131211 presentation investor seminar london - rio tinto · 11 december 2013 london investor seminar...

TRANSCRIPT

11 December 2013London

Investor SeminarDelivering greater value for shareholders

©2013, Rio Tinto, All Rights Reserved

Cautionary statement

This presentation has been prepared by Rio Tinto plc and Rio Tinto Limited (“Rio Tinto”) and consisting of the slides for a presentation concerning Rio Tinto. By reviewing/attending this presentation you agree to be bound by the following conditions.

Forward-looking statementsThis presentation includes forward-looking statements. All statements other than statements of historical facts included in thispresentation, including, without limitation, those regarding Rio Tinto’s financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relating to Rio Tinto’s products, production forecasts and reserve and resource positions), are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Rio Tinto, or industryresults, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements.

Such forward-looking statements are based on numerous assumptions regarding Rio Tinto’s present and future business strategies and the environment in which Rio Tinto will operate in the future. Among the important factors that could cause Rio Tinto’s actual results, performance or achievements to differ materially from those in the forward-looking statements include, among others, levels of actual production during any period, levels of demand and market prices, the ability to produce and transport products profitably, the impact of foreign currency exchange rates on market prices and operating costs, operational problems, political uncertainty and economic conditions in relevant areas of the world, the actions of competitors, activities by governmental authorities such as changes in taxation or regulation and such other risk factors identified in Rio Tinto's most recent Annual Report on Form 20-F filed with the United States Securities and Exchange Commission (the "SEC") or Form 6-Ks furnished to the SEC. Forward-looking statements should, therefore, be construed in light of such risk factors and undue reliance should not be placed on forward-looking statements. These forward-looking statements speak only as of the date of this presentation.

Nothing in this presentation should be interpreted to mean that future earnings per share of Rio Tinto plc or Rio Tinto Limited will necessarily match or exceed its historical published earnings per share.

2

©2013, Rio Tinto, All Rights Reserved

Agenda3

Introduction, outlook and strategy Sam Walsh

Capital allocation and performance Chris Lynch

Diamonds & Minerals Alan Davies

Energy Harry Kenyon-Slaney

Break

Iron Ore Andrew Harding

Wrap up Sam Walsh

Q & A

11 December 2013London

Emergency procedureAndaz Hotel

11 December 2013London

Sam WalshChief executive

©2013, Rio Tinto, All Rights Reserved

Delivering greater value for shareholders6

Lower operating costs*

Exploration & evaluation*

Lower capexDeliver approved projects

• Pilbara 290• Oyu Tolgoi phase 1• Kestrel• Argyle underground• AP60

Divest non-core assets

$3.3bn announced or completed this year

Increase production

• Pilbara records• Thermal coal

Q3 record• Cu recovery

$1.8bn

$0.8bn

* Year to date figures as at end of October 2013

©2013, Rio Tinto, All Rights Reserved

7

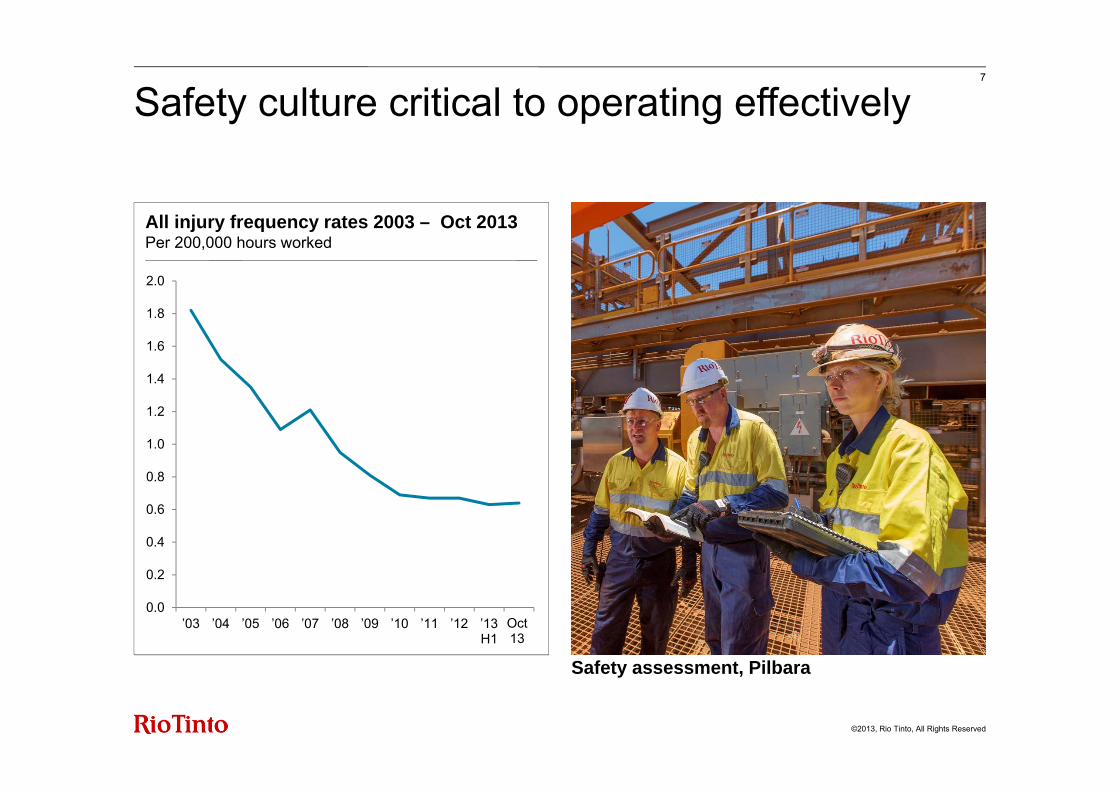

Safety culture critical to operating effectively

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 H1

Oct13

All injury frequency rates 2003 – Oct 2013Per 200,000 hours worked

Safety assessment, Pilbara

©2013, Rio Tinto, All Rights Reserved

• Four key operating assets + two tier one greenfield projects

• Progress already made in 2013 towards executing the strategy− Disposals of $1.8 billion from non-

