11 february 2015 per strömberg, ceo sven lindskog, cfo fileprofit for the period 879 531 2,667...

TRANSCRIPT

11 February 2015

Per Strömberg, CEO

Sven Lindskog, CFO

Q4 report 2014 - Press and analyst meeting

Q4 strong sales development and investments for

continued growth • Net sales increased by 6.2%

• In local currency +5.6%

• Increased sales in ICA Sweden and Rimi Baltic

• EBIT excluding non-recurring items +2%

• Large strategic investments for continued growth

• Acquisition of Apotek Hjärtat finalized • Integration according to plan

• Norwegian divestment ongoing

• Permission from the Swedish FSA to conduct

insurance business • Preparations continues to launch P&C** insurance by the

end of the year

• The Board proposes a dividend of 9.50 SEK

2

MSEK Q4 YTD

2014 2013 2014 2013*

Net Sales 23,180 21,820 87,174 82,993

EBIT excl. non-recurring items 1,081 1,058 3,937 3,695

EBIT 1,065 753 4,097 3,482

Profit for the period 879 531 2,667 1,424

EBIT margin excl. non-recurring items 4.7% 4.8% 4.5% 4.5%

EBIT margin 4.6% 3.5% 4.7% 4.2%

Earnings per ordinary share, SEK 4.09 2.49 12.53 7.18

*2013 proforma

** Property & Casualty

The market in Sweden

• Repo rate still at zero – Riksbanken maintained the rate in

December

• Food inflation rate* higher in Q4: +1.3%, 0.6% FY 2014

• Total retail market showed strong development in 2014;

+3.8% in fixed prices. Growth for food retail was +1.5% in

fixed prices

3

*DHI

Segments during the quarter

ICA Sweden

• Store sales growth outperformed market • Increased market shares in Q4

• Investing for future growth • New stores, Cura pharmacies and Online

• Strategic priorities better than plan: • PL share increased to 22.7% (21.5)

• 14 new ICA stores established in 2014 • No of pharmacies 67 (58) end of Q4

4

Online update

• Successful launch in November • 4 stores in Östergötland, off to a good start

• Online platform works well

• Extended test in Q1 - more stores in Östergötland

• Further launches starting in Q2 • New regions

• Technical upgrade of IT-platform

• ICA Online is well received by customers and retailers

5

Segments during the quarter (cont’d)

Rimi Baltic

• Solid Q4 with continued good sales and profitability growth

• Increased market shares during Q4 for Rimi Baltic • Improving in all countries, particularly in Latvia

• Ambitious programme for store conversions and new

stores, mainly in Lithuania • Total Rimi Baltic 2014: 12 new stores

• In total 242 stores by year end

ICA Bank

• Business volume continues to increase

• Adverse repo rate impact

• Number of customers increased in 2014 to 656 000 (+ 7%)

6

Segments during the quarter (cont’d.)

ICA Real Estate

• Långeberga project in final stage with good progress

• Norwegian real estate is made ready for divestment

• Awaiting closure of ICA Norway divestment

• Sales process ready to be initiated late 2015

Portfolio companies

• Hemtex and Cervera deliver full year profit

• Divestment process of Cervera is initiated

7

The new pharmacy business

• Transaction closed on January 15, 2015 • Apotek Hjärtat included in ICA Gruppen from that date

• Pharmacy business (Apotek Hjärtat + Cura apotek) reported as

separate segment from Q1 2015

• Apotek Hjärtat is a solid business with strong momentum: • Sales 2014 of SEK 9.6 bn (8.3)

• EBIT 2014 of 401 MSEK (288)

• CEO of ICA Gruppen’s Pharmacy business: Anders Nyberg

(former CEO of Apotek Hjärtat)

