140 years continental 1871 – 2011 years continental 1871 – 2011 ... greatwall (tianjin ii plant)...

TRANSCRIPT

140 Years Continental1871 – 2011

1 / Jay Kunkel / © Continental AG

Automotive News China Conference

1

Jay KunkelPresident Continental China

Automotive News China Conference

China - Moving from Volume to Value

China – Moving from Volume to Value

a. How to manage the largest but most fragmented market ?

b. How to cope with changing regulatory policies ?

c. How to manage the demand for Fuel Efficiency, Safety and

2 / Jay Kunkel / © Continental AG

Automotive News China Conference

Information?

d. How to manage to develop and retain the required skill-sets?

China – Moving from Volume to Value

a. How to manage the largest but most fragmented market ?

b. How to cope with changing regulatory policies ?

c. How to manage the demand for Fuel Efficiency, Safety and

3 / Jay Kunkel / © Continental AG

Automotive News China Conference

Information?

d. How to manage to develop and retain the required skill-sets?

Opportunities – Low Vehicle DensityLow car density presents market opportunities, but growth in megacities is limited

above 55

40-55

30-40

below 30 Beijing:

191

Shanghai:

per 1,000 people

4 / Jay Kunkel / © Continental AG

Automotive News China Conference

Shanghai:

74National Vehicle density

(per 1,000 inhabitants)

785USA

Russia 254

Germany 536

China 53

Source: CSM light vehicle density database; National statistic reports

Opportunities – World class Chinese OEMs jump on the global stageChina becomes critical for the success of global OEMs

29% 12% 18% 14% 19%7% 12% 19% 13% 2% 15% 13% 100% 19% 97%

5%

51%

99% 83%

50%

75%

100%

8.2 7.6 7.5 6.8 6.7 5.3 3.5 3.2 2.4 2.3 1.7 1.6 1.4 1.3 1.1 0.9 0.8 0.7 0.6

2011 Global and China light vehicle sales of top 20 OEM groups

Global volume, mn unitsChina’s Contribution Rest of World Contribution

Total Volume

5 / Jay Kunkel / © Continental AG

Automotive News China Conference

Source: JD Power & Roland Berger

GM*: excluding SGMW; SAIC *: including SGMW

0%

25%

More and more regional involvement in global vehicle Planning, Development, Process and Design Verification and Purchase DecisionResult

Opportunities – Capacity ExtensionThe total number of car assembly plants will increase from 120 in 2011 to 142 in 2015

Greatwall (Tianjin II Plant)

Mid-size car, Hover H7

est. SOP:2012

Tianjin

BAIC Beijing C50. C60. C71, EV

est. SOP:2011

Beijing

ChangAn Auto (Beijing Plant)

Own brand passenger cars and new energy vehicles

SOP:2012

Cherymini-van

est. SOP: 2011

BAIC-Chongqing YinxiangMini van

SOP: 2012

Beijing Hyundai (III plant)Accent, Elantra, Yuedong, Sonata etc.

SOP:2012

Geely (Chengdu Plant)

Gleagle GX7, Emgrand EV8

SOP:2011

Daqing

Geely Volvo Volvo models

In Plan

Changan- Ford Mini van

SOP: 2012

Dongfeng Yueda Kia Motor Kia Forte, Soul, Carnival, Cerato, Optima, Rio

In plan

6 / Jay Kunkel / © Continental AG

Automotive News China Conference

SOP: 2012FAW VW Audi, Jetta, Sagitar, Magotan etc.

Foshan

Dongfeng-RenaultRenault Logon, Fluence

In plan

Guangzhou

ChangAn PSA (Hafei Plant)SOP: 2012

Shenzhen

Zengcheng

Shanghai VW

PVs

In plan

Kaifeng

Hangzhou

Dongfeng YulongLuxgen 7 SUV, MPV etc.

SOP:2011

BYD (Changsha plant)

Yizheng

SVW (Yizheng Plant)

Capacity: 300,000

SOP:2012

Shanghai

Chongqing

Changsha

Wuhan

Dongfeng Honda (Wuhan II plant)

Hongda CRV, CIvic, Spirior

DPCA (PSA)Peugeot 207/307, Picasso, Elysee, etc.