core assets− Material productivity improvement

and cost savings− Disciplined and prioritised capex

• La Granja and Resolution provide strong pipeline for growth through phased and prioritised development

• Clear roadmap to become a first quartile producer

8

Copper 4+2 strategy set to create substantial and sustainable value for shareholders

©2013, Rio Tinto, All Rights Reserved

• Divesting or curtailing high cost production to focus on strongest margin businesses

• Over $450 million of cost reductions achieved to October 2013, despite weather impact (c.$60 million)

• Expect more cost savings next year to achieve $1 billion in 2014 vs. 2012

• Increased productivity across the business

• 21% reduction in global headcount

• Suspension of Gove refinery to focus on bauxite business (c.7-8Mt/a)

9

Transforming Rio Tinto Alcan through reducing cost, improving productivity and strengthening the portfolio

Closures and curtailmentsThousand tonnes

Aluminium cash cost curve*US$ per tonne

500

1000

1500

2000

2500

3000

RoW China25% 75%50%

Price

* Cost curve includes an estimate of premiums as a credit to costs

0100

200300400500

600700

Beauharnois- 2009

Anglesey- 2009

St Jean**- 2009

Soral**- 2009

Lynemouth- 2011

Shawinigan- 2013

** Indicates a partial closure

©2013, Rio Tinto, All Rights Reserved

Our businesses are well placed to meet global demand growth

10

World GDP compositionTrillions of 2005 PPP$ Percentage of world GDP

Source: Global Insight

35%

40%

45%

50%

55%

60%

65%

70%

75%

2000 2005 2010 2015 2020 2025

Chinese urbanisationPercentage of population

+260 Million urban population

+170 Million urban population

Source: NBS, McKinsey Global Institute

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

140

2000 2005 2010 2015 2020 2025

North America

Europe

Japan-Korea

China

India

Other Asia

C & S America

RoW

Emerging markets (RHS)

©2013, Rio Tinto, All Rights Reserved

A consistent strategy with clear priorities11

Greater value for shareholders

Invest in and operate long-life,low-cost, expandable operations

Clear priorities for 2013

Improve performance

Strengthen the balance sheet

Deliver results

Strategy

Priorities

Outcome

11 December 2013London

Chris LynchChief financial officer

©2013, Rio Tinto, All Rights Reserved

Cos

t Red

uctio

ns

Effic

ienc

yIm

prov

emen

ts

Gra

de

Stri

p R

atio

s

Ope

ratio

nal

Rea

dine

ss/

Ram

p up

Mar

ket d

riven

volu

me

redu

ctio

ns

One

-offs

& o

ther

Tota

l Cas

hC

ost I

mpa

ct

• On track to achieve $2 billion target for full year 2013

• Targeting further savings in 2014 to reach $3 billion full-year improvement vs 2012

• Global headcount net reduction of ~3,800 since 30 June 2012

• More than 1,500 separate initiatives being implemented across the business

• Sharing practices across the Group to leverage cost reduction efforts

Pre tax operating cash cost variance2013 October year to date, US$ million

13

Strong performance on operating cash costs

Aluminium

Copper

Energy

Other PGs & central

1,826

Iron Ore

©2013, Rio Tinto, All Rights Reserved

• Year to date spend around 50% lower than 2012

• Strong project pipeline to supply future reserves and resources− 28 major projects ongoing − across 10 commodities− in 19 countries

• Already exceeded 2013 target of $750 million reduction in full year exploration and evaluation spend

• Reduced spend to be sustained in 2014 and beyond

Exploration and evaluation costsUS$ million (pre tax)

14

Targeted reductions in exploration and evaluation spend

$812 million

-

250

500

750

1,000

1,250

1,500

Oct-12 YoY saving Oct-13

Iron ore evaluation Copper evaluationAluminium evaluation Energy evaluationD&M evaluation Central exploration

©2013, Rio Tinto, All Rights Reserved

• Iron ore growth pathway optimised at a lower capital intensity

• $2 billion reduction in sustaining capital across the Group

• Five major projects completed so far in 2013

• Growth in the most attractive commodities

• Sequencing the best projects to optimise capex

Expected capital expenditure profile*US$ billion

15

Delivering strong growth and lower capital expenditure

17.6

<14

<11

~8

0

5

10

15

20

2012A 2013F 2014F 2015F

Sustaining Pilbara sustaining Pilbara growth Other growth

* Forecast capex is subject to variation in future exchange rates

>20%

>20%

>20%

©2013, Rio Tinto, All Rights Reserved

Capital allocation priorities16

Balance sheet Cash returns to shareholders

Growth and sustaining capex

Progressive dividends

Essentialsustaining capex

From:

