1.307 production of audit working papers to the …...1.307 (september 04) 19. the sfc has indicated...

TRANSCRIPT

1.307 (September 04)

1

STATEMENT 1.307 GENERAL GUIDANCE

PRODUCTION OF AUDIT WORKING PAPERS TO THE SECURITIES AND FUTURES COMMISSION

UNDER SECTION 179 OF THE SECURITIES AND FUTURES ORDINANCE

(Issued March 2004; revised September 2004 (name change))

Contents Paragraphs

PART I - INTRODUCTION 1 - 9

PART II - DIRECTION GIVEN BY THE SFC TO AN AUDITOR UNDER SECTION 179(1)(iv)

10 - 44

Introduction 10 - 16

Production of audit working papers 17 - 33

Explanations of audit working papers produced 34 - 44

PART III - DIRECTION GIVEN BY THE SFC TO AN EMPLOYEE OF AN AUDITOR UNDER SECTION 179(1)(v)

45 - 51

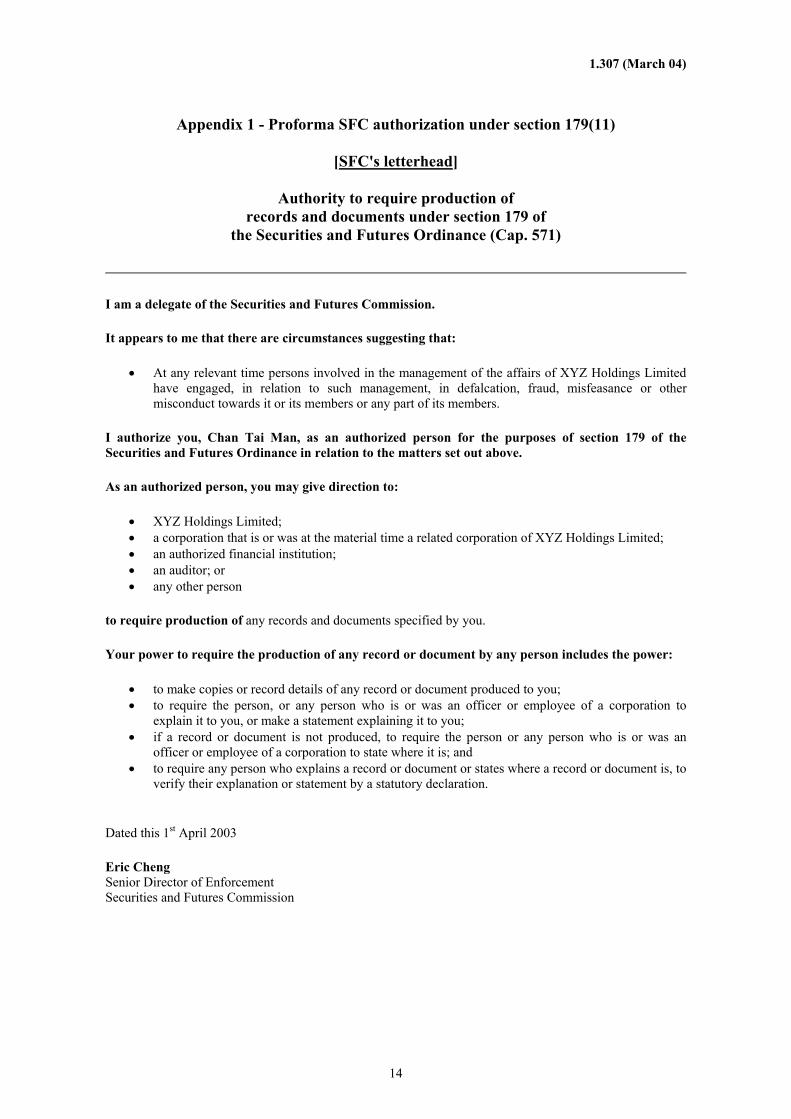

Introduction 45

Grounds for giving a direction 46 - 47

Response to SFC's direction 48 - 51

PART IV - RELEVANT PROVISIONS OF THE SFO REQUIRING THE ATTENTION OF THOSE WHO HAVE BEEN GIVEN A DIRECTION BY THE SFC UNDER SECTION 179(1)(iv) OR 179(1)(v)

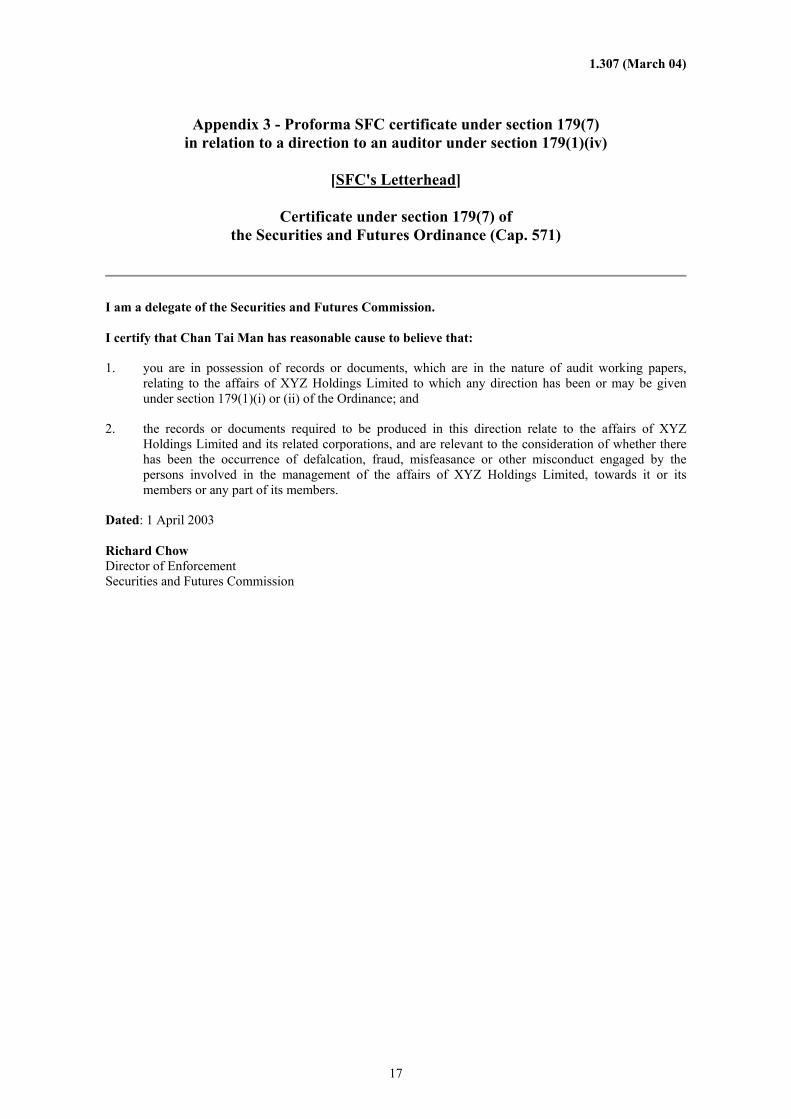

52 - 57

Introduction 52

Application to Court of First Instance relating to non-compliance 53

Use of incriminating evidence in proceedings 54

Lien claimed on records or documents 55

Magistrate's warrants 56

Destruction of documents 57

APPENDICES

1.307 (September 04)

STATEMENT 1.307 GENERAL GUIDANCE

PRODUCTION OF AUDIT WORKING PAPERS TO THE SECURITIES AND FUTURES COMMISSION

UNDER SECTION 179 OF THE SECURITIES AND FUTURES ORDINANCE

PART I - INTRODUCTION

1. The Securities and Futures Ordinance (SFO), which came into effect on 1 April 2003, consolidates ten existing ordinances which regulated the securities and futures market into one single ordinance and makes various amendments to securities law in Hong Kong generally.

2. In this Guidance, all the sections mentioned are in respect of the SFO unless otherwise stated. To make the language of this Guidance simpler and more direct, the male pronoun is used throughout. In addition, the term employee includes a current or former employee of an auditor and the term listed corporation includes a corporation which is or was listed.

3. The SFO enshrines a number of new regulatory initiatives including the strengthening of the Securities and Futures Commission's (SFC) powers to enquire into listed corporations' affairs. Under section 179, the SFC is empowered to require production of records and documents concerning listed corporations from third parties, including such corporations' auditors, bankers and persons who have dealt with such corporations.