• Integration process runs according to plan

8

The quarter in numbers

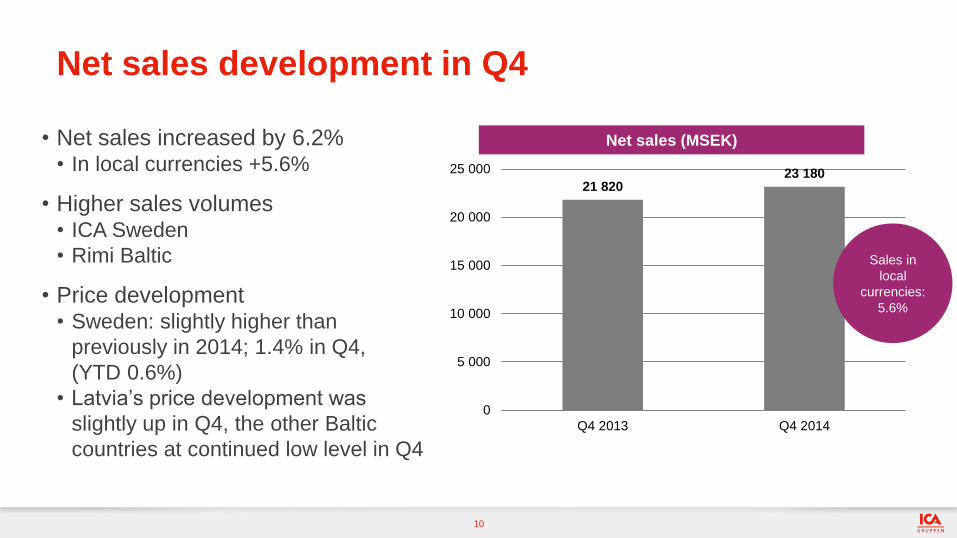

Net sales development in Q4

• Net sales increased by 6.2% • In local currencies +5.6%

• Higher sales volumes • ICA Sweden

• Rimi Baltic

• Price development • Sweden: slightly higher than

previously in 2014; 1.4% in Q4,

(YTD 0.6%)

• Latvia’s price development was

slightly up in Q4, the other Baltic

countries at continued low level in Q4

Net sales (MSEK)

Net sales

+5.8%

10

21 820 23 180

0

5 000

10 000

15 000

20 000

25 000

Q4 2013 Q4 2014

Sales in

local

currencies:

5.6%

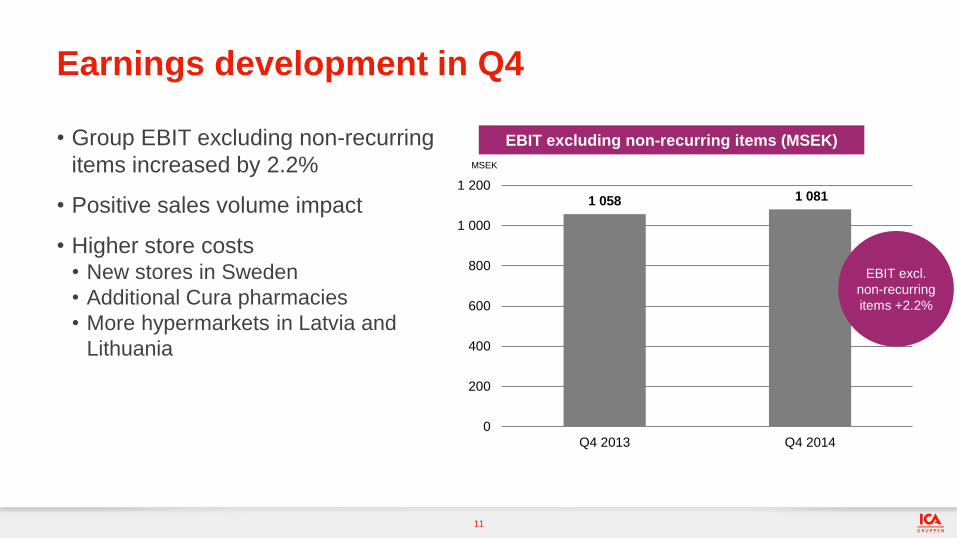

Earnings development in Q4

• Group EBIT excluding non-recurring

items increased by 2.2%

• Positive sales volume impact

• Higher store costs • New stores in Sweden

• Additional Cura pharmacies

• More hypermarkets in Latvia and

Lithuania

EBIT excluding non-recurring items (MSEK)

11

1 058 1 081

0

200

400

600

800

1 000

1 200

Q4 2013 Q4 2014

MSEK

EBIT excl.

