121002 final the hidden secrets to your property insurance

DESCRIPTION

A Public Adjuster who is licensed and bonded in 2 states shares the secrets to getting a property insurance company to treat you fairly and pay you enough to cover ALL of your covered damage.TRANSCRIPT

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 1

“The Hidden

Secrets to Your

Property

Insurance…

Your Insurance

Company Is Scared to

Death You Will Learn!”

Scott J Melrose

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 2

“The Hidden Secrets to Your Property

Insurance…

Your Insurance Company Is Scared to Death You

Will Learn”

Copyright © 2012 by Scott J Melrose

All rights reserved. No part of this book may be

reproduced or transmitted in any form or by any means

without written permission from the author.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 3

Forward

Scott hit the nail right on the head. As a Real Estate investor, I have to deal with insurance companies all the time. In my experience, they will do everything they can to pay you as little as they can get away with. Scott understands the plight of the homeowner and the business owner when they have damage to their property. He gets you the maximum settlement possible. His book will open the eyes of a lot of people. It’s a shame so many homeowners don’t realize they could and should get more than the insurance company paid them. Bottom line is you should never file an insurance claim without using someone like Scott. Read his book and you will never file a claim without Scott or a Public Adjuster again. Great book thank you.

Paul J Da Costa

Realtor and Real Estate Investor.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 4

Dedication

Thanks to so many people:

- My colleagues and trainers who have taught

me so much;

- The insurance companies who create the

opportunities to make a living by helping

my clients get what they deserve in the first

place;

- My beautiful and wonderful wife Sue for her

support and understanding as I established

myself in this business and wrote this book;

- Most of all, my past, present and future

clients who put their trust in me to get the

insurance companies to treat them fairly and

pay them enough to cover their damages.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 5

TABLE OF CONTENTS

CHAPTER 1 6

WHAT MADE THE DIFFERENCE?

CHAPTER 2 12

“JUST WHAT IS A PUBLIC ADJUSTER ANYWAY?”

CHAPTER 3 16

“WHAT DOES MY POLICY COVER?”

CHAPTER 4 30

“HOW MUCH SHOULD THE Y PAY ME?”

CHAPTER 5 42

“WHAT ABOUT THE REASONS TO NOT CALL A PUBLIC ADJUSTER?”

CHAPTER 6 65

WHAT YOU NEED TO KNOW BEFORE SPENDING ANOTHER DOLLAR ON PROPERTY INSURANCE

CHAPTER 7 79

“WHAT ABOUT MY COMMERCIAL PROPERTY?”

CHAPTER 8 85

“OK HOW DO I CHOOSE MY PUBLIC ADJUSTER?”

CHAPTER 9 90

EPLIOG

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 6

Chapter One

What Made the Difference?

In a nice neighborhood in your

town, two families bought homes on

the same street. The homes and the

families were very much alike.

They were smart, educated, and got

along well with all the other

neighbors.

Their homes were very much

alike as well. In fact, they were

the same model and built in the

same year. Both were tastefully

updated and kept in beautiful

condition.

Then last summer came “the

storm”. Like many other homes,

“the storm” pelted both homes with

large hail and tore off shingles,

siding and fence sections with the

high winds that came with “the

storm”. The damage to each home

was similar as well.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 7

But, there was one big

difference. One of the homeowners

got a check for thousands of

dollars. The other homeowner was

“denied” and received… nothing. In

fact, the second homeowner even

lost their “claim free discount”

just for trying to get the money

they felt they deserved.

Have you ever wondered, just

what makes this kind of difference

in the outcome? It isn’t always

the amount of damage or even that

one has a “good” insurance company

or a “good” agent. In fact, this

happens all the time.

It happens when neighbors have

the same policy with the same

company. It happens when they have

the same agent. It even happens

when the insurance company sends

out the same adjuster on the same

day.

The difference comes from what

people know and how they use that

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 8

knowledge – the hidden secrets to

their policies.

Getting paid fairly for your

damage doesn’t have to be random.

Some people know who to call and

ask to help them. Those fortunate

people get what the insurance

company should pay them. They use

it to get thousands or even tens of

thousands of dollars in

settlements, while neighbors get…

the treatment.

And that is why I am writing

this book about how thousands of

homeowners can benefit by hiring an

advocate to work with their

insurance company. For that is the

whole purpose of the service: To

give homeowners knowledge and

representation – representation

that will get them the ca$h their

insurance company should be paying

them.

You see my service as an

advocate for the homeowner is a

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 9

unique service. It’s about a fancy

word in the insurance industry,

indemnify. Indemnify is one of

those fancy words the insurance

companies use to confuse homeowners

– even those with Ivy League

educations.

The Barron’s Dictionary of

Insurance Terms defines indemnify

as, “Compensate for loss”. Well

that’s fine, but just what does it

mean in your case? Just how do you

figure out exactly how much you

should get for your damage?

Each day, I represent

homeowners on a broad range of

properties, types of damage, and

coverage issues. I assist the

homeowners, no matter which type of

damage or which insurance company.

Not just storms and fires, but

any kind of damage that is sudden

and accidental; whether leaky

pipes, damaged floors, fireplace

mishaps, broken furnaces,

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 10

vandalism, leaky roofs, and dozens

of other types of damage.

Right now, I‘m thinking of

some of the stories of past

clients. One lady got a denial

from her insurance company for hail

damage – even though many neighbors

got money. Then she replaced the

roof out of her own pocket. You

will be shocked when I tell you how

I was able to get her the money to

pay for the roof.

Every type of damage is in

those stories: storm damage, fire

damage, smoke damage, cracked

tiles, gouged hardwood, stained

carpet, stained hardwood, leaky

pipes, water damaged laminate

floors, water in cabinets, and

dozens of others.

So, what’s so special about me

that allows me to get my clients

thousands – or even tens of

thousands – of dollars that their

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 11

insurance companies would not pay

them?

Well, it comes down to a

specific license, training,

experience, and the commitment to

fight for my clients. What makes

it all possible is the license I

hold for a position that most

people have never heard of.

