14. the multiple-equation gmm -...

TRANSCRIPT

14. The Multiple-Equation GMM

Hayashi p. 258-295

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 1

Multiple-Equation GMM (MEGMM)

Allows handling a system of mulitple equations

Can be expressed as a single-equation GMM estimator by suitably spe-cifying the matrices and vectors comprising the single-equation GMMformula

We could develop its large-sample properties in the same way as forsingle-equation GMM

Special cases of MEGMM correspond to some well known estimators:

– Under conditional homoskedasticity, MEGMM reduces to the full-information iv efficient(FIVE) estimator, which in turn reduces to3SLS if the set of IVs is common to all equations.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 2

Multiple-Equation GMM (cont’d)

– If we assume all the regressors are predetermined, 3SLS reduces toseemingly unrelated regressions (SUR), which in turn reduces tomultivariate regression when all the equations have the same regressors.

– The multiple-equation system can be written as an equation systemwith its coefficients constrained to be the same across equations. TheGMM estimator for this system is a special case of single-equationGMM.

– The GMM estimator with all the regressors predetermined and errorsconditionally homoskedastic is the random-effects(RE) estimator

– Thus, SUR and RE are equivalent estimators

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 3

The Multiple-Equation Model (cont’d)

Assumption 4.1 (Linearity): There are M linear equations

yim = z′imδm + εim (m = 1, 2, ...,M ; i = 1, 2, ..., n)

where:n = sample size,

zim = Lm-dimensional vector of regressors,

δm = the conformable coefficient vector, and

εim = an unobservable error term in the m-th equation.

Oryim = z

′im

(1×Lm)

δm(Lm×1)

+ εim (m = 1, 2, ...,M ; i = 1, 2, ..., n)

Note: (i) No a priori assumption about cross equation error correlation, (ii)No cross equation parameter restriction

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 4

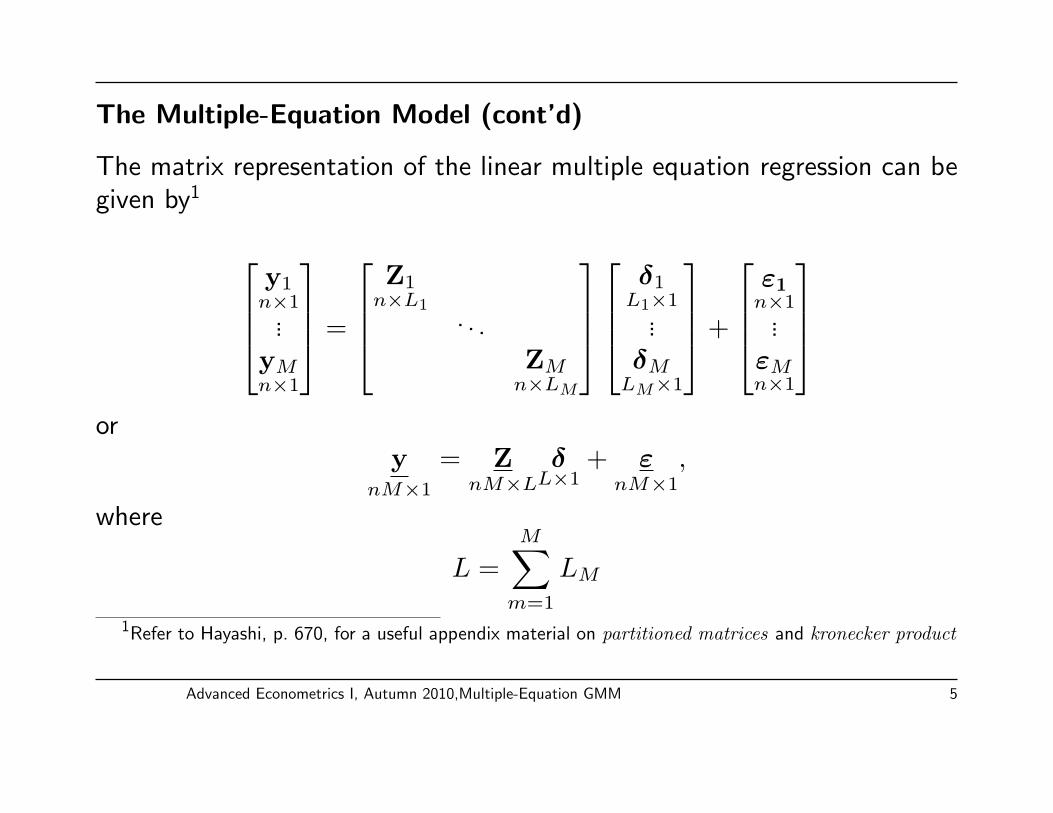

The Multiple-Equation Model (cont’d)

The matrix representation of the linear multiple equation regression can begiven by1

y1n×1

...yMn×1

=

Z1

n×L1. . .

ZMn×LM

δ1

L1×1...δM

LM×1

+

ε1n×1

...εMn×1

or

ynM×1

= ZnM×L

δL×1

+ εnM×1

,

where

L =

M∑m=1

LM

1Refer to Hayashi, p. 670, for a useful appendix material on partitioned matrices and kronecker product

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 5

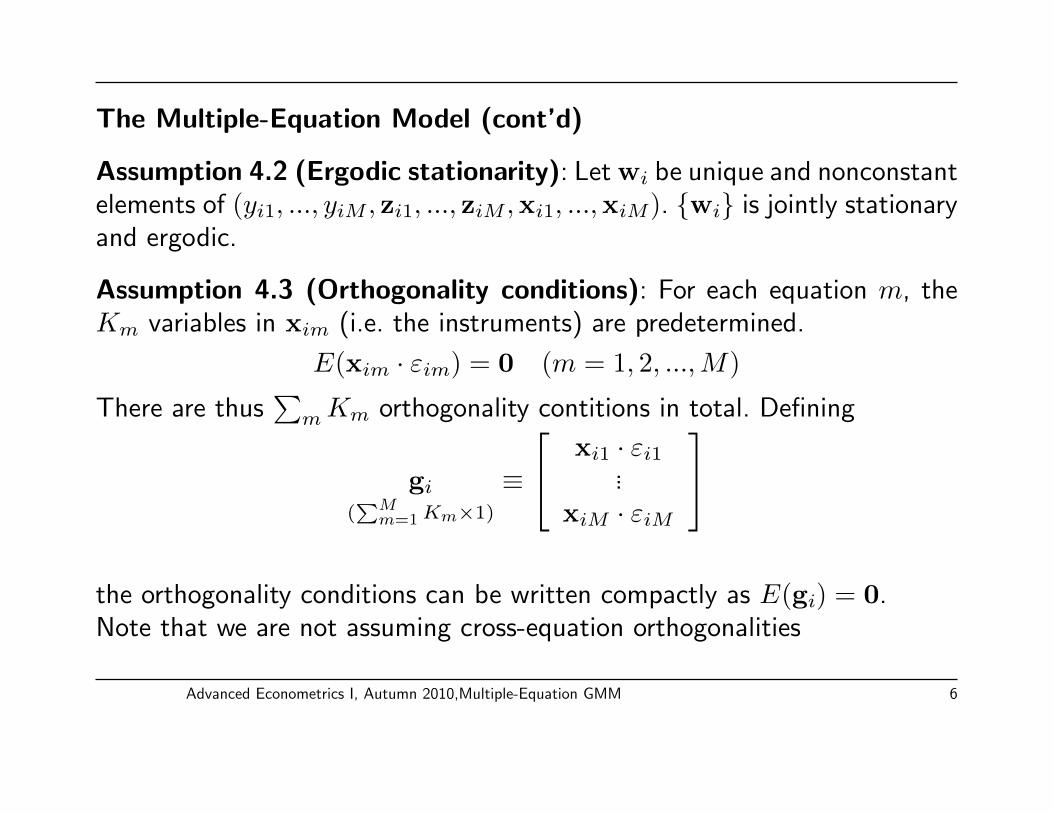

The Multiple-Equation Model (cont’d)

Assumption 4.2 (Ergodic stationarity): Let wi be unique and nonconstantelements of (yi1, ..., yiM , zi1, ..., ziM ,xi1, ...,xiM). {wi} is jointly stationaryand ergodic.

Assumption 4.3 (Orthogonality conditions): For each equation m, theKm variables in xim (i.e. the instruments) are predetermined.

E(xim · εim) = 0 (m = 1, 2, ...,M)

There are thus∑

mKm orthogonality contitions in total. Defining

gi

(∑M

m=1 Km×1)≡

xi1 · εi1...

xiM · εiM

the orthogonality conditions can be written compactly as E(gi) = 0.Note that we are not assuming cross-equation orthogonalities

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 6

GMM Moment Conditions and Model identification

Given the orthogonality condition, identification could be established inmuch the same way as in the single-equation GMM case

g(wi; δ) ≡

xi1 · (yi1 − z′i1δ1)

...

xiM · (yiM − z′iMδM)

,

The orthogonality condition can be written as E[g(wi; δ)] = 0. Thecoefficient vector is identified if δ = δ is the only solution to the system ofequations

E[g(wi; δ)] = 0

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 7

GMM Moment Conditions and Model identification (cont’d)

The expanded orthogonality conditions can be given as follows

E[g(wi; δ)] ≡

E[xi1 · (yi1 − z′i1δ1)]

...

E[xiM · (yiM − z′iM δM)]

=

E(xi1 · yi1)...

E(xiM · yiM)

− E(xi1z

′i1)δ1

...

E(xiMz′iM)δM

=

E(xi1 · yi1)...

E(xiM · yiM)

−E(xi1z

′i1) . . . 0

... . . . ...

0 . . . E(xiMz′iM)

δ1...δM

≡ σxy

(k×1)− Σxz

(K×L)δ

(L×1)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 8

GMM Moment Conditions and Model identification (cont’d)

The moment conditions for each equation in the MEGMM are the same asthe moment condition we derived for the single-equation GMM model

The system of equations determining δ can also be arrived at in the sameway as

Σxzδ = σxy

The MEGMM Σxz is block diagonal. Recall that a necessary and sufficientcondition for identification of the single-equation GMM is that Σxz be offull column rank.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 9

GMM Moment Conditions and Model identification (cont’d)

If Km = Lm for m = 1, . . . ,M , then δ is exactly identified and δ1...δM

=

Σ−1x1z1σx1y1...

Σ−1xMzMσxMyM

If Km > Lm for some m, then solving

E[gi(δ)] = σxy(k×1)

− Σxz(K×L)

δ(L×1)

= 0

requires the rank condition

Assumption 4.4 (rank condition for identification): For each m(=

1, 2, . . . ,M), E(ximz′im)(Km × Lm) is of full column rank.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 10

GMM Moment Conditions and Model identification (cont’d)

That is, all coefficient vectors (δ1, . . . , δM) can be uniquely determined iffeach coefficient vector δM is uniquely determined.

This is the case if the orthogonality assumption holds for each equation.

Assumption 4.5 (gi is a martingale difference sequence with finitesecond moments):{gi} is a joint martingale difference sequence. E(gig

′i)

is nonsingular.

Note, as is also the case for ergodic stationarity, that this assumption isstronger than requiring the same for each equation.

We use S for Avar(g), the asymptotic variance of (g) (i.e. the variance ofthe limiting distribution of

√ng)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 11

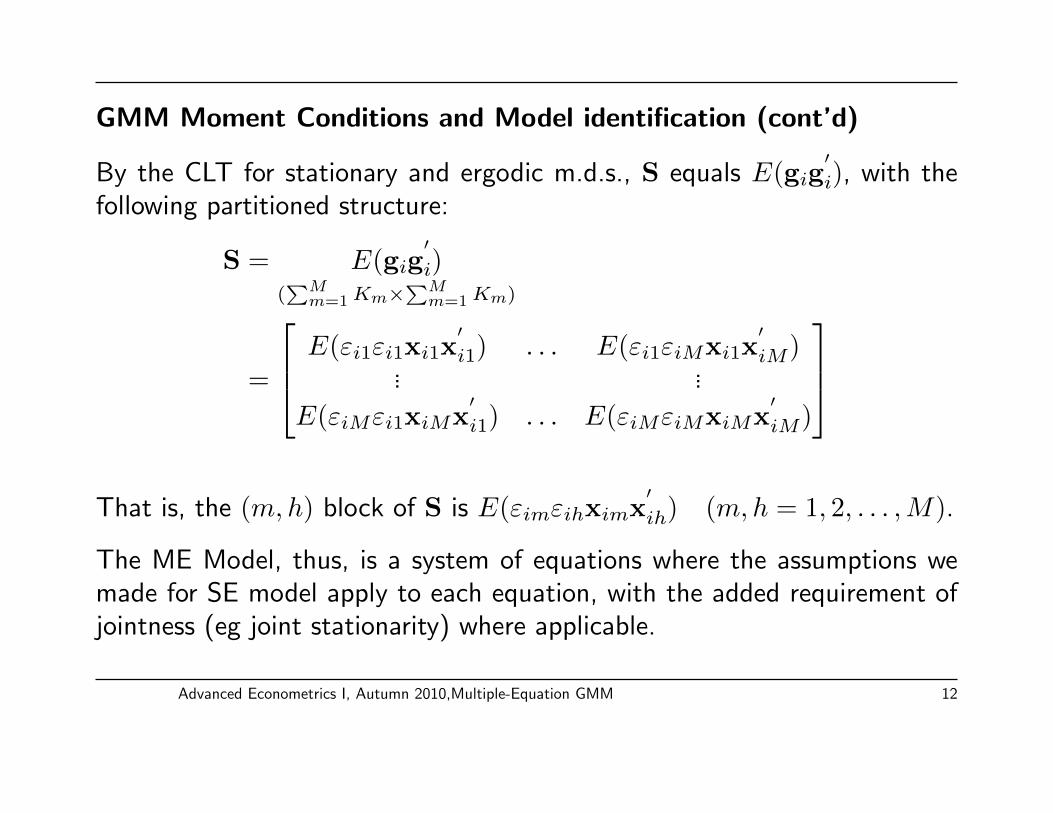

GMM Moment Conditions and Model identification (cont’d)

By the CLT for stationary and ergodic m.d.s., S equals E(gig′i), with the

following partitioned structure:

S = E(gig′i)

(∑M

m=1 Km×∑M

m=1 Km)

=

E(εi1εi1xi1x′i1) . . . E(εi1εiMxi1x

′iM)

... ...

E(εiMεi1xiMx′i1) . . . E(εiMεiMxiMx

′iM)

That is, the (m,h) block of S is E(εimεihximx

′ih) (m,h = 1, 2, . . . ,M).

The ME Model, thus, is a system of equations where the assumptions wemade for SE model apply to each equation, with the added requirement ofjointness (eg joint stationarity) where applicable.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 12

MEGMM Sample Moment

As in the SEGMM case, let δ be a hypothetical value of the true parametervector δ and define gn(δ) to be its sample analogue, which is given by:

gn(δ)(∑M

m=1 Km×1)=

1n

∑ni=1 xi1 · (yi1 − z

′i1δ1)

...1n

∑ni=1 xiM · (yiM − z

′iM δM)

=

1n

∑ni=1 xi1 · yi1

...1n

∑ni=1 xiM · yiM

− 1

n

∑ni=1 xi1z

′i1δ1

...1n

∑ni=1 xiMz

′iM δM

=

1n

∑ni=1 xi1 · yi1

...1n

∑ni=1 xiM · yiM

−1

n

∑ni=1 xi1z

′i1

. . .1n

∑ni=1 xiMz

′iM

δ1...δM

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 13

MEGMM Sample Moment (cont’d)

Thus,

gn(δ)(∑M

m=1 Km×1)≡ sxy − Sxzδ,

where

sxy ≡

1n

∑ni=1 xi1 · yi1

...1n

∑ni=1 xiM · yiM

,Sxz ≡

[1n

∑ni=1 xi1z

′i1

. . . 1n

∑ni=1 xiMz

′iM

]

Orgn(δ)

(∑M

m=1 Km×1)= sxy

(K×1)− Sxz

(K×L)

δL×1)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 14

MEGMM,identification

If Km = Lm for m = 1, . . . ,M then X′mZm is a square matrix and so

δm = S−1xmzmSxmym, m = 1, . . . ,M

Therefore,δ = (δ1, . . . , δM)

′

SolvesSxy

(K×1)− Sxz

(K×L)

δ(L×1)

= 0

If each equation is identified and Km > Lm for some m, then it is notpossible to find some δ that solves the moment conditions.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 15

MEGMM,identification (cont’d)For the overidentified model, let W be a K×K positive definite symmetricmatrix given by

W =

W11 W12 . . . W1M

W′12 W22 . . . W2M

... ... . . . ...

W′1M W

′2M . . . WMM

Such that W→

pW. The GMM estimator then solves

δ(W) = argminδ

J(δ,W) = ngn(δ)′Wgn(δ)

= argminδ

n(sxy − Sxzδ

)′W(sxy − Sxzδ

)Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 16

MEGMM,identification (cont’d)

Straightforward but tedious algebra should give

δ(W) =(S′xzWSxz

)−1S′xzWsxy =

S′x1z1

W11Sx1z1 S′x1z1

W12Sx2z2 . . . S′x1z1

W1MSxMzM

S′x2z2

W′12Sx1z1 S

′x2z2

W21Sx2z2 . . . S′x2z2

W2MSxMzM... ... . . . ...

S′xMzM

W′1MSx1z1 S

′xMzM

W′2MSx2z2 . . . S

′xMzM

WMMSxMzM

−1

×

S′x1z1

∑Mm=1 W1msxmym

S′x2z2

∑Mm=1 W2msxmym

...

S′xMzM

∑Mm=1 WMmsxmym

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 17

Multiple-Equation GMM Defined

The definition of the MEGMM estimator is the same as in the SEGMM,provided that the weighting matrix W is now

∑mKm ×

∑mKm.

Multiple-equation GMM estimator: δ(W) = (S′xzWSxz)

−1S′xzWsxy,

Its sampluing error: δ(W)− δ = (S′xzWSxz)

−1S′xzWg.

Features specific to the MEGMM are:

(i) sxy is a stacked vector,

(ii) Sxz is a block diagonal matrix,

(iii) accordingly, the size of the weighting matrix is∑

mKm×∑

mKm,

(iv) g, the sample mean of gi, is stacked vector, given by

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 18

Multiple-Equation GMM Defined (cont’d)

g ≡ 1

n

n∑i=1

gi =

1n

∑ni=1 xi1 · εi1

...1n

∑ni=1 xiM · εiM

= gn(δ)

given these features, the MEGMM estimator

δ(W) = (S′xzWSxz)

−1S′xzWsxy

can be written out in full.

Required: the Wmh(Km ×Kh) has to be the (m,h) block of W(m,h =1, 2, . . . ,M)

[See Hayashi (2000), p. 267]

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 19

MEGMM Asymptotics

The mechanics of asymptotics for multiple-equation GMM is similar to thatfor single-equation GMM so long as:

(i) δ,Σxz,S,gi, sxy, and Sxz are as defined for the multiple-equationGMM, and

(ii) the multiple-equaion GMM assumptions are used.

δ in the case of multiple equations is a stacked vector of parameterscomposed of coefficients from different equation.

We could conduct hypothesis testing involving cross-equation restrictions.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 20

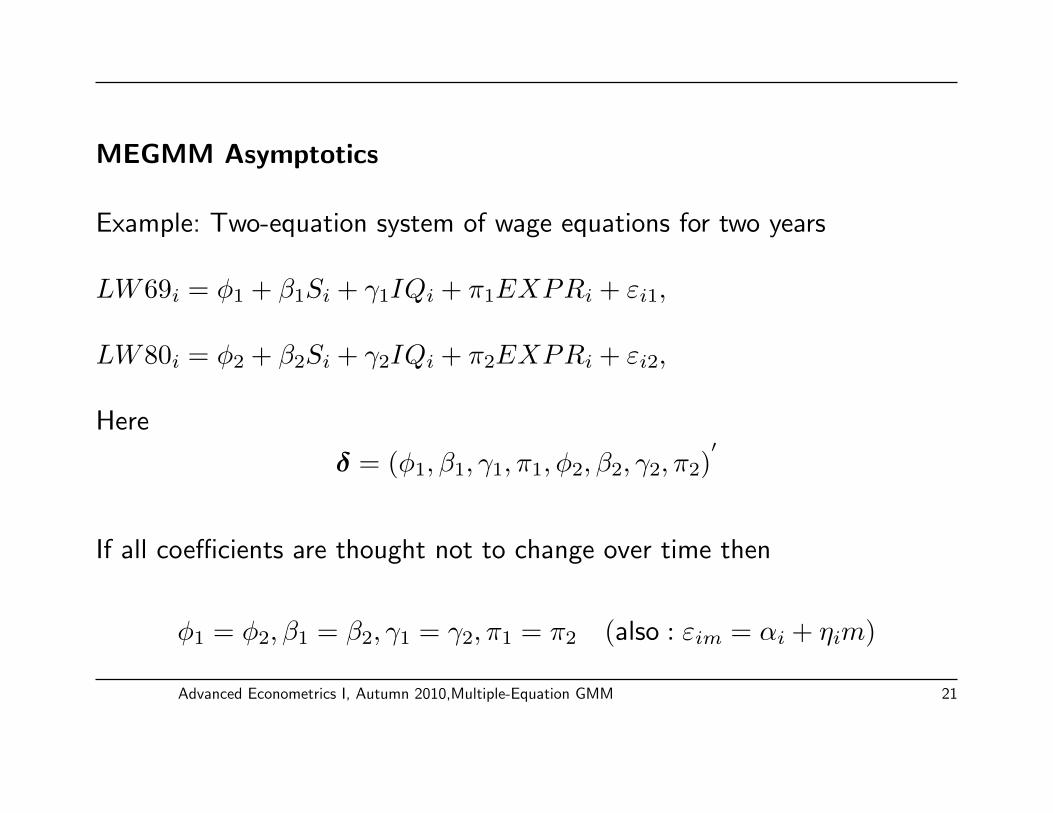

MEGMM Asymptotics

Example: Two-equation system of wage equations for two years

LW69i = φ1 + β1Si + γ1IQi + π1EXPRi + εi1,

LW80i = φ2 + β2Si + γ2IQi + π2EXPRi + εi2,

Here

δ = (φ1, β1, γ1, π1, φ2, β2, γ2, π2)′

If all coefficients are thought not to change over time then

φ1 = φ2, β1 = β2, γ1 = γ2, π1 = π2 (also : εim = αi + ηim)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 21

We could test this as:

H0 : φ1 = φ2, β1 = β2, γ1 = γ2, and, π1 = π2

The Hypothesis can be written as Rδ = r, where.

R =

1 0 0 0 −1 0 0 00 1 0 0 0 −1 0 00 0 1 0 0 0 −1 00 0 0 1 0 0 0 −1

, r =

0000

.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 22

MEGMM Asymptotics

(Test of overidentifying restriction) The number of orthogonality conditionsis K =

∑mKm and the number of coefficients is L =

∑mLm. The degrees

of freedom for the J statistic is thus K − L =∑

mKm −∑

mLm.

Proposition 4.1 (consistent estimation of contemporaneous errorcross-equation moments): Let δm be a consistent estimator of δm, and

let εim ≡ yim − z′imδm be the implied residual for m = 1, 2, . . . ,M . Under

Assumptions 4.1 and 4.2, plus the assumption that E(zimz′ih) exists and is

finite for all m,h(= 1, 2, . . . ,M),

σmh →pσmh,

whereσmh ≡

1

n

n∑i=1

εimε′ih and σmh ≡ E(εimεih)

Provided that E(εimεih) exists and is finite.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 23

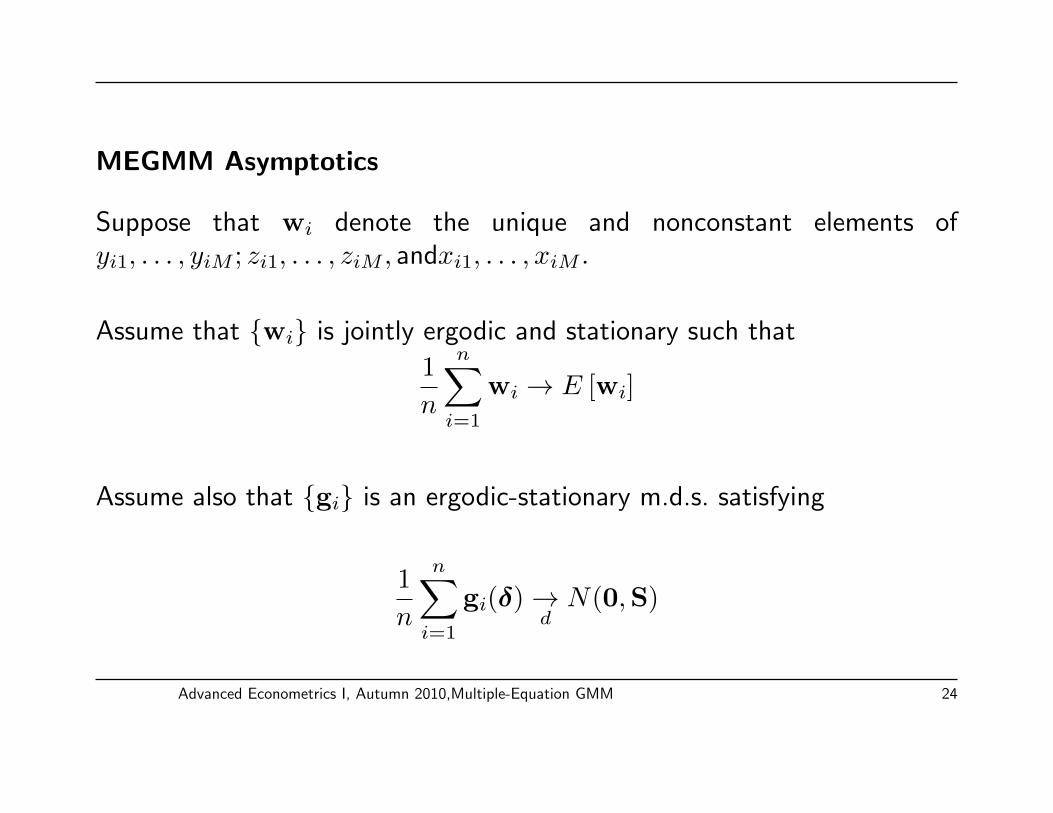

MEGMM Asymptotics

Suppose that wi denote the unique and nonconstant elements ofyi1, . . . , yiM ; zi1, . . . , ziM , andxi1, . . . , xiM .

Assume that {wi} is jointly ergodic and stationary such that

1

n

n∑i=1

wi → E [wi]

Assume also that {gi} is an ergodic-stationary m.d.s. satisfying

1

n

n∑i=1

gi(δ)→dN(0,S)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 24

where, as before

S = E[gi(δ)gi(δ′)]

=

E[xi1x

′i1ε

2i1] E[xi1x

′i2εi1εi2] . . . E[xi1x

′iMεi1εiM ]

E[xi2x′i1εi2εi1] E[xi2x

′i2ε

2i2] . . . E[xi2x

′iMεi2εiM ]

... ... . . . ...

E[xiMx′i1εiMεi1] E[xiMx

′i2εiMεi2] . . . E[xiMx

′iMε

2iM ]

Assumption 4.6(finite fourth moments): E[(ximk · · · zihj)2] exists andis finite for all k(= 1, 2, . . . ,Km), j(= 1, 2, . . . , Lh),m, h(= 1, 2, . . . ,M),where ximk is the k-th element of xim and zihj is the j-th element of zih.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 25

MEGMM Asymptotics

Estimation of S: the multiple-equation version formula for consistentlyestimating S is given by

S =

S11 S12 . . . S1M

S′12 S22 . . . S2M... ... . . . ...

S′1M S

′2M . . . SMM

where

Smh =1

n

n∑i=1

ximx′ihεimεih

Proposition 4.2 (consistent estimation of S, the asymptotic varianceof g): Let εm be a consistent estimator of εm, and let εim ≡ yim − z

′imδm

be the implied residual for m = 1, 2, . . . ,M .

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 26

MEGMM Asymptotics

Under Assumptions 4.1, 4.2, and 4.6, S is consistent for S.

Potential initial consistent estimators of δ:

1. δ(IK) = (δ1(IK1)′, . . . , δM(IKM

)′)′

2. Single equation efficient GMM estimators:

δm(S−1mm), m = 1, . . . ,M

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 27

MEGMM Asymptotics

Since S is consistent for S, the MEGMM estimator that uses S−1 asthe weighting matrix, δ(S−1), is an efficient MEGMM estimator withminimum asymptotic variance.

Thus,

Avar(δ(S−1)) = (Σ′xzS−1Σxz),

Avar(δ(S−1)) = (S′xzS−1Sxz)

−1.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 28

Single- vs. Multiple-Equation GMM

Single-equation GMM is a special case of multiple-equation GMM

In SEGMM, apply GMM on each equation separately with equationspecific weight matrix Wmm; so that

δm(Wmm) = (S′xmzmWmmSxmzm)

−1S′xmzmWmmSxmym

m = 1, . . . ,M

This is MEGMM with a block diagonal weight matrix

W = diag(W11, . . . ,WMM)

Question: When is multiple-equation efficient GMM equivalent to singleequation efficient GMM?

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 29

Single- vs. Multiple-Equation GMM

Two cases:

1. Each equation is just identified ⇒ the weight matrix does not matter(obvious case)

2. At least one equation is overidentified but S = E[gi(δ)gi(δ)′] is block

diagonal (not so obvious case)

S = diag(S11, . . . ,SMM)

= diag(E[xi1x′i1ε

2i1], . . . , E[xiMx

′iMε

2iM ])

That is, if the equations are unrelated as in

E[ximx′ihεimεih] = 0 for all m 6= h

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 30

15. Special Cases of MEGMM: FIVE, 3SLSand SUR

Hayashi, pp. 274-294

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 31

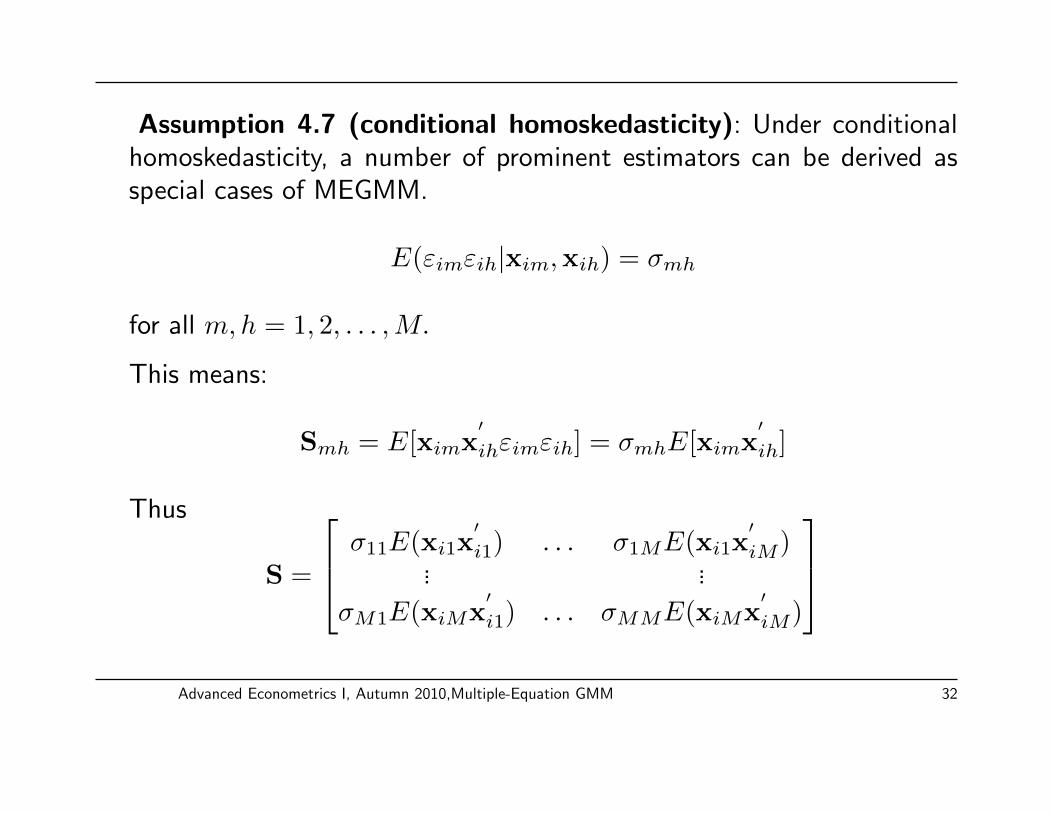

Assumption 4.7 (conditional homoskedasticity): Under conditionalhomoskedasticity, a number of prominent estimators can be derived asspecial cases of MEGMM.

E(εimεih|xim,xih) = σmh

for all m,h = 1, 2, . . . ,M.

This means:

Smh = E[ximx′ihεimεih] = σmhE[ximx

′ih]

Thus

S =

σ11E(xi1x′i1) . . . σ1ME(xi1x

′iM)

... ...

σM1E(xiMx′i1) . . . σMME(xiMx

′iM)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 32

Full-Information Instrumental Variables Efficient (FIVE)

An estimator of S in this case is

S =

σ11 · (1n∑n

i=1 xi1x′i1) . . . σ1M · (1n

∑ni=1 xi1x

′iM)

... ...

σM1 · (1n∑n

i=1 xiMx′i1) . . . σMM · (1n

∑ni=1 xiMx

′iM)

,where, for some consistent estimator δm of δ,

σmh ≡1

n

n∑i=1

εimεih; εim ≡ yim − z′imδm (m,h = 1, ,M)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 33

FIVE

- σmh →p σmh provided that E(zimz′ih) (and assumptions 4.1 and 4.2)

- 1n

∑i ximx

′ih →p E(ximx

′ih), which exists and is finite (by ergodic

stationarity)

Therefore, S is consistent for S.

The FIVE estimator of δ, denoted δFIV E, is thus

δFIV E ≡ δ(S−1)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 34

FIVE

Large-sample properties of FIVE:

Under the conditions of

a. Assumptions 4.1-4.5 and 4.7,b. E(zimz

′ih) exists and finite for all m,h(= 1, 2, . . . ,M), and

c. S and S given above:

We have large-sample properties of FIVE in that

i. S→p S;

ii. δFIV E ≡ δ(S−1) is consistent, asymptotically normal, and efficient with

Avar(δ(S−1)) = (Σ′xzS−1Σxz)

−1;

iii.

Avar(δ(S−1)) = (S′xz

ˆS−1Sxz)−1 is consistent for Avar(δFIVE)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 35

FIVE

iv. Sargan’s Statistic:

J(δFIVE, S−1) ≡ n · gn(δFIVE)

′S−1gn(δFIVE)→

dχ2

(∑m

(Km − Lm)

),

wheregn(·) = gn(δ)

(∑M

m=1 Km×1)≡ sxy − Sxzδ

The initial estimator δm needed to calculate S is usually the 2SLSestimator.

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 36

Three-Stage Least Squares (3SLS)

Assumptions:

(a) Conditional homoskedasticity

E[εimεih|xim,xih] = σmh

for all m,h = 1, 2, . . . ,M.

⇒ Smh = E[ximx′ihεimεih] = σmhE[ximx

′ih]

(b) Common set of instruments across all equations

xi1 = xi2 = . . . = xim = xik×1

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 37

3SLS

The 3SLS moment conditions can be given by

gi(Mk×1)

=

xiεi1...

xiεiM

= εi ⊗ xi, with εi(M×1)

≡

εi1...εiM

The 3SLS Efficient Weight matrix is

S3SLS(Mk×Mk)

=

σ11E[xix

′i] σ12E[xix

′i] . . . σ1ME[xix

′i]

σ12E[xix′i] σ22E[xix

′i] . . . σ2ME[xix

′i]

... ... . . . ...

σ1ME[xix′i] σ2ME[xix

′i] . . . σMME[xix

′i]

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 38

3SLS

Or compactly as

S3SLS(Mk×Mk)

= Σ(M×M)

⊗ E[xix′i]

(k×k),

where

Σ(M×M)

= E[εiε′i] =

σ11 σ12 . . . σ1M

σ12 σ22 . . . σ2M... ... . . . ...

σ1M σ2M . . . σMM

Then

S−13SLS = Σ−1(M×M)

⊗ E[xix′i]−1

(k×k)

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 39

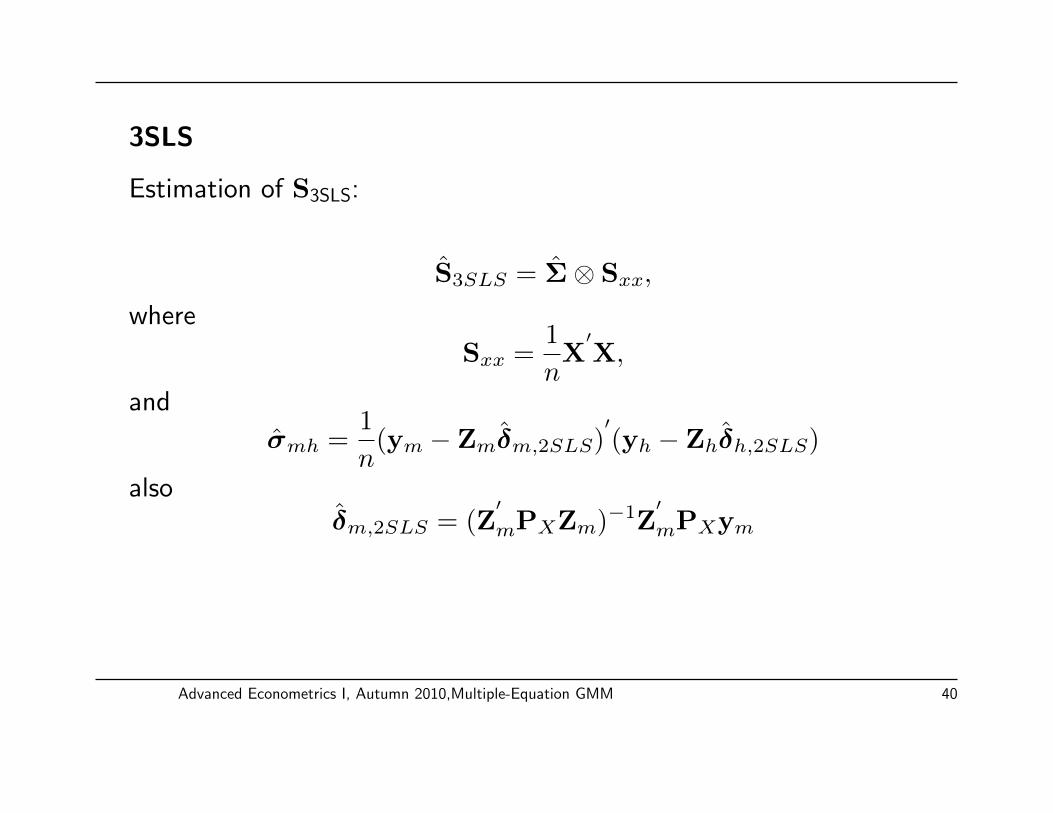

3SLS

Estimation of S3SLS:

S3SLS = Σ⊗ Sxx,

where

Sxx =1

nX′X,

and

σmh =1

n(ym − Zmδm,2SLS)

′(yh − Zhδh,2SLS)

alsoδm,2SLS = (Z

′mPXZm)−1Z

′mPXym

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 40

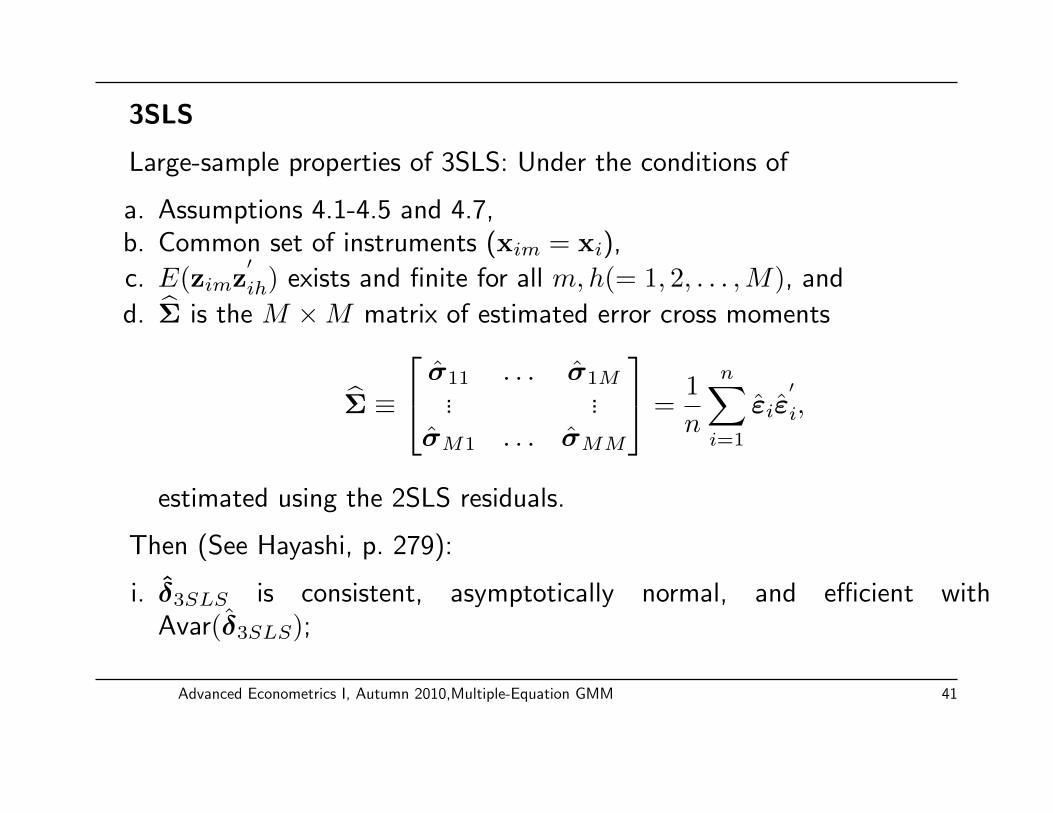

3SLS

Large-sample properties of 3SLS: Under the conditions of

a. Assumptions 4.1-4.5 and 4.7,b. Common set of instruments (xim = xi),

c. E(zimz′ih) exists and finite for all m,h(= 1, 2, . . . ,M), and

d. Σ is the M ×M matrix of estimated error cross moments

Σ ≡

σ11 . . . σ1M... ...

σM1 . . . σMM

=1

n

n∑i=1

εiε′

i,

estimated using the 2SLS residuals.

Then (See Hayashi, p. 279):

i. δ3SLS is consistent, asymptotically normal, and efficient withAvar(δ3SLS);

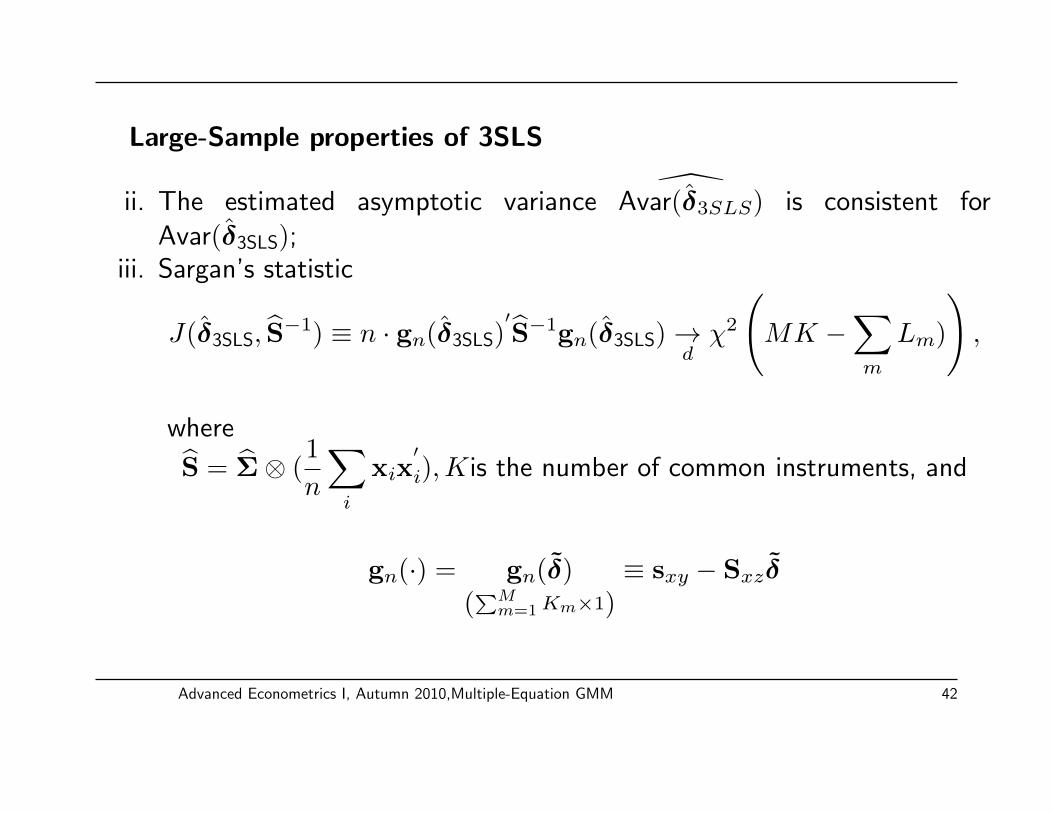

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 41

Large-Sample properties of 3SLS

ii. The estimated asymptotic variance Avar(δ3SLS) is consistent forAvar(δ3SLS);

iii. Sargan’s statistic

J(δ3SLS, S−1) ≡ n · gn(δ3SLS)

′S−1gn(δ3SLS)→

dχ2

(MK −

∑m

Lm)

),

where

S = Σ⊗ (1

n

∑i

xix′i),Kis the number of common instruments, and

gn(·) = gn(δ)(∑M

m=1 Km×1)≡ sxy − Sxzδ

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 42

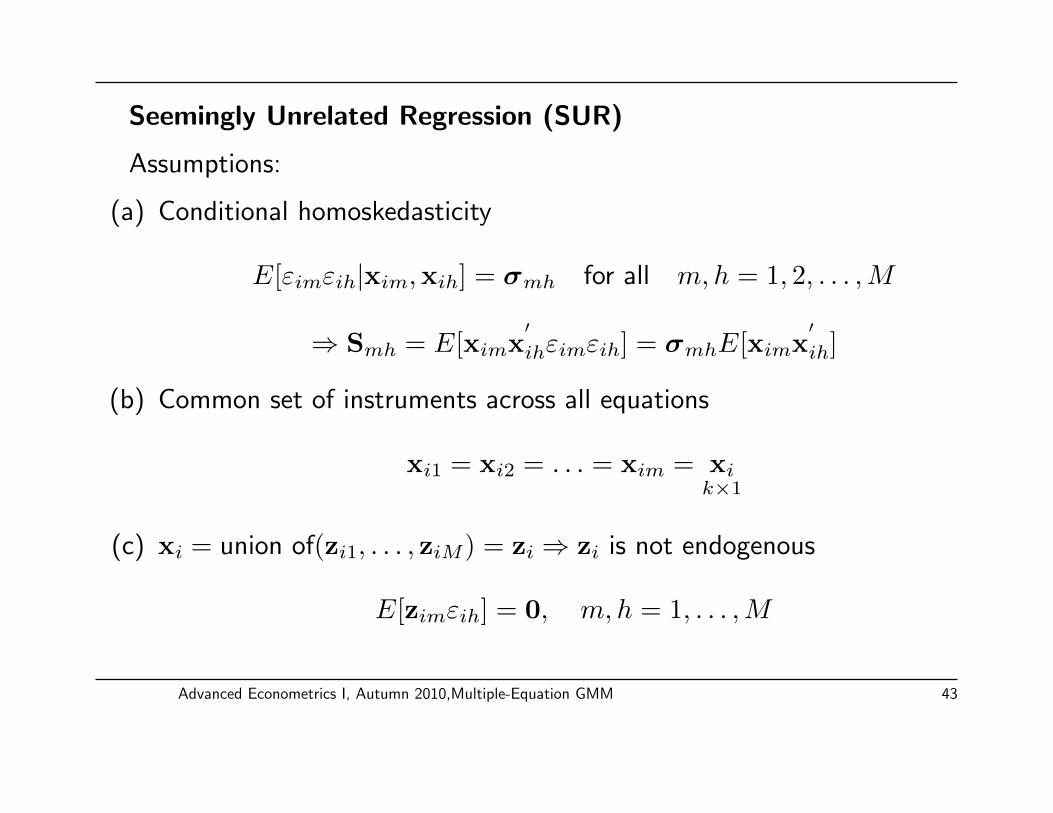

Seemingly Unrelated Regression (SUR)

Assumptions:

(a) Conditional homoskedasticity

E[εimεih|xim,xih] = σmh for all m,h = 1, 2, . . . ,M

⇒ Smh = E[ximx′ihεimεih] = σmhE[ximx

′ih]

(b) Common set of instruments across all equations

xi1 = xi2 = . . . = xim = xik×1

(c) xi = union of(zi1, . . . , ziM) = zi ⇒ zi is not endogenous

E[zimεih] = 0, m, h = 1, . . . ,M

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 43

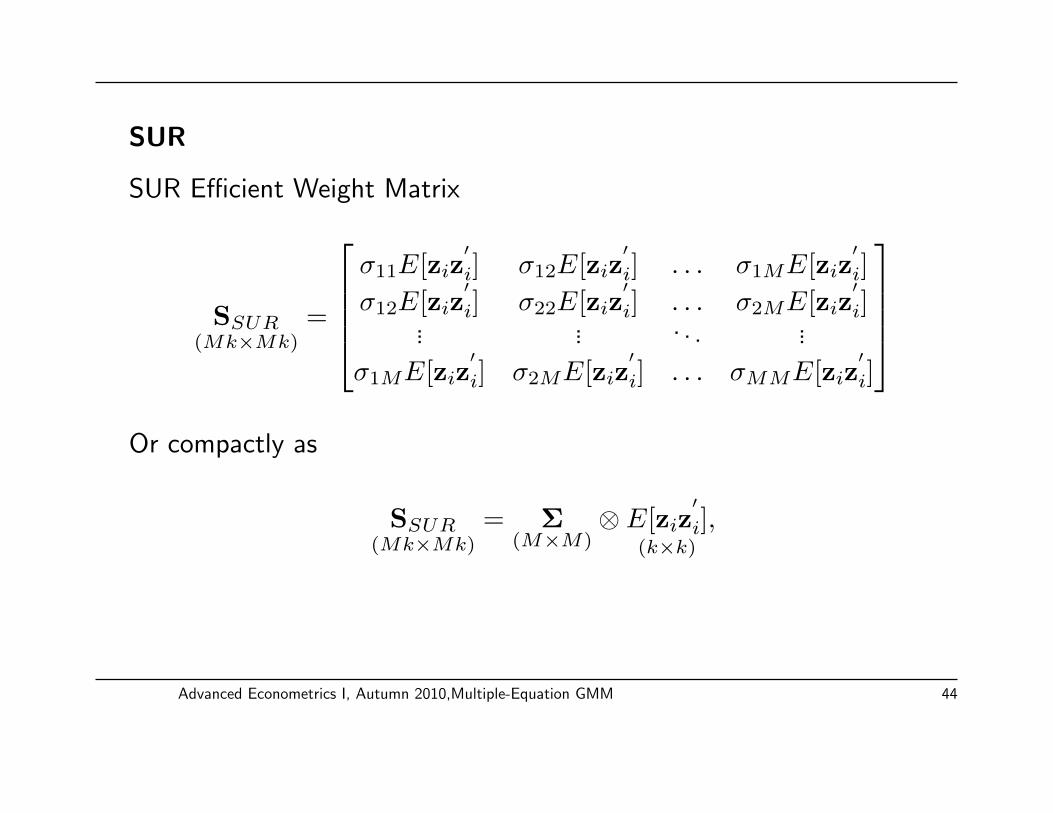

SUR

SUR Efficient Weight Matrix

SSUR(Mk×Mk)

=

σ11E[ziz

′i] σ12E[ziz

′i] . . . σ1ME[ziz

′i]

σ12E[ziz′i] σ22E[ziz

′i] . . . σ2ME[ziz

′i]

... ... . . . ...

σ1ME[ziz′i] σ2ME[ziz

′i] . . . σMME[ziz

′i]

Or compactly as

SSUR(Mk×Mk)

= Σ(M×M)

⊗ E[ziz′i]

(k×k),

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 44

SUR

Estimating SSUR

SSUR = ΣSUR ⊗ Szz,

where

Szz =1

nZ′Z,

and

σmh =1

n(ym − Zmδm,OLS)

′(yh − Zhδh,OLS)

alsoδm,OLS = (Z

′mZm)−1Z

′mym

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 45

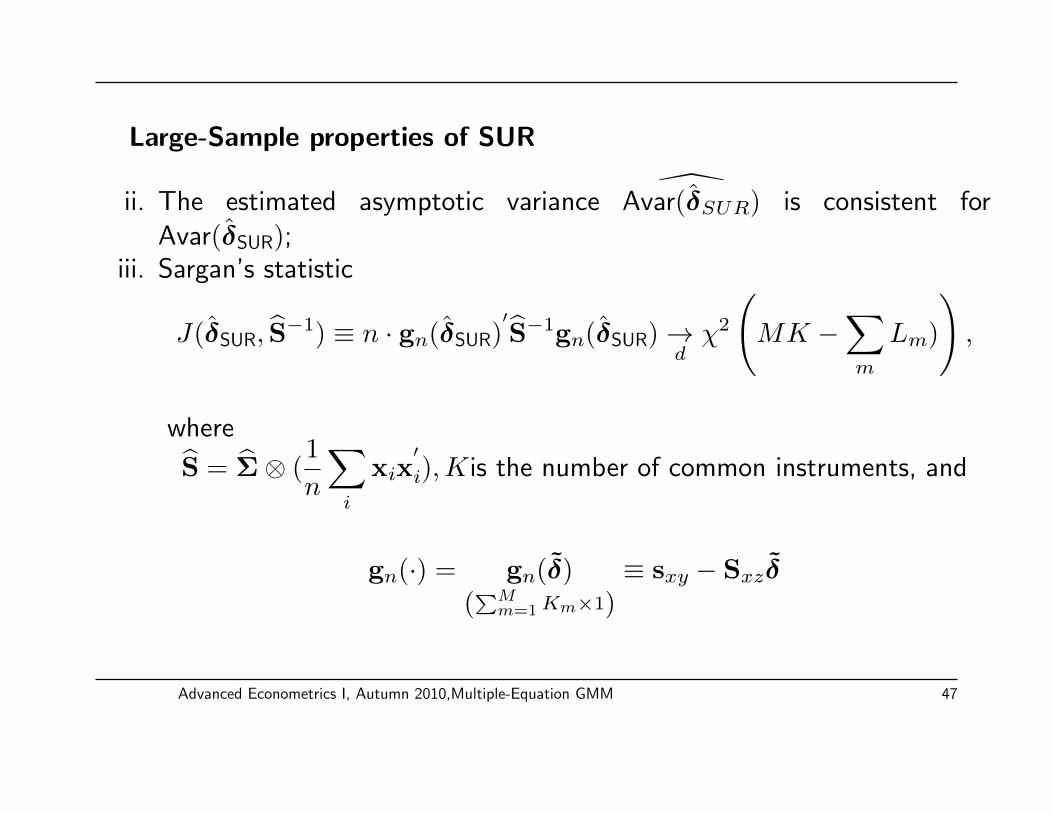

Large-Sample properties of SUR

Under the conditions of

a. Assumptions 4.1-4.5 and 4.7,b. Common set of instruments (xim = xi),c. xi = union of(zi1, . . . , ziM)

d. Σ is the M ×M matrix of estimated error cross moments

Σ ≡

σ11 . . . σ1M... ...

σM1 . . . σMM

=1

n

n∑i=1

εiε′

i,

estimated using the OLS residuals.

Then (See Hayashi, p. 281):

i. δSUR is consistent, asymptotically normal, and efficient with Avar(δSUR);

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 46

Large-Sample properties of SUR

ii. The estimated asymptotic variance Avar(δSUR) is consistent forAvar(δSUR);

iii. Sargan’s statistic

J(δSUR, S−1) ≡ n · gn(δSUR)

′S−1gn(δSUR)→

dχ2

(MK −

∑m

Lm)

),

where

S = Σ⊗ (1

n

∑i

xix′i),Kis the number of common instruments, and

gn(·) = gn(δ)(∑M

m=1 Km×1)≡ sxy − Sxzδ

Advanced Econometrics I, Autumn 2010,Multiple-Equation GMM 47