To:

1 2 3

Iterative cycle of:1 2 3

Debt reduction

Compelling growth

Further cash

returns to shareholders

©2013, Rio Tinto, All Rights Reserved

• $3.3 billion of divestments announced or completed this year− $2.3 billion of cash proceeds

received, including Northparkes− $1 billion expected to complete in

2014 (Clermont)

• Capturing value now from assets that no longer fit our strategy− >20 divestments worth a total of

$16.9 billion completed since 2008− Focus on value realisation

Clockwise from top left: Clermont, Eagle, Sebree, Palabora and Northparkes

17

Progressing non-core asset disposals

©2013, Rio Tinto, All Rights Reserved

18

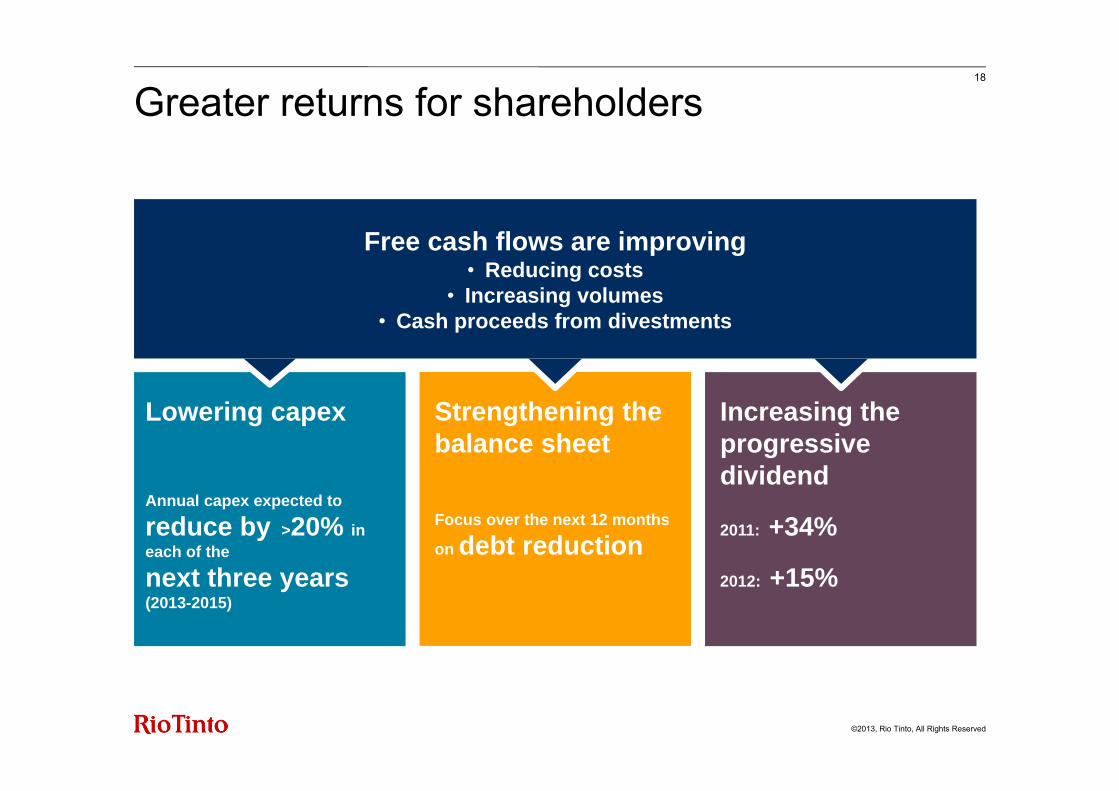

Greater returns for shareholders

Lowering capex

Annual capex expected to

reduce by >20% in each of the

next three years (2013-2015)

Increasing the progressive dividend

2011: +34%

2012: +15%

Strengthening the balance sheet

Focus over the next 12 months

on debt reduction

Free cash flows are improving• Reducing costs

• Increasing volumes • Cash proceeds from divestments

Alan DaviesChief executive, Diamonds & Minerals

11 December 2013London

©2013, Rio Tinto, All Rights Reserved

• Portfolio of industry leading businesses

• Mid-to-late cycle commodities with demand growth in later stages of economic development

• Titanium dioxide business is well placed to supply growing demand for pigment

• Richard’s Bay Minerals acquisition earnings accretive from day one

• Diamonds well positioned for profitable growth

• Strong underlying position in borates, with optionality to grow

• Supplying the growing Asian salt market

• Advancing a tier one iron ore project in Guinea

20

A leader in our markets

Clockwise from top left: Havre St Pierre, Diavik, Dampier Salt, Simandou and Boron

©2013, Rio Tinto, All Rights Reserved

• Strategy focused on:− Creating demand-led, integrated

operations that are responsive to the changing external environment

− Generating proprietary market insight

− Driving returns through increasing productivity, flexibility and cutting costs

− Strengthening position in traditional segments and entering attractive new markets