I’m a licensed and bonded

Public Adjuster.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 12

Chapter Two

“Just What Is a Public Adjuster

Anyway?”

Public Adjusting has a long

history in the United States. One

of the early Public Adjusters was

also one of our founding fathers…

Benjamin Franklin.

It’s not surprising at all

that Dr. Franklin was a skilled

negotiator for his clients.

Knowing his skill as a negotiator,

I’m sure he helped people get good

settlements.

States began setting up

Licensing structures for Public

Adjusters in the late 1800’s. So,

public adjusting has been around in

a formal structure for well over

100 years.

As I write this book, 44

states and the District of Columbia

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 13

have a licensing structure or

regulation set up and operating.

Virginia’s law goes into effect

January 1, 2013.

Once the Virginia law goes

into effect only Alaska, Arkansas,

South Dakota and Wisconsin will

have no licensing structure or

regulation set up.

Alabama is a special case.

While it does have a licensing

structure, only an attorney

licensed in Alabama is permitted to

hold the Public Adjuster’s license

in that state.

Many states follow a model law

that has been approved by the

National Association of Insurance

Commissioners – NAIC. That model

law describes a public adjuster as:

"any person who, for compensation or any other

thing of value, acts on behalf of an insured”

Each state has its own nuances

in the law it adopts. For example,

my home state of Illinois actually

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 14

requires anyone who negotiates with

the insurance company for someone

else to be a licensed Public

Adjuster.

Violating that law is a

misdemeanor in Illinois. On the

other hand, many states allow

contractors to negotiate with

insurance companies. They work to

get payment for repairs they are

making.

Part of the Florida law forced

property owners wait for 48 hours

after having damage to hire a

Public Adjuster. The Florida

Supreme Court struck down that part

of the law in 2012.

Some states have what are

called “fee caps”. A “fee cap”

limits the percentage of a

settlement the Public Adjuster may

receive.

The “fee cap” ends up keeping

property owners from getting the

help they need on smaller claims.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 15

You see the amount of work it

takes to help a homeowner with

claim is about the same until you

get into very large claims. The

work becomes much more extensive at

say $50,000 or so.

When the percentage of a

settlement the Public Adjuster can

receive is limited, it’s no longer

worth it to work on a small claim.

Many Public Adjusters won’t work on

claims under about $30,000 – even

in states without a “fee cap”.

The insurance companies love

fee caps because they end up not

having to pay on many claims that

could get the homeowners thousands

of dollars. The homeowners in most

cases don’t even realize they could

collect money on the damage at all.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 16

Chapter Three

“What Does My Policy Cover?”

The insurance industry created

the first standardized homeowners

insurance policy in 1943. It was

called a standard policy.

The standard policy was

limited compared to current

policies. It covered only fire and

lightning. Not surprisingly, banks

played a big role in creating the

standardized homeowner’s insurance

policy.

I will give both the banks and

the insurance companies their do.

The post-WWII housing explosion in

the United Sates would not have

been possible with the homeowner’s

policies. Even though the standard

policy was created, so the banks

cover their own butts.

Current policies come in three

different types: Basic, Broad or

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 17

Special. The special is also

called “all risk” or “all peril”.

The type that you have can make a

tremendous difference in how much

you get paid for damage.

The basic policy is rarely if

ever sold to home owners these

days. You can still find it for

rental property though.

The basic policy covers 9

named types of damage. The

industry uses the word “peril” for

a type of damage. Those 9 perils

are:

- Fire

- Lightning

- Explosion

- Windstorm and hail

- Riot or civil commotion

- Vehicles (not driven by

owner)

- Smoke

- Volcanic eruption

- Vandalism or malicious

mischief

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 18

Some of these types of damage

can come from unexpected causes

though. Smoke in particular is an

under claimed cause of damage.

You see, smoke can come from a

cooking mishap. It can come from a

fireplace mishap. Smoke can even

come from a damaged furnace.

We’ll go over the impact of

that smoke damage when we discuss

some actual clients.

The broad policy adds an

additional 7 named perils to bring

the total to 16. Those 7 perils

are:

- Falling objects

- Weight of ice and snow

- Accidental discharge of

water

- Tearing apart, cracking,

burning or bulging (of

HVAC)

- Frozen pipes (when building

is properly heated)

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 19

- Artificially generated

electrical current

- Collapse

Now we come to the type of

homeowner’s policy that the

vast majority of people have.

It’s the special or “all risk”

or “all peril” policy. The

industry name is “HO-3”.

In the all-risk policy, it

covers any damage that is

sudden and accidental as long

as the policy does not

specifically exclude it up

front. What’s excluded? Here

is a good start on common

exclusions in an all-risk

policy:

- Flood (you can get flood

coverage from the federal

government in a specific

policy though)

- Earthquake (called ground

movement)

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 20

- Damage from most types of

pests (especially insects

and members of the rodent

family)

- Wear and tear (including

most damage caused by pets)

- Negligence

- Mold (unless caused by a

covered peril)

- Ongoing damage that is not

addressed (mitigation is

important)

- War (when the Japanese bomb

your town, that’s not

covered)

While that looks like a lot,

those exclusions leave many types

of losses that are covered that

most people don’t realize. My

colleagues and I have gotten

homeowners paid thousands or even

tens of thousands of dollars for

the following types of damage:

- Cracked ceramic tile

- Gauged hardwood floor

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 21

- Water damaged hardwood

floor

- Damaged laminate floor

- Soaked carpet

- Stains or spills on carpet

- Toilet overflows

- Broken pipes

- Tub or shower overflows

- Water damaged sub-floor

- Water back-up from sewer or

sump pump(requires

endorsement)

- Building code updates

(check your policy)

- Damaged personal property

- Damaged clothing

- Damaged granite counter

tops

- Smoke damage from a cracked

heat exchanger

- Smoke damage from a faulty

water heater

- Smoke damage from a

fireplace in the garage

- Stolen computers

- Stolen furnace

- Stolen water heater

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 22

- Stolen cabinets

- Damage from break in

- Damage from tenants

- Damage from raccoons (one

of the few types of pest

damage that is often

covered; raccoon droppings

are treated as hazardous

waste)

- Cars driving into the house

(your homeowner’s policy

will pay much more than

going directly through the

driver’s auto policy)

- Stolen copper pipes

- Stolen wiring

- Garbage truck hitting

garage

- Eggs on siding

- Dent from baseball in

siding

- Melted siding from a hot

grill

- Stolen jewelry

- Stolen property while

traveling

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 23

- Loss of use of home or

business property

- Tear out and repair when

pipes burst or break

- Frozen pipes

- Damage caused by the

homeowners themselves.