non-recurring

items +2.2%

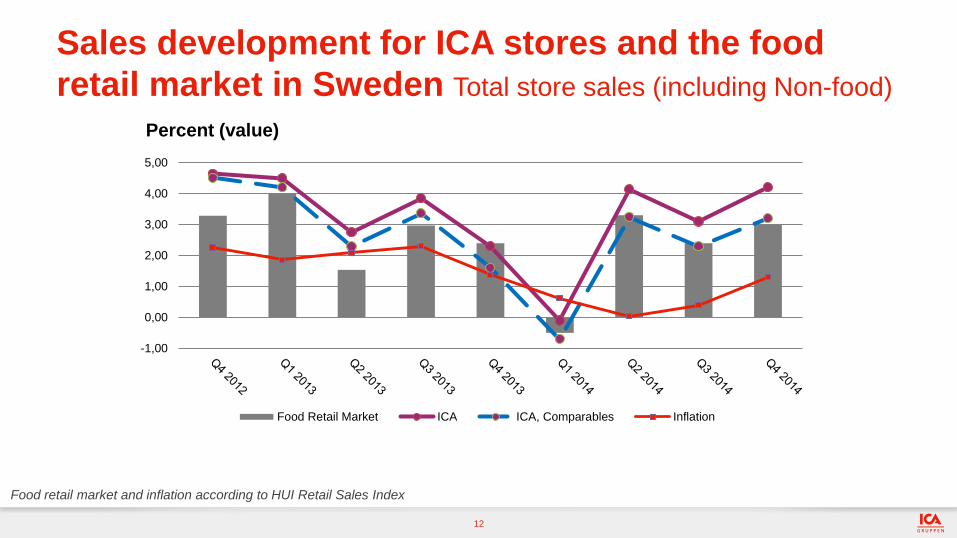

Food retail market and inflation according to HUI Retail Sales Index

Sales development for ICA stores and the food

retail market in Sweden Total store sales (including Non-food)

12

-1,00

0,00

1,00

2,00

3,00

4,00

5,00

Food Retail Market ICA ICA, Comparables Inflation

Percent (value)