• Relentless focus on safety

Argyle underground block cave, Australia

21

Operating demand-led operations in attractive markets

©2013, Rio Tinto, All Rights Reserved

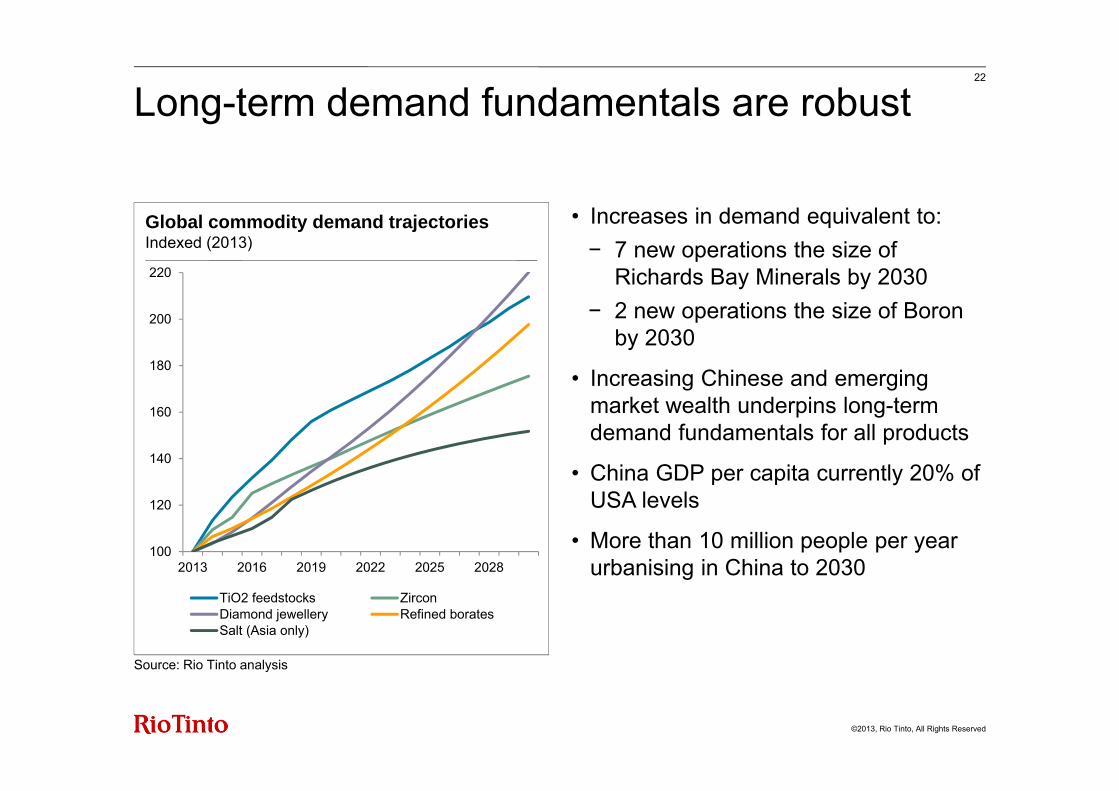

• Increases in demand equivalent to:− 7 new operations the size of

Richards Bay Minerals by 2030− 2 new operations the size of Boron

by 2030

• Increasing Chinese and emerging market wealth underpins long-term demand fundamentals for all products

• China GDP per capita currently 20% of USA levels

• More than 10 million people per year urbanising in China to 2030

Global commodity demand trajectoriesIndexed (2013)

Source: Rio Tinto analysis

22

Long-term demand fundamentals are robust

100

120

140

160

180

200

220

2013 2016 2019 2022 2025 2028

TiO2 feedstocks ZirconDiamond jewellery Refined boratesSalt (Asia only)

©2013, Rio Tinto, All Rights Reserved

• Demand-led operating philosophy: − Diamonds production ramping up to

meet growing demand− Zircon and rutile production adjusted

to market demand− Planned RTFT furnace 5 shut

brought forward− UGS facility temporarily taken offline− Temporary shut downs at Havre-

Saint-Pierre and QMM− Production vacation shut downs

at Boron mine and boric acid plant• Increasing integration and flexibility:− System and process optimisation− Market to mine integration− Working capital reviews

23

A responsive market-driven business

Richards Bay Minerals, South Africa

©2013, Rio Tinto, All Rights Reserved

0

20

40

60

80

100

2012 2013 2014

• 2013 cash operating costs ~9% lower than 2012

• $30m in annualised savings of support cost from streamlining the organisation structure

• Reduction of over 1000 positions during 2013

• Businesses expected to deliver 10% increase in labour productivity by 2015

• Cost and productivity improvements will enhance structural position of business as volumes return

• Capital programme focused only on necessary sustaining, replacement and completion of major projects

24

Driving operating performance by cutting costs, improving productivity and managing capital

Cash operating costs*

Indexed (2012)

Capital expenditure*

Indexed (2012)

* Operating businesses, does not include the Simandou project

-55%

-14%

020406080

100

2012 2013 2014 2015Sustaining Development

©2013, Rio Tinto, All Rights Reserved

0

40

80

120

160

2011 2012 2013 2014Feedstock Inventory Pigment Inventory

• Strong medium and longer-term fundamentals underpinned by growth in pigment demand in emerging economies

• Fixed price multi-year TiO2 contracts continue to be replaced

• Pigment inventory built up through 2012 has been unwound during 2013

• Increasing pigment production expected to result in higher feedstock demand in 2014 and reduce inventory levels across the value chain

• Co-products add significant value• Expecting consistent zircon demand in

2014, with some inventory overhang challengesSource: Rio Tinto analysis

* 2014 estimated industry finished product inventory

25

Titanium dioxide fundamentals remain strong

TiO2 contract volumesPercentage

Industry finished product inventory Indexed (2011)