And I could add many more types of

covered damage. But, you get the

idea by now.

Here’re a couple of things

most people are missing. First,

dozens (maybe hundreds) of types of

damage are covered. Still most

homeowners only even consider

filing for damage like a large fire

or major storm damage.

Second, payment for damage can

add up a lot quicker than people

realize. It happens because the

policy is designed to pay enough to

bring the property back to pre-loss

condition.

Here’s where that fancy word

we used back in Chapter 1 comes in.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 24

The fancy word is indemnify. For

the homeowner it means to pay

enough to put the property back in

pre-loss condition.

So, how does that work

exactly? Let’s look at a common

type of loss that homeowners almost

always overlook – cracked ceramic

tile.

An important characteristic of

ceramic tile is that it is made by

laminating a high definition photo

onto the visible surface of the

tile. The appearance of the tile

varies by lot.

Usually that same exact tile –

often the same manufacturer’s lot –

is no longer available. In that

case, the insurance company must

pay to replace all of the tile.

They pay to replace all of it, even

if in more than one room.

What if the tile runs under

cabinets? Those cabinets must be

removed and re-installed.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 25

What if the cabinets have

granite counter tops? The granite

counter tops need to be removed and

re-installed.

What if the tile runs under

appliances? The appliances must be

moved (by professionals) and re-

installed.

You see how it can all add up.

Here’s an example. One of my

clients in Hazel Crest, IL had a

hailstorm go through her

neighborhood.

Many of her neighbors were

able to get some kind of payment

from their insurance company. Her

insurance company denied her claim

for hail damage to the roof.

Since she replaced the roof

with money out of her own pocket,

it was too late for me to help her

directly with the hail damage.

However, while performing the

damage audit, I found a cracked

ceramic tile.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 26

I was able to get her a

settlement that was over $12,000.00

for that cracked tile because of

the factors I just listed. It was

a large floor that ran under

cabinets with expensive counter

tops. She even had commercial

grade appliances.

Let’s look at a couple of

things that happened to me before I

knew about Public Adjusters and

just how policies work.

I dropped the battery from my

cordless drill and gauged the

hardwood floor in my brand new

home. Not knowing any better, I

ran out to the big box home

improvement store and bought a can

of wood repair glop. Glop is a

technical term by the way. ;-)

Over a weekend, I filled the

gauged area with several coats of

glop. I carefully made it level.

Then I masked off the good part of

the floor while sanding the

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 27

hardened glop to be level and

smooth.

Once I had that looking OK, I

got some magic markers. I colored

in the hardened glop to match the

rest of the floor as closely as I

could. I made the best of it, but

the floor has never been quite the

same.

I didn’t understand back then

that the policy covers that damage.

Not only would the policy cover,

but also it would pay to repair and

refinish the entire floor – in

three large rooms.

Another time I left the plate

out from under a potted plant in

the family room. By the time my

wife caught it, water getting

through the dirt and the metal pot

created a huge rust stain in the

middle of the carpet.

Not knowing any better, we

just lived with the damage. The

policy covers that damage as well

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 28

though. The policy would pay to

replace all of the carpet, and the

pad. If the sub floor were

damaged, it would be covered as

well.

One of the people who trained

me as a Public Adjuster has a young

son. While he was giving his son a

bath, he got a phone call. While

on the phone call, his son decided

to see how quickly he could empty

the tub with his toy bucket onto

the floor.

Some of that water even got

into the vent. That water went all

the way down to the basement and

damaged the furnace. Yes, it’s a

covered loss. The owner got enough

money to make all of the repairs.

So, what made the difference

between the damage the homeowner

has to “live with” and damage that

the homeowner gets paid?

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 29

The difference is access to a

licensed and bonded Public

Adjuster.

You see, as a Public Adjuster,

my job is to get the homeowner the

highest settlement possible under

their policy. The policy is a

contract. When all conditions of

the policy are met, that contract

directs the insurance company to

indemnify – pay – the homeowner.

You may be wondering about

fairness to the insurance

companies. You may be asking, “If

everyone gets that kind of

settlement, what happens to

insurance rates?”

We’ll go over how insurance

companies pay in the next chapter.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 30

Chapter Four

“How Much Should They Pay

Me?”

We ended Chapter 4 by looking

at how a small bit of damage to one

ceramic tile can trigger a 5-figure

payment from the homeowner’s

policy. Does that type of claim

treat the insurance company badly?

Well, first of only a small

fraction of people who have similar

damage ever report or get paid for

it. Those who report most of the

types of damage I listed on their

own will be lucky to get any

payment at all. The lucky few who

do will get a pittance.

Why does that happen? We’ll

talk about it some more later, but

it comes down to the conditions

required for payment and presenting

the damage properly to the

insurance company.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 31

Right now, let’s go over

the general state of payments for

damage by insurance companies.

Since the mid 1990’s the

insurance industry has been hiring

high-powered management consultants

to teach them how to be able to pay

out less on damage claims.

The insurance companies have

turned this into a science. You

can read about it in a book titled,

Delay, Deny, Defend: Why Insurance

Companies Don’t Pay Claims and What

You Can Do about It by Jay Feinman.

The ISBN is 9781591843153.