SOP: 2013

Chengdu

Gleagle GX7, Emgrand EV8

Geely Volvo Volvo models

In Plan

Nanchang

JMC (Jiangling Motors II plant)

Ford Transit, Landwind, Baowei, S-Drive

SOP: 2011

SOP: 2013

Nanjing

SGM-WulingChevrolet Lechi, Baojun( first model GP50), Wuling Mini-vans

Liuzhou

In plan

In plan

Source: CSM plant capacity report, media reports

Opportunities - Local Brand DevelopmentVehicle content (= Value) is significantly increasing with local brand differentiation

Local Brands Restructured Brands

CHERY

New JV Local Brands

Revival of high-end brands

Chinese Brands

7 / Jay Kunkel / © Continental AG

Automotive News China Conference

GEELY

Low end segment High-end segment

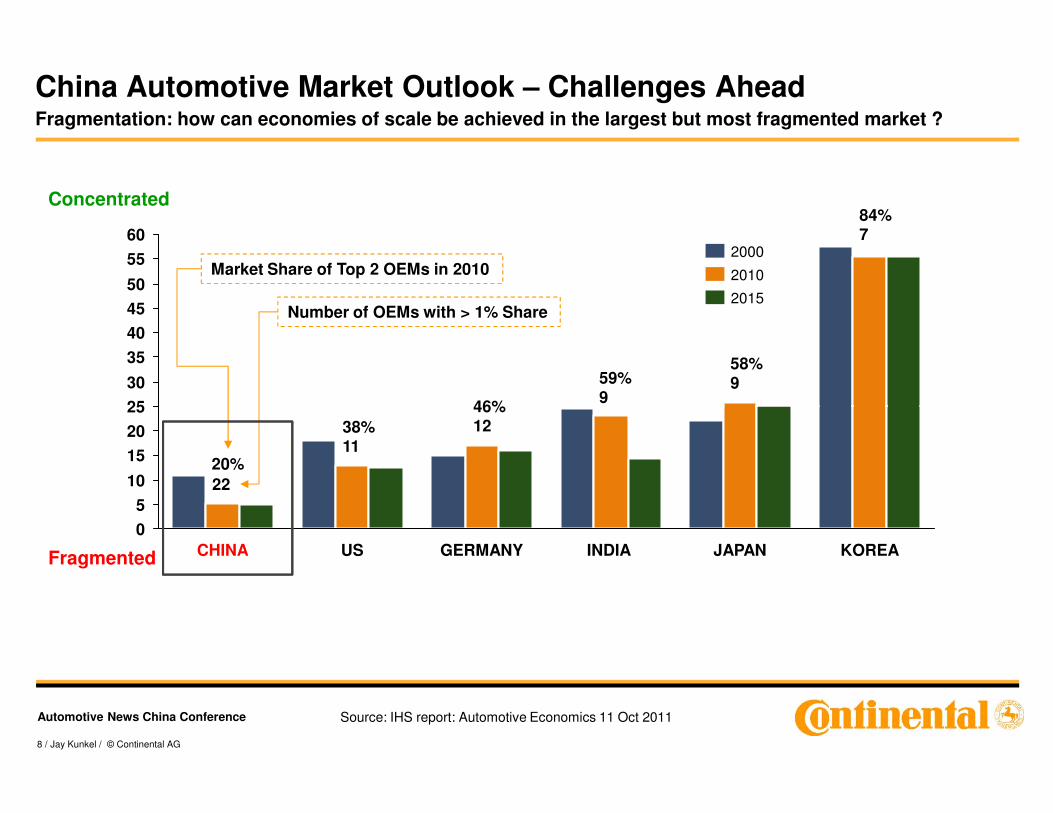

Chinese brands are moving upwards to higher-end C and D segments with

increasing content

25

30

35

40

45

50

55

60

46%

59%9

58%9

84%7

2015

2010

2000

Market Share of Top 2 OEMs in 2010

Number of OEMs with > 1% Share

Concentrated

China Automotive Market Outlook – Challenges AheadFragmentation: how can economies of scale be achieved in the largest but most fragmented market ?

8 / Jay Kunkel / © Continental AG

Automotive News China Conference

0

5

10

15

20

25

INDIAGERMANYUSCHINA JAPAN KOREA

20%

38%11

46%12

22

Fragmented

Source: IHS report: Automotive Economics 11 Oct 2011

China Market OutlookVehicle content / value instead of volume development for sustainable growth in future

ChinaChina

CAGR =21%

2007/2011

CAGR =9%

2012/2016

10,919

21,200

CAGR =18%

2012/2016

China unit: mn EURChina unit: mn EUR

Vehicle Production Development – 2007 / 2011; - 2012 / 2016

Market Value Development (Continental Portfolio)

– 2012 / 2016

9 / Jay Kunkel / © Continental AG

Automotive News China Conference

Source: - IHS_Vehicle_Production_Forecast_04_10_2012 (2007-2010)- IHS_LV_Production_Bodystyle_GC_2012M02 (2011-2016)

China

RoW

22%

78%2012 2016

10,919 Volume Market Share – 2011 / 2016

China

RoW

26%

74%

Source: Continental Internal Study- Based on Continental Product portfolio

2011 2016

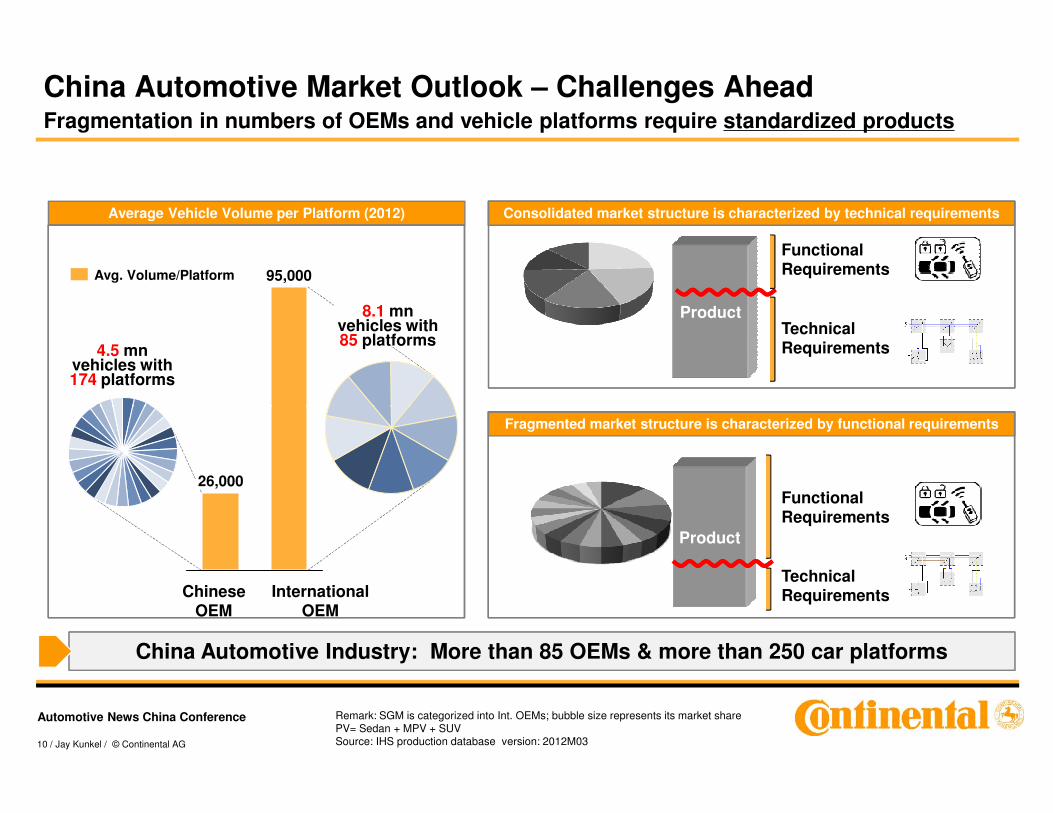

China Automotive Market Outlook – Challenges AheadFragmentation in numbers of OEMs and vehicle platforms require standardized products

Consolidated market structure is characterized by technical requirements

Product

Functional Requirements

TechnicalRequirements

Average Vehicle Volume per Platform (2012)

95,000

4.5 mnvehicles with 174 platforms

8.1 mnvehicles with 85 platforms

Avg. Volume/Platform

10 / Jay Kunkel / © Continental AG

Automotive News China Conference

China Automotive Industry: More than 85 OEMs & more than 250 car platforms

Product

Functional Requirements

TechnicalRequirements

Fragmented market structure is characterized by functional requirements

Remark: SGM is categorized into Int. OEMs; bubble size represents its market sharePV= Sedan + MPV + SUVSource: IHS production database version: 2012M03

Chinese OEM

26,000

International OEM

Technology / Product Life Cycle Management: Current Situation

Strategy is based upon development of advanced technology

� No significant focus on reduction of cost / achievement of economies of scale?

� Where economies of scale are achieved, have the products failed to become “Cash Cows”?

� Leaves products vulnerable as the product matures

Sales

Product

Development

Introduction Growth DeclineMaturity

Vulnerable to Price competition

Existing Technology /Product Life Cycle

Management focuses on

TPLC Management influences how steeply

11 / Jay Kunkel / © Continental AG

Automotive News China Conference

Eu

ros

Sales

Total

Profit

TimeFree Cash

Flow

Profit Margin

Management focuses on the early phases of the technology/product life

cycle targeting installations on high end

vehicle

influences how steeply this curve declines

Technology / Product Life Cycle Management: Alternative Strategy

Affordable Vehicle Product Strategy

� Use affordable vehicle applications to extend product/technology’s life cycle

� Develop products for low cost/high-volume applications

� Use development advantages to reduce costs, reduce weight, and consolidate components

Sales

Product

Development

Introduction Growth DeclineMaturity

Standardization of product design at early stages facilitates improved Life Cycle Management through later stage

cost reductions, facilitating economies of

12 / Jay Kunkel / © Continental AG

Automotive News China Conference

Eu

ros

Sales

Total

Profit

TimeFree Cash

Flow

Profit Margin

cost reductions, facilitating economies of scale

Technology / Product Life Cycle Management: Alternative StrategyAffordable Vehicle Product Strategy

� Use affordable vehicle applications to extend product/technology’s life cycle

� Develop products for low cost/high-volume applications

� Use advanced technology to reduce costs, reduce weight, and consolidate components

Sales

Product

Development

Introduction Growth DeclineMaturity

As growth of a technology begins to reach its peak, beginning integrating the

technology into systems and modules

13 / Jay Kunkel / © Continental AG

Automotive News China Conference

Eu

ros

Sales

Total

Profit

TimeFree Cash

Flow

Profit Margin

technology into systems and modules

Front caliper

FA-L

Actuation

ABA

ABS MK100 Airbag Control

Unit (SPEED)

Chassis

& Safety

Powertrain

Fuel supply EMS Easy U Temp. Sensor

Intake Air

Transmission

East Platform

ElectronicThrottle Control

Standardization for Market Specific SolutionsExamples of technology development in China for China

Knock Sensor

Wheel Speed

Sensor

Transmission

Speed Sensor

Engine Speed Sensor

14 / Jay Kunkel / © Continental AG

Automotive News China Conference

Powertrain

Interior

Instrument

ClusterImmobilizer

Basic Function

Controller (BFC)

Integrated solution

Radio+HVAC

EASY PASE &

Start/Stop Button

Integrated Instrument

Cluster & Compact

Function Controller

Bluetooth

Car Kit

Development of Market Specific Solutions - local engineering as key success factor

Heihe - 2002

Changchun - 1995

Zhangjiagang - 2005

Nanjing - 2011

Engineering Centers in China

15 / Jay Kunkel / © Continental AG

Automotive News China Conference

Shanghai-2009Jiading - 2009

Changshu - 2010

Wuhu - 1995

China – Moving from Volume to Value

a. How to manage the largest but most fragmented market ?

b. How to cope with changing regulatory policies ?

c. How to manage the demand for Fuel Efficiency, Safety and

16 / Jay Kunkel / © Continental AG

Automotive News China Conference

Information?

d. How to manage to develop and retain the required skill-sets?

Consolidation

Policy

Incentives

Regulations

China Automotive Market Outlook – Challenges Ahead How to cope with changing regulatory policies ?

•Revised Foreign Investment

Catalogue

•Five-Year Plan for developing New

Energy Vehicles

•Revised government vehicle

catalogue in favor of local brands

1.8 L

•Limitation of Vehicle Fuel

•The “winners” – dominating OEM groups

•Go West

•New JV brands

17 / Jay Kunkel / © Continental AG

Automotive News China Conference

Consolidation

Capacity Extension

Local Brands Fuel Efficiency

Key Components

New Energy Vehicle

Market growth in valueResult

Consumption•Direct Injection, Turbocharger, Start-Stop

•EPS, CAN bus, ESC, TPMS, DCT

•EV and Plug-In Hybrid

Summary of Factors Impacting China Car Sales in 2011Positive demand factors outnumber & outlast those negatives in the coming years

Imp

ac

t Demand/Supply side

Low vehicle density

Demand side

Strong growth potential from lower Tier 3 /4 cities

Demand side

JV brand development

Demand side

Increasing vehicle export

Demand side

IOEMs ramp up capacity Po

sit

ive

Supply side

Electronic content growth

Demand side

Subsidy for Fuel Efficient Vehicle / NEV

18 / Jay Kunkel / © Continental AG

Automotive News China Conference

Demand side

End of Incentive Policy

Demand side

Macro Economy Development

Supply sideInsufficient

Manufacturing Capacity

Supply side

Japan Earthquake

Increasing vehicle export IOEMs ramp up capacity

Time2011 2012-15

Ne

ga

tive Demand side

Ownership Cost including Parking Fees and Gasoline Cost

Demand side

Vehicle ownership restriction (few cities)

growth

China – Moving from Volume to Value

a. How to manage the largest but most fragmented market ?

b. How to cope with changing regulatory policies ?

c. How to manage the demand for Fuel Efficiency, Safety and

19 / Jay Kunkel / © Continental AG

Automotive News China Conference

Information?

d. How to manage to develop and retain the required skill-sets?

Combustion engine

Diesel direct injection 25%

Energy management

Power on demand - Steering, climate 6%*Advanced energy management- Start/stop 2 – 7%

Driver

e.Horizon(Telematics, ACC, ADAS) 5%

Body

Light weight brake system,lower brake drag 1 - 2%

Regulations on Fuel Efficiency – how to address it in China ?Local development and manufacturing of key technologies

20 / Jay Kunkel / © Continental AG

Automotive News China Conference

Diesel direct injection 25%Gasoline direct injection 15%Diesel SCR** 5%Turbocharger 7.5%

Alternative drive concepts

Hybrid electric vehicle including regenerative brake system 25%

Tires

Low rolling resistance, TPMS 2 - 5%

Transmission

Double clutch transmission 3%

**SCR: Selective Catalytic Reduction

*% : possible reduction of fuel consumption

Active Safety Safety Telematics

TCUTelematics Control Unit

e-Horizon

EPSPowerpack

ChassisController

EASElectronic Air Suspension

ESCElectronicStabilityControl

HMI

Vehicle-to-XCommunication

AFFP®

AcceleratorForce FeedbackPedal

Sensors

Wheel Brakes

Megatrend: Safety – how to address it in China ?Local development and manufacturing of key technologies

21 / Jay Kunkel / © Continental AG

Automotive News China Conference

Vehicle Surrounding SensorsPassive Safety

SRLShort Range Lidar

SMRShort & Mid Range Radar 24GHz

LRRLong Range Radar77GHz

CameraACU + CISSAirbag Control Unit+ Crash Impact

Sound Sensing

pSAT, gSATPressure and Acceleration Satellites

PPS pSatPedestrianProtectionSystem

evSATSensor forHigh-VoltageBattery Cut-off

Megatrend: Information – how to address it in China ?Local development and manufacturing of market specific solutions

Auto LinQ

22 / Jay Kunkel / © Continental AG

Automotive News China Conference

Mobile View

Car View Home View

Partner View

Box solution with front-end,

back-end and connectivity

components as China specific solution

Safe and intuitive HMIoperation in the car through use of

Voice Recognition and Text-to-

Speech

Open platform for attractive

local Apps which personalize car

over life cycle

China – Moving from Volume to Value

a. How to manage the largest but most fragmented market ?

b. How to cope with changing regulatory policies ?

c. How to manage the demand for Fuel Efficiency, Safety and

23 / Jay Kunkel / © Continental AG

Automotive News China Conference

Information?

d. How to manage to develop and retain the required skill-sets?

Customer proximity as a key success factorContinental in China

Headquarters @ Shanghai

Shanghai Beijing

Chongqing

Liuzhou

Guangzhou

Wuhan

Hangzhou

6 2 3

2 2

2 1 2

1 1 2

2 1

1 1

1

1

1

1

1

1

Headquarters: 1

1

2

Manufacturing: 18

Tianjin

Changshu

Changchun

Wuhu

Zhangjiagang 1

1

24 / Jay Kunkel / © Continental AG

Automotive News China Conference

Status: Jan. 2012

Nanjing

Heihe

Hangzhou

Taipei1

1

1

1 1

1

1

1Lianyungang

Ninghai

Hefei

Jinan

1

Engineering: 10

Sales : 19

Total Employees > 16,000Total Employees > 16,000

Comprehensive benefits

Internal transfer

Retention bonus program

Competitive salary

Employee

China Automotive Market Outlook – Challenges Ahead Need for Local Experts – how to manage to develop and retain the required skill-sets?

25 / Jay Kunkel / © Continental AG

Automotive News China Conference

Internal & External Training

Motivation (employee

events)

Company Culture

Internal transfer & Career

development

Employee

retention

Need for local expertsPeople – critical success factor for moving to value

Entrepreneurship

Exciting job challenges

Early responsibility

Attraction Retention

26 / Jay Kunkel / © Continental AG

Automotive News China Conference

challenges

Open doors & open views

Multifaceted career opportunities

Performance-oriented working atmosphere

Localization of Entire Value ChainInvestment in HR - Employees make THE difference!

HR Awards in 2011 Global Engineering Excellence Network

A platform between Continental and leading Chinese engineering universities to strengthen

education for engineers for businesses

• 100 Best HRM Companies of 2011

• Outstanding Performance for Best Campus Recruitment of 2011

• Most Popular Employer on Campus (Automobile Components Industry) 2011

27 / Jay Kunkel / © Continental AG

Automotive News China Conference

• China's Ideal Employers, 2011

• Top 15 Ideal Employer in High Ethical Standards 2011

SummaryChina – from Volume to Value: converting challenges into opportunities

Local Talent

Individual mobilityFuel efficiencySafety, Information, Affordable cars

�Standardization

�Software instead of Hardware

�Time to market

Fragmentation

Policies Growth

�Employer of choice

�Retention of key talents Cost

Recruiting

Skill sets

Retention

Local Talent

28 / Jay Kunkel / © Continental AG

Automotive News China Conference

Government targetsProduct development

Local technology�Localize new technologies

�Specific Chinese product

roadmap

Policies

Competitiveness Localization of value chainBrand imageLocations

�Strong invest into

engineering

�Product development in

China for China

Growth

29 / Jay Kunkel / © Continental AG

Automotive News China ConferenceThank you for your attention!