Store sales in Sweden

Development compared with the same period 2013

13

October-December 2014 January-December 2014

Store sales excl. VAT MSEK Development

total

Development

comparable MSEK

Development

total

Development

comparable

Maxi ICA Stormarknad 8,383 5.4% 3.3% 31,152 3.4% 2.2%

ICA Kvantum 6,653 5.9% 3.5% 25,230 4.5% 2.2%

ICA Supermarket 8,114 2.2% 2.6% 32,261 1.7% 1.4%

ICA Nära 3,835 2.7% 2.9% 15,712 1.3% 2.1%

Total 26,985 4.2% 3.1% 104,356 2.8% 1.9%

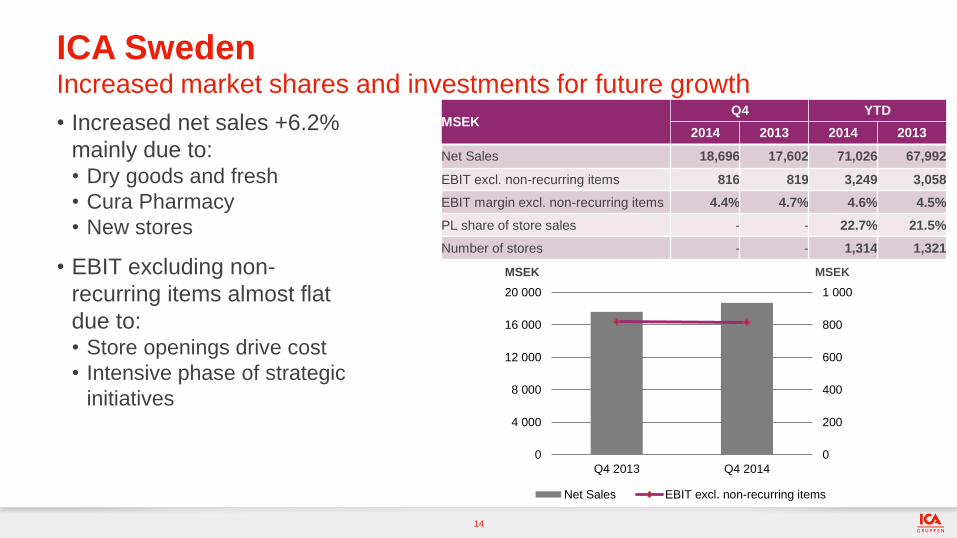

ICA Sweden Increased market shares and investments for future growth

• Increased net sales +6.2%

mainly due to: • Dry goods and fresh

• Cura Pharmacy

• New stores

• EBIT excluding non-

recurring items almost flat

due to: • Store openings drive cost

• Intensive phase of strategic

initiatives

MSEK MSEK

14

MSEK Q4 YTD

2014 2013 2014 2013

Net Sales 18,696 17,602 71,026 67,992

EBIT excl. non-recurring items 816 819 3,249 3,058

EBIT margin excl. non-recurring items 4.4% 4.7% 4.6% 4.5%

PL share of store sales - - 22.7% 21.5%

Number of stores - - 1,314 1,321

0

200

400

600

800

1 000

0

4 000

8 000

12 000

16 000

20 000

Q4 2013 Q4 2014

Net Sales EBIT excl. non-recurring items

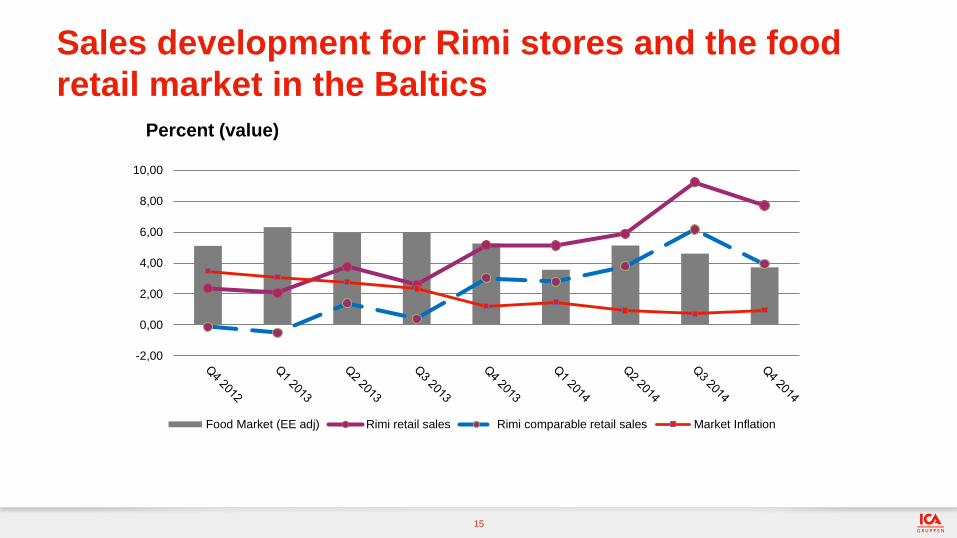

Sales development for Rimi stores and the food

retail market in the Baltics

15

Percent (value)

-2,00

0,00

2,00

4,00

6,00

8,00

10,00

Food Market (EE adj) Rimi retail sales Rimi comparable retail sales Market Inflation