Or you can view the 2007

PBS/Bloomberg Markets program,

“Insurance 9-1-1, The Insurance

Hoax” hosted by David Brancaccio –

a Walter Cronkite Award Winner.

You can purchase it from PBS. Or

you can find it on youtube.com – in

three parts.

Both the book and the video

will show you just how serious the

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 32

insurance companies are about

paying as little as they can. But,

you already knew that or you

wouldn’t still be reading.

Brancaccio and two reporters

from Bloomberg Markets Magazine

review how the insurance companies

have made a systematic effort to

reduce their payments on claims.

That effort happened at the same

time their profits skyrocketed.

Also, Smart Money Magazine

interviewed a former insurance

company adjuster. That adjuster

told Smart Money Magazine that 80%

of the former employer’s clients

ended up with 25 to 40 cents on the

dollar. The comparison was against

homeowners who got an independent

estimate – from say a Public

Adjuster.

Then there is the Florida

study. After one of the bad

hurricane seasons in the early

2000’s, two of the largest

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 33

insurance companies decided not to

write new policies in parts of

Florida.

Florida told them to either

write new policies in the whole

state or write none. The two

companies chose… none. The two

companies have over half of the

market. When they pulled out, it

created a mess in Florida.

Florida wanted to fill the gap

and create some choice for their

residents. Florida created a state

run insurance company. It’s called

Citizens Property Insurance

Corporation.

This company was new and not

used to the higher settlements when

a Public Adjuster helps the

homeowner. Citizens Property

Insurance Corp. was alarmed by the

difference between payouts when a

Public Adjuster worked on the

claim. So, they demanded an

investigation.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 34

The Florida Legislature’s

Office of Program and Policy

Analysis & Government

Accountability studied over 72,000

claims. OPPAGA found that the

Public Adjusters were not doing

anything wrong. The Public

Adjusters were just being more

thorough to document everything the

policyholder should get.

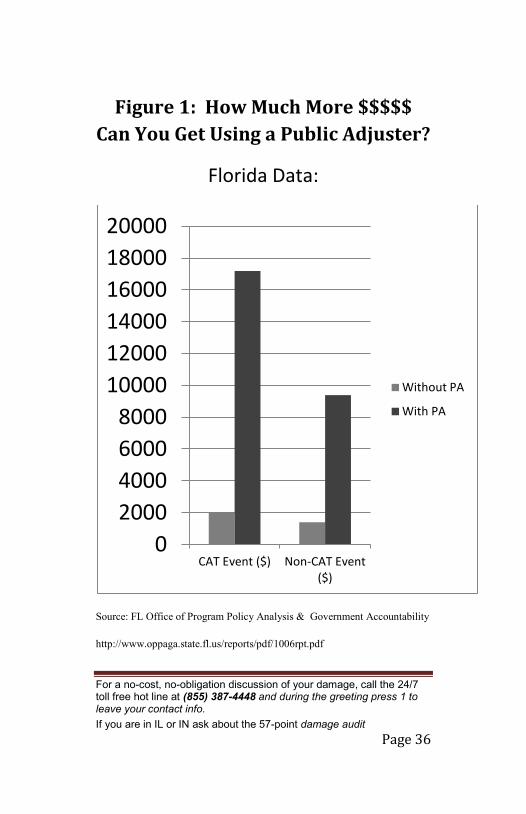

So just how much more were

homeowners getting when they used a

Public Adjuster? The OPPAGA study

of the 2005 hurricane season found

that using a Public Adjuster

increased the settlement from an

average of $1391 to $9379 when no

named storm was present. That’s a

574% increase.

If a named storm was involved,

the difference was even greater.

Then the average settlement went

from $2029 without a Public

Adjuster to $17,187 with a Public

Adjuster. The difference for the

claims with a named storm was 747%.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 35

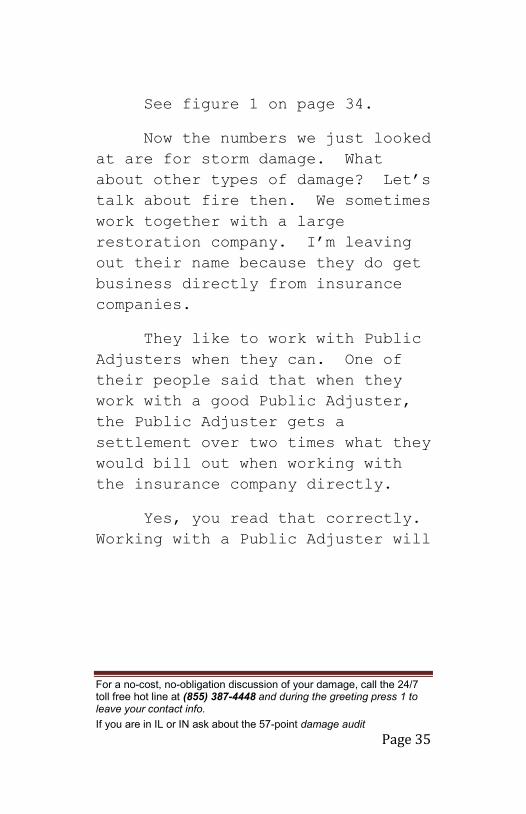

See figure 1 on page 34.

Now the numbers we just looked

at are for storm damage. What

about other types of damage? Let’s

talk about fire then. We sometimes

work together with a large

restoration company. I’m leaving

out their name because they do get

business directly from insurance

companies.

They like to work with Public

Adjusters when they can. One of

their people said that when they

work with a good Public Adjuster,

the Public Adjuster gets a

settlement over two times what they

would bill out when working with

the insurance company directly.

Yes, you read that correctly.

Working with a Public Adjuster will

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 36

Figure 1: How Much More $$$$$

Can You Get Using a Public Adjuster?

Florida Data:

Source: FL Office of Program Policy Analysis & Government Accountability

http://www.oppaga.state.fl.us/reports/pdf/1006rpt.pdf

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

CAT Event ($) Non-CAT Event ($)

Without PA

With PA

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 37

get the homeowner a settlement

twice as high as dealing directly

with the insurance company and

their restoration company. That

observation comes from a key person

working for a major restoration

company.