4. This Guidance deals with the situations where directions are given by the SFC under section 179(1)(iv) to an auditor and under section 179(1)(v) to an employee of an auditor under the "any other person" category.

5. Part II of this Guidance provides guidance to an auditor of a listed corporation who is given directions by the SFC under section 179(1)(iv) to produce the audit working papers and to provide or make any explanation or statement in respect of the audit working papers that have been produced.

6. Part III of this Guidance provides guidance to an auditor's employee who is given directions by the SFC under section 179(1)(v) to produce the audit working papers and to provide or make any explanation or statement in respect of the audit working papers that have been produced.

7. Part IV of this Guidance highlights the relevant provisions of the SFO requiring the attention of those who have been given directions by the SFC under section 179(1)(iv) or 179(1)(v).

8. The Appendices to this Guidance include a number of proforma documents provided to the Hong Kong Institute of Certified Public Accountants (HKICPA) by the SFC. Auditors should note that these documents are only sample documents and should expect variations of them.

9. This Guidance has been prepared in consultation with the SFC.

2

1.307 (September 04)

PART II - DIRECTION GIVEN BY THE SFC TO AN AUDITOR UNDER SECTION 179(1)(iv)

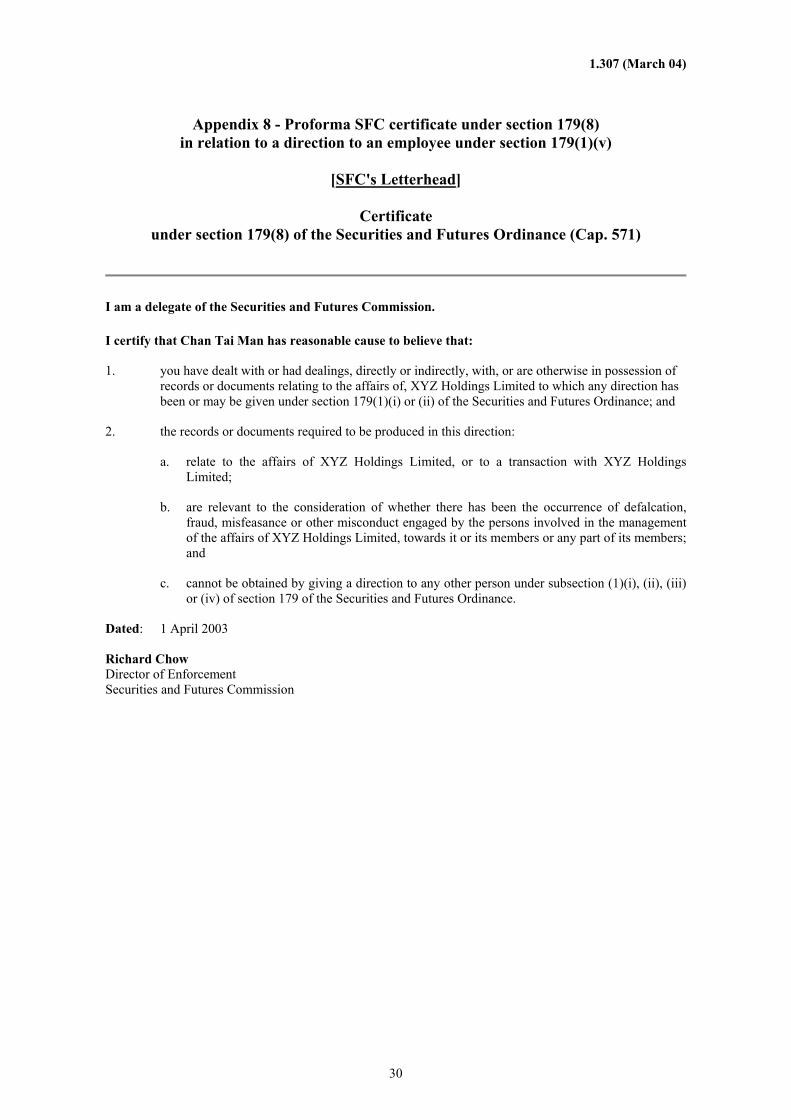

INTRODUCTION

10. Under section 179(1)(iv) an authorized person (as defined in section 179(11) - see paragraph 17 below) is empowered to give a direction to require an auditor (as defined by the Securities and Futures (Miscellaneous) Rules - see paragraph 11 below) of a listed corporation to produce any record or document, which is in the nature of audit working papers (as defined in section 178 - see paragraph 12 below), relating to the affairs of the listed corporation. The authorized person can exercise this power in relation to a listed corporation where:

a. it appears to the SFC that there are circumstances suggesting that at any time since the formation of the corporation the business of the corporation has been conducted:

- with intent to defraud its creditors, or the creditors of any other person; - for any fraudulent or unlawful purpose; or - in a manner oppressive to its members or any part of its members;

b. it appears to the SFC that there are circumstances suggesting that the corporation was formed for any fraudulent or unlawful purpose;

c. it appears to the SFC that there are circumstances suggesting that persons concerned in the process by which the corporation became listed (including that for making the securities of the corporation available to the public in the course of such process) have engaged, in relation to such process, in defalcation, fraud, misfeasance or other misconduct;

d. it appears to the SFC that there are circumstances suggesting that at any time since the formation of the corporation persons involved in the management of the affairs of the corporation have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members;

e. it appears to the SFC that there are circumstances suggesting that at any time since the formation of the corporation members of the corporation or any part of its members have not been given all the information with respect to its affairs that they might reasonably expect; or

f. the SFC decides to provide assistance to regulators outside Hong Kong under section 186 in relation to an investigation which relates to the corporation.

Definition of auditor

11. Auditor is defined in the Securities and Futures (Miscellaneous) Rules, for the purposes of section 179, to mean:

a. a certified public accountant (practising) as defined in the Professional Accountants Ordinance who provides, or provided, services to a listed corporation;

b. any practice unit within the meaning of the Professional Accountants Ordinance, that provides, or provided, services to a listed corporation; or

c. a person appointed (whether or not he remains so appointed) to be an auditor of a listed corporation for the purposes of any enactment of a place outside Hong Kong which imposes on such person responsibilities comparable to those imposed on an auditor by the Companies Ordinance.

3

1.307 (March 04)

Definition of audit working papers

12. Audit working papers are defined in section 178 to mean any record or document prepared by or on behalf of the auditor and any record or document obtained and retained by or on behalf of the auditor, for or in connection with the performance of any of his functions relating to the conduct of any audit of the accounts of a listed corporation.

Informing the client is prohibited

13. An auditor should note that he is obliged to maintain confidentiality in respect of all matters relating to the SFC's investigation and therefore is prohibited from informing the client that the SFC has given a direction to require the production of the audit working papers in respect of the audit of its financial statements. To inform the client is a crime under section 378. Accordingly, the client's prior approval cannot and should not be sought by an auditor.

Production of information in information systems

14. Where any information or matter contained in any record or document required to be produced is recorded otherwise than in a legible form, the powers conferred on the SFC to require the production of the record or document include the power to require the production of a reproduction of the recording of the information or matter in a legible form (section 189).

Auditor to establish policies and procedures

15. It is recommended that given the requirements under section 179, an auditor of a listed corporation should consider establishing his own policies and procedures in relation to the production of audit working papers to the SFC as a risk management practice. A senior partner of the auditor, with professional risk management responsibility, should be the designated partner to deal with the SFC's authorized person and to liaise with the lawyer engaged by the auditor. The designated partner should, where resources permit, not have been involved in the audit of the listed corporation concerned. A direction to require the production of audit working papers should be handled by the designated partner. The authorized person's review of the audit working papers that have been produced should take place in the presence of a representative of an auditor appointed by the designated partner.

16. It is in the best interest of the auditor to cooperate with the SFC in its investigations. Failing that there may be potential reputation risk to the auditor in terms of adverse publicity.

PRODUCTION OF AUDIT WORKING PAPERS

SFC's authorized persons

17. Under section 179(11) the SFC may authorize in writing any person as an authorized person for the purposes of exercising its powers under section 179. A proforma SFC authorization is attached as Appendix 1 to this Guidance.

Grounds for giving a direction

18. Section 179(7) states that the authorized person shall not give any direction under section 179(1)(iv) to an auditor to require the production of any record or document concerning a listed corporation unless the authorized person has reasonable cause to believe, and the SFC certifies in writing that the authorized person has reasonable cause to believe, that the auditor is in possession of any record or document, which is in the nature of audit working papers, relating to the affairs of a listed corporation and is relevant to the consideration of whether there has been occurrence of the circumstances set out in section 179(1) (see paragraph 10 above). Accordingly, a direction will not be given by the authorized person without reasonable suspicion and the auditor can therefore be satisfied that the SFC's enquiries will have real substance and focus.

