11 tips for financial success

TRANSCRIPT

FINANCIAL11 TIPS FOR YOUR JOURNEY TO

SUCCESS

Don't Take Financial AdviceFrom Family & Friends#1

Okay, so this may be a bit overstated. But it makes the point. We hear stories over and overagain of doctors and other practitioners who say “my father told me to invest in…” or “all of mycolleagues are doing this…”

Why do we so easily do what everyone else does? It doesn't make sense.

The majority of individuals, families, and businesses are poor money managers and financialdecision makers. Yes, of course, there are some of us who have very wise and financially astutefriends and family. But they are few and far between.

We are all products of our experiences – these experiences create our world view, our reality.But that is not reality. It is our perception of reality. While it’s certainly not a bad idea to getadvice from multiple people, getting opinions from too many unqualified people can leave youwith information overload. Too much misinformation and you’re bound to [subconsciously]make choices accordingly.

Control the Decision-MakingProcess, Ignore the Results #2

Similar to point #1, point #2 involves focusing on making decisions based on accurateinformation and context.

Outcome Bias is a problem that most of us face. We make decisions based on pastresults, even if those results were a fluke.

A better idea is to look at the information you have when it’s time to make a decision. Wecannot control the results. Only the process. The most successful physicians, athletes, andbusinessmen and women only focus on what they can control.

Understand that Financial PeopleDo Not Know All Things Finance#3

Insurance advisors are not tax gurus. CPAs are not insurance experts. CFOs are not investmentspecialists. And many investment pros know little about accounting and financial management.

Just like in the medical field – a cardiologist will certainly know more than the average personabout neurology or urology, but he still isn’t a neurologist or urologist. He’s a cardiologist.

A CPA may understand everything there is to know about tax law, but likely will not know asmuch as they think they know about investments and insurance (unless he or she has beenspecifically and extensively trained in a certain area).

Your team should be built with advisors that have verified specialties in various arenas – i.e.tax, insurance, investments, estate planning, and business planning.

Do not expect just one advisor to know everything. And if they pretend they do, run as fast asyou can.

Save 20-30% of Your Gross Income#4It’s all about discipline. You won’t have any strategic financial decisions to make if you don’thave the assets to make them with.

It may be a simple idea, but saving 30% of income is rare. If you can do this it will be hard to fail.

Understand Time Value of Money Principlesand the Fact That Money Has a Cost#5

Americans all over the place are over paying for debt, services and so much more. When youover pay for a debt or service you lose the ability to earn interest on that money.

A quick example – if you overpay on homeowners insurance by $50 per month ($600 per year)you lose the ability to invest that money. Assuming that money would have earned a 4%interest rate annually you would have lost a total of $50,927 over the course of a 30 yearmortgage.

If family that wastes $1,500 a month (an amount that is not uncommon for American families)– that amounts to $1,527,805 of lost capital after 30 years. (Assuming a 4% interest rate)

That’s a lot of money.

Don't Forget That Cash is Always King#6This one is short and sweet. A major reason to save is so you’ll have cash when opportunitiescome along. When you have capital good opportunities will find you – trust me.

Don't Fall Into the 401(k)/403(b) Trap#7As you can see, these points are building on one another. The main issue with putting too much(or all) of your savings into a 401(k) or 403(b) is the fact that it’s locked up till you’re 59 ½.

Oh yeah… and the fees are usually ridiculous. Research has shown that annual fees in qualifiedplans are consistently above 2-2.5% per year. That’s going to equate to a 30% reduction in yourlong-term reduction of your account value.

Better hope the market flies upwards if you’re heavily committed to a 401(k) type plan.

Your Thinking Will Evolve Over Time#8Recognizing that your thinking (and your desires) will change over time is one of the mostmature decisions you can make.

The 50 year old thinks differently than he did at 25. And the 70 year old thinks differently thatshe did at 45. Understanding that you will wish you had done or hadn't done certain things inthe future is the first step in what we call ‘The Foresight Process.’

The more effectively we can plan and make decisions based on how we’re going to feel in thefuture, rather than how we feel today, will yield an extremely valuable long-term outcome.

An Average Rate of Return Can Be VeryDeceptive#9

Financial planners and ‘gurus’ have been using average rates of return to predict future resultsfor years. This shows an incredible amount of ignorance – many of us used to believe itourselves.

What they should be looking at is the true rate of return, known in the financial industry as theCAGR (Compound Annual Growth Rate). The CAGR is the effective rate earned each year.

Numbers lie. In order to get the truth about numbers, we have to put them in accurate context.

(Continued on the next page)

An Average Rate of Return Can Be VeryDeceptive (Continued...)#9

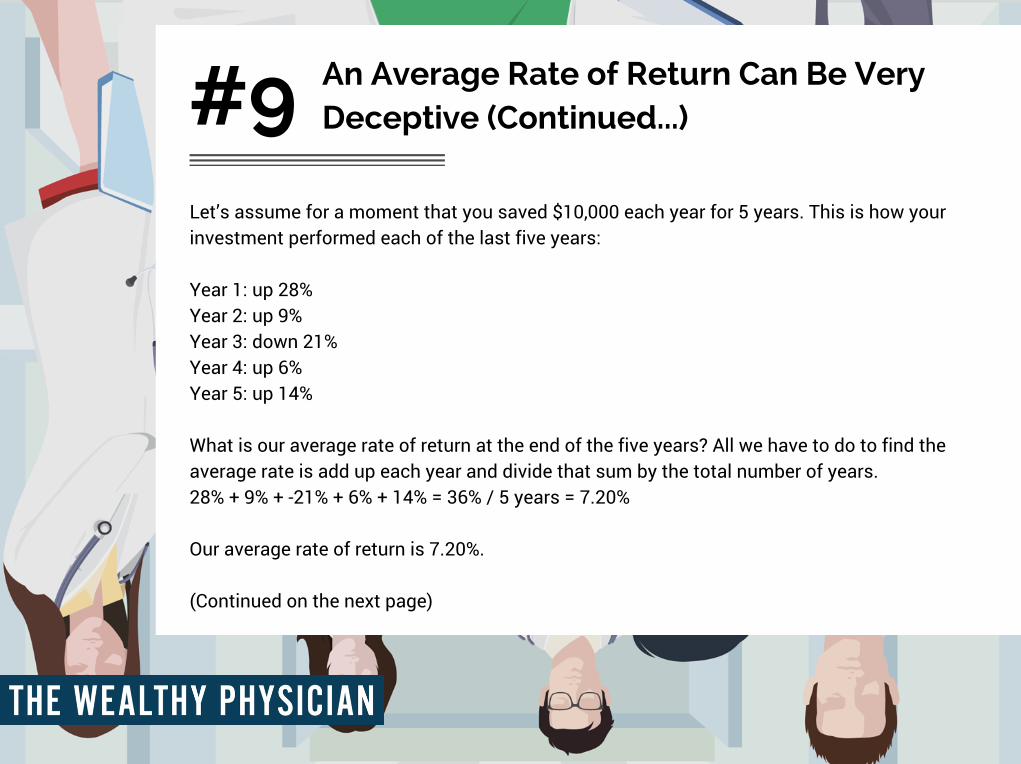

Let’s assume for a moment that you saved $10,000 each year for 5 years. This is how yourinvestment performed each of the last five years:

Year 1: up 28%Year 2: up 9%Year 3: down 21%Year 4: up 6%Year 5: up 14%

What is our average rate of return at the end of the five years? All we have to do to find theaverage rate is add up each year and divide that sum by the total number of years.28% + 9% + -21% + 6% + 14% = 36% / 5 years = 7.20%

Our average rate of return is 7.20%.

(Continued on the next page)

An Average Rate of Return Can Be VeryDeceptive (Continued...)#9

While the average rate of return is 7.20%, at the end of the 5th year our account looks like this:

But, if we expect a 7.20% average and run it as a CAGR (as most people do), it would look likethis:

This isn’t how rate of return works. It varies year to year. It is volatile.

(Continued on the next page)

An Average Rate of Return Can Be VeryDeceptive (Continued...)#9

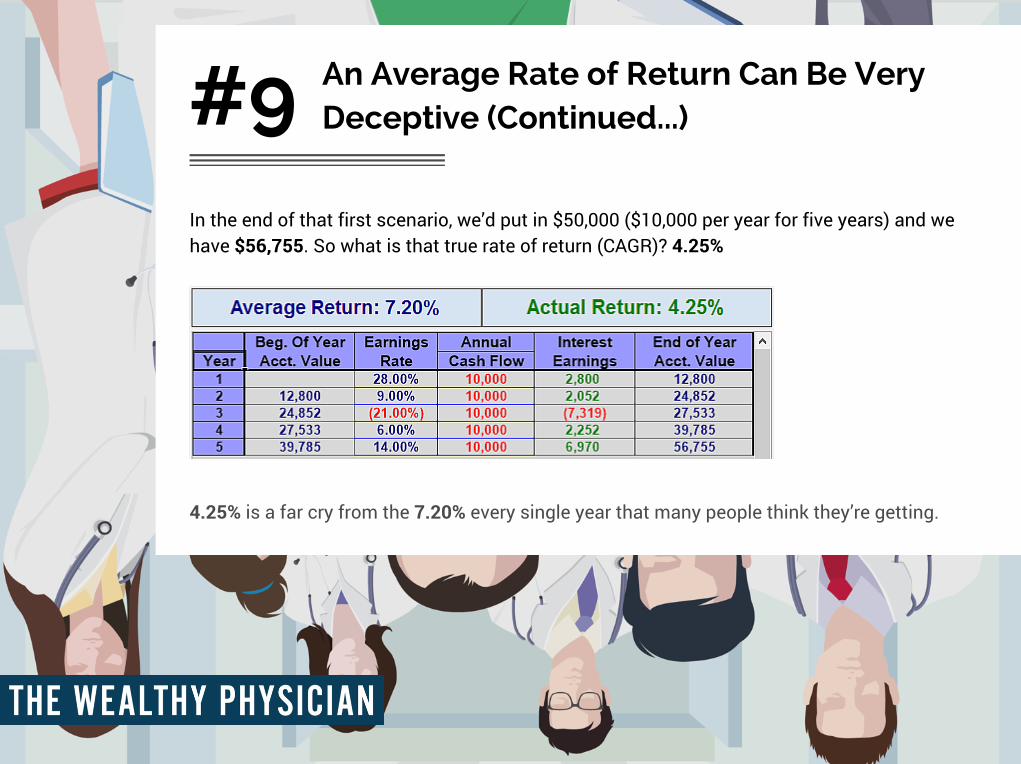

In the end of that first scenario, we’d put in $50,000 ($10,000 per year for five years) and wehave $56,755. So what is that true rate of return (CAGR)? 4.25%

4.25% is a far cry from the 7.20% every single year that many people think they’re getting.

Conventional Wisdom is Often Wrong#10“This `telephone' has too many shortcomings to be seriously considered as a practical form ofcommunication. The device is inherently of no value to us.”- Western Union internal memo, 1878

As you've seen so far, conventional wisdom – the accepted knowledge of the majority – inmany cases in completely wrong.

Todd Langford, the mastermind behind the software company TruthConcepts.com, has saidthat one of the worst phrases in the world is “if it sounds too good to be true, it probably is.”This is such a tragic phrase because nearly anything of value seemed at one point oranother, to be too good to be true.

Think about it – modern advances in medicine, airplanes, electricity, automobiles, personalcomputers, the internet all seemed to good to be true at one point in time.

Seek Independent, Objective & SpecializedAdvice From People That Recognize TheyDon't Know Everything

#11Finally, and along with point #3, we encourage you to seek unbiased, expert, and open-mindedadvice. By open-minded we really mean humble.

Luckily, most of the tremendously competent financial advisors, the ones with a vast amount ofexpertise in their fields, will not feel the urge to know it all. So maybe that’s the first litmus test.

You want an advisory team that thinks outside the box. Because, if they’re inside the box theywill try to get you in the box with them – and then you’ll get the same results as the majority:mediocrity.