By the way, all the numbers

and stories I just shared

understate the impact of a Public

Adjuster on settlements. You see,

all those numbers and most of the

stories don’t reflect people who

were wrongly denied. Many of my

own clients would get literally

nothing without help.

The insurance companies

regularly deny people for claims

that could and should be paid. I

help get those people paid by

presenting the claim properly.

It could be a homeowner with a

broken pipe in the basement, who

tells the insurance company he has

a “flood”. If you remember, flood

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 38

is one of the exclusions to all of

these policies.

I like to refer to flood as

the “f-word” because it trips up so

many homeowners. Words such as

“accidental discharge” or “water

back-up” or “overflow from a

blockage” work so much better.

Also, the numbers don’t

reflect a situation one of my

colleagues worked on. A homeowner

had a whole house fire. She had

contacted the insurance company

before working with my colleague.

Her insurance company’s

adjuster “forgot” to remind her

that she was covered for the loss

of use of her home. Instead of

staying in a hotel that was direct

billed to the insurance company,

she and her children were sleeping

in her car in the driveway.

The homeowner did stay in a

hotel – after my colleague took

care of the situation.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 39

Another trick insurance

companies like to use after a large

loss is the “Trojan Dumpster”. You

remember the story of the Trojan

horse? That’s the story of the

Greeks failing to take the city of

Troy.

The Greeks made a show of

breaking up their camp and leaving.

Just before boarding ships, they

left a huge horse outside the gates

of Troy.

The Trojans thought they had

successfully weathered the storm

and brought the horse inside the

city gates as they celebrated. The

Trojans did not count on the small

group of Greek soldiers hiding

inside the horse.

Once the Trojans were

exhausted from celebrating, the

Greeks hidden in the horse emerged

and opened the gates to Troy. This

allowed the Greek army, which had

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 40

stayed nearby to finally conquer

Troy.

Often after a large fire or

major storm, the insurance company

will quickly send out a dumpster.

The homeowner finds the dumpster

handy to get rid of all the things

that have been ruined.

The insurance company adjuster

will show up after the dumpster has

been removed. When the homeowners

try to get paid for those damaged

items, they are at the mercy of the

insurance company adjuster.

You see, one of the seven

conditions we have been discussion

is that the insurance company has

the right to inspect any damage

they are paying for.

Pictures are not enough. They

have the right to inspect the

damaged items. If you can no

longer produce those items for

inspection, they don’t have to pay

for them.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 41

That’s true even if the

insurance company sent the dumpster

you used to dispose of the items.

So beware before throwing out

damaged items from a fire or other

large loss.

I spoke with a lady who had

tornado damage. She and her

husband had already tossed their

large swing set/play center in the

dumpster the insurance company

happily provided.

I warned her about the need to

have the actual swing set available

for examination by the insurance

company adjuster. She was less

than happy with my news. I do hope

that she and her husband pulled it

out of the dumpster so they could

be paid properly for it.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 42

Chapter Five

“What about the Reasons to Not

Call a Public Adjuster?”

Now for those of you who are

not yet convinced, there can only

be seven reasons. Let’s go over

them:

First, you may be thinking,

“My damage looks small. I can just

live with it or make a minor repair

myself. I’ll wait until something

really big happens to call the

insurance company.” Well, only a

trained professional can truly tell

whether damage that looks small can

give you a big payment or not.

“Is MY Damage Big Enough?”

Often damage that looks and is

“small” can cause the insurance

company to pay a lot. With the

right person, telling them in the

right way sometimes the insurance

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 43

company will pay to replace an

entire surface because the surface

is no longer repairable.

That surface can be a floor

(tile, hardwood or laminate), a

roof or siding. There are dozens

of ways for this to happen, so get

a professional – a Public Adjuster

- to see if your damage is a lot

bigger than it looks.

Also, often we need to address

damage under the surface that you

may not see by looking at the

outside. A good Public Adjuster

will make sure the insurance

company addresses ALL of the

damage.

Even if the damage looks small

and you can “fix” it with a small

inexpensive repair, you may be

jeopardizing the very thing you are

trying to preserve. You see a

small patch job on one part of the

house can allow the insurance

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 44

company to pay you a lot less once

you do have “big” damage.

Almost daily I see people who

have cost themselves thousands of

dollars because they made a “small”

repair themselves. It’s so sad

when they could have gotten a much

better outcome by making one simple

phone call.

Another part of this objection

is when people are afraid that the

insurance company will jack up

their rates for filing a claim.

Insurance is regulated on a

state-by-state basis. So, there

are some differences from state to

state.

For the states that I

currently am licensed (IL & IN)

insurance is regulated by the

Department of Insurance in that

state. Those same departments

issue my license in each state.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 45

It is against the regulations

of the Department of Insurance for

an insurance company to:

- Drop a homeowner

- Choose not to renew a

homeowner

- Raise the homeowner’s

premiums.

The one thing that they can mess

with for filing a claim is a

“claim-free” discount.

The “claim-free” discount is a

small bribe the insurance company

offers in return for not filing a

claim. It typically is about $150

or so.

When you file a claim, the

insurance company will withhold

that discount for 3 years. The net

effect is like adding about $500 or

so to your deductible.

Therefore, it just means your

deductible hurdle is a little bit

higher. I take it into account

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 46

prior to any recommendation on

filing a claim.

“Hey Melrose, I’m Pretty Smart Myself”

A second reason you might not

be convinced yet, is that you think

you can do this yourself and save

the fee. Yes, Public Adjusters do

charge a fee for their services.

Licensed and bonded Public

Adjusters have to maintain a

license. That includes continuing

education. Being paid for the

service is Public Adjusters feed

their families.

However, remember the data on

how much more people end up with

when they use a Public Adjuster?

The state of Florida data says that

homeowners who use Public Adjusters

get 574% to 747% higher settlements

for their claims.

