

(861)

(589) 2

(591) (60) 27

18393

Rate

(Rs/t)

Rate

(Rs/KWh)Rs/t

18966 3.97 -4184.01 -391

(591) (60) Production (Kt)

Power Scrap Credits

MM Works Cost

ABPActualVar.

(63) (289)

Fixed Cost MM Conversion Cost

Rs/t937 ABP874 Actual(63) Var.

R5 R6 R7 R8

R2R1 R3

R4

34 34 Cost Management & Review Corporate Strategy & Planning

NBM: Cost Analysis Jun’15 (ABP vs. Actual)

14

ABP 52

Yield %Cons

(kwh/t)Actual 75

ABP 96.60% 105Actual 96.60% 93Impact (Rs/T) (0) (49)Net Impact

(Rs/T)

Rs/t2190320505

(1398)

(57) (188) (29) (360)

Stores R&M Fuel &

GasesOthers Rs. Cr.

Rs/t Rs/t Rs/t Rs/t 3.45 Rs/t

ABP 231 440 382 540 3.59 2937Actual 174 253 353 180 2068Impact

(Rs/T)(57) (188) (29) (360) 0.14 (869)

Major Reasons in detail : Cons . -49

R2/R4/R5/R7/R8: Favourable impact of higher volume ( Postponment of SD to July ) Price -481

Volume -339

Total -869

(548) 4

664

Rs/t

ABP

(548) (45) Production (Kt)

Power

ABP

Rate

(Rs/t)

Scrap Credits

(1398)

18966 3.97

Rs/t

NBM Works Cost

-404

(548) (45)

18436 4.01

Rate

(Rs/kwh)

14

-390

NBM Conversion Cost

Actual

Fixed Cost

Var.

(869)

479 Actual

Var.

(185)

(185)

R5 R6 R7 R8

R2R1 R3

R4

35 35 Cost Management & Review Corporate Strategy & Planning

HSM: Cost Analysis Jun’15 (ABP vs. Actual)

(7) (17) (1) (1)

Prodn :

Yield Cons Rate Cons Rate ABP 350

(%) (Gcal/t) (Rs/GCal) (kwh/t) (Rs/kwh) Act. 341

ABP 98.20% 0.272 1097 87 3.97 -9

Act. 98.21% 0.272 1073 82 4.01

Impact (Rs/t) (2) (0) (7) (21) 3

Net Impact (Rs/t) (7) (17)

Yield Impact (2)

Rs/t

ABP 21181

Act. 20935

Var. (246)

(43) 24

Stores R&M Rs cr

Rs/t Rs/t Rs/t

ABP 89 319 14 ABP 1937

Act. 46 343 14 Act. 1790

Impact (Rs/t) (43) 24 (0.2) Var. (147)

Major Reasons in detail : Cons (15)

Vol 21

Price/ Exp (154)

Total (147)

HSM Conversion Cost

412

HSM Works Cost

Rolls

(246)

(54) (147)

Rs/t

161

-216

(1)

Rate

(Rs/t)

19244

19145

(101)

417

Input Slab Fuel Power

Packing Fixed Cost

6 (25)

Credits

Rs/t

(25)

Others

136

Rs/t

(103)

-215

(103)

41 53

Rs/t Rs/t

95 78

R10 Due to lower volume

R6 Due to lower volumes Rs13/t and Rs 11/t due to clearing pending service bills

(54) (25) 6(25)

R5 R6 R7 R8 R10

R2R1 R3 R4

R9

36 36 Cost Management & Review Corporate Strategy & Planning

TSC Rolling: Cost Analysis Jun’15 (ABP vs. Actual)

(40) 6 18

Cons. Cons Rate Cons Rate Prodn:

(Kg/t) (Gcal/t) (Rs/GCal) (kwh/t) (Rs/kwh) ABP 211

ABP 97.53% 0.199 1363 115 3.97 Act. 192

Act. 98.20% 0.185 1253 115 4.01

Impact (Rs/t) (139) (19) (20) 1 5

Net Impact (Rs/t) (40) 6

Yield Impact 3

Rs/t

ABP 22520

Act. 22645

Var. 125

(42) 53 (5) 13

Stores R&M Rs cr

Rs/t Rs/t Rs/t

ABP 105 281 14 ABP 2552

Act. 62 334 14 Act. 2514

Impact (Rs/t) (42) 53 (0.0) Var. (38)

Major Reasons in detail :

Cons (138)

Vol 99

Price/ Exp 2

R7 Due to two new rolls that has been drawn, howevr YTD cost is as per plan. Total (38)

R10 Due to lower volume

CreditsRate

(Rs/t) Rs/t

TSCR Conversion

Cost

27 18

125

TSCR Works Cost

31 63 (38)

27

165 666

196 729

Rolls Fixed Cost

19968 -117

20130 -98

165

Input Fuel Power

R6 Due to Entry guide & Exit Guide of finishing stands F#1 to F#6 of Rs 0.70 Crs charged in June which was plan in

May and higher normal expenditure of Rs 0,26 Crs due to shut down

120

115

(5)

Others

Rs/t

97

110

1331 63

Rs/t Rs/t

Packing

Rs/t

R5 R6 R7 R9 R10

R2R1 R3 R4

R8

37 37 Cost Management & Review Corporate Strategy & Planning

CRM: Cost Analysis Jun’15 (ABP vs. Actual)

(27) 20 57

Prodn:

Cons. Cons Rate ABP 164

(Kg/t) (Kg/t) (Rs/kwh) Act. 151

ABP 1040 6.73 3.97 Gap (13)

Act. 1037 6.38 4.01

Impact (Rs/t) (61) (49) 5

Net Impact (Rs/t) 20

Yield Impact (23)

Overall Yield

ABP 95.58%

Act. 95.88% Rs/t

ABP 26785

Act. 25934

Var. (850)

81 (265) (13) (50) (33) (33)

Stores R&M Fuel &

GasesRolls

Packing &

DespatchOthers Rs cr

Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t Rs/t

ABP 366 1164 343 155 400 215 20 ABP 5398

Act. 447 899 330 105 367 182 20 Act. 5183

Impact (Rs/t) 81 (265) (13) (50) (33) (33) 0.4 Var. (215)

Major Reasons in detail :

Cons (31)

R3 Lower volume impact Vol 216

Price/ Exp (400)

Total (215)

R11 Due to higher expenditure on account of GW Rs 24/t & Rs109/t due to lower volume

R5 Due to extra charging of Industrial Chemical caustic soda, being Rs39/t

Unplanned charging of Weblogic Licenses Rs12/t,

Clearing of old service bills, being Rs29/t

R6 Mech - R & M B scheme of SPM Gear Box of Rs 2.80 Crs not consumed due to delay in delivery

