1999 journal

TRANSCRIPT

INTERNATIONAL CO-OPERATIVEBANKING ASSOCIATIONJOURNAL NO. 11 1999

INTERNATIONALCO-OPERATIVE BANKING

ASSOCIATION•

SEMINAR•

Capital, Demutualizationand Governance

SPEAKERS :

Commentators

Contacts - ICBA Presidentand Regional Chairmen

INTERNATIONAL CO-OPERATIVEBANKING ASSOCIATION No. 11: 1999

CONTENTS Page

Claude Béland 3A word from the President

Mervyn Pedelty 5“Capital, Democratisationand Governance”

P.V. Prabhu 19Capital, Demutualisation andGovernance - Indian CooperativeCredit & Banking Scenario

Jacques Henrichon 38“The Relationship Between the InspectorGeneral of Financial Institutions and theMouvement Desjardins”

Klaus P. Fischer 48The Colombian Crisis of FinancialCooperatives, a Corporate Governance Crisis

61

Claude Béland 64“Co-operative Banks in a FinancialWorld in Mutation: Challengesand Outlooks”

71

warmly welcome you to beauti-

ful Québec City and to this seminar of

the International Co-operative Banking

Association.

We have chosen as a theme topics

that, in my opinion, are the key issues

facing cooperatives in a global environ-

ment brought about by a very rapid and

spectacular progression of communica-

tion technologies and data transmission.

This has penetrated boundaries and

made markets closer. With this, as you all

know, competition has sharpened and

there is a need for companies to give a

greater push to improve customer ser-

vice. We have been speaking about this

for a few months, not to say for a few

years, in the cooperative sector; we know

that cooperatives cannot escape this real-

ity. Many cooperatives are facing prob-

lems of capitalization and I must tell you

that again yesterday, at the Executive

Committee meeting of the International

Co-operative Banking Association, we

found it regrettable to lose some mem-

bers that are under restrictions of a

national law or market laws to transform

to share capital companies. Cooperatives

are facing problems of capitalization. You

also know that the insurance sector, in

many countries, is being flooded by a

wave of demutualization. All of this

brings us back to the theme of our semi-

nar “Capital, Demutualization and

Governance”.

To discuss these important topics, we

have the great pleasure of having four

speakers who are experts in this field.

First, Mr. Mervyn Pedelty, of United

Kingdom, Mr. P.V. Prabhu, from India,

Mr. Jacques Henrichon, Deputy Ins-

pector General at the Québec govern-

ment, and Mr. Klaus Fischer, professor at

l'Université Laval, in Québec.

Four guests will comment on the

speakers: Mr. Enrique Rodrigez, of

3

A word from the president

Mr. Claude Béland, President of the Mouvementdes caisses Desjardins, and president of the

INTERNATIONAL CO-OPERATIVE BANKING ASSOCIATION

I

Ladies and Gentlemen,

SwedBank, Mr. Carlos Heller, Director

General of Crédicoop of Argentina,

Mr. Erastus Mureithi, Director General

of the Co-operative Bank of Kenya and

finally, Mr. Alban D'Amours, Inspector

and Auditor General of the Mouvement

des caisses Desjardins.

4

Good morning Ladies and Gentlemen

hat makes mutual and co-

operative ventures special? What makes

them different from conventional share-

holder companies? And what makes

them better?

We need answers to all these ques-

tions — because these are the questions

that ordinary people have increasingly

been asking since the 1980s. And until

very recently, I am not convinced that we

have been giving them the answers they

want to hear. As managers of Co-opera-

tive Banks, we are all facing a historic

challenge. The very concept of mutual

ownership appears to be under sustained

attack in many countries. And, at the

same time we are seeing significant

changes in the way that financial services

are conceived, targeted and delivered.

Traditional barriers between banking,

insurance, investments and securities are

melting away, as are the traditionally sep-

arate distribution channels which satisfy

customers’ needs for these various prod-

ucts. It’s not a time for complacency. But

nor is it a time for panic. And it’s certain-

ly not a time for abandoning the values

and principles of co-operation. But now

- as always - we must think about how

we apply these principles and values.

And in particular how we apply them in

three critical areas:

• capital

• democratisation

• and governance.

Capital remains the key to continuing

success. Lower barriers to entry, compe-

tition from all sides – including new

entrants like supermarkets - and innova-

tions like the Internet are transforming

today’s financial services. And to stay at

the cutting edge we must continue to

5

“Capital, Democratisation and Governance”

Mervyn PedeltyChief Executive, Co-operative bank p.l.c.

(Manchester, United Kingdom)

W

invest, and optimise the capital we use in

our businesses. Democracy is a part of

our culture.

In fact, you could say it’s our corner-

stone. Part of what makes mutuals and

co-operatives unique. After all, we are

ultimately owned by our members.

Others, like my own bank, adhere to co-

operative values and principles —

although the bank, of course, is owned

by The Co-operative Wholesale Society

(CWS), not by the bank’s own cus-

tomers.

Even so, CWS, our parent, is very

much a mutually owned membership

organisation. But here, too, in talking

about democracy and membership, we

are dealing with a moving target.

Members must have a real say in the

business. Democracy must have sub-

stance as well as form. Over the past few

decades – in the UK Building Society,

Insurance and Co-operative sectors - I

would argue that many mutually owned

organisations and co-operatives have lost

sight of their ultimate purpose. That

purpose being the need to recognise,

work for and reward their members. As

co-operative and mutual organisations,

we must improve the way in which we

respond to the needs of our members.

We need to think about governance

and ownership. And their relevance in

today’s changing world. That’s why the

word ‘democratisation’ is the right one.

Because profitably and efficiently

meeting the needs of our members and

customers is an ongoing process. Espe-

cially in the face of a rising tide of demu-

tualisation. Demutualisation is not an

isolated phenomenon.

We’ve certainly seen it in the UK. But

it’s also happening in parts of continen-

tal Europe, for example in Belgium and

in Australia, South Africa, Canada and

the United States. And the argument is

always the same.

We’re told that ‘the tide of history’ is

turning against mutual ownership. For

instance, both AMP and Colonial, large

Australian insurers, recently demutu-

alised. AMP’s head of global acquisitions,

Jonathan Schwarts, commented that:

‘The average mutual has a culture, an

organisational structure, a cost structure

and mode of operating that was set for a

set of social circumstances and a regula-

tory environment that no longer exists.’

A pretty clear point of view, I think

you’ll agree. But is it true? Has our mutu-

al, co-operative approach passed its sell-

by date?

For more than 200 years the UK

building societies enjoyed continuing

success as providers of mortgages and

savings products. That changed in 1989

when one of the leading UK societies —

Abbey National — converted itself into a

bank. The decision to convert came not

from the members, but from the Board.

And the results were dramatic. In fact

that single decision created a ‘domino

effect’ which has since fundamentally

changed the mutual movement in the

UK.

So why did Abbey National demu-

talise and convert itself? Their argument

ran as follows. In the 1970s, they saw

6

growing competition as the quoted

banks began to offer mortgage products,

and muscle in on the Building Societies’

traditional territory.