4

1.307 (September 04)

19. The SFC has indicated that as a matter of practice, for mutual convenience, the authorized person

will issue a letter, preceding a direction, granting an auditor a choice to produce audit working papers either at the auditor's office or the SFC's office. If an auditor elects to produce the audit working papers at his office, it is a condition that the auditor agrees to keep the audit working papers in secured facilities at the auditor's office, which must be under the control of the designated partner. The auditor must also agree to continue to keep the audit working papers in the secured facilities until being advised by the authorized person that he is no longer required to keep the audit working papers in the secured facilities. A time period will be set by the authorized person for the auditor to respond. If the auditor does not respond by the time set, the authorized person will give a direction to require the production of the audit working papers at the SFC's office. A proforma SFC letter preceding a direction under section 179(1)(iv) to require the production of audit working papers is attached as Appendix 2 to this Guidance.

20. The proforma SFC letter in Appendix 2 indicates that the SFC reserves its statutory right to take possession of the original audit working papers at any time it considers necessary. However, section 179(2)(a)(i) only states that a power to require the production of any record or document by any person includes the power to make copies or otherwise record details of the record or document. The HKICPA is therefore of the view that the SFC does not have the statutory power to take possession of the original audit working papers in the absence of a valid search warrant. As a matter of practice, the SFC has indicated that it recognizes the inconvenience caused to an auditor of having his original audit working papers in the SFC's custody and usually requires the production of the original audit working papers and then takes and retains copies. The SFC has indicated that it will not bear the cost of photocopies. An auditor should note that it is necessary to maintain control of the audit working papers to ensure their continued integrity. Accordingly, an auditor should at all times retain control over the original audit working papers.

21. A SFC certificate under section 179(7) that an authorized person has reasonable cause to believe that an auditor is in possession of audit working papers is issued by a delegate of the SFC, who is of the rank of Associate Director of Enforcement or above. A proforma SFC certificate is attached as Appendix 3 to this Guidance.

22. Based on the decision made by an auditor as to where he will produce the audit working papers in his response to the SFC's letter preceding a direction mentioned in paragraph 19 above, the authorized person takes either of the following steps:

a. issues a covering letter (Appendix 4(a)), normally addressed to the senior partner of an auditor, enclosing a direction (Appendix 4(b)) to require the production of audit working papers at the auditor's office; or

b. issues a covering letter (Appendix 5(a)), normally addressed to the senior partner of the auditor, enclosing a direction (Appendix 5(b)) to require the production of audit working papers at the SFC's office.

23. In the SFC's covering letter enclosing the direction, the authorized person will also attach the following documents:

a. the SFC authorization letter under section 179(11) (Appendix 1);

b. the SFC certificate under section 179(7) (Appendix 3);

c. a copy of section 179; and

d. a copy of the SFC's Personal Information Collection Statement (Appendix 10).

5

1.307 (September 04)

Implications of being served with a direction

24. An auditor should note that a direction given by an authorized person has serious implications. There is effectively no option but to comply since non-compliance without reasonable excuse constitutes a criminal offence. The authorized person wants to exercise the powers conferred promptly and in some cases immediately and accordingly, an auditor should treat the matter with prompt attention and importance.

25. An auditor who complies with a requirement under any provisions of the SFO, including section 179, shall not incur any civil liability, whether arising in contract, tort, defamation, equity or otherwise, to any person by reason only of that compliance (section 380(3)).

26. Penalties in the form of fines and/or imprisonment may be imposed on an auditor if it is found that the auditor:

a. without reasonable excuse fails to comply with a requirement imposed on him by the authorized person (section 179(13));

b. who in purported compliance with a requirement imposed on him produces any record or document or provides or makes an explanation or statement which is false or misleading in a material particular and knows that or is reckless as to whether the record or document or the explanation or statement is false or misleading in a material particular (section 179(14)); or

c. who with intent to defraud, fails to comply with a requirement imposed on him or in purported compliance with a requirement imposed produces any record or document or provides or makes an explanation or statement which is false or misleading in a material particular (section 179(15)).

27. An auditor should note that he is assisting SFC's investigation of a listed corporation. However, an auditor should be aware that should the authorized person come across any alleged misconduct of the auditor, the SFC is permitted under section 378 to disclose such alleged misconduct to the HKICPA or the relevant law enforcement agencies.

Response to SFC's direction

28. When an auditor is given a direction, as described in paragraph 22 above, by the authorized person to require the production of audit working papers, the auditor is recommended to take the following initial steps promptly before producing the audit working papers:

a. check to ensure that the SFC certificate and direction given are in accordance with the legislation (for general guidance, see the SFC's proforma certificate (Appendix 3) and direction (Appendix 4(b) or 5(b))), and seek legal advice; and

b. once the validity of the SFC certificate and direction are established after seeking legal advice:

i. establish the scope of the direction and the client group companies involved, and apply the auditor's policies and procedures; and

ii. consider promptly establishing a dialogue with the authorized person in order to get a better understanding of what the investigation relates to with a view to minimizing the disruption caused to the auditor.

29. The SFC has indicated that, if a suitable dialogue is established promptly, the authorized person will be reasonable in allowing sufficient time for an auditor to comply if valid reasons exist. An auditor should note that what are considered to be valid reasons will be determined by the authorized person on a case by case basis.

6

1.307 (March 04)

a. sets forth the auditor's understanding of the purpose for which the production of audit

b. describes the audit process and the limitations inherent in a financial statement audit;

c. explains the purpose for which the audit working papers were prepared, and that any

d. states that the audit was not planned or conducted in contemplation of the purpose for which

e. states that the audit and the audit working papers do not supplant other inquiries and

f. requests the authorized person, where circumstances permit, to put as many questions as

An auditor should issue the letter promptly, preferably while establishing a dialogue with the

31. An auditor may wish to obtain a signed acknowledgment copy of the letter as evidence of the SFC's

Requirement for the production of audit working papers before audit has been completed

32. The authorized person may give a direction to require the production of the audit working papers

a. additional information may be added as a result of further tests and review by supervisory

b. any audit results and conclusions reflected in the incomplete audit working papers may

Letter to the SFC prior to producing audit working papers

30. An audit performed in accordance with Statements of Auditing Standards is not planned or conducted in contemplation of being used by the SFC in its investigation and therefore may not be suitable for the purpose of the SFC's investigation. To avoid any misunderstanding, once an auditor establishes that the direction to require the production of audit working papers is valid, before or in the course of producing the audit working papers, he may wish to issue a letter to the authorized person that:

working papers is being required;

individual conclusions must be read in the context of the auditor's report on the financial statements;

the production of audit working papers is being granted or to assess the client's compliance with laws and regulations;

procedures that are to be undertaken by the SFC for its purposes; and

possible to the auditor in writing. This will minimize the disruption caused to the auditor. However, the auditor should note that the SFC has indicated that it does have the statutory powers to demand oral questioning as the SFC considers this to be a more effective method of obtaining information and the method that it will usually employ.

authorized person. However, the letter should not slow down the process of complying with the direction.

receipt of the letter. An acknowledgement cannot, however, be a precondition to complying with the direction. An example of a letter containing the elements described above is attached as Appendix 11 to this Guidance.

before the audit has been completed and the auditor's report released. In such circumstances an auditor should note that, when the audit has not been completed, the audit working papers are necessarily incomplete because:

personnel; and

change.

7

1.307 (September 04)

33. If a direction is given to require the production of audit working papers prior to completion of the

audit, an auditor should consider issuing the letter attached as Appendix 11 to this Guidance, appropriately modified, and including an additional paragraph along the following lines: " We have been engaged to audit the financial statements of XYZ Holdings Limited for the year ended [date] in accordance with Statements of Auditing Standards issued by the Hong Kong Institute of Certified Public Accountants, but have not yet completed our audit. Accordingly, at this time we do not express any opinion on the company's financial statements. Furthermore, the contents of the audit working papers may change as a result of additional audit procedures and review of the audit working papers by supervisory personnel of our firm. Accordingly, our audit working papers are incomplete."

EXPLANATIONS OF AUDIT WORKING PAPERS PRODUCED

Power to require to provide explanations of audit working papers that have been produced - sections 179(2), (3) and (4)

34. The authorized person is empowered under section 179(2) to require an auditor to provide or make any explanation or statement in respect of the audit working papers that have been produced (including, in so far as applicable, a description of the circumstances under which they were prepared or created, details of all instructions given or received in connection with them, and an explanation of the reasons for the making of entries contained in them or the omission of entries from them). It is expected that the authorized person's requests for explanation will usually relate to the audit engagement. If the auditor is in any doubt as to the acceptability of any question put to him by the authorized person, he should consider taking legal advice.

35. The SFC has indicated that it will do its best to ensure that the authorized person is sufficiently qualified to be able to understand what he is being given. In return, it is expected that an auditor will do his utmost to explain matters in clear and simple terms to the authorized person.

36. The authorized person either gives a direction to require an auditor to provide explanations orally at a meeting of the audit working papers that have been produced or gives a direction to require an auditor to provide explanations in writing of the audit working papers that have been produced. Accordingly, the authorized person takes either of the following steps:

a. issues a covering letter (Appendix 6(a)), normally addressed to the senior partner of an auditor, enclosing a direction (Appendix 6(b)) to require the auditor to explain orally at a meeting the audit working papers that have been produced. If any of the audit working papers are missing, the auditor is required to state where they are. The meeting will take place either at the SFC's offices or the auditor's; or

b. issues a covering letter (Appendix 7(a)), normally addressed to the senior partner of an auditor, enclosing a direction (Appendix 7(b)) to require the auditor to explain in writing the audit working papers that have been produced. If any of the audit working papers are missing, the auditor is required to state in writing where they are.

37. In the SFC's covering letter enclosing the direction, the authorized person will also attach the following documents:

a. the SFC authorization letter under section 179(11) (Appendix 1);

b. a copy each of section 179 and section 187; and

c. a copy of the SFC's Personal Information Collection Statement (Appendix 10).

38. In relation to a direction given by the authorized person to require an auditor to provide explanations in writing, it is recommended that all written explanations should be provided to the authorized person via the designated partner.

8

1.307 (March 04)

39. In relation to a direction given by the authorized person to require an auditor to provide explanations

orally, where the authorized person considers that a particular member of the audit team is the suitable person to provide the explanation, an auditor would normally cooperate with the authorized person in arranging for that member of the audit team to be interviewed by the authorized person.

40. An auditor should note that in the event that an employee of the auditor is the suitable person to provide the explanation, the authorized person normally also gives a direction under section 179(1)(v) to that employee (see Part III below). In such circumstances an auditor should seek the permission of the authorized person if he wishes to contact the employee. Obtaining the authorized person's permission before contacting the employee is important in order to prevent any inadvertent breaches of confidentiality and secrecy provisions. The SFC has indicated that the authorized person will in most instances grant permission to an auditor to contact his employee.

41. An auditor should note that whatever explanation is given to the authorized person, whether orally or in writing, could have very serious consequences if litigation against the auditor ensues as any statement or other document produced is likely to be disclosed on discovery in subsequent litigation. However, the SFC has indicated that the likelihood of disclosure by the SFC in any potential litigation against an auditor is small. Under section 378, an authorized person is under an obligation to keep all the materials obtained in the course of performing his functions in strict confidence, as are all SFC staff. Accordingly, except for those disclosures permitted by section 378 (all for proper law enforcement or regulatory purposes), the SFC will not disclose any materials to any third party. Likewise, in any civil litigation in which a third party requests the discovery of documents or explanations from the SFC, the SFC will, to the extent it is legally able, resist that request. This is an area where an auditor should seek legal advice.

42. The SFC has indicated that there are presently 3 common methods of recording interviews:

a. by long hand recording;

b. by video; and

c. by audio tape.

The authorized person elects one of the forms of interview. Whilst the authorized person will attempt to accommodate requests for a specified form of interview it may not always be possible. An auditor should consider making a request for a copy of the records of the interview. However, the authorized person may not always be able to furnish a copy immediately due to the need to preserve secrecy and protect the integrity of the investigation.

43. The authorized person may in writing require an auditor providing or making an explanation or statement to verify within a reasonable period specified in the requirement the explanation or statement by statutory declaration, which may be taken by the authorized person (section 179(3)).

44. If an auditor does not provide or make an explanation or statement in accordance with a requirement under section 179 for the reason that the explanation or statement was not within the auditor's knowledge or in the auditor's possession, the authorized person may in writing require the auditor to verify within a reasonable period specified in the requirement by statutory declaration, which may be taken by the authorized person, that the auditor was unable to comply or fully comply (as the case may be) with the requirement for that reason (section 179(4)).

9

1.307 (March 04)

PART III - DIRECTION GIVEN BY THE SFC TO AN EMPLOYEE OF AN AUDITOR UNDER SECTION 179(1)(v)

INTRODUCTION

45. Under section 179(1)(v) an authorized person is empowered to give a direction to any other person requiring the production, within the time and at the place specified in the direction, of any record and document concerning a listed corporation which is under investigation by the SFC. The authorized person can exercise this power in respect of any of the circumstances set out in section 179(1) (see paragraph 10 above). Under section 179(2), a power to require the production of any record or document by any person includes the power to require the person to provide or make any explanation or statement in respect of the record or document.

GROUNDS FOR GIVING A DIRECTION

46. Section 179(8) states that the authorized person shall not give any direction under section 179(1)(v) to a person to require the production of any record or document unless the authorized person has reasonable cause to believe, and the SFC certifies in writing that the authorized person has reasonable cause to believe, that:

a. the person has dealt or has had dealings, directly or indirectly, with, or is otherwise in possession of any record or document relating to the affairs of a listed corporation; and

b. the record or document required to be produced under the direction relates to the affairs of a listed corporation or to a transaction with a listed corporation and cannot be obtained from the listed corporation, a related company of the listed corporation, its bankers or the auditor.

47. If the authorized person, in the course of exercising his powers under section 179(1)(iv), and after discussion with the auditor's designated partner, finds that an employee of the auditor is the suitable person to provide the explanation on certain audit working papers, the authorized person will issue a direction under section 179(1)(v) to the employee to require him to produce the audit working papers and provide explanations of them.

RESPONSE TO SFC'S DIRECTION

48. In giving a direction under section 179(1)(v) to an employee of an auditor, the authorized person will normally attach it to a covering letter together with the SFC authorization under section 179(11) and the SFC certificate under section 179(8). An employee of an auditor should ensure that the SFC authorization, certificate and direction given are in accordance with the legislation. For general guidance, see the SFC's proforma authorization (Appendix 1), certificate (Appendix 8) and direction (Appendices 9(a) and 9(b)) as attached to this Guidance.

49. Once the validity of the SFC authorization, certificate and direction given is established, an employee of an auditor should promptly establish a dialogue with the authorized person and get the authorized person's permission to contact the auditor. An employee of an auditor should note that obtaining the authorized person's permission before contacting the auditor is important in order to prevent any inadvertent breaches of confidentiality and secrecy provisions. The SFC has indicated that the authorized person will grant permission to an employee of an auditor to contact the auditor in order to obtain the relevant audit working papers for production to the authorized person. The SFC has also indicated that, in accordance with its practice to generally allow the auditor to keep the original documents, the auditor will, after the meeting to explain the documents, be allowed to retain the originals of those documents produced by the employee for the purpose of the meeting to explain them. The SFC will allow the auditor's designated partner to attend the interview for this purpose, but, in any event, the employee's lawyer can also do this.

10

1.307 (March 04)

50. Once the permission of the authorized person is obtained to contact an auditor, an employee of an auditor may wish to contact the auditor and provide the auditor with a copy of the covering letter received from the authorized person together with its enclosures of the SFC authorization, certificate and direction. Unless the employee has his own lawyer, it would be advisable for an employee of an auditor to request the auditor to provide the assistance of the auditor's lawyer.

51. An employee of an auditor should also note that certain guidance provided in Part II of this Guidance is also relevant to him, in particular paragraphs 13, 24 to 27, 34, 35, and 39 to 44.