0%

25%

50%

75%

100%

2011 2012 2013 2014 2015

Longer-term pricing Shorter-term pricing

*

©2013, Rio Tinto, All Rights Reserved

020406080

100

2011 2012 2013

• Aligning capacity utilisation to market demand

• Two production rebuilds coincided with softer market conditions in 2012

• Further decisions to curtail production throughout 2013

• Maintaining options to participate in market demand growth where appropriate− Zulti-South studies underway to

sustain RBM smelter capacity − Studies to extend the mine life of

Havre-St-Pierre− Options to expand QMM − Exploratory work in Mozambique

26

Demand-led operating philosophy with the flexibility to respond to market changes

TiO2 feedstock production (100% basis)Capacity = 100

Zircon production (100% basis)Indexed (2011)

020406080

100

2011 2012 2013

-55%

-25%

©2013, Rio Tinto, All Rights Reserved

• Near-term pressures due to tight liquidity and Indian rupee volatility but strong industry fundamentals supporting price appreciation

• Ramp up of production from Argyle & Diavik and structural cost savings deliver step change in unit costs

• Second crusher at Argyle operational by 2015 with total production ramping up to 20mctpa

• All three underground mining pipes at Diavik at capacity

• Undergoing incremental production capacity improvement work

27

Diamonds are well positioned for profitable growth

Diamond production (Rio Tinto Share)Million carats

Expected unit costs Indexed (2012 )

020406080

100

2012 2013 2014 2015

0.05.0

10.015.020.025.0

2012 2013 2014 2015Argyle Diavik Murowa

CAGR 23%

- 30-40%

©2013, Rio Tinto, All Rights Reserved

• Tier one orebody at Boron, California

• Borates demand growth driven by US housing, Chinese industrials and global agriculture

• Supplying high quality products to high demand end-users

• Options for incremental capacity expansions in response to market conditions

• MDDK* introduces a new process and commissioning during 2014

• Jadar lithium-borate project in pre-feasibility

• Potash development joint venture in Saskatchewan, CanadaSource: Rio Tinto analysis

*MDDK – Modified Direct Dissolving of Kernite

28

Aligning borates production to market demand

Global refined borates demandMillion tonnes (boric oxide B2O3 equivalent)

Expected unit costs Indexed (2012)

70

80

90

100

2012 2013 2014 2015

00.5

11.5

22.5

2012 2013 2014 2015 2016 2017 2018 2019 2020

AgricultureEnergy EfficiencyUrbanisation

2012-2020 CAGR %

6

5

4

- 8-10%

©2013, Rio Tinto, All Rights Reserved

• Three operations in Western Australia with a combined capacity of ~10.5Mt

• Demand growth driven by Chinese imports to fuel automotive, construction and electronic sectors

• Potential for incremental expansion in response to demand growth in China and Indonesia

• ‘Back to basics’ operating approach:− 14% reduction in unit costs between

2012 and 2013− Labour productivity increased 8%

between 2012 and 2013

Source: China National Chemical Information Centre

29

Dampier Salt is focused on building capability to deliver greater value

Chinese salt importsMillion tonnes

Labour productivityIndexed (2012)

1.6 2.7 4.1 5.17.5

0

2

4

6

8

2009 2010 2011 2012 2013F

8090

100110120130

2012 2013 2014 2015

CAGR 47%

+ 15-20%

©2013, Rio Tinto, All Rights Reserved

• Largest known undeveloped high grade iron ore deposit in the world

• 100Mtpa progressive mine development

• >40 year mine life with a first quartile cost position

• 650km trans-Guinean railway and port near Conakry

• Complements the Pilbara, providing product and market diversification

• Unique development teamwith full commitment and alignment between the partners

30

Advancing a tier one iron ore project in Guinea

Infrastructure images are illustrations

Min

e Pr

ojec

tPo

rt &

Rai

l Inf

rast

ruct

ure

Proj

ect

©2013, Rio Tinto, All Rights Reserved

Require Investment Framework ratification and infrastructure funding plan to accelerate

End-state integrated mine and infrastructure project

Govt. of Guinea

IFC

SimferJersey

(Chalco & Rio Tinto)

Simandou mine project

Mine operator

Infrastructure investor/s

Simandou port and rail

infrastructure project

Infrastructure operator

31

Investment framework structure

Haulage agreement

• Constructive and collaborate process to finalise the Investment Framework and funding plan

• Holistic approach to infrastructure development with third party/ infrastructure company involvement in funding and construction

• Additional investors will reduce capital funding requirements of existing partners

• Will bring complementary skills to fund, build and participate in the infrastructure

©2013, Rio Tinto, All Rights Reserved

• Generating significant free cash flow

• Creating demand-led, integrated operations with distinctive market insight

• Improving operating performance by cutting costs, driving productivity and delayering the organisation

• Strengthening position in traditional segments and entering attractive new markets

• Maintaining options to participatein market demand growth where appropriate

• Advancing a tier one iron ore project in Guinea

32

Delivering value for shareholders

Drill pads at Simandou, Guinea

Harry Kenyon-SlaneyChief executive, Energy

11 December 2013London

©2013, Rio Tinto, All Rights Reserved

Rio Tinto Energy is getting back to basics by reducing costs and delivering value