And, of course, banks were able to

provide a much wider range of products

and services because of the way in which

they were financed and regulated. To

respond, the building societies had to

offer more. Which called for investment

— and for more capital. According to

Peter Birch, the Chief Executive of Abbey

National at the time: ‘Abbey National’s

choice was either to see its traditional

and only market erode or test the con-

version hurdles.’ The key advantage of

the status of being a listed Public Limited

Company – a “PLC” - was the ability to

issue shares. In effect, Abbey National

could ‘print money’ in order to raise cap-

ital to expand or to finance the acquisi-

tion of other institutions. Through the

conversion of Abbey National we all

learned some crucial lessons. Lessons, in

particular, about capital, democratisation

and governance. Access to capital was —

and still is — one of the main motives

for demutualising. Mutuals, by their very

nature, are democratic — but that very

democracy can be turned against them.

The argument goes that members of a

mutual should always have the right to

vote on their legal status.

Even if that vote deprives future gen-

erations of the right to membership. And

if the Board decides to recommend con-

version, it’s very difficult for opposing

members to win a ballot on staying as a

mutual. That, in turn, tells us a lot about

attitudes to governance. Building soci-

eties have unique governance structures

— which, apparently, have very little sig-

nificance to most of their members.

Abbey National members believed they

could gain something of immediate

value — its shares, and therefore money

— by sacrificing something with little or

no perceived value to them— their

membership of the society. And that, of

course, could be said to have been very

much a part of a culture of greed that

was increasingly seen in the UK during

the 1980s. It’s difficult to say how much

that culture had to do with the Abbey’s

loss of mutual status. But moral and

long-term arguments do seem almost

powerless against the immediate lure of

‘free money’.

Morally, there was a strong case

against demutualisation. Morally, one

could argue that the members had no

right to fritter away the reserves built up

in trust by the hard working inter and

post-war generations. But that argument

cut little ice with the current members

— nor, apparently, with the government.

Because government, too, has a clear role

in enabling — by simply not preventing

— demutualisation. But for a while the

Abbey National remained out on its

own. Then, in the Spring of 1994, the

Cheltenham and Gloucester Building

Society announced plans to convert and

sell its business to Lloyds Bank. It ulti-

mately became Lloyds Bank’s specialist

mortgage lending arm. Later the same

year, the Halifax Building Society and the

Leeds Permanent Building Society

7

announced their intention of merging

under the Halifax name — and then to

convert to bank status three years later.

As you can see from table 1 (page 16),

many further deals were to follow — and

1997 became a very significant year. At

that point the financial windfalls to

members from converting mutuals

reached a peak.

35 billion pounds – or 55 billion US

dollars - was released into the British

economy through the conversion of the

mutual building societies. And one in

three UK adults received shares. And a

new form of gambling then emerged.

People tried to guess which societies

would be next in line to convert. The

trend of ‘carpetbagging’ began. It’s inter-

esting to note that the term ‘carpetbag-

ger’ dates back to the period of recon-

struction following the American civil

war. ‘Carpetbaggers’ were Americans

from the North who travelled to the

South to take advantage of the low prop-

erty and asset prices, or to gain political

advancement. Southerners believed that

they could tell true Southern American

gentlemen from such opportunists be-

cause Southern ‘gentlemen’ carried prop-

er leather bags, not bags made from car-

pet material. In more recent times it

seems that Peter Robinson, the former

Chief Executive of Woolwich Building

Society, reclaimed the term during the

demutualisation of his building society.

He allowed 30,000 people to join after

the society’s decision to convert was

made public. He then announced a deci-

sion to back-date the qualifying date, so

they were not eligible for the windfall

payments. He explained his actions say-

ing “I have no concern about not enfran-

chising carpetbaggers.”

These so-called ‘carpetbaggers’ placed

money in deposit accounts to become

members and so be in the front line for

free shares This also gave them voting

rights to sway the outcome of a ballot.

However, over the next two years the tide

turned and there was growing reaction

against ‘carpetbagging’ investors. And the

media began to emphasise one of the key

competitive advantages of the building

societies — price. It has been an interest-

ing reaction.

Until quite recently many mutual

organisations treated their members

almost as if they did not exist. As cus-

tomers they were recognised, of course,

but frequently not as members with

membership rights. All too often, many

of these organisations seemed to have

been run primarily for the benefit of the

directors, senior management team and

staff of the institution. Many seemed to

have forgotten or neglected their roots.

And, they were often protected by their

mutual status from the critical gaze of

institutional and individual sharehold-

ers. Certainly, the true owners - the

members - rarely appeared to be encour-

aged to get involved. The importance of

membership – and the rights conferred

by membership – were rarely adequately

communicated or demonstrated.

It is, therefore, probably no surprise

that the members themselves had gener-

ally taken no interest in the way in which

8

their society was run. In fact, until the

1980’s, the majority would not even have

been aware that they were members - or

what that meant. So why has member-

ship not been taken more seriously by

these institutions until recently - that is,

until the advent of the‘carpetbaggers’?

Well, apart from apathy, old habits

and - some might also say - self-interest

by the Boards of Directors, there may be

a deeper philosophical dilemma here.

Long standing mutuals owned by indi-

vidual members tend to acquire a very

large “membership” over time. It is not

difficult for these membership details to

become out of date as time passes. To

clean up this accumulated data, and then

to activate the membership base is a

more difficult, arduous and costly

process the longer it is left undone.

Particularly if it has been left virtually

untouched for ten, twenty or thirty years

- or even longer! And, communicating

actively with a large membership is an

extremely expensive process. Member-

ship can run into millions, or at least

many hundreds of thousands. Few com-

panies publicly quoted on a stock

exchange have a shareholder base of that

size. So, it might be reasonable to allow

the ‘benefit of the doubt’ to some of

those mutuals. Given the costs involved

of communicating properly and actively

reaching out to their membership, per-

haps they simply decided that it could

not be afforded. So they spent what bud-

get they could afford on relating to, and

communicating with, the small minority

of their member base that took member-

ship and democracy seriously. In other

words, they solved their philosophical

dilemma of whether to be an active mass

membership organisation or, alternative-

ly, an organisation that just looks after

the small minority of members who take

an interest, by taking the easier, less

expensive route.

I don’t know. Perhaps we will never

know the real answer, but it is worth

pondering. Because that dilemma is just

as relevant today as it was 10 or 20 years

ago.

Table 2 (page 16) shows the impact of

mergers and conversions on the UK

Building Society sector. In 1988, there

were 131 registered Building Societies in

the UK. Now there are just 71. Balances

within the sector have been decimated

Mortgage assets within the sector

have more than halved over the past two

to three years.(Table 3)

Whilst total assets show an equally

marked decline. (Table 4)

Insurance companies have also

demutualised at a steady rate over the

past 10 years. Currently there are only

23 mutual insurance companies, a 44%

decline since 1988.

Most of the mutual insurance com-

panies that have converted over the past

8 years are shown on (Table 5). The most

current is Scottish Widows which, sub-

ject to approval, will join the Lloyds TSB

Group in the early part of next year. As

the table shows, unlike Building Society

conversions, demutualisation is occur-

ring on a more gradual basis and there-

fore there is not one significant year.

9

Turning back now to the UK Buil-

ding Societies, they are now starting to

fight back. Maybe it is to counteract the

sudden realisation by their members that

they can control the future of their soci-

ety. Many Building Societies have decid-

ed to reduce their “profits” by offering

better mortgage and saving rates than

their non-mutual competitors. If you

like, they have started to provide their

members with some tangible benefits of

membership

As a result, they’re now achieving

consistently high positions in the ‘Best

Buy’ tables.