PART IV - RELEVANT PROVISIONS OF THE SFO REQUIRING THE ATTENTION OF THOSE WHO HAVE BEEN GIVEN A DIRECTION BY

THE SFC UNDER SECTION 179(1)(iv) OR 179(1)(v)

INTRODUCTION

52. The following provisions of the SFO are considered relevant to an auditor being given a direction under section 179(1)(iv) or an employee of an auditor being given a direction under section 179(1)(v):

• Application to Court of First Instance relating to non-compliance • Use of incriminating evidence in proceedings

• Lien claimed on records or documents

• Magistrate's warrants

• Destruction of documents

APPLICATION TO COURT OF FIRST INSTANCE RELATING TO NON- COMPLIANCE

53. If an auditor or an employee of an auditor fails to do anything upon being required to do so by the authorized person, the authorized person may, by originating summons or originating motion, make an application to the Court of First Instance in respect of the failure, and the Court may inquire into the case. If the Court is satisfied that there is no reasonable excuse for the auditor or the employee of the auditor not to comply with the requirement, the Court may order the auditor or employee of the auditor to comply with the requirement within the period specified by the Court; and if the Court is satisfied that the failure was without reasonable excuse, punish the auditor or the employee of the auditor, and any other person knowingly involved in the failure, in the same manner as if the auditor or the employee of the auditor and where applicable, that other person had been guilty of contempt of court (section 185).

USE OF INCRIMINATING EVIDENCE IN PROCEEDINGS

54. An auditor or an employee of an auditor is not excused from complying with a requirement imposed on the auditor or the employee of the auditor under section 179(1)(iv) or 179(1)(v) only on the ground that to do so might tend to incriminate the auditor or the employee of the auditor. However, if the auditor or the employee of the auditor claims before providing or making the explanation or statement under the requirement that to do so might incriminate the auditor or the employee of the auditor, section 187 provides that the explanation or statement provided shall not be admissible in evidence against the auditor or the employee of the auditor in criminal proceedings in a court of law other than those in which the auditor or the employee of the auditor is charged with an offence under section 179(13), (14) or (15) or 184, or under section 219(2)(a), 253(2)(a) or 254(6)(a) or (b), or under Part V of the Crimes Ordinance, or for perjury. The auditor or the employee of the auditor, where applicable, should seek legal advice as to how the claim would be made, before providing the explanation or statement.

11

1.307 (March 04)

LIEN CLAIMED ON RECORDS OR DOCUMENTS

55. Where an auditor or an employee of an auditor in possession of any record or document required to be produced claims a lien on the record or document, the requirement to produce the record or document shall not be affected by the lien, no fees shall be payable for the production and the production shall be without prejudice to the lien (section 188).

MAGISTRATE'S WARRANTS

56. If a magistrate is satisfied on information on oath laid by the authorized person that there are reasonable grounds to suspect that there is, or is likely to be, on premises specified in the information any record or document which may be required to be produced, the magistrate may issue a warrant authorizing a person specified in the warrant, a police officer, and such other persons as may be necessary to assist in the execution of the warrant to enter the premises so specified, if necessary by force, at any time within the period of 7 days beginning on the date of the warrant and search for, seize and remove any record or document which may be required to be produced (section 191).

DESTRUCTION OF DOCUMENTS

57. An auditor or an employee of an auditor commits an offence if he destroys, falsifies, conceals or otherwise disposes of, or causes or permits the destruction, falsification, concealment or disposal of, any record or document required to be produced. Penalties for this offence carry fines and imprisonment (section 192).

12

1.307 (September 04)

APPENDICES

The proforma documents set out in Appendices 1 - 9 were provided to the HKICPA by the SFC. These are examples of the typical documents the SFC will issue to exercise its powers under section 179. Those issued by the SFC in particular cases may vary.

Appendix 1 - Proforma SFC authorization under section 179(11)

Appendix 2 - Proforma SFC letter preceding a section 179(1)(iv) direction to require the production of audit working papers

Appendix 3 - Proforma SFC certificate under section 179(7) in relation to a direction to an auditor under section 179(1)(iv)

Appendix 4(a) - Proforma SFC covering letter to the auditor to require the production of audit working papers at the auditor's office

Appendix 4(b) - Proforma SFC direction to the auditor to require the production of audit working papers at the auditor's office

Appendix 5(a) - Proforma SFC covering letter to the auditor to require the production of audit working papers at the SFC's office

Appendix 5(b) - Proforma SFC direction to the auditor to require the production of audit working papers at the SFC's office

Appendix 6(a) - Proforma SFC covering letter to the auditor to require to provide or make any explanation or statement of audit working papers orally at a meeting

Appendix 6(b) - Proforma SFC direction to the auditor to require to provide or make any explanation or statement of audit working papers and state where they are, orally at a meeting

Appendix 7(a) - Proforma SFC covering letter to the auditor to require to provide or make any explanation or statement of audit working papers in writing

Appendix 7(b) - Proforma SFC direction to the auditor to require to provide or make any explanation or statement of audit working papers and state where they are in writing

Appendix 8 - Proforma SFC certificate under section 179(8) in relation to a direction to an employee under section 179(1)(v)

Appendix 9(a) - Proforma SFC covering letter to the employee to require the production of audit working papers and to provide or make any explanation or statement of audit working papers and state where they are at a meeting

Appendix 9(b) - Proforma SFC direction to the employee to require the production of audit working papers and to provide or make any explanation or statement of audit working papers and state where they are at a meeting

Appendix 10 - SFC's Personal Information Collection Statement

Appendix 11 - Example letter issued by an auditor to the SFC before producing audit working papers

13

1.307 (March 04)

Appendix 1 - Proforma SFC authorization under section 179(11)

[SFC's letterhead]

Authority to require production of records and documents under section 179 of

the Securities and Futures Ordinance (Cap. 571)

I am a delegate of the Securities and Futures Commission.

It appears to me that there are circumstances suggesting that:

• At any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members.

I authorize you, Chan Tai Man, as an authorized person for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above.

As an authorized person, you may give direction to:

• XYZ Holdings Limited; • a corporation that is or was at the material time a related corporation of XYZ Holdings Limited; • an authorized financial institution; • an auditor; or • any other person

to require production of any records and documents specified by you.

Your power to require the production of any record or document by any person includes the power:

• to make copies or record details of any record or document produced to you; • to require the person, or any person who is or was an officer or employee of a corporation to

explain it to you, or make a statement explaining it to you; • if a record or document is not produced, to require the person or any person who is or was an

officer or employee of a corporation to state where it is; and • to require any person who explains a record or document or states where a record or document is, to

verify their explanation or statement by a statutory declaration.

Dated this 1st April 2003

Eric Cheng Senior Director of Enforcement Securities and Futures Commission

14

1.307 (March 04)

Appendix 2 - Proforma SFC letter preceding a section 179(1)(iv) direction to require the production of audit working papers

[SFC's Letterhead]

Confidential

Urgent

By fax (1234 5678) & By Hand

1 April 2003 Our Ref: 888/EN/88 ABC & Co. Certified Public Accountants [Address] Attn : Mr. ABC - Senior Partner

Dear Sirs

Section 179 Inquiry - Direction to produce records and documents

The Securities and Futures Commission is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am authorized for the purposes of section 179 of the Securities and Futures Ordinance.

I will shortly be issuing a direction to your firm for production of records and documents in connection with your audit engagement with XYZ Holdings Limited.

Before doing that, we are as a matter of practice for our mutual convenience willing to grant you a choice to:

a. produce to me the originals of the records or documents specified in the direction at the offices of the Securities and Futures Commission; or

b. produce to me the originals of the records or documents at your offices.

You must let us know by the close of business of 7 April 2003 which you wish to choose. If we do not hear from you by then, we will issue a direction to produce at our offices. If you elect to produce the records and documents to me at your offices, this is upon condition that you agree to keep them in secured facilities at your office, which must be under the control of a designated partner of your firm who has no involvement in your audit engagement with XYZ Holdings Limited. I and/or other authorized persons will attend your offices to inspect, make copies or otherwise record details of the records and documents upon prior notice, which will usually be 48 hours, but may be less if we feel the circumstances warrant it. You must agree to continue to keep the records and documents in the secured facilities until further notice as we may wish to inspect the documents again. We will inform you when you are no longer required to keep the records and documents in the secured facilities. We reserve our statutory right to take possession of the originals at any time we consider necessary.

15

1.307 (March 04)

Please have the appropriate partner in your firm call me to discuss the precise arrangements for this matter. My number is 2842-7666. I look forward to hearing from you. Yours faithfully Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

16

1.307 (March 04)

Appendix 3 - Proforma SFC certificate under section 179(7) in relation to a direction to an auditor under section 179(1)(iv)

[SFC's Letterhead]

Certificate under section 179(7) of the Securities and Futures Ordinance (Cap. 571)

I am a delegate of the Securities and Futures Commission. I certify that Chan Tai Man has reasonable cause to believe that:

1. you are in possession of records or documents, which are in the nature of audit working papers, relating to the affairs of XYZ Holdings Limited to which any direction has been or may be given under section 179(1)(i) or (ii) of the Ordinance; and

2. the records or documents required to be produced in this direction relate to the affairs of XYZ Holdings Limited and its related corporations, and are relevant to the consideration of whether there has been the occurrence of defalcation, fraud, misfeasance or other misconduct engaged by the persons involved in the management of the affairs of XYZ Holdings Limited, towards it or its members or any part of its members.

Dated: 1 April 2003 Richard Chow Director of Enforcement Securities and Futures Commission

17

1.307 (March 04)

Appendix 4(a) - Proforma SFC covering letter to the auditor to require the production of audit working papers at the auditor's office

[SFC's Letterhead]

Confidential

Urgent By fax (1234 5678) & By Hand 1 April 2003 Our Ref: 888/EN/88 ABC & Co. Certified Public Accountants [Address] Attn : Mr. ABC - Senior Partner Dear Sirs Section 179 Inquiry - Direction to produce records and documents The Securities and Futures Commission ("Commission") is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am authorized for the purposes of section 179 of the Securities and Futures Ordinance. A copy of my authorization is enclosed. At the same time as you receive this letter I will serve you with a direction under section 179 of the Securities and Futures Ordinance to produce records and documents. I enclose a copy of section 179 of the Securities and Futures Ordinance, for your information. If you have any questions, please call me on 2842-7666. You must comply with this direction Please note that if you do not comply with this direction to produce records and documents, or you give us false or misleading information, you may commit an offence under section 179(13), (14) or (15) of the Securities and Futures Ordinance. This inquiry is confidential When you answer this direction, you are a person assisting the Commission in the performance of its functions. Section 378 of the Securities and Futures Ordinance imposes obligations of secrecy upon you. You must not disclose anything about this inquiry to anyone. It is a criminal offence to fail to comply with section 378. Please note, however, that you may consult a lawyer about this request without breaching your obligation of secrecy.

18

1.307 (March 04)

The Personal Data (Privacy) Ordinance Your answers to this direction may include personal data as defined in the Personal Data (Privacy) Ordinance. This Ordinance authorizes the Commission to collect and use personal data to perform its functions as a financial regulator. In this regard, we draw your attention to the attached Personal Information Collection Statement which sets out the Commission's policies and practices with regard to any personal data provided by you to us. Yours faithfully Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

Enc. s.179 Direction and Certificate s.179 Authority a copy of s.179 of the Securities and Futures Ordinance SFC's Personal Information Collection Statement

19

1.307 (March 04)

Appendix 4(b) - Proforma SFC direction to the auditor to require the production of audit working papers at the auditor's office

[SFC's Letterhead]

Direction to produce records and documents under section 179 of the Securities and Futures Ordinance (Cap. 571)

To: ABC & Co. Certified Public Accountants [Address]

Date: 1 April 2003

It appears to Eric Cheng, as delegate of the Securities and Futures Commission, that there are circumstances suggesting that at any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members. Mr. Eric Cheng has authorized me for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above. A copy of my authority is attached to this direction. I have reasonable cause to believe that:

1. you are in possession of records or documents, which are in the nature of audit working papers, relating to the affairs of XYZ Holdings Limited to which any direction has been or may be given under section 179(1)(i) or (ii) of the Ordinance; and

2. the records or documents required to be produced in this direction relate to the affairs of XYZ Holdings Limited and its related corporation, and are relevant to the consideration of whether there has been the occurrence of defalcation, fraud, misfeasance or other misconduct engaged by the persons involved in the management of the affairs of XYZ Holdings Limited, towards it or its members or any part of its members.

I require you to produce the following records and documents:

• the audit working papers relating to the affairs of XYZ Holdings Limited (including all correspondence and notes of meeting/discussion with the employees, management and the board of directors of XYZ Holdings Limited) for the period(s) [ ].

You must produce the above records and documents at your offices at:

[Address]

on 8 April 2003. Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

20

1.307 (March 04)

Appendix 5(a) - Proforma SFC covering letter to the auditor to require the production of audit working papers at the SFC's office

[SFCs Letterhead]

Confidential

Urgent By fax (1234 5678) & By Hand 1 April 2003 Our Ref: 888/EN/88 ABC & Co. Certified Public Accountants [Address] Attn : Mr. ABC - Senior Partner Dear Sirs Section 179 Inquiry - Direction to produce records and documents The Securities and Futures Commission ("Commission") is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am authorized for the purposes of section 179 of the Securities and Futures Ordinance. A copy of my authorization is enclosed. At the same time as you receive this letter I will serve you with a direction under section 179 of the Securities and Futures Ordinance to produce records and documents. I enclose a copy of section 179 of the Securities and Futures Ordinance, for your information. If you have any questions, please call me on 2842-7666. You must comply with this direction

Please note that if you do not comply with this direction to produce records and documents, or you give us false or misleading information, you may commit an offence under section 179(13), (14) or (15) of the Securities and Futures Ordinance.

This inquiry is confidential

When you answer this direction, you are a person assisting the Commission in the performance of its functions. Section 378 of the Securities and Futures Ordinance imposes obligations of secrecy upon you. You must not disclose anything about this inquiry to anyone. It is a criminal offence to fail to comply with section378.

Please note, however, that you may consult a lawyer about this request without breaching your obligation of secrecy.

21

1.307 (March 04)

The Personal Data (Privacy) Ordinance

Your answers to this direction may include personal data as defined in the Personal Data (Privacy) Ordinance. This Ordinance authorizes the Commission to collect and use personal data to perform its functions as a financial regulator. In this regard, we draw your attention to the attached Personal Information Collection Statement which sets out the Commission's policies and practices with regard to any personal data provided by you to us. Yours faithfully Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

Enc. s.179 Direction and Certificate s.179 Authority a copy of s.179 of the Securities and Futures Ordinance SFC's Personal Information Collection Statement

22

1.307 (March 04)

Appendix 5(b) - Proforma SFC direction to the auditor to require the production of audit working papers at the SFC's office

[SFC's Letterhead]

Direction to produce records and documents

under section 179 of the Securities and Futures Ordinance (Cap. 571)

To: ABC & Co. Certified Public Accountants [Address]

Date: 1 April 2003

It appears to Eric Cheng, as delegate of the Securities and Futures Commission, that there are circumstances suggesting that at any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members. Mr. Eric Cheng has authorized me for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above. A copy of my authority is attached to this direction. I have reasonable cause to believe that:

1. you are in possession of records or documents, which are in the nature of audit working papers, relating to the affairs of XYZ Holdings Limited to which any direction has been or may be given under section 179(1)(i) or (ii) of the Ordinance; and

2. the records or documents required to be produced in this direction relate to the affairs of XYZ Holdings Limited and its related corporation, and are relevant to the consideration of whether there has been the occurrence of defalcation, fraud, misfeasance or other misconduct engaged by the persons involved in the management of the affairs of XYZ Holdings Limited, towards it or its members or any part of its members.

I require you to produce the following records and documents:

• the audit working papers relating to the affairs of XYZ Holdings Limited (including all correspondence and notes of meeting/discussion with the employees, management and the board of directors of XYZ Holdings Limited) for the period(s) [ ].

You must produce the above records and documents at the SFC's office at:

8/F Chater House 8 Connaught Road Central Hong Kong

by 8 April 2003. Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

23

1.307 (March 04)

Appendix 6(a) - Proforma SFC covering letter to the auditor to require to provide or make any explanation or statement

of audit working papers orally at a meeting

[SFC's Letterhead]

Confidential Urgent By fax (1234 5678) & By hand 1 April 2003 Our Ref: 888/EN/88 ABC & Co. Certified Public Accountants [Address] kl Attn : Mr. ABC - Senior Partner Dear Sirs Section 179 Inquiry - Direction for an explanation or statement The Securities and Futures Commission ("Commission") is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am authorized for the purposes of section 179 of the Securities and Futures Ordinance. A copy of my authorization is enclosed. Enclosed with this letter is a direction under section 179 of the Securities and Futures Ordinance to explain the audit working papers that have been produced and if any of the audit working papers are missing, to state where they are. Please meet with us at 2:30 p.m. on 8 April 2003 to give us your explanation and statement. The meeting will be at: The Securities and Futures Commission

8/F Chater House 8 Connaught Road Central Hong Kong

I enclose a copy of sections 179 and 187 of the Securities and Futures Ordinance, for your information. Please read these sections before you attend this meeting. If you have any questions, please call me on 2842-7666. You must comply with this direction

Please note that if you do not comply with this direction you may commit an offence under section 179(13), (14) or (15) of the Securities and Futures Ordinance.

24

1.307 (March 04)

Use of incriminating evidence in proceedings You must give us your explanation or statement, but section 187(2) of the Securities and Futures Ordinance limits the admissibility in evidence of our requirement and your explanation or statement if your explanation and statement might tend to incriminate you. If, before you provide or make your explanation or statement, you claim that your explanation or statement might tend to incriminate you, then the requirement and your explanation or statement will not be admissible in evidence against you in criminal proceedings except proceedings in respect of your explanation or statement for:

• an offence under sections 179(13), (14) or (15), or section 184 of the Securities and Futures Ordinance,

• an offence under section 219(2)(a), section 253(2)(a) or section 254(6)(a) or (b) of the Securities and Futures Ordinance,

• an offence under Part V of the Crimes Ordinance (Cap. 200); or • perjury.

This inquiry is confidential When you comply with this direction, you are a person assisting the Commission in the performance of its functions. Section 378 of the Securities and Futures Ordinance imposes obligations of secrecy upon you. You must not disclose anything about this inquiry to anyone. It is a criminal offence to fail to comply with section 378. Please note, however, that you may consult a lawyer about this request without breaching your obligation of secrecy. The Personal Data (Privacy) Ordinance Your answers to this direction may include personal data as defined in the Personal Data (Privacy) Ordinance. This Ordinance authorizes the Commission to collect and use personal data to perform its functions as a financial regulator. In this regard, we draw your attention to the attached Personal Information Collection Statement which sets out the Commission's policies and practices with regard to any personal data provided by you to us. Yours faithfully Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

Enc. s.179 Direction s.179 Authority a copy of sections 179 and 187 of the Securities and Futures Ordinance SFC's Personal Information Collection Statement

25

1.307 (March 04)

Appendix 6(b) - Proforma SFC direction to the auditor to require to provide or make any explanation or statement

of audit working papers and state where they are, orally at a meeting

[SFC's Letterhead]

Direction to explain documents and state where documents are

under section 179 of the Securities and Futures Ordinance (Cap. 571)

To: Mr. ABC ABC & Co. Certified Public Accountants [Address]

Date: 1 April 2003

It appears to Eric Cheng, as delegate of the Securities and Futures Commission ("Commission"), that there are circumstances suggesting that at any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members.

Mr. Eric Cheng has authorized me for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above.

A copy of my authority is attached to this direction.

You are a partner of ABC & Co., auditor of XYZ Holdings Limited.

I require you to provide an explanation of the following records and documents produced to me:

• audit working papers in relation to the audit of XYZ Holdings Limited for the year [ ].

The following documents have not been produced to me. I require you to state where they are:

• correspondence between ABC & Co. and XYZ Holdings Limited in relation to the audit engagement of ABC & Co. with XYZ Holdings Limited.

Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

26

1.307 (March 04)

Appendix 7(a) - Proforma SFC covering letter to the auditor to require to provide or make any explanation or statement

of audit working papers in writing

[SFC's Letterhead]

Confidential Urgent By fax (1234 5678) & By hand 1 April 2003 Our Ref: 888/EN/88 ABC & Co. Certified Public Accountants [Address] Attn : Mr. ABC - Senior Partner Dear Sirs Section 179 Inquiry - Direction for a written explanation or statement The Securities and Futures Commission ("Commission") is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am authorized for the purposes of section 179 of the Securities and Futures Ordinance. A copy of my authorization is enclosed. Enclosed with this letter is a direction under section 179 of the Securities and Futures Ordinance to explain the audit working papers that have been produced and if any of the audit working papers are missing, to state where they are. You must give your written explanation and statement to us by 8 April 2003. I enclose a copy of sections 179 and 187 of the Securities and Futures Ordinance, for your information. If you have any questions, please call me on 2842-7666. You must comply with this direction Please note that if you do not comply with this direction you may commit an offence under section 179(13), (14) or (15) of the Securities and Futures Ordinance. Use of incriminating evidence in proceedings You must give us your explanation or statement, but section 187(2) of the Securities and Futures Ordinance limits the admissibility in evidence of our requirement and your explanation or statement if your explanation and statement might tend to incriminate you. If, before you provide or make your explanation or statement, you claim that your explanation or statement might tend to incriminate you, then the requirement and your explanation or statement will not be admissible in evidence against you in criminal proceedings except proceedings in respect of your explanation or statement for:

27

1.307 (March 04)

• an offence under sections 179(13), (14) or (15), or section 184 of the Securities and Futures Ordinance,

• an offence under section 219(2)(a), section 253(2)(a) or section 254(6)(a) or (b) of the Securities and Futures Ordinance,

• an offence under Part V of the Crimes Ordinance (Cap. 200); or • perjury.

This inquiry is confidential When you comply with this direction, you are a person assisting the Commission in the performance of its functions. Section 378 of the Securities and Futures Ordinance imposes obligations of secrecy upon you. You must not disclose anything about this inquiry to anyone. It is a criminal offence to fail to comply with section 378. Please note, however, that you may consult a lawyer about this matter without breaching your obligation of secrecy. The Personal Data (Privacy) Ordinance Your answers to this direction may include personal data as defined in the Personal Data (Privacy) Ordinance. This Ordinance authorizes the Commission to collect and use personal data to perform its functions as a financial regulator. In this regard, we draw your attention to the attached Personal Information Collection Statement which sets out the Commission's policies and practices with regard to any personal data provided by you to us. Yours faithfully Chan Tai Man Authorized person under section 179 of the

Securities and Futures Ordinance

Enc. s.179 Direction s.179 Authority a copy of sections 179 and 187 of the Securities and Futures Ordinance SFC's Personal Information Collection Statement

28

1.307 (March 04)

Appendix 7(b) - Proforma SFC direction to the auditor to require to provide or make any explanation or statement of audit working papers and state where they are in writing

[SFC's Letterhead]

Direction to give an explanation and make a statement in writing

under section 179 of the Securities and Futures Ordinance (Cap. 571)

To: Mr. ABC ABC & Co. Certified Public Accountants [Address]

Date: 1 April 2003

It appears to Eric Cheng, as delegate of the Securities and Futures Commission, that there are circumstances suggesting that at any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members. Mr. Eric Cheng has authorized me for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above. A copy of my authority is attached to this direction. You are a partner of ABC & Co., auditor of XYZ Holdings Limited. I require you to provide an explanation in writing of the following records and documents produced to me:

• with respect to the supporting documents for the transactions between XYZ Holdings Limited and Crook Company Limited in the financial year [ ], why did ABC & Co. in note 1 of the audit report state that "ABC & Co. have not been provided with adequate transaction records for all the transactions between XYZ and Crook".

The following documents have not been produced to me. I require you to state in writing where they are:

• correspondence between ABC & Co. and XYZ Holdings Limited in relation to the audit engagement of ABC & Co. with XYZ Holdings Limited.

You must send your explanation and statement to me at:

The Securities and Futures Commission 8/F Chater House 8 Connaught Road Central Hong Kong

by 8 April 2003. Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

29

1.307 (March 04)

Appendix 8 - Proforma SFC certificate under section 179(8) in relation to a direction to an employee under section 179(1)(v)

[SFC's Letterhead]

Certificate

under section 179(8) of the Securities and Futures Ordinance (Cap. 571)

I am a delegate of the Securities and Futures Commission.

I certify that Chan Tai Man has reasonable cause to believe that:

1. you have dealt with or had dealings, directly or indirectly, with, or are otherwise in possession of records or documents relating to the affairs of, XYZ Holdings Limited to which any direction has been or may be given under section 179(1)(i) or (ii) of the Securities and Futures Ordinance; and

2. the records or documents required to be produced in this direction:

a. relate to the affairs of XYZ Holdings Limited, or to a transaction with XYZ Holdings Limited;

b. are relevant to the consideration of whether there has been the occurrence of defalcation, fraud, misfeasance or other misconduct engaged by the persons involved in the management of the affairs of XYZ Holdings Limited, towards it or its members or any part of its members; and

c. cannot be obtained by giving a direction to any other person under subsection (1)(i), (ii), (iii) or (iv) of section 179 of the Securities and Futures Ordinance.

Dated: 1 April 2003

Richard Chow Director of Enforcement Securities and Futures Commission

30

1.307 (March 04)

Appendix 9(a) - Proforma SFC covering letter to the employee to require the production of audit working papers and to provide

or make any explanation or statement of audit working papers and state where they are at a meeting

[SFC's Letterhead]

Confidential

Urgent By hand (To be opened by the addressee only) 1 April 2003 Our Ref: 888/EN/88 Mr. Employ Yee c/o ABC & Co. Certified Public Accountants [Address] Dear Sir Section 179 Inquiry - Direction to produce records and documents and to give an explanation or statement The Securities and Futures Commission ("Commission") is conducting an inquiry under section 179 of the Securities and Futures Ordinance into XYZ Holdings Limited. I am an authorised person for the purposes of section 179 of the Securities and Futures Ordinance. A copy of my authorisation is enclosed. At the same time as you receive this letter I will serve you with a direction under section 179 of the Securities and Futures Ordinance to produce records and documents and to explain documents and state the whereabouts of any missing documents. Please meet with us at 2:30 p.m. on 10 April 2003 to give us your explanation and statement. The meeting will be at:

The Securities and Futures Commission 8th Floor, Chater House 8 Connaught Road Central Hong Kong

I enclose a copy of sections 179 and 187 of the Securities and Futures Ordinance for your information. Please read these sections before you attend this meeting.

If you have any questions, please contact me on 2842-7666.

You must comply with this direction

If you do not comply with this direction, or you give us false or misleading information, you may commit an offence under section 179(13), (14) or (15) of the Securities and Futures Ordinance.

31

1.307 (March 04)

Use of incriminating evidence in proceedings

You must give us your explanation or statement, but section 187(2) of the Securities and Futures Ordinance limits the admissibility in evidence of our requirement and your explanation or statement if your explanation or statement might tend to incriminate you.

If, before you provide or make your explanation or statement, you claim that your explanation or statement might tend to incriminate you, then the requirement and your explanation or statement will not be admissible in evidence against you in criminal proceedings except proceedings in respect of your explanation or statement for:

• an offence under section 179(13), (14) or (15), or section 184 of the Securities and Futures Ordinance;

• an offence under section 219(2)(a), section 253(2)(a) or section 254(6)(a) or (b) of the Securities and Futures Ordinance;

• an offence under Part V of the Crimes Ordinance (Cap. 200); or • perjury.

This inquiry is confidential

When you answer this direction, you are a person assisting the Commission in the performance of its functions. Section 378 of the Securities and Futures Ordinance imposes obligations of secrecy upon you. You must not disclose anything about this inquiry to anyone. It is a criminal offence to fail to comply with section 378.

Please note, however, that you may consult a lawyer about this request without breaching your obligation of secrecy. The Personal Data (Privacy) Ordinance

Your answers to this direction may include personal data as defined in the Personal Data (Privacy) Ordinance. This Ordinance authorizes the Commission to collect and use personal data to perform its functions as a financial regulator. In this regard, we draw your attention to the attached Personal Information Collection Statement which sets out the Commission's policies and practices with regard to any personal data provided by you to us.

Yours faithfully

Chan Tai Man Authorized person under section 179 of the Securities and Futures Ordinance

Encl. s. 179 Direction and Certificate s. 179 Authority a copy of sections 179 and 187 of the Securities and Futures Ordinance SFC's Personal Information Collection Statement

32

1.307 (March 04)

Appendix 9(b) - Proforma SFC direction to the employee to require the production of audit working papers and to provide

or make any explanation or statement of audit working papers and state where they are at a meeting

[SFC's Letterhead]

Direction to produce records and documents

under section 179 of the Securities and Futures Ordinance (Cap. 571)

To: Mr. Employ Yee c/o ABC & Co. Certified Public Accountants [Address]

Date: 1 April 2003

It appears to Eric Cheng, as delegate of the Securities and Futures Commission, that there are circumstances suggesting that at any relevant time persons involved in the management of the affairs of XYZ Holdings Limited have engaged, in relation to such management, in defalcation, fraud, misfeasance or other misconduct towards it or its members or any part of its members. Mr Eric Cheng has authorized me for the purposes of section 179 of the Securities and Futures Ordinance in relation to the matters set out above. A copy of my authority is attached to this direction. I have reasonable cause to believe that:

1. you have dealt with or had dealings, directly or indirectly, with, or are otherwise in possession of records or documents relating to the affairs of, XYZ Holdings Limited to which any direction has been or may be given under section 179(1)(i) or (ii) of the Securities and Futures Ordinance ; and

2. the records or documents required to be produced in this direction:

a. relate to the affairs of XYZ Holdings Limited, or to a transaction with XYZ Holdings Limited;

b. are relevant to the consideration of whether there has been the occurrence of defalcation, fraud, misfeasance or other misconduct engaged by the persons involved in the management of the affairs of XYZ Holdings Limited, towards it or its members or any part of its members; and

c. cannot be obtained by giving a direction to any other person under subsection (1)(i), (ii), (iii) or (iv) of section 179 of the Securities and Futures Ordinance.

I require you to produce the following records and documents:

• the audit working papers relating to all the transactions between XYZ Holdings Limited and Crook Company Limited during the period [ ] to [ ].

You must produce the records and documents at the offices of the Securities and Futures Commission, 8th Floor, Chater House, 8 Connaught Road Centre, Hong Kong on 10 April 2003.

33

1.307 (March 04)

I also require you to provide an explanation of the following records and documents:

• the audit working papers relating to all the transactions between XYZ Holdings Limited and Crook Company Limited during the period [ ] to [ ].

The following records or documents have not been produced to me. I require you to state where they are:

• [ ]

Chan Tai Man Authorized person under section 179 of the

Securities and Futures Ordinance

34

1.307 (March 04)

Appendix 10 – SFC's Personal Information Collection Statement

Securities and Futures Commission

Personal Information Collection Statement

1. The Personal Information Collection Statement ("PICS") is made in accordance with the guidelines issued by the Office of the Privacy Commissioner for Personal Data. The PICS sets out the policies and practices of the Securities and Futures Commission ("SFC") with regard to your Personal Data 1.

Purpose of Collection

2. The SFC will use the Personal Data provided by you for one or more of the following purposes:

2.1 to administer the Securities and Futures Ordinance ("SFO"), rules, regulations, codes and guidelines made or promulgated pursuant to the powers vested in the SFC as in force at the relevant time and to carry out its functions as a financial regulator, including:

• to promote, encourage and enforce proper conduct, competence and integrity of persons carrying on activities regulated by the SFC under any of the relevant provisions in the conduct of such activities;

• to supervise, monitor and regulate: (i) the activities carried on by recognized

exchange companies, recognized clearing houses, recognized exchange controllers or recognized investor compensation companies, or by persons carrying on activities regulated by the SFC under any of the relevant provisions; and (ii) such of the activities carried on by registered institutions as required to be regulated by the SFC under any of the relevant provisions;

• to encourage the provision of sound, balanced and informed advice regarding

transactions or activities related to financial products;

• to co-operate with and provide assistance to regulatory authorities or organizations, whether formed or established in Hong Kong or elsewhere;

• to assess the fitness and properness of licensed/registered persons to remain

licensed/registered under the SFO;

• to promote, encourage and enforce the adoption of appropriate internal controls and risk management systems by (i) persons carrying on activities regulated by the SFC; or (ii) registered institutions in the conduct of activities regulated by the SFC, under any of the relevant provisions;

• to suppress illegal, dishonourable and improper practices in the securities and

futures industry;

2.2 for research and statistical purposes; and

2.3 other purposes as permitted by law.

3. Failure to provide the requested Personal Data may result in the SFC being unable to perform its statutory functions under the SFO.

_________________________ 1Personal Data means personal data as defined in the Personal Data (Privacy) Ordinance, Cap 486 ("PDPO")

35

1.307 (March 04)

Transfer/Matching of Personal Data

4. Personal Data may be disclosed by the SFC to other financial regulators in Hong Kong (including the Hong Kong Exchanges and Clearing Limited and the Hong Kong Monetary Authority), government bodies (including the Hong Kong Police and the Independent Commission Against Corruption) and overseas regulatory bodies as required under the law or pursuant to any regulatory/investigatory assistance arrangements between the SFC and other regulators (local/overseas).

5. For the purposes of carrying out its regulatory functions, Personal Data may be disclosed by the SFC to the relevant Courts, Panels, Tribunals and Committees.

6. Personal Data may be used by the SFC and/or disclosed by the SFC to the above organizations/bodies for the purposes of verifying/matching2 those data.

Access to Data

7. You have the right to request access to and correction of your Personal Data in accordance with the provisions of the PDPO. Your right of access includes the right to request a copy of your Personal Data provided to the SFC. The SFC has the right to charge a reasonable fee for processing any data access request.

Enquiries