• “Run it like you own it” − fostering a culture of performance

and cost control

• Over $600m of cost reductions to the end of October 2013

• Stakeholder engagement

• Technology to leverage resource base

• Optimising the portfolio− Binding agreement for sale of

Clermont bringing in $1.015 billion− Binding agreement for the sale of

Blair Athol

34

Hail Creek, Australia

©2013, Rio Tinto, All Rights Reserved

International seaborne thermal coal cost curve 2013US$ per tonne FOB Newcastle

International seaborne premium hard coking coal cost curve 2013US$ per tonne FOB Newcastle

• Industry wide challenges

− Adjusting costs in a declining price environment

− Declining product qualities

− Limited project finance

• Australia specific challenges− Infrastructure contracts incentivising

uneconomic supply− Strong Australian dollar− Increased Government taxes and

approval obligations− Reduced labour and capital

productivity− Increased community-led challenge

35

Around one third of global seaborne thermal coal production has been loss-making this year

200

100

100 200 300

Australia

Mixed including Canada, United States, Mongolia

High 2013 Benchmark

Low 2013 BenchmarkAverage 2013 Benchmark

Mtpa

100

400200 600

Indonesia

Mixed including Australia, Colombia, Indonesia, South Africa

Mixed including Russia, United States

Average 2013 SpotHigh 2013 Spot

Low 2013 Spot

Mtpa

Source: Wood Mackenzie

©2013, Rio Tinto, All Rights Reserved

7 8

4114 1 8

256

334

200

250

300

350

2012 Europe JKT China India Brazil RoW 2018

Thermal coal

• China, India and emerging South East Asian countries continued urbanisation and industrialisation driving demand

Coking coal

• Strong steel demand in China and India support coking coal

• Non-prime and semi-soft coking coals increasingly needed in the long run to manage scarcity of prime hard coking coal

Source: Wood Mackenzie coal market service (H2 2013)

36

Strong long-term fundamentals for coal demand

(24) 490

67 40 (6)

896

1067

600700800900

10001100

2012 Europe JKT China India OtherAsia

RoW 2018

Seaborne thermal coal demand to grow 19% by 2018Million tonnes

Seaborne metallurgical coal demand to grow 30% by 2018Million tonnes

©2013, Rio Tinto, All Rights Reserved

• Large, option-rich ore bodies with premium quality thermal and semi-soft coking coal serviced by existing supply chain in NSW

• 0.6 billion tonnes reserves and1.6 billion tonnes resources*

• Transforming our business through− Aggressive cost reductions− Productivity improvements− Effective use of emerging market

suppliers− Embedding an ‘owner operator’

value-focused mindset

37

Hunter Valley assets are world class thermal coal resources with transformed cost position

Hunter Valley Operations, NSW

* Rio Tinto share as reported in Rio Tinto 2012 annual reserve and resource table for Hunter Valley region.

Bengalla Mine – Hunter Valley, NSW

©2013, Rio Tinto, All Rights Reserved

Cos

t Red

uctio

ns

Effic

ienc

yIm

prov

emen

ts

Gra

de

Stri

p R

atio

s

Ope

ratio

nal

Rea

dine

ss/

Ram

p up

Mar

ket d

riven

volu

me

redu

ctio

ns

One

-offs

& o

ther

Tota

l Cas

hC

ost I

mpa

ct

• $600 million savings to October 2013

• $1 billion in ongoing savings by end of 2014

• $30/t reduction in operating costs 2013 compared with 2012

• Cost reduction and productivity gains achieved at Rio Tinto Coal Australia− 27% increase in labour productivity− 7% increase in truck utilisation− 12% reduction in spend on parts

and consumables − Further spend reduction of 13%

targeted in consumable costs by using emerging market suppliers

Group pre tax operating cash cost variance2013 October year to date, US$ million

38

Improving performance through costreductions and productivity gains

Aluminium

Copper

Energy

Other PGs & central

1,826

Iron Ore

$600m+

©2013, Rio Tinto, All Rights Reserved

• Mount Thorley Warkworth, Bengallamines and Hunter Valley operations are moving down the cost curve

• Annual savings:− $61m, contract labour− $41m, consultants and external

services− $38m, maintenance, repair and

overhaul activities− $37m, equipment hire− $29m, improved mine operations

39

We are improving our position on the cost curve

Source: Wood Mackenzie (adj. for announced cost reductions achieved)

Australian thermal coal cost curve 2013US$ per tonne fob Newcastle

0

100

0 100 200

BengallaHVO

MTW

Mtpa

2012 2013

Mount Thorley Warkworth, New South Wales

©2013, Rio Tinto, All Rights Reserved

• Unit cash costs are now 14% below September 2010

• >1,500 individual initiatives undertaken in Energy

• Stretch targets for the business going forward have been set

• Production increases driven by− Kestrel expansion− HVO and MTW efficiency

increases− Bengalla extension− Clermont ramp up**

40

Rio Tinto Coal Australia has reduced unit cash coststo below 2010 levels while increasing productivity

68days

40

0

20

40

60

2011 Actual 2012 Actual 2013 Expected 2014 fcst

RTCA Clermont & Blair Athol

100 86

RTCA RTCA_AUD

14% reduction below Sept. 2010 levels

US$ A$

** Clermont mine is in the process of being sold.

Rio Tinto Coal Australia unit cash costs*Indexed (three month rolling average)

Australian coal saleable productionMillion tonnes (100% basis)

* Calculated on a Rio Tinto share basis

©2013, Rio Tinto, All Rights Reserved

• RTCM has established itself as a premium hard coking coal producer

• Significantly improved asset performance achieved by reducing operating costs and increasing productivity

• Challenges remain due to infrastructure constraints and broader market conditions

• Strong engagement with the Government of Mozambique and other key stakeholders on the establishment of a globally competitive coal chain solution

We are working to secure a new pathwayfor our coal business in Mozambique

41

Benga Mine, Mozambique

©2013, Rio Tinto, All Rights Reserved

• Uranium has an important part to play in the global energy mix

• Our portfolio is:− Geographically diverse− Increasingly low cost− Includes high grade projects at

Ranger 3 Deeps (Australia) and Roughrider (Canada)

• Current market conditions are weak but strong demand growth is forecast over next decade

The long-term outlook for uranium ispositive within the global energy mix

42

ERA, Australia (Ranger 3 Deeps)

Rossing Mine, Namibia

©2013, Rio Tinto, All Rights Reserved

Our Energy group’s transformationis delivering sustainable results

• Confident of long term industry fundamentals

• Aggressive spend reduction program

• Business wide improvement program

• ‘Owner operator’ value-focused mindset and culture – ensuring sustainable gains, through the commodity cycle

43

Hail Creek, Australia

Break

11 December 2013London

11 December 2013London

Andrew HardingChief executive, Iron Ore

©2013, Rio Tinto, All Rights Reserved

• Driving efficiency though fully integrated operations

• Lowest cost large volume producer

• Continuous optimisation of capital efficient growth pathways

• Low capital growth projects delivered within time and budget

• Leading sales and marketing strategies

• Reaping the benefits of implementing new technology

Cape Lambert screenhouse

46

Sector leadership continues todeliver strong returns

©2013, Rio Tinto, All Rights Reserved

• Capital intensity to reduce from mid $150s/t to $120-130/t (100% basis)

• Mine production capacity to increase from 290 Mt/a to more than 350 Mt/a by 2017− Rapid low-cost growth to more

than 330 Mt in 2015− 40-50 Mt/a mine capacity growth

from brownfield expansions− Silvergrass and Koodaideri

greenfield mines deferred− Expectations for sustaining

capital requirements unchanged

Mine capacity potential (average annualised)Million tonnes per annum

47

Breakthrough Pilbara growth pathway provides a $3 billion saving in growth capital

200

225

250

275

300

325

350

375

400

2012 2013 2014 2015 2016 2017 2018

©2013, Rio Tinto, All Rights Reserved

• Port and rail expansion to 360Mt/a approved June 2012

• Expected completion during H1 2015

• All wharf topside modules installed

• New stackers, reclaimer and dumper cells on site

• Rail bridge, culvert construction and rail duplication well progressed

New road bridge

48

Infrastructure development to 360 Mt/a is progressing on budget and on schedule

New stacker reclaimer beingdelivered – Cape Lambert

New car dumper being delivered– Cape Lambert

Progress on new car dumper– Cape Lambert

©2013, Rio Tinto, All Rights Reserved

• Initiatives at existing operations will see production of more than 330mt in 2015

• $400m capex approved to date

• Key activities− Minor plant modifications, including

additional crushing and screening− Additional mobile equipment to utilise

plant capacity

Drilling in the Pilbara

49

Brownfield expansions and productivity improvements at less than $15/t

Example mines Indicative Mt/aWest Angelas ~6Yandi ~8Brockman 2 life extension of existing plant ~8

Paraburdoo ~7Nammuldicontract crush & screening ~9

Other ~6 – 10

©2013, Rio Tinto, All Rights Reserved

Silvergrass ~21 Mt/a• Optimisation will increase capacity

and reduce capital cost• Required for growth ramp-up to 360

Mt/a• Share Nammuldi BWT infrastructure• Investment decision deferred until

third quarter 2014 at the earliest

Koodaideri ~30 Mt/a• First production not needed before

2019• No longer required for growth ramp• Investment decision deferred until

2016 at the earliest• Would require a 180km railway lineIron ore stacker

50

Opportunities to defer greenfield mine development reduces medium term capital expenditure

©2013, Rio Tinto, All Rights Reserved

• Record nine month Pilbara mine production of 184 Mt (YoY +4%)

• 64 Mt record production in Q3 2013

• Cape Lambert B first ore on ship four months ahead of schedule – 24 August

• Commissioning continues to deliver ahead of anticipated ramp-up

• Low spend, high return productivity initiatives are ‘business as usual’ across fully integrated mine, rail and port system

51

Pilbara operations and 290 Mt/a ramp-up in top gear

Pilbara mine productionMillion tonnes per quarter

Tonnes shipped – new CLB facilityMillion tonnes cumulative

01020304050607080

Q1 Q2 Q3 Q4

01234567

Anticipated ramp‐upActual

Aug Sep Oct Nov

2010201120122013

290

237

2013

©2013, Rio Tinto, All Rights Reserved

9% reduction in mining costs to Q3 2013• Higher payload from light weight truck trays

• Improved mine planning− Increased truck utilisation− Lower tyre and fuel consumption− Reduced blasting requirements− Decreased haul distances

• Improved maintenance tactics

14% reduction in contractor costs to Q3 2013• Increased employee engagement,

reduced labour hire and other contractors

• Negotiated decreases in contractor rates

• Targeted contractor selection processes

• Competitively testing more of our maintenance work

52

Pilbara operations achieving sustainable cost reductions

Mining cost per tonne of material movedIndexed (Q3 2012)

Total contractor costsAUD millions

10091

YTD Q3 2012 YTD Q3 2013

900950

1,0001,0501,1001,1501,200

YTD Q3 2012 YTD Q3 2013Sustaining Operations Growth Operations

14%

©2013, Rio Tinto, All Rights Reserved

Port capacity

• Parker Point – increased ship loading rates by nearly 1,000 tonnes per hour

• Car dumper work standardisation –improvements in excess of 2 Mt/a and enabled faster train turnaround times

Rail fleet

• Continued braking and train cycle improvements result from electronic controlled pneumatic brakes

Ship Loader – Cape Lambert

53

Driving productivity through a large numberof targeted improvement initiatives

©2013, Rio Tinto, All Rights Reserved

• Unencumbered rail and port network wholly-owned by IOC (Rio Tinto 58.7%)

• CEP project adds mining fleet, ore delivery, grinding and spiral capacity and power infrastructure

• 2013 first 9 months saleable production of 11.4Mt, 12% higher than 2012

• Operational performance to match new capacity as quickly as possible

• Consistently high quality products with the lowest phosphorus in the industry

54

Iron Ore Company of Canada: integrated mine to port production system

©2013, Rio Tinto, All Rights Reserved

0

200

400

600

800

1,000

1,200

2010 2015 2020 2025 2030

For exported goodsReplacement domestic demandNew domestic demand

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 (e)

Source: China National Bureau of Statistics, CISA, Rio Tinto Source: Rio Tinto

55

Chinese resurgence in steel demand this year, with further steady growth ahead

Chinese steel demandMillion tonnes per annum

Crude steel demand projectionsMillion tonnes per annum

2.2%7.5%

9.1%

©2013, Rio Tinto, All Rights Reserved

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2015 2020 2025 2030

China JKT EU27 India ASEAN Middle East Other

Source: Rio Tinto Source: United Nations, Global Insight, Rio Tinto

56

Other developing regions should ensurea strong long-run demand for iron ore

Total iron ore requirementsMillion tonnes

Growth fundamentals 2010-30 CAGR

6.1

2.0

0.3

0 5 10

GDP per capita

Urbanpopulation

Population

6.1

2.3

1.0

0 5 10

3.7

2.2

1.0

0 5 10

GDP percapita

Urbanpopulation

Population

2.4

1.9

1.6

0 5 10

China

ASEAN Middle East

India

©2013, Rio Tinto, All Rights Reserved

0

200

400

600

800

1000

Announced for 2008-10 Completed by Q4 2010

Certain Probable Possible

• New seaborne supply capacity continues to be constrained− Reduced sources of project

financing− Protracted approvals processes− Mid tier/junior projects based on

inferior resources

• In addition to seaborne supply, Chinese domestic iron ore is increasingly difficult to access and costly to produce

Announced and completed seaborne iron ore production capacity (global)Million tonnes

Source: UNCTAD, Rio Tinto analysis

57

On-going constraint to the development of new iron ore supply

0

200

400

600

800

1000

Announced for 2012-14 Completed by Q3 2013

Others completed

Rio Tinto additional capacity

©2013, Rio Tinto, All Rights Reserved

MonthlyQ Lagged

Q Actual

Spot

• Pilbara Blends continue to be base load products for Asian steel industry

• Unprecedented demand for 2014 off-take opportunities due to our reputation of providing stable quality and reliable supply

• Of our 2014 volume:− ~60% committed under long term

contracts− ~15% expiring long term contracts

that will likely be renewed − ~10% new long term contracts

• At least 15% of 2014 production uncontracted for sale into the spot market, in support of robust and transparent indices

2014 Pilbara off-take agreementsby pricing mechanism

58

Rapid uptake of 2014 off-take opportunitieswith unfulfilled demand for Rio Tinto iron ores

©2013, Rio Tinto, All Rights Reserved

• Breakthrough Pilbara growth pathway provides a $3 billion saving in growth capital

• Proven operational performance across the integrated supply chain

• Lowest cost iron ore producer, continuing to reduce operating costs

• Delivering major projects ahead of schedule and under budget

• Leading sales and marketing strategies

• Development and utilisation of innovative, new technology

Coastal infrastructure – November 2013

59

Sector leadership continues to deliver strong returns

11 December 2013London

Sam WalshChief executive

©2013, Rio Tinto, All Rights Reserved

Operating demand-led operations in attractive marketsDiamonds & Minerals

A diverse portfolio of sector leading businesses61

Maintaining position as lowest-cost large-volume producer

Shaping a tier one low cost asset portfolio

Continuing the transformation to improve our portfolio of businesses

Iron ore

Copper

Aluminium

Improving the cost position of our Energy businessesEnergy

Delivering greater value for shareholders by:Product group

©2013, Rio Tinto, All Rights Reserved

Delivering greater value for shareholders62

Lower operating costs*

Exploration & evaluation*

Lower capexDeliver approved projects

• Pilbara 290• Oyu Tolgoi phase 1• Kestrel• Argyle underground• AP60

Divest non-core assets

$3.3bn announced or completed this year

Increase production

• Pilbara records• Thermal coal

Q3 record• Cu recovery

$1.8bn

$0.8bn

* Year to date figures as at end of October 2013

11 December 2013London

Investor SeminarDelivering greater value for shareholders