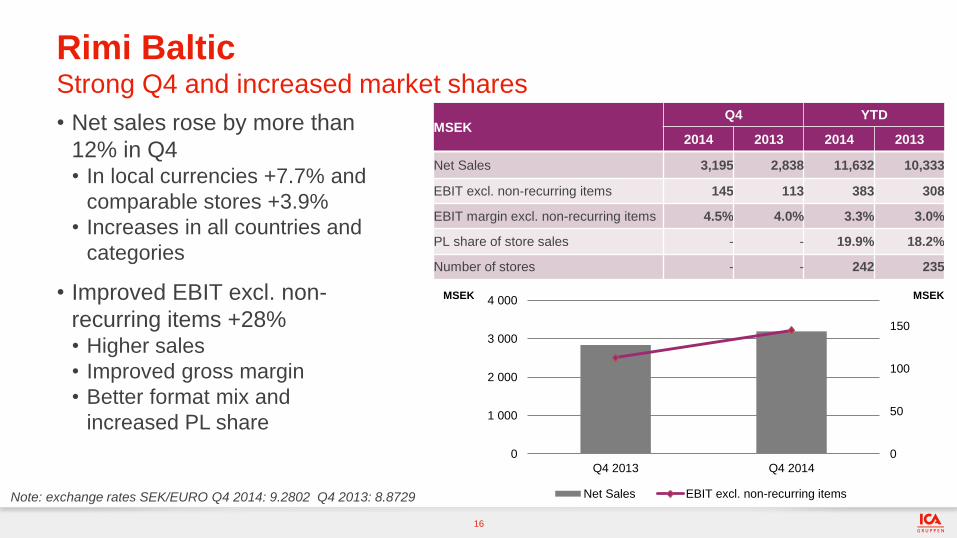

Rimi Baltic Strong Q4 and increased market shares

• Net sales rose by more than

12% in Q4 • In local currencies +7.7% and

comparable stores +3.9%

• Increases in all countries and

categories

• Improved EBIT excl. non-

recurring items +28% • Higher sales

• Improved gross margin

• Better format mix and

increased PL share

16

Note: exchange rates SEK/EURO Q4 2014: 9.2802 Q4 2013: 8.8729

MSEK Q4 YTD

2014 2013 2014 2013

Net Sales 3,195 2,838 11,632 10,333

EBIT excl. non-recurring items 145 113 383 308

EBIT margin excl. non-recurring items 4.5% 4.0% 3.3% 3.0%

PL share of store sales - - 19.9% 18.2%

Number of stores - - 242 235

0

50

100

150

0

1 000

2 000

3 000

4 000

Q4 2013 Q4 2014

Net Sales EBIT excl. non-recurring items

MSEK MSEK

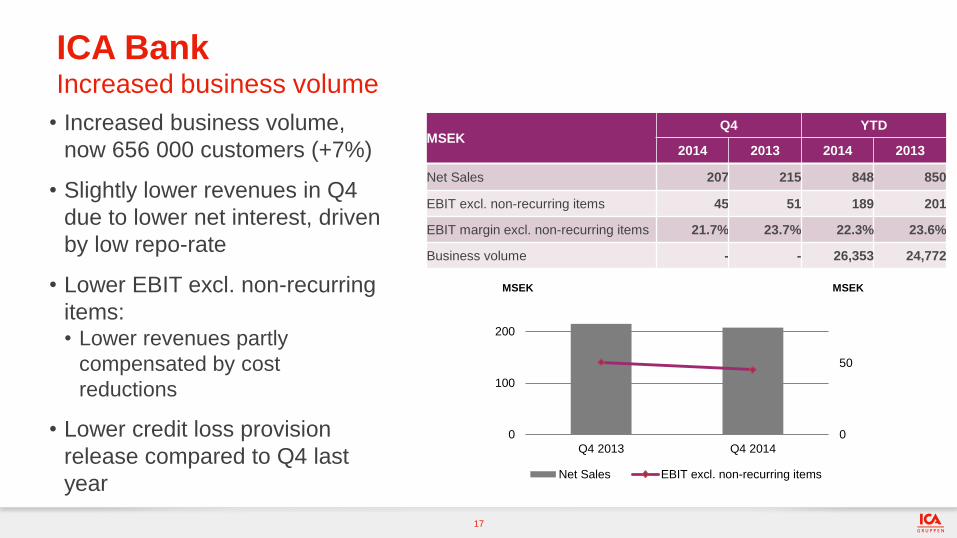

ICA Bank Increased business volume

• Increased business volume,

now 656 000 customers (+7%)