Also, remember the Smart

Money Magazine interview with a

former insurance company adjuster.

She said her insurance company’s

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 47

clients routinely ended up with

much less. They got only 25 to 40

cents on the dollar - compared to

those who got an independent

appraisal.

In the 2007 Article by David

Dietz and Darrell Preston of

Bloomberg Markets Magazine, “Home

Insurance Secret Tactics Cheat Fire

Victims, Hike Profits”, the two

authors document funny business by

multiple insurance companies.

Dietz and Preston quoted an

email from a manager at a major

insurance company to “…resist the

temptation of paying more just to

move this type of file.” They also

quoted Jo Ann Katzman, a former

claims adjuster at a major

insurance company. Ms Katzman told

about pep talks to keep claim

payments down and prizes awarded to

adjusters who deny fire claims by

blaming the fire on arson.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 48

Yes, you can go up against the

insurance company on your own if

you want to. But, consider this:

If you were deciding this in court,

would you let the insurance company

hire an attorney to represent both

of you? I didn’t think so. Why do

that same thing now when there

isn’t even a neutral judge present

to protect your rights?

Those who are truly smart know

when to bring in a specialist.

They hire someone who works in the

field every day. They know it’s

not worth the time to keep up with

something they use once every

decade or so.

They also know spending the

time and hassle to grind out a

payment from the insurance company

will cost them in their own

productivity. Or it could cost

them in time they would rather

spend with friends and family.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 49

How often do you want to say

to a loved one, “I’m sorry? I’ll

miss your event because I have to

stay home for the contractor to

come out for an estimate. Maybe

I’ll make it next time.”

“What Am I Paying the Agent For?”

Some people just call their

agent when they have damage. It

“seems” logical. After all, “He’s

the guy I’m paying for this policy.

He should know.” Sadly, that’s

rarely the case.

Agents get lots of training –

on how to SELL insurance. The

companies conveniently skip the

dozens of types of damage that

people do get paid for. Agents

don’t even learn how to use the

software that generates claim

estimates.

In fact, the agents who want

to get paid top dollar on their own

personal claims know who to call.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 50

It’s NOT their own company

adjusters.

One of my colleagues was

called out to a house for a water

stain on the ceiling. The stain

was small. There was no opening in

the roof. The walls and floor were

undamaged.

My colleague had to

reluctantly tell the client that

the damage was not large enough to

submit to the insurance company.

When he was walking down the

stairs to leave, he noticed a huge

blue stain in the carpet. He

missed that stain because he had

been looking at the ceiling. The

carpet ran throughout the first

floor and up the stairs.

He asked the homeowner,

“What’s the deal with the blue

stain?” The homeowner told an

interesting story about the stain.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 51

When the homeowner’s son does

laundry, he piles up the laundry

basket until its overflowing.

Next, the son puts the detergent

bottle on top of the pile of

clothes. Then he drags the basket

down the stairs, letting it bounce

on each step.

One time the bottle of

detergent fell and cracked. It

tumbled to the bottom of the stairs

and dumped out all the detergent

while the son stood there

dumbfounded. As much as he tried,

the homeowner could not get out the

huge blue stain.

My colleague responded that

the stain was sudden and accidental

damage. Therefore, it would be

covered by the homeowner’s policy.

After my colleague wrote up

the claim, he was about to leave –

for a second time. The homeowner

said, “By the way I’m a (well known

insurance company) agent.”

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 52

My colleague replied, “That’s

OK, I don’t discriminate!” And the

homeowner said, “No, no, you’re not

getting it. I had no idea that

damage was covered.

If the insurance companies

don’t even tell their own agents

about what is covered? How are the

homeowners supposed to know?

If the insurance companies did

share all of these secrets with

their agents, the agents would tell

the homeowners. Telling the agents

would cost them a lot more money.

That’s one big reason why you

need a Public Adjuster to level the

playing field.

The Two-Step; Does It Work?

You might be thinking, “I’ll

get my offer from the insurance

company’s guy and then call Melrose

to see if he can improve the

offer.” Does that actually work?

It depends. Is your objective to

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 53

pay the lowest amount possible for

any service you use?

Or, is your objective to end

up with the most cash possible in

your own pocket?

How Do You Get the Most Ca$h for Your

Damage?

When it comes to dealing with

the insurance company and their

expert adjusters, those are two

different matters. You see a

homeowner can torpedo their claim

with ONE WRONG WORD.

There is one word in

particular that you NEVER want to

say to the insurance company. Know

what it is? It’s that “f-word” we

talked about earlier – flood.

In the hundred of policies

I’ve reviewed for homeowners, I

have met… one… who had a flood

policy from the federal government

program.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 54

Even he was using it in a way

that would not get him paid though.

We’ll talk about that more when we

discuss what endorsements should be

included in your policy.

Also, your policy has seven

conditions that you need to meet

before they will pay. If you have

skipped a step, it could be big

trouble for you.

When the insurance company

adjuster shows up, the adjuster can

reduce or even deny the claim for

that alone. Some of those I can’t

help once the insurance company

adjuster has his own set of

pictures or his notes on what he

saw before the homeowner fulfilled

their obligations under the policy.

Be careful when you talk to

anyone at the insurance company

about your claim. You see,

anything you say can and will be

used against you. What you say can

and often does allow the insurance

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 55

company to reduce or even deny your

claim.

Even if you say everything

correctly, you need to give the

insurance company an estimate. To

get paid fully, you need to use the

same format the insurance companies

use. It’s called Xactimate.

If you meet the insurance

company adjuster by yourself, the

adjuster usually will make that

lowball offer of 25 to 40 cents on

the dollar. He’ll then inform the

insurance company of the amount.

And, the insurance company

expects to get away with the

lowball offer. Once you make that

misstep, getting full payment

becomes a fight.

“But Scott, They Already Gave Me a

Check!”

Another reason you may not

have already called me for an

appointment is that they already

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 56

gave you a check. Maybe you cashed

it too. Well, it’s not too late to

help you. Even if they denied your

claim, it’s not too late to call in

a Public Adjuster.