IEM - EDT upgrade material of Rs 3.66 Crs delivery delayed by 20 days. Will reach Jamshedpur by July

-753

CreditsRate

(Rs/t) Rs/t

Rate

(Rs/t)

146380

22

HR Zinc Power

142989

CRM Conversion Cost

Rs/t

(720) 57

(850)

CRM Works Cost

133

(27)

(215)

(720)

133

Cons

(kwh/t)

125

128

15

1206

1338

Fixed Cost

21387

20751 -696

(658)

R5 R6 R7 R8 R9

R2R1 R3 R4

R10 R11

38 38 Cost Management & Review Corporate Strategy & Planning

LD3 TSCR (Combined): Cost Analysis Jun’15 (ABP vs. Actual)

(129) ###

Scrap Credit Ferro Alloys Rolls Packing

Cons

(kg/thr)

Rate

(Rs/t)

Cons

(kg/thr)Rs/thr

Cons

(kg/thr)

Rate

(Rs/t)Rs/thr Rs/thr Prodn :

ABP 1146 13686 83 -731 10.46 132617 165 120 ABP 211

Act. 1137 13680 79 -477 10.44 123405 196 115 Act. 192

Impact (Rs/t) (122) (7) (43) (3) (96)

Net Impact (Rs/t) (129) 253 (100) 31 (5)

Yield Impact (2)

Rs/t

22520

22668

148

32 142 (74) 0 ### 188

Stores R&MFuel &

GasesOthers Fixed Cost

Cons

(kg/thr)

Rate

(Rs/t)Rs/thr Rs/thr Rs/thr

Cons

(kwh/thr)

Rate

(Rs/Mwh)Rs/thr Rs/thr Rs/t

ABP 6.12 79664 535 609 615 192 3,971 719 1334 8959

Act. 6.02 74516 567 751 541 201 4,014 611 1522 9171

Impact (Rs/t) (39) 32 142 (74) 45 (109) 188 213

Major Reasons in detail : Cons 63

Vol 208

Price (58)

Total 213

(88) (88)

HM+Scrap Lime

(45)

253

(88)

148

LD 3 TSCR Works

Cost

Rate

(Rs/t)

9950

9379

ABP

Act.

Var.

(39) 213

Act.

Var.

PowerRefractoriesLD 3 TSCR

Conversion Cost

ABP

R1 R4 R5 R6

R7 R8 R9 R10 R12 R13R11

R2 R3

39 39 Cost Management & Review Corporate Strategy & Planning

^

(ABP V ACT)

(Variance Rs./t 275 ADV)

-1 18 13 38

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

1161 1033 -1 3021 2437 18 482 269 13 1453 811 38

10 33 15 51

11 15 2 13

Rs/t -275

PLAN 1195

ACTUAL 1471

VARIANCE -275

30 -13 49 -410

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

1459 906 30 985 1023 -13 0 -606 49 8194 12258 -410 Expenditure 270

34 3 410 Volume 56

4 10 Change in WIP 49

Exp. Var. Exp. Var.

OMQ : Iron Ore Cost : June '15

Vol. Var.

Vol. Var.

Vol. Var.

Vol. Var.

Contracts & repairs Depreciation Change in WIP

Stores Power Others

Exp. Var. Exp. Var. Exp. Var. Exp. Var.

Wages

Vol. Var. Vol. Var.

Royalty, DMF & NMET

Exp. Var.

R1 R2 R3 R4

R5 R6 R7 R8

KPI Plan Act

Total Spend ( Rs Crs) 168 181

Total Despatch (LT) 14.02 12.32 *

* Lower despatches due to lower offtake of fines ore at JSR Works.

40 40 Cost Management & Review Corporate Strategy & Planning

^ ^

OMQ : Iron Ore Cost : June ’15 (ABP V

ACT)

(Variance : Rs. 275/T ADV)

R2: Stores (Rs 33/t F): Consumption lower than plan at Noamundi & Joda processing plant (P: Rs

14.91 Crs ,A: Rs.9.41 Crs)

R3: Power (Rs 15/t F): Consumption lower than plan at Noa processing plant (P: Rs 2.12 Crs , A:

Rs.1 .62Crs).

R4: Others (Rs 51/t F): Lower expenditure on GA/TM at OMQ (P: Rs 9 Crs, A: Rs. 5.8 Crs)

R5: Contracts & Repairs (Rs 34/t F): Lower spend by Noamundi & Joda processing plant & Mining

(P: Rs 10.26 Crs, A: Rs.5.20Crs) as the ordering is in process.

R7: Change in WIP (Rs 49/t F): Inventory impact by Rs. 6 Cr for increase in inventory due to lower

offtake of ore at Works.

R8: Royalty, DMF & NMET (Rs. 410 /t A) :

a. Royalty ( Rs. 92 /t F) : Decrease in IBM declared market rates for fines for mines in Orissa :

Plan : Lumps Rs 4932 /t, Fines Rs 2454 /t , Act : Lumps Rs 4001 /t, Fines Rs 2150/t &

Jharkhand : ABP: : Lumps Rs 4777 /t , Fines Rs 3259 /t, Actual : : Lumps Rs 3608 /t , Fines Rs

2643 /t

b. DMF & NMET (Rs. 502 /t A) : Provision taken for DMF@ 100% royalty and NMET @ 2% of royalty

as per new MMDR act of Rs 61.89 Crs is not in the plan.

Reasons for Expenditure Variance

41 41 Cost Management & Review Corporate Strategy & Planning

KPI Plan Act

Total Spend ( Rs Crs) 92.74 88.98

Total Despatch ( LT) 1.90 1.91

(ABP V ACT)

(Variance Rs./t 198 ADV)

2 -1 4 60

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

-34 -38 2 1663 1674 -1 111 104 4 847 737 60

2 4 58

1 0 1

-198

PLAN 2737

ACTUAL 2935

VARIANCE -198

-31 2 -9 -224

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t) Expenditure208

1615 1684 -31 471 470 2 130 148 -9 404 835 -224 Volume 9

36 2 10 SP sales 2

5 0 0

June '15West Bokaro : CC Cost :

Vol. Var. Vol. Var. Vol. Var.

Wages Govt. Levies Depreciation Royalty

Exp. Var. Exp. Var. Exp. Var.

Vol. Var. Vol. Var. Vol. Var.

Exp. Var.Exp. Var.Exp. Var.

Contracts & OthersPower (DVC)Stores & ContractsSecondary Product Sales

R1 R2 R3 R4

R5 R6 R7R8

42 42 Cost Management & Review Corporate Strategy & Planning

West Bokaro : CC Cost : June ’15 (ABP V ACT) (Variance : Rs. 198/T ADV) R4: Contract and others (Rs.58/t F ) : Lower spend than planned.

R5: Wages (Rs.36/t A), R7: Depreciation (Rs.10/t A) : Overall expenditure is within plan impact of

change in production mix of CC & Coal by-products on account of change is ash from 16% to 16.5%

and higher CC yield. (P 49% , A 60%)

R3: Royalty , DMF & NMET (Rs. 224/t A) : Royalty as per plan. Provision made for DMF@ 100%

royalty and NMET @ 2% of royalty as per new MMDR act of Rs 4.21 Crs (Rs 220/t CC) was not in

plan.

Reasons for Expenditure Variance

Royalty PLAN ACTUAL

Qty (LT) Rate

Amount

(Rs. Lakhs) Qty (LT) Rate

Amount

(Rs. Lakhs)

Clean Coal 1.90 209 397.46 1.91 207 395.8

Middlings 1.41 98 137.69 0.53 98 52.2

Tailings 0.60 301 180.60 0.00 0.0 0.0

Rejects 0.21 56 11.76 0.18 56 10.35

Total 727.51 458.38

Total Clean Coal Middling Tailing

Plan 100% 57% 28% 15%

Actual 100% 64% 25% 11%

Change in clean coal and by product mix +7% -3% -4%

43 43 Cost Management & Review Corporate Strategy & Planning

KPI Plan Act

Total Spend ( Rs Crs) 73 75

Total Despatch ( LT) 0.64 0.55

R9

R9: Lower CC volume due to lower RC production due to water seepage at 6&7 Pits colliery, adverse

geological condition at Digwadih.

June '15

(Variance Rs./t 3019 ADV)

-1214 -141 -40 -58

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

-1778 -851 -1214 600 591 -141 730 646 -40 115 130 -58

70 37 28

71 77 30

Rs./t -3019

PLAN 8458

ACTUAL 11477

VARIANCE -3019

22 34 -373 -1248

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t)

Plan

(Rs L)

Act

(Rs L)

Var

(Rs/t) Expenditure 621

-53 -58 22 725 601 34 3392 3106 -373 1722 2160 -1248 Volume 1206

72 430 1061 Stowing Asst. 22

38 803 187 SP sales 1214

Exp. Var. Exp. Var. Exp. Var.

(ABP V ACT)

Coal By- Prodn for sale Power Stores Depreciation

Jharia: CC Cost :

Vol. Var. Vol. Var.

Vol. Var. Vol. Var. Vol. Var.

Stowing Asst. Contract & Misc. Wages Others

Exp. Var. Exp. Var. Exp. Var.

Vol. Var.

R1 R2 R3 R4

R5 R6 R7 R8

44 44 Cost Management & Review Corporate Strategy & Planning

R1 : Coal By Product (Rs 1214/t A ) : Lower sale of by product due to non-availability of

permission from MOC, permission received and despatch started from 27.6.15.

R2 : Power : (Rs.70/t A) :

Higher purchase of power

due to shut down of

Captive power plant.

R3 : Stores : (Rs.37/t F): Lower spend than plan

R5 : Stowing Assistance (Rs 22/t F) : Due to higher stowing.

R6: Contract & Misc (Rs 72 /t A) : Slag worth Rs. 0.84 crs has been booked under C & H.

R7: Wages (Rs.430/t F) : : Impact of increment and DA increase not affected.( P : 94.72%, A 87.4%)

R8 : Others (Rs. 1061/t A) : Rs.184/ t A is on account of stock impact. : Provision made for DMF@

100% royalty and NMET @ 2% of royalty as per new MMDR act of Rs 3.12 Crs (Rs 593/t CC A) is

not in the plan and inventory impacts.

Reasons for Expenditure Variance

JHARIA : CC Cost : June ’ 15 (ABP V ACT) (Variance : Rs. 3019/T ADV)

PART. UoM ACTUAL PLAN

Captive Purchase Comb Captive Purchase Comb

UNIT LU 0.01 123.25 123.26 40.10 85.14 125.24

EXP Rs. L 2.59 616.60 619.19 137.26 478.20 615.46

T&D Exp Rs. L 5.38 26.42

CPU Rs/U 259 5 5.31 3.42 5.62 5.13

45 45 Cost Management & Review Corporate Strategy & Planning

Projection: Jul’15

46 Cost Management & Review Corporate Strategy & Planning

Overall production & KPI Proj. for CSI Area: Jul’15

ABP Projection Diff.

1. Production

Hot Metal Production KT 887 898 11

Sinter Production KT 699 689 (10)

Pellet KT 525 535 10

Coke Production KT 385 363 (22)

2. Major KPI's

Sinter % % 46% 46% 0%

Pellet % % 36% 36% 0%

Agglomerates % % 82% 82% 0%

Captive coal % % 35% 35% 0%

Coke Rate kg/thm 434 418 (17)

PCI Rate kg/thm 132 140 8

Fuel Rate kg/thm 566 557 (9)

Total Hot Metal Cost Rs/thm 13511 12960 (551)

UOMParticularsJul'15

47 Cost Management & Review Corporate Strategy & Planning

(Fig in KT) July’15 Production Projection :

Shortfall 0 to 2% in yellow and > 2% in red

KT KT KT

D 36 36 0

C 55 55 0

F 109 109 0

G 182 173 (9)

H 250 262 12

I 255 263 8

A-I BF 887 898 11

HM Pooling 11 10 (1)

BF (KT) Jul'15 ABP Jul'15 Proj. Var. Status

Jul'15 ABPJul'15

Proj.Var wrt ABP Status

Coke-Jsr (BF+Nut) 269 263 (6)

HMC(Screened) 116 100 (16)

Total Coke (BF+Nut) 385 363 (22)

Net Sinter 699 689 (10)

Pellet 525 535 10

48 Cost Management & Review Corporate Strategy & Planning

Fuel Rate: Jul’15 Projection (kg/thm)

BFce

Coke rate PCI+ Tar Fuel rate ABP Proj. ABP Proj. ABP Proj.

649 3 652 D 542 535 30 30 572 565

528 43 571 C 527 515 45 45 572 560

448 107 555 F 427 409 125 135 552 544

461 146 607 G 430 413 145 150 575 563

454 145 599 H 425 403 145 160 570 563

440 129 569 I 415 402 145 150 560 552

459 126 585 A-I 434 418 132 140 566 558

PCI Rate - July'15 Fuel Rate - July'15ACT – July’14 Coke Rate - July'15

49 Cost Management & Review Corporate Strategy & Planning

LD1: Cost & KPI (Projection) LD#1 - BILLET Jul'15 Aug'15 Sep'15

A-June'15 Jun-15 Particulars UOM ABP Projn.

Impact ABP vs Proj. (Rs/t)

ABP Projn.

ABP Projn.

Total w.r.to

consn.

w.r. to

Price

801 268 Prodn from LD#1 LS kT 284 284 284 284 245 245

12 3 Prodn from LD#3 LS kT 0 0 0 0 2 2

813 271 Total Billet Prodn. kT 284 284 284 284 247 247

1045 1043 Hot Metal kg/t 1040 1040 (573) 0 (573) 1028 1028 1041 1041

54 54 Scrap kg/t 65 65 0 0 0 77 77 65 65

1099 1097 HM+Scrap kg/t 1105 1105 1105 1105 1105 1105

(501) (510) Scrap Credit Rs/t (590) (500) 90 90 (590) (500) (588) (500)

75.3 71.0 Lime kg/t 76 74 (17) (17) (0) 76 75 76 75

19.5 19.4 Fe. Alloys. kg/t 20.0 20.0 27 0 27 20.0 20.0 20.0 20.0

0.81 0.80 DS Comp. kg/t 1.10 0.85 (10) (10) 0 1.10 0.90 1.10 0.90

0.150 0.131 Fuel Gcal/t 0.173 0.150 (46) (48) 2 0.173 0.150 0.173 0.149

92 94 Power kWh/t 94 93 (4) (4) 0 94 94 99 99

290 262 Stores Rs/t 329 300 (28) 329 295 329 320

180 159 R&M Rs/t 233 233 0 208 208 335 335

7.25 6.42 Refractory Kg/t 6.70 6.70 0 - 0 6.80 6.80 9.40 9.40

356 353 Labour Rs/t 348 348 0 348 348 399 399

200 202 Depreciation Rs/t 191 191 0 191 191 219 219

139 173 GW/ Town Medical/ LTC Rs/t 154 154 0 154 154 177 177

444 423 Others Rs/t 357 357 0 337 337 376 376

5596 5418 Conversion Cost (HM to

Billet) Rs/t 5783 5768 (15) 5773 5783 6286 6330

50 Cost Management & Review Corporate Strategy & Planning

LD2: Cost & KPI (Projection)

ABP Projection

Total Cons./Vol Price/mix

927 Production kT 329 347 360 360 328 328

1119 HM+ Scrap kg/t 1109 1109 (29) 0 (29) 1109 1109 1109 1109

(498) Scrap Credit Rs/t (442) (442) 0 0 0 (442) (442) (442) (442)

47 Iron Ore kg/t 56 56 0 0 0 56 56 56 56

69 Lime kg/t 71 69 (26) (20) (6) 71 69 71 69

8.97 Fe. Alloys. kg/t 10.18 9.50 (191) (85) (105) 10.18 9.50 10.18 9.50

2.95 DS Comp. kg/t 3.09 2.95 (16) (8) (8) 3.09 2.95 3.09 2.95

14 Dolomite kg/t 18 15 (6) (6) 0 18 18 18 18

347 Fuel & Gases Rs/t 376 364 (12) (12) 343 343 379 379

63 Power kWh/t 60 60 0 0 0 55 55 60 60

216 Stores Rs/t 207 190 (17) (10) (7) 207 207 207 207

235 Repairs & Maint. Rs/t 173 164 (9) (9) (0) 197 197 246 246

5.85 Refractory kg/tcs 7.29 6.74 (43) (43) 0 5.7 5.7 7.29 7.29

314 Labour Rs/t 299 284 (16) (16) 0 273 273 300 300

180 Depreciation Rs/t 179 170 (9) (9) 0 164 164 180 180

121 GW/ Town Medical

/ LTCRs/t 130 93 (36) (5) (31) 119 93 130 94

35 Utilities Rs/t 32 32 0 (2) 2 32 32 32 32

62 Shared Services Rs/t 55 55 0 (3) 3 55 55 55 55

0 Technical Cons Rs/t 5 5 0 (0) 0 5 5 5 5

2 IT EXP Rs/t 5 5 0 (0) 0 5 5 5 5

0 LD 3 Adj Rs/t 0 0 0 0 0 0 0 0 0

64Carriage & Handling Rs/t 78 65 (13) (4) (10) 78 78 78 78

71 Others Rs/t 74 74 0 (4) 4 74 74 74 74

5669Conversion Cost

(HM to Slab)Rs/t 5939 5517 (422) (224) (198) 5797 5513 6012 5749

LD#2 & SC Sep-15

ProjectionABP

Jul-15

Projection

Aug-15

Impact ABP vs Projn. (Rs/t)YTD

June 15Particulars UOM ABP

51 Cost Management & Review Corporate Strategy & Planning

LD3: Cost & KPI (Projection) LD#3 TSC

Total Cons./Vol Price/mix

605 Production kT 231 231 226 226 224 224

1100 HM+ Scrap kg/t 1118 1110 (161) (114) (47) 1118 1110 1,118 1,110

(446) Scrap Credit Rs/t (599) (599) 0 0 0 (599) (599) (599) (599)

44 Iron Ore kg/t 55 55 0 0 0 55 55 55 55

76 Lime kg/t 77 76 (21) (5) (16) 81 76 77 76

10.09 Fe. Alloys. kg/t 10.21 10.00 (109) (27) (82) 10.21 10.00 10.21 10.00

2.39 DS Comp. kg/t 2.80 2.39 (23) (23) 0 2.80 2.39 2.80 2.39

8 Dolomite kg/t 18 15 (7) (7) 0 18 18 18 18

318 Fuel & Gases Rs/t 337 337 0 0 305 305 340 340

79 Power kWh/t 75 75 0 0 0 75 75 75 75

348 Stores Rs/t 420 350 (70) 0 (70) 420 350 420 420

364 Repairs & Maint. Rs/t 332 318 (14) 0 (14) 282 386 314 283

6.61 Refractory kg/tcs 5.97 5.97 0 0 0 5.97 5.97 5.97 5.97

137 Labour Rs/t 111 111 0 0 0 114 114 115 115

484 Depreciation Rs/t 422 422 0 0 0 432 432 435 435

97GW/ Town Medical/ LTC Rs/t 77 62 (15) 0 (15) 79 62 80 62

1 Utilities Rs/t 15 0 (15) 0 (15) 15 0 15 -

71 Shared Services Rs/t 52 45 (7) 0 (7) 52 45 52 45

1 IT Exp Rs/t 7 7 0 0 0 7 7 7 7

96 Carriage & Handling Rs/t 118 100 (18) 0 (18) 118 100 118 100

95 Others Rs/t 129 90 (39) 0 (39) 129 90 129 90

6135Conversion Cost

(HM to Slab)Rs/t 6373 5874 (498) (176) (322) 6416 6011 6373 5950

Jul-15 Aug-15 Sep-15

YTD

June 15Particulars UOM ABP Projection ABP Projection ABP Projection

Impact ABP vs Projn. (Rs/t)

52 Cost Management & Review Corporate Strategy & Planning

WRM: Cost & KPI (Projection)

WRM(E) Jul'15 Aug'15 Sep'15

A-June'15 Jun-15 Particulars UOM ABP Projn.

Impact ABP vs Proj.

(Rs/t) ABP Projn. ABP Projn.

Total w.r.to

consn.

w.r. to

Price

106 34 Production kT 28.0 37.0 38.0 38.0 36.0 36.0

97.38% 97.52% Yield % 97.20% 97.50% 0 0 0 97.52% 97.50% 97.52% 97.50%

(456) (447) Scrap Credit Rs/t (425) (450) (25) (425) (425) (425) (428)

0.194 0.196 Fuel Gcal/t 0.190 0.190 0 0 0 0.190 0.190 1.837 1.837

121 121 Power kWh/t 140 121 (76) (76) 0 121 121 121 121

65 66 Rolls Rs/t 65 65 0 65 65 65 65

267 279 Stores Rs/t 290 285 (5) 290 280 290 290

455 375 R&M Rs/t 850 568 (282) 429 471 506 519

0 0 Refractory Rs/t 107 0 (107) 0 0 0 0

885 912 Labour Rs/t 1132 857 (275) 834 834 881 881

40 42 Depreciation Rs/t 50 38 (12) 37 37 39 39

211 265 GW/ Town Medical/

LTC Rs/t 295 223 (72) 217 217 229 229

374 417 Others Rs/t 476 360 (116) 350 350 370 370

3116 3164 Conversion Cost Rs/t 4335 3285 (1050) 3156 3178 3316 3332

53 Cost Management & Review Corporate Strategy & Planning

MM: Cost & KPI (Projection)

MM Jul'15 Aug'15 Sep'15

A-June'15 Jun-15 Particulars UOM ABP Projn.

Impact ABP vs Proj.

(Rs/t) ABP Projn. ABP Projn.

Total w.r.to

consn.

w.r. to

Price

109.3 37.7 Production kt 36.5 37.0 37 37 35 35

97.26% 97.27% Yield % 97.26% 97.26% 0 (0) 0 97.26% 97.26% 97.26% 97.26%

(413) (391) Scrap Credit Rs/t (418) (450) (33) (418) (450) (418) (450)

0.309 0.309 Fuel Gcal/t 0.310 0.310 0 0 0 0.310 0.310 0.310 0.310

65 45 Power kWh/t 60 60 0 0 0 60 60 61 61

56 58 Rolls Rs/t 50 50 0 55 55 60 55

152 103 Stores Rs/t 165 150 (15) 165 150 165 150

335 322 R&M Rs/t 367 362 (5) 466 540 801 789

0 0 Refractory Cost Rs/t 0 0 0 0 0 0 0

728 709 Labour Rs/t 745 735 (10) 745 745 775 775

6 7 Depreciation Rs/t 5 5 (0) 5 5 5 5

142 158 GW/ Town Medical/

LTC Rs/t 165 163 (2) 165 165 172 172

320 312 Others Rs/t 287 283 (4) 287 287 299 299

2542 2407 Conversion Cost Rs/t 2675 2590 (85) 2795 2807 3186 3124

54 Cost Management & Review Corporate Strategy & Planning

NBM: Cost & KPI (Projection) NBM Jul'15 Aug'15 Sep'15

A-June'15 Jun-15 Particulars UOM ABP Projn.

Impact ABP vs Proj.

(Rs/t) ABP Projn. ABP Projn.

Total w.r.to

consn.

w.r. to

Price

230 75 Production kt 78 53 78 78 75 75

96.60% 96.60% Yield % 96.60% 96.60% 0 0 0 96.60% 96.60% 96.60% 96.60%

(405) (390) Scrap Credit Rs/t (404) (404) (0) (404) (404) (404) (404)

0.222 0.222 Fuel Gcal/t 0.220 0.225 9 9 (0) 0.220 0.220 0.220 0.220

93 93 Power kWh/t 95 105 40 40 0 95 95 95 95

38 34 Rolls Rs/t 50 50 0 50 50 50 50

122 174 Stores Rs/t 176 215 39 176 192 176 176

232 253 R&M Rs/t 463 906 443 206 226 200 200

0 0 Refractory Rs/t 0 250 250 0 0 0 0

214 219 Labour Rs/t 204 300 96 204 204 212 212

173 176 Depreciation Rs/t 171 251 81 171 171 178 178

64 83 GW/ Town Medical/

LTC Rs/t 71 105 34 71 71 74 74

184 180 Others Rs/t 160 235 75 160 160 166 140

1948 2068 Conversion Cost Rs/t 2315 3361 1046 2072 2089 2090 2066

55 Cost Management & Review Corporate Strategy & Planning

HSM: Cost & KPI (Projection) HSM

ABP Projection

Total Impact Cons./Vol Price/mix

863 Production kT 255 290 361 327 351 350

98.19% Yield % 98.20% 98.20% -18 0 -18 98.20% 98.20% 98.20% 98.20%

(222) Scrap Credit Rs/t (215) (215) 0 0 0 (215) (215) (241) (241)

0.282 Fuel & Gases Gcal/t 0.300 0.300 0 0 0 0.275 0.275 0.275 0.275

89 Power kWh/t 90 90 0 0 0 85 85 85 85

23 Utilities Rs/t 20 20 0 -3 3 20 20 20 20

76 Stores Rs/t 166 166 0 0 0 87 87 81 81

267 Repair & Maint. Rs/t 370 325 -45 -45 0 230 254 212 213

66Rolls Cost Rs/t 131 131 0 -18 18 173 173 95 95

59 Packing Cost Rs/t 78 78 0 -11 11 78 78 78 78

260 Labour Rs/t 298 262 -36 -36 0 209 231 215 216

176 Depreciation Rs/t 203 178 -24 -24 0 143 158 147 148

46 GW/ Town Medical

/ LTCRs/t 71 62 -9 -9 0 50 55 51 52

48 Shared Services Rs/t 37 37 0 -5 5 37 37 37 37

12 Insurance Rs/t 12 11 -1 -1 0 12 13 12 12

0 Technical Cons Rs/t 7 6 -1 -1 0 5 5 5 5

3 IT Expenses Rs/t 11 10 -1 -1 0 8 8 8 8

56 Other Expenses Rs/t 77 50 -27 -7 -20 77 50 77 50

1891 Conversion Cost Rs/t 2283 2121 -162 -161 -1 1918 1944 1823 1793

Aug-15

ProjectionABP

Sep-15

YTD

June 15ABPParticulars

Jul-15

RemarksProjectionImpact ABP vs Projn. (Rs/t)

UOM

56 Cost Management & Review Corporate Strategy & Planning

TSC Rolling: Cost & KPI (Projection)

Rolling Mill

ABP Projection

Total Impact Cons./Vol Price/mix

591 Production kT 225 225 220 220 218 220

97.62% Yield % 97.53% 97.53% (27) 0 (27) 97.53% 97.53% 97.53% 97.53%

(103) Scrap Credit Rs/t (117) (117) 0 0 0 (117) (117) (117) (117)

0.189 Fuel & Gases Gcal/t 0.186 0.190 (19) 5 (24) 0.190 0.190 0.192 0.190

115 Power kWh/t 109 109 (10) 0 (10) 113 113 114 114

76 Utilities Rs/t 5 0 0 0 0 5 0 5 0

76 Stores Rs/t 98 90 (8) 0 (8) 100 90 101 90

286 Repair & Maint. Rs/t 287 256 (31) 0 (31) 221 388 251 205

164Rolls Cost Rs/t 165 145 -20 0 -20 165 145 165 145

120 Packing Cost Rs/t 120 120 0 0 0 120 120 120 120

0 Labour Rs/t 69 69 0 0 0 70 70 71 71

604 Depreciation Rs/t 523 523 0 0 0 534 535 539 539

16GW/ Town Medical/ LTC Rs/t 33 33 0 0 0 34 34 34 34

28 Shared Services Rs/t 28 28 0 0 0 28 28 28 28

0 Insurance Rs/t 5 3 -2 0 -2 5 3 5 3

3 IT Rs/t 6 6 0 0 0 6 6 6 6

61 Other Expenses Rs/t 54 54 0 0 0 54 54 54 54

2496 Conversion Cost Rs/t 2469 2348 (121) 6 (122) 2451 2526 2480 2354

Jul-15 Aug-15 Sep-15

ABP ProjectionYTD

June 15Particulars UOM ABP Projection

Impact ABP vs Projn. (Rs/t)Remarks

57 Cost Management & Review Corporate Strategy & Planning

CRM: Cost & KPI (Projection) CRM Jul-15 Aug-15 Sep-15

YTD

June 15 Particulars UOM ABP

Projectio

n

Impact ABP vs Projn. (Rs/t) Re

mar

ks

ABP Projectio

n

ABP Projectio

n Total Impact

Due to

Cons./Vol

Due to

Price/mix

453 Production kT 16 89 156 95 166 166

95.75% Overall Yield % 95.51% 95.51%

95.51

% 95.51%

95.51

% 95.51%

1038 HR Consumption Kg/t 1039 1034 (155) (116) (39) 1041 1039 1039 1039

(720) Scrap Credit Rs/t (714) (557) 157 157 0 (775) (738) (748) (748)

6.25 Zinc Kg/t 1.32 6.60 780 711 69 6.11 6.25 6.65 6.65

347 Fuel & Gases Rs/t 462 351 0 0 0 352 434 353 353

127 Power kWh/t 177 150 (106) (106) 0 129 150 129 129

389 Stores Rs/t 2331 749 (1582) (3280) 1698 433 958 377 519

621 Repair & Maint. Rs/t 6429 1826 (4602) (7998) 3396 606 993 504 504

89 Rolls Cost Rs/t 203 39 -163 (172) 9 131 84 108 48

361 Packing & Despatch Rs/t 400 360 (40) 0 (40) 400 360 400 360

518 Labour Rs/t 4626 860 (3766) (3766) 0 490 803 460 460

625 Depreciation Rs/t 5798 1078 (4720) (4720) 0 617 1011 580 580

151 GW/ Town Medical

/ LTC Rs/t 1606 299 (1307) (1307) 0 170 279 160 160

36 Utilities Rs/t 264 264 0 (1156) 1156 36 36 36 36

45 Shared Services Rs/t 296 55 (241) (241) 0 41 67 41 41

19 Insurance Rs/t 160 30 (130) (130) 0 22 36 22 22

4 Consultancy charge Rs/t 51 51 0 (221) 221 5 5 5 5

9 IT Exp Rs/t 109 20 (89) (89) 0 12 19 11 11

71 Other Exp Rs/t 727 135 (592) (592) 0 100 164 100 100

4780 Conversion Cost Rs/t 24489 7820 (16669) (23028) 6470 4911 6822 4715 4746

58

Cost Management & Review - CS&P

58 Cost Management & Review Corporate Strategy & Planning

R1: LD2 : Crane girder repairing, product mix & Power dip : (9 kt)

WOI : F fce -Tuyere burning due to material defect & lower agglomerate : (3kt)

: H fce -Sinter & Pellet plant shutdown & high moisture coke : (4 kt)

: I fce -Ore feeder jammed,O2 reduce due to unavailability of Ore, Sinter & SFC tripped : (2kt)

R2: LD2 : Breakout in caster 1 & 2 , caster 1 cap off due to slide gate plate leakage & LF2 roof jam stuck up : (7kt)

WOI : H fce –Replacement of HBF tuyere cooler as burnt in contact with molten hot metal : (8 kt)

I fce - OWH1 gate feedback fault:

R3: LD1 : Turn over cooling bed failure : (0.4kt)

LD2 : SEN choke, caster3 hydraulic fail, vessel 2 tilt drive break down & mould control fail (6kt)

WOI : H fce - Power dip (3rd Jun’15) due to external power failure : (5 kt)

R4: LD1 : Turn over cooling bed & secondary cooling failure in caster 2 : (1kt)

LD2 : Flair stack issue, C1 machine restriction, Vsl 3 hood leakage, caster 1 break out & C2 TCM problem : (8 kt)

Loss of Crude Steel Production (kt) : Jun’15 Total loss LD1 & LD2 : 53 kt , Outage : Iron making (WOI) 22 kt & Steel making 31 kt)

18

15

11 9

34%

62%

84%

100%

0%

20%

40%

60%

80%

100%

120%

0

2

4

6

8

10

12

14

16

18

20

R1Others

R2Operation

R3Electrical

R4Mechanical

Loss (KT) Percentage

LD1 LD2 LD3 Total

ABP 274 349 216 839

MBP 274 354 194 822

Actual 271 305 196 771

Gap wrt ABP -4 -44 -20 -68

Gap wrt MBP -4 -49 2 -51

Crude steel prodn.(kt)

BF : F BF : H BF : I Other BF Total

ABP 121 256 256 262 895

MBP 121 256 226 262 865

Actual 115 224 221 275 835

Gap wrt ABP -6 -32 -35 13 -60

Gap wrt MBP -6 -32 -5 13 -30

Furnace wise HM prodn.(kt)

59

Cost Management & Review - CS&P

59 Cost Management & Review Corporate Strategy & Planning

Opportunity Loss ( Rs. Crs) : Jun’15

SL no.Impact

(Rs. Crs)Remarks

1 Cost of Break downs/Instability:

1.R1 Cost of break down at LD Shops . 47

Impact of plant outage- Total Crude Steel production loss

(plant outage/Process disturbance) : 53 kt

Less HM pooling : 22kt

1.R2Loss of production at Sinter plant &

Pellet Plant2

1) SP2 - Breakdown in combustion air fan, conveyor belt failure

& high number of interruptions (8kt)

2) SP4 - Receiving belt, Sinter Cooler breakdown, extension &

boulder formation & high return fines (13kt)

3) Pellet Plant - Voltage dip (3rd Jun’15), gas shortage & dryer

#1 discharge belt failure (17kt)

1.R3 Demurrage Charges 16 Vessel: Rs. 10.03 crs; Rail: Rs. 3.09 crs; EOL Rs.3.03 Crs

Sub total 65

2 Less availability of Captive Raw Materials:

Sub Total 49

Total 114

2.R4 Iron ore shortage/ Mine Closure 49i. Usage of Bought Out Metallic (Ore : 104 kt, pellet : Nil).

ii. Fixed Cost impact of Khond bond closure

60

Cost Management & Review - CS&P

60 Cost Management & Review Corporate Strategy & Planning

Loss of Crude Steel Production (kt) : A-Jun’15

28

25

16 15

34%

63%

82%

100%

0%

20%

40%

60%

80%

100%

120%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

R1Operation

R2Others

R3Mechanical

R4Electrical

Loss (KT) Percentage

LD1 LD2 LD3 Total

ABP 811 1019 600 2430

MBP 831 1024 578 2433

Actual 813 927 605 2345

Gap wrt ABP 2 -92 5 -84

Gap wrt MBP -18 -97 27 -88

Crude steel prodn.(kt)

BF : C-F BF : G BF : H BF : I Total

ABP 636 523 765 730 2655

MBP 636 523 765 730 2654

Actual 637 512 715 724 2588

Gap wrt ABP 1 -11 -50 -6 -67

Gap wrt MBP 1 -11 -50 -6 -67

Furnace wise HM prodn.(kt)

61

Cost Management & Review - CS&P

61 Cost Management & Review Corporate Strategy & Planning

Reason for cost increase: May vs June’15

May'15 June'15 Gap

Description Prod (KT)

Cost (Rs./t)

Prod (KT)

Cost (Rs./t)

Prod (KT)

Cost (Rs./t)

HM 891 12799 835 13497 -56 698

WSS 725 21494 786 22031 61 537

Description UoM May'15 June'15 Gap Impact (Rs./t)

Reason

Agglomerates % 81 77 -4 218

Pellet MSD SP#3 B/D

Coke Rate Kg/thm 401 413 12 Lower Agglomerates

Maintenance & Flux Rs./thm 133 MSD at Pellet, LD#3, CRM etc.

Higher captive ore cost Rs./thm 163 Lower production (Impact on Fixed Cost)

Rs./thm 184 HM production is lower by 56 KT (6%)

Sub Total Rs./thm 698

Mix Impact Rs./tss -140 Usage of slab and billet from stock produced in May'15 at lower rates.

Others Rs./tss -21 Total Rs./tss 537

62

Cost Management & Review - CS&P

62 Cost Management & Review Corporate Strategy & Planning

Hot Metal Cost variation : Jun’15(Proj.) vs Jun’15 (Act): (Rs./thm)

R1: Higher fuel rate by 5 kg/thm (Proj : 560 kg/thm, Act: 565 kg/thm)

R2: Higher conversion cost due to lower production (Proj : 850 kt, Act : 835 kt)

R3: Higher iron ore cost (Proj : Rs. 2107/t, Act : Rs. 2340/t)

R4: Higher flux consumption (Proj : 190/thm, Act : 221/thm)

R5: Cost reduction ideas envisaged was lower than plan.

AB

P

Cost is higher by Rs. 294/thm

Hig

her

Fu

el R

ate

Hig

her

iro

n o

re c

ost

MA

Y’1

5

13203 77

70 57 45 44 13497

R1 R2 R3 R4 R5

Low

er P

rod

uct

ion

Jun

’15

(P

roj)

Jun

’15

(A

ct)

Hig

her

flu

x u

sage

Oth

ers

63

Cost Management & Review - CS&P

63 Cost Management & Review Corporate Strategy & Planning

Q1 vs Q2: RM & CSI KPIs

Q4 FY15

Particulars UOM

Q1 FY16 Q2 FY16 H1 FY16 Q2 vs

Q1

Actual ABP Exp. Gap ABP Exp. Gap ABP Exp. Gap Gap w.r.t

Q1

82 Agglomerate % 83 81 -2.0 83 83 0.0 83 82 -1.0 2.0

16 Coke Ash % 15.9 16 0.1 15.8 16.4 0.6 15.8 16.2 0.4 0.4

410 Coke Rate Kg/thm 427 408 -19.0 434 418 -16.0 431 413 -18.0 10.0

135 PCI Rate Kg/thm 132 145 13.0 131 143 12.0 132 144 12.0 -2.0

544 Fuel Rate Kg/thm 559 553 -6.0 565 561 -4.0 563 557 -6.0 8.0

457 Carbon Rate Kg/thm 470 465 -5.0 475 471 -4.0 473 468 -5.0 6.0

634 WB Production KT 570 596 26.0 430 451 21.0 1000 1040 40.0 -145.0

213 Jharia KT 272 248 -24.0 275 277 2.0 547 525 -22.0 29.0

36 Captive Coal % 34 36 2.0 34 34 0.0 34 35 1.0 -2.0

64

Cost Management & Review - CS&P

64 Cost Management & Review Corporate Strategy & Planning

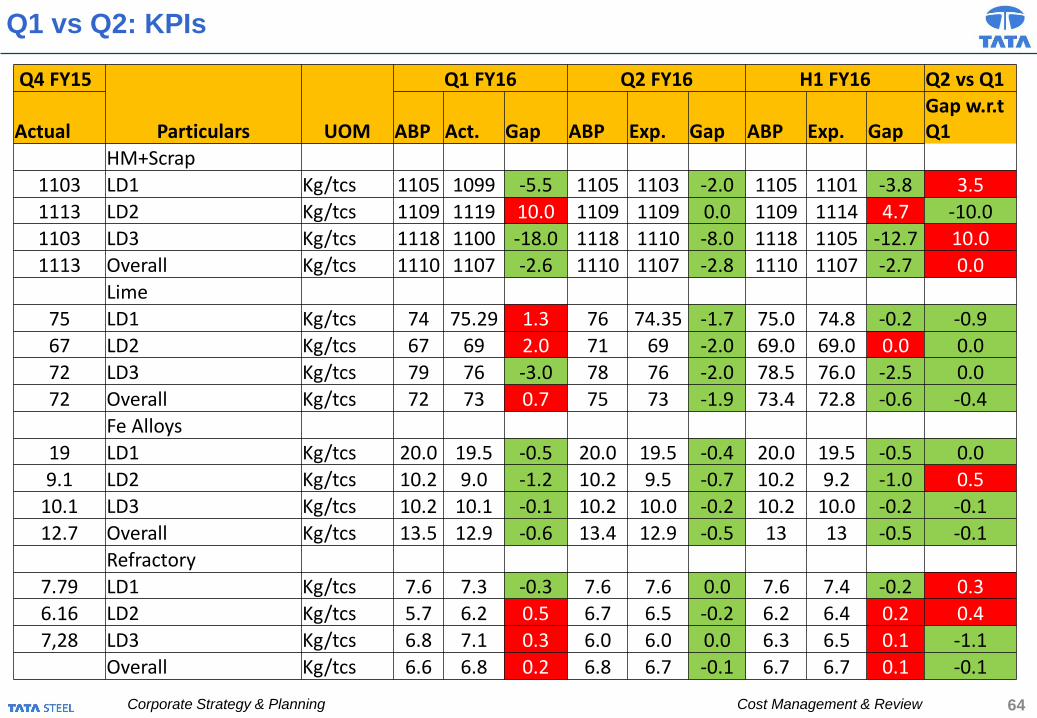

Q1 vs Q2: KPIs

Q4 FY15

Particulars UOM

Q1 FY16 Q2 FY16 H1 FY16 Q2 vs Q1

Actual ABP Act. Gap ABP Exp. Gap ABP Exp. Gap Gap w.r.t Q1

HM+Scrap

1103 LD1 Kg/tcs 1105 1099 -5.5 1105 1103 -2.0 1105 1101 -3.8 3.5

1113 LD2 Kg/tcs 1109 1119 10.0 1109 1109 0.0 1109 1114 4.7 -10.0

1103 LD3 Kg/tcs 1118 1100 -18.0 1118 1110 -8.0 1118 1105 -12.7 10.0

1113 Overall Kg/tcs 1110 1107 -2.6 1110 1107 -2.8 1110 1107 -2.7 0.0

Lime

75 LD1 Kg/tcs 74 75.29 1.3 76 74.35 -1.7 75.0 74.8 -0.2 -0.9

67 LD2 Kg/tcs 67 69 2.0 71 69 -2.0 69.0 69.0 0.0 0.0

72 LD3 Kg/tcs 79 76 -3.0 78 76 -2.0 78.5 76.0 -2.5 0.0

72 Overall Kg/tcs 72 73 0.7 75 73 -1.9 73.4 72.8 -0.6 -0.4

Fe Alloys

19 LD1 Kg/tcs 20.0 19.5 -0.5 20.0 19.5 -0.4 20.0 19.5 -0.5 0.0

9.1 LD2 Kg/tcs 10.2 9.0 -1.2 10.2 9.5 -0.7 10.2 9.2 -1.0 0.5

10.1 LD3 Kg/tcs 10.2 10.1 -0.1 10.2 10.0 -0.2 10.2 10.0 -0.2 -0.1

12.7 Overall Kg/tcs 13.5 12.9 -0.6 13.4 12.9 -0.5 13 13 -0.5 -0.1

Refractory

7.79 LD1 Kg/tcs 7.6 7.3 -0.3 7.6 7.6 0.0 7.6 7.4 -0.2 0.3

6.16 LD2 Kg/tcs 5.7 6.2 0.5 6.7 6.5 -0.2 6.2 6.4 0.2 0.4

7,28 LD3 Kg/tcs 6.8 7.1 0.3 6.0 6.0 0.0 6.3 6.5 0.1 -1.1

Overall Kg/tcs 6.6 6.8 0.2 6.8 6.7 -0.1 6.7 6.7 0.1 -0.1

65

Cost Management & Review - CS&P

65 Cost Management & Review Corporate Strategy & Planning 65 Cost Management & Review Corporate Strategy & Planning

Production & Cost Performance: Q1 vs. Q2 FY16

Particulars Q1 FY'16 Act Q2 FY'16 Act. Var. (Q2 over Q1)

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Iron Making

Hot Metal 2588 13228 2661 13120 73 -108

Steel Making Production & Conversion Cost

LD1- Billet 813 5596 815 5854 2 258

LD2- Slab 927 5669 1035 5590 108 -79

LD3- Slab 605 6135 681 5945 76 -190

Crude Steel 2345 19025 2531 19060 186 35

WRM 106 3116 111 3257 5 141

MM 109 2542 109 2833 0 291

NBM 230 1948 206 2405 -24 457

HSM - HR (Gross) 863 1891 967 1943 104 52

TSCR - HR (Gross) 591 2496 664 2409 73 -87

CRM 453 4780 329 6429 -124 1649

LP Saleable 796 19863 801 20517 5 654

FP Saleable 1432 22388 1610 22309 178 -79

WSS 2228 21817 2411 21714 183 -103

* Includes DMF impact from Apr'15 onwards

66

Cost Management & Review - CS&P

66 Cost Management & Review Corporate Strategy & Planning 66 Cost Management & Review Corporate Strategy & Planning

Production & Cost Performance: Q1 FY16 (ABP vs. Act)

Particulars Q1 FY'16 ABP Q1 FY'16 Act. Var. (Act over ABP)

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Prodn Kt

Cost Rs/t

Raw Materials

Iron Making

Hot Metal 2655 13704 2588 13228 -67 -476

Steel Making Production & Conversion Cost

LD1- Billet 811 5957 813 5596 2 -361

LD2- Slab 1019 5742 927 5669 -92 -73

LD3- Slab 600 6646 605 6135 5 -511

Crude Steel 2430 19739 2345 19025 -85 -714

WRM 106 3505 106 3116 0 -389

MM 107 2673 109 2542 2 -131

NBM 205 2365 230 1948 25 -417

HSM - HR (Gross) 1007 1918 863 1891 -144 -27

TSCR - HR (Gross) 585 2743 591 2496 6 -247

CRM 496 4925 453 4780 -43 -145

LP Saleable 798 21091 796 19863 -2 -1228

FP Saleable 1574 23552 1432 22388 -142 -1164

WSS * 2372 22724 2228 21817 -144 -907

* Includes DMF impact from Apr'15 onwards