• Slightly lower revenues in Q4

due to lower net interest, driven

by low repo-rate

• Lower EBIT excl. non-recurring

items: • Lower revenues partly

compensated by cost

reductions

• Lower credit loss provision

release compared to Q4 last

year

17

MSEK Q4 YTD

2014 2013 2014 2013

Net Sales 207 215 848 850

EBIT excl. non-recurring items 45 51 189 201

EBIT margin excl. non-recurring items 21.7% 23.7% 22.3% 23.6%

Business volume - - 26,353 24,772

0

50

0

100

200

Q4 2013 Q4 2014

Net Sales EBIT excl. non-recurring items

MSEK MSEK

ICA Real Estate Stable business development

• Net sales in line with Q4 last

year

• Lower EBIT excl. non-recurring

items: • Significantly higher depreciation

due to changed assessment of

life length

• Large divestments end Q3 2014

• Partly off-set by income from

new investments

18

MSEK Q4 YTD

2014 2013 2014 2013

Net Sales 575 573 2,253 2,255

Depreciation -130 -107 -515 -421

EBIT excl. non-recurring items 95 123 409 473

EBIT margin excl. non-recurring items 16.5% 21.5% 18.2% 21.0%

0

50

100

150

0

100

200

300

400

500

600

700

Q4 2013 Q4 2014

Net Sales EBIT excl. non-recurring items

MSEK MSEK

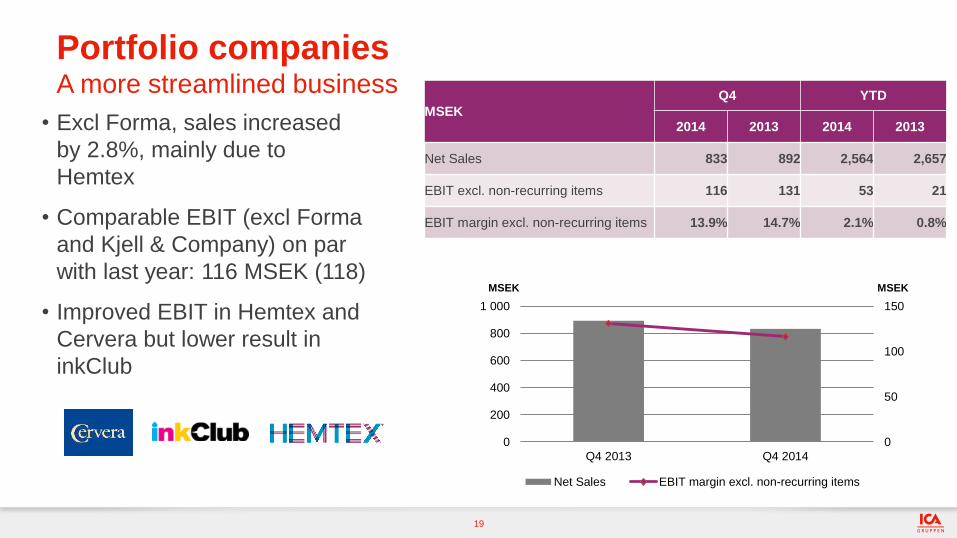

Portfolio companies A more streamlined business

• Excl Forma, sales increased

by 2.8%, mainly due to

Hemtex

• Comparable EBIT (excl Forma

and Kjell & Company) on par

with last year: 116 MSEK (118)

• Improved EBIT in Hemtex and

Cervera but lower result in

inkClub

19

MSEK

Q4 YTD

2014 2013 2014 2013

Net Sales 833 892 2,564 2,657

EBIT excl. non-recurring items 116 131 53 21

EBIT margin excl. non-recurring items 13.9% 14.7% 2.1% 0.8%

0

50

100

150

0

200

400

600

800

1 000

Q4 2013 Q4 2014

Net Sales EBIT margin excl. non-recurring items

MSEK MSEK

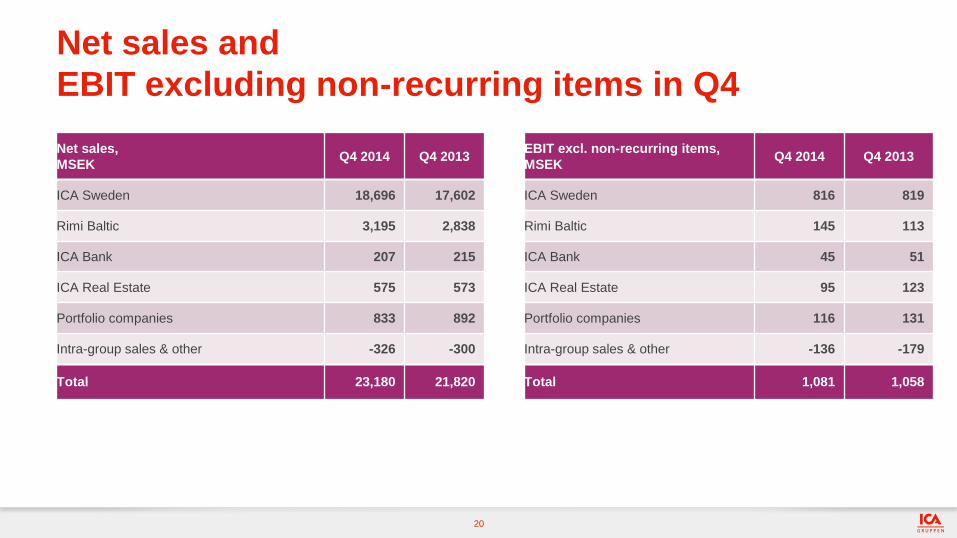

Net sales and

EBIT excluding non-recurring items in Q4

20

Net sales,

MSEK Q4 2014 Q4 2013

ICA Sweden 18,696 17,602

Rimi Baltic 3,195 2,838

ICA Bank 207 215

ICA Real Estate 575 573

Portfolio companies 833 892

Intra-group sales & other -326 -300

Total 23,180 21,820

EBIT excl. non-recurring items,

MSEK Q4 2014 Q4 2013

ICA Sweden 816 819

Rimi Baltic 145 113

ICA Bank 45 51

ICA Real Estate 95 123

Portfolio companies 116 131

Intra-group sales & other -136 -179

Total 1,081 1,058

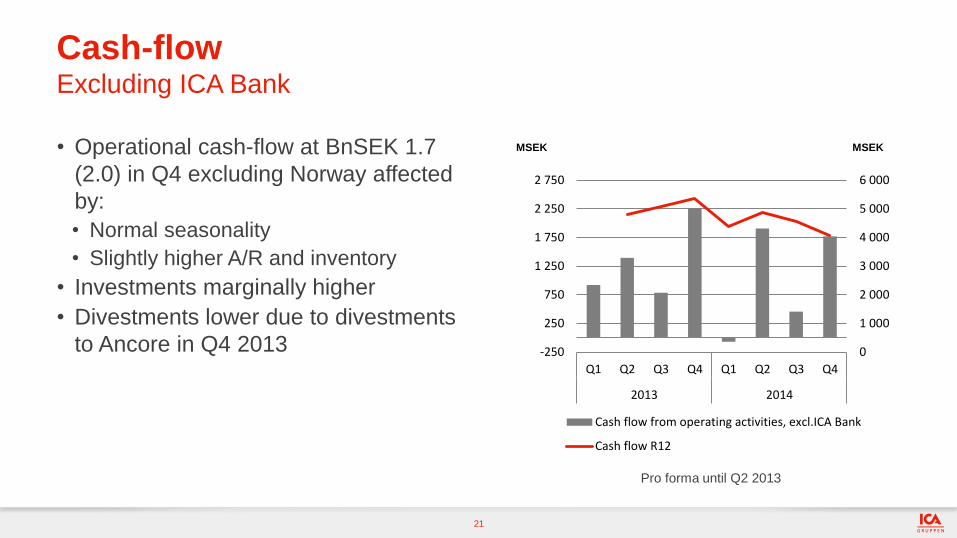

Cash-flow Excluding ICA Bank

• Operational cash-flow at BnSEK 1.7

(2.0) in Q4 excluding Norway affected

by:

• Normal seasonality

• Slightly higher A/R and inventory

• Investments marginally higher

• Divestments lower due to divestments

to Ancore in Q4 2013

Pro forma until Q2 2013

21

0

1 000

2 000

3 000

4 000

5 000

6 000

-250

250

750

1 250

1 750

2 250

2 750

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014

Cash flow from operating activities, excl.ICA Bank

Cash flow R12

MSEK MSEK

Long-term

goal <2.0x

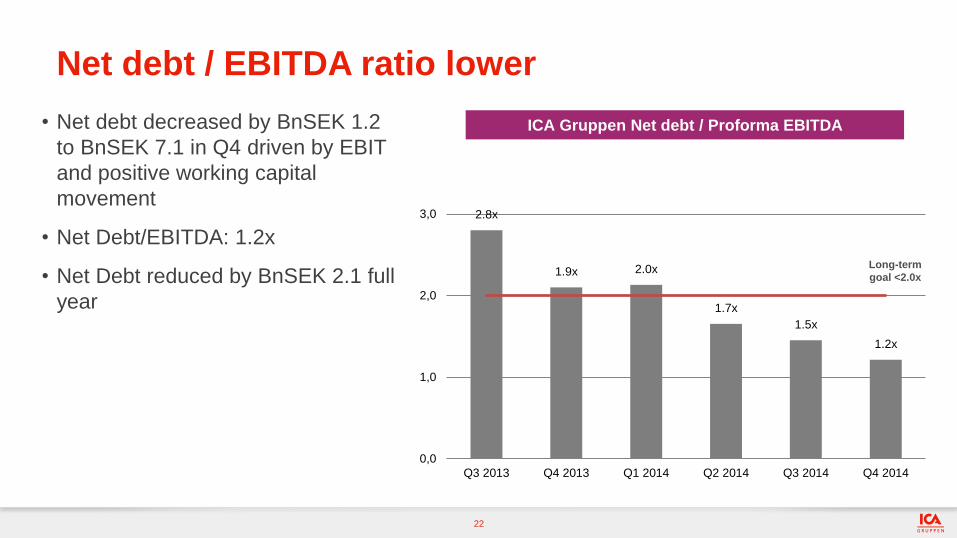

Net debt / EBITDA ratio lower

• Net debt decreased by BnSEK 1.2

to BnSEK 7.1 in Q4 driven by EBIT

and positive working capital

movement

• Net Debt/EBITDA: 1.2x

• Net Debt reduced by BnSEK 2.1 full

year

ICA Gruppen Net debt / Proforma EBITDA

22

2.8x

1.9x 2.0x

1.7x

1.5x

1.2x

0,0

1,0

2,0

3,0

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014

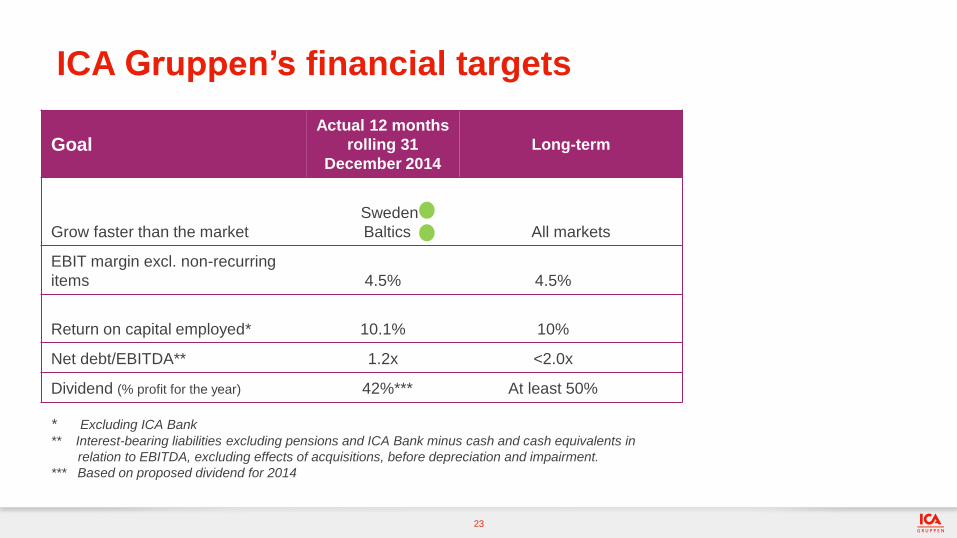

Goal Actual 12 months

rolling 31

December 2014

Long-term

Grow faster than the market

Sweden

Baltics All markets

EBIT margin excl. non-recurring

items 4.5% 4.5%

Return on capital employed* 10.1% 10%

Net debt/EBITDA** 1.2x <2.0x

Dividend (% profit for the year) 42%*** At least 50%

* Excluding ICA Bank

** Interest-bearing liabilities excluding pensions and ICA Bank minus cash and cash equivalents in

relation to EBITDA, excluding effects of acquisitions, before depreciation and impairment.

*** Based on proposed dividend for 2014

ICA Gruppen’s financial targets

23

Outlook

Sweden • Continued positive development for ICA Sweden

• High project activity drive investments/costs

• According the HUI the total food market is expected to grow

by 1.5% in 2015

Baltics • Continued sales growth for Rimi Baltic – positive signs in all

countries

• Continued focus on new establishments

• 15-20 store openings in 2015, mainly in Lithuania

ICA Bank • Lower repo rate impacts future earnings expectations

• Strong focus on increasing products per customer

24

Outlook (cont’d)

ICA Real Estate

• Expansion of Helsingborg distribution center to be finalized

• Divested properties to Ancore gives lower revenues short-term

• Norwegian properties to be divested when ICA Norway

divestment is finalized

Streamlining and growth • Complete the divestment of ICA Norway

• Successful integration of Apotek Hjärtat

• Process initiated to divest Cervera

25

Summary

• Continued positive development during the fourth quarter • Net sales +6%

• EBIT excluding non-recurring items +2%

• Increased market shares in Sweden and the Baltics

• Acquisition of Apotek Hjärtat finalized and integration process

in start-up phase

• Divestment of ICA Norway ongoing

• Our work with other strategic priorities continues according to

plan, among others: • Online

• CRM

• Build ICA Gruppen’s new health position

26

2015-02-11

27

Disclaimer

The information is such that ICA Gruppen AB (publ) is obliged to make public pursuant to the

Securities Market Act (SFS 2007:528) and/or the Act on Trade with Financial Instruments (SFS

1991:980). The information was distributed to media for publication on February 11, 2015 at 7.00 CET.

This report contains forward-looking statements that reflect the Board of Directors’ and management’s

current views with respect to certain future events and potential financial performance. Although the

Board of Directors and the management believe that the expectations reflected in such forward-looking

statements are reasonable, no assurance can be given that such expectations will prove to have been

correct. Accordingly, results could differ materially from those set out in the forward-looking statements

as a result of, among other factors, (i) changes in economic, market and competitive conditions, (ii)

success of business and operating initiatives, (iii) changes in the regulatory environment and other

government actions, (iv) fluctuations in exchange rates and (v) business risk management.

This report does not imply that the Company has undertaken to revise these forward-looking

statements, beyond what is required under the company’s registration contract with Nasdaq

Stockholm, if and when circumstances arise that will lead to changes compared to the date when

these statements were provided.

28