Often a Public Adjuster can

still help. You’ll need to talk

about the details to see. In most

states by law, a Public Adjuster

can “re-open” your claim up to 365

days after the date of your loss.

I won’t sugar coat this. It’s

a lot tougher to get you ca$h in

this case. It can and does happen

though. So, what are you waiting

for? Talk with a Public Adjuster!

Even if they gave you what you

think is a “good” settlement, you

can have damage they did not

address that is worth THOUSANDS to

you!

Remember the restoration

company we looked at earlier? The

one who also does insurance work.

Even though they get much of their

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 57

business directly from the

insurance company, they LOVE to

work with a Public Adjuster when

they can.

One of their top guys shared

the reason with me. He said that

when they work with a Public

Adjuster, we get the homeowners

twice what the insurance company

would pay out. This contractor is

NOT a cut-rate contractor either.

“A Nice Man Came to the Door and It’s So

Convenient!”

When a big storm hits,

construction companies send out

salesmen to go door to door to sign

up business. Those companies can

seem like such a good option. They

will promise to get your work taken

care of and guarantee that you

don’t have to come out of pocket.

I’ll admit it’s a tempting

offer… on the surface. It’s

convenient and takes a lot of the

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 58

hassle out of getting your damage

addressed.

Did you know though that your

insurance company is not required

by law to listen to them or respect

their estimate? In fact, very few

of them use the state of the art

estimating software – Xactimate,

the gold standard of the estimating

industry – that Public Adjusters

use.

“My Contractor Is Not Acting Legally?!?!?”

In at least one state

(Illinois), representing a

homeowner on insurance settlements

without the proper license – Public

Adjuster – is not even legal. Yes,

that includes contractors. It

especially is meant for “storm

chasers”.

Don’t take my word for it by

the way. Ask the contractor (in

IL) if he is complying with 215

ILCS 5/1510 and 215 ILCS 5/1605.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 59

Not complying is a Class A

misdemeanor under 215 ILCS 5/1610.

So why would the insurance

company even talk with them? It’s

simple really. How much leverage

can a contractor who is not acting

legally have over the insurance

company?

If you answered, “Not much.”

You’re right. The insurance

company is typically willing to

talk with contractors. Why? It’s

because they KNOW they can get away

with paying less money than when

you have the proper and legal

advocate. Guess who? A licensed

and bonded Public Adjuster can do a

much better job of representing

YOUR interests.

How Do You KNOW How Well Your

Contractor Is Performing?

So then, how can the

contractor still work and get

enough money so they don’t go

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 60

broke? Well, if they addressed

everything that a thorough

Xactimate estimate would call for,

they wouldn’t. They would lose

money.

So how do they make up for not

getting enough money from the

insurance company to cover the

costs for a true repair? The only

way they can make that up is skip

parts of the repair that are in a

good Xactimate estimate.

So am I saying you’re getting

a “bad” repair? It depends. Some

contractors are skilled enough to

skip things that may not matter to

getting the repair “functional”.

Are they doing everything to bring

the property back to pre-loss

condition though? They can’t.

The only way to get ALL of the

damage properly addressed by the

policy is to get an estimate in

Xactimate by someone trained and

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 61

incentivized to get you the most

money possible under your policy.

That’s a licensed and bonded

Public Adjuster.

“Will I Have Enough Money to Make the

Repairs?”

Again, it depends. One more

place where it helps to have a

Public Adjuster instead of just a

contractor is when you have a

complex job with damage to the

interior and the exterior. You

see, when the damage is that

complex, a Public Adjuster can get

the insurance company to tack on

the funds to pay for a general

contractor (overhead, profit,

taxes, permits and insurance)

whether you hire one or not.

Adding on the general

contractor’s fee can add up to 25-

30% to what you would get. Again,

you are not required to hire one if

you don’t want to.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 62

Now anyone can go out and

spend the kind of money for a

repair that the folks who have more

money than brains spend. If you

hire one of those companies that

are all over the TV channels, you

probably will spend more money than

you need to.

Just Who Should You Hire?

Contractors are scrambling

right now. It’s a very good bet

that a contractor who has been

working in your town for many years

with a good reputation is available

at a reasonable price these days.

A Public Adjuster’s job is to

get you the money for your repairs.

We stay neutral among reliable

local contractors. You are going

to have to do some shopping. Check

references and check with your

local government and supply houses.

You Just Want Your House Fixed – and

Fixed Right!

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 63

The seventh and final reason

you may be thinking of not calling

is that you may be concerned about

how much hassle and time this will

take. Well, the path to the least

hassle – other than putting your

head in the sand and letting the

damage just sit there for eternity

– is to call a licensed and bonded

Public Adjuster.

You see, a Public Adjuster can

keep the insurance company from

making you jump through lots of

unnecessary hoops. You won’t have

to give the insurance company 3

estimates from contractors who are

like herding cats. The contractors

know the insurance companies are

going to force you to accept the

lowest bid.

They know up front, that they

are bidding against each other to

cut corners the most – and get paid

the least…

or

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 64

putting in a few hours of work

for no pay whatsoever.

When you call a Public

Adjuster, you won’t be stuck with

getting only the money from the

lowest bid. That’s the guy willing

to cut the most corners by the way.

You won’t have to play phone tag

with the insurance company either.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 65

Chapter Six

What You Need to Know Before

Spending Another Dollar on

Property Insurance

This chapter is based on a

process I perform in homes hundreds

of times each year. It’s called a

policy analysis.

In the home, I translate a

homeowner’s policy into English so

the homeowner can understand their

coverage. Out of the several

hundred policies, I have examined

only one had all the bases covered.

The first thing I look at is

the type of policy. I strongly

believe that a homeowner’s best

value for the money is in the “all-

risk” or HO-3 policy. You pay a

little bit more for it than a Broad

or HO-2 policy. But the all-risk

policy gives you so much more in

coverage that it is one of the true

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 66

bargains in financial services

available.

