13.3. annual percentage rate (apr) and the rule of 78 annual interest rate (apr) table 13.3 annual...

TRANSCRIPT

13.3. Annual Percentage Rate (APR) and the Rule of 78

A. Find the APR of a loan.

B. Use the rule of 78 to find the refund and payoff

of a loan.

C. Find the monthly payment for a loan using an

online calculator.

Objectives

Truth-in-Lending: APR to Z

We have studied several types of consumer credit: credit

cards, revolving charges, and add-on interest. Before 1969,

it was almost impossible to compare the different types of

credit accounts available to consumers.

In an effort to standardize the credit industry, the

government enacted the federal Truth-in-Lending Act of

1969.

A key feature of this law is the inclusion of the total

payment, the amount financed, and the finance charges

in credit contracts.

Annual Percentage Rate and the Rule of 78

How can we compare loans? To do so, two items are of

crucial importance: the finance charge and the annual

percentage rate (APR).

A look at annual percentage rates will enable us to

compare different credit options.

For example, suppose you can borrow $200 for a year at

8% add-on or get the same $200 by paying $17.95 each

month.

Which is the better deal? In the first instance, you borrow

$200 at 8% add-on, which means that you pay 8% of $200,

or $16, in finance charges.

Annual Percentage Rate and the Rule of 78

The charge you pay per $100 financed is .

On the other hand, if you pay $17.95 per month for 12

months, you pay a total of $215.40.

Here the finance charge per $100 financed is

. Obviously, the second loan is a better

deal.

Annual Percentage Rate and the Rule of 78

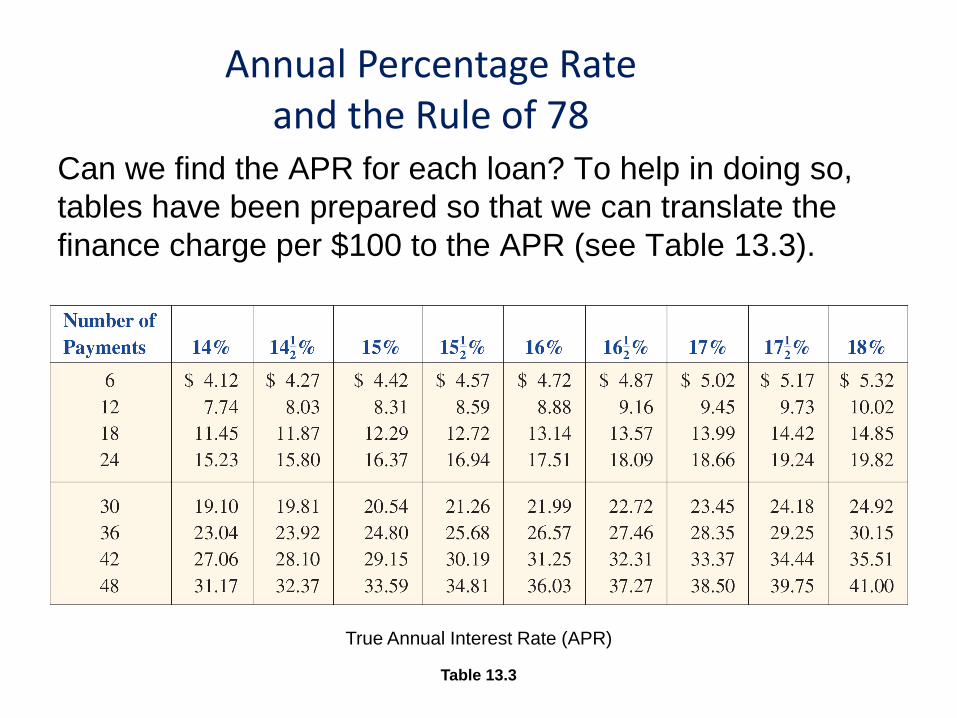

Can we find the APR for each loan? To help in doing so,

tables have been prepared so that we can translate the

finance charge per $100 to the APR (see Table 13.3).

True Annual Interest Rate (APR)

Table 13.3

Annual Percentage Rate and the Rule of 78

Note that the finance charge is the total dollar amount you

are charged for credit. It includes interest and other

charges such as service charges, loan and finder’s fees,

credit-related insurance, and appraisal fees.

The annual percentage rate (APR) is the charge for credit

stated as a percent.

In general, the lowest APR corresponds to the best credit

buy regardless of the amount borrowed or the period of

time for repayment.

For example, suppose you borrow $100 for a year and pay

a finance charge of $8.

APR

If you keep the entire $100 for the whole year and then pay

$108 all at one time, then you are paying an APR of 8%.

On the other hand, if you repay the $100 plus the $8

finance charge in 12 equal monthly payments (8% add-on),

you do not have use of the $100 for the whole year.

What, in this case, is your APR?

APR

The formulas needed to compute the APR are rather

complicated, and as a consequence, tables such as

Table 13.3 have been constructed to help you find the

APR.

True Annual Interest Rate (APR)

Table 13.3

APR

These tables are based on the cost per $100 of the amount

financed. To use Table 13.3, you must first find the finance

charge per $1 of the amount financed and then multiply by

100.

Thus, to find the APR on the $100 borrowed at 8% add-on

interest and repaid in 12 equal payments of $9, first find the

finance charge per $100 as follows:

1. The finance charge is $108 – $100 = $8.

2. The charge per $100 financed is

APR

Since there are 12 payments, look across the row labeled

12 in Table 13.3 until you find the number closest to $8.

True Annual Interest Rate (APR)

Table 13.3

APR

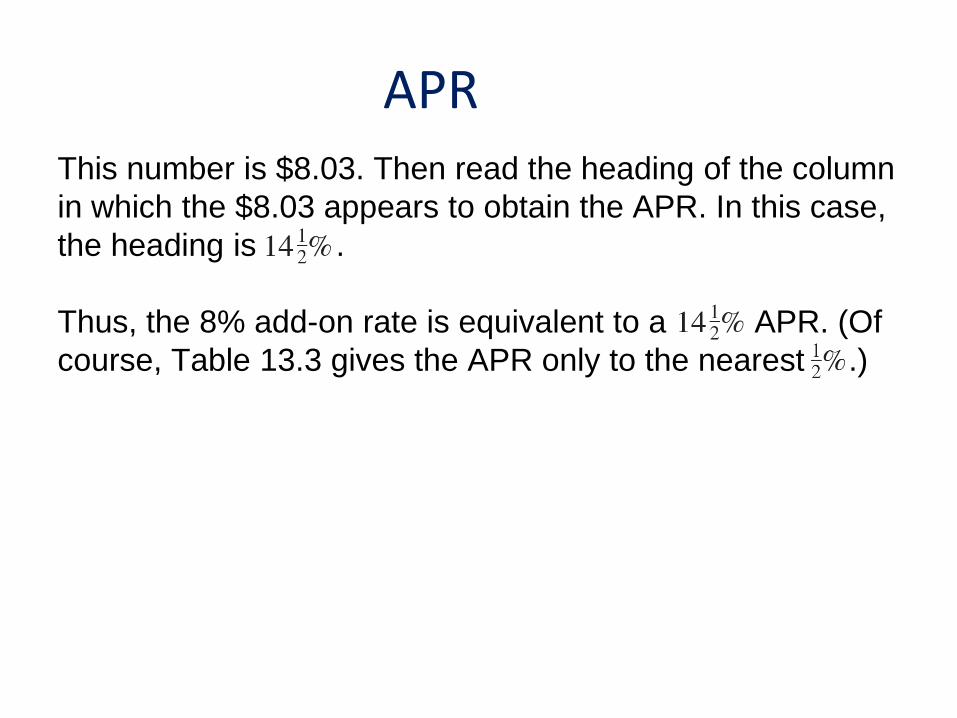

This number is $8.03. Then read the heading of the column

in which the $8.03 appears to obtain the APR. In this case,

the heading is .

Thus, the 8% add-on rate is equivalent to a APR. (Of

course, Table 13.3 gives the APR only to the nearest .)

APR

Example

Mary Lewis bought some furniture that cost $1400. She paid $200 down and agreed to pay the balance in 30 monthly installments of $48.80 each. What was the APR for her purchase?

Solution

We first find the finance charge per $100 as follows:

SolutionWe now turn to Table 13.3 and read across the row labeled 30 (the number of payments) until we find the number closest to $22. This number is $21.99. We then read the column heading to obtain the APR, 16%.

The Rule of 78

In many cases you are entitled to a partial refund of the finance charge! The problem is to find how much you should get back. One way of calculating the refund is to use the rule of 78.

This rule assumes that the final payment includes a portion, say, $a, of the finance charge, the payment before that includes $2a of the finance charge, the second from the final payment includes $3a of the finance charge, and so on.

The Rule of 78

If the total number of payments is 12, then the finance charge is paid off by the sum of a + 2a + 3a + 4a + 5a + 6a+ 7a + 8a + 9a + 10a + 11a + 12a = 78a dollars.

If the finance charge is F dollars, then

78a = F

soa = .

This is the reason for the name “rule of 78.” Now suppose you borrow $1000 for 1 year at 8% add-on interest.

The Rule of 78

The interest is $80, and the monthly payment is one-twelfth of $1080, that is, $90.

If you wish to pay off the loan at the end of 6 months, are you entitled to a refund of half the $80 interest charge? Not according to the rule of 78.

Your remaining finance charge payments, according to this rule, are

The Rule of 78of 78

Since F = $80, you are entitled to a refund of , or

$21.54. There are six payments of $90 each for a total of

$540, so you would need to pay $540 – $21.54 = $518.46

to cover the balance of the loan.

Notice that to obtain the numerator of the fraction , we

had to add 1 + 2 + 3 + 4 + 5 + 6.

If there were n payments remaining, then to find the

numerator, we would have to add.

The Rule of 78

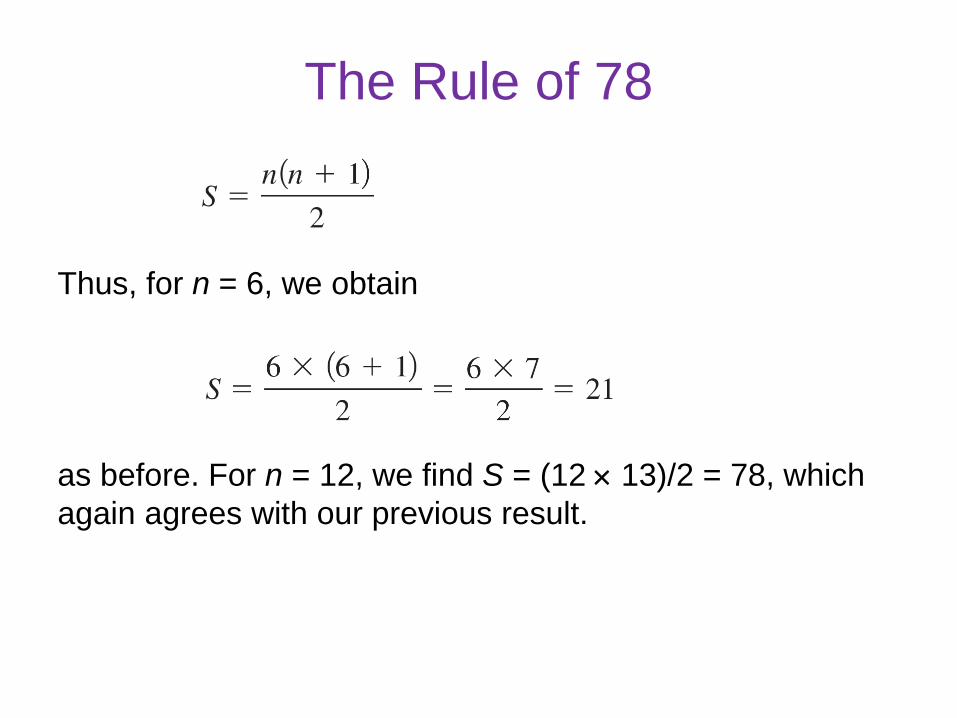

There is an easy way to do this. Let us call the sum S.

Then we can write the sum S twice, once forward and once

backward.

If we add these two lines, we get

and because there are n terms on the right,

The Rule of 78

Thus, for n = 6, we obtain

as before. For n = 12, we find S = (12 13)/2 = 78, which

again agrees with our previous result.

The Rule of 78

In general, if the loan calls for a total of n payments and the

loan is paid off with r payments remaining, then the

unearned interest is a fraction a/b of the total finance

charge, with the numerator

and the denominator

Formula for the Unearned interest u

Thus,

Thus, the unearned interest u is as shown below.

Actuary Formulas for the Refund u and the Payoff

There is another way of calculating refunds and payoffs: by

using a formula.

Example 3 – Refunds and Payoffs Using Formulas

Refer to Example 1, where Mary Lewis bought furniture

costing $1400 with $200 down and 30 payments of $48.80.

Assume that Mary wants to pay off the loan after 24

payments. Find

(a) the refund using the rule of 78.

(b) the refund using the formula.

(c) the payoff using the rule of 78.

(d) the payoff using the formula.

Example 3 – Solution

(a) Using the rule of 78, the refund is

where r = 30 – 24 = 6, n = 30, and

Thus, the refund using the rule of 78 is

(b) The refund using the formula is

where r = 6, PMT = $48.80, and V is the value from the

APR table corresponding to 6 and an APR of 16%

(note that the APR in Example 1 was 16%).

cont’dExample 3 – Solution

This value is $4.72.

Thus, the refund is

(c) The payoff using the rule of 78 is

cont’dExample 3 – Solution

(d) The payoff using the formula is

where i = .

cont’dExample 3 – Solution

Since in Example 1 the APR = 16%,

and the payoff is

cont’dExample 3 – Solution

Applications

Realistically, there are more factors associated with loans

than the APR and the rule of 78. In most cases you need a

calculator to do the work! We illustrate the use of such a

calculator in Example 4.

Example 4 the Net

Suppose that the purchase price of a car is $15,000.

There is no cash rebate, your trade-in is $4000, you do not

owe any money on your trade-in, the down payment is

$2000, and you want to finance the car at 10% for 36

months.

What is your monthly payment?

Example 4 – Solution

Steps 1 and 2 (see Figure 13.4) are to enter your zip code

and the vehicle sales price: ($15,000).

Figure 13.4

Skip the sales tax ($0) and the title and registration ($0) for

now.

Next enter the value of your trade-in ($4000), the amount

you owe on your trade-in ($0), and the cash down payment

($2000).

In step 4, enter the Loan Term in months (36) and the

Finance Rate (10%). Press

cont’dExample 4 – Solution

As you can see in Figure 13.5, your monthly payment will

be $290.

By the way, you can also find out about your maintenance

costs and leasing. You can even figure out what car you

can afford by selecting the topic!

cont’dExample 4 – Solution

Figure 13.5