But there have also been some other

inventive initiatives. For instance, the

Britannia Building Society gives a share

of its annual profits to its members

determined by the number of products

held and the length of membership.

These strategies — and others like them

— have started to win back for the build-

ing societies a growing share of the

mortgage market. And, they are now

starting to punch well above their weight

in the UK mortgage market

As seen on Table 6, page 18, they cur-

rently provide 33 per cent of net new

lending, against their market share of

outstanding balances of 22 per cent.

They also account for about 33 per cent

of new deposit balances, against their

market share of 17 per cent share of out-

standing deposits. This swing back to

mutuality was apparently confirmed in

July 1997. Members of the Nationwide,

the largest remaining UK building soci-

ety, voted overwhelmingly against pro-

conversion candidates standing for elec-

tion to the board. Many commentators

saw this vote as a reaction against the

“get-rich-quick” culture of the 1980s —

and, to some extent at least, as a response

to the tone set by the newly elected

Labour government. Others — more

cynically — put it down to the absence

of credible pro-conversion candidates for

the board. Later, Nationwide announced

that it had changed its rules so that all

new members would have to donate the

proceeds of any conversion windfall to a

charity — and many other societies were

quick to follow suit.

The new rule removed the incentive

for ‘carpetbaggers’ to join the society —

and ensured that members were less like-

ly to be swayed by the lure of short-term

financial gains.

Also in 1997, the new Labour govern-

ment brought in a series of amendments

to the Building Societies Act. To achieve

conversion, at least 50 per cent of invest-

ing members must now take part in the

vote and 75 per cent of those voting

must vote in favour. Among borrowing

members, only a simple majority of

those voting is required. So has the tide

turned? Probably not. In July last year,

1998, members of the Nationwide

Building Society were once again asked

to vote on a motion proposing conver-

sion, and for pro-conversion candidates

standing for election to the board.

The conversion motion was defeated

but, this time, much more narrowly.

Comfortingly — at least for people

like us — the pro-conversion candidates

10

were not particularly successful in win-

ning votes. But pressure on the Nation-

wide continues.

A leading UK national newspaper,

The Sunday Express, argued – and even

led a front page campaign - that if the

society converted, 2 billion pounds

would be donated to good causes via the

new anti-carpetbagger charity rule

adopted by the Nationwide.

That campaign has now died down

— but the threat remains.

This year the members of the large

Bradford and Bingley Building Society

also voted to convert — directly against

the recommendations of their own

board. It’s the first time this has occurred

— and the conversion of Bradford and

Bingley will now take place over the next

two years. Although we can expect a

strong rearguard action from disen-

chanted members who resisted the

process, it must also be recognised that

the Bradford and Bingley was the only

society which failed to protect itself

against the carpetbaggers with a new rule

change. Not surprisingly, many observers

are puzzled by this. So what does the

future hold for UK building societies?

With mortgage assets of 100 billion

pounds – 160 billion US dollars - and

annual profits of a billion pounds,

they’re still a significant force in the mar-

ket But even so, the Building Societies

Association is arguing for even stronger

legal protection against carpetbaggers.

And it wants demutualisation voting

hurdles for borrowing members to be set

as high as those for investing members.

However, in July this year, the UK

government announced that it did not

have enough parliamentary time to

bring in these measures. The Treasury

Minister, Patricia Hewitt, also felt that

these changes could not be guaranteed to

prevent more conversions anyway. In her

words, “The responsibility for saving the

mutual sector lies above all with the

mutuals themselves and their members”.

A clear and unequivocal message. Even

so, the surviving building societies —

few as they are — have learned their les-

son. They have built their own defences

against the ‘carpetbaggers’. Some of these

defences have been as a result of chang-

ing their Society rules in the ways I have

just described. Other defences have been

as a consequence of recognising that they

have a duty to encourage closer involve-

ment by their members in their societies.

And of the need to communicate more

to them - even if it costs money to do so.

They have come to recognise the

need to make membership meaningful,

and to provide real and tangible benefits

to their members. This recognition has

been in the form of more competitive

pricing on both sides of the balance

sheet, as well as by promoting the

“mutual” difference. Only history will

show whether the rear-guard actions of

the Nationwide and other Building

Societies will be successful in stemming

the tide of demutualisation in the UK.

Even both of the UK’s largest motor-

ing organisations — the AA and the

RAC – have also elected to convert. And

our own parent company, CWS, was

11

obliged to defend itself against a hostile

bid from a corporate raider in 1997. And

the experience in the UK has been mir-

rored in many other parts of the world,

including Canada, the United States and

South Africa. In Canada the four leading

mutual insurers — Mutual Life,

Manulife Financial, Sun Life and Canada

Life — are in the process of demutualis-

ing. They’ll be distributing shares worth

more than 10 billion Canadian dollars to

their Canadian policyholders. The ratio-

nale appears to be the same — easier

access to capital markets, and a currency

for mergers and acquisitions. Here, too,

government agreement has been crucial

— because, here in Canada, the law has

been changed to permit mutual societies

to demutualise. And here, too, in

Canada, there are organisations resisting

the process.

“The Co-operators” is an insurance

co-operative founded more than 50 years

ago by a group of Saskatchewan wheat

farmers. Soon afterwards a similar initia-

tive started in Ontario. The two joined

forces, and became the largest wholly

Canadian-owned multi-line insurance

company. They have announced their

intention to remain true to their origins.

But the flood of international demutuali-

sations continues. Though not, it seems,

everywhere. In some countries —

notably the Netherlands, Germany and

France — the regulatory constraints are

far tougher. There are restrictions on

winding up mutuals — restrictions that

mostly prevent UK-style carpetbagging.

And in the event of a conversion, the

owners of mutual banks are not allowed

to gain any personal benefit from the sale

of their shares. The results speak for

themselves. In the Netherlands, I under-

stand that mutual banks account for

35 per cent of all retail deposits. And, in

Germany the figure for mutuals is about

30 per cent, while just under 20 per cent

of total deposits are held in co-operative

banks.

In fact two out of three German

banks are mutually owned. To keep pace

with new developments in technology —

and service — 164 co-operatives have

merged over the last year.

In fact, some observers believe that

the total number of co-operative banks

in Germany may drop as low as 800

within five years — as modernisation

continues. There is a similar picture in

France, where mutual banks account for

37 per cent of retail deposits. Co-opera-

tive banking groups like Crédit Mutuel

and Crédit Agricole are large and very

successful. They’ve even acquired shares

in commercial banks. Indeed, the mutual

sector has even aroused complaints from

non-mutual competitors about the

‘mutualisation’ of the French economy!

On the strength of these figures, legal

restrictions do seem to help. But is this

the right road to travel? Clearly, it’s

important to create a supportive public

policy environment in which mutuals

can thrive. France and Germany recog-

nise that it’s wrong to turn a healthy,

competitive mutual into an investor-

owned organisation simply to satisfy

short-term interests. So we should, in my

12

belief, continue to champion the cause of

government support for thriving and

independent mutuals. But at the same

time we must address the key issues I’ve

already identified. And we must protect

ourselves, as the Nationwide Building

Society has done in the UK, by tipping

the balance in favour of mutuality and

long-term benefit.

It has taken generations to build up

our mutual institutions into the success-

ful institutions of today. And we owe it to

those generations to protect their legacy

with every resource at our disposal.

Regrettably, moral constraints are not

enough. But nor, on its own, is legal pro-

tection. To make a real success of ‘new

mutualism’ we must return to those

three key issues: capital, democratisation,

and governance. Demutualisations have

often been motivated by the desire to

raise capital on the stock market.

Mutuals need to offer an alternative to

this — and one alternative is to use our

existing capital more efficiently. To max-

imise the loyalty, involvement — and

profitability — of our members. To

reward them for buying more products

and services from us. And to think, cre-

atively, about partnerships with non-

mutual companies. By outsourcing and

joint-venturing — and keeping a clear

focus on the things we do best — we can

increase our efficiency, as well as offering

new products and services. We also need

to think about capital, the lifeblood of

our businesses across the world. We need

to look at the way in which Co-operative

Banks raise capital. We need to share our

experiences, so that we can all learn from

each other. In researching this presenta-

tion, it became evident that there is no

one single source which has an overview

of the many ways in which Co-operative

Banks across the world raise their capital.

This is such an important issue that I

would like to propose a study. A research

project if you like. One to which we

could all contribute. To help us under-

stand this important issue. I therefore

invite the ICBA to look at the possibility

of carrying out an international survey

to review capital raising for co-opera-

tives... And I hope we can all find the

means to help fund it. Because we will all

ultimately benefit from the results.

What about democratisation? Clearly

we need to look at new ways of building

the relationship with members. Ways

that are not solely dependent on price.

We must deliver value in many ways.

Through unrivalled quality of service.

Through the most advanced service

channels — including telephone and

Internet banking. And through competi-

tively priced products. Mutuality is no

excuse for second-rate services. At The

Co-operative Bank in the U.K. we recog-

nise that the definition of value must be

far broader than this — because that’s

what our customers are telling us. We

surveyed 1.2m customer households

using a detailed questionnaire. We asked

how we could deepen our relationship

with them. The results were very clear.

They want democratisation. Because

they want to be more deeply involved in

product, service and policy development.

13

But to encourage that participation —

and increase its value — our customers

were telling us that we must also behave

in a socially responsible and ethical man-

ner. Traditionally, we’ve been seen as

responsive to the concerns of communi-

ty and society. That has been one of our

strengths. Yet many mutuals and co-

operatives have acted in the past like

non-mutual and non-co-operative com-

panies. They sorely neglected their mem-

bership and their customers. My own

bank also went down this road in the

1980s. But the recent success of our ethi-

cal stance shows just how wrong we

were. It has attracted new customers. It

has boosted the value of our brand enor-

mously. And it proves that social respon-

sibility has nothing to do with woolly-

minded philanthropy. Nor has it any-

thing to do with poor quality products,

second rate levels of service and low lev-

els of profitability. In fact it shows that

social responsibility is crucial to the con-

tinuing success of mutuals and co-opera-

tive banks. So how can you define the

social and ethical stance that your partic-

ular co-operative institution should be

taking?

You don’t. The answer must come

from your members and your customers

— after all, it’s their money! Every three

years my own bank invites customers to

vote on how their money should, and

should not, be invested. By putting them

in the driving seat, we’ve deepened our

relationship with them — and given

ourselves a unique position in the UK

banking market.

We’ve also given customers the

chance to participate in the campaigns

that we run with charities, and to decide

how money should be allocated to them.

By building the relationship with cus-

tomers, these schemes provide a power-

ful form of added value. And it’s worth

far more than a short-term price differ-

ence.

In France, Crédit Mutuel, like our-

selves in the UK, have promoted a more

socially responsible approach. For

instance, Crédit Mutuel backed the move

towards a 35-hour week. They also sup-

port youth employment programmes.

And they’ve focused on channelling

resources into local development to

combat economic and social exclusion.

We have actively promoted the benefits

of co-operative and mutual ownership to

the general public and to our govern-

ments. In the UK, for instance, The Co-

operative Political Party has played a sig-

nificant role in reviving the debate about

“new mutualism”.

It has published four papers on the

subject, covering issues as diverse as

ownership of football clubs and social

exclusion. As a movement – within the

UK at least - we’ve often been inward-

looking and we’ve often failed to set out

the intellectual arguments for a healthy

co-operative and mutual sector. That is

changing — and it must continue to

change. But governments also have a

responsibility. A responsibility to think

through these ownership issues more

carefully. Privatisation and demutualisa-

tion are partly the result of an ideology

14

that appears to recognise only one effi-

cient form of ownership - the investor-

owned company. The truth is that we

need a rich diversity of ownership,

because of the social and economic ben-

efits it produces. This year, one of The

UK Co-operative Party's pamphlets

called for a Royal Commission on

Ownership to be established by the new

Labour Government. Its aim would be to

encourage a campaign of mutualisation

in Britain. This is the kind of policy pro-

posal that we need to trigger a real

debate about the potential of mutuality

in the modern world. For two decades,

the political focus has been on the opti-

mal balance between public ownership

versus private ownership. I believe we

need an equal focus on mutuality and

co-operation. I hope that every bank

here will encourage their government to

take a long, hard look at the real impor-

tance of mutual and co-operative owner-

ship. This is the challenge of new mutu-

alism. We cannot — and must not —

resort to sentiment in our efforts to pre-

serve our co-operative status.

But our heritage, and our values,

should inspire our actions — and pro-

vide us with a ‘moral compass’. We

must continue to modernise — and to

democratise — because only through

member democracy can we demon-

strate the real value of mutual and co-

operative ownership. We must continue

to advocate the benefits of mutual

ownership — and continue to ensure

that our governments listen to us.

Because it is our responsibility — and

our duty — to build a strong co-opera-

tive and mutual sector for the genera-

tions that will follow us.

15

16

TABLE 1

TABLE 2

17

TABLE 3

TABLE 4

18

TABLE 5

TABLE 6

19

P.V. PRABHU, trustee-Secretary, national centrefor management development in agriculture & Rural

Development Banking, bangalore, India

Capital, demutualisation and governance- indian cooperative credit & banking scenario

T

I New Economic Policy - Financialand Banking Sector Reforms

he deepening economic crisis in

the country in 1991 characterised by bal-

ance of payment problems, disrupted

industrial production, depleted foreign

exchange reserve, budgetary deficit com-

bined with accelerated inflationary

trends prompted the Government to ini-

tiate major policy changes designed to

correct the macro-economic imbalance

and effect structural adjustments.

Important connotations of this policy

package are:

1. Liberalisation

• Dismantling the control regime

• Delicensing and decontrolling indus-

tries and trade

• Reformation of fiscal and financial

policies

• Encouraging direct foreign invest-

ment; opening up of economy

2. Market orientation

• Minimum role and involvement of

Government in influencing market

mechanism

• Competition

3. Privatisation

• Divesting Government ownership of

economic enterprises

• Encouraging promotion of private

sector enterprises

4. Globalisation

• Encouraging free flow of foreign

capital and technology

• Encouraging establishment of inter-

national joint ventures

• Dismantling restrictive trade regime

and permitting entry of MNCs.

The financial sector reforms are an

important component of the overall

scheme of structural reforms. Reserve

Bank of India, the country's central bank

and monetary authority took initiative to

set up the Reforms Committee and rec-

ommendations of which were aimed at

improving the productivity, efficiency

and profitability of the banking system.

They also aimed at providing the bank-

ing system much needed operational

flexibility and functional autonomy. The

following were the major components of

the reforms recommended by the

Committee:

1. Relaxing the barriers towards entry of

private banks in the banking system.

2. Liberalisation of branch licensing

policy.

3. Reorganisation of the banking struc-

ture.

4. Capital restructuring of Indian

banks.

5. Introduction of prudential norms

covering capital adequacy, income

recognition, asset classification and

provisioning.

6. Administered interest regime to give

way to market driven interest rate

regime.

7. Reduction of the proportion of

directed credit programmes.

8. Reduction of statutory reserve requi-

rements with a view to releasing

resources for profitable lending.

9. Strengthening the organisational and

legal framework for better recovery of

bank loans.

10.Establishment of an Asset Recons-

truction Fund to take care of the loss

assets of banks.

The prudential norms including cap-

ital adequacy were initially made applic-

able to Commercial Banks. Though the

Reforms Committee in its report had not

covered cooperative banking sector, RBI

made some of the recommendations

applicable to cooperative banks includ-

ing Agricultural and Rural Development

Banks and Urban Coop. Banks particu-

larly the norms relating to income recog-

nition, asset classification and provision-

ing for Non-Performing Assets (NPAs).

The Committee on Banking Regula-

tions and Supervisory Practices (Basle

Committee) had, in July 1988, laid down

an agreed framework, on international

convergence of capital measure and capi-

tal standards. This framework required

the banks to measure capital adequacy

on the basis of risk weighted assets and

get a minimum standard of 8% particu-

larly for banks conducting significant

international business. The framework

suggested by the Basle Committee was to

be applied by banking supervisory

authorities of various countries. Indian

commercial banks which have branches

abroad were required to achieve the

norm of 8% by March 31, 1994. Foreign

banks operating in India were required

to achieve this norm by March 31, 1993.

Other banks were required to achieve the

norm of 4% by March 31, 1993 and 8%

by March 31, 1996.

Prudential norms relating to capital

adequacy were perhaps not made applic-

able to RRBs and cooperative banks

(viz., Urban Cooperative Banks, ARDBs

and State / District Coop. Banks) for the

20

reason that they are not doing any signif-

icant international business. Also in the

case of cooperative banks, the share capi-

tal raised is linked to the loans disbursed

by them. Even though the Basle Commi-

ttee released the framework in July 1988,

it was made applicable to Commercial

Banks in India only in 1993 after the eco-

nomic policy reforms were introduced in

the country. It is reported that 25 out of

27 public sector banks have achieved the

8% capital adequacy norm.

Substantial financial assistance has

been provided by the Government of

India for cleansing of the Balance Sheets

and Recapitalisation of public sector

banks including Regional Rural Banks

from out of successive budgetary alloca-

tions. Such funding support provided by

the Government upto February 28, 1998

was of the order of Rs.200 billion. Seve-

ral financially sound public sector banks

including State Bank of India, the biggest

bank in the country and two of its sub-

sidiaries have successfully raised capital

from the capital market at a premium.

In order to introduce greater compe-

tition in the banking system, the RBI

gave approval for establishment of new

banks in the private sector with mini-

mum equity of Rs.1 billion which has

since been raised to Rs.2 billion. Nine

such new private sector banks have been

set up in the country which have raised

capital from primary market. NPAs of

new private sector banks ranged between

1% and 7% whereas in the public sector,

9 banks had NPAs of over 10% in

1998-99. Because of the market pressures

and application of various regulatory

norms, some of the large public sector

banks have reported substantial losses in

1998-99 resulting in total wiping out of

their net worth. For all the 27 public sec-

tor banks put together, their net profit

was 34.6% lower in 1998-99 over the

previous year.

In April 1998, the Reserve Bank of

India proposed to further strengthen the

existing capital adequacy, income recog-

nition, asset classification and provision-

ing norms as well as disclosure require-

ments of banks and achieve greater

transparency in banking operations and

bring these up to or exceed international

standards after taking into account the

recommendations of the Committee on

Banking Sector Reforms (second genera-

tion). Some of the major recommenda-

tions of the Committee for strengthen-

ing the Banking system are as under:

1. Stepping up of the minimum Capital

Adequacy Ratio from the existing

8% to 10% by 2002.

2. A 5 per cent weightage to be assigned

to investments in Government and

Approved Securities to hedge against

market risk.

3. Net NPAs to be brought down to

below 5% by 2000 and 3% by 2002

and banks with international pres-

ence to reduce gross NPA to 5 per

cent and 3 per cent by 2000 and 2002

and net NPAs to 3 per cent and 0 per

cent respectively.

4. Further tightening of the Prudential

Norms relating to Income Recogni-

tion (reduction of present norm of

21

180 days for considering an asset as

NPA to 90 days in a phased manner

by 2002). Asset Classification (redu-

tion in the period for classifying a

NPA as 'Doubtful Asset' to 18 months

and eventually to 12 months) and

Provisioning (1% provision even on

Standard Assets).

5. Cooperative Banks to reach a mini-

mum of 8 per cent capital to risk

weigted assets over a period of 5 years

by raising capital from members

without any assistance from Govern-

ment.

The Reserve Bank of India has

already advised the public sector banks

to raise minimum required Capital

Adequacy ratio from 8 per cent to 9 per

cent by end March 2000 and thereafter

10 per cent.

The action on other major recom-

mendations are under examination of

the authorities.

II Cooperative Credit and BankingStructure

India adopted Raiffeisen model of

rural credit cooperatives in the begin-

ning of this century to combat the prob-

lems of usury and indebtedness of farm-

ers and to rejuvenate the then stagnant

rural economy. From that stage, the

cooperative movement in India came a

long way, mainly through the efforts and

contribution of cooperators, Govern-

ments and members. Today, the short-

term credit structure specialising in pro-

duction credit is functioning with 3-tier

structure (SCB at apex level, DCCBs at

district level and PACS at grassroot level)

in 15 States and with 2-tier structure

(without DCCBs) in 12 States/Union

Territories. The LT structure specialising

in investment credit, is functioning with

a federal 2-tier structure (SCARDBs at

apex level and PCARDBs at block level,

with or without branches) in 11 States

and with unitary structure (SCARDB

with branches at lower level) in 8 States.

In one State, ST and LT structures are

integrated and the integrated structure is

catering to both investment and produc-

tion credit needs of its clients through

SCBs, DCCBs and PACS.

The origin of urban credit movement

in India can be traced to the close of the

nineteenth century. Following the suc-

cess of urban credit institutions in

Germany and Italy during the latter half

of eighteenth century, some middle class

Maharastrian families settled in the erst-

while Baroda State started a mutual aid

society in 1889. When the Cooperative

Societies Act of 1904 conferred legal sta-

tus to credit societies, the first urban

cooperative credit society was registered

in the then Madras province in October

1904. The failure of local joint stock

banks in the country gave an impetus to

the urban cooperative credit societies.

Later the economic boom created by the

Second World War provided a stimulus

to the growth of urban banks in India.

They grew not only in number but also

in size, diversifying their activities con-

siderably.

22

The network of financial coopera-

tives is presented in the following chart:

Credit Societies: Apart from the

above three major structures of coopera-

tive credit and banking sector, there are

38000 credit societies which are similar

to Credit Unions providing credit ser-

vices to members from the savings raised

from them.

Cooperative Bank of India (COBI):

Establishment of Cooperative Bank of

India at the national level has been a

major development in our country as

this is expected to fill the systemic gap in

the cooperative banking sector. COBI

will also serve as a balancing centre for

drawing surplusses and for deploying

funds covering the entire cooperative

banking sector. The capital base of

Rs.1000 million of COBI is expected to

be raised from member institutions in

relation to their relative financial

strenght. This Bank, however, has not

been operationalised because of delay in

securing the formal

banking licence from

RBI due to certain legal

hurdles.

Performance

The cooperative credit

structure covering ST

and LT put together

accounts for 69% of the

rural credit outlets

(107639 out of 155398).

Though they are not

comparable with com-

mercial banks in terms

of resources (CBs: Rs.5000 billion,

Cooperatives Rs.1067 billion) mainly

due to their poor deposit base, they are

favourably placed in terms of coverage

and outreach. They cover 647636 vil-

lages spread across 514 districts and

102 million operational holdings. Their

total membership is 98 million (bor-

rowing membership 42%). Of them,

42% are small farmers and 26% belong

to the weaker sections. On an average, a

primary unit covers 7 villages. Their

share in outstanding rural credit is

about 40% and they account for almost

50% of the annual credit flow in the

rural sector, of which about 60% is pro-

duction credit and 30% investment

credit.

Urban cooperative banks which

operate mostly in urban areas, play a

significant role in the non-agriculture

sector with over 6 million members

serving the banking needs of people

with small and modest means. They

23

account for about 6% of the entire

banking deposits and are totally self-

reliant in the matter of resources.

The position of resources and out-

reach of all the 3 structures viz., ST, LT

and UCBs as on March 31, 1998 is

pressented in the following table:

Major strengths and weaknesses of

Cooperatives

The major strengths and weaknesses

of cooperatives (ST & LT structures)

which serve agricultural and rural sector

are discussed below:

Strengths:

Network: As already stated, the

branches / grassroot level network of

cooperatives form 69% of rural credit

network in the country, virtually cover-

ing every village.

Vast human resources: The ST coop-

eratives employ around 220000 persons

and LT structure another 31000 persons.

Most of them are from local areas, well

versed with their area / clientele, their

needs and psychology. This invaluable

asset is one of the reasons for sustainable

performance of cooperatives in terms of

provision of credit, despite constraints

and competition.

Long standing experience in purvey-

ing rural credit: Cooperatives represent

the oldest rural credit delivery system

with over 8 decades of experience in

agricultural lending and they are fully

aware of problems and prospects of rural

lending.

Functional Societies: Besides provid-

ing avenues for deployment of resources,

the functional societies (marketing,

weavers, salary earners, consumer, etc.)

provide the benefit of linking of credit

with marketing.

Lower reserve requirements: Ever

since the application of Banking Regula-

tion Act to cooperatives, they are requir-

ed to maintain 3% and 25% of their time

and demand liabilities towards CRR

and SLR respectively. (CBs presently:

10% and 25%). This provides a greater

24

liquidity to cooperatives.

Refinance on concessional terms: Out

of the annual refinance provided by

National Bank for Agriculture and Rural

Development (NABARD), cooperatives

are presently enjoying more than 75%

share under production credit and 60%

share under investment credit. They also

enjoy concessions with regard to interest

rate and tenure of refinance.

Other support: NABARD is provid-

ing financial assistance to cooperatives

both through loans and grants from

Cooperative Development Fund and

R & D Fund for their operational impro-

vement and HRD.

Weaknesses :

Poor Resource Base: The total

resources of cooperatives were Rs.1067

billion of which around Rs.360 billion

were borrowings. The deposits mobilised

by rural and semi-urban branches of

commercial banks were Rs.1500 billion.

Except in 2 or 3 States, the resources of

primary units are very poor. On account

of poor resource base, a vertical depen-

dence on higher financial institutions is

evident. ARDBs are non-resource based

institutions though in the recent years,

some of them have made a beginning in

mobilising deposits.

Low business levels: The low business

levels, particularly at the level of PACS

(Average Rs.1.3 million), is one of the

major reasons for non-viability of coop-

eratives. The problem is more pro-

nounced in LT structure, particularly at

PCARDB level in some States.

Poor Recovery: The macro level reco-

very (loan repayment) rates were 84%

for SCBs, 60% for SCARDBs, 68% for

DCCBs and 56% for PCARDBs. 12 out

of 28 SCBs (less than 80%), 11 out

of 19 SCARDBs and 171 out of 363

DCCBs have comparatively less recovery

(less than 60%). 9 each of SCBs and

SCARDBs and 67 DCCBs suffer with

recovery less than 40%. Chronic over-

dues under ST (Rs.28 billion) and LT

structure (Rs.5 billion) pose serious

problem to the recycling of funds by

these institutions.

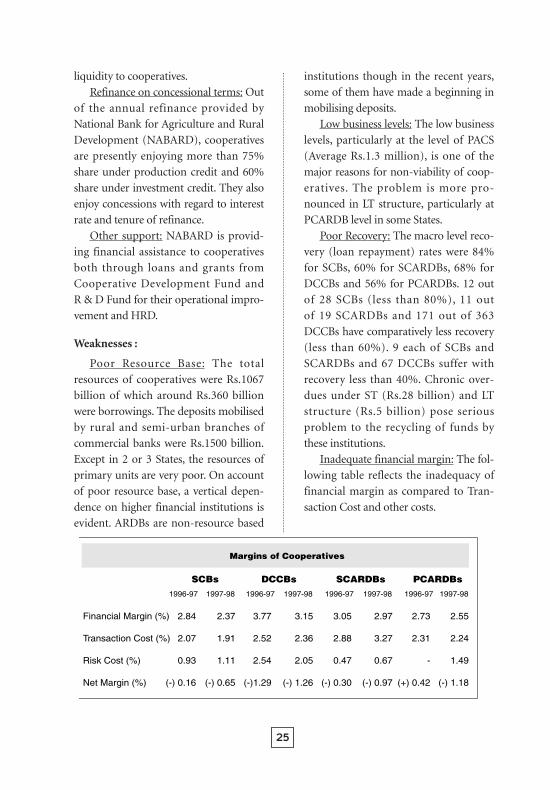

Inadequate financial margin: The fol-

lowing table reflects the inadequacy of

financial margin as compared to Tran-

saction Cost and other costs.

25

It may be seen that the financial mar-

gin is inadequate to meet transaction

and risk costs. On the basis of State aver-

ages, SCBs in 8 States, DCCBs in 20

States and SCARDBs / PCARDBs in all

the 19 States had negative net margins.

The increase in the negative net margin

as on March 31, 1998 was due to sizeable

increase in the risk cost on account of

implementation of provisioning norms.

Poor MIS: On account of poor data

flow, the managerial decision process is

not properly supported resulting in

delayed or imperfect decisions or both.

Process of computerisation of coopera-

tives is rather slow.

Lack of functional autonomy: Exter-

nal factors, affecting the functional

autonomy of cooperatives are targeting

both their democratic character and

operational liberty. This is affecting the

operations and efficiency of the coopera-

tives.

Unrealisable Asset: The unrealisable

assets consisting of accumulated losses,

imbalances in asset coverage and short-

fall in provisions for non-performing

assets in respect of a large number of

cooperatives (ST & LT structure) are esti-

mated at around Rs.70 billion (Rs.60 bil-

lion under ST and Rs.10 billion under LT

structures) against owned funds of

Rs.117 billion.

Imbalances in Profitability: Coopera-

tives in India are a strange pyramid with

large profitability at apex level and lower

profits or losses at grassroot level.

Operational Losses: The operational

losses of cooperation credit institutions

is a matter of serious concern and the

banks should make earnest efforts to

attain current and sustainable viability.

The working results as on March 31,

1998 are presented in the following table:

Non-compliance with Banking Regu-

lations: Due to erosion in capital as also

in deposits, several DCCBs are not com-

plying with the provisions of the Ban-

king Regulation Act and as such, are not

26

eligible for concessional funding support

from national financial institutions like

NABARD.

III Nature of Capitalisation issuesin India

Capital

Capital is one of the major indicators

of the financial strength of an enterprise.

For a banking institution, capital covers

risk of losses apart from reposing confi-

dence of the depositors and other credi-

tors.

In our context, capital has one more

important function and relevance.

Borrowing power of a financial cooper-

ative is linked to net worth as stipulated

in the Law. Net worth here means equi-

ty plus reserves minus accumulated

losses. For example, in Karnataka State,

borrowing power of a cooperative bank

is limited to 10 times the net worth.

This means the bank can raise deposits,

borrow funds from market or obtain

loan / refinance from financial institu-

tion to the extent of the borrowing

power in relation to net worth. Because

of this limitation, business expansion of

a bank is directly linked to its capital

base. In the case of Cooperative Agri-

culture & Rural Development Banks

engaged in term lending for agricul-

ture, the central bank has imposed a

ceiling on their raising deposits from

public which is limited to the banks net

worth. If the net worth or equity has

been eroded by losses, the bank will be

too keen to enhance the capital for

facilitating raising additional public

deposits.

Capital, in a broader sense is the

owned funds consisting of share capital

and reserves. Reserves represent profit

earned over the years that have not been

distributed to shareholders and retained

in the business. The accumulation of

such retained reserves reflects financial

soundness, stability and growth of

banks.

The capital base of cooperative credit

and banking institutions increases

steadily with the growth in business as it

is linked to loans and borrowers are

compulsorily required to contribute to

the share capital certain percentage of

loans ranging from 2.5% to 10%. This

system is quite different from Commer-

cial Banks, both public and private sector

banks, who raise capital from Govern-

ment and market by public issues. In

most of the public sector banks, capital is

held wholly or partly by the Government

with controlling interests. It is for this

reason, in the recent years, for augment-

ing the capital base of public sector

banks, Government of India have con-

tributed substantial sum to meet the

capital adequacy norms.

Reserves are results of profits and

there is limitation for augmentation of

reserves by S.T. and L.T. cooperative

structures due to inadequacy of profits

or because of operational losses as dis-

cussed earlier. Statutorily the coopera-

tives are required to set apart 25% of the

profits to Reserves and invest such

Reserves outside their business.

27

The positon of owned funds of coop-

erative banking structure consisting of

share capital and statutory reserves as on

March 31, 1997 is given in the following

table:

Cooperative banks in India, other

than Urban Cooperative Banks, besides

raising share capital from members,

which is linked to loans, also receive

equity contribution from the Govern-

ment as a matter of State policy. Such

capital held by State Governments in the

cooperative banking structure ranges

from 10% to 20% as indicated in the

Table below:

Though the Government contribu-

tion to the equity of cooperatives was

helpful initially, there is a growing feeling

among cooperatives, some of which are

fairly strong, to repatriate Government

equity in order to minimise State control

and interference in their working. In any

case, in the context of new economic

policy and financial sector reforms,

Government support by way of addi-

tional capital is not likely to forthcome to

cooperative banks in any significant

manner in the coming years.

In the private sector banks, equity is

held mostly by public and financial insti-

tutions. Besides promotors' investment

in equity, they enter the capital market

on their own strength to augment capital

to meet the international standards and

it may not pose any serious problem

unless they are in bad shape.

Capitalisation

As mentioned earlier in this paper,

cooperatives have share linking norm in

terms of which the borrowing members

are required to take up a certain percent-

age of loans towards share capital. While

the banks would like to augment capital

by increasing this ratio of capital to loan,

the borrower may not be interested in

increasing the rate of linkage as it would

put additional burden on him and ren-

der the loan less attractive. Also, there is

'nil' or inadequate return on such capital.

Because of low level of profitability,

majority of the banks have not been pay-

ing dividend on share capital. Even the

best of the cooperatives cannot normally

pay dividend over 15% on capital in view

of the legal restrictions and cooperative

28

policy of limited return on capital.

Cooperatives are expected to utilise prof-

its for augmenting owned funds by way

of reserves.

Based on the recommandation of All

India Rural Credit Survey Committee in

1954, Government as a matter of State

policy, has been contributing to the share

capital of cooperative credit and banking

institutions to make them financially

strong. For such shareholding by Gover-

nments, NABARD provides loans at con-

cessional rate from out of the special

fund viz., National Rural Credit (Long-

term Operation) Fund maintained by it.

There is no equity contribution to Urban

Coop. Banks by the Government and

they raise their equity entirely from

members.

As compared to public and private

sector banks, the shares of cooperatives

neither appreciate in value nor they are

traded in the secondary market. Also,

they are constrained to raise capital

through the primary market. These are

the bottlenecks for augmenting capital

by cooperatives.

Cooperative Banks have not made

any significant attempt for capitalisation

and most of them continue the age old

practice of raising equity from members

in relation to the borrowing. One reason

for this could be non-application of cap-

ital adequacy norm. They may soon

realise the inadequacy of capital with

application of international standards.

The growth in the capital is found to be

not commensurate with the growth in

business for the following reasons:

• Borrowers obtaining second and sub-

sequent loans may have to take up

additional shares only marginally.

• Face value of the share which was

earlier Rs.10 /- has not been raised in

some banks even though the rupee

value has decreased over the years

due to inflation. Even where changes

are made, it is still found to be much

lower. Face value of the share should

be much higher for ensuring growth

in equity.

• Share linking to loans is still lower at

3% and 5% in some banks and unless

this ratio is enhanced, equity growth

will not be substantial.

• Shareholders have a right to redeem

their holdings when loan liability is

cleared. However, by convention, it is

observed in some Cooperative Banks

(particularly L.T. structure) that the

entire equity holding of a member is

adjusted against the last loan instal-

ment thus depriving the bank of

much needed capital. This practice

needs a relook for retaining some

portion of the shares held by mem-

ber-borrowers.

Recapitalisation

Cooperatives, in keeping with their

principles, have been operating as service

sector institutions. There was no serious-

ness on their part to work as economic

enterprises. They were subjected to sev-

eral controls and restrictions by mone-

tary / refinancing authorities and Gover-

nment. Until 1994, they were required to

mobilise deposits and provide loans at

29

regulated interest rates with inadequate

spread / margin even to meet their trans-

action and other costs. The advances

were also regulated by the Government

through a system of directed credit for

priority sectors or poverty alleviation

programmes. Cooperative banks along

with public sector banks were also

required to implement Agricultural and

Rural Debt Relief Scheme (ARDRS) in

1990 under which benefits given to

farmers (towards defaulted loans) upto

certain extent were to be reimbursed to

the banks by the Government. The coop-

eratives were put to a disadvantage and

suffered liquidity problems as Govern-

ment support in relation to volume of

loans waived was not provided for fully

and that, further, there was considerable

delay even in the settlement and release

of dues. More than anything, implemen-

tation of this populist scheme resulted in

vitiating the recovery climate which even

otherwise was not so good. These, cou-

pled with the application of provisioning

norms for NPAs have resulted in sub-

stantial losses to cooperative banks.

Hence, cooperatives have been pleading

with the Government for funding sup-

port as one time measure to cover losses

by recapitalisation on the lines of sup-

port extended to public sector banks.

The estimated funding support for banks

in ST and LT structures for cleansing

their balance sheets is of the order of

Rs.70 billion. Response to this demand

has not been positive so far. There is,

however, no such proposal for support to

UCBs, as most of them are working in

profits and where Governments have no

equity holding. In the context of changed

economic policy, State Governments'

future support for increasing capital base

of cooperative banks will not be encour-

aging. On the contrary, cooperatives may

have to retire Government equity hold-

ing by stages in due course for their own

autonomy.

Prudential Norms: As a follow-up of

the financial sector Reforms Committee

recommendations, prudential norms

involving income recognition, asset clas-

sification, provisioning, valuation of

investments and capital adequacy were

introduced to various banks in India

beginning from 1992-93 as under:

The capital adequacy norms have not

been made applicable to cooperative

banks (including UCBs) and Regional

Rural Banks so far.

With a view to preparing the Balance

Sheet and Profit & Loss Account and

reflecting bank's actual financial health, a

proper system for recognition of income,

classification of assets and provisioning

on a prudential basis was found to be

essential. While the norms for income

recognition is based on record of recov-

ery (realised income), the classification

30

of assets has to be done on the basis of

objective criteria which would ensure a

uniform and consistent application of

norms. It would be necessary that the

provisions are made on the basis of clas-

sification of assets into 4 different cate-

gories viz., standard, sub-standard,

doubtful and loss.

After classification of assets, the

aggregate NPAs and their proportion to

total outstanding advances in respect of

banks in the ST and LT structures as on

March 31, 1998 are given in the follow-

ing table :

While the first reforms committee dit

not examine and make any specific rec-

ommendation to cooperative banks as to

the application of various norms, the

second generation of reforms (yet to be

made applicable) include the following

specific references to cooperative banks :

• There should be no recourse to the

scheme of debt waiver.

• Cooperative banks should reach capi-

tal adequacy of 8% over a period of

5 years.

• Cooperative credit institutions to

enhance their capital through sub-

scription by members and not by

Government.

• The present duality of control over

the cooperative credit institutions

by State Governments and RBI /

NABARD should be eliminated and

all coop. banking institutions should

come under the discipline of B.R. Act

by suitable amendments of the said

Act.

The capital adequacy norms are

expected to be introduced to cooperative

banks shortly. A big question is whether

cooperative banks would be able to

adhere to the capital adequacy norm of

8% especially when the erosion in their

assets has been increasing from year to

year. A quick study of the two banks in

Karnataka State (SCB & SCARDB) made

for assessing the adequacy or inadequacy

of capital requirement by application of

norms stipulated for commercial banks

reveals that while the SCB's capital of

10% of the risk weighted assets is found

to be above the prescribed standard, in

respect of SCARDB, the equity ratio of

5.3% is much below the required level.

Quality of Assets: There is one basic

difference in the standard of assets

acquired by the cooperative rural bank-

ing sector in India as compared to the

public and private sector banks. The

aggregate exposure of cooperative banks

loans portfolio in agricultural advances

is as high as 80% while that of commer-

cial banks at best may not exceed 20%.

The risk of lending is greater in our con-

ditions of agriculture looking to the

small size of holding, lack of irrigation

facilities, non-adoption of modern tech-

nology, fluctuation in the prices of

31

agri-products, marketing inadequacies

and above all poor economic conditions

of majority of farmers. Their risks are

not adequately covered by insurance

though the Government have recently

announced a package of comprehensive

crop insurance cover.

The assets created by cooperative

banks by advancing term loans for agri-

culture are secured by mortgages, whose

market value in no case is less than the

loans advanced. But these secured

advances or standard assets of the banks

are in reality substandard or risk assets

because of difficulties in converting them

into cash for realisation of dues. This has

posed serious problem and non-per-

forming assets (NPAs) of banks are dan-

gerously much above the containable

limit or above any accepted international

standard. Though in the balance sheet,

the capital of several cooperative banks is

apparently regarded as adequate, it might

prove grossly inadequate in several cases

to meet the international standards

against the risk weighted assets and thus

this threat of capital erosion has to be

converted as an opportunity for recapi-

talisation or funding by innovative

means from the global experiences. I am

afraid that this serious problem of high

level of NPAs, depleting profitability due

to provisioning on the lines stipulated by

the regulatory agency and certain opera-

tional compulsions of business develop-

ment in a liberalised competitive market

economy, may endanger the future of

cooperative credit and banking sector in

India unless remedial measures are taken

in a systematic and time bound manner.

This calls for in-depth study of the prob-

lems, gaining knowledge from the expe-

riences and practices of comparable

cooperative banking enterprises in other

countries, steps to improve the quality of

assets and their risk coverage, innova-

tions in the long practiced cooperative

way of carrying out business operations

and above all augmenting funds and

capital base through non-traditional

means.

IV Demutualisation

Cooperative identity and values have

been intensively deliberated upon at the

international forum and even the princi-

ples have been redefined not long ago.

Though there have been some compro-

mises here and there, the basic principles

have remained intact. One-member-

one-vote and limited returns on capital

are in fact the major constraints in aug-

menting capital in cooperatives. For a

successful and profitable cooperative

bank, there are quite a few of them even

in India, raising capital from market

besides member-holdings, is not going to

be a major problem. But how it is going

to be beneficial to the general public or

the corporate sector by holding on to the

cooperative principles of one-member-

one-vote and limited returns? We want

access to capital market and at the same

time do not wish to give up or dilute the

cooperative principles. Unfortunately,

'self-help' and 'mutual help' aspects in

cooperatives are not strong enough to

raise capital from members more than

32

what is mandatorily necessary. Like in a

credit cooperative, equity holding by

member in certain ratio is essential for

loan availment. If option is given, bor-

rowing member may not opt for holding

any additional shares except perhaps

what is essential for membership. I

would say that lack of member-interest,

member-involvement, member-partici-

pation and above all member-loyalty to

the cooperatives is a major cause of

worry for the future of cooperatives.

'Mutuality' in cooperatives is a major

casualty which will also act as a major

constraint for augmenting capital

through members.

There have been some isolated

attempts in France and Canada revealed

in ICBA Journals where shares and cer-

tificates are issued to members and non-

members quoted in stock markets carry-

ing dividends but without voting rights.

I feel that a cooperative bank with long

standing and popular by its services can

successfully raise capital from the market

through innovative capital instruments -

shares or otherwise - even without vot-

ing rights provided the bank is able to

repose investors confidence about rea-

sonable safety of investment and returns

on capital. Without resorting to demutu-

alisation as to members' rights and own-

ership, cooperative banks will also have

to evolve measures for member loyalty

and mutuality.

V Governance - Quality and Impact

Cooperative credit and banking

organisations (barring the Urban Coo-

perative Banks) were promoted and

established mostly at the instance of the

Government in its search for an institu-

tional arrangement to dispense rural

credit. The Government patronage and

preferential treatment besides conces-

sional funding support and equity par-

ticipation in the banking sector have, in a

way, helped in building up the structure.

At the same time, however, banks have