If you own a house that you

are no longer living in, see the

chapter on commercial policies.

Once you no longer live in the

house, it becomes a commercial

property and requires a commercial

policy

The change to commercial

policy applies even if you have

family members living there. I

have met owners who thought their

agent was doing them a favor and

saving them a few bucks by keeping

the policy a homeowner’s policy.

In fact, those agents are

putting the coverage in jeopardy.

I have worked with an owner who

received nothing from a whole house

fire because his family lived in it

while he lived elsewhere.

Sadly, he contacted me too

late in the process to help him at

all. The insurance company already

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 67

had many recorded statements and

written responses that doomed his

chances to collect for the damage.

Another thing to check is

whether the homeowner has a “forced

place” policy. The lender imposes

these policies when the homeowner

allows their policy to lapse.

Forced-place policies are

limited in their coverage. I have

seen some that specifically exclude

weather. That means lightning is

not covered. The forced-place

policy that excludes weather is

weaker than even the standard

policy – which has been extinct for

many years.

Also, the forced placement

policy costs a multiple of what a

normal homeowner’s policy costs.

And to top it off, the forced-place

policy is designed to pay off the

lender for a total loss – not

allowing the homeowner to rebuild.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 68

If you have one of these

forced-place policies, I urge you

to replace it with a normal

homeowner’s policy as soon as you

have 2 nickels to rub together.

One of the most important

numbers in the policy is your

amount for the dwelling coverage.

It’s shown as “Coverage A” under

many homeowner’s policies.

The Coverage A number has two

jobs. Each one comes into play if

you have a total loss. The type of

loss we concerned with here could

be a whole house fire or a tornado

carrying the house off to Kansas.

If, God forbid, you have that

total loss, the amount of Coverage

A needs to be large enough to:

- Pay off any mortgage(s)

- Pay enough to totally

rebuild from the ground up.

The lenders are pretty good at

keeping their butts covered, so I

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 69

don’t concern myself with checking

that out. I do mention it to the

homeowner though in case they want

to check it out.

Being able to rebuild though

is a bigger concern. The Coverage

A amount needs to be large enough

to pay to totally rebuild the house

from the ground up. That number is

typically higher than what the

house would sell for.

In my area at this time, $130

per square foot is a typical number

contractors tell me they need to

rebuild completely. Check on you

area and for your type of house.

In nicer neighborhoods in my

area, it might take $150, $200 or

even more per square foot. Check

for your metro area and your

neighborhood. It varies a lot.

Another thing to check on that

is a bit beyond what I look at in a

policy review is the issue of “full

replacement value” versus “extended

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 70

replacement value”. The reasons I

haven’t been directly involved with

are:

- This issue has not been an

issue in my markets to date

- You should look at the full

policy to make sure what

you have.

The episode of NOW hosted by

David Brancaccio we discussed

earlier spends much of the episode

on this specific issue. Prior to

the southern California fires of

2003, many insurance companies

quietly changed the language of

their policies.

After the change to the

“Extended Replacement Value”, many

homeowners lost about 60% of their

coverage in the case of a total

loss. Some owners reported

noticing the change and asking

their agent.

According to the homeowners,

the agents told them that it was

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 71

the same or even a better policy.

Unfortunately, that turned out not

to be the case.

The next part to look at in a

policy review is an endorsement for

“water back-up”. An endorsement is

additional coverage for a specific

peril or risk that the insurance

company can offer.

When you have water back-up

through the sewer or sump pump,

that water has traveled through the

ground outside. Therefore, the

water is contaminated by whatever

is around the outside of your home.

Those contaminants can be

fertilizer, animal droppings,

pesticides and herbicides – just to

name a few. The water from such a

back-up is deemed hazardous waste.

The industry terms are Category 3

or “black water”.

No, black water is not just a

song by the Doobie Brothers. It

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 72

can cost you big money without the

proper coverage.

When black water is in the

home, the settlement for a proper

clean up of an unfinished basement

is usually around $10,000. Most

insurance companies will sell this

coverage in increments of $5000 or

$10,000.

A finished basement will need

a minimum of around $20,000 to re-

build. That’s even if “partially”

finished.

When buying insurance for my

own home with a finished basement,

I would get as much coverage for

water back-up as they would sell

me. If they will only sell me

$10,000, I would change insurance

companies.

I know that sounds awfully

strong. However, I have talked to

many homeowners who have no

coverage or inadequate coverage for

this type of loss. Unfortunately,

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 73

they didn’t talk to me until after

they needed it.

Another coverage to look at is

one called “All Laws and

Ordinances”. The way this

endorsement works comes down to the

type of damage you have.

Let’s say you have damage that

affects one of the systems in your

house. For example, you could have

a small fire in the kitchen that

damages the electrical system.

When you get your permits to

have the work done, your local

government will make you bring that

system up to the current code. If

you have the right endorsement,

that repair is covered. If you

don’t have it, or don’t have

enough, then it’s out of your

pocket.

How much is enough? The best

way to figure that is to consider

how old your house is and what

systems have been updated recently.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 74

One owner I worked with has a house

that is over 80 years old.

Half the house still has the

original wiring. He has the kind

that runs bare wire along

insulators that are attached to the

rafters. It would take him tens of

thousands of dollars just on that

system alone.

What about plumbing systems?

What if some damage forced you to

update the entire plumbing system?

Damage could also affect items

like stair width, stair slope,

window size, or how high a window

is off the floor. Imagine what it

takes to cut a hole in a brick wall

to make a window bigger.

One town in my metro area a

special requirement any time a

house in the older part of town has

a major rehab. Those houses must

comply with ADA - the Americans

with Disabilities Act.

For a no-cost, no-obligation discussion of your damage, call the 24/7 toll free hot line at (855) 387-4448 and during the greeting press 1 to leave your contact info.

If you are in IL or IN ask about the 57-point damage audit

Page 75

For a major renovation in that

area, you